financial services sector: insurance services - mit.gov.jo · 7.0 swot analysis ... swot analysis...

TRANSCRIPT

Financial Services Sector: Insurance Services

Trade In Services Benchmarking Study

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

i

Table of Contents

1.0 RESEARCH ........................................................................................................ 1

1.1 PREVIOUS RESEARCH ........................................................................................ 1

1.2 CURRENT RESEARCH ........................................................................................ 1

2.0 SECTOR ANALYSIS .......................................................................................... 2

2.1 SECTOR CONTEXT ............................................................................................. 2

3.0 GENERAL BUSINESS ENVIRONMENT........................................................... 17

4.0 LEGISLATIVE AND REGULATORY ENVIRONMENT ..................................... 18

4.1 MEASURES RELATED TO DOMESTIC REGULATION ............................................... 18

4.2 MEASURES RELATED TO PROFESSIONAL QUALIFICATION .................................... 23

4.3 EFFECT OF MEASURES ON INTERNATIONAL PARTICIPATION IN THE MARKET .......... 24

5.0 GATS RESTRICTIVENESS MEASURES ......................................................... 24

5.1 GATS COMMITMENTS OF THE SECTOR/ SUB- SECTOR ........................................ 24

6.0 BENCHMARKING ............................................................................................ 26

6.1 COMPETITIVE STRENGTHS................................................................................ 28

6.2 COMPETITIVE WEAKNESSES ............................................................................. 28

6.3 POTENTIAL FOR GROWTH ................................................................................. 29

7.0 SWOT ANALYSIS ............................................................................................ 30

8.0 OPPORTUNITY SCAN ..................................................................................... 31

9.0 CONSTRAINTS TO DEVELOPMENT ............................................................... 31

9.1 CONSTRAINTS (FOR THE SECTOR INCLUDING BUT NOT LIMITED TO TECHNICAL,

EDUCATIONAL, INSTITUTIONAL, HUMAN SKILLS) BOTH IN TERMS OF SECTOR GROWTH

AND TRADE IN SERVICES ........................................................................................ 31

9.2 RELATED POLICY FACTORS .............................................................................. 32

9.3 SPECIFIC RECOMMENDATIONS FOR REMEDIAL ACTIONS ...................................... 32

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

ii

List of Tables TABLE 1: INSURANCE CONTRIBUTION IN GDP IN 2007 ................................................... 3

TABLE 2: INSURANCE CONTRIBUTION IN GDP FOR ARAB COUNTRIES ............................. 5

TABLE 3: SELECTED FIGURES FOR JORDANIAN INSURANCE COMPANIES FOR THE YEAR

2007 .................................................................................................................. 6

TABLE 4: SELECTED FIGURES FOR THE TOP JORDANIAN INSURANCE COMPANIES BY

SHAREHOLDERS' EQUITY ..................................................................................... 7

TABLE 5: SELECTED RATIOS FOR JORDANIAN INSURANCE COMPANIES FOR THE YEAR

2007 .................................................................................................................. 8

TABLE 6: SELECTED RATIOS FOR THE TOP 8 JORDANIAN INSURANCE COMPANIES FOR BY

MARKET SHARE .................................................................................................. 9

TABLE 7: SELECTED FIGURES FOR JORDANIAN INSURANCE MARKET 1999-2007 .......... 10

TABLE 8: CLASSES OF INSURANCE BUSINESS LICENSES PER CPC CODE ..................... 11

TABLE 9: TYPES OF LICENSES ISSUED TO INSURANCE COMPANIES .............................. 12

TABLE 10: THE CHARACTERISTICS OF THE SIX LARGEST INSURANCE COMPANIES IN THE

MARKET FOR LIFE INSURANCE: ........................................................................... 13

TABLE 11: CHARACTERISTICS OF THE SIX LARGEST INSURANCE COMPANIES IN THE

MARKET FOR NON-LIFE INSURANCE ..................................................................... 14

TABLE 12: TAKAFUL PREMIUMS OF ARAB REGION ....................................................... 15

TABLE 13: DEVELOPMENT AUXILIARY SERVICES PROFESSIONALS 2003-2007 .............. 16

TABLE 14: INSURANCE PREMIUMS PRODUCTION CHANNELS FOR 2007 ......................... 17

TABLE 15: THE LEGISLATIVE FRAMEWORK OF INSURANCE SECTOR .............................. 19

TABLE 16: GATS COMMITMENTS INSURANCE SUB-SECTOR ....................................... 25

TABLE 17: INSURANCE BENCHMARKING OF NEIGHBORING COUNTRIES ......................... 26

TABLE 18: MINIMUM CAPITAL REQUIREMENTS ............................................................ 27

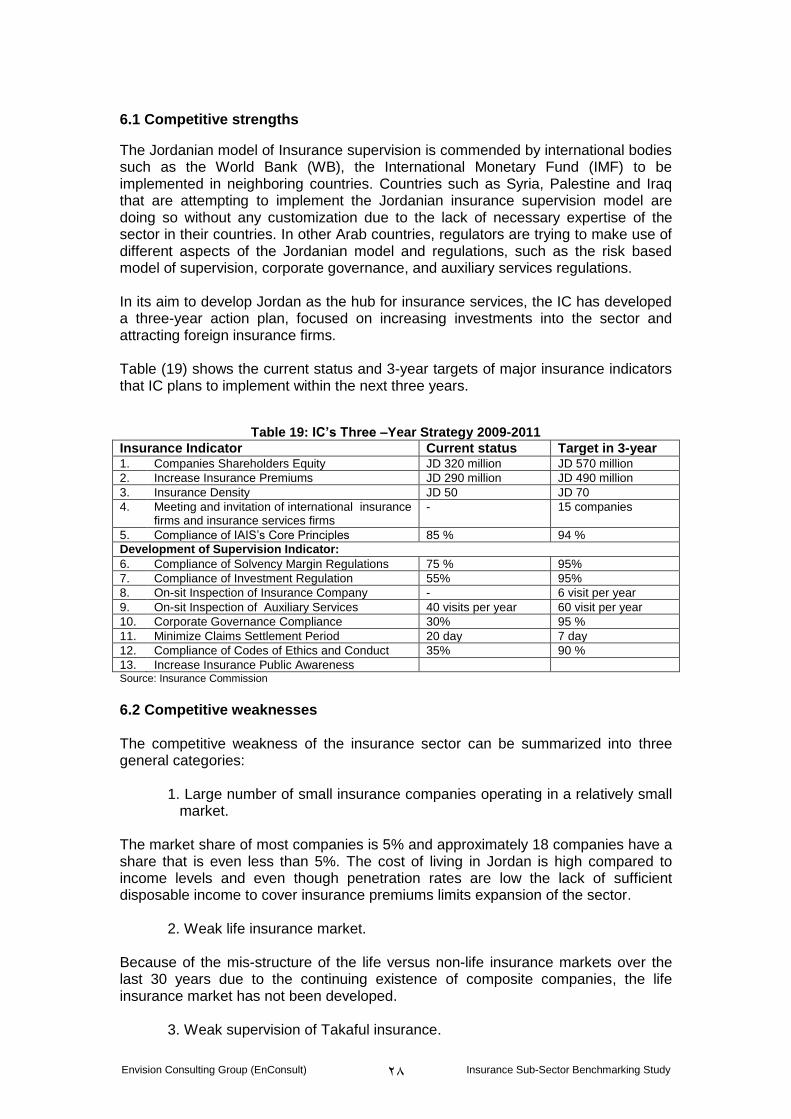

TABLE 19: IC’S THREE –YEAR STRATEGY 2009-2011 ................................................. 28

TABLE 20: INSURANCE COMPANIES FACING PROBLEMS THROUGH LAST DECADE .......... 29

TABLE 21: SWOT ANALYSIS OF THE JORDANIAN INSURANCE SECTOR ......................... 30

FIGURES:

FIGURE 1: JORDANIAN INSURANCE MARKET STRUCTURE…………………...…4

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

iii

ANNEXES ANNEX 1: INSTRUCTIONS OF THE BASIS OF INVESTING THE FUNDS OF THE INSURANCE

COMPANY AND DETERMINING THE NATURE AND THE LOCATION OF THE INSURANCE

COMPANY’S ASSETS THAT MATCH ITS INSURANCE OBLIGATIONS .......................... 35

ANNEX 2: IC’S MAIN SOURCE OF FUNDS ...................................................................... 43

ANNEX 3: INSURANCE CORE PRINCIPLES (ICP) ........................................................... 44

ANNEX 4: SAMPLE INSURANCE COMPANIES AND OFFICIALS INTERVIEWED .................... 48

ANNEX 5: MANAGERS FROM THE FOLLOWING COMPANIES WERE INTERVIEWED ............. 49

ANNEX 6: LIST OF REGULATIONS, INSTRUCTIONS AND DECISIONS ISSUED FOR THE

INSURANCE SECTOR .......................................................................................... 50

ANNEX 7:. INSTRUCTIONS FOR GRANTING AND RENEWING THE LICENSE TO TRANSACT

INSURANCE BUSINESS ....................................................................................... 55

ANNEX 8: INSTRUCTIONS FOR OPENING A BRANCH OF AN INSURANCE COMPANY ......... 60

ANNEX 9: INSURANCE SERVICES, CPCPROV CODE 812 ............................................... 63

ANNEX 10: QUESTIONNAIRE ...................................................................................... 64

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

iv

List of Acronyms Accounting and Auditing Organization for Islamic Financial Institutions

