final draft_britain's valuable property credentials - bpf report_withalledits

TRANSCRIPT

TOSCAFUND December 2015

Authors: Dr Savvas Savouri, Toscafund Chief Economist, and Professor Richard Jackman, London School of Economics

Research Assistants: Boris But, Nas Christodoulopoulos, Katie Orlandi and Vikram Lopez Y Royo

BRITAIN’S

PROPERTY CREDENTIALS

A British Property Federation commissioned report

prepared by TOSCAFUND

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

2 December 2015

The report was commissioned by the British Property Federation (BPF) and prepared by

Toscafund Asset Management LLP (Toscafund).

The BPF is the membership organisation for the UK real estate industry. It represents all those involved in real estate

ownership and investment. It works with Government and regulatory bodies to help the real estate industry grow and

thrive, to the benefit of its members and the economy as a whole.

Toscafund, based in London, is a leading multi-asset management firm founded in 2000. Toscafund currently manages

over $3bn on a fully discretionary basis in a variety of strategies that include Commercial Real Estate.

Authors

Dr Savvas P. Savouri Chief Economist – Toscafund Asset Management

Since 2008 Savvas Savouri has been a partner and chief economist at Toscafund Asset Management, having headed

economics and strategy departments at a number of investment banks. Before entering financial services Savvas taught

at the LSE, Oxford University and Moscow State University. Savvas was awarded a doctorate in Econometrics and

Mathematical Economics from the LSE where he also obtained masters and bachelor degrees in the same discipline.

Professor Emeritus Richard Jackman Professor of Economics – London School of Economics and Political Science

Professor Richard Jackman joined the LSE teaching staff in 1968 after his MA in Economics from Cambridge University.

Richard has co-authored four books and has over 80 articles in refereed journals. During his time at the LSE, Richard’s also

been a visitor Professor in Economics at the University of Iowa and worked as a consultant with the World Bank. He has

worked with the London Boroughs’ Association (now known as London Councils) and the Department of the

Environment in connection with its studies on local government finance.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

3 December 2015

Executive Summary

� We believe that the conventional ways of quantifying Commercial Real Estate (CRE) are ineffective, and that the

‘economic’ definition of CRE is wider and more complex. Nor is it correct to identify CRE with the Blue Book category

‘non-residential property’ as some non-residential property is not commercial, while some CRE is classed as ‘other

structures’.

� Our current estimate of CRE is £1,662bn, which is just over 20% of net wealth, in 2014.

� In this report we define CRE as property whose main function is to generate income for its owner. Therefore we

consider the Private Rental Sector (such as buy-to-let, student hostels, etc) as an integral part, contributing £42bn

market rent in our estimate for 2014.

� According to conventional national income accounting procedures, the contribution of CRE to GDP is measured by

the rent (actually paid or implicit) generated by such properties. This amounts to around £94bn or 5% of GDP in

2014.

� For comparative purposes we have included the yield for 10 year Gilts, the most conventionally used risk-free or

swap rate for CRE.

Chart A: Capital Values of CRE and PRS Chart B: Yield comparison between CRE and 10 year Gilt

Source: VOA, Scottish Assessors (Scottish Government statistics), IPD (MSCI), DCLG (ONS), Stats Wales, NI Housing Executive, Wriglesworth Consultancy (part of Instinctif Partners), LSL

Property Services, Bloomberg, Toscafund

� Whilst all this income percolates down to households, much of it is hidden rather than apparent. For example, most

pension funds are invested mainly in equities, but the value of equities derives to a large extent from the CRE that

they finance.

� The main contribution of CRE to economic welfare lies not in its contribution to GDP, but in its contribution to the

built environment, to employment and to economic development.

� The growth of real wages depends on the growth of capital, of which CRE forms a large part, at least keeping pace

with the growth of population. This requires substantial investment in CRE over the coming years.

� The greater flexibility of CRE means that it is no longer so much of a barrier to the revival of depressed regions: new

industries can flourish in premises vacated by the old.

� CRE is much more heavily taxed than other factors of production or types of wealth. One consequence of this is that

some buildings are left empty or remain in unproductive use. Notably, the tax on CRE is much higher than the tax on

dwellings, in particular owner occupied housing. This leads to a correspondingly enormous misallocation of savings,

which is poured into domestic housing rather than productive investment.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2005 2009 2010 2011 2012 2013 2014

Tri

llio

ns

Commercial real estate Private Rented Sector

0

1

2

3

4

5

6

7

2005 2009 2010 2011 2012 2013 2014

%

CRE yield 10 year Gilt yield

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

4 December 2015

Preface

In the second part an orderly sequence is followed as we try to establish quantitative values for what Britain’s Commercial

Real Estate (CRE) means to the economy. Ahead of that, Part 1 of this research paper covers an assortment of topics,

issues and themes relating to the UK’s CRE. Since the section's elements do not flow in a sequential narrative we have

opted to present the contents page rather differently from the convention, using a circle rather than a table (we return to

tradition in Section 2).

The use of a circle makes the point that whilst sections can indeed be followed around the ‘circumference’ in THAT

sequence, readers may wish instead to shift across the diameter, or indeed travel to the centre and then move radially in

whichever direction their thematic interest may choose to take them.

The over-arching point of Section 1 is that the UK’s CRE is a cornerstone (sic) asset, not a sector per se, as it is all too often

narrowly seen. Just as our manufacturers and exporters demand built space to function so to do our business service

sectors. For its part agriculture has been transformed by CRE, green houses amongst an assortment of buildings which

have improved our productive capacity and freed up labour and land for other productive uses, for which property once

more has been an essential element. Across in residential markets the expansion once more in the Private Rental Sector

(PRS) is contributing to the UK having a more mobile labour force with all the positive economic and indeed social

externalities which follow from this. As well as we perform productive functions CRE is essential for us during recreational

time, with of course recreational time for some productive and commercial valuable time for others; our vignette on the

use of CRE for the manufacture of goods facing one another on our contents clock.

To reiterate CRE is a crucial factor input without which the UK economy could not possibly function, and without whose

continuous development the UK would not have the economy it has today. This is not hyperbole but an irrefutable

axiom. Moreover this is not to say that certain sectors and industries do not directly ‘serve’ the UK’s commercial space;

construction and maintenance activity, building product making, property services and agency sectors, just a handful. In

fact were we to collect together these, and other sectors which are recognised as serving the UK's CRE, we would come to

the ‘conventional’ conclusion its CRE only somehow represents a rather modest c2% of the UK’s GDP. The reality is that

were one to fully account for all its tangible contributions, the figure would, in fact, rise to over 5%. Moreover, even this

figure does not do proper justice to the wider economic importance of CRE. The crucial point is that NO other sector

contributing to the UK’s GDP could function without the nations CRE which also contributes to large parts of the UK

balance sheet. To repeat we should cease to view CRE as a sector and instead honour it as one of the pillars (sic) of the UK

economy. It is a crucial factor input working alongside our nation’s human capital. Indeed, we should see property as we

do labour as over-arching all elements of the economy, not a particular ‘segment’ within it.

In Section 2 the point is made more formally that the ‘economic value’ of CRE should be viewed from the perspective of it

as a factor input and provider of balance sheet wealth and income extensively across the UK. This first section is instead

made up of vignettes relating to CRE, presenting ideas surrounding its often overlooked contribution to our lives and

how exactly it impacts us. It also tries to expose misunderstandings which often arise concerning the contribution of CRE.

Section 1 is in no way exhaustive of these, simply illustrative. And to repeat the topics, issues and themes covered in

Section 1 are not presented in a top-table manner, where sections are sequenced in some inviolate order, but as a ‘round

table’, where all face one another as complements and part of a whole, or put different illustrating that its CRE is not

simply part of the UK's economy but the latter is nothing without it.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

