farm adjustment to domestic policy reform: lessons from the new zealand experience allan rae...

TRANSCRIPT

Farm Adjustment to Domestic Policy Reform: Lessons from the

New Zealand Experience

Allan RaeDepartment of Applied and International

Economics

Massey University

New Zealand

What do the rich countries spend on their farmers?

• US$231 billion on directly supporting farm incomes in 2001 (OECD)

• This is 31% of value of farm production• Another US$54 billion spent on indirect

support (R&D, marketing, infrastructure etc)

• This total is slightly higher than in 1986-88• WTO controls largely ineffective

SPENDING by WTO DOMESTIC SUPPORT CATEGORIES: 1997

(US$ billion)

EU JAPAN USA Green 20.5 21.6 51.2 Blue 23.0 0 0 Amber (AMS) 56.6 25.8 6.2 TOTAL 100.7 47.7 58.3 Source: WTO G/AG/NG/S/12/Rev.1, 12 March 2001.

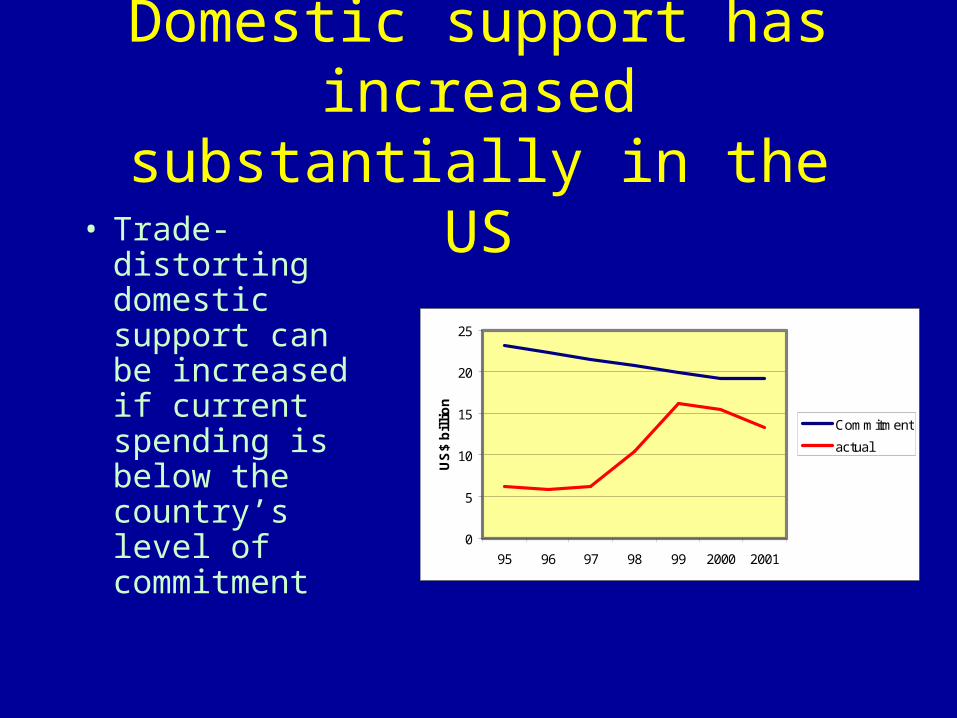

Domestic support has increased substantially in the US

• Trade-distorting domestic support can be increased if current spending is below the country’s level of commitment

0

5

10

15

20

25

95 96 97 98 99 2000 2001

US

$ b

illi

on

Commitment

actual

Increasing Domestic Support Payments can Further Distort

Trade

• ‘Amber box’ payments clearly impact on production levels and trade

• But ‘green box’ payments probably also do to some extent: – Increase farm investment– Increase ability to borrow for above– Farmers become less averse to risk– Protect farm from bankruptcy