AAOIFI

American International Group AIG

American Life Insurance Co. ALICO

Arab Union Reinsurance Co. AURe

Bahrain Insurance Association BIA

Central Bank of Bahrain CBB

Capital Market Authority CMA

Central Product Classification CPC

Financial Sector Assessment Program FSAP

General Agreement on Trade in Services GATS

Gross Domestic Product GDP

International Association of Insurance Supervisors

IAIS

International Accounting Standards Board

IASB

Insurance Commission IC

Insurance Core Principles ICP

Islamic Financial Services Board IFSB

International Monetary Fund IMF

Jordan Insurance Federation JIF

Memorandum Of Understanding MOU

Qatar Financial Center Authority QFCA

Qatar Insurance Platform QIP

Research and Development R&D

Syrian Insurance Company SIC

Syrian Insurance Supervisory Commission

SISC

Societe Tunisians d'Assurances et de Reassurances

STAR

Strengths, Weaknesses, Opportunities, Threats

SWOT

Third Party Administrator TPA

World Bank WB

World Trade Organization WTO

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

1

1.0 Research 1.1 Previous research The previous research conducted on the Jordanian insurance sector was:

Assessment of Trade-in-Services of Jordan-Part II- Sector Assessment. The assessment time frame was October 2005-April 2006. The analysis was historical and descriptive of the sector during the period. Analysis of problems and related issues were presented in a cursory manner. In some sections of this paper, it was noticed that some information related to the recent development in insurance sector were not clearly stated, which could lead to erroneous conclusions.

Insurance Regulation in Jordan New Rules-Old System by Dimitri Vittas.1 This study analyzed the insurance sector up to the end of 2003. The main modernization process of establishing the Jordanian Insurance Commission (IC) in 1999 and related regulations were analyzed, and the major challenges that the sector faces in developing life insurance sub-sector was addressed. The study was part of the FSAP (Financial Sector Assessment Program) of Jordan; the author Mr. Vittas was a member of the assessment mission.

1.2 Current Research Under CPCProv utilized for this study; the services under consideration are:

1. 8140 – Services auxiliary to insurance and pension funding

81401 - Insurance broking and agency services

81402 - Insurance and pension consultancy services

81403 - Average and loss adjustment services

81404 - Actuarial services

81405 - Salvage administration services

81409 – Other services auxiliary to insurance and pension funding, such as: TPA (Third Party Administration in Health Insurance). Re-insurance Broking services.

Data collection difficulties occurred for Code 81212 -Pension and Annuity Services, which is defined as “Insurance underwriting services providing incomes (annuities) upon retirement according to contributions paid to pension schemes during economically active lifetime. Pension fund management services are included”. The difficulty arose because private pension schemes by the insurance sector have not been developed yet in Jordan to support existing public pension schemes (Social Security, Government Civil and Military Retirement). Pension fund management services, which were to be analyzed under Code 81212, are not placed under Insurance Commission supervision and control and as such are not included in the insurance sector in Jordan. Research employed for conducting the present study is as follows:

1 World Bank Policy Research Working Paper 3298, May 2004

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

2

Since passage of the Insurance Act No. 33 of 1999, it is not permitted for new insurance companies to operate as a composite company, a company that offers both life and non-life insurance. This measure was taken in order for the Jordanian insurance sector to comply with best international standards. However, those companies that were operating as composite firms before the 1999 act are allowed to continue to operate as composite firms, offering both life and non-life policies..

Data collection activities for this study have focused on several specific areas:

1. Desk research and primary data acquisition from the Insurance Commission and other insurance-related professional and regulatory bodies.

2. The standard questionnaire was used in interviews with Insurance

Commission officials and key insurance experts working within the sector. However, with regard to services auxiliary to insurance and pension funding (Code 8140), another set of questions were determined as more relevant to the data collection process. Annex four details documentation of the interviews.

2.0 Sector Analysis 2.1 Sector Context There are twenty-nine insurance` companies operating in Jordan; only one company is licensed solely as a life insurance company (American Life Insurance Company ALICO- a foreign branch and member of American Insurance Group (AIG), ten are licensed as non-life companies, and eighteen are composite companies that are licensed as life and non-life carriers, a practice that is not longer permitted by law. Other important parties within the insurance sector are insurance supportive services (Auxiliary services). Figure 1 on the following page shows the structure of the Jordanian insurance market. As noted in the figure, there are no reinsurance companies operating in Jordan per se; however, local reinsurance (Retrocession)2, between local direct insurance companies is quite active in the market and retrocession is a practice utilized by all local companies. The Jordanian insurance sector has been one of the growing sectors in the country over the last decade. The total premium income for 2007 amounted to JD 291.6 million (US $ 411.9 million). 3Total gross premiums have been growing steadily over the last decade at an average of 15%, according to the Insurance Commission of Jordan (IC). This growth rate is promising, regardless of the fact that the insurance sector's contribution to GDP is very low compared to the world average: there is 2.6% penetration rate)4 in Jordan as shown in Table 1 below, compared to a world average of 9-10 percent.5

2 Re-insurance (Retrocession) is the re-allocation and distribution of the purchased risks of one insurance company

among other insurance companies within the local market 3 Insurance Commission data

4 Penetration rate; is the local Insurance contribution in the national economy; measured by the total insurance

premiums divided by the gross domestic production (GDP) 5 Insurance Commission data

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

3

Table 1: Insurance Contribution in GDP in 2007

Type of Insurance Insurance Premiums Percentage % of GDP

Total Insurance Premiums 291.6 2.6

Total General Insurance 262.464 2.34

Motor Insurance

Marine & Transport insurance

Aviation Insurance

Fire & Other Damage to Property Insurance

Liability Insurance

Credit and Surety ship Insurance

Other General Insurance

Medical Insurance

129.99

20.39

3.268

42.201

6.506

0.784

7.438

51.887

1.16

0.18

0.03

0.38

0.06

0.01

0.07

0.46

Total Life- Insurance 29.18 0.26%

Source: Insurance Commission, Seventh Annual Report 2007

Total life-insurance contribution to GDP is very weak in Jordan, 0.26% out of 2.6% for the total insurance sector as shown above. This weak contribution, although affected by various factors, is primarily due to the historical unstructured balance of life and non-life insurance which weakens the life insurance sub-sector: Composite firms, grandfathered in under the 1999 law, still offer life and non-life policies and as a result, life insurance as a specialty has not develop thereby weakening the life insurance sub-sector. However, interestingly, the only foreign branch of ALICO that is specialized in life insurance and has garnered 60% of the Jordanian life insurance market, was developed in Jordan. Beyond the preponderance of composite firms in the market, as shown in Figure 1, other factors have contributed to the lack of specialization of the life insurance sub-sector over the last decade. The other factors would include perceived Islamic regional factors that prohibit the purchasing life insurance; the high cost of living within the Jordan relative to income which precludes access to income necessary for large numbers of Jordanians to purchase insurance policies; and the absence of income-tax exemption for paid life insurance premiums. All of these factors limit the sub-sector. However, when looking at the sector in total, the insurance penetration rate for Jordan is one of the highest among neighboring countries as shown in Table 2.

Figure 1: Jordanian Insurance Market Structure

Insurance Commission

Jordan Insurance Federation

Composite Companies

Jordan International Jordan French Jordan Insurance Islamic Insurance (Takaful) General Arabia Insurance National Insurance Middle East Insurance Arab Assurers Arab Life and Accident Insurance Arab German Insurance Jerusalem Insurance United Insurance Arab Jordanian Insurance Group Al Nisr Al Arabi Insurance Al Yarmouk Insurance Gerasa Insurance Delta Insurance Euro Arab Insurance Company

Non-Life Companies

Arab Union International Insurance Holy Land Insurance Al-Manara Insurance (Al-Waha) Arab Orient Insurance Al- Barakah Takaful Insurance Oasis Insurance Philadelphia Insurance Housing Loan Insurance First Insurance (Takaful) Mediterranean and Gulf Insurance

Life Companies

American Life Insurance (ALICO)

Insurance Supportive Services

Agents 426

Reinsurance Brokers 4

Brokers 56

Actuarial Services 13

Loss Adjusters 37

Insurance Consultancy 11

Health Third Party Administrators

11

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

5

As shown in Table 2, which depicts the insurance contribution to GDP for Arab countries, the sector contribution in Jordan is far above that of the average rate of 1.3% of other Arab countries. Only the sector contributions in Lebanon, at 2.9%, and Morocco, at 3.0%, are slightly above Jordan (2.6%), due primarily to the existence of a market for life-insurance that is more developed than that of Jordan.