5 December 2015

Contents

Introduction 7

Part 1. Evolution of Britain’s CRE sector 8

1.1 The externalities (social benefits) of Britain’s CRE 8

1.1.1 The ‘direct’ externalities of CRE 8

1.2 Infrastructure and transport 9

1.2.1 Construction and the Growth of GDP 9

1.2.2 Bringing derelict CRE back to economic life 10

1.2.3 Britain’s CRE is better connected 11

1.2.4 King’s Cross Central: A case study in inclusive regeneration 13

1.2.5 CRE: Walking on water 14

1.2.6 CRE flying high 15

1.3 Offices and IT 16

1.3.1 CRE in the clouds 16

1.3.2 CRE and the internet 16

1.3.3 Google: search for a real presence 17

1.3.4 Sometimes developing Britain's CRE does not quite reach The Pinnacle 17

1.3.5 Global purpose & competitiveness 18

1.3.6 A real second home in Britain 19

1.3.7 A Central Point: CRE unchanging on the outside but evolving within 20

1.4 Educating CRE 21

1.4.1 British universities 21

1.4.2 An educated CRE case study: The University of Buckingham 21

1.4.3 Britain's Real Commercial Education Industry 22

1.4.4 Education, Education & Education 23

1.4.5 Case Study: Students, UNITE-d 23

1.5 Great retail developments 24

1.5.1 The Amazon story: Reading between the real estate lines 24

1.5.2 CREacting commercial space in a flash 25

1.5.3 All change: The moving story of Aldwych Station 25

1.5.4 CREating new Markets from old 26

1.5.5 Gateshead's MetroCentre; A Real development turning point 26

1.5.6 Ring in positive change: Birmingham's Bull Ring Centre story 27

1.5.7 High street Real estate, the butcher, and baker and... 28

1.5.8 Betting on a continued real estate need 28

1.6 Hospitality & Leisure 30

1.6.1 Center Parcs building its fifth British resort, creating 2,700 jobs 30

1.6.2 Licensed to change 30

1.6.3 Hotels: A home from home 31

1.6.4 Who could have accurately pictured that? 31

1.6.5 Britain's built ReCREational space 32

1.6.6 A Real Olympian effort 32

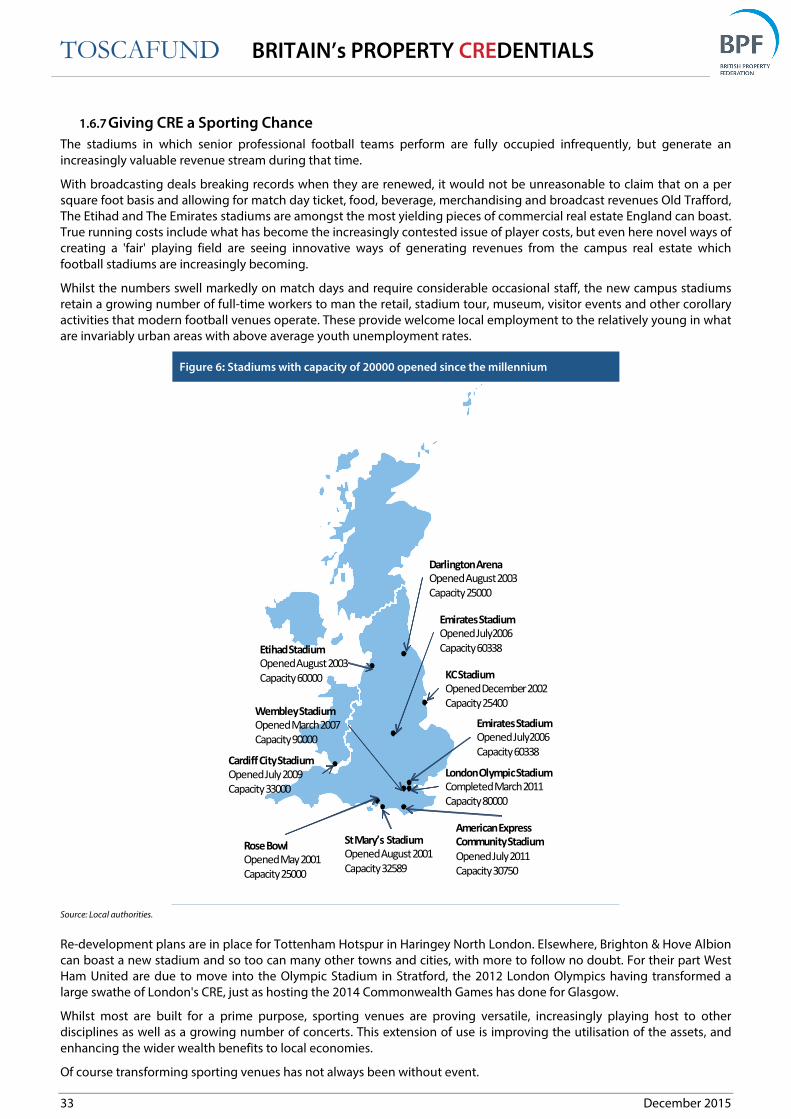

1.6.7 Giving CRE a Sporting Chance 33

1.6.8 Britain’s winning CREw 34

1.7 Private Rental Sector 36

1.7.1 Britain's Modern Work Houses 36

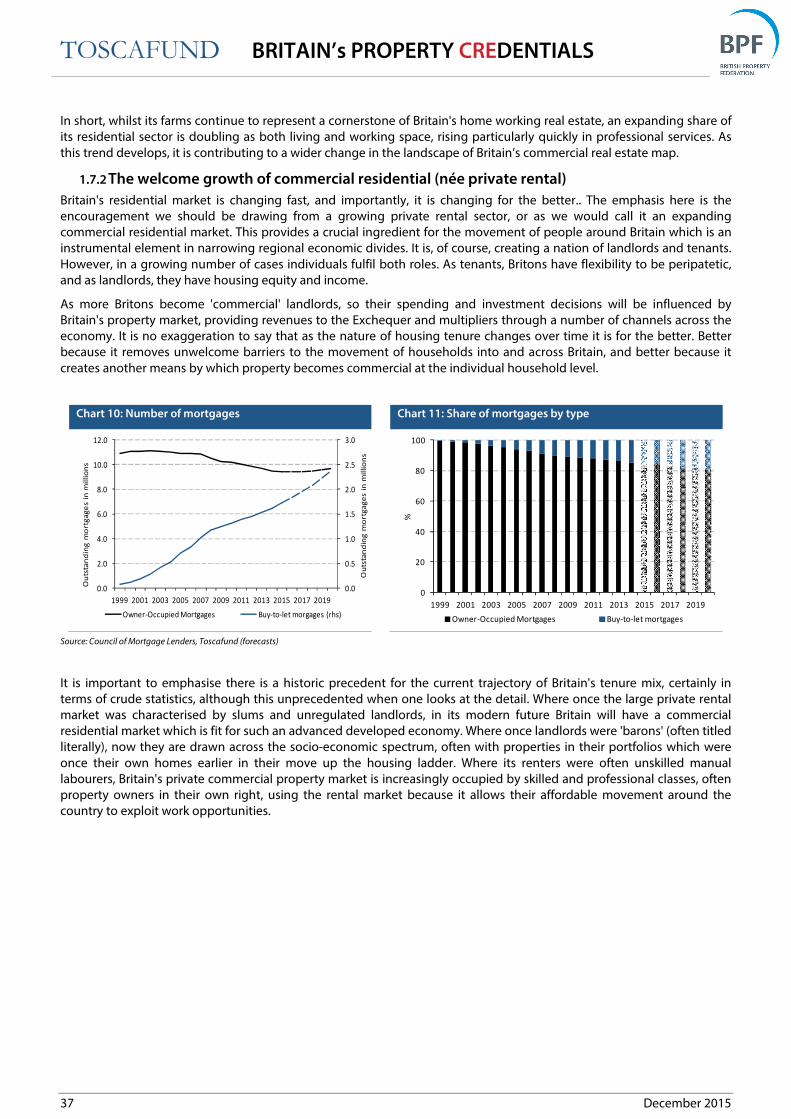

1.7.2 The welcome growth of commercial residential (née private rental) 37

1.8 Manufacturing CREativity 38

1.8.1 Real estate’s Food for thought 38

1.9 Flexibility 38

1.9.1 Property arriving from above 38

1.9.2 Protean property 39

1.9.3 Our future is in the clouds but still very real 39

1.9.4 The regeneration of Nine Elms & Battersea: a case study in regeneration and relocation 40

1.9.5 Time to open up Britain's CRE 41

1.9.6 Mixed and change of use property: all for the better 41

1.9.7 Productive Property 42

1.9.8 Self-contained property 42

