expansion and deepening of asean integration with...

TRANSCRIPT

Talking ASEAN on RCEP ProgressJakarta, March, 2014

Expansion and Deepening of ASEAN Integrationwith the Broader Region by Imam Pambagyo

1

REGIONAL COMPREHENSIVE ECONOMIC PARTNERSHIP Expansion and Deepening of ASEAN Integration with the Broader Region

Iman Pambagyo, Directorate-General for International Trade Cooperation

April 2014

2

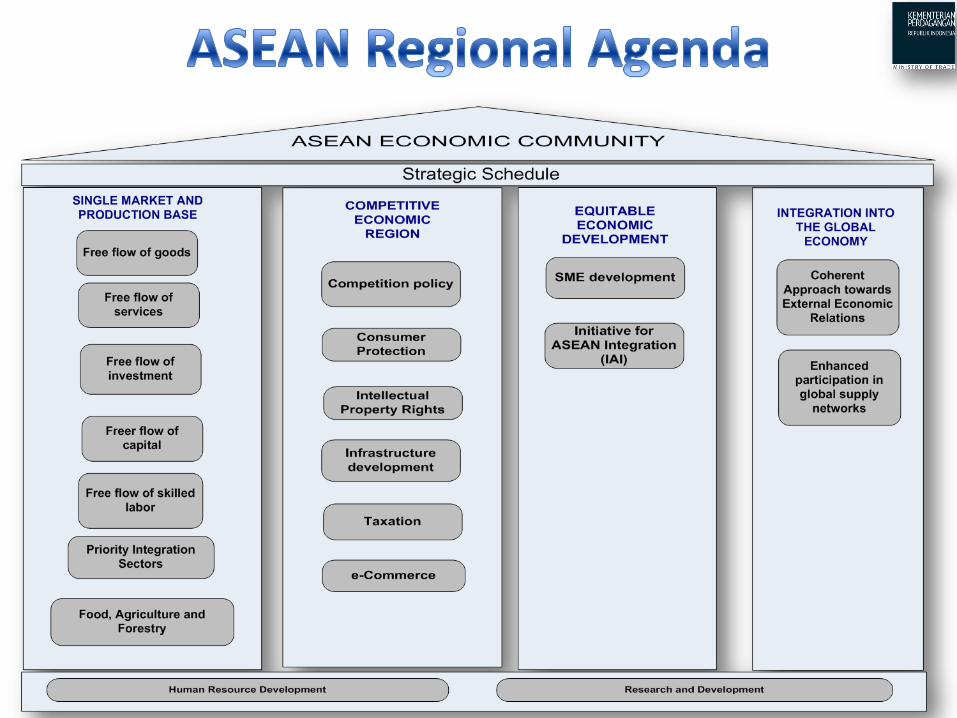

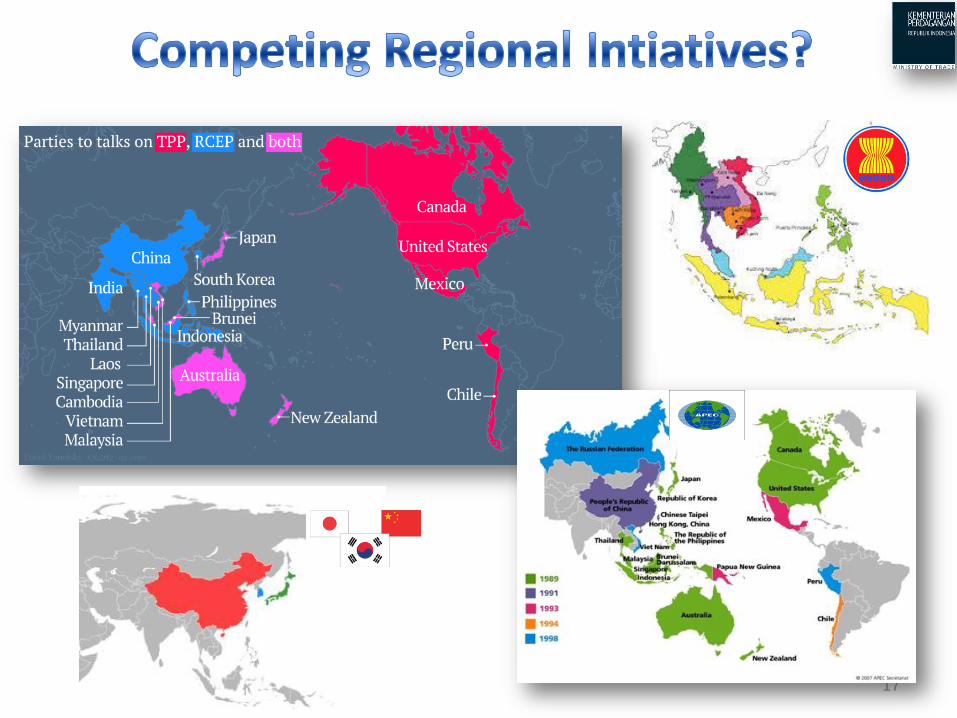

There are three mega-regional initiatives taking shape:

- Regional Comprehensive Economic Partnership (16) - Trans-Pacific Partnership (12) - Trans-Atlantic Trade & Investment Partnership (29) What will the region look like in future? Should ASEAN and Indonesia take an active role in reshaping the region?

3

4

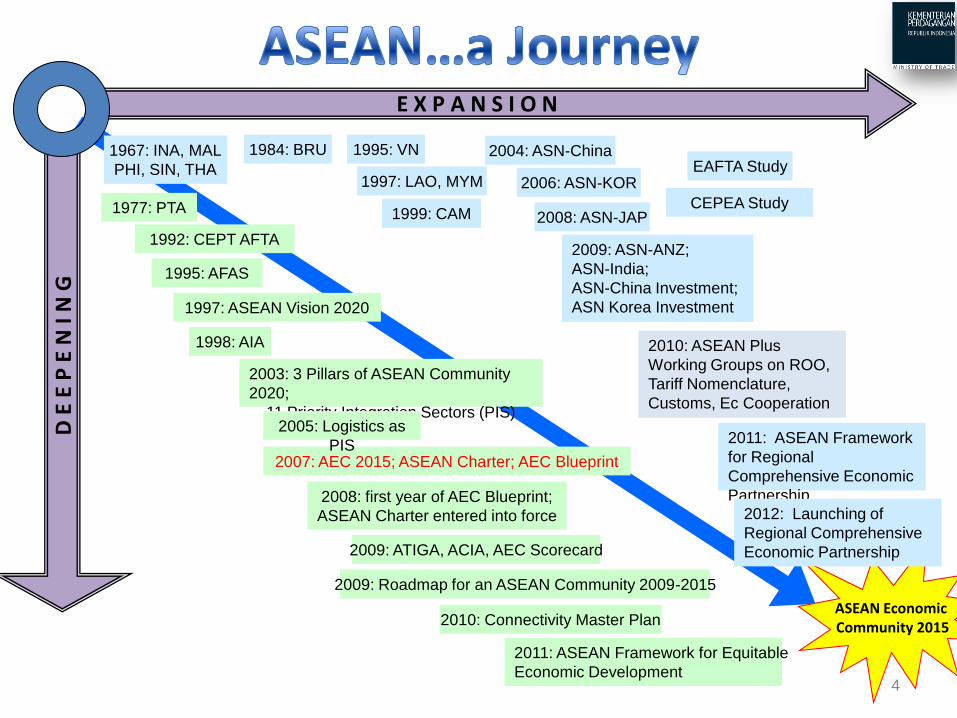

E X P A N S I O N

D E

E P

E N

I N

G

1967: INA, MAL

PHI, SIN, THA

1977: PTA

1992: CEPT AFTA

1984: BRU 1995: VN

1997: LAO, MYM

1999: CAM

1995: AFAS

2004: ASN-China

2006: ASN-KOR

2008: ASN-JAP

2009: ASN-ANZ;

ASN-India;

ASN-China Investment;

ASN Korea Investment

EAFTA Study

CEPEA Study

1997: ASEAN Vision 2020

1998: AIA

2003: 3 Pillars of ASEAN Community

2020;

11 Priority Integration Sectors (PIS)

2007: AEC 2015; ASEAN Charter; AEC Blueprint

2008: first year of AEC Blueprint;

