€¦ · xls file · web view · 2016-11-15all cpm estimates are internal omd estimates, ......

TRANSCRIPT

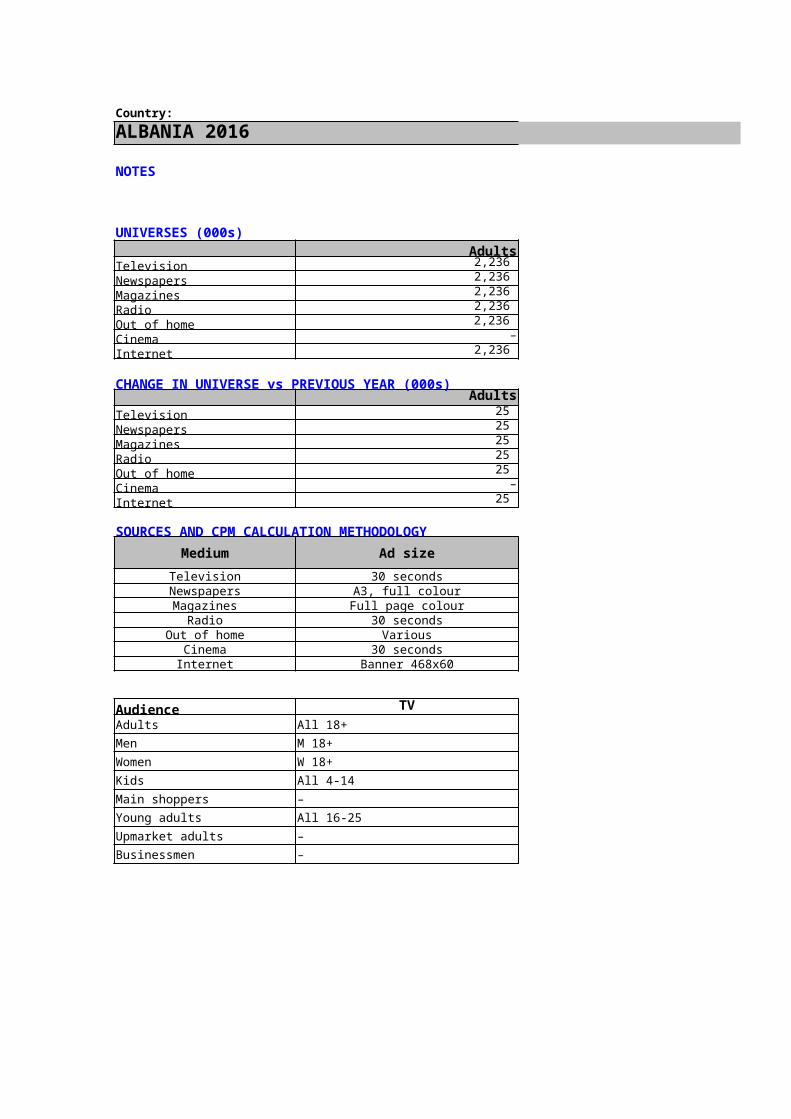

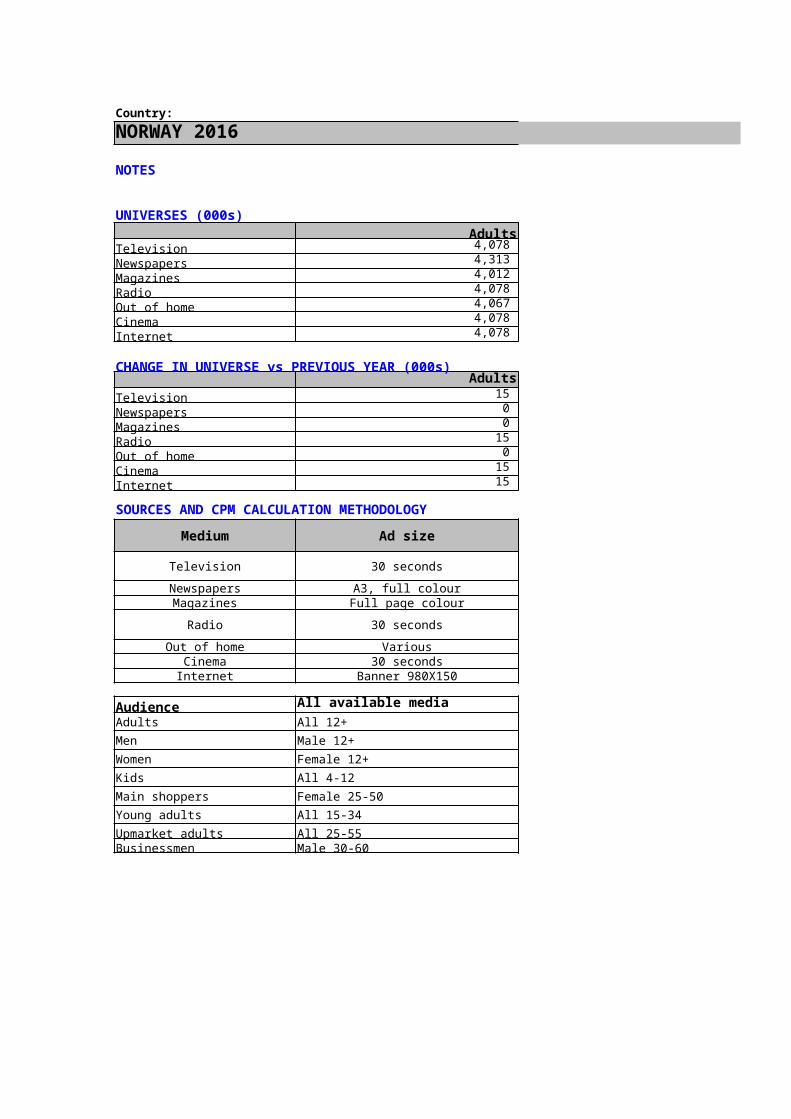

Country:ALBANIA 2016

NOTES

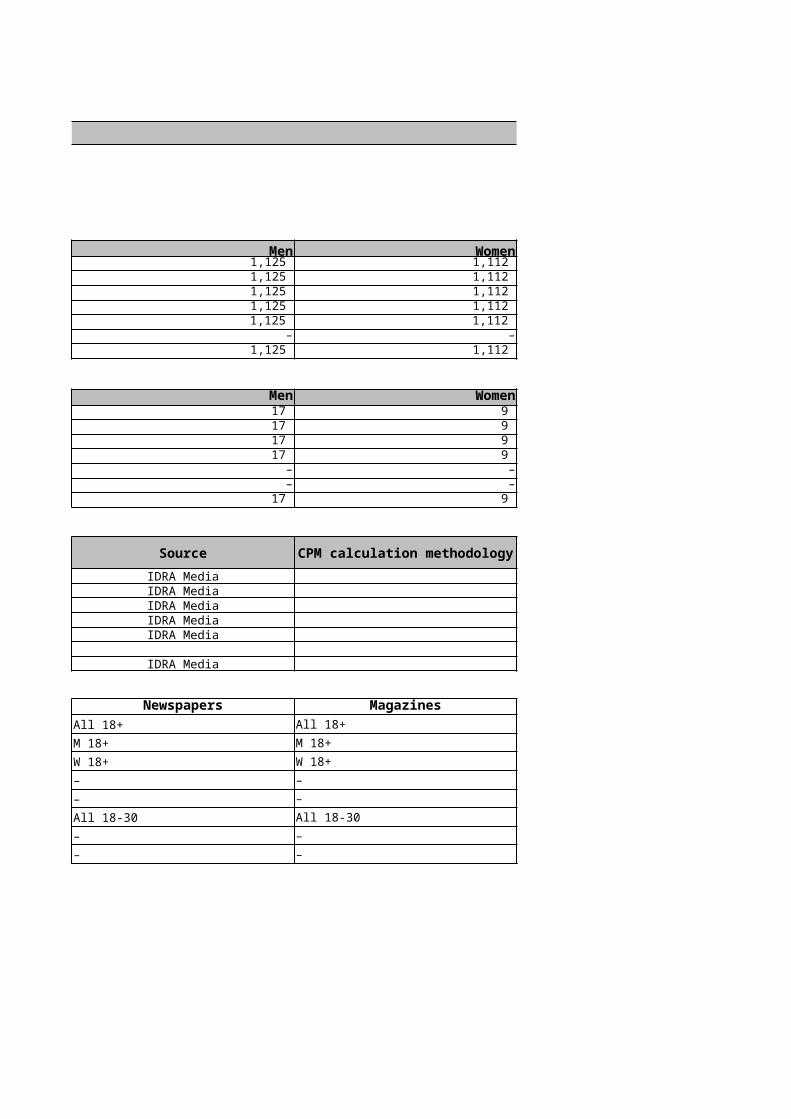

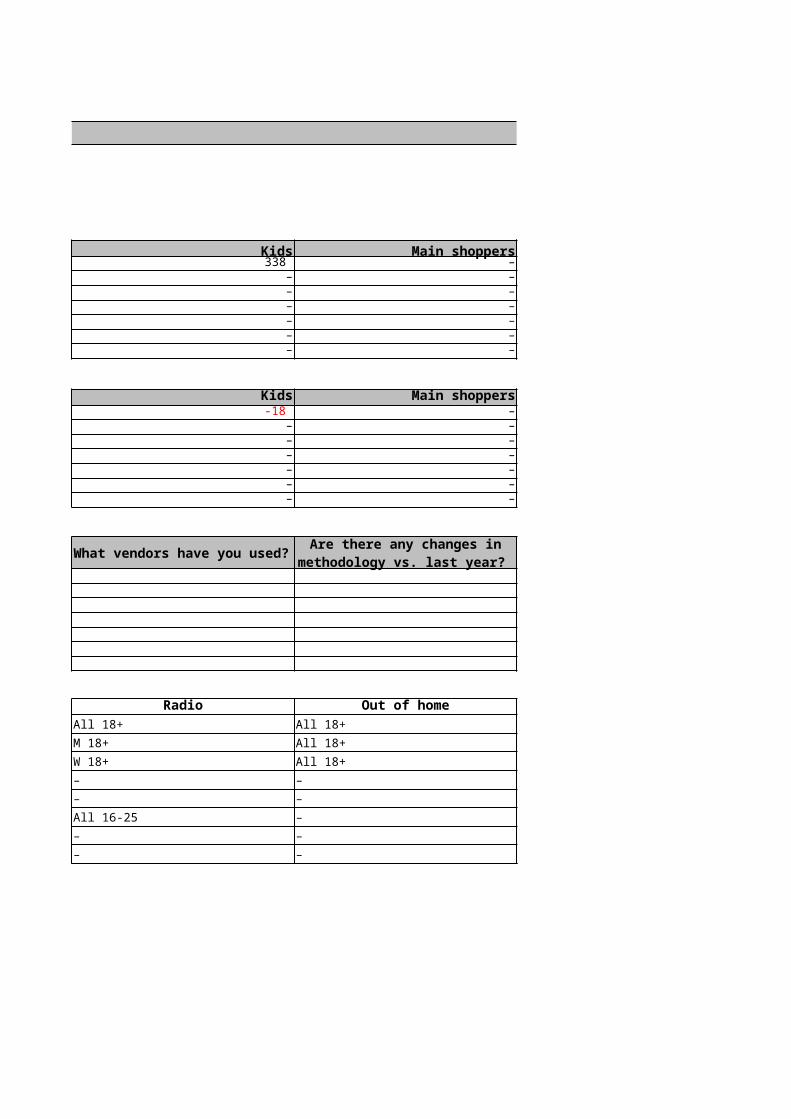

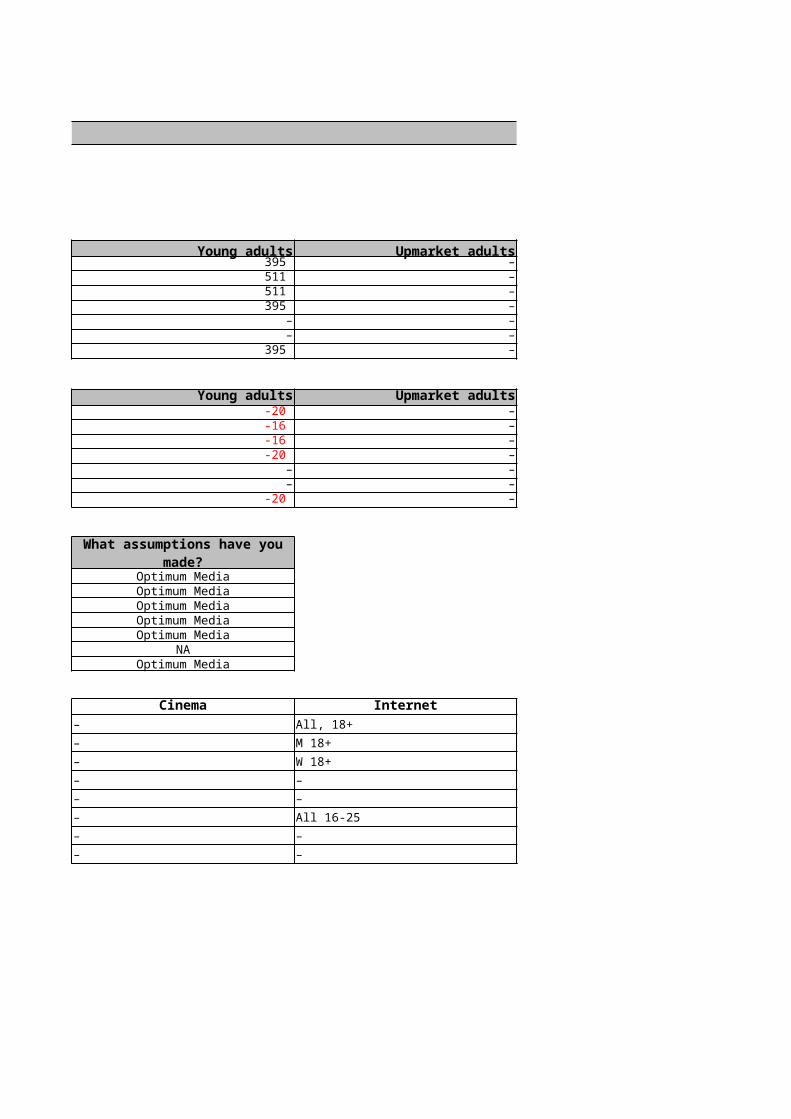

UNIVERSES (000s)Adults Men

Television 2,236 1,125 Newspapers 2,236 1,125 Magazines 2,236 1,125 Radio 2,236 1,125 Out of home 2,236 1,125 Cinema – –Internet 2,236 1,125

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 25 17 Newspapers 25 17 Magazines 25 17 Radio 25 17 Out of home 25 –Cinema – –Internet 25 17

SOURCES AND CPM CALCULATION METHODOLOGYMedium Ad size SourceTelevision 30 seconds IDRA Media

Newspapers A3, full colour IDRA MediaMagazines Full page colour IDRA Media

Radio 30 seconds IDRA MediaOut of home Various IDRA Media

Cinema 30 secondsInternet Banner 468x60 IDRA Media

Audience TV NewspapersAdults All 18+ All 18+Men M 18+ M 18+Women W 18+ W 18+Kids All 4-14 –Main shoppers – –Young adults All 16-25 All 18-30Upmarket adults – –Businessmen – –

ALBANIA 2016

Women Kids Main shoppers 1,112 338 – 1,112 – – 1,112 – – 1,112 – –

1,112 – –– – –

1,112 – –

Women Kids Main shoppers9 -18 –9 – –9 – –9 – –– – –– – –9 – –

Magazines Radio Out of homeAll 18+ All 18+ All 18+M 18+ M 18+ All 18+W 18+ W 18+ All 18+– – –– – –All 18-30 All 16-25 –– – –– – –

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

ALBANIA 2016

Young adults Upmarket adults Businessmen 395 – – 511 – – 511 – – 395 – –

– – –– – –

395 – –

Young adults Upmarket adults Businessmen-20 – –-16 – –-16 – –-20 – –

– – –– – –

-20 – –

Optimum MediaOptimum MediaOptimum MediaOptimum MediaOptimum Media

NAOptimum Media

Cinema Internet– All, 18+– M 18+– W 18+– –– –– All 16-25– –– –

What assumptions have you made?

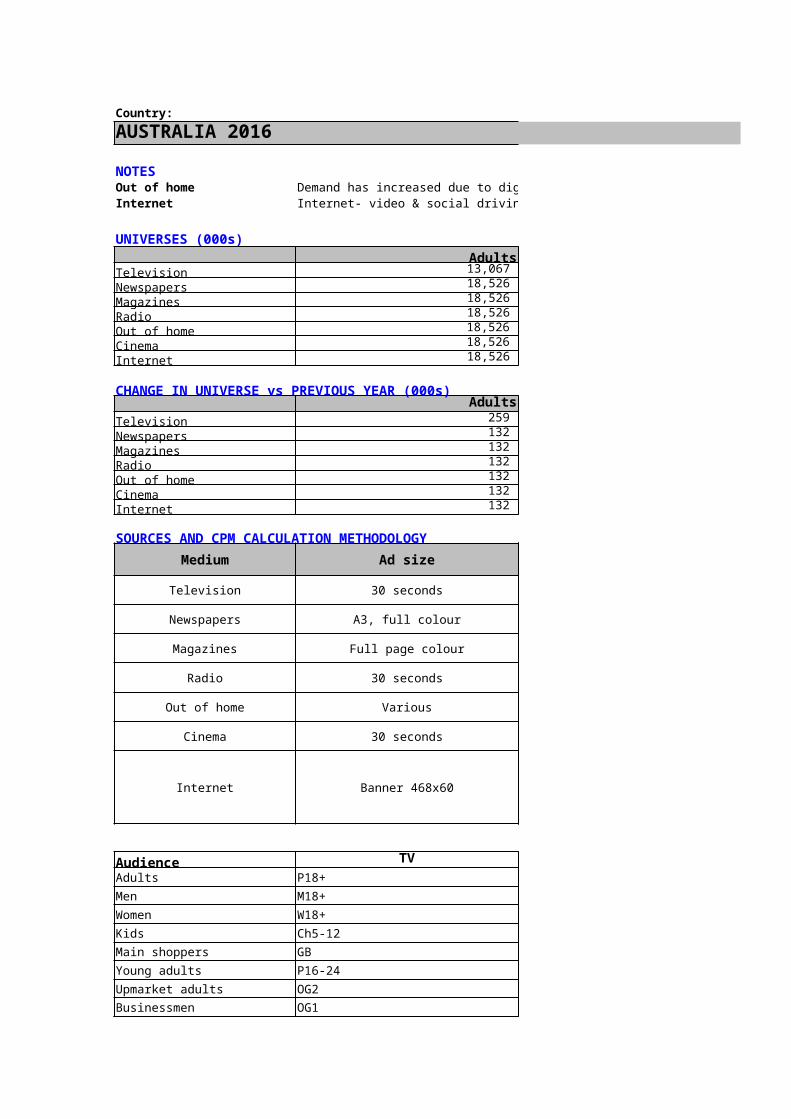

Country:AUSTRALIA 2016

NOTESOut of home Demand has increased due to digitisation of the medium, more premium inventory available.Internet Internet- video & social driving demand. Limited inventory in Australia.

UNIVERSES (000s)Adults Men

Television 13,067 6,409 Newspapers 18,526 9,105 Magazines 18,526 9,105 Radio 18,526 9,105 Out of home 18,526 9,105 Cinema 18,526 9,105 Internet 18,526 9,105

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 259 123 Newspapers 132 55 Magazines 132 55 Radio 132 55 Out of home 132 55 Cinema 132 55 Internet 132 55

SOURCES AND CPM CALCULATION METHODOLOGYMedium Ad size Source

Television 30 seconds Oztam

Newspapers A3, full colour Roy Morgan

Magazines Full page colour Roy Morgan

Radio 30 seconds Nielsen

Out of home Various MOVE

Cinema 30 seconds Cinema attendance Audience data

Internet Banner 468x60 Nielsen

Audience TV NewspapersAdults P18+ P18+Men M18+ M18+Women W18+ W18+Kids Ch5-12 Not SurveyedMain shoppers GB GBYoung adults P16-24 P16-24Upmarket adults OG2 P18+HH Income 100k +Businessmen OG1 P18+Professional

AUSTRALIA 2016

Demand has increased due to digitisation of the medium, more premium inventory available.Internet- video & social driving demand. Limited inventory in Australia.

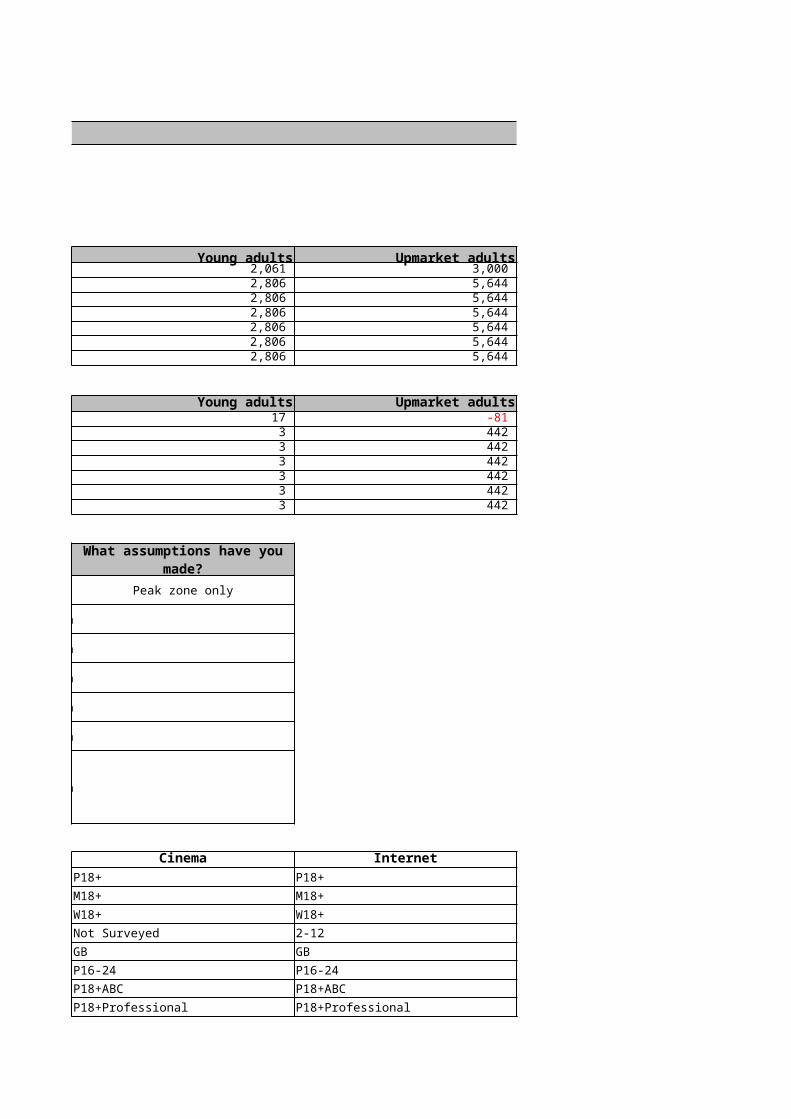

Women Kids Main shoppers 6,658 1,632 6,360 9,420 865 12,911 9,420 865 12,911 9,420 865 12,911

9,420 865 12,911 9,420 865 12,911

9,420 865 12,911

Women Kids Main shoppers137 36 121

77 -43 -142 77 -43 -142 77 -43 -142 77 -43 -142 77 -43 -142 77 -43 -142

No based on 2015 plus inflation

No based on 2015 plus inflation

No based on 2015 plus inflation

No based on 2015 plus inflation

No based on 2015 plus inflation

No based on 2015 plus inflation

No based on 2015 plus inflation

Magazines Radio Out of homeP18+ P18+ P18+M18+ M18+ M18+W18+ W18+ W18+Not Surveyed Not Surveyed Not SurveyedGB GB GBP16-24 P16-24 P16-24P18+HH Income 100k + P18+HH Income 100k + P18+HH Income 100k +P18+Professional P18+Professional P18+Professional

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

Ave Peak Rate /Ave Peak Audience (1/1/13 - 8/9/13

consolidated data)

Total Metro 5 cap City- 7/9/10 Network (incl digital channels)

Ave Metro Full Page rates/Readership figures

Ave Full Page rates/Readership figures

Ave Metro Rates/Nielsen Radio Audience data

Ave Metro Rates/Move Audience data

Ave Cinema Rate/Cinema attendance Audience data

Nielsen Market Intelligence/Online Consumer report/SMI market

spend figures/Ceasa/IAB PWC expenditure estimates/market

knowledge

AUSTRALIA 2016

Young adults Upmarket adults Businessmen 2,061 3,000 3,081 2,806 5,644 3,490 2,806 5,644 3,490 2,806 5,644 3,490

2,806 5,644 3,490 2,806 5,644 3,490

2,806 5,644 3,490

Young adults Upmarket adults Businessmen17 -81 -20 3 442 300 3 442 300 3 442 300 3 442 300 3 442 300 3 442 300

Peak zone only

Cinema InternetP18+ P18+M18+ M18+W18+ W18+Not Surveyed 2-12GB GBP16-24 P16-24P18+ABC P18+ABCP18+Professional P18+Professional

What assumptions have you made?

Country:

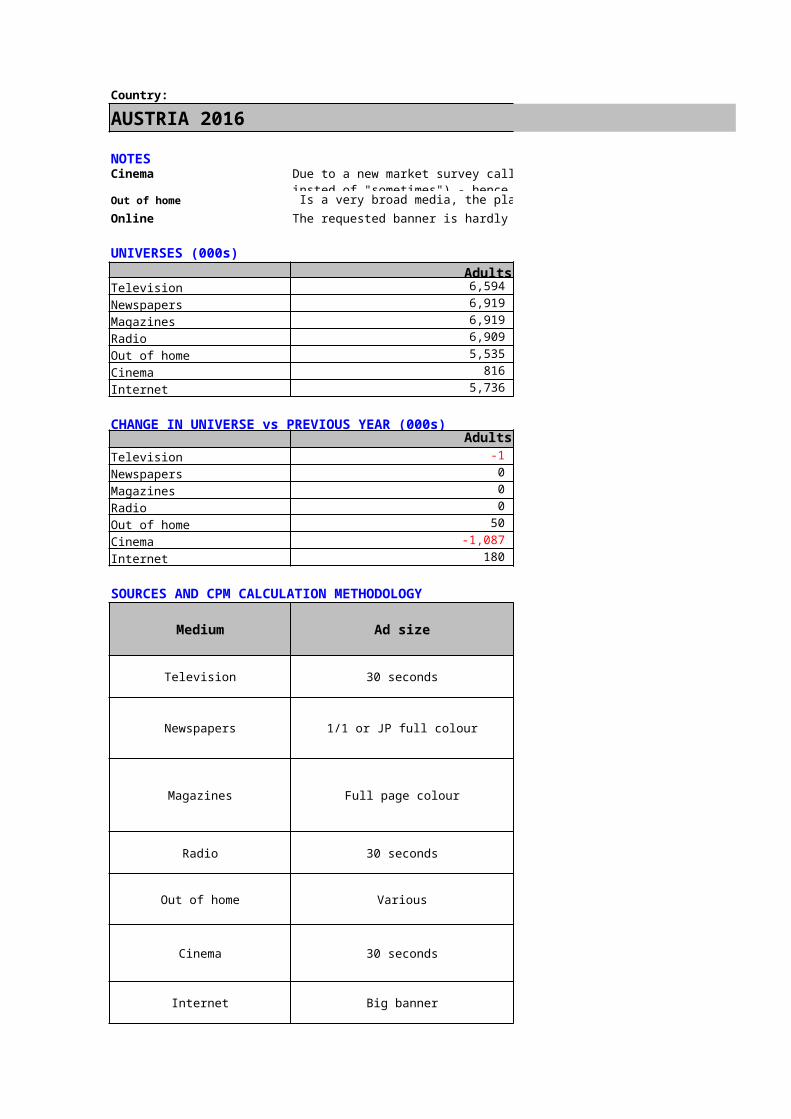

AUSTRIA 2016

NOTESCinema

Out of home Is a very broad media, the planning tools are not made for special target groups, so the gap for specific target groups are bigger than in total population. Online The requested banner is hardly booked so the CPT for this size is not relevant. Client switch to other formats e.g. HalfpageAd - the CPM for Halfpage. Deflation of Online due to start of programmatic era.

UNIVERSES (000s)Adults Men

Television 6,594 3,198 Newspapers 6,919 3,350 Magazines 6,919 3,350 Radio 6,909 3,347 Out of home 5,535 2,680 Cinema 816 416 Internet 5,736 2,890

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television -1 -1 Newspapers 0 0 Magazines 0 0 Radio 0 0 Out of home 50 20 Cinema -1,087 -452 Internet 180 59

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds

Newspapers 1/1 or JP full colour MA 2015Price 2016

Magazines Full page colour MA 2015Price 2016

Radio 30 seconds Radiotest 2015/ _Price 2016

Out of home Various OSA Q1/2016

Cinema 30 seconds CineMA

Internet Big banner OMD estimation

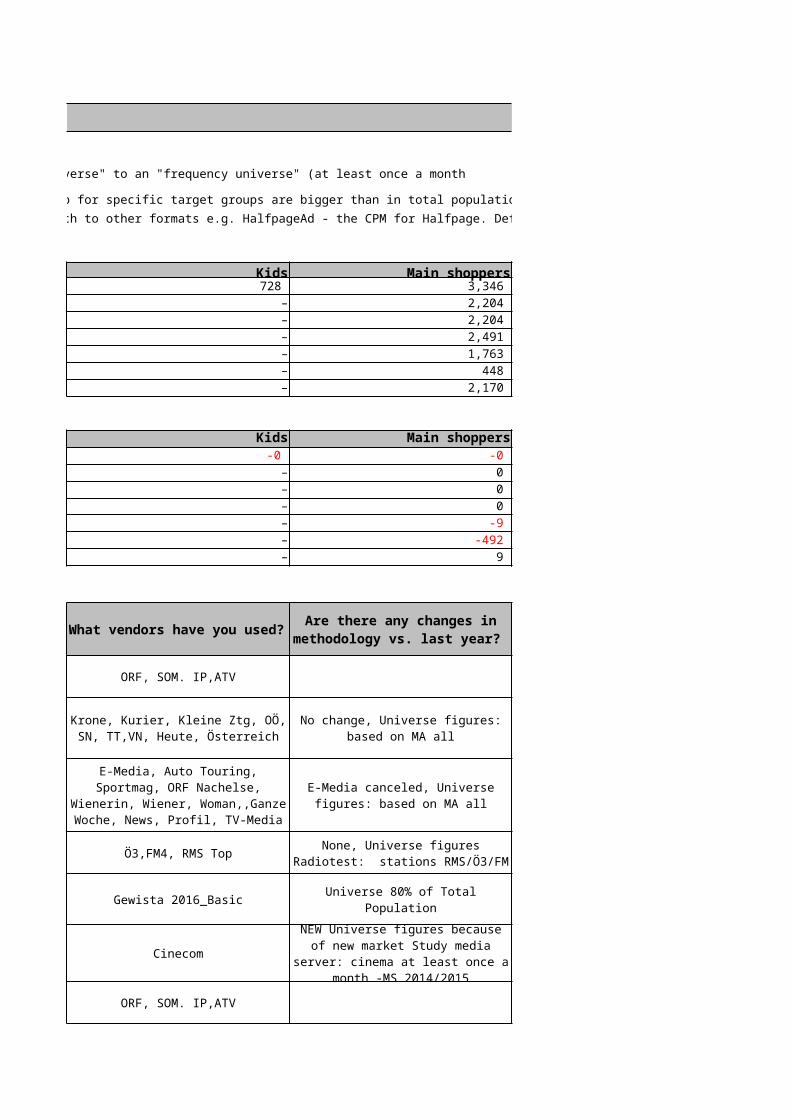

Due to a new market survey called Media-Server the universe changed from a "scale based universe" to an "frequency universe" (at least once a month insted of "sometimes") - hence the huge drop in audience size

Teletest 2016 / Forecast MW Prgn. 2.2

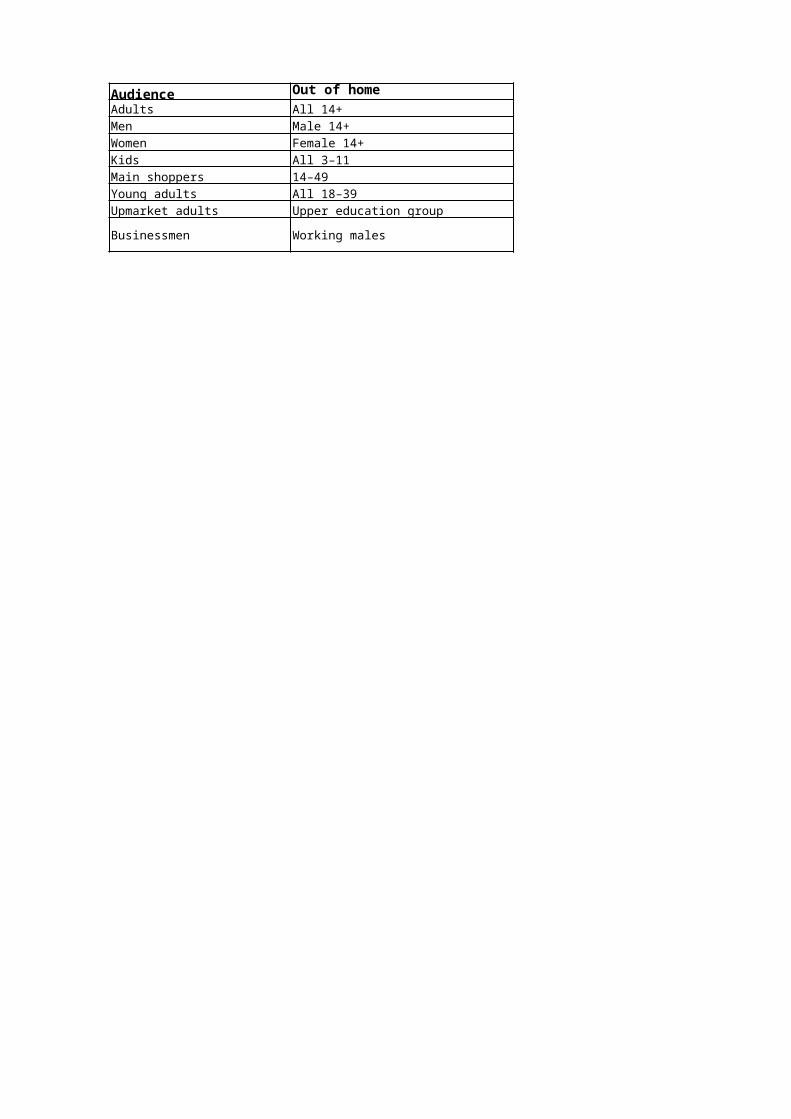

Audience Out of home RadioAdults All 14+ All 18+Men Male 14+ Male 18+Women Female 14+ Female 18+Kids All 3–11 All 3–11Main shoppers 14–49 14-49 y, E/B1-3aYoung adults All 18–39 18-29 yearsUpmarket adults Upper education group 18+ E/B1-2

Businessmen Working malesM E/B1-3a, working

AUSTRIA 2016

Is a very broad media, the planning tools are not made for special target groups, so the gap for specific target groups are bigger than in total population. The requested banner is hardly booked so the CPT for this size is not relevant. Client switch to other formats e.g. HalfpageAd - the CPM for Halfpage. Deflation of Online due to start of programmatic era.

Women Kids Main shoppers 3,395 728 3,346 3,569 – 2,204 3,569 – 2,204 3,562 – 2,491 2,855 – 1,763 400 – 448 2,846 – 2,170

Women Kids Main shoppers-1 -0 -0 0 – 0 0 – 0 0 – 0

30 – -9 -635 – -492 121 – 9

30'' CPT ORF, SOM. IP,ATV

1/1 4c

1/1 4c

30'' CPT Ö3,FM4, RMS Top

Gewista 2016_Basic Universe 80% of Total Population

Cinecom

Banner 468x60 ORF, SOM. IP,ATV

Due to a new market survey called Media-Server the universe changed from a "scale based universe" to an "frequency universe" (at least once a month insted of "sometimes")

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

Krone, Kurier, Kleine Ztg, OÖ, SN, TT,VN, Heute, Österreich

No change, Universe figures: based on MA all

E-Media, Auto Touring, Sportmag, ORF Nachelse, Wienerin, Wiener,

Woman,,Ganze Woche, News, Profil, TV-Media

E-Media canceled, Universe figures: based on MA all

None, Universe figures Radiotest: stations RMS/Ö3/FM

24 Bogen/80.000 conatcts in total/März/14 days/Bevölkerung

30''/Indx 100/National Channel /Price 2016

NEW Universe figures because of new market Study media server:

cinema at least once a month -MS 2014/2015

All other mediaAll 18+Male 18+Female 18+All 3–1114–49, ABC1All 18–2918+, ABMale ABC1 – working at executive level or above

AUSTRIA 2016

The requested banner is hardly booked so the CPT for this size is not relevant. Client switch to other formats e.g. HalfpageAd - the CPM for Halfpage. Deflation of Online due to start of programmatic era.

Young adults Upmarket adults Businessmen 1,224 3,334 1,715 1,272 2,033 1,244 1,272 2,033 1,244 1,261 2,982 1,481 1,018 1,626 995 348 311 195 1,251 1,912 1,206

Young adults Upmarket adults Businessmen-0 -1 -0 0 0 0 0 0 0 0 0 0

10 8 -22 -311 -346 -219

14 22 -20

What assumptions have you made?

GFK had a scandal but we do not know how this affects Radiotest

data

Country:

BOSNIA & HERZEGOVINA 2016

NOTES

UNIVERSES (000s)Adults Men

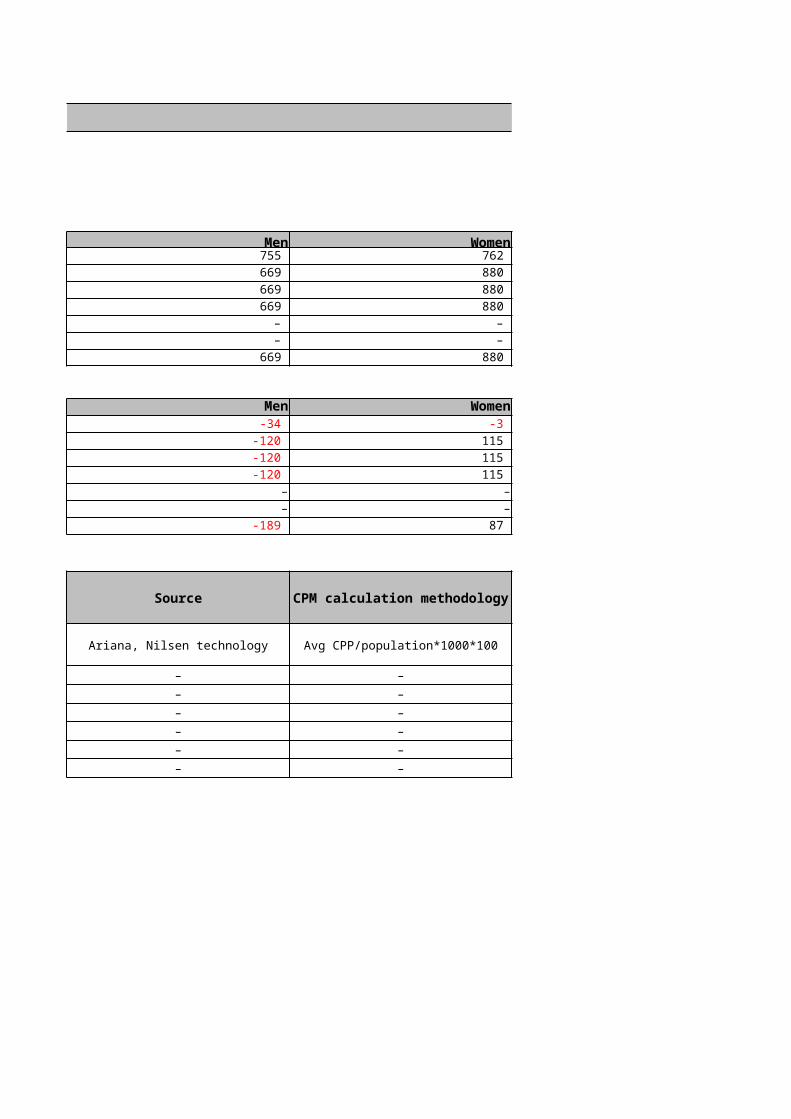

Television 2,638 755 Newspapers 2,405 669 Magazines 2,405 669 Radio 2,405 669 Out of home – – Cinema – – Internet 2,405 669

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television -20 -34 Newspapers -253 -120 Magazines -253 -120 Radio -253 -120 Out of home – –Cinema – –Internet 868 -189

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds Ariana, Nilsen technology

Newspapers A3, full colour –Magazines Full page colour –

Radio 30 seconds –Out of home Various –

Cinema 30 seconds –Internet Banner 468x60 –

Audience All mediaAdults All 20+Men M 18-49Women W 18-49Kids All 4-14Main shoppers All 25-55Young adults All 16-22Upmarket adults All 25-45

Businessmen M 30-49

BOSNIA & HERZEGOVINA 2016

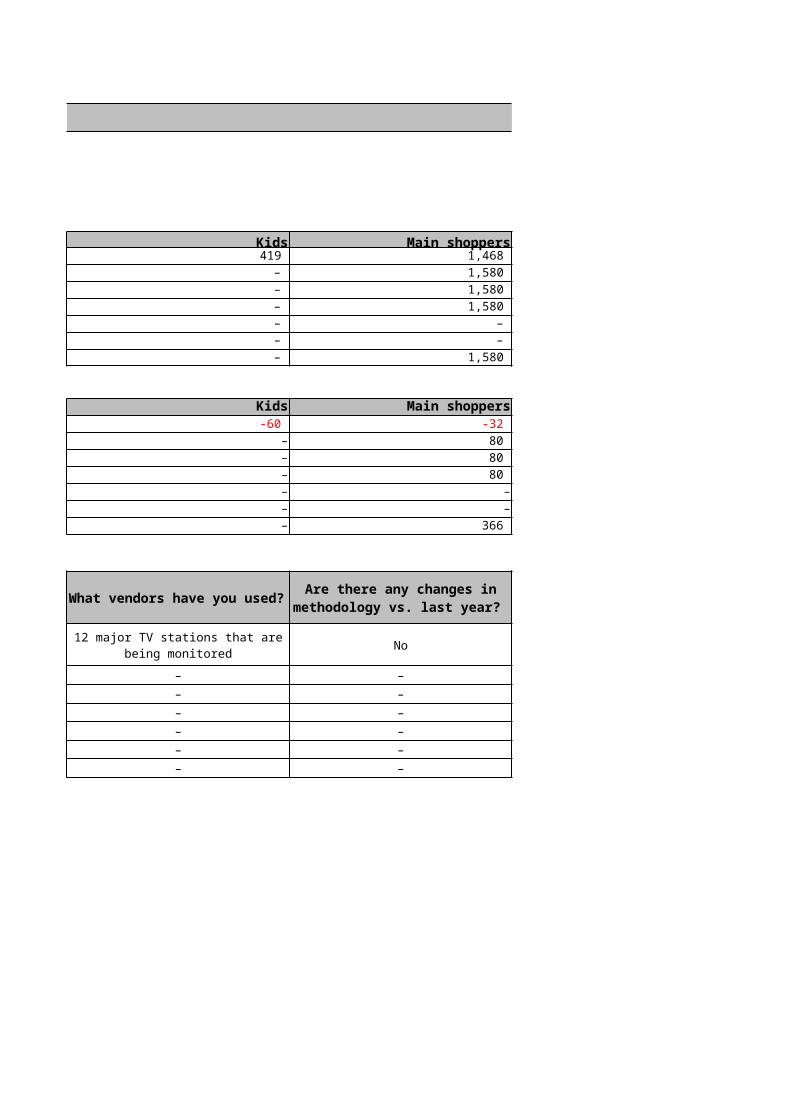

Women Kids Main shoppers 762 419 1,468 880 – 1,580 880 – 1,580 880 – 1,580

– – – – – –

880 – 1,580

Women Kids Main shoppers-3 -60 -32

115 – 80 115 – 80 115 – 80

– – –– – –

87 – 366

Avg CPP/population*1000*100 No

– – –– – –– – –– – –– – –– – –

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

12 major TV stations that are being monitored

BOSNIA & HERZEGOVINA 2016

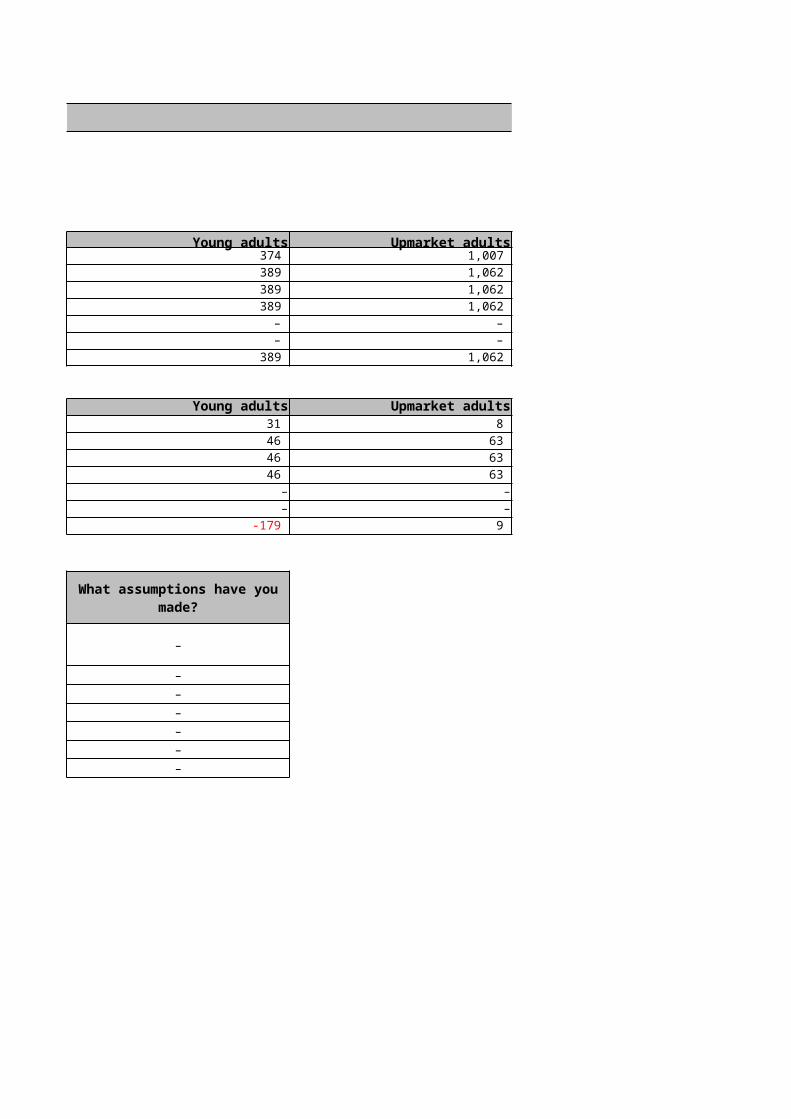

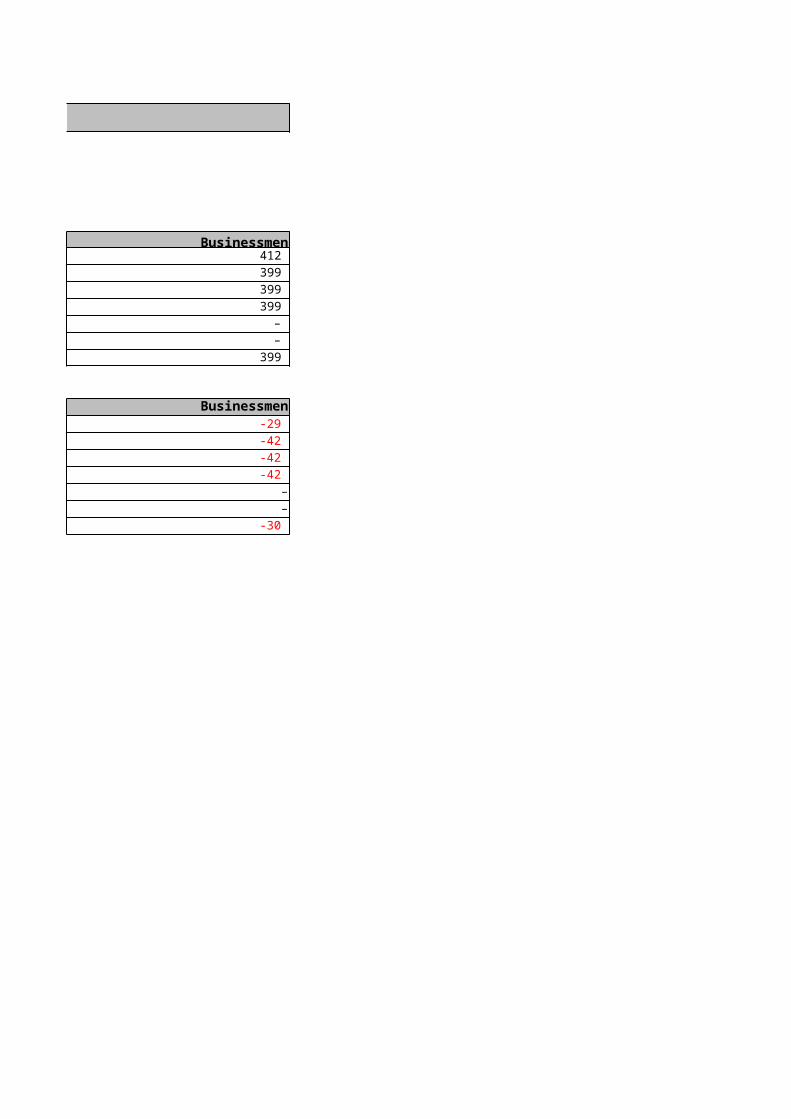

Young adults Upmarket adults Businessmen 374 1,007 412 389 1,062 399 389 1,062 399 389 1,062 399

– – – – – –

389 1,062 399

Young adults Upmarket adults Businessmen31 8 -29 46 63 -42 46 63 -42 46 63 -42

– – –– – –

-179 9 -30

–

––––––

What assumptions have you made?