1.9.9 Moving buildings: It's elementary 43

1.9.10 Britain's sustainably eco-friendly built-scape 44

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

6 December 2015

Part 2. Analytics of Britain’s CRE sector: concepts and numbers 45

2.1 Definition and Value 45

2.1.1 Definition 45

2.1.2 Some taxing concerns over CRE taxonomy 46

2.1.3 Valuation 47

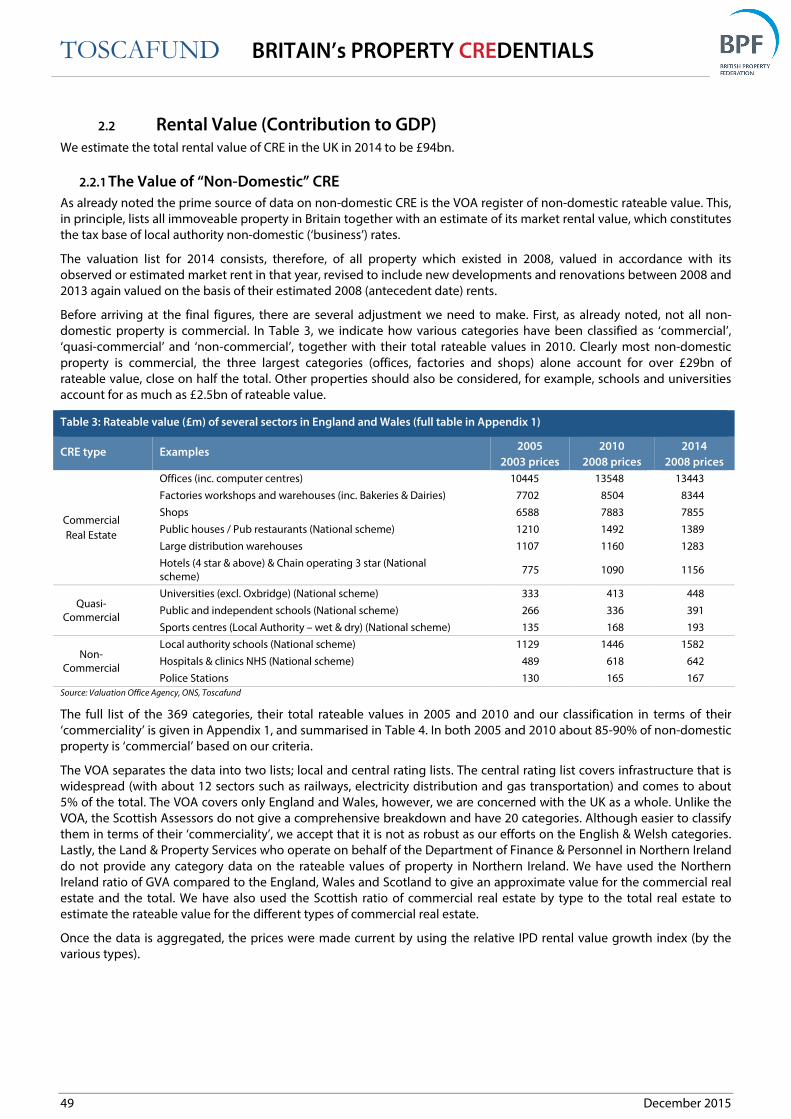

2.2 Rental Value (Contribution to GDP) 49

2.2.1 The Value of “Non-Domestic” CRE 49

2.2.2 The Value of Private Rental Housing 51

2.2.3 CRE and the generation of household income 53

2.3 The Asset Value of CRE (CRE as an investment class) 54

2.3.1 The value of Britain's CRE: AcCREdited and AcCREtive 54

2.3.2 The Asset Value of CRE 54

2.3.3 CRE as a proportion of national wealth 56

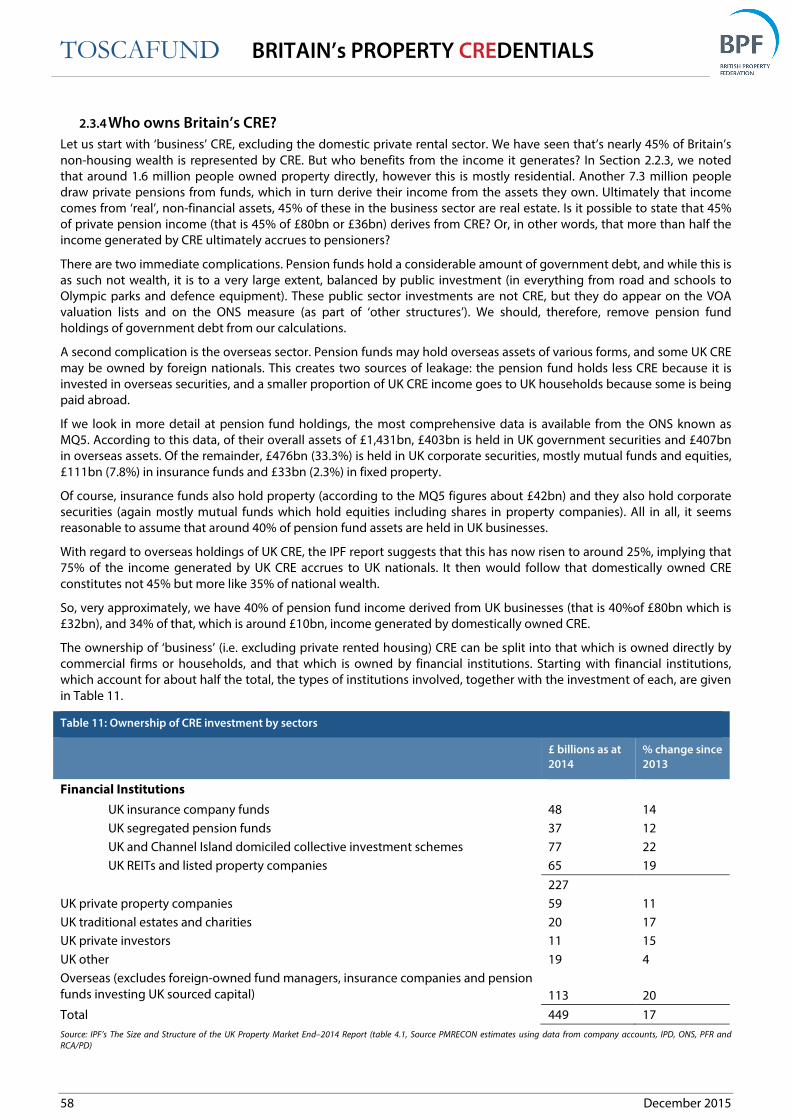

2.3.4 Who owns Britain’s CRE? 58

2.3.5 Ownership – the significance of foreign capital 59

2.3.6 Understanding the reason for foreign capital 60

2.4 Employment 62

2.4.1 A CREator of jobs 62

2.4.2 ‘Multiplier’ externalities 63

2.4.3 The employment value Britain's CRE construction 64

2.5 CRE and Taxation 66

2.5.1 The burden of taxation on CRE relative to other factors of production 66

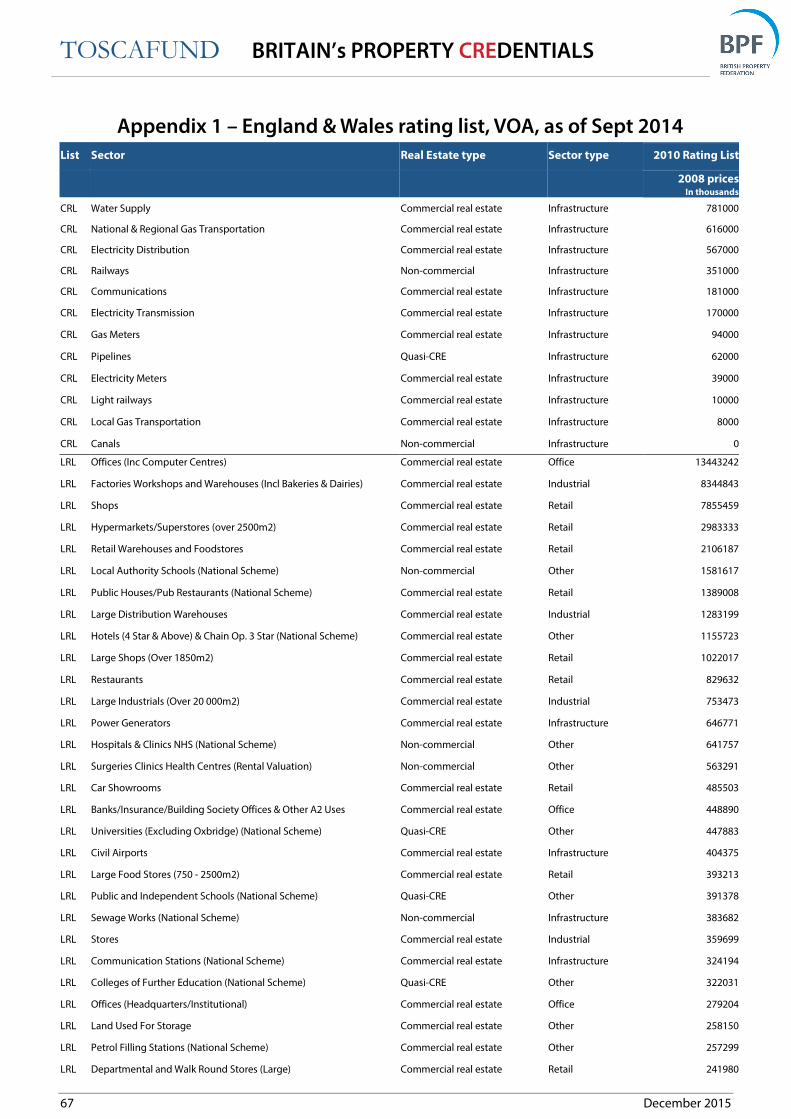

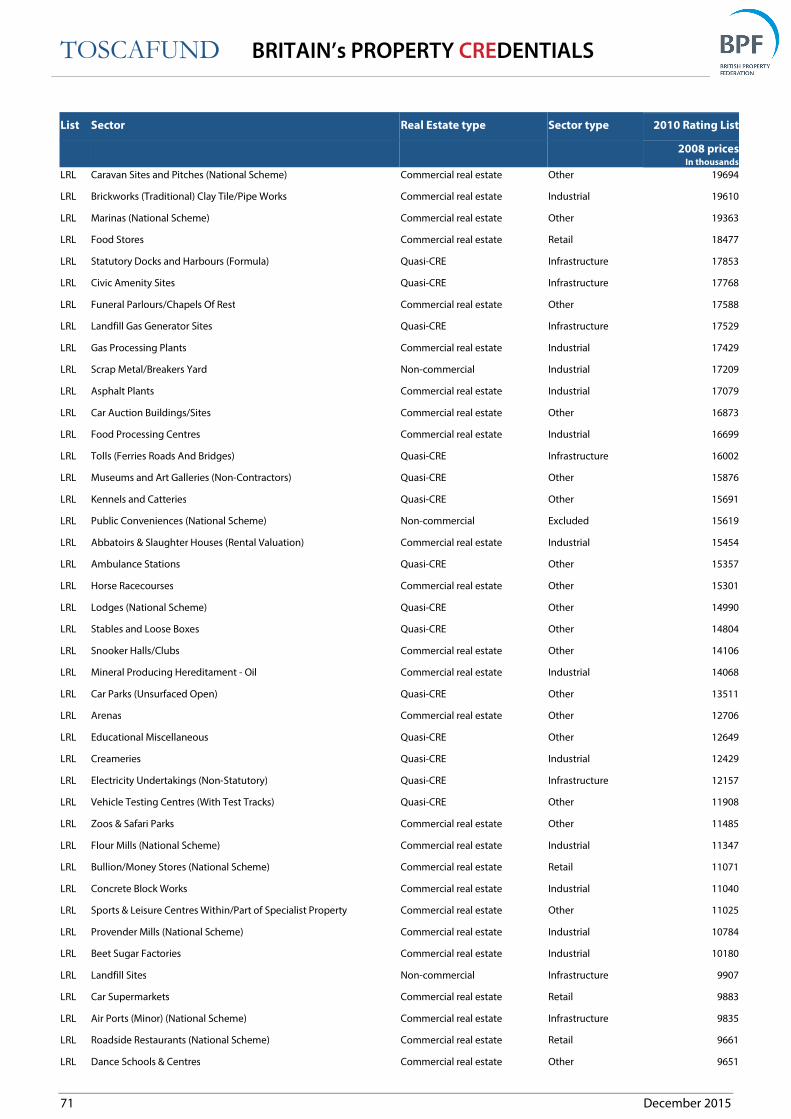

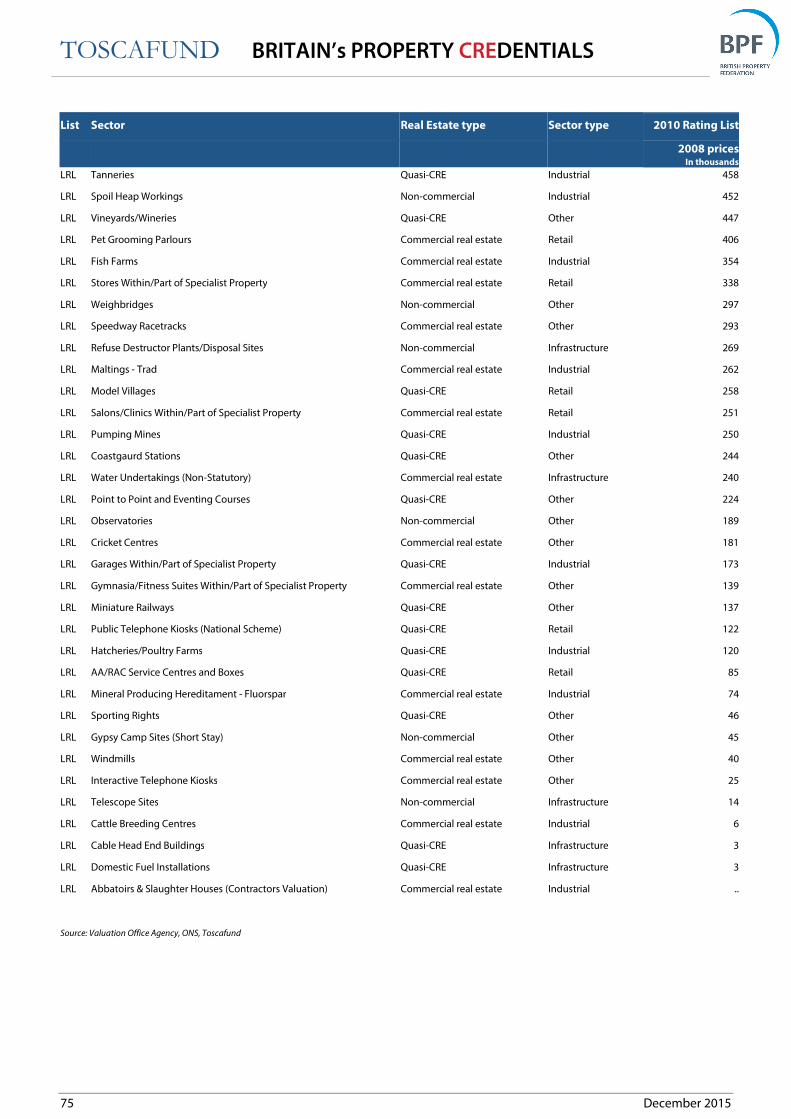

Appendix 1 – England & Wales rating list, VOA, as of Sept 2014 67

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

7 December 2015

Introduction

In this report, we argue that commercial real estate (CRE) makes a great, if not always fully recognised, contribution to

Britain’s economy, its environment and to the well-being of its people. But that contribution could, and should be

greater. The report identifies some factors hindering CRE from achieving its full potential, in particular fiscal arrangements

that discourage investment and thereby reduce its contribution to economic activity and growth.

We define CRE as property that generate income for its owner. This is not, however, the only function – on the contrary,

CRE makes an important contribution to the environment, to employment and to economic development – but we

suggest that without income generation real estate cannot be defined as ‘commercial’. This definition, based on function,

is wider than those sometimes used and includes, for example, property such as airports and buy-to-let housing. We

argue that the best measure of the contribution of CRE to GDP is the market rent generated by commercial property. In

2014, this amounted to just over £94bn in the UK - about 5.4% of GDP, or around one-quarter of the contribution of ‘non-

human’ inputs to national output.