ASEAN Charter entered into force

2009: ATIGA, ACIA, AEC Scorecard

ASEAN Economic Community 2015

2005: Logistics as

PIS

2010: ASEAN Plus

Working Groups on ROO,

Tariff Nomenclature,

Customs, Ec Cooperation

2010: Connectivity Master Plan

2011: ASEAN Framework

for Regional

Comprehensive Economic

Partnership

2011: ASEAN Framework for Equitable

Economic Development

2009: Roadmap for an ASEAN Community 2009-2015

2012: Launching of

Regional Comprehensive

Economic Partnership

5

6

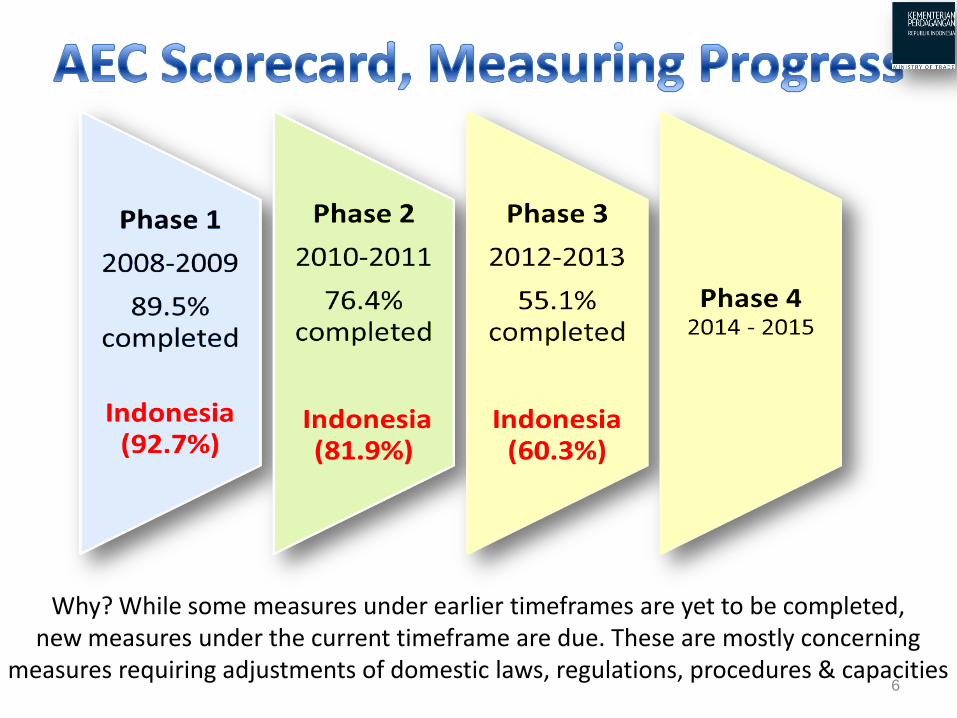

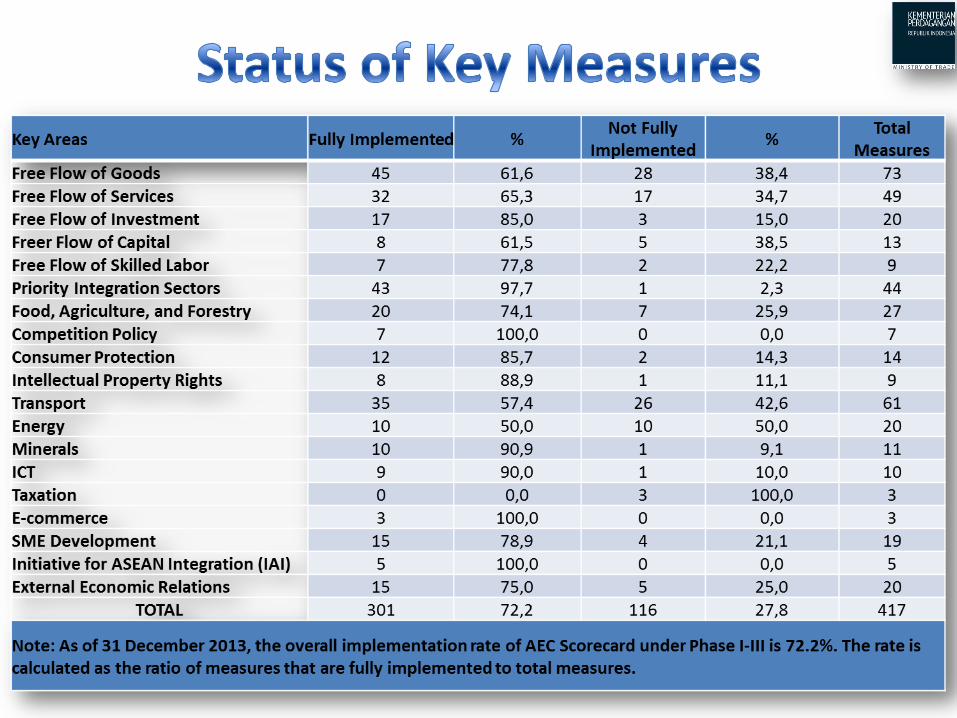

Why? While some measures under earlier timeframes are yet to be completed, new measures under the current timeframe are due. These are mostly concerning

measures requiring adjustments of domestic laws, regulations, procedures & capacities

7

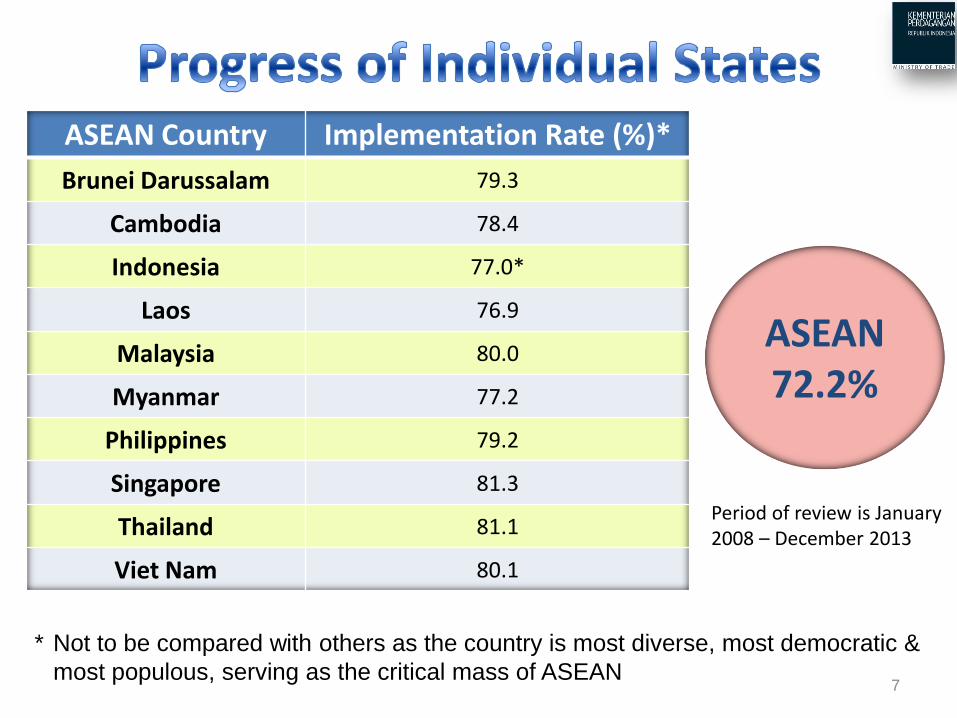

ASEAN Country Implementation Rate (%)*

Brunei Darussalam 79.3

Cambodia 78.4

Indonesia 77.0*

Laos 76.9

Malaysia 80.0

Myanmar 77.2

Philippines 79.2

Singapore 81.3

Thailand 81.1

Viet Nam 80.1

ASEAN 72.2%

Period of review is January 2008 – December 2013

* Not to be compared with others as the country is most diverse, most democratic &

most populous, serving as the critical mass of ASEAN

8

9

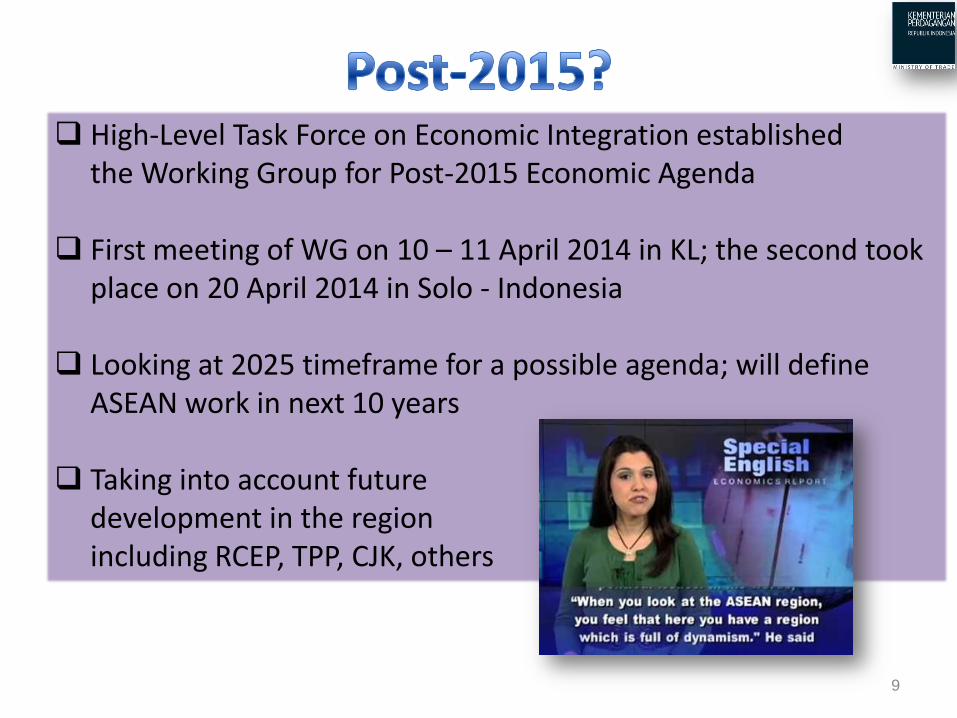

High-Level Task Force on Economic Integration established the Working Group for Post-2015 Economic Agenda First meeting of WG on 10 – 11 April 2014 in KL; the second took place on 20 April 2014 in Solo - Indonesia

