financial accounting project

TRANSCRIPT

9/4/2016

FINANCIAL ACCOUNTING RESEARCH

PROJECT Performance Evaluation and Ratio Analysis of

Pharmaceutical Companies

PRESENTED BY:

TEAM NO. 3

ARPIT TANDON (MYDM-2018-10)

ASHISH DONGRE (MYDM-2018-11)

ASHISH JAIN (MYDM-2018-12)

ATUL KUMAR DWIVEDI (MYDM-2018-13)

BALAKUMAR G.R (MYDM-2018-14)

FACULTY: Dr. R. Radhakrishna

SUBJECT CODE:

1 | P a g e

CONTENTS

TOPICS PAGE NO.

1 ABSTRACT 2

2 COMPANY OVERVIEW

3

3 RATIO ANALYSIS

Current Ratio

Quick Ratio

Solvency Ratio

Debt to Equity Ratio

Inventory Turnover Ratio

Collection Period (DAYS)

Assets Turnover Ratio

Operating Margin Ratio

Net Margin Ratio

Return on Total Assets

Ratio

Return on Equity Ratio

4-9

4 REFERENCES 10

2 | P a g e

ABSTRACT

The thesis applies Performance Evaluation and Ratio Analysis of pharmaceutical companies

listed in S&P 500. It means evaluating how well the company performs. The main aim is

achieved through ratio analysis of two pharmaceutical (Pfizer and AbbVie) companies in the

US. Different financial ratios have been evaluated like liquidity ratios, asset management ratios,

profitability ratios, market value ratios, debt management ratios and finally to measure the best

performance between two companies. The mathematical calculation has been established for

ratio analysis between two companies from 2013-2015. It is the most important factor for

performance evaluation. The graphical analysis and comparisons are applied between two

companies for measurement of all types of financial ratio analysis. Liquidity ratio is conveying

the ability to repay short-term creditors. It determines performance of short term creditor of both

pharmaceutical companies under the three categories such as current ratio, quick ratio and

cash ratio. Asset management ratio is measurement how effectively a company uses and controls

its assets. It’s also quantified into seven categories for both pharmaceutical companies such as

account receivable turnover, average collection period, inventory turnover, account payable

turnover, account payable turnover in days, fixed asset turnover, total asset turnover.

Profitability ratio evaluates how well a company is performing by analyzing and how profit

was earned relative to sales, total assets and net worth for both pharmaceutical companies.

Debt coverage ratio is used for performing the property insufficient to collect their

mortgage for both companies and market value is performed to analyze their future

market value of the stock market. Overall analyses are measured between both Pfizer and

AbbVie.

NOTE: Inspite of collecting data for the 3 financial years i.e. 2013-2015, we have added

2012 data in the table in order to calculate the net receivables.

Keyword: Financial analysis, ratio analysis, Pfizer company financial analysis, AbbVie

financial analysis.

3 | P a g e

Company Overview

Pfizer Inc. is an American global pharmaceutical corporation headquartered in New York

City, with its research headquarters in Groton, Connecticut. It is among the world's largest

pharmaceutical companies. Pfizer is listed on the New York Stock Exchange, and its shares have

been a component of the Dow Jones Industrial Average since 2004.

Pfizer develops and produces medicines and vaccines for a wide range of medical disciplines,

including immunology, oncology, cardiology, diabetology/endocrinology, and neurology.

Pfizer's products include the blockbuster drug Lipitor (atorvastatin), used to lower LDL blood

cholesterol.

AbbVie Inc. is a pharmaceutical company that discovers, develops, and markets

both biopharmaceuticals and small molecule drugs. It originated in 2013 as a spin-off of Abbott

Laboratories.

AbbVie developed adalimumab, which is marketed under the trade name Humira,

a biopharmaceutical treatment for autoimmune diseases that has exceeded $10 billion in global

sales. AbbVie’s portfolio of medicines also includes AndroGel, Creon, Duodopa and

Duopa, Kaletra, Lupron, Niaspan, Norvir, Sevoflurane, Synagis,Synthroid, TriCor and

Trilipix, Viekira, and Zemplar.

