fab investment outlook – foundry, memory and led market - clark tseng.pdf · fab investment...

TRANSCRIPT

Fab Investment Outlook – Foundry, Memory and LED

Clark Tseng, Sr. Research Manager, SEMI

Vietnam Semiconductor Strategy Summit September 16-17, 20214

Outline

Fab Investment & Capacity Trend Memory and Foundry Investment Outlook LED Investment Outlook Summary

Economic Trends: GDP and Some Indicators

3 July, 2014

Source: IMF and Others, July 2014

Dow Jones Industrial Average hits a new record of over 17,000 points July 3, 2014

US unemployment rate: 6-year low dropping to 6.1 (lowest since 2008) Source: Reuters July 3, 2014)

Consumer Comfort Index improving 2011: -47 2012: -38 2013: -31 2014: -29 Source: Bloomberg (6-24-14)

S&P 500 surges to new record with over 1985 July 3, 2014

YoY in % 2011 2012 2013 2014 2015Contribution to World in 2012

World 3.9 3.2 3.0 3.4 3.9Advanced Economies: 1.7 1.4 1.3 2.2 2.3USA (update 6-16-14) 1.8 2.8 1.9 1.7 3.0 23.6Euro Area: 1.5 -0.7 -0.5 1.2 1.5 18.4 Germany 3.1 0.9 0.5 1.7 1.6France 2.0 0.0 0.3 1.0 1.5

Japan -0.6 1.4 1.5 1.4 1.0 7.4UK 1.0 0.3 1.8 2.9 2.5 4.1

Emerging Markets: 6.2 5.0 4.7 4.9 5.3China 9.3 7.7 7.7 7.4 7.1 8.1India 6.3 4.7 4.4 5.4 6.4 2.4Brazil 2.7 1.0 2.3 1.3 2.7

GDP World others 2011 2012 2013 2014 2015 2016World Bank (June 14) 2.8 2.5 2.4 2.8 3.4 3.5IC Insight (Jan 14) 3.2 2.7 2.8 3.4Henderson (May 14) 3.0 2.5 2.4 3.0 3.6 3.7DuPont (Jan 14) 3.0 2.5 2.4 3.1UBS (Apr 14) 3.2 2.7 2.5 3.2 3.4

Economic Trends 2014 Semiconductor Revenue Forecasts

August, 2014

Economic Trends 2015 Semiconductor Revenue Forecasts

August, 2014

Fab Investments & Capacity

Fab Construction Spending

Construction Spending by Segments - Led by Foundries

Stronger Investment Momentum in 2014 and 2015

Fab Equipment Spending: Industry Cycles

10

Investment in Fabs (Front End): Construction + Equipping

13

Most (not all) construction spending goes into new facilities.

Low Single Digit Capacity Growth

~10.7 M 200mm equiv./month

Shift of Capacity Share (including discrete)

~19.4 M 200mm equiv./month

Source: SEMI World Fab Forecast

Foundry and Memory Lead Capacity Growth

Capacity: Fab Equipment Spending vs Capacity

17

SEMI World Fab Forecast: Since downturn the industry

spends more money on upgrading existing facilities

Average change rates 2003 – 2007 2010 - 2014 2011-2015*

Fab Equipment 18% 29% 5%

Fab Capacity 17% 4% 3%

* 2011-2015: excluding 2010 because fab equipment growth was unusual high

Micron Feb 2014: Industry bit supply growth slowing:

DRAM: 49% in 2010 to 24% in 2015

NAND: 74% in 2010 to 45% in 2015

Capacity: Begin Volume Production Per Node

18

Forecast 3Q14

Changing Landscape: The Industry Consolidates

19

Number may not ad up to 100 due to rounding

20

Memory and Foundry Investment Outlook

Fab Equipment Spending- Driven by Foundry and Memory

Both NAND and DRAM See Strong Growth

Source: SEMI World Fab Forecast, August 2014

Foundry Investment by Region

Source: SEMI World Fab Forecast, August 2014

LED Fab Investments

Global Revenues for Packaged LEDs 2013 - 2018

LEDs in Lighting

27% CAGR

Source: SEMI Opto/LED Fab Forecast, August 2014

LED Dedicated Fabs Changing LED Landscape

4 5 9

7 16 74

1 2 10

7 9 21 China

Japan

S. Korea 3 8 16

SEAsia 0 0 4

Taiwan 14 24 44

2001

36

127,124

Year (begin operation)

Total count of LED fabs*

Capacity in 4-inch EQs w/m

2006

64

376,400

2015

178 (152 EPI)

~3,100,000

Americas Europe/Mideast

*Fab number includes both LED epitaxy and chip facilities.