Some Policies can be Inefficient in Raising Farm Net Incomes

• World prices may fall as a result• Farm costs rise as production expands• Capitalised into land values & captured by

landowners• Some capture by imperfectly-competitive off-farm

agents• Hinders allocation of labour & capital to off-farm

opportunities• So process becomes a ‘treadmill’

Increasing Pressures to Eliminate Domestic Support

• Enlargement of EU

• Possible return to US budget deficits

• Reduction of trade barriers, if achieved, puts more pressure on domestic support

• Sense of outrage from developing countries

• Increasing public awareness

Key Impediment to Reform is the Perceived Adjustment Problem

• Assumption that $100 reduction in support will:

$100 reduction in net farm household income

widespread bankruptcy

massive exodus from farming

Will argue, supported by NZ evidence, that above is extremely unlikely

Unlikely that household income falls by amount of support reduction

• Farmers adjust to price changes– Diversify– Reduce/substitute inputs– Change farmland use

• Increase farm productivity• Allocate larger share of labour/capital to off-farm

activities• Farm income a declining share of total household

income• Enhance competitiveness within marketing channel

The New Zealand Experience

• Little assistance to farming before mid-1960s

• BoP crises led to objective of increasing farm production & export revenues

• New programmes to stabilise/support prices, subsidise inputs, tax concessions, grants for land development & stocking

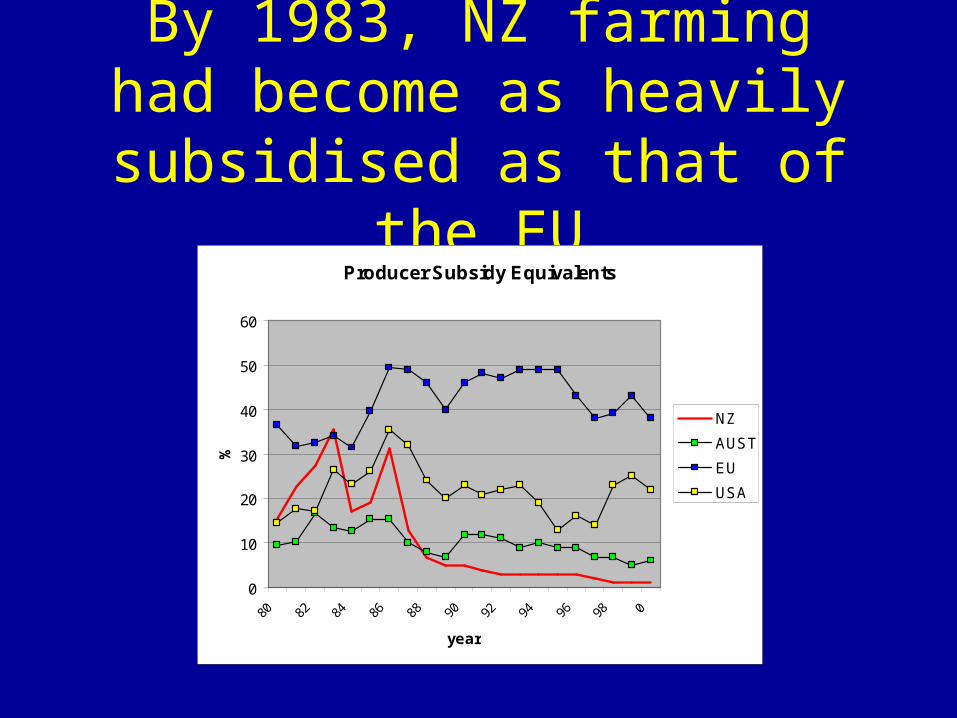

By 1983, NZ farming had become as heavily subsidised as

that of the EUProducer Subsidy Equivalents

0

10

20

30

40

50

60

80 82 84 86 88 90 92 94 96 98 0

year

%

NZ

AUST

EU

USA

Sheep and beef farms were the most heavily supported

Assistance to Pastoral Agriculture: Pre Deregulation

0

200

400

600

800

1000

1200

1400

80 81 82 83 84

year

Ass

ista

nce

(N

Z$m

illi

on

)