Table 2: Insurance Contribution in GDP for Arab Countries

Country 2005 2006

Morocco 2.9% 3.0%

Lebanon 2.9% 2.9%

Jordan 2.4% 2.6%

UAE 2.2% 2.2%

Tunisia 1.8% 2.0%

Palestine 1.6% 1.9%

Bahrain 1.9% 1.8%

Qatar 1.5% 1.4%

Oman 1.2% 0.9%

Egypt 0.9% 0.8%

Kuwait 0.8% 0.7%

Algeria 0.6% 0.5%

Saudi Arabia 0.5% 0.5%

Sudan 0.6% 0.5%

Mauritania 0.5% 0.4%

Syria 0.5% 0.4%

Libya 0.4% 0.3%

Yemen 0.3% 0.3%

Average 1.3% 1.3%

Source: Jordan Insurance Federation/ Department of Studies Training and Development.

There is potential for the development in the local insurance market toward increasing its contribution to the economy. However, growth would be dependent upon the IC taking a leading role in this regard through the implementation of their integrated three-year strategy6 and different annual policies and programs for a strong professional and regulatory framework that ensures that the insurance sector replicates international best standards. Tables 3 through 7 present important insurance indicators related to Jordanian insurance companies including financial, technical and statistical information for the year 2007. Table 3 shows selected financial and technical figures for the Jordanian insurance companies as of the year ended 2007. Taking the total investment indicator for each company we notice that ten largest local insurance companies as measured by total assets, and the only foreign insurance branch accounts for 64% of the total investments for the sector. The other indicators, shareholders-equity, and total premiums written for the same ten firms, accounts for 66%, 66%, and 60%respectively

6 IC Three Year Strategy 2009-2011

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

6

Table 3: Selected Figures for Jordanian Insurance Companies for the year 2007

Insurance Company Total

Investments Total Assets

Technical Provision

Shareholders' Equity

Total Premiums Written In

Jordan

Gross Claims Paid In-Jordan

Net Profit before Tax

Arab German Insurance 12,159,129 39,815,787 8,203,401 11,242,924 22,971,779 28,534,163 1,192,626

Arab Jordanian Insurance Group 10,302,074 15,747,656 3,572,329 11,065,797 10,001,619 6,208,848 2,196,355

Al Nisr Insurance 24,228,757 28,450,949 7,959,371 17,778,963 11,577,833 7,259,713 2,784,718

American Life Insurance 76,084,572 80,779,959 48,400,293 28,227,731 17,368,355 7,393,732 6,215,433

Arab Orient Insurance 16,592,044 27,755,715 8,669,947 12,523,505 25,824,460 14,044,665 1,948,419

Oasis Insurance 2,857,815 4,327,014 2,783,770 -729,666 7,728,859 8,429,746 4,576,404

Euro Arab Insurance Group 11,218,607 16,399,646 5,758,826 7,476,389 10,891,861 7,606,277 1,773,335

Arab Assurers 10,233,540 18,223,367 4,297,301 9,245,424 10,631,528 7,985,455 1,246,825

Al- Barakah Takaful Insurance 8,377,378 9,899,246 2,404,519 5,457,203 4,546,586 4,046,908 601,876

Arab Life & Accident Insurance 17,810,955 25,758,171 11,842,538 10,272,188 14,192,8477 10,207,1468 1,365,906

Al Manara Insurance 17,298,281 18,755,736 2,832,079 14,723,582 2,910,827 3,420,677 5,322,662

Arab Union International Insurance 7,246,879 10,078,026 4,242,014 5,037,202 4,190,809 3,235,426 1,336,562

Delta Insurance 9,192,795 11,245,946 1,794,171 7,452,766 4,541,408 1,926,600 1,394,529

General Arabia Insurance 14,507,752 19,335,252 4,354,903 12,244,901 9,656,344 5,962,040 1,280,338

Gerasa Insurance 3,339,995 6,042,804 3,543,443 1,801,234 3,174,629 4,708,958 -644,068

Holy Land Insurance 6,284,347 8,715,566 3,241,819 3,444,408 5,541,746 3,880,691 172,035

Islamic Insurance 16,067,821 19,015,513 3,932,596 12,124,748 10,070,111 5,694,566 1,246,838

Jerusalem Insurance 14,082,101 18,527,357 7,123,385 9,216,596 10,217,435 6,512,720 2,060,674

Jordan French Insurance 5,326,246 20,707,079 8,896,459 3,445,875 15,880,226 15,536,915 2,607,608

Jordan Insurance 42,701,113 61,458,769 14,632,798 35,690,138 24,188,7629 11,146,87810 4,544,035

Jordan International Insurance 26,781,012 36,684,857 7,379,746 21,624,909 16,113,898 14,839,266 2,966,246

Middle East Insurance 58,763,146 66,285,046 8,942,752 39,601,120 18,767,569 10,101,073 4,385,045

National Ahlia Insurance 4,336,624 9,711,754 2,999,758 4,606,720 7,868,842 5,227,499 468,543

Philadelphia Insurance 6,011,811 8,192,692 3,145,980 4,579,284 3,590,833 3,309,843 322,316

United Insurance 13,762,832 18,636,007 3,683,115 12,312,858 7,830,430 6,918,181 396,083

AL Yarmouk Insurance 9,978,211 12,381,818 3,368,933 7,165,943 6,349,183 3,240,434 -220,221

Housing Loan 6,997,418 9,191,628 0 9,132,044 0 0 -867,956

Mediterranean & Gulf Insurance 9,791,158 14,069,879 964,844 10,095,730 5,020,175 182,251 132,279

Total 462,334,413 636,193,239 188,971,090 326,860,516 291,648,954 207,560,671 16,734,027 Source: Insurance Commission, Seventh Annul Report 2007

7 1,079,515 400,963 total premiums, gross claims paid outside Jordan respectively 8 1,079,515 400,963 total premiums, gross claims paid outside Jordan respectively 9 9,664,092, 4,408,310 total premiums, gross claims paid outside Jordan respectively 10 9,664,092, 4,408,310 total premiums, gross claims paid outside Jordan respectively

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

7

Table 4: Selected Figures for the Top Jordanian Insurance Companies by Shareholders' Equity

Insurance

Company

Total

Investment

Total

Assets

Technical

Provision

Shareholders

Equity

Total Premiums Written In

Jordan

Gross Claims Paid

In Jordan

Net Profit

before Tax

Middle East Insurance 58,763,146 66,285,046 8,942,752 39,601,120 18,767,569 10,101,073 4,385,045

Jordan Insurance 42,701,113 61,458,769 14,632,798 35,690,138 24,188,762(11 11,146,87812 -4,544,035

American Life Insurance 76,084,572 80,779,959 48,400,293 28,227,731 17,368,355 7,393,732 6,215,433

Jordan International Insurance 26,781,012 36,684,857 7,379,746 21,624,909 16,113,898 14,839,266 2,966,246

Al Nisr Insurance 24,228,757 28,450,949 7,959,371 17,778,963 11,577,833 7,259,713 2,784,718

Al Manara Insurance 17,298,281 18,755,736 2,832,079 14,723,582 2,910,827 3,420,677 -5,322,662

Arab Orient Insurance 16,592,044 27,755,715 8,669,947 12,523,505 25,824,460 14,044,665 1,948,419

General Arabia Insurance 14,507,752 19,335,252 4,354,903 12,244,901 9,656,344 5,962,040 1,280,338

Islamic Insurance 16,067,821 19,015,513 3,932,596 12,124,748 10,070,111 5,694,566 1,246,838

Arab German Insurance 12,159,129 39,815,787 8,203,401 11,242,924 22,971,779 28,534,163 1,192,626

Arab Jordanian Insurance Group 10,302,074 15,747,656 3,572,329 11,065,797 10,001,619 6,208,848 2,196,355

Arab Life & Accident Insurance 17,810,955 25,758,171 11,842,538 10,272,188 14,192,84713 10,207,14614 1,365,906 Source: Insurance Commission/ The Seventh Annul Report 2007

11 9,664,092, 4,408,310 total premiums, gross claims paid outside Jordan respectively 12 9,664,092, 4,408,310 total premiums, gross claims paid outside Jordan respectively 13 1,079,515 400,963 total premiums, gross claims paid outside Jordan respectively 14 1,079,515 400,963 total premiums, gross claims paid outside Jordan respectively

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

8

Utilizing data from Table 3, Table 4 lists the top insurance companies in terms of shareholders equity. We noticed that those companies have also, the top total investment, total assets, and technical provision, total premiums, and gross claims paid. In terms of the net profit before tax, the picture is different; as we can see, some large companies like Jordan Insurance Co. recorded the high losses JD 4.5 million, where other much smaller companies listed in Table 3 recorded relatively high levels of net profits. Two of the insurance companies shown in Table 4 have branches outside Jordan; Jordan Insurance and Arab Life & Accident Insurance.

