rating matrix indigrid invit - icici...

TRANSCRIPT

May 17, 2017

Public Issue

First power transmission InvIT… Sterlite Power Grid Ventures has come out with an initial public offer (IPO) of India Grid Trust (IndiGrid), India's second infrastructure investment trust (InvIT). IndiGrid InvIT IPO has proposed a price band of | 98-100 per unit aggregating up to | 2,250 crore. The issue opens on May 17 and closes on May 19. It will be listed on both exchanges. Sponsor, Sterlite Power Grid Ventures, is one of the leading independent private sector power transmission companies operating across the country. It owns 11 inter-state transmission projects with a total network of 30 transmission lines of around 7,733 circuit km and nine substations having 13,890 MVA of transmission capacity. Of the 11 inter-state transmission projects, IndiGrid will initially acquire two projects viz. Bhopal Dhule Transmission Co and Jabalpur Transmission Co with a total network of eight transmission lines of around 1,936 circuit km and two substations having 6,000 MVA capacity across four states. Investors will be offered returns predominantly in the form of interest and dividend.

Overview Issue proceeds will be utilised towards reduction of debt of the both projects. Both transmission assets are operational and will distribute at least 90% of net cash available for distribution to InvIT unit holders. Transmission assets, in general, have reasonably higher certainty of cash flow with assured tariffs. Cash flow, however, is projected to decline over the course of the project agreement life. Therefore, it may result in a decline in yield to InvIT unitholders. The cash flow will improve as and when new projects are acquired by InvIT.

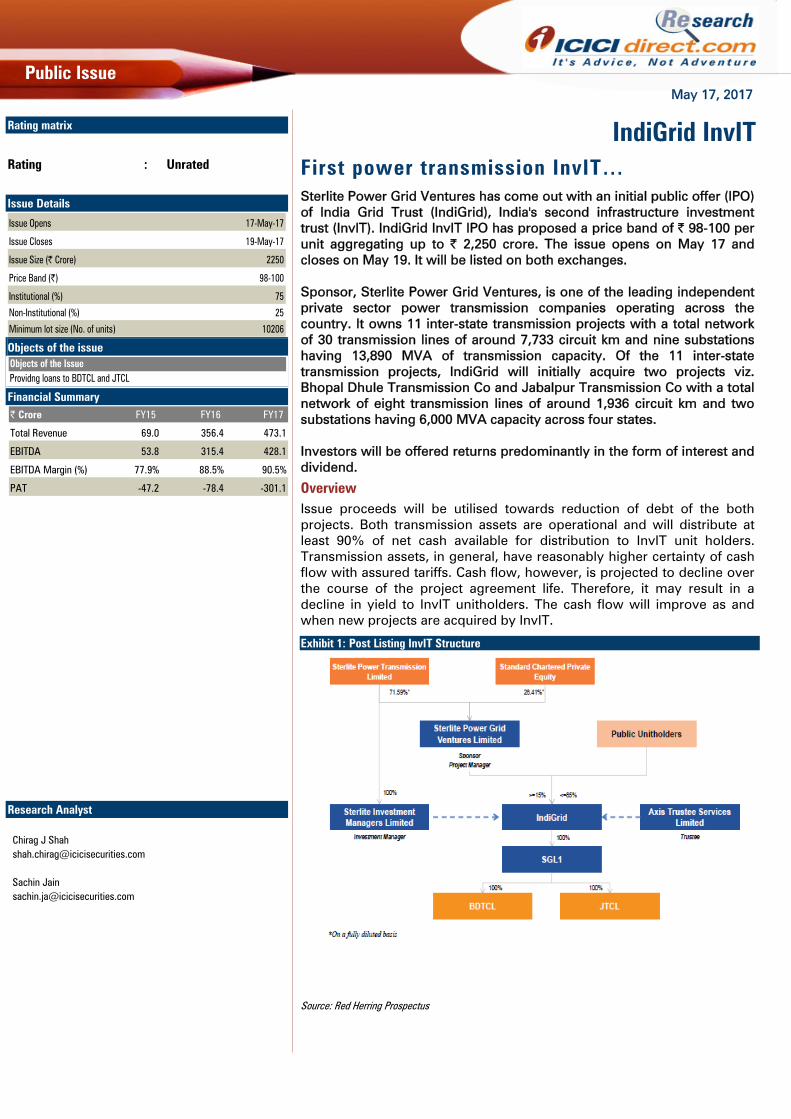

Exhibit 1: Post Listing InvIT Structure

Source: Red Herring Prospectus

IndiGrid InvITRating matrix

Rating : Unrated Issue Details

Issue Opens 17-May-17

Issue Closes 19-May-17

Issue Size (| Crore) 2250

Price Band (|) 98-100

Institutional (%) 75

Non-Institutional (%) 25

Minimum lot size (No. of units) 10206

Objects of the issue Objects of the IssueProvidng loans to BDTCL and JTCL

Financial Summary | Crore FY15 FY16 FY17

Total Revenue 69.0 356.4 473.1

EBITDA 53.8 315.4 428.1

EBITDA Margin (%) 77.9% 88.5% 90.5%

PAT -47.2 -78.4 -301.1

Research Analyst Chirag J Shah [email protected] Sachin Jain [email protected]

ICICI Securities Ltd. | Retail Research

Page 2

Competitive Strengths Stable cash flows from assets with minimal counter party risks

• Revenues are derived out of contracted tariffs under long term contracts (up to 35 years) from assets with relatively low operating and maintenance costs

• Inter-state power transmission projects receive tariffs on the basis of availability, irrespective of the quantum of power transmitted through the line

• Power transmission projects are characterised by low levels of operating risk. The initial portfolio assets are operational power transmission projects with an operating history of at least a year and no construction risks or major capital expenditure requirements.

