entry and exit echoes - nyu.edu · entry and exit echoes ∗ boyan jovanovic and chung-yi tse †...

TRANSCRIPT

Entry and Exit Echoes∗

Boyan Jovanovic and Chung-Yi Tse†

October 27, 2008

Abstract

While aggregate data do not show the investment echoes predicted byvintage-capital models, echoes arise in rates of entry and exit of firms at theindustry level. Moreover, industries where prices decline rapidly experienceearly ‘shakeouts’. The relation emerges naturally in a vintage-capital modelin which exit of firms sometimes accompanies the replacement of their capital,and in which a shakeout is the first replacement ‘echo’ of the capital createdwhen the industry is born.

1 Introduction

Figure 1 shows that industries where prices decline rapidly experience early ‘shake-outs’ — simultaneous exits of a fraction of incumbent firms. Data also show repeatedechoes in entry and exit in several industries.

We set up a vintage-capital model that explains this relation. We argue thatproducers sometimes exit an industry when their capital comes up for replacement.Replacement is optimal when there is capital-embodied technical progress. Before itsoptimal replacement date, the sunk costs in the capital stock will keep a firm in theindustry. But at the replacement date, the firm may no longer be as efficient as someother potential adopters of frontier technology, and will choose to exit. Viewed inthis way, a shakeout is but an ‘echo’ of the burst of investment that occurs when anindustry comes into being.

If one can associate a shakeout with capital replacement, then the pattern inFigure 1 follows immediately: Where technological progress is more rapid, prices fallfaster and capital is replaced more frequently. The Figure uses data from Gort and

∗We thank A. Gavazza, M. Gort, X. Gabaix, S. Greenstein, C. Helfat, O. Licandro, S. Klepper, S.Kortum and M. Kredler for comments, R. Agarwal for providing data, and the NSF and KauffmanFoundation for support. In earlier versions, the title of this paper was “Creative Destruction at theIndustry Level.”

†NYU and Hong Kong University, respectively.

1

0

10

20

30

40

50

60

70

0 0.1 0.2 0.3 0.4 0.5 0.6

Average annual rate of decline of the product price

Fluorescent lamps

PenicillinElectric Shavers

DDT

StyreneTV

Records

Zippers

Age of the industry at the shakeout date (years)

Figure 1: Technological progress and industry age at shakeout

Klepper (1982, henceforth GK).1 The pattern is that the shakeout occurs earlier inthose industries in which technological progress — as measured by the rate at whichits product price declined prior to the shakeout — is faster.2 As we shall show, thesame pattern arises in subsequent echoes — the faster the technological progress, themore frequent the echoes.

Ours is primarily a model of investment echoes. To make it a theory of exitechoes then requires explaining why capital replacement may sometimes cause exit.Our explanation is that as firms age, they sometimes lose the ability to implementnew technology (which in turn is embodied in new capital). The assertion is roughlythat ‘old dogs can’t learn new tricks’. We do not explain why they cannot, we insteadparameterize this tendency in the form of a hazard rate of losing implementation skillexogenously and randomly.3 A loss of implementation skill does not induce an exit

1GK measure an industry’s age from the date that the product was commercially introduced,i.e., from the date of its first sales. The shakeout period is defined as the epoch during which thenumber of firms is declining. GK say that an ‘exit’ occurs when a firm stops making the productin question, even if that firm continues to make other products. GK time the start of the shakeoutwhen net entry becomes negative for an appreciable length of time. The shakeout era typicallybegins when the number of producers reaches a peak and ends when the number of producers againstabilizes at a lower level.

2Table 7 of GK reports the number of years until shakeout for 39 industries. But only for 8 ofthem does Table 5 report data on the rate of price decline up to the shakeout. These are the eightreported in Figures 1 and 4.

3Deeper reasons for why firms find it hard to adopt new technology are modeled by Klepper andThompson (2006) and Chatterjee and Rossi-Hansberg (2007).

2

right away. Rather, it induces an exit when all the capital that a firm owns reachesreplacement age. Using our model and the GK data we then estimate that this losshazard is between three and seventeen percent per year.

We also provide direct new evidence that firms with old capital are more likelyto exit: In the air-transportation industry, exiting firms have capital that is on av-erage eight years older than the capital of the surviving firms; in Section 6 we shalldisplay this highly significant relation both for the U.S. and for the world as a whole.A related pattern emerges at the two-digit-industry level: Sectors that face morerapidly declining equipment-input prices experience higher rates of entry and exit(Samaniego, 2006). In other words, a sector that enjoys a high rate of embodiedtechnological change will have a high rate of entry and exit, or what one would nor-mally understand to be a higher level of creative destruction.

All technological change in our model is embodied in capital, which means thatTFP should be constant when one adjusts inputs for quality. During the shakeout, afraction of the capital stock is replaced by new capital; the number of efficiency unitsof capital stays the same but the productivity of capital per physical unit rises.

The model is a standard vintage-capital model; Mitchell (2002) and Aizcorbe andKortum (2005) use it to analyze industry equilibrium in steady state, i.e., the station-ary case in which the effect of initial conditions has worn off, and after any possibleinvestment spikes that may be caused by initial conditions have vanished. Jovanovicand Lach (1989) use it to analyze transitional dynamics but they generate neither ashakeout nor repeated investment echoes. We shall derive damped investment echoesthat relate to the constant investment echoes derived by Boucekkine, Germain andLicandro (1997, henceforth BGL) in a similar GE model and by Mitra, Ray and Roy(1991) in a model where there is no progress but in which capital is replaced becauseit wears out. A number of other papers relate Figure 1, among them, Caballero andHammour (1994), Klepper (1996), and Utterback and Suarez (1993). Some relatealso to the repeated echoes that we shall document below. We shall discuss this workin Section 5.

Plan of the paper.–Section 2 presents the model. Section 3 and 4 describe tests ofthe two main propositions. Section 5 discusses other models. Section 6 links capitalreplacement to firm exit empirically. Section 7 presents the model’s implications forTFP growth and Section 8 concludes the paper. The Appendix contains some proofs.

2 Model

Consider a small industry that takes as given the rate of interest, r, and the priceof its capital. The product is homogeneous, and technology improves exogenously atthe rate g. To use a technology of vintage t, however, a firm must buy capital ofthat vintage. The productivity of vintage-0 capital is normalized to 1, and so theproductivity of vintage-t capital is egt.

3

Each firm is of measure zero and takes prices as given. Let p be industry price,q industry output, and D (p, t) the demand curve at date t, assumed continuous inboth arguments. Production of the good becomes feasible at t = 0.

The price of capital is unity for all t. Capital must be maintained at a cost ofc per unit of time; c does not depend on the vintage of the capital, nor on time.Capital cannot be resold to firms outside the industry; it has a salvage value of zero.We assume that willingness to pay at small levels of q is high enough to guaranteethat investment will be positive immediately.4

Implementation costs.–Relative to their contribution to industry output, newfirms implement new technologies more than incumbents do; incumbents seem toface some additional costs of adopting new technology. Let τ denote the age of thefirm and let ε (τ) be that firm’s cost of installing a unit of frontier capital. Since thecost of all capital is unity, the total cost of buying and installing capital of a τ -yearold firm then is 1+ε (τ). We assume that ε (τ) is a Poisson process, independent overfirms. Its initial condition ε (0) = 0 with Poisson parameter λ and jump size κ > 0.This means that among firms aged τ , a fraction e−λτ will be on a par with entrantsin their ability to adopt technology, and a fraction 1− e−λτ will face costs of at least1 + κ.

Industry output.–Capital is the only input. Let Kt (s) be the date-t stock ofactive capital of vintage s or older, not adjusted for quality. Industry output at timet is the sum of the outputs of all the active capital

q (t) =

Z t

0

egsdKt (s) . (1)

Capital ceases to be active when it is scrapped.

Evolution of the capital stock.–Because capital is supplied to the industry ata constant price, the investment rate will exhibit damped echoes. Any mass pointthat occurs will repeat itself, though in a damped form. That is, if a mass-pointof investment ever forms, will recur at a periodicity of T , and the size of the masspoint will diminish over time. Moreover, there must be an initial mass point att = 0 because no capital is in place when the industry comes into being. After thatinitial mass point, capital evolves smoothly until date T when the original capitalis completely replaced by vintage-T capital. This is the second industry investmentspike. The third investment spike then occurs at date 2T , when all the vintage-Tcapital is replaced, and so on. Since the inter-spike waiting times are T , and sincethe first spike occurs at t = 0, the date of the i’th investment spike is (i− 1)T , fori = 1, 2, .... Let i (t) be the integer index of the most recent spike.5 We plot i (t) inFigure 2.

4Sufficient for this is thatR∞0

e−rtD−1 (0, t) dt > 1.5Formally, i (t) = max {i ∈ integers | i ≥ 1 and (i− 1)T ≤ t}.

4

t T

1

2

0

3

2T 3T

i(t)i(t)

Figure 2: The number of spikes, i (t).

