financial analysts meeting december 7, 2005

TRANSCRIPT

Lighting Strategy: Accelerating profitable growth

- Building on strength in existing businesses - Shaping the future in new business areas

Theo van Deursen, President & CEO Philips Lighting

Financial Analysts MeetingDecember 7, 2005

2

Forward Looking StatementsForward Looking StatementsThis document contains certain forward-looking statements with respect to the financial condition, results of operations and business of Philips and certain of the plans and objectives of Philips with respect to these items (including, but not limited to, cost savings) in particular the outlook paragraph in this report. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements. These factors include, but are not limited to, levels of consumer and business spending in major economies, changes in consumer tastes and preferences, changes in law, the performance of the financial markets, pension costs, the levels of marketing and promotional expenditures by Philips and its competitors, raw materials and employee costs, changes in exchange and interest rates (in particular, changes in the euro and the US dollar can materially affect results), changes in tax rates and future business combinations, acquisitions or dispositions and the rate of technological changes. Statements regarding market share, including as to Philips’ competitive position, contained in this document are based on outside sources such as specialized research institutes, industry and dealer panels in combination with management estimates. Where information is not yet available to Philips, those statements may also be based on estimates and projections prepared by outside sources or management. Rankings are based on sales unless otherwise stated.

Use of non-GAAP InformationIn presenting and discussing the Philips Group’s financial position, operating results and cash flows, management uses certain non-GAAP financial measures. These non-GAAP financial measures should not be viewed in isolation as alternatives to the equivalent GAAP measure and should be used in conjunction with the most directly comparable US GAAP measure(s). A discussion of the non-GAAP measures included in this document and a reconciliation of such measures to the most directly comparable US GAAP measure(s) are contained in this document.

