energy economics and policy (ss 2007) - cepe - eth z¼rich

TRANSCRIPT

1

Scriptum of the course No. 351-0510-00

Energy Economics and Policy

(Energiewirtschaft und Energiepolitik)

SS 2007

24 May 2007

Prof. Dr.-Ing. Eberhard Jochem

Chair of economics and energy economics Lehrstuhl für Nationalökonomie und Energiewirtschaft

2

Content Date Page (Übersicht zur Vorlesung) 3

Recommended books, monographs, statistics, and publications 7

I) Energy resources, sustainability, energy statistics

• Reserves and resources of non-renewable energies 22.3. 13

• Energy statistics 29.3. 24

• Ecological economics, sustainability concept 29.3. 31

• The concept of sustainable development 5.4. 38

II) Drivers of energy demand

• Energy flow diagram, starting at the energy services 12.4. 43

• Exercise/ Übung 1 discussion and solutions 12.4.

• Energy efficiency potentials and energy intensities 19.4. 45

• Private households, services, industry, transportation, prices 26.4.

• Cost of energy conversion and end-energy uses, external cost 3.5.

III) Energy economic analysis and projections

• Scenario technique, modelling, and boundary conditions 10.5. 60

• Development of energy demand by different types of models-

advantages and limitations of different types of models 24.5.

IV) Obstacles and market imperfections and related portfolios of energy- and climate policy

• Obstacles of energy efficiency and substitution 31.5.

• Market imperfections and policy instruments I 7.6.

• Energy and climate policy II and their evaluation 14.6.

V) Annex

• Glossary 32

You will find additional information for the course and the exercises at

http://www.cepe.ethz.ch/education/EnergyEconomicsCepe

3

Energy economics and policy (SS 2007)

Prof. Dr.-Ing. Eberhard Jochem Course: Thursdays, 15-17 h, room: ML H44

Start: March 22, 15.15 h, room: ML H44

Objectives:

The students are introduced to basic knowledge of resource and energy economics, to renewable and non-renewable energies, energy statistics, energy markets, energy efficiency potentials, obstacles and market imperfections and related energy policies.

The methods covered are cost estimation of new energy technologies, scenario technique, energy models (bottom up and top down), and external cost of energy use. The energy policy section covers general and specific policy instruments and also includes climate change policy, related instruments and their implementation.

In general, the students mostly educated in natural sciences and engineering have the opportunity to develop their "coupling competence" to concepts of economics and policy and to use this knowledge in their professional life in interdisciplinary working teams. There are two chances to deepen the knowledge of the course: three exer-cises and a written paper (of about 10 to 12 pages) related to issues of energy eco-nomics and policy.

Overview of the course: Energy Economics and Policy (Energiewirtschaft und Energiepolitik)

No. date Topic/Thema lecturer Bibliography

Introduction and energy resources and energy statistics

1

22.3.

Energy as natural resource • economics of natural resources • reserves & resources of energy

Wickart/ Jochem

K. Blok 2006, Chapt. 4 Spreng, 1995, Kap. 1 BFE and IEA/OECD

2

29.4. Energy statistics (descriptive) • Definitions, units, conversion fac-

tors • Energy balances (specially Swit-

zerland) • cumulative energy demand

Energy and sustainability • ecological economics

Jochem www.admin.ch/bfe/ http://www.iea.org/ www.worldenergy.org K. Blok 2006, Chapt. 2 K. Blok 2006, Chapt. 6

CEPE / D-MTEC ETH Zentrum ZUE E 8 CH-8092 Zürich Tel. +41-44632 06 50 Fax +41-44-632 10 50 http://www.cepe.ethz.ch

4

• Brundlandt-Commission; • sustainability concepts

3 5.4. Drivers of energy demand • Energy flow diagrams of indus-

trialised countries & world • Energy services and intensities • climate change and environ-

mental pollution

Jochem K. Blok, 2006, Chapt. 2

4 12.4. Exercise 1 discussion and so-lutions

M. Jakob Literature of the first three courses

Energy demand and conversion - Drivers, sectors, and cost

5 19.4. Energy chains and efficiency • Energy services, useful energy,

final energy with respect to space heat, service sector, in-dustry

• Energy efficiency potentials, theoretical, technical, welfare-economic, macro and micro-economic, expected

• The 2000 Watt/cap society

Jochem K. Blok 2006, Chapt. 10 Hensing, Pfaffenberger, Ströbele 1998, Goldemberg, J. 2000; Kap. 6; Romm, J.J. 1999: Cool Com-panies Geiger, B. u.a., 1999 Jochem et al. 2003

6 26.4. Energy services and demand (Perspectives of the BFE) • private households • service and industrial sector • transport sector • conversion sector • structural change

Jochem K. Blok 2006, Chapt. 3 BFE 2007, Synthesis Report Diekmann, J. u.a. 1999,

7 3.5. Cost of energy conversion and end-use technologies) • technologies in cost competition • cost reduction by learning and

economies of scale • cost optimal mix of energy con-

version technologies

Jochem K. Blok 2006, Chapt. 11 Hensing, Pfaffenberger, Ströbe-le 1998, Kap. 11 Hirschberg, Jakob 1999

7 3.5. External cost and their inter-nalisation • external effects (environment,

resources) • Identification, quantification,

monetarisation • external cost in energy conver-

sion and use

Jochem Stiglitz, J. 2000, Kap. 8 Pindyck, Rubinfeld 1998, Kap. 18 Pearce und Turner 1990, Kap. 4-6

5

Energy economic analysis and projections

8 10.5. Scenario techniques and boundary conditions • Methodology of Scenario design • examples of the energy perspec-

tives Energy modelling • macro economic energy models • process-oriented energy models • linking TD und BU models (hy-

brid models)

Jochem Energy perspectives, BFE, 2007 K. Blok 2006, Chapt. 14 Jochem/Jakob, 2003 Hensing, Pfaffenberger, Ströbele 1998, Chap..11 Heinloth, K. 1998, K. Blok 2006, Chapt. 14 Goldemberg, J. 2000, Kap.6 Jochem, Kuntze, Patel 2000

9 24.5. Energy demand projections and limitations of methods • macro models (technology pro-

gress, closed causal relation-ships)

• Simulation und Optimising of bot-tom up (BU) models (techn. pro-gress, partial analyses)

• combination of model types by Integration (soft and hard links)

Jochem K. Blok 2006, Chapt. 14 Hensing, Pfaffenberger, Ströbele 1998, Kap. 11 K. Blok, 2006 Chapt. 14 Heinloth, K. 1997, Kap. 1 und 14 Bartzsch, W.H. 1997

Obstacles, market imperfections, opportunities, and energy and climate policy

10 31.5. Obstacles of energy efficiency and substitution • company internal problems and

situations • Preferences, prestige, psycho-

logical aspects • legal and other unfavourable

boundary conditions

Aebi-scher

Sorrell et al. 2004, Chapt. 2-5 Jochem, 2004; Ostertag u.a. 2000 Jochem, Kuntze, Patel 2000

11 7.6. Market imperfections • Market power, the role of media • external effects of technological

options • international issues (competi-

tiveness)

Energy policy instruments I • general instruments • international co-ordination (EU,

G8, OECD, Kyoto)

Jochem Sorrell et al. 2006, Chapt. 2-5 Ostertag 2003 Jochem, Kuntze, Patel 2000Ziesing u.a. 1997 Hensing, Pfaffenberger, Ströbe-le 1998, Chapt.. 13 – 15 Sorrell et al. 2004 Chapt. 7 + 8 K. Blok 2006, Chapt. 15

12 14.6. Energy policy instruments II • sector- und technology specific

policy measures

Jochem

Sorrell et al. 2006 Chapt 7 and 8 K. Blok 2006, Chapt. 15

6

• Policy portfolios as reaction on simultaneous obstacles

• International trade

Evaluation of energy and climate policies • evaluation criteria • direct and indirect effects • policies of innovation • long term effects (discounting?)