4 | P a g e

1. CURRENT RATIO:

The Current Ratio is a liquidity and an efficiency ratio that measures a firm's ability to pay off its short-term liabilities with

its current assets. A current ratio of 2:1 is considered satisfactory.

Pfizer Inc. (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Total current assets $43,804,000,000 $55,595,000,000 $56,244,000,000 $64,831,000,000

Total current liabilities $29,399,000,000 $21,587,000,000 $23,366,000,000 $29,186,000,000

Current Ratio 1.489982652 2.575392597 2.407087221 2.221304735

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Total current assets $16,314,000,000 $16,081,000,000 $17,848,000,000 $15,354,000,000

Total current liabilities $10,894,000,000 $11,393,000,000 $6,879,000,000 $6,776,000,000

Current Ratio 1.497521572 1.411480743 2.594563163 2.265938606

Analysis: In 2015, the current ratio of AbbVie is higher as compared to Pfizer. It implies that a higher current ratio is

always more favorable than a lower current ratio because it shows the company can more easily make current debt

payments. In 2014, Pfizer has a higher ratio as compared to AbbVie. In this case, Pfizer can more easily make current debt

payments. In 2013, AbbVie has a higher value compared to Pfizer. Thus for this year, AbbVie can easily make more current

debt payments.

2. QUICK RATIO:

The Quick Ratio or Acid Test Ratio is a liquidity ratio that measures the ability of a company to pay its current liabilities

when they come due with only quick assets. Quick assets are current assets that can be converted to cash within 90 days

or in the short-term. A quick ratio of 1:1 is an ideal ratio.

Pfizer Inc. (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Total current assets $16,314,000,000 $16,081,000,000 $17,848,000,000 $15,354,000,000

Prepaid exp. and other $1,458,000,000 $1,952,000,000 $1,234,000,000 $1,320,000,000

Inventories, net $1,719,000,000 $1,124,000,000 $1,150,000,000 $1,091,000,000

Quick Assets $13,137,000,000 $13,005,000,000 $15,464,000,000 $12,943,000,000

Total current liabilities $29,399,000,000 $21,587,000,000 $23,366,000,000 $29,186,000,000

Quick Assets 0.446851934 0.602445917 0.661816314 0.443466045

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Total current assets $16,314,000,000 $16,081,000,000 $17,848,000,000 $15,354,000,000

Prepaid exp. and other $1,458,000,000 $1,952,000,000 $1,234,000,000 $1,320,000,000

Inventories, net $1,719,000,000 $1,124,000,000 $1,150,000,000 $1,091,000,000

Quick Assets $13,137,000,000 $13,005,000,000 $15,464,000,000 $12,943,000,000

Total current liabilities $10,894,000,000 $11,393,000,000 $6,879,000,000 $6,776,000,000

Quick Assets 1.205893152 1.141490389 2.248001163 1.910123967

Analysis: In 2015, the Quick ratio of Pfizer is slightly higher as compared to AbbVie. It implies that there are more quick

assets as compared to current liabilities. In 2014, Pfizer has a comparatively higher value as compared to Abbvie. In this

case, Pfizer has more quick assets than current liabilities. As the ratio increases so does the liquidity of the company. In

2013, AbbVie has a higher value when compared to Pfizer. Hence, AbbVie would be able to have more quick assets

compared to current liabilities.

