eq industry 5.1 hmsi - icici...

TRANSCRIPT

ICICI Securities Ltd. | Retail Equity Research

May 25, 2017

MotoGaze May 2017

New fiscal commences on good note!

Overall auto volumes for April 2017 grew 9.5% YoY. This is primarily

attributable to positive consumer sentiments (ongoing marriage season &

recovery from demonetisation). Growth was also partly supported by

higher stock filling (by OEMs) at dealer level to normalise inventory level

in the system (after liquidation of BS III vehicles). Overall 2-W volumes

grew 10.5% YoY, strongly supported by scooter space (grew 25.5% YoY).

HMSI – the second largest 2-W player registered strong growth of 34%

YoY thereby narrowing the gap between itself & market leader HMCL. The

overall PV segment continued its strong growth momentum, registering

growth of 14.4% YoY. The growth was supported by both cars & utility

vehicle (UV), which reported growth of 15.4% YoY & 16.9% YoY,

respectively. The PV market leader, MSIL, reported strong volume growth

of 19.5% YoY and continued to outpace overall industry growth. Overall

CV volumes declined 25% YoY as M&HCV volumes reported sharp de-

growth of 50.9% YoY, while LCV segment reported moderate de-growth

of 5.4% YoY for April 2017. M&HCV players were unable to ramp up and

produce higher BS IV vehicles in April 2017 as OEMs were planning to

gradually increase their production thereby impacting volumes for April

2017. The 3-W volumes fell 6.3% YoY as domestic volumes continued to

decline (down 18% YoY). However, the same was offset by some export

recovery (volume up 22.7% YoY). A good harvest season & higher MSPs

supported domestic tractor volumes, which grew 19.3% YoY.

HMSI & MSIL dominate in April 2017

Strong volume growth was largely registered by two players viz. HMSI (in

the 2-W space) & MSIL (in the 4-W) space driving overall auto volumes for

the industry. HMSI reported strong volume growth of 34% YoY to 578,777

units, led by robust growth in its scooter segment (Activa volumes up

33.6% YoY to 312,632 units). Its strong volume growth further narrowed

the gap (to 16,841 units) between HMSI & market leader HMCL. MSIL (in

the 4-W space) continued to outpace the industry, with volumes up 19.5%

YoY to 150,768 units. Of the top 10 selling PV models, seven models

continue to be of MSIL. However, the top selling car – Alto has now been

replaced by Swift for April 2017. Apart from that, TVS’ mopeds volumes

declined 12.9% YoY to 59,674 units mainly due to high base

Near term hiccup fading away; long term story intact

After four years of subdued growth (FY12-16 volume CAGR of 4%), auto

demand recovered. Volumes were up 11.1% YoY in 7MFY17.

Demonetisation had a short-term (<six months) negative impact mainly

due to deferral of vehicle purchase, impacting FY17 volumes, which grew

5.1% YoY. However, we believe long term growth expectations of the

sector remain intact, primarily supported by the positive impact of the

Seventh Pay Commission, emission norms (BS VI by 2020) & vehicle

scrappage policy. Further, the Indian Meteorological Department (IMD)

predicts near normal monsoon at 96% of long period average (LPA) for

upcoming monsoon season 2017, which is positive for the economy.

Normal monsoon will be positive for rural areas thereby boosting auto

demand (especially 2-W & tractor segment). We expect industry volumes

to grow >8%, with 2W, PV & CV segment likely to grow 8%, 9% & 8%

YoY, respectively, in FY18E.

For April 2017, the BSE Auto Index was up 3.5% outperforming the

benchmark index, which surged 1%. In our I-direct auto coverage, we

remain bullish on frontline OEM stocks like Maruti Suzuki and Eicher

Motors. However, with the favourable impact of operating leverage due to

increased demand, the earnings growth trajectory for ancillary stocks is

likely to remain on the uptrend.

Sector View

Equal weight

Volume performance for April 2017

Company Gr. YoY(%)

Hero Motocorp -2.8

Bajaj Auto 0.0

TVS Motors 8.4

Maruti Suzuki 19.5

Tata Motors -21.4

Ashok Leyland -30.4

Mahindra and Mahindra -6.0

Key players & industry volume growth – Apr’17 (%)

7.5

-2.3

21.2

-4.0

58.1

8.2

-45.8

-29.8

1.4

-62.0

9.5

-2.8

0.0

8.4

34.3

19.5

-21.4

-6.0

3.6

-30.4

Industry

HMCL

BAL

TVS

HMSI

Maruti

TML

M&M

Hyundai

ALL

MoM

YoY

Source: Siam

Key players & industry volume growth FY17 (%)

5.1

0.5

-5.9

10.8

12.6

9.8

6.1

2.5

4.7

3.3

Industry

HMCL

BAL

TVS

HMSI

Maruti

TML

M&M

Hyundai

ALL

FY17 gr

Source: Siam

Research Analyst

Nishit Zota

Vidrum Mehta

ICICI Securities Ltd. | Retail Equity Research

Page 2

HMSI drives overall two-wheeler volumes!

For April 2017, overall 2-W volumes grew 10.5% YoY mainly supported by

scooters segment, which reported strong growth of 25.5% YoY. The

motorcycle segment reported growth of 5.7% YoY. The moped segment,

which in the past registered >15% YoY growth, has taken a breather in

the past two or three months, with volumes down 12.9% YoY. Further,

overall domestic 2-W volumes grew 7.3% YoY while exports volumes

grew 40% YoY for April 2017. For FY17, the 2-W segment registered 5.2%

YoY growth, driven by scooter segment (up 11.3% YoY) and mopeds (up

23.3% YoY). The motorcycle segment registered modest growth of 1.6%

YoY for FY17. For April 2017, the 3-W volumes declined 6.3% YoY, as

domestic volumes continued to remain weak (down 18% YoY). However,

the same was offset by an export recovery (volume up 22.7% YoY). For

April 2017, the domestic tractor volume grew 19.3% YoY 54,917 units.

Market share movement

According to data released by the Society of Indian Automobile

Manufacturers (Siam), the domestic market share of two and three-

wheeler players as of April 2017 is mentioned below.