Ziesing u.a. 1997 Hensing, Pfaffenberger, Ströbele 1998, Kap. 13 – 15 Sorrell et al. 2006 Chapt 7 and 8 K. Blok 2006, Chapt. 15 Hensing, Pfaffenberger, Ströbe-le 1998, Kap. 13 – 15

13 21.6 Conclusions of the course discussion of exercise No.3

Jochem, Wickart

Sorrell et al. 2006 Blok 2006 Manuscript Jochem

exam

5.7.

Semester end exam (eventu-ally, some who leave earlier have to pass an oral exam)

Jochem, Wickart

no manuscript allowed, only small calculator accepted

Important Information (Mitteilungen) for Testate and exams

Testate conditions for the Testate:

• for all students to receive 3 credits: active participation at the courses, passing 2 exercises out of 3 minimum, and passing the exam

exams Students who want to pass a Semester-Endprüfung : the written 90 minutes lasting exam takes place at July 5, 2007 between 15.15-16.45 h Confirmation per Email the latest until one day before the examination day at: [email protected], 044 632 03 98.

Exercises/ Übun-gen

The course has two hours per week and three exercises. The exercises have to be made within two weeks after distribution. The results of the exercises will be explained in some of the second hour of the course. The solutions will be simultaneously published at the homepage of CEPE (http://www.cepe.ethz.ch/education/EnergyEconomicsCepe). Specific hours for exercises are not planned.

You may ask the following assis-tents

Sprechstunde via oral or e-mail confirmation: Andrea Honegger Tel.-No.: 044 632 05 76 (course and exercises: Prof. Jochem) [email protected] Marcel Wickart Tel.-No.: 044 632 03 98 (Economic aspects) [email protected] Bernard Aebischer Tel.-No.: 044 632 41 95 (technical and policy aspects) [email protected]

7

8

Recommended books, monographs, statistics, and publications Recommended books and monographs Banks F.E. (2000). Energy Economics: A Modern Introduction, Kluwer Academic Publishers,

Dordrecht

Blok K. (2006). Introduction to Energy Analysis, Techne Press, Amsterdam, the Netherlands

Hensing I., W. Pfaffenberger und W. Ströbele (1998). Energiewirtschaft – Einführung in Theo-rie und Politik, Oldenbourg, München, Germany

Griffin J.M. und H.B. Steele (1986), Energy Economics and Policy, Academic Press, Orlando

Sorrell S., O’Malley E., Schleich, J. and Scott, S. (2004). The Economics of Energy Efficiency – Barriers to Cost-Effective Investment, Edward Elgar Publishing Limited, Cheltenham, UK

Important energy statistics BFE, Bundesamt für Energie, (several years). Schweizerische Gesamtenergiestatistik 2005.

Bern ; http://www.bfe.admin.ch/themen/00526/00541/00542/00631/index.html?lang=de

BFE Bundesamt für Energie, (several years). Schweizerische Elektrizitätsstatistik, 2005. Bern 2006. http://www.bfe.admin.ch/themen/00526/00541/00542/00630/index.html?lang=de

IEA/OECD, (several years) Energy Balances for OECD-countries. Paris 2001; www.iea.org/stat.htm

World Energy Council (WEC). (several years) Country statistics and survey on energy re-sources. http://www.worldenergy.org/wec-geis/edc/default.asp

Publications to individual issues of the course Baron, R., Jochem, E. Kristof, K. (2005): Studie zur Konzeption eines Programms für die

Steigerung der Materialeffizienz in mittelständischen Unternehmen. Arthur D. Little, Fh-Inst. f. System- und Innovationsforschung, Wuppertal-Institut, Wiesbaden/Karlsruhe/-Wuppertal

Bartzsch, W.H. (1997), Betriebswirtschaftslehre für Ingenieure.

Bonomo, S., M. Filippini und P. Zweifel (1998), “Neue Aufschlüsse über die Elektrizitäts-nachfrage der schweizerischen Haushalte”, Schweiz. Zeitschrift für Volkswirtschaft und Statistik, Vol.134 (3), S. 415-436.

Commission of the European Communities (2006) Action Plan for Energy Efficiency: Realis-ing the Potential COM(2006)545 final, October 19, Brussels

Cuhls, K., Blind, K., Grupp., H. (1998), Delphi '98 Umfrage. Studie zur globalen Entwicklung von Wissenschaft und Technik. Methoden- und Datenband. Fh-ISI im Auftrag des BMBF, Karlsruhe, Februar 1998

Diekmann, J. u.a. (1999), Energie-Effizienz-Indikatoren. Umwelt und Ökonomie 32 Physika Heidelberg

Filippini, M. (1997), Elements of the Swiss Market for Electricity. Physica-Verlag, Berlin.

Geiger. B., E. Gruber, W. Megele (1999), Energieverbrauch und Einsparung in Gewerbe, Handel und Dienstleistung. Physika Heidelberg

Goldemberg, Jose (2000), World Energy Assessment. UNDP New York , Kap. 6 End-use efficiency

9

Heinloth, Klaus, (1997), Die Energiefrage – Bedarf und Potentiale, Nutzung, Risiken und Kos-ten. Vieweg, Braunschweig.

Hirschberg, S. und M. Jakob (1999), Cost Structure of the Swiss Electricity Generation under Consideration of External Costs, SAEE Seminar Strompreise zwischen Markt und Kos-ten: Führt der freie Strommarkt zur Kostenwahrheit?, Bern.

Hunt, S. und G. Shuttleworth (1996), Competition and Choice in Electricity, Wiley, Chichester

IEA (International Energy Agency) (2006): Energy Technology Perspectives 2006 – Scenarios and Strategies – in support of the G8 Plan of Action. OECD, Paris

IPCC (Intergovernmental Panel on Climate Change) (2001): Climate Change 2001 - Mitiga-tion: Contribution of Working Group III to TAR. Cambridge Univ. Press, Cambridge UK

Jochem, E., U. Kuntze, M. Patel (2000), Economic Effects of Climate Change Policy - Under-standing and Emphasizing the Costs and Benefits. ISI Karlsruhe

Jochem, E., Jakob, M. (2003), Energieperspektiven und CO2-Reduktionspotenziale in der Schweiz bis 2010, vdf-Verlag, ISBN 3-7281-2916-X.

Jochem, E. (edr) (2004), Steps towards a sustainable development - A White Book for R&D of energy-efficient technologies, ISBN 3-9522705-0-4.

Jochem, E. (2007): Using Energy and Materials More Efficiently – Large and Profitable Poten-tials, But Little Attention from Energy and Climate Policy. Die Energiepolitik zwischen Wettbewerbsfähigkeit, Versorgungssicherheit und Nachhaltigkeit Vierteljahreshefte zur Wirtschaftsforschung 76(2007)1, p.50-62

Keating, M. (1995), Agenda for Change, Centre for Our Common Future, Geneva (ex. auch auf Deutsch)

Markewitz, P. u.a. (1998), Modelle für die Analyse energiebedingter Klimagasreduktions-Strategien. Reihe Umwelt, Forschungszentrum Jülich

OECD/IEA (2005), Resources to Reserves – Oil & Gas Technologies for the Energy Markets of the Future, International Energy Agency (IEA), Paris.

Ostertag, K. (2003): No-Regret Potentials in Energy Conservation – An Analysis of Their Relevance, Size, and Determinants. Physica , Heidelberg

Pearce, D.W. und R.K. Turner (1990), Economics of natural resources and the environment, Harvester Wheatsheaf, New York, Kapitel 4-6

Pindyck, S.R. und D.L. Rubinfeld (1998), Mikroökonomie, 4. Auflage, München: Oldenbourg.

Romm, J. J. (1999), Cool companies - How the Best Businesses Boost Profits and Productiv-ity by Cutting Greenhouse Gas Emissions. Earthscan, London.

Samuelson, P.A. und W.D. Nordhaus (1998), Volkswirtschaftslehre, Ueberreuter, Anhang 5 und 7.

Spreng D. (1995), Graue Energie, vdf-Hochschulverlag an der ETH Zürich

Spreng D. und J. Schwarz (1993), Energie – ihre Bedeutung für die Wirtschaft, Bundesamt für Konjunkturfragen, EDMZ Bern, Bestellnummer: 724.316 d

Stiglitz J.E. (2000), Economics of the Public Sector, W. W. Norton, New York

Rahmeyer F. (1999), Preisbildung im natürlichen Monopol, WiST Heft 2, Februar 1999, S.69-75.