Table 5: Selected Ratios for Jordanian Insurance Companies for the year 2007

Company Insurance

Loss Ratio (1)

Operating Profit

Margin (2)

Retention Ratio

(3)

Return on

Assets (4)

Return on

Equity (5)

Market Share Gross

Premiums Written In Jordan (6)

Arab German Ins 85% 5% 58% 3% 11% 8%

Arab Jordanian Ins 65% 15% 74% 14% 20% 3%

Al Nisr Insurance 79% 13% 61% 10% 16% 4%

American Life Ins 45% 13% 94% 8% 22% 6%

Arab Orient Insurance 82% 5% 45% 7% 16% 9%

Oasis Insurance 135% -34% 53% -106% N/A 3%

Euro Arab Assurers 87% 9% 77% 11% 24% 4%

Arab Assurance 87% 12% 73% 7% 13% 4%

Al- Barakah Takaful 101% -35% 90% 6% 11% 2%

Arab Life & Accident 74% 4% 73% 5% 13% 5%

Al Manara Insurance 353% -111% 67% -28% -36% 1%

Arab Union International

99% -10% 80% 14% 27% 1%

Delta Insurance 70% 9% 34% 12% 19% 2%

General Arabia Ins 70% 7% 39% 7% 10% 3%

Gerasa Insurance 107% -26% 81% -11% -36% 1%

Holy Land Insurance 76% 2% 83% 2% 13% 2%

Islamic Insurance 76% 0% 66% 7% 10% 3%

Jerusalem Insurance 71% 14% 66% 11% 22% 4%

Jordan French Ins 92% -2% 65% -13% -76% 5%

Jordan Insurance 74% 7% 43% -7% -13% 8%

Jordan International Ins 88% 3% 74% 8% 14% 6%

Middle East Insurance 68% 10% 43% 7% 11% 6%

National Ahlia Ins 75% 13% 50% 5% 10% 3%

Philadelphia Insurance 85% -4% 82% 4% 7% 1%

United Insurance 86% -3% 67% 2% 3% 3%

AL Yarmouk Insurance 121% -2% 51% -2% -3% 2%

Housing Loan N/A N/A N/A -9% -10% 0%

Mediterranean & Gulf 67% -6% 26% 1% 1% 2%

Total 85% 3% 61% 3% 5% 100%

1- loss ratio (for non-life written premiums inside Jordan) = net claims cost/net earned premiums 2- Operating profit margin (for written premiums inside Jordan) = net technical profit/gross written

premiums. 3- Retention ratio (for written premiums inside Jordan) = net written premiums/ gross written

premiums. 4- Return on assets = net profit before tax/total assets 5- Return on equity = net profit before tax / shareholders' equity

Source: Insurance Commission/ the Seventh Annul Report 2007

Table 5 above shows selected financial and technical ratios of the sector. The most important technical ratios in the insurance industry are loss ratio and retention ratio: the average rates for the market are 85% and 61%, respectively. For an insurance company to make a profit, loss ratio should be less than 100%. Given that other factors are stable, such as the level of risk, size of capital, and re-insurance arrangements, the insurance company’s retention ratio is very important. Higher retention indicates that the firm is retaining more risk and consequently making more

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

9

profit. If the insurance company is able to retain risk, the ratio would be higher with a higher profit margin assuming certain levels of claims paid. The retention ratio of the insurance industry in Jordan is relatively low at 61%. The low retention rate indicates that rather than retaining risk, the insurance agencies are acting as brokers: they receive commissions for policies and then resell them rather than holding the risk and managing the policy. In a technical view, to act as an insurance agency you should retain risk, handle it and receive the profit from the technical operation. When brokerage activities are predominate among firms, the firms receive quick commissions but do not contribute to increasing the profit of the sector. Ten insurance companies have retention ratios that are below the industry average in Jordan of 61%. Although these companies are small, compared to others in the market companies, their retention rates are not lower due to size but to an operational decision to broker policies. Local insurance companies need to improve their technical insurance operations to increase retention.

Table 6: Selected Ratios for the Top 8 Jordanian Insurance Companies for by Market Share

Company Insurance

Loss Ratio

Operating Profit

Margin

Retention Ratio

Return on

Assets

Return on

Equity

Market Share of

Gross Written

Premiums Inside Jordan

Arab Orient Insurance

82% 5% 45% 7% 16% 9%

Jordan Insurance 74% 7% 43% -7% -13% 8%

Arab German Insurance

85% 5% 58% 3% 11% 8%

Middle East Insurance

68% 10% 43% 7% 11% 6%

Jordan International Insurance

88% 3% 74% 8% 14% 6%

American Life Insurance (ALICO)

45% 13% 94% 8% 22% 6%

Arab Life & Accident Insurance

74% 4% 73% 5% 13% 5%

Jordan French Insurance

92% -2% 65% -13% -76% 5%

Source: Insurance Commission/ the Seventh Annul Report 2007

Utilizing the data in Table 5, Table 6 shows the top eight firms in terms of market share of written premiums which ranges from 5%-9%. The remaining companies that are shown in Table 5 have less than a 5% market share. Of the top eight, the highest retention ratio is 94% for the American Life Insurance Company (ALICO), the only foreign life branch; ALICO also has a good loss ratio of 45%. Two of the largest local companies, Jordan Insurance Company and Middle East Insurance Company, have only a 43% retention ratio.

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

11

Table 7: Selected Figures for Jordanian Insurance Market 1999-2007

Items 1999 2000 2001 2002 2003 2004 2005 2006 2007

Total Investments 149.7 146.7 150.6 169.0 214.2 264.9 410.1 408.0 462.3

Total Assets 211.0 211.0 236.6 260.5 308.5 366.1 526.2 548.0 636.2

Technical Provisions 89.9 97.9 109.3 123.4 131.6 143.2 156.2 170.8 189.0

Shareholders' Equity

85.2 85.0 88.6 90.9 124.1 161.4 277.2 285.1 326.9

Gross Premiums Written In Jordan

99.8 104.2 120.4 146.9 171.5 191.4 219.3 258.7 291.6

Net Premiums Written In Jordan

62.8 64.3 76.5 94.0 114.2 126.9 139.3 158.1 179.3

Gross Claims Paid for Premiums written In Jordan

64.0 67.7 79.8 86.0 107.7 123.9 142.8 174.5 207.6

Net Profit before Tax

7.8 5.2 6.5 12.6 22.0 40.0 90.6 21.5 16.7

Solvency Margin 204.6% 231.6% 263.2% 289.1% 253.0%

Retention Ratio 62.9% 61.7% 63.5% 64.0% 66.6% 66.3% 63.5% 61.1% 61.5%

Loss Ratio (Non-life Insurance)

78.9% 80.8% 81.7% 75.8% 78.3% 78.5% 79.5% 85.1% 85.1%

Expense Ratio (Non-life Insurance)

24.3% 27.1% 24.6% 21.3% 13.3% 12.9% 13.7% 15.0% 13.4%

Return on Assets 3.7% 2.3% 2.7% 4.8% 7.1% 10.9% 17.2% 3.9% 2.6%

Return on Shareholders' Equity

9.1% 6.1% 7.3% 13.9% 17.7% 24.8% 32.7% 7.5% 5.1%

Technical Provisions/ Shareholders' Equity

105.5% 115.2% 123.4% 135.7% 106.0% 88.7% 56.4% 59.9% 57.8%

Total Investment /Total Assets

71% 66.4% 63.6% 64.9% 69.4% 72.4% 77.9% 74.5% 72.7%

Source: Insurance Commission/ the Seventh Annual Report 2007

Table 7 shows the trend of financial and technical insurance indicators over the last nine years. While the absolute values of most figures exhibit stable growth including net profit before tax, some important technical insurance ratios, like the retention ratio has been stable but at a low rate, in terms of industry standards, of +/- 60%. The low retention rate indicates that, and supplements the discussion above in terms of life insurance, that insurance companies are not developing as agency with all the inherent risks thereof, but rather act more as brokers, in which they pass the risk on and do not retain it. Additionally, the loss ratio (net claims cost/net earned premiums) increased from 78.9% in 1999 to 85% in 2007. The increase in loss ratio is considered a negative indicator; firms are making lower profit margins because of competition in similar products that are not markedly differentiated and the large number of companies operating in a very small market.

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

11

Table 8 below depicts the types of insurance licenses available and their corresponding CPC/WTO classification.

Table 8: Classes of Insurance Business Licenses per CPC Code

CPC/WTO Code Reference Number15

License

81292 Motor Vehicle insurance services

1 Motor Insurance License

1681293 Marine, aviation and other transport insurance services

2 Marine and Transport Insurance License

3 Aviation Insurance License

81295 Fire and other property damage insurance services

4 Fire & Other Damage to Property Insurance License

81297 General liability insurance services

5 Liability Insurance License

6 Credit and Suretyship Insurance License

81296 Pecuniary loss insurance services

7 General Insurance License

81291 Accident and health insurance services

8 Medical Insurance License

81211 Life insurance and pension fund services

9 Life Assurance License

81211 Life insurance and pension fund services

10 Marriage & Birth Assurance License

81212 Pension and annuity services 11 Annuities or Pension Assurance Insurance

81211 Life insurance and pension fund services

12 Investment Linked Assurance License

81211 Life insurance and pension fund services

13 Permanent Health Assurance License

81211 Life insurance and pension fund services

14 Management of Group Pension Funds Assurance license

81211 Life insurance and pension fund services

15 Additional Insurances

Source: Insurance Commission/ the Seventh Annual Report 2007

Table 8 compares the insurance license codes granted by the Insurance Commission with its equivalent CPC codes. There are some differences in coding between the two sources such as Credit and Suretyship Insurance License, which does not have an equivalent CPC code, and marine, transport and aviation licenses are grouped under one code. Experts interviewed for the study noted that It is important to have one code of insurance license as all related technical and financial reports, data, and statistics should follow one international code. In this regard International Association of Insurance Supervision is the international organization responsible for uniformity of these codes. The reference numbers given in Table 8 are utilized in Table 9 below.