Exhibit 1: Domestic market share movement in two-wheelers

12.85

38.49

12.67

26.54

9.46

11.38

36.86

14.15

26.86

10.74

9.67

34.97

12.27

32.94

10.15

0

5

10

15

20

25

30

35

40

45

Bajaj Auto Hero MotoCorp TVS Motors HMSI Others

(%

)

Apr-16 Mar-17 Apr-17

Source: Siam, Data used is YTD

Exhibit 2: Domestic market share movement in three-wheelers

57.6

28.0

8.4

6.1

49.5

29.5

10.2

10.8

43.6

28.0

9.4

19.0

0 10 20 30 40 50 60 70

Bajaj Auto

Piaggio

M&M

Others

(%)

Apr-16 Mar-17 Apr-17

Source: Siam, Data used is YTD

The overall 2-W segment volumes grew 10.5% YoY in April

2017. HMSI reported robust volume growth of 34.3% YoY;

thereby gaining market share (up 641 bps YoY) to 32.9%. On the

flip side, HMCL volumes declined 2.8% YoY thereby losing its

market share, which is currently at ~35%

In April 2017, domestic 3W volumes declined 18% YoY. This

is mainly after the top two players viz. - Bajaj Auto & Piaggio

reported volume de-growth of 37.9% YoY & 17.8% YoY,

respectively, resulting in a loss of market share. The other

players viz. - TVS reported decent volume growth while Atul

Auto also posted strong YoY growth (mainly due to low base

of last year)

ICICI Securities Ltd. | Retail Equity Research

Page 3

Exhibit 3: Domestic market share movement in motorcycles

19.6

50.4

6.8

14.7

18.0

51.3

7.0

13.815.7

50.7

6.6

17.8

0

10

20

30

40

50

60

70

Bajaj Auto Hero Motocorp TVS motor Honda

(%

)

Apr-16 Mar-17 Apr-17

Source: Company, ICICIdirect.com Research

Exhibit 4: Domestic market share movement in scooters/scooters

17.8

12.9

56.2

13.014.1 14.7

56.9

14.3

10.9

13.5

62.8

12.8

0

10

20

30

40

50

60

70

Hero Motocorp TVS Motors Honda Others

(%

)

Apr-16 Mar-17 Apr-17

Source: Siam, Data used is YTD

Overall motorcycle volumes grew 5.7% YoY in April 2017.

HMCL continues to be the market leader in the space with

share of ~51%

Overall scooter volumes grew 25.5% YoY in April 2017.

HMSI’s scooter segment grew 40.4% YoY, thereby gaining

market share, which was at 62.8%

ICICI Securities Ltd. | Retail Equity Research

Page 4

Exhibit 5: Market share movement in executive motorcycle (<125 cc) segment*

18.1

58.1

6.5

17.2

0

10

20

30

40

50

60

70

Apr-15

May-15

Jun-15

Jul-15

Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

(%

)

0

4

8

12

16

20

(%

)

Bajaj Auto (RHS) Hero Motocorp (LHS) TVS (RHS) HMSI (RHS)

Source: Siam * only top 4 two-wheeler OEMs

Exhibit 6: Market share movement in motorcycle greater than 125 cc segment

58.4

4.4

18.4

18.8

0

10

20

30

40

50

60

70

80

Apr-15

May-15

Jun-15

Jul-15

Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

(%

)

0

4

8

12

16

20

24

(%

)

Bajaj Auto (LHS) Hero Motocorp (RHS) TVS (RHS) HMSI (RHS)

Source: Siam *only top three vehicle two-wheeler OEMs

HMCL continues to dominate the executive motorcycle

segment (<=125 cc) in India with a market share of ~58%.

HMSI’s volumes have been more volatile thereby resulting in

wide fluctuation in its market share in eight to nine months

BAL continues to dominate the executive motorcycle

segment (<=125 cc) in India with market share of 58%.

HMSI’s market share recovered significantly to 18.8% largely

due to a recovery in volume of its ‘CB series’ in April 2017

ICICI Securities Ltd. | Retail Equity Research

Page 5

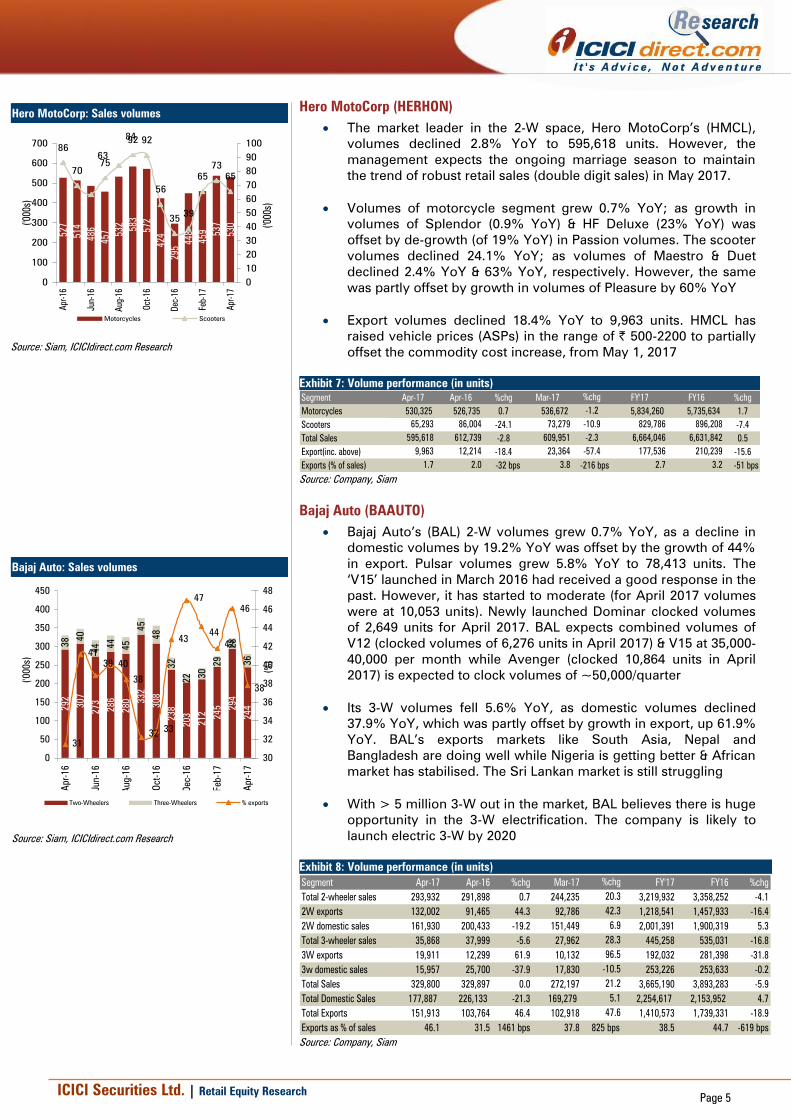

Hero MotoCorp (HERHON)

The market leader in the 2-W space, Hero MotoCorp’s (HMCL),

volumes declined 2.8% YoY to 595,618 units. However, the

management expects the ongoing marriage season to maintain

the trend of robust retail sales (double digit sales) in May 2017.