VDI-Gesellschaft für Energietechnik (2000), Energie und nachhaltige Entwicklung, VDI/GET Düsseldorf

Viscusi W. K., Vernon, J. M. und Harrington, J. (1995), Economics of regulations and antitrust, second edition, MIT Press, Chapt 11.

Ziesing H.-J. et al. (1997), Szenarien und Massnahmen zur Minderung von CO2-Emissionen in Deutschland. in: Politikszenarien für den Klimaschutz. Band 1 (Stein und Strobel Hrsg.) Reihe Umwelt Forschungszentrum Jülich.

10

Overview and short introduction

The core competence of the students participating in this course is in the fields of natural and environmental sciences, engineering, construction, or architecture. The objective of the course is to develop "coupling competence" of neighbouring disci-plines, methods and data, relevant for energy economics and energy policy analysis (see Figure 0-1). Energy economics and policy is a quite interdisciplinary field of sci-entific analysis and basic knowledge in energy technology, thermodynamics, and micro economics is a prerequisite to fully benefit from the course.

Energy statistics

- descriptive- analytical- Data sourcesEnergy resources

- Reserves- Resources

Eficient use of energy

- Potentials of efficiency- Energy services

Energy policy- Measures and portfolios

- national, Canton level- EU und international

Obstacles andMarket imperfections

- company internal obstacles - general deficits- sectoral obstacles

Energy projections

- Scenario technique- Modelling

Markets and externalities- Production cost and prices- External cost

Energy demand- drivers, - specific demand

Engineering

Construction

EnvironmentalSciences

Physics

Energy statistics

- descriptive- analytical- Data sourcesEnergy resources

- Reserves- Resources

Eficient use of energy

- Potentials of efficiency- Energy services

Energy policy- Measures and portfolios

- national, Canton level- EU und international

Obstacles andMarket imperfections

- company internal obstacles - general deficits- sectoral obstacles

Energy projections

- Scenario technique- Modelling

Markets and externalities- Production cost and prices- External cost

Energy demand- drivers, - specific demand

Engineering

Construction

EnvironmentalSciences

Physics

Figure 0-1: Overview over the course on "Energy Economics and Policy" – devel-oping coupling competence to other disciplines, methods and statistics

Energy use is labelled as the "blood" of industrialised countries to stress the impor-tance of a simple mean that allows societies to live in great comfort and safety. How-ever, the easy and inexpensive availability is increasing at stake because of three challenges: (1) a foreseeable tenfold increase of global gross domestic product which could induce at least a fivefold increase in primary energy demand, (2) the expected energy price increases due to the maximum production of oil within the next decades, and (3) the climate change mainly due to the 80% fossil fuel use of primary energy at present. The course will cover the analysis and possible solutions of these chal-lenges by pointing to methods of analysis, potential solutions, their obstacles and optional policies.

11

At what level of economics we are talking about? There are different levels of economics and the same expression (such as cost or benefit) may not mean the same at those different levels. This fact leads to many misunderstandings in discussions and readings in journals. The course distinguishes four levels of economics, which is important to keep in mind (see Figure 0-2):

• the level of business economics and project evaluation (see Chapt. 5),

• the sectoral (micro) economic level such as the energy supply sector (Chapt. 6, 9)

• the macro economic level (see Chapt. 8, 9), and

• the welfare economics level (including external costs and benefits not in-cluded in market prices of products and services; see Chapt. 11)

The course covers these four levels and refers to the different types of quantitative models. The course also refers to typical models that are being used at the different levels of economic evaluation; and there are types of models that build a bridge be-tween the different levels; e.g., the input/output model is a very convenient and pow-erful model type building a bridge between the process-oriented bottom up models and the macro economic models; the latter also can handle externalities in principle (see Figure 0-2).

Key issues : technological change, shifts in energy supply, energy-economy interactions, energy-

environment interactions and energy-society interactions

external effects(external costsand benefits)

economics(economy-wide and

macro effects)

energy system assessment(supply and demand,

technology)

business economics(project evaluation)

Micro :Sector level

« micro-micro » :Technology and site

level

Macro :National/regional

level

bottom-up, technology-

oriented

top-down, sector-

oriented

Types ofmodels:

I/O-models

Level ofeconomics :

Figure 0-2: Overview of different levels of economic analysis

However, this course can only give an overview on aspects of energy technologies, on energy models, obstacles, motivations, market imperfections, and policies. There are additional courses on these issues at ETH, but this course tries to give a holistic view how all the elements of technology innovation and potentials, of economics and

12

behavioural sciences as well as policy sciences work together – a gigantic causal relationship of a part of a society.

13

I. Resources of energy, sustainable development, and energy statistics

Energy as a natural resource and its role in the economy and society

Objectives:

The understanding of natural resources and the state of the art of statistics are the objectives of this section of the course. The student should be able to distinguish different types of reserves and resources and understand the reserve to production ratio, stationary and dynamic, the theory of natural economics (back stop technology, Hotelling rule) and the national energy statistics (energy flow diagram), the cumula-tive energy demand and some understanding of the role of energy in industrialised countries. Finally, the basic principle of sustainable development (in its hard and soft interpretation) should be known.

I.1. Reserves and resources of non-renewable energies

If sustainability demands that “present generations should use non-renewable re-sources without compromising the capacity of future generation to satisfy their own needs”, two questions arise regarding fossil fuels:

• What are the theoretically maximum quantities of fossil fuels mankind could use in the future? How long will they last, giving constant or even increasing use in the future decades?

• What are the alternatives of fossil fuels? Can they be developed early enough and at similar cost and prices as the cost level of fossil fuel is today?

Global primary energy demand can be distinguished in several phases (see Figure I.1-1): (1) a long period over eight decades with slowly increasing demand (1.7 % per year) until the end of World War II which resulted in an increase by a factor of 4 be-tween 1875 and 1950. (2) A steep increase (by 4.7 % per year) and also in per capita energy use between 1950 and 1979; (3) still an increase in global energy demand, but not faster than the growth of world population, which means a stagnation per cap-ita primary energy use thereafter (see Figure I.1-1).

For the uninformed reader this may be frightening as only 15 % of world population (about 1 Bill. people) are living in the comfortable level of an industrialised country, and there may be another 8 Bill people who will want to live as comfortable as the industrialised world does. This would mean a tenfold increase of global gross domes-tic product at the end of this century compared to today and again a fourfold increase of primary energy demand where an improvement of energy productivity of 1 % per year has been already considered.

However, there is some indication that the increase in primary energy demand will slow down; the per capita world primary energy demand stabilised during the last 25 to 30 years around 70 GJ/cap and year (see Figure I.1-1). The reason is higher effi-ciency gains as the usual 1 % per in OECD countries and a substantial energy effi-

14

ciency improvement in former centrally planed economies where waste of energy (being a public good) was extremely high compared to Western levels.

The experience of the two oil price crises in 1973 and 1979/80 (see Figure I.1-2) showed a substantial reaction of markets, technology producers, and policy making leading to more efficient use of energy and energy substitution towards natural gas, nuclear power and renewable energies. Awareness has grown that fossil fuel re-sources are not abundant, but need constant exploration efforts and improvement of the production technologies, but also alternative energy sources in the longer term.

Nuclear powerNatural gas

Lignite

Oil

Hard coal

Wood

Figure I.1-1 World primary energy demand, per capita energy use, and world population, 1875 to 2000

The so called "oil crisis" of 1973 already has changed the structure of primary energy use of the world: whereas in 1973, oil use accounted for 45 % of total primary energy use, 27 years later the share of oil has dropped to 34.9 % (see Figure I.1-3) and tends to achieve 33 % within this decade. Natural gas and nuclear energy grew dur-ing this period by five percentage points or six respectively. The share of coal re-mained rather unchanged at around 24 %, which means that coal use increased dur-ing this period and quite substantially contributed to the increasing CO2 emissions and atmospheric CO2 concentration. Major additional coal use occurred in the emerg-ing countries of China and India, both countries owning large domestic coal reserves.