Looking at 2025 timeframe for a possible agenda; will define ASEAN work in next 10 years Taking into account future development in the region including RCEP, TPP, CJK, others

10

11

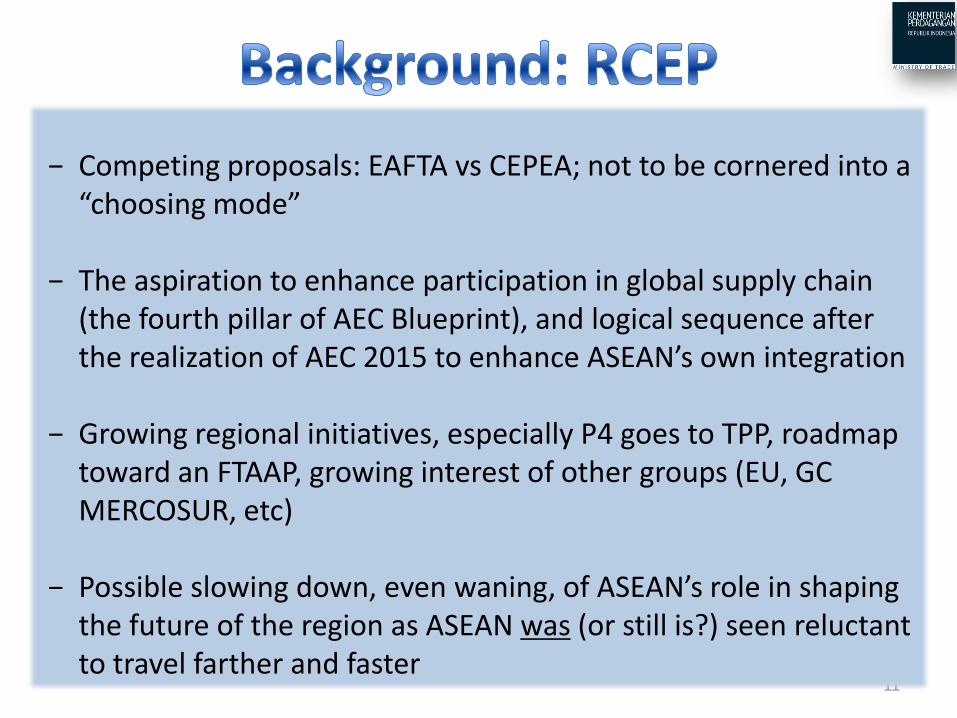

− Competing proposals: EAFTA vs CEPEA; not to be cornered into a

“choosing mode” − The aspiration to enhance participation in global supply chain

(the fourth pillar of AEC Blueprint), and logical sequence after the realization of AEC 2015 to enhance ASEAN’s own integration

− Growing regional initiatives, especially P4 goes to TPP, roadmap

toward an FTAAP, growing interest of other groups (EU, GC MERCOSUR, etc)

− Possible slowing down, even waning, of ASEAN’s role in shaping

the future of the region as ASEAN was (or still is?) seen reluctant to travel farther and faster

12

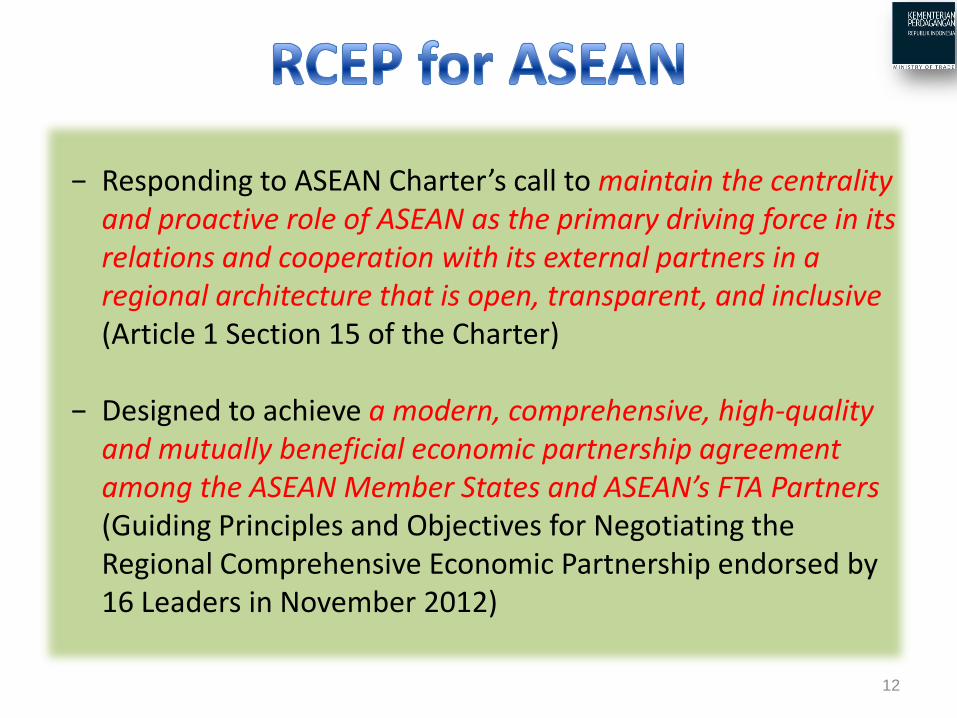

− Responding to ASEAN Charter’s call to maintain the centrality and proactive role of ASEAN as the primary driving force in its relations and cooperation with its external partners in a regional architecture that is open, transparent, and inclusive (Article 1 Section 15 of the Charter) − Designed to achieve a modern, comprehensive, high-quality and mutually beneficial economic partnership agreement among the ASEAN Member States and ASEAN’s FTA Partners (Guiding Principles and Objectives for Negotiating the Regional Comprehensive Economic Partnership endorsed by 16 Leaders in November 2012)

13

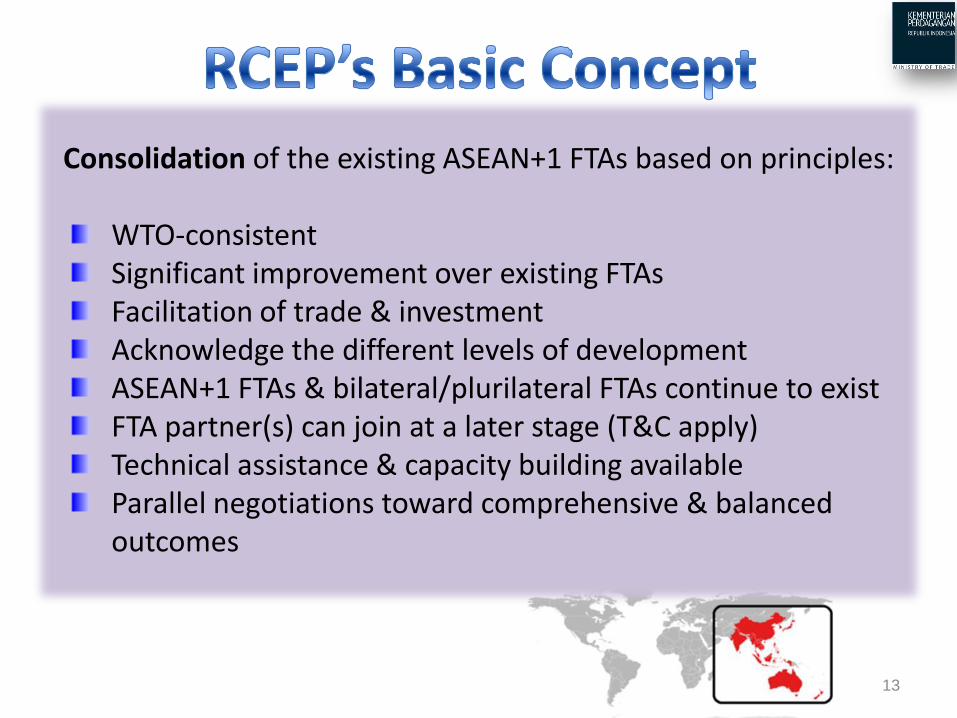

Consolidation of the existing ASEAN+1 FTAs based on principles:

WTO-consistent Significant improvement over existing FTAs Facilitation of trade & investment Acknowledge the different levels of development ASEAN+1 FTAs & bilateral/plurilateral FTAs continue to exist FTA partner(s) can join at a later stage (T&C apply) Technical assistance & capacity building available Parallel negotiations toward comprehensive & balanced

outcomes

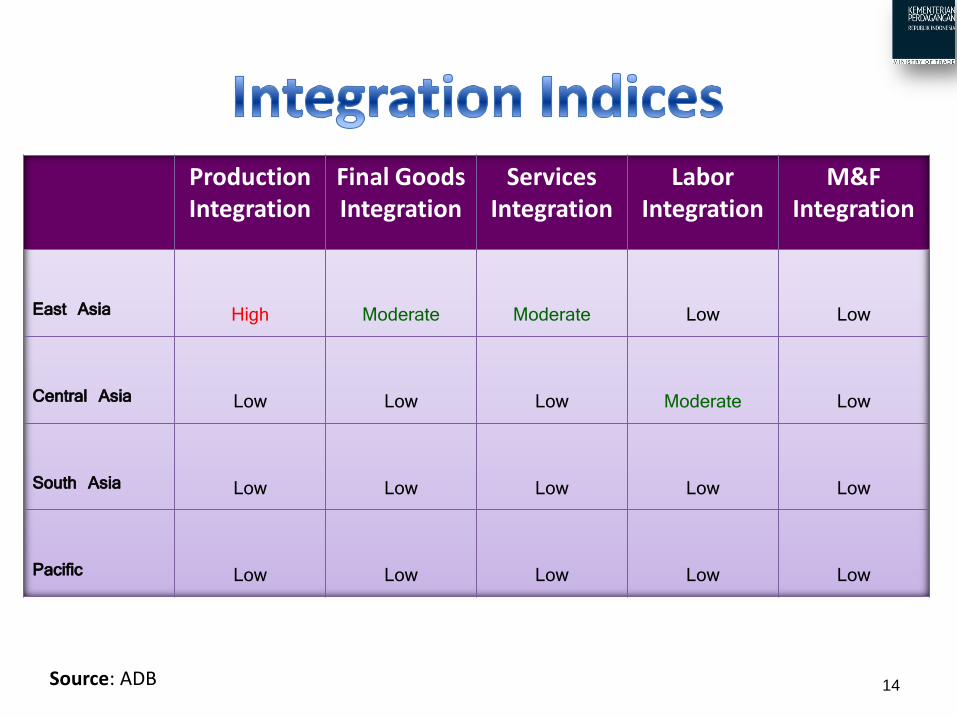

Production Integration

Final Goods Integration

Services Integration

Labor Integration

M&F Integration

East Asia

High

Moderate

Moderate

Low

Low

Central Asia

Low

Low

Low

Moderate

Low

South Asia

Low

Low

Low

Low

Low

Pacific

Low

Low

Low

Low

Low

Source: ADB 14

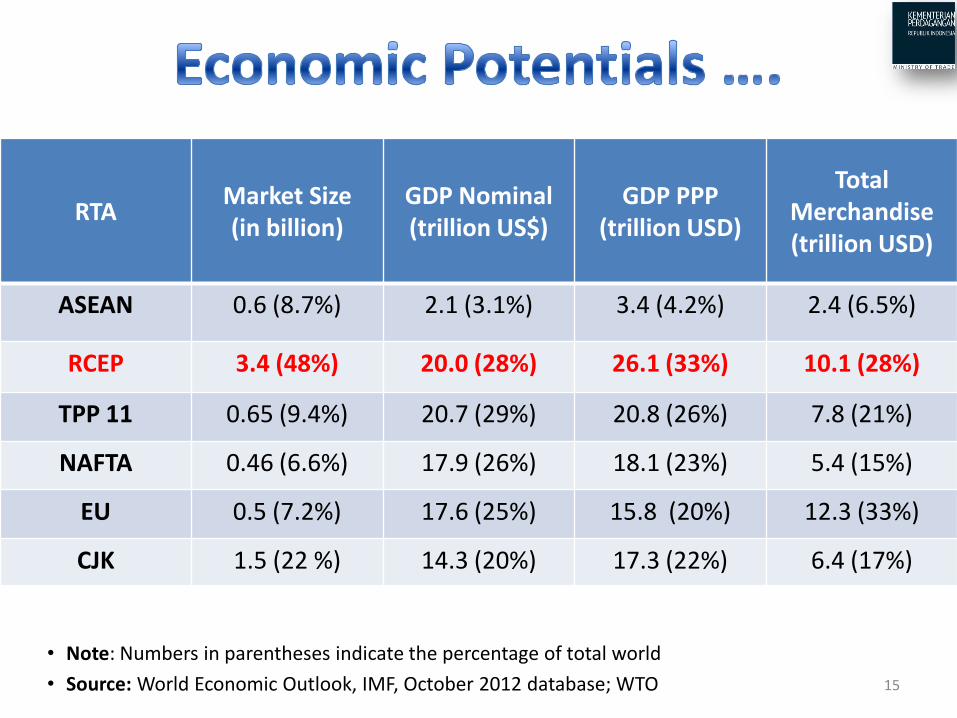

RTA Market Size (in billion)

GDP Nominal (trillion US$)

GDP PPP (trillion USD)

Total Merchandise (trillion USD)

ASEAN 0.6 (8.7%) 2.1 (3.1%) 3.4 (4.2%) 2.4 (6.5%)

RCEP 3.4 (48%) 20.0 (28%) 26.1 (33%) 10.1 (28%)

TPP 11 0.65 (9.4%) 20.7 (29%) 20.8 (26%) 7.8 (21%)

NAFTA 0.46 (6.6%) 17.9 (26%) 18.1 (23%) 5.4 (15%)

EU 0.5 (7.2%) 17.6 (25%) 15.8 (20%) 12.3 (33%)

CJK 1.5 (22 %) 14.3 (20%) 17.3 (22%) 6.4 (17%)

15

• Note: Numbers in parentheses indicate the percentage of total world

• Source: World Economic Outlook, IMF, October 2012 database; WTO

16

17

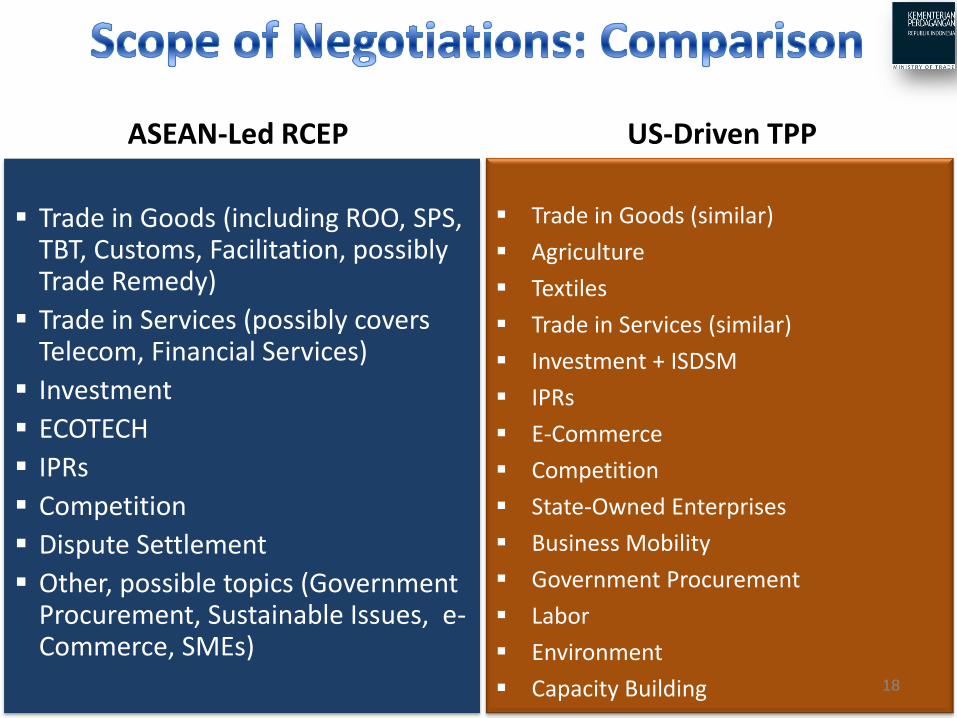

ASEAN-Led RCEP

Trade in Goods (including ROO, SPS, TBT, Customs, Facilitation, possibly Trade Remedy)

Trade in Services (possibly covers Telecom, Financial Services)

Investment

ECOTECH

IPRs

Competition

Dispute Settlement

Other, possible topics (Government Procurement, Sustainable Issues, e-Commerce, SMEs)

US-Driven TPP

Trade in Goods (similar)

Agriculture

Textiles

Trade in Services (similar)

Investment + ISDSM

IPRs

E-Commerce

Competition

State-Owned Enterprises

Business Mobility

Government Procurement

Labor

Environment

Capacity Building

18

19

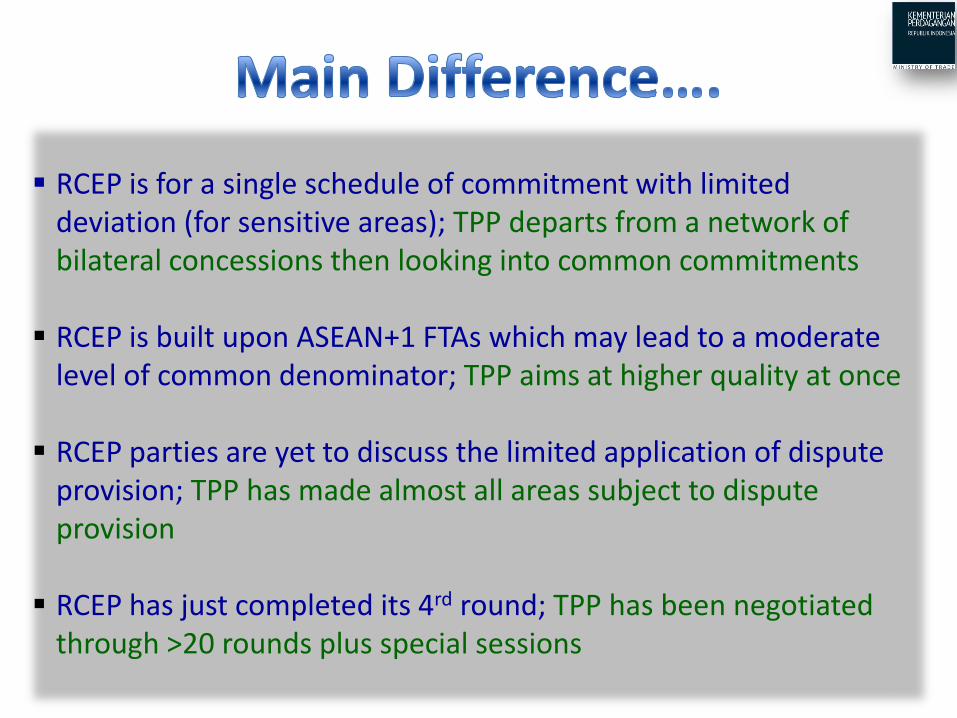

RCEP is for a single schedule of commitment with limited deviation (for sensitive areas); TPP departs from a network of bilateral concessions then looking into common commitments RCEP is built upon ASEAN+1 FTAs which may lead to a moderate level of common denominator; TPP aims at higher quality at once RCEP parties are yet to discuss the limited application of dispute provision; TPP has made almost all areas subject to dispute provision RCEP has just completed its 4rd round; TPP has been negotiated through >20 rounds plus special sessions

20

But, how will the RCEP benefit its

Members?