15 Reference Numbers are applied in Table 7 16 WTO 81294 Freight insurance services is covered in License No. 3

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

12

Table 9: Types of Licenses Issued to Insurance Companies

Insurance Company Types of Licenses Issued to Companies

Reference Numbers from Table 6 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Arab German Insurance √ √ √ √ √ √ √ √ √ √ Arab Jordanian Insurance Group √ √ √ √ √ √ √ √ √ √ Al Nisr Insurance √ √ √ √ √ √ √ √ √ √ American Life Insurance √ √ √ √ √ √ Arab Orient Insurance √ √ √ √ √ √ Oasis Insurance √ √ √ √ √ √ Euro Arab Insurance Group √ √ √ √ √ √ √ √ √ √ Arab Assurers √ √ √ √ √ √ √ √ √ √ Al- Barakah Takaful Insurance √ √ √ √ √ Arab Life & Accident Insurance √ √ √ √ √ √ √ √ √ √ √ Arabian Seas Insurance √ √ √ √ √ Arab Union International Insurance √ √ √ √ √ Delta Insurance √ √ √ √ √ √ √ √ √ √ General Arabia Insurance √ √ √ √ √ √ √ √ √ √ Gerasa Insurance √ √ √ √ √ √ √ √ √ √ Holy Land Insurance √ √ √ √ √ Islamic Insurance √ √ √ √ √ √ √ √ √ √ Jerusalem Insurance √ √ √ √ √ √ √ √ √ √ Jordan French Insurance √ √ √ √ √ √ √ √ √ √ √ Jordan Insurance √ √ √ √ √ √ √ √ √ √ Jordan International Insurance √ √ √ √ √ √ √ √ √ √ Middle East Insurance √ √ √ √ √ √ √ √ √ √ National Insurance √ √ √ √ √ √ √ √ √ √ Philadelphia Insurance √ √ √ √ √ United Insurance √ √ √ √ √ √ √ √ √ √ Al Yarmouk Insurance √ √ √ √ √ √ √ √ √ √ Housing Loan Mediterranean & Gulf Insurance

Source: Insurance Commission/ the Seventh Annual Report 2007

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

13

Table 9 lists the types of licenses issued to insurance companies. Most of the insurance companies, both life and non-life have been licensed under all insurance classes of business. However the trend of operations for those classes varies from one company to another, for example some composite companies, while grandfathered in with a life insurance licensure, do not actually develop their life insurance portfolio. However, whether actively utilizing all licenses obtained from the Insurance Commission, the companies keep the licenses for future opportunities. Only two insurance companies are licensed for credit insurance (No.6), the third company has been out of the market. Seven insurance companies operate as non-life insurance companies and are licensed for all the non-life classes of business. None of the insurance companies are licensed for No.7, 10, 14, .Pecuniary Loss insurance services, Marriage & Birth Assurance License, and Life insurance and pension fund services, respectively.

Life-Insurance Table 10 below gives the characteristics of the six largest life insurance providers, out of the 17 that are licensed to provide only life insurance and are operating in the market. As shown below, the largest provider of life-insurance is the foreign branch and only non-composite firm, ALICO, with a market share of 45%. The other five firms are composite. The next to the largest company is Al-Niser Al-Arabi Insurance Company with a market share of 12.2%. The lowest market share is the 3.7% held by the Islamic Insurance Company. This table indicates the lack of development in the life-insurance sub-sector in Jordan. The domination of market share (45%) by a life specialized foreign branch is due basically to the absence of local competition in life insurance. All other life-insurance providers are composite companies with no intention of developing their life insurance portfolios. Even the only Takaful composite company,(Islamic Insurance Company, with a market share 3.7%, uses its life portfolio is to serve the Islamic bank housing loan portfolio: the Jordanian Islamic Bank is the main share holder of Islamic Insurance Company.

Table 10: The characteristics of the six largest insurance companies in the market for life insurance:

Name Year established

Sub sector Domestically owned equity

(%)

Foreign equity (%)

Share of total life insurance premiums(%)

American Life Insurance Co. (ALICO)

1958 Life insurance 0% 100% 45%

Al Niser Al-Arabi insurance Co.

1976 Composite 98.3% 1.7% 12.2%

Jordan insurance Co.

1951 Composite 81.4% 18.6% 11.7%

Arab Life & Accident Insurance Co.

1981 Composite 91.7% 8.3% 6.4%

Middle East Insurance Co.

1962 Composite 93.9% 6.1% 4.4%

Islamic Insurance Co.

1996 Composite, Takaful17

94.2% 5.8% 3.7%

Source: Insurance commission

17 Takaful insurance is a type of insurance that adheres to Islamic principles in terms of transparency, risk, and interest.

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

11

Non-life Insurance Ten companies in Jordan are licensed to offer only non-life insurance. Table 9 below depicts the characteristics of the largest six providers of non life insurance, of which five are composites. The company possessing the largest non-life market share that operates as non-life only is Arab Orient Insurance. With market share of 9.8% this company is owned by a Jordanian bank, the Jordan Kuwait Bank of which the main shareholders are Kuwaiti nationals. From Table 10 and 11 we can see that the foreign equity exists in the Jordanian insurance market in differing percentages in most Jordanian companies

Table 11: Characteristics of the six largest insurance companies in the market for non-life insurance

Name Year of established

Sub sector Domestically owned

equity (%)

Foreign equity (%)

Share in total non-life

insurance premiums (%)

Arab Orient Insurance Co.

1996 Non-life 77.7% 22.3% 9.8%

Arab German insurance Co.

1996 Composite 67.2% 32.8% 8.4%

Jordan Insurance Co.

1951 Composite 81.4% 18.6% 7.9%

Middle East insurance Co.

1962 Composite 77.4% 22.4% 6.7%

Jordan International insurance Co.

1996 Composite 90.1% 9.9% 5.9%

Jordan French Insurance Co.

1976 Composite 92.5% 7.5% 5.7%

Source: Insurance commission data

Composite (life & non-life) Insurance Composite firms are represented in both Table 10 and 11 as they are allowed to offer life and non-life through a grandfather clause in the 1999 Insurance Act. As shown in Table 11, five of the top 6 companies in non-life insurance are also composite companies. Most other composite companies' and non-life companies' market share is on average less that 5%. This indicates the large number of small insurance companies operating in the market. Takaful Insurance Takaful insurance, roughly translated as “Joint Guarantee,” is Islamic insurance and adheres to Islamic principles. Takaful products are structured to remove three key elements not acceptable according to Islamic principles;

Contract of transparency (Al-Gharar) Other insurance companies may obscure the nature of their clients business and may be insuring prohibited activities that are not acceptable and not disclosed, for example, the insuring of a restaurant that sells alcohol.

Gambling or Game of Chance (Al-Maisir) Companies may have invested in stock market, which is considered speculation.

Interest income or Expense (Al-Riba) The Takaful Products offer similar benefits and features of traditional products.

In the Arab region, the use of Takaful insurance varies from one area to another. However the Arab area could be sub-divided into three main sections as shown in Table 12, where Jordan considered being within Arab Eastern countries, along with Syria, Palestine, Lebanon and Yemen.

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

15

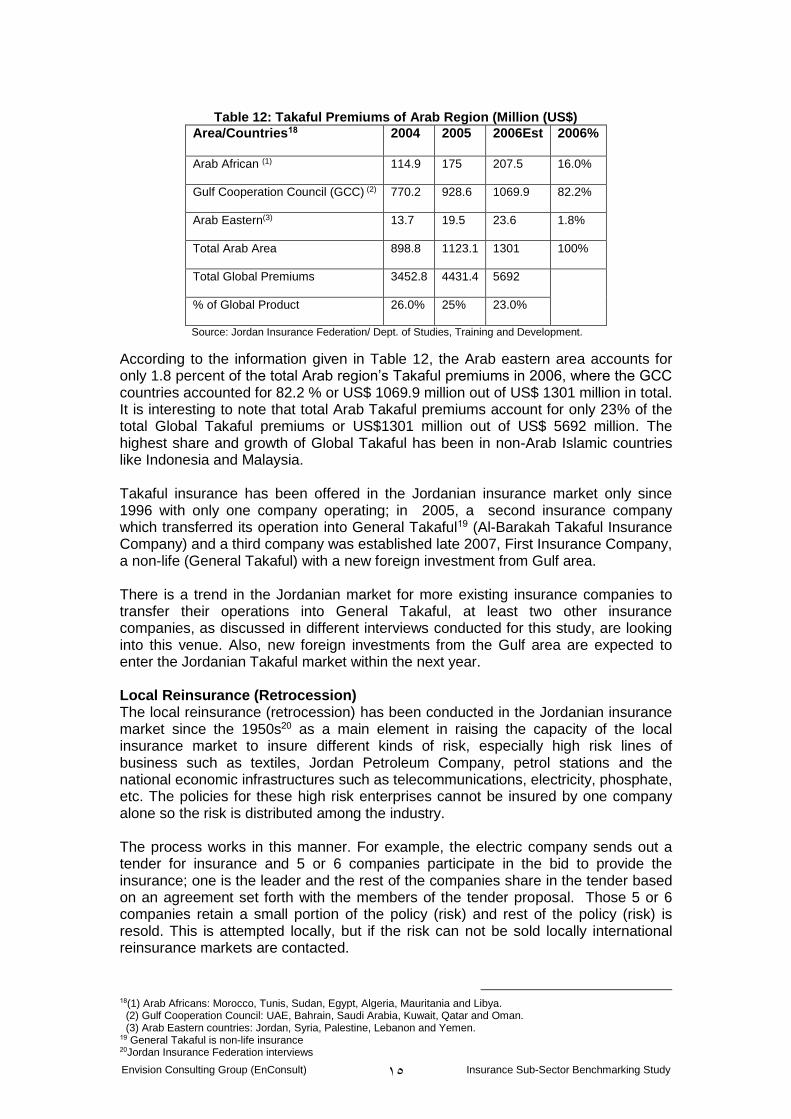

Table 12: Takaful Premiums of Arab Region (Million (US$)