We shall show that equilibrium is indeed of the form described in the previousparagraph: All the capital created at one spike date is replaced at the followingspike date, T periods later. Therefore the capital stock at date t comprises capitalcreated at the most recent spike date i (t), plus the flow of investment, x (t) , over thepreceding T periods.Let Xi denote the size of the i’th investment spike. At date t, then, the amount of

capital accounted for by the last spike is Xi(t), and the date-t cumulative distributionof capital by vintage is

Kt (s) = Xi(t) +

Z s

max(0,t−T )x (u) du. (2)

We portray Kt (s) in Figure 3. It has exactly one discontinuity at (i (t)− 1)T .

2.1 Equilibrium

The definition of equilibrium is simple if x (t) > 0 for all t. BGL call this the ‘noholes’ assumption because when it holds, the vintage distribution of capital in usehas no gaps in it. The Appendix provides conditions — in (20) — that guarantee the‘no holes’ outcome.DEFINITION: A constant-T equilibrium consists of a product-price function p (t) ,

a retirement-age of capital, T, investment flows x (t) > 0, and investment spikes Xi

accruing at dates (i− 1)T, (i = 1, 2, ...) that satisfy, for each t ≥ 0, the followingthree conditions:

1. Optimal retirement of capital : The revenue of a vintage-t machine at datet0 ∈ [t, t+ T ] is egtp (t0). Since price declines monotonically, it is optimal toreplace vintage-t capital as soon as its revenue equals its maintenance cost:

egtp (t+ T ) = c. (3)

5

Kt(s)

s

Xi(t)

t(i(t)-1)T t-T

.

Figure 3: The date-t distribution of capital by vintage, s.

2. Optimal investment : Only entrants and incumbents for whom ε (τ) = 0 willinvest, because for them the total cost of a new machine is unity. If investmentx (t) > 0, the present value of a new capital good must equal its cost. Thepresent value of the net revenues derived from that (vintage-t) unit of capitalmust satisfy

1 =

Z t+T

t

e−r(s−t)¡egtp (s)− c

¢ds. (4)

If the RHS of (4) were ever less than unity, x (t) would be zero.6

3. Market clearing:

D (p (t) , t) = eg(i(t)−1)TXi(t) +

Z t

max(0,t−T )egsx (s) ds. (5)

Since the industry does not exist before date zero, x (t) = 0 for t < 0, so thatD (p (0) , 0) = X1.

Proposition 1 If demand satisfies (20)7, a constant-T equilibrium exists, with

p (t) = p0e−gt, (6)

6Proposition 4 of BGL covers that case which arises when there is too high an initial stock ofcapital. This cannot be true at t = 0 in our model, and we shall state conditions in (20) that excludeit as an equilibrium possibility at any date.

7For example, the demand function D (p, t) = pε for ε > 1 satisfies (20). A necessary andsufficient condition for x (t) > 0 for t ≥ 0 is that output increase with t which, in turn, requireseither that the demand shift to the right fast enough or that it be sufficiently elastic.

6

wherep0 = cegT . (7)

and where T uniquely solvesµr + c

c

¶(r + g) = ge−rT + regT . (8)

Proof. (i) First we show that (6), (7), and (8) imply (3) and (4): Eq. (6) and(7) imply (3) for all t ≥ 0, i.e., exit occurs at all t ≥ T . When substituted into (4),(6) and (7) also imply 1 = c

R t+Tt

e−r(s−t)¡eg(t−s)egT − 1

¢ds, which is equivalent to

1 + c1− e−rT

r= cegT

1− e−(r+g)T

r + g. (9)

Multiplying by r (r + g) /c we have r (r + g)+c (r + g)¡1− e−rT

¢= cr

¡egT − e−rT

¢,

and cancelling cre−rT and combining terms we reach (8). Therefore if T solves (8),(4) holds.(ii) Exactly one solution T to (8): The LHS of (8) is constant and exceeds r+ g.

On the other hand, the RHS of (8) is continuous and strictly increases from r + gto infinity, having the derivative rg

¡egT − e−rT

¢> 0 for T > 0. Therefore the two

curves have exactly one strictly positive intersection.(iii) (5) holds: We invoke (20) and invoke the proof in the Appendix.The time path of prices depends on the productivity of the latest vintage of capital.

Because the supply curve for new, more productive capital is infinitely elastic, p (t)depends on the cost side alone.

2.2 The nature and frequency of the spikes

Relation to Figure 1.–The negative pattern arises across steady states indexed byg; a situation in which each industry experiences its specific rate of technologicalprogress g. Implicitly differentiating (8) in the Appendix, we reach the result:

Proposition 2 The replacement cycle is shorter if technological progress is faster:

∂T

∂g= −

r+cc+ (gT − 1) egT

g2 (egT − e−rT )< 0. (10)

Thus, industries with higher productivity growth should have an earlier shakeout andmore frequent subsequent spikes.8

The second relation concerns the rate at which investment echoes or investmentspikes die off:

8We interpret g as an invariant property of an industry. But it can be interpreted as applying onlyto a given epoch in the lifetime of a given industry, and subject to occasional shifts. In Aizcorbe andKortum (2005), e.g., one can think of such shifts as tracing out the relation between technologicalchange and the lifetime of computer chips.

7

Proposition 3 Investment spikes decay geometrically. That is,

Xn = e−gT (n−1)X1 (11)

for n = 1, 2, ....

Proof. Because p (t) is continuous at T , the number of efficiency units replacedat the spikes is a constant, X1, which means that Xn = e−gTXn−1, and (11) follows.

The spike dates remain T periods apart, at 0, T, 2T, 3T, .... The spikes occurregularly because technological progress occurs at the steady rate g. Asymptotically,however, the spikes vanish and the equilibrium becomes like the one that Mitchell(2002) and Aizcorbe and Kortum (2005) analyze.

Firm exit at the investment spike.–At a replacement spike at date t, say, allfirms that need to replace their capital bought that capital at date t− T . All firms,whatever their age was at date t−T had ε = 0 at that time Among those, a fraction1 − e−λT will have experienced a jump in ε and will not find it profitable to invest.These firms will then exit.

The remaining parameters of the model are the maintenance cost c and the rateof interest r. The following claim is proved in the Appendix:

Proposition 4

(i)∂T

∂c< 0. And, if gc < r2, (ii)

∂T

∂r> 0, (iii)

∂ (gT )

∂g> 0

A rise in the maintenance cost, c, reduces the lifetime of capital as one would expect.Since replacing capital constitutes an investment, when the rate of interest rises thatform of investment is discouraged, and it will occur less frequently.

3 T vs. g: Testing Proposition 2

We shall begin by proxying the age, T , of an industry at its first replacement spike,by the industry’s age at which the shakeout of its firms begins. This measure willunderlie the first test of the model. And as suggested by (6), we shall proxy the rateof technological progress, g, by the rate at which the price of the product declines.Since replacement episodes are in the model caused by technological progress, wefirst check if industries with higher productivity growth experience earlier shakeouts.That is, we ask whether industries with a high g have a low T as Proposition 2 claimsand, if so, how well the solution for T to (8) fits the cross-industry data on g and T .

8

Product name g(1) T (1) g(2) T (2)

Auto tires 0.03 21Ball-point pens 0.07 >28 0.07 >18CRT 0.04 24Computers 0.07 19DDT 0.20 12 0.13 16Electric shavers 0.05 8 0.01 5.5Fluorescent lamps 0.21 2 0.21 2.5Nylon 0.03 >34 0.03 >21Home & farm freezers 0.02 18Penicillin 0.57 7 0.57 8.5Phonograph records 0.03 36 0.02 8.5Streptomycin 0.31 22Styrene 0.06 31 0.07 12Television 0.05 33 0.08 8Transistors 0.17 15Zippers 0.04 63 0.05 38

Table 1 : The data in Figures 4 and 5.9

We now describe the procedure by which we choose the model’s parameters. ByProposition 1, a unique solution to (8) for T exists; denote it by T (r, c, g). In Table 1,T (1) is the date that GK find that Stage 4 (the shakeout stage) begins in their variousindustries. In a couple of cases the shakeout had not yet begun, and they are censored.The annual rate at which the price declines, averaged over the period

h0, T (1)

iis g(1)i .

We do not have observations on r and c; we find r = .07 a reasonable guess, butwish to check robustness with respect to this assumption and therefore choose threealternative values for r, namely .02, .07 and .12 and in each case estimate c. Theestimation routine minimizes the sum of squared deviations of the model from thedata for the eight industries for which we have complete information on both g andT :

minc

(8X

i=1

hT(1)i − T

³r, c, g

(1)i

´i2).

The data and the three implicit functions T (g, r, c) fitted to them are shown in Figure4. The estimates of c and their standard errors are reported in the figure. The R2

9The variable definitions are: T (1) = age at the start of shakeout, g(1) = average annual price

decline onh0, T (1)

i, T (2) = the number of years elapsed between the start of stage 2 and the midpoint

of the shakeout stage, and g(2) = annual price decline over stages 2 and 3.

9

0

10

20

30

40

50

60

70

0 0.1 0.2 0.3 0.4 0.5 0.6

Annual price decline, g

T

FLL

PENESH

DDT

STE

TVPHR

ZP r = .02 c = .026 (.011)

r = .07 c = .039 (.013)

r = .12 c = .053 (.021)

T (r , c , g )~

Figure 4: The relation between T and g for the eight uncensored GKobservations; censored observations not used here.

was roughly .53 in each case. Since r makes little difference to the predicted relationwe shall proceed with the value r = .07 for the remainder of the analysis.