5 | P a g e

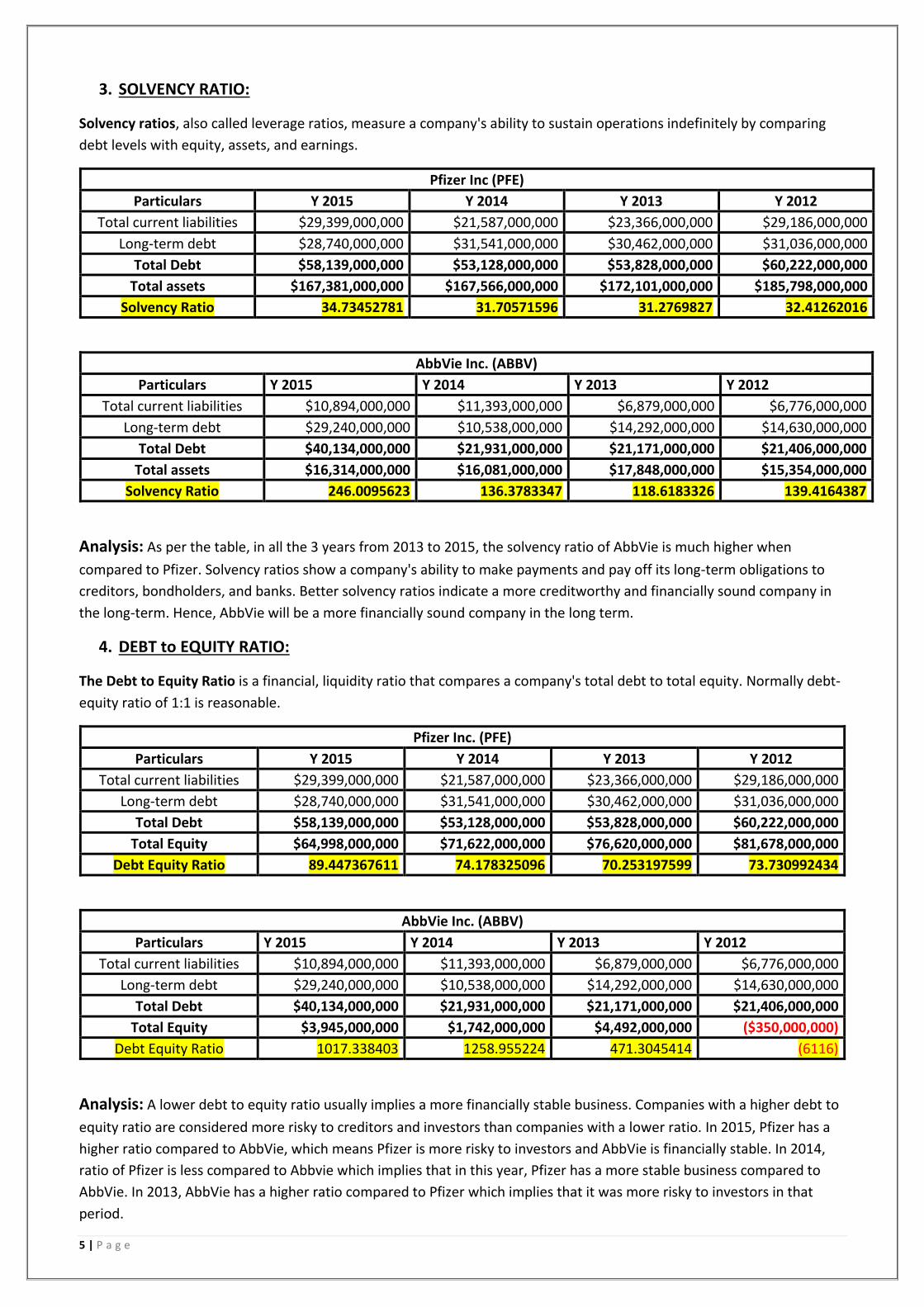

3. SOLVENCY RATIO:

Solvency ratios, also called leverage ratios, measure a company's ability to sustain operations indefinitely by comparing

debt levels with equity, assets, and earnings.