3

Agenda

• Philips Lighting

• Shaping the future

– LCD backlighting– Solid State Lighting

• Profitable growth via key business drivers

• Continuous improvement, control of costs and assets

4

Philips Lighting

Our Mission

We understand people…and improve their lives with lighting

Our Vision

The Clear Leader; Setting the pace in the lighting industry

5

Philips Lighting

2004

Sales EUR 4.6 billionComparable Sales growth +5%

EBIT EUR 591 millionor 13.1% of sales

Net Operating Capital EUR 1.5 billion

Return on NOC 37%

Employees 44,000

Capital expenditure EUR 189 millionDepreciation EUR 201 million

2005 Q3 YTD+ 5%

Excl. Lumileds

6

Philips Lighting: Key Product Areas

Lamps Lighting Electronics

LuminairesAutomotive, Special Lighting & UHP

Solid State LightingModules

7

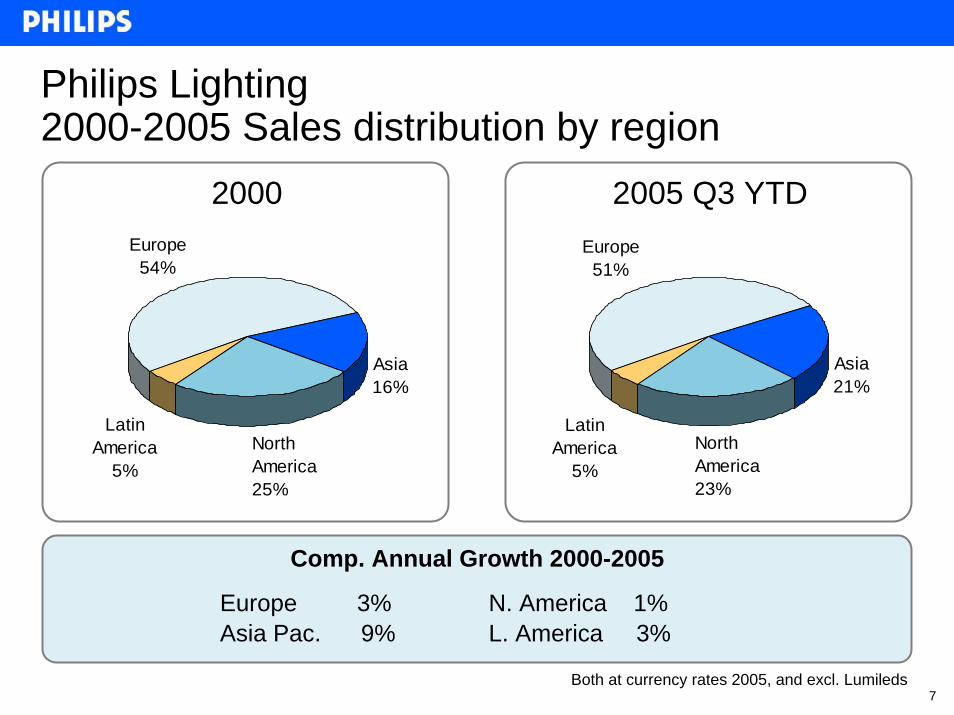

Asia21%

Latin America

5%North America23%

Europe51%

Asia16%

Latin America

5%North America25%

Europe54%

Philips Lighting 2000-2005 Sales distribution by region

2000 2005 Q3 YTD

Comp. Annual Growth 2000-2005

Europe 3%Asia Pac. 9%

N. America 1%L. America 3%

Both at currency rates 2005, and excl. Lumileds

8

Philips Lighting – Sales per Business Group

49%

15%

18%

18%

Lamps

AutomotiveSpecial Lighting

& UHP

Luminaires2005 Q3 YTD

Lamps 3%Luminaires 0%

ASU 9%Lighting Electronics 2%

Comp. Annual Growth 2000-2005

Lighting Electronics

Excl. Lumileds

9

Philips Lighting: leading around the worldValue market shares per business per region 2005

Not Applicable

Not Applicable

W. Europe L. America Japan

Lamps

Lumi-naires

LightingElec.

Auto-motive

Asia/PacificN. America TotalE. Europe

Not Applicable

number 1 not in top 3number 2 or 3

SpL.

UHP

10

Philips Lighting strategy

• Profitable growth via

• Building on strength– In emerging countries– With leading (global) accounts– In Business to Business

• Shaping the future– In (consumer) display applications– In Solid State Lighting (LEDs, OLEDs, lasers)

11

Philips Lighting strategy

• Building on strength, Shaping the future via

• Key business drivers– End user driven innovation, building on technology leadership– Marketing excellence– Supply excellence– Committed and competent people, living our values

• on basis of:– A learning organization (continuous improvement)– Control of costs and assets

12

Agenda

• Philips Lighting

• Shaping the future

– LCD backlighting– Solid State Lighting

• Profitable growth via key business drivers

• Continuous improvement, control of costs and assets

13

Growth in (consumer) display applicationsPhilips Aptura for LCD backlighting systems

• New fluorescent solution for LCD: Creating a new viewing experience

• Wider viewing angle• Better contrast• Less motion blur

• Launch Q1 2006

14

The LCD TV market is growing fast

0

5

10

15

20

25

30

2005 2006 2007 2008

Million units LCD TV (>=32”) market volume

15

Aptura creates clear market excitement

Aptura is awarded at the CES (Jan.’05), at the SID (May’05) and received the Eisa Innovation Award at the IFA Sept.’05.

16

Aptura LCD backlighting:Advanced manufacturing capabilities (China)

17

Agenda

• Philips Lighting

• Shaping the future

– LCD backlighting– Solid State Lighting

• Profitable growth via key business drivers

• Continuous improvement, control of costs and assets

18

A brief history of (white) light sources

Open wood fire Oil Filament Gas discharge

Solid State Laser

In-organic LED

Organic LED

19

Lumileds’ leadership in high power in-organic LEDs

• JV established in 1999

• Philips increased ownership to 96.5% in November 2005

• Industry leader in high power LED’s (LUXEON platform)

20

Lumileds Leadership

Luxeon High Power LED

• In all 3 colours and white

• Highest performance in – Lumens/Watt– Lumens/$– Lumens/cm2

• Longest life (50K hrs at 70%)