But the economic value of CRE is not just an input to current production; it also constitutes a significant component of

marketable wealth. We estimate the current market value of CRE at around £1,658bn, which represents 20.6% of total net

wealth. Often, commercial development is financed through debt, equity or other financial instruments that are

themselves held by pension funds, banks or other intermediaries, so the claims on the income generated by CRE are

much more widely dispersed than might otherwise be expected.

Whilst income generation is a crucial part of the puzzle, CRE brings value in other ways too. Our towns and cities are

largely made of CRE, and confer wider benefits on the community. These wider benefits are, known as ‘externalities’.

There are other effects on the wider economy too. The construction and maintenance of CRE is a significant sector of

economic activity that contributes to the range of employment opportunities. CRE also contributes a substantial amount

of tax revenue. Indeed this report argues that, being immobile, CRE is an easy target for taxation and in consequence is

overtaxed relative to other factors of production.

The report is structured as follows. Part 1 illustrates CRE’s contribution with some striking examples taken from different

sectors, some better known such as the great developments in retail, hotels and leisure, but also many less obvious

where CRE has played a crucial role including transport and infrastructure, professional services and IT, universities and

private rented housing. From this wide range of examples we draw out a number of themes, for example flexibility,

allowing buildings designed for one purpose to be easily converted into another.

Part 2 turns from illustrations to statistics. We provide detailed information and sources for the estimates and claims

made in this introduction. We set out our definition of CRE and show how it can be measured using Valuation Office

Agency data on rateable values and housing data, and indicate why it differs from measures used elsewhere (for example

the Office for National Statistics’ Blue Book category of ‘non-residential buildings’). We derive estimates of the asset value

of CRE from these rental values. We note that despite all this, remarkably, the value of CRE has lagged behind that of

other assets such as dwellings. So lastly in this section we investigate the burden of taxation on commercial property. In

the UK the tax system is somewhat unbalanced and imposes higher rates of taxation on commercial property than on

other forms of investment, in particular owner-occupied housing (which now constitutes the bulk of the nation’s stock of

wealth).

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

8 December 2015

Part 1. Evolution of Britain’s CRE sector

1.1 The externalities (social benefits) of Britain’s CRE Let us begin by considering forms of property that, whilst only existing to facilitate the flow of people and materials –

bridges and tunnels – are a crucial built part of Britain’s commercial economy. After all, there can be no denying these

built features contribute towards GDP and that without them GDP would be materially lower, but by how much? The

answer lies in the realm of measurement of which good Jeremy Bentham termed felitous calculus. Before we begin our

attempt to quantify the value of property, we must illustrate its essential worth.

1.1.1 The ‘direct’ externalities of CRE

Whilst the concept of externality is widely recognised, there are disputes as to what should be included, and how such

elements should be measured. Our focus in this section is on the latent economic value of built infrastructure, and in

particular, the role of CRE.

There is considerable debate surrounding the cost-benefits of HS2. Whilst its critics argue that HS2 cannot possibly justify

the economic and environmental costs, its supporters present an argument based on the benefits of improved

connectivity and capacity, externalities which whilst impossible to precisely measure, will prove considerable all the

same. The argument behind HS2 is that the whole rail link, including new stations, will produce both a direct commercial

return along with much more important externality benefits. We will look at the HS2 project later in Part 1.2.3.

Externalities exist where some activity leads to direct benefits to some third party from which the person providing the

activity cannot or does not receive any payment, such as a silencer fitted to a car exhaust where the manufacturer cannot

recoup the cost from all the people who experience the less noisy environment. When considering CRE, there are two

major types of externality, which might be termed ‘amenity’ externalities and agglomeration externalities. Amenity

externalities exist when CRE creates a more pleasant built environment and thus enhances the quality of life for people

living and working in that area. These externalities are difficult to measure but clearly important: every developer knows

that local planning committees require a high quality of design in any new development and indeed the visual impact of

new buildings can play an important role in the regeneration of an area. Of course, the developer can hope for a higher

price for a more attractive building but much of the benefit accrues to local residents and those working in the area, who

cannot be made to pay for it. In Part 1 of this report we describe many examples of commercial development leading to

the regeneration of an area, from the refurbishment of the Victorian station hotels at King’s Cross and St Pancras to

Birmingham’s Bullring.

Externalities can also be created through relationships between firms rather than from firms to consumers. These are

known as ‘agglomeration economies‘, they exist when the productivity of one enterprise is increased by the proximity of

others. An example near to hand is London’s ‘silicon roundabout’, at the junction of Old Street and City Road. As with

California’s ‘silicon valley’, having a large number of small firms enables each to benefit from the ideas and developments

of others so that all are more productive but none is able to charge for the benefits it provides for the others. London

provides many examples of agglomeration of more traditional professional services also, such as the lawyers in the Inns

of Court.

We can also identify ‘co-ordination externalities’, which arise when businesses provide complementary services near to

each other, for example coffee shops and cafes located in shopping streets or in retail parks. Each contributes to the

overall experience, the cafes benefit from the trade brought in by shoppers, while at the same time providing rest and

refreshment to enable the shoppers to keep going for longer.

In all these cases, the economic contribution of the particular property may exceed the rent the landlord can charge.

Large-scale developments can sometimes ‘internalise’ a part of these externalities, most often however, it is not feasible.

In some cases, there will be insufficient investment by the developer in activities generating positive externalities

because much of the benefit goes to third parties. With commercial developments, much of the potential development

gain in land values can be effectively taxed away by planning authorities wanting to ensure as large as possible benefit to

the community as a whole from the commercial investment.

While specific examples can convey the importance of these effects, actual measures are more difficult to obtain. One

approach is to measure the appreciation of local property prices, in particular of housing, on the basis that if a

development improves an area people are willing to pay more to live there. Again this has to be done on a case study

basis.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

9 December 2015

1.2 Infrastructure and transport Before looking at examples of CRE, we must look at the physical and organisational structure of the UK. Without

investment in this key area, there will be bottlenecks as the growth of UK’s production and distribution of goods and

services increases. In this section, we consider transport hubs and their networks.

1.2.1 Construction and the Growth of GDP

Economic growth depends on investment but investment takes many forms, not only physical capital but also research

and development and the education and training of the workforce. Within tangible physical capital we see investment in

plant and machinery, vehicles and infrastructure as well as into commercial and residential property. After years of

stagnation following the financial crash of 2008, growth has returned to the UK economy and with it, we will argue, the

need for greatly increased investment in CRE. Consider just one example: airports. Most major airports in the UK are now

privately owned (albeit heavily regulated) and generate profits for their owners. The VOA rateable values for England &

Wales for airports come to £0.5bn (0.8% of the total, current prices, as of September 2014). According to our definitions

we have characterised Britain’s airports as elements of its CRE asset base. The gross income they generate derives from

charging airlines for landing slots (and in charging retailers for retail sites in the terminals) and their contribution to GDP

consists of these rents or charges less any material input costs (such as heating and lighting). In all these respects they are

equivalent to other commercial companies and thus properly part of CRE.

And clearly airports play a crucial role in economic growth. Every day we hear from business leaders how economic

growth is being held back by lack of airport capacity and this is even though passenger figures for Heathrow and Gatwick,

for instance, are regularly breaking new highs. In fact, between them these airports catered for well over 110m

passengers in 2014. Whilst terminals have enjoyed considerable investment, runway capacity has been slow to increase.

Rising passenger numbers are edging Britain’s main airports towards their capacity, with the Department for Transport

forecasting that London’s main airports could be “full” by 2025.

Keenly-interested observers such as the CBI suggest that lack of investment in runway capacity has restricted growth in,

for instance, Heathrow (53%) to one-third the rate enjoyed by Paris Charles de Gaulle (142%) over the past 20 years, and

slower also that the 84% recorded by Frankfurt. The inference is that failure to increase airport capacity damages Britain’s

competitiveness. The CBI cited a survey of large multinationals in which 85% considered air connections to both

established and emerging markets a significant factor in their decision over where to invest.

The 2014 CBI report which examined airport activity warned “Our network offers spare capacity where there is little

demand [for flights to emergent nations] and no capacity where demand is greatest”. It concluded that “a hub airport

with spare capacity offers the greatest chance of new routes to emerging markets. UK businesses want to see additional

hub capacity prioritised as the best prospect for supporting new trade”. The CBI was categorical in its statement that once

the Davies Commission had published their report, “it is imperative that the government of the day acts immediately to

create the necessary planning policy statement and statutory instruments to get building by the end of the parliament”.

Addressing the Commission directly, the CBI report pleaded “it must balance the economic imperative with

environmental considerations and logistical realities to serve the government with a politically deliverable solution”.

For an open-economy capitalising on mobility into and out of it by people and goods airports have, in our view, to be

considered crucial factor in economic growth. In the UK, investment in terminals must now make way for investment in

infrastructure, that is runways, to raise capacity for international travel.

While airports are a clear example of the importance of one type of CRE to economic growth, the commercial sector as a

whole is sometimes characterised as being rather less exciting. Of course people need buildings to work in, but some say

new technologies can manage without it, or at least diminish its importance. In our view this conclusion is misleading.

This report includes examples, from cloud technology to the Post Office, where technological change has led not to a

reduced demand for CRE but a change in the way we use it, the technology leading to new services and different types of

use and with them a demand for different types of CRE.

But nor should one ignore the continuing demand for traditional types of CRE such as offices, shops and hotels. We have

already seen that CRE accounts for a large proportion (more than a quarter) of the capital stock, and leaving aside

dwellings, non-residential CRE accounts for an even larger proportion (close on 30%) of ‘commercial capital’. As the

quantity and quality of CRE improves, work will become more productive and job opportunities, and wages, will increase.

The UK economy is expected to experience growth in the labour force over the medium term; only if this is matched by a

more rapid growth in other inputs including CRE can wages grow and employment opportunities improve.

Our leading example though carries a warning sign. The growth of airports has been restricted largely by planning

controls, which are of course understandable in the case of airports because of their adverse environmental effects (noise

and air pollution). Equally for many other types of CRE, the environmental effects are positive and indeed a major part of

the contribution a new development makes to economic welfare.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

10 December 2015

1.2.2 Bringing derelict CRE back to economic life

Its new name is no accident, for the St Pancras Renaissance Hotel (which opened its doors in 2011) has delivered an

economic boost to an area blighted for decades because large parts of its real estate remained derelict. Whilst this

particular Renaissance is one of many which have been seen over time, Britain is still home to a great deal of once

economic active real estate which is now moribund. There is great potential for such assets to be brought back to

commercial life and to deliver economic benefits through restoration and then subsequent operation.

The Renaissance has been an impressive restoration of The Midland Grand Hotel designed by George Gilbert Scott and

which fully opened in 1873, only to close in 1935. From 1935, until work began on its revival, the building was largely

derelict and if anything an economic liability. Now with its 211 rooms, 34 suites, numerous restaurants and bars, it is an

impressive and economically-enhancing asset.

In close proximity, neighbouring King’s Cross station stands The Great Northern Hotel, designed by Lewis Cubitt, a

building which pre-dates The Midland Grand Hotel, opening for business in 1854. Like its neighbour and indeed other

grand and more modest station hotels across Britain, the fortunes of the Midland Grand suffered during the period in

which rail passenger numbers fell. The consequences of this decline would ripple out to all those businesses which had

come to rely in some way on its guests.

