euro credit pilot

TRANSCRIPT

10

2010

Euro Credit Pilot

Economics & FI/FX Research Credit Research Equity Research Cross Asset Research

“2010's last quarter-slice”

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 2 See last pages for disclaimer.

Contents 4 Story of the month: 2010's final act: A Midsummer Night’s Dream or

Macbeth

6 Credit Drivers

6 Macro: Still a long way to go for deleveraging

7 Micro Fundamentals: Earnings season forecast iBoxx

8 Debt-Equity Linkage: Earnings forecast & development

9 Credit Quality Trend: State of "slack" in corporate ratings

10 Market Technicals: A look in the rear-view mirror

11 Valuation & Timing

13 Other credit markets

13 Credit derivatives – Liquidity squeeze in single names?

14 Securitization: UK prime RMBS vs. weak UK housing market

15 EEMEA: Less leveraged credit map is emerging

16 Sector Allocation

17 Earnings Calendar

23 Fundamental Credit Views

23 Telecommunications (Marketweight)

29 Media (Marketweight)

31 Technology (Marketweight)

33 Automobiles & Parts (Marketweight)

35 Utilities (Marketweight)

42 Oil & Gas (Overweight)

44 Industrial Goods & Services (Core) (Underweight)

48 Aerospace & Defense (Marketweight)

49 Industrial Transportation (Overweight)

51 Basic Resources (Marketweight)

52 Chemicals (Underweight)

54 Construction & Materials (Underweight)

56 Health Care (Underweight)

58 Personal & Household Goods (Core) (Marketweight)

60 Tobacco (Overweight)

61 Food & Beverage (Overweight)

63 Travel & Leisure (Underweight)

64 Retail (Underweight)

66 Banks (Marketweight)

74 Financial Services (Marketweight)

74 Insurance (Marketweight)

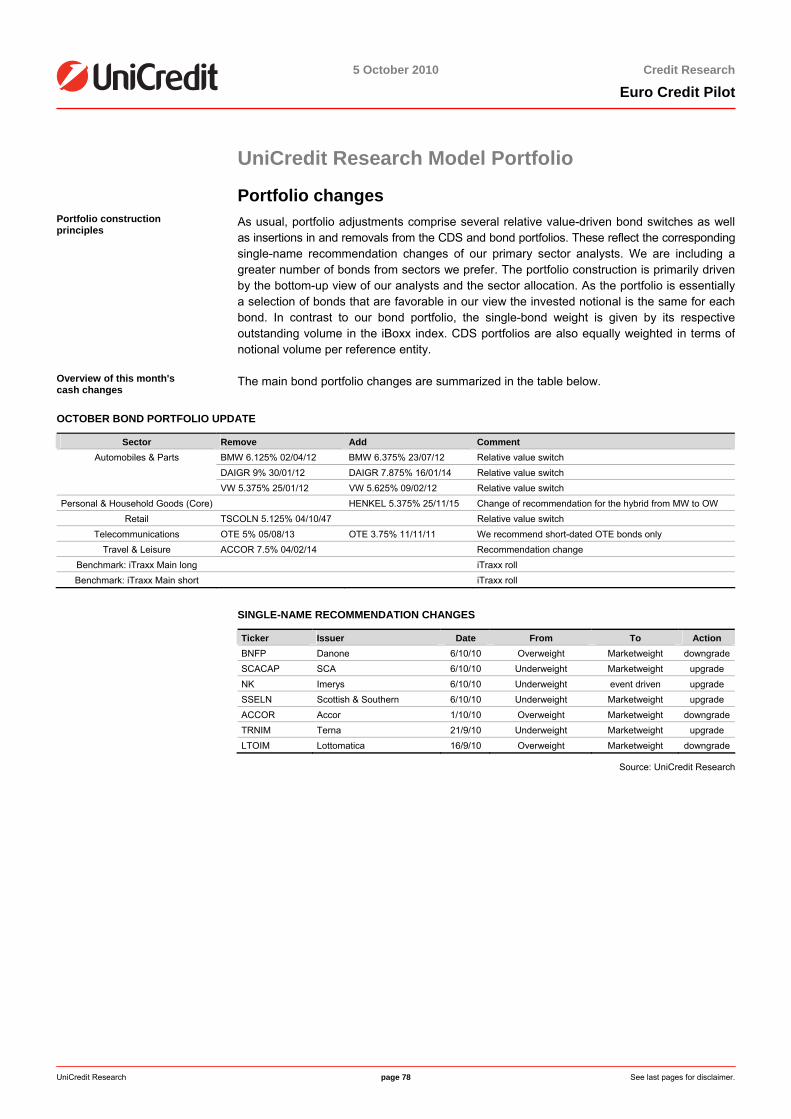

78 UniCredit Research Model Portfolio

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 3 See last pages for disclaimer.

From an investor's perspective, October is a classic in-between month – the largest part of the year is already behind us, but the focus is not (yet) fully on next year. Hittingthe home stretch, however, investors will worry about getting in this year's harvest.And for fixed income investors, it has been a good year (at least for those that avoidedthis year's credit bombs – European periphery), as the YTD total return for the iBoxxnon-financials, for example, stands at 6.4%. However, this is almost exclusively due tothe underlying interest rate dynamics, as the YTD credit return in the index is evenbelow 0.4%! While in the remainder of this year one probably cannot turn around a badyear, a volatile "final act" might destroy a good overall performance. Hence, the centralquestion is: Will the final act turn out to be a comedy or a tragedy?

■ Macro Outlook: In order to bring the excessive leverage to more sustainable levels, private and public sectors need to reduce spending and increase savings. However, the deleveragingprocess has a very unpleasant deflationary side effect, which could exacerbate theleverage problem via the so-called "debt-snowball-effect".

■ Micro Fundamentals: EPS estimates for the upcoming quarters are expected to remain relatively stable in 4Q and are likely to improve in 2011.

■ Debt-Equity-Linkage: Against the backdrop of an anticipated slowdown of economicactivity, it seems odd that forward EPS are still showing strong increases. However, this rise stems from an arithmetic effect and the actual EPS estimates are being loweredacross Europe, except for Germany.

■ Credit Quality Trend: Given the subdued growth environment, the question is wherecompanies stand in terms of rating slack, e.g., whether they have headroom in their financial profile compared to the criteria of the rating agencies ahead of the anticipated slowdown.

■ Market Technicals: While 2009 was an exceptional year for non-financials investment grade issuance activity, 2010 will be the year of high-yield bonds and covered bonds.

■ Valuation & Timing: We expect spread volatility to remain high despite stable creditfundamentals on the back of potential growth weaknesses ahead.

■ Other Credit Markets: Credit Derivatives: We take a look at recent liquidity data for single-name CDS referencing iTraxx Europe members. Apparently, liquidity is much betterthan anecdotal evidence suggests. Securitization: Recently, a battery of unsupportive data were released for the UK, which underline a weakening trend on the UK mortgage market. EEMEA: A less leveraged credit map is emerging.

■ Allocation: We stick to our defensive strategy.

■ Model Portfolio: Our financials portfolio outperformed the benchmark by 100bp, while the non-financials portfolio outperformed by 9bp.

Dr. Philip Gisdakis (UniCredit Bank) +49 89 378-13228 [email protected]

Dr. Tim Brunne (UniCredit Bank) +49 89 378-13521 [email protected]

Markus Ernst (UniCredit Bank) +49 89 378-14213 [email protected]

Dr. Stefan Kolek (UniCredit Bank) +49 89 378-12495 [email protected]

Dr. Christian Weber, CFA (UniCredit Bank) +49 89 378-12250 [email protected]

Corporate Credit Research Financials Credit Research

Bloomberg UCCR

Internet www.research.unicreditgroup.eu

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 4 See last pages for disclaimer.

Story of the month

2010's final act: A Midsummer Night’s Dream or Macbeth From an investor's perspective, October is a classic in-between month – the largest

part of the year (and hopefully also the largest part of the required performance) isalready behind us, but the focus is not (yet) fully on next year. Hitting the home stretch, however, investors will worry about getting in this year's harvest. And for fixed incomeinvestors, it has been a good year (at least for those that avoided this year's creditbombs – European periphery), as the YTD total return for the iBoxx non-financials, for example, stands at 6.4%. However, this is almost exclusively due to the underlyinginterest rate dynamics, as the YTD credit return in the index is even below 0.4%! Whilein the remainder of this year one probably cannot turn around a bad year, a volatile "final act" might destroy a good overall performance. Hence, the central question is:Will the final act turn to out to be a comedy or a tragedy? The short (and balanced)answer is: a Macbeth-like bloodbath is not very likely, but there might well be some factors that could disturb a Midsummer Night's Dream.

Double-dip concerns, China property price bubble and European sovereign debt crisis remain the most dominant "bearish" drivers

The risks (that we have referred to frequently) are:

■ Double-dip recession fears in the US (as well as in Europe), and potential negativeimplications from what appears to be the resolution strategy "en vogue", i.e. quantitative easing. What started as a kind of "next level" after cutting policy rates close to zero in order to bringdown longer-term yields appears to evolve into something like intentionally weakeningcentral bank balance sheets in order to devaluate the own currency (some commentatorsare already referring to "currency war"). The problem emerging for credit investors fromthese developments (besides the general uncertainties that arise on the back of movinginto the unchartered territory of multiple unilateral currency interventions) is that weakeningthe currency by triggering rising inflation expectations may well result in a sharp andsubstantial rise in longer-term refinancing costs, which is particularly painful when thecountry needs to borrow substantial amounts also from private (or foreign) investors (and not just from its own central bank). However, rising government bond yields might result ina crowding out of private sector borrowers that currently benefit from inflows from investorsdesperately hunting for (minimal) yield.

■ The implications from a (potentially bursting) property bubble in China (i.e., a possibleinstability in the Chinese financial system and a drag on consumption – which would be important to "bail out" the developed economies – due to a declining perception of wealth)

■ The smoldering European sovereign debt crisis.

In particular the latter will have an impact on European credit risk for two reasons: first, thepoor performance of credit markets – secondary spreads, as well as primary volumes – have shown how sensitively investors react to this topic. And second, even when governmentshave learned their lesson, the short-term impact of austerity measures will likely not be positive for markets. In this respect, the IMF published an interesting article on the economicimpact of the fiscal adjustment processes in its October 2010 World Economic Outlook. Thetheoretical background for the notion of fiscal adjustments is the hypothesis of "expansionaryfiscal contraction" – fiscal retrenchment can stimulate growth even in the short term. However, the present IMF study shows that a short-term economic contraction is a more likely outcome. Nevertheless, expansionary effects can occur when the contraction comes on the back ofgovernment solvency concerns, or when the adjustment process is structured in a proper way, i.e. when it increases confidence of households and businesses. The main findings ofthe study are that a fiscal consolidation of 1% of GDP reduces GDP growth by 0.5% withintwo years and raises the unemployment rate by 0.3%. The recent numbers regarding the Greek budget projections seem to basically confirm these findings (i.e., they even overshootthe findings, as the targeted adjustment of the deficit of 10% – from 13% to 3% – results in a

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 5 See last pages for disclaimer.

projected recession of 7.5% [a multiple of 0.75% per 1% consolidation], while the unemploymentrate is expected to rise by 5% [a multiple of 0.5%]). The study also mentions that declininginterest costs and a decline in the real value of the domestic currency typically support theeconomy – two factors that hardly apply to Greece (which, by the way, is the main criticism ofthe common currency). However, the study is also a warning for those who hope that thecurrent process of fiscal consolidation, in particular in Europe (which we welcome), will take place without any impact on the real economy. The concern is, in fact, that this kind ofadjustment will in the short term – weigh on growth.

Is the next phase a political crisis?

The ability and willingness of governments to put their finances back on a sustainable pathhave been and still are a major concern of investors. The Greek sovereign debt crisis is themost prominent example in this respect this year. In April 2009, the G-20 agreed to triple the lending resources of the IMF to USD 750bn, thereby acknowledging the severity of the fiscal difficulties in many countries around the globe. Since then, the IMF has repeatedly highlightedthe necessity of austerity measures and appealed to sovereign governments to return tosustainable debt and deficit levels. The ECB has assumed this role within the eurozone,continuously calling for fiscal prudence.

Necessity and economic impact of fiscal consolidation

As mentioned above, the IMF acknowledges in its World Economic Outlook that fiscalconsolidation measures will have a negative impact on economic output and unemployment.Historically, such short-term pain has been rewarded with a long-term improvement of the respective country's economic output, primarily due to the long-term stimulation of private consumption and investment. Unfortunately, the positive long-term benefits of austerity in highly indebted but developed countries will be even less pronounced than suggested by thehistorical precedents. Developed countries are trapped in a catch-22 situation, due to subdued growth potential. Monetary policy is effectively already at its limits and currencydevaluation is not an option for many countries that are trying to boost net exports. Adversedemographic developments in developed countries will put further pressure on their respective fiscal situation and growth outlook. However, austerity measures are inevitable toavoid a deadly debt spiral. Hence, most countries in the Western world will have to managesubstantial economic and social challenges. This translates into an unpopular political task.

Sovereign debt crisis followed by a political crisis?

To date, governments are reiterating their commitment to cut public spending and reducesovereign debt. However, implementation of the measures requires priority for a long time. It may take years for the benefits of fiscal prudence to become apparent. Policy makers areputting at risk their public support as the measures are clearly unpopular. According to theIMF, cutting public spending, hiking tax rates and overhauling national pension systems are all necessary and will at the same time negatively impact economic output and unemployment. Publicsupport for the reform agenda is already shrinking in many countries. On 29 September,Spain faced its first general strike in eight years and about 100,000 people gathered inBrussels for an anti-austerity march. Governments on both sides of the Atlantic face decliningpublic support. There are now several minority-led governments in the eurozone, showing that clear political majorities are lacking for the most pressing policy topics. There is alsodisagreement at the most senior level of the EMU. European governments need to agree onreform of the Stability and Growth Pact in order to enforce national fiscal discipline, but a political compromise currently seems almost impossible. In its history, Europe has successfullycoped with more challenging problems. However, a political crisis is a current downside risk,leading to the obvious repercussions for risky asset markets and negative feedback loops on sovereign debt risk premia. During 4Q, European parliaments will have to pass the 2011budgets. On the EU level, many compromises regarding financial market regulation, the futureof the EFSF and the reform of the Stability and Growth Pact will have to be found. These arethe next milestones.

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 6 See last pages for disclaimer.