• Maintenance of annual availability for each of the initial portfolio assets in excess of 98% since commissioning for which maximum incentive revenues under the respective transmission service agreements (TSAs) have been earned. Maintaining availability of initial portfolio assets in excess of 98%, gives the right to claim incentives under TSA, ensuring adequate upside to maximise availability. The amount of incentive revenue earned increases as availability levels increase, with a maximum incentive revenue earned for maintaining 98% availability

• Tariffs under TSAs are billed and collected pursuant to the PoC mechanism. Under the PoC mechanism, payments are made to a central payment pool while proceeds are distributed proportionately to all transmission services providers, like initial portfolio assets. Any shortfall in collection of transmission charges by CTU is shared on a pro rata basis by all transmission service providers. Payment securities in the form of a revolving letter of credit, a surcharge of 1.25% for late payments and lack of alternate power infrastructure deter beneficiaries from defaulting. This mechanism diversifies counter party risk, ensures a stable cash flow independent of asset utilisation and provides payment security

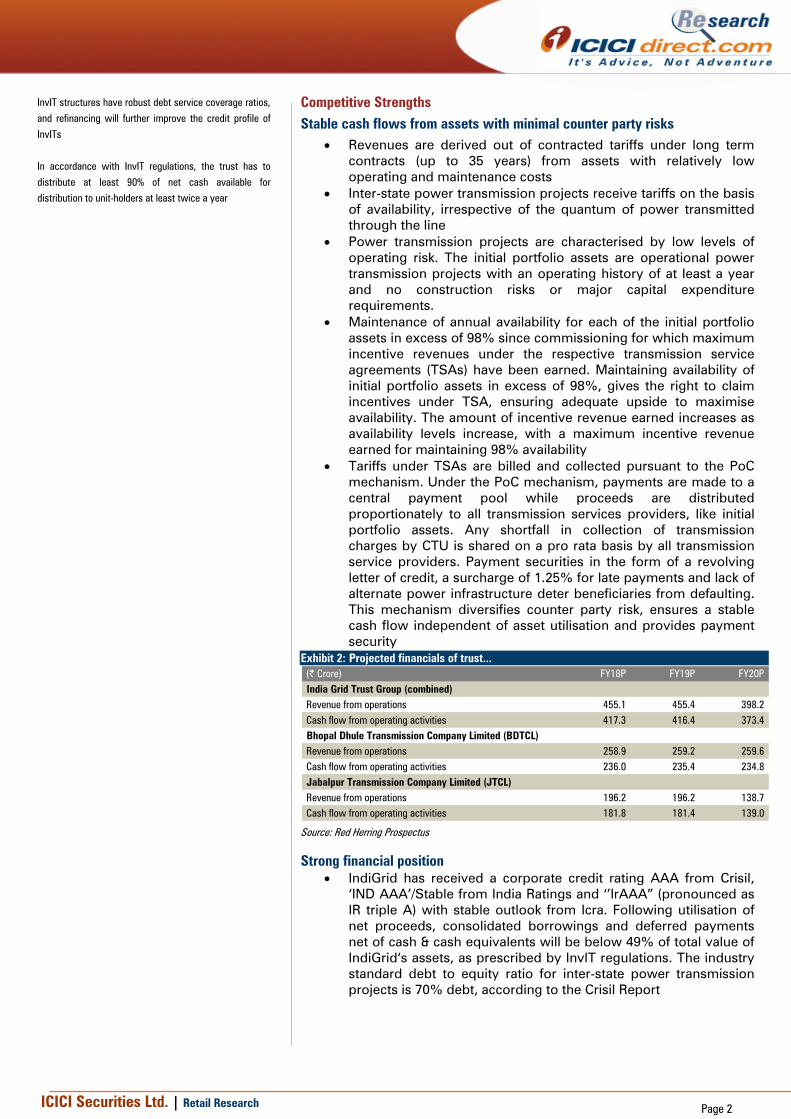

Exhibit 2: Projected financials of trust... (| Crore) FY18P FY19P FY20PIndia Grid Trust Group (combined)Revenue from operations 455.1 455.4 398.2 Cash flow from operating activities 417.3 416.4 373.4 Bhopal Dhule Transmission Company Limited (BDTCL)Revenue from operations 258.9 259.2 259.6 Cash flow from operating activities 236.0 235.4 234.8 Jabalpur Transmission Company Limited (JTCL)Revenue from operations 196.2 196.2 138.7 Cash flow from operating activities 181.8 181.4 139.0

Source: Red Herring Prospectus

Strong financial position • IndiGrid has received a corporate credit rating AAA from Crisil,

‘IND AAA’/Stable from India Ratings and ‘’IrAAA” (pronounced as IR triple A) with stable outlook from Icra. Following utilisation of net proceeds, consolidated borrowings and deferred payments net of cash & cash equivalents will be below 49% of total value of IndiGrid‘s assets, as prescribed by InvIT regulations. The industry standard debt to equity ratio for inter-state power transmission projects is 70% debt, according to the Crisil Report

InvIT structures have robust debt service coverage ratios,

and refinancing will further improve the credit profile of

InvITs

In accordance with InvIT regulations, the trust has to

distribute at least 90% of net cash available for distribution to unit-holders at least twice a year

ICICI Securities Ltd. | Retail Research

Page 3

Ownership and location of assets • Each of the initial portfolio assets is located in strategically

important areas for electricity transmission connectivity, delivering power from generating centres to load centres to meet inter-regional power deficits. Once a transmission project has been commissioned, it requires relatively low levels of expenditure to operate and maintain, which means the relevant initial portfolio assets will have the benefit of owning a critical asset without incurring significant operational costs. In particular, with periodic maintenance, transmission assets will have a useful life of 50 years, according to Lahmeyer

• The transmission lines of initial portfolio assets are predominantly located in areas where developing alternate lines may be challenging due to the terrain, challenges in obtaining rights of way, limited corridors and high construction costs

Strong lineage, support from sponsor • Sponsor is one of the leading power transmission companies in

the private sector, with extensive experience in identifying, successfully bidding, designing, financing, constructing, operating and maintaining power transmission projects across India

• Sponsor owns 11 inter-state power transmission projects, comprising 30 power transmission lines and nine sub-stations, with a total network of approximately 7,733 ckm of power transmission lines with 13,890 MVA of transformation capacity, at different stages of development. Recently, the Sponsor won bids for two transmission projects in Brazil, in auctions conducted by the Brazilian electricity regulatory authority, Agencia Nacional de Energia Electrica. The Sponsor has worked alongside third party contractors, vendors, financial institutions, government agencies and regulators for the proper execution, development and functioning of the initial portfolio assets and the ROFO assets