Our estimate of c is in the range of typical maintenance spending. McGrattanand Schmitz (1999) report that in Canada, total maintenance and repair expenditureshave averaged 5.7 percent of GDP over the period from 1981 to 1993, and 6.1 percentif one goes back to 1961. These estimates are relative to output, however, whereasours are relative to the purchase price of the machine which is normalized to unity.Relative to output, maintenance costs are one hundred percent at the point whenthe machine is retired (this is equation [3]). Maintenance costs are constant overthe machine’s lifetime, whereas the value of the machine’s output relative to thenumeraire good is egT when the machine is new. Now egT averages around e1.7 = 5.5— see Figures 14 and 15 — so that as a percentage of output, maintenance spendingranges between 18 and 100 percent. Therefore, c must stand partly for wages toworkers as a fixed-proportion input as in the original vintage-capital models likeArrow (1962) and Johansen (1959) that had a fixed labor requirement.

3.0.1 Testing Proposition 2 using an alternative definition of T

We now entertain a different definition of T ; one that may provide a better test ofthe model, and one that will provide us with more observations. The main reason fordoing this is that GK’s ‘Stage 1,’ defined as the period during which the number ofproducers is still small (usually two or three), may not contain what we would callan investment spike. During stage 1, only a few firms enter, a number that is in someindustries — autos and tires, e.g., — much smaller than the number of firms that exit

10

during the shakeout.

The model predicts a date-zero investment spike X1 = D (p0, 0), without whichthere would be no exit spike at date T . Not all the GK industries will fit this,however. Indeed, GK state that rarely is a product’s initial commercial introductionimmediately followed by rapid entry. Autos, e.g., had very low sales early on, and ittook years for sales to develop.10 Therefore the spike is better defined at or aroundthe time when the entry of firms was at its highest. Moreover, in GK, for manyindustries, the shakeouts were not completed until a few years after they first began.It may thus be more appropriate to designate the shakeout date as the midpoint ofthe shakeout episode instead of as the start date of the shakeout episode.

In light of this, let T (2) be the time elapsed between the industry’s ‘Takeoff’ date(which is when Stage 2 begins) and the midpoint of the the industry’s shakeoutepisode (the midpoint of Stage 4). This revised definition for bT calls for adjustingbg to be the rate of the average annual price decline between the takeoff date (whichcomes after the industry has completed stage 1), and the first shakeout date. We callthis variable g(2). This allows us to enlarge the sample. The additions are as follows:

1. For six of the GK industries, complete information for price-declines in Stages2 and 3 (but not Stage 1) is available. They can now be added to the analysis;

2. The two censored observations listed in Table 2 will also be added;

3. We replace the GK information for the TV by that reported in Wang (2006),who compiled the data from the Television Factbook. This change may betterreflect the history of the TV industry as GK dated the birth of the industryas early as 1929, while according to Wang, the commercial introduction of TVstarts only in 1947.

The estimation procedure.–The inclusion of the two censored observations leadsus to use maximum likelihood. We set r = 0.07 and assume that the distributionof c over industries is log-normal: For all firms in industry i, ln ci is a draw fromN (ln c, σ2). We then estimate c and σ to fit the model to the data; the details are inthe Appendix.

The estimate of c = 0.078 is a bit higher than with the previous sample. Thisis because T is smaller under the new definition, and a higher replacement cost isneeded to generate the earlier replacement. Figure 5 plots the predicted T for theindustry for which c = c. For the two truncated observations, Ball—point pens andNylon, the data points represent the respective means conditional on their truncatedvalues.10Klepper and Simons (2005), however, do find an initial spike for TVs and Penicillin — both start

out strong after WW2. There may be a problem with the TV birthday being set at 1929 as GKhave it. During WW2 the Government had banned the sale of TVs.

11

0

10

20

30

40

50

60

0 0.1 0.2 0.3 0.4 0.5 0.6

g

ESH

PHR

ZP

STE

TV

DDT

FLL

PEN

Transistors

Cathode Ray

Computer

Ball Point

Auto Tire

Freezer

Streptomycin

Nylon

σ = 2.27 (0.85)c = 0.078_

Figure 5: T and g using the alternative definition of T

4 Echoes: Testing Proposition 3

Let us first elaborate on the content of Proposition 3

1. Shakeouts should diminish geometrically in absolute terms. Relative to the sizeof the industry, however, the decline will be faster than (11) indicates becauseindustry output increases from its date-zero level — both because price declinesand because the demand curve tends to shift to the right over time.

2. Moreover, exit spikes should coincide with entry spikes.

3. The inter-spike waiting times should depend negatively on g as Proposition 2claims.

This section tests these implications using Agarwal’s extension and update of theGK data, described fully in Agarwal (1998).11 The products are listed and somestatistics on them presented in Table 3 in the Appendix.

A procedure for detecting spikes must recognize the following features of the data:

(A) Length of histories differ by product.–Coverage differs widely over products,from 18 years (Video Cassette Recorders) to 84 years (Phonograph Records).

11The evidence hitherto is mixed: Cooper and Haltiwanger (1996) find industry-wide retoolingspikes, but GK did not report second shakeouts, though this may in part be because the GK datararely cover industry age to the point t = 2T where we ought to observe a second shakeout. In anycase, Agarwal’s data cover more years and contain entry and exit separately, and we shall use themto study this question.

12

(B) The volatility of entry and exit declines as products age.–The model predictsthat the volatility of entry and exit should decline with industry age. Other factorsalso imply such a decline: (i) Convex investment costs at the industry level, as inCaballero and Hammour (1994), and (ii) Firm-specific c’s. Both (i) and (ii) wouldtransform our Xn from spikes into waves and, eventually, ripples.12

Hodrick-Prescott residuals in entry and exit rates.–Our spike-detection procedureis in the spirit of the investment-spike literature that defines a spike as an unusuallyhigh investment rate.13 Roughly speaking, we shall say that a spike in a series Ytoccurs whenever its HP residual is more than two standard deviations above its mean.‘Roughly’, because of adjustments for (A) and (B) above. We constrain industry i’strend, τ , by

AiXt=2

(τ t − τ t−1) ≤ aAbi ,

where Ai is the age at which an industry’s coverage ends. We set a = 0.005 for bothseries. Because both series are heteroskedastic, with higher variances in earlier years,we chose b = 0.7 for both entry and exit (If b were unity, an industry with longercoverage would have a larger fraction of its observations explained by the trend). Thetrend therefore explains about the same fraction of the variation in short-coverageindustries as in long-coverage industries.

This fixes problem (A), but not (B): The HP residual, ut ≡ Yt − τ t, is stillheteroskedastic, the variance being higher at lower ages. To fix this, we assume thatthe standard-deviation depends on product age as follows:

σt = σ0t−γ, (12)

where σ0 ≥ 0 and γ ≥ 0 are product-specific parameters estimated by maximizingthe normal likelihood14

AiYt=1

1p2πσ2t

exp

Ã−12

∙utσt

¸2!.

12Spikes may also dissipate because (i) A positive shock to demand would start a new spikeand series of echoes following it; these would mix with the echoes stemming from the initialinvestment spike, (ii) Random machine breakdowns at the rate δ would transform (11) intoXn = e−(g+δ)T (n−1)X1, which decays faster with n.13Gourio and Kashyap (2007) record a spike whenever investment exceeds twenty percent of the

beginning-of-period capital stock, which is roughly 2.5 times the level of replacement investment.This leads to 15-20 percent of the years being spike years. Our procedure produces a weightedaverage of 4.3 percent of the years as exit-spike years and 5.6 percent as entry-spike years.14Although the HP residuals are not independent and unlikely to be normal, this procedure still

appears to have removed the heteroskedasticity in the sense that the spikes were as likely to occurlate in an industry’s life as they were to occur early on.

13

The spike-detection algorithm.–If at some date the HP residual is more than twostandard deviations above its mean of zero, then that date is a spike date. But weshall allow for the possibility that unusually high replacement will take up to threeperiods. Thus we shall say that a series Yt in a certain time window is above ‘normal’if one or more of the following events occurs

1-period spike: ut > 2σt,

2-period spike: ut > σt and ut+1 > σt+1,

3-period spike: ut >2

3σt and ut+1 >

2

3σt+1 and ut−1 >

2

3σt−1.

The cutoff levels of 2, 1, and 23times σt were chosen in the expectation that each

of the three events would carry the same (small) probability of being true under thenull. The latter depends on the distribution and the serial correlation of the ut whichwe do not know. But, again for the normal case, these probabilities turned out to beroughly the same. That is,

1− Φ (2) = 0.023, (1− Φ (1))2 = 0.025, andµ1− Φ

µ2

3

¶¶3= 0.016.