Having been closed for 12 years – but fallen into a state of near dereliction for a period before – The Midland Grand has

recently re-opened its doors and come back to commercial life and generating considerable economic multipliers. Just as

its fortunes had previously moved in tandem with rail travel so it is again, now benefiting moreover from its proximity to

the Eurostar.

Chart 1: Rail passenger miles on franchised operators’ services, quarterly

Source: ONS (Office of Rail Regulation), Toscafund

Over in Holborn is the Rosewood London Hotel boasting 262 rooms, 44 suites, three restaurants and a handful of bars.

Originally completed in 1914 to a design by Percy Monckton, the building was not intended to be a hotel, but rather as

the headquarters of Pearl Assurance Company. In 1989, Pearl relocated their HQ from Chancery Court to Peterborough,

leaving the building unoccupied and economically idle. This idleness would end as redevelopment began in earnest in

the late 1990s and a hotel opening in 2000. Then in 2013, after £85mn of investment, the Grade II listed building re-

opened as a luxury five star hotel.

Not far away from the Rosewood Hotel is the now idle Bow Street Magistrates Court, a building finished in 1881. Over

time, high profile defendants have passed through the doors including the Pankhurst sisters, Oscar Wilde and Dr Crippen.

The building was finally vacated in 2006 having been sold to Irish developers hoping to convert it into a boutique hotel,

the plan derailed by events of 2008. As long as it remains economically inactive, the opportunity costs of its idleness

increase. Those unsure of the practicalities in converting a court house to a hotel need only look across from Covent

Garden to Soho, where the Grade II listed building which was once Great Marlborough Street Magistrates Court – where

Oscar Wilde was also a defendant, as were John Lennon and Mick Jagger - is now a 112-room hotel.

We could go on and map the locations across the length and breadth of Britain of imposing buildings that once provided

employment and economic multipliers which now lie inactive. One wonders whether the economic benefits of a

commercial revival of dormant or idle real estate are appreciated, or whether the mounting opportunity cost of real

estate inactivity is fully understood.

0

2

4

6

8

10

'02

-03

'03

-04

'04

-05

'05

-06

'06

-07

'07

-08

'08

-09

'09

-10

'10

-11

'11

-12

'12

-13

'13

-14

'14

-15

'15

-16

Ra

il p

ass

en

ge

rs o

n f

ran

ch

ise

d o

pe

rato

rs' se

rvic

es,

bn

mil

es

Long distance operators London and South East operators Regional operators

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

11 December 2015

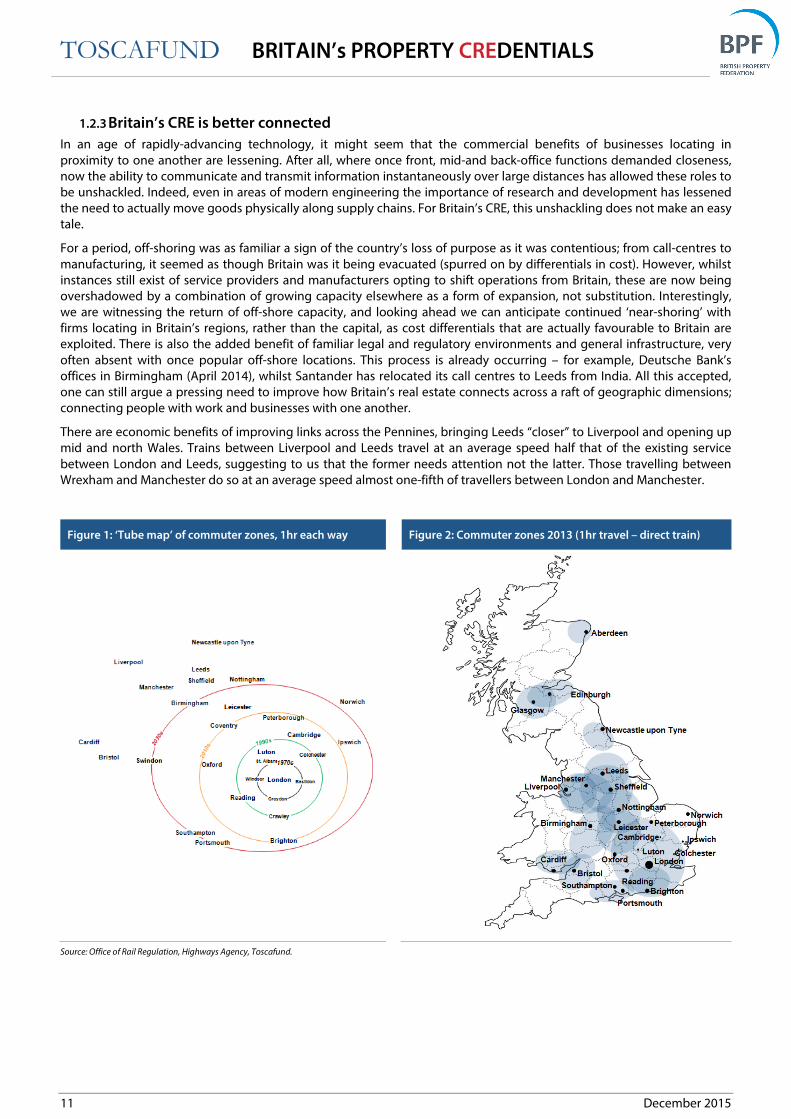

1.2.3 Britain’s CRE is better connected

In an age of rapidly-advancing technology, it might seem that the commercial benefits of businesses locating in

proximity to one another are lessening. After all, where once front, mid-and back-office functions demanded closeness,

now the ability to communicate and transmit information instantaneously over large distances has allowed these roles to

be unshackled. Indeed, even in areas of modern engineering the importance of research and development has lessened

the need to actually move goods physically along supply chains. For Britain’s CRE, this unshackling does not make an easy

tale.

For a period, off-shoring was as familiar a sign of the country’s loss of purpose as it was contentious; from call-centres to

manufacturing, it seemed as though Britain was it being evacuated (spurred on by differentials in cost). However, whilst

instances still exist of service providers and manufacturers opting to shift operations from Britain, these are now being

overshadowed by a combination of growing capacity elsewhere as a form of expansion, not substitution. Interestingly,

we are witnessing the return of off-shore capacity, and looking ahead we can anticipate continued ‘near-shoring’ with

firms locating in Britain’s regions, rather than the capital, as cost differentials that are actually favourable to Britain are

exploited. There is also the added benefit of familiar legal and regulatory environments and general infrastructure, very

often absent with once popular off-shore locations. This process is already occurring – for example, Deutsche Bank’s

offices in Birmingham (April 2014), whilst Santander has relocated its call centres to Leeds from India. All this accepted,

one can still argue a pressing need to improve how Britain’s real estate connects across a raft of geographic dimensions;

connecting people with work and businesses with one another.

There are economic benefits of improving links across the Pennines, bringing Leeds “closer” to Liverpool and opening up

mid and north Wales. Trains between Liverpool and Leeds travel at an average speed half that of the existing service

between London and Leeds, suggesting to us that the former needs attention not the latter. Those travelling between

Wrexham and Manchester do so at an average speed almost one-fifth of travellers between London and Manchester.

Figure 1: ‘Tube map’ of commuter zones, 1hr each way Figure 2: Commuter zones 2013 (1hr travel – direct train)

Source: Office of Rail Regulation, Highways Agency, Toscafund.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

12 December 2015

Figure 3: HS2 & HS3 plans Table 1: Statistics for selective rail journey across Britain

Time

(hr:min)

Average

Speed (mph)

HS2 Av

Speed

London Manchester 02:07 90.3 169

London Leeds 02:12 84.4 134

London Sheffield 02:05 77.7 123

London Birmingham 01:22 76.3 128

London Nottingham 01:44 72.9 111

Birmingham Bristol 01:21 69.3 Newcastle Manchester 02:23 65.1

London Southampton 01:14 63.2

Middlesbrough Sheffield* 01:56 52.8

Manchester Sheffield 00:48 52.4

Manchester Leeds 00:49 51.9

Birmingham Swansea* 03:01 51.8

Cardiff Liverpool* 03:16 50.6

Glasgow Inverness 03:50 48.4

Manchester Nottingham 01:49 46.7

Edinburgh Aberdeen 02:50 46.0

Middlesbrough Liverpool* 03:36 43.7

Leeds Liverpool 01:50 41.0

Lincoln Manchester* 02:20 39.8

Birmingham Wrexham* 02:09 34.0

Manchester Wrexham* 02:37 21.9

Source: HS2 website, Toscafund. Note: Black line signifies 70mph – National Speed Limit applies - *No direct trains, 1 or 2 stops required.

The table above highlights marked differences in average train travel speeds between regional hubs, some journeys all

the slower because they require passengers to change train. Of course, plans exist to improve the rail network

independently from HS2. The Chancellor, as recently as March 2015, has championed a HS3 high-speed rail link between

Manchester and Leeds, which he argued would reduce the travel time between these cities from 50 to 30 minutes and

help create a “northern global powerhouse”. Following on from George Osborne’s encouragement for improved links

across the Pennines, five cities across the North of England – Leeds, Liverpool, Manchester, Newcastle and Sheffield -

issued a joint report entitled ‘One North’ making the case for major investment in both rail and road links east to west to

improve the economic fortunes of the north by better connecting them. The reality is that the better connection being

encouraged is between commercial centres, and therefore CRE.

Some will throw back at us the argument made earlier that with mobile technology there should be no such thing as

“idle” travelling time. Others will point to “speedy” road links between locations otherwise poorly served by rail. Some will

claim there is no 'commercial' need for rail upgrades to the routes, for example between Wrexham and Manchester. The

argument is that these centres do not have much in the way of a “commercial connection”. Our response is: ‘forge a

reliable and speedy rail link between these, and their commercial connection will become real enough, by far better

commercially connecting their CRE’.