Volumes of motorcycle segment grew 0.7% YoY; as growth in

volumes of Splendor (0.9% YoY) & HF Deluxe (23% YoY) was

offset by de-growth (of 19% YoY) in Passion volumes. The scooter

volumes declined 24.1% YoY; as volumes of Maestro & Duet

declined 2.4% YoY & 63% YoY, respectively. However, the same

was partly offset by growth in volumes of Pleasure by 60% YoY

Export volumes declined 18.4% YoY to 9,963 units. HMCL has

raised vehicle prices (ASPs) in the range of | 500-2200 to partially

offset the commodity cost increase, from May 1, 2017

Exhibit 7: Volume performance (in units)

Segment Apr-17 Apr-16 %chg Mar-17 %chg FY'17 FY16 %chg

Motorcycles 530,325 526,735 0.7 536,672 -1.2 5,834,260 5,735,634 1.7

Scooters 65,293 86,004 -24.1 73,279 -10.9 829,786 896,208 -7.4

Total Sales 595,618 612,739 -2.8 609,951 -2.3 6,664,046 6,631,842 0.5

Export(inc. above) 9,963 12,214 -18.4 23,364 -57.4 177,536 210,239 -15.6

Exports (% of sales) 1.7 2.0 -32 bps 3.8 -216 bps 2.7 3.2 -51 bps

Source: Company, Siam

Bajaj Auto (BAAUTO)

Bajaj Auto’s (BAL) 2-W volumes grew 0.7% YoY, as a decline in

domestic volumes by 19.2% YoY was offset by the growth of 44%

in export. Pulsar volumes grew 5.8% YoY to 78,413 units. The

‘V15’ launched in March 2016 had received a good response in the

past. However, it has started to moderate (for April 2017 volumes

were at 10,053 units). Newly launched Dominar clocked volumes

of 2,649 units for April 2017. BAL expects combined volumes of

V12 (clocked volumes of 6,276 units in April 2017) & V15 at 35,000-

40,000 per month while Avenger (clocked 10,864 units in April

2017) is expected to clock volumes of ~50,000/quarter

Its 3-W volumes fell 5.6% YoY, as domestic volumes declined

37.9% YoY, which was partly offset by growth in export, up 61.9%

YoY. BAL’s exports markets like South Asia, Nepal and

Bangladesh are doing well while Nigeria is getting better & African

market has stabilised. The Sri Lankan market is still struggling

With > 5 million 3-W out in the market, BAL believes there is huge

opportunity in the 3-W electrification. The company is likely to

launch electric 3-W by 2020

Exhibit 8: Volume performance (in units)

Segment Apr-17 Apr-16 %chg Mar-17 %chg FY'17 FY16 %chg

Total 2-wheeler sales 293,932 291,898 0.7 244,235 20.3 3,219,932 3,358,252 -4.1

2W exports 132,002 91,465 44.3 92,786 42.3 1,218,541 1,457,933 -16.4

2W domestic sales 161,930 200,433 -19.2 151,449 6.9 2,001,391 1,900,319 5.3

Total 3-wheeler sales 35,868 37,999 -5.6 27,962 28.3 445,258 535,031 -16.8

3W exports 19,911 12,299 61.9 10,132 96.5 192,032 281,398 -31.8

3w domestic sales 15,957 25,700 -37.9 17,830 -10.5 253,226 253,633 -0.2

Total Sales 329,800 329,897 0.0 272,197 21.2 3,665,190 3,893,283 -5.9

Total Domestic Sales 177,887 226,133 -21.3 169,279 5.1 2,254,617 2,153,952 4.7

Total Exports 151,913 103,764 46.4 102,918 47.6 1,410,573 1,739,331 -18.9

Exports as % of sales 46.1 31.5 1461 bps 37.8 825 bps 38.5 44.7 -619 bps

Source: Company, Siam

Hero MotoCorp: Sales volumes

527

514

486

457 532

583

572

424

295

448

459 537

530

86

70

75

92 92

56

3539

65

73

65

63

84

0

100

200

300

400

500

600

700

Apr-

16

Jun-1

6

Aug-1

6

Oct-

16

Dec-1

6

Feb-1

7

Apr-

17

('000s)

0

10

20

30

40

50

60

70

80

90

100

('000s)

Motorcycles Scooters

Source: Siam, ICICIdirect.com Research

Bajaj Auto: Sales volumes

292

307

273

286

280 3

32

308

238

203

212

245 294

244

38 4

0

44 44

45

45

48

32

22 30

29

28

36

31

41

39 40

38

3233

43

47

44

42

46

38

0

50

100

150

200

250

300

350

400

450

Apr-16

Jun-16

Aug-16

Oct-16

Dec-16

Feb-17

Apr-17

('0

00s)

30

32

34

36

38

40

42

44

46

48

(%

)

Two-Wheelers Three-Wheelers % exports

Source: Siam, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 6

TVS Motors (TVSSUZ)

TVS’ volumes (2-W+3-W) for April 2017 came in at ~2.5 lakh

units, up 8.5% YoY. The 2-W & 3-W volumes grew 8.4% YoY &

11.7% YoY in April 2017

Motorcycle segment volumes grew 10.4% YoY to 99,890 units.

Volumes of Apache grew 48.2% YoY to 39,942 units. Volumes of

Starcity 125 & Sport grew 52.1% YoY to 8373 units & 38% YoY to

24,683 units, respectively. Its scooter volumes grew 28.6% YoY to

81,443 units, mainly attributable to Pep+ (up 31.5% YoY to 9,570

units), Jupiter (up 33.8% YoY to 58,644 units) & Wego (up 27.9%

YoY to 8,124 units). Its moped (new TVS XL 100) volumes

declined by 12.9% YoY at 59,674 units mainly due to high base.