Table 3 summarizes the results in more detail. The 33 products are listed al-phabetically and are so numbered. To explain the table, let us focus on product 23,Phonograph Records and read across the row. Records were first commercialized,i.e., sold, in 1908. Being the oldest product, it also is the product for which we havethe most observations, 84, since (with one exception) the series all end in 1991. Thenext four entries are the exit and entry spikes, by age of industry and by calendaryear. There are seven one-year spikes and one two-year spike, this being the lastexit spike. The 1934 exit spike is labelled in red because it falls in the GK shakeoutregion the dates of which are in the last column of the table. See Figure 6 wherethe GK shakeout region is shaded. The remaining columns report the correlationsbetween the entry and exit series.15 The raw series are negatively correlated — whenthe industry is young, entry is higher than exit, and later the reverse is true — but thecorrelation is slight (-0.07). The trends (i.e., the τ ’s) are more negatively correlated(-0.27). The HP residuals, on the other hand, are positively correlated; our modelsuggests that this should be so because the spikes should coincide. The correlationsaveraged across products are at the bottom of the table.

Figure 6 plots the exit and entry series for Phonograph records, in each caseplotting the HP trend and the two-standard-deviation band. Spikes are circled ingreen. Let us note the following points:

15Since neither the entry nor the exit rate is defined in the first year of the raw series, both seriesbegin in the second year.

14

Phonograph Record Entry Rates

0

0.5

1

1.5

2

2.5

3

1909 1914 1919 1924 1929 1934 1939 1944 1949 1954 1959 1964 1969 1974 1979 1984 1989

GK Stage 4

NBER recession years

=

Phonograph Record Exit Rates

0

0.1

0.2

0.3

0.4

0.5

0.6

1909 1914 1919 1924 1929 1934 1939 1944 1949 1954 1959 1964 1969 1974 1979 1984 1989

GK Stage 4

Figure 6: Spikes in the Phonograph-Record Industry

15

0

5

10

15

20

25

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16

g

T(2)

-T(1

)

Jet Engines

Phonograph records

Heat Pumps

Radiant Heating Antibiotics

Outboard Motors

Recording Tapes

42

c = 1.12 (0.05)

Figure 7: Exits: The relation between T2 − T1 and g

1. For both entry and exit the spikes are evenly distributed as a function of indus-try age, predominating neither early nor late in the life of the industry. Table 3shows this is true in most industries. This suggests that the heteroskedasticityadjustment in (12) is adequate.

2. The number of entry and exit spikes is equal — four entry and four exit spikes.But only the final, fourth spikes coincide in that they are within one year ofeach other. There were ten other products for which this was so. In seven outof the ten, there is at least one instance where an entry an exit spikes occur inthe same year.

3. The second exit spike is well in the GK region, but there should also have beenan entry spike in that region. Over all the industries the number of entry spikes(67 in all) is slightly less than the number of entry spikes (79 in all), for the nineindustries in which the GK region does contain an Agarwal spike, it is alwaysan exit spike — see the red numbers in Table 3.

4. Just as our model predicts, however, T2,i−T1,i is negatively related to gi. Thatis, analogously to the result in Figures 4, the first exit spike is followed soonerby the second exit spike in those industries i where prices decline faster. Wenow calculate bg as the rate of average price decline during the years coveredby T2 − T1. To maximize the number of observations, we include products forwhich price information is available for as little as 70% of the time during theyears covered by T2 − T1. For Outboard Motors and Recording Tapes, however,price went up during those years which is inconsistent with the model. Butthey both had above-average T2 − T1 values, 42 and 17 respectively, and while

16

0

5

10

15

20

25

30

35

40

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.2

g

T(2)

-T(1

)

Jet Engines

Electric Shavers

Ball-point Pens Styren

Antibiotics

Phonograph RecordsVideo Cassette

Recorders

c = 2.91 (0.02)

Figure 8: Entry: The relation between T2 − T1 and g

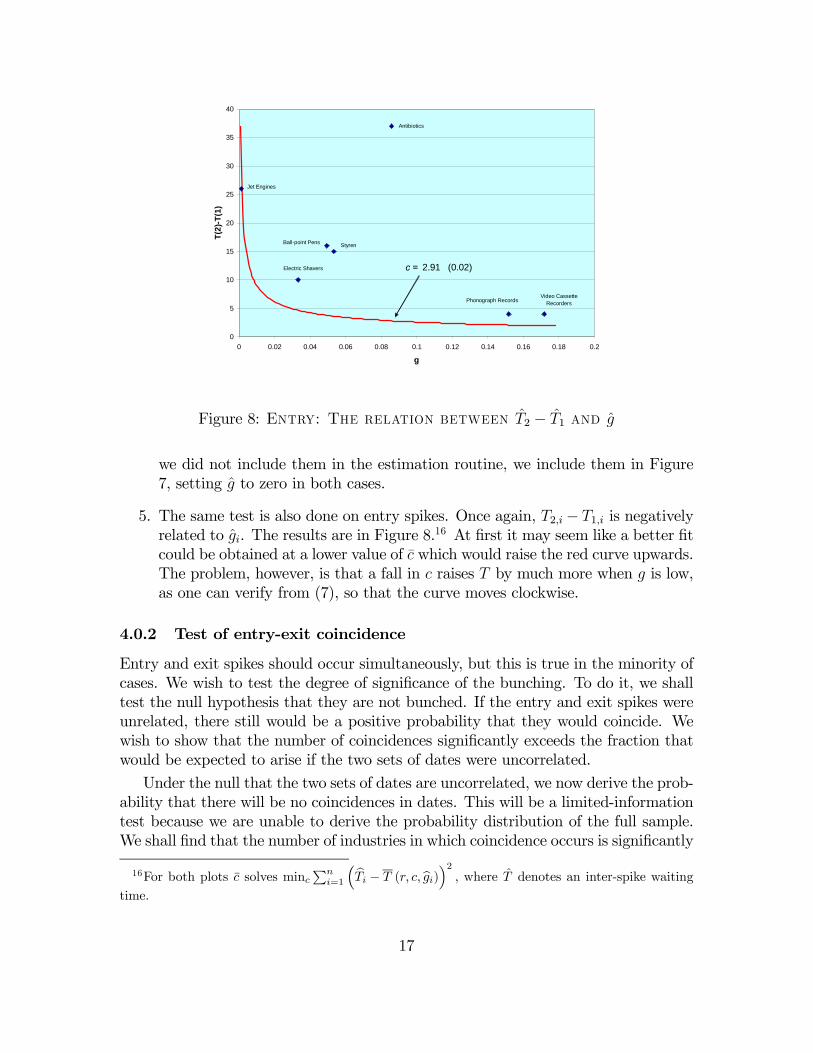

we did not include them in the estimation routine, we include them in Figure7, setting g to zero in both cases.

5. The same test is also done on entry spikes. Once again, T2,i− T1,i is negativelyrelated to gi. The results are in Figure 8.16 At first it may seem like a better fitcould be obtained at a lower value of c which would raise the red curve upwards.The problem, however, is that a fall in c raises T by much more when g is low,as one can verify from (7), so that the curve moves clockwise.

4.0.2 Test of entry-exit coincidence

Entry and exit spikes should occur simultaneously, but this is true in the minority ofcases. We wish to test the degree of significance of the bunching. To do it, we shalltest the null hypothesis that they are not bunched. If the entry and exit spikes wereunrelated, there still would be a positive probability that they would coincide. Wewish to show that the number of coincidences significantly exceeds the fraction thatwould be expected to arise if the two sets of dates were uncorrelated.

Under the null that the two sets of dates are uncorrelated, we now derive the prob-ability that there will be no coincidences in dates. This will be a limited-informationtest because we are unable to derive the probability distribution of the full sample.We shall find that the number of industries in which coincidence occurs is significantly

16For both plots c solves mincPn

i=1

³bTi − T (r, c, bgi)´2 , where T denotes an inter-spike waitingtime.

17

larger than implied by this null. Suppose an industry has τ periods of coverage andthat during these τ periods there were NE entry spikes and NX exit spikes. Supposeentry spikes happened at dates t1, t2, ..., tientry (τ). Suppose that the dates of the entryspikes were not correlated with the dates of the exit spikes. Suppose, moreover, thatan exit spike was equally likely to fall at any date. No match will arise if and onlyif none of the NX exit spikes matches any of the NE entry spikes. In other words,under the null hypothesis, H0, the spikes are exchangeable random variables whichare correlated only in so far as they cannot fall at the same date as another spike.Exit-spike i is equally likely to fall in each ‘free’ year that the GK data cover. Wecondition on the entry-spike dates. Only their number matters, not their actual dates:Any set of dates would produce the same likelihood (13).To derive the probabilities, begin by placing the exit spikes in random order

i = 1, ..., NX . Then under H0: “entry and exit dates are uncorrelated”, the probabilitythat the first exit spike falls in one of the τ −NE bins not occupied by an entry spikeis τ−NE

τ. Since no two exit spikes can occupy the same bin, conditional on this event,

the probability second randomly chosen spike date will produce no match is τ−NE−1τ−1 .