Credit Drivers

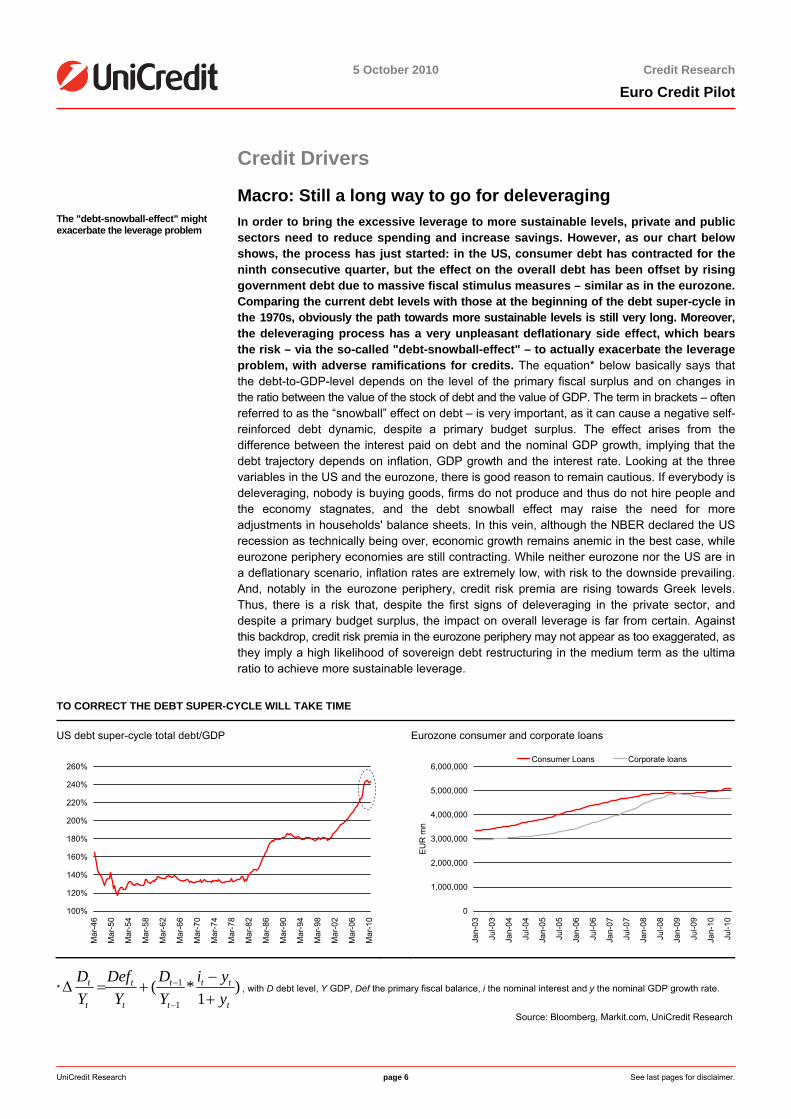

Macro: Still a long way to go for deleveraging The "debt-snowball-effect" might exacerbate the leverage problem

In order to bring the excessive leverage to more sustainable levels, private and publicsectors need to reduce spending and increase savings. However, as our chart belowshows, the process has just started: in the US, consumer debt has contracted for theninth consecutive quarter, but the effect on the overall debt has been offset by risinggovernment debt due to massive fiscal stimulus measures – similar as in the eurozone.Comparing the current debt levels with those at the beginning of the debt super-cycle inthe 1970s, obviously the path towards more sustainable levels is still very long. Moreover,the deleveraging process has a very unpleasant deflationary side effect, which bearsthe risk – via the so-called "debt-snowball-effect" – to actually exacerbate the leverageproblem, with adverse ramifications for credits. The equation* below basically says thatthe debt-to-GDP-level depends on the level of the primary fiscal surplus and on changes inthe ratio between the value of the stock of debt and the value of GDP. The term in brackets – oftenreferred to as the “snowball” effect on debt – is very important, as it can cause a negative self-reinforced debt dynamic, despite a primary budget surplus. The effect arises from thedifference between the interest paid on debt and the nominal GDP growth, implying that thedebt trajectory depends on inflation, GDP growth and the interest rate. Looking at the threevariables in the US and the eurozone, there is good reason to remain cautious. If everybody isdeleveraging, nobody is buying goods, firms do not produce and thus do not hire people andthe economy stagnates, and the debt snowball effect may raise the need for moreadjustments in households' balance sheets. In this vein, although the NBER declared the USrecession as technically being over, economic growth remains anemic in the best case, whileeurozone periphery economies are still contracting. While neither eurozone nor the US are ina deflationary scenario, inflation rates are extremely low, with risk to the downside prevailing.And, notably in the eurozone periphery, credit risk premia are rising towards Greek levels.Thus, there is a risk that, despite the first signs of deleveraging in the private sector, anddespite a primary budget surplus, the impact on overall leverage is far from certain. Againstthis backdrop, credit risk premia in the eurozone periphery may not appear as too exaggerated, asthey imply a high likelihood of sovereign debt restructuring in the medium term as the ultimaratio to achieve more sustainable leverage.

TO CORRECT THE DEBT SUPER-CYCLE WILL TAKE TIME

US debt super-cycle total debt/GDP Eurozone consumer and corporate loans

100%

120%

140%

160%

180%

200%

220%

240%

260%

Mar

-46

Mar

-50

Mar

-54

Mar

-58

Mar

-62

Mar

-66

Mar

-70

Mar

-74

Mar

-78

Mar

-82

Mar

-86

Mar

-90

Mar

-94

Mar

-98

Mar

-02

Mar

-06

Mar

-10

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

EU

R m

n

Consumer Loans Corporate loans

* )1

*(1

1

t

tt

t

t

t

t

t

t

yyi

YD

YDef

YD

+−

+=Δ−

− , with D debt level, Y GDP, Def the primary fiscal balance, i the nominal interest and y the nominal GDP growth rate.

Source: Bloomberg, Markit.com, UniCredit Research

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 7 See last pages for disclaimer.

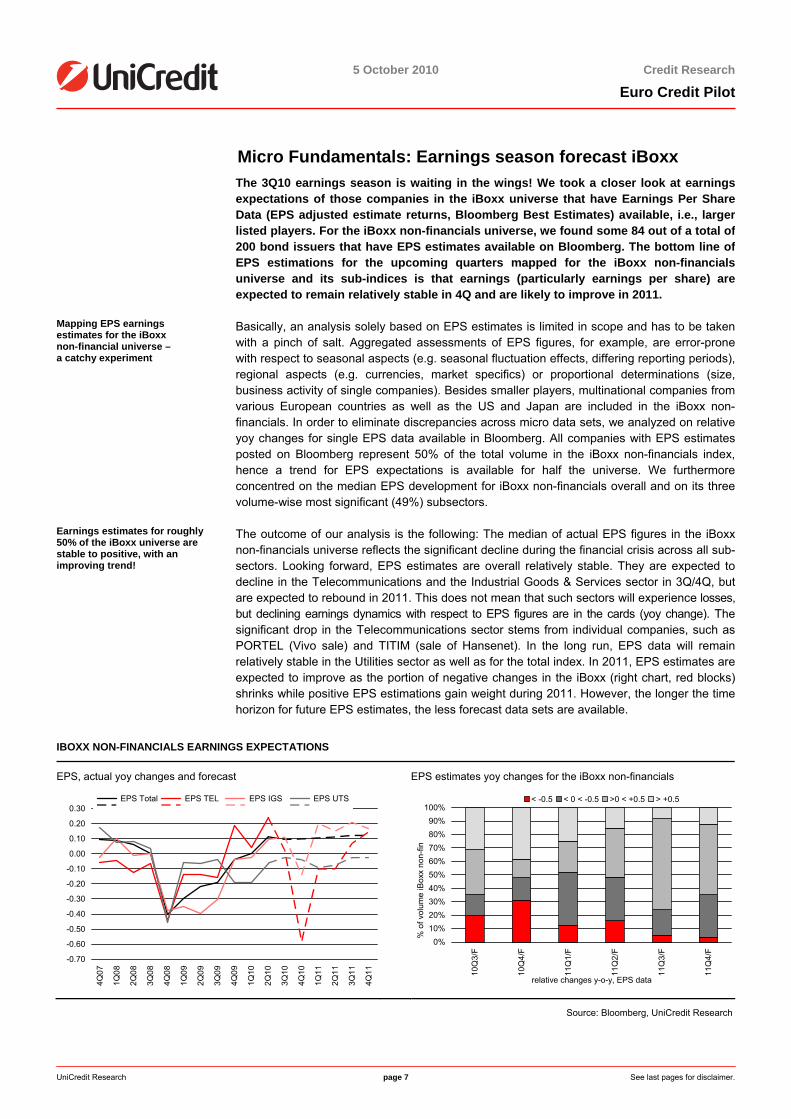

Micro Fundamentals: Earnings season forecast iBoxx The 3Q10 earnings season is waiting in the wings! We took a closer look at earnings

expectations of those companies in the iBoxx universe that have Earnings Per Share Data (EPS adjusted estimate returns, Bloomberg Best Estimates) available, i.e., largerlisted players. For the iBoxx non-financials universe, we found some 84 out of a total of 200 bond issuers that have EPS estimates available on Bloomberg. The bottom line of EPS estimations for the upcoming quarters mapped for the iBoxx non-financials universe and its sub-indices is that earnings (particularly earnings per share) areexpected to remain relatively stable in 4Q and are likely to improve in 2011.

Mapping EPS earnings estimates for the iBoxx non-financial universe – a catchy experiment

Basically, an analysis solely based on EPS estimates is limited in scope and has to be takenwith a pinch of salt. Aggregated assessments of EPS figures, for example, are error-prone with respect to seasonal aspects (e.g. seasonal fluctuation effects, differing reporting periods),regional aspects (e.g. currencies, market specifics) or proportional determinations (size,business activity of single companies). Besides smaller players, multinational companies fromvarious European countries as well as the US and Japan are included in the iBoxx non-financials. In order to eliminate discrepancies across micro data sets, we analyzed on relativeyoy changes for single EPS data available in Bloomberg. All companies with EPS estimatesposted on Bloomberg represent 50% of the total volume in the iBoxx non-financials index, hence a trend for EPS expectations is available for half the universe. We furthermoreconcentred on the median EPS development for iBoxx non-financials overall and on its three volume-wise most significant (49%) subsectors.

Earnings estimates for roughly 50% of the iBoxx universe are stable to positive, with an improving trend!

The outcome of our analysis is the following: The median of actual EPS figures in the iBoxxnon-financials universe reflects the significant decline during the financial crisis across all sub-sectors. Looking forward, EPS estimates are overall relatively stable. They are expected to decline in the Telecommunications and the Industrial Goods & Services sector in 3Q/4Q, butare expected to rebound in 2011. This does not mean that such sectors will experience losses, but declining earnings dynamics with respect to EPS figures are in the cards (yoy change). The significant drop in the Telecommunications sector stems from individual companies, such asPORTEL (Vivo sale) and TITIM (sale of Hansenet). In the long run, EPS data will remain relatively stable in the Utilities sector as well as for the total index. In 2011, EPS estimates areexpected to improve as the portion of negative changes in the iBoxx (right chart, red blocks)shrinks while positive EPS estimations gain weight during 2011. However, the longer the timehorizon for future EPS estimates, the less forecast data sets are available.

IBOXX NON-FINANCIALS EARNINGS EXPECTATIONS

EPS, actual yoy changes and forecast EPS estimates yoy changes for the iBoxx non-financials

-0.70

-0.60

-0.50

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

EPS Total EPS TEL EPS IGS EPS UTS

0%10%20%30%40%50%60%70%80%90%

100%

10Q

3/F

10Q

4/F

11Q

1/F

11Q

2/F

11Q

3/F

11Q

4/F

relative changes y-o-y, EPS data

% o

f vol

ume

iBox

x no

n-fin

< -0.5 < 0 < -0.5 >0 < +0.5 > +0.5

Source: Bloomberg, UniCredit Research

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 8 See last pages for disclaimer.

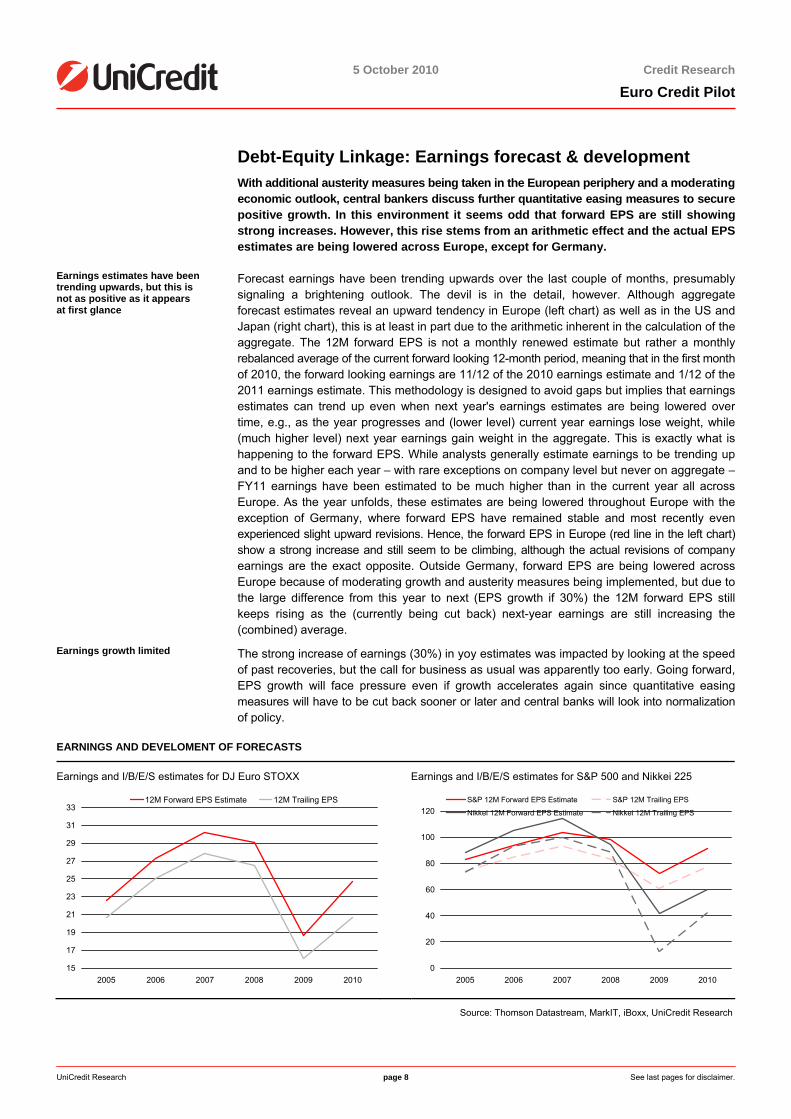

Debt-Equity Linkage: Earnings forecast & development With additional austerity measures being taken in the European periphery and a moderating

economic outlook, central bankers discuss further quantitative easing measures to securepositive growth. In this environment it seems odd that forward EPS are still showingstrong increases. However, this rise stems from an arithmetic effect and the actual EPSestimates are being lowered across Europe, except for Germany.

Earnings estimates have been trending upwards, but this is not as positive as it appears at first glance

Forecast earnings have been trending upwards over the last couple of months, presumablysignaling a brightening outlook. The devil is in the detail, however. Although aggregateforecast estimates reveal an upward tendency in Europe (left chart) as well as in the US andJapan (right chart), this is at least in part due to the arithmetic inherent in the calculation of theaggregate. The 12M forward EPS is not a monthly renewed estimate but rather a monthlyrebalanced average of the current forward looking 12-month period, meaning that in the first monthof 2010, the forward looking earnings are 11/12 of the 2010 earnings estimate and 1/12 of the2011 earnings estimate. This methodology is designed to avoid gaps but implies that earningsestimates can trend up even when next year's earnings estimates are being lowered overtime, e.g., as the year progresses and (lower level) current year earnings lose weight, while(much higher level) next year earnings gain weight in the aggregate. This is exactly what ishappening to the forward EPS. While analysts generally estimate earnings to be trending upand to be higher each year – with rare exceptions on company level but never on aggregate –FY11 earnings have been estimated to be much higher than in the current year all acrossEurope. As the year unfolds, these estimates are being lowered throughout Europe with theexception of Germany, where forward EPS have remained stable and most recently evenexperienced slight upward revisions. Hence, the forward EPS in Europe (red line in the left chart)show a strong increase and still seem to be climbing, although the actual revisions of companyearnings are the exact opposite. Outside Germany, forward EPS are being lowered acrossEurope because of moderating growth and austerity measures being implemented, but due tothe large difference from this year to next (EPS growth if 30%) the 12M forward EPS stillkeeps rising as the (currently being cut back) next-year earnings are still increasing the(combined) average.