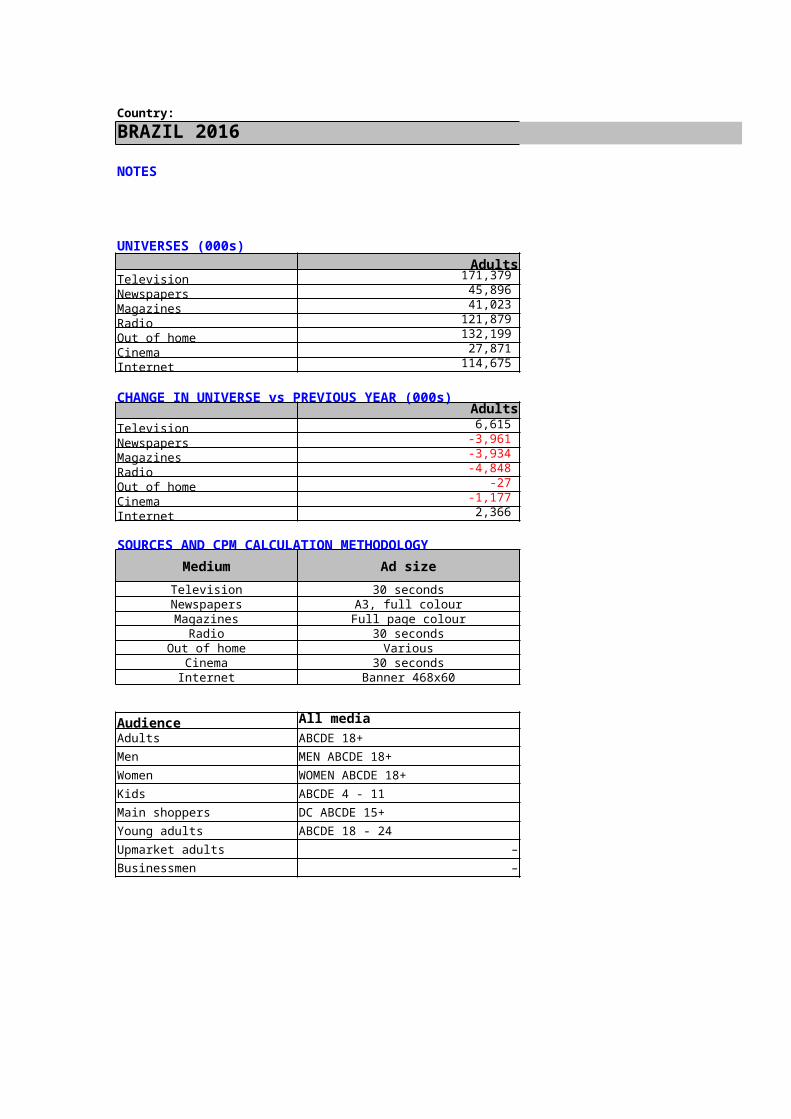

Country:BRAZIL 2016

NOTES

UNIVERSES (000s)Adults Men

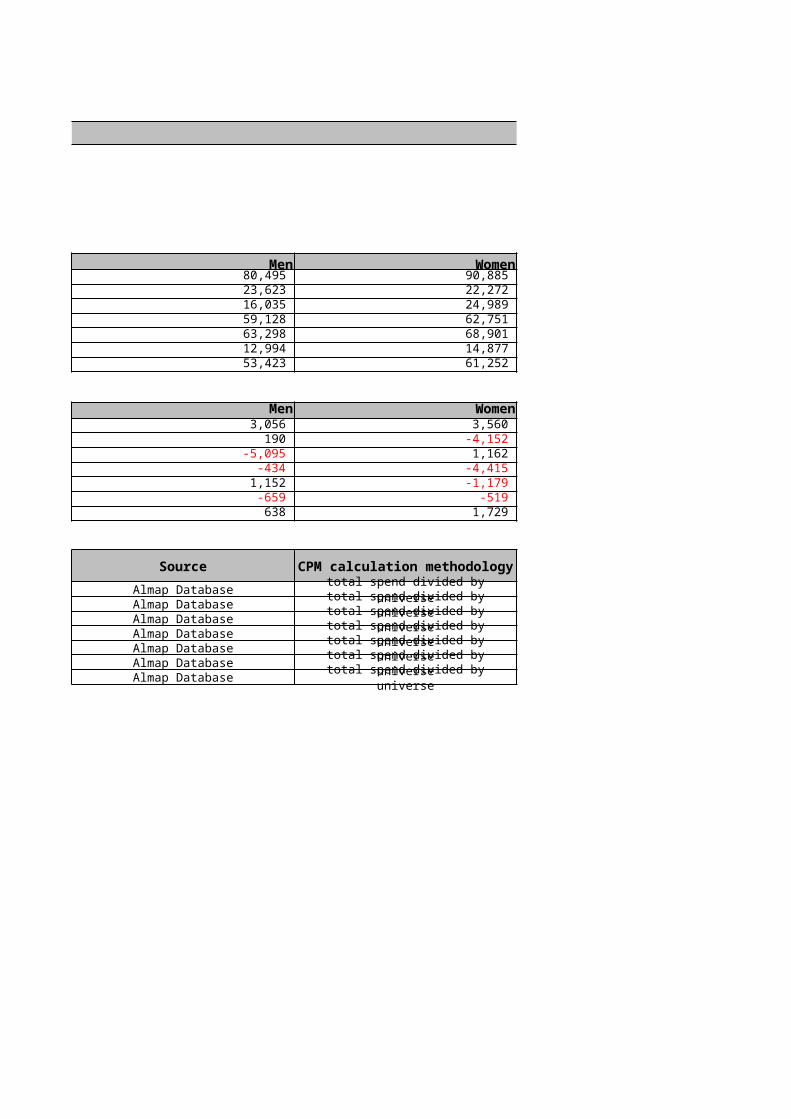

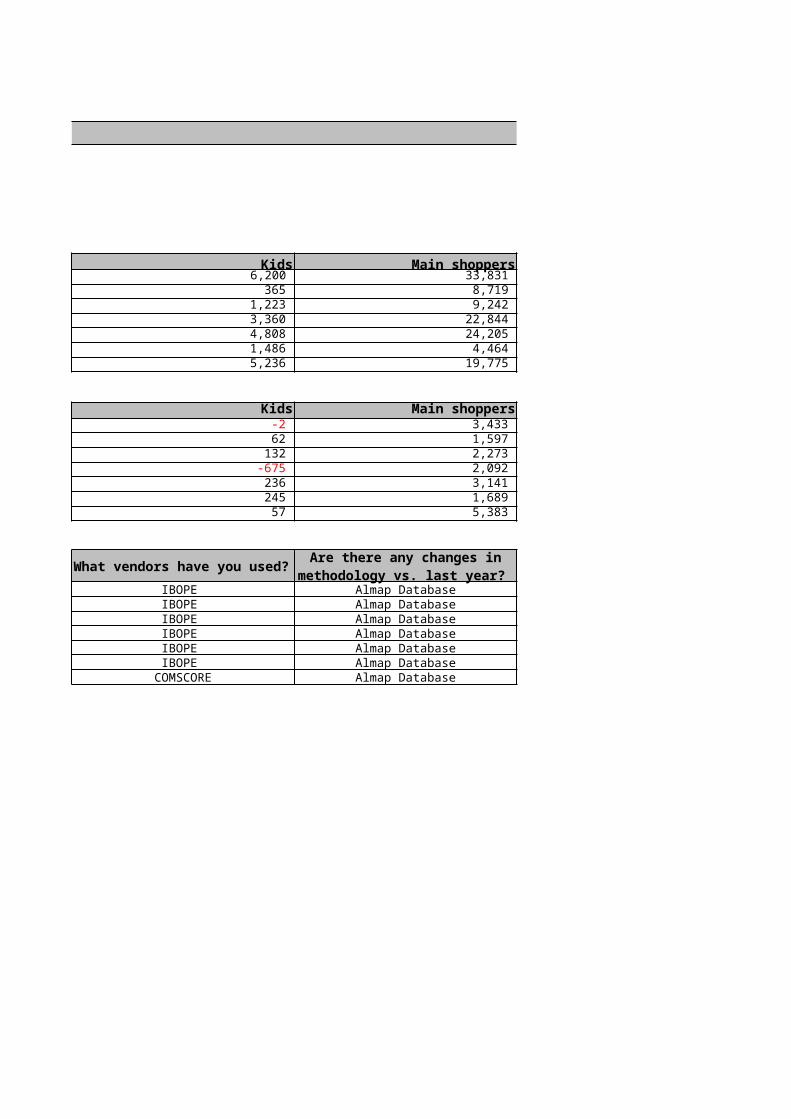

Television 171,379 80,495 Newspapers 45,896 23,623 Magazines 41,023 16,035 Radio 121,879 59,128 Out of home 132,199 63,298 Cinema 27,871 12,994 Internet 114,675 53,423

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 6,615 3,056 Newspapers -3,961 190 Magazines -3,934 -5,095 Radio -4,848 -434 Out of home -27 1,152 Cinema -1,177 -659 Internet 2,366 638

SOURCES AND CPM CALCULATION METHODOLOGYMedium Ad size SourceTelevision 30 seconds Almap Database

Newspapers A3, full colour Almap DatabaseMagazines Full page colour Almap Database

Radio 30 seconds Almap DatabaseOut of home Various Almap Database

Cinema 30 seconds Almap DatabaseInternet Banner 468x60 Almap Database

Audience All mediaAdults ABCDE 18+Men MEN ABCDE 18+Women WOMEN ABCDE 18+Kids ABCDE 4 - 11Main shoppers DC ABCDE 15+Young adults ABCDE 18 - 24Upmarket adults –Businessmen –

BRAZIL 2016

Women Kids Main shoppers 90,885 6,200 33,831 22,272 365 8,719 24,989 1,223 9,242 62,751 3,360 22,844 68,901 4,808 24,205 14,877 1,486 4,464 61,252 5,236 19,775

Women Kids Main shoppers3,560 -2 3,433

-4,152 62 1,597 1,162 132 2,273

-4,415 -675 2,092 -1,179 236 3,141

-519 245 1,689 1,729 57 5,383

total spend divided by universe IBOPE Almap Databasetotal spend divided by universe IBOPE Almap Databasetotal spend divided by universe IBOPE Almap Databasetotal spend divided by universe IBOPE Almap Databasetotal spend divided by universe IBOPE Almap Databasetotal spend divided by universe IBOPE Almap Databasetotal spend divided by universe COMSCORE Almap Database

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

BRAZIL 2016

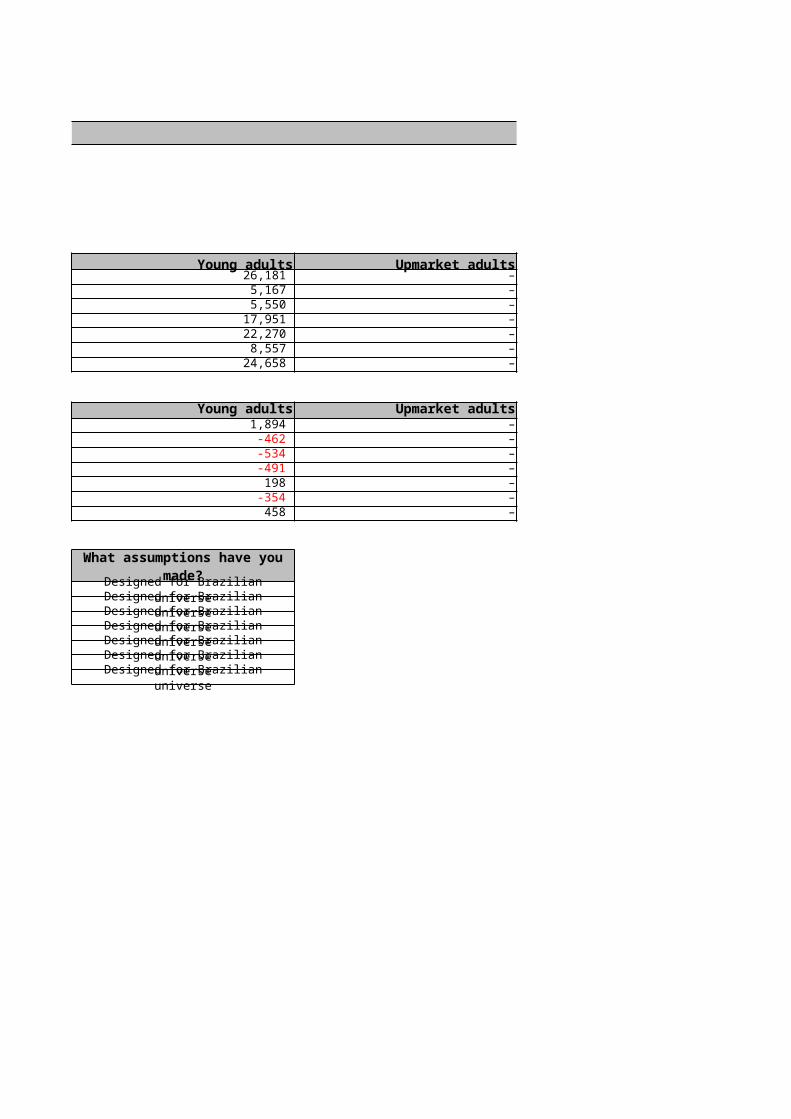

Young adults Upmarket adults Businessmen 26,181 – – 5,167 – – 5,550 – – 17,951 – – 22,270 – – 8,557 – – 24,658 – –

Young adults Upmarket adults Businessmen1,894 – –-462 – –-534 – –-491 – –198 – –

-354 – –458 – –

Designed for Brazilian universeDesigned for Brazilian universeDesigned for Brazilian universeDesigned for Brazilian universeDesigned for Brazilian universeDesigned for Brazilian universeDesigned for Brazilian universe

What assumptions have you made?

Country:

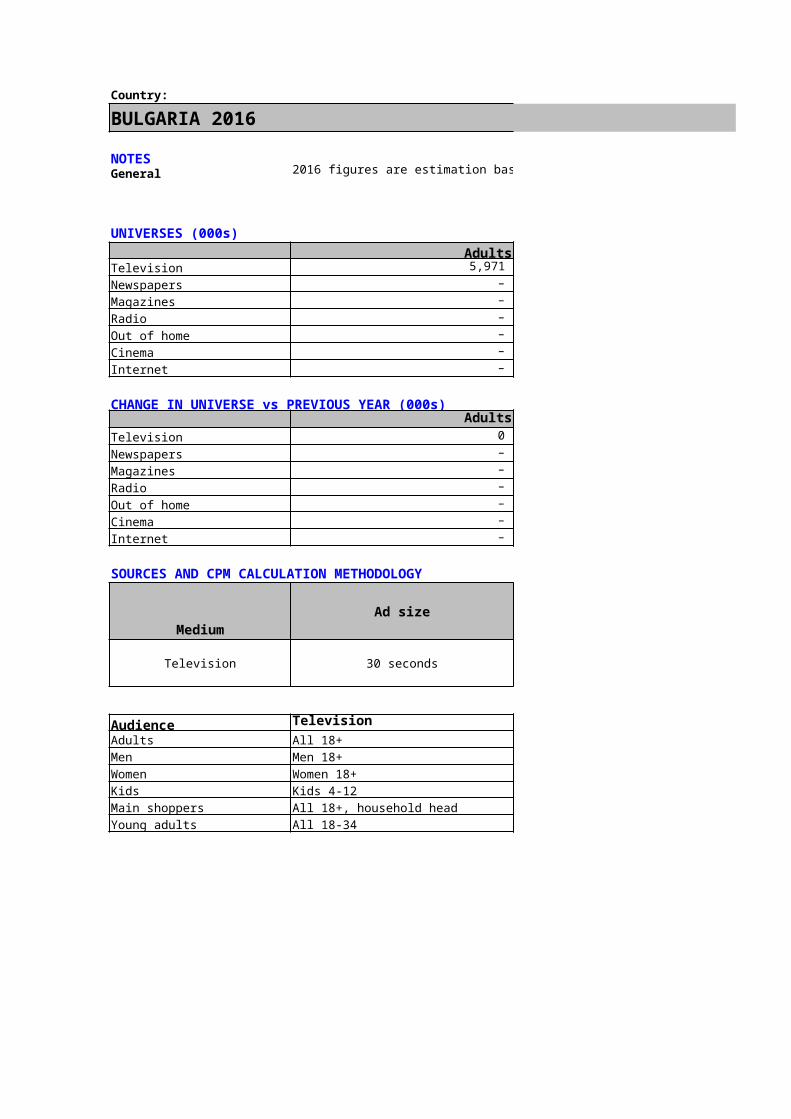

BULGARIA 2016

NOTESGeneral 2016 figures are estimation based on 2015 and expected change

UNIVERSES (000s)Adults Men

Television 5,971 2,938 Newspapers – – Magazines – – Radio – – Out of home – – Cinema – – Internet – –

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 0 0 Newspapers – – Magazines – – Radio – – Out of home – – Cinema – – Internet – –

SOURCES AND CPM CALCULATION METHODOLOGY

MediumAd size Source

Television 30 seconds

Audience TelevisionAdults All 18+Men Men 18+Women Women 18+Kids Kids 4-12Main shoppers All 18+, household headYoung adults All 18-34

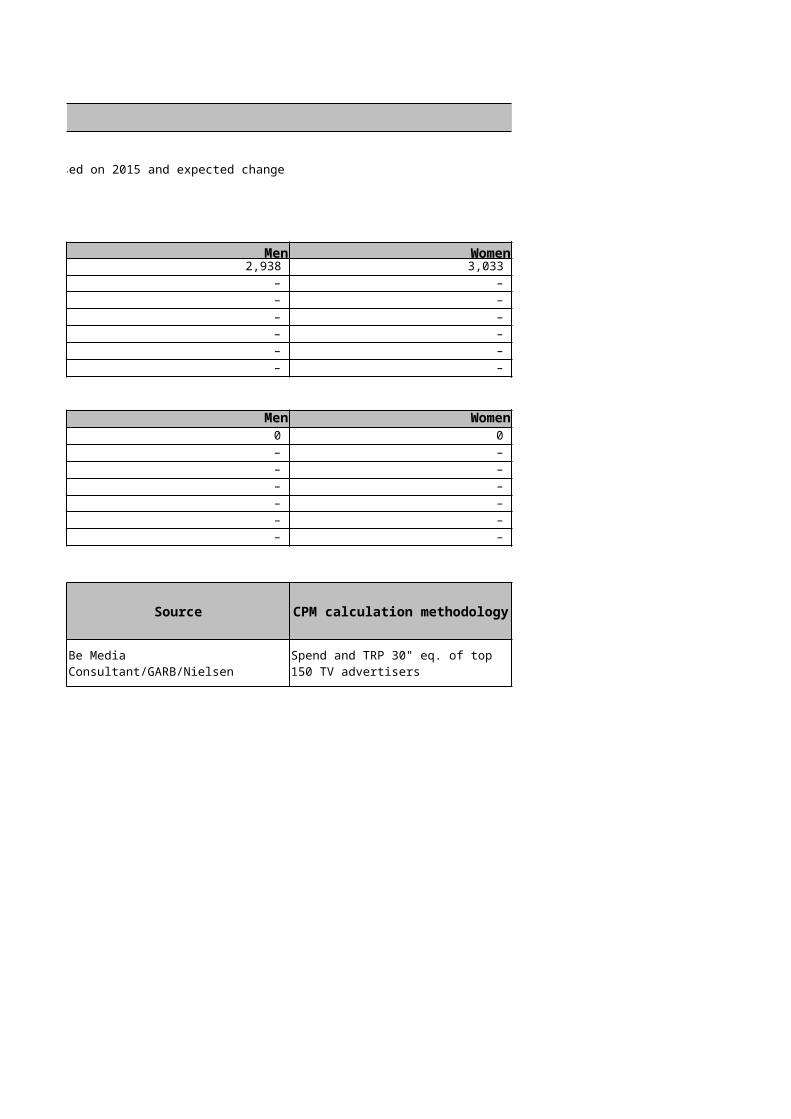

Be Media Consultant/GARB/Nielsen

BULGARIA 2016

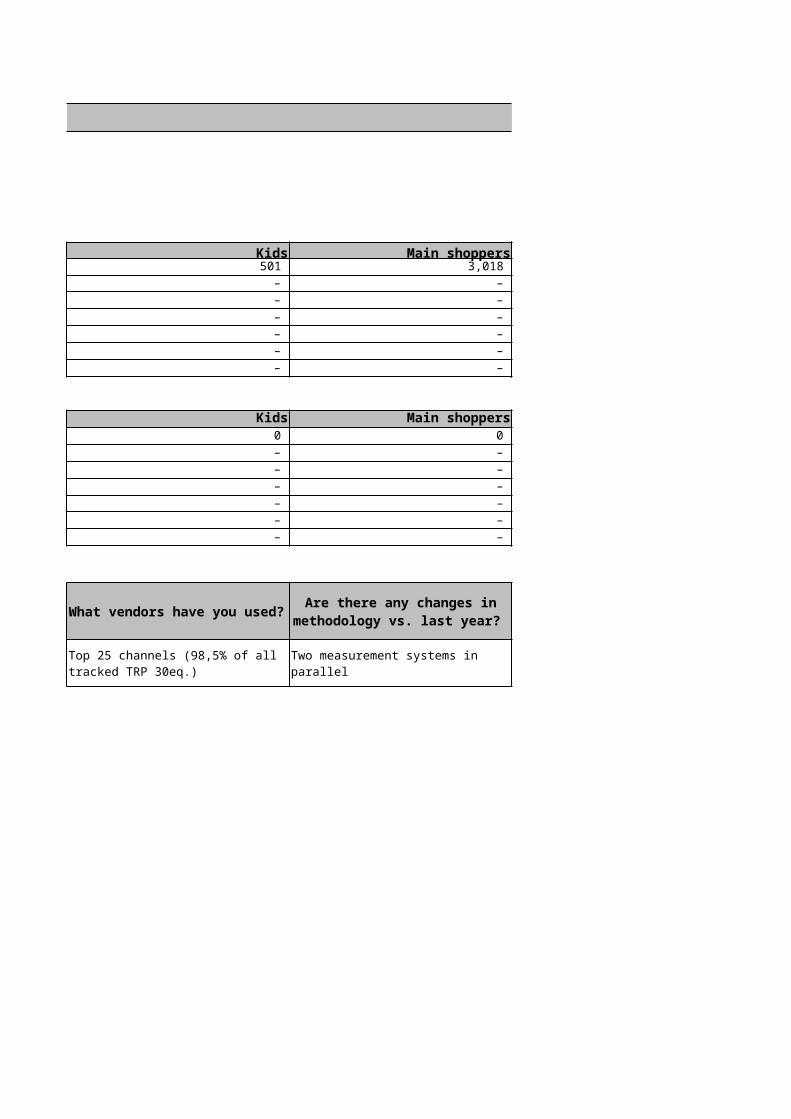

Women Kids Main shoppers 3,033 501 3,018

– – – – – – – – – – – – – – – – – –

Women Kids Main shoppers0 0 0 – – – – – – – – – – – – – – – – – –

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

Spend and TRP 30" eq. of top 150 TV advertisers

Top 25 channels (98,5% of all tracked TRP 30eq.)

Two measurement systems in parallel

BULGARIA 2016

Young adults Upmarket adults Businessmen 1,504 – –

– – – – – – – – – – – – – – – – – –

Young adults Upmarket adults Businessmen0 – – – – – – – – – – – – – – – – – – – –

What assumptions have you made?

Close estimation of spends according to our expertise

Country:

CANADA 2016

NOTESGeneral

Cinema Cinema advertising spend is not measured or reported in Canada and the medium is not bought on a CPM basis.

UNIVERSES (000s)Adults Men

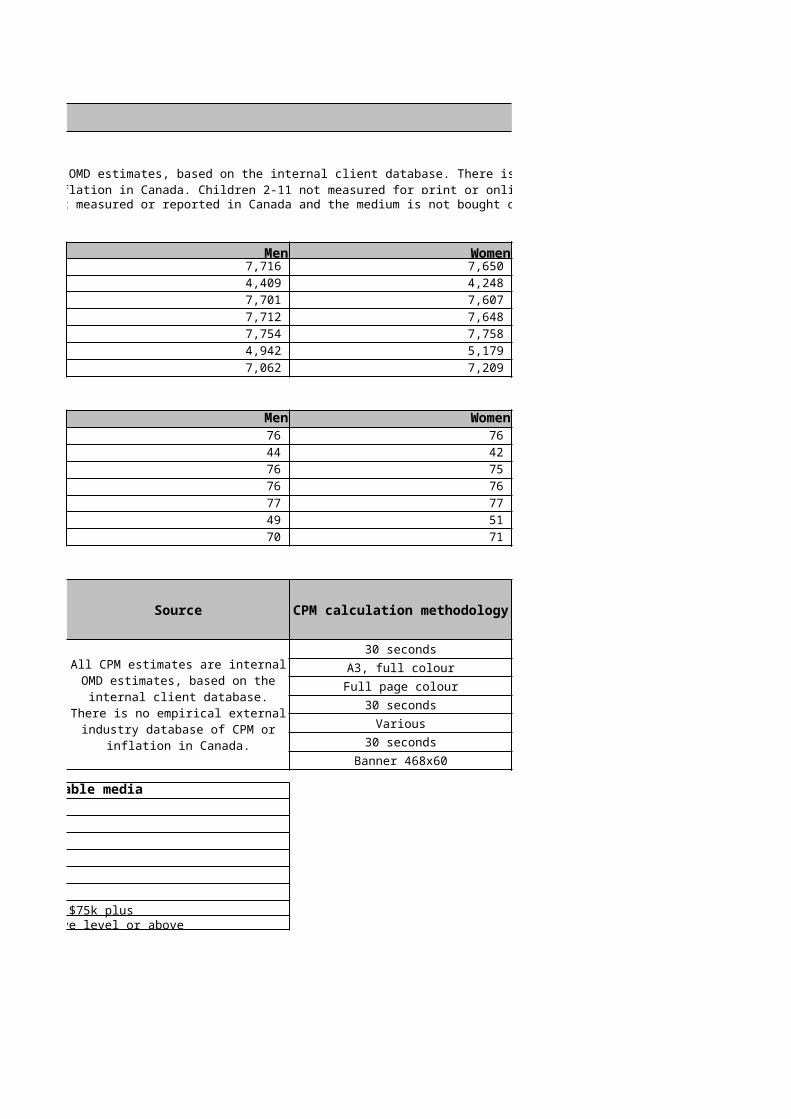

Television 15,367 7,716 Newspapers 8,657 4,409 Magazines 15,309 7,701 Radio 15,360 7,712 Out of home 15,512 7,754 Cinema 10,122 4,942 Internet 14,271 7,062

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 152 76 Newspapers 86 44 Magazines 152 76 Radio 152 76 Out of home 154 77 Cinema 100 49 Internet 141 70

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 secondsNewspapers A3, full colourMagazines Full page colour

Radio 30 secondsOut of home Various

Cinema 30 secondsInternet Banner 468x60

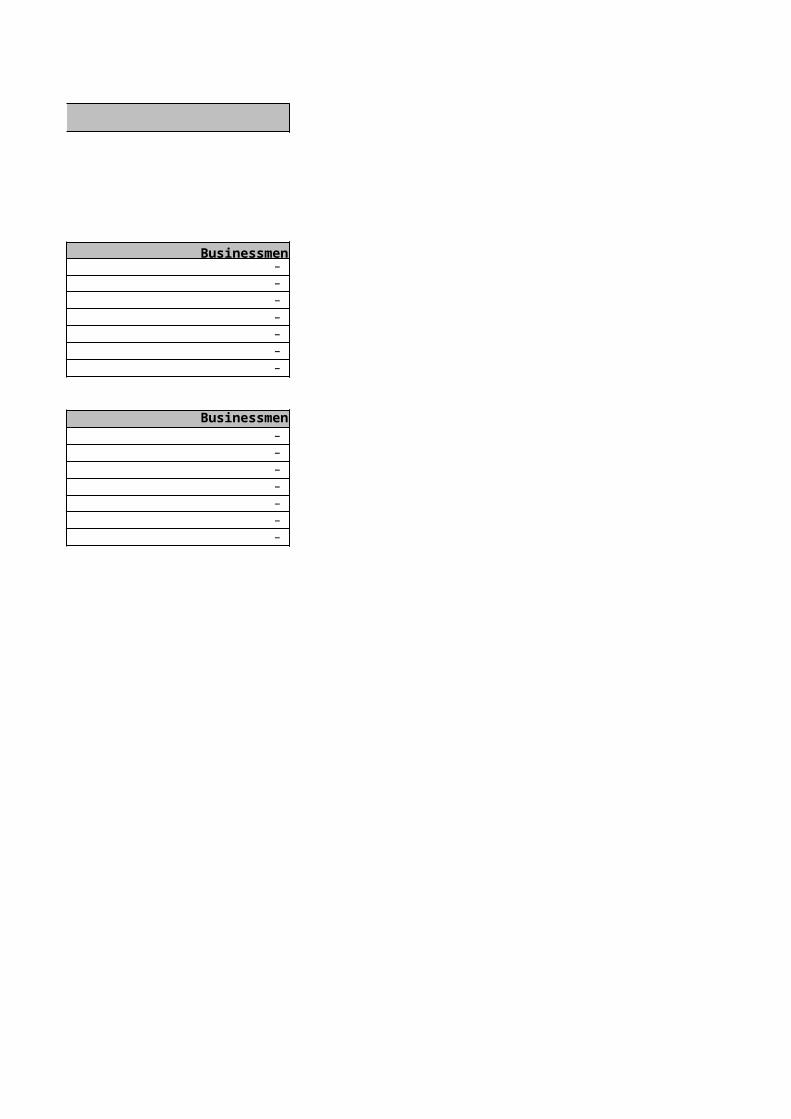

Audience All available mediaAdults All 25–54Men Male 25–54Women Female 25–54Kids All 2–11Main shoppers Female, 25–54Young adults All 18–34Upmarket adults Adults 25–54, Household income $75k plusBusinessmen Male ABC1 – working at executive level or above

All CPM estimates are internal OMD estimates, based on the internal client database. There is no empirical external industry database of CPM or inflation in Canada. Children 2-11 not measured for print or online exposure.

All CPM estimates are internal OMD estimates, based on the

internal client database. There is no empirical external industry

database of CPM or inflation in Canada.

CANADA 2016

Cinema advertising spend is not measured or reported in Canada and the medium is not bought on a CPM basis.

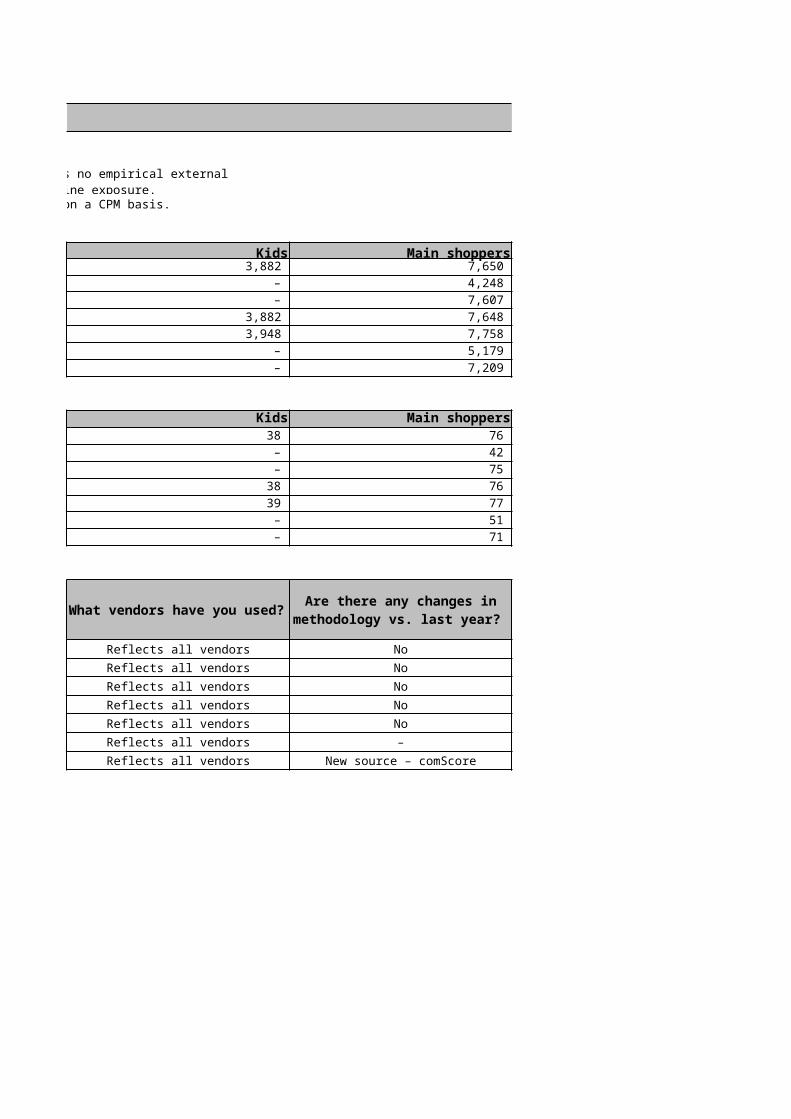

Women Kids Main shoppers 7,650 3,882 7,650 4,248 – 4,248 7,607 – 7,607 7,648 3,882 7,648 7,758 3,948 7,758 5,179 – 5,179 7,209 – 7,209

Women Kids Main shoppers76 38 76 42 – 42 75 – 75 76 38 76 77 39 77 51 – 51 71 – 71

30 seconds Reflects all vendors NoA3, full colour Reflects all vendors No

Full page colour Reflects all vendors No30 seconds Reflects all vendors No

Various Reflects all vendors No30 seconds Reflects all vendors –

Banner 468x60 Reflects all vendors New source – comScore

All CPM estimates are internal OMD estimates, based on the internal client database. There is no empirical external industry database of CPM or inflation in Canada. Children 2-11 not measured for print or online exposure.

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

CANADA 2016

Young adults Upmarket adults Businessmen 8,461 7,086 – 4,566 4,846 – 8,475 8,609 – 8,463 7,017 – 8,528 7,366 – 6,289 6,010 – 7,196 6,422 –

Young adults Upmarket adults Businessmen84 70 – 45 48 – 84 85 – 84 69 – 84 73 – 62 60 – 71 64 –

–––––––

What assumptions have you made?

Country:

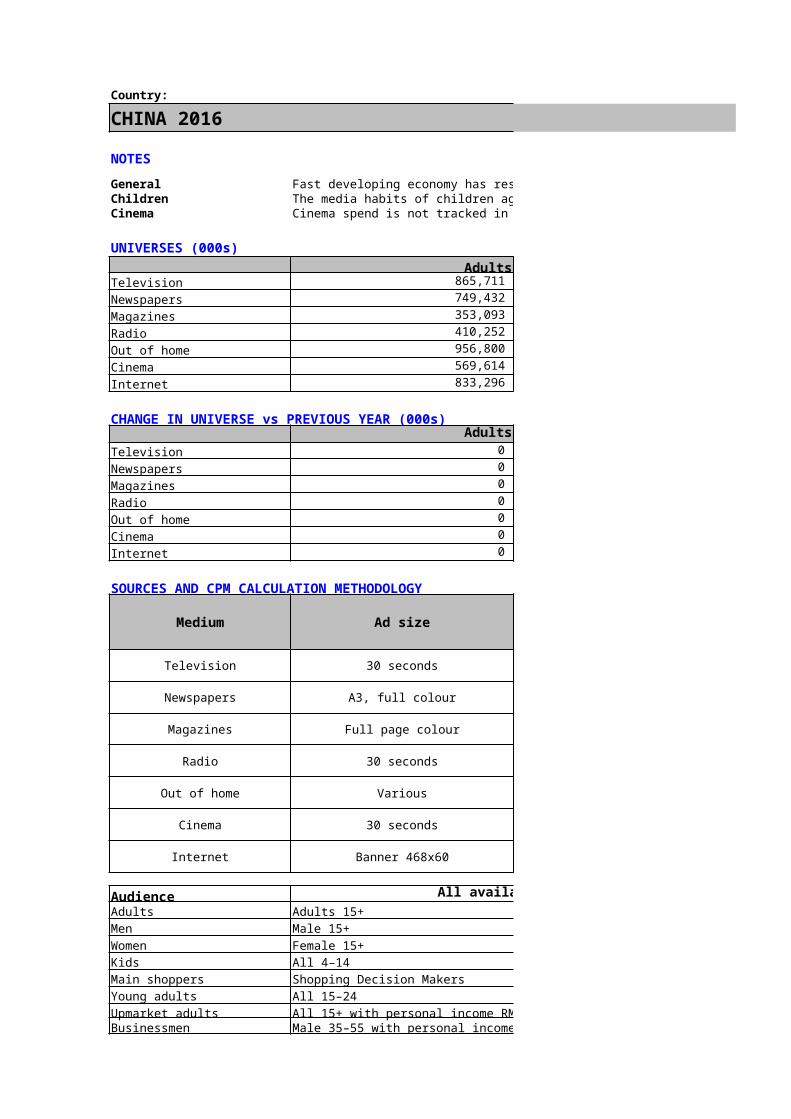

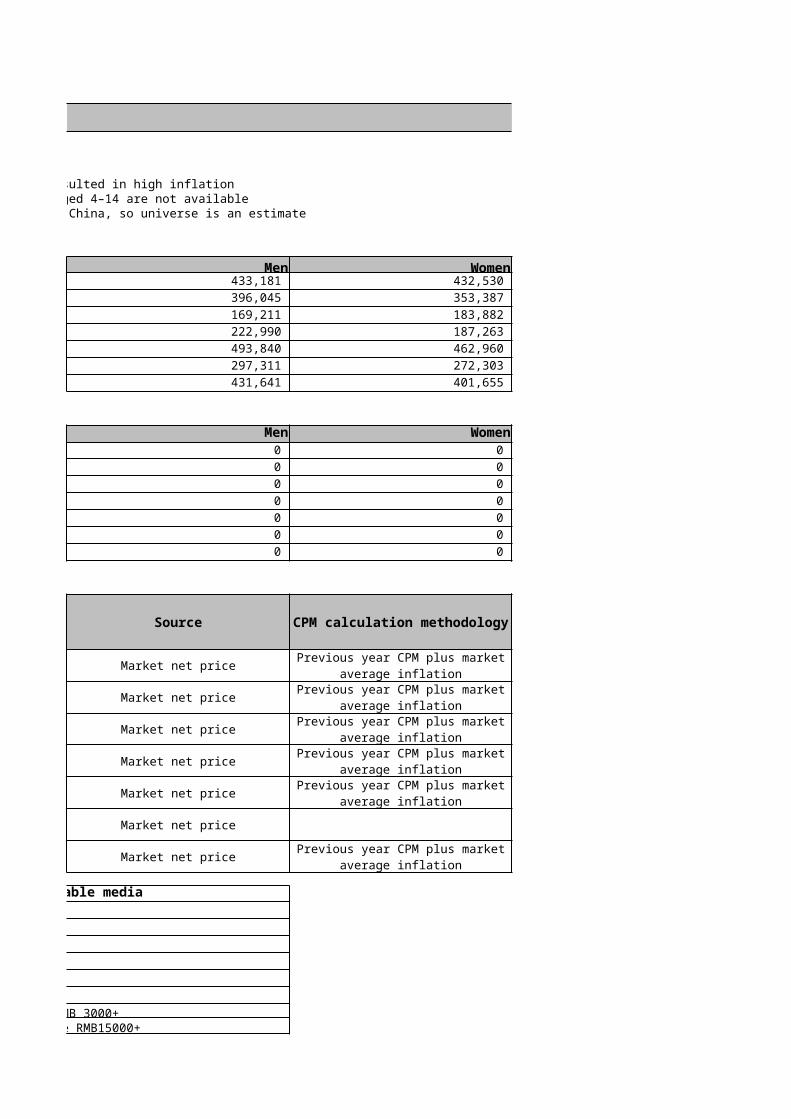

CHINA 2016

NOTES

General Fast developing economy has resulted in high inflationChildren The media habits of children aged 4–14 are not availableCinema Cinema spend is not tracked in China, so universe is an estimate

UNIVERSES (000s)Adults Men

Television 865,711 433,181 Newspapers 749,432 396,045 Magazines 353,093 169,211 Radio 410,252 222,990 Out of home 956,800 493,840 Cinema 569,614 297,311 Internet 833,296 431,641

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 0 0 Newspapers 0 0 Magazines 0 0 Radio 0 0 Out of home 0 0 Cinema 0 0 Internet 0 0

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds Market net price

Newspapers A3, full colour Market net price

Magazines Full page colour Market net price

Radio 30 seconds Market net price

Out of home Various Market net price

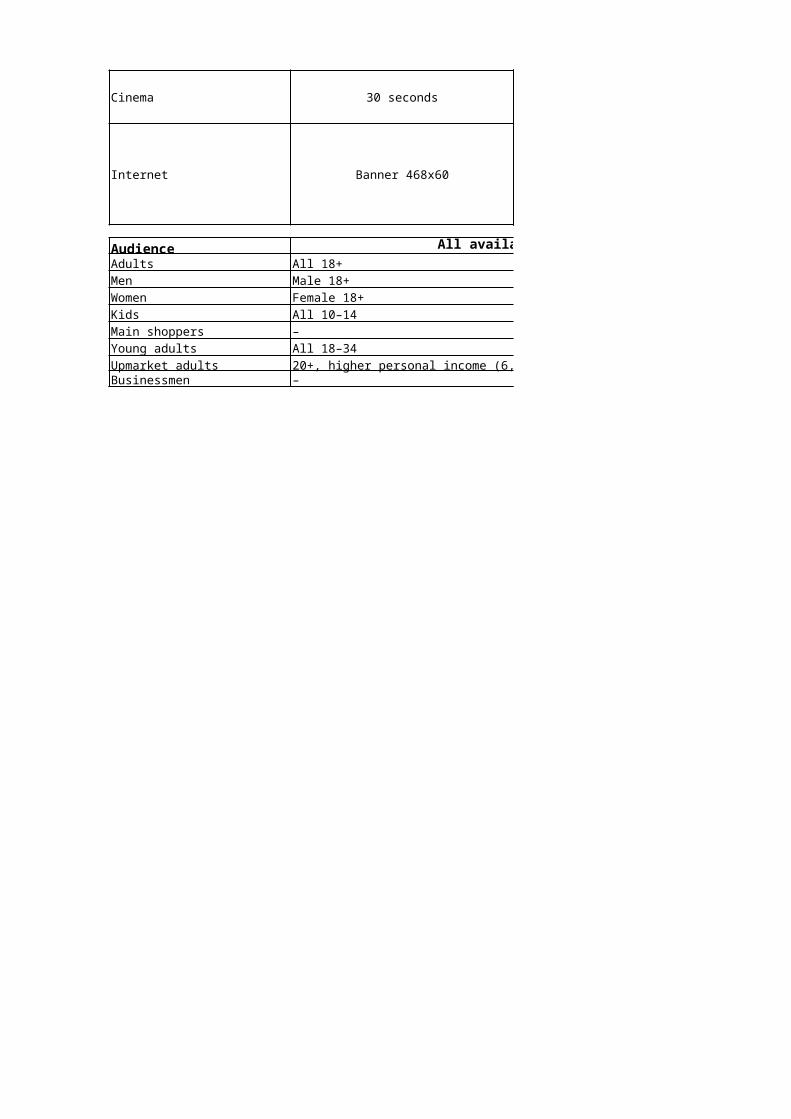

Cinema 30 seconds Market net price

Internet Banner 468x60 Market net price

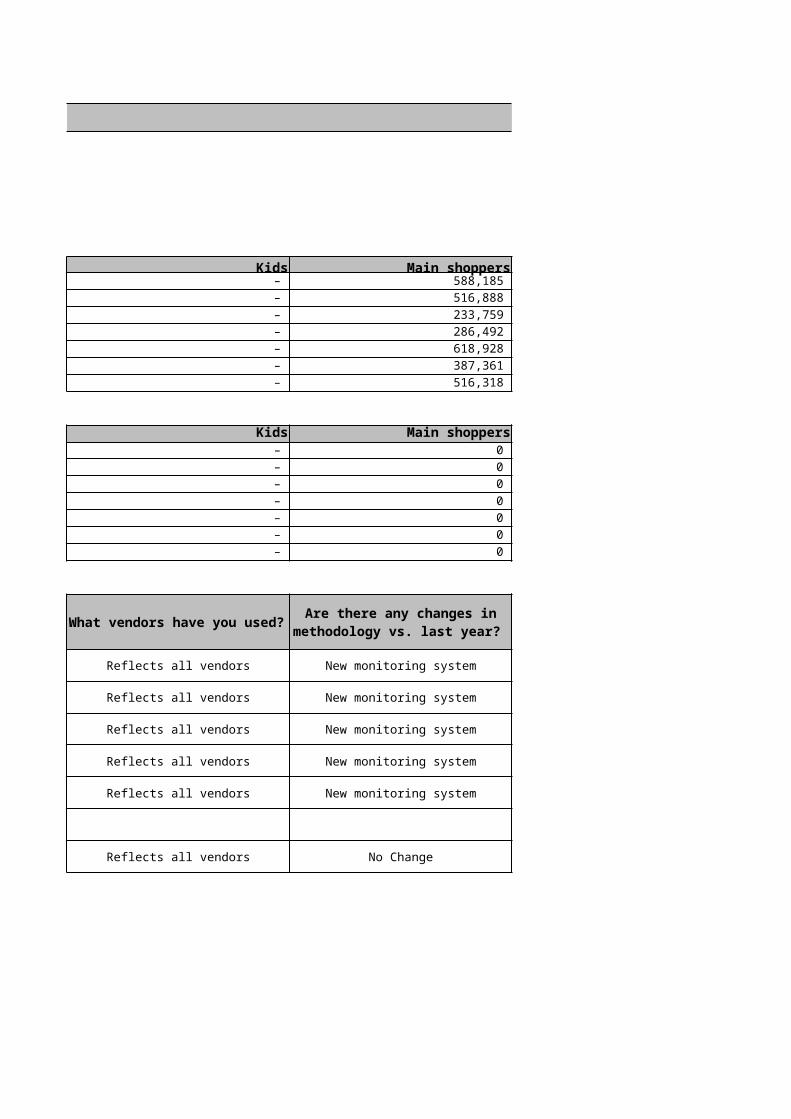

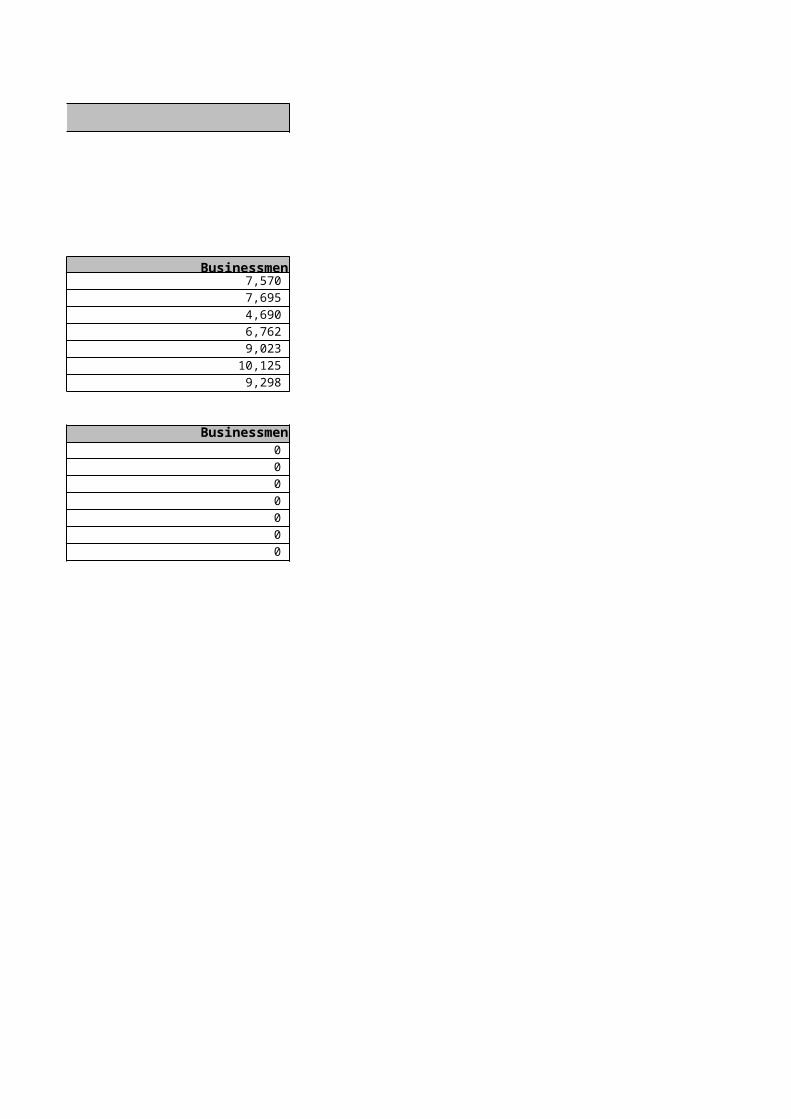

Audience All available mediaAdults Adults 15+Men Male 15+Women Female 15+Kids All 4–14Main shoppers Shopping Decision MakersYoung adults All 15–24Upmarket adults All 15+ with personal income RMB 3000+Businessmen Male 35–55 with personal income RMB15000+

CHINA 2016

The media habits of children aged 4–14 are not availableCinema spend is not tracked in China, so universe is an estimate

Women Kids Main shoppers 432,530 – 588,185 353,387 – 516,888 183,882 – 233,759 187,263 – 286,492 462,960 – 618,928 272,303 – 387,361 401,655 – 516,318

Women Kids Main shoppers0 – 0 0 – 0 0 – 0 0 – 0 0 – 0 0 – 0 0 – 0

Reflects all vendors New monitoring system

Reflects all vendors New monitoring system

Reflects all vendors New monitoring system

Reflects all vendors New monitoring system

Reflects all vendors New monitoring system

Reflects all vendors No Change

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

Previous year CPM plus market average inflation

Previous year CPM plus market average inflation

Previous year CPM plus market average inflation

Previous year CPM plus market average inflation

Previous year CPM plus market average inflation

Previous year CPM plus market average inflation

CHINA 2016

Young adults Upmarket adults Businessmen 181,114 577,623 7,570 154,992 521,966 7,695 103,487 256,237 4,690 71,692 314,505 6,762 235,124 654,198 9,023 182,805 453,900 10,125 246,413 594,240 9,298

Young adults Upmarket adults Businessmen0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

What assumptions have you made?