Export (15% of sales) volumes grew 27.1% YoY to 36,052 units,

supported by growth of 43.9% YoY in its 2-W exports

Exhibit 9: Volume performance (in units)

Segment Apr-17 Apr-16 %chg Mar-17 %chg FY'17 FY16 %chg

Motorcycles 99,890 90,491 10.4 95,671 4.4 1,075,248 1,016,807 5.7

Scooters 81,443 63,341 28.6 84,173 -3.2 870,863 813,277 7.1

Mopeds 59,674 68,518 -12.9 71,135 -16.1 910,519 738,547 23.3

Total 2-W Sales 241,007 222,350 8.4 250,979 -4.0 2,856,630 2,579,141 10.8

3-Wheelers 5,303 4,746 11.7 5,362 -1.1 69,254 110,821 -37.5

Total Sales 246,310 227,096 8.5 256,341 -3.9 2,925,884 2,689,962 8.8

Exports(incl. in above) 36,052 28,354 27.1 37,164 -3.0 422,536 454,550 -7.0

Exports as % of sales 15.0 12.8 14.8 14.8 17.6

Domestice sales 210,258 198,742 5.8 219,177 -4.1 2,503,348 2,235,412 12.0

Source: Company, Siam

Honda Motorcycles & Scooters India (HMSI)

For April 2017, HMSI’s volumes grew 34.3% YoY to 578,777 units.

This was after domestic scooter & motorcycle volumes grew

35.4% YoY & 15.2% YoY, respectively

The growth in domestic motorcycles can mainly be attributed to

strong volume growth of 51.2% YoY to 100,824 units. Apart from

that, volume of CB Unicorn grew 156.3% YoY to 20,659 units.

Domestic scooter volume grew 35.4% YoY, supported by growth

across its models. Volumes of Activa & Dio grew 33.6% YoY &

189.1% YoY to 312,632 & 43,948 units, respectively. HMSI’s Navi

has received a lukewarm response as it just managed to clock

volumes of ~63,000 since its launch in February 2016

Export volumes grew 58.7% YoY to 27,045 units, led by strong

growth in both motorcycle & scooter segment. Strong growth in

the export market increased its overall share by 72 bps YoY to

4.7% in April 2017

Exhibit 10: Volume performance (in units)

Segment Apr-17 Apr-16 %chg Mar-17 %chg FY'17 FY16 %chg

Motorcycles 183,182 158,956 15.2 84,638 116.4 1,557,557 1,538,255 1.3

Scooters 368,550 272,119 35.4 254,218 45.0 3,210,671 2,836,964 13.2

Total Sales 578,777 431,075 34.3 366,090 58.1 5,008,188 4,448,063 12.6

Exports(incl.above) 27,045 17,040 58.7 27,234 -0.7 283,151 200,141 41.5

Exports as % of sales 4.7 4.0 72 bps 7.4 -277 bps 5.7 4.5 115 bps

Domestice sales 551,732 414,035 33.3 338,856 62.8 4,725,077 4,247,922 11.2

Source: Company, Siam

TVS Motors: Sales volumes

90

96

95

95

114

123

122

68

58

60

58

96

100

63 65

68

68

77 8

5

92

73

56 71

69

84

81

69 7

6

77

77

77

80 9

0

78

66

72

78

71

60

25

75

125

175

225

275

325

Apr-16

Jun-16

Aug-16

Oct-16

Dec-16

Feb-17

Apr-17

(%

)

Motorcycles Scooters Mopeds

Source: Siam, ICICIdirect.com Research

HMSI: Motorcycles & scooter sales volumes

159

147

143

120

143

184

167

96

53

139

120

85

183

272

268

265

309 3

49 3

56

303

203

152

229

250

254

369

0

100

200

300

400

500

600

Apr-16

Jun-16

Aug-16

Oct-16

Dec-16

Feb-17

Apr-17

('0

00s)

Motorcycles Scooters

Source: Siam, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 7

MSIL dominates PV segment

The overall passenger vehicles segment for April 2017 registered growth

of 14.4% YoY to 338,289 units. Domestic PV volumes increased 14.7%

YoY to 277,602 units while export volumes grew 13.2% YoY to 60,687

units. Within sub-segments of the PV space, utility vehicles (UVs)

continued to report good volume growth of 16.9% YoY. Volumes of

passenger cars also picked up, with the segment reporting growth of

15.4% YoY. On the flip side, vans registered de-growth of 7.5% YoY for

April 2107. Market leader MSIL continued to outperform the industry, with

volumes up 19.5% YoY to 151,215 units.

For April 2017, utility vehicle (UV) volumes were up 16.9% YoY at 83,999

units, supporting the overall PV market. The UV1 sub-segment grew

14.2% YoY to 62,570 units, driven by Maruti Suzuki’s Vitara Brezza, which

has done exceptionally well in a short period since its launch in March

2016, to climb to first position as the highest selling UV model in India. For

April 2017, Vitara Brezza clocked overall volumes of 10,653 units &

Hyundai’s Creta, which clocked volumes of 13,545 units. M&M’s TUV3OO,

which was launched in September 2015, has not helped the company to

capitalise on the UV1 space. For April 2017, volumes of TUV3OO grew

8.2% YoY to 2,086 units. Volumes in the UV2 space increased 7.2% YoY

to 16,784 units, supported by volume growth in Toyota (launched

refreshed Innova) volume grew 54.3% YoY to 6,589 units. Honda’s BR-V,

which is also classified in the UV2 space, received a modest consumer

response since its launch in May 2016 as till date it has clocked volumes of

~23,000 units.

The commercial vehicles volume declined 25% YoY to 45,552 units & was

mainly attributable to M&HCV volumes, which declined 50.9% YoY to

12,842 units. LCV volumes were also adversely impacted with volumes

down 5.4% YoY to 32,710 units. The MHCV/LCV volume ratio was at 28:72

in April 2017 vs. the average ratio 40:60 over the past 36 months.