Earnings growth limited The strong increase of earnings (30%) in yoy estimates was impacted by looking at the speedof past recoveries, but the call for business as usual was apparently too early. Going forward,EPS growth will face pressure even if growth accelerates again since quantitative easingmeasures will have to be cut back sooner or later and central banks will look into normalizationof policy.

EARNINGS AND DEVELOMENT OF FORECASTS

Earnings and I/B/E/S estimates for DJ Euro STOXX Earnings and I/B/E/S estimates for S&P 500 and Nikkei 225

15

17

19

21

23

25

27

29

31

33

2005 2006 2007 2008 2009 2010

12M Forward EPS Estimate 12M Trailing EPS

0

20

40

60

80

100

120

2005 2006 2007 2008 2009 2010

S&P 12M Forward EPS Estimate S&P 12M Trailing EPS

Nikkei 12M Forward EPS Estimate Nikkei 12M Trailing EPS

Source: Thomson Datastream, MarkIT, iBoxx, UniCredit Research

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 9 See last pages for disclaimer.

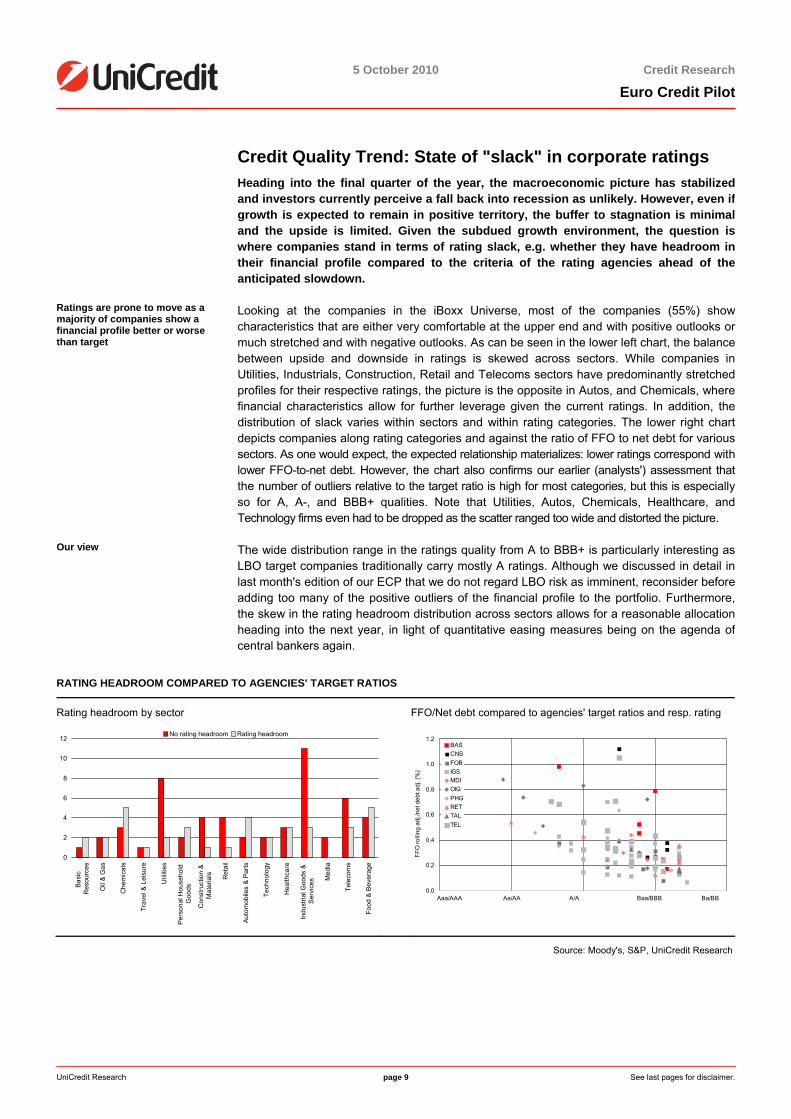

Credit Quality Trend: State of "slack" in corporate ratings Heading into the final quarter of the year, the macroeconomic picture has stabilized

and investors currently perceive a fall back into recession as unlikely. However, even ifgrowth is expected to remain in positive territory, the buffer to stagnation is minimaland the upside is limited. Given the subdued growth environment, the question iswhere companies stand in terms of rating slack, e.g. whether they have headroom intheir financial profile compared to the criteria of the rating agencies ahead of theanticipated slowdown.

Ratings are prone to move as a majority of companies show a financial profile better or worse than target

Looking at the companies in the iBoxx Universe, most of the companies (55%) showcharacteristics that are either very comfortable at the upper end and with positive outlooks ormuch stretched and with negative outlooks. As can be seen in the lower left chart, the balancebetween upside and downside in ratings is skewed across sectors. While companies inUtilities, Industrials, Construction, Retail and Telecoms sectors have predominantly stretchedprofiles for their respective ratings, the picture is the opposite in Autos, and Chemicals, wherefinancial characteristics allow for further leverage given the current ratings. In addition, thedistribution of slack varies within sectors and within rating categories. The lower right chartdepicts companies along rating categories and against the ratio of FFO to net debt for varioussectors. As one would expect, the expected relationship materializes: lower ratings correspond withlower FFO-to-net debt. However, the chart also confirms our earlier (analysts') assessment thatthe number of outliers relative to the target ratio is high for most categories, but this is especiallyso for A, A-, and BBB+ qualities. Note that Utilities, Autos, Chemicals, Healthcare, andTechnology firms even had to be dropped as the scatter ranged too wide and distorted the picture.

Our view The wide distribution range in the ratings quality from A to BBB+ is particularly interesting asLBO target companies traditionally carry mostly A ratings. Although we discussed in detail inlast month's edition of our ECP that we do not regard LBO risk as imminent, reconsider beforeadding too many of the positive outliers of the financial profile to the portfolio. Furthermore,the skew in the rating headroom distribution across sectors allows for a reasonable allocationheading into the next year, in light of quantitative easing measures being on the agenda ofcentral bankers again.

RATING HEADROOM COMPARED TO AGENCIES' TARGET RATIOS

Rating headroom by sector FFO/Net debt compared to agencies' target ratios and resp. rating

0

2

4

6

8

10

12

Basi

c R

esou

rces

Oil

& G

as

Che

mic

als

Trav

el &

Lei

sure

Util

ities

Pers

onal

Hou

seho

ld

Goo

ds

Con

stru

ctio

n &

M

ater

ials Ret

ail

Auto

mob

iles

& P

arts

Tech

nolo

gy

Hea

lthca

re

Indu

stria

l Goo

ds &

S

ervi

ces M

edia

Tele

com

s

Food

& B

ever

age

No rating headroom Rating headroom

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0 3 6 9 12

BASCNSFOBIGSMDIOIGPHGRETTALTEL

Aaa/AAA Aa/AA A/A Baa/BBB Ba/BB

FFO

rolli

ng a

dj./n

et d

ebt a

dj. (

%)

Source: Moody's, S&P, UniCredit Research

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 10 See last pages for disclaimer.

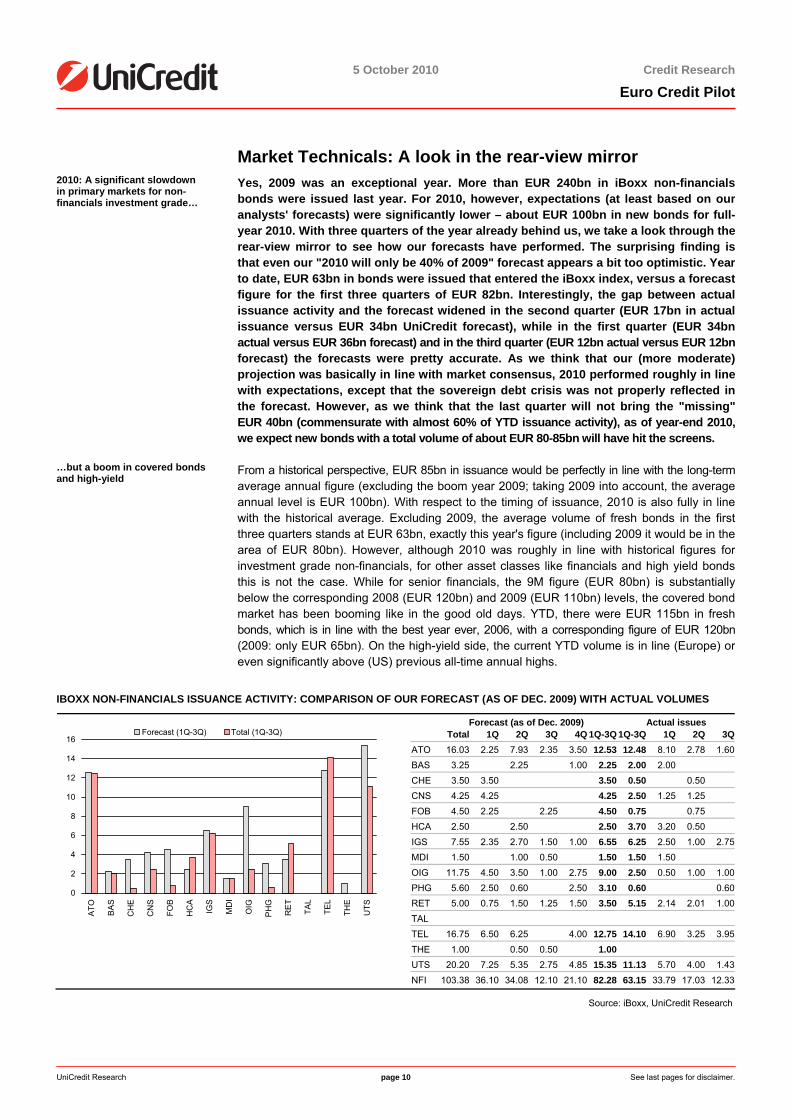

Market Technicals: A look in the rear-view mirror 2010: A significant slowdown in primary markets for non-financials investment grade…

Yes, 2009 was an exceptional year. More than EUR 240bn in iBoxx non-financials bonds were issued last year. For 2010, however, expectations (at least based on ouranalysts' forecasts) were significantly lower – about EUR 100bn in new bonds for full-year 2010. With three quarters of the year already behind us, we take a look through therear-view mirror to see how our forecasts have performed. The surprising finding isthat even our "2010 will only be 40% of 2009" forecast appears a bit too optimistic. Yearto date, EUR 63bn in bonds were issued that entered the iBoxx index, versus a forecastfigure for the first three quarters of EUR 82bn. Interestingly, the gap between actualissuance activity and the forecast widened in the second quarter (EUR 17bn in actualissuance versus EUR 34bn UniCredit forecast), while in the first quarter (EUR 34bnactual versus EUR 36bn forecast) and in the third quarter (EUR 12bn actual versus EUR 12bnforecast) the forecasts were pretty accurate. As we think that our (more moderate)projection was basically in line with market consensus, 2010 performed roughly in linewith expectations, except that the sovereign debt crisis was not properly reflected inthe forecast. However, as we think that the last quarter will not bring the "missing"EUR 40bn (commensurate with almost 60% of YTD issuance activity), as of year-end 2010, we expect new bonds with a total volume of about EUR 80-85bn will have hit the screens.

…but a boom in covered bonds and high-yield

From a historical perspective, EUR 85bn in issuance would be perfectly in line with the long-termaverage annual figure (excluding the boom year 2009; taking 2009 into account, the averageannual level is EUR 100bn). With respect to the timing of issuance, 2010 is also fully in linewith the historical average. Excluding 2009, the average volume of fresh bonds in the firstthree quarters stands at EUR 63bn, exactly this year's figure (including 2009 it would be in the area of EUR 80bn). However, although 2010 was roughly in line with historical figures forinvestment grade non-financials, for other asset classes like financials and high yield bondsthis is not the case. While for senior financials, the 9M figure (EUR 80bn) is substantially below the corresponding 2008 (EUR 120bn) and 2009 (EUR 110bn) levels, the covered bondmarket has been booming like in the good old days. YTD, there were EUR 115bn in freshbonds, which is in line with the best year ever, 2006, with a corresponding figure of EUR 120bn(2009: only EUR 65bn). On the high-yield side, the current YTD volume is in line (Europe) or even significantly above (US) previous all-time annual highs.

IBOXX NON-FINANCIALS ISSUANCE ACTIVITY: COMPARISON OF OUR FORECAST (AS OF DEC. 2009) WITH ACTUAL VOLUMES

Forecast (as of Dec. 2009) Actual issues Total 1Q 2Q 3Q 4Q 1Q-3Q 1Q-3Q 1Q 2Q 3QATO 16.03 2.25 7.93 2.35 3.50 12.53 12.48 8.10 2.78 1.60BAS 3.25 2.25 1.00 2.25 2.00 2.00CHE 3.50 3.50 3.50 0.50 0.50CNS 4.25 4.25 4.25 2.50 1.25 1.25FOB 4.50 2.25 2.25 4.50 0.75 0.75HCA 2.50 2.50 2.50 3.70 3.20 0.50IGS 7.55 2.35 2.70 1.50 1.00 6.55 6.25 2.50 1.00 2.75MDI 1.50 1.00 0.50 1.50 1.50 1.50OIG 11.75 4.50 3.50 1.00 2.75 9.00 2.50 0.50 1.00 1.00PHG 5.60 2.50 0.60 2.50 3.10 0.60 0.60RET 5.00 0.75 1.50 1.25 1.50 3.50 5.15 2.14 2.01 1.00TAL TEL 16.75 6.50 6.25 4.00 12.75 14.10 6.90 3.25 3.95THE 1.00 0.50 0.50 1.00 UTS 20.20 7.25 5.35 2.75 4.85 15.35 11.13 5.70 4.00 1.43

0

2

4

6

8

10

12

14

16

ATO BA

S

CH

E

CN

S

FOB

HC

A

IGS

MD

I

OIG

PH

G

RE

T

TAL

TEL

THE

UTS

Forecast (1Q-3Q) Total (1Q-3Q)

NFI 103.38 36.10 34.08 12.10 21.10 82.28 63.15 33.79 17.03 12.33

Source: iBoxx, UniCredit Research

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 11 See last pages for disclaimer.