• Sponsor has been awarded more projects through the TBCB process, for the development of transmission lines by the government, than any other private player in the market. Recently, the Sponsor was awarded the NER System Strengthening Scheme –II (Part-B) & V (NER-ii) inter-state power transmission project, through the TBCB process

• The Sponsor has also been appointed as project manager. Members of the Sponsor‘s board of directors and management team have extensive experience in the power transmission industry and have established track records in negotiating, structuring and financing investments in power transmission assets and managing those assets. For one of the initial portfolio assets, BDTCL, the Ministry of Power awarded SGL1 a Silver Shield for 2013-14 in the category of ‘Early Completion of Transmission Projects‘

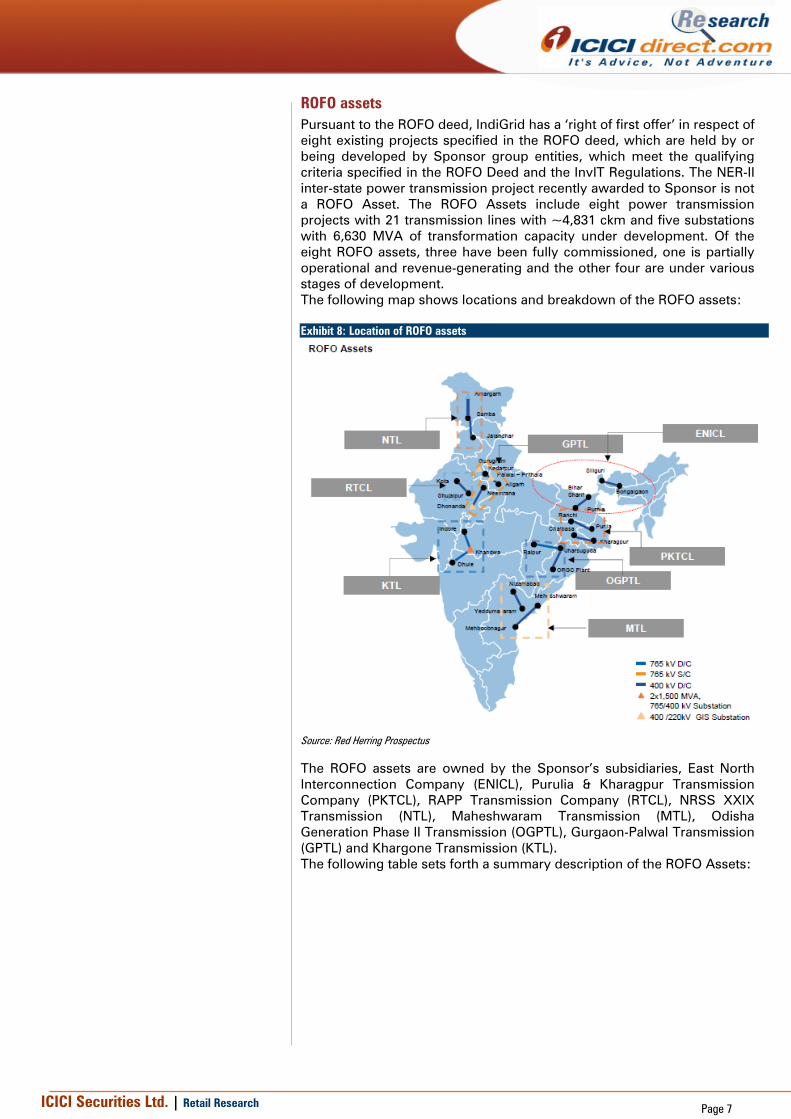

Rights to Sponsor’s pipeline of power transmission projects Pursuant to the ROFO deed with Sponsor, IndiGrid has a right of first offer with respect to eight inter-state power transmission projects, having a transmission network of 21 power transmission lines of ~4,831 ckm and five substations, with a transformation capacity of 6,630 MVA. Of the eight ROFO three have been commissioned, one is partially operational and four remain under various stages of development. Under the ROFO deed or otherwise, any potential acquisitions of power transmission projects will be assessed for their suitability with the investment mandate and is subject to mutual agreement between the Sponsor and the investment manager on behalf of IndiGrid, as well as approval by unitholders.