Market share movement

According to Siam, the domestic market share for passenger vehicles (PV)

and commercial vehicles (CV) in April 2017 was as follows:

Exhibit 11: Domestic market share movement in passenger vehicles

48.4

17.5

5.1

9.4

0.9

18.9

47.4

16.7

5.7

7.8

0.8

21.6

51.9

16.1

5.1

7.0

0.3

19.6

0 10 20 30 40 50 60

Maruti

Hyundai

Tata Motors

M&M

GM

Others

(%)

Apr-16 Mar-17 Apr-17

Source: Siam, Data used is YTD * passenger vehicles as per Siam include Vans like Gio, Maxximo, Eeco, Ace

MSIL continues to dominate the PV segment & with

continued strong volume growth (outpacing the industry

growth) its market share is now at 51.9% in April 2017

ICICI Securities Ltd. | Retail Equity Research

Page 8

Exhibit 12: Market share movement in A2 segment

30.9

25.9

63.1

67.4

0

10

20

30

40

50

60

70

80

Apr-15

May-15

Jun-15

Jul-15

Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

(%

)

Hyundai Maruti

Source: Siam, Top two PV OEMs considered

Exhibit 13: Domestic market share movement in commercial vehicles

17.7

24.0

43.4

14.9

18.7

25.3

42.8

13.2

15.4

36.3 35.6

12.6

0

5

10

15

20

25

30

35

40

45

50

ALL M&M Tata Motors Others

(%

)

Apr-16 Mar-17 Apr-17

Source: Siam Data used is YTD

Exhibit 14: Segmental share in CVs

28.2

41.0

71.8

59.0

0

10

20

30

40

50

60

70

80

Apr-15

May-15

Jun-15

Jul-15

Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

(%

)

M&HCV LCV

Source: Siam

The A2 segment is the bread & butter category of the

passenger car segment. The segment has witnessed some

demand revival primarily supported by MSIL & TML

The M&HCV & LCV volumes declined 50.9% YoY & 5.4%

YoY in April 2017. Thus, overall CV volumes declined 25%

YoY. With the M&M product portfolio more tilted towards

LCV segment against Tata Motors (TML) & Ashok Leyland;

its market share expanded in April 2017

The MHCV/LCV ratio was at 28:72 in April 2017, mainly

after M&HCV volumes declined sharply by 50.9% YoY. The

average M&HCV volume (over the past 36 months) has

been ~40% of the total CV sales. It has been more than

four years when the MHCV/LCV ratio was at similar levels

of 28:72 in November 2012; being more biased towards

the LCV space

ICICI Securities Ltd. | Retail Equity Research

Page 9

Tata Motors (TELCO)

Tata Motors’ standalone volumes declined 21.4% YoY to 30,972

units after strong volume growth in its PV business was offset by

sharp volume de-growth in its CV business

Domestic M&HCV & LCV volumes declined 60% YoY & 15.6% YoY,

respectively. The domestic car segment was up 23.2% YoY to

11,220 units, mainly driven by Tiago, (clocked volumes of 4,115

units) & new Tigor, which clocked volume of 3,638 units. Its

domestic UV space grew 15.7% YoY to 1,607 units, driven by the

new Hexa (clocked volumes of 1,213 units)

JLR’s wholesale volumes grew 2.4% YoY at 41,923 units. Jaguar

volumes were up 37.2% YoY to 12,608 units, mainly driven by F-

Pace, which clocked volumes of ~5,000 units. Land Rover

volumes fell 7.7% YoY to 29,315 units, mainly impacted by decline

in volumes of Discovery. We believe North America & Chinese

market must have witnessed strong growth in April 2017

Exhibit 15: Volume performance (in units)

Segment Apr-17 Apr-16 %chg Mar-17 %chg FY'17 FY16 %chg

Domestic MHCV 4,653 11,642 -60.0 17,648 -73.6 148,901 156,961 -5.1

Domestic LCV 11,364 13,460 -15.6 18,228 -37.7 174,281 170,264 2.4

Domestic Pass.Car Sales 11,220 9,106 23.2 13,032 -13.9 136,184 107,808 26.3

Domestic UV 1,607 1,389 15.7 2,401 -33.1 18,758 18,613 0.8

Exports 2,128 3,785 -43.8 5,836 -63.5 64,199 58,068 10.6

Total Sales 30,972 39,382 -21.4 57,145 -45.8 542,323 510,997 6.1

Jaguar 12,608 9,188 37.2 20,492 -38.5 178,676 102,106 75.0

Landrover 29,315 31,745 -7.7 51,117 -42.7 421,934 441,979 -4.5

Total JLR Sales 41,923 40,933 2.4 71,609 -41.5 600,610 544,085 10.4

Source: Company, Siam

Maruti Suzuki India (MARUTI)

Maruti Suzuki’s (MSIL) volumes increased 19.5% YoY to 151,215

units. The LCV clocked volumes of 411 units in April 2017

Its domestic mini car segment grew 21.9% YoY, after domestic

volumes of Alto & Wagon R grew 35.9% YoY & 6.6% YoY to

22,549 units & 16,348 units, respectively. MSIL has discontinued to

production of DZire Tour. Its Baleno & Vitara Brezza has been well

accepted by customers registering domestic volumes of 17,530

units & 10,653 units, respectively. S-Cross has received a

lukewarm response, since its launch, with domestic volume for

April 2017 at 2,676 units

Export volumes declined 29% YoY, with its share at 4.4% of sales

Exhibit 16: Volume performance (in units)

Segment Apr-17 Apr-16 %chg Mar-17 %chg FY'17 FY16 %chg

Omni, Eeco,Versa 13,938 14,520 -4.0 11,628 19.9 152,009 143,471 6.0

Alto, Wagon-R, Zen, Swift,Ritz,

Celerio, Dzire,Baleno 102,481 77,606 32.1 91,672 11.8 998,831 974,928 2.5

SX4, Swift Dzire Tour, Ciaz 7,024 8,875 -20.9 6,084 15.5 97,060 92,536 4.9

Total Passengers 123,443 101,001 22.2 109,384 12.9 1,247,900 1,210,935 3.1

Gypsy, Vitara,Ertiga,Brezza 20,638 16,044 28.6 18,311 12.7 195,741 94,416 107.3

Total Domestic 144,081 117,045 23.1 127,695 12.8 1,443,641 1,305,351 10.6

LCV (Super Carry) 411 0 NA 304 NA 900 0 NA

Exports 6,723 9,524 (29.4) 11,764 -42.9 124,062 123,897 0.1

Total Sales 151,215 126,569 19.5 139,763 8.2 1,568,603 1,429,248 9.8

Exports as % of sales 4.4 7.5 8.4 7.9 8.7

Source: Company, Siam.