Sheepmeat

Wool

Beef

Dairy

By 1984, economic problems had become acute:

• Govt deficit reached 9% of GDP

• Debt servicing was 15% of govt spending

• Persistent current account deficit

• Over-valued exchange rate

• Excessive monetary growth

• Rapid inflation

• Heavy selling of $NZ

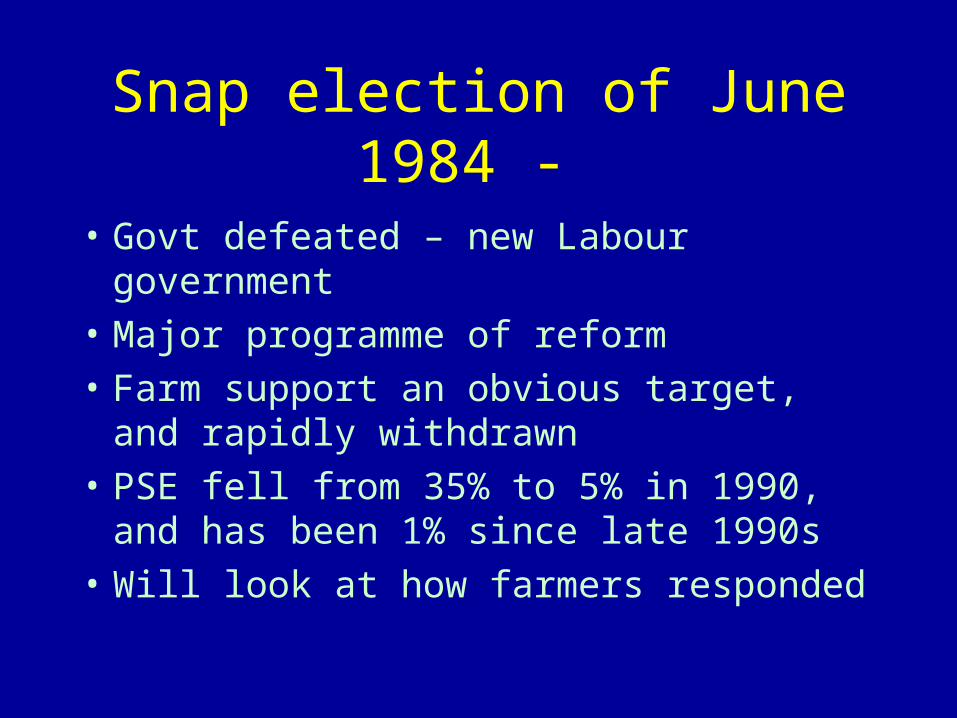

Snap election of June 1984 -

• Govt defeated – new Labour government

• Major programme of reform

• Farm support an obvious target, and rapidly withdrawn

• PSE fell from 35% to 5% in 1990, and has been 1% since late 1990s

• Will look at how farmers responded

But reforms weren’t limited to farming

• Immediate 20% devaluation in 1984• Removal of financial & exchange market controls• Free float of NZ$• Import quota system dismantled• Import tariffs progressively lowered• Privatisation of many govt. activities• Central Bank autonomy & inflation targets (1989)• Labour market deregulation (1991)

What happened to farm incomes in this environment?

• Focus on sheep & beef farms, as had been the most favoured by support

• Removal of support need not lead to permanent fall in income

Real Farm Profts: NZ 'All classes" Sheep & Beef Farm

0

20,000

40,000

60,000

80,000

100,000

120,000

76 78 80 82 84 86 88 90 92 94 96 9820

00

year ending

con

stan

t 19

94-9

5 N

Z$

per

far

m

Actions taken by farmers:Changes in product mix

• Transparent world price signals• Between 1984-89 –

– Sheep numbers fell from 70.3 to 64.6 million– Beef cattle numbers rose from 4.5 to 4.9

million– Deer numbers rose from 0.2 to 0.6 million

• Now, sheep = 44 million, and deer 1.8 million

Actions taken by farmers:Changes in land use

• Between 1984 & 1994, grassland area in sheep/beef fell by 1.93 mill. ha (-16%).