ICICI Securities Ltd. | Retail Research

Page 4

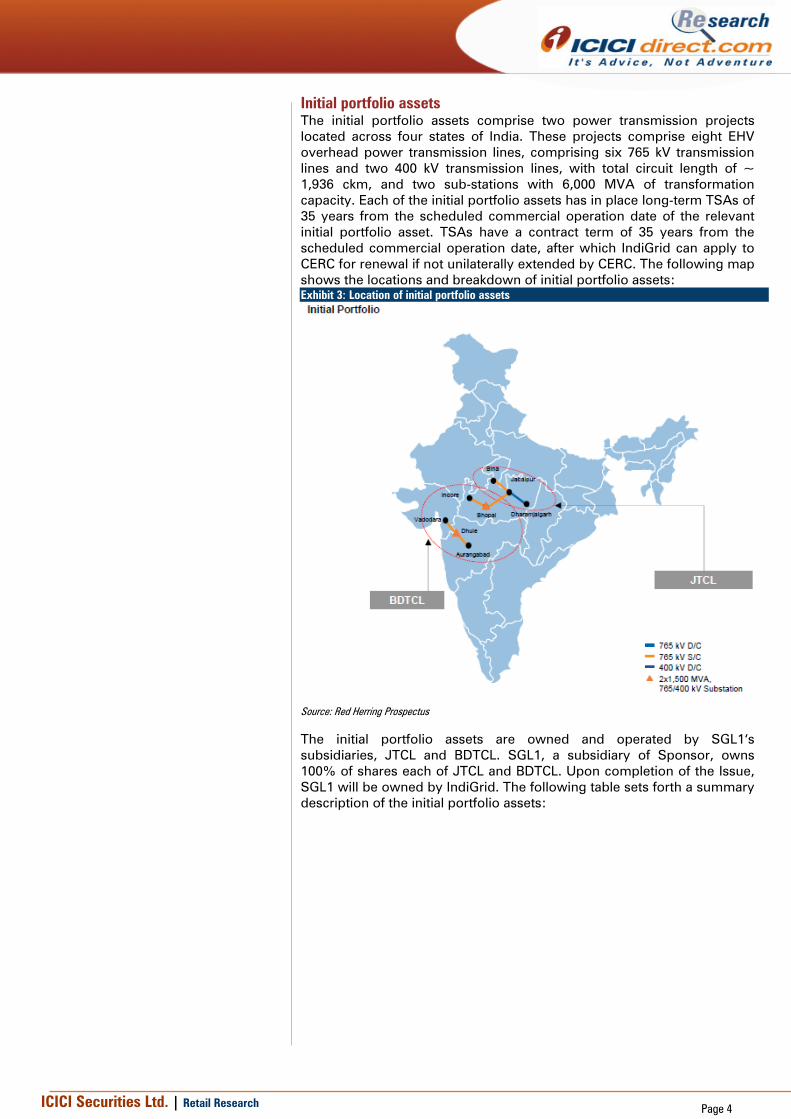

Initial portfolio assets The initial portfolio assets comprise two power transmission projects located across four states of India. These projects comprise eight EHV overhead power transmission lines, comprising six 765 kV transmission lines and two 400 kV transmission lines, with total circuit length of ~ 1,936 ckm, and two sub-stations with 6,000 MVA of transformation capacity. Each of the initial portfolio assets has in place long-term TSAs of 35 years from the scheduled commercial operation date of the relevant initial portfolio asset. TSAs have a contract term of 35 years from the scheduled commercial operation date, after which IndiGrid can apply to CERC for renewal if not unilaterally extended by CERC. The following map shows the locations and breakdown of initial portfolio assets: Exhibit 3: Location of initial portfolio assets

Source: Red Herring Prospectus

The initial portfolio assets are owned and operated by SGL1‘s subsidiaries, JTCL and BDTCL. SGL1, a subsidiary of Sponsor, owns 100% of shares each of JTCL and BDTCL. Upon completion of the Issue, SGL1 will be owned by IndiGrid. The following table sets forth a summary description of the initial portfolio assets:

ICICI Securities Ltd. | Retail Research

Page 5

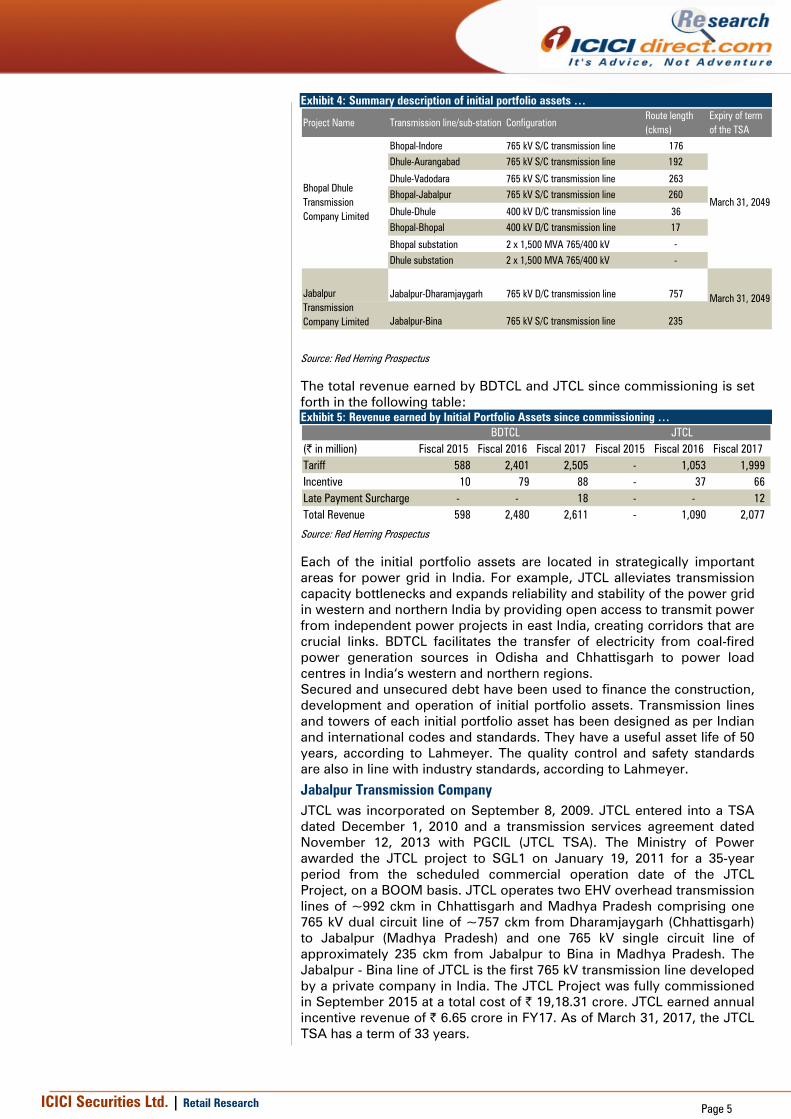

Exhibit 4: Summary description of initial portfolio assets …

Project Name Transmission line/sub-station ConfigurationRoute length (ckms)

Expiry of term of the TSA

Bhopal-Indore 765 kV S/C transmission line 176Dhule-Aurangabad 765 kV S/C transmission line 192

Dhule-Vadodara 765 kV S/C transmission line 263Bhopal-Jabalpur 765 kV S/C transmission line 260

Dhule-Dhule 400 kV D/C transmission line 36Bhopal-Bhopal 400 kV D/C transmission line 17

Bhopal substation 2 x 1,500 MVA 765/400 kV -

Dhule substation 2 x 1,500 MVA 765/400 kV -

Jabalpur-Dharamjaygarh 765 kV D/C transmission line 757

Jabalpur-Bina 765 kV S/C transmission line 235

Bhopal Dhule Transmission Company Limited

Jabalpur Transmission Company Limited

March 31, 2049

March 31, 2049

Source: Red Herring Prospectus

The total revenue earned by BDTCL and JTCL since commissioning is set forth in the following table: Exhibit 5: Revenue earned by Initial Portfolio Assets since commissioning …

(| in million) Fiscal 2015 Fiscal 2016 Fiscal 2017 Fiscal 2015 Fiscal 2016 Fiscal 2017Tariff 588 2,401 2,505 - 1,053 1,999 Incentive 10 79 88 - 37 66 Late Payment Surcharge - - 18 - - 12 Total Revenue 598 2,480 2,611 - 1,090 2,077

BDTCL JTCL

Source: Red Herring Prospectus

Each of the initial portfolio assets are located in strategically important areas for power grid in India. For example, JTCL alleviates transmission capacity bottlenecks and expands reliability and stability of the power grid in western and northern India by providing open access to transmit power from independent power projects in east India, creating corridors that are crucial links. BDTCL facilitates the transfer of electricity from coal-fired power generation sources in Odisha and Chhattisgarh to power load centres in India‘s western and northern regions. Secured and unsecured debt have been used to finance the construction, development and operation of initial portfolio assets. Transmission lines and towers of each initial portfolio asset has been designed as per Indian and international codes and standards. They have a useful asset life of 50 years, according to Lahmeyer. The quality control and safety standards are also in line with industry standards, according to Lahmeyer.