Country:

CROATIA 2016

NOTESGeneral

Target groups

Cinema There is no 30" cinema spot in Croatia. Negotiations for prices.

TV Women on Television are getting harder to reach, once very focused on few national channels and easier to reach are watching more and more payTV channels.Newspapers Newspaper and magazines are recording even further decline of reach and readership figures and are trying to keep stable prices. Radio Radio in a small decline year to year regarding reach figures, increasing the cost.

UNIVERSES (000s)Adults Men

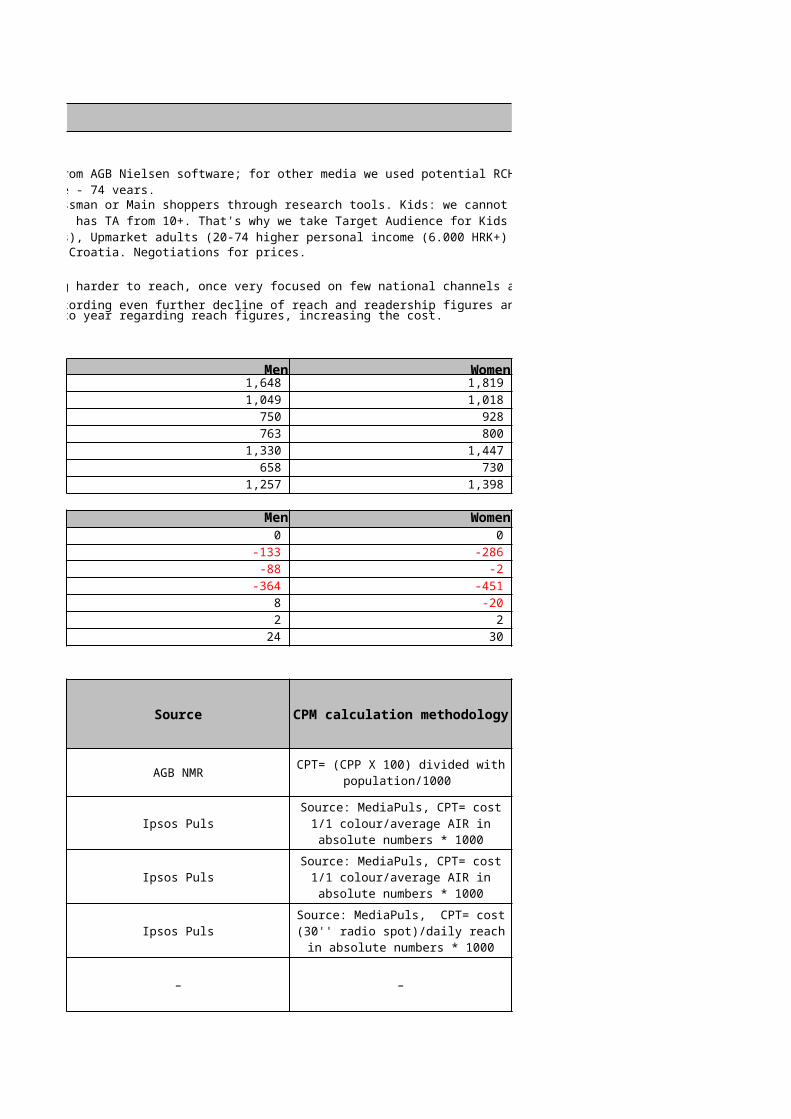

Television 3,468 1,648 Newspapers 2,068 1,049 Magazines 1,678 750 Radio 1,564 763 Out of home 2,795 1,330 Cinema 1,387 658 Internet 2,635 1,257 CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)

Adults MenTelevision 0 0 Newspapers -419 -133 Magazines -89 -88 Radio -814 -364 Out of home 5 8 Cinema 2 2 Internet 34 24

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds AGB NMR

Newspapers A3, full colour Ipsos Puls

Magazines Full page colour Ipsos Puls

Radio 30 seconds Ipsos Puls

Out of home Various –

For TV we have exact figures from AGB Nielsen software; for other media we used potential RCH (BRANDpuls) on Census figures because in other research tools we have limited upper age - 74 years. We cannot define the TG Businessman or Main shoppers through research tools. Kids: we cannot take 4-14 because it is not comparable. TV panel has TA from 4 years+. Other media (non TV ) has TA from 10+. That's why we take Target Audience for Kids 10-14. CPT targets for non TV media: Adults (18-74), Men (18-74 Males), Women (18-74 Females), Upmarket adults (20-74 higher personal income (6.000 HRK+)

Cinema 30 seconds –

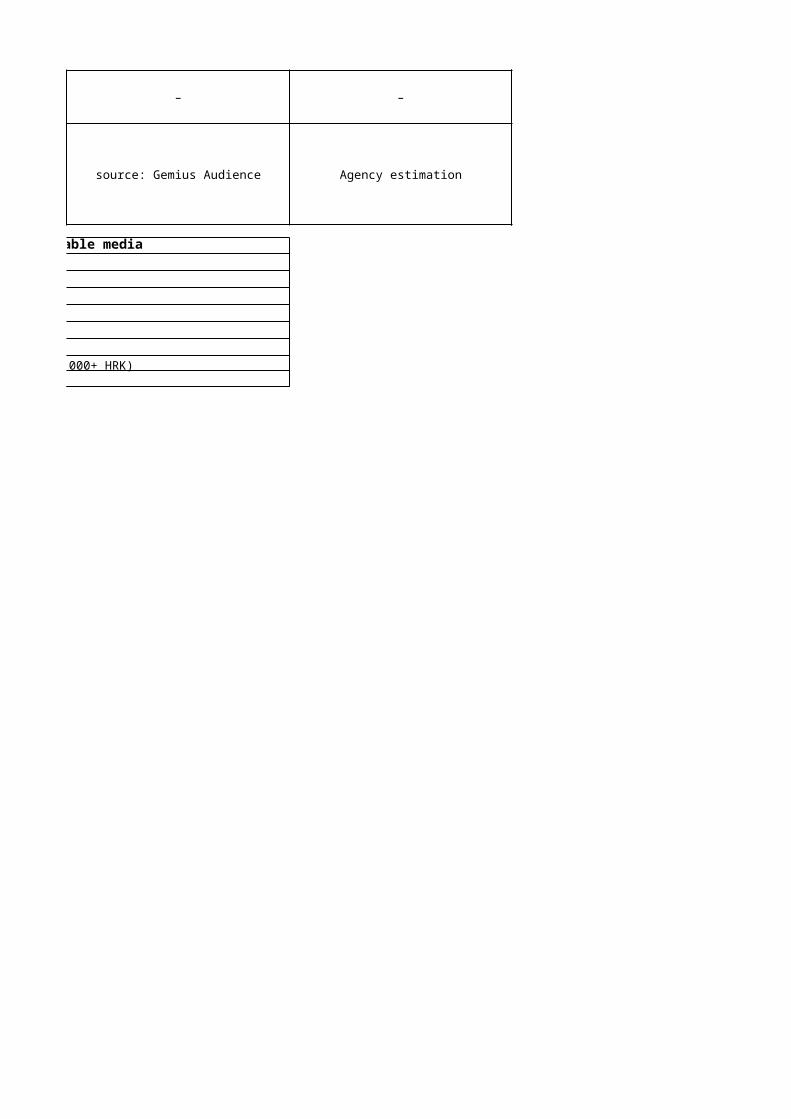

Internet Banner 468x60 source: Gemius Audience

Audience All available mediaAdults All 18+Men Male 18+Women Female 18+Kids All 10–14Main shoppers –Young adults All 18–34Upmarket adults 20+, higher personal income (6,000+ HRK)Businessmen –

CROATIA 2016

There is no 30" cinema spot in Croatia. Negotiations for prices.

Women on Television are getting harder to reach, once very focused on few national channels and easier to reach are watching more and more payTV channels.Newspaper and magazines are recording even further decline of reach and readership figures and are trying to keep stable prices. Radio in a small decline year to year regarding reach figures, increasing the cost.

Women Kids Main shoppers 1,819 234 – 1,018 44 – 928 64 – 800 33 – 1,447 209 – 730 115 – 1,398 212 –

Women Kids Main shoppers0 0 –

-286 -124 – -2 -72 –

-451 -150 – -20 -6 –

2 8 – 30 12 –

No change

5 National newspapers No change

Top 5 Magazines No change

Top 5 Radio stations No change

– – No change

For TV we have exact figures from AGB Nielsen software; for other media we used potential RCH (BRANDpuls) on Census figures because in other research tools we have limited upper age - 74 years. We cannot define the TG Businessman or Main shoppers through research tools. Kids: we cannot take 4-14 because it is not comparable. TV panel has TA from 4 years+. Other media (non TV ) has TA from 10+. That's why we take Target Audience for Kids 10-14. CPT targets for non TV media: Adults (18-74), Men (18-74 Males), Women (18-74 Females), Upmarket adults (20-74 higher personal income (6.000 HRK+)

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

CPT= (CPP X 100) divided with population/1000

Main national channels (6 channels)..based on channel mix

Source: MediaPuls, CPT= cost 1/1 colour/average AIR in absolute

numbers * 1000

Source: MediaPuls, CPT= cost 1/1 colour/average AIR in absolute

numbers * 1000

Source: MediaPuls, CPT= cost (30'' radio spot)/daily reach in

absolute numbers * 1000

– – No change

Agency estimation – No change

CROATIA 2016

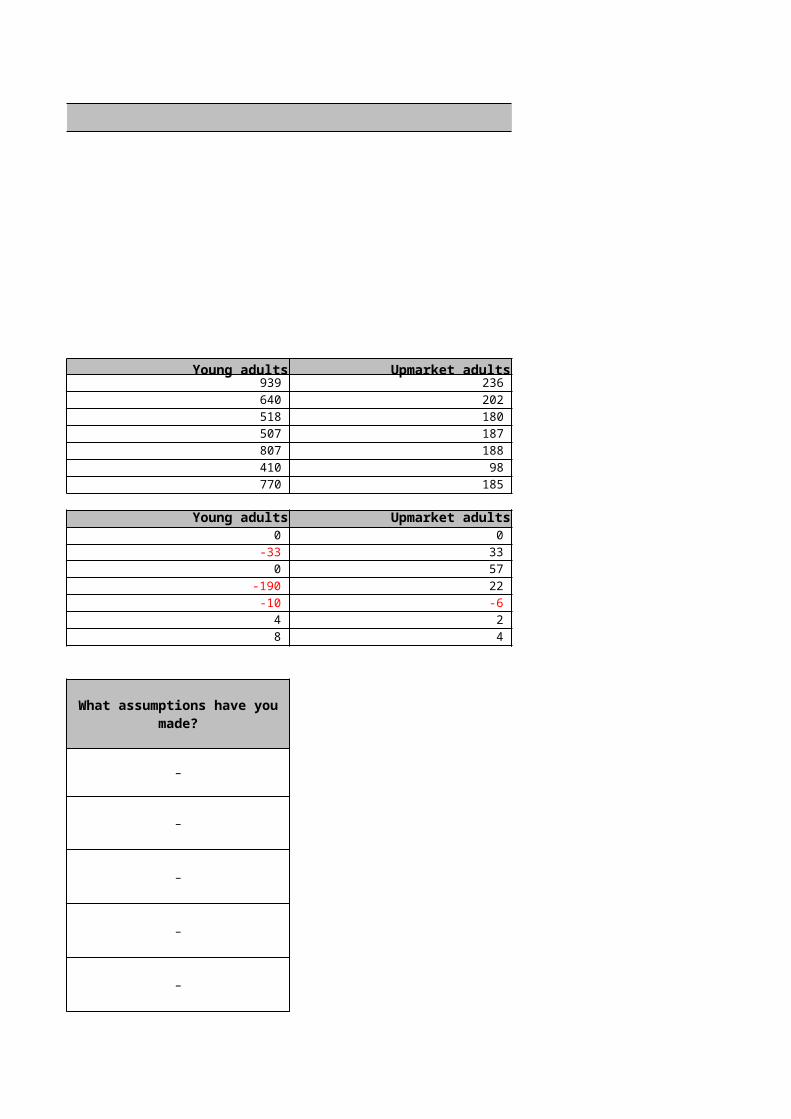

Young adults Upmarket adults Businessmen 939 236 – 640 202 – 518 180 – 507 187 – 807 188 – 410 98 – 770 185 –

Young adults Upmarket adults Businessmen0 0 –

-33 33 – 0 57 –

-190 22 – -10 -6 –

4 2 – 8 4 –

–

–

–

–

–

What assumptions have you made?

–

Since AdEx is not considered valid, we used our estimation,

Country:

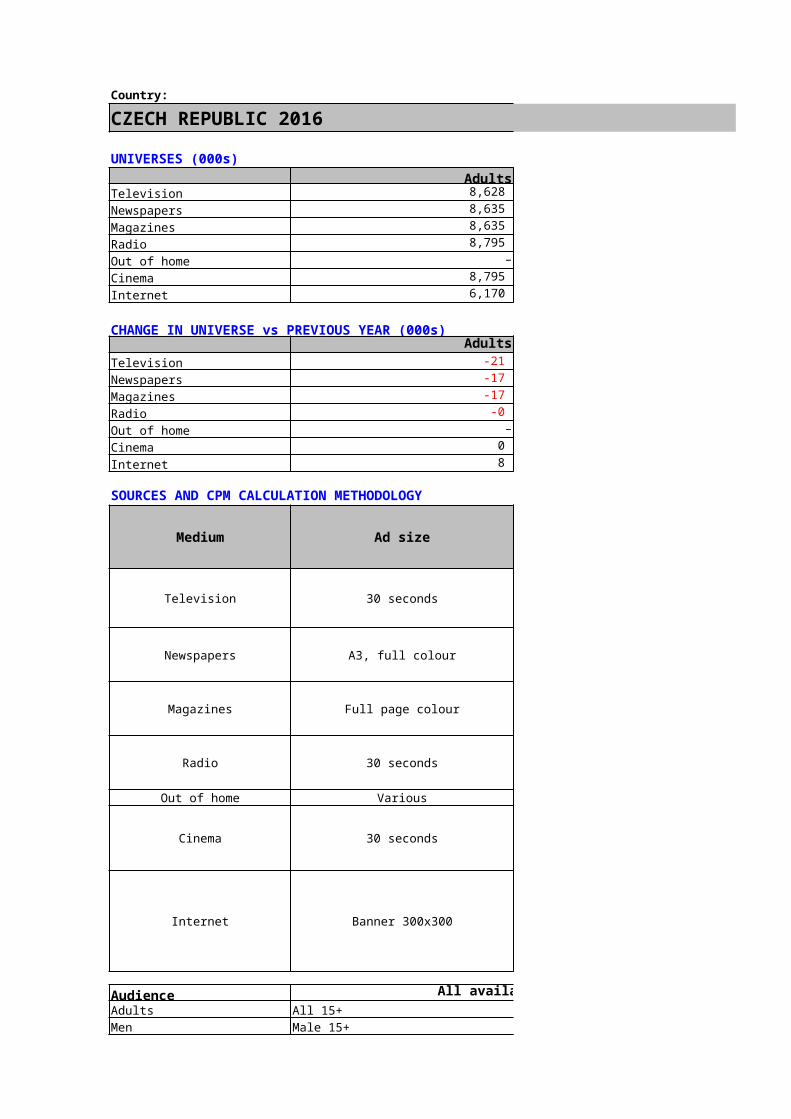

CZECH REPUBLIC 2016

UNIVERSES (000s)Adults Men

Television 8,628 4,191 Newspapers 8,635 4,260 Magazines 8,635 4,260 Radio 8,795 4,340 Out of home – –Cinema 8,795 –Internet 6,170 3,136

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television -21 -4 Newspapers -17 1 Magazines -17 1 Radio -0 -0 Out of home – –Cinema 0 –Internet 8 -4

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds

Newspapers A3, full colour

Magazines Full page colour

Radio 30 seconds

Out of home Various –

Cinema 30 seconds

Internet Banner 300x300

Audience All available mediaAdults All 15+Men Male 15+

Peoplemeters, Mediaresearch - ATO (01.01. - 30.6.2016)

Media projekt - SKMO - GfK Praha, Median 1.10.2015 -

31.3.2016

Media projekt - SKMO - GfK Praha, Median 1.10.2015 -

31.3.2016

RADIO PROJEKT 4. Q 2015 - 1. Q 2016

Peoplemeters, Mediaresearch - ATO (01.01. - 30.6.2016)

Netmonitor (01.01.2015 - 31.3.2016), SPIR -

Mediaresearch, Gemius; Average CPT of the most affinest websites,

used Banner 300x300

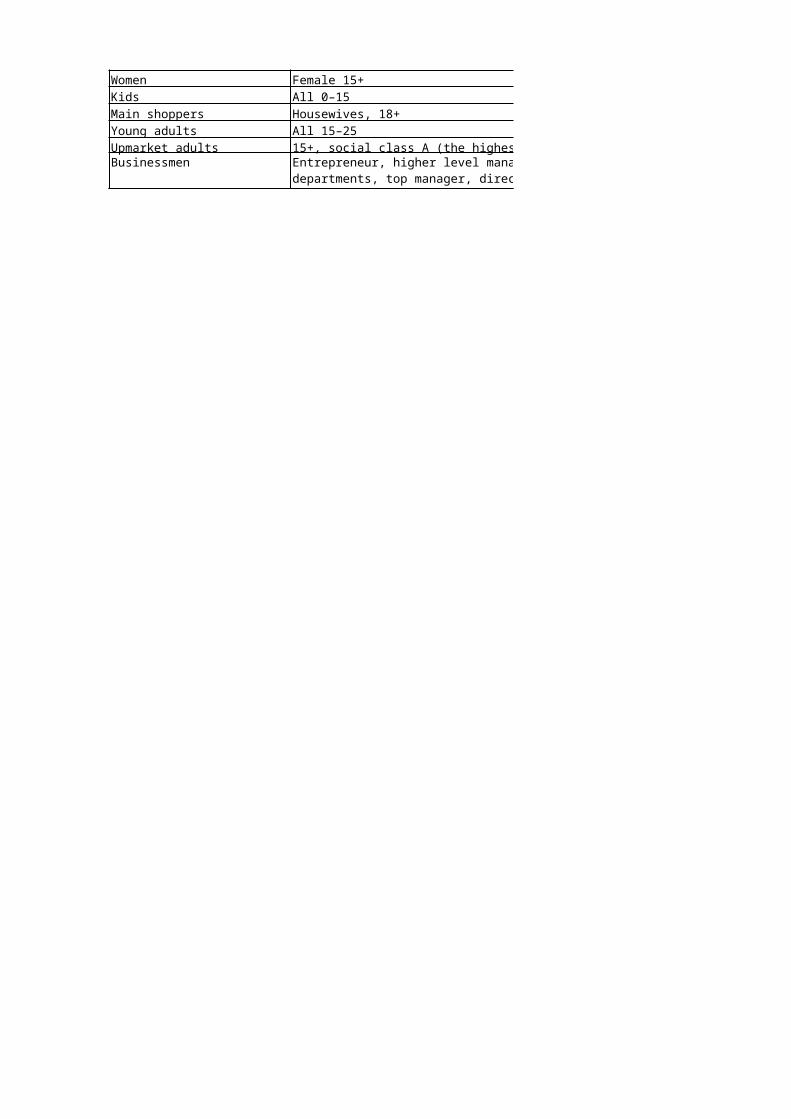

Women Female 15+Kids All 0–15Main shoppers Housewives, 18+Young adults All 15–25Upmarket adults 15+, social class A (the highest level)Businessmen Entrepreneur, higher level manager supervising several departments,

top manager, director

CZECH REPUBLIC 2016

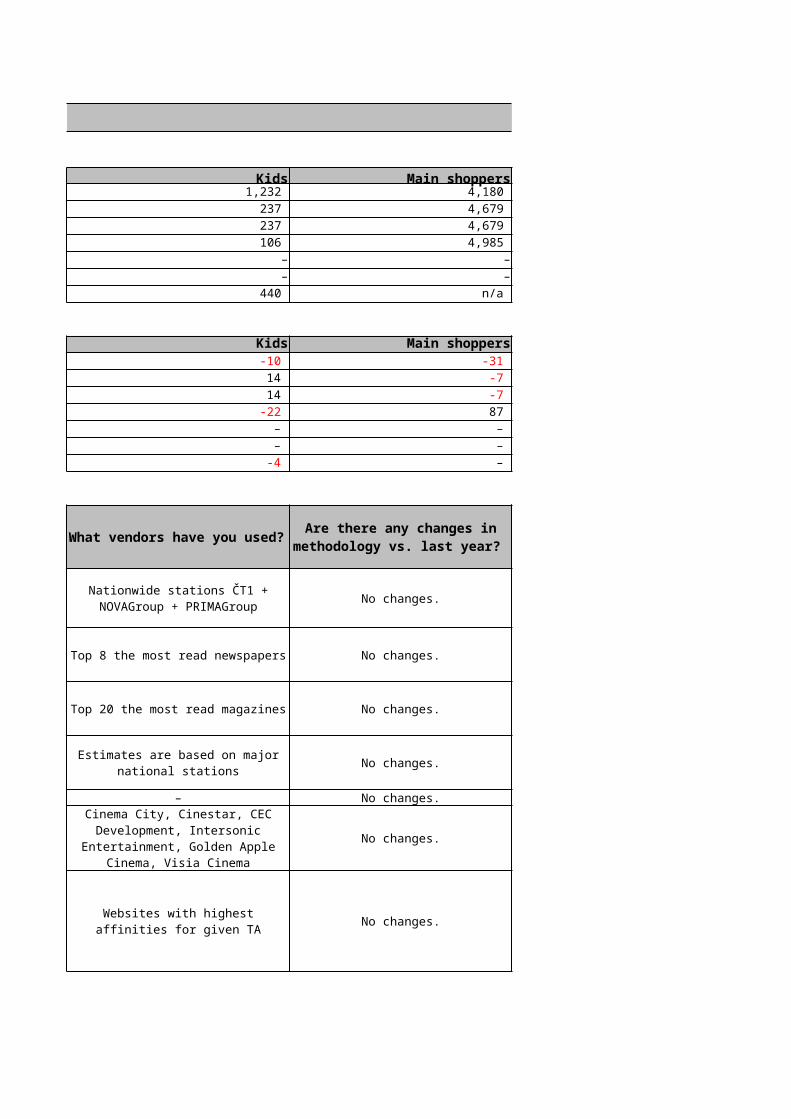

Women Kids Main shoppers 4,437 1,232 4,180 4,375 237 4,679 4,375 237 4,679 4,419 106 4,985

– – –– – –

3,035 440 n/a

Women Kids Main shoppers-17 -10 -31 -18 14 -7 -18 14 -7 11 -22 87

– – – – – –

12 -4 –

No changes.

Top 8 the most read newspapers No changes.

Top 20 the most read magazines No changes.

No changes.

– – No changes.

No changes.

No changes.

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

Total estimated spend divided by universe.

Nationwide stations ČT1 + NOVAGroup + PRIMAGroup

Estimated discounts applied on gross prices of the used vendors.

Estimated discounts applied on gross prices of the used vendors.

Total estimated spend divided by universe.

Estimates are based on major national stations

Total estimated spend divided by universe.

Cinema City, Cinestar, CEC Development, Intersonic

Entertainment, Golden Apple Cinema, Visia Cinema

Average CPT of the most affinest websites. Estimated discounts applied on gross prices of the

used vendors.

Websites with highest affinities for given TA

CZECH REPUBLIC 2016

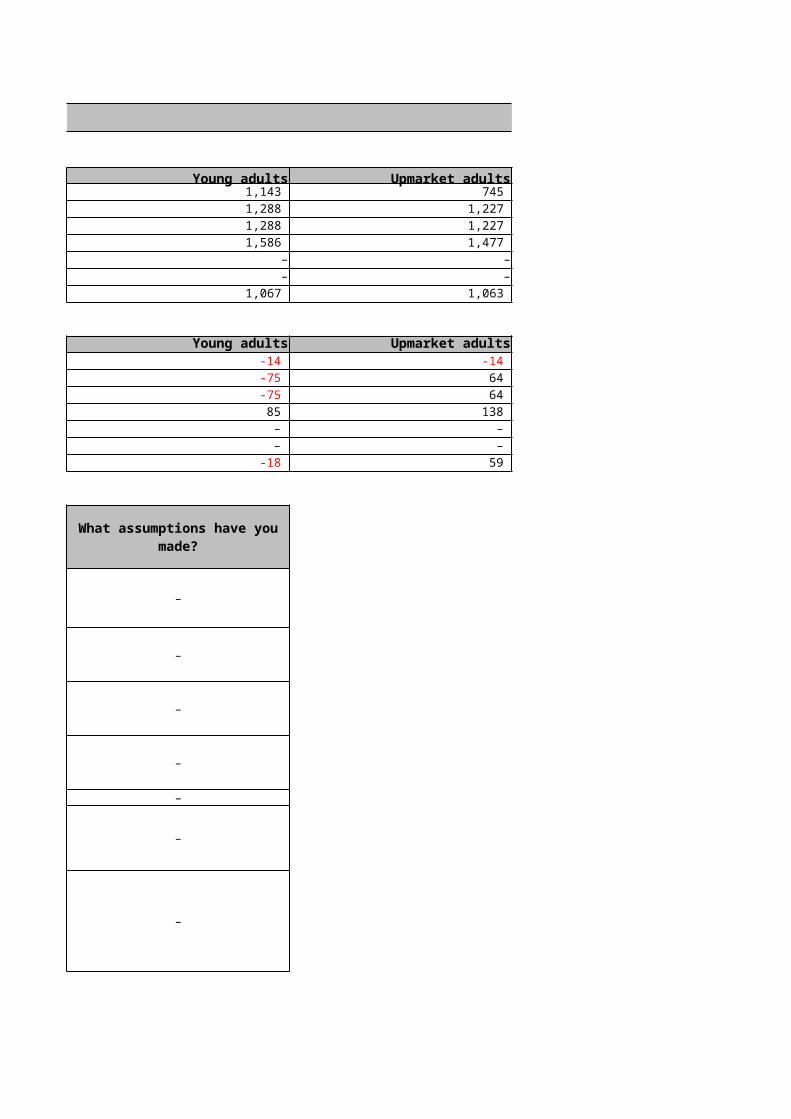

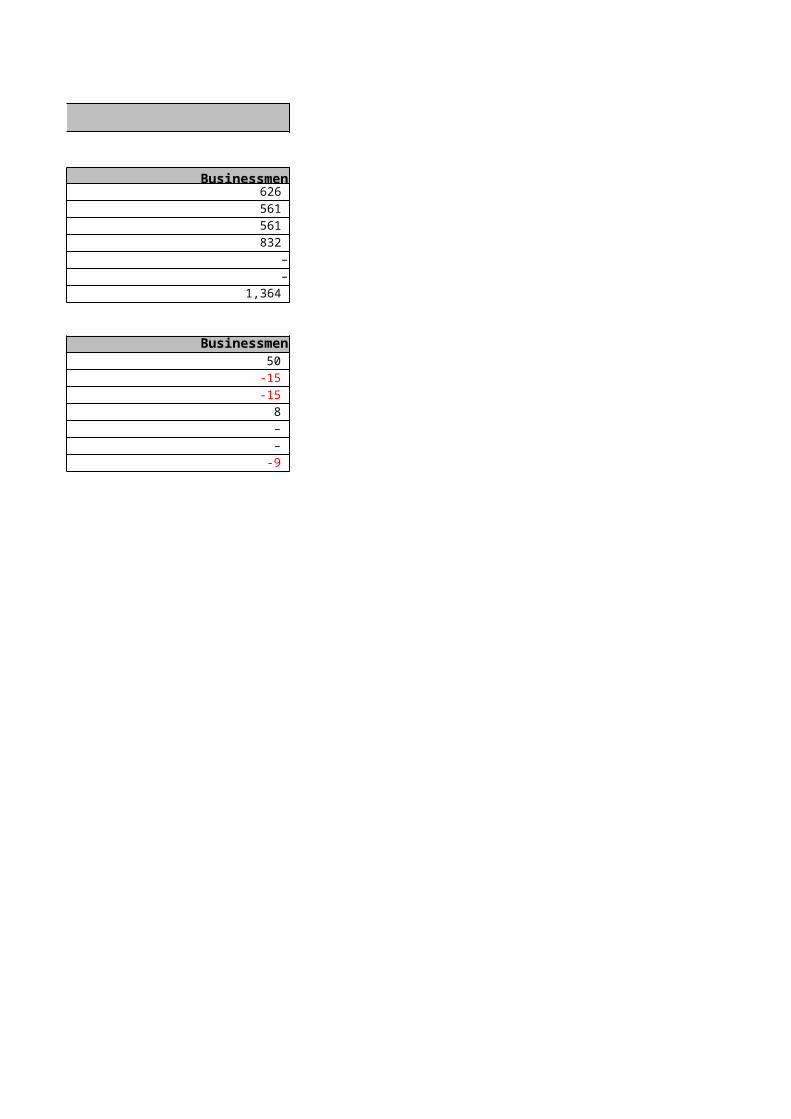

Young adults Upmarket adults Businessmen 1,143 745 626 1,288 1,227 561 1,288 1,227 561 1,586 1,477 832

– – –– – –

1,067 1,063 1,364

Young adults Upmarket adults Businessmen-14 -14 50 -75 64 -15 -75 64 -15 85 138 8 – – – – – –

-18 59 -9

–

–

–

–

–

–

–

What assumptions have you made?

Country:

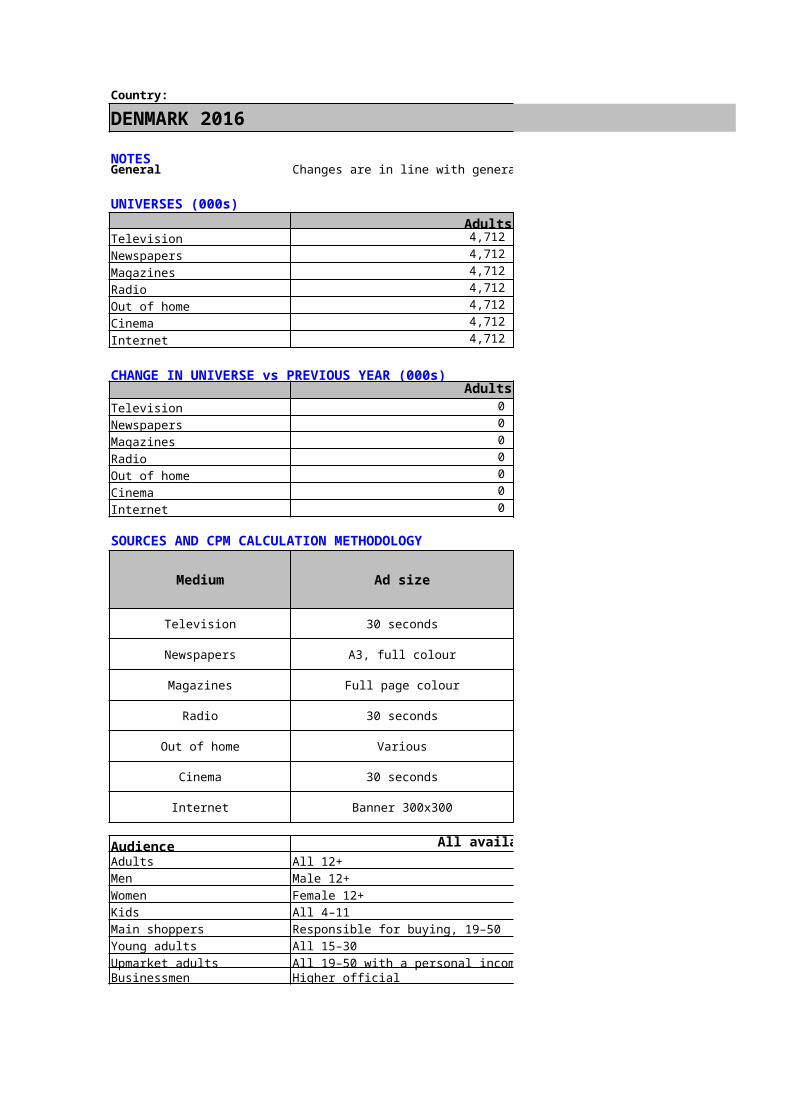

DENMARK 2016

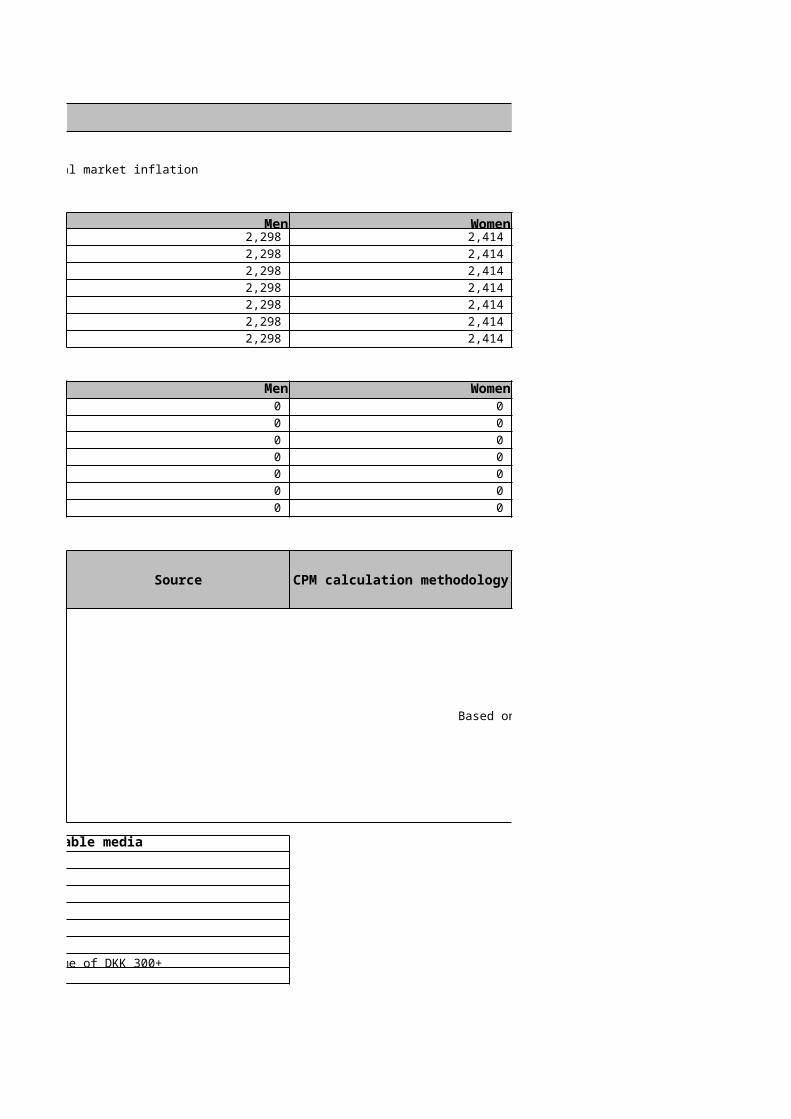

NOTESGeneral Changes are in line with general market inflation

UNIVERSES (000s)Adults Men

Television 4,712 2,298 Newspapers 4,712 2,298 Magazines 4,712 2,298 Radio 4,712 2,298 Out of home 4,712 2,298 Cinema 4,712 2,298 Internet 4,712 2,298

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 0 0 Newspapers 0 0 Magazines 0 0 Radio 0 0 Out of home 0 0 Cinema 0 0 Internet 0 0

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds

Based on average advertiser within OMD Denmark

Newspapers A3, full colour

Magazines Full page colour

Radio 30 seconds

Out of home Various

Cinema 30 seconds

Internet Banner 300x300

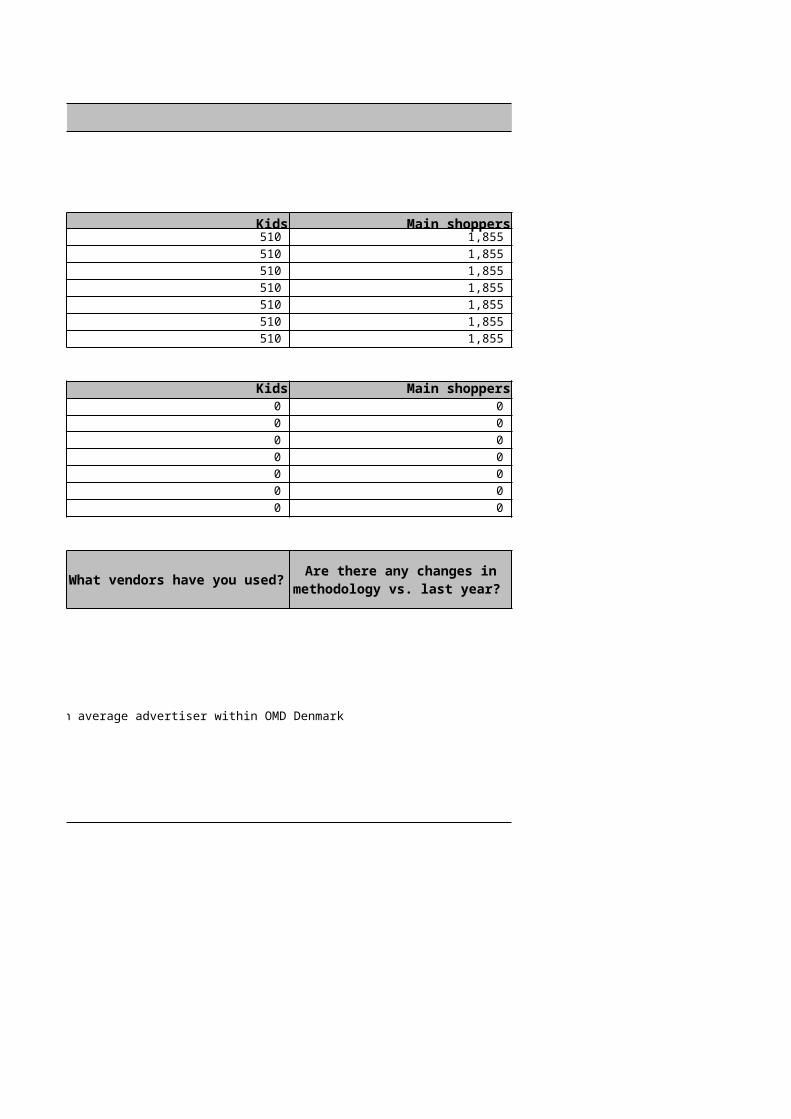

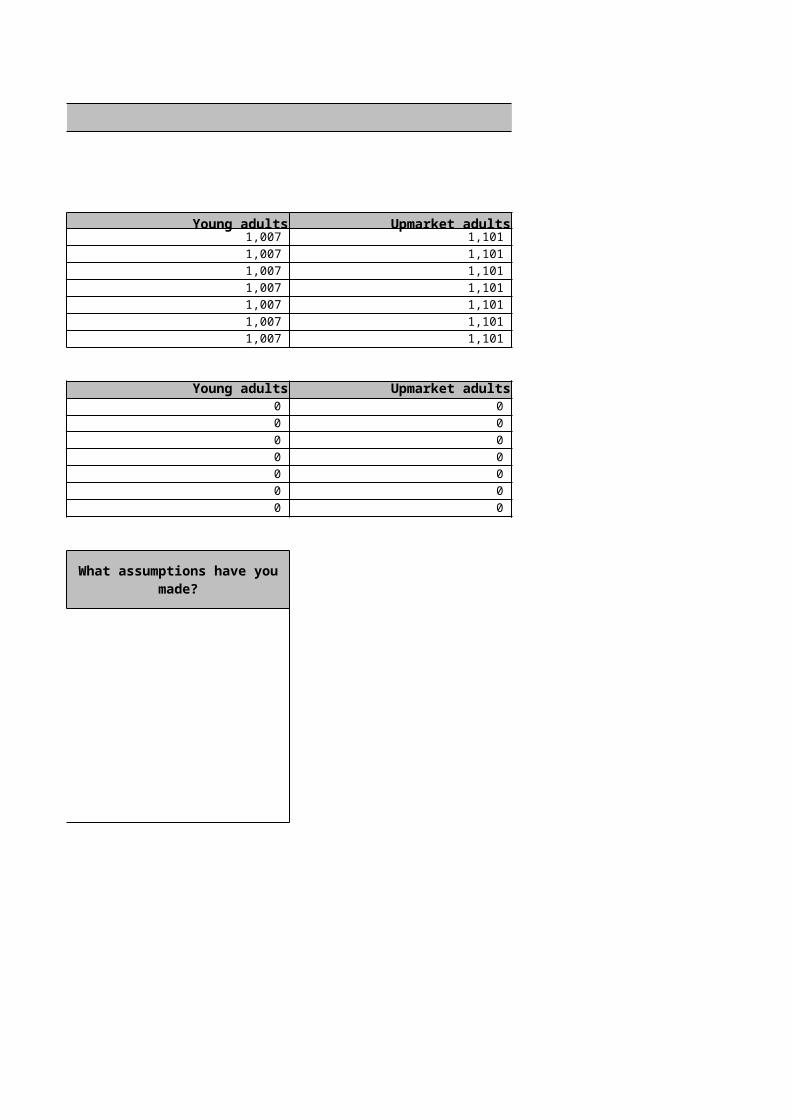

Audience All available mediaAdults All 12+Men Male 12+Women Female 12+Kids All 4–11Main shoppers Responsible for buying, 19–50Young adults All 15–30Upmarket adults All 19–50 with a personal income of DKK 300+Businessmen Higher official

DENMARK 2016

Women Kids Main shoppers 2,414 510 1,855 2,414 510 1,855 2,414 510 1,855 2,414 510 1,855 2,414 510 1,855 2,414 510 1,855 2,414 510 1,855

Women Kids Main shoppers0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Based on average advertiser within OMD Denmark

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

DENMARK 2016

Young adults Upmarket adults Businessmen 1,007 1,101 584 1,007 1,101 584 1,007 1,101 584 1,007 1,101 584 1,007 1,101 584 1,007 1,101 584 1,007 1,101 584

Young adults Upmarket adults Businessmen0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Based on average advertiser within OMD Denmark

What assumptions have you made?