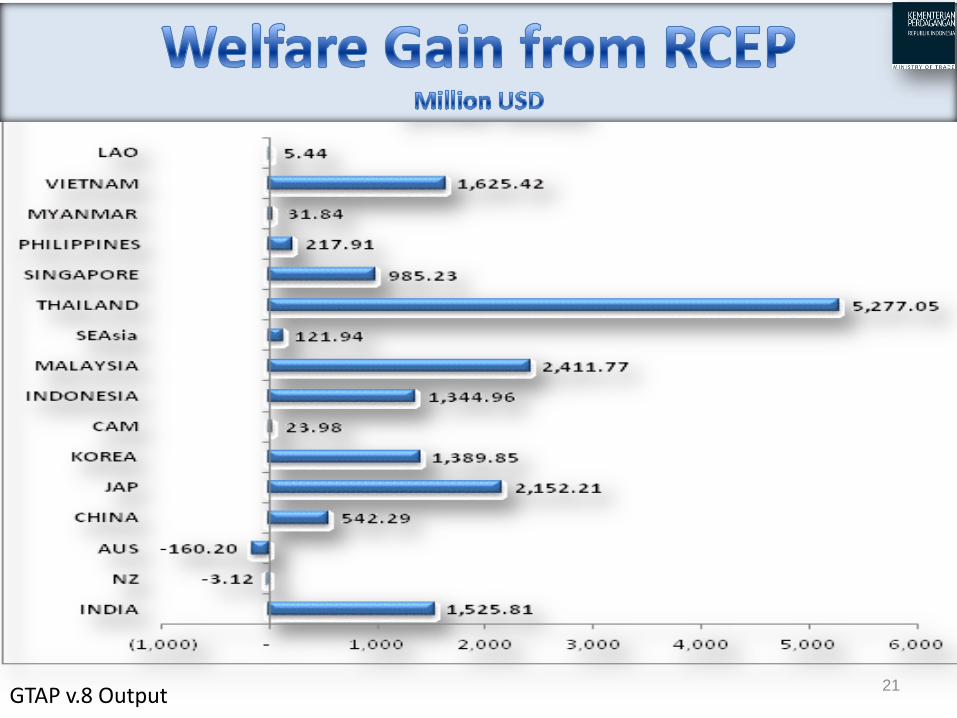

GTAP v.8 Output 21

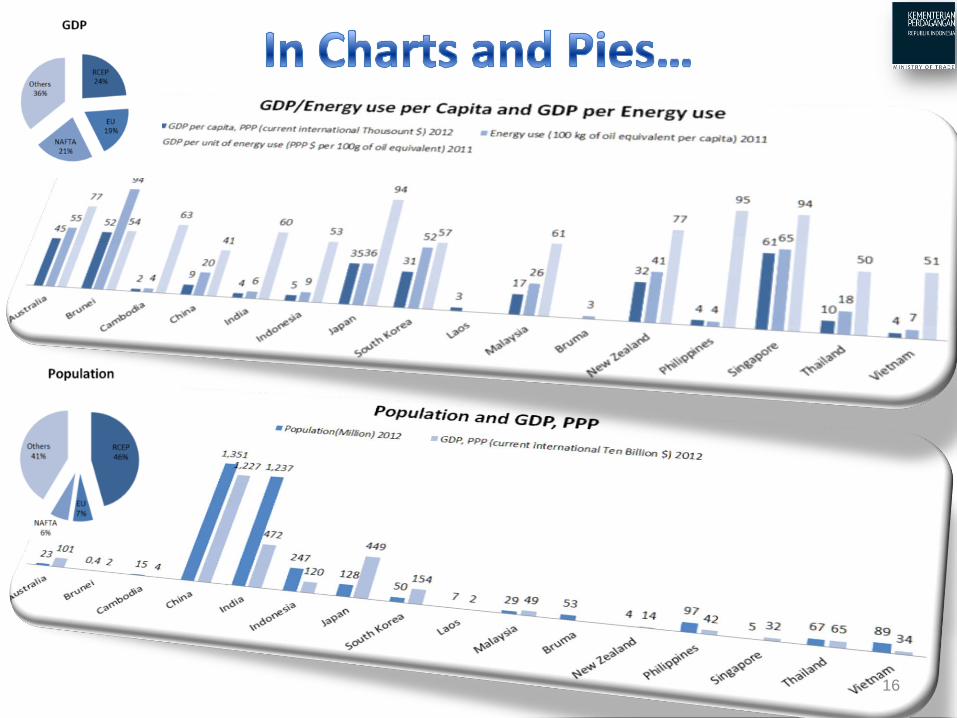

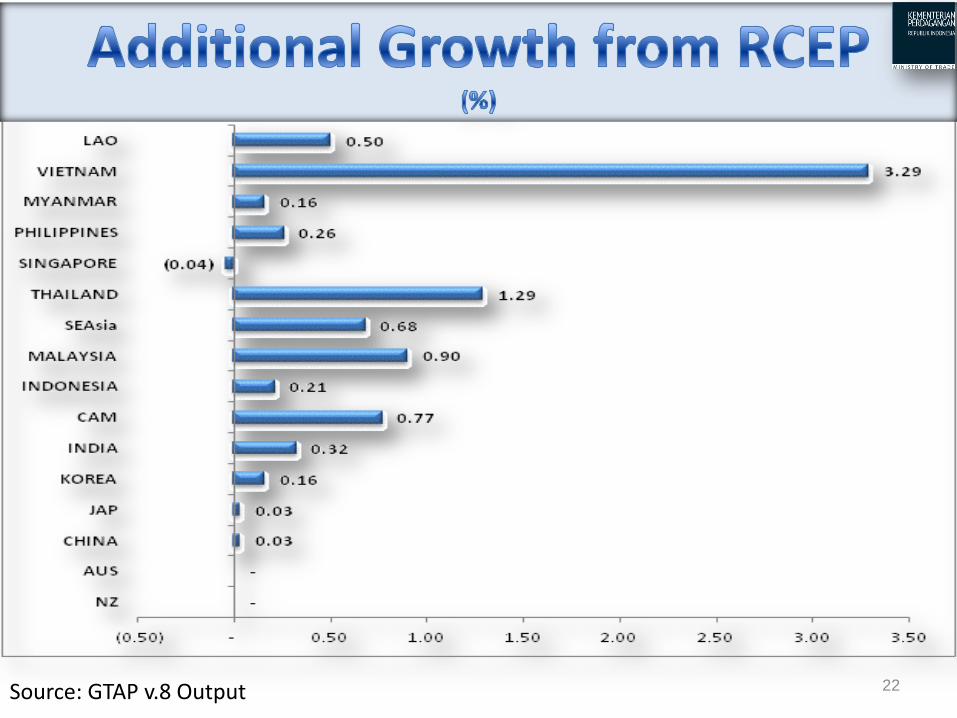

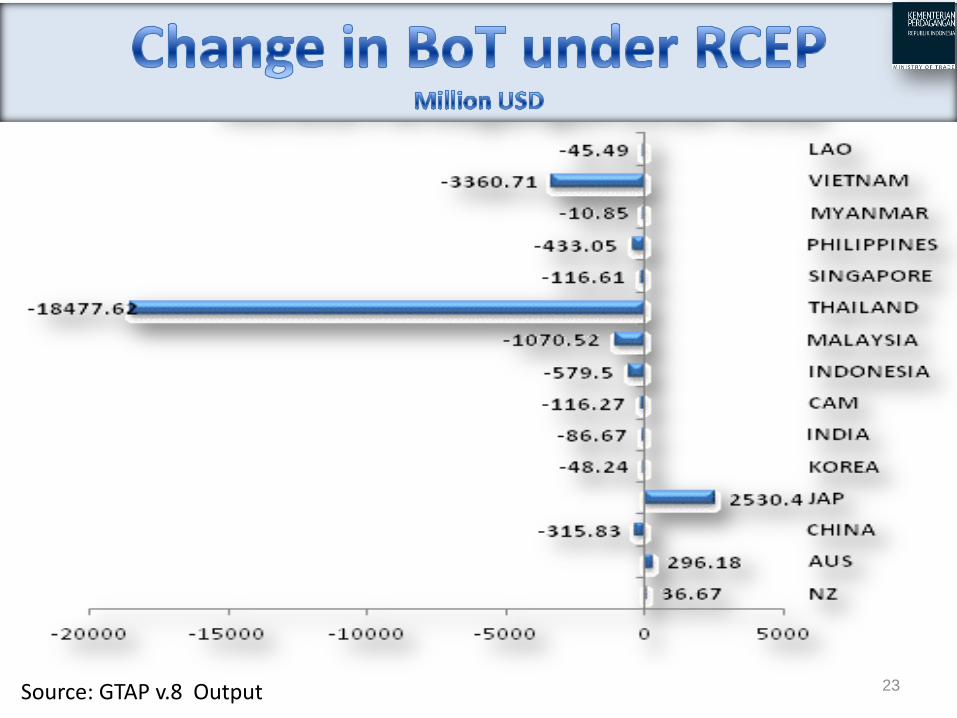

Source: GTAP v.8 Output 22

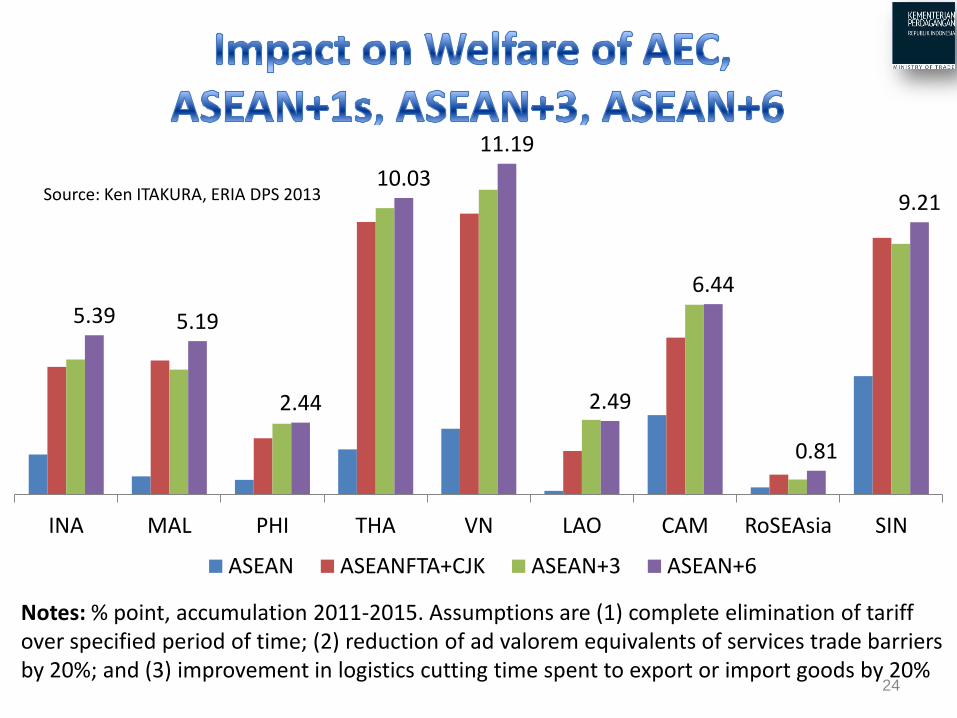

Source: GTAP v.8 Output 23

24

5.39 5.19

2.44

10.03

11.19

2.49

6.44

0.81

9.21

INA MAL PHI THA VN LAO CAM RoSEAsia SIN

ASEAN ASEANFTA+CJK ASEAN+3 ASEAN+6

Source: Ken ITAKURA, ERIA DPS 2013

Notes: % point, accumulation 2011-2015. Assumptions are (1) complete elimination of tariff over specified period of time; (2) reduction of ad valorem