Proceeding in this way sequentially until the NX ’th exit spike, the probability underH0 that there is no match is

1− ρ ≡NXYi=1

µτ −NE − (i− 1)

τ − (i− 1)

¶. (13)

Denote the solution for ρ by ρ = ψ (τ ,NX , NE). The formula conditions on τ ,NX and NE all three of which generally differ over industries. For industry j write

ρj = ψ¡τ j, N j

X , NjE

¢. (14)

Then ρj is the probability that industry j has at least one match. Now define thedichotomous random variable mj as follows: Let

mj =

½1 if industry j has at least one exit-entry match0 otherwise

so that mj = 1 with probability ρj and mj = 0 with probability 1− ρj. That is, mj

is binomially distributed.The Likelihood function. — Let ρj be the parameter for industry j, defined in (14).

Among the 31 industries for which ρj can be defined, let J be the set of industriesfor which mj = 1. The likelihood of the sample is

L (m1, ...,m31) =Yj∈J

ρjYj /∈J

¡1− ρj

¢= 4.6852846× 10−9. (15)

The p-value.–The p-value is the probability of obtaining a result at least asextreme as the one that was actually observed (in our case 7 industries for which

18

0

0.05

0.1

0.15

0.2

0.25

0 1 2 3 4 5 6 7 8 9 10 11

# industries with at least one coincidence

Freq

uenc

y un

der H

0

# observed

Figure 9: Frequency distribution of M under H0

m = 1), given H0. Let the collection of industries be I; that is, I = {1, 2, ..., 31} is aset consisting of 31 elements. Let M =

Pj∈I mj. In our context,

p7 = PrnM ≥ 7 |

¡τ j, N j

X , NjE

¢31j=1

and H0

o.

Of course, H0 determines the ρj via (13). Let JM be the collection of M-elementsubsets of I. That is, JM = {J ⊂ I | #J =M}. Then,

pn =XM≥n

XJ∈JM

Yj∈J

ρjYj /∈J

¡1− ρj

¢This is the likelihood of all possible values ofM that equal n or more. The probabilitydistribution ofM under H0 is pn+1−pn and it is shown in Figure 9. Since p7 = 0.0217,we reject H0 at the 5% but not at the 1% level.

5 Other explanations

Our model and Propositions 1 and 2 are supply-side arguments. In relating to pastwork it is convenient to divide it into demand side and supply side types of explana-tions.

5.1 Demand-side explanations

These we divide into aggregate and industry-level.

19

5.1.1 Aggregate demand

Gourio and Kashyap (2007) find investment spikes to be procyclical (Gourio andKashyap), and other work finds exits to be countercyclical. The concern this raisesis that what we have termed as ‘echoes’ are instead reflections of the business cycle.Be they aggregate or industry demand shocks, however, it would seem that they

should produce an asychronicity between entry and exit: Entry should occur whendemand is high and exits should happen when demand is low. Our clustering testshows, however, that entry and exit spikes tend go together. Now we ask if entryspikes are less likely and exit spikes more likely to occur during NBER recessionyears.17

This logic would seem to have been at work in the Phonograph industry in that, asFigure 6 shows, that in the two of the four exit spikes — the 1913 and the 1974 spikes —occurred during recession years and none of the entry spike dates did. However, thisasymmetry does not show up in other industries. When we consider all the industriesthere is no correlation between recession years and spike dates. Our tests are simplecomparisons of means. Let τ j be the number of years of coverage of industry j, andτRj the number of recession years contained in τ j. Similarly, let φj be the number ofspikes in industry j and φRj the number of those spikes that fall in a recession year.

18

Then we ask if either of the following inequalities is significant:Pj φ

RjP

j φj≷P

j τRjP

j τ j.

The demand hypothesis implies that for exits the LHS should exceed the RHS andthat for entry the LHS should be less than the RHS. It turns out that the LHS issmaller for both exit and entry, but neither difference is significant. We interpretthis as a test of differences in the means based on

Pj τ j independent samplings. See

Appendix Table 4.

17The NBER dates are in quarters but our spike dates are in years. A given year was deemed arecession year if any of the following criteria was met: (1) if a NBER recession was underway forthe whole year, (2) if a NBER recession started in the first 2 quarters of the year, (3) if a NBERrecession ended in the last 2 quarters of the year. There are two exceptions, Both the 1918 and 1990recessions started in the 3rd quater and ended in the 1st quater of the following year.18Take for example product 23, Phonograph Records. Here τ = 83. The coverage 1909 to 1991

during which 19 years were recession years. ThusτRjτj= 19

83 . For exit spikes, the second and the fourth

spikes, in 1933 and 1973-74, respectively, are in recession years. Then φRj = 2 and

φRjφj

=2

19.

Because of time aggregation, demand fluctuations can induce a spike in that x(t) reacts positivelyto changes in demand.

20

5.1.2 Industry demand

Caballero and Hammour (1994) find that if replacement of capital causes interruptionsin production, it is optimal to replace capital when demand temporarily drops, forthen the foregone sales are at their lowest. Klenow (1998) finds that when, in addition,the productivity of new capital rises with cumulative output, a firmwill replace capitalwhen the recovery is about to start. This raises the productivity growth of the newcapital.

If an exit spike is caused by a fall in industry demand, we should observe a fallin output around the time of the spike. Moreover, a demand decline produces ashakeout and a decline in p. If demand does not decline then there is no shakeoutand no decline in p. We divide the GK industries into those in which output fell duringthe shakeout period, and into those in which output rose. For the analysis in Figure4, among the industries where output fell during the shakeout,19 the average pair was³bg, bT´ = (0.07, 30.4), whereas among the industries where output rose,20 the averagepair

³bg, bT´ = (0.28, 13.3) . For the analysis in Figure 5, the corresponding figures

are³bg, bT´ = (0.05, 17.3)21 and ³g, bT´ = (0.21, 11.2) .22 Yet the demand hypothesis

implies the opposite: Prompted by the decline in output, g (the measured decline inp) should have been higher and T should have been lower in the first sample than inthe second. Thus demand shifts do not seem to explain the patterns in GK’s sample.

5.2 Supply-side explanations

Echo effects were first discussed in the growth literature. In a one-consumption-goodGE model, for the interest rate to remain constant in the face of variations in the rateof investment that inevitably occur along the transition path from arbitrary initialconditions, the instantaneous utility of consumption must be linear. Then, if therate of technological progress is also constant, the investment echoes will have theconstant periodicity that they also have in our model, but they will not be damped.Rather, the investment profile simply repeats itself every T periods — see Mitra et al.(1991) and BGL. Johansen (1959) and Arrow (1962) assume a production functionfor the sole final good that is Leontieff in capital and labor. In that case the effectivemaintenance cost is the wage multiplied by the labor requirement per machine. Sincewages rise at the same rate as the rate at which the labor requirement declines, andthe maintenance rate is then constant in units of the consumption good. Thus ourmaintenance cost, c, has an exact counterpart in these models. Since these models

19DDT, Electic shavers, Phonograph records, TV, and Zippers.20Fluorescent lamps, Penicillin, and Styrene.21The industries in note 19 plus Auto tyres and CRT.22The industries in note 20 plus Freezers and Transistors. GK did not report whether output fell

or rose during the shakeout for Computers and Streptomycin.

21

have no costs of rapid adjustment, the infinitely-elastic supply of capital that weassume amounts to the same thing.

Endogenous technological change.–Our model assumes that technological changeis exogenous. Klepper (1996) assumes firms do research, and his model appears toimply that leading firms would squeeze out the inefficient fringe more quickly inindustries where there is more technological opportunity and, hence, faster-decliningproduct prices. The difference between our model and his concerns the fate of thefirms in the first cohort of entrants: In our model the first cohort is the least efficient,whereas in Klepper’s model, the first cohort is the most efficient because it has donethe most research. In Grossman and Helpman (1991) and Aghion and Howitt (1992),monopoly incumbents are periodically replaced by more efficient entrants. Tse (2001)extends the model to allow for more than a single producer.

Exit after learning through experience.–Gort and Klepper (1982, henceforth GK)observed that a shakeout usually comes after a wave of entry. Horvath, Schivardi andWoywode (2003) argue that if a run-up in entry occurs at some point in the industry’slife, then some time later, a fraction of the entrants will have found themselves unfitto be in that industry — a type of learning that Jovanovic (1982) stresses — and willthen exit en masse. The argument of Horvath et al. (2003) would measure thelearning period by T . After exactly T periods, a firm discovers whether it has highcosts and should exit. To develop this argument fully one would have to somehow toshow first that a firm’s learning about productivity is likely to take place all at onceand not gradually as one usually assumes. And, second, one would need to explainwhy learning should occur sooner in those industries where p is declining rapidly.

Technological advances by incumbents.–When a new technology raises the effi-cient scale of firms, it crowds some of them out of the industry; so argue Hopenhayn(1993) and Jovanovic and MacDonald (1994). The assembly-line technology, e.g.,probably raised the optimal scale of auto-manufacturing plants and caused a largereduction in the number of auto producers. Klepper (1996) argues that larger firmsdo more R&D than small firms because they can spread its results over a larger num-ber of units; because they invent at a faster rate, large firms then drive smaller firmsout, often by acquiring them.