Pfizer Inc (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Total current liabilities $29,399,000,000 $21,587,000,000 $23,366,000,000 $29,186,000,000

Long-term debt $28,740,000,000 $31,541,000,000 $30,462,000,000 $31,036,000,000

Total Debt $58,139,000,000 $53,128,000,000 $53,828,000,000 $60,222,000,000

Total assets $167,381,000,000 $167,566,000,000 $172,101,000,000 $185,798,000,000

Solvency Ratio 34.73452781 31.70571596 31.2769827 32.41262016

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Total current liabilities $10,894,000,000 $11,393,000,000 $6,879,000,000 $6,776,000,000

Long-term debt $29,240,000,000 $10,538,000,000 $14,292,000,000 $14,630,000,000

Total Debt $40,134,000,000 $21,931,000,000 $21,171,000,000 $21,406,000,000

Total assets $16,314,000,000 $16,081,000,000 $17,848,000,000 $15,354,000,000

Solvency Ratio 246.0095623 136.3783347 118.6183326 139.4164387

Analysis: As per the table, in all the 3 years from 2013 to 2015, the solvency ratio of AbbVie is much higher when

compared to Pfizer. Solvency ratios show a company's ability to make payments and pay off its long-term obligations to

creditors, bondholders, and banks. Better solvency ratios indicate a more creditworthy and financially sound company in

the long-term. Hence, AbbVie will be a more financially sound company in the long term.

4. DEBT to EQUITY RATIO:

The Debt to Equity Ratio is a financial, liquidity ratio that compares a company's total debt to total equity. Normally debt-

equity ratio of 1:1 is reasonable.

Pfizer Inc. (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Total current liabilities $29,399,000,000 $21,587,000,000 $23,366,000,000 $29,186,000,000

Long-term debt $28,740,000,000 $31,541,000,000 $30,462,000,000 $31,036,000,000

Total Debt $58,139,000,000 $53,128,000,000 $53,828,000,000 $60,222,000,000

Total Equity $64,998,000,000 $71,622,000,000 $76,620,000,000 $81,678,000,000

Debt Equity Ratio 89.447367611 74.178325096 70.253197599 73.730992434

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Total current liabilities $10,894,000,000 $11,393,000,000 $6,879,000,000 $6,776,000,000

Long-term debt $29,240,000,000 $10,538,000,000 $14,292,000,000 $14,630,000,000

Total Debt $40,134,000,000 $21,931,000,000 $21,171,000,000 $21,406,000,000

Total Equity $3,945,000,000 $1,742,000,000 $4,492,000,000 ($350,000,000)

Debt Equity Ratio 1017.338403 1258.955224 471.3045414 (6116)

Analysis: A lower debt to equity ratio usually implies a more financially stable business. Companies with a higher debt to

equity ratio are considered more risky to creditors and investors than companies with a lower ratio. In 2015, Pfizer has a

higher ratio compared to AbbVie, which means Pfizer is more risky to investors and AbbVie is financially stable. In 2014,

ratio of Pfizer is less compared to Abbvie which implies that in this year, Pfizer has a more stable business compared to

AbbVie. In 2013, AbbVie has a higher ratio compared to Pfizer which implies that it was more risky to investors in that

period.

6 | P a g e

5. INVENTORY TURNOVER RATIO:

The inventory turnover ratio is an efficiency ratio that shows how effectively inventory is managed by comparing cost of

goods sold with average inventory for a period.

Pfizer Inc. (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Cost of good sales $9,648,000,000 $9,577,000,000 $9,586,000,000 $9,821,000,000

Inventories $7,513,000,000 $5,663,000,000 $6,166,000,000 $6,076,000,000

Average Inventories $6,588,000,000 $5,914,500,000 $6,121,000,000

Inventories Turnover Ratio 1.464480874 1.619240849 1.566083973

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Cost of goods sold $4,500,000,000 $4,426,000,000 $4,581,000,000 $4,508,000,000

Inventories $1,719,000,000 $1,124,000,000 $1,150,000,000 $1,091,000,000

Average Inventories $1,421,500,000 $1,137,000,000 $1,120,500,000

Inventory Turnover Ratio 3.165670067 3.892700088 4.088353414

Analysis: Inventory turnover is a measure of how efficiently a company can control its merchandise, so it is important to

have a high turn. It shows that the company can effectively sell the inventory it buys. In 2015, 2014 as well as in 2013,

AbbVie has a higher ratio compared to Pfizer which means AbbVie can efficiently control its merchandise. On the contrary,

Pfizer’s ratio reflects dull business, over investment in inventory, wrong valuation of stock and stock of unsaleable &

obsolete goods.