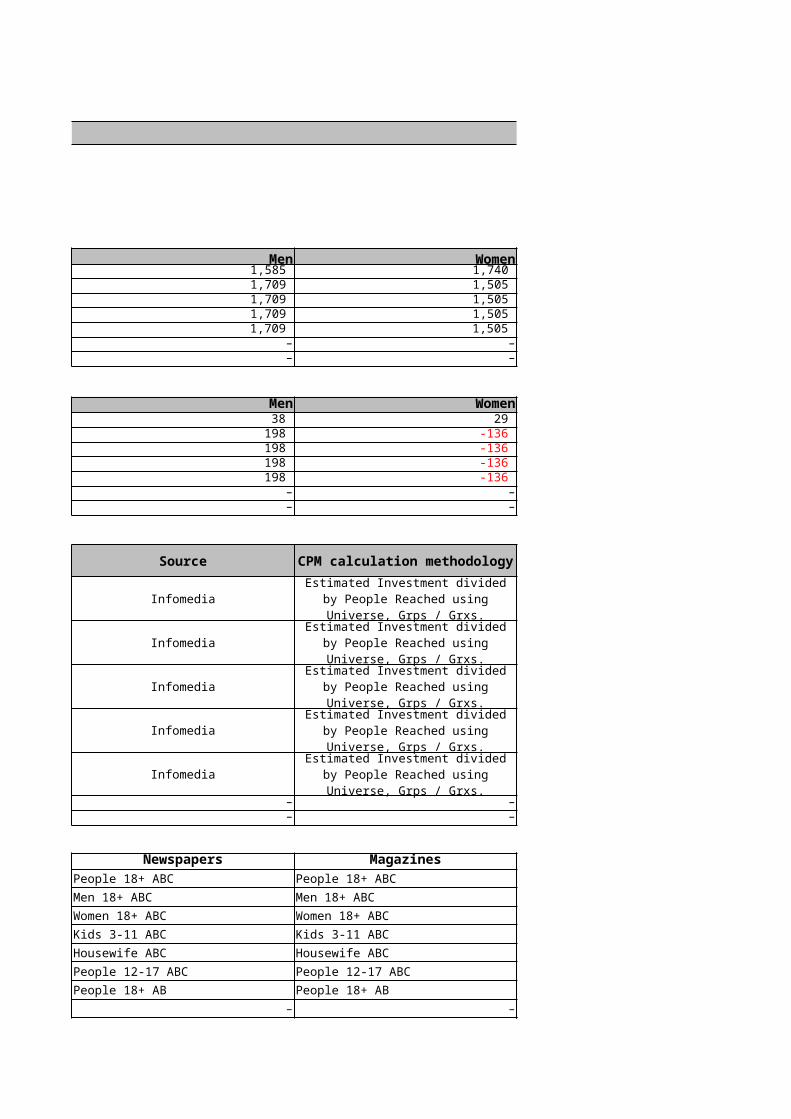

Country:ECUADOR 2016

NOTES

UNIVERSES (000s)Adults Men

Television 3,325 1,585 Newspapers 3,214 1,709 Magazines 3,214 1,709 Radio 3,214 1,709 Out of home 3,214 1,709 Cinema – –Internet – –

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 67 38 Newspapers 62 198 Magazines 62 198 Radio 62 198 Out of home 62 198 Cinema – –Internet – –

SOURCES AND CPM CALCULATION METHODOLOGYMedium Ad size Source

Television 30 seconds Infomedia

Newspapers A3, full colour Infomedia

Magazines Full page colour Infomedia

Radio 30 seconds Infomedia

Out of home Various Infomedia

Cinema 30 seconds –Internet Banner 468x60 –

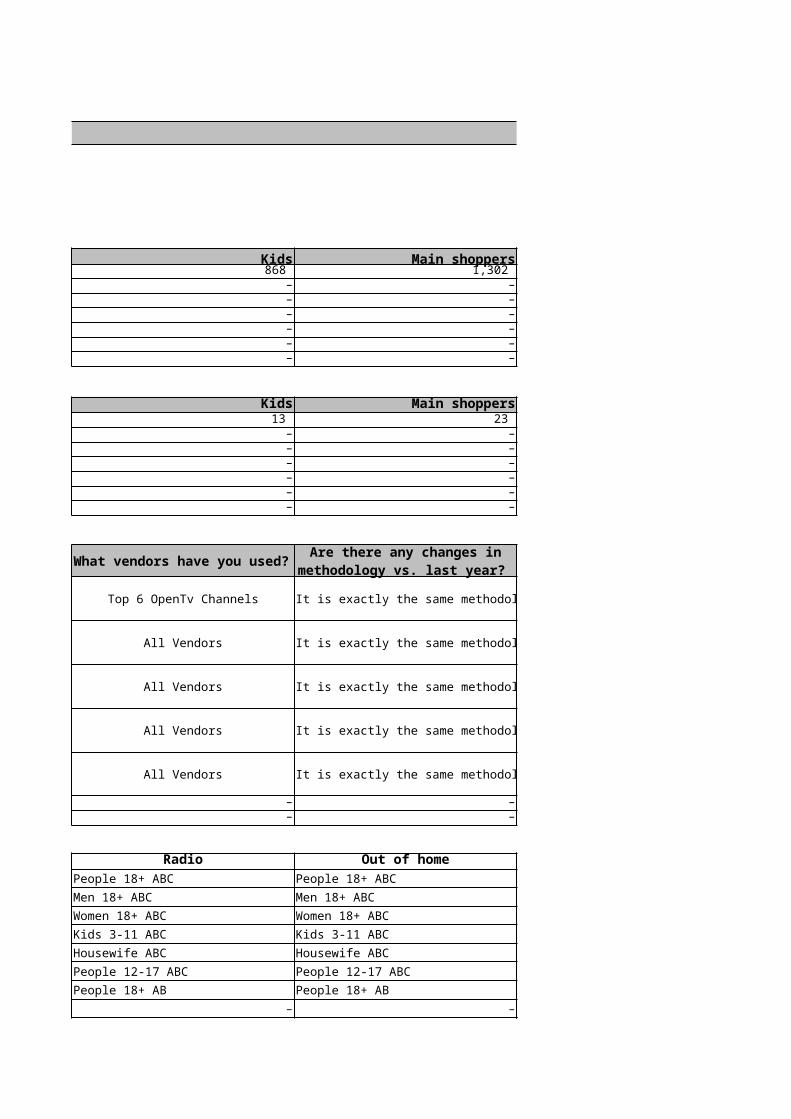

Audience TV NewspapersAdults People 18+ ABC People 18+ ABCMen Men 18+ ABC Men 18+ ABCWomen Women 18+ ABC Women 18+ ABCKids Kids 3-11 ABC Kids 3-11 ABCMain shoppers Housewife ABC Housewife ABCYoung adults People 12-17 ABC People 12-17 ABCUpmarket adults People 18+ AB People 18+ ABBusinessmen – –

ECUADOR 2016

Women Kids Main shoppers 1,740 868 1,302 1,505 – – 1,505 – – 1,505 – –

1,505 – –– – –– – –

Women Kids Main shoppers29 13 23

-136 – –-136 – –-136 – –-136 – –

– – –– – –

Top 6 OpenTv Channels It is exactly the same methodology.

All Vendors It is exactly the same methodology.

All Vendors It is exactly the same methodology.

All Vendors It is exactly the same methodology.

All Vendors It is exactly the same methodology.

– – –– – –

Magazines Radio Out of homePeople 18+ ABC People 18+ ABC People 18+ ABCMen 18+ ABC Men 18+ ABC Men 18+ ABCWomen 18+ ABC Women 18+ ABC Women 18+ ABCKids 3-11 ABC Kids 3-11 ABC Kids 3-11 ABCHousewife ABC Housewife ABC Housewife ABCPeople 12-17 ABC People 12-17 ABC People 12-17 ABCPeople 18+ AB People 18+ AB People 18+ AB

– – –

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

Estimated Investment divided by People Reached using Universe,

Grps / Grxs.Estimated Investment divided by People Reached using Universe,

Grps / Grxs.Estimated Investment divided by People Reached using Universe,

Grps / Grxs.Estimated Investment divided by People Reached using Universe,

Grps / Grxs.Estimated Investment divided by People Reached using Universe,

Grps / Grxs.

ECUADOR 2016

Young adults Upmarket adults Businessmen 595 1,901 – 524 1,826 – 524 1,826 – 524 1,826 –

524 1,826 –– – –– – –

Young adults Upmarket adults Businessmen7 50 –

10 35 –10 35 –10 35 –10 35 –

– – –– – –

–

–

–

–

–––

Cinema Internet– –– –– –– –– –– –– –– –

What assumptions have you made?

Country:

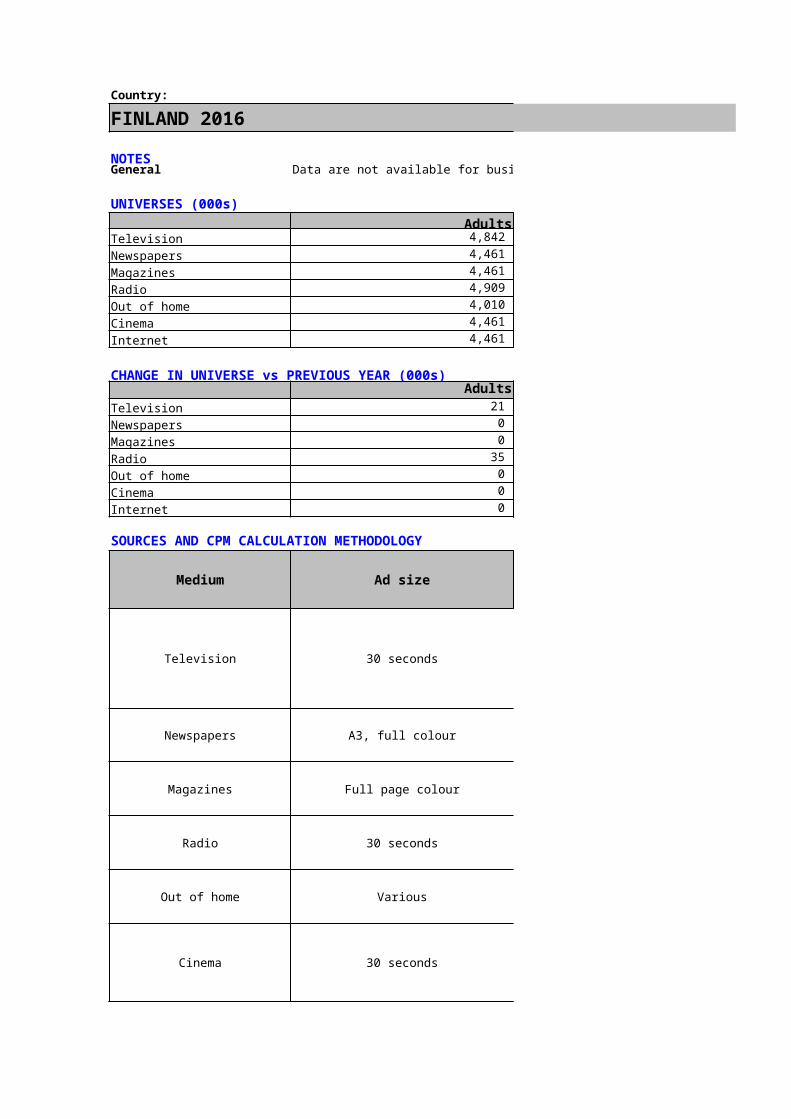

FINLAND 2016

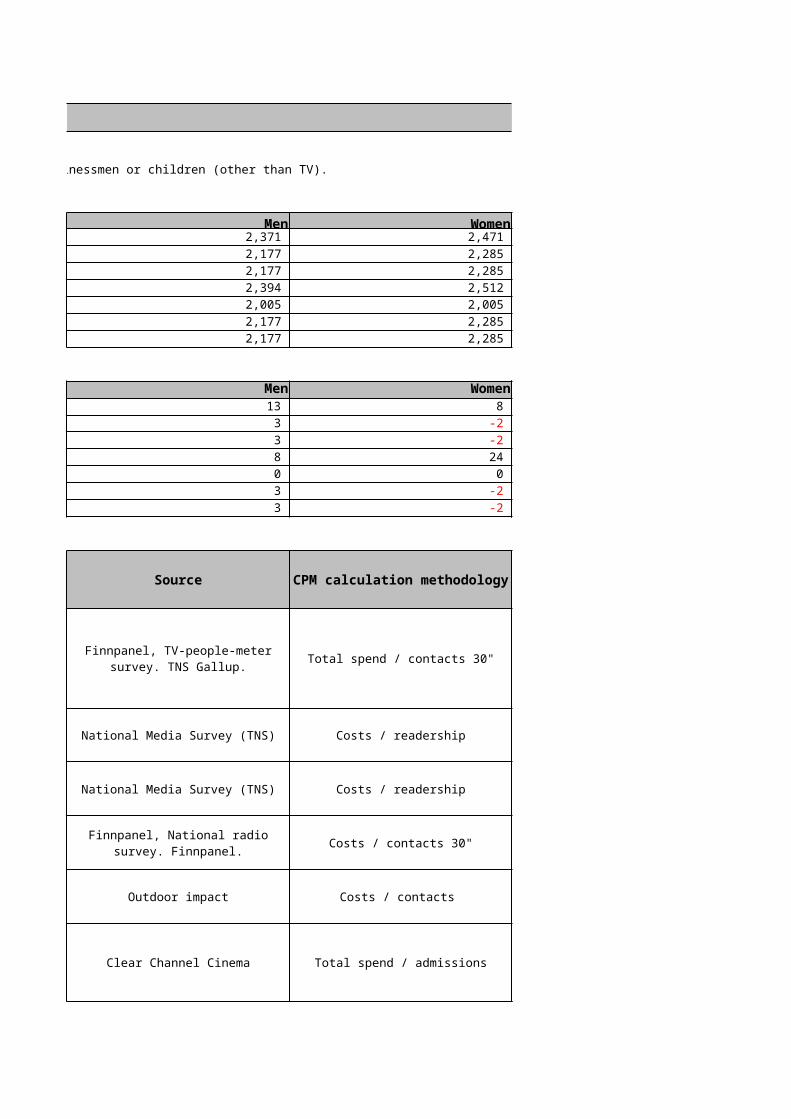

NOTESGeneral Data are not available for businessmen or children (other than TV).

UNIVERSES (000s)Adults Men

Television 4,842 2,371 Newspapers 4,461 2,177 Magazines 4,461 2,177 Radio 4,909 2,394 Out of home 4,010 2,005 Cinema 4,461 2,177 Internet 4,461 2,177

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 21 13 Newspapers 0 3 Magazines 0 3 Radio 35 8 Out of home 0 0 Cinema 0 3 Internet 0 3

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds

Newspapers A3, full colour National Media Survey (TNS)

Magazines Full page colour National Media Survey (TNS)

Radio 30 seconds

Out of home Various Outdoor impact

Cinema 30 seconds Clear Channel Cinema

Finnpanel, TV-people-meter survey. TNS Gallup.

Finnpanel, National radio survey. Finnpanel.

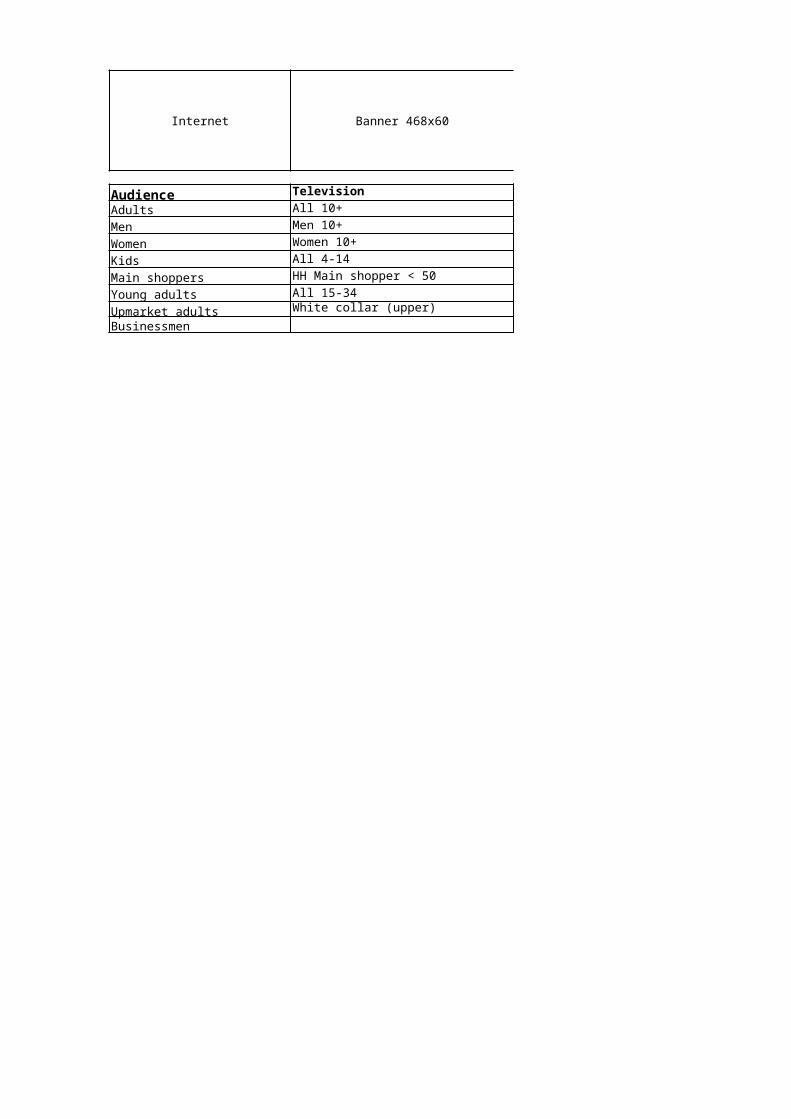

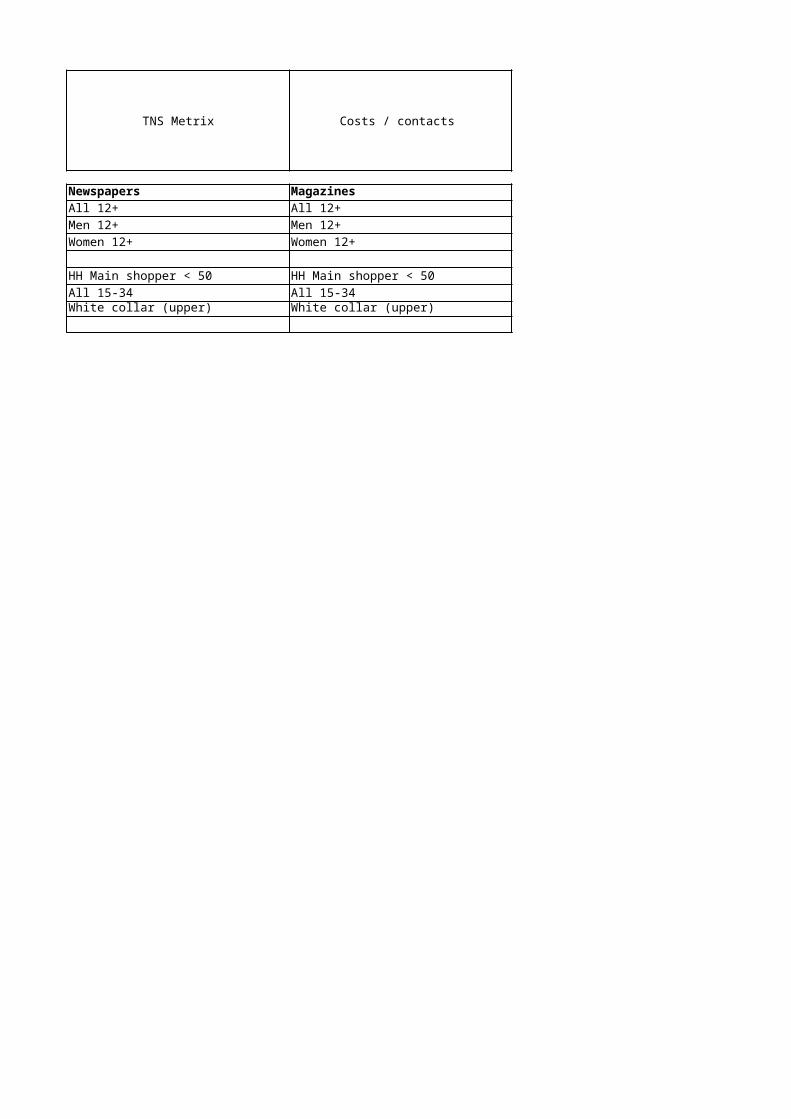

Internet Banner 468x60 TNS Metrix

Audience Television NewspapersAdults All 10+ All 12+Men Men 10+ Men 12+Women Women 10+ Women 12+Kids All 4-14Main shoppers HH Main shopper < 50 HH Main shopper < 50Young adults All 15-34 All 15-34Upmarket adults White collar (upper) White collar (upper)Businessmen

FINLAND 2016

Data are not available for businessmen or children (other than TV).

Women Kids Main shoppers 2,471 655 1,254 2,285 – 1,256 2,285 – 1,256 2,512 – 1,915 2,005 – 1,199 2,285 – 1,256 2,285 – 1,256

Women Kids Main shoppers8 4 0

-2 – -26 -2 – -26 24 – 1 0 – 0

-2 – -26 -2 – -26

Total spend / contacts 30" No

Costs / readership No

Costs / readership TOP 5 Magazines sales houses No

Costs / contacts 30" Top 4 radio sales houses No

Costs / contacts JCD, Clear Channel No

Total spend / admissions Clear Channel No

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

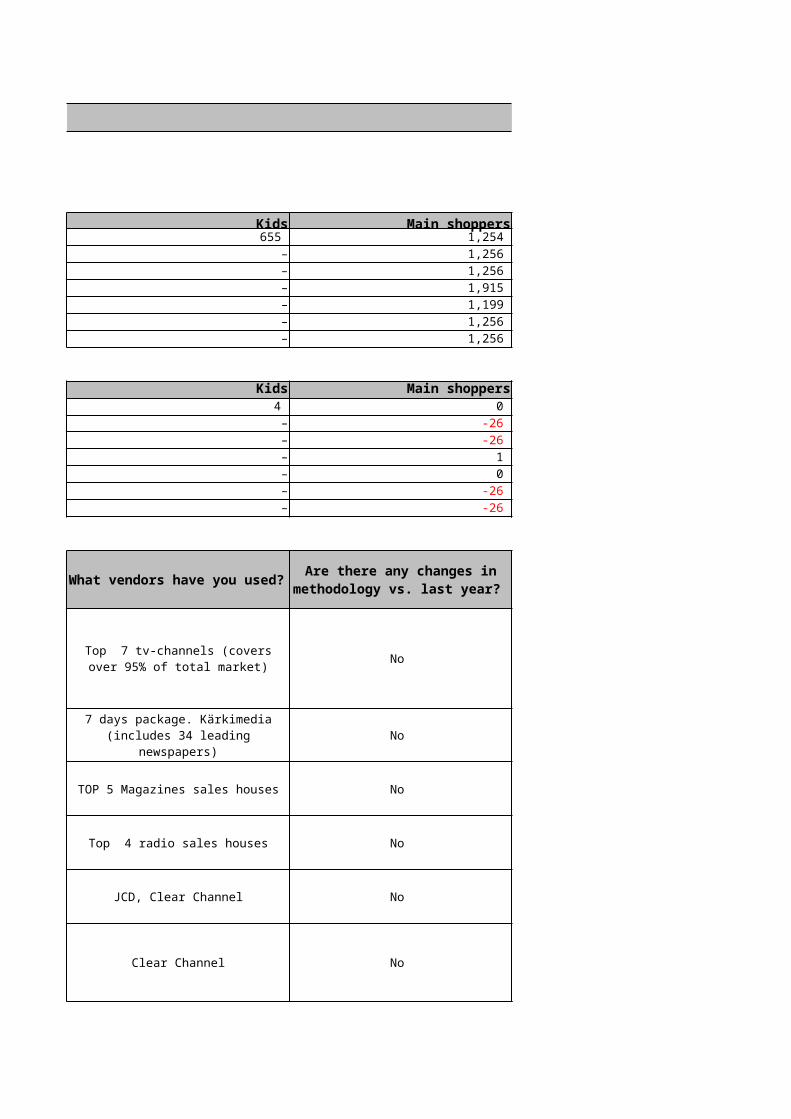

Top 7 tv-channels (covers over 95% of total market)

7 days package. Kärkimedia (includes 34 leading newspapers)

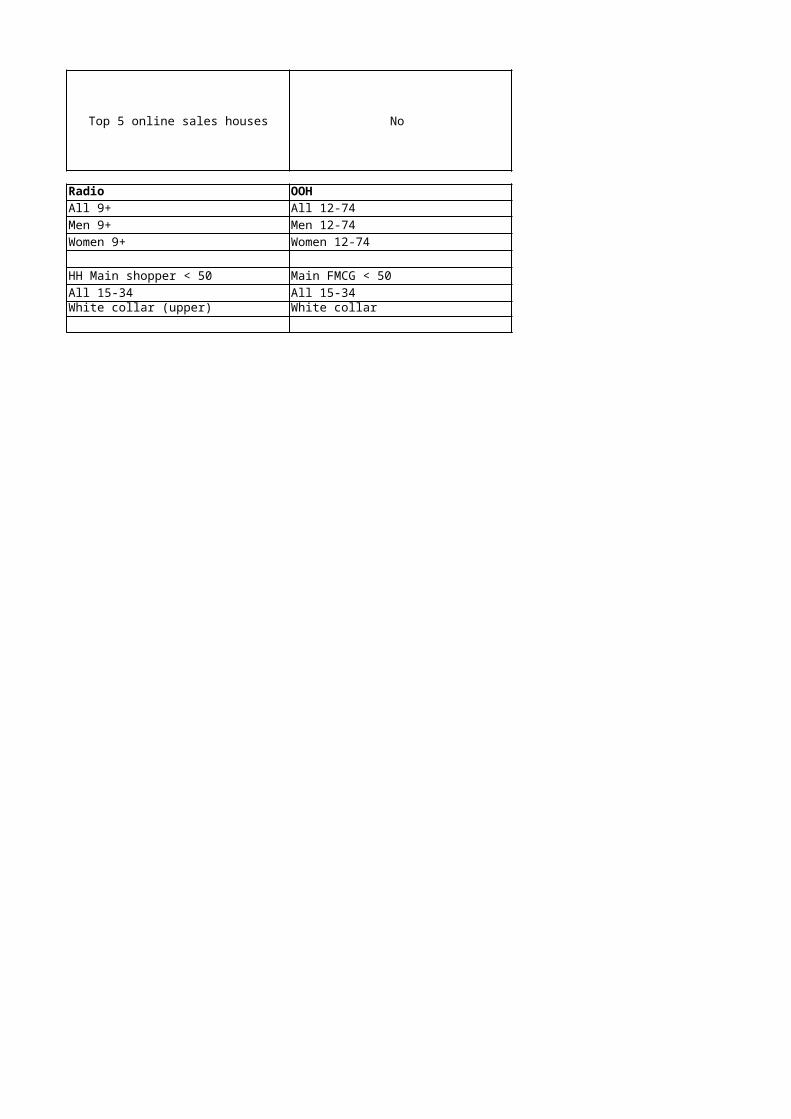

Costs / contacts Top 5 online sales houses No

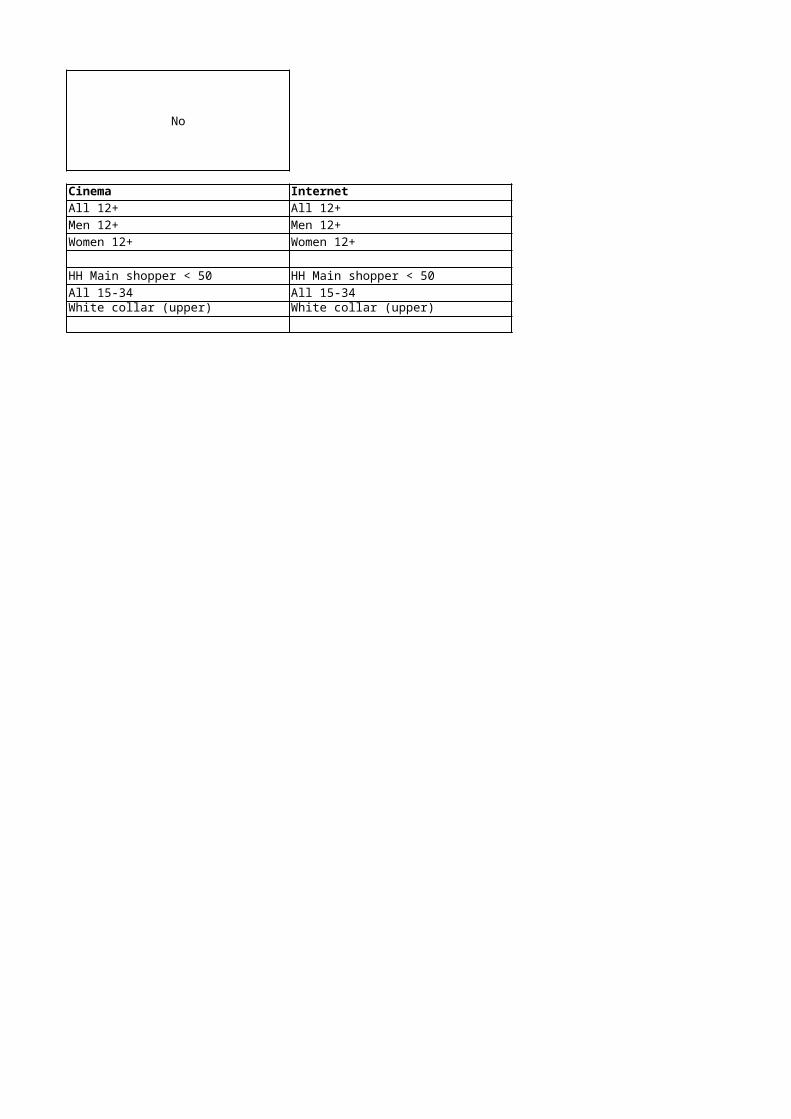

Magazines Radio OOHAll 12+ All 9+ All 12-74Men 12+ Men 9+ Men 12-74Women 12+ Women 9+ Women 12-74

HH Main shopper < 50 HH Main shopper < 50 Main FMCG < 50All 15-34 All 15-34 All 15-34White collar (upper) White collar (upper) White collar

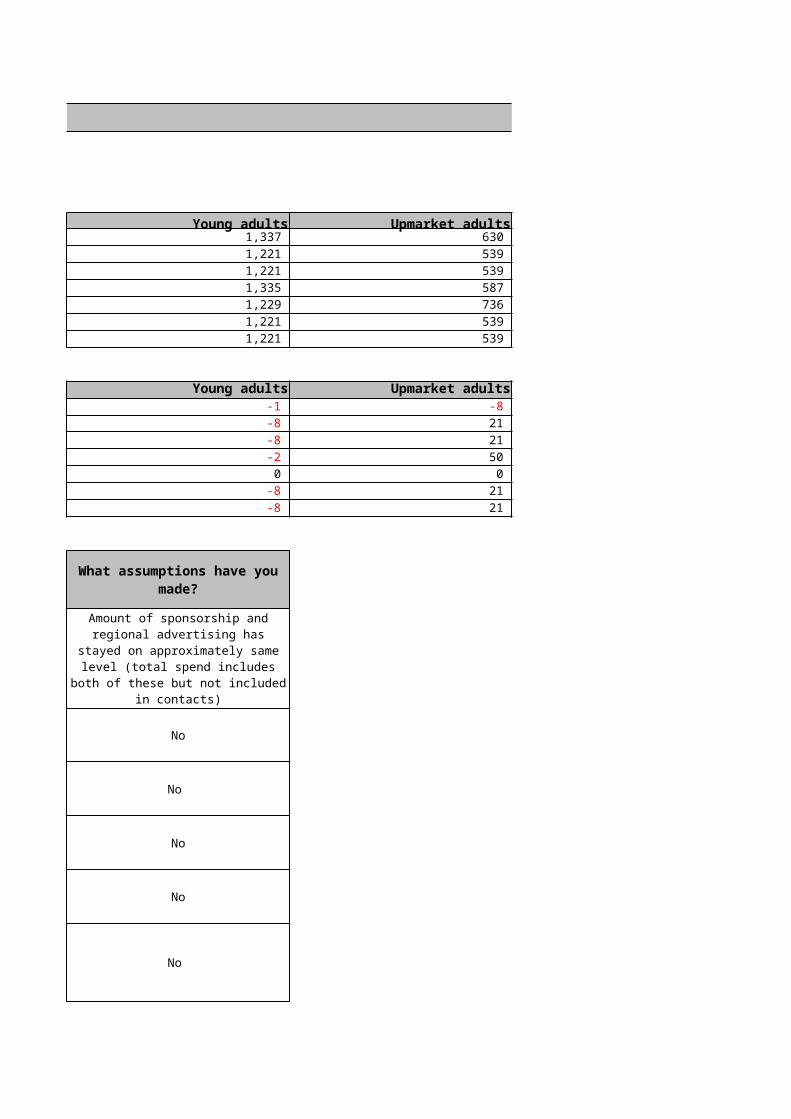

FINLAND 2016

Young adults Upmarket adults Businessmen 1,337 630 – 1,221 539 – 1,221 539 – 1,335 587 – 1,229 736 – 1,221 539 – 1,221 539 –

Young adults Upmarket adults Businessmen-1 -8 –-8 21 –-8 21 –-2 50 –0 0 –

-8 21 –-8 21 –

No

No

No

No

No

What assumptions have you made?

Amount of sponsorship and regional advertising has stayed on

approximately same level (total spend includes both of these but

not included in contacts)

No

Cinema InternetAll 12+ All 12+Men 12+ Men 12+Women 12+ Women 12+

HH Main shopper < 50 HH Main shopper < 50All 15-34 All 15-34White collar (upper) White collar (upper)

Country:FRANCE 2016

NOTES

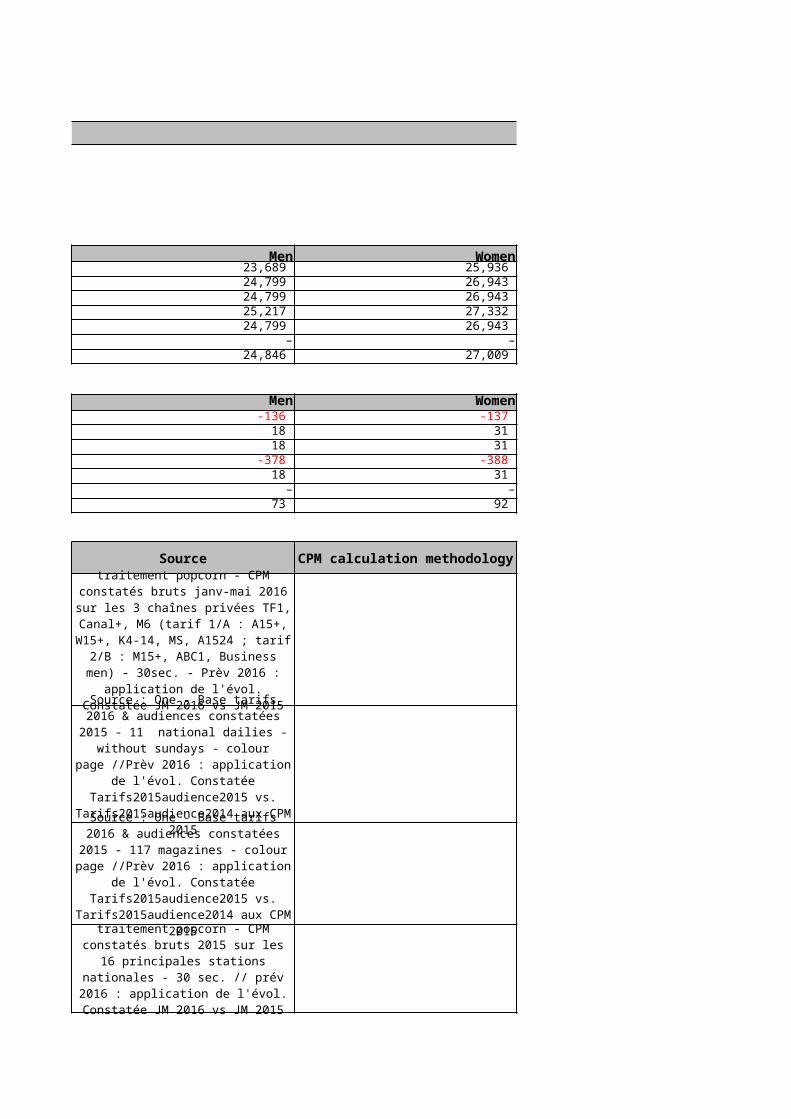

UNIVERSES (000s)Adults Men

Television 49,625 23,689 Newspapers 51,742 24,799 Magazines 51,742 24,799 Radio 52,549 25,217 Out of home 51,742 24,799 Cinema 59,300 –Internet 51,855 24,846

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television -273 -136 Newspapers 49 18 Magazines 49 18 Radio 276 -378 Out of home 49 18 Cinema 1,514 –Internet 165 73

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds

Newspapers A3, full colour

Magazines Full page colour

Radio 30 seconds

Out of home Various

Source : Médiamétrie - traitement popcorn - CPM constatés bruts janv-mai 2016 sur les 3 chaînes privées TF1, Canal+, M6 (tarif 1/A : A15+, W15+, K4-14, MS, A1524 ; tarif 2/B : M15+, ABC1, Business men) - 30sec. - Prèv

2016 : application de l'évol. Constatée JM 2016 vs JM 2015

aux CPM 2015Source : One - Base tarifs 2016 & audiences constatées 2015 - 11

national dailies - without sundays - colour page //Prèv 2016 :

application de l'évol. Constatée Tarifs2015audience2015 vs.

Tarifs2015audience2014 aux CPM 2015

Source : One - Base tarifs 2016 & audiences constatées 2015 - 117 magazines - colour page //Prèv

2016 : application de l'évol. Constatée

Tarifs2015audience2015 vs. Tarifs2015audience2014 aux CPM

2015Source : Médiamétrie - traitement popcorn - CPM constatés bruts

2015 sur les 16 principales stations nationales - 30 sec. //

prév 2016 : application de l'évol. Constatée JM 2016 vs JM 2015

aux CPM2015

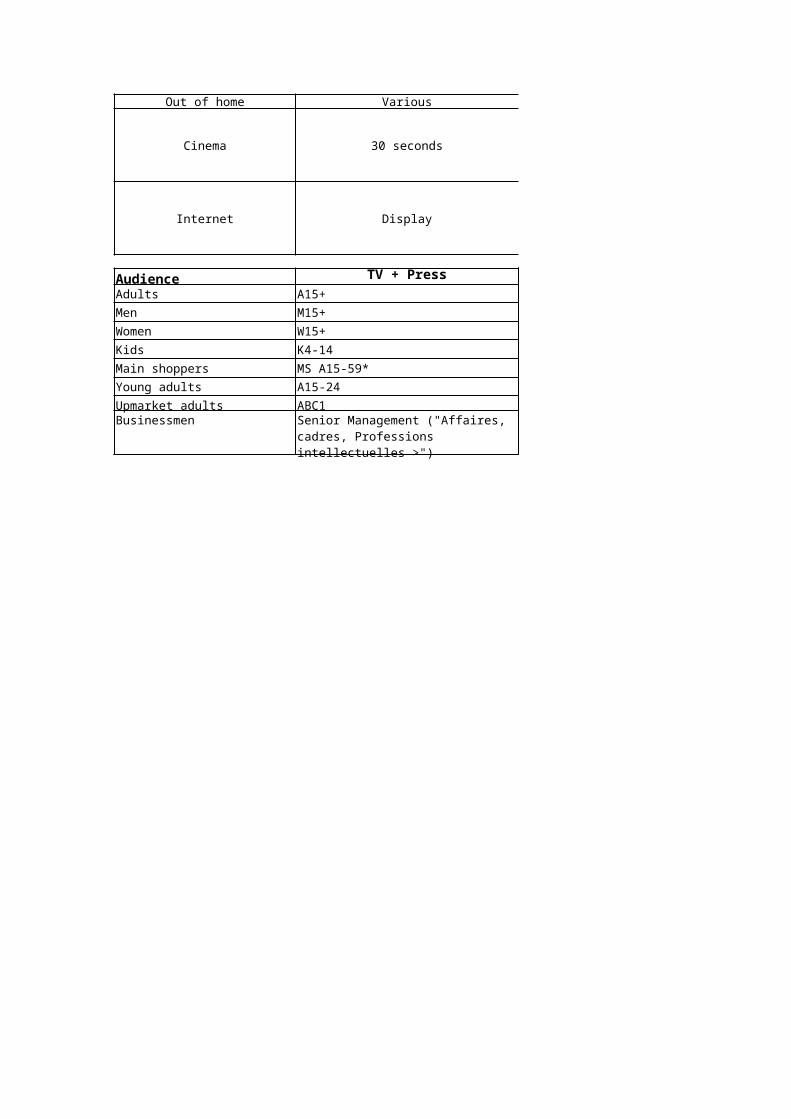

Cinema 30 seconds

Internet Display

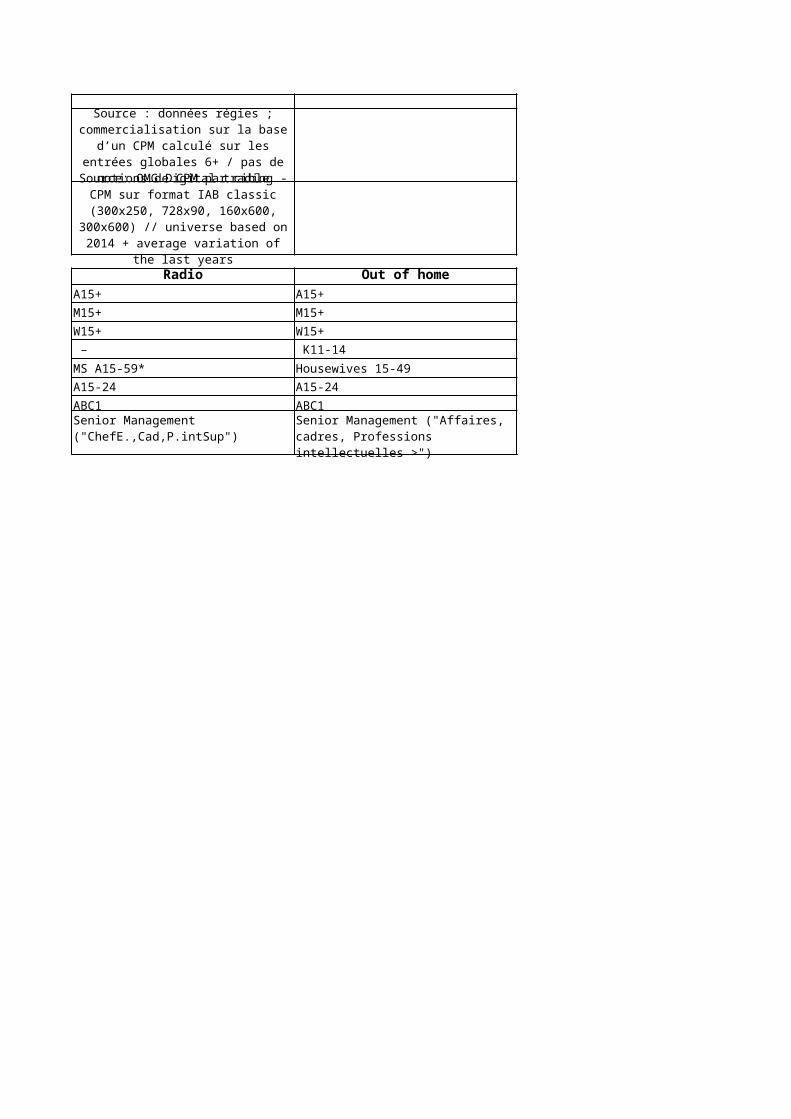

Audience TV + Press RadioAdults A15+ A15+Men M15+ M15+Women W15+ W15+Kids K4-14 – Main shoppers MS A15-59* MS A15-59*Young adults A15-24 A15-24Upmarket adults ABC1 ABC1Businessmen

Source : données régies ; commercialisation sur la base d’un

CPM calculé sur les entrées globales 6+ / pas de notions de

CPM par cibleSource: OMG Digital trading - CPM sur format IAB classic (300x250, 728x90, 160x600,

300x600) // universe based on 2014 + average variation of the

last years

Senior Management ("Affaires, cadres, Professions intellectuelles >")

Senior Management ("ChefE.,Cad,P.intSup")