Valuation & Timing

Tactical View: Volatile despite stable credit fundamentals… October is a kind of in-between month in markets. Investors do not yet focus on the new year

(which will be the case in November/December), but the old year is almost over, at leastperformance-wise. We say "Almost" because a bad year's performance can probably not beturned around in October alone, but a good year's performance can be destroyed. And forfixed income investors, it has been a good year, as the YTD total return for the iBoxx non-financials, for example, stands at 6.4%. However, this is almost exclusively due to the underlying interest rate dynamics, as the YTD credit return in the index (defined by spreadcarry plus mark-to-market performance due to spread changes) is even below 0.4%! Forfinancials (which include also subordinated paper), this is somewhat different: the credit return contributed 1.6% to the total return of 6.7%. However, as the total return has already beenhigher earlier this year (7% for non-financials at the end of August), investors might wonder how much of the performance can still be lost. From a credit investor's perspective, the risks seem to be moderated by the typical spread-yield correlation: when yields go up (and the declining yields have been the major performance drivers), spreads tend to tighten (andspreads remained remarkably resilient against the backdrop of extremely low yield levels).Moreover, since credit fundamentals, in particular for European investment grade non-financials, appear to be fairly sound, we do not expect a drastic spread blowout, even if fearsregarding a deteriorating economic outlook were to materialize. Any spread blowout will – in the first place – be driven by sentiment rather than by a real deterioration of creditfundamentals. On the other hand, many structural problems that the crisis revealed remain unresolved and market sentiment remains fragile. In particular in the current environment, inwhich portfolio managers have realized handsome returns, they might opt to err on the side ofcaution in order to protect this year's good performance, and hence might overreact in terms of hedging should a spread-widening trend crystallize. This refers not only to concernsregarding the financial system, but includes also structural problems (like overcapacity) on thenon-financials side. Capacity utilization, for example, amounts to only 75% in the US and Europe. Although it is still rising from historically low levels below 70%, there is still asubstantial gap to pre-crisis utilization rates (80%-85% area). However, demand weakness that arises on the back of austerity packages in Europe and the weak US labor market mayonly be temporarily camouflaged by demand from emerging Asia. We have our doubts thatChina alone can balance these deficiencies in the developed world on a sustainable basis.However, such fears will ultimately translate into a deterioration of credit fundamentals, whichmarkets will take into account rapidly.

Strategic View: …on potential growth weaknesses The risk drivers on a more strategic time horizon are not new: a potentially stronger-than-

expected slowdown in economic activity in the US and in the eurozone (austerity measures),and a potential bursting of the property bubble in China. This would have major implicationsfor the Chinese financial system and ultimately for the Chinese growth model, as authorities aim to shift it more towards domestic consumption rather than exports. The latter is inparticular important if China is expected to "bail out" the developed world. However, privateconsumption is very much driven by the perception of wealth of the consumer. Should a bubble burst, a lot of private household wealth will be destroyed, which will not motivate Chineseconsumers to purchase goods from the Western world. Last but not least, the Europeansovereign debt crisis is not yet over. A major risk factor is still the parliamentary debate regarding 2011 budget cuts, which are due in the coming weeks and months, and which maycreate headline risks. Volatile times lie ahead.

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 12 See last pages for disclaimer.

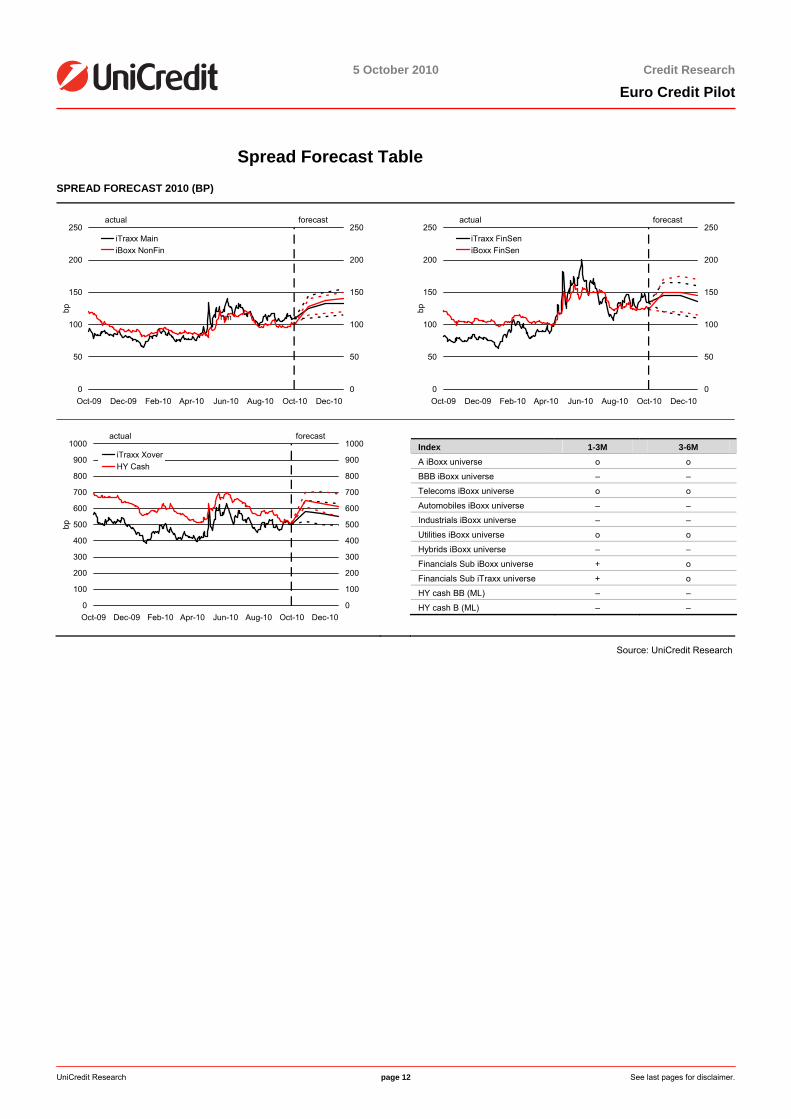

Spread Forecast Table SPREAD FORECAST 2010 (BP)

0

50

100

150

200

250

Oct-09 Dec-09 Feb-10 Apr-10 Jun-10 Aug-10 Oct-10 Dec-10

bp

0

50

100

150

200

250iTraxx MainiBoxx NonFin

actual forecast

nm

0

50

100

150

200

250

Oct-09 Dec-09 Feb-10 Apr-10 Jun-10 Aug-10 Oct-10 Dec-10

bp

0

50

100

150

200

250iTraxx FinSeniBoxx FinSen

actual forecast

0

100

200

300

400

500

600

700

800

900

1000

Oct-09 Dec-09 Feb-10 Apr-10 Jun-10 Aug-10 Oct-10 Dec-10

bp

0

100

200

300

400

500

600

700

800

900

1000iTraxx XoverHY Cash

actual forecast

Index 1-3M 3-6M A iBoxx universe o o

BBB iBoxx universe – –

Telecoms iBoxx universe o o

Automobiles iBoxx universe – –

Industrials iBoxx universe – –

Utilities iBoxx universe o o

Hybrids iBoxx universe – –

Financials Sub iBoxx universe + o

Financials Sub iTraxx universe + o

HY cash BB (ML) – –

HY cash B (ML) – –

Source: UniCredit Research

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 13 See last pages for disclaimer.

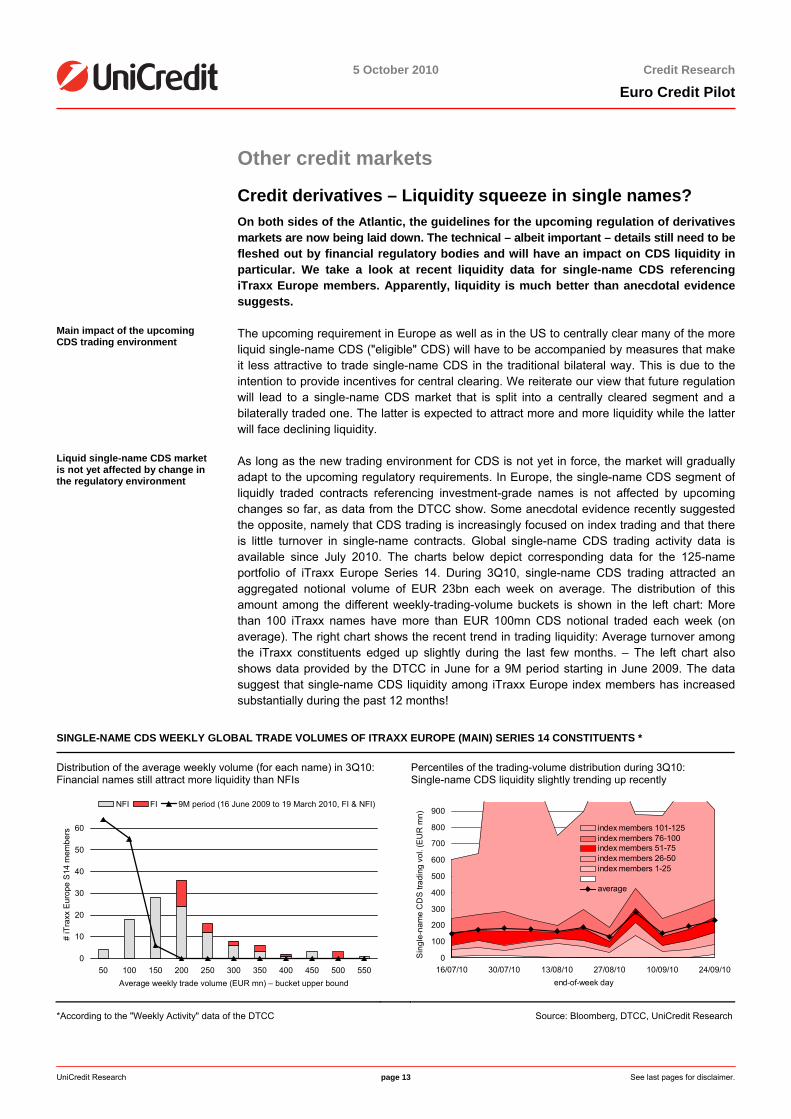

Other credit markets

Credit derivatives – Liquidity squeeze in single names? On both sides of the Atlantic, the guidelines for the upcoming regulation of derivatives

markets are now being laid down. The technical – albeit important – details still need to befleshed out by financial regulatory bodies and will have an impact on CDS liquidity inparticular. We take a look at recent liquidity data for single-name CDS referencing iTraxx Europe members. Apparently, liquidity is much better than anecdotal evidencesuggests.

Main impact of the upcoming CDS trading environment

The upcoming requirement in Europe as well as in the US to centrally clear many of the more liquid single-name CDS ("eligible" CDS) will have to be accompanied by measures that makeit less attractive to trade single-name CDS in the traditional bilateral way. This is due to theintention to provide incentives for central clearing. We reiterate our view that future regulation will lead to a single-name CDS market that is split into a centrally cleared segment and abilaterally traded one. The latter is expected to attract more and more liquidity while the latterwill face declining liquidity.

Liquid single-name CDS market is not yet affected by change in the regulatory environment

As long as the new trading environment for CDS is not yet in force, the market will graduallyadapt to the upcoming regulatory requirements. In Europe, the single-name CDS segment of liquidly traded contracts referencing investment-grade names is not affected by upcoming changes so far, as data from the DTCC show. Some anecdotal evidence recently suggestedthe opposite, namely that CDS trading is increasingly focused on index trading and that there is little turnover in single-name contracts. Global single-name CDS trading activity data is available since July 2010. The charts below depict corresponding data for the 125-name portfolio of iTraxx Europe Series 14. During 3Q10, single-name CDS trading attracted anaggregated notional volume of EUR 23bn each week on average. The distribution of thisamount among the different weekly-trading-volume buckets is shown in the left chart: More than 100 iTraxx names have more than EUR 100mn CDS notional traded each week (on average). The right chart shows the recent trend in trading liquidity: Average turnover amongthe iTraxx constituents edged up slightly during the last few months. – The left chart also shows data provided by the DTCC in June for a 9M period starting in June 2009. The datasuggest that single-name CDS liquidity among iTraxx Europe index members has increasedsubstantially during the past 12 months!

SINGLE-NAME CDS WEEKLY GLOBAL TRADE VOLUMES OF ITRAXX EUROPE (MAIN) SERIES 14 CONSTITUENTS *

Distribution of the average weekly volume (for each name) in 3Q10: Financial names still attract more liquidity than NFIs

Percentiles of the trading-volume distribution during 3Q10: Single-name CDS liquidity slightly trending up recently

0

10

20

30

40

50

60

50 100 150 200 250 300 350 400 450 500 550Average weekly trade volume (EUR mn) – bucket upper bound

# iT

raxx

Eur

ope

S14

mem

bers

NFI FI 9M period (16 June 2009 to 19 March 2010, FI & NFI)

0

100

200

300

400

500

600

700

800

900

16/07/10 30/07/10 13/08/10 27/08/10 10/09/10 24/09/10end-of-week day

index members 101-125index members 76-100index members 51-75index members 26-50index members 1-25

average

Sin

gle-

nam

e C

DS

trad

ing

vol.

(EU

R m

n)

*According to the "Weekly Activity" data of the DTCC Source: Bloomberg, DTCC, UniCredit Research

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 14 See last pages for disclaimer.

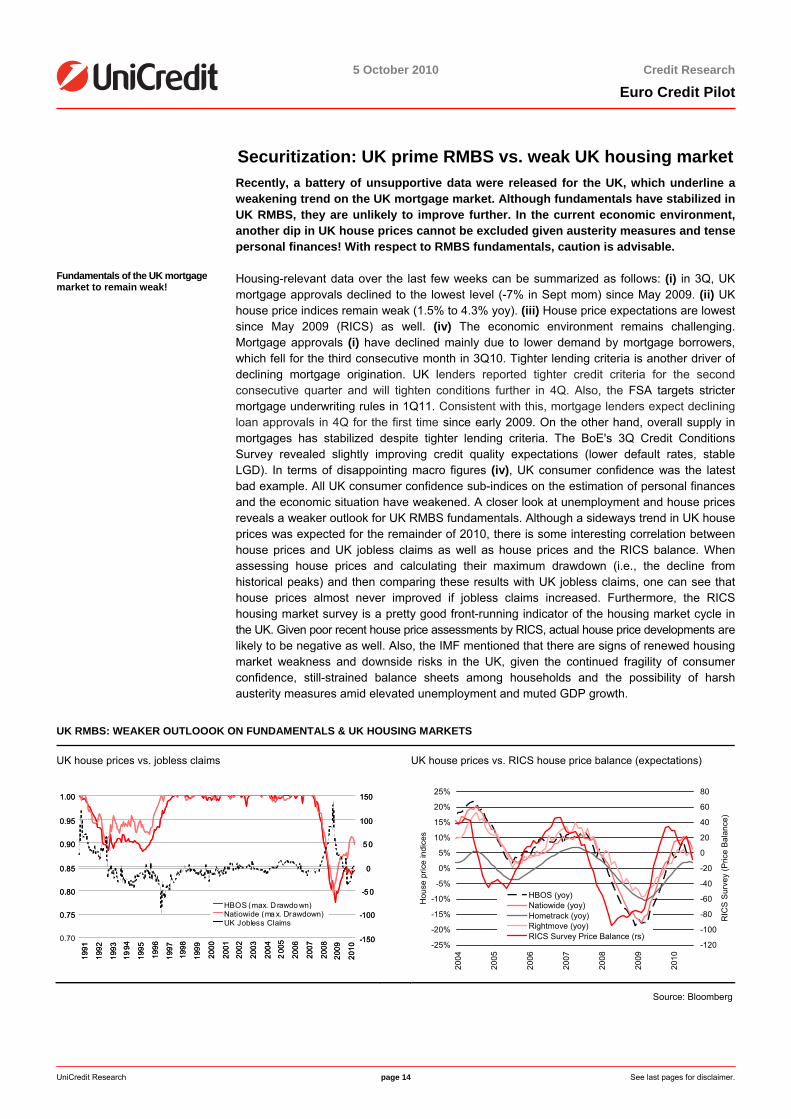

Securitization: UK prime RMBS vs. weak UK housing market Recently, a battery of unsupportive data were released for the UK, which underline a

weakening trend on the UK mortgage market. Although fundamentals have stabilized in UK RMBS, they are unlikely to improve further. In the current economic environment,another dip in UK house prices cannot be excluded given austerity measures and tense personal finances! With respect to RMBS fundamentals, caution is advisable.