21

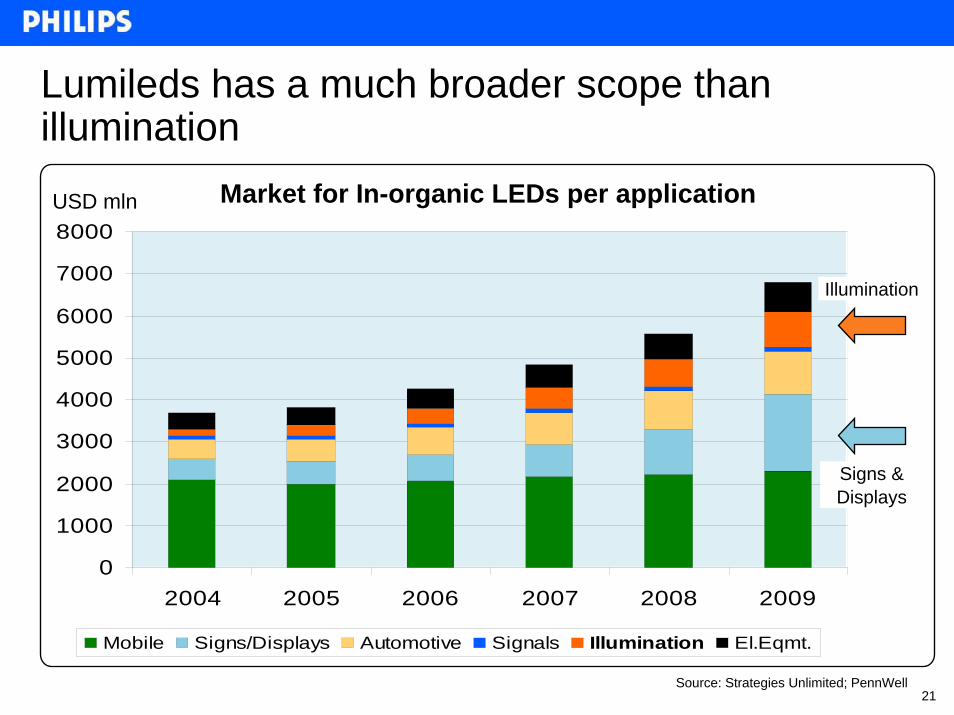

Lumileds has a much broader scope than illumination

Source: Strategies Unlimited; PennWell

0

1000

2000

3000

4000

5000

6000

7000

8000

2004 2005 2006 2007 2008 2009

Mobile Signs/Displays Automotive Signals Illumination El.Eqmt.

USD mln Market for In-organic LEDs per application

Illumination

Signs & Displays

22

Lumileds is well positioned to continue its past (above market average) growth

Illumination + automotive front lighting

LCD Backlighting

Mobile Flash

Automotive exterior

Automotive interior

Mobile displays

Signs

= Lumileds key player

23

Lumileds performance

August 04 / July 05

Sales: US$ 324 million

EBIT: US$ 83 million

Annual Growth: 28%

Operating margin: 25.6%

Employees: 1760

24

Lumileds: Increases Philips Lighting growth by 1%

46%

5%15%

17%

17%

Lamps

Lighting Electronics

AutomotiveSpec.Light.

& UHP

Luminaires

2005 Q3 YTD

Comp.An.Growth 2000-2005

Lamps 3%

Luminaires 0%

ASU 9%

L.Electr. 2%

Lighting 2,8%

Lumileds 27%

Together 3,8%Lumileds

25

Why acquire Agilent’s stake in Lumileds?

• Builds on Philips’ leading global position in lighting

• Gives Philips a controlling share in the leading LED company

• Extends Philips’ involvement to all segments of the LED value chain

• Gives Philips access to strong portfolio of over 200 LED patents

• Deepens Philips’ presence in the higher-growth, higher-margin segments of the LED market

26

We will continue the value creation

• Lumileds will continue with its success in value creation– High % of Lumileds activities are outside Lighting business scope– Lumileds will operate separately in these markets– They will drive the technology and learning curve

• Lumileds and existing Lighting Businesses will be aligned in addressing existing Lighting markets and customers

• In short: – Lumileds is now a separate unit in Lighting – Alignment with existing businesses where it makes business sense

27

Financial targets of Lumileds

• Philips will consolidate Lumileds as of November 28, 2005.