Area/Countries18 2004 2005 2006Est 2006%

Arab African (1) 114.9 175 207.5 16.0%

Gulf Cooperation Council (GCC) (2) 770.2 928.6 1069.9 82.2%

Arab Eastern(3) 13.7 19.5 23.6 1.8%

Total Arab Area 898.8 1123.1 1301 100%

Total Global Premiums 3452.8 4431.4 5692

% of Global Product 26.0% 25% 23.0%

Source: Jordan Insurance Federation/ Dept. of Studies, Training and Development.

According to the information given in Table 12, the Arab eastern area accounts for only 1.8 percent of the total Arab region’s Takaful premiums in 2006, where the GCC countries accounted for 82.2 % or US$ 1069.9 million out of US$ 1301 million in total. It is interesting to note that total Arab Takaful premiums account for only 23% of the total Global Takaful premiums or US$1301 million out of US$ 5692 million. The highest share and growth of Global Takaful has been in non-Arab Islamic countries like Indonesia and Malaysia. Takaful insurance has been offered in the Jordanian insurance market only since 1996 with only one company operating; in 2005, a second insurance company which transferred its operation into General Takaful19 (Al-Barakah Takaful Insurance Company) and a third company was established late 2007, First Insurance Company, a non-life (General Takaful) with a new foreign investment from Gulf area. There is a trend in the Jordanian market for more existing insurance companies to transfer their operations into General Takaful, at least two other insurance companies, as discussed in different interviews conducted for this study, are looking into this venue. Also, new foreign investments from the Gulf area are expected to enter the Jordanian Takaful market within the next year. Local Reinsurance (Retrocession) The local reinsurance (retrocession) has been conducted in the Jordanian insurance market since the 1950s20 as a main element in raising the capacity of the local insurance market to insure different kinds of risk, especially high risk lines of business such as textiles, Jordan Petroleum Company, petrol stations and the national economic infrastructures such as telecommunications, electricity, phosphate, etc. The policies for these high risk enterprises cannot be insured by one company alone so the risk is distributed among the industry. The process works in this manner. For example, the electric company sends out a tender for insurance and 5 or 6 companies participate in the bid to provide the insurance; one is the leader and the rest of the companies share in the tender based on an agreement set forth with the members of the tender proposal. Those 5 or 6 companies retain a small portion of the policy (risk) and rest of the policy (risk) is resold. This is attempted locally, but if the risk can not be sold locally international reinsurance markets are contacted.

18(1) Arab Africans: Morocco, Tunis, Sudan, Egypt, Algeria, Mauritania and Libya. (2) Gulf Cooperation Council: UAE, Bahrain, Saudi Arabia, Kuwait, Qatar and Oman. (3) Arab Eastern countries: Jordan, Syria, Palestine, Lebanon and Yemen. 19 General Takaful is non-life insurance 20Jordan Insurance Federation interviews

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

16

Auxiliary services (Insurance Supportive Services) Auxiliary services consist of seven insurance support services that are shown in Table 13 below. Auxiliary services in the Jordanian insurance market have been developed through out the last decade due to the regulatory framework that established the Insurance Commission of Jordan in 1999 and placed this component of the insurance sector is under its purview. Table 13 shows the development trend and growth of auxiliary services since 2003. As shown above, the largest percentage growth was in Insurance Consultancy which grew over 57% over the period. Actuarial Services grew over 30%, followed by insurance brokers at 22%

Table 13: Development Auxiliary Services Professionals 2003-2007

Auxiliary Service Professions

2003

2004

2005

2006

2007

Growth %

Insurance Agent 247 286 392 385 426 11%

Insurance Brokers 15 24 36 46 56 22%

Reinsurance Brokers - - 1 4 4 0%

Loss Adjuster 38 36 33 33 37 12%

Actuarial Services 17 6 6 10 13 30%

Insurance Consultancy - - 1 7 11 57%

Health Third Party Administrators - - - 10 11 10%

Source: Insurance Commission Annual Report 2007

Table 14 shows the insurance premiums for tight agents,21 brokers22, and bancassurance23 for the year 2007. Tight agent production accounts for the highest share, 16% or JD 46 million of JD 292 million, among the other production channels; brokers constitute 5% and bancassurance 0.4%. If we eliminate the motor premium production (car insurance) of tight agents (JD 27 million out of JD 46 million), the share of 16% would drop to 6.5% and the broker’s premium production would decrease to 2%.24 These conclusions indicate clearly how the contribution of insurance premiums production channels in the market is still very weak because the majority of auxiliary service premiums is related to car insurance. Production of car or motor premiums is very easy and straight forward and does not promotes agency. IC needs to take more steps to increase and strengthen those important production channels.

21A tight agent is an agent that can only be an agent for one insurance company 22The broker represents the client and can therefore deal with any insurance company 23 A commercial bank sells an insurance product. The bank would be a tight agent for a particular insurance company; however they are classified as bancassurance. 24 JD 12 million - JD 5.7 million /JD 292 million

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

17

Table 14: Insurance Premiums Production Channels for 2007

Insurance license Tight agents Brokers Bancassurance

Life 4,335,456 579,090 1,043,793

Motor 27,322,815 5,682,243 271,123

Marine & Transport 2,450,871 1,008,296 0

Aviation 0 516,344 0

Fire & Other Damage to Property 4,471,325 1,157,542 0

Credit and Surety ship 0 0 0

Others 712,288 482,018 9,501

Health 6,751,075 2,743,102 0

Total 46,043,923 12,168,637 1,324,418

Source: Insurance Commission Annual Report 2007

3.0 General Business Environment Certain economic activities, like investment in undeveloped land and developed property registered the highest rate of growth and development over the last decade, both on the domestic level and in terms of foreign investment from primarily the Gulf area. The Jordanian insurance sector is directly and positively affected by these developments, as insurance is essential to maintaining the stability and security of these investments by covering any risk that these investments may face. The effect and evidence within the insurance sector is noted by a steady growth of insurance premiums on an average of 15% over the last few years, according to the Insurance Commission25. On the International level, the Jordanian insurance sector has also been affected negatively in certain areas. Two important examples can be noticed in this regard: 1. The events of September 11, in the USA caused many problems for the Jordanian insurance sector regarding the high cost, terms, and conditions of re-insurance packages that the local insurance market obtains from international re-insurance markets. As mentioned above, there are no Jordanian re-insurance companies currently operating in the market26. Leading insurance groups started to raise their prices of re-insurance and institute tight terms and conditions after 9/11. The result was that local insurance companies had difficultly obtaining re-insurance coverage from those leading groups and local companies were forced to obtain re-insurance coverage form other sources. As a result, unsecured insurance companies started to enter the local market. Local companies sold to unsecured reinsurance companies to keep their retention rates low so most of those premiums went to the international re-insurance companies and was not held domestically. For example if a local company sells 97% of policy with a 100JD premium to an international re-insurance firm, 3JDs of the premium stays in Jordan but 97 JD goes to the international market and does not help the local economy.

25 Interviews at the insurance commission 26By law Jordanian companies can be licensed for re-insurance however local insurance companies are not interested in the market because the re-insurance companies have to possess very high levels of capital (US$100,000,000 minimum capital requirement);.Moreover, the local market is very small. In re-insurance, one company buys risk from many among different markets regionally or around the world as compared to retrocession which is the pooling of local resources. Re-insurance is a cross border operation and companies have to be able to do business around the world.

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

18

Based on interviews with insurance agents, brokers, reinsurance brokers, loss adjusters, insurance consultant, and health third party administrators (TPA), participants feel that while the IC passes down the required legislative rules for licensing auxiliary services according to the best international practices, local field practices, in most cases, are far below international standards with regard to the code of ethics and conduct, claims handling, and insurance technical knowledge. Moreover, efficient mentoring of regulations related to those services is

lacking.