FRANCE 2016

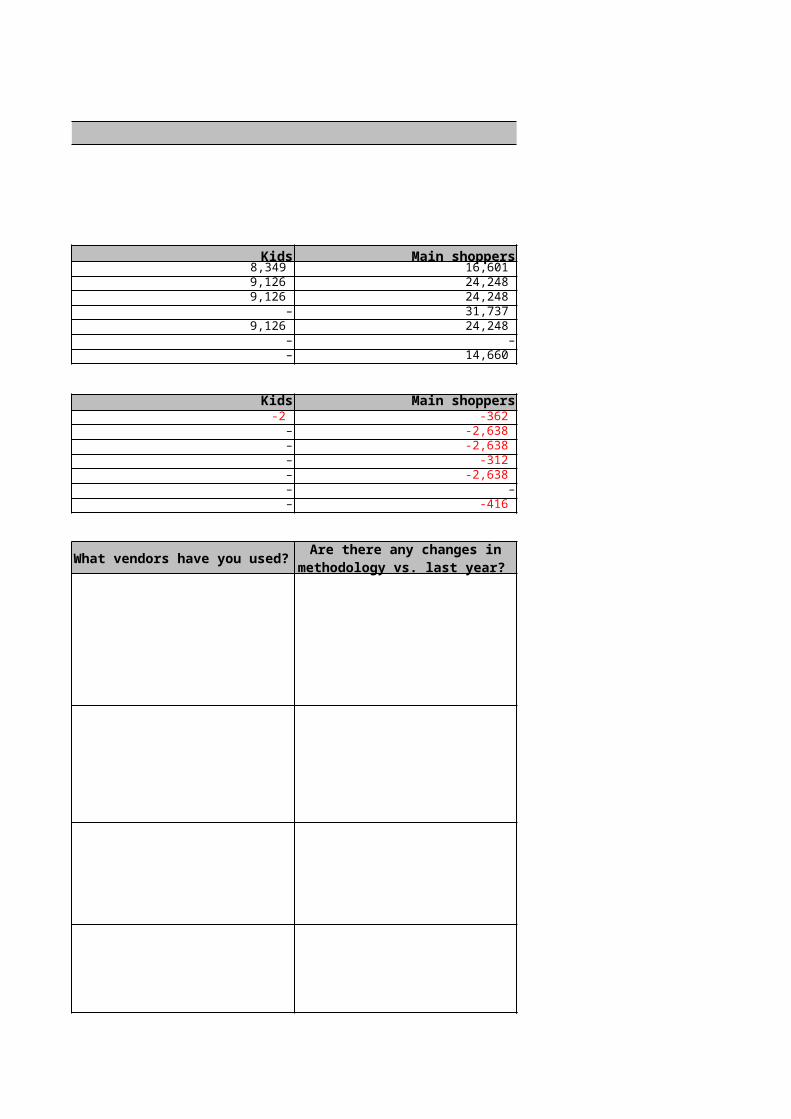

Women Kids Main shoppers 25,936 8,349 16,601 26,943 9,126 24,248 26,943 9,126 24,248 27,332 – 31,737 26,943 9,126 24,248

– – – 27,009 – 14,660

Women Kids Main shoppers-137 -2 -362

31 – -2,638 31 – -2,638

-388 – -312 31 – -2,638

– – –92 – -416

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

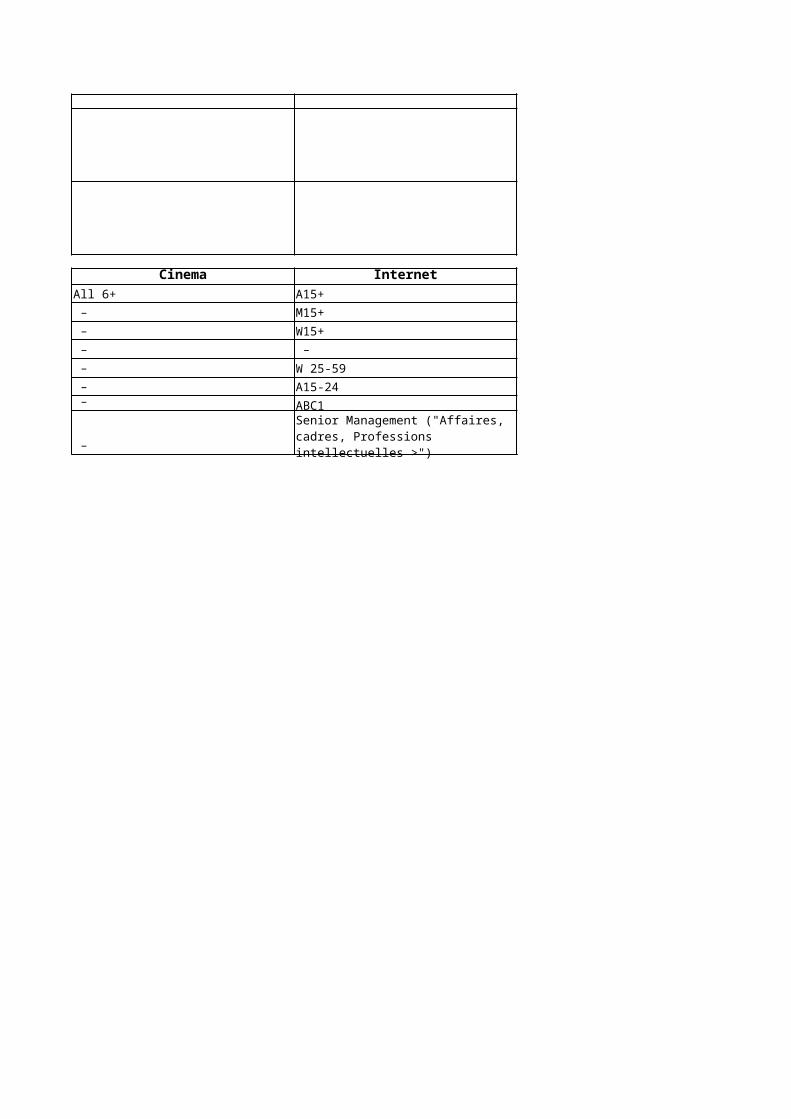

Out of home Cinema InternetA15+ All 6+ A15+M15+ – M15+W15+ – W15+

K11-14 – – Housewives 15-49 – W 25-59A15-24 – A15-24ABC1 – ABC1

–

Senior Management ("Affaires, cadres, Professions intellectuelles >")

Senior Management ("Affaires, cadres, Professions intellectuelles >")

FRANCE 2016

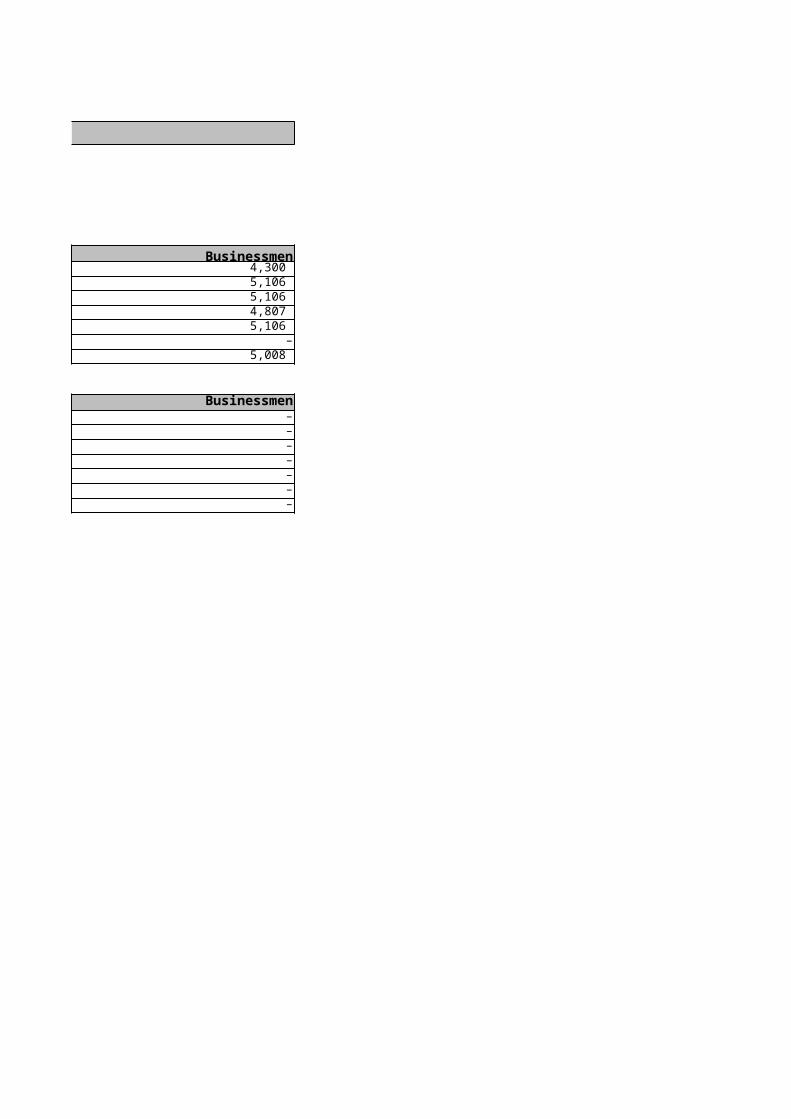

Young adults Upmarket adults Businessmen 6,909 12,437 4,300 7,272 13,630 5,106 7,272 13,630 5,106 7,782 13,429 4,807 7,272 13,630 5,106

– – – 7,302 13,556 5,008

Young adults Upmarket adults Businessmen13 -402 –

-24 -160 –-24 -160 –-44 -184 –-24 -160 –

– – –-15 -90 –

-0.56

-0.6

-0.56

-0.79

What assumptions have you made?

-0.65

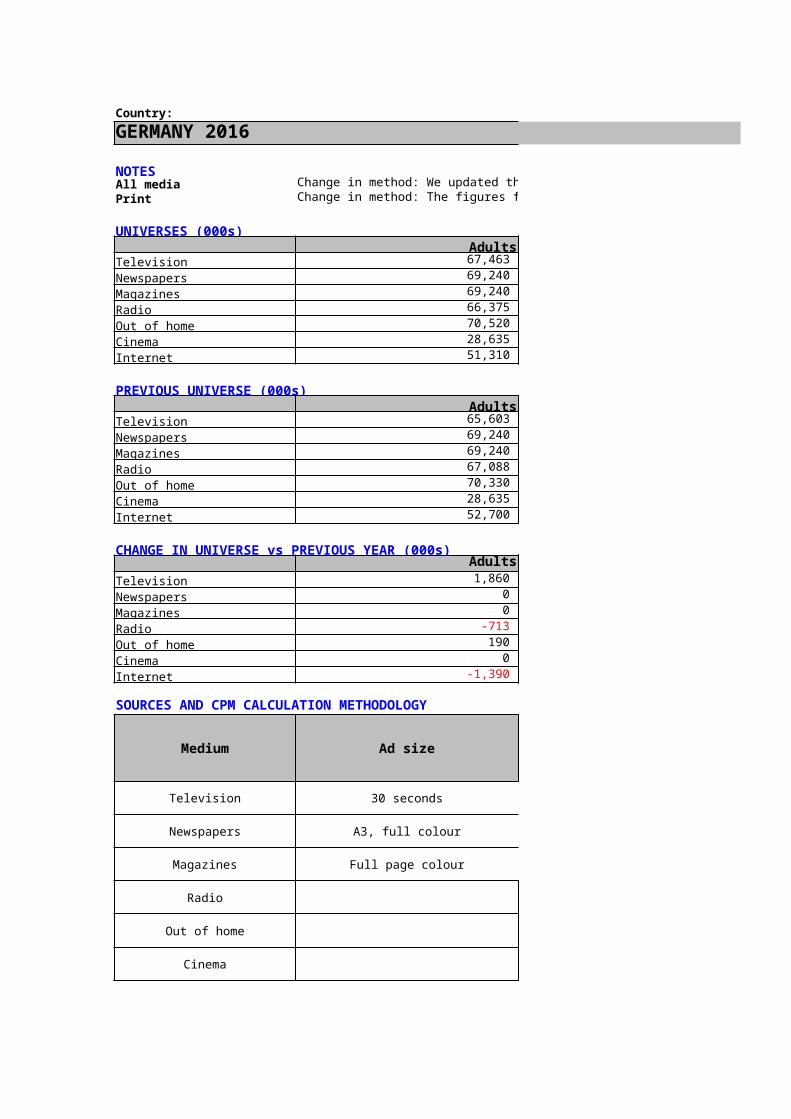

Country:GERMANY 2016

NOTESAll media Change in method: We updated the discounts corresponding to our inflation spending ticker. The figures are not comparable to 2014Print Change in method: The figures for Newspapers are on 1.000er page corner and full colour.

UNIVERSES (000s)Adults Men

Television 67,463 32,748 Newspapers 69,240 33,810 Magazines 69,240 33,810 Radio 66,375 32,349 Out of home 70,520 34,590 Cinema 28,635 14,727 Internet 51,310 26,590

PREVIOUS UNIVERSE (000s)Adults Men

Television 65,603 32,030 Newspapers 69,240 33,810 Magazines 69,240 33,810 Radio 67,088 32,809 Out of home 70,330 34,460 Cinema 28,635 14,727 Internet 52,700 27,500

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 1,860 718 Newspapers 0 0 Magazines 0 0 Radio -713 -460 Out of home 190 130 Cinema 0 0 Internet -1,390 -910

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds AGF GFK TV Scope

Newspapers A3, full colour MA Presse I 2016

Magazines Full page colour MA Presse I 2016

Radio

Out of home

Cinema

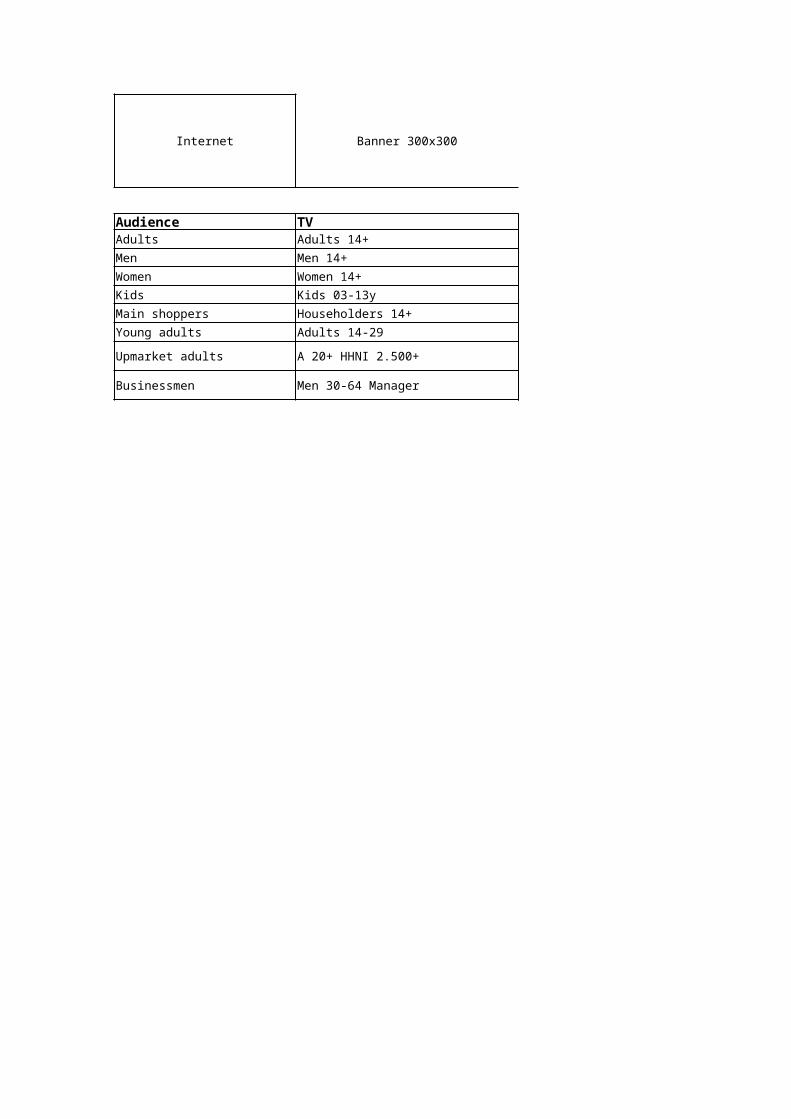

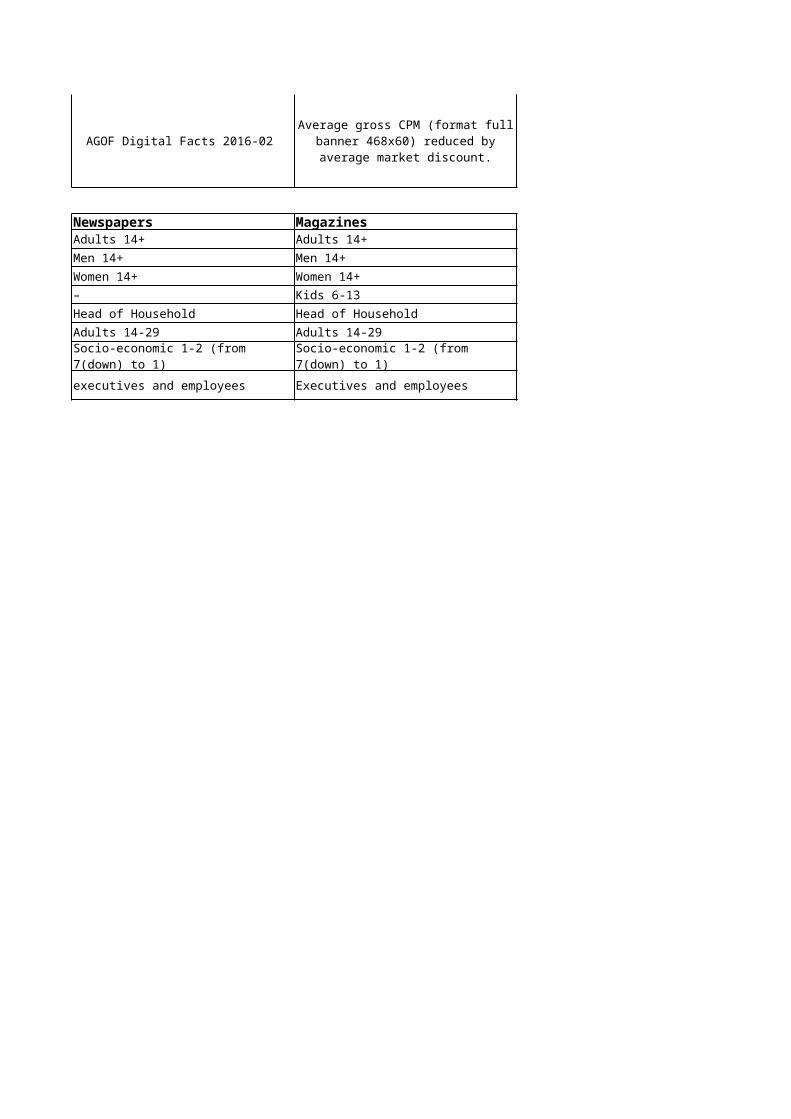

Internet Banner 300x300 AGOF Digital Facts 2016-02

Audience TV NewspapersAdults Adults 14+ Adults 14+Men Men 14+ Men 14+Women Women 14+ Women 14+Kids Kids 03-13y –Main shoppers Householders 14+ Head of HouseholdYoung adults Adults 14-29 Adults 14-29

Upmarket adults A 20+ HHNI 2.500+

Businessmen Men 30-64 Manager executives and employees

Socio-economic 1-2 (from 7(down) to 1)

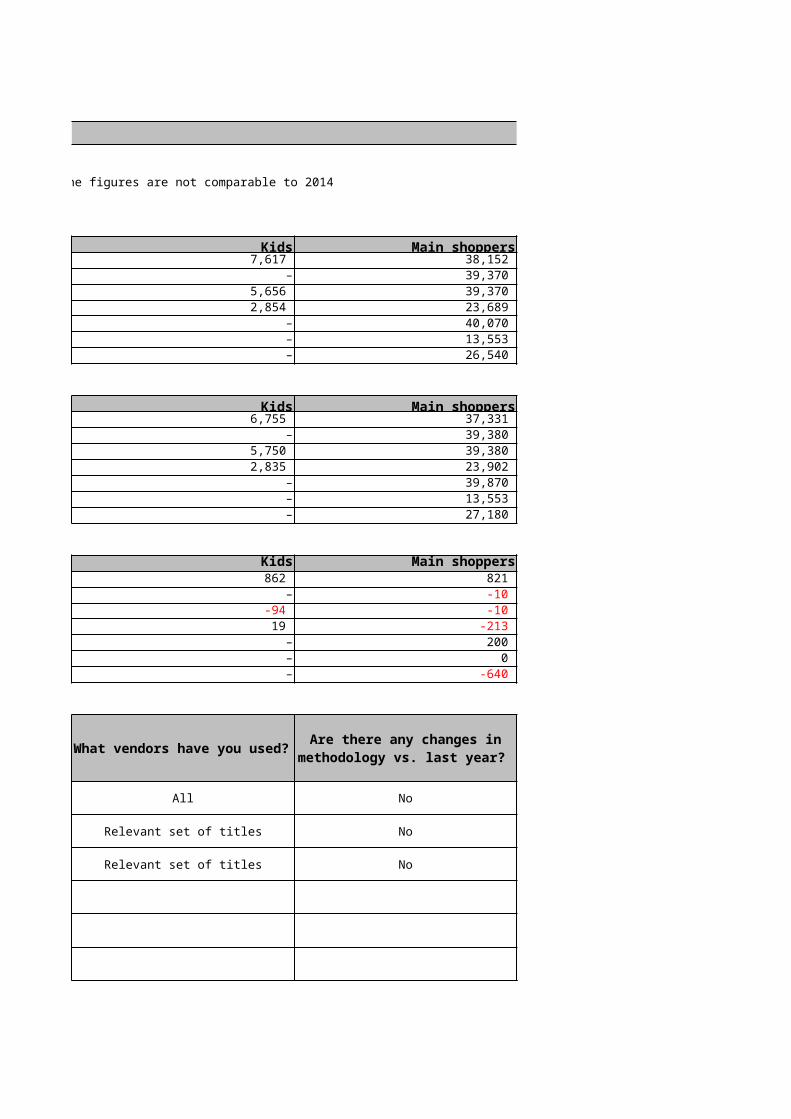

GERMANY 2016

Change in method: We updated the discounts corresponding to our inflation spending ticker. The figures are not comparable to 2014Change in method: The figures for Newspapers are on 1.000er page corner and full colour.

Women Kids Main shoppers 34,714 7,617 38,152 35,430 – 39,370 35,430 5,656 39,370 34,027 2,854 23,689 35,930 – 40,070 13,908 – 13,553 24,720 – 26,540

Women Kids Main shoppers 33,573 6,755 37,331 35,430 – 39,380 35,430 5,750 39,380 34,280 2,835 23,902 35,860 – 39,870 13,908 – 13,553 25,210 – 27,180

Women Kids Main shoppers1,141 862 821

0 – -10 0 -94 -10

-253 19 -213 70 – 200 0 – 0

-490 – -640

All No

1.0000er page corner Relevant set of titles No

full page Relevant set of titles No

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

9 main stations 06 - 01 oclock 30"

Magazines Radio CinemaAdults 14+Men 14+Women 14+Kids 6-13 – Head of Household Householders 20-59 Head of HouseholdAdults 14-29 Adults 18-29 Adults 14-29

Executives and employees Executives and employees

Average gross CPM (format full banner 468x60) reduced by average market discount.

Average CPM of top 200 sites by reach

Yes, AGOF now integrated Mobile Reach figures. So now it is "digital facts" instead of "internet facts". CPTs are not compareable to

2015.

Adults 14+ Adults 14+Men 14+ Men 14+Women 14+ Women 14+All 10-13

Socio-economic 1-2 (from 7(down) to 1)

Adults 20-59 Household net income Euro 2.500+

Adults 20+ Household net income Euro 2.500+Executives, self-employed, freelancers

GERMANY 2016

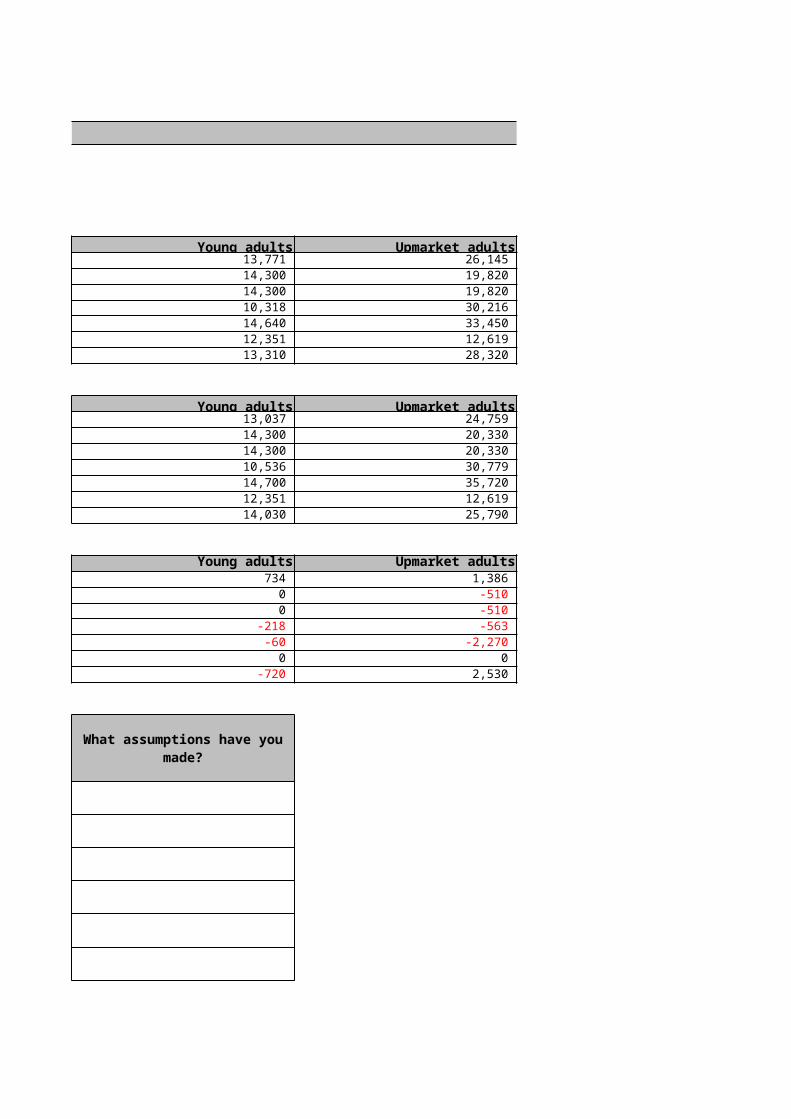

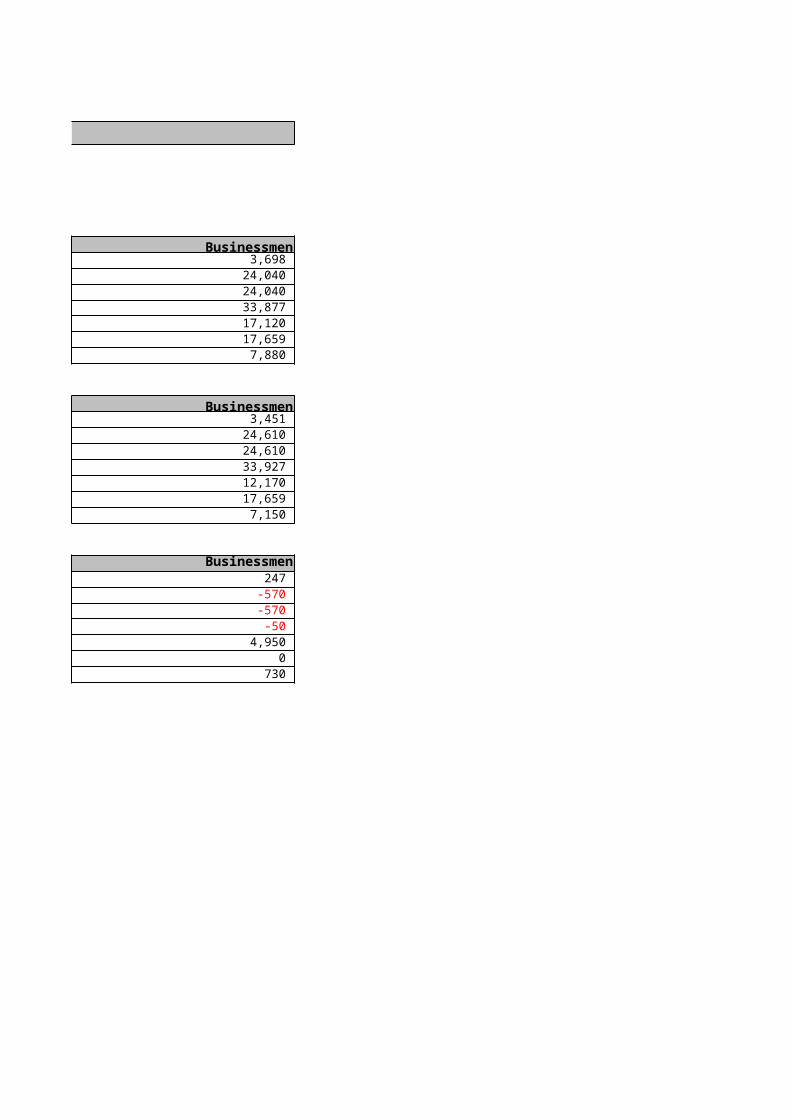

Young adults Upmarket adults Businessmen 13,771 26,145 3,698 14,300 19,820 24,040 14,300 19,820 24,040 10,318 30,216 33,877 14,640 33,450 17,120 12,351 12,619 17,659 13,310 28,320 7,880

Young adults Upmarket adults Businessmen 13,037 24,759 3,451 14,300 20,330 24,610 14,300 20,330 24,610 10,536 30,779 33,927 14,700 35,720 12,170 12,351 12,619 17,659 14,030 25,790 7,150

Young adults Upmarket adults Businessmen734 1,386 247

0 -510 -570 0 -510 -570

-218 -563 -50 -60 -2,270 4,950

0 0 0 -720 2,530 730

What assumptions have you made?

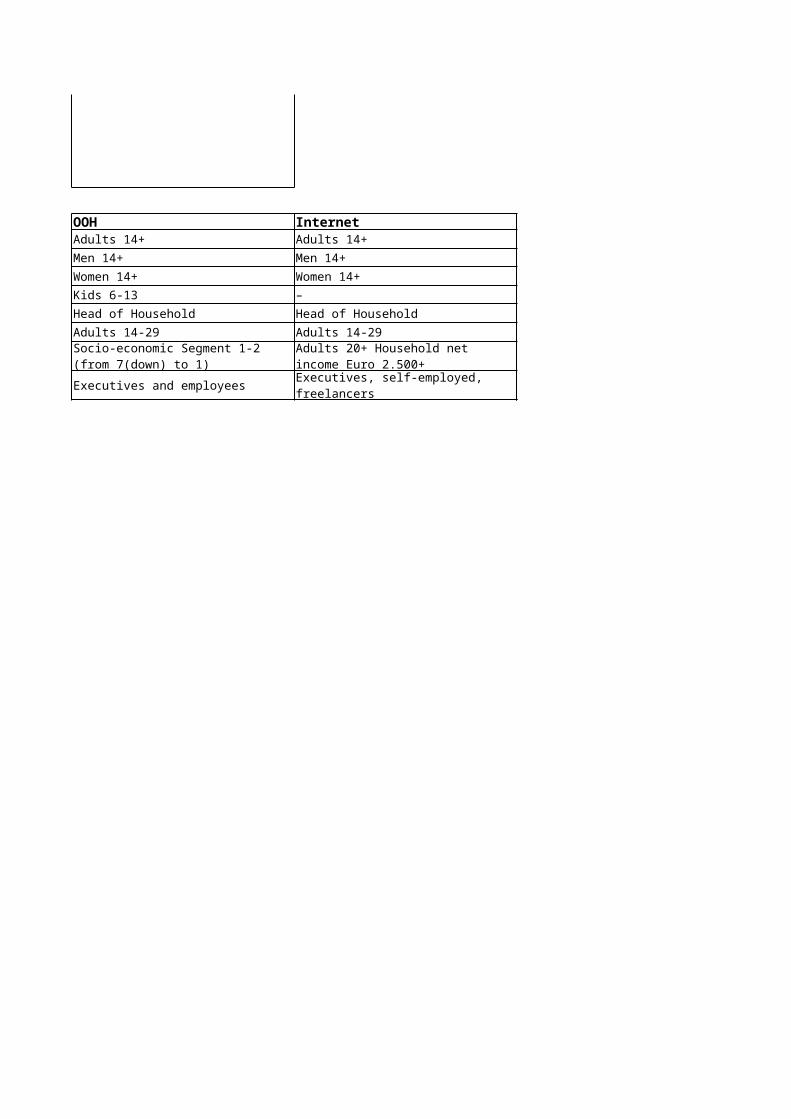

OOH InternetAdults 14+ Adults 14+Men 14+ Men 14+Women 14+ Women 14+Kids 6-13 –Head of Household Head of HouseholdAdults 14-29 Adults 14-29

Executives and employees

Socio-economic Segment 1-2 (from 7(down) to 1)

Adults 20+ Household net income Euro 2.500+Executives, self-employed, freelancers

Country:

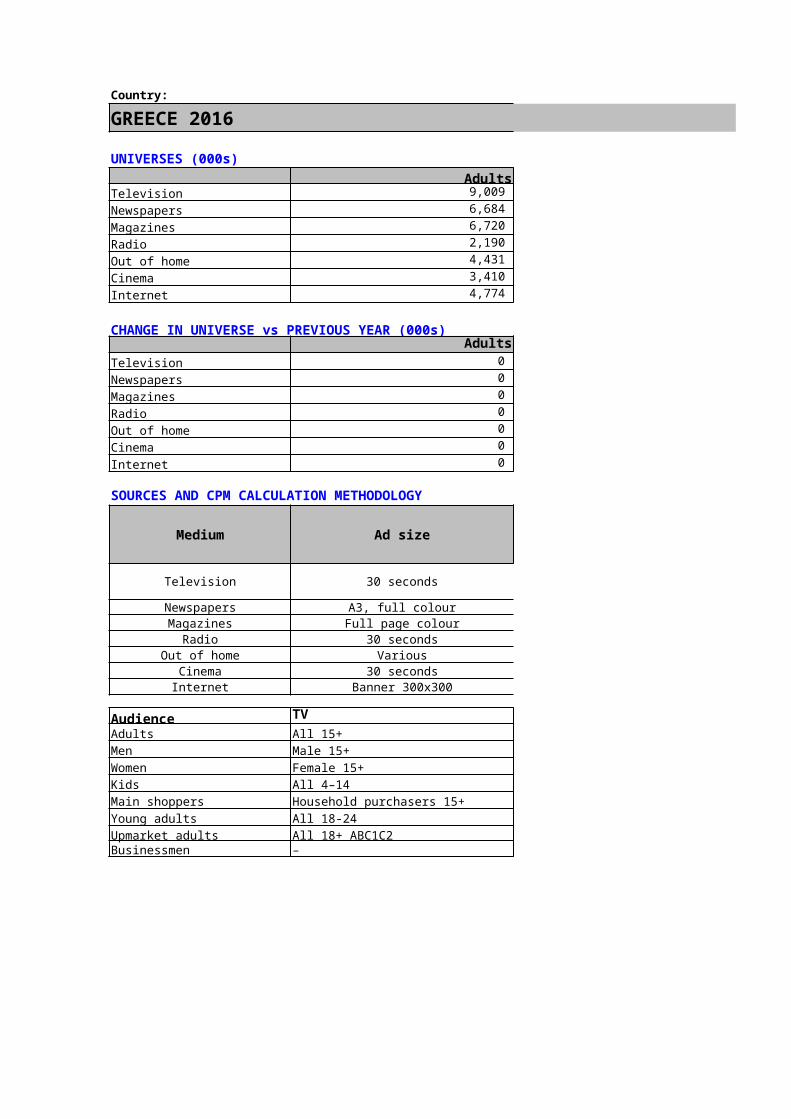

GREECE 2016

UNIVERSES (000s)Adults Men

Television 9,009 4,354 Newspapers 6,684 3,289 Magazines 6,720 3,304 Radio 2,190 1,137 Out of home 4,431 2,227 Cinema 3,410 1,653 Internet 4,774 2,516

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 0 0 Newspapers 0 0 Magazines 0 0 Radio 0 0 Out of home 0 0 Cinema 0 0 Internet 0 0

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds Nielsen Audience Measurement

Newspapers A3, full colour –Magazines Full page colour –

Radio 30 seconds –Out of home Various –

Cinema 30 seconds –Internet Banner 300x300 –

Audience TV OOHAdults All 15+ All 18-64Men Male 15+ Male 18-64Women Female 15+ Female 18-64Kids All 4–14 –Main shoppers Household purchasers 15+ Household purchasers 18-64Young adults All 18-24 All 18-24Upmarket adults All 18+ ABC1C2 All 18+ ABC1C2Businessmen – –

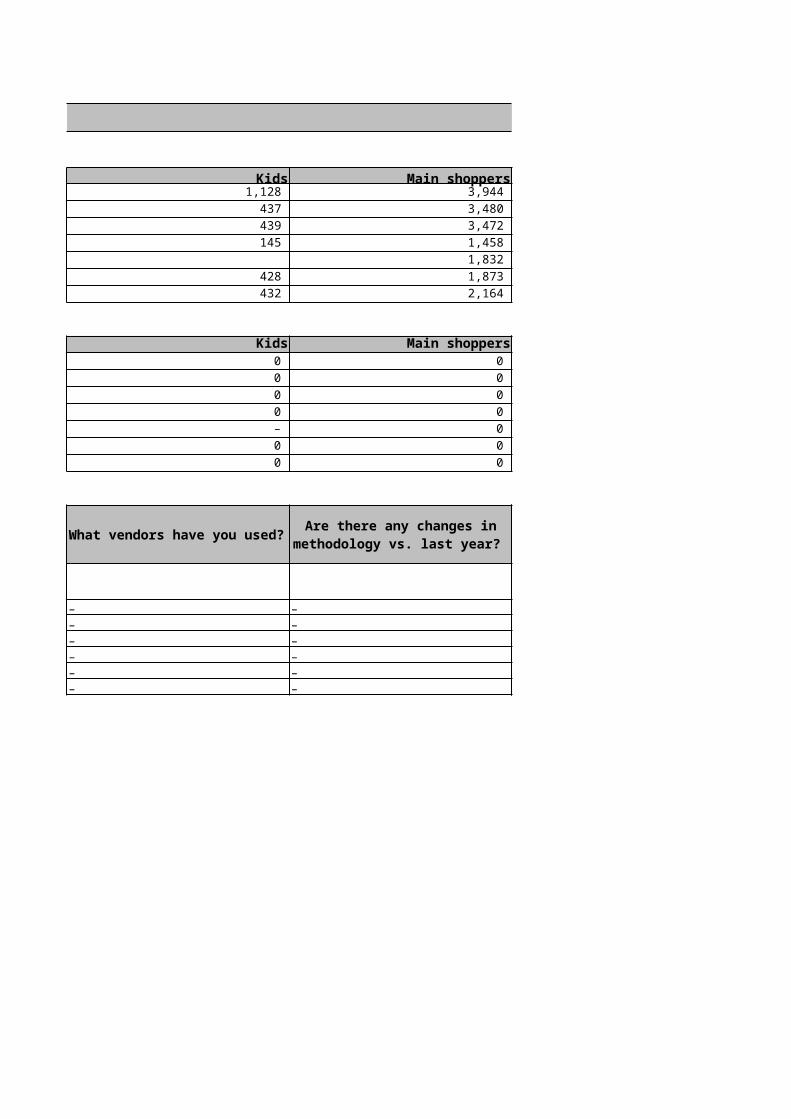

GREECE 2016

Women Kids Main shoppers 4,654 1,128 3,944 3,395 437 3,480 3,417 439 3,472 1,053 145 1,458 2,205 1,832 1,757 428 1,873 2,259 432 2,164

Women Kids Main shoppers0 0 0 0 0 0 0 0 0 0 0 0 0 – 0 0 0 0 0 0 0

– – –– – –– – –– – –– – –– – –

All other mediaAll 18-70Male 18-70Female 18-70All 13-17Household purchasers 18-70All 18-24All 18+ ABC1C2–

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

CPR per sec *100*30 /target universe population

GREECE 2016

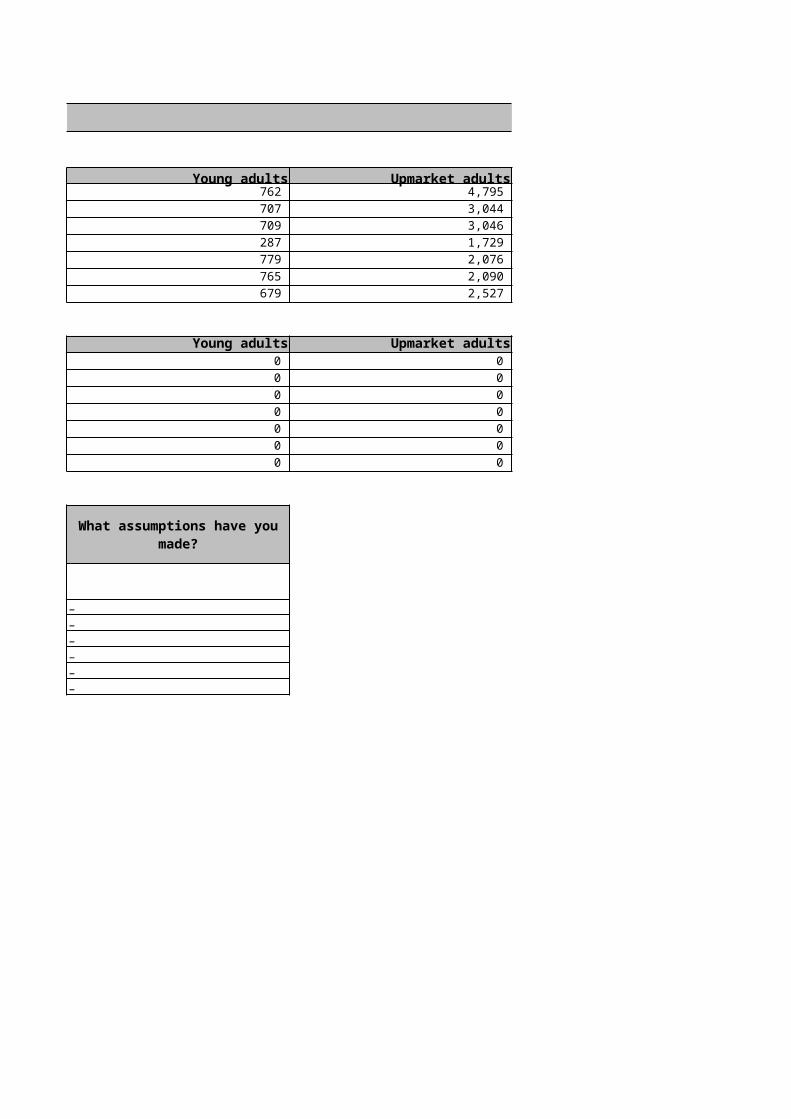

Young adults Upmarket adults Businessmen 762 4,795 – 707 3,044 – 709 3,046 – 287 1,729 – 779 2,076 – 765 2,090 – 679 2,527 –

Young adults Upmarket adults Businessmen0 0 – 0 0 – 0 0 – 0 0 – 0 0 – 0 0 – 0 0 –

––––––

What assumptions have you made?

`

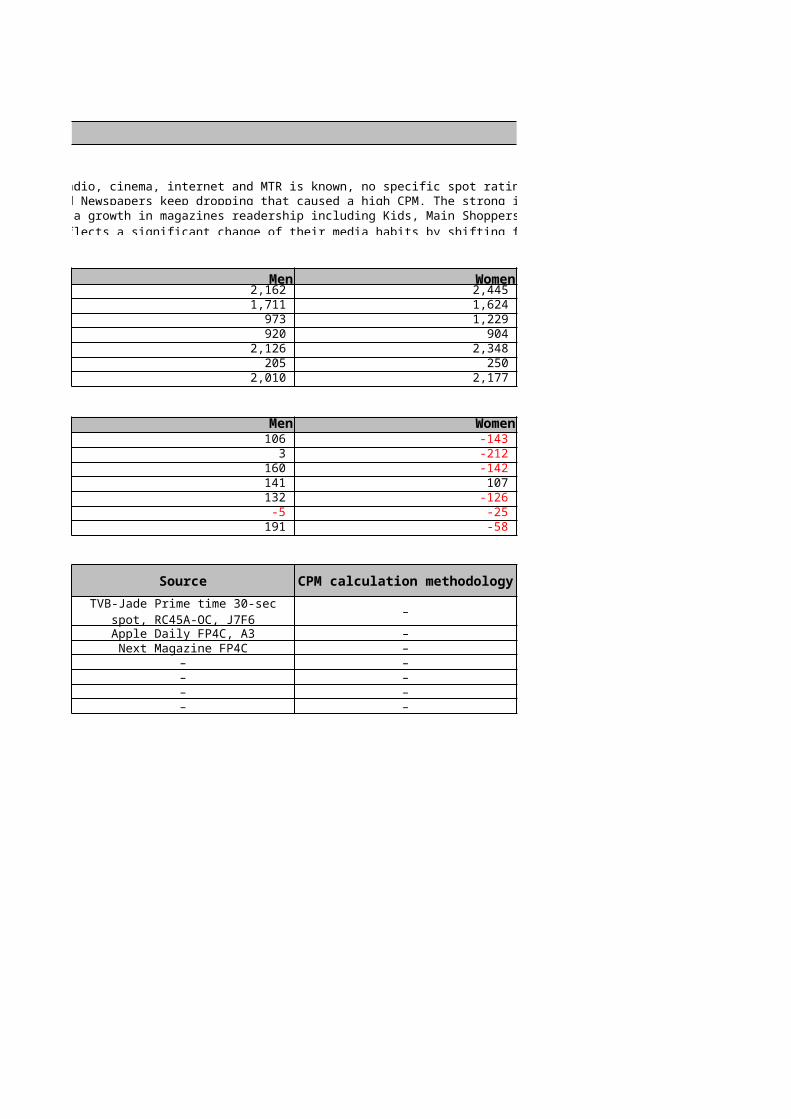

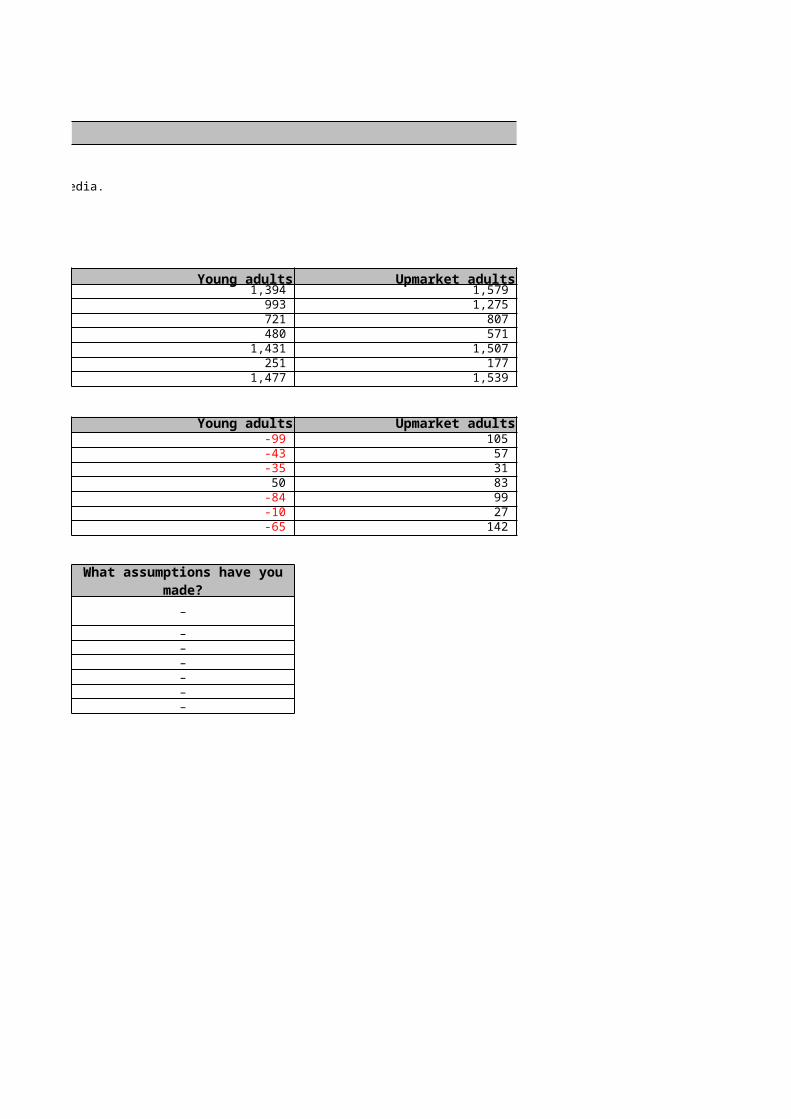

Country:HONG KONG 2016

NOTESGeneral While overall penetration of radio, cinema, internet and MTR is known, no specific spot rating is available. Therefore, CPM cannot be provided for these media.TV/Newspapers The media consumption of TV and Newspapers keep dropping that caused a high CPM. The strong inflation is due to this drop in target consumption on TV and NewspaperMagazines

UNIVERSES (000s)Err:509 Men

Television 4,607 2,162 Newspapers 3,336 1,711 Magazines 2,201 973 Radio 1,825 920 Out of home 4,474 2,126 Cinema 456 205 Internet 4,186 2,010

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television -37 106 Newspapers -208 3 Magazines 17 160 Radio 250 141 Out of home 7 132 Cinema -29 -5 Internet 132 191

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds

Newspapers A3, full colour Apple Daily FP4C, A3Magazines Full page colour Next Magazine FP4C

Radio 30 seconds –Out of home Various –

Cinema 30 seconds –Internet Banner 300x300 –

Audience All available mediaAdults People 18-64Men Male 18-64Women Female 18-64Kids Parents with Kids 4-15Main shoppers Shopping Decision MakersYoung adults People 18-34Upmarket adults People 18-64, MHI$40K+Businessmen PMEPT

Several target groups recorded a growth in magazines readership including Kids, Main Shoppers and Businessmen while the magazine readership of Young Adults keep dropping. That reflects a significant change of their media habits by shifting from Offline to Online media.