6. COLLECTION PEROID (DAYS):

The Average Collection Period or Days' Sales in Receivables, measures the number of days it takes a company to collect

cash from its credit sales. This calculation shows the liquidity and efficiency of a company's collections department.

Pfizer Inc. (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Revenues $48,851,000,000 $49,605,000,000 $51,584,000,000 $54,657,000,000

Receivables $8,176,000,000 $8,401,000,000 $9,357,000,000 $10,675,000,000

Average Receivables $8,288,500,000 $8,879,000,000 $10,016,000,000

Collection Period (Days) 61.92918262 65.33282935 70.87158809

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Revenues $22,859,000,000 $19,960,000,000 $18,790,000,000 $18,380,000,000

Receivables $4,730,000,000 $3,735,000,000 $3,854,000,000 $4,298,000,000

Average Receivables $4,232,500,000 $3,794,500,000 $4,076,000,000

Collection Periods (Days) 67.58224332 69.3884018 79.17722193

Analysis: A lower ratio is more favorable because it means companies collect cash earlier from customers and can use

this cash for other operations. A higher ratio indicates a company with poor collection procedures and customers who are

unable or unwilling to pay for their purchases. In 2015, 2014 as well as in 2013, AbbVie has a higher value when compared

to Pfizer which means AbbVie is unable to convert sales into cash as quickly as firms with lower ratios. On the contrary,

Pfizer’s account receivables are good and won’t be written off as bad debts.

7 | P a g e

7. ASSETS TURNOVER RATIO:

The Asset Turnover Ratio is an efficiency ratio that measures a company's ability to generate sales from its assets by

comparing net sales with average total assets.

Pfizer Inc. (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Revenues $48,851,000,000 $49,605,000,000 $51,584,000,000 $54,657,000,000

Total assets $167,381,000,000 $167,566,000,000 $172,101,000,000 $185,798,000,000

Assets Turnover Ratio 0.2918551090 0.2960326080 0.2997309719 0.2941743183

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

Revenues $22,859,000,000 $19,960,000,000 $18,790,000,000 $18,380,000,000

Total assets $53,050,000,000 $27,513,000,000 $29,198,000,000 $27,008,000,000

Assets Turnover Ratio 0.430895382 0.72547523 0.643537229 0.6805391

Analysis: This ratio measures how efficiently a firm uses its assets to generate sales, so a higher ratio is always more

favorable. Higher turnover ratios mean the company is using its assets more efficiently. Lower ratios mean that the

company isn't using its assets efficiently and most likely have management or production problems. In 2015, 2014 & 2013

data (acc to the table), AbbVie has a higher ratio when compared to Pfizer. Thus, AbbVie is using its assets more efficiently

whereas Pfizer is likely to have production problems.

8. OPERATING MARGIN RATIO:

The Operating Margin Ratio, also known as the operating profit margin, is a profitability ratio that measures what

percentage of total revenues is made up by operating income.

Pfizer Inc. (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

EBIT $8,965,000,000 $12,240,000,000 $15,716,000,000 $11,242,000,000

Revenues $48,851,000,000 $49,605,000,000 $51,584,000,000 $54,657,000,000

Operating Margin Ratio 18.351722585 24.674931963 30.466811414 20.568271219

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

EBIT $7,537,000,000 $3,411,000,000 $5,664,000,000 $5,817,000,000

Revenues $22,859,000,000 $19,960,000,000 $18,790,000,000 $18,380,000,000

Operating Margin Ratio 32.97169605 17.08917836 30.14369345 31.64853101

Analysis: The operating profit margin ratio is a key indicator for investors and creditors to see how businesses are

supporting their operations. In 2015, AbbVie has a higher ratio when compared to Pfizer. It implies that the company is

making enough money from its ongoing operations to pay for its variable costs as well as its fixed costs. In 2014, AbbVie

has a lesser ratio when compared to Pfizer, which implies that the business' operating activities are not sustainable. In

2013, the ratio of both Pfizer & AbbVie are almost equal (Pfizer being slightly higher).