15

70

60

50

40

30

20

10

1861 1870 1890 1910 1 930 195 0 1970 1990

P ennsy l-van ischer Ö l ‚B oom ‘

B eg innR uss ischer Ö lexporte

S um a tra P roduktion beg inn t

E n tdeckung S p indle top Te xas

N ach kriegs-w iederau fbau

U nterbruchIran ischer L ie fe rungen

S uez K rise

Yo m K ip ur

R evo lu tion in Iran

O P E C fü hrt neues P reis-system u nd, spä te r, Q uo-tenrege lung e in

P ro duktion in V en nezuela wächst

A ngs t vor K nap phe it in U S A

E ntdeckung in O st-Texa s

Figure I.1-2 Development of the oil price (at constant prices of 1992), 1861 to 1992, in US $ per barrel [159 l ]

Figure I.1-3 Share of primary energy use, world, 1973 and 2000

Non renewable reserves and resources – concepts and indicators The non-renewable resources – whether energy or many minerals – have much in common regarding their use by mankind. Questions arise around issues such as: How long will the resource be available given ever increasing production and use? How easily available are they going to be and at what cost? What portion of the total resources has already been used or at least discovered? Can future technology im-provement increase the availability at present cost, or at what cost in the future?

The answers are different depending on the non-renewable resource in question. There is, however, some joint set of definitions and also the economic theory on natural resources (see also the course and publications from Lucas Bretschger, ETH Zürich).

16

The definitions are quite important to understand the complex processes on explora-tion, production, exhaustion of non-renewable resources, particularly of energy re-sources like coal, oil, natural gas and uranium. The ignorance of these issues in in-dustrialised countries is enormous, just by citing a technical newspaper (CHEMan-ager, March 23, 2007, first page, first article: "In about 40 years the so far discovered resources of oil will be depleted"). This statement is totally incorrect and implies that mankind will run out of oil after the middle of this century. This statement was written in the same way in 1960 at a much lower yearly oil production rate. The relation be-tween proven reserves and present yearly oil production was about 40 years for al-most all decades of the last century. So where is the concept to understand this?

Geologists say that mankind is close to the moment when it has used half of the re-sources of oil that may become recoverable in the long future. And they distinguish as follows among the reserves and resources for any non-renewable resource (see Figure I.1-4):

• Proven reserves are fields of oil, natural gas, or coal that have been clearly identified in their magnitude and the production cost to make them available to energy or material markets. They are known to be economically recover-able.

• Additional recoverable reserves are either those that are known, but not eco-nomically recoverable, or those that would be economically recoverable, but have not yet been explored and quantified, only notified by prospection.

Cumulated past consumption

Proven reserves

known, non-profitable and unknown profitable reservoirs

additionallyrecoverable

resources

unknown and non-profitable

resources

explo-ration

technical progress

hypothetical resources

Menge

Unsicherheit

Ressourcen

Quantity

Uncertainty

Resources

Figure I.1-4: Scheme of natural resources, structured in: resources already used in the past, proven reserves (partially economically producible and par-tially not), and resources to be discovered, both economically produc-ible or not

• Hypothetical resources have not yet been discovered, but the geologists es-timate based on their knowledge on the history of earth over hundred millions of years that in certain areas of the globe (e.g. in deep oceans, in the arctic or in certain areas of Alaska or Africa) should be some additional occurrences of oil (or gas, or coal).

17

The exact determination of the maximum production of a non-renewable is not easy because of several reasons (see also Figure I.1-5). Technical progress in secondary and tertiary production of oil may shift the line between recoverable and non-recoverable resources in the future decades (see Figure I.1-4). Some experts as-sume that total recoverable resources of conventional crude oil are in the order of 2’000 Gt whereas others assume a potential of 2'600 Gt. This dispute is not unimpor-tant for the decades to come, as the 50 % depletion of oil resources is expected dur-ing the next decades (see Figure I.1-5).

Figure I.1-5 Expected times of the depletion mid-point of crude oil in the next few decades, depending on assumption of recoverable resources , techni-cal progress, and future global demand of oil products.

The time of the depletion mid-point of crude oil does not only depend on the recover-able resources, but also on the oil demand within the next decades. If energy effi-ciency makes fast progress and the substitution of oil products (heating oil, gasoline, diesel and jet fuel, petro-chemically based plastics develops quite fast), one can ex-pect a late mid depletion point for oil (e.g. after 2030).

The timing of the depletion mid-point is quite important, as at this point in time the global energy price level is likely to increase substantially. Crude oil will be still the market leader in those times and today, almost a 100 % of the world road, ship and air transport are dependent on oil products. This is one extreme challenge the world economy is facing in the next few decades and one reason why large automobile manufacturers and governments are intensively searching for fuel alternatives (syn-thetic fuels from coal (where large reserves exist), biomass, and solar hydrogen).

The stationary reserve to production ratio of conventional oil and natural gas

The ratio of proven reserves to yearly consumption of a non-renewable energy (sta-tionary duration of reserves, statische Reichweite) which is for oil about 40 years or for natural gas about 60 years is often misunderstood as a period when production of this non-renewable energy would stop. This perception however does not at all re-flect the technical or even theoretical availability of non-renewable resources. The

oil production in Mio t per year

18

stationary duration of proven reserves SD is the relation of economically recoverable quantity of known reserves Qknown and the yearly production of this resource P:

SD = Qknown / P ;

It does not include known, but not economically recoverable reserves and, more im-portantly, does not include new reserves (at present being undiscovered resources) which will be explored in the future where it is an open question whether they will be economically producible or not at the prices at that time in the future (see Figure I.1-4). This is obvious if one considers the stationary reserve to production rate of natural gas (see Figure I.1-6). When it became clear that the long term growth per-spectives of natural gas demand look better than of crude oil, the stationary ratio of reserves to production increased from 40 years in the 1960s to 60 years in the 1990s.

The concept of stationary reserve to production ratio simply refers to entrepre-neurial considerations that 40 years of proven and economically producible oil reserves (or 60 years of natural gas reserves) is a sufficient signal not to invest more than business as usual in exploration of new fields.

020406080

100120140160180

1960 1970 1980 1990

KummulierteFörderung (Bill. m3)Ursprüngliche Vorräte(Bill. m3)Statische Reichweite(Jahre)

Cumulated production(Bill. m3) Proven res. at a givenpoint in time (Bill. m3)

Stationary reserve-production ratio (years)

Figure I.1-6 Natural gas: proven reserves, recovery, stationary reserve-production ratio

Technical, economic, and policy aspects The decline of the oil price in 1985, five years after the steep oil price increase influ-enced by the revolution in Iran was due to the fact that the high oil price made pro-duction of crude oil in difficult environments possible, e.g. the North Sea (where pro-duction is peaking in this decade even with enhanced oil recovery, see Figure I.1-7), the Mexican Golf, Alaska or Siberia.

Oil fields are producing not more than 30% of the oil in place if they are recovered just by using the pressure of the oil field. With increasing oil prices, additional techni-cal measures become profitable as well as very difficult production areas of the world (see Figure I.1-7):

19

• Secondary enhancement injects steam and/or CO2 into the reservoir increas-ing the viscosity of the crude oil in place or maintaining a minimum pressure in the reservoir.

• Tertiary enhancement uses – alternatively or in addition to the secondary en-hancement – surfactants changing the surface tension of the crude oil in nar-row structures of the oil reservoir.

• Finally, drilling and production in very deep parts of the oceans or in very cold climates is making progress and opens up new opportunities with increasing crude oil prices.

At the cost level of deep water production or in the Arctic, enhanced oil recovery (EOR) will become competitive and also unconventional oil from tar sands and oil shales (between 20 and 60 $ per barrel; see Figure I.1-7).

Source: IEA 2005

Figure I.1-7 Production cost of conventional and unconventional oil from different production fields in different regions of the world

To conclude: the depletion mid-point of crude oil production is uncertain, but it is very likely to happen during the period of 2015 to 2030. The decrease of production is expected to be rather slow as unconventional oil as well as secondary and tertiary enhancement will contribute given gradually increasing oil price levels.