TVB-Jade Prime time 30-sec spot, RC45A-OC, J7F6

HONG KONG 2016

While overall penetration of radio, cinema, internet and MTR is known, no specific spot rating is available. Therefore, CPM cannot be provided for these media.The media consumption of TV and Newspapers keep dropping that caused a high CPM. The strong inflation is due to this drop in target consumption on TV and Newspaper

Women Kids Main shoppers 2,445 1,167 2,742 1,624 804 1,948 1,229 614 1,493 904 437 1,157 2,348 1,116 2,642 250 123 271 2,177 1,161 2,435

Women Kids Main shoppers-143 150 339 -212 100 116 -142 75 209 107 75 221

-126 175 386 -25 30 45 -58 183 439

– – –

– – –– – –– – –– – –– – –– – –

Several target groups recorded a growth in magazines readership including Kids, Main Shoppers and Businessmen while the magazine readership of Young Adults keep dropping. That reflects a significant change of their media habits by shifting from Offline to Online media.

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

HONG KONG 2016

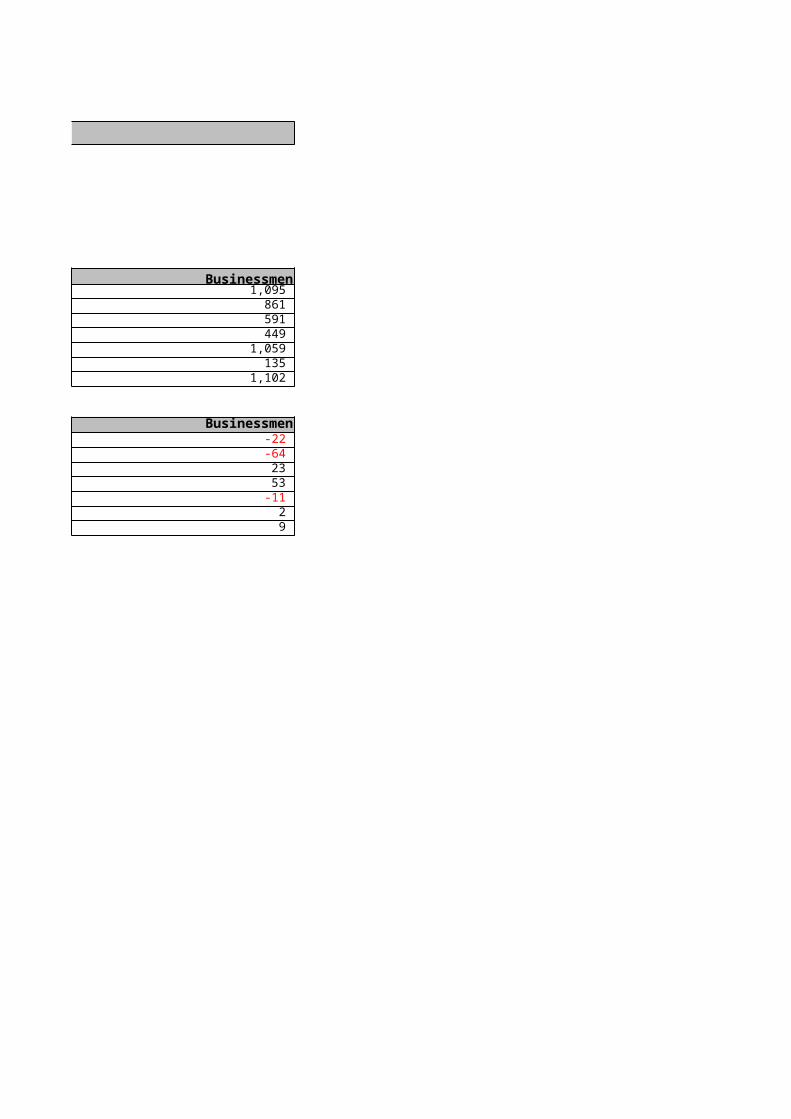

Young adults Upmarket adults Businessmen 1,394 1,579 1,095 993 1,275 861 721 807 591 480 571 449 1,431 1,507 1,059 251 177 135 1,477 1,539 1,102

Young adults Upmarket adults Businessmen-99 105 -22 -43 57 -64 -35 31 23 50 83 53

-84 99 -11 -10 27 2 -65 142 9

–

––––––

What assumptions have you made?

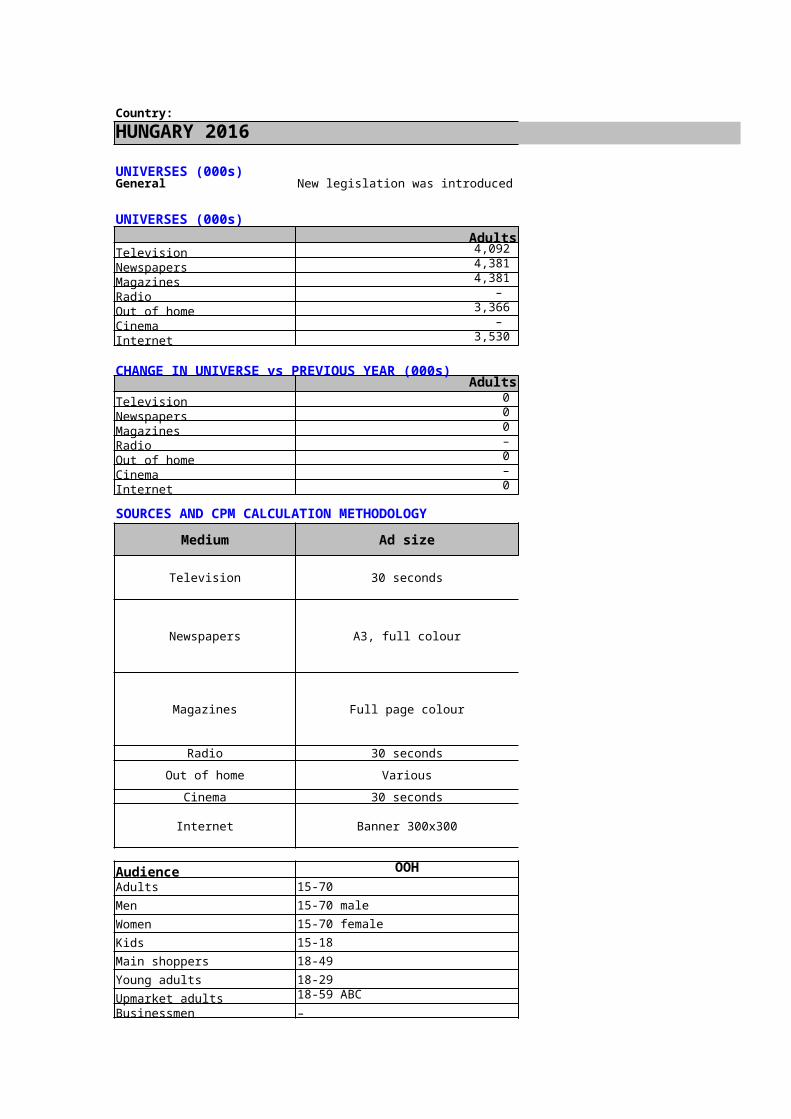

Country:HUNGARY 2016

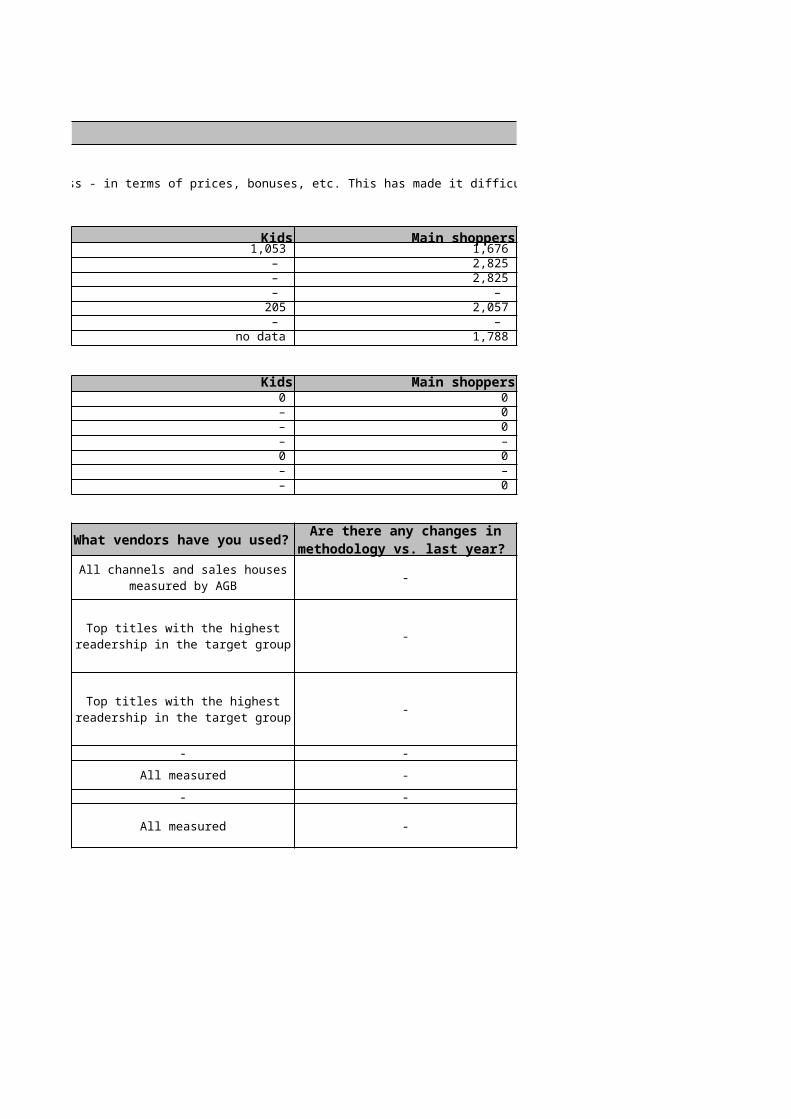

UNIVERSES (000s)General New legislation was introduced in Hungary in 2015, which has affected our media buying process - in terms of prices, bonuses, etc. This has made it difficult to compare inflation figures in 2016 vs. 2015.

UNIVERSES (000s)Adults Men

Television 4,092 2,040 Newspapers 4,381 2,215 Magazines 4,381 2,215 Radio – – Out of home 3,366 1,598 Cinema – – Internet 3,530 1,701

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 0 0 Newspapers 0 0 Magazines 0 0 Radio – – Out of home 0 0 Cinema – – Internet 0 0

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds AGB Hungary

Newspapers A3, full colour TGI/NOK

Magazines Full page colour TGI/NOK

Radio 30 seconds No source

Out of home Various SzondaIpsos

Cinema 30 seconds No source

Internet Banner 300x300 Gemius and OMG estimations

Audience OOH All other mediaAdults 15-70 A 18-49Men 15-70 male 18-49 maleWomen 15-70 female 18-49 femaleKids 15-18 CHD4-14Main shoppers 18-49 MS18-49Young adults 18-29 A18-29Upmarket adults 18-59 ABC A18-59 AB (p)Businessmen – A25-59 Manager, self-employed

HUNGARY 2016

New legislation was introduced in Hungary in 2015, which has affected our media buying process - in terms of prices, bonuses, etc. This has made it difficult to compare inflation figures in 2016 vs. 2015.

Women Kids Main shoppers 2,051 1,053 1,676 2,166 – 2,825 2,166 – 2,825

– – – 1,768 205 2,057

– – – 1,830 no data 1,788

Women Kids Main shoppers0 0 0 0 – 0 0 – 0 – – – 0 0 0 – – – 0 – 0

-

-

-

- - -

All measured -

- - -

All measured -

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

Total yearly net investment divided by the total number of EQ GRP delivered in that certain year.

All channels and sales houses measured by AGB

Calculation is based on an average campaign's (based on the top titles by target audiance) net

budget (OMG estimation) and this campaign's reach%

Top titles with the highest readership in the target group

Calculation is based on an average campaign's (based on the top titles by target audiance) net

budget (OMG estimation) and this campaign's reach%

Top titles with the highest readership in the target group

Calculation is made by our outdoor specilist, Odex (as every

year)

Average campain's budget divided by the universe of the given

audience

HUNGARY 2016

New legislation was introduced in Hungary in 2015, which has affected our media buying process - in terms of prices, bonuses, etc. This has made it difficult to compare inflation figures in 2016 vs. 2015.

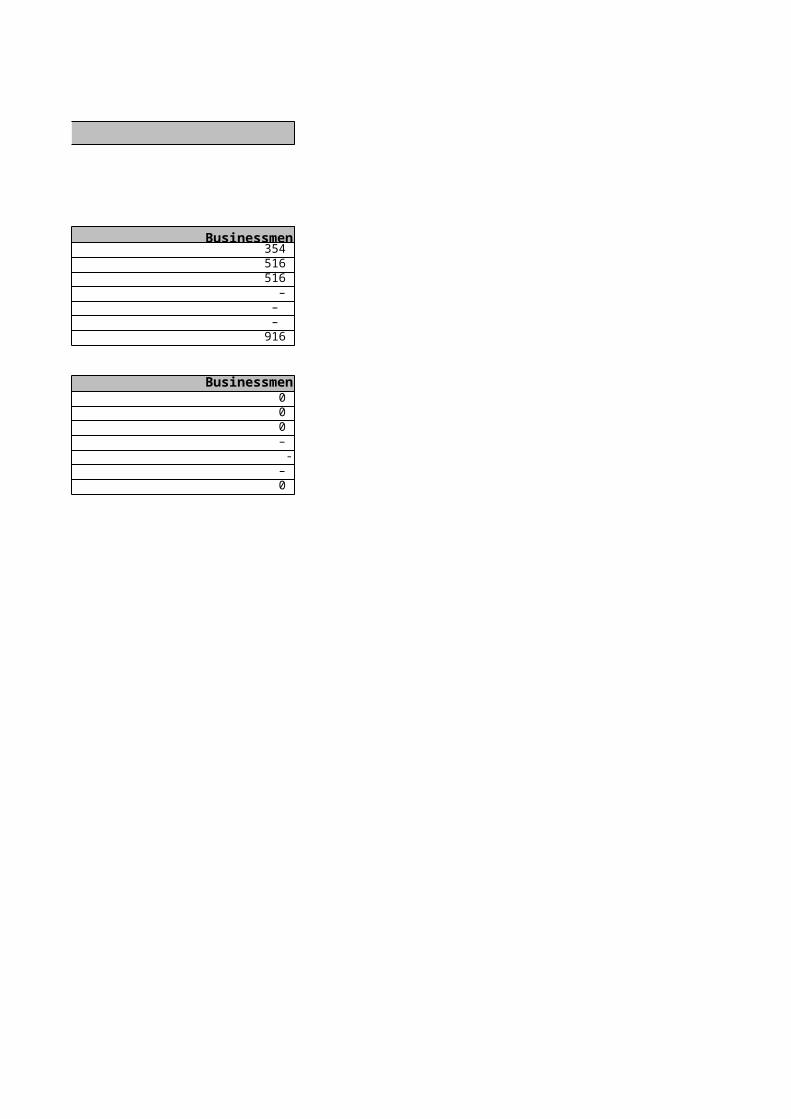

Young adults Upmarket adults Businessmen 1,322 2,513 354 1,472 1,211 516 1,472 1,211 516

– – – 720 1,985 –

– – – 1,518 1,195 916

Young adults Upmarket adults Businessmen0 0 0 0 0 0 0 0 0 – – – 0 0 - – – – 0 0 0

-

-

-

-

-

What assumptions have you made?

Country:INDONESIA 2016

NOTESGeneral

UNIVERSES (000s)Adults Men

Television 30,817 21,453 Newspapers 35,609 24,117 Magazines 35,609 24,117 Radio – – Out of home – – Cinema – – Internet – –

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 1,284 1,118 Newspapers 554 386 Magazines 554 386 Radio – –Out of home – –Cinema – –Internet – –

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds Arianna Nielsen

Newspapers 1/1 or JP full colour

Magazines Full page colour

Radio 30 seconds –Out of home Various –

Cinema 30 seconds –Internet Big banner –

Audience All available mediaAdults All 25+Men Male 15+Women Female 15+Kids All 5-9Main shoppers –Young adults All 20-24Upmarket adults –Businessmen –

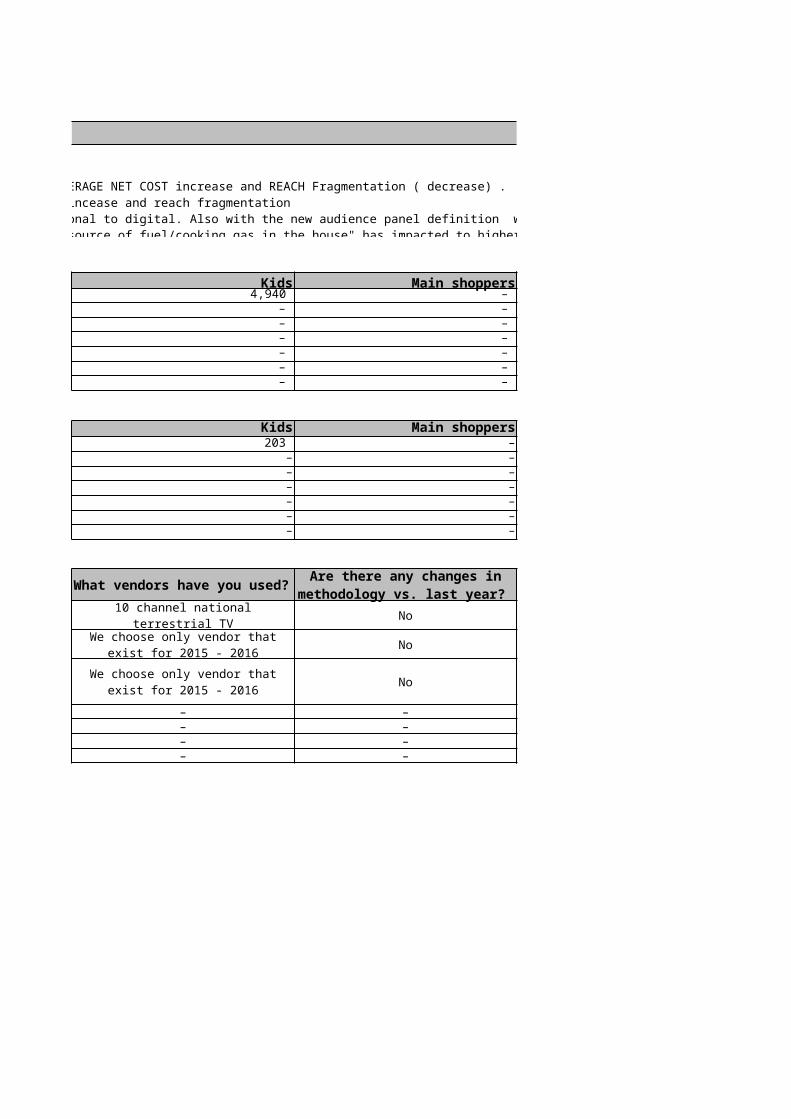

To ensure consistency, we're following the 2014 methodology, then adding on the Effect of AVERAGE NET COST increase and REACH Fragmentation ( decrease) . We're basing the COST and REACH Effect on FY projection, therefore tend to have some UP ( additional ) margin of cost incease and reach fragmentationThe higher inflation is caused by audience fragmentation, where audience shift from traditional to digital. Also with the new audience panel definition which changed from solely expenditure in the past but in 2016 also include "source of drinking water, electricity and source of fuel/cooking gas in the house" has impacted to higher inflation for overall target audience.

Nielsen Fusion, Readership or R&F

Nielsen Fusion, Readership or R&F

INDONESIA 2016

Women Kids Main shoppers 21,118 4,940 – 23,804 – – 23,804 – –

– – – – – – – – – – – –

Women Kids Main shoppers977 203 –375 – –375 – –

– – –– – –– – –– – –

10 channel national terrestrial TV No

No

No

– – –– – –– – –– – –

To ensure consistency, we're following the 2014 methodology, then adding on the Effect of AVERAGE NET COST increase and REACH Fragmentation ( decrease) . We're basing the COST and REACH Effect on FY projection, therefore tend to have some UP ( additional ) margin of cost incease and reach fragmentationThe higher inflation is caused by audience fragmentation, where audience shift from traditional to digital. Also with the new audience panel definition which changed from solely expenditure in the past but in 2016 also include "source of drinking water, electricity and source of fuel/cooking gas in the house" has impacted to higher inflation for overall target audience.

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

t sec cost (net after appliying the disc) divided by viewership (gross)

Net cost divided by gross impressions

We choose only vendor that exist for 2015 - 2016

Net cost divided by gross impressions

We choose only vendor that exist for 2015 - 2016

INDONESIA 2016

Young adults Upmarket adults Businessmen 5,937 – – 6,321 – – 6,321 – –

– – – – – – – – – – – –

Young adults Upmarket adults Businessmen680 – –

95 – –95 – –

– – –– – –– – –– – –

––––

To ensure consistency, we're following the 2014 methodology, then adding on the Effect of AVERAGE NET COST increase and REACH Fragmentation ( decrease) . We're basing the COST and REACH Effect

The higher inflation is caused by audience fragmentation, where audience shift from traditional to digital. Also with the new audience panel definition which changed from solely expenditure in the past but in

What assumptions have you made?

Only for the disc (by applying our regular disc in each channel)

We choose only the category that has highest spend within Jan Mar period (due to limitations of data, the software can not drilldown the

data for full year)

Country:

ITALY 2016

NOTESTV TV Business man inflaion is due to the growth of the Business Man universe in 2016. Print Smaller/cheaper print titles disappear from the market, hence average market price goes up.

UNIVERSES (000s)Adults Men

Television 52,335 25,136 Newspapers 52,993 25,488 Magazines 52,993 25,488 Radio 52,612 25,283 Out of home – – Cinema 52,993 – Internet 45,134 22,036

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 0 0 Newspapers 0 0 Magazines 0 0 Radio 0 0 Out of home – – Cinema – – Internet 1,738 433

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds Auditel/Nielsen

Newspapers A3, full colour Audipress/Nielsen

Magazines Full page colour Audipress/Nielsen

Radio 30 seconds Radiomonitor/Nielsen

Out of home Various Nielsen

Cinema 30 seconds Audimovie/Nielsen

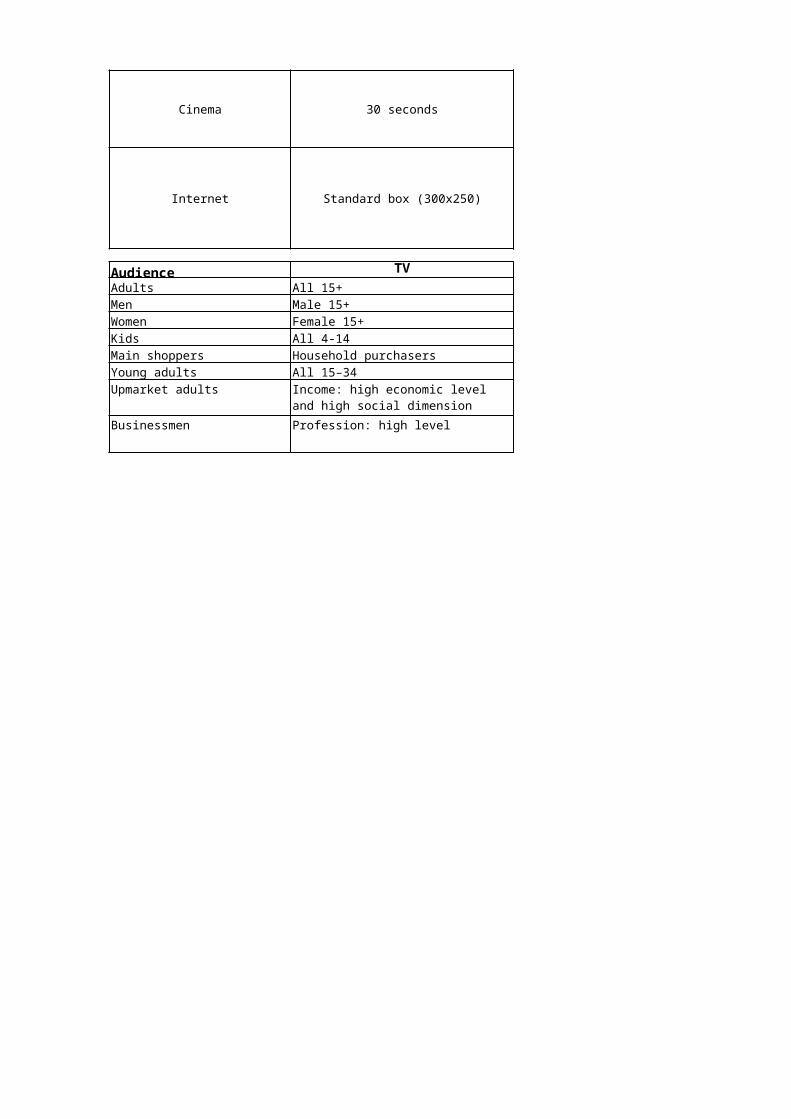

Internet Standard box (300x250)

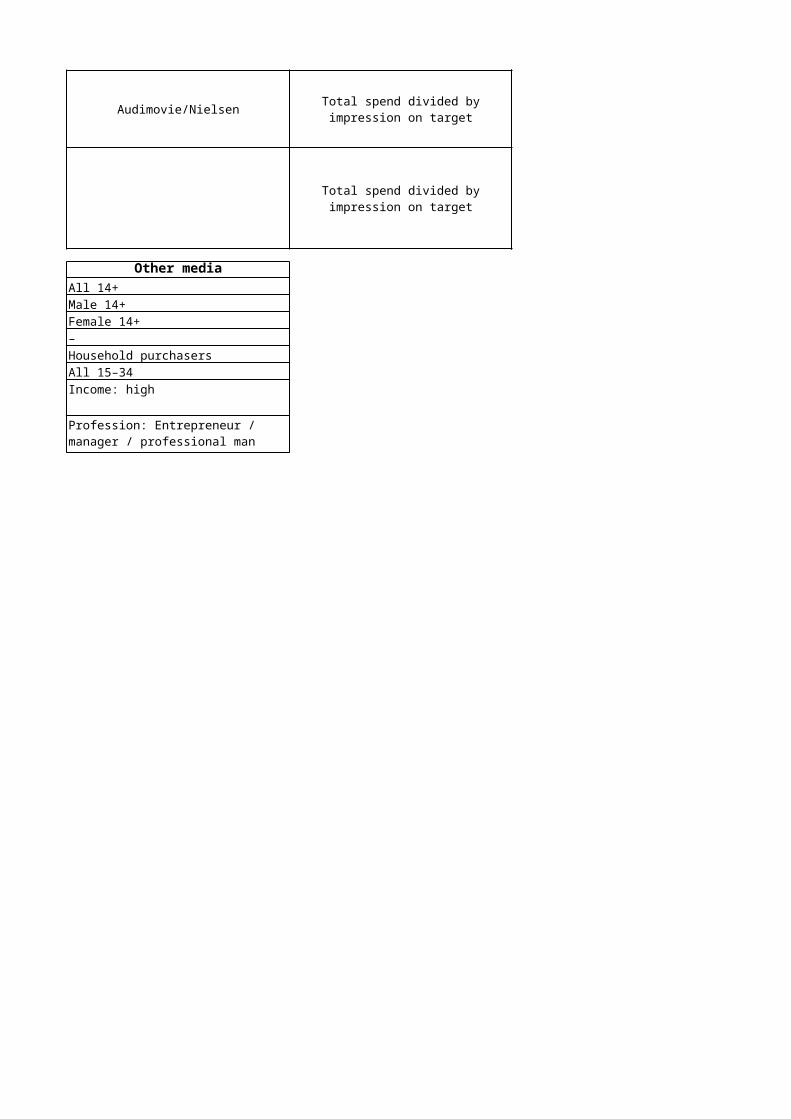

Audience TV Other mediaAdults All 15+ All 14+Men Male 15+ Male 14+Women Female 15+ Female 14+Kids All 4-14 –Main shoppers Household purchasers Household purchasersYoung adults All 15–34 All 15–34Upmarket adults Income: high

Businessmen Profession: high level

Income: high economic level and high social dimension

Profession: Entrepreneur / manager / professional man

ITALY 2016

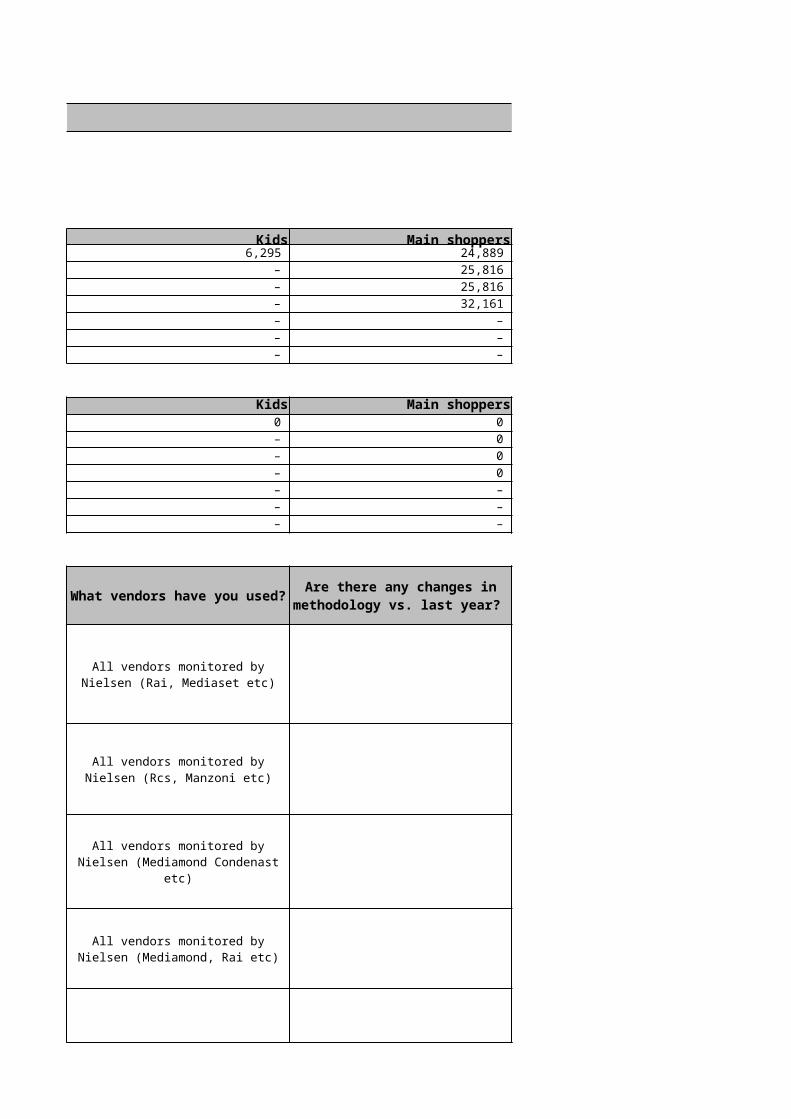

TV Business man inflaion is due to the growth of the Business Man universe in 2016. Smaller/cheaper print titles disappear from the market, hence average market price goes up.

Women Kids Main shoppers 27,198 6,295 24,889 27,505 – 25,816 27,505 – 25,816 27,329 – 32,161

– – – – – –

23,098 – –

Women Kids Main shoppers0 0 0 0 – 0 0 – 0 0 – 0 – – – – – –

1,305 – –

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

Total spend divided by impression on target

All vendors monitored by Nielsen (Rai, Mediaset etc)

Total spend divided by impression on target

All vendors monitored by Nielsen (Rcs, Manzoni etc)

Total spend divided by impression on target

All vendors monitored by Nielsen (Mediamond Condenast etc)

Total spend divided by impression on target

All vendors monitored by Nielsen (Mediamond, Rai etc)

Total spend divided by impression on target

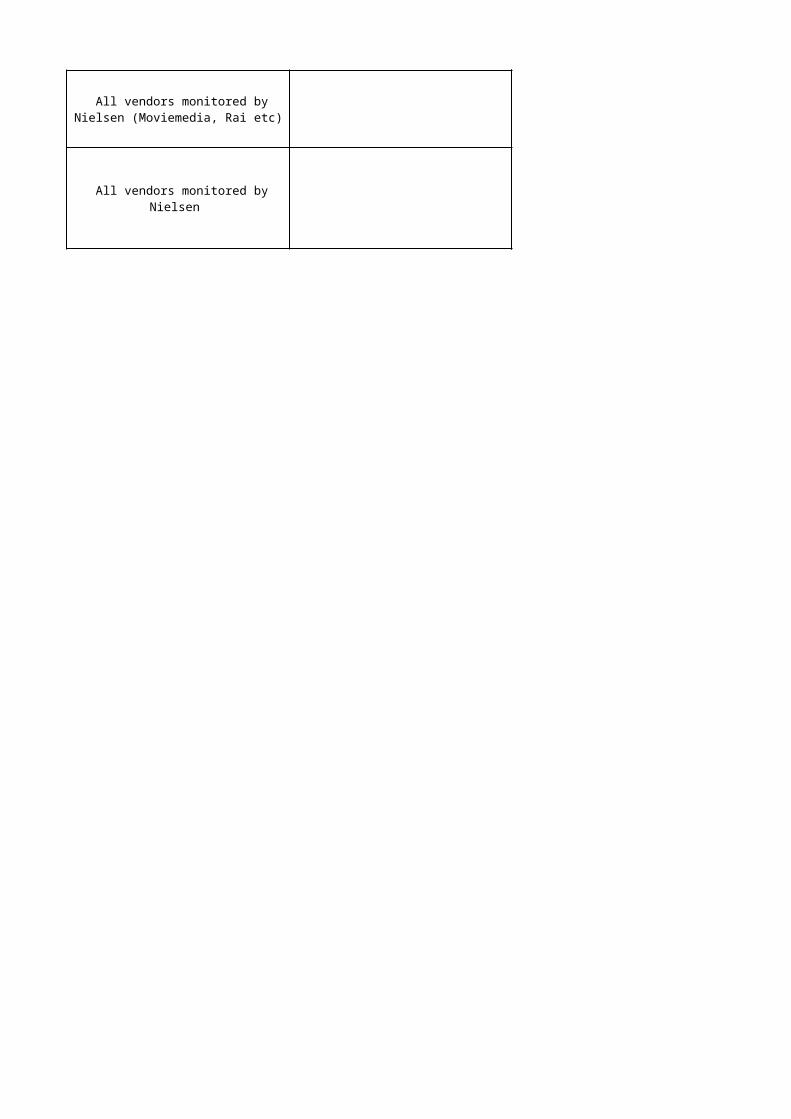

All vendors monitored by Nielsen (Moviemedia, Rai etc)

Total spend divided by impression on target All vendors monitored by Nielsen

ITALY 2016

Young adults Upmarket adults Businessmen 12,963 9,668 2,570 13,369 – – 13,369 – – 13,240 – 3,223

– – – – – – – – –

Young adults Upmarket adults Businessmen0 107 332

-83 – – -83 – –

0 – – – – – – – – – – –

What assumptions have you made?

While TV is struggling to increase investments after a 4-year crisis audience is suffering. For this

reason, there is an increase of cpt

Very tough time for press in Italy caused by a continuous reduction

of investments. Although readership is losing less than

previous years with a little increase for digital copies

Very tough time for press in Italy caused by a continuous reduction

of investments. Although readership is losing less than

previous years simple because today it is a smaller and faithful

target

Radio is stable, like in previous years. It is still a very important media for automotive and retail, and audience is mostly in by car

driving. Stable

2016 started with a great increase of audience do to Italian movies.

Therefore, cpm is decreasing

Increase of special and qualitative positions and programmatic planning is influencing media

inflation that is growing

Country:

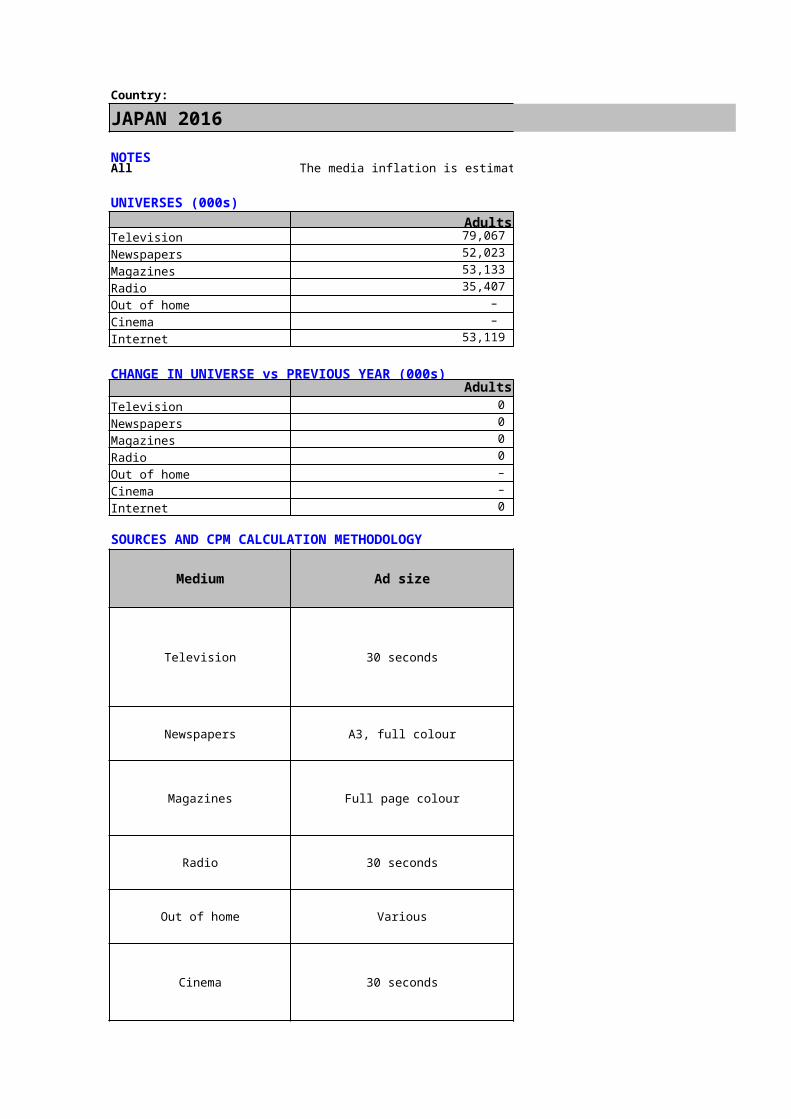

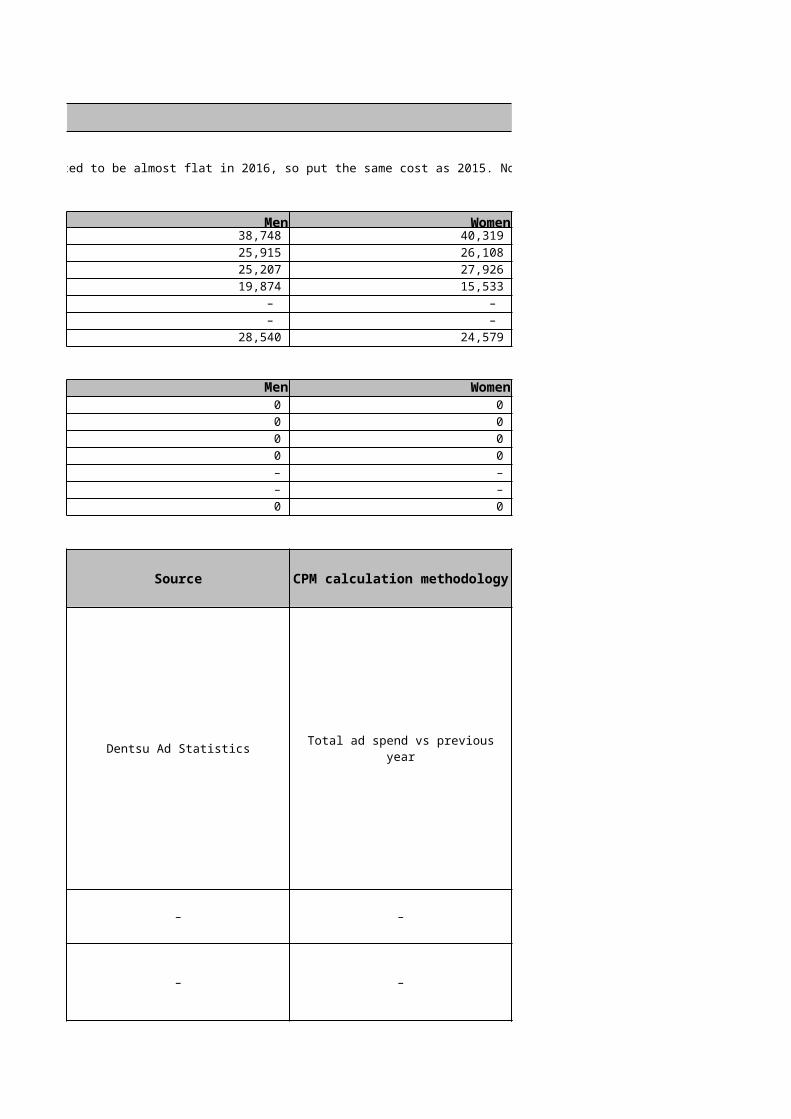

JAPAN 2016NOTESAll The media inflation is estimated to be almost flat in 2016, so put the same cost as 2015. Not change for the media reach, so the universe is not changed from 2015 figure.

UNIVERSES (000s)Adults Men

Television 79,067 38,748 Newspapers 52,023 25,915 Magazines 53,133 25,207 Radio 35,407 19,874 Out of home – – Cinema – – Internet 53,119 28,540

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 0 0 Newspapers 0 0 Magazines 0 0 Radio 0 0 Out of home – – Cinema – – Internet 0 0

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds

Dentsu Ad StatisticsNewspapers A3, full colour

Magazines Full page colour

Radio 30 seconds

Out of home Various –

Cinema 30 seconds –

Internet Standard box (300x250) Dentsu Ad Statistics

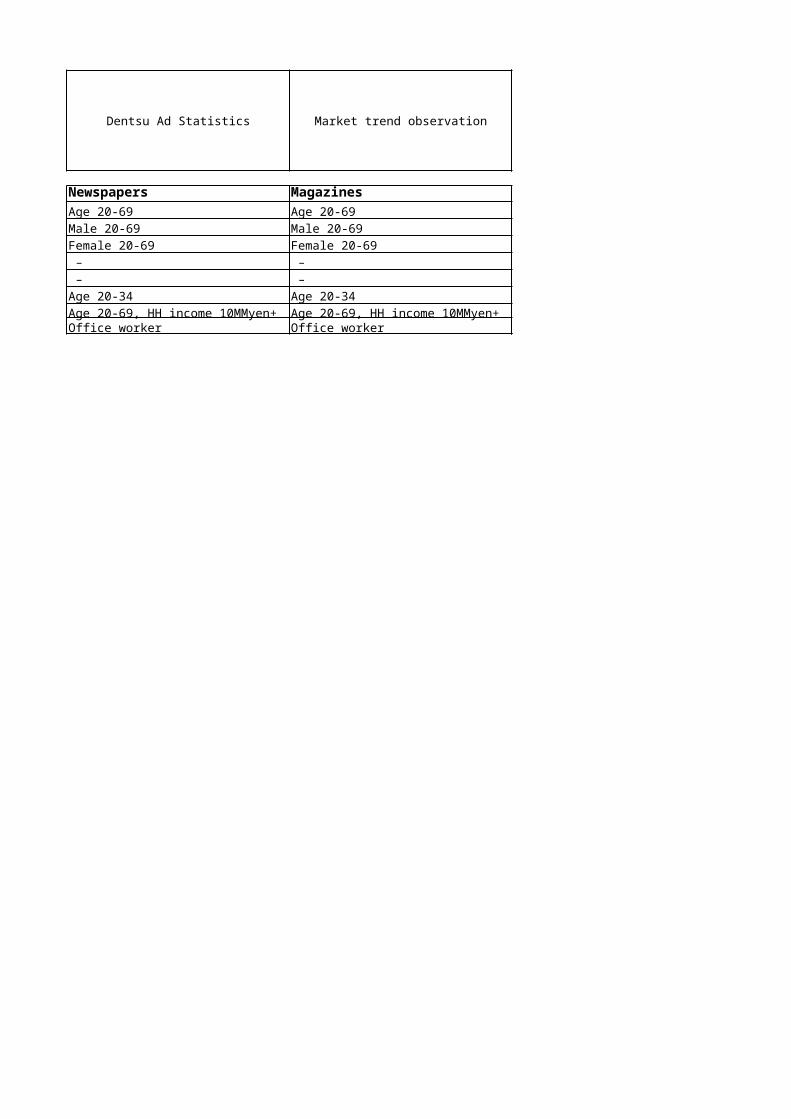

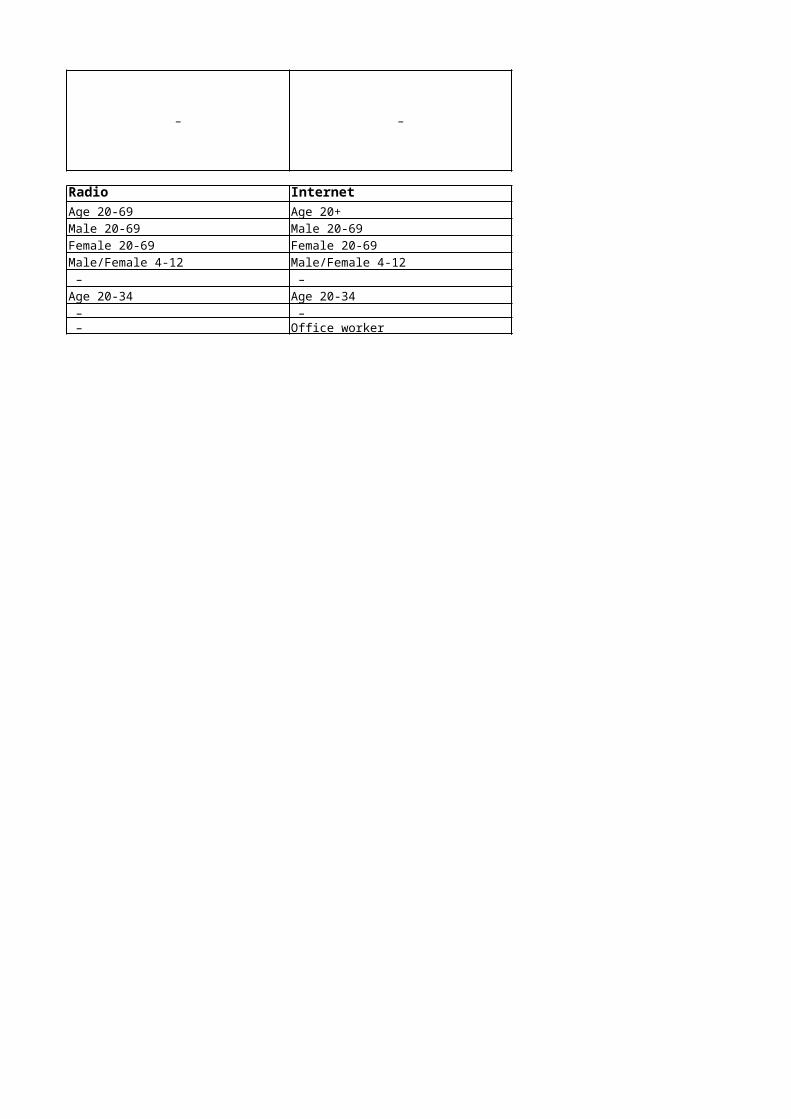

Audience Television NewspapersAdults Age 20-69 Age 20-69Men Male 20-69 Male 20-69Women Female 20-69 Female 20-69Kids Male/Female 4-12 – Main shoppers – – Young adults Age 20-34 Age 20-34Upmarket adults – Age 20-69, HH income 10MMyen+Businessmen – Office worker

JAPAN 2016

The media inflation is estimated to be almost flat in 2016, so put the same cost as 2015. Not change for the media reach, so the universe is not changed from 2015 figure.