8 | P a g e

9. NET MARGIN RATIO:

Net Margins Ratio is a profitability ratio that measures the amount of net income earned with each dollar of sales

generated by comparing the net income and net sales of a company.

Pfizer Inc. (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

EAT $6,986,000,000 $9,168,000,000 $22,072,000,000 $14,598,000,000

Revenues $48,851,000,000 $49,605,000,000 $51,584,000,000 $54,657,000,000

Net Margins Ratio 14.300628442 18.482007862 42.788461538 26.708381360

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

EAT $5,144,000,000 $1,774,000,000 $4,128,000,000 $5,275,000,000

Revenues $22,859,000,000 $19,960,000,000 $18,790,000,000 $18,380,000,000

Net Margins Ratio 22.50317162 8.887775551 21.96913252 28.69967356

Analysis: This ratio also indirectly measures how well a company manages its expenses relative to its net sales. In 2015,

Pfizer’s ratio is less when compared to AbbVie. It implies that Pfizer has generated less revenues. In 2014 & 2013, Pfizer

has generated more revenues which means it has either maintained its revenues or lowered its expenses.

10. RETURN ON TOTAL ASSETS RATIO :

The Return on Total Assets Ratio, often called the return on total assets, is a profitability ratio that measures the net

income produced by total assets during a period by comparing net income to the average total assets. . Since company

assets' sole purpose is to generate revenues and produce profits, this ratio helps both management and investors see how

well the company can convert its investments in assets into profits.

Pfizer Inc. (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

EBIT $8,965,000,000 $12,240,000,000 $15,716,000,000 $11,242,000,000

Total assets $167,381,000,000 $167,566,000,000 $172,101,000,000 $185,798,000,000

Return on Total Assets 5.3560439954 7.3045844622 9.1318469968 6.0506571653

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

EBIT $7,537,000,000 $3,411,000,000 $5,664,000,000 $5,817,000,000

Total assets $53,050,000,000 $27,513,000,000 $29,198,000,000 $27,008,000,000

Return on Total Assets 14.20735156 12.3977756 19.39858894 21.5380628

Analysis: In all the 3 years, 2015, 2014 & 2013, AbbVie has got the highest ratio when compared to Pfizer. It implies that

a higher ratio is more favorable to investors because it shows that the company is more effectively managing its assets to

produce greater amounts of net income.