2. The mortgage crisis that started in the USA four years ago has also affected

the sector as well. Foreign and local investors established a mortgage insurance company two years ago, during the real estate boom, that specialized only in the insurance of housing loans that Jordanian banks offered to individuals and corporations. The company was licensed by the IC with very high expectations that this line of insurance would develop on the local and regional level. Unfortunately, the company did not issue any insurance policies for the two years it was in existence. The company's license was cancelled in January 2009 by the IC, causing the loss of one of the insurance companies listed in Figure1, the Housing Loan Insurance Company (Darkom). The reason for the company not issuing a single housing loan insurance policy for two years can be attributed to the USA mortgage crisis coupled with a weak public awareness of the insurance market.

The setting up of new agencies or insurance brokerage firms lies within the purview of the Insurance Commission. The Companies Law does not apply to firms providing insurance and insurance service firms.

4.0 Legislative and Regulatory Environment

4.1 Measures related to domestic regulation Insurance Commission of Jordan (Regulator) In 1999, the government of Jordan passed the New Framework of Insurance Supervision, which accompanied the establishment of the Insurance Commission according to Insurance Regulatory Act No. 33 of 1999 and the amendments thereof. The IC has a corporate status and is financially and administratively independent. The Commission's main objectives are to protect the rights of the insured, improve the performance of the insurance companies and develop insurance products in the Kingdom. Since the establishment of the Commission, a number of pieces of legislation including regulations, instructions and decisions were issued pursuant to the

The sequence of these events allowed for non-internationally rated re-insurance companies to enter the Jordanian insurance market; providing the local market with un-secured re-insurance packages, which forced the Insurance Commission (IC) to issue a regulation, The Re-Insurance Arrangement Instruction No. (4) of 2002 (Re-insurance Instructions and the Amendment there of), .which regulates re-insurance arrangement that the local insurance companies have with international re-insurers. The Act required that all policies must be written and set forth procedures to document and in writing how the re-insurance will take place, and placed guidelines for which of the international rated insurance companies were allowed to operate in the market. In regards to tendering, the Act created written procedures of handling tenders for re-insurance required that companies must have made re-insurance arrangements before entering the tender, among others. This regulation has been the first of its nature on the regional level and has a position effect to get the international credit rating in three years time to maintain their market share of re-insurance in Jordan.

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

19

Insurance Regulatory Act No. 33. These pieces of legislation regulate financial, corporate, and the market issues in accordance with the needs of the Jordanian insurance market and in keeping with recently developed international standards. The most important topics that the legislation covers is minimum capital of insurance and reinsurance companies, solvency margins, reinsurance, technical provisions, corporate governance, professional code of conduct and ethics, basis of investing the assets of insurance companies and regulating the business of insurance supporting services providers such as insurance agents and brokers, reinsurance brokers, loss adjustors, actuaries and administrating expenses and medical insurance services. The main source of IC funds is the annual fee payable by the insurance company, whereby the percentage shall not exceed 0.75 % of the gross written premiums. Annex No.2 shows the main sources of IC funding. The IC follows the rules of insurance supervision recommended by International Association of Insurance Supervision (IAIS), and the latter's Insurance Core Principles (ICPs) are integrated into IC regulations. The core principles are provided in Annex 3.

Most of the legislation issued by the Insurance Commission is posted on the IC’s website: www.irc.gov.io. The number of regulations, instructions and decisions are to numerous to list here, however a complete listing is provided in Annex 6. The table below provides the number of edicts issued over the period 1999, the date of establishment of the IC, to 2007 per the phases of the IC's chronological legislative framework.

Table 15: The Legislative Framework of Insurance Sector

Phases No. of

Regulations(1)

No. of Instructions(2)

No. of Decisions(3) Total

1st Phase 1999-2003

6 12 11 29

2nd Phase 2004-2006

1 17 28 46

3rd Phase 2007-To date

1 4 10 15

Total 8 33 49 -

(1) Regulations: Issued by the Council of Ministers upon a recommendation of IC. (2) Instructions: Issued by the Board of Directors of IC. (3) Decisions: Issued by the Director General of IC.

IC’s three-year strategy 2009-2011 points out that IC will develop its legislative framework up to the international insurance supervision practice, and be able to issue an average of six legislative instructions on a yearly basis. This would reflect the advanced and positive legislative environment that IC trying to accomplish within the next three years. However, as stated earlier, despite the number of pieces of model legislation regulating the sector, monitoring of the regulations and compliance is weak because although the IC now has 78 professional supervisory staff, it still does not have the capacity in terms of manpower to monitor effectively.27 Moreover, the expected issuing of six legislative instructions (Regulations, Instructions, Decisions) on yearly basis for the period of 2009-2011, taking into account the above set of legislative instructions already issued, may have an adverse effect on the sector. There should be a balance between the issuance of regulations, close monitoring of the regulations, and the evaluation of its effect over the sector by an independent professional party. A stable legislative strategy is always required and expected by both local and foreign investors toward reaching advance international best practices environment.

27Jordan Insurance Federation Interviews

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

21

Professionals from The Jordanian Insurance Federation, the membership of which encompasses all the insurance companies and auxiliary services professionals, who were interviewed for this study agreed that the insurance market was highly and heavily regulated in a very short period of time from 2003-2006 to the extent that the ability of the IC to monitor the number of regulations is questioned. According to the interviews, besides a shortage of manpower, there a high level of turnover in IC staff because financial packages in the private sector are much more attractive than those of the IC, which affects IC effectiveness. Consistency is also an issue not only in terms of monitoring but in terms of regulation issuance: insurance companies face new regulations on a continuous basis, which makes it difficult for the companies to comply with such a large number of regulations. This is especially true because most insurance companies in Jordan are small in size and their market share of premiums is less than 5%, according to IC’s sources. To meet the requirements of the new regulations, more administrative and technical operational expenses are required, which negatively affects the local companies because they do not have the manpower to keep up with all regulations effectively. Regulations to Establish an Insurance Company

Under "Instruction No. 1 of 2003: Instructions for Granting and Renewing a License to Transact Insurance Business and the Amendments Thereof", the following requirements must be met to establish an insurance company as set forth in regulation. The full instruction is provided in Annex: ARTICLE 3 A. The following data must be provided.

1) Type of insurance required to be transacted. 2) Classes of insurance required to be transacted. 3) Authorized capital and the amount earmarked for underwriting. 4) Names of the constituents, chosen addresses for the purpose of notification

and the number of shares for each of them. 5) Name and address of the legal counselor during establishment. 6) Name and address of the Auditor during establishment. 7) Name and address of the Actuary during establishment. 8) Name and address of the accredited bank by the constituents during

establishment. B. Along with the following documents

1) Signed memorandum of association and articles of association of the Company.

2) Constituent minutes of meetings that include the election of the constituents committee which shall supervise the establishment procedures and the authorized signatories during establishment.

3) Detailed information about the constituents, including information about their educational qualifications, experiences, ownership in other companies and their membership in the board of directors of these companies.

4) Business Plan for the first three financial years of the operation of the Company.

5) A certificate from the Actuary that includes his approval based on calculating the premium rates; the adequacy of the Technical Provisions, and the possibility of compliance with the Solvency Margin and the Minimum Guarantee Fund during the first three years of the operation of the Company.

6) A list of the proposed names for the post of the director general of the Company and the key employees therein, with a detailed description that includes the qualifications and expertise of each of them

7) Copies of the agreement forms that will be concluded with insurance Agents, insurance Brokers, Reinsurance Brokers and the providers of insurance services.

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

21

8) Proof of paying the fees and charges legally determined. 9) Any other requirements, data, documents or information requested by the

Director General. C. The applicant shall present a written declaration that all the data and documents submitted correct and consistent with the provisions of the Act, Regulations, Instructions and Decisions issued pursuant thereto, as the case may be. ARTICLE 4 Also the following must be submitted according to the section given alphabetically below:

a) A detail business plan that includes a strategic plan, activates, organizational chart, details of computerized systems to be used

b) The types of obligations and liabilities and risks of company c) Projected Financial Statement for 3 years d) Distribution Channels e) Re-insurance arrangements f) Statement of each type of insurance policy offered g) Technical basis proposed by an actuarial for each type of business h) Projection of business development i) Written company policies, procedures and system, including corporate

governance, anti-money laundering and secure Information Technology systems.

j) Asset and liability management policy k) Emergency strategy l) Description of the accounting system m) Human Resources plan

A proposed financial statement for 5 years based on sensitivity analysis must also be submitted. Article 7 stipulates that the applicant must show what value-added will be given to the sector by the granting of the application. The proof of value-added has now become an important criterion for whether the IC issues a license for a new company. Applicants are notified in one month as to the completeness of the application; final approval takes 3 months according to the regulation. After approval, a financial certificate from a bank approving the payment of the full minimum capital is required. To open a foreign branch, all of the above requirements must PLUS the ones given below:

1) Detailed description of the qualifications and expertise for the Authorized Manager.

2) A copy of the license to transact insurance business in the home country 3) Certified statement that proves the solvency margin of the foreign company

from its regulator 4) Audited balance sheet for three years 5) Profile of the mother company 6) Last annual report of the mother company 7) Proof that foreign company is assigned proactive credit rating (top ranking,

Group1) 8) Other requirements as stipulated by the Secretary General 9) Application for transacting insurance types or classes.