• We aim for Lumileds to achieve annual Sales growth of 25%, and 25% EBIT based on pre-acquisition accounting.

• The purchase price allocation will result in one-time charges for in process R&D assets and for continued amortization of other intangible assets.

• Impact on EBIT of Lighting will be known by year-end.

28

Philips Lighting operates in the In-organic LED system illumination market

0

0.5

1

1.5

2

2.5

3

2004 2005 2006 2007 2008 2009

USD billion World-wide: Business and residential

Estimated by Philips at 3 times the LED component market as stated by Strategies Unlimited; PennWell

29

Philips Lighting is with In-organic LEDsespecially active in decorative outdoor and shop lighting…

30

Creating atmosphere in cities

Demo Philips outdoor lighting application centre, France

31

Creating atmosphere in cities

Demo Philips outdoor lighting application centre, France

32

Creating atmosphere in cities

Demo Philips outdoor lighting application centre, France

33

Examples of projects installed in 2005

Palacio Diputación de Palencia, Spain

34

Examples of projects installed in 2005

Lagos Martianez, Spain

35

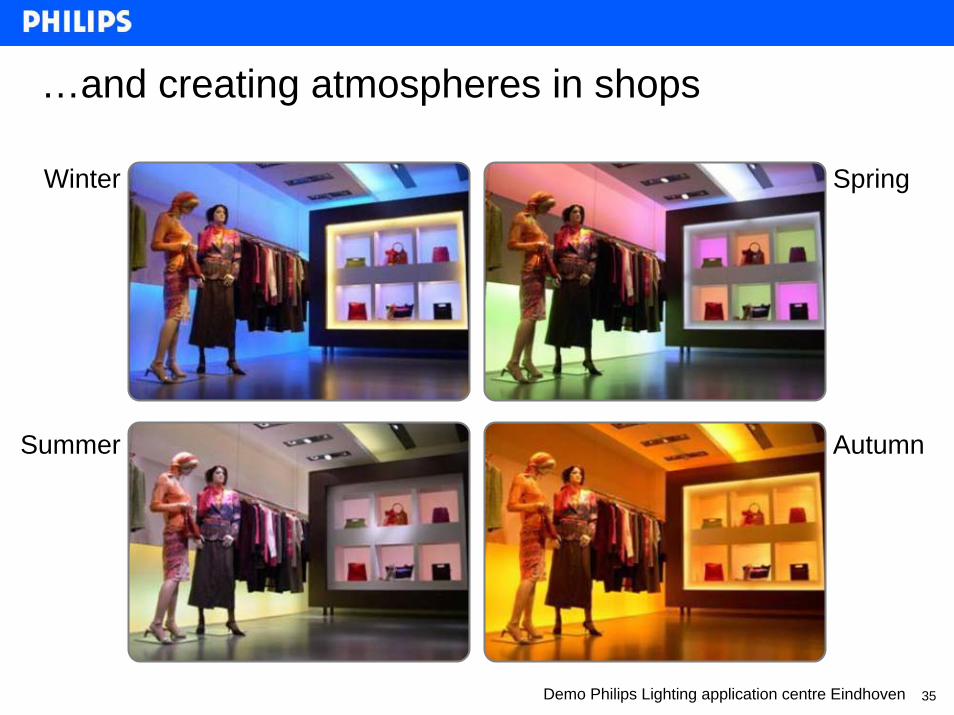

…and creating atmospheres in shops

Winter Spring

Summer Autumn

Demo Philips Lighting application centre Eindhoven

36

Product portfolio 2005LEDFloodEquinox Ledline2

Origami

Minicolour

LED uplighter / step

LEDAmazon

LEDspot & controllerRoadstud

37

Solid State Lighting modules ….……enabling OEM luminaires concepts

38

We explore new applications….e.g. with Philips Medical Systems creating an Ambient Experience during hospital diagnostics

39

We explore new applications…………or creating a Bathroom experience…..