equivalents of services trade barriers by 20%; and (3) improvement in logistics cutting time spent to export or import goods by 20%

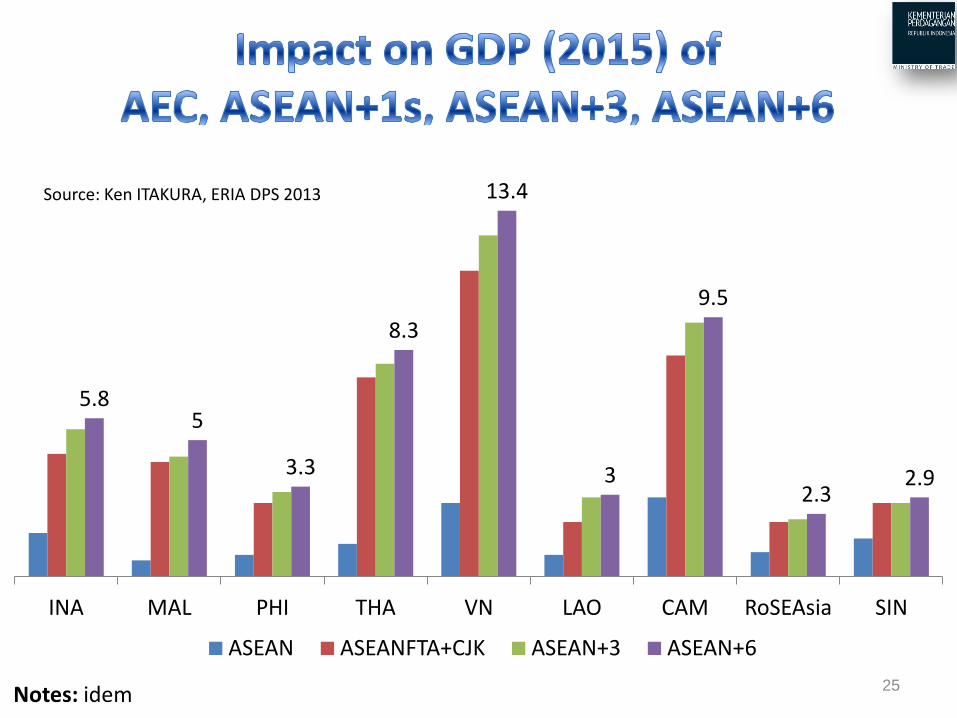

25

5.8 5

3.3

8.3

13.4

3

9.5

2.3 2.9

INA MAL PHI THA VN LAO CAM RoSEAsia SIN

ASEAN ASEANFTA+CJK ASEAN+3 ASEAN+6

Source: Ken ITAKURA, ERIA DPS 2013

Notes: idem

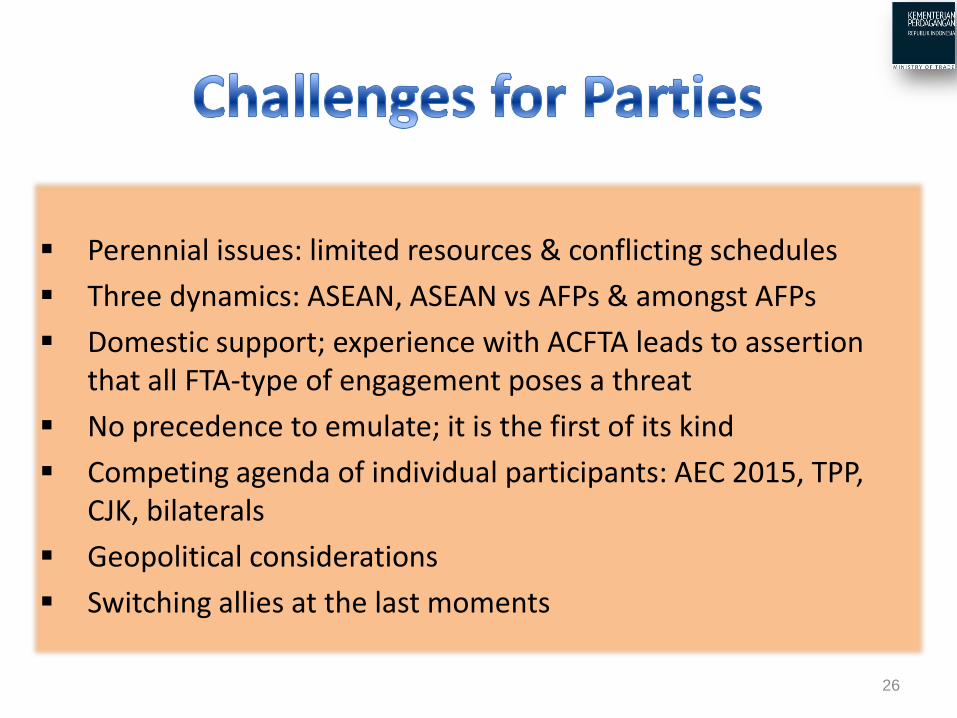

Perennial issues: limited resources & conflicting schedules

Three dynamics: ASEAN, ASEAN vs AFPs & amongst AFPs

Domestic support; experience with ACFTA leads to assertion that all FTA-type of engagement poses a threat