Maruti Suzuki India: sales volumes

123

99

137

132 149

134

136

118 1

44

130

140

151

127

7.5

4.4

0

20

40

60

80

100

120

140

160

Apr-16

Jun-16

Aug-16

Oct-16

Dec-16

Feb-17

Apr-17

('0

00s)

0

2

4

6

8

10

12

(%

)

Total Sales Export %

Source: Siam, ICICIdirect.com Research

Tata Motors: Domestic sales volume

28.6

31.2

31.6

29.3

29.2

33.7

36.1

25.8

29.8

33.2

33.4 41.4

18.0

10.8

8.8

12.6

13.9

13.8 15.0

16.8

13.1

11.1 13.2

14.1

15.7

12.9

0

10

20

30

40

50

60

70

Apr-16

Jun-16

Aug-16

Oct-16

Dec-16

Feb-17

Apr-17

(000's

)

CV Sales PV Sales

Source: Company, ICICIdirect.com Research

Jaguar Land Rover sales volume

43.9

47.4 51.8

40.9 46.2

47.2

42.3

52.9

53.1

48.7 5

4.6

71.6

41.9

0

20

40

60

80

100

Apr'1

6

May'1

6

June'1

6

July

'16

Aug'1

6

Sept'1

6

Oct'1

6

Nov'1

6

Dec'1

6

Jan'1

7

Feb'1

7

Mar'1

7

Apr'1

7

(%

share o

f total volu

mes)

10

20

30

40

50

60

70

80

(000's

)

% Jaguar % LR JLR total volumes(RHS)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 10

Ashok Leyland (ASHLEY)

Ashok Leyland’s (ALL) volumes declined 30.4% YoY to 7,090

units, as M&HCV volumes declined 42.4% YoY to 4,532 units. LCV

volumes grew by 10.6% YoY to 2,558 units

Volumes of M&HCV passenger declined 23.8% YoY to 1,286 units

while M&HCV goods volumes declined 47.5% YoY to 3,246 units

Exports grew 2.1% YoY, with overall share at 9.6% of sales. ALL

had ~10,664 unsold BS-III vehicles as of March 31, 2017, of which

(~2,000 units) will be exported. The remaining will be replaced

with BS-IV compliant engines, resulting in one-time additional cost

of | 20-30 crore

Mahindra and Mahindra (MAHMAH)

M&M’s overall automotive volumes declined 6% YoY to 39,357

units. Its core UV segment (including exports) declined 14.5% YoY

to 18,363 units. TUV3OO has not helped M&M, with volumes up

8.2% YoY to 2,086 units. KUV1OO volumes declined 58.5% YoY to

2,200 units. Volumes of XUV5OO also declined 29.1% YoY to

2,073 units

M&M’s tractor volumes grew 21.6% YoY to 26,001 units, post a

good harvest season, good progress in Rabi sowing and increased

MSPs. The domestic tractor industry volumes grew 19.3% YoY

54,917 units in April 2017 & grew 18% YoY (582,844 units) for

FY17

Exhibit 17: Volume performance (in units)

Segment Apr-17 Apr-16 %chg Mar-17 %chg FY'17 FY16 %chg

M&HCV Passenger 1,286 1,688 -23.8 2,372 -45.8 22,592 25,721 -12.2

M&HCV Goods 3,246

6,181 -47.5 12,886 -74.8 90,690 84,034 7.9

LCV 2,558 2,313 10.6 3,424 -25.3 31,774 30,603 3.8

Passenger Vehicles - 0 NA 0 NA - 97 -100.0

Total Sales 7,090 10,182 -30.4 18,682 -62.0 145,056 140,455 3.3

Exports 682 668 2.1 1,174 -41.9 11,792 13,133 -10.2

Exports as % of sales 9.6 6.6 6.3 8.1 9.4

Source: Company, Siam

Exhibit 18: Volume performance (in units)

Segment Apr-17 Apr-16 %chg Mar-17 %chg FY'17 FY16 %chg

UV’s 18,363 21,484 -14.5 23,827 -22.9 222,541 222,513 0.0

4-Wheeler pickups 14,360 11,834 21.3 20,334 -29.4 172,032 162,521 5.9

M & HCV 706 1,113 -36.6 2,574 -72.6 15,327 13,376 14.6

Total 4wheeler Sales 34,391 35,602 -3.4 48,260 -28.7 417,080 403,090 3.5

3-Wheeler 3,438 3,755 -8.4 5,062 -32.1 52,306 54,975 -4.9

Total Domestic Auto Sales 37,829 39,357 -3.9 53,322 -29.1 469,386 458,065 2.5

Exports 1,528 2,506 -39.0 2,709 -43.6 37,241 36,033 3.4

Total Auto Sales 39,357 41,863 -6.0 56,031 -29.8 506,627 494,098 2.5

Exports as % of sales 3.9 6.0 4.8 7.4 7.3

Tractors - Domestic 25,081 20,704 21.1 17,973 39.5 248,409 202,046 22.9

- Exports 920 682 34.9 1,364 -32.6 14,583 11,545 26.3

Total Tractors 26,001 21,386 21.6 19,337 34.5 262,992 213,591 23.1

Exports as % of sales 3.5 3.2 7.1 5.5 5.4

Source: Company, Siam

Mahindra and Mahindra: Sales volume

41.9

40.7

39.0

39.5

40.6 4

6.1 5

2.0

32.5 36.4

39.3 42.7

56.0

39.4

0

10

20

30

40

50

60

70

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

(000's

)

Source: SIAM, ICICIdirect.com Research

Mahindra and Mahindra: Tractor sales

21.4

23.0

30.2

17.6

13.5

30.6

45.2

17.3

14.0

15.9

15.0

19.3

26.0

0

5

10

15

20

25

30

35

40

45

50

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

(000's

)

Source: SIAM, ICICIdirect.com Research

Ashok Leyland: Total sales

7.9

7.5 8.7

8.2

8.2 9.0

9.6

6.9 8

.8

12.1

11.3

15.3

4.5

2.3

2.4

2.4

2.3

2.7 3

.1 3.0

2.6

1.9

2.8

2.7

3.4

2.6

0

2

4

6

8

10

12

14

16

18

20

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

(000's

)

M&HCV LCV

Source: Siam, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 11

Top domestic model wise volumes for April 2017

Exhibit 19: Top 10 passenger vehicle – Models sold in India (in units)