Consolidations for other reasons.–Some shakeouts no doubt occur because of thestandardization of products so that some of the variants fall by the wayside and theirproducers exit. The focus on the diesel technology was one reason for the mass exodusof automobile producers that relied on other technologies as a source of power for themodels they built. The winning model forces out other models and their producers.Utterback and Suarez (1993) argue that a dominant design emerges: More generally,consolidations and merger waves can occur for reasons unrelated to drops in demandand to advances in technology. Deregulation, for instance, has led to merger wavesin the airlines and banking industries (Andrade et al. 2001) and to a sharp fall in thenumbers of producers.

22

Evidence shows there are investment spikes — Cooper and Haltiwanger (1996),Gourio and Kashyap (2007). Repeated echo effects in entry and exit seem to bepresent in the data and they are clear indications that a vintage-capital replacementmotive is one of their causes. It remains for us to link the exit decision to the age ofa firm’s capital stock and we shall do that in Section 6.

6 Capital replacement and exit

Our model assumes that ε (τ) jumps at the rate λ, but really only the first jumpmatters, since that first jump suffices to disqualify a firm from competing in themarket for new capital. The general question can be put as follows: ‘Do incumbentfirms develop a disadvantage in setting up machines and plants of the newest vintagesand, if so, how quickly?’ The literature offers some indirect evidence. Prusa andSchmitz (1994) find that a firm’s initial product is better than its second product, itssecond better than its third, and so on. Christensen (1997) cites examples of disk-drive producers and printer producers that failed to invest in the new technologiesthat entrants brought in. Henderson (1993) finds that incumbents are less successfulat research efforts to exploit radical innovation than entrants are. Supporting thevintage-capital model generally, Filson and Gretz (2004, Tables 1-5) support theproportion that ‘new firms and industry laggards are the most likely pioneers of newproduct generations.’ Their Tables 1-5 show that in the early days of a product (herea diameter of a disk), new entrants lead the pack in terms of quality (here defined asstorage capacity). As the format matures, the incumbents become leaders. There are5 new generations of drives in the data set; all of them were pioneered by spin-outs.23

To this evidence we shall add some direct evidence that airline companies aremore likely to exit when their capital is old. But in the next subsection we shall firstestimate λ using the GK data.

6.1 Estimating λ

Let φ ≡ X1

qTbe the fraction of capacity replaced at the first shakeout. As a first

approximation we assume that all firms are of the same size. Since ε is independentover firms, the fraction of firms that exit is y ≡

¡1− e−λT

¢φ. Next, let

z ≡ q0qT

be the initial output of the industry relative to its output at the shakeout date. From(7), p0 = cegT . Then from (5) ,

q0 = D¡cegT , 0

¢= X1

23The evidence is not unanimous, however. Dunne (1994) finds that the age of a plant is unrelatedto the tendency to adopt advanced technology.

23

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 0.1 0.2 0.3 0.4 0.5 0.6

z

y

TV

ESH

DDT

PEN

FLL

Figure 10: The fit of (17) with the smaller sample

Since all of the initial capacity is replaced at T , it must mean that X1 = q0 and thattherefore

Proposition 5 The fraction of firms that exit at T is

y =¡1− e−λT

¢z. (16)

The restriction in (16) holds regardless of why output has grown. Output mayhave grown because the demand curve shifted out, or it may have grown becausedemand is elastic so that the price decline led output to grow. The end result in (16)is the same.We have two sets of estimates of λ. For the first, we calculate bzi from GK’s table

5 as the inverse of the rate of output increase from the date industry i was born up tothe date when the number of firms in the industry peaked. We calculate yi = GK’sTable 4 column 3. This is the total decrease in the number of firms for a period oftime that lasted, on average, for 5.4 years after the date at which the number of firmsin the industry peaked. We calculate Ti from GK’s table 7 as the number of yearsbetween the birth of the industry to the beginning of the shakeout; the numbersreported in the T (1) column in Table 1. Firms may also exit for reasons that areoutside the model.24 To represent these other exits we add a constant, β0, to the

RHS of the regression equation. Thus, we suppose that yi = β0+³1− e−λTi

´zi+ui,

where the ui are sector-specific disturbances. We use non-linear least squares; i.e.,

minλ,β0

Xi

³yi − β0 −

³1− e−λTi

´zi´2

. (17)

24Dunne, Roberts and Samuelson (1988) discuss evidence and models of entry and exit in manu-facturing.

24

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0 0.2 0.4 0.6 0.8 1 1.2

z

y

Transistor

PEN

Tyre

FLL

CR

TV

DDT

ESH

PH

Figure 11: The fit of (17) with the larger sample

The are five industries in GK in which the required by, bz, and bT data are available.The estimates and the resulting fit are shown in Fig 10.Estimates of λ with the alternative definition of y, z, and T .–The second es-

timate of λ comes from a larger sample that we can get if we use the alternativedefinitions of y, z, and T that takes the date of the first spike to be the takeoff dateof an industry, i.e., the start of GK’s Stage 2. The values for the revised bT are thenumbers shown in the T (2) column in Table 1. In that case, if we ignore as negligiblethe capacity created before the takeoff date, bz should equal the inverse of the rateof output increase during GK’s stages two and three only. There are 5 industries inGK for which output data, as well as information on by, are available from the takeoffdate to the shakeout date but not earlier. These industries can now be added to theanalysis. As we explain in Section 3, for the TV industry, we find it better to use theinformation from Wang (2006) in place of GK. The results and the fit for the largerdata set (no of observations = 9) are described in Figure 11.

6.2 Evidence on aircraft retirement and airline exit

We now report our findings using data on aircraft where accurate information on ageis available. Among exiting firms, the age of the capital stock is always T . Survivingcapital is generally younger than that. If demand was almost perfectly inelastic, therewould be very little investment between the spike dates, and the capital stock amongsurviving firms would be almost as old as that among exiting firms. On the otherhand, if demand is highly elastic, most of the existing capital would be quite young.Thus if we let aS be the average age of the surviving firms’ capital stock, unless we

25

0

5

10

15

20

25

30

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Exiting airlines

Surviving airlinesno. of planes operated by surviving airlines = 87

1122

2007

27893021

4159

no. of planes operated by exiting airlines = 1

9

28 43

86

76

33

10

2514

5

Age of capital in years

year

Figure 12: Age of capital among exiters and survivors in the U.S. airlineindustry, 1960-2003.

specify the demand curve all we can say is that

0 < aS < T. (18)

Figure 12 shows the empirical counterparts of aS (blue dots) and T (red dots)for the airline industry. In the U.S., the airplanes of exiting airlines were on average7 years older than those of the surviving airlines. After weighing by the numberof observations, the difference is highly significant. Balloon size is for each seriesproportional to the square root of the number of observations, but the constant ofproportionality is larger for the exiting capital series so as to allow us to see howsample size of that series too evolves over time.

Figure 13 shows almost as strong a difference among all the world airlines. Capitalof exiting airlines was four years older than the capital of surviving airlines and thedifference in the means is again highly significant. Surprisingly, perhaps, the U.S.carriers operated older planes than the carriers based in other countries. A descriptionof the data is in the Appendix, but a summary is in Table 2:

26

0

5

10

15

20

25

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Exiting airlines

Surviving airlines

97

871

3004

4062

5527 7118

11169210

24

35

49

86

259

129

178

53

2

Age of capital

Figure 13: Age of capital of exiters and survivors in among all theworld’s airlines, 1960-2003.

U.S. WorldSurvivors Exiters Survivors Exiters

Average age (yrs) 10.4 17 9.8 13.7Std. dev. of age 7.5 9.4 7.4 9.4# of airlines 231 181 1140 659# of plane-year obs. 95,147 530 213,650 2,092

Table 2 : The data in Figures 12 and 13.

As reported in the table, a plane is counted as one observation for each year of its life.An airline is counted at most twice — as a survivor and then possibly as an exiter.25

Three other pieces of evidence link exit decisions to the need to replace capital tothe decision to exit

1. Plant exit.–Salvanes and Tveteras (2004) find that old plants are (i) less likelyto exit, but (ii) more likely to exit when their equipment is old. Fact (i) theyattribute to the idea that plants gradually learn their productivity and exit if

25Many companies lease their planes. Our argument extends to such companies as well. Thecompetitive leasing price would be p(t) − c per period with airlines making zero profits at eachinstant. Our argument is that whether an airline leases or buys its equipment does not affect itsability to make use of it.

27

the news is unfavorable as Jovanovic (1982) argued. Fact (ii) they attribute tothe vintage-capital effect on exit.

2. The trading of patent rights.–The renewal of a patent is similar to replacing apiece of capital in the sense that a renewal cost must be paid if the owner ofthe patent is to continue deriving value from it. If that owner sells the patentright, he effectively exits the activity that the patent relates to. Serrano (2006)finds that the probability of a patent being traded rises at its renewal dates,indicating that the decision to exit is related to the wearing out of a patentright.

3. Higher embodied technical progress raises exit.–A faster rate of decline in theprice of capital makes it optimal to replace capital more frequently. If replace-ment sometimes leads to exit, we should see more exit where there is moreembodied progress. Samaniego (2006) indeed finds that in sectors where theprices of machinery inputs fall faster, the firms using those machines experiencehigher rates of exit.