Fundamentals of the UK mortgage market to remain weak!

Housing-relevant data over the last few weeks can be summarized as follows: (i) in 3Q, UK mortgage approvals declined to the lowest level (-7% in Sept mom) since May 2009. (ii) UK house price indices remain weak (1.5% to 4.3% yoy). (iii) House price expectations are lowest since May 2009 (RICS) as well. (iv) The economic environment remains challenging. Mortgage approvals (i) have declined mainly due to lower demand by mortgage borrowers,which fell for the third consecutive month in 3Q10. Tighter lending criteria is another driver ofdeclining mortgage origination. UK lenders reported tighter credit criteria for the second consecutive quarter and will tighten conditions further in 4Q. Also, the FSA targets stricter mortgage underwriting rules in 1Q11. Consistent with this, mortgage lenders expect declining loan approvals in 4Q for the first time since early 2009. On the other hand, overall supply inmortgages has stabilized despite tighter lending criteria. The BoE's 3Q Credit ConditionsSurvey revealed slightly improving credit quality expectations (lower default rates, stableLGD). In terms of disappointing macro figures (iv), UK consumer confidence was the latest bad example. All UK consumer confidence sub-indices on the estimation of personal finances and the economic situation have weakened. A closer look at unemployment and house pricesreveals a weaker outlook for UK RMBS fundamentals. Although a sideways trend in UK houseprices was expected for the remainder of 2010, there is some interesting correlation betweenhouse prices and UK jobless claims as well as house prices and the RICS balance. Whenassessing house prices and calculating their maximum drawdown (i.e., the decline fromhistorical peaks) and then comparing these results with UK jobless claims, one can see thathouse prices almost never improved if jobless claims increased. Furthermore, the RICShousing market survey is a pretty good front-running indicator of the housing market cycle in the UK. Given poor recent house price assessments by RICS, actual house price developments are likely to be negative as well. Also, the IMF mentioned that there are signs of renewed housing market weakness and downside risks in the UK, given the continued fragility of consumerconfidence, still-strained balance sheets among households and the possibility of harshausterity measures amid elevated unemployment and muted GDP growth.

UK RMBS: WEAKER OUTLOOOK ON FUNDAMENTALS & UK HOUSING MARKETS

UK house prices vs. jobless claims UK house prices vs. RICS house price balance (expectations)

0.75

0.80

0.85

0.90

0.95

1.00

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

200

5

2006

2007

2008

2009

2010

-150

-100

-5 0

0

5 0

100

150

0.70

HBOS (max. D rawdo wn)Natiowide (ma x. Drawdown)UK Jobless Claims

0.75

0.80

0.85

0.90

0.95

1.00

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

200

5

2006

2007

2008

2009

2010

-150

-100

-5 0

0

5 0

100

150

0.70

HBOS (max. D rawdo wn)Natiowide (ma x. Drawdown)UK Jobless Claims

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2004

2005

2006

2007

2008

2009

2010

Hou

se p

rice

indi

ces

-120

-100

-80

-60

-40

-20

0

20

40

60

80

RIC

S S

urve

y (P

rice

Bala

nce)

HBOS (yoy)Natiowide (yoy)Hometrack (yoy)Rightmove (yoy)RICS Survey Price Balance (rs)

Source: Bloomberg

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 15 See last pages for disclaimer.

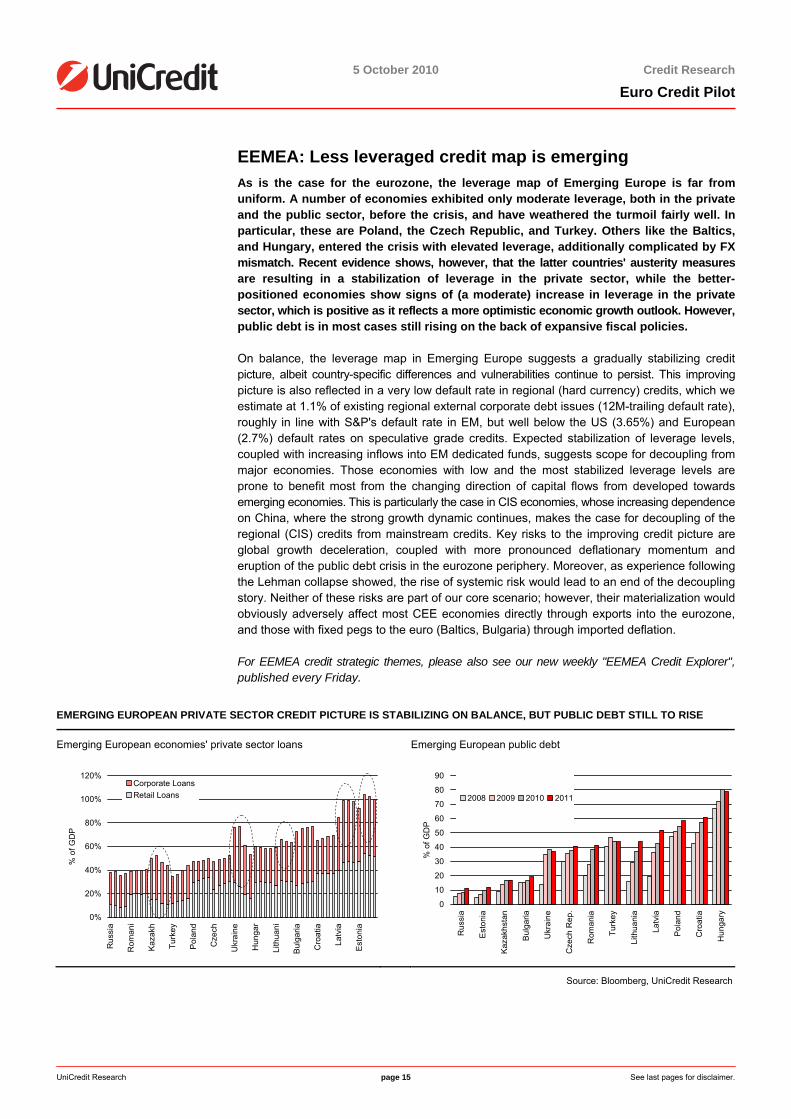

EEMEA: Less leveraged credit map is emerging As is the case for the eurozone, the leverage map of Emerging Europe is far from

uniform. A number of economies exhibited only moderate leverage, both in the privateand the public sector, before the crisis, and have weathered the turmoil fairly well. Inparticular, these are Poland, the Czech Republic, and Turkey. Others like the Baltics,and Hungary, entered the crisis with elevated leverage, additionally complicated by FXmismatch. Recent evidence shows, however, that the latter countries' austerity measuresare resulting in a stabilization of leverage in the private sector, while the better-positioned economies show signs of (a moderate) increase in leverage in the privatesector, which is positive as it reflects a more optimistic economic growth outlook. However, public debt is in most cases still rising on the back of expansive fiscal policies.

On balance, the leverage map in Emerging Europe suggests a gradually stabilizing creditpicture, albeit country-specific differences and vulnerabilities continue to persist. This improvingpicture is also reflected in a very low default rate in regional (hard currency) credits, which weestimate at 1.1% of existing regional external corporate debt issues (12M-trailing default rate), roughly in line with S&P's default rate in EM, but well below the US (3.65%) and European (2.7%) default rates on speculative grade credits. Expected stabilization of leverage levels,coupled with increasing inflows into EM dedicated funds, suggests scope for decoupling frommajor economies. Those economies with low and the most stabilized leverage levels areprone to benefit most from the changing direction of capital flows from developed towardsemerging economies. This is particularly the case in CIS economies, whose increasing dependence on China, where the strong growth dynamic continues, makes the case for decoupling of theregional (CIS) credits from mainstream credits. Key risks to the improving credit picture areglobal growth deceleration, coupled with more pronounced deflationary momentum and eruption of the public debt crisis in the eurozone periphery. Moreover, as experience followingthe Lehman collapse showed, the rise of systemic risk would lead to an end of the decouplingstory. Neither of these risks are part of our core scenario; however, their materialization would obviously adversely affect most CEE economies directly through exports into the eurozone,and those with fixed pegs to the euro (Baltics, Bulgaria) through imported deflation.

For EEMEA credit strategic themes, please also see our new weekly "EEMEA Credit Explorer", published every Friday.

EMERGING EUROPEAN PRIVATE SECTOR CREDIT PICTURE IS STABILIZING ON BALANCE, BUT PUBLIC DEBT STILL TO RISE

Emerging European economies' private sector loans Emerging European public debt

0%

20%

40%

60%

80%

100%

120%

Rus

sia

Rom

ani

Kaz

akh

Turk

ey

Pol

and

Cze

ch

Ukr

aine

Hun

gar

Lith

uani

Bul

garia

Cro

atia

Latv

ia

Est

onia

% o

f GD

P

Corporate Loans Retail Loans

0

10

20

30

40

50

60

70

80

90

Rus

sia

Est

onia

Kaz

akhs

tan

Bul

garia

Ukr

aine

Cze

ch R

ep.

Rom

ania

Turk

ey

Lith

uani

a

Latv

ia

Pol

and

Cro

atia

Hun

gary

% o

f GD

P

2008 2009 2010 2011

Source: Bloomberg, UniCredit Research

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 16 See last pages for disclaimer.

Sector Allocation Given our concerns regarding a potential materialization of macroeconomic headline

risks, we stick to our cautious stance towards investment grade corporate credit risk.We prefer more stable and less cyclical sectors, such as Industrial Transportation (i.e.Toll Roads), Food & Beverages and Tobacco. However, we also stick to our morecyclical bet in overweighting Oil & Gas. We remain underweight in cyclical sectors likeIndustrial Goods & Services and Construction & Materials, as well as in Health Care(which is a non-cyclical sector but trading very tight). Chemicals (which we alsounderweight) is a special case. Although the industry tends to be more cyclical ingeneral, the iBoxx sector mainly consists of the German heavyweights BASF, Bayerand Linde (accounting for more than 60% of the outstanding volume and ranging in thesingle-A rating category), which either operate in stable niches (industrial gases in thecase of Linde) or diversified into non-cyclical operations (pharmaceuticals in the case of Bayer and oil and gas in the case of BASF). Nevertheless, we believe that the sectoroffers little value compared to other industries.

CREDIT ALLOCATION TABLE

As of 4 October 2010

Current recommendation

iBoxx weight (%)

YTD spread change

Current spread level

Macro allocation Sovereigns AAA OW 34.9 -16.1 -23.3Sovereigns ex-AAA MW 27.8 63.0 121.3Sub-Sovereigns OW 13.1 4.7 29.2Covered Bonds OW 4.1 49.2 114.5Financials MW 9.5 -7.2 188.8Non-Financials UW 10.7 8.0 99.9Sector allocation NFI Telecommunications TEL MW 16.8 23.7 115.8Media MDI MW 1.6 -21.3 113.9Technology THE MW 0.8 -7.3 94.0Automobiles & Parts ATO MW 9.3 -20.0 77.7Utilities UTS MW 25.5 21.6 96.3Oil & Gas OIG OW 7.3 11.1 97.6Industrial Goods & Services (Core) IGS UW 6.4 -15.0 105.2Aerospace & Defense AED MW 0.8 36.3 133.0Industrial Transportation ITR OW 3.6 41.9 155.7Basic Resources BAS MW 2.3 15.2 160.9Chemicals CHE UW 4.3 -10.2 79.0Construction & Materials CNS UW 3.4 36.3 176.9Health Care HCA UW 6.4 2.2 49.3Personal & Household Goods (Core) PHG MW 1.9 -11.8 71.0Tobacco TOB OW 2.3 -11.6 81.1Food & Beverage FOB OW 2.8 -19.5 69.7Travel & Leisure TAL UW 0.7 -109.9 155.6Retail RET UW 4.0 -3.4 81.9Quality allocation NFI AAA OW 0.2 -10.9 25.3AA OW 12.5 0.5 50.6A MW 49.2 3.6 75.9BBB UW 38.1 12.2 147.4

Source: UniCredit Research

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 17 See last pages for disclaimer.