If Britain is to become a truly connected national economy then it demands 21st century links across its length and

breadth, boasting average travel speeds broadly in line across all its regional dimensions. This achievable ambition

should be the foremost aim of spending on transport infrastructure.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

13 December 2015

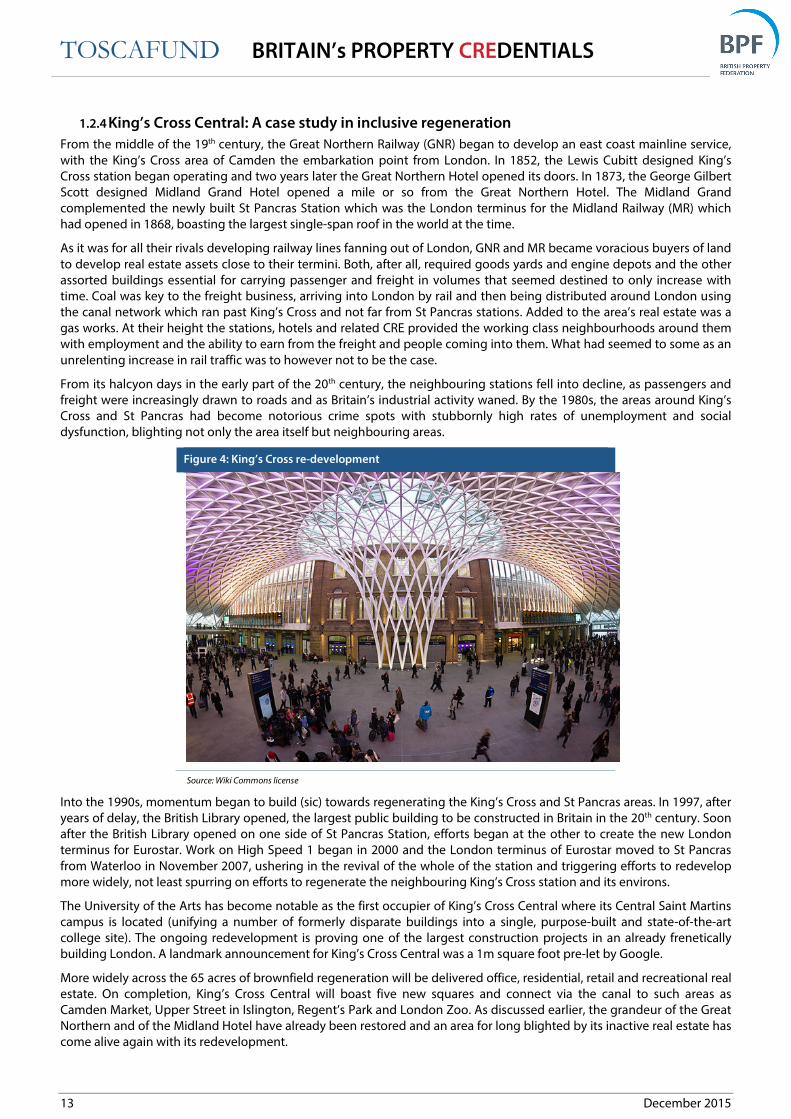

1.2.4 King’s Cross Central: A case study in inclusive regeneration

From the middle of the 19th century, the Great Northern Railway (GNR) began to develop an east coast mainline service,

with the King’s Cross area of Camden the embarkation point from London. In 1852, the Lewis Cubitt designed King’s

Cross station began operating and two years later the Great Northern Hotel opened its doors. In 1873, the George Gilbert

Scott designed Midland Grand Hotel opened a mile or so from the Great Northern Hotel. The Midland Grand

complemented the newly built St Pancras Station which was the London terminus for the Midland Railway (MR) which

had opened in 1868, boasting the largest single-span roof in the world at the time.

As it was for all their rivals developing railway lines fanning out of London, GNR and MR became voracious buyers of land

to develop real estate assets close to their termini. Both, after all, required goods yards and engine depots and the other

assorted buildings essential for carrying passenger and freight in volumes that seemed destined to only increase with

time. Coal was key to the freight business, arriving into London by rail and then being distributed around London using

the canal network which ran past King’s Cross and not far from St Pancras stations. Added to the area’s real estate was a

gas works. At their height the stations, hotels and related CRE provided the working class neighbourhoods around them

with employment and the ability to earn from the freight and people coming into them. What had seemed to some as an

unrelenting increase in rail traffic was to however not to be the case.

From its halcyon days in the early part of the 20th century, the neighbouring stations fell into decline, as passengers and

freight were increasingly drawn to roads and as Britain’s industrial activity waned. By the 1980s, the areas around King’s

Cross and St Pancras had become notorious crime spots with stubbornly high rates of unemployment and social

dysfunction, blighting not only the area itself but neighbouring areas.

Figure 4: King’s Cross re-development

Source: Wiki Commons license

Into the 1990s, momentum began to build (sic) towards regenerating the King’s Cross and St Pancras areas. In 1997, after

years of delay, the British Library opened, the largest public building to be constructed in Britain in the 20th century. Soon

after the British Library opened on one side of St Pancras Station, efforts began at the other to create the new London

terminus for Eurostar. Work on High Speed 1 began in 2000 and the London terminus of Eurostar moved to St Pancras

from Waterloo in November 2007, ushering in the revival of the whole of the station and triggering efforts to redevelop

more widely, not least spurring on efforts to regenerate the neighbouring King’s Cross station and its environs.

The University of the Arts has become notable as the first occupier of King’s Cross Central where its Central Saint Martins

campus is located (unifying a number of formerly disparate buildings into a single, purpose-built and state-of-the-art

college site). The ongoing redevelopment is proving one of the largest construction projects in an already frenetically

building London. A landmark announcement for King’s Cross Central was a 1m square foot pre-let by Google.

More widely across the 65 acres of brownfield regeneration will be delivered office, residential, retail and recreational real

estate. On completion, King’s Cross Central will boast five new squares and connect via the canal to such areas as

Camden Market, Upper Street in Islington, Regent’s Park and London Zoo. As discussed earlier, the grandeur of the Great

Northern and of the Midland Hotel have already been restored and an area for long blighted by its inactive real estate has

come alive again with its redevelopment.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

14 December 2015

1.2.5 CRE: Walking on water

It is unlikely that many of those walking along the Thames Embankment will be aware it was once marsh land. For it was

only in 1862, after a great many previous attempts had been thwarted, that the Sir Joseph Bazalgette project began.

On the completion of the Embankment, it had reclaimed a total of 22 acres of land from the Thames. Reclaimed too were

the Victoria - again along the north bank of the Thames - and Albert - along its south - Embankments. The embanking of

the Thames was, of course, far from the only way its natural landscape has been complemented over time by man-built

landscape.

We argue that a bridge or a tunnel should be considered Commercial Real Estate. Let us consider this with some actual

instances.

Over the years, bridges and tunnels have been added so as to connect the north and south sides of a rapidly expanding

London. Along the stretch where the Thames passes through the capital, the first fixed crossing was built by the Romans,

where London Bridge now straddles.

More bridges have been added to the London stretch of The Thames quite recently, the Millennium and Jubilee

pedestrian bridges in 2002. There is even talk of a Garden Bridge beginning near Temple Station linked to the Southbank

Centre. In a moment, we will consider another scheme being hotly debated, but before we do, let us return to those

bridges added in the 19th century.

A railway bridge across the Thames was opened in 1864 by St Paul’s (later renamed Blackfriars). This carried trains of the

London, Chatham and Dover Railway line. Alongside this bridge a second St Paul’s bridge would open in 1886, becoming

Blackfriars Bridge in 1937. The original St Paul’s bridge would however be removed in 1985 with its rail traffic taken

instead by Waterloo Station. Its southern abutment and a series of imposing piers would remain testament to its

existence, and from 1985 until 2009 the piers would remain curiosities to those walking across – the second – Blackfriars

Bridge. They were reclaimed by the railway when a state of the art station was opened in 2012.

The piers of the original Blackfriars (nee St Paul’s) Bridge now support the world’s first station with platforms that span a

river. It is also the world’s largest solar bridge, providing 50% of the station’s energy needs. Whilst we can debate whether

railways stations and tracks constitute CRE, many of those travelling to, through or from Blackfriars Station will be doing

so for commercial good. It is also instructive to reflect on how bridges across the Thames were once lined by shops and

homes with tolls commonly levied on those crossing them.

This section began by reflecting on a particular instance where marsh land has been reclaimed to create London’s

impressive Embankment. We suggested that few of those walking or driving along it would know it was not “natural”, just

as many today may be unaware of other instances of land reclamation around us; for instance the Fenns. With this in

mind and in wondering where else land will be reclaimed it is impossible not to think of the Thames Estuary Airport,

which is part of a far larger reclamation plan for the Thames Gateway.

Much like the Embankment before it, the Estuary Airport idea has been talked about for some time, the first proposals

dating to the 1970s. Most recently those supporting the idea of an island airport point to successful precedents: the

airports in Osaka, Japan and Hong Kong. Proponents also present figures suggesting the value of the economic and

commercial benefits to areas in and around the new airport, bringing windfalls first in its construction and then

operation.

What cannot be in any doubt is the very real London Gateway development at Thurrock in Essex. This ambitious project is

forecast to last another 10 years and generate tens of thousands of jobs as DP World invest upwards of £1.5bn in the

scheme to create 2,700 metres of quay. Alongside the port infrastructure will sit considerable commercial real estate, the

distribution part alone occupying a 300 hectare site with planning permission for 10 million square feet of developed

space across its logistics park. The project comprises, amongst other elements one of the world’s largest deep-water

ports to handle the biggest container ships, a port complemented by one of Europe’s largest logistics parks and another

instance of overseas capital (in this instance from the UAE) entering the UK and targeting commercial infrastructure

projects.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

15 December 2015

1.2.6 CRE flying high

As affordable air travel took off, so too did an increasing number of holidaying Britons, and as the airports swelled with

those opting to travel abroad, the effects were felt at home. From coastal guest houses and holiday camps, to the

restaurants, bars and entertainment venues which relied heavily on seasonable tourism, a section of British commercial

real estate fell into decline, property which by its nature was regionally concentrated, blighting entire towns.

Although Britons continue to travel abroad with growing frequency and rising numbers, Britain’s tourist industry has

more recently enjoyed a renaissance, doing so as both Britons themselves opt to spend part of their leisure time on their

own shores and as a rising number of international tourists enter the country. Indeed, Britain is now the world’s eighth

most popular destination, with a historic high of 33 million visits1 in 2013, this growth being spurred on by arrivals from

emerging markets.

Tourists coming to Britain bring with them considerable windfalls to the economy, not least to our external account in

delivering valuable foreign income. Improved CRE has been a major contributor to this revival, bringing improvements to

hotel and recreational real estate but also to the transport network, including the development of regional airports.

Indeed, the budget airline model which at first proved so damaging to the fortunes of Britain’s domestic holiday sector is

now contributing strongly to its revival. For along with road and rail travel, affordable internal air travel is allowing visitors

to spend their time in Britain in a variety of different locations.

Budget airlines are also allowing Briton’s to travel around their country more affordably for both leisure and work. Indeed,

entirely new commuter classes have been created and so too inventive new acronyms; notably WILLIE – Work In London,

Live In Edinburgh. As we have already emphasised, such mobility can only help improve the growth mix across Britain,

and improvements to CRE is the structural element that makes this possible.

1 The figures relate to the number of completed visits, not the number of visitors. Anyone entering or leaving more than once in the same period is counted on each visit. The count of visits relates to UK residents returning to this country and to overseas residents

leaving it.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

16 December 2015

1.3 Offices and IT Despite the impact of technology in creating a virtual economic dimension, built space remains essential not only for

“traditional” activity but for the virtual world to function effectively. Offices currently account for a quarter of all

commercial real estate.