Jabalpur Transmission Company JTCL was incorporated on September 8, 2009. JTCL entered into a TSA dated December 1, 2010 and a transmission services agreement dated November 12, 2013 with PGCIL (JTCL TSA). The Ministry of Power awarded the JTCL project to SGL1 on January 19, 2011 for a 35-year period from the scheduled commercial operation date of the JTCL Project, on a BOOM basis. JTCL operates two EHV overhead transmission lines of ~992 ckm in Chhattisgarh and Madhya Pradesh comprising one 765 kV dual circuit line of ~757 ckm from Dharamjaygarh (Chhattisgarh) to Jabalpur (Madhya Pradesh) and one 765 kV single circuit line of approximately 235 ckm from Jabalpur to Bina in Madhya Pradesh. The Jabalpur - Bina line of JTCL is the first 765 kV transmission line developed by a private company in India. The JTCL Project was fully commissioned in September 2015 at a total cost of | 19,18.31 crore. JTCL earned annual incentive revenue of | 6.65 crore in FY17. As of March 31, 2017, the JTCL TSA has a term of 33 years.

ICICI Securities Ltd. | Retail Research

Page 6

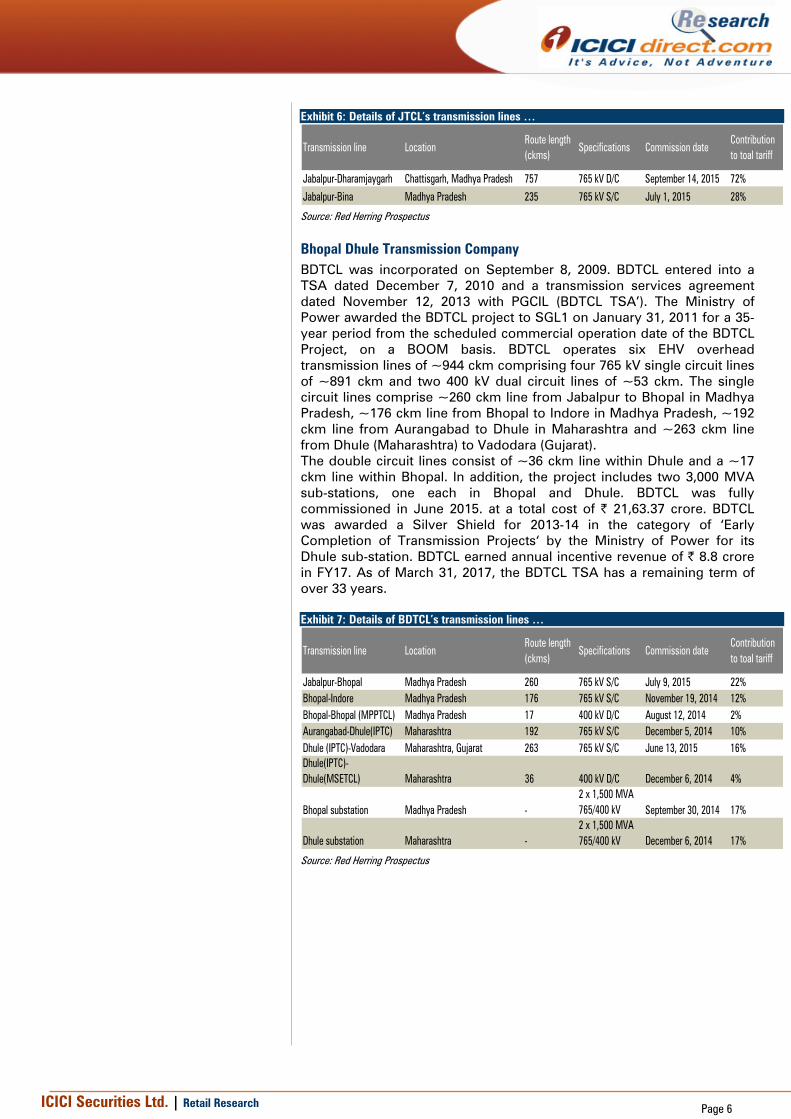

Exhibit 6: Details of JTCL’s transmission lines …

Transmission line LocationRoute length (ckms)

Specifications Commission dateContribution to toal tariff

Jabalpur-Dharamjaygarh Chattisgarh, Madhya Pradesh 757 765 kV D/C September 14, 2015 72%

Jabalpur-Bina Madhya Pradesh 235 765 kV S/C July 1, 2015 28%

Source: Red Herring Prospectus

Bhopal Dhule Transmission Company BDTCL was incorporated on September 8, 2009. BDTCL entered into a TSA dated December 7, 2010 and a transmission services agreement dated November 12, 2013 with PGCIL (BDTCL TSA’). The Ministry of Power awarded the BDTCL project to SGL1 on January 31, 2011 for a 35-year period from the scheduled commercial operation date of the BDTCL Project, on a BOOM basis. BDTCL operates six EHV overhead transmission lines of ~944 ckm comprising four 765 kV single circuit lines of ~891 ckm and two 400 kV dual circuit lines of ~53 ckm. The single circuit lines comprise ~260 ckm line from Jabalpur to Bhopal in Madhya Pradesh, ~176 ckm line from Bhopal to Indore in Madhya Pradesh, ~192 ckm line from Aurangabad to Dhule in Maharashtra and ~263 ckm line from Dhule (Maharashtra) to Vadodara (Gujarat). The double circuit lines consist of ~36 ckm line within Dhule and a ~17 ckm line within Bhopal. In addition, the project includes two 3,000 MVA sub-stations, one each in Bhopal and Dhule. BDTCL was fully commissioned in June 2015. at a total cost of | 21,63.37 crore. BDTCL was awarded a Silver Shield for 2013-14 in the category of ‘Early Completion of Transmission Projects‘ by the Ministry of Power for its Dhule sub-station. BDTCL earned annual incentive revenue of | 8.8 crore in FY17. As of March 31, 2017, the BDTCL TSA has a remaining term of over 33 years. Exhibit 7: Details of BDTCL’s transmission lines …