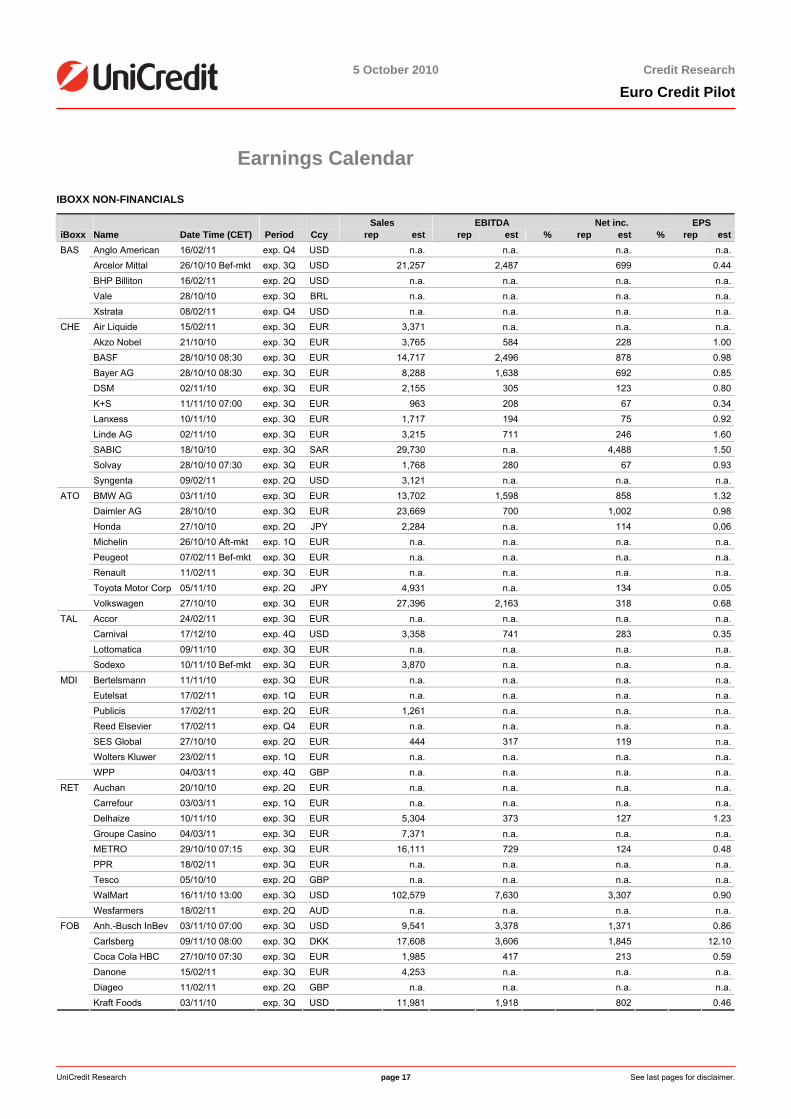

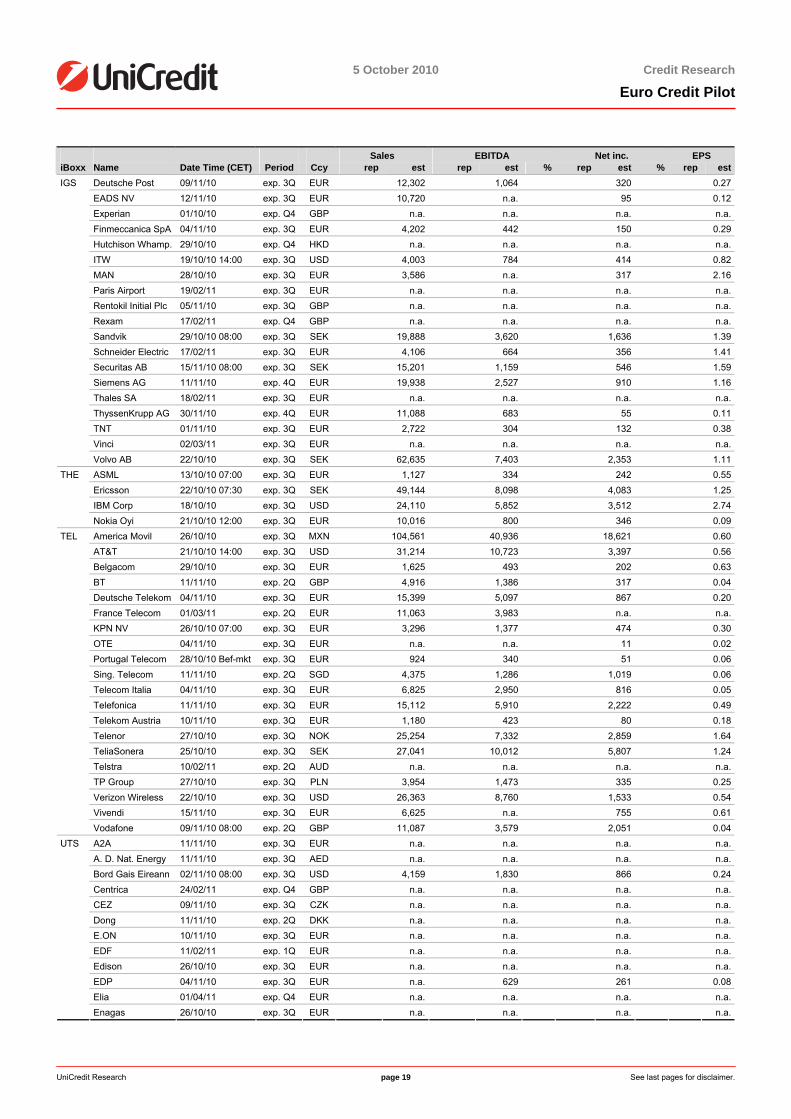

Earnings Calendar

IBOXX NON-FINANCIALS

Sales EBITDA Net inc. EPS iBoxx Name Date Time (CET) Period Ccy rep est rep est % rep est % rep est

Anglo American 16/02/11 exp. Q4 USD n.a. n.a. n.a. n.a.Arcelor Mittal 26/10/10 Bef-mkt exp. 3Q USD 21,257 2,487 699 0.44BHP Billiton 16/02/11 exp. 2Q USD n.a. n.a. n.a. n.a.Vale 28/10/10 exp. 3Q BRL n.a. n.a. n.a. n.a.

BAS

Xstrata 08/02/11 exp. Q4 USD n.a. n.a. n.a. n.a.Air Liquide 15/02/11 exp. 3Q EUR 3,371 n.a. n.a. n.a.Akzo Nobel 21/10/10 exp. 3Q EUR 3,765 584 228 1.00BASF 28/10/10 08:30 exp. 3Q EUR 14,717 2,496 878 0.98Bayer AG 28/10/10 08:30 exp. 3Q EUR 8,288 1,638 692 0.85DSM 02/11/10 exp. 3Q EUR 2,155 305 123 0.80K+S 11/11/10 07:00 exp. 3Q EUR 963 208 67 0.34Lanxess 10/11/10 exp. 3Q EUR 1,717 194 75 0.92Linde AG 02/11/10 exp. 3Q EUR 3,215 711 246 1.60SABIC 18/10/10 exp. 3Q SAR 29,730 n.a. 4,488 1.50Solvay 28/10/10 07:30 exp. 3Q EUR 1,768 280 67 0.93

CHE

Syngenta 09/02/11 exp. 2Q USD 3,121 n.a. n.a. n.a.BMW AG 03/11/10 exp. 3Q EUR 13,702 1,598 858 1.32Daimler AG 28/10/10 exp. 3Q EUR 23,669 700 1,002 0.98Honda 27/10/10 exp. 2Q JPY 2,284 n.a. 114 0.06Michelin 26/10/10 Aft-mkt exp. 1Q EUR n.a. n.a. n.a. n.a.Peugeot 07/02/11 Bef-mkt exp. 3Q EUR n.a. n.a. n.a. n.a.Renault 11/02/11 exp. 3Q EUR n.a. n.a. n.a. n.a.Toyota Motor Corp 05/11/10 exp. 2Q JPY 4,931 n.a. 134 0.05

ATO

Volkswagen 27/10/10 exp. 3Q EUR 27,396 2,163 318 0.68Accor 24/02/11 exp. 3Q EUR n.a. n.a. n.a. n.a.Carnival 17/12/10 exp. 4Q USD 3,358 741 283 0.35Lottomatica 09/11/10 exp. 3Q EUR n.a. n.a. n.a. n.a.

TAL

Sodexo 10/11/10 Bef-mkt exp. 3Q EUR 3,870 n.a. n.a. n.a.Bertelsmann 11/11/10 exp. 3Q EUR n.a. n.a. n.a. n.a.Eutelsat 17/02/11 exp. 1Q EUR n.a. n.a. n.a. n.a.Publicis 17/02/11 exp. 2Q EUR 1,261 n.a. n.a. n.a.Reed Elsevier 17/02/11 exp. Q4 EUR n.a. n.a. n.a. n.a.SES Global 27/10/10 exp. 2Q EUR 444 317 119 n.a.Wolters Kluwer 23/02/11 exp. 1Q EUR n.a. n.a. n.a. n.a.

MDI

WPP 04/03/11 exp. 4Q GBP n.a. n.a. n.a. n.a.Auchan 20/10/10 exp. 2Q EUR n.a. n.a. n.a. n.a.Carrefour 03/03/11 exp. 1Q EUR n.a. n.a. n.a. n.a.Delhaize 10/11/10 exp. 3Q EUR 5,304 373 127 1.23Groupe Casino 04/03/11 exp. 3Q EUR 7,371 n.a. n.a. n.a.METRO 29/10/10 07:15 exp. 3Q EUR 16,111 729 124 0.48PPR 18/02/11 exp. 3Q EUR n.a. n.a. n.a. n.a.Tesco 05/10/10 exp. 2Q GBP n.a. n.a. n.a. n.a.WalMart 16/11/10 13:00 exp. 3Q USD 102,579 7,630 3,307 0.90

RET

Wesfarmers 18/02/11 exp. 2Q AUD n.a. n.a. n.a. n.a.Anh.-Busch InBev 03/11/10 07:00 exp. 3Q USD 9,541 3,378 1,371 0.86Carlsberg 09/11/10 08:00 exp. 3Q DKK 17,608 3,606 1,845 12.10Coca Cola HBC 27/10/10 07:30 exp. 3Q EUR 1,985 417 213 0.59Danone 15/02/11 exp. 3Q EUR 4,253 n.a. n.a. n.a.Diageo 11/02/11 exp. 2Q GBP n.a. n.a. n.a. n.a.

FOB

Kraft Foods 03/11/10 exp. 3Q USD 11,981 1,918 802 0.46

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 18 See last pages for disclaimer.

Sales EBITDA Net inc. EPS iBoxx Name Date Time (CET) Period Ccy rep est rep est % rep est % rep est

SABMiller 18/11/10 08:00 exp. 2Q USD n.a. n.a. n.a. n.a.Südzucker 14/10/10 exp. 2Q EUR 1,616 n.a. n.a. 0.34

FOB

Unilever 04/11/10 08:00 exp. 3Q EUR 11,514 n.a. 1,261 0.43BAT 24/02/11 exp. 1Q GBP n.a. n.a. n.a. n.a.Fortune Brands 22/10/10 exp. 3Q USD 1,737 307 112 0.74Henkel 10/11/10 exp. 3Q EUR 3,789 422 283 0.64Imperial Tobacco 02/11/10 exp. Q4 GBP n.a. n.a. n.a. n.a.Japan Tobacco 28/10/10 08:00 exp. 2Q JPY 1,514 n.a. n.a. 5.66LVMH 04/02/11 exp. 2Q EUR 4,418 n.a. n.a. n.a.Philip Morris 21/10/10 exp. 3Q USD 6,917 3,250 1,859 1.01

PHG

Procter & Gamble 29/10/10 exp. 1Q USD 20,169 5,224 3,028 1.00BG Group plc 02/11/10 08:00 exp. 3Q USD 4,159 1,830 866 0.24BP P.L.C 02/11/10 08:00 exp. 3Q USD 73,702 10,833 4,824 0.26ENI 28/10/10 exp. 3Q EUR 21,487 5,611 1,533 0.47Gazprom 13/10/10 exp. 2Q RUB 724,916 294,293 176,268 n.a.OMV 10/11/10 07:30 exp. 3Q EUR 5,485 863 291 1.09Pemex 01/03/11 exp. 3Q MXN n.a. n.a. n.a. n.a.Repsol YPF 11/11/10 08:00 exp. 3Q EUR 11,670 2,127 499 0.39Schlumberger 22/10/10 12:00 exp. 3Q USD 6,546 1,770 891 0.71Shell 28/10/10 08:00 exp. 3Q USD 68,085 8,280 4,430 0.72StatoilHydro 03/11/10 exp. 3Q NOK 133,525 44,154 10,776 3.41Total 29/10/10 exp. 3Q EUR 36,292 7,705 2,563 1.24

OIG

Transneft 02/06/11 exp. 3Q RUB 96,489 40,138 16,129 2,271.2AstraZeneca 28/10/10 08:00 exp. 3Q USD 7,880 3,485 2,115 1.49Bristol-Myers Sq. 22/10/10 exp. 3Q USD 4,919 1,528 988 0.53GlaxoSmithKline 21/10/10 exp. 3Q GBP 6,956 2,433 1,509 0.29Johnson & Joh. 19/10/10 exp. 3Q USD 15,161 4,581 3,192 1.15Merck & Co. 22/10/10 exp. 3Q USD 11,195 3,432 2,552 0.82Merck KGaA 26/10/10 exp. 3Q EUR 2,434 458 277 1.36Novartis 21/10/10 exp. 3Q USD 12,637 2,770 2,621 1.19Pfizer 20/10/10 exp. 3Q USD 16,653 5,908 4,068 0.51Roche 03/02/11 exp. Q4 CHF n.a. n.a. n.a. n.a.

HCA

Sanofi-Aventis 28/10/10 exp. 3Q EUR 7,873 n.a. 2,301 1.73Bouygues 02/12/10 17:45 exp. 3Q EUR 16 n.a. -401 n.a.Ciments Francais 08/11/10 exp. 3Q EUR n.a. n.a. n.a. n.a.CRH 02/03/11 exp. Q4 EUR n.a. n.a. n.a. n.a.Holcim 10/11/10 07:00 exp. 3Q CHF 6,041 1,530 678 2.03Imerys 03/11/10 Aft-mkt exp. 3Q EUR 811 n.a. 68 n.a.Italcementi 03/11/10 exp. 3Q EUR 1,294 273 56 0.23Lafarge 05/11/10 exp. 3Q EUR 4,678 n.a. n.a. 1.81Saint-Gobain 25/02/11 exp. 3Q EUR 10,318 n.a. n.a. n.a.

CNS

Vinci 02/03/11 exp. 3Q EUR n.a. n.a. n.a. n.a.3M Company 28/10/10 15:00 exp. 3Q USD 6,783 1,912 1,093 1.51ABB 28/10/10 exp. 3Q USD 7,848 1,177 697 0.31Abertis 04/11/10 exp. 3Q EUR 1,098 n.a. 169 0.23Adecco S.A. 09/11/10 exp. 3Q EUR 4,861 223 126 0.66Alstom 04/11/10 exp. 2Q EUR 4,601 n.a. n.a. n.a.APRR 24/02/11 exp. 2Q EUR n.a. n.a. n.a. n.a.Areva 23/02/11 exp. 3Q EUR n.a. n.a. n.a. n.a.Atlantia 11/11/10 exp. 3Q EUR n.a. n.a. n.a. n.a.Atlas Copco 22/10/10 exp. 3Q SEK 17,344 3,744 2,260 1.92Brisa 02/11/10 exp. 3Q EUR 198 143 66 0.11Caterpillar 21/10/10 13:30 exp. 3Q USD 10,362 1,449 685 1.09Danaher 21/10/10 12:00 exp. 3Q USD 3,157 668 378 0.55

IGS

Deere & Co. 24/11/10 exp. 4Q USD 6,362 692 399 0.92

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 19 See last pages for disclaimer.

Sales EBITDA Net inc. EPS iBoxx Name Date Time (CET) Period Ccy rep est rep est % rep est % rep est

Deutsche Post 09/11/10 exp. 3Q EUR 12,302 1,064 320 0.27EADS NV 12/11/10 exp. 3Q EUR 10,720 n.a. 95 0.12Experian 01/10/10 exp. Q4 GBP n.a. n.a. n.a. n.a.Finmeccanica SpA 04/11/10 exp. 3Q EUR 4,202 442 150 0.29Hutchison Whamp. 29/10/10 exp. Q4 HKD n.a. n.a. n.a. n.a.ITW 19/10/10 14:00 exp. 3Q USD 4,003 784 414 0.82MAN 28/10/10 exp. 3Q EUR 3,586 n.a. 317 2.16Paris Airport 19/02/11 exp. 3Q EUR n.a. n.a. n.a. n.a.Rentokil Initial Plc 05/11/10 exp. 3Q GBP n.a. n.a. n.a. n.a.Rexam 17/02/11 exp. Q4 GBP n.a. n.a. n.a. n.a.Sandvik 29/10/10 08:00 exp. 3Q SEK 19,888 3,620 1,636 1.39Schneider Electric 17/02/11 exp. 3Q EUR 4,106 664 356 1.41Securitas AB 15/11/10 08:00 exp. 3Q SEK 15,201 1,159 546 1.59Siemens AG 11/11/10 exp. 4Q EUR 19,938 2,527 910 1.16Thales SA 18/02/11 exp. 3Q EUR n.a. n.a. n.a. n.a.ThyssenKrupp AG 30/11/10 exp. 4Q EUR 11,088 683 55 0.11TNT 01/11/10 exp. 3Q EUR 2,722 304 132 0.38Vinci 02/03/11 exp. 3Q EUR n.a. n.a. n.a. n.a.