1.3.1 CRE in the clouds

As its traditional manufacturing has made way for a wide range of services, Britain’s CRE has been filled less and less by

plant and machinery and more and more by telephonic equipment, computers and all the servers and IT backups

essential to their operations. At first, the spatial demands of this kit was considerable, noisy “comms” rooms, which whilst

sometimes relatively small, often take up a not insignificant share of scarce and costly office space. However, as

equipment became more powerful, it began to shrink, and improved software required smaller hardware. More recently,

cloud computing has proven transformational, growing at 50% annually.

By utilising “The Cloud”, an ever growing number of businesses across Britain are able to do away with a large amount of

their individual computing infrastructure, thus releasing them from hardware which is expensive in both monetary and

floor-space terms. Whilst these changes within offices are relatively small, they are just one of a great many changes seen

across Britain’s CRE, and consequently leads us to another, the growth of data centres.

Across Britain, there are now 210 data centres. These provide their clients with a range of services including data storage,

security and business continuity. The choice of location for these relies on a range of requirements including proximity to

power grids and telecommunication infrastructure. Furthermore, there has to be consideration of transport links and

closeness of emergency services, since these will affect risk and security. In terms of their management, whilst Data

Centres are labour un-intensive, what staffing is demanded is highly specialist and carefully selected.

Just as the internet is altering how we shop, so too does virtual data storage and management. Just as the internet is far

from eliminating the need for retail CRE across Britain but instead changing the precise configuration of property

required to deal with “click and collect” spending, so too with virtual data storage. In place of its proliferated “comms

rooms”, Britain, faster than almost any other economy, is seeing the development of a relatively new type of CRE, Data

Centres. Whilst some may carry the title Cloud Centres, these are all very much Real Estate that the modern British

economy could not possibly function without.

1.3.2 CRE and the internet

To satisfy their durable, consumable and particularly food needs, Britons once almost exclusively visited stores to scan

shelves from which we would pick the goods that the customer would then transport home. Now we are increasingly

scanning websites to simply click for delivery. The implications of this behavioural change are proving as profound on the

CRE market as they are being misinterpreted. Whilst the nature of the ongoing shift is unprecedented, it is wrong to

imagine that the built landscape for retail is being altered for the first time or necessarily for 'the worse'.

The ongoing migration of footfall retail custom to the internet is having a profound influence on Britain's CRE. However,

far from reducing the precise floor space required by the grocery and non-food sectors, it is altering the nature of the

property needed, where it is needed to be and what form it needs to be in.

In place of CRE to display wares for shoppers to consider, Britain has a growing need for large central sheds from which to

distribute goods clicked from websites. In some cases these act as large hubs for more local distribution centres.

Behavioural shifts in retail are far from unknown, the superstores and retail parks that we are now so familiar with date

(for the most part) from the 1990s, and just as the development of these formats required an entirely new property

profile, so too do the new generation with the rise of internet-based sales and home delivery. British households are

changing their patterns of consumption and the impact on its CRE has not been confined to goods but services.

Consider the travel agents that were once ubiquitous on high streets. Whilst still present, their numbers have fallen

markedly. There has been a migration of the sector's property requirement, rather than its total elimination. Where staff

occupied relatively small high street travel agencies, they now sit in large call centres, and where once bookings were

almost entirely for travel abroad, Britain is seeing a growth in vacationing on its own shores, ushering yet more change to

its CRE landscape as holiday parks expand to meet this need.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

17 December 2015

1.3.3 Google: search for a real presence

Google has dramatically altered how we behave and is a service that we can connect to practically everywhere, two

million searches are made in Britain. With £3.4bn and £70.8m in UK revenue and profit respectively, Google directly

employs 52,069 workers around the world and only 1,835 in Britain.

For a time, Google became the symbol of all the threats to Britain's CRE. Many saw a business so dominant across virtual

space that it would confine itself to only a modest physical presence, and concerns over the real estate take-up of Google

and the growing numbers of other web-accessed businesses led to talk of a 'paradigm shift in the need for CRE across

Britain. This idea was summarily quashed when, on 17 January 2013, it was revealed that Google had pre-let a staggering

one million square feet of space at London's King’s Cross.

The Google/King’s Cross letting announcement was made all the more remarkable by the fact that Argent, the

developers behind the area's 2.4-acre regeneration, planned on restricting any single occupier to one 10th of what will be

delivered to Google. From being the epitome all the challenges to Britain's CRE, Google was recast as a role model for all

the benefits that the virtual world can offer the real estate world.

1.3.4 Sometimes developing Britain's CRE does not quite reach The Pinnacle

The development of The Shard and redevelopment of King’s Cross Central in London and Birmingham's Bullring Centre

stand up as examples of Britain's modern CRE being enhanced by perseverance and innovative design combined with

capital and even occupiers from overseas. However, not all planned developments have progressed as relatively

smoothly as these.

Plans for The Bishopsgate Tower were submitted in June 2005 and approved within a year, with demolition of existing

property beginning 12 months later. Preparation for construction started in May 2008, and within six months it was

announced that the originally speculative building had won two pre-lets, one for 80,000 square feet of office space and

the other for the restaurant intended to top the 945 foot, 63-floor tower (scaled down from 1,007 feet because of Civil

Aviation Authority concerns). Even at its reduced height the building, on being topped out, would be the highest in The

City of London and second tallest across the EU. Funding for the project was sourced from Saudi Arabia's Economic

Development Corporation and Arab Investments.

Even after the financial crisis struck work continued on what had by this time been renamed The Pinnacle, but whose

curling design led to it more fondly become known as The Helter Skelter. By the beginning of 2012 the Pinnacle's core

had reached the sixth floor and even uncertainty over continued funding seemed to have ended. Then work stopped, for

reasons, so it was suggested, ranging from a funding shortfall to problems with pre-lets because of the building’s

unconventional and impractical interior specifications. Construction has been suspended since, with speculation at one

point that the part built structure would be levelled and a less ambitious scheme undertaken. More recent talk has

suggested that when the project does resume, following approval of its re-design, it will be with the same eye-catching

exterior but much altered interior floor plans.

The experience of The Bishopgate Tower/The Pinnacle/Helter Skelter, blends a great many themes covered in this report.

The ambition to upgrade 'underbuilt' office CRE with a mix-use skyscraper funded from overseas, built speculatively and

with a wholly unusual and controversial design. It also perfectly illustrates how “events” over the inevitable drawn-out

development time line which large projects demand, can derail and delay. The reality all the same is that this unfinished

building happens to be located at the heart of the City of London’s thriving commercial underwriting and insurance

district, where other proximate schemes, 20 Fenchurch Street (the “Walkie-Talkie”) and 122 Leadenhall Street (The

“Cheesegrater”) having both proven that it is always possible to deal successfully with “events”.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

18 December 2015

1.3.5 Global purpose & competitiveness

To ensure its success, a large part of Britain's commercial property estate has to compete with international rivals. In this

brief section, we explain why Britain's commercial property estate holds a privileged position explained by a range of

factors. Some are exogenous to the property estate per se, such as Britain occupying a time zone positioned favourably

for around the clock activity for those in the Americas as much as those across Asia. In addition, Britain’s real estate is

located in an English-speaking economy with a long tradition of being home, for some an adopted home, to a highly

educated and skilled work force. Other factors are, however, very much endogenous, such as quality of build and

provenance of ownership. Most important of all, has been the pragmatism needed to deliver the type of property

essential for success even if this has meant a degree of development upheaval, and nowhere has this been more in

evidence than in London and in particular the “Square Mile”.

Around the City, one can identify place names that trace the Gates that once allowed access through the defensive

“London Wall”, and within the historic City of London, there are institutions that have occupied the same “premises” for

centuries. From the imposing Bank of England on Threadneedle Street, to the seemingly timeless George and Vulture

chop house in Castle Court, many date from the 18th century and some from long before. The idea, however, that the City

of London is unchanging is not something one familiar at close quarters with it would accept. For all its apparent

timelessness, the City of London has in fact been in constant evolution, with its buildings replaced with almost indecent

haste according to some.

Few aspects of the City’s architecture have seemed beyond limits: a large part of the original Bank of England styled by Sir

John Soane was demolished to make way for the Sir Herbert Baker creation present today. Even the “City institution” that

is the George and Vulture restaurant has come close to demolition. The reality is that whilst the names of its streets have

become timeless symbols of its position in global finance, the City of London’s architecture has not simply matched

contemporary design, but defined it. From the “Nat West Tower” opened in 1980, to the Lloyds Building first unveiled in

1986, to the “Gherkin”, 18 years later, London’s skyline has been in constant flux, a rate of change which has only

accelerated over time, creating a sense, in some cases, of architectural disposability. With each new construction comes a

new group of tenants, often including those who could not have been anticipated even a handful of years earlier, hence,

there is a natural evolution in the occupational character of London’s office space.

London is in the throes of delivering noticeable improvements to its transport infrastructure. It can look forward to

Crossrail and other upgrades to under and over-ground rail systems. By 2020, London will boast a number of impressive

new business districts, centred on the transport hubs of Paddington, London Bridge and King’s Cross, the latter being the

embarkation and disembarkation point for Eurostar.

The delivery of HS2, Crossrail, the Northern line extension and other transport improvements are all part of London’s

future. Returning our focus to its past, one could chronicle the City of London’s history in global finance back many

centuries, over which the nature and origin of its occupiers has changed and changed again and so too its property

estate.

TOSCAFUND BRITAIN’s PROPERTY

19

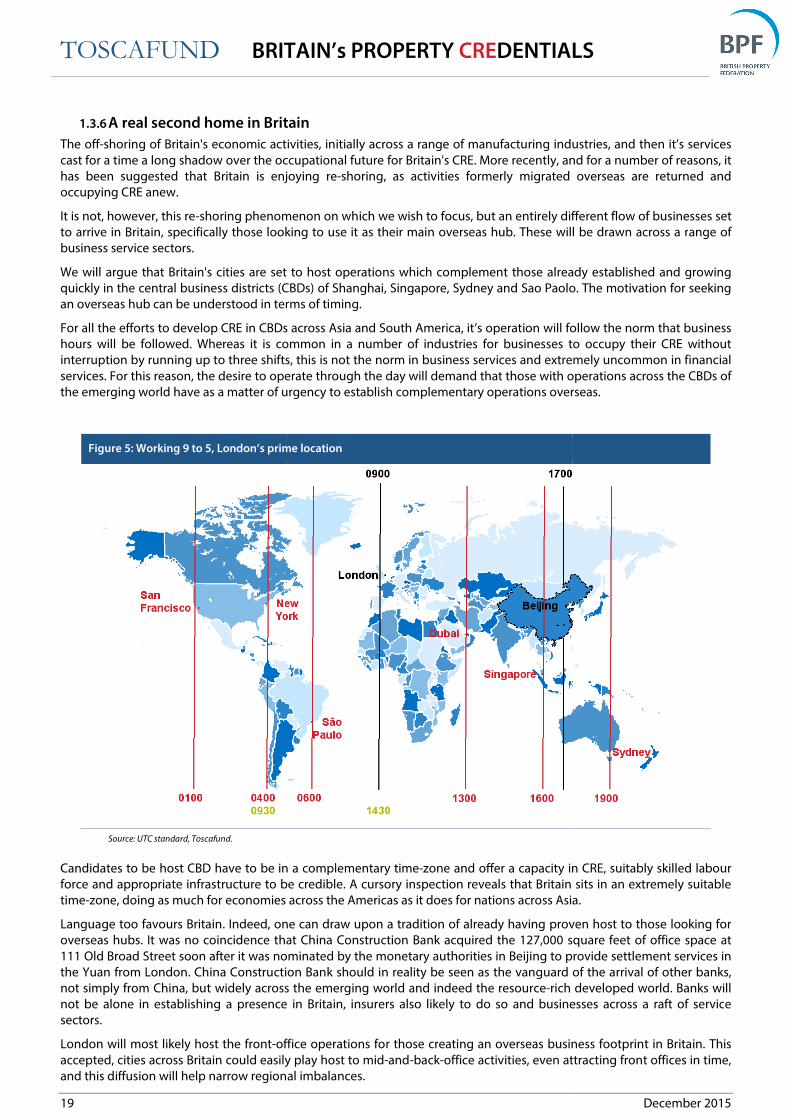

1.3.6 A real second home in Britain

The off-shoring of Britain's economic activities, initially across a range of manufacturing industries, and then i

cast for a time a long shadow over the occupational future for Britain's CRE. More recently, and for a number of reasons,

has been suggested that Britain is enjoying re

occupying CRE anew.