Transmission line LocationRoute length (ckms)

Specifications Commission dateContribution to toal tariff

Jabalpur-Bhopal Madhya Pradesh 260 765 kV S/C July 9, 2015 22%Bhopal-Indore Madhya Pradesh 176 765 kV S/C November 19, 2014 12%Bhopal-Bhopal (MPPTCL) Madhya Pradesh 17 400 kV D/C August 12, 2014 2%Aurangabad-Dhule(IPTC) Maharashtra 192 765 kV S/C December 5, 2014 10%Dhule (IPTC)-Vadodara Maharashtra, Gujarat 263 765 kV S/C June 13, 2015 16%Dhule(IPTC)-Dhule(MSETCL) Maharashtra 36 400 kV D/C December 6, 2014 4%

Bhopal substation Madhya Pradesh -2 x 1,500 MVA 765/400 kV September 30, 2014 17%

Dhule substation Maharashtra -2 x 1,500 MVA 765/400 kV December 6, 2014 17%

Source: Red Herring Prospectus

ICICI Securities Ltd. | Retail Research

Page 7

ROFO assets Pursuant to the ROFO deed, IndiGrid has a ‘right of first offer’ in respect of eight existing projects specified in the ROFO deed, which are held by or being developed by Sponsor group entities, which meet the qualifying criteria specified in the ROFO Deed and the InvIT Regulations. The NER-II inter-state power transmission project recently awarded to Sponsor is not a ROFO Asset. The ROFO Assets include eight power transmission projects with 21 transmission lines with ~4,831 ckm and five substations with 6,630 MVA of transformation capacity under development. Of the eight ROFO assets, three have been fully commissioned, one is partially operational and revenue-generating and the other four are under various stages of development. The following map shows locations and breakdown of the ROFO assets: Exhibit 8: Location of ROFO assets

Source: Red Herring Prospectus

The ROFO assets are owned by the Sponsor’s subsidiaries, East North Interconnection Company (ENICL), Purulia & Kharagpur Transmission Company (PKTCL), RAPP Transmission Company (RTCL), NRSS XXIX Transmission (NTL), Maheshwaram Transmission (MTL), Odisha Generation Phase II Transmission (OGPTL), Gurgaon-Palwal Transmission (GPTL) and Khargone Transmission (KTL). The following table sets forth a summary description of the ROFO Assets:

ICICI Securities Ltd. | Retail Research

Page 8

Exhibit 9: Summary description of ROFO assets Project Location Status DescriptionENICL Assam, Bihar, West

BengalCommissioned in November 2014 Two 400 kV D/C lines

PKTCL Jharkhand, West Bengal

Kharagpur-Chaibasa line commissioned on June 2016 and Purulia-Raachi Line commissioned on January 07, 2017

Two 400 kV D/C lines

RTCL Rajasthan, Madhya Pradesh

Commissioned in February 2016 One 400 kV D/C line

NTL Punjab, Jammu & Kashmir

One line commissioned in June 2016 and other lines are expected to be in operation by October 2018

Three 400 kV D/C lines and 400/220 kV D/C GIS substations with 630 MVA transmission capacity

MTL Telangana Expected operation by June 2018 Two 400 kV D/C lines and four 400 kV line baysOGPTL Odisha & Chattisgarh Expected operation by August 2019 One 765 kV D/C transmission line and one 400 kV

D/C transmission lineGPTL Rajasthan, Haryana

and Uttar PradeshExpected operation by September 2019

Five 400 kV D/C lines, three 400/220 kV GIS substations with 1000 MVA transmission capacity each and two 400 kV line bays at 400 kV Dhonanda substation

KTL Madhya Pradesh and Maharashtra

Expected operation by July 2019 Two 400 kV D/C transmission lines, two 765 kV D/C transmission line, one 765/400 kV substation with 2 x1,500 MVA transmission capacity at Khandwa and two 765 kV line bays and 7x80 MVAR Switchable line reactors (1 unit as spare) along 800Ω NGR and MVA transmission capacity at its auxilliaries for Khandwa Pool-Dhule 765 kV D/C at 765/400 kV Dhule substation.

Source: Red Herring Prospectus

The construction status of the ROFO Assets under construction is mentioned below: Exhibit 10: Summary description of ROFO assets

Project Foundations Tower Erection StringingRoute length (ckms)