IGS

Volvo AB 22/10/10 exp. 3Q SEK 62,635 7,403 2,353 1.11ASML 13/10/10 07:00 exp. 3Q EUR 1,127 334 242 0.55Ericsson 22/10/10 07:30 exp. 3Q SEK 49,144 8,098 4,083 1.25IBM Corp 18/10/10 exp. 3Q USD 24,110 5,852 3,512 2.74

THE

Nokia Oyi 21/10/10 12:00 exp. 3Q EUR 10,016 800 346 0.09America Movil 26/10/10 exp. 3Q MXN 104,561 40,936 18,621 0.60AT&T 21/10/10 14:00 exp. 3Q USD 31,214 10,723 3,397 0.56Belgacom 29/10/10 exp. 3Q EUR 1,625 493 202 0.63BT 11/11/10 exp. 2Q GBP 4,916 1,386 317 0.04Deutsche Telekom 04/11/10 exp. 3Q EUR 15,399 5,097 867 0.20France Telecom 01/03/11 exp. 2Q EUR 11,063 3,983 n.a. n.a.KPN NV 26/10/10 07:00 exp. 3Q EUR 3,296 1,377 474 0.30OTE 04/11/10 exp. 3Q EUR n.a. n.a. 11 0.02Portugal Telecom 28/10/10 Bef-mkt exp. 3Q EUR 924 340 51 0.06Sing. Telecom 11/11/10 exp. 2Q SGD 4,375 1,286 1,019 0.06Telecom Italia 04/11/10 exp. 3Q EUR 6,825 2,950 816 0.05Telefonica 11/11/10 exp. 3Q EUR 15,112 5,910 2,222 0.49Telekom Austria 10/11/10 exp. 3Q EUR 1,180 423 80 0.18Telenor 27/10/10 exp. 3Q NOK 25,254 7,332 2,859 1.64TeliaSonera 25/10/10 exp. 3Q SEK 27,041 10,012 5,807 1.24Telstra 10/02/11 exp. 2Q AUD n.a. n.a. n.a. n.a.TP Group 27/10/10 exp. 3Q PLN 3,954 1,473 335 0.25Verizon Wireless 22/10/10 exp. 3Q USD 26,363 8,760 1,533 0.54Vivendi 15/11/10 exp. 3Q EUR 6,625 n.a. 755 0.61

TEL

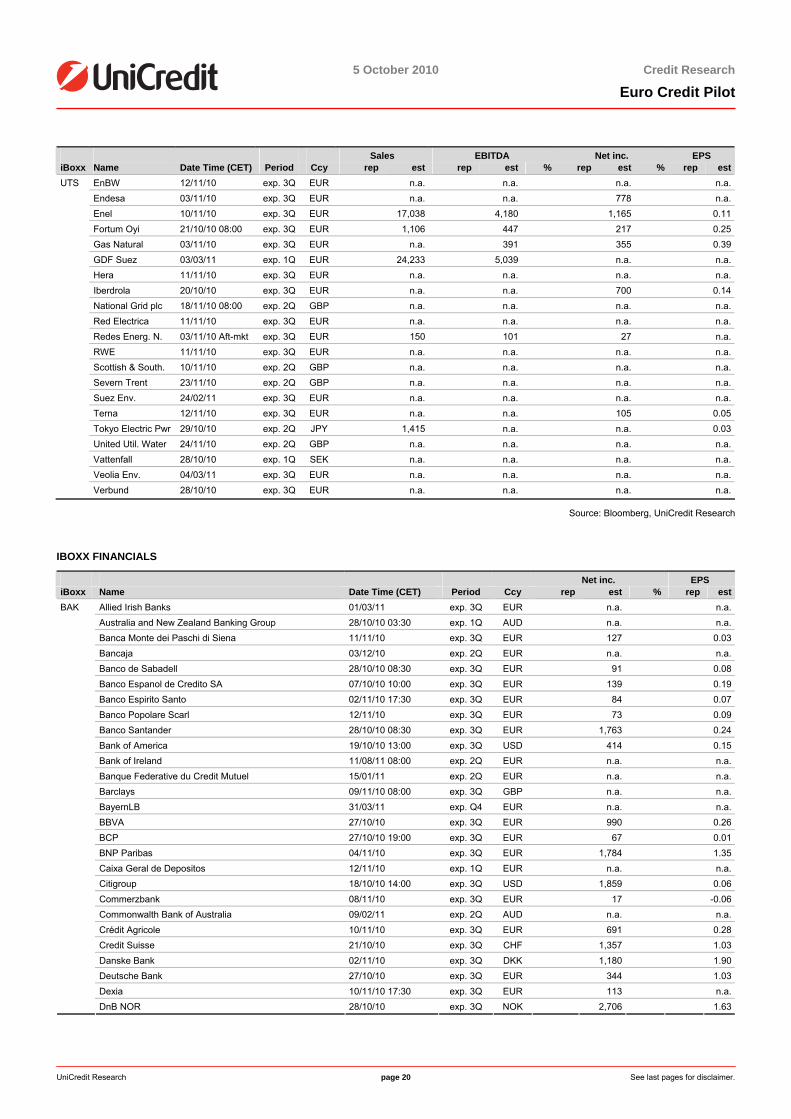

Vodafone 09/11/10 08:00 exp. 2Q GBP 11,087 3,579 2,051 0.04A2A 11/11/10 exp. 3Q EUR n.a. n.a. n.a. n.a.A. D. Nat. Energy 11/11/10 exp. 3Q AED n.a. n.a. n.a. n.a.Bord Gais Eireann 02/11/10 08:00 exp. 3Q USD 4,159 1,830 866 0.24Centrica 24/02/11 exp. Q4 GBP n.a. n.a. n.a. n.a.CEZ 09/11/10 exp. 3Q CZK n.a. n.a. n.a. n.a.Dong 11/11/10 exp. 2Q DKK n.a. n.a. n.a. n.a.E.ON 10/11/10 exp. 3Q EUR n.a. n.a. n.a. n.a.EDF 11/02/11 exp. 1Q EUR n.a. n.a. n.a. n.a.Edison 26/10/10 exp. 3Q EUR n.a. n.a. n.a. n.a.EDP 04/11/10 exp. 3Q EUR n.a. 629 261 0.08Elia 01/04/11 exp. Q4 EUR n.a. n.a. n.a. n.a.

UTS

Enagas 26/10/10 exp. 3Q EUR n.a. n.a. n.a. n.a.

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 20 See last pages for disclaimer.

Sales EBITDA Net inc. EPS iBoxx Name Date Time (CET) Period Ccy rep est rep est % rep est % rep est

EnBW 12/11/10 exp. 3Q EUR n.a. n.a. n.a. n.a.Endesa 03/11/10 exp. 3Q EUR n.a. n.a. 778 n.a.Enel 10/11/10 exp. 3Q EUR 17,038 4,180 1,165 0.11Fortum Oyi 21/10/10 08:00 exp. 3Q EUR 1,106 447 217 0.25Gas Natural 03/11/10 exp. 3Q EUR n.a. 391 355 0.39GDF Suez 03/03/11 exp. 1Q EUR 24,233 5,039 n.a. n.a.Hera 11/11/10 exp. 3Q EUR n.a. n.a. n.a. n.a.Iberdrola 20/10/10 exp. 3Q EUR n.a. n.a. 700 0.14National Grid plc 18/11/10 08:00 exp. 2Q GBP n.a. n.a. n.a. n.a.Red Electrica 11/11/10 exp. 3Q EUR n.a. n.a. n.a. n.a.Redes Energ. N. 03/11/10 Aft-mkt exp. 3Q EUR 150 101 27 n.a.RWE 11/11/10 exp. 3Q EUR n.a. n.a. n.a. n.a.Scottish & South. 10/11/10 exp. 2Q GBP n.a. n.a. n.a. n.a.Severn Trent 23/11/10 exp. 2Q GBP n.a. n.a. n.a. n.a.Suez Env. 24/02/11 exp. 3Q EUR n.a. n.a. n.a. n.a.Terna 12/11/10 exp. 3Q EUR n.a. n.a. 105 0.05Tokyo Electric Pwr 29/10/10 exp. 2Q JPY 1,415 n.a. n.a. 0.03United Util. Water 24/11/10 exp. 2Q GBP n.a. n.a. n.a. n.a.Vattenfall 28/10/10 exp. 1Q SEK n.a. n.a. n.a. n.a.Veolia Env. 04/03/11 exp. 3Q EUR n.a. n.a. n.a. n.a.

UTS

Verbund 28/10/10 exp. 3Q EUR n.a. n.a. n.a. n.a.

Source: Bloomberg, UniCredit Research

IBOXX FINANCIALS

Net inc. EPS iBoxx Name Date Time (CET) Period Ccy rep est % rep est

Allied Irish Banks 01/03/11 exp. 3Q EUR n.a. n.a.Australia and New Zealand Banking Group 28/10/10 03:30 exp. 1Q AUD n.a. n.a.Banca Monte dei Paschi di Siena 11/11/10 exp. 3Q EUR 127 0.03Bancaja 03/12/10 exp. 2Q EUR n.a. n.a.Banco de Sabadell 28/10/10 08:30 exp. 3Q EUR 91 0.08Banco Espanol de Credito SA 07/10/10 10:00 exp. 3Q EUR 139 0.19Banco Espirito Santo 02/11/10 17:30 exp. 3Q EUR 84 0.07Banco Popolare Scarl 12/11/10 exp. 3Q EUR 73 0.09Banco Santander 28/10/10 08:30 exp. 3Q EUR 1,763 0.24Bank of America 19/10/10 13:00 exp. 3Q USD 414 0.15Bank of Ireland 11/08/11 08:00 exp. 2Q EUR n.a. n.a.Banque Federative du Credit Mutuel 15/01/11 exp. 2Q EUR n.a. n.a.Barclays 09/11/10 08:00 exp. 3Q GBP n.a. n.a.BayernLB 31/03/11 exp. Q4 EUR n.a. n.a.BBVA 27/10/10 exp. 3Q EUR 990 0.26BCP 27/10/10 19:00 exp. 3Q EUR 67 0.01BNP Paribas 04/11/10 exp. 3Q EUR 1,784 1.35Caixa Geral de Depositos 12/11/10 exp. 1Q EUR n.a. n.a.Citigroup 18/10/10 14:00 exp. 3Q USD 1,859 0.06Commerzbank 08/11/10 exp. 3Q EUR 17 -0.06Commonwalth Bank of Australia 09/02/11 exp. 2Q AUD n.a. n.a.Crédit Agricole 10/11/10 exp. 3Q EUR 691 0.28Credit Suisse 21/10/10 exp. 3Q CHF 1,357 1.03Danske Bank 02/11/10 exp. 3Q DKK 1,180 1.90Deutsche Bank 27/10/10 exp. 3Q EUR 344 1.03Dexia 10/11/10 17:30 exp. 3Q EUR 113 n.a.

BAK

DnB NOR 28/10/10 exp. 3Q NOK 2,706 1.63

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 21 See last pages for disclaimer.

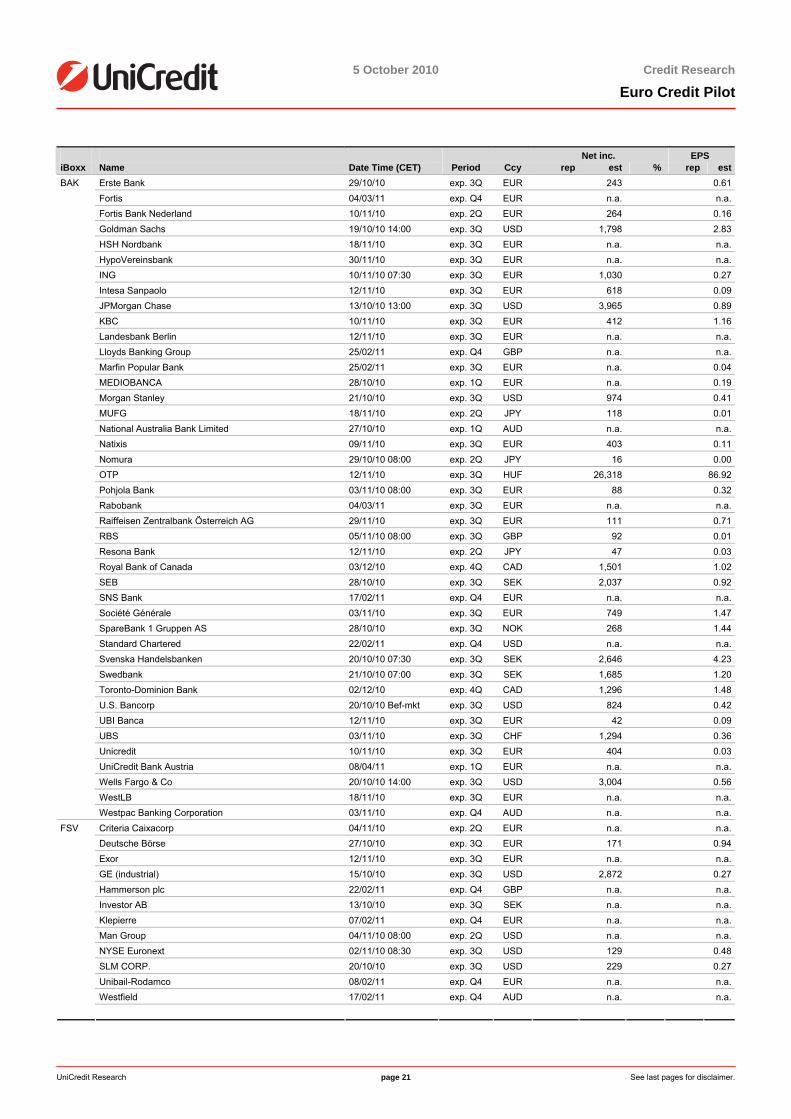

Net inc. EPS iBoxx Name Date Time (CET) Period Ccy rep est % rep est

Erste Bank 29/10/10 exp. 3Q EUR 243 0.61Fortis 04/03/11 exp. Q4 EUR n.a. n.a.Fortis Bank Nederland 10/11/10 exp. 2Q EUR 264 0.16Goldman Sachs 19/10/10 14:00 exp. 3Q USD 1,798 2.83HSH Nordbank 18/11/10 exp. 3Q EUR n.a. n.a.HypoVereinsbank 30/11/10 exp. 3Q EUR n.a. n.a.ING 10/11/10 07:30 exp. 3Q EUR 1,030 0.27Intesa Sanpaolo 12/11/10 exp. 3Q EUR 618 0.09JPMorgan Chase 13/10/10 13:00 exp. 3Q USD 3,965 0.89KBC 10/11/10 exp. 3Q EUR 412 1.16Landesbank Berlin 12/11/10 exp. 3Q EUR n.a. n.a.Lloyds Banking Group 25/02/11 exp. Q4 GBP n.a. n.a.Marfin Popular Bank 25/02/11 exp. 3Q EUR n.a. 0.04MEDIOBANCA 28/10/10 exp. 1Q EUR n.a. 0.19Morgan Stanley 21/10/10 exp. 3Q USD 974 0.41MUFG 18/11/10 exp. 2Q JPY 118 0.01National Australia Bank Limited 27/10/10 exp. 1Q AUD n.a. n.a.Natixis 09/11/10 exp. 3Q EUR 403 0.11Nomura 29/10/10 08:00 exp. 2Q JPY 16 0.00OTP 12/11/10 exp. 3Q HUF 26,318 86.92Pohjola Bank 03/11/10 08:00 exp. 3Q EUR 88 0.32Rabobank 04/03/11 exp. 3Q EUR n.a. n.a.Raiffeisen Zentralbank Österreich AG 29/11/10 exp. 3Q EUR 111 0.71RBS 05/11/10 08:00 exp. 3Q GBP 92 0.01Resona Bank 12/11/10 exp. 2Q JPY 47 0.03Royal Bank of Canada 03/12/10 exp. 4Q CAD 1,501 1.02SEB 28/10/10 exp. 3Q SEK 2,037 0.92SNS Bank 17/02/11 exp. Q4 EUR n.a. n.a.Société Générale 03/11/10 exp. 3Q EUR 749 1.47SpareBank 1 Gruppen AS 28/10/10 exp. 3Q NOK 268 1.44Standard Chartered 22/02/11 exp. Q4 USD n.a. n.a.Svenska Handelsbanken 20/10/10 07:30 exp. 3Q SEK 2,646 4.23Swedbank 21/10/10 07:00 exp. 3Q SEK 1,685 1.20Toronto-Dominion Bank 02/12/10 exp. 4Q CAD 1,296 1.48U.S. Bancorp 20/10/10 Bef-mkt exp. 3Q USD 824 0.42UBI Banca 12/11/10 exp. 3Q EUR 42 0.09UBS 03/11/10 exp. 3Q CHF 1,294 0.36Unicredit 10/11/10 exp. 3Q EUR 404 0.03UniCredit Bank Austria 08/04/11 exp. 1Q EUR n.a. n.a.Wells Fargo & Co 20/10/10 14:00 exp. 3Q USD 3,004 0.56WestLB 18/11/10 exp. 3Q EUR n.a. n.a.