No precedence to emulate; it is the first of its kind

Competing agenda of individual participants: AEC 2015, TPP, CJK, bilaterals

Geopolitical considerations

Switching allies at the last moments

26

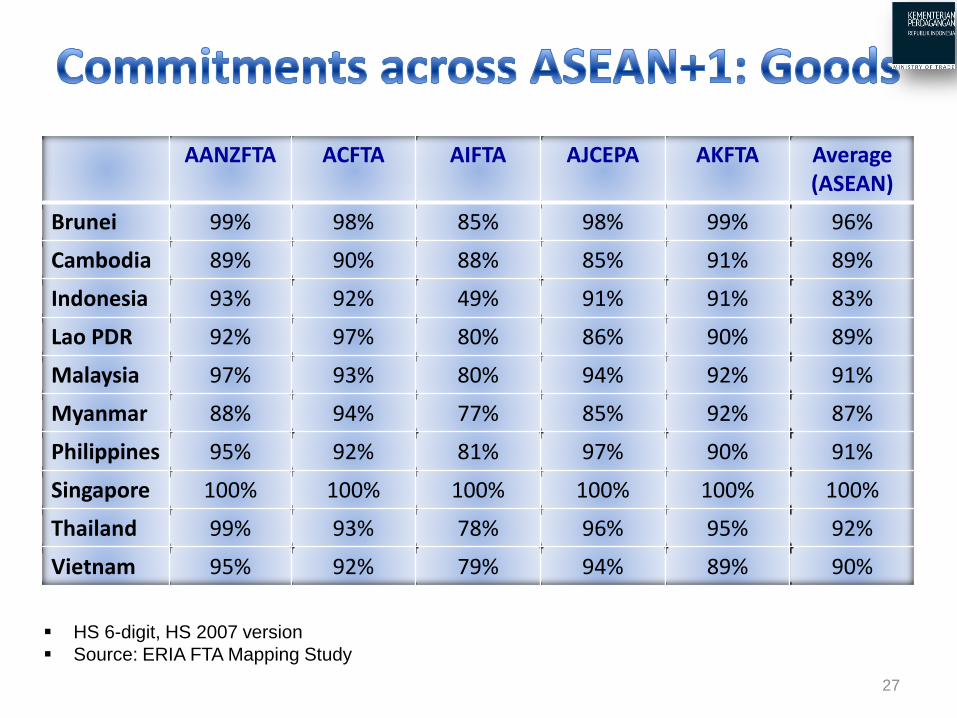

27

AANZFTA ACFTA AIFTA AJCEPA AKFTA Average (ASEAN)

Brunei 99% 98% 85% 98% 99% 96%

Cambodia 89% 90% 88% 85% 91% 89%

Indonesia 93% 92% 49% 91% 91% 83%

Lao PDR 92% 97% 80% 86% 90% 89%

Malaysia 97% 93% 80% 94% 92% 91%

Myanmar 88% 94% 77% 85% 92% 87%

Philippines 95% 92% 81% 97% 90% 91%

Singapore 100% 100% 100% 100% 100% 100%

Thailand 99% 93% 78% 96% 95% 92%

Vietnam 95% 92% 79% 94% 89% 90%

HS 6-digit, HS 2007 version

Source: ERIA FTA Mapping Study

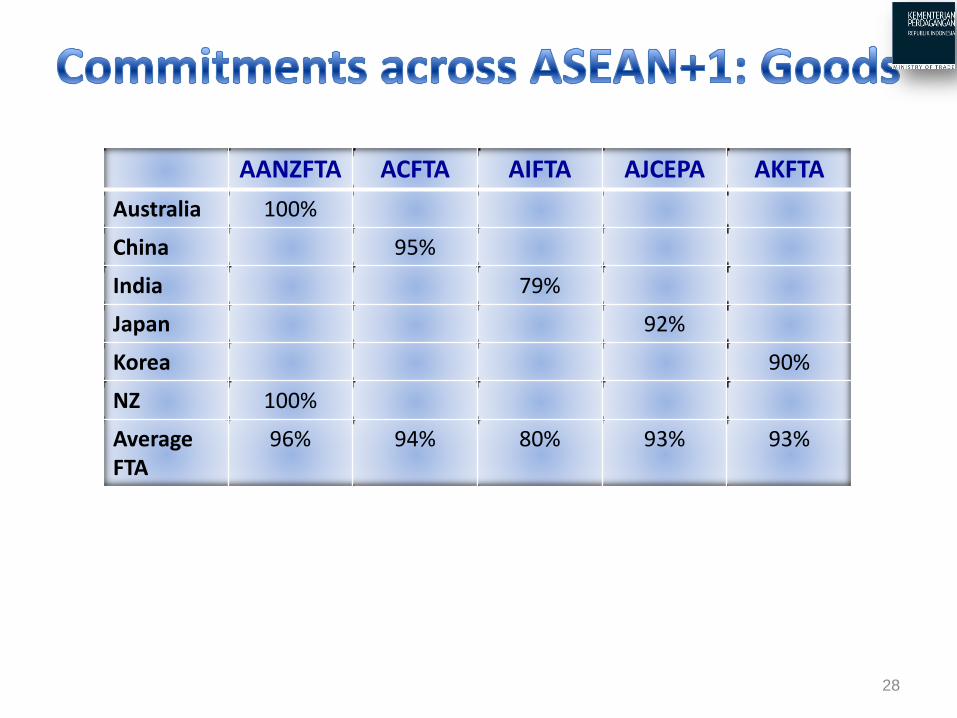

28

AANZFTA ACFTA AIFTA AJCEPA AKFTA

Australia 100%

China 95%

India 79%

Japan 92%

Korea 90%

NZ 100%

Average FTA

96% 94% 80% 93% 93%

29

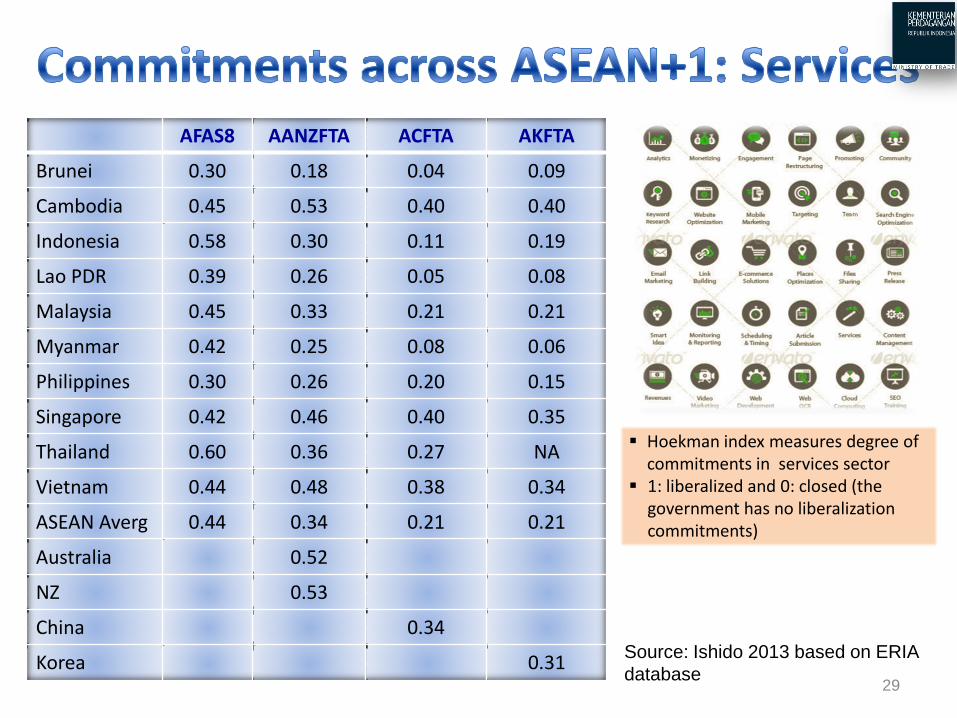

AFAS8 AANZFTA ACFTA AKFTA

Brunei 0.30 0.18 0.04 0.09

Cambodia 0.45 0.53 0.40 0.40

Indonesia 0.58 0.30 0.11 0.19

Lao PDR 0.39 0.26 0.05 0.08

Malaysia 0.45 0.33 0.21 0.21

Myanmar 0.42 0.25 0.08 0.06

Philippines 0.30 0.26 0.20 0.15

Singapore 0.42 0.46 0.40 0.35

Thailand 0.60 0.36 0.27 NA

Vietnam 0.44 0.48 0.38 0.34

ASEAN Averg 0.44 0.34 0.21 0.21

Australia 0.52

NZ 0.53

China 0.34

Korea 0.31

Hoekman index measures degree of commitments in services sector

1: liberalized and 0: closed (the government has no liberalization commitments)

Source: Ishido 2013 based on ERIA

database

30

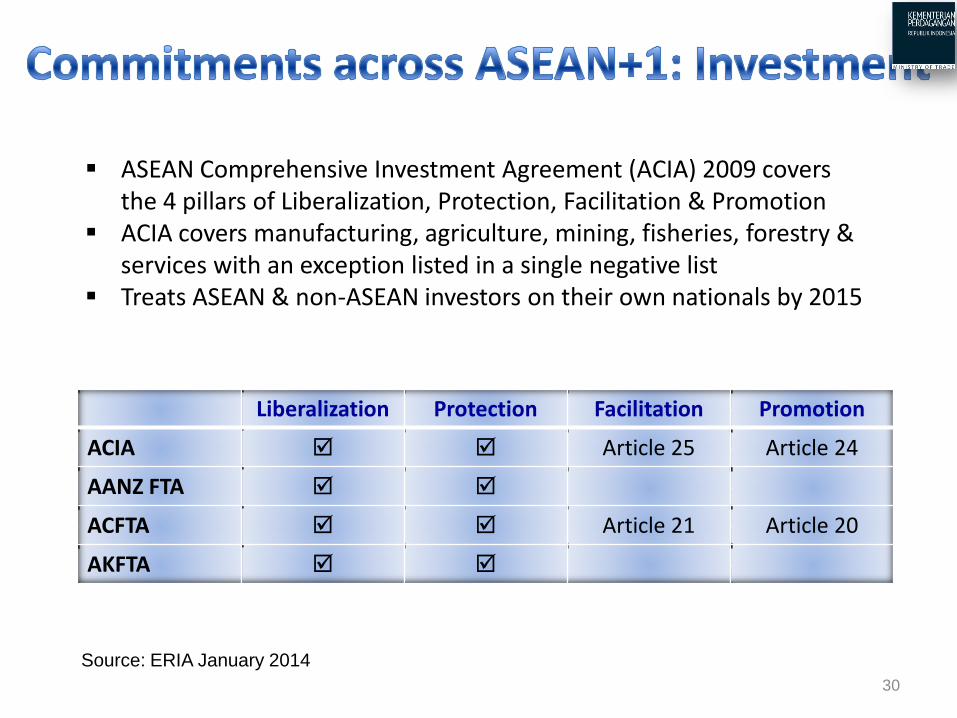

ASEAN Comprehensive Investment Agreement (ACIA) 2009 covers the 4 pillars of Liberalization, Protection, Facilitation & Promotion ACIA covers manufacturing, agriculture, mining, fisheries, forestry & services with an exception listed in a single negative list Treats ASEAN & non-ASEAN investors on their own nationals by 2015