LED Fab Capacity by Region, 2014

Worldwide LED Epitaxy capacity to reach 2.6 M in 2014 (4” equivalent per month)

Source: SEMI Opto/LED Fab Forecast , August 2014

World LED Capacity Trend LED Epitaxy capacity (4” equivalent per month)

Source: SEMI Opto/LED Fab Forecast , August 2014

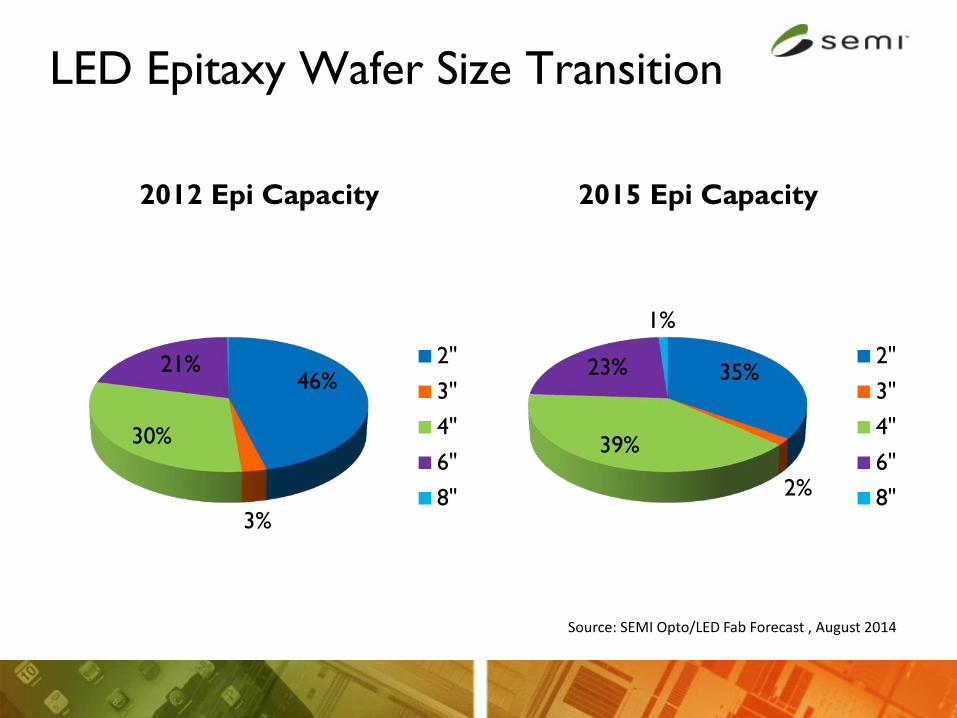

LED Epitaxy Wafer Size Transition

46%

3%

30%

21%

2012 Epi Capacity

2"

3"

4"

6"

8"

35%

2%

39%

23%

1%

2015 Epi Capacity

2"

3"

4"

6"

8"

Source: SEMI Opto/LED Fab Forecast , August 2014

LED Wafer Fab Equipment Spending

$1,931

$2,647

$1,530

$1,102 $1,189$1,401

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2010 2011 2012 2013 2014 2015

LED Equipment Spending(US$ millions)

Source: SEMI Opto/LED Fab Forecast, August 2014

Equipment Spending by Region China Percent of Global Spending – 40%

0

200

400

600

800

1000

1200

1400

EU-ME Americas Japan Korea Taiwan China

2011 2012 2013 2014 2015

Equipment Spending By Region (in millions) 2011 - 2015

Source: SEMI Opto/LED Fab Forecast, August 2014

Southeast Asia Market – Key Facts

2014 Status

Installed Fab Capacity ~1.3 million 200mm wafers/month

Packaging & Test Strong presence of subcon and IDM facilities in the region

(including 20 assembly & test operations in Singapore)

Semiconductor Materials ~$6.7 billion

Semiconductor Equipment ~$2.0 billion range

Source: SEMI World Fab Forecast, WWSEMS, & MMDS

Summary

Summary

Overall Outlook - Positive outlook for the global economy in 2014 - Mid to high single-digit revenue growth for semiconductors

Fab Investment & Capacity - Fab investment is expected to show continuous growth into 2015

led by foundry and memory manufacturers. - Both NAND Flash and DRAM are seeing strong investment

rebound. - Mobility, wireless, and connectivity remain the growth engines.

LED Investment - Lighting applications to drive LED market growth. - LED investment to recover in 2015.