6.2.1 Firm exit

A firm ‘exits’ in the GK data when it stops producing a product. In the theorypresented so far, firms can exit only at ages T, 2T, and so on. Pooling over products,Agarwal and Gort (1996, Figure 2) show that hazard rates for firm exit tend torise once age exceeds 30 or 40 years, and perhaps this is because their capital is oldand needs replacing. It is conceivable that mixtures over industries could producedownward-sloping hazards. The fact is, however, that firms in every industry canand do fail at young ages and for reasons often unrelated to the age of their capital.Thus as a theory of exit within a particular industry, the model as it stands is quiteinadequate. The object here is not to seek a general theory of firm exit but, rather,only to show that our theory of the shakeout is robust to the introduction of otherreasons for exit.

We shall now show that the model can produce exit spikes every T periods, andstill have a realistic exit hazard. To do it, we shall assume that firms experience costshocks and that there is a frictionless used-capital market within the industry. Thismarket becomes active if firms have different c’s. We continue to assume that capitalhas zero value to anyone outside the industry. Suppose, then, that c rises permanentlywhen the firm or plant is τ years old, and suppose further that the hazard, h (τ), ofsuch an event is decreasing in τ , perhaps because of a positive effect that learning bydoing exerts on the firm’s production efficiency.

A firm that experiences a rise in c will immediately sell its capital to firms in theindustry that have not experienced such a rise, and extract the full value of the profitsthat the machine will yield until its replacement date. The investment condition (4)is then unchanged because the resale value of the capital fully captures what the

28

firm would have obtained for itself had its c remained at its original level. The newowner of the capital would choose to retire it at the same date that the original ownerwould have had he not experienced a rise in c and therefore the exit condition (3) alsoremains unchanged, as does (5). Equilibrium is therefore exactly the same. However,now there will be two kinds of exit: (i) When the firm’s capital is up for replacementand that the firm’s implementation cost has gone up since the last time capital wasinstalled, and this hazard is zero except for spikes every T periods, (ii) When thefirm’s c has risen, which has the hazard h (τ). For τ < T , the exit hazard is just hand it is decreasing in τ . At τ = T , (i) dominates (ii) since time is continuous. Butover a discrete time period, (ii) could dominate (i), in which case the exit hazardwould decrease monotonically.26

The general point is that the GK observations that Figure 1 portrays concern in-dustry aggregates. Our model too is mainly about these aggregates and it is probablyconsistent with a wide variety of assumptions about turbulence at the more microlevel.

7 Implications for productivity growth

The model has no labor, and so TFP is simply the productivity of capital.27 If theprice of capital used to deflate investment spending were per unit of quality, then allthe technological progress would appear in the capital stock, the resulting measureof the capital stock would be given by (1) and would equal output, with TFP beingconstant at unity. On the other hand, if no adjustment is made for quality so thatthe price index used to deflate investment was unity, then the capital stock would begiven by K (t, t) as given by (2) when evaluated at s = t, and TFP would equal

TFPt =qt

K (t, t). (19)

Thus TFP rises smoothly until the shakeout date, and then it experiences an upwardjump during the shakeout when the number of physical units of capital falls, but thenumber of their efficiency units stays unchanged.

7.1 TFP growth vs. dispersion

Proposition 2 implies that faster TFP-growing industries should show greater TFPdispersion. Dwyer (1998) derives the same relation in a similar model. In a group

26This applies only to a firm that enters with frontier technology. If an entrant were to come inwith used capital, he would replace it before his firm reached age T .27One way to add labor to the model is to have one worker per machine, and to interpret c as the

wage. Labor productivity would then be the same as the productivity of the physical units of capitaland would equal the expression in (19). A shakeout would be accompanied by a sharp decline inemployment.

29

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7g

gT

PH

ZP

TV

ESH

STE

DDT

FLL

PEN

c = 0.039

Figure 14: TFP growth and the max/min TFP ratio

of textile industries he found that the relation was positive and significant.28 Dwyermeasured dispersion by the TFP ratio of the tenth percentile plants to the ninetiethpercentile plants. TFP growth ranged from about two percent to about eight percentand the TFP ratio ranged between 2.4 to 4.6.

Our model cannot generate such large dispersion, even when we measure disper-sion as the ratio of the most productive to the least productive producer. Figure 14plots the logarithm of

lnTFPmaxTFPmin

= gT

as a function of g. It shows, in other words, the comparative steady-state relationbetween inequality and growth.29 The relation is positive, but for the less-than-ten-percent range of TFP growth (which would include all of Dwyer’s industries), themost we can explain is a ratio of about 1.75. Table 5 of Aizcorbe and Kortum (2005)reports a result similar to the one portrayed in Figure 14 — when g is larger, gT shouldgo up.

Figure 14 is based on the information in Figure 4, and on the least-squares estimatec = 0.039. If we switch to measuring T by the time between the industry’s takeoff andthe midpoint of the shakeout episode while adjusting the measure of g accordingly,and if we use the ML estimate of c reported in Figure 5, we get the results shown in

28At the two-digit level, Oikawa (2006) finds a positive relation between TFP growth and TFPdispersion measured by the standard deviation of the logs.29Moreover, the model’s implications for inequality have a curious discontinuity at g = 0. Namely,

if g is really zero, then everyone should be using the same quality machine and there should be noTFP inequality. But a steady state with a very small g would have TFP inequality of at least unity.

30

0

1

2

3

4

5

6

7

8

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7g

gT

ESHPH

CRT

ZPSTETV

DDT

FLL

PENc=0.0776

Trans

Comp

TireFreezer

Strep

Figure 15: TFP growth and the max/min TFP ratio with the alternativedefinition of T — predicted and actual

Figure 15. Note that Figures 14 and 15 portray the very same information portrayedin Figures 4 and 5 — no new information is added. The difference is merely that thevariable plotted on the vertical axis is gT instead of T . Since the data do not haveT declining with g as fast as the model predicts, the relation between g and gT issteeper than the model predicts. This is especially evident in Figure 15.

A further difficulty with the model as an explanation of TFP dispersion is thatthe dynamics of TFP do not quite match the dynamics of actual plants in the data.In a word, too much leapfrogging goes on. In the data TFP-rank reverses sometimes,but we hardly ever see the ‘last shall be first’ phenomenon of the least productiveproducer suddenly becoming the most productive. In our model, a plant would movesmoothly down the distribution of percentiles until it reached the last percentile, andit then would suddenly jump back up to the first percentile, and so on. Analysisof productivity transitions by Baily, Hulten, and Campbell (1992, Table 3) does notbear this out. Plants move up and down the various quintiles of the distributionand the transition matrix is fairly full. Moreover, births tend to be of below averageproductivity.

On the positive side, a supporting fact in Baily et al.’s transition matrix is thatmore plants (14 percent) move from the bottom quintile to the top quintile than thereverse (5 percent). One reason why we do not see the dramatic ‘last shall be first’rank reversals is the tendency for a plant’s TFP to grow as it ages.30 Thus a new,

30Parente (1994) models learning of the technology with the passage of time, and Klenow (1998)models learning as a function of cumulative output.

31

0

0.5

1

1.5

2

2.5

3

3.5

0 10 20 30 40 50 60Age of the Industry

g*m

in(t,

T)g=0.03

g=0.05

g=0.2

g=0.56

Figure 16: Transitional dynamics in productivity dispersion

cutting-edge plant does not immediately have the highest productivity. Rather, itsproductivity grows as it ages, as Bahk and Gort (1993), and Table 5 of Baily et al.(1993) document. This would explain why a new plant does not enter at the top ofthe distribution of TFP in the way that this model predicts and why, as Table 5 ofBaily et al. (1993) shows they tend to rise from the bottom to the top TFP quintileby the time they are 10-15 years old.Transitional dynamics in productivity dispersion.–The model implies that in the

initial stages of an industry’s life, the distribution of TFP across producers should befanning out. How fast it does so, however, should depend on the rate of technologicalprogress, i.e., on g. This is the rate at which the productivity of new capital gains atthe expense of old capital. But after the industry reaches age T , no further fanningout takes place, because old capital begins to be withdrawn. Thereafter, dispersionremains constant at its steady-state level. In Figure 16 we show how the fanning outprocess depends on the industry’s growth rate by plotting, for four different values ofg, the logarithm of

lnTFPmaxTFPmin

= gmin (t, T )

where t is the age of the industry. In contrast, learning models like that of Jovanovic(1982) are ambiguous on this score: The dispersion among survivors can become morenarrow over time if certain distributional assumptions are met, as was the case forthe distribution that Jovanovic (1982) used — the variance of the truncated normaldistribution is smaller than the variance of the untruncated distribution.

32

8 Conclusion

This paper started out with a graphical display of evidence that industry shake-outs of firms occur earlier in industries where technological progress is faster. Weargued that other models of shakeouts were not able to explain this fact, whereasour vintage-capital model does so by predicting earlier replacement when capital-embodied technological progress is fast. We supported this claim with evidence fromthe airline industry that showed firm exits to be positively related to the age of thecapital stock.

By inferring technological progress in the inputs from the decline in the priceof the output as our model predicted, we found that the model fits fairly well thenegative relation between technological progress and the onset of the shakeout. More-over, we found that subsequent investment spikes, too, are also more frequent wheretechnological progress is fast.