BAK

Westpac Banking Corporation 03/11/10 exp. Q4 AUD n.a. n.a.Criteria Caixacorp 04/11/10 exp. 2Q EUR n.a. n.a.Deutsche Börse 27/10/10 exp. 3Q EUR 171 0.94Exor 12/11/10 exp. 3Q EUR n.a. n.a.GE (industrial) 15/10/10 exp. 3Q USD 2,872 0.27Hammerson plc 22/02/11 exp. Q4 GBP n.a. n.a.Investor AB 13/10/10 exp. 3Q SEK n.a. n.a.Klepierre 07/02/11 exp. Q4 EUR n.a. n.a.Man Group 04/11/10 08:00 exp. 2Q USD n.a. n.a.NYSE Euronext 02/11/10 08:30 exp. 3Q USD 129 0.48SLM CORP. 20/10/10 exp. 3Q USD 229 0.27Unibail-Rodamco 08/02/11 exp. Q4 EUR n.a. n.a.Westfield 17/02/11 exp. Q4 AUD n.a. n.a.

FSV

<date>

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 22 See last pages for disclaimer.

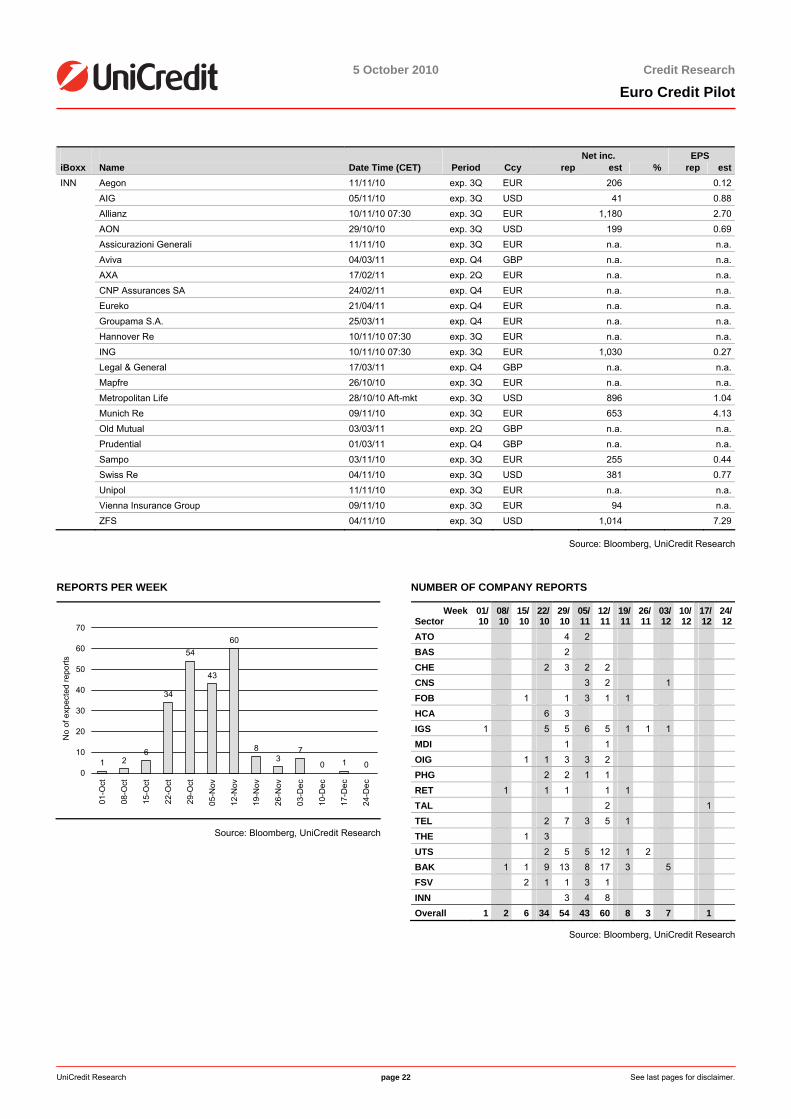

Net inc. EPS iBoxx Name Date Time (CET) Period Ccy rep est % rep est

Aegon 11/11/10 exp. 3Q EUR 206 0.12AIG 05/11/10 exp. 3Q USD 41 0.88Allianz 10/11/10 07:30 exp. 3Q EUR 1,180 2.70AON 29/10/10 exp. 3Q USD 199 0.69Assicurazioni Generali 11/11/10 exp. 3Q EUR n.a. n.a.Aviva 04/03/11 exp. Q4 GBP n.a. n.a.AXA 17/02/11 exp. 2Q EUR n.a. n.a.CNP Assurances SA 24/02/11 exp. Q4 EUR n.a. n.a.Eureko 21/04/11 exp. Q4 EUR n.a. n.a.Groupama S.A. 25/03/11 exp. Q4 EUR n.a. n.a.Hannover Re 10/11/10 07:30 exp. 3Q EUR n.a. n.a.ING 10/11/10 07:30 exp. 3Q EUR 1,030 0.27Legal & General 17/03/11 exp. Q4 GBP n.a. n.a.Mapfre 26/10/10 exp. 3Q EUR n.a. n.a.Metropolitan Life 28/10/10 Aft-mkt exp. 3Q USD 896 1.04Munich Re 09/11/10 exp. 3Q EUR 653 4.13Old Mutual 03/03/11 exp. 2Q GBP n.a. n.a.Prudential 01/03/11 exp. Q4 GBP n.a. n.a.Sampo 03/11/10 exp. 3Q EUR 255 0.44Swiss Re 04/11/10 exp. 3Q USD 381 0.77Unipol 11/11/10 exp. 3Q EUR n.a. n.a.Vienna Insurance Group 09/11/10 exp. 3Q EUR 94 n.a.

INN

ZFS 04/11/10 exp. 3Q USD 1,014 7.29

Source: Bloomberg, UniCredit Research

REPORTS PER WEEK

1 26

34

54

43

60

83

7

0 1 00

10

20

30

40

50

60

70

01-O

ct

08-O

ct

15-O

ct

22-O

ct

29-O

ct

05-N

ov

12-N

ov

19-N

ov

26-N

ov

03-D

ec

10-D

ec

17-D

ec

24-D

ec

No

of e

xpec

ted

repo

rts

Source: Bloomberg, UniCredit Research

NUMBER OF COMPANY REPORTS

WeekSector

01/10

08/10

15/10

22/10

29/10

05/11

12/11

19/11

26/11

03/12

10/12

17/12

24/12

ATO 4 2 BAS 2 CHE 2 3 2 2 CNS 3 2 1FOB 1 1 3 1 1 HCA 6 3 IGS 1 5 5 6 5 1 1 1MDI 1 1 OIG 1 1 3 3 2 PHG 2 2 1 1 RET 1 1 1 1 1 TAL 2 1TEL 2 7 3 5 1 THE 1 3 UTS 2 5 5 12 1 2 BAK 1 1 9 13 8 17 3 5FSV 2 1 1 3 1 INN 3 4 8 Overall 1 2 6 34 54 43 60 8 3 7 1

Source: Bloomberg, UniCredit Research

5 October 2010

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 23 See last pages for disclaimer.

Fundamental Credit Views

Telecommunications (Marketweight) Sector key figures Sector Wrap-Up Weight in iBoxx NFI: Current ASW spread: change mom/YTD: Euro STOXX TEL YTD:

16.8% 115.8bp +0.6/+23.7 -1.1%

Sector drivers: Currently, fundamentals are still taking a backseat in the assessment of telecom credits and the underlying sovereign debt crisis and macroeconomic environment are still the main drivers of spreads. For 4Q10, we mainly assume three possible scenarios: 1) The sovereign debt crisis appears more manageable and the related negative sentiment calms down. In this case, the telecom average sector bond spread should see a stronger recovery than the NFI average bond spread. 2) The sovereign debt crisis and austerity measures weigh more strongly on the economic development than expected and we face a so-called "double-dip" scenario. Then, telecom bonds are likely to benefit in general from their "safe-haven" status and low cyclicality compared to other sectors. 3) The situation remains basically unchanged. In this case, telecom bond spreads, in particular those of OTE, PT, TEF and TI will continue to stabilize at currently exaggerated levels. The 2Q10 earnings season indicated a positive development for telecom incumbents in 2H10. The vast majority of telecom operators reported better-than-expected results for 2Q10, showing stronger-than-expected top-line growth driven by the macroeconomic recovery, while all incumbents continue their cost reduction programs, i.e., EBITDA often also exceeded consensus estimates as the EBITDA margin remained stable or even improved or declined less than expected. With regard to shareholder remuneration, the trend towards longer-term direction continues (already announced by Telefonica, Vodafone and DT), i.e., France Telecom proposed a minimum dividend of EUR 1.40 p.a., as well as the trend to share buybacks (DT started its share buyback program and Telenor announced a new share buyback program; FT did not rule it out). On the M&A front, clearly the acquisition of PT's stake in Brasilcel/Vivo by Telefonica dominated the headlines. More recently, Vivendi clearly stated its willingness to acquire minorities in Canal+ France and SFR. However, so far, M&A was definitely not a major spread driver in 2010. The main spread driver currently remains the sovereign debt development and the macro environment, while in the last month the recovery in sovereign spreads benefited the telecom sector average spread. It currently seems that our scenario 1, which drove spreads in August and September, might take a backseat and scenario 2 might drive telecom spreads in October. Last month's recap: In September, the iBoxx average Telecoms sector spread tightened by around 4bp to 119bp, while the NFI spread also tightened by 4bp to 102bp. Hence, the telecom sector spread performed in line with the iBoxx NFI average spread. In absence of company-related newsflow during September, spreads were largely driven by the positive macroeconomic newsflow. High-beta bonds (OTE, TITIM, BRITEL) outperformed low-beta bonds in the Telecoms sector. Moreover, PORTEL and TELEFO bonds underperformed, driven by further sovereign concerns.

Current Ratings (Moody's/S&P/Fitch)

Credit Profile

Name (Ticker): Recommendation Weight in iBoxxComment Telecommunications sector

A2s/A-s/A-s Stable America Movil (AMXLMM): No recommendation (event-driven coverage) 1.6%In June, America Movil made its debut in the EUR and GBP bond markets, as it issued EUR 1.0bn (7Y), EUR 750mn (12Y) and GBP 650mn (20Y) notes. America Movil is Mexico's largest wireless operator with a market share of approximately 71%. In addition, it is positioned as a leading regional mobile telecom service provider in Latin America with over 206 million wireless subscribers. Globally, it ranks No. 8 in the global telecom universe in terms of revenues and EBITDA. It generated a strong operating cash flow of over USD 10bn in the last twelve months ending 31 March 2010, stand-alone, and should have a low leverage of 1.3x adjusted debt to EBITDA for year-end 2010 (expected by Moody's pro forma for the recent acquisitions of Telmex and Telint). The integration of recent acquisitions of Telmex and Telint (reason for the new issues: refinancing these acquisitions) will help America Movil to return its targeted leverage of adjusted debt-to-EBITDA back to its guidance of below 1x. The new issues were well received in the Eurobond market as a good diversification in the single A-rated telecom segment.

A2n/Awn/As Stable AT&T (T): Marketweight 2.4%AT&T reported better-than-expected 2Q10 results and revised its outlook up. Sales increased by 0.6% yoy to USD 30.81bn versus USD 30.53bn in 1Q10. The group EBITDA rose yoy by 5.6% and 1.3% qoq to USD 10.95bn. In 2Q10, FOCF generation fell to USD 3.7bn (USD 7.6bn in 1H10) from USD 3.8bn in 2Q09, mainly due to higher working capital-related cash outflows, while FFO exceeded last year's 2Q by USD 1.5bn, partially offset by yoy higher capex of USD 0.8mn. The company used USD 2.5bn of FOCF for dividend payments, while the remainder was not sufficient to offset cash outflows for the acquisition of Alltel assets from Verizon for USD 2.35bn. Net debt (derived from the reported balance sheet) increased yoy from USD 66.8bn to USD 68.6bn, according to our calculations. AT&T's reported annualized net debt-to-EBITDA (LTM) declined qoq to 1.5x from 1.6x (YE09: 1.7x). AT&T has updated its earnings outlook for full-year 2010 due to improved revenue trends and strong execution: Previously, the company expected stable-to-improved earnings per share, stable-to-improved consolidated operating income margins and free cash flow in line with 2008 results. The company now expects strong earnings per share growth for full-year 2010, improved consolidated operating income margins and FOCF above 2008 levels (USD 13.3bn). Capex is expected to rise to USD 18-19bn due to higher wireless capacity investments (USD 17.3bn in 2009). On 28 July 2010, S&P placed its single-A rating on AT&T on creditwatch with negative implications, as the company may not be able to achieve financial metrics (fully adjusted net debt to EBITDA ratio below 2.0x, i.e., reported net debt to EBITDA slightly above 1.0x) fully supportive of the current rating within a reasonable timeframe. The rating action followed a statement of the company during its 2Q10 earnings call that in the future it will consider using excess FCF for purposes other than debt reduction, including possibly for share repurchases. However, current spread levels of its euro-denominated bonds discount for these risks as well as for a potential downgrade to a low single A rating. (3Q10 results: 21 October)

5 October 2010

5 October 2010 Credit Research

Euro Credit Pilot

UniCredit Research page 24 See last pages for disclaimer.

Current Ratings (Moody's/S&P/Fitch)

Credit Profile

Name (Ticker): Recommendation Weight in iBoxxComment Telecommunications sector