Women Kids Main shoppers 40,319 – – 26,108 – – 27,926 – – 15,533 – –

– – – – – –

24,579 – –

Women Kids Main shoppers0 – – 0 – – 0 – – 0 – – – – – – – – 0 – –

Total ad spend vs previous year

– –

– –

– –

– –

– – –

– – –

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

Market trend observation – –

Magazines Radio InternetAge 20-69 Age 20-69 Age 20+Male 20-69 Male 20-69 Male 20-69Female 20-69 Female 20-69 Female 20-69 – Male/Female 4-12 Male/Female 4-12 – – – Age 20-34 Age 20-34 Age 20-34Age 20-69, HH income 10MMyen+ – – Office worker – Office worker

JAPAN 2016

Young adults Upmarket adults Businessmen 19,644 10,047 29,383 6,851 7,299 18,530 15,365 7,373 20,658 5,381 4,097 12,980

– – – – – –

17,138 7,257 22,384

Young adults Upmarket adults Businessmen0 0 0 0 0 0 0 0 0 0 0 0 – – – – – – 0 0 0

Ad spend is flat

–

–

What assumptions have you made?

Inflation: flat as both the demand and supply are increasing

Country:

KAZAKHSTAN 2016NOTESGeneral

UNIVERSES (000s)Adults Men

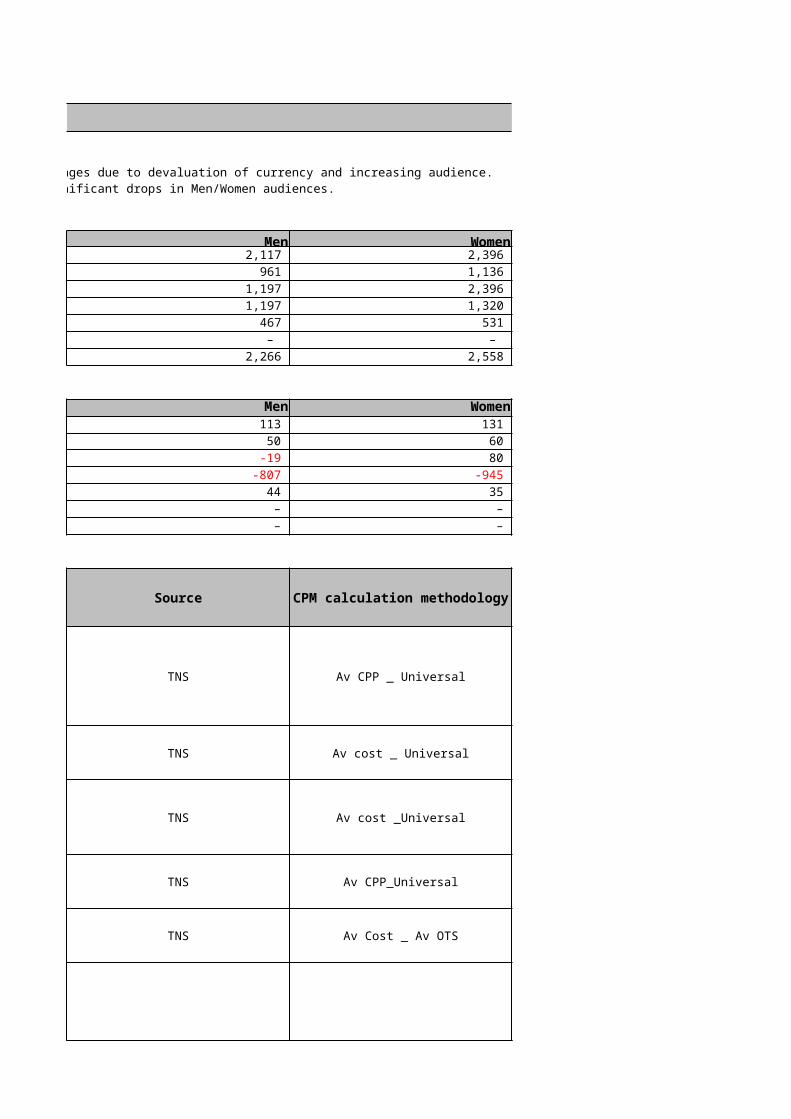

Television 5,763 2,117 Newspapers 5,763 961 Magazines 5,763 1,197 Radio 5,763 1,197 Out of home 1,154 467 Cinema – – Internet 4,824 2,266

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 304 113 Newspapers 199 50 Magazines 199 -19 Radio 304 -807 Out of home -12 44 Cinema – – Internet – –

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds TNS

Newspapers A3, full colour TNS

Magazines Full page colour TNS

Radio 30 seconds TNS

Out of home Various TNS

Cinema 30 seconds

Huge change in Print price changes due to devaluation of currency and increasing audience.Radio price changed due to significant drops in Men/Women audiences.

Internet Banner 468x60 TNS

Audience TV NewspapersAdults 18+ 18+Men 18-54 35-54Women 18-54 35-54Kids 6-15 6-15Main shoppers 20-64 25-64Young adults 20-25 20-25Upmarket adults 25-64 25-64Businessmen 25-54 20-44

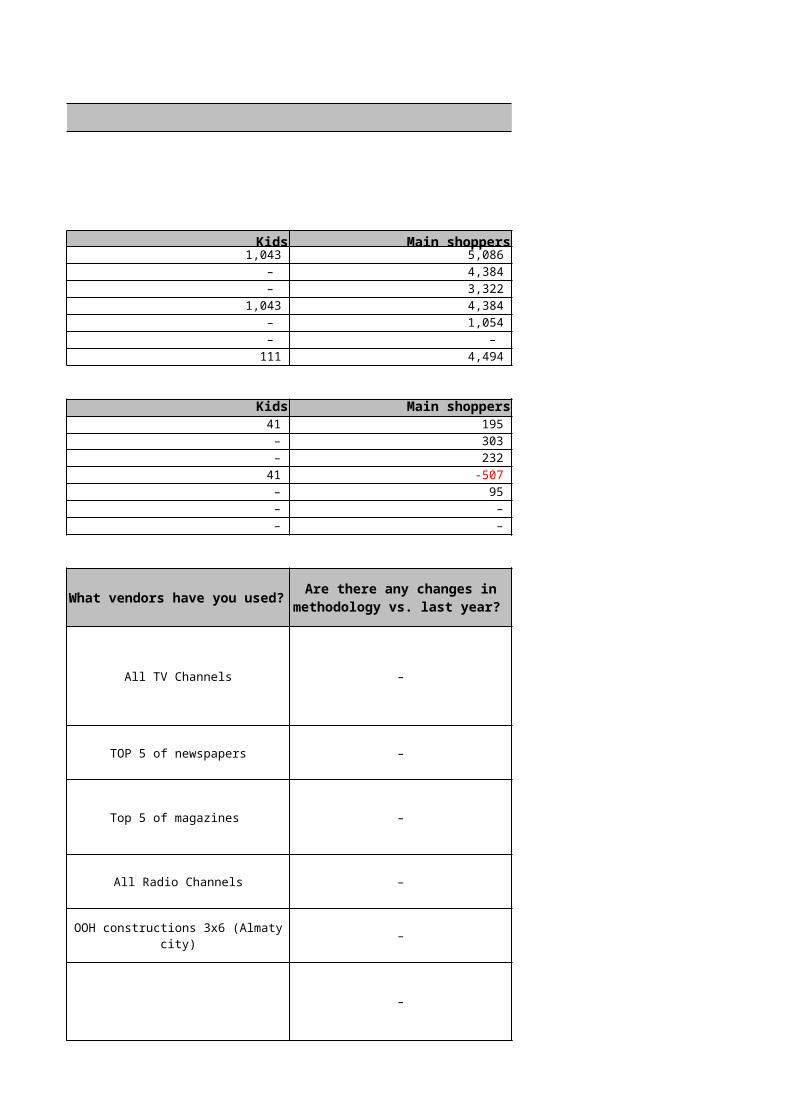

KAZAKHSTAN 2016

Women Kids Main shoppers 2,396 1,043 5,086 1,136 – 4,384 2,396 – 3,322 1,320 1,043 4,384 531 – 1,054

– – – 2,558 111 4,494

Women Kids Main shoppers131 41 195

60 – 303 80 – 232

-945 41 -507 35 – 95 – – – – – –

Av CPP _ Universal All TV Channels –

Av cost _ Universal ТОР 5 of newspapers –

Av cost _Universal Top 5 of magazines –

Av CPP_Universal All Radio Channels –

Av Cost _ Av OTS –

–

Huge change in Print price changes due to devaluation of currency and increasing audience.Radio price changed due to significant drops in Men/Women audiences.

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

OOH constructions 3х6 (Almaty city)

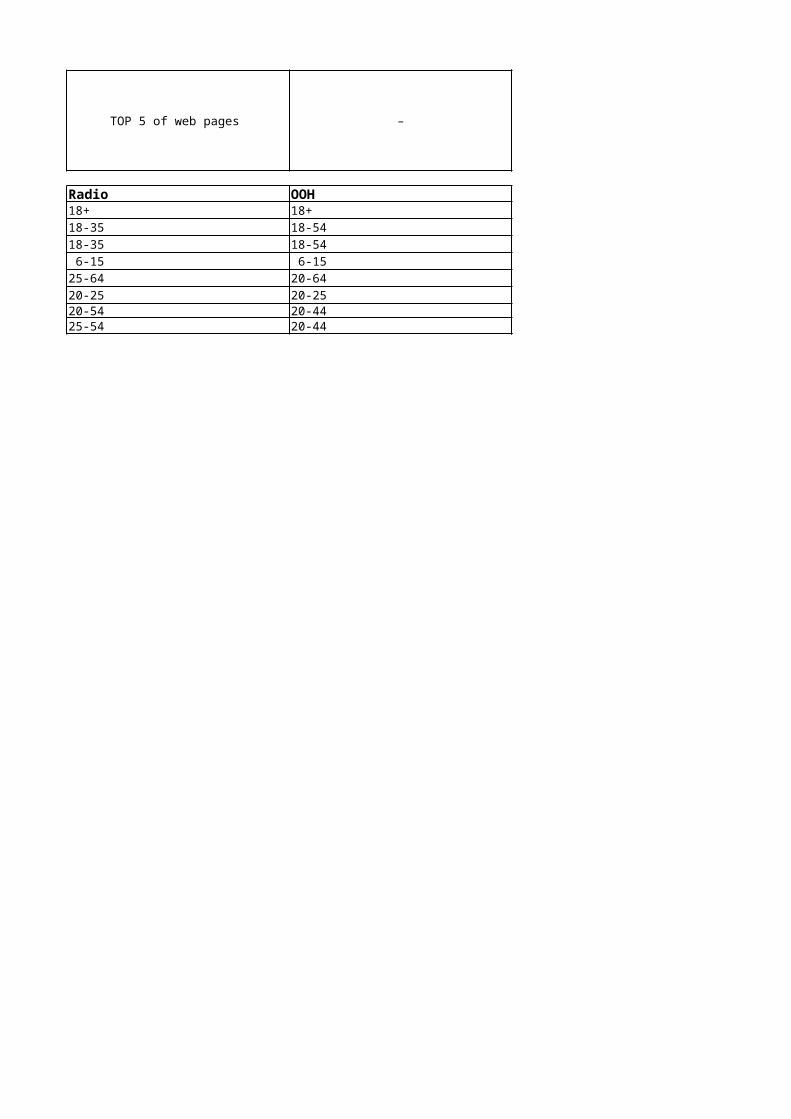

Av CPP_Universal TOP 5 of web pages –

Magazines Radio OOH18+ 18+ 18+18-35 18-35 18-5418-54 18-35 18-54 6-15 6-15 6-1520-44 25-64 20-6420-25 20-25 20-2525-44 20-54 20-4420-44 25-54 20-44

KAZAKHSTAN 2016

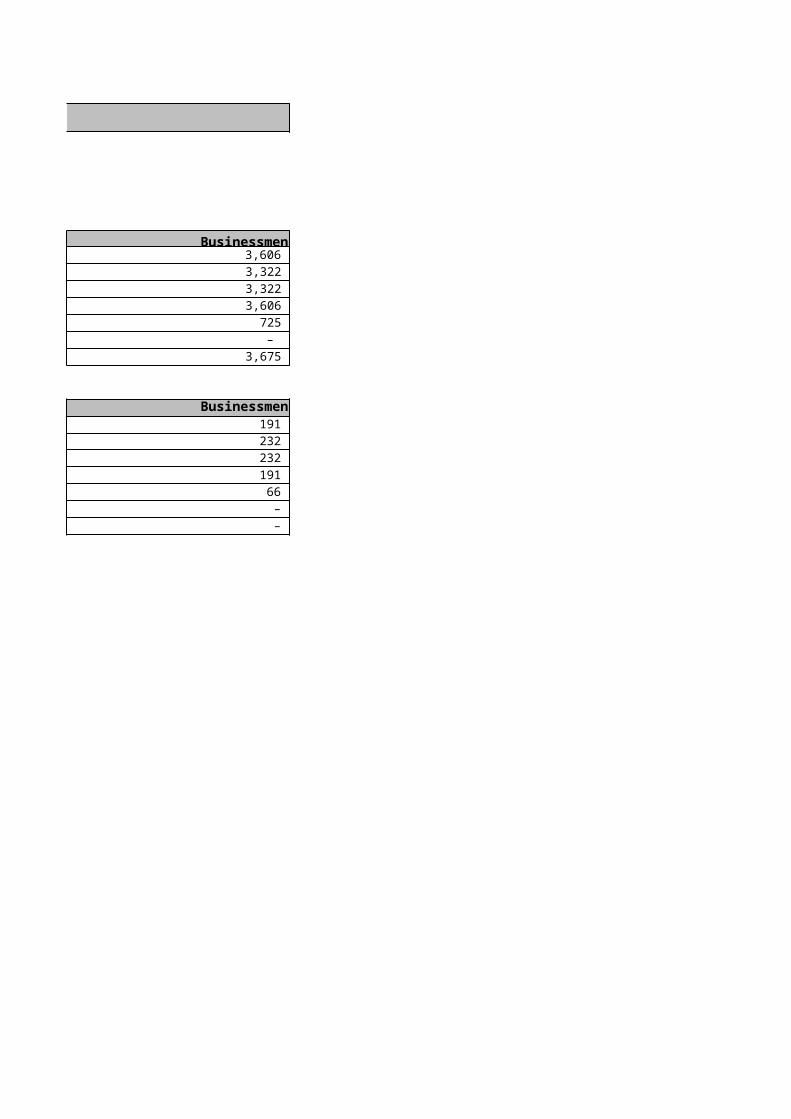

Young adults Upmarket adults Businessmen 810 4,384 3,606 810 4,384 3,322 810 2,621 3,322 810 4,307 3,606 199 725 725

– – – 962 3,675 3,675

Young adults Upmarket adults Businessmen26 138 191

-25 303 232 -25 141 232 26 61 191 27 66 66 – – – – – –

–

–

–

–

–

–

What assumptions have you made?

–

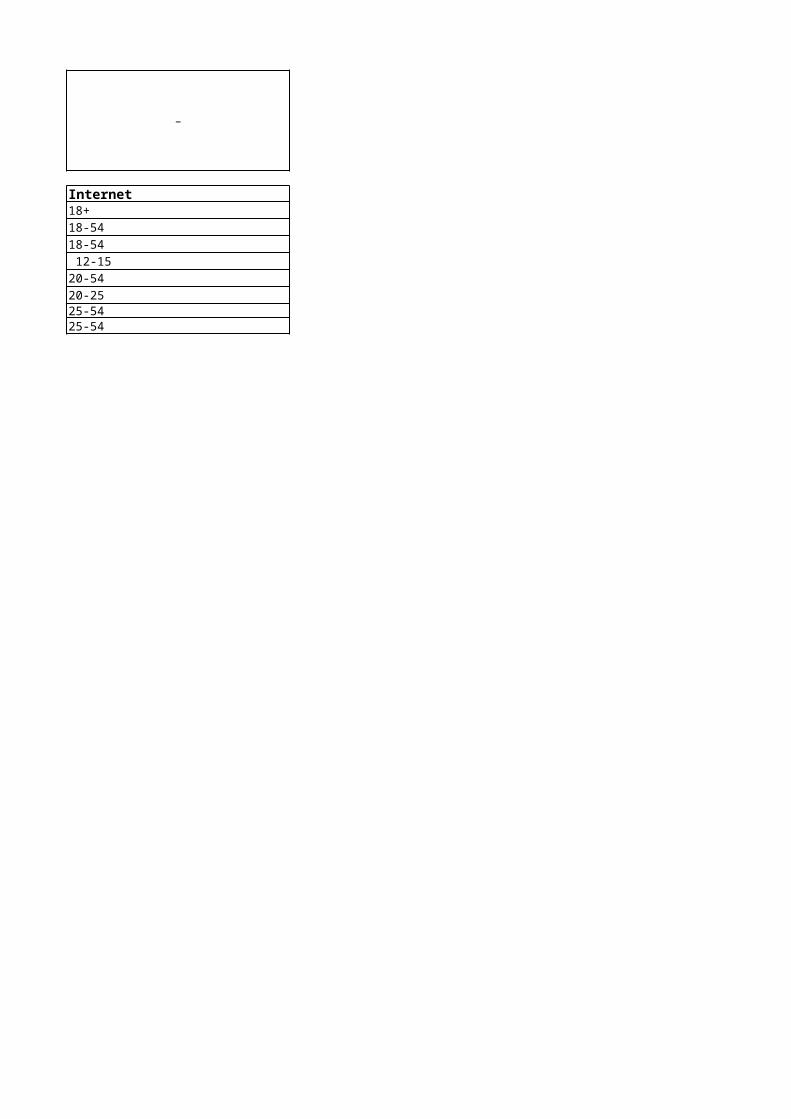

Internet18+18-5418-54 12-1520-5420-2525-5425-54

Country:

LITHUANIA 2016NOTES

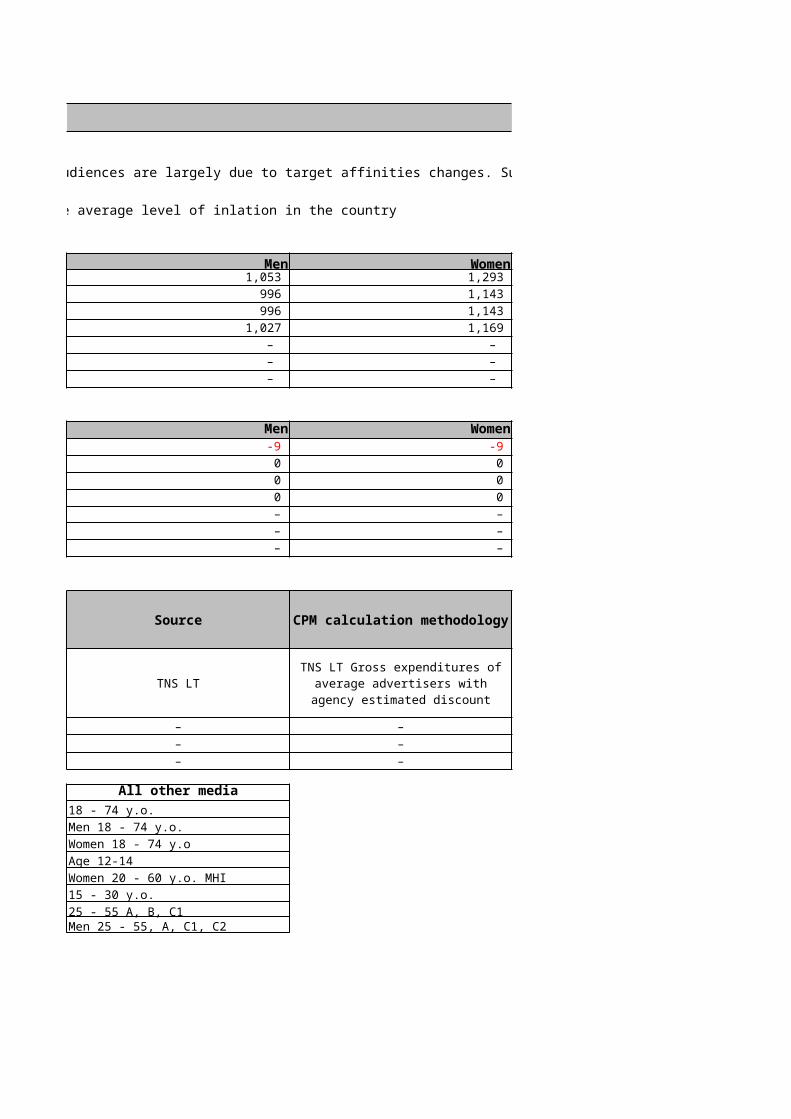

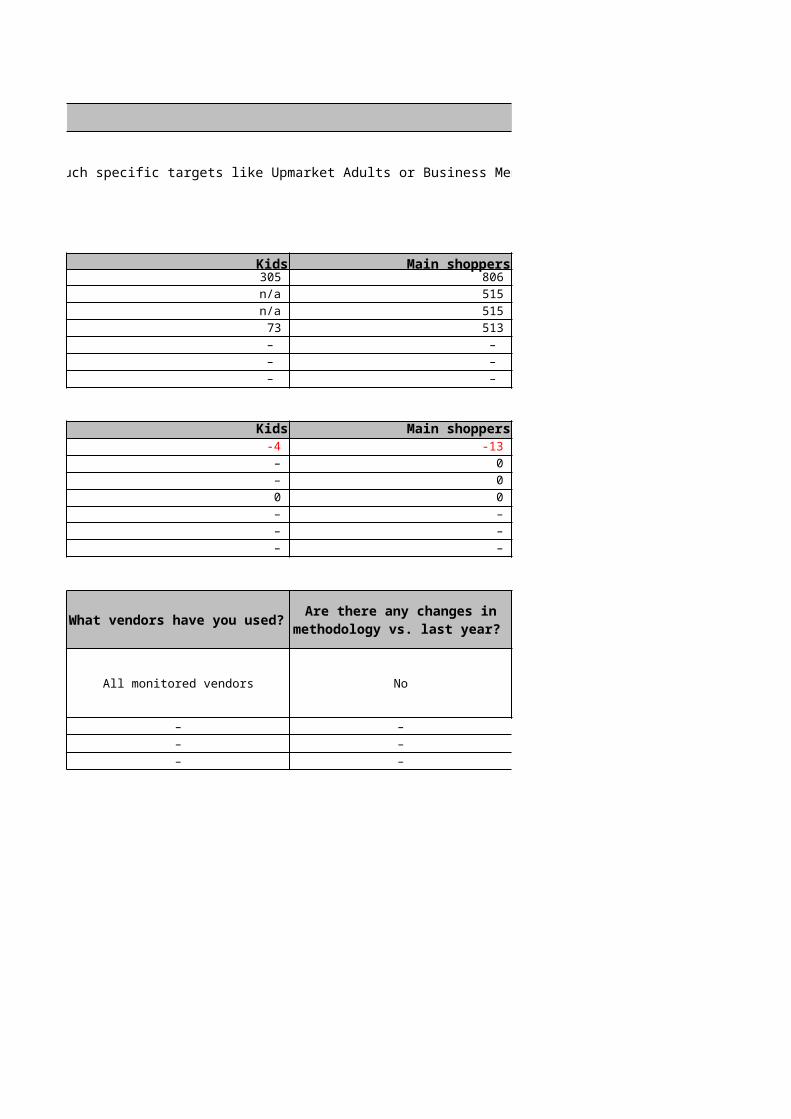

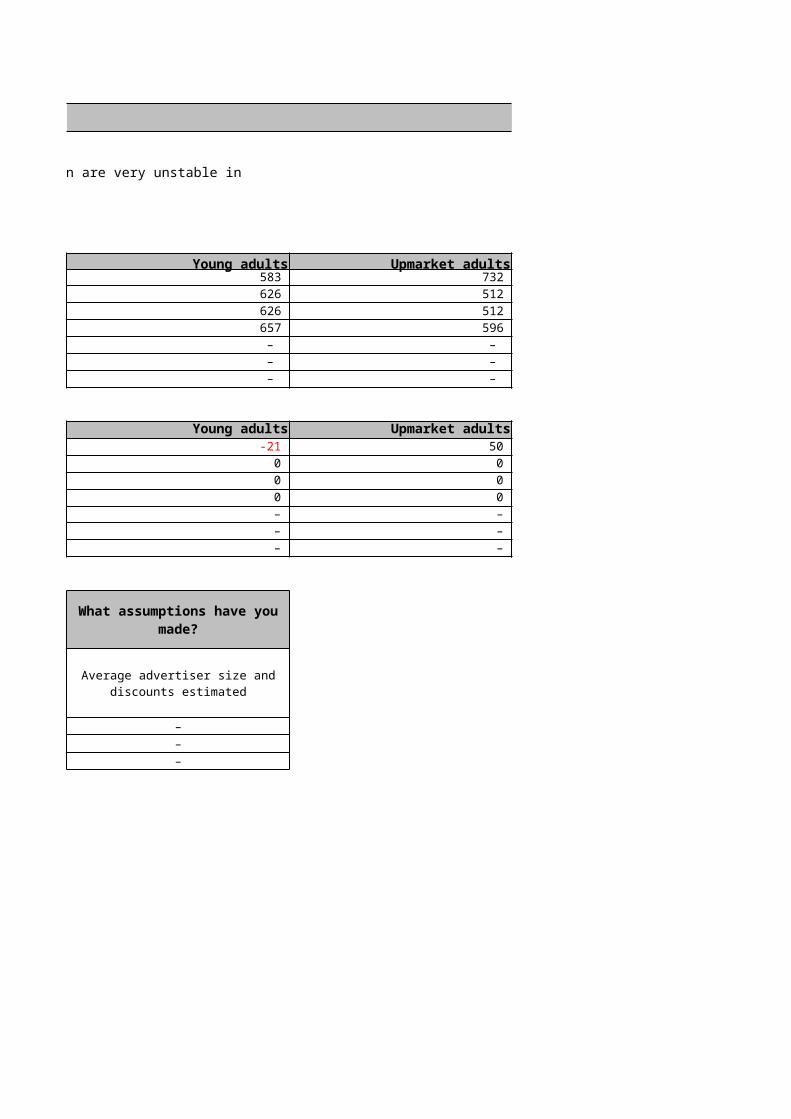

All Changes in cost for niche audiences are largely due to target affinities changes. Such specific targets like Upmarket Adults or Business Men are very unstable in terms of sample sizes.

TV For TV it is inline with the average level of inlation in the country

UNIVERSES (000s)Adults Men

Television 2,346 1,053 Newspapers 2,139 996 Magazines 2,139 996 Radio 2,196 1,027 Out of home – – Cinema – – Internet – –

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television -18 -9 Newspapers 0 0 Magazines 0 0 Radio 0 0 Out of home – – Cinema – – Internet – –

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds

TNS LTNewspapers A3, full colourMagazines Full page colour

Radio 30 secondsOut of home Various –

Cinema 30 seconds –Internet Banner 468x60 –

Audience Television All other mediaAdults 18+ 18 - 74 y.o.Men Men 18+ Men 18 - 74 y.o.Women Women 18+ Women 18 - 74 y.oKids Age 4-14 Age 12-14Main shoppers Women 20 - 60 y.o. MHI Women 20 - 60 y.o. MHIYoung adults 15 - 30 y.o. 15 - 30 y.o.Upmarket adults 25 - 55 A, B, C1 25 - 55 A, B, C1Businessmen Men 25 - 55, A, C1, C2 Men 25 - 55, A, C1, C2

LITHUANIA 2016

Changes in cost for niche audiences are largely due to target affinities changes. Such specific targets like Upmarket Adults or Business Men are very unstable in terms of sample sizes.

For TV it is inline with the average level of inlation in the country

Women Kids Main shoppers 1,293 305 806 1,143 n/a 515 1,143 n/a 515 1,169 73 513

– – – – – – – – –

Women Kids Main shoppers-9 -4 -13 0 – 0 0 – 0 0 0 0 – – – – – – – – –

All monitored vendors No

– – –– – –– – –

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

TNS LT Gross expenditures of average advertisers with agency

estimated discount

LITHUANIA 2016

Changes in cost for niche audiences are largely due to target affinities changes. Such specific targets like Upmarket Adults or Business Men are very unstable in terms of sample sizes.

Young adults Upmarket adults Businessmen 583 732 562 626 512 235 626 512 235 657 596 379

– – – – – – – – –

Young adults Upmarket adults Businessmen-21 50 -8

0 0 0 0 0 0 0 0 0 – – – – – – – – –

–––

What assumptions have you made?

Average advertiser size and discounts estimated

Country:

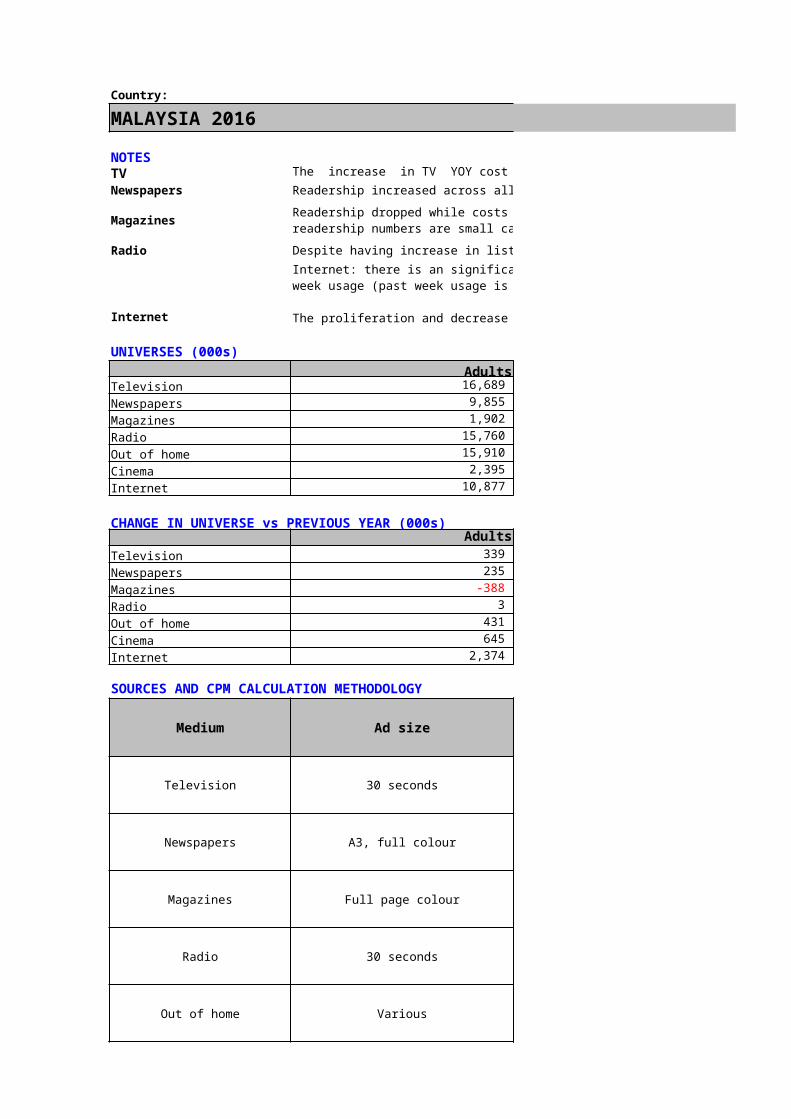

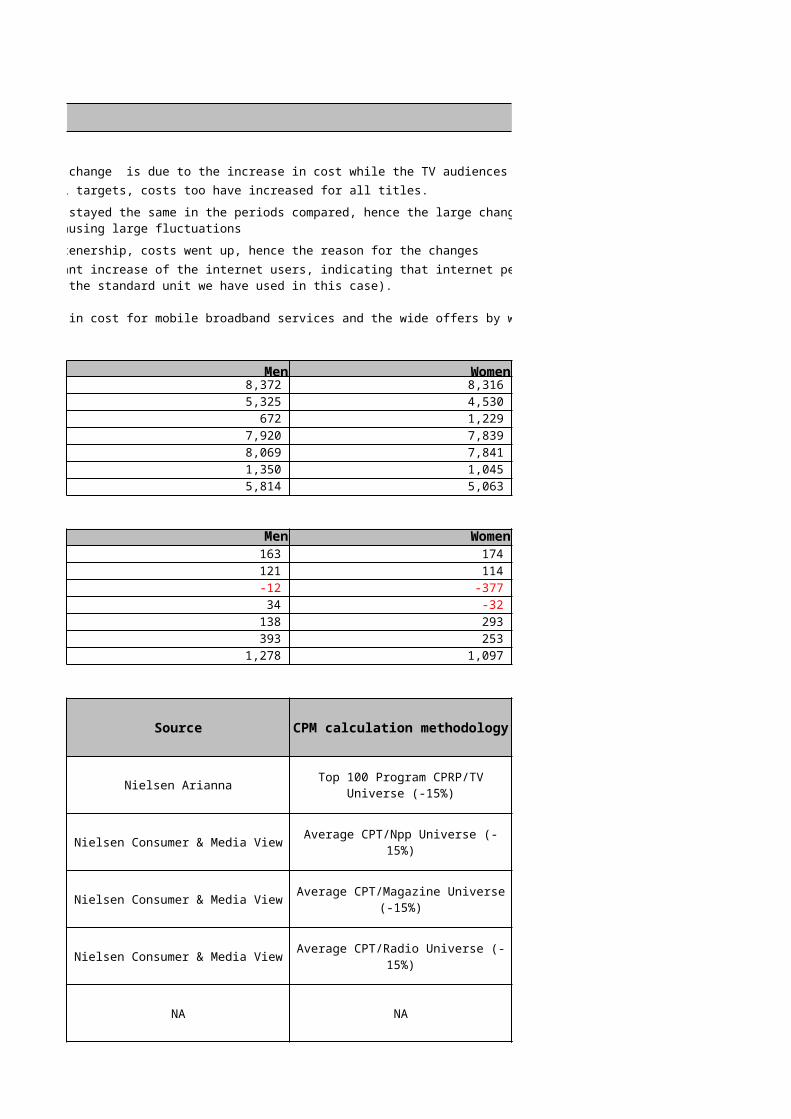

MALAYSIA 2016NOTESTV The increase in TV YOY cost change is due to the increase in cost while the TV audiences penetration remain relatively stable Newspapers Readership increased across all targets, costs too have increased for all titles.

Magazines

Radio Despite having increase in listenership, costs went up, hence the reason for the changes

Internet

UNIVERSES (000s)Adults Men

Television 16,689 8,372 Newspapers 9,855 5,325 Magazines 1,902 672 Radio 15,760 7,920 Out of home 15,910 8,069 Cinema 2,395 1,350 Internet 10,877 5,814

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 339 163 Newspapers 235 121 Magazines -388 -12 Radio 3 34 Out of home 431 138 Cinema 645 393 Internet 2,374 1,278

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds Nielsen Arianna

Newspapers A3, full colour Nielsen Consumer & Media View

Magazines Full page colour Nielsen Consumer & Media View

Radio 30 seconds Nielsen Consumer & Media View

Out of home Various NA

Readership dropped while costs stayed the same in the periods compared, hence the large changes. Readership in Malaysia is getting smaller so, by target, readership numbers are small causing large fluctuations

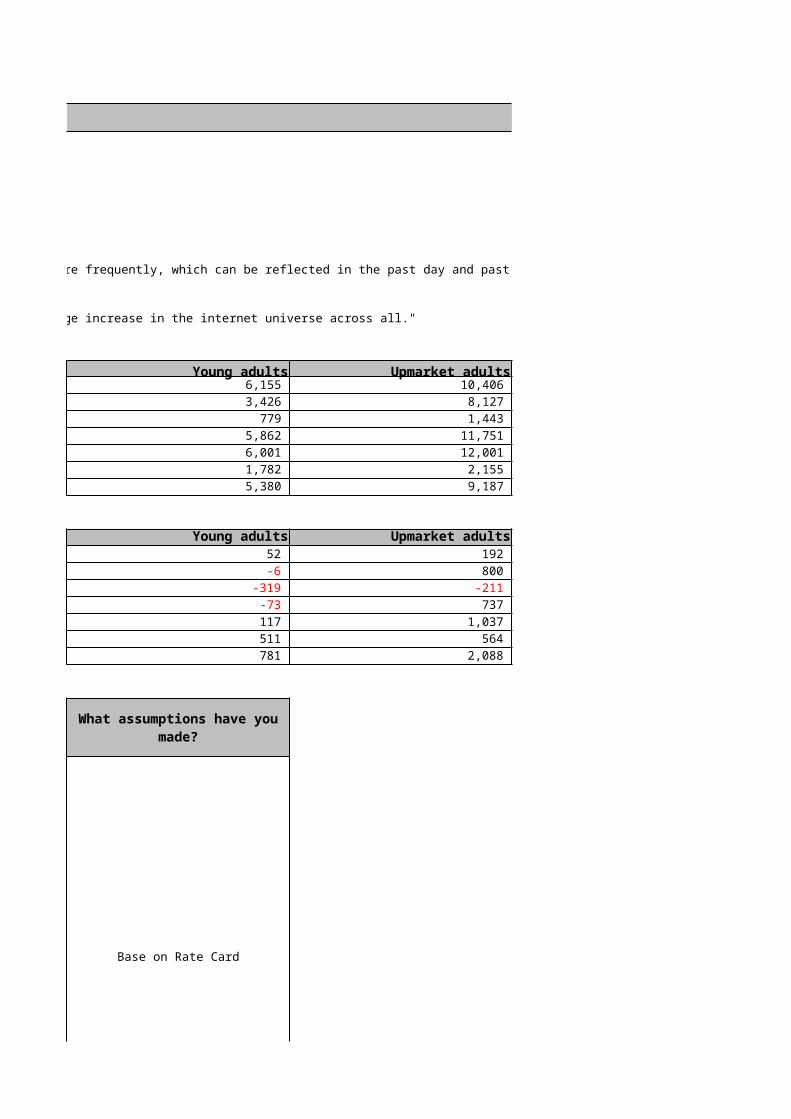

Internet: there is an significant increase of the internet users, indicating that internet penetration in Malaysia has increased, and also accessing it more frequently, which can be reflected in the past day and past week usage (past week usage is the standard unit we have used in this case). The proliferation and decrease in cost for mobile broadband services and the wide offers by wireless broadband operators have mainly contributed to the huge increase in the internet universe across all."

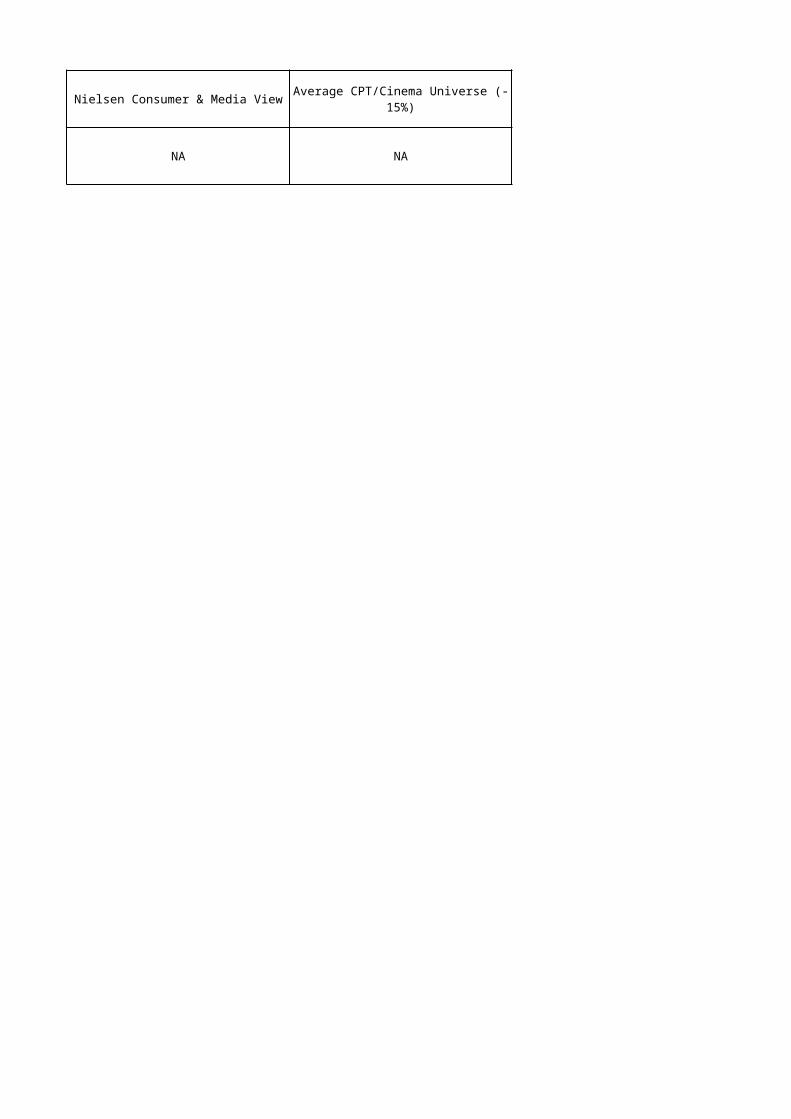

Cinema 30 seconds Nielsen Consumer & Media View

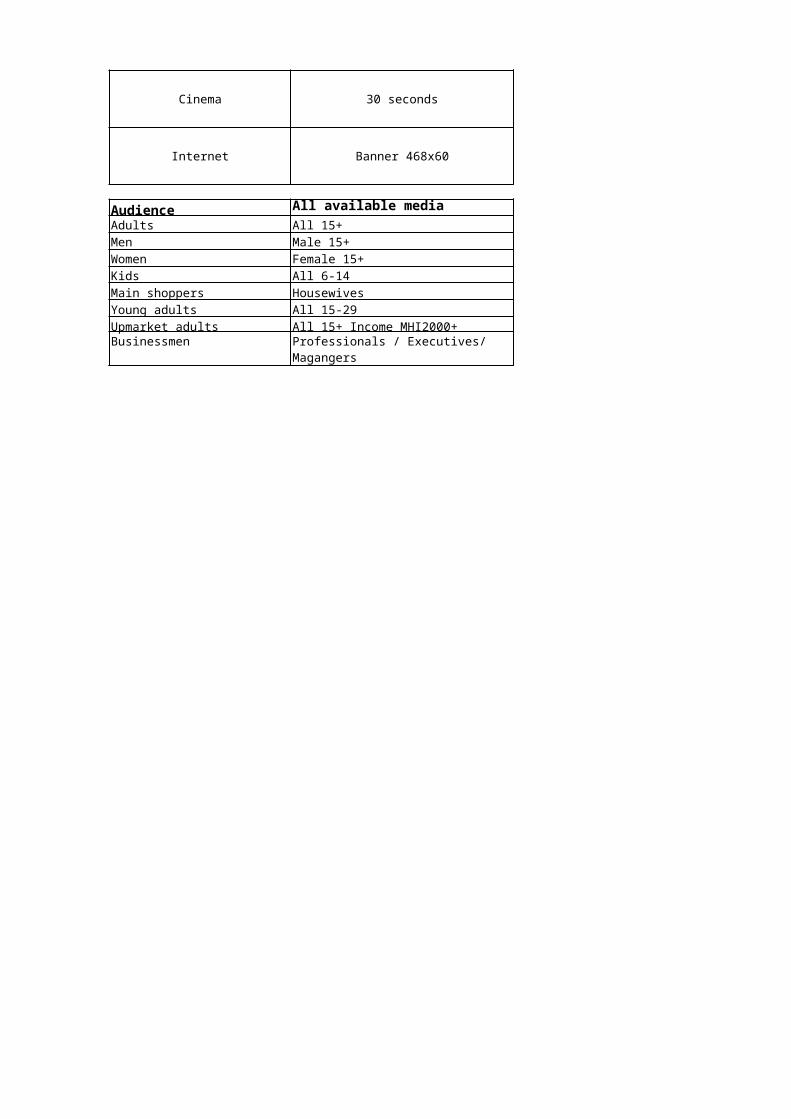

Internet Banner 468x60 NA

Audience All available mediaAdults All 15+Men Male 15+Women Female 15+Kids All 6-14Main shoppers HousewivesYoung adults All 15-29Upmarket adults All 15+ Income MHI2000+Businessmen Professionals / Executives/

Magangers

MALAYSIA 2016

The increase in TV YOY cost change is due to the increase in cost while the TV audiences penetration remain relatively stable Readership increased across all targets, costs too have increased for all titles.