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

22

Other Regulatory Bodies Currently, different independent regulators like the Insurance Commission, Stock Exchange Commission, Central Bank of Jordan, and the Companies Controller Department have there own regulations pertaining to insurance and therefore make it extremely difficult for insurance companies to comply and deal with the edits of those authorities; especially in some situations where no cooperation is existent between authorities. For example the situation arises where one regulator could issue a regulation, which may adversely affect the regulation of another independent regulator; making the companies comply with the first one, while not being able to comply with the second regulation. The Jordanian Insurance Federation, which encompasses all the insurance companies, has lobbied for a more comprehensive and integrated legislative and regulatory environment from the Government, under which financial sector supervision would be under one regulatory independent authority similar to that of Canada or the UK.

There are also public shareholding companies operating in the Jordanian financial sector that are selling insurance related services to certain lines of business in the local market but are not regulated under the IC. Some are under the supervision of the Central Bank of Jordan, such as the Loan Guarantee Company that operates as an insurance company; it issues securities for banks that give small loans and export guarantees to exporters. Others like health and private pension funds have no supervision; they have their own independent regulators. Islamic Banking Regulations Islamic Banks operating as Jordanian Banks are regulated by the IC. The Islamic Financial Services Board (IFSB) is the equivalent for the Islamic insurance market of the International Association of Insurance Supervisors-IAIS. The two organizations work together and complement each others work. The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI); is working to establish national regulatory frameworks for the Islamic financial industry. Currently the IC does not have the means to monitor where or not the Islamic insurance companies are in actuality complying with Sha'ria law. Jordan Insurance Federation (JIF) Jordan Insurance Federation is the legal representative of all insurance companies operating in the market. The Federation in its current status was established in the mid 1989 and has the following key functions:

The legal representative of all insurance companies

Manage the pool of 3rd -party foreign motor insurance across the board of Jordan.

Manage the implementation of the Orange Card Agreement between some Arab countries, that is the 3rd -party motor insurance between the member countries with regard to premiums, and claims settlement. There is an office in each insurance company federation of all members.

Serve the insurance companies by holding of different training courses for their staff.

Independent authorities that regulate the financial sector should have a high level of cooperation and create MOUs between them. Because financial services today are highly complicated and integrated, banks are offering different insurance products such as bancassurance (the selling of insurance products by banks). The absence of efficient cooperation and sharing of information may lead to an unhealthy situation;

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

23

As a member in the Arab Insurance Federation, Jordan Insurance Federation held and hosted different conferences, and training courses on the Arab regional level.

JIF also manages special pools of insurance underwriting for certain lines of businesses, where some insurance companies agree to participate, in those pools, to underwrite policies for hard to insure business.28 Participation in special pools of insurance is not mandatory.

Membership in the federation is mandatory for all insurance companies operating in the market. There are 29 insurance companies that make up the general assembly of the federation. The General assembly selects the Board of Directors and the Chairman of the federation. 4.2 Measures related to professional qualification As set for by Insurance Commission regulations, the following requirements are set upon the professions listed below: Insurance Agent

1) A diploma degree -2yr degree- in any subject 2) Security clearance from the Public Security Department 3) 2 years experience in insurance or a 30-day training certificate of completion

from an insurance company 4) Official identification (passport, national card) 5) An agency agreement with an insurance company 6) Two photos 7) Sit for the exam given by the Insurance Commission 8) Fee of 250JD

To Be a Broker:

1) A four- year university degree OR 8 years experience in an insurance company

2) Senior position in an insurance company for 5 years 3) Security clearance from the Public Security Department 4) Sit for the exam given by the Insurance Commission 5) Fee is 500JD

Insurance Consultant

1) A four- year university degree plus 12 years experience OR if no degree, 20 years experience in an insurance company

6) Security clearance from the Public Security Department 7) Sit for the exam given by the Insurance Commission 8) Fee is 500JD

Re-insurance broker

2) A four- year university degree plus 12 years experience OR if no degree, 20 years experience in an insurance company

3) Security clearance from the Public Security Department 4) Sit for the exam given by the Insurance Commission 5) Fee is 1000JD

Loss Adjusters

1) A four- year university degree plus 5 years experience 6) Security clearance from the Public Security Department 7) Sit for the exam given by the Insurance Commission

28 For example motor insurance for large hauling vehicles that most insurance companies would not want to insure.

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

21

2) Fee is 1000JD Actuarial

1) Must hold the rank of Fellow in one of the five international Actuarial Institutes( (British, American, Swiss, German, French)

2) If rank is below full Fellow, such has as an Associate, must have 5 years experience under the supervision of a member who is a Fellow.

3) Fees are 500JD All IC staff must complete various professional training programs and acquire international qualification in insurance, accounting and finance. The IC invests heavily in further professional training to keep its staff educated on recent international practices in insurance supervision. The professional training programs such as CII, LOMA, BIFI, and CFA. New regulations state that agents and employees of the IC and employees insurance companies should hold at least a first level university degree. However many practitioners currently operating in the market do not hold a degree. 4.3 Effect of measures on international participation in the market

According to IC officials, the assessment of compliance of the Jordanian insurance sector to the Core Principle (CPs) has reached 85%. It is expected that at the end of the three-year strategy of the IC this percentage of compliance will reach 94%. This indicator will have a very positive effect with regard to the advancement of insurance supervision, which will make Jordan more attractive to international investment groups to enter the Jordanian insurance market. Furthermore, the Insurance Commission of Jordan has a strategic objective of developing Jordan as a regional insurance centre in the area. The IC has already put into action its three-year strategy 2009-2011 whereby, international insurance investment groups will be invited to Jordan to start their operations in a very advanced international insurance supervisory framework and environment. It is expected according to IC’s above strategy, that 15 international insurance companies and auxiliary insurance services companies will enter the Jordanian insurance market, with IC inviting on average five companies each year starting in the year 2009.29 The heavy regulations environment according to the best international practices is a positive security factor for most foreign investment. However, once these firms have entered the market, the number of regulations and lack of adequate monitoring may lead less than expected results.

5.0 GATS Restrictiveness Measures 5.1 GATS commitments of the sector/ sub- sector Table 16 shows the GATS restrictiveness measures regarding the insurance sector, the limitation on market access, and national treatment according to the following modes of supply:

1. Cross-Border 2. Consumption abroad 3. Commercial presence 4. Presence of natural persons

The restrictions for entering the local insurance market have been removed recently due to the fact that IC is a member of IAIS and practices best practices. And the IAIS

29Insurance Commission Three- Year Strategy (2009-2011)

Envision Consulting Group (EnConsult) Insurance Sub-Sector Benchmarking Study

25

supervises According to WTO regulations; no national insurance company should enjoy a privileged treatment over a foreign insurance company or a foreign branch.

Table 16: GATS Commitments Insurance Sub-Sector Category Limits on Market Access Limits on National Treatemetn

a) Life, insurance services

including health insurance services (CPC 81211) and (CPC 81212) excluding pension fund management.

b) Non- life insurance services (including accident insurance) (CPC 8129)

1) Commercial presence is

required. 2) None (Unbound) 3) Access is restricted to public

share holding companies constituted in Jordan and to branches of foreign insurance companies.

4) Unbound, except as indicated in the horizontal section.

1) Commercial presence is

required. 2) None (Unbound) 3) None 4) Unbound, except as indicated

in the horizontal section.

c) Reinsurance and retrocession (CPC 81299)

1) None 2) None 3) Access is restricted to Public

Share Holding companies constituted in Jordan and to branches of foreign reinsurance companies.

4) Unbound, except as indicated in horizontal section.

1) None 2) None 3) None 4) Unbound, except as indicated

in horizontal section.

d) Auxiliary Services (CPC 8140)

Agency services (CPC 81401)

1) None (Unbound) 2) None (Unbound) 3) None (Access restricted to

Jordanian natural persons, Jordanian general partnerships with majority ownership by Jordanians, and limited liability companies with Jordanians as majority in board of directors. Insurance agent or director of agent company must be Jordanian nationals)

4) Unbound, except as indicated in the horizontal section. Insurance agent or director of agent company must be Jordanian nationals.

1) None (Unbound) 2) None (Unbound) 3) None 4) Unbound, except as indicated

in the horizontal section.

Insurance consultancy (CPC 81402 excluding

pension consultancy)

1) None 2) None 3) None 4) Unbound, except as indicated

in horizontal section.

1) None 2) None 3) None 4) Unbound, except as indicated

in horizontal section.

Average and loss adjustment services (CPC 81403)

1) None (Unbound) 2) None (Unbound) 3) None 4) Unbound, except as indicated

in the horizontal section.

1) None (Unbound) 2) None (Unbound) 3) None 4) Unbound, except as indicated

in the horizontal section. Source: WTO Services Database

The Jordanian insurance sector, embodied by the Insurance Commission, complies with WTO recommendations. Thus, every party operating in the Jordanian insurance market as an insurance company, branch of an insurance company, or an auxiliary service receives equal treatment according to IC officials.