9 | P a g e

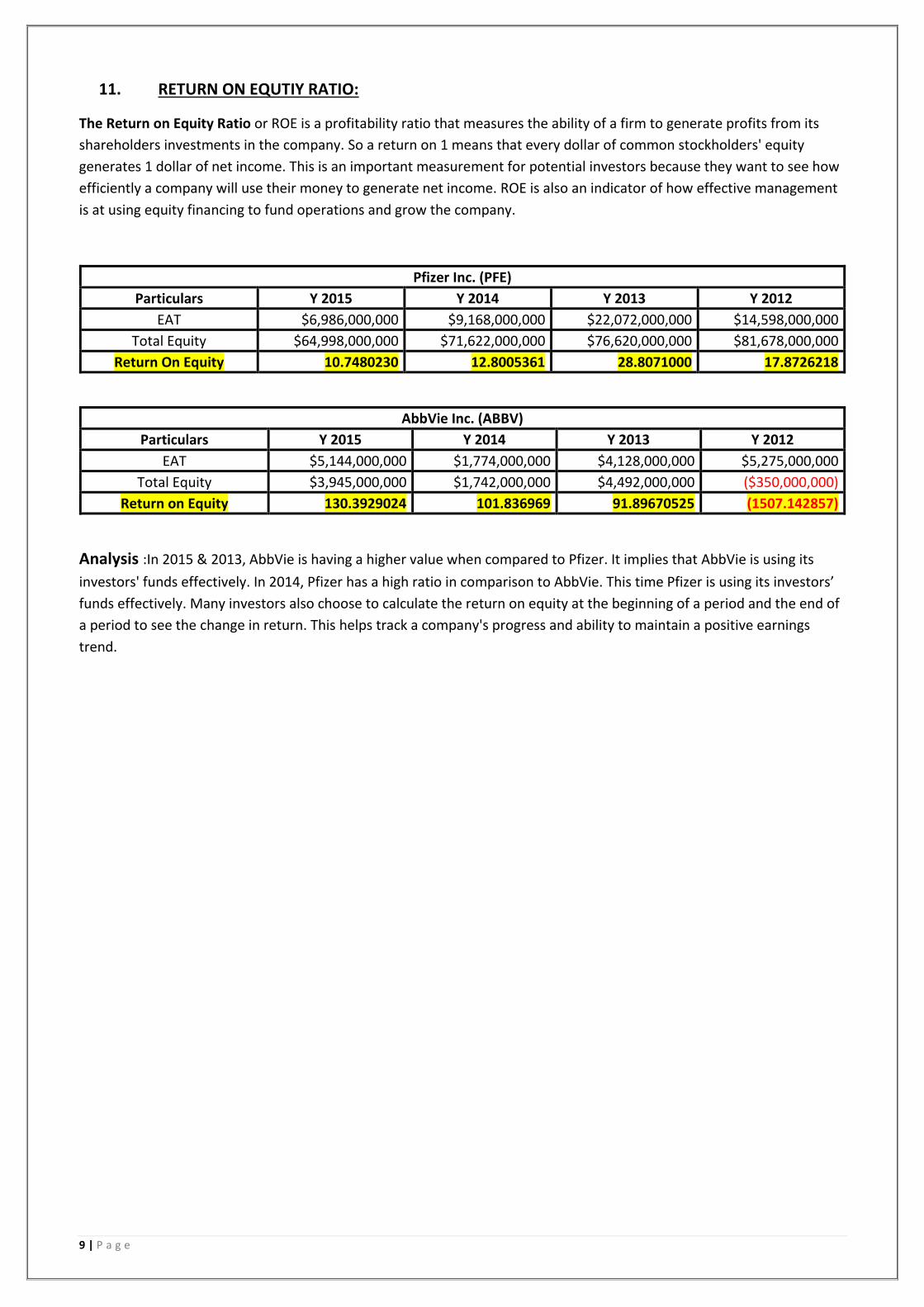

11. RETURN ON EQUTIY RATIO:

The Return on Equity Ratio or ROE is a profitability ratio that measures the ability of a firm to generate profits from its

shareholders investments in the company. So a return on 1 means that every dollar of common stockholders' equity

generates 1 dollar of net income. This is an important measurement for potential investors because they want to see how

efficiently a company will use their money to generate net income. ROE is also an indicator of how effective management

is at using equity financing to fund operations and grow the company.

Pfizer Inc. (PFE)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

EAT $6,986,000,000 $9,168,000,000 $22,072,000,000 $14,598,000,000

Total Equity $64,998,000,000 $71,622,000,000 $76,620,000,000 $81,678,000,000

Return On Equity 10.7480230 12.8005361 28.8071000 17.8726218

AbbVie Inc. (ABBV)

Particulars Y 2015 Y 2014 Y 2013 Y 2012

EAT $5,144,000,000 $1,774,000,000 $4,128,000,000 $5,275,000,000

Total Equity $3,945,000,000 $1,742,000,000 $4,492,000,000 ($350,000,000)

Return on Equity 130.3929024 101.836969 91.89670525 (1507.142857)

Analysis :In 2015 & 2013, AbbVie is having a higher value when compared to Pfizer. It implies that AbbVie is using its

investors' funds effectively. In 2014, Pfizer has a high ratio in comparison to AbbVie. This time Pfizer is using its investors’

funds effectively. Many investors also choose to calculate the return on equity at the beginning of a period and the end of

a period to see the change in return. This helps track a company's progress and ability to maintain a positive earnings

trend.

10 | P a g e

REFERENCES

1. CALCBENCH - http://www.calcbench.com/

2. FINANCIAL ACCOUNTING BY M.R AGGARWAL

3. INVESTOPEDIA - http://www.investopedia.com/