• Of this – – 1.08 mill. ha dairy, deer,vineyards, other

hort, urban uses– 0.85 mill. ha forestry, retirement of marginal

land

Actions taken by farmers:Changes in input use

• Fertiliser the major share of variable costs

• Use immediately fell from 15.5 kg / SU to 6-7 kg

• Fertiliser sales were 45% lower in 1988 than 3 years earlier

• Sales have since recovered

Actions taken by farmers:Rise in productivity

Aggregate Agriculture: Real output & inputs

90

100

110

120

130

140

150

73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93

year

Ind

ices

(19

72/7

3 =

100

)

output nonfactor inputs capital labour land

Agricultural TFP rose

• By 1.8% p.a. 1972-84 (pre-deregulation)

• By 4.0% 1985-98 (post-deregulation)

• Such gains aided farming to weather financial stresses of deregulation

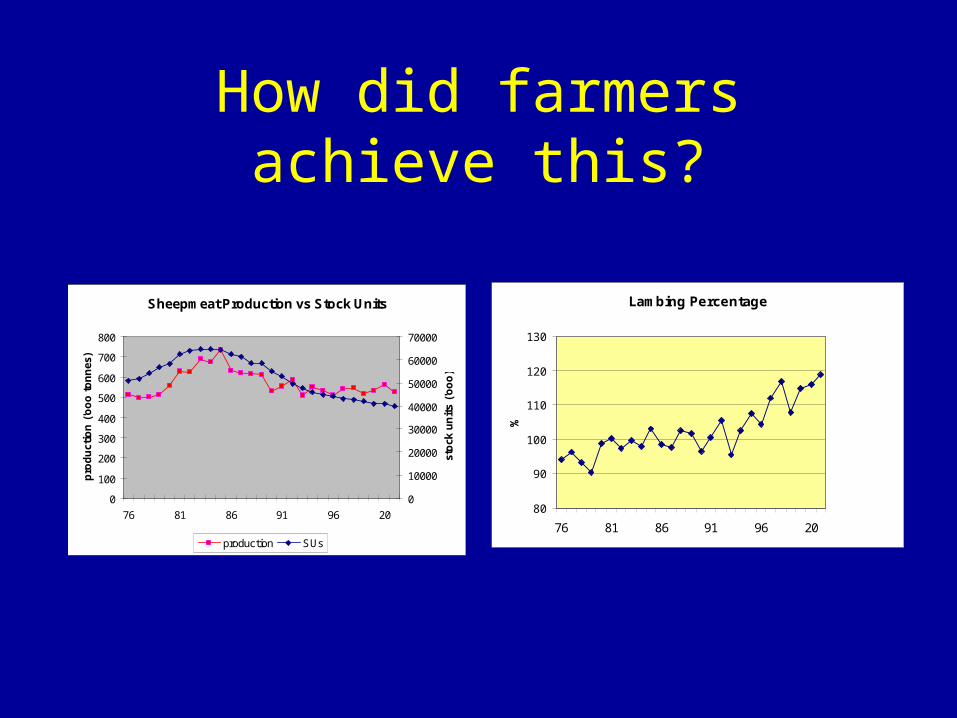

How did farmers achieve this?