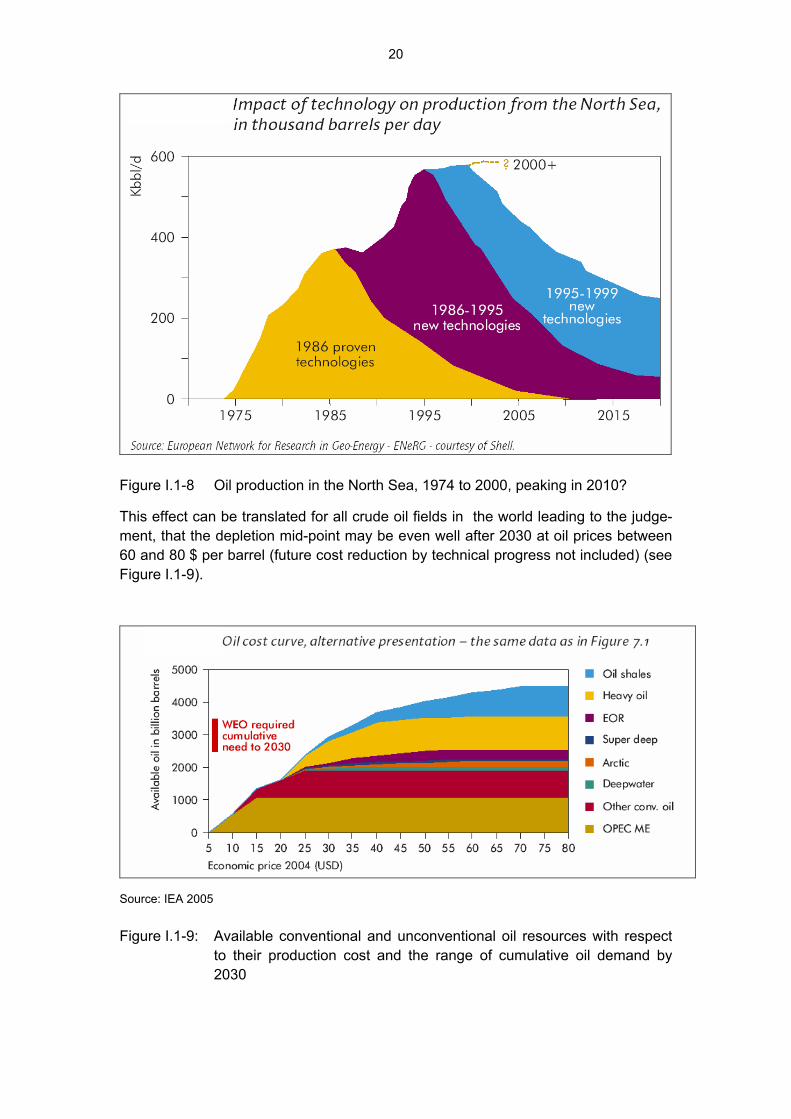

This effect can be observed quite nicely in the case of the North Sea oil recovery, starting with primary technologies in the 1970s and 1980, but new recovery tech-nologies and cost reductions of the enhanced recovery methods contributed to a bet-ter recovery rate of the fields in the North Sea (see Figure I.1-8).

20

Figure I.1-8 Oil production in the North Sea, 1974 to 2000, peaking in 2010?

This effect can be translated for all crude oil fields in the world leading to the judge-ment, that the depletion mid-point may be even well after 2030 at oil prices between 60 and 80 $ per barrel (future cost reduction by technical progress not included) (see Figure I.1-9).

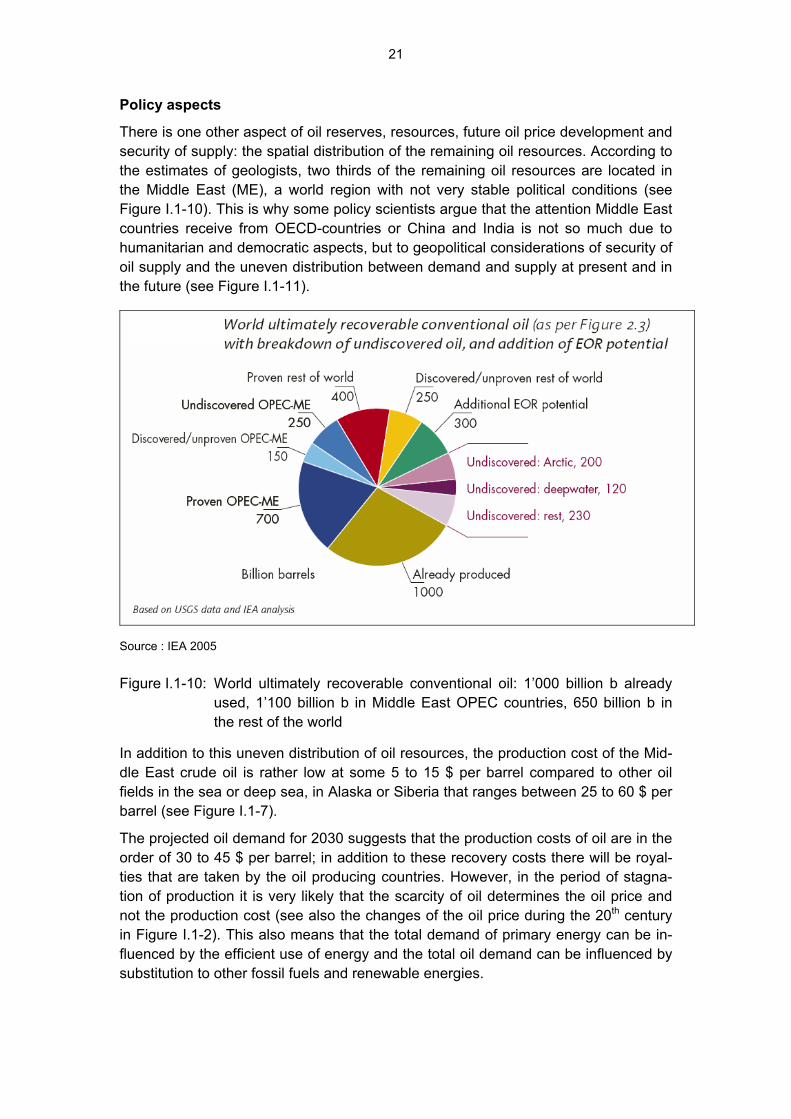

Source: IEA 2005

Figure I.1-9: Available conventional and unconventional oil resources with respect to their production cost and the range of cumulative oil demand by 2030

21

Policy aspects

There is one other aspect of oil reserves, resources, future oil price development and security of supply: the spatial distribution of the remaining oil resources. According to the estimates of geologists, two thirds of the remaining oil resources are located in the Middle East (ME), a world region with not very stable political conditions (see Figure I.1-10). This is why some policy scientists argue that the attention Middle East countries receive from OECD-countries or China and India is not so much due to humanitarian and democratic aspects, but to geopolitical considerations of security of oil supply and the uneven distribution between demand and supply at present and in the future (see Figure I.1-11).

Source : IEA 2005

Figure I.1-10: World ultimately recoverable conventional oil: 1’000 billion b already used, 1’100 billion b in Middle East OPEC countries, 650 billion b in the rest of the world

In addition to this uneven distribution of oil resources, the production cost of the Mid-dle East crude oil is rather low at some 5 to 15 $ per barrel compared to other oil fields in the sea or deep sea, in Alaska or Siberia that ranges between 25 to 60 $ per barrel (see Figure I.1-7).

The projected oil demand for 2030 suggests that the production costs of oil are in the order of 30 to 45 $ per barrel; in addition to these recovery costs there will be royal-ties that are taken by the oil producing countries. However, in the period of stagna-tion of production it is very likely that the scarcity of oil determines the oil price and not the production cost (see also the changes of the oil price during the 20th century in Figure I.1-2). This also means that the total demand of primary energy can be in-fluenced by the efficient use of energy and the total oil demand can be influenced by substitution to other fossil fuels and renewable energies.