References

[1] Agarwal, Rajshree. “Evolutionary Trends of Industry Variables.” InternationalJournal of Industrial Organization 16, no. 4 (July 1998): 511-25.

[2] –––, and Michael Gort. “The Evolution of Markets and Entry, Exit andSurvival of Firms.” Review of Economics and Statistics 78, no. 3. (Aug., 1996):489-98.

[3] Aghion, Philippe and Howitt, Peter, “A Model of Growth Through CreativeDestruction,” Econometrica, March 1992, 60(2), 323-351.

[4] Aizcorbe, Ana and Samuel Kortum. “Moore’s Law and the Semiconductor In-dustry: A Vintage Model.” Scand. J. of Economics 107, no. 4 (2005): 603—630.

[5] Andrade, Gregor; Mitchell, Mark and Stafford, Erik. “New Evidence and Per-spective on Mergers.” Journal of Economic Perspectives, Spring 2001, 15(2), pp.103-120.

[6] Arrow, Kenneth. “The Economic Implications of Learning by Doing.” Review ofEconomic Studies 29, no. 3 (June 1962): 155 - 173..

[7] Atkeson, Andrew and Patrick Kehoe. “Industry Evolution and Transition: TheRole of Information Capital.” FRB Minneapolis staff report 162 (August 1993).

[8] Bahk, Byong-Hyong and Michael Gort. “Decomposing Learning by Doing in NewPlants.” Journal of Political Economy, Vol. 101, no. 4. (Aug., 1993), pp. 561-583.

33

[9] Baily, Martin, Charles Hulten and David Campbell. “Productivity Dynamics inManufacturing Plants.”Brookings Papers on Economic Activity, Microeconomics(1992): 187-249

[10] Boucekkine, Raouf, Marc Germain, and Omar Licandro. “Replacement Echoesin the Vintage Capital Growth Model.” Journal of Economic Theory 74 (1997):333-48.

[11] Caballero, Ricardo and Mohamad L. Hammour. “The Cleansing Effect of Reces-sions.” American Economic Review 84, no. 5 (December 1994): 1350-68.

[12] Chatterjee, Satyajit and Esteban Rossi-Hansberg. “Spin-offs and the Market forIdeas.” mimeo. 2008

[13] Christensen, Clayton. The Innovator’s Dilemma. Cambridge: HBS Press, 1997.

[14] Cooper, Russell and John Haltiwanger “Evidence on Macroeconomic Comple-mentarities.” Review of Economics and Statistics 78, no. 1 (February 1996):78-93.

[15] Dunne, Timothy, Mark Roberts; Larry Samuelson. “Patterns of Firm Entry andExit in U.S. Manufacturing Industries.” RAND Journal of Economics 19, no. 4(Winter, 1988): 495-515.

[16] Dunne, Timothy. “Plant Age and Technology use in U.S. Manufacturing Indus-tries.” RAND Journal of Economics 25, no. 3 (Autumn, 1994): 488-499.

[17] Dwyer, Douglas. “Technology Locks, Creative Destruction, and Nonconvergencein Productivity Levels.” Review of Economic Dynamics 1, no. 2 (April 1998):430-473.

[18] Evans, David. “The Relationship Between Firm Growth, Size, and Age: Esti-mates for 100 Manufacturing Industries.” Journal of Industrial Economics 35,no. 4 (June 1987): 567-81.

[19] Filson, Darren and Richard Gretz. “Strategic Innovation and Technology Adop-tion in an Evolving Industry.” Journal of Monetary Economics 51, no. 1 (January2004): 89-121.

[20] Gavazza, Alessandro. “Leasing and Secondary Markets: Theory and Evidencefrom Commercial Aircraft”, Yale University, March 2007.

[21] Gort, Michael and Steven Klepper “Time Paths in the Diffusion of Market In-novations,” Economic Journal 92 (1982): 630-53.

[22] Gourio, Francois and Anil Kashyap. “Investment spikes: New facts and a general

34

[23] equilibrium exploration.” Journal of Monetary Economics 54 (2007): 1—22.

[24] Grossman, Gene M. and Helpman, Elhanan, “Quality Ladders in the Theory ofGrowth,” Review of Economic Studies, January 1991, 58(1), 43—61.

[25] Henderson, Rebecca. “Underinvestment and Incompetence as Responses to Rad-ical Innovation: Evidence from the Photolithographic Alignment Equipment In-dustry.” RAND Journal of Economics 24, no. 2 (Summer 1993): 248-270.

[26] Hopenhayn, Hugo. “The Shakeout.” wp#33 Univ. Pompeu Fabra, April 1993.

[27] Horvath, Michael, Fabiano Schivardi and Michael Woywode. “On Industry Life-Cycles: Delay, Entry, and Shakeout in Beer Brewing.” International Journal ofIndustrial Organization 19, no. 7 (2003): 1023-1052.

[28] Johansen, Leif. “Substitution versus Fixed Production Coefficients in the Theoryof Economic Growth: A Synthesis.” Econometrica 27, no. 2 (April 1959): 157-176.

[29] Jovanovic, Boyan. “Selection and the Evolution of Industry.” Econometrica 50,no. 3 (June 1982): 649-70.

[30] –––, and Saul Lach “Entry, Exit, and Diffusion with Learning by Doing.”American Economic Review 79, no. 4 (September 1989): 690-99.

[31] –––, and Glenn MacDonald. “The Life Cycle of a Competitive Industry.”Journal of Political Economy 102 (April 1994): 322-47.

[32] –––, and Peter L. Rousseau. “General-Purpose Technologies.” Handbook ofEconomic Growth vol. 1B Amsterdam: Elsevier (2006): 1181-224.

[33] Klenow, Peter. “Learning Curves and the Cyclical Behavior of ManufacturingIndustries.” Review of Economic Dynamics 1, no. 2 (May 1998): 531-50.

[34] Klepper, Steven, “Entry, Exit, Growth, and Innovation over the Product LifeCycle,” American Economic Review 86 no. 3 (June 1996): 562 - 83.

[35] –––, and Kenneth Simons. “Industry Shakeouts and Technological Change.”International Journal of Industrial Organization 23, no. 2-3 (2005): 23-43.

[36] McGrattan Ellen, and James A. Schmitz, Jr.. “Maintenance and Repair: TooBig to Ignore.” Federal Reserve Bank of Minneapolis Quarterly Review 23, no. 4(Fall 1999): 2—13.

[37] Mitchell, Matthew. “Technological Change and the Scale of Production.” Reviewof Economic Dynamics 5, no. 2 (April 2002): 477-88.

35

[38] Mitra, Tappan, Debraj Ray and Rahul Roy. “The Economics of Orchards: AnExercise in Point-input, Flow-output Capital Theory.” Journal of Economic The-ory, 53, no. 1 (1993): 12-50.

[39] Oikawa, Koki. “Uncertainty-Driven Growth.” New York University, January2006.

[40] Parente Stephen L., 1994. “Technology Adoption, Learning-by-Doing, and Eco-nomic Growth,” Journal of Economic Theory. Elsevier, vol. 63, no. 2 (1994):346-69.

[41] Prusa, Thomas and James Schmitz. “Are New Firms an Important Source ofInnovation? : Evidence from the PC Software Industry.” Economics Letters 35,no. 3 (March 1991): 339-342.

[42] Prusa, Thomas and James Schmitz. “Can Companies Maintain Their InitialInnovation Thrust? A Study of the PC Software Industry.” Review of Economicsand Statistics 76, no. 3 (August 1994): 523-40.

[43] Salvanes, Kjell and Ragnar Tveteras. “Plant Exit, Vintage Capital and the Busi-ness Cycle.” Journal of Industrial Economics LII, no. 2 (June 2004): 255-76.

[44] Samaniego, Roberto M. “Entry, Exit and Investment-Specific TechnicalChange.” Unpublished manuscript, George Washington University, 2006.

[45] Serrano, Carlos. “The Dynamics of the Transfer and Renewal of Patents.” Uni-versity of Toronto, March 2006.

[46] Tse, Chung Yi, “The Distribution of Demand, Market Structure and Investmentin Technology,” Journal of Economics, October 2001, 73(3), 275—297.

[47] Utterback, James, and Fernando Suárez, “Innovation, Competition, and Indus-try Structure,” Research Policy 22 (1993): 1-21.

[48] Wang, Zhu. “Learning, Diffusion and Industry Life Cycle”, manuscript, FederalReserve Bank of Kansas City, 2006.

36

EXIT ENTRY

spike dates

spike dates

Product &

yr of comm intr.

Length of raw series

in yrs since comm intro

in calendar

yr

in yrs since comm intro

in calendar

yr

Corr btw smoothd entry and exit rates

Corr btw entry and

exit residuals

Corr btw

entry and exit rates

G-K Stage 4

1 Antibiotics 44 7 1955 2 1950 -0.46 -0.04 -0.30 not in G-K 1948 19 1967 39 1987

32 1980

2 Artificial Christmas Trees

54 8 1946 35 1973 -0.52 -0.02 -0.21 1968-1969

1938 18 1956 49 1987 43 1981