Term of TSA

ENICL 100% 100% 100% 909 25 years

RTCL 100% 100% 100% 403 35 years

PKTCL 100% 100% 100% 546 35 years

NTL In Progress In Progress In Progress 887 35 years

MTL In Progress In Progress In Progress 447 35 years

OGPTL In Progress In Progress In Progress 715 35 years

GPTL In Progress Yet to start Yet to start 271 35 years

KTL In Progress Yet to start Yet to start 624 35 years

Source: Red Herring Prospectus

ICICI Securities Ltd. | Retail Research

Page 9

Risk factors The assumptions in projections of revenue from operations and cash flow from operating activities are inherently uncertain and subject to various significant risks and uncertainties The projections are forward-looking statements, which are subject to a number of assumptions, including assumptions concerning inflation, which affect the escalable component of tariffs. Although prepared after due and careful deliberation, the assumptions underlying the projections are inherently uncertain and are subject to significant business, economic, financial, regulatory and competitive risks, uncertainties and contingencies, many of which are outside of the investment manager‘s control and subject to change. In addition, revenue from operations is dependent on a number of factors, including the performance of transmission systems, which may decrease for a number of reasons. There is no assurance that the assumptions will be realised or that actual distributions will be as projected. If IndiGrid does not achieve the projected operating results, it may be unable to make the expected distributions, in which case the market price of the Units may decline materially or it may be in default under the InvIT Regulations. The investment manager will not, and disclaims any obligation to, furnish updated business plans or projections to Unitholders, or to otherwise make public such information. The Trust may be unable to make distributions to unitholders comparable to Unitholders’ estimated or anticipated distributions or level of distributions may fall Distributions will be based on the net distributable cash flows available for distribution. The amount of cash available for distribution to Unitholders principally depends upon the amount of cash that IndiGrid receives as dividends or the interest and principal payments from portfolio assets, which, in turn, depends on the amount of cash that the relevant portfolio assets generate from operations and may fluctuate. Further, the method of calculation of the net distributable cash flows may change subsequently due to regulatory changes. Any change in applicable laws in India or elsewhere (including, for example, tax laws and foreign exchange controls) may limit ability to pay or maintain distributions to Unitholders. Furthermore, no assurance can be given that IndiGrid will be able to pay or maintain the levels of distributions or that the level of distributions will increase over time, or that future acquisitions will increase distributable cash flow to Unitholders. Any reduction in, or delay/default of, payments of distributions could materially and adversely affect the market price of Units. As a result of all these factors, IndiGrid cannot guarantee that it will have sufficient cash generated from operations to achieve distributable or realized profits or surplus in any future period in order to make distributions every six months or at all.

Net losses have been sustained in past and may be experienced in future Net losses have been sustained in all fiscal years, including on a combined basis in the last three fiscal years reported in the combined financial statements. IndiGrid cannot assure that it can attain net profits in the future or that any such losses will not affect the cash available for distribution to unitholders. Any changes to current tariff policies or modifications of tariffs standards by regulatory authorities could have a material adverse effect on business, prospects, financial condition, results of operations and cash flows The initial portfolio assets have no ability or flexibility to charge more for regulated services than is provided for under the relevant tariff. In accordance with regulations, transmission licensees such as the Initial Portfolio Assets are entitled to recover their approved tariffs from Inter-

ICICI Securities Ltd. | Retail Research

Page 10

State Transmission System (ISTS) charges collected by the Central Transmission Utility (CTU). In the event of any change in the operating statutory parameters of the CTU, or a failure or delay on the part of the CTU, to make the corresponding payments to the Initial Portfolio Assets, their counterparty risk may increase significantly and business, prospects, financial condition, results of operations and cash flows may be materially and adversely affected. Any negative change in the operating statutory parameters of the National Load Despatch Centre (NLDC), the Regional Load Despatch Centres (RLDCs) or the State Load Despatch Centres (SLDCs), as applicable, may negatively impact the corresponding availability of the assets of Initial Portfolio Assets and in turn materially and adversely impact the business, prospects, financial condition, results of operations and cash flows of the Initial Portfolio Assets. Any such unfavourable changes, particularly to tariff, payment pooling and dispatch regulations, could have a material adverse effect on business, prospects, financial condition, results of operations and cash flows. Initial Portfolio Assets, Sponsor and its Associates and Trustee are involved in certain legal proceedings Litigation and other claims and regulatory proceedings against the Initial Portfolio Assets or their management could result in unexpected expenses and liabilities and could also materially and adversely affect business, prospects, financial condition, results of operations and cash flows. Currently, there are outstanding legal proceedings against Initial Portfolio Assets that are incidental to their business and operations, including certain criminal proceedings against certain of their directors and management. These proceedings are pending at different levels of adjudication before various courts, tribunals, enquiry officers and appellate tribunals. Such proceedings could divert management time and attention, and consume financial resources in their defence. Further, an adverse judgment in some of these proceedings could have a material adverse effect on business, prospects, financial condition, results of operations and cash flows. In addition, the Sponsor (also acting as the Project Manager) and its Associates and the Trustee are involved in litigation, claims and other proceedings relating to the conduct of their businesses, including compensation claims, civil matters, criminal matters and tax disputes. Any such litigation and/or regulatory proceedings could harm reputation and materially and adversely affect business, prospects, financial condition, results of operations and cash flows.

ICICI Securities Ltd. | Retail Research

Page 11

Brief Biography of Sponsor’s Directors a) Pravin Agarwal Pravin Agarwal is a Non-Executive Director of the Sponsor. He has been associated with the Sterlite group since its inception and has over 30 years of experience in general management and commercial affairs in infrastructure industry. b) Pratik Agarwal Pratik Agarwal is a Non-Executive Director of the Sponsor. He holds a Masters degree in Business Administration from London Business School and a Bachelor’s degree from Wharton Business School. He has also been the Managing Director and Chief Executive Officer of Sterlite Power Transmission Limited since June 2016. He is also the vice-chairman of Sterlite Power Grid Ventures Limited. Pratik Agarwal has over 10 years of experience in building core infrastructure businesses in ports, power transmission and broadband sector in India. Pratik Agarwal is also the Chairman of the Transmission Task Force constituted by FICCI. c) Anand Agarwal Anand Agarwal is a Non-Executive Director of the Sponsor. He has obtained his bachelor’s degree in metallurgical engineering from the Indian Institute of Technology, Kanpur and his master’s degree in Science and doctorate in Materials Engineering from Rennselaer Polytechnic Institute, United States of America. He has over 20 years of experience in manufacturing, quality assurance and business development. He has been the Chief Executive Officer of STL since 2003. He joined STL in 1995, and has held various positions in STL, including, operations, projects, business development and sales. He also serves as a director on the board of other companies in the Sterlite Group, engaged in infrastructure development and joint ventures operating in Brazil and China. d) AR Narayanaswamy AR Narayanswamy is an independent director of the Sponsor. He is a chartered accountant and management consultant with over 40 years of industry experience in accountancy, financial management and information technology across several industry verticals. He serves as a director on the board of various companies forming a part of the Sterlite group. e) Avaantika Kakkar Avaantika Kakkar is an Independent Director of the Sponsor. She has obtained her bachelor’s degree in law from Indian Law Society’s Law College. She has over 15 years of experience as a lawyer in structured finance, foreign direct investment in real estate, private equity and on market and off market acquisition transactions and joint ventures. At present, she is a partner and co-head of the competition and anti-trust laws practice of Khaitan & Co., Advocates and Solicitors. f) Udai Dhawan Udai Dhawan is a Non-Executive, Nominee Director of Standard Chartered Private Equity on the Board of the Sponsor. He holds a master of business administration from the Wharton School, University of Pennsylvania. He is a qualified chartered accountant and a member of the Institute of Chartered Accountants of India. He has over 20 years of experience in the field of financial services and is currently working with Standard Chartered Private Equity (India) Limited.