Despite having increase in listenership, costs went up, hence the reason for the changes

Women Kids Main shoppers 8,316 3,628 4,762 4,530 NA 3,389 1,229 NA 835 7,839 NA 5,436 7,841 NA 5,455 1,045 NA 429 5,063 NA 3,154

Women Kids Main shoppers174 -68 108 114 – 721

-377 – 33 -32 – 944 293 – 1,064 253 – 196

1,097 – 1,412

NO

NO

NO

NO

NA NA NO

Readership dropped while costs stayed the same in the periods compared, hence the large changes. Readership in Malaysia is getting smaller so, by target, readership

Internet: there is an significant increase of the internet users, indicating that internet penetration in Malaysia has increased, and also accessing it more frequently, which can be reflected in the past day and past week usage (past week usage is the

The proliferation and decrease in cost for mobile broadband services and the wide offers by wireless broadband operators have mainly contributed to the huge increase in the internet universe across all."

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

Top 100 Program CPRP/TV Universe (-15%)

All FTA Channel (TV1, TV2, TV3, NTV7, 8TV & TV9)

Average CPT/Npp Universe (-15%)

Based on titles covered in Nielsen Media Index

Average CPT/Magazine Universe (-15%)

Based on titles covered in Nielsen Media Index

Average CPT/Radio Universe (-15%)

Based on staion covered in Nielsen Media Index

NO

NA NA NO

Average CPT/Cinema Universe (-15%)

Based on 30sec cost, average of all cinema & halls

MALAYSIA 2016

Young adults Upmarket adults Businessmen 6,155 10,406 2,491 3,426 8,127 1,654 779 1,443 222 5,862 11,751 2,239 6,001 12,001 2,247 1,782 2,155 411 5,380 9,187 1,842

Young adults Upmarket adults Businessmen52 192 -161 -6 800 76

-319 -211 -71 -73 737 177 117 1,037 146 511 564 96 781 2,088 331

Base on Rate Card

Internet: there is an significant increase of the internet users, indicating that internet penetration in Malaysia has increased, and also accessing it more frequently, which can be reflected in the past day and past week usage (past week usage is the

The proliferation and decrease in cost for mobile broadband services and the wide offers by wireless broadband operators have mainly contributed to the huge increase in the internet universe across all."

What assumptions have you made?

Base on Rate Card

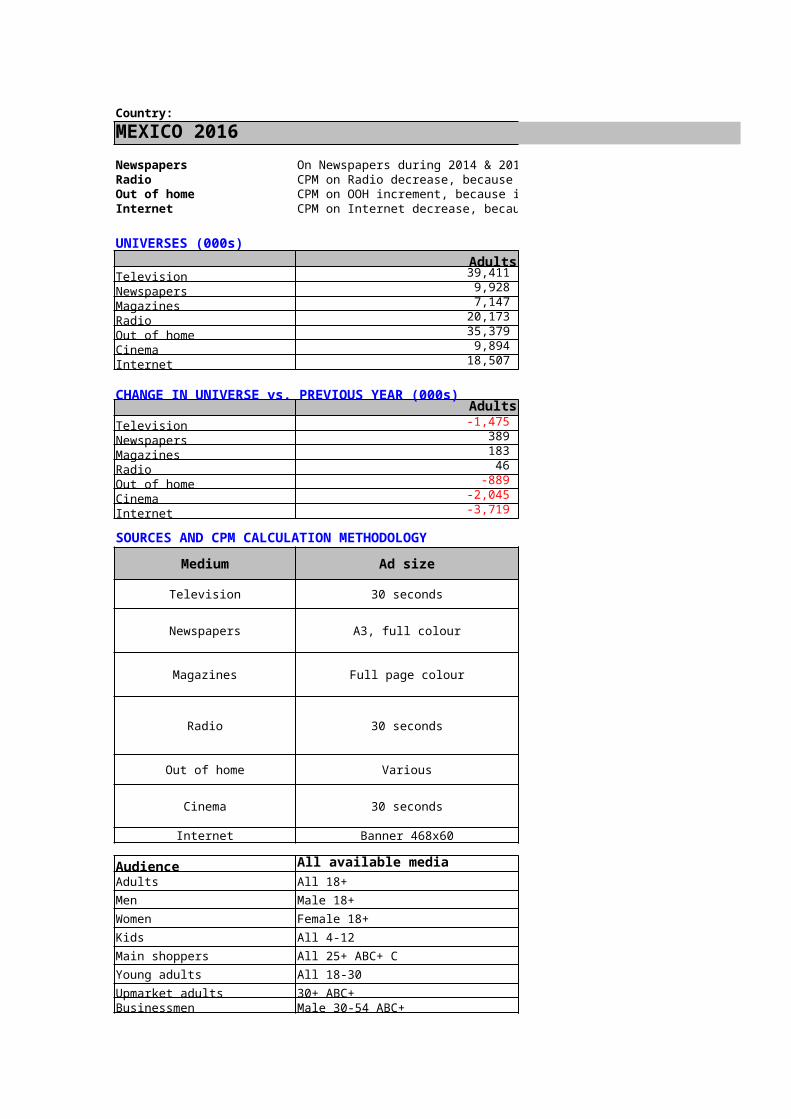

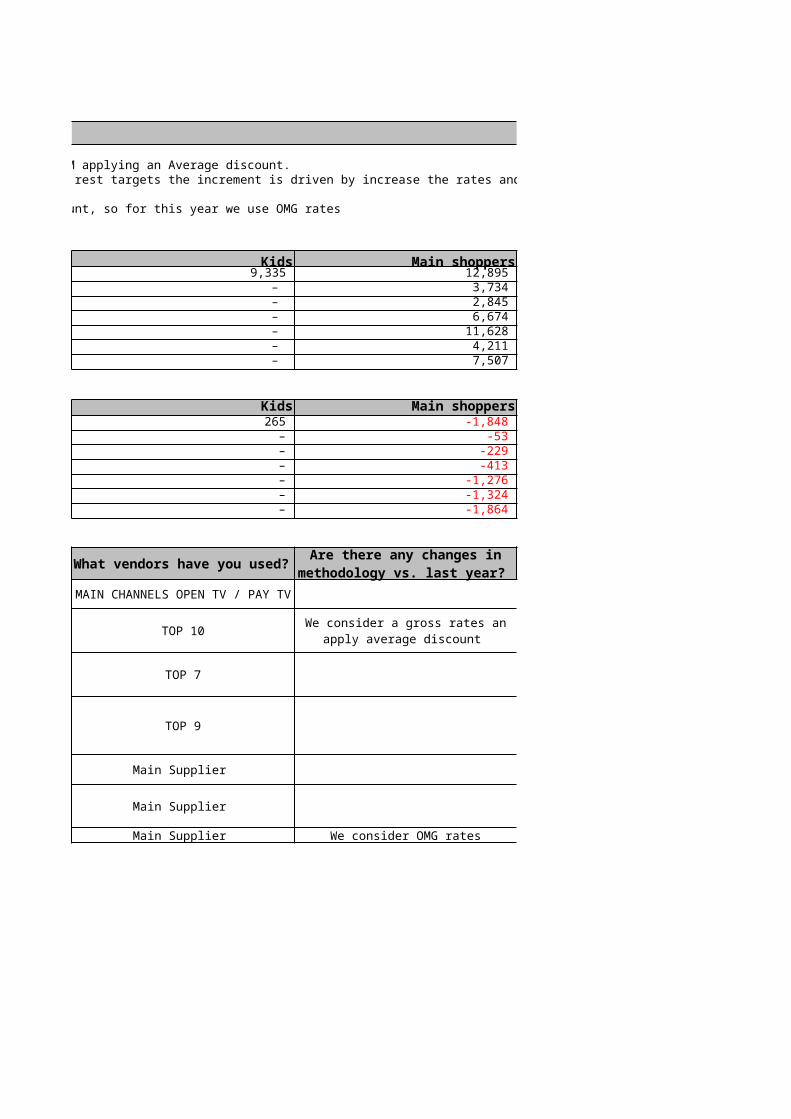

Country:MEXICO 2016Newspapers On Newspapers during 2014 & 2015 used gross rates, so we updated CPM in 2014 and 2015 for CPM applying an Average discount. Radio CPM on Radio decrease, because in some stations increase the audience (Business Men). On the rest targets the increment is driven by increase the rates and maintain similar levels of audience, but it isn't the same levels and the percent varies. Out of home CPM on OOH increment, because in some sites decrease the audience and maintain same rates.Internet CPM on Internet decrease, because in 2015 we used gross rates plus an applying average discount, so for this year we use OMG rates

UNIVERSES (000s)Adults Men

Television 39,411 18,860 Newspapers 9,928 5,778 Magazines 7,147 3,012 Radio 20,173 10,041 Out of home 35,379 16,684 Cinema 9,894 5,019 Internet 18,507 9,471

CHANGE IN UNIVERSE vs. PREVIOUS YEAR (000s)Adults Men

Television -1,475 -469 Newspapers 389 168 Magazines 183 -90 Radio 46 291 Out of home -889 -611 Cinema -2,045 -854 Internet -3,719 -1,663

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds NIELSEN IBOPE

Newspapers A3, full colour EGM

Magazines Full page colour EGM

Radio 30 seconds EGM

Out of home Various NIELSEN IBOPE

Cinema 30 seconds Main Supplier

Internet Banner 468x60 Main Supplier

Audience All available mediaAdults All 18+Men Male 18+Women Female 18+Kids All 4-12Main shoppers All 25+ ABC+ CYoung adults All 18-30Upmarket adults 30+ ABC+Businessmen Male 30-54 ABC+

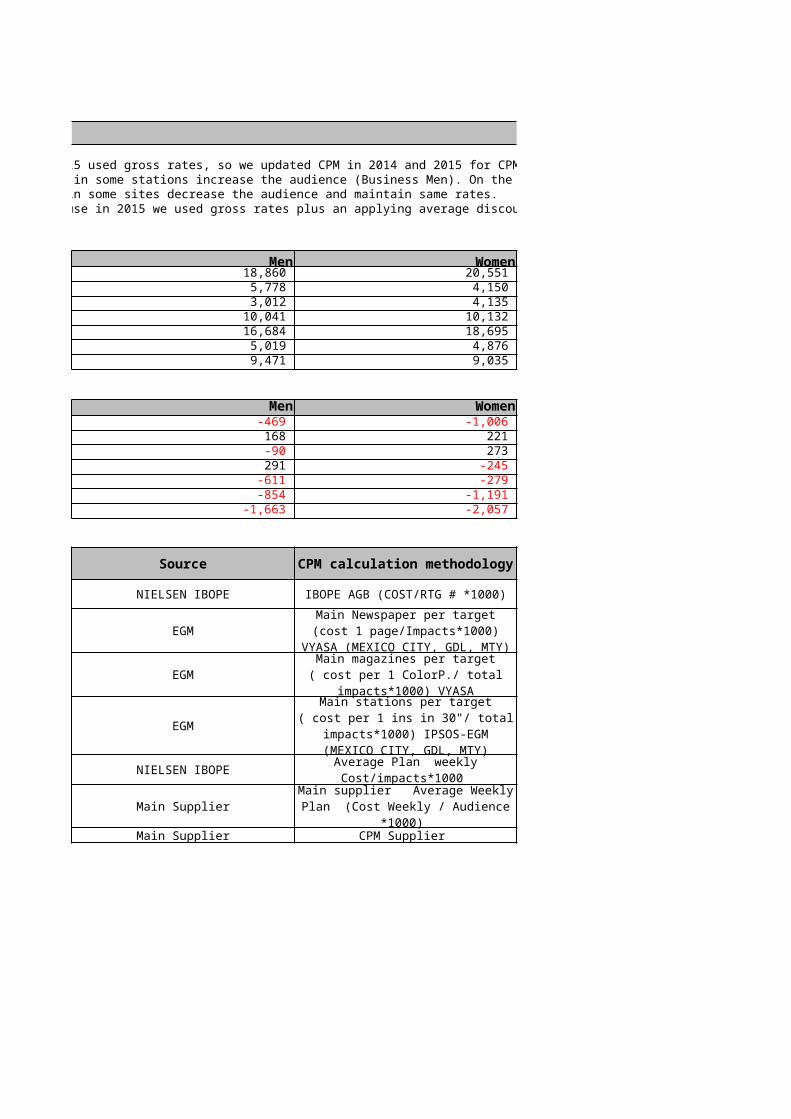

MEXICO 2016On Newspapers during 2014 & 2015 used gross rates, so we updated CPM in 2014 and 2015 for CPM applying an Average discount. CPM on Radio decrease, because in some stations increase the audience (Business Men). On the rest targets the increment is driven by increase the rates and maintain similar levels of audience, but it isn't the same levels and the percent varies. CPM on OOH increment, because in some sites decrease the audience and maintain same rates.CPM on Internet decrease, because in 2015 we used gross rates plus an applying average discount, so for this year we use OMG rates

Women Kids Main shoppers 20,551 9,335 12,895 4,150 – 3,734 4,135 – 2,845 10,132 – 6,674 18,695 – 11,628 4,876 – 4,211 9,035 – 7,507

Women Kids Main shoppers-1,006 265 -1,848

221 – -53 273 – -229

-245 – -413 -279 – -1,276

-1,191 – -1,324 -2,057 – -1,864

IBOPE AGB (COST/RTG # *1000)

TOP 10

TOP 7

TOP 9

Main Supplier

Main Supplier

CPM Supplier Main Supplier We consider OMG rates

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

MAIN CHANNELS OPEN TV / PAY TV

Main Newspaper per target (cost 1 page/Impacts*1000) VYASA (MEXICO CITY, GDL, MTY)

We consider a gross rates an apply average discount

Main magazines per target ( cost per 1 ColorP./ total impacts*1000)

VYASAMain stations per target ( cost per 1 ins in 30"/ total impacts*1000) IPSOS-EGM (MEXICO CITY,

GDL, MTY)Average Plan weekly Cost/impacts*1000

Main supplier Average Weekly Plan (Cost Weekly / Audience

*1000)

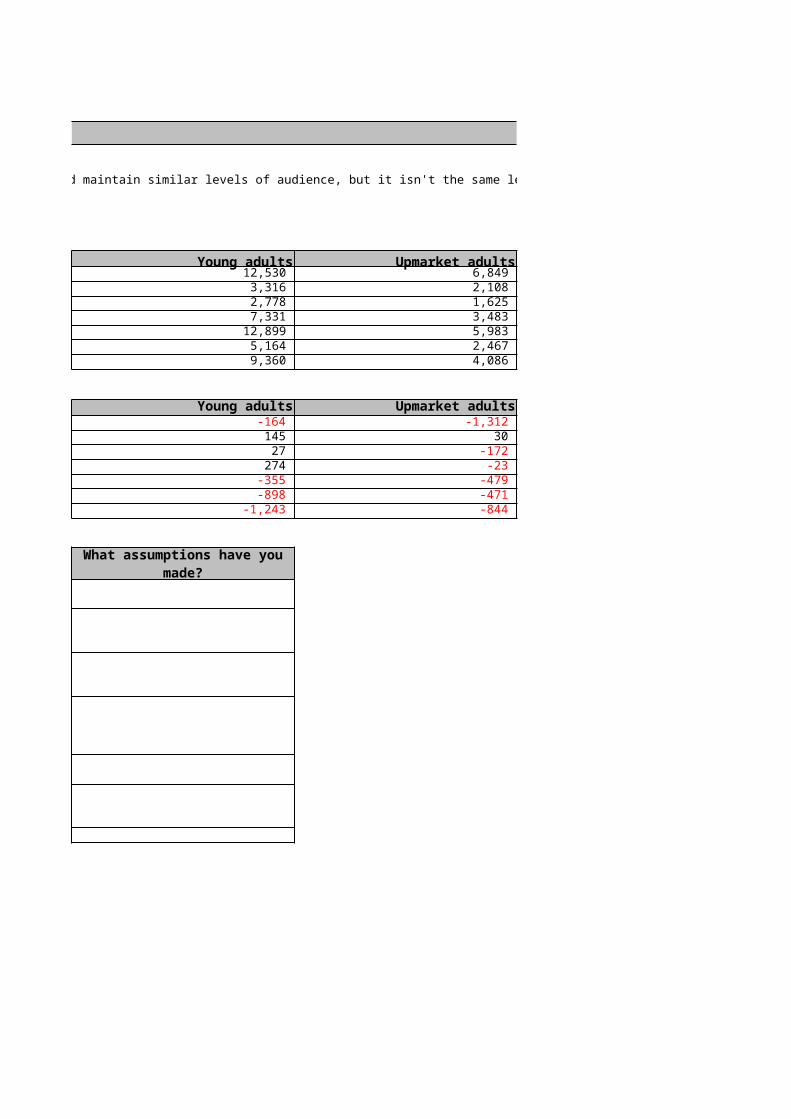

MEXICO 2016

CPM on Radio decrease, because in some stations increase the audience (Business Men). On the rest targets the increment is driven by increase the rates and maintain similar levels of audience, but it isn't the same levels and the percent varies.

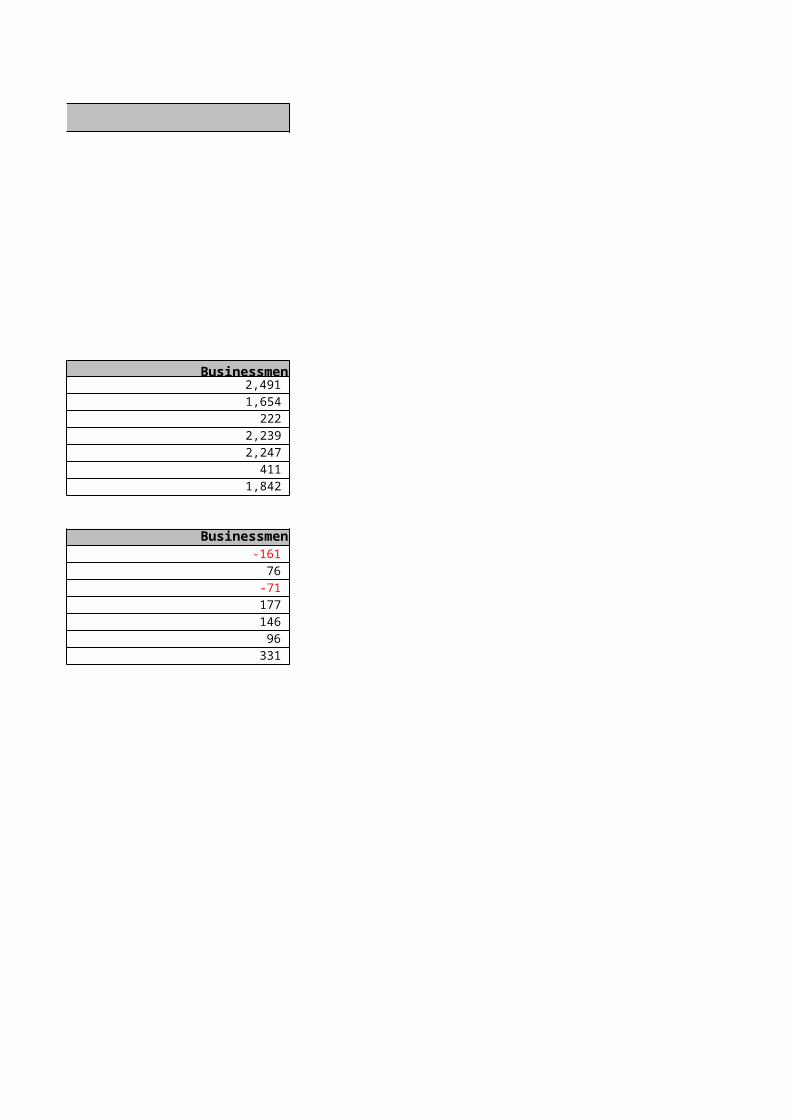

Young adults Upmarket adults Businessmen 12,530 6,849 3,235 3,316 2,108 607 2,778 1,625 440 7,331 3,483 953 12,899 5,983 1,496 5,164 2,467 837 9,360 4,086 1,270

Young adults Upmarket adults Businessmen-164 -1,312 -650 145 30 -98

27 -172 -104 274 -23 60

-355 -479 -255 -898 -471 -131

-1,243 -844 -308

What assumptions have you made?

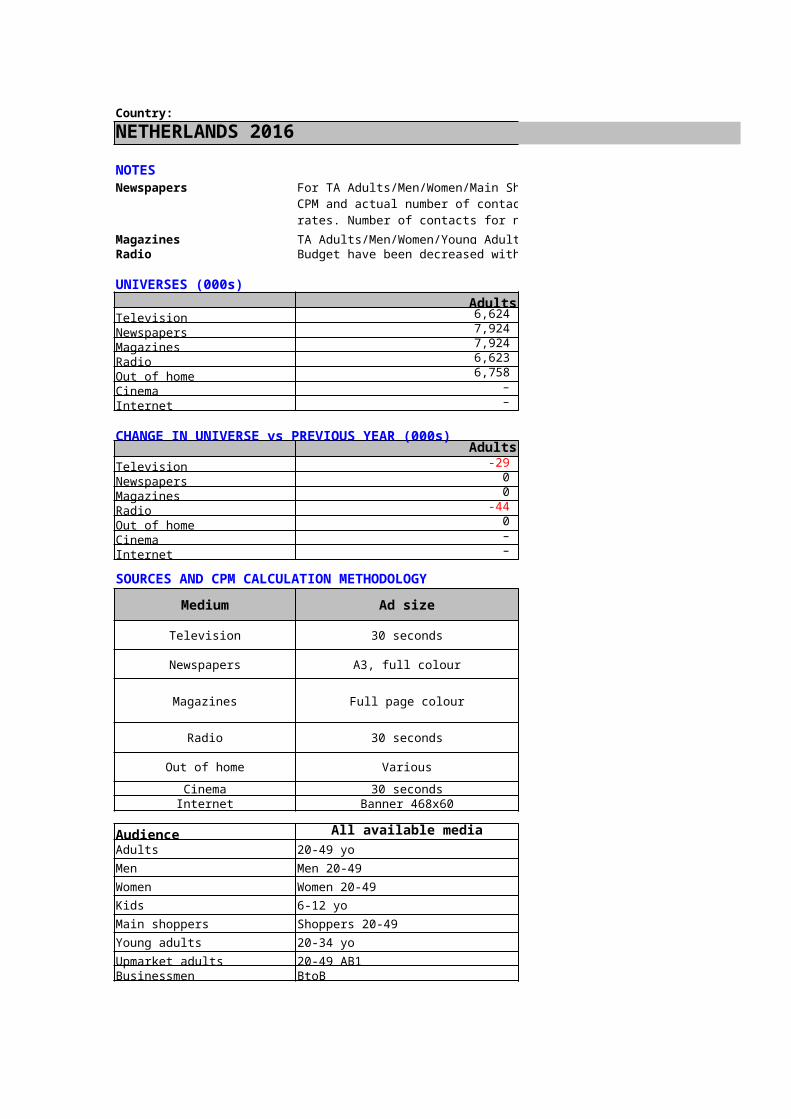

Country:NETHERLANDS 2016NOTESNewspapers

MagazinesRadio Budget have been decreased with 6%. Discounts have been increased with 5%, channel mix as in 2015.

UNIVERSES (000s)Adults Men

Television 6,624 3,319 Newspapers 7,924 3,691 Magazines 7,924 3,691 Radio 6,623 3,057 Out of home 6,758 3,397 Cinema – – Internet – –

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television -29 -15 Newspapers 0 0 Magazines 0 0 Radio -44 -94 Out of home 0 0 Cinema – – Internet – –

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds SKO

Newspapers A3, full colour NOM

Magazines Full page colour NOM

Radio 30 seconds NLO

Out of home Various

Cinema 30 seconds –Internet Banner 468x60 –

Audience All available mediaAdults 20-49 yoMen Men 20-49Women Women 20-49Kids 6-12 yoMain shoppers Shoppers 20-49Young adults 20-34 yoUpmarket adults 20-49 AB1Businessmen BtoB

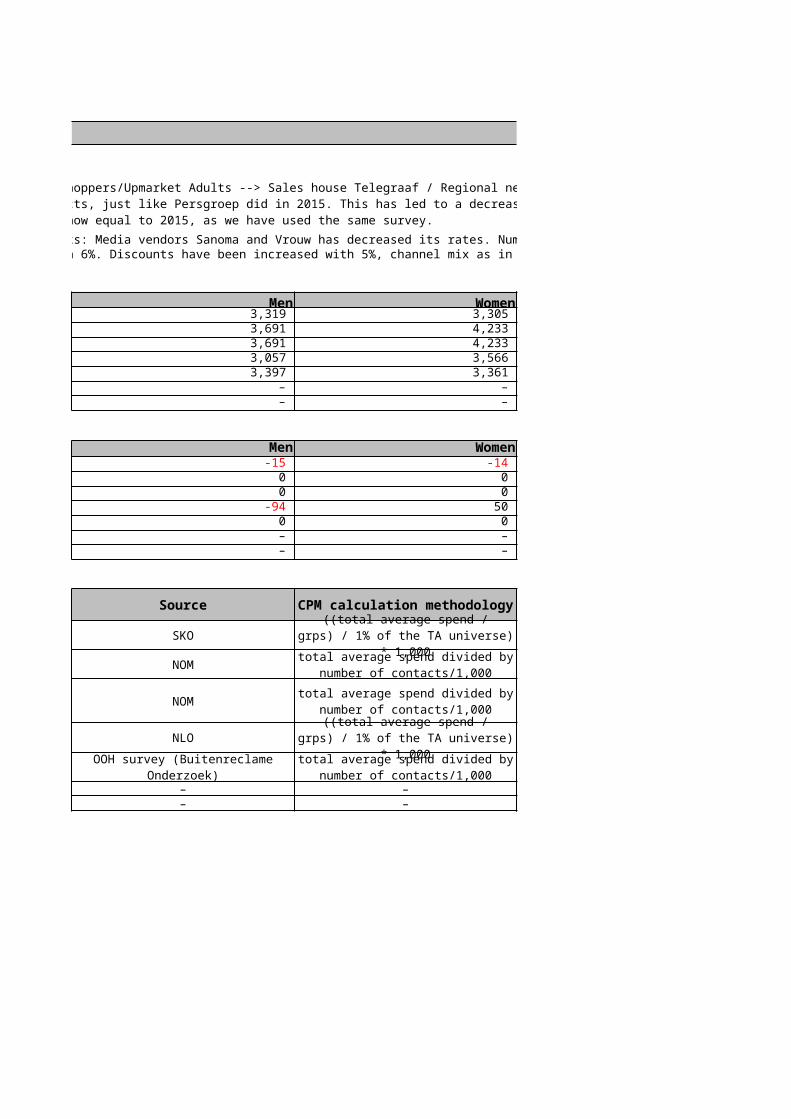

For TA Adults/Men/Women/Main Shoppers/Upmarket Adults --> Sales house Telegraaf / Regional newspapers have implemented a new ratecard methodology based on CPM and actual number of contacts, just like Persgroep did in 2015. This has led to a decrease of the rates. NRC Handelsblad has also decreased it's rates. Number of contacts for now equal to 2015, as we have used the same survey.

TA Adults/Men/Women/Young Adults: Media vendors Sanoma and Vrouw has decreased its rates. Number of contacts for now equal to 2015, as we have used the same

OOH survey (Buitenreclame Onderzoek)

NETHERLANDS 2016

Budget have been decreased with 6%. Discounts have been increased with 5%, channel mix as in 2015.

Women Kids Main shoppers 3,305 1,338 3,671 4,233 – 5,187 4,233 – 5,187 3,566 – 4,057 3,361 – 4,364

– – – – – –

Women Kids Main shoppers-14 -15 -35

0 – 0 0 – 0

50 – -101 0 – 0 – – – – – –

No changes

No changes

Ster, OMS, SRG, Q-Music No changes

No changes

– – –– – –

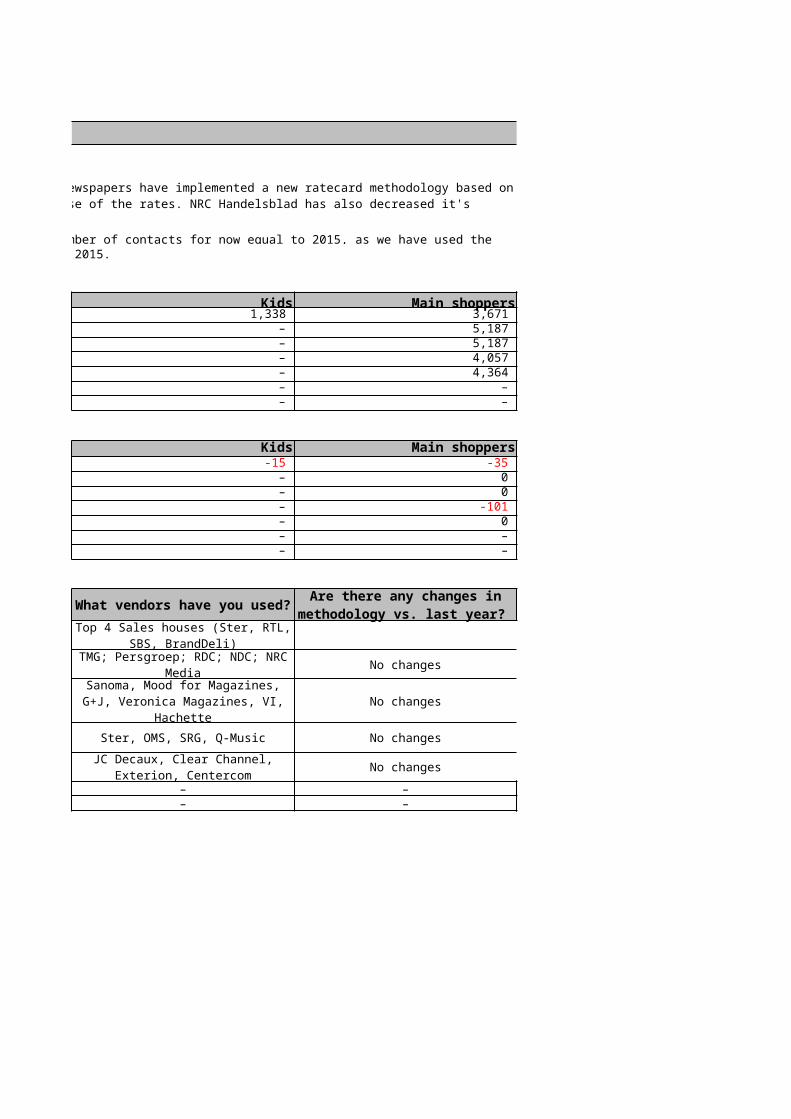

For TA Adults/Men/Women/Main Shoppers/Upmarket Adults --> Sales house Telegraaf / Regional newspapers have implemented a new ratecard methodology based on CPM and actual number of contacts, just like Persgroep did in 2015. This has led to a decrease of the rates. NRC Handelsblad has also decreased it's rates. Number of contacts for

TA Adults/Men/Women/Young Adults: Media vendors Sanoma and Vrouw has decreased its rates. Number of contacts for now equal to 2015, as we have used the same

CPM calculation methodology

What vendors have you used?

Are there any changes in methodology vs. last year?

((total average spend / grps) / 1% of the TA universe) * 1,000

Top 4 Sales houses (Ster, RTL, SBS, BrandDeli)

total average spend divided by number of contacts/1,000

TMG; Persgroep; RDC; NDC; NRC Media

total average spend divided by number of contacts/1,000

Sanoma, Mood for Magazines, G+J, Veronica Magazines, VI,

Hachette((total average spend / grps) / 1%

of the TA universe) * 1,000total average spend divided by

number of contacts/1,000JC Decaux, Clear Channel,

Exterion, Centercom

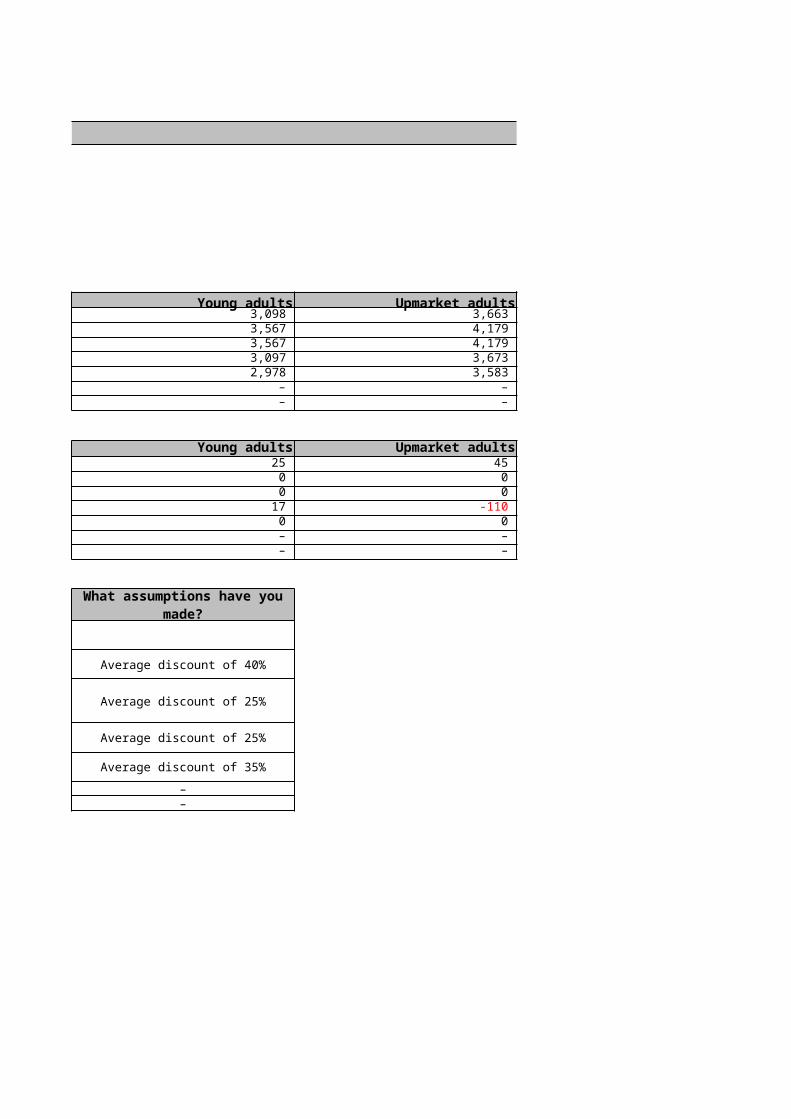

NETHERLANDS 2016

Young adults Upmarket adults Businessmen 3,098 3,663 1,215 3,567 4,179 1,276 3,567 4,179 1,276 3,097 3,673 1,062 2,978 3,583 2,723

– – – – – –

Young adults Upmarket adults Businessmen25 45 -39 0 0 0 0 0 0

17 -110 21 0 0 0 – – – – – –

Average discount of 40%

Average discount of 25%

Average discount of 25%

Average discount of 35%

––

What assumptions have you made?

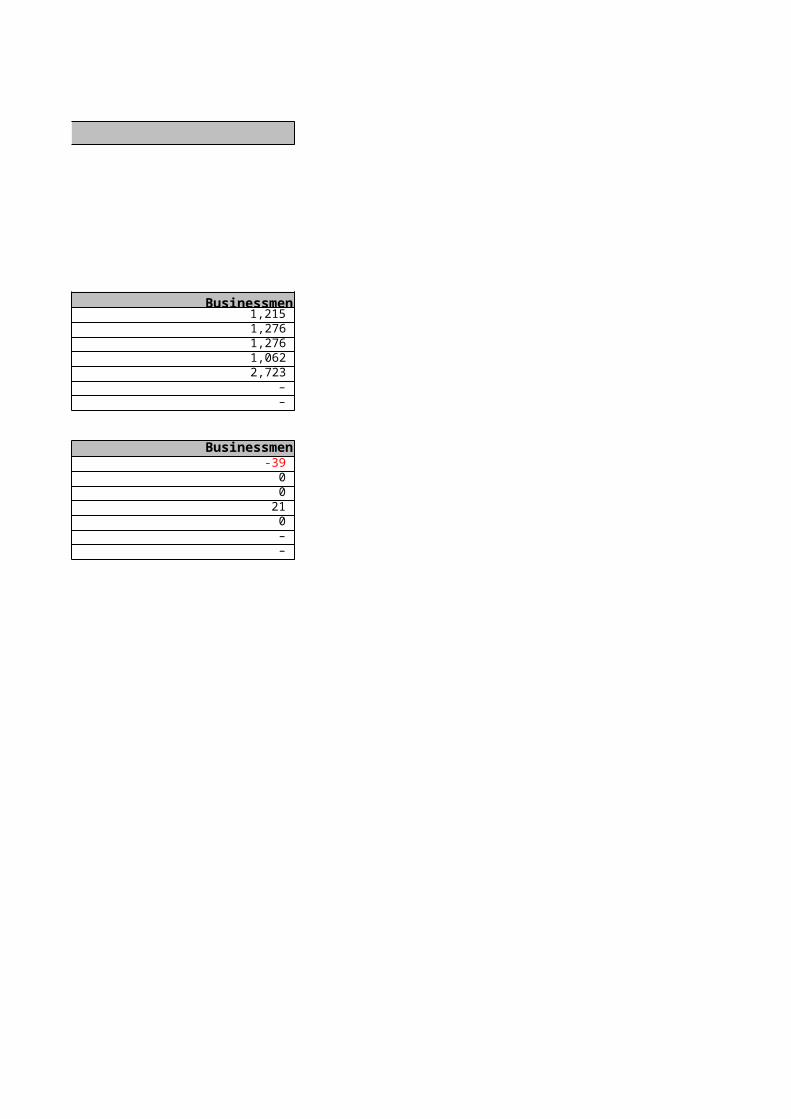

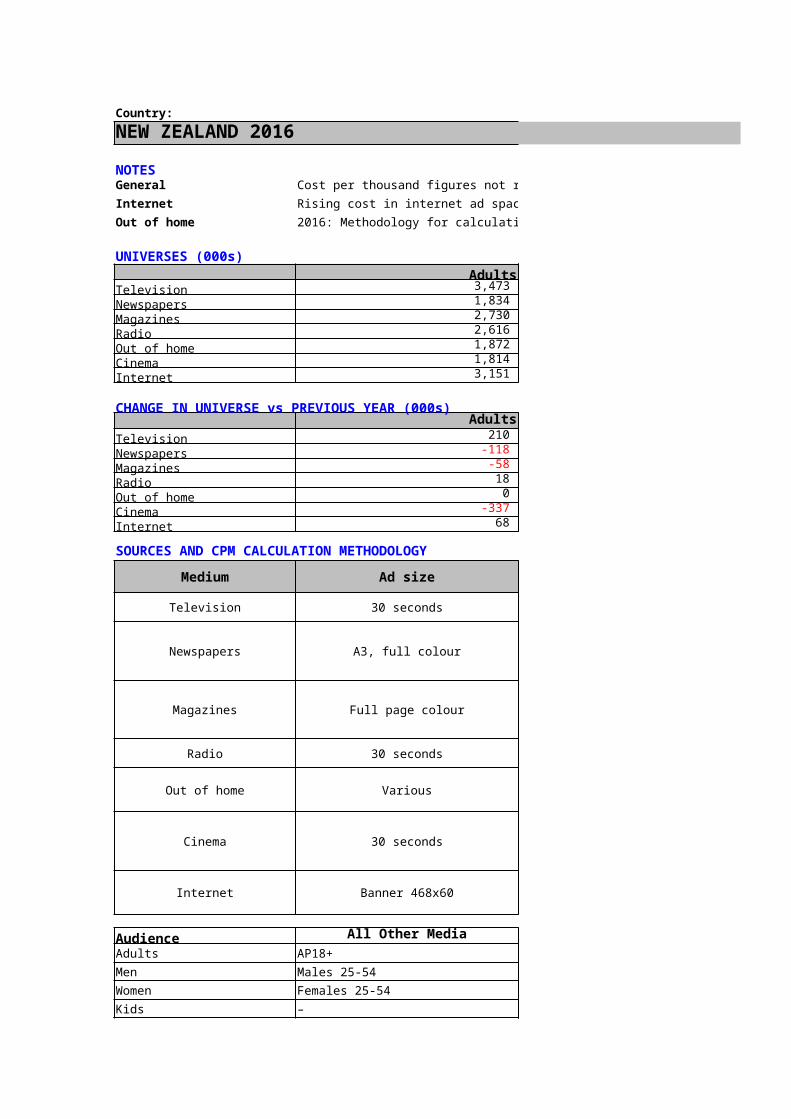

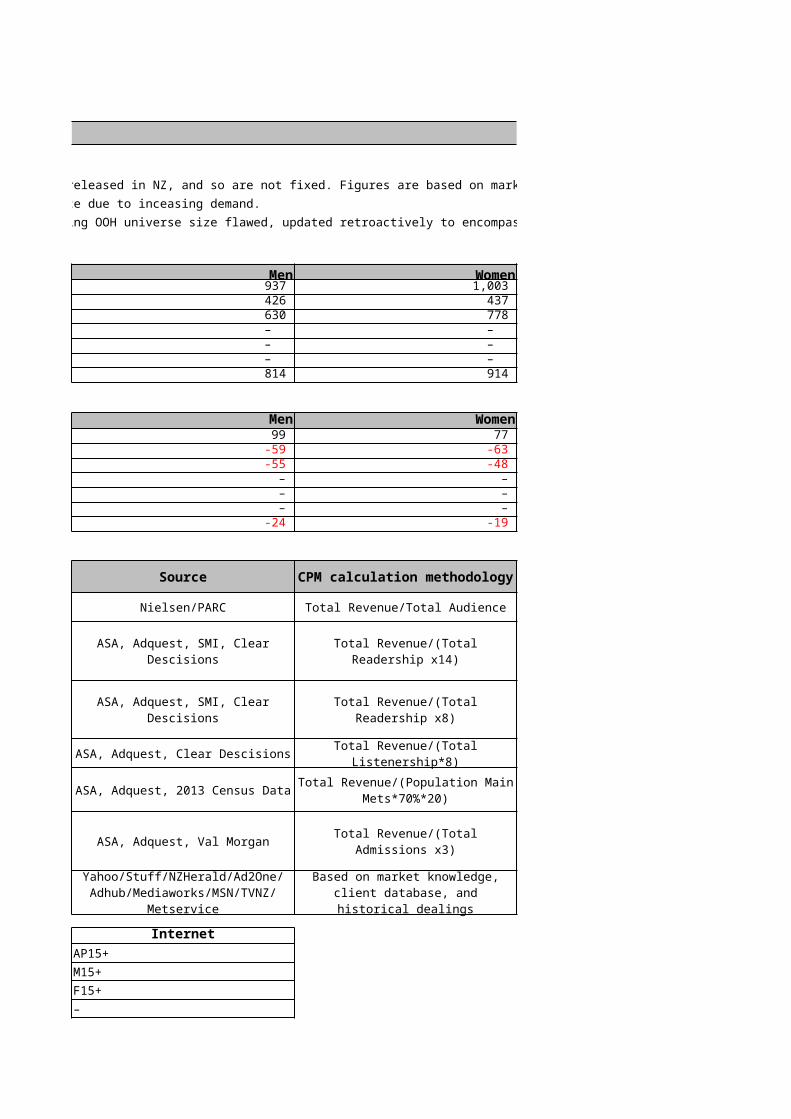

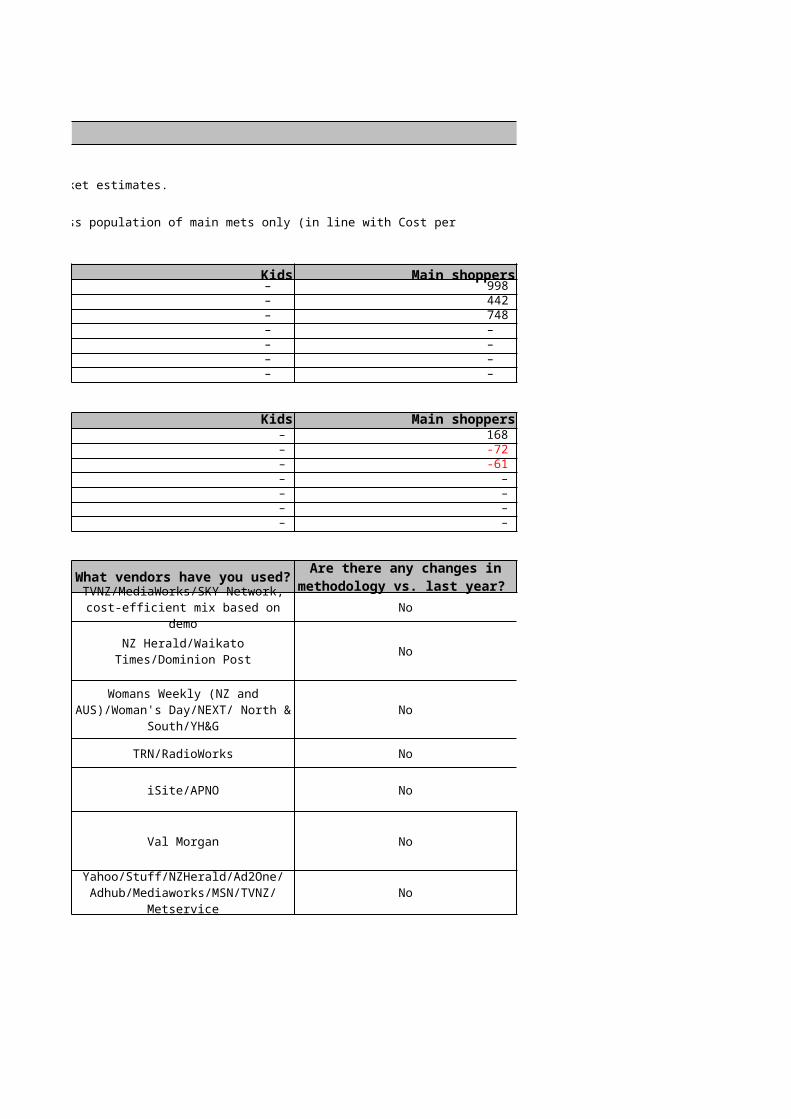

Country:NEW ZEALAND 2016NOTESGeneral Cost per thousand figures not released in NZ, and so are not fixed. Figures are based on market estimates.Internet Rising cost in internet ad space due to inceasing demand. Out of home 2016: Methodology for calculating OOH universe size flawed, updated retroactively to encompass population of main mets only (in line with Cost per Thousand calculations)

UNIVERSES (000s)Adults Men

Television 3,473 937 Newspapers 1,834 426 Magazines 2,730 630 Radio 2,616 – Out of home 1,872 – Cinema 1,814 – Internet 3,151 814

CHANGE IN UNIVERSE vs PREVIOUS YEAR (000s)Adults Men

Television 210 99 Newspapers -118 -59 Magazines -58 -55 Radio 18 – Out of home 0 – Cinema -337 – Internet 68 -24

SOURCES AND CPM CALCULATION METHODOLOGY

Medium Ad size Source

Television 30 seconds Nielsen/PARC

Newspapers A3, full colour

Magazines Full page colour

Radio 30 seconds ASA, Adquest, Clear Descisions

Out of home Various ASA, Adquest, 2013 Census Data

Cinema 30 seconds ASA, Adquest, Val Morgan

Internet Banner 468x60