22

0

200

400

600

800

1000

Afrika Nord Amerika Süd Amerika Asien Europa Mittlerer Osten Ozeanien

Produktion Verbrauch

Figure I.1-11 The uneven regional distribution of oil production and oil use, in million tons per year

Africa and the Middle East produce an enormous surplus of oil that is absorbed by the industrialised and emerging countries in North America, Europe and Asia (see Figure I.1-11). The patterns of production and consumption of natural gas are similar to those of the oil, the difference being that

• the exploitation started about 50 years later,

• the natural gas is more difficult to transport reflected in not one world market, but in three regional markets (North America, Africa, and Europe/Asia) deter-mined by the transportation by pipelines. This will change in the future by liq-uefied natural gas.

• the ratio of proven reserves to yearly consumption is now 60 years due to the faster increase of gas production that was 2.0 % per year during the last 15 years (oil: 1.3 % per year).

• the distribution of natural gas over the earth is somewhat better than for oil, but not too much as natural gas fields often go with fields of conventional crude oil. The largest resources of natural gas are again in the Middle East, which expects increasing world market shares in oil (see Figure I.1-12) as well as in natural gas some decades later.

23

50

63

16.5

25.929

35

24.1

27.9

39.7

42.5

37.1

49

0

10

20

30

40

50

60

70

1980 1990 2000 2010 2020 2030

Zeit

Prod

uktio

nsan

teil

an d

er

Wel

terd

ölfö

rder

ung

OPEC insgesamt

Naher Osten (OAPEC)

World oil production 1985-2020. Source : CEPE, 2001

world oil proven reserves 2000• Saudi Arabia 25.3% • Iraq 10.8%• Kuwait 9.3%• Arab Emirates 9.2%• Iran 8.7%• Qatar et al. 3.0%• Middle East 66.3%

Middle East

totalSh

are

of o

il p

rodu

ctio

n of

glo

bal p

rodu

ctio

n

time

Figure I.1-12 Re-concentration of oil production in the Near East, owning two thirds of global oil resources

Concluding remarks Looking at the period of industrialised countries in a very long perspective of mankind the use of oil and other fossil fuel will be not more than an episode which was first spelled out by M. King Hubbert in 1949 (see Figure I.1-13).

-10 -8 -6 -4 -2 heute 2 4 6 8 10

20

40

60

80

100

Erd

ölve

rbra

uch

(in b

elie

bige

n E

inhe

iten

Zeitabstand von heute (in Tausenden von Jahren)

0

World oil production and use seen in the geological periods

(according to M. Hubert, 1949: the Hubbert`s pimple)

Time from today (in 1000 years)today

Oil

cons

umpt

ion

(in a

nyun

it)

-10 -8 -6 -4 -2 heute 2 4 6 8 10

20

40

60

80

100

Erd

ölve

rbra

uch

(in b

elie

bige

n E

inhe

iten

Zeitabstand von heute (in Tausenden von Jahren)

0

World oil production and use seen in the geological periods

(according to M. Hubert, 1949: the Hubbert`s pimple)

Time from today (in 1000 years)today

Oil

cons

umpt

ion

(in a

nyun

it)

Figure I.1-13: The peaking of the world use of fossil fuels within a few centuries

24

The conclusions of these considerations are as follows:

• Oil resources will be available for far more than 100 years, so will natural gas and coal. But oil production is likely to peak within the next 30 to 40 years which is critical from the macro economic point of view threatening the eco-nomic development of the emerging and developing countries.

• The critical moment is not the moment of depletion of a non-renewable re-source, but after its depletion mid-point, if shrinking oil product demand is not in line with shrinking oil production; if there is a mismatch, high price in-creases of oil have to be expected.

• The uneven distribution of oil (and of natural gas) resources will give raise to many political tensions in the future, particularly in the Middle East, question-ing continuous economic development and social sustainability at a global level.

• The question of resource availability for future generations is not critical for fossil fuels, but extremely critical from the point of view of CO2 emissions: the critical question is where to dispose the CO2, as even at present emission rates mankind would need three atmospheres to avoid unsustainable climate changes (see Chapt. 1.2).

• Energy price increases in the 1970s demonstrated a stagnation of per capita primary energy demand for at least 15 years. This is a good message when world population stops growing which is expected in the second half of this century.

I.2. Energy Statistics If energy use increasingly becomes an issue of major concern, the measurement of energy use also gains importance. This means that policy makers and companies need solid information on energy use of the various kinds, their conversion efficien-cies and substitution potentials and their cost and prices; but all this implies clear definitions of the energy itself at the national and international level. Some of the en-ergy terms used are likely to be misunderstood due to traditional wording in different communities, branches and disciplines. Generally, a distinction is made at three lev-els:

(1) Primary energy, where two interpretations are possible: - the physical definition: Energy recovered from natural resources, but not con-verted by any succeeding process, i.e. crude oil, hard coal, natural gas, gas from coal mines, lignite, solar energy, wind, hydro power, fire wood, geothermal energy, wave energy, and uranium ores; - the energy economics definition: energy that is produced domestically or im-ported to a country; this can be primary energy in the physical sense or con-verted forms of energy (e.g. oil products like heating oil, gasoline, electricity). Industrial or municipal wastes being burnt in large boilers may also be consid-ered as primary energy as well as methane from landfill, sewage plants or fer-mentation plants.

25

(2) Final Energy any energy that is used by end users such as private households, services, in-dustrial companies, car drivers, trams, or trains mostly sold via markets, Final energy may also be heat generated by solar collectors or wood collected pri-vately in (private or public forests), or bio-ethanol from agricultural crops.

(3) Useful energy this form of energy is energy after the conversion of the final energies, e.g. heat from radiators, power transmitted to the axis of a car, light coming from a bulb, or the information and transformation in electronic devices and appliances.

(4) Energy Service Finally, the obvious purpose of the impact of the useful energy is called the en-ergy service which may be a comfortable room, a cooked meal. a transport from A to B, a ton of steel or cement, a beer bottle or a newspaper.

The mere data on energy use of these different forms on a national level may not be comparable, because most of them are gathered by observing their flow via markets. In rural areas, and particularly in developing countries, however, energies like fire-wood or dung are only partially traded; much is simply collected by the end user.

Having distinguished these three levels of energy use, one can ask about today’s losses of a national or continental energy system (see Figure I.2-1).

Space Heat 52,200

Process Heat 49,800

Other Drives 20,500

Illumination 800

Information, 1500Communication

Motive Power 14,100

Useful Energy of Final Energy Sectors

9,500 PJ non-energetic use

Final energy 294,800 PJ

Primary energy447,150 PJ

Industry 97,000 PJTransportation 79,000 PJPrivate households 79,200 PJTrade, commerce, 39,600 PJEtc.

143,650 PJ

Transformation losses

Energy Services

Heated Rooms(

Industrial Products

Mobility

Automation,Cooling

Illuminated Areas (

PC-, Phone- andInternet Use

in m )

(in tons)

(in Pass.km)

in m )

2

2

Losses for generating useful energy

Useful energy (incl. 7400 PJ distribution losses)

PJ

Sources: OECD 2005, ISI Karlsruhe140,800 154,000 PJ

Plastics,Asphalt

32.1%31.5% 34.5%

Figure I.2-1 Energy Flow Diagram for the World 2003

Energy losses can be distinguished on four levels, three of them are energy losses and the fourth is inefficient use of energy-intensive materials and too heavy moving parts and vehicles:

• Today, more than 440’000 PJ per year of global primary energy demand de-liver almost 300’000 PJ of final energy to customers, resulting in a loss of al-most 145'000 PJ for power generation, refineries, coke making and losses for

26

distribution and transmission. The largest losses stem from thermal power plants with efficiencies around 30 to 40%.

• The conversion of final energy to useful energy in boilers, engines, electrical motors, furnaces, kilns, and bulbs or computers generate losses of 155'000 PJ. The poorest efficiencies being in road transportation between 20 and 30% (and bulbs with 5 to 10 %). Thus, 250’000 PJ or two-thirds of primary energy demand is presently lost in energy conversion, mostly as low- and medium-temperature heat (UNDP/WEC/UNDESA, 2000). The conversion efficiencies of the Swiss transformation sector are somewhat better due to high shares of hydropower.