Tiles Bath Shower

Demo in Philips Lighting Application Centre Eindhoven

40

We explore new applications…… light in textiles, controlled by SMS messages

IFA, Sept 2005

41

Agenda

• Philips Lighting

• Shaping the future

– LCD backlighting– Solid State Lighting: OLEDs

• Profitable growth via key business drivers

• Continuous improvement, control of costs and assets

42

Organic LEDs

• Organic LEDs are flat diffuse light sources

• Potential for large area light sources

• Many new design-options (thin, flat, transparent, tunable, flexible...)

• New business opportunities for the lighting world

+-

1.8m

m

43

OLED initially targeted lighting markets

• Automotive– Signaling– Interior

• Signage– Advertising– Emergency lighting

• Special Lighting– Decorative– Accent lighting

44

Some samples of Philips OLED solutions

45

Roadmap for OLED Lighting

Size, efficiency, lifetime

time2006 2008 2010 2015

46

Agenda

• Philips Lighting

• Shaping the future

– LCD backlighting– Solid State Lighting: Lasers

• Profitable growth via key business drivers

• Continuous improvement, control of costs and assets

47

Laser applications in Lighting

• Develop basic laser technology– We acquired 49% stake and obtained management control

in Cedova, a start-up venture for laser manufacturing

• First volume laser application: movement-sensor– Mouse launched with Logitech

• Monitor laser developments for projection systems

48

Agenda

• Philips Lighting

• Shaping the future

• Profitable growth via key business drivers

– End user driven innovation, building on technology leadership

– Marketing excellence– Supply excellence

• Continuous improvement, control of costs and assets

49

New market themes drive growth in Lighting

latentawareness

latentawareness

emergingawarenessemerging

awarenessincreasingawarenessincreasingawareness

highawareness

highawareness

decreasinginterest

decreasinginterest

End

use

r / M

arke

t Aw

aren

ess

See and be seen

Total costof ownership

Safety

Lifestylelighting

Maturity

Today

Tomorrow

Yesterday

Light &health

50

Market theme concept: Safety

The same street before and after

• The street with new solution– Uses less energy– Provides higher quality light– Provides greater safety

51

Market theme concept: Lifestyle lighting

52

Market theme concept: Light & Health

Water purification Infra red sauna

53

Also product-technology innovation willcontinue to drive growth in Lighting

Time

High

Low

End

use

r / M

arke

t Aw

aren

ess IncandescentFluorescent

Halogen

HID

UHP

CFL

Lasers

latentawareness

latentawareness

emergingawarenessemerging

awarenessincreasingawarenessincreasingawareness

highawareness

highawareness

decreasinginterest

decreasinginterest

EUVOLED

LED

54

Building on technology leadershipDevelopment R&D % and size patent portfolio

Patent portfolio increase 2000 – 2005: 68% *)

*) Excluding Lumileds

Increasing R&D effort

33.3

3.8

4.4

4.2

5.3

0

1

2

3

4

5

6

2002 2003 2004 E2005 2006

%

Lumileds

19461782

1604

1480

1303

1155

2158

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2200

2000 2001 2002 2003 2004 2005E

# of Patent Families

*) Excluding Lumileds

*

55

Innovation drives investment for growth (2005)

0%10%20%30%40%50%60%70%80%90%

100%

R&D Capex Marcom Sales

MatureGrowthEmerging

56

Agenda

• Philips Lighting

• Shaping the future

• Profitable growth via key business drivers

– End user driven innovation, building on technology leadership– Marketing excellence– Supply excellence