ICICI Securities Ltd. | Retail Research

Page 12

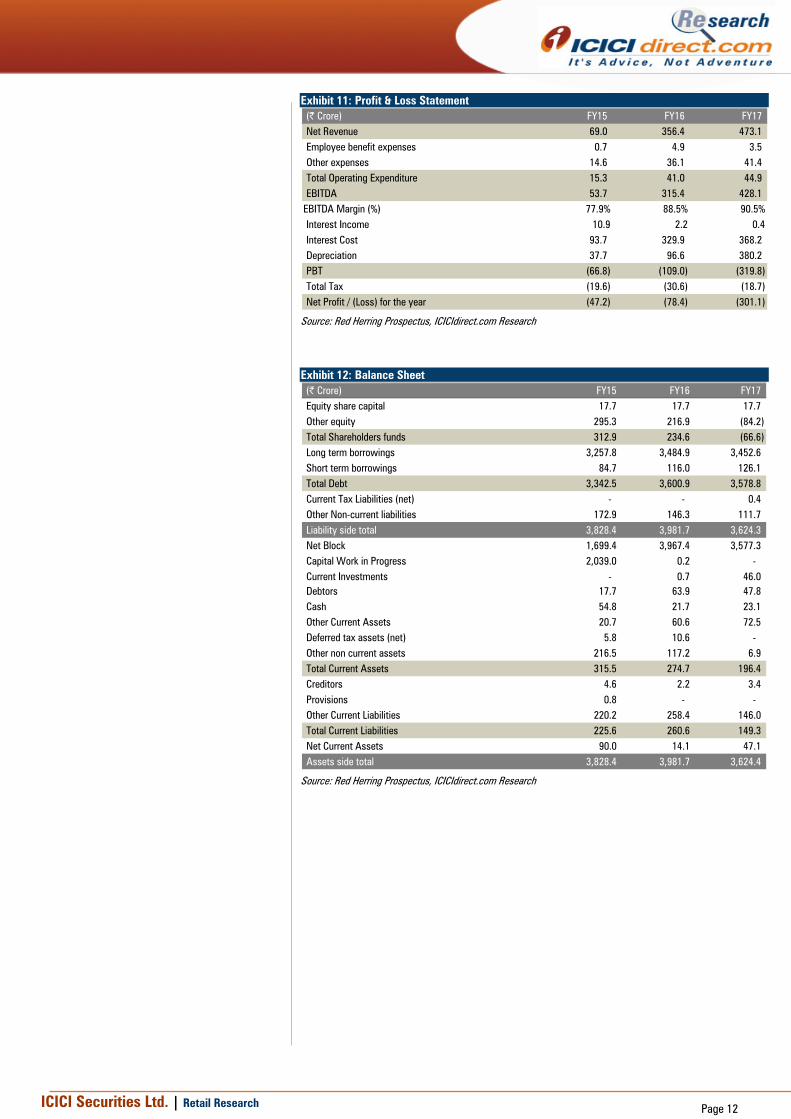

Exhibit 11: Profit & Loss Statement (| Crore) FY15 FY16 FY17Net Revenue 69.0 356.4 473.1 Employee benefit expenses 0.7 4.9 3.5 Other expenses 14.6 36.1 41.4 Total Operating Expenditure 15.3 41.0 44.9 EBITDA 53.7 315.4 428.1

EBITDA Margin (%) 77.9% 88.5% 90.5%Interest Income 10.9 2.2 0.4Interest Cost 93.7 329.9 368.2 Depreciation 37.7 96.6 380.2 PBT (66.8) (109.0) (319.8) Total Tax (19.6) (30.6) (18.7) Net Profit / (Loss) for the year (47.2) (78.4) (301.1)

Source: Red Herring Prospectus, ICICIdirect.com Research

Exhibit 12: Balance Sheet

(| Crore) FY15 FY16 FY17Equity share capital 17.7 17.7 17.7 Other equity 295.3 216.9 (84.2) Total Shareholders funds 312.9 234.6 (66.6) Long term borrowings 3,257.8 3,484.9 3,452.6 Short term borrowings 84.7 116.0 126.1 Total Debt 3,342.5 3,600.9 3,578.8 Current Tax Liabilities (net) - - 0.4 Other Non-current liabilities 172.9 146.3 111.7 Liability side total 3,828.4 3,981.7 3,624.3 Net Block 1,699.4 3,967.4 3,577.3 Capital Work in Progress 2,039.0 0.2 - Current Investments - 0.7 46.0 Debtors 17.7 63.9 47.8 Cash 54.8 21.7 23.1 Other Current Assets 20.7 60.6 72.5 Deferred tax assets (net) 5.8 10.6 - Other non current assets 216.5 117.2 6.9 Total Current Assets 315.5 274.7 196.4 Creditors 4.6 2.2 3.4 Provisions 0.8 - - Other Current Liabilities 220.2 258.4 146.0 Total Current Liabilities 225.6 260.6 149.3 Net Current Assets 90.0 14.1 47.1 Assets side total 3,828.4 3,981.7 3,624.4

Source: Red Herring Prospectus, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Research

Page 13

RATING RATIONALE ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts' valuation for a stock. Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction; Buy: >10%/15% for large caps/midcaps, respectively; Hold: Up to +/-10%; Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk, ICICI Securities Limited, 1st Floor, Akruti Trade Centre, Road No 7, MIDC, Andheri (East) Mumbai – 400 093

ICICI Securities Ltd. | Retail Research

Page 14

ANALYST CERTIFICATION We /I, Chirag Shah, PGDBM and Sachin Jain, CA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures: ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com. ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances. This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months. ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of interest at the time of publication of this report. It is confirmed that Chirag Shah, PGDBM and Sachin Jain, CA, Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report. Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. It is confirmed that Chirag Shah, PGDBM and Sachin Jain, CA, Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report. ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report. We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.