• The losses at the useful energy level sum up to 140'000 PJ, again almost one third of the primary energy. High losses are in the buildings sector and indus-trial process heat. These energy losses that are scarcely mentioned (pres-ently almost 39% of the Swiss primary energy demand) could be substantially reduced or even avoided through such technologies as low-energy buildings, membrane techniques or biotechnology processes instead of thermal proc-esses, and lighter vehicles or re-use of waste heat.

• The last level is reducing the demand of useful energy by avoiding large de-mand of energy-intensive materials such as steel, aluminium, paper, plastics, copper, glass etc. In addition to this material efficiency by better construction, improved material properties and recycling there are further options such as substitution of these materials by biomass based materials (wood, starch, natural fibres) or by pooling of products and machines which are not very much operated by a single owner, such as harvest and construction machines (renting) or cars and light trucks (car sharing). This potential of indirect energy efficiency is about 0.5 % per year or 2'200 PJ per year globally (or twice the present primary energy demand of Switzerland).

Energy conversion coefficients

Energy use and losses are measured in very different scales what has to be under-stood by historical reasons. The English system (including the USA and the Com-monwealth) developed differently from metering systems at the European continent in the 19th and 20th century. In addition, special sectors like the oil or coal sector developed its own measuring systems such as Mtoe (million tonnes of oil equivalent), barrels, or Mtoe (million tonnes of coal equivalent). Although, presently accepted en-ergy measures are only Joules and kWh by international convention, the traditional systems still prevail in many countries and even international institutions such as the International Energy Agency (IEA) or the European Statistical Office (Eurostat). Therefore, some conversion factors are mentioned here to facilitate reading interna-tional and national energy statistics (see Table I.2-1).

The typical energy flow in energy statistics has the opposite direction as shown in Figure I.2-2, because the traditional energy economics perspective starts from supply and not from the energy demand-inducing drivers of an economy or private house-holds.

27

Table I.2-1 Energy statistics – energy conversion factors

Unit Conversion to joules (multiply by …)

Remarks

calorie (cal) 4.1868 Old unit for quantities of heat

ton-of-oil-equivalent (toe) 41.868 · 109 Defined as 107 kcal. The toe is widely used in international energy statistics

barrel-of-oil-equivalent (boe)

approx. 6.1 · 109 Conversion values range from 6.06 to 6.12 · 109

ton-of-coal-equivalent (tce)

28.6 · 109 Used as the main unit of energy in China

kilowatt-hour (kWh) 3.6 · 106 Used mainly for electricity

British-thermal-unit (BTU) 1.055 · 103 Used in the USA: other units include the therm (105 BTU) and the quad (1015 BTU)

watt-year (Wyr) 31.5· 106 Useful unit for analytical applica-tions: if one uses 1 W on average, one uses 1 Wyr in a year

Source: Gesamtenergiestatistik der Schweiz 2005 (Joint Energy Statistic of Switzerland)

28

Figure I.2-2 Energy Flow Diagram of Switzerland 2005

Energy consumption data of countries or other entities vary from year to year be-cause of several reasons:

• Changes in activity levels (number of people, number of households, electri-cal appliances, or cars, person kilometers, ton kilometers, number of jobs, tons of steel). These influences can be considered by defining specific energy demand which takes the change of drivers into account.

• Change of yearly weather fluctuations (cold/warm winter; moderate/hot sum-mer) has to be adjusted by heating degree days and cooling degree days. Heating degree days: are number of days below 12°C multiplied by the differ-ence between 12°C and the average temperature of those days (Switzerland: 3600; France: 2300; Scandinavia 4400 to 6000 heating degree days). The correction of the final energy which is used for heating is corrected by the fol-lowing formula:

Final Energyheating, I, corr = Final energyheating, i . HDDav30 / HDDi

where HDDav30 is the 30 years average heating degree day figure and

HDDi the actual heating degree day figure

The same correction is made for electricity demand regarding cooling degree days which is more important in warm climates. The cooling degree days above 25°C are about 80 for Zurich, 300 for Milano, and more than 1000 for subtropical and tropical regions. They may gain more importance in the next decades due to the greenhouse effect of climate change.

Weather can influence primary energy by 1 to 2%

• Short term fluctuations of industrial structures (particularly during the phases of the business cycles in industry sectors by different growth of the energy-intensive basic goods industries). In the take off period manufacturing indus-tries order more steel and other energy-intensive basic material than in the down swing period when it is unclear how much market demand will shrink. The business cycle can influence primary energy by 0.5 %

Often used energy indicators

In order to characterise the level energy use or the performance in efficiency terms, energy statistics use typical energy indicators such as the following often applied ones:

1. Primary energy intensity is defined as the relation of primary energy use per unit of GDP (which can be expressed for international comparison in exchange rates

29

or purchasing power parity (Switzerland: 3.140 GJ/CHF2004)). (See also the dy-namics of energy intensities for various countries in Figure I.2-3).

2. Final energy intensity is defined as the relation of final energy use per unit of GDP. (Switzerland: 730 GJ/CHF2004).

3. Per capita primary energy use. (Switzerland: 160 GJ/capita).

4. Per capita final energy use. (Switzerland: 117 GJ/capita).

5. Share of imported primary energy (import dependence is defined as the sum of domestically produced primary energy (e.g. natural gas, coal, oil, hydro, refuse, wood, solar, wind) relative to primary energy demand of a country): Switzerland: 54 %

Ener

gy in

tens

ity [M

J/D

M '8

5 G

DP]

1860 1900 1950 2000 2050

China

Great Britain

Germany

France

Japan

FormerSoviet Union

India

Eastern Europe

35

15

20

25

30

0

5

10

Expected trend developmentDevelopment for high capitaland technology transfer

Countries withstate trade

Germany referenceGermany CO2-reduction of 80%

Time

Source: Chandler et al., 1990; CEC, 1996; calculations (with monetary parity) by ISI, 1997

Figure I.2-3 Development of the primary energy intensities of different countries, 1860-2050

Primary energy Intensities of countries

The dynamics of energy intensities of countries have quite typical patterns (see Figure I.2-3):

• With increasing industrialization, motorization, and automation (including pri-vate households) energy intensity increases, before it passes a maximum, and is reduced by increasing shares of GDP contributed by the service sec-tors.

• The decline of energy intensity is caused by several effects: the growth of the service sector and saturation in building up the basic capital stock and infra-structure of a country. In addition, there may be saturation in energy intensive consumer goods such as electric appliances and cars.

30

• The maximum of energy intensity of a proceeding industrializing country is not reached by a later industrializing country due to know-how and technology transfer.

• Energy intensities of OECD countries declined by 0.5 to 1.8 % per year during the last 15 years, while former centrally planned economies reduced their en-ergy intensities between 3.6 % (Russia since 1995) and 6% annually (China).

• The relatively high primary energy intensities of countries in economic transi-tion in the 1980s and thereafter are due to two facts: (1) The Gross Domestic Product (GDP) values are expressed in Market Exchange Rates (MER) which underestimate the standard of living and the related energy services (2) The former centrally planned economies considered energy as public good and energy use was either without any cost or at very low subsidised levels lead-ing to very wasteful investments and behaviour in energy use.

Converting national currencies into one common currency

There are some notable differences when converting national currencies to one cur-rency such as US$ or Euros by Market Exchange Rates (MER) or Purchasing Power Parities (PPP). However, the differences may not be over-estimated when investigat-ing income effects between countries with similar standards of living. If the under-standing of the global economy comes from a conceptualization and modeling at the level of individual economies, subject to common influences (oil prices, information, FDI, US interest rates, US$-yen, US$-Euro etc exchange rates) then it is clear that:

• each country's development is partly based on engaging with international trade, so that its citizens' purchasing power is partly based on what they can purchase from abroad (using MER exchange rates) and partly based on do-mestic incomes and prices, and therefore partly based on PPP-type prices;

• in comparing countries, MERs can be very misleading because (a) they re-flect temporary factors irrelevant to purchasing power, such as speculation, and (b) the MER's do not provide a good indication of the level or growth rates for the mix of products bought by the lower income, usually rural, households. (There are many issues here, e.g. the rural households may rely on non-marketed traditional agricultural products, and these will not be in MER, and may be badly covered by PPP.)