S.No. Models Apr-16 Models Apr-17

1 Alto 16,583 Swift 23,802

2 Swift 15,661 Alto 22,549

3 Wagon R 15,323 Baleno 17,530

4 DZIRE TOUR 13,256 Wagon R 16,348

5 Elite i20 11,147 Elite i20 12,668

6 Grand i10 9,840 Grand i10 12,001

7 Kwid 9,795 VITARA BREZZA 10,653

8 Baleno 9,562 Creta 9,213

9 Celerio 8,548 DZIRE TOUR 8,606

10 Omni 8,356 Celerio 8,425

Source: Siam

Exhibit 20: Top 10 two-wheelers – Models sold in India (in units)

S.No. Models Apr-16 Models Apr-17

1 Activa 233,935 Activa 312,632

2 Splendor 224,238 Splendor 226,681

3 HF Deluxe 116,567 HF Deluxe 143,794

4 Passion 98,976 CB Shine 100,824

5 TVS XL Super 67,045 Passion 80,053

6 Glamour 66,756 Glamour 62,713

7 CB Shine 66,691 Jupiter 58,527

8 CT 66,409 TVS XL Super 57,938

9 Pulsar 50,419 Pulsar 50,219

10 Jupiter 43,256 CT 45,003

Source: Siam

ICICI Securities Ltd. | Retail Equity Research

Page 12

State wise sales mix for Q3FY17 (October – December 2016)

Exhibit 21: Top 10 state wise PV volume for Q3FY17 (in units)

64338

59605

54653

49862

47031

44288

39850

38168

31475

105628

0

20000

40000

60000

80000

100000

120000

Maharashtra

Guja

rat

U.P

.

Karnataka

Kerala

Tam

il N

adu

Delh

i

Haryana

Raja

sthan

Tela

ngana

Passenger Vehicles (PVs) Sales

Source: Siam

Exhibit 22: Top 10 state wise 2-W volume for Q3FY17 (in units)

438,0

30

346,5

84

268,1

57

256,4

06

255,6

87

233,5

57

213,1

29

185,7

06

155,5

27

497,1

90

0

100,000

200,000

300,000

400,000

500,000

600,000

U.P

.

Maharashtra

Tam

il N

adu

Raja

sthan

Karnataka

Guja

rat

Andhra

pradesh

Madhya

Pradesh

West

Bengal

Bih

ar

2-W Sales

Source: Siam

State wise market share of PV for Q3FY17

Maharashtra

21%

Gujarat

9%

U.P.

8%

Karnataka

7%

Kerala

7%

Tamil Nadu

6%

Delhi

6%

Haryana

5%

Rajasthan

5%

Others

33%

Source: Siam, ICICIdirect.com Research

State wise market share of 2-W for Q3FY17

U.P.

12%

Maharashtra

11%

Tamil Nadu

9%

Rajasthan

7%

Karnataka

7%

Gujarat

7%

Andhra pradesh

6%

Madhya

Pradesh

5%

West Bengal

5%

Others

31%

Source: Siam, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 13

State wise sales mix for Q3FY17 (October – December 2016)

Exhibit 23: Top 10 state wise CV volume for Q3FY17 (in units)

14,2

15

11,7

37

11,7

08

10,7

34

9,9

52

9,8

56

8,8

83

7,7

53

7,3

19

25,4

51

0

5,000

10,000

15,000

20,000

25,000

30,000

Maharashtra

U.P

.

Tam

il N

adu

Guja

rat

Raja

sthan

Andhra

pradesh

Karnataka

West

Bengal

Madhya

Pradesh

Haryana

CV Sales

Source: Siam

Exhibit 24: Top 10 state wise 3-W volume for Q3FY17 (in units)

11625

11052

9207

8904

8529

7682

7679

6465

5374

14204

0

2000

4000

6000

8000

10000

12000

14000

16000

Guja

rat

Andhra

pradesh

Maharashtra

Bih

ar

U.P

.

Karnataka

Tam

il N

adu

Tela

ngana

Kerala

Oris

sa

3-W Sales

Source: Siam

State wise market share of CV for Q3FY17

Maharashtra

15%

U.P.

9%

Tamil Nadu

7%

Gujarat

7%

Rajasthan

7%

Andhra pradesh

6%

Karnataka

6%

West Bengal

5%

Madhya

Pradesh

5%

Others

33%

Source: Siam, ICICIdirect.com Research

State wise market share of 3-W for Q3FY17

Gujarat

12%

Andhra pradesh

10%

Maharashtra

9%

Bihar

8%

U.P.

8%

Karnataka

7%

Tamil Nadu

7%

Telangana

7%

Kerala

5%

Others

27%

Source: Siam, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 14

News & views

GST to have neutral to positive impact on auto industry!

We believe GST will have a neutral to positive impact on the overall auto &

auto ancillary space. The effective higher tax rate will largely be passed on

to consumers as OEMs are likely to hike vehicle prices (ASPs). The shift of

the market from the unorganised to the organised ones will actually be

positive for most auto ancillary players, which currently face stiff

competition from unbranded/local players (which skip their tax liability) vs.

organised ones. The transition (from current tax regime to GST)

clarification is still awaited (by the industry) from the government, which

will actually have an impact on the outstanding inventory at the dealer

levels. The following table explains the segment wise current tax bracket.

The expected tax rate after GST implementation and its impact on various

segments is as follows:

Exhibit 25: Impact of GST on various Auto segments

Segment Tax rate

earlier

GST Rate View Impact

2-W 24.3 28.0

The price of 2-Ws<350 cc will increase marginally by 0.5%. Given that there is a

cess of 3% on motorcycles>350cc, the price increase post GST will by 2.6%.