• Continuous improvement, control of costs and assets

57

Marketing Excellence: building the Brand

58

Sense & Simplicity: Philips IMAGEO

• Candle-like ambience without flames

• Last for more than 24 hours, before recharging

• Rechargeable without taking the LED out of the glass

• Switch on/off by tilting the glass

59

Sense & Simplicity: Philips IMAGEO

The intimacy of realcandle-light, but morecolorful

• Real candle with battery operated LED inside

• Long lasting: 100 hours

60

Agenda

• Philips Lighting

• Shaping the future

• Profitable growth via key business drivers

– End user driven innovation, building on technology leadership– Marketing excellence– Supply excellence

• Continuous improvement, control of costs and assets

61

Supply excellence: delivery reliabilityTotal Philips Lighting

80

85

90

95

2001 2002 2003 2004 2005Q3YTD

%

62

Agenda

• Philips Lighting

• Shaping the future

• Profitable growth via key business drivers

• Continuous improvement, control of costs and assets

63

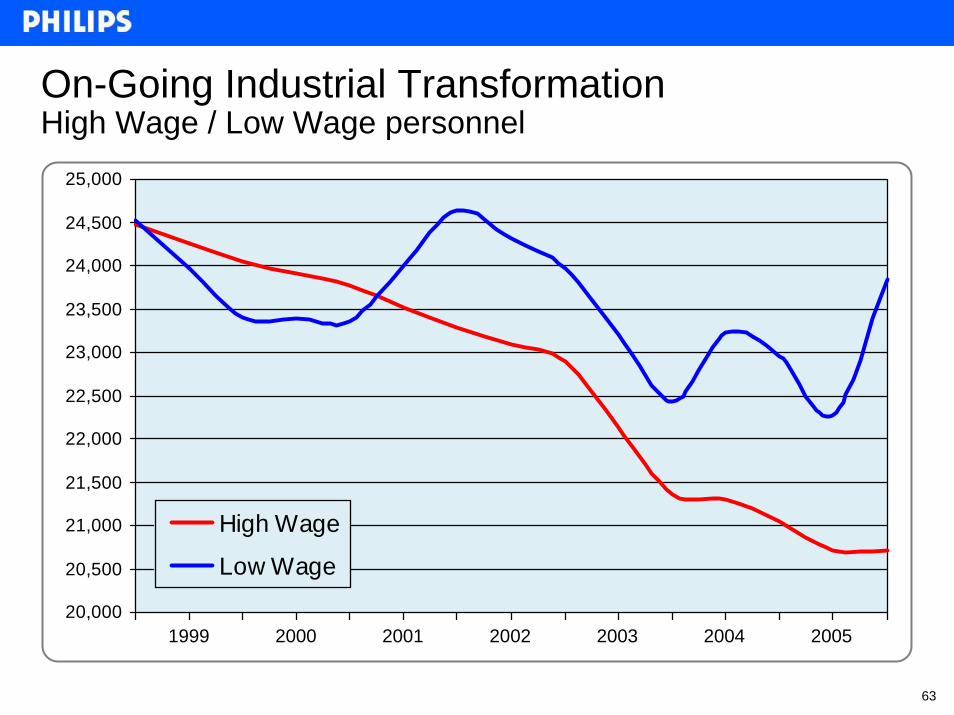

On-Going Industrial TransformationHigh Wage / Low Wage personnel

20,000

20,500

21,000

21,500

22,000

22,500

23,000

23,500

24,000

24,500

25,000

High Wage

Low Wage

1999 2000 2001 2002 2003 2004 2005

64

Net Operating Capital turns Continuous improvement

1.5

2

2.5

3

3.5

'96 '97 '98 '99 '00 '01 '02 '03 '04 '05 Q3YTD

65

Working Capital turns Continuous improvement

2

4

6

8

10

'96 '97 '98 '99 '00 '01 '02 '03 '04 '05 Q3YTD

66

Continuous Improvement:BEST in Philips LightingAll metrics show ample room for improvement

• Applying model from European Foundation for Quality Management: from 600 points today towards 700 in coming years

• Business Balanced Scorecards: focus on essentials

• Improve business processes– Systematic deployment of business targets into concrete action

plans on all levels– Cycle time reduction– Black belts: growing population of process champions– Process survey tools: from 5 towards 7 level

• Quality improvement competition: 40 % participation of all employees

67