Sheepmeat Production vs Stock Units

0

100

200

300

400

500

600

700

800

76 81 86 91 96 20

pro

du

ctio

n (

'oo

o t

on

nes

)

0

10000

20000

30000

40000

50000

60000

70000

sto

ck u

nit

s ('o

oo

)

production SUs

Lambing Percentage

80

90

100

110

120

130

76 81 86 91 96 20%

…and something similar for beef cattle

Beef Production vs Stock Units

0

100

200

300

400

500

600

700

76 81 86 91 96 20

pro

du

ctio

n (

'000

to

nn

es b

on

e-in

)

0

5000

10000

15000

20000

25000

30000

35000

sto

ck u

nit

s ('0

00)

production SU

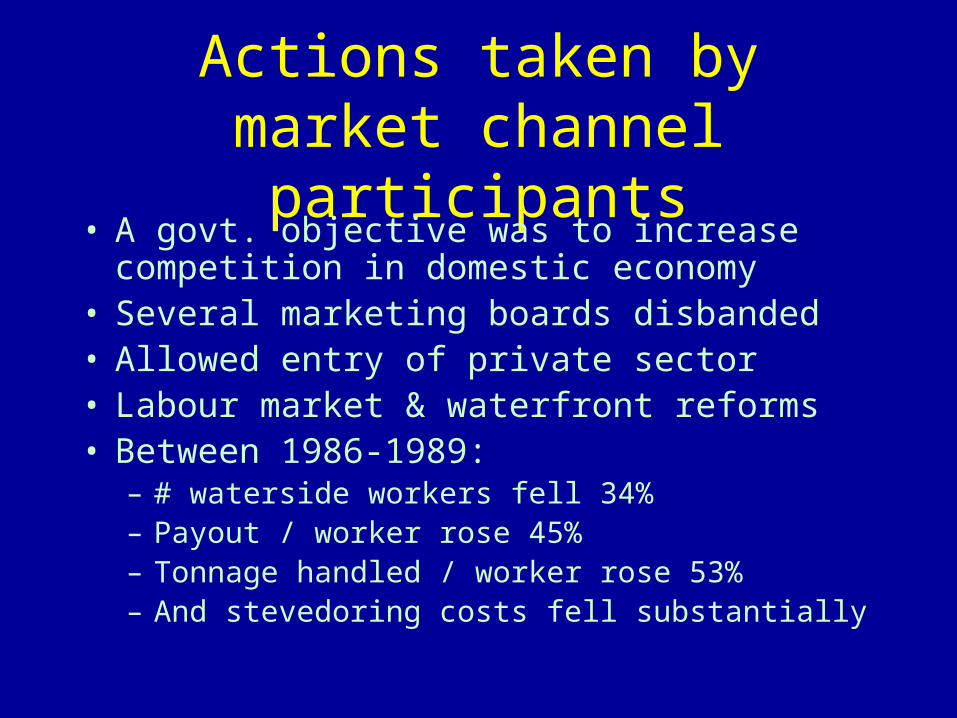

Actions taken by market channel participants

• A govt. objective was to increase competition in domestic economy

• Several marketing boards disbanded• Allowed entry of private sector• Labour market & waterfront reforms• Between 1986-1989:

– # waterside workers fell 34%– Payout / worker rose 45%– Tonnage handled / worker rose 53%– And stevedoring costs fell substantially

Impacts on meat processing sector

• 1984-94: 25% processors closed– As livestock numbers fell & new technology

was required

• Replaced by smaller hi-tech plants

• Comparing 1995 with 1983– Bull beef

• New York prices 12% lower

• Farm price 40% higher

Government facilitation of farm adjustment

• Farmers weren’t protected by existing social welfare benefits

• Special Assistance to Farming Programme (’86 – ’89) gave equivalent benefit

• Exit Grants Scheme 1988• Loan discounting scheme (debt restructuring and some

write-off)• About 20% farm debt written off and 5% farms were

sold• Govt worked with local support groups (advice &

counselling)

Lessons

• Farmers can overcome subsidy reduction• Helped by reforms in other sectors, and macro• Lower incomes short-term• Enhanced efficiency & productivity• Adjustment benefits not always rapid• Role for govt. adjustment assistance• Positive environmental impacts