However, motorcycle above 350 cc contributes only 0.4% of the domestic 2-W sales

Neutral

Small car/SUV (Length<4 m; engine

size<1200 cc/1500 cc for petrol/diesel

vehicles)

24.3 28.0

Although the gap between current tax incidence & GST appears optically high,

prices of these vehicles will increase in the range of ~1-3% post GST

implementation, because the base (ex-showroom price) will also change with GST

implementation. This potential price increase will not have an impact on demand

Neutral

Sedan/SUV (length> 4 m;engine size< 1500

cc)

32.3 43.0

Prices of these vehicles will increase ~6%. Prices of cars like Ciaz & Ertiga fall in

this segment, which form ~9% of Maruti's domestic sales

Negative

Sedan/SUV (length> 4 m with engine

size>1500 cc)

35.9 43.0

Prices of these vehicles will increase ~0.5%. There will not be an negative impact

on demand due to the potential price rise

Neutral

CV 24.3 28.0 Prices of these vehicles will increase ~0.5%. Hence, the impact will be neutral Neutral

Tractors 11.9 12.0 Prices of tractors will reduce ~1% Neutral

Source: cbec.gov.in, Company, ICICIdirect.com Research;

ICICI Securities Ltd. | Retail Equity Research

Page 15

ICICIdirect.com Research Universe (Auto & Auto ancillary)

CMP M Cap

(|) TP(|) Rating (| Cr) FY16 FY17E FY18E FY16 FY17E FY18E FY16 FY17E FY18E FY16 FY17E FY18E FY16 FY17E FY18E

Amara Raja (AMARAJ) 836 930 Hold 14280 28.5 29.4 37.3 29.3 28.4 22.4 18.1 17.1 13.7 31.2 26.2 27.9 23.2 20.1 21.2

Apollo Tyre (APOTYR) 223 280 Buy 11246 21.7 21.8 19.7 10.3 10.2 11.3 6.5 7.9 8.6 19.9 13.6 11.0 17.1 15.0 12.2

Ashok Leyland (ASHLEY) 83 100 Buy 23363 2.5 4.0 4.8 32.6 20.7 17.2 11.8 11.6 9.6 22.8 20.8 22.6 17.4 17.4 18.8

Bajaj Auto (BAAUTO) 2770 3000 Hold 80155 126.8 132.3 155.4 23.4 22.5 19.1 17.5 18.0 15.0 42.2 30.5 33.5 29.9 22.4 24.0

Balkrishna Ind. (BALIND) 1476 1400 Buy 14269 58.7 77.0 83.8 20.1 15.3 14.1 11.2 9.6 7.6 20.4 22.5 24.7 20.3 22.5 24.7

Bharat Forge (BHAFOR) 1092 1150 Buy 25449 28.0 30.5 44.6 39.0 35.8 24.5 17.6 17.9 13.4 16.5 14.8 19.5 18.3 17.4 21.5

Bosch (MICO) 22978 25250 Buy 72151 410.2 567.0 566.2 55.2 40.0 40.0 36.0 37.5 26.1 15.1 15.8 15.8 22.5 21.4 25.3

Eicher Motors (EICMOT) 27460 30500 Buy 74169 655.9 833.2 1019.4 41.9 33.0 26.9 24.8 18.4 14.7 39.2 41.1 39.1 36.0 33.6 30.9

Exide Industries (EXIIND) 229 270 Buy 19435 7.3 8.2 9.4 31.2 28.0 24.2 19.0 17.7 14.4 19.4 18.7 20.4 14.0 14.1 14.8

Hero Mototcorp (HERHON) 3566 3975 Buy 71210 156.9 169.1 199.6 22.7 21.1 17.9 15.2 14.3 11.9 53.6 43.5 49.0 39.4 33.0 36.3

JK Tyre & Ind (JKIND) 166 215 Buy 3773 21.0 16.6 18.1 7.9 10.1 9.2 5.8 8.1 6.5 20.1 11.2 11.8 29.1 15.8 18.2

Mahindra CIE (MAHAUT) 241 280 Buy 7770 4.5 10.3 13.5 53.8 23.3 17.8 16.8 11.5 9.1 5.4 10.8 12.6 6.9 11.1 13.2

Maruti Suzuki (MARUTI) 6865 7200 Buy 207463 151.3 242.9 280.1 45.4 28.3 24.5 21.4 18.6 15.8 23.9 26.3 26.5 16.9 20.3 20.4

Motherson (MOTSUM) 427 450 Hold 59909 11.1 16.7 22.9 38.5 25.5 18.6 15.1 10.5 7.8 16.0 22.2 28.4 19.6 23.1 25.0

Wabco India (WABTVS) 5825 7000 Buy 11067 107.7 118.6 158.4 54.1 49.1 36.8 37.9 32.4 24.8 19.4 17.8 19.4 25.5 24.5 26.8

Sector / Company

RoE (%)EPS (|) P/E (x) EV/EBITDA (x) RoCE (%)

Source: ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 16

Exhibit 26: Auto raw material index

RM Auto Index

103

77

96

70

80

90

100

110

May-12

Jul-12

Sep-12

Nov-12

Jan-13

Mar-13

May-13

Jul-13

Sep-13

Nov-13

Jan-14

Mar-14

May-14

Jul-14

Sep-14

Nov-14

Jan-15

Mar-15

May-15

Jul-15

Sep-15

Nov-15

Jan-16

Mar-16

May-16

Jul-16

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Source: Bloomberg, Reuters, Company, ICICIdirect.com Research

Exhibit 27: Currency movements

70

80

90

100

110

120

130

140

150

160

170

Nov-12

Feb-13

May-13

Aug-13

Nov-13

Feb-14

May-14

Aug-14

Nov-14

Feb-15

May-15

Aug-15

Nov-15

Feb-16

May-16

Aug-16

Nov-16

Feb-17

May-17

US$INR US$JPY US$EUR

Volatility in the currency markets is impacting raw material prices for companies with imported

components and lower natural hedges.

Source: Company, ICICIdirect.com Research

The in-house raw material index reflects the combination of

various input materials (steel, rubber, aluminium, plastics)

for OEMs, which have April 2012 as base year at 100. The

chart had showed a declining trend in the past. However,

prices have started moving northwards over the past one

year, indicating that the benefit of lower input cost has

peaked out

ICICI Securities Ltd. | Retail Equity Research

Page 17

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Sector view:

Over weight compared to index

Equal weight compared to index

Under weight compared to index

Index here refers to BSE 500

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities Ltd. | Retail Equity Research

Page 18

ANALYST CERTIFICATION

We /I, Nishit Zota, MBA (Finance) and Vidrum Mehta, MBA (Finance) Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research

report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s)

or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving Nishit Zota, MBA (Finance) and Vidrum Mehta, MBA (Finance) this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or

strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment

decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The

recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities

accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk

Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are

not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Nishit Zota, MBA (Finance) and Vidrum Mehta, MBA (Finance) Research Analysts of this report have not received any compensation from the companies mentioned in the report in the

preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Nishit Zota, MBA (Finance) and Vidrum Mehta, MBA (Finance) Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.

ICICI Securities Ltd. has received an investment banking mandate from Mahindra Life Space Developers Ltd, which is an associate of Mahindra & Mahindra Ltd. This report is prepared based on publicly

available information."