Liberalization Protection Facilitation Promotion

ACIA Article 25 Article 24

AANZ FTA

ACFTA Article 21 Article 20

AKFTA

Source: ERIA January 2014

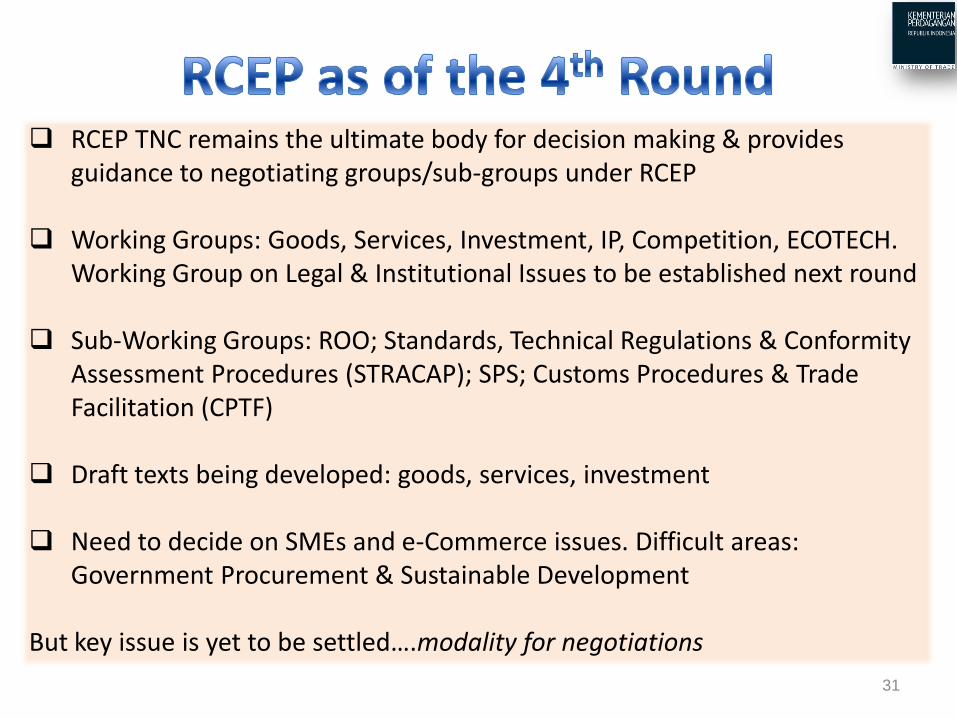

31

RCEP TNC remains the ultimate body for decision making & provides guidance to negotiating groups/sub-groups under RCEP Working Groups: Goods, Services, Investment, IP, Competition, ECOTECH. Working Group on Legal & Institutional Issues to be established next round

Sub-Working Groups: ROO; Standards, Technical Regulations & Conformity Assessment Procedures (STRACAP); SPS; Customs Procedures & Trade Facilitation (CPTF) Draft texts being developed: goods, services, investment Need to decide on SMEs and e-Commerce issues. Difficult areas: Government Procurement & Sustainable Development But key issue is yet to be settled….modality for negotiations

32

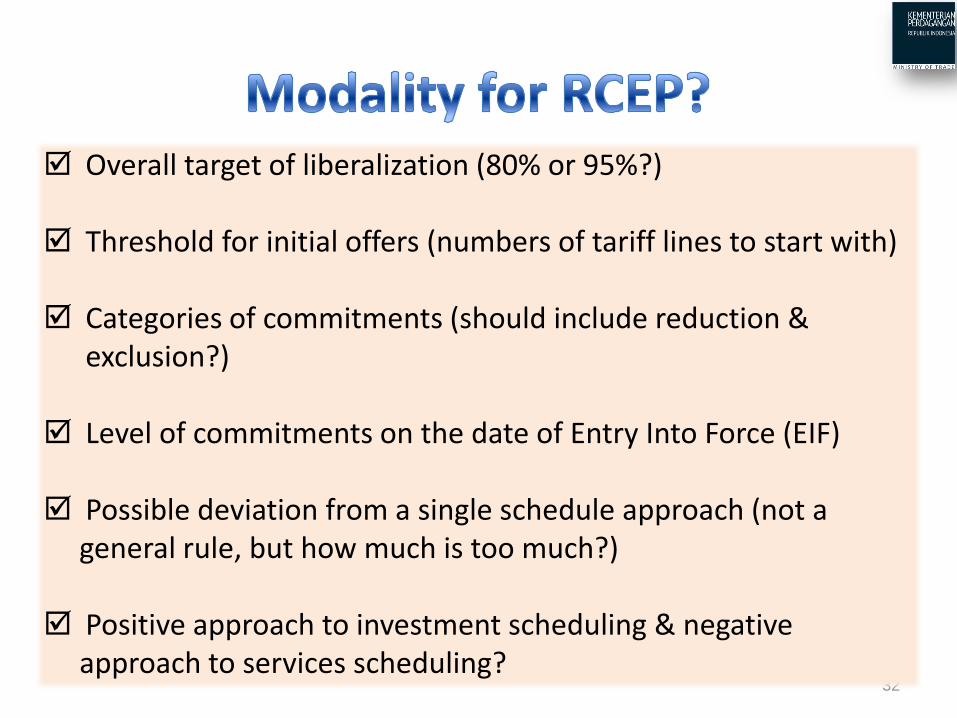

Overall target of liberalization (80% or 95%?)

Threshold for initial offers (numbers of tariff lines to start with)

Categories of commitments (should include reduction & exclusion?)

Level of commitments on the date of Entry Into Force (EIF)

Possible deviation from a single schedule approach (not a general rule, but how much is too much?)

Positive approach to investment scheduling & negative

approach to services scheduling?

33

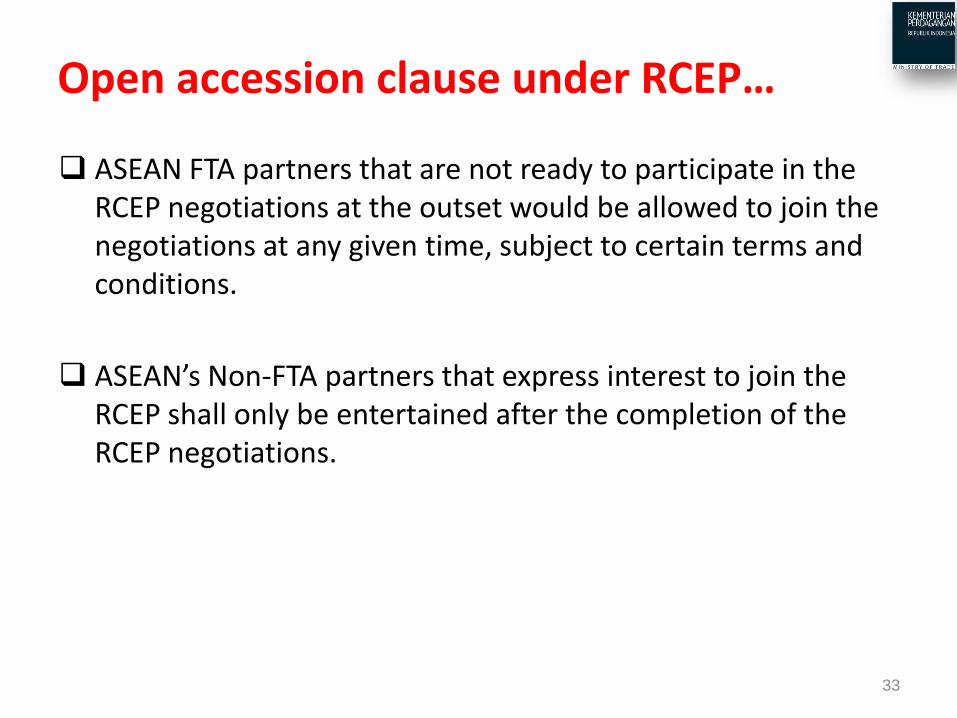

Open accession clause under RCEP…

ASEAN FTA partners that are not ready to participate in the RCEP negotiations at the outset would be allowed to join the negotiations at any given time, subject to certain terms and conditions.

ASEAN’s Non-FTA partners that express interest to join the RCEP shall only be entertained after the completion of the RCEP negotiations.

34