It is not, however, this re-shoring phenomenon on which we wish to focus, but an entirely different flow of businesses set

to arrive in Britain, specifically those looking to use it as their main overseas hub. These will be drawn across a r

business service sectors.

We will argue that Britain's cities are set to host operations which complement those already established and growing

quickly in the central business districts (CBDs) of Shanghai, Si

an overseas hub can be understood in terms of timing.

For all the efforts to develop CRE in CBDs across Asia and South America, it’s operation will follow the norm that business

hours will be followed. Whereas it is common in a number of

interruption by running up to three shifts, this is not the norm in business services and extremely uncommon in financial

services. For this reason, the desire to operate through the day will demand tha

the emerging world have as a matter of urgency to establish complementary operations overseas

Figure 5: Working 9 to 5, London’s prime location

Source: UTC standard, Toscafund.

Candidates to be host CBD have to be in a complementary time

force and appropriate infrastructure to be credible. A cursory inspection reveals that Britain sits in an extremely suitable

time-zone, doing as much for economies acr

Language too favours Britain. Indeed, one can draw upon a tradition of already having proven host to those looking for

overseas hubs. It was no coincidence that China Construction Bank acquired the 127,0

111 Old Broad Street soon after it was nominated by the monetary authorities in Beijing to provide settlement services in

the Yuan from London. China Construction Bank should in reality be seen as the vanguard of the arriv

not simply from China, but widely across the emerging world and indeed the resource

not be alone in establishing a presence in Britain, insurers also likely to do so and businesses across a raft of servic

sectors.

London will most likely host the front-office operations for those creating an overseas business footprint in Britain. This

accepted, cities across Britain could easily play host to mid

and this diffusion will help narrow regiona

BRITAIN’s PROPERTY CREDENTIALS

A real second home in Britain

shoring of Britain's economic activities, initially across a range of manufacturing industries, and then i

cast for a time a long shadow over the occupational future for Britain's CRE. More recently, and for a number of reasons,

Britain is enjoying re-shoring, as activities formerly migrated overseas are returned and

shoring phenomenon on which we wish to focus, but an entirely different flow of businesses set

to arrive in Britain, specifically those looking to use it as their main overseas hub. These will be drawn across a r

We will argue that Britain's cities are set to host operations which complement those already established and growing

quickly in the central business districts (CBDs) of Shanghai, Singapore, Sydney and Sao Paolo.

an overseas hub can be understood in terms of timing.

For all the efforts to develop CRE in CBDs across Asia and South America, it’s operation will follow the norm that business

hours will be followed. Whereas it is common in a number of industries for businesses to occupy their CRE without

interruption by running up to three shifts, this is not the norm in business services and extremely uncommon in financial

services. For this reason, the desire to operate through the day will demand that those with operations across the CBDs of

the emerging world have as a matter of urgency to establish complementary operations overseas

Figure 5: Working 9 to 5, London’s prime location

to be in a complementary time-zone and offer a capacity in CRE, suitably skilled labour

force and appropriate infrastructure to be credible. A cursory inspection reveals that Britain sits in an extremely suitable

zone, doing as much for economies across the Americas as it does for nations across Asia.

Language too favours Britain. Indeed, one can draw upon a tradition of already having proven host to those looking for

overseas hubs. It was no coincidence that China Construction Bank acquired the 127,000 square feet of office space at

111 Old Broad Street soon after it was nominated by the monetary authorities in Beijing to provide settlement services in

the Yuan from London. China Construction Bank should in reality be seen as the vanguard of the arriv

not simply from China, but widely across the emerging world and indeed the resource-rich developed world. Banks will

not be alone in establishing a presence in Britain, insurers also likely to do so and businesses across a raft of servic

office operations for those creating an overseas business footprint in Britain. This

accepted, cities across Britain could easily play host to mid-and-back-office activities, even attracting front offices i

onal imbalances.

DENTIALS

December 2015

shoring of Britain's economic activities, initially across a range of manufacturing industries, and then it’s services

cast for a time a long shadow over the occupational future for Britain's CRE. More recently, and for a number of reasons, it

shoring, as activities formerly migrated overseas are returned and

shoring phenomenon on which we wish to focus, but an entirely different flow of businesses set

to arrive in Britain, specifically those looking to use it as their main overseas hub. These will be drawn across a range of

We will argue that Britain's cities are set to host operations which complement those already established and growing

ngapore, Sydney and Sao Paolo. The motivation for seeking

For all the efforts to develop CRE in CBDs across Asia and South America, it’s operation will follow the norm that business

industries for businesses to occupy their CRE without

interruption by running up to three shifts, this is not the norm in business services and extremely uncommon in financial

t those with operations across the CBDs of

the emerging world have as a matter of urgency to establish complementary operations overseas.

zone and offer a capacity in CRE, suitably skilled labour

force and appropriate infrastructure to be credible. A cursory inspection reveals that Britain sits in an extremely suitable

oss the Americas as it does for nations across Asia.

Language too favours Britain. Indeed, one can draw upon a tradition of already having proven host to those looking for

00 square feet of office space at

111 Old Broad Street soon after it was nominated by the monetary authorities in Beijing to provide settlement services in

the Yuan from London. China Construction Bank should in reality be seen as the vanguard of the arrival of other banks,

rich developed world. Banks will

not be alone in establishing a presence in Britain, insurers also likely to do so and businesses across a raft of service

office operations for those creating an overseas business footprint in Britain. This

office activities, even attracting front offices in time,

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

20 December 2015

The reality is that Britain stands poised to be chosen as the preferred overseas hub for a raft of businesses from across the

emerging world. These promise to deliver wide ranging wealth benefits and generate considerable economic multipliers.

For Britain to welcome such arrivals, an expansion in its CRE capacity will be crucial, not simply in London but widely

across all its cities.

1.3.7 A Central Point: CRE unchanging on the outside but evolving within

One of the first skyscrapers in London, Centre Point has slid down the list to become the city's joint 27th tallest building.

This said it dominates the sky line from much of central London, and since 1995 can boast Grade II listed status. Centre

Point is an intriguing example of how so much has changed since its completion in 1966. The 385-ft office tower,

designed by Richard Seifert, stood empty for five years having been built speculatively. Its developer, the controversial

Harry Hyams, hoped for a single occupier for Centre Point, and stubbornly rejected offers to lease individual floors. On

finally receiving tenants, it has seen an evolution in occupiers which illustrates the changing nature of Britain's economy.

From July 1980 to March 2014, the building was the headquarters of the Confederation of British Industry (CBI). Occupiers

now in the building include US talent agency William Morris Agency; the state-owned national oil company of Saudi

Arabia, Aramco; Chinese oil company Petrochina; and electronic gaming company EA Games, a range of tenants who are

notable for being multinational, as much as multi-sector.

As well as a varied group of office occupiers, Centre Point is home to Paramount which opened in 2008, initially operating

as a private members club, this was changed in 2010 with Paramount opening to the general public. Occupying the top

three floors of the building, Paramount includes event space on the 31st floor, a bar and restaurant on 32nd and a 360-

degree viewing gallery on the 33rd floor – the top floor of the building.

In February 2013, the global members club for creative industries, ‘Apartment 58’, launched APT58 at Centre Point. The

members club, on the lower floors of the building, features a night club, meeting rooms, a locker and mail service and a

lounge. The venue also includes a late-license ground floor street-food concept restaurant.

Having passed through a series of owners since Hyams, Centre Point is now in the hands of Almacantar. It has received

planning permission to further refurbish the building. Its occupancy profile will change again, with plans for its

redevelopment into 82 luxury apartments, a pool, spa and gymnasium and 42,000 square feet of retail and restaurant

space.

With Centre Point, we have another example of British CRE unchanging on the outside and for periods economically

inactive on the inside, and whose occupation has evolved rapidly over recent years, spurred on by overseas tenants and

their capital, producing positive economic multipliers and externalities to commercial and indeed residential real estate

around it. These changes have been spurred on too by improvements to transport infrastructure in the vicinity of the real

estate.

TOSCAFUND BRITAIN’s PROPERTY CREDENTIALS

21 December 2015

1.4 Educating CRE Education is one of the UK’s most property hungry “commercial” sectors, we reflect on the recent and prospective

growth.

1.4.1 British universities

There may be some curiosity as to why Britain still has a predominance of non-profit making Universities and other

institutions of higher education, which we have identified as quasi-CRE? After all, the enhancement they provide to the

human capital of their students will associate in general with a long-term gain which should attract commercial and

entrepreneurial interest. The reality is that there are many privately and very commercially operated colleges across

Britain serving the needs of students originating mostly from overseas. Their reputations are, almost without exception,

inferior, precisely because of suspicions over their motivation. There is certain to be a suspicion that the motivation

behind the college is less about improving the human capital of students than about raising the financial capital of its

operators. It is for this reason, where reputation concerns are either real or imagined, that so many HEIs remain

stubbornly within the realms of quasi CRE rather than morphing into its direct form.

The University of Buckingham is an institution holding a Royal Charter and has a strong reputational standing, but it

operates with a funding structure outside of the norm; a HEI which could rightly be considered to be in the private sector.

The University of Buckingham operates with charitable status, but it’s model is nonetheless commercial. Looking ahead,

we would not be surprised if established HEIs begin to alter their models to move closer to the funding practice of the

University of Buckingham, and so overcoming reputational risk as they become “more commercial”.

1.4.2 An educated CRE case study: The University of Buckingham

The University of Buckingham’s size should not distract from the growth that it has achieved and the potential it

promises, more than doubling its student body in five years, and investing generously to maintain this momentum.

Whilst it may operate with charitable status as a non-profit making body dedicated to education and research, it can

boast being Britain's first independently funded University holding a Royal Charter. It is also unique in offering two year