• In comparing countries, PPP becomes increasingly irrelevant as people in-creasingly satisfy their basic needs; after a certain threshold, the happiness literature shows convincingly that higher incomes do not bring much more happiness; since the PPP/MER debate is about welfare, this implies that GDP per head on a PPP basis is less relevant at higher income levels than GDP per head on a MER basis, since the MER-GDP allows spending to be valued at world prices.

31

I.3. Ecological Economics and the concept of sustainable development

Neoclassical economics consider the natural resources as rather independent for the economic system (see Figure I.3-2). The resources taken out from the earth are only priced with production cost at the margin, and sometimes by royalties representing the fact that some capital has to be gained. This is needed to substitute the use of natural resources by capital investments (more efficient use, substitution by another resource, and another source of income for the producing country; see Dubai in con-trast to many other oil producing countries such as Nigeria, Algeria, Venezuela).

The release of wastes or rest emissions into the environment has generally no price (e.g. rest of water pollution such as salts, non-degradable chemicals, hormones; rest of air emissions: release of greenhouse gases, NOx, SO2, small particles).

Ecological economics try to assess the economic value of those streams of masses (see Figure I.3-1) taken out of the earth or deposited back into the environment by estimating the cost for substituting the non-renewable natural resource, the external cost of emissions, or by using the cost for avoiding the emissions as shadow prices.

Market forproductioninputs, e.g.

labour, capital

Marketfor goods

and services

Money

Goodse.g.

labo

ur

e.g. salaries, wages

e.g. subsidies

e.g. taxes

e.g. social securitybenefits

e.g. taxes

Companies

Public authorityat federal,

regional andlocal level

PrivateHouseholds

Natural resources

Natural environment Natural

environment

foreign producers foreign consumers

Market forproductioninputs, e.g.

labour, capital

Marketfor goods

and services

Money

Goodse.g.

labo

ur

e.g. salaries, wages

e.g. subsidies

e.g. taxes

e.g. social securitybenefits

e.g. taxes

Companies

Public authorityat federal,

regional andlocal level

PrivateHouseholds

Natural resources

Natural environment Natural

environment

foreign producers foreign consumers

Figure I.3-1 Cycle of money and goods in an economy – a simplified circular model

Economics of natural resources

Non-renewable resources recovered by mankind will gradually shrink and will have to be substituted by some other natural resource. The use of a non-renewable natural

32

resource may be substituted by a more intelligent use of it (efficiency strategy) using additional capital (and/or labour and know-how). Or it may be substituted by another material that however will undergo the same path of scarcity as long as it is a non-renewable natural resource.

When these substitution processes occur, the rule of Hoteling says that the price of the scarce resource (e.g. crude oil) increases by the interest rate of public institutions which is around 3% per year. This may not be reached in reality in many cases as the technological progress reduces the recovery cost in the order of 1% annually.

Given this situation of scarcity of non-renewable natural resources, there are two possibilities to handle the problem:

• the search for a renewable natural resource, or

• the substitution of natural resources by capital and know-how to ever improv-ing efficiencies.

The only available renewable natural resource – the back stop technology

The sun is the only “renewable resource” (for a longer period of some thousands or even billion years, see Figure I.3-2). The sun delivers in its direct or indirect forms (wind, hydro, wave power, bio-mass) the only natural resource on which mankind can draw upon for millions of years in the future. The energy amount of the sun's radia-tion falling onto the earth is many times higher than the present global primary en-ergy demand. the question is more how to collect this supply of abundant energy in an economic way, i.e., without applying too much resources of capital and labour.

Economy

GeologyClimate

Flora Fauna

Sun

Purification of solar radiation(P. Kesselring)

- 6Efficiency factor

„Bread“: Hydropower 10„Wine“: Carbon cycle Biomass 10- 3

„Cognac“: Biomass Hydrocarbon 10- 8

GeologyClimate

Flora Fauna

Climate and mountains

EconomyEconomy

GeologyClimate

Flora Fauna

GeologyClimate

Flora Fauna

SunSun

Purification of solar radiation(P. Kesselring)

- 6Efficiency factor

„Bread“: Hydropower 10„Wine“: Carbon cycle Biomass 10- 3

„Cognac“: Biomass Hydrocarbon 10- 8

GeologyClimate

Flora Fauna

GeologyClimate

Flora Fauna

Climate and mountains

Figure I.3-2 Ecological Economics – in contrast to neoclassical economics ecologi-cal economics are considering the economy as part of the natural en-vironment

The efficiencies of solar radiation are low (between 0.1% to 10-8; see Figure I.3-2), but the production cost of these forms of primary energy are either zero or ranging in cost categories similar to those of non-renewable energy uses. As the conversion of

33

non-renewable fossil energy use was very convenient in the past and related conver-sion technologies quite advanced and cheap, the new technologies of converting direct and indirect forms of solar energy into final energies are often quite costly. However, those renewable energy technologies with some decades of experience have experienced quite substantial cost reductions due to learning and economies of scale (see Figure I.3-3).

Figure I.3-3 Development of cost of electricity generation of photovoltaics, wind energy, solar thermal power plants, and electricity from bio mass as function of yearly power generation in relation to constant electricity generation costs of conventional power plants (at present and in the future with carbon capture and storage (CCS).

The starting values of the cost ranges refer to the present global electricity genera-tion by these technologies (except conventional thermal power generation at the ba-sis (see Figure I.3-3). The ends for wind and biomass may be overstated and may end at the 100% line. The decline of the generation cost results from the observed experience curves that include learning and economies of scale effects (e.g. Photo-poltaics: -20% cost reduction for each doubling of generation; biomass between -5 % and -15 % as a range of uncertainty). The percentages reflect the share of today’s electricity demand.

The new renewable energies can also be considered as "back stop" technologies as they limit the application of fossil fuels in the next decades if fossil fuels, particularly oil, experience rising production cost (tertiary recovery, see Chapt. I.1) and rising prices and politically uncertain availability of the crude oil in the Middle East where two thirds of the remaining resources are located (see Figure I.3-4). On the other

34

hand, it is expected that renewable energies have declining prices and production cost (see above). As fossil fuels have high external cost (see below) these costs have either to be internalised or renewables should have some financial incentives to level the economic playing field of the technologies and also the option of more effi-cient energy use.

There are many forms of renewable energies (see Figure I.3-5) such as the direct forms of thermal and photovoltaic solar use or many indirect forms such as hydro power, wind power, various applications of biomass such as wood, fermentation of biomass, and other forms such as wave power. Geothermal energy is a further form of "almost" renewable energy.

50

63

16.5

25.929

35

24.1

27.9

39.7

42.5

37.1

49

0

10

20

30

40

50

60

70

1980 1990 2000 2010 2020 2030

Zeit

Prod

uktio

nsan

teil

an d

er

Wel

terd

ölfö

rder

ung

OPEC insgesamt

Naher Osten (OAPEC)

World oil production 1985-2020. Source : CEPE, 2001

world oil proven reserves 2000• Saudi Arabia 25.3% • Iraq 10.8%• Kuwait 9.3%• Arab Emirates 9.2%• Iran 8.7%• Qatar et al. 3.0%• Middle East 66.3%

Middle East

total

Shar

e of

oil

pro

duct

ion

of g

loba

l pro

duct

ion

time

Figure I.3-4 Re-concentration of oil production in the Middle East, owning two thirds of global oil resources and proven reserves

35

wood

rain

Solar radiation

CoalOil

Natural gasWood

HydropowerWave energy--Wind

Sun

climate system

substancesorganic

mill. of years wood

rain

Solar radiation

CoalOil

Natural gasWood

HydropowerWave energy--Wind

Sun

climate system

substancesorganic

mill. of years

Figure I.3-5 The sun as the most important energy source for the future and its different forms of direct and indirect solar energy

The unsustainable use of fossil energies today

In addition to conventional emissions, which have been in the focus of environmental policy in the 1960s to 1980s in industrialised countries and still are of major impor-tance in emerging countries and mega cities in developing countries, the CO2 emis-sions from fossil energies gained major attention during the last 20 years (Toronto Conference in 1987).

While the traditional emissions get washed out by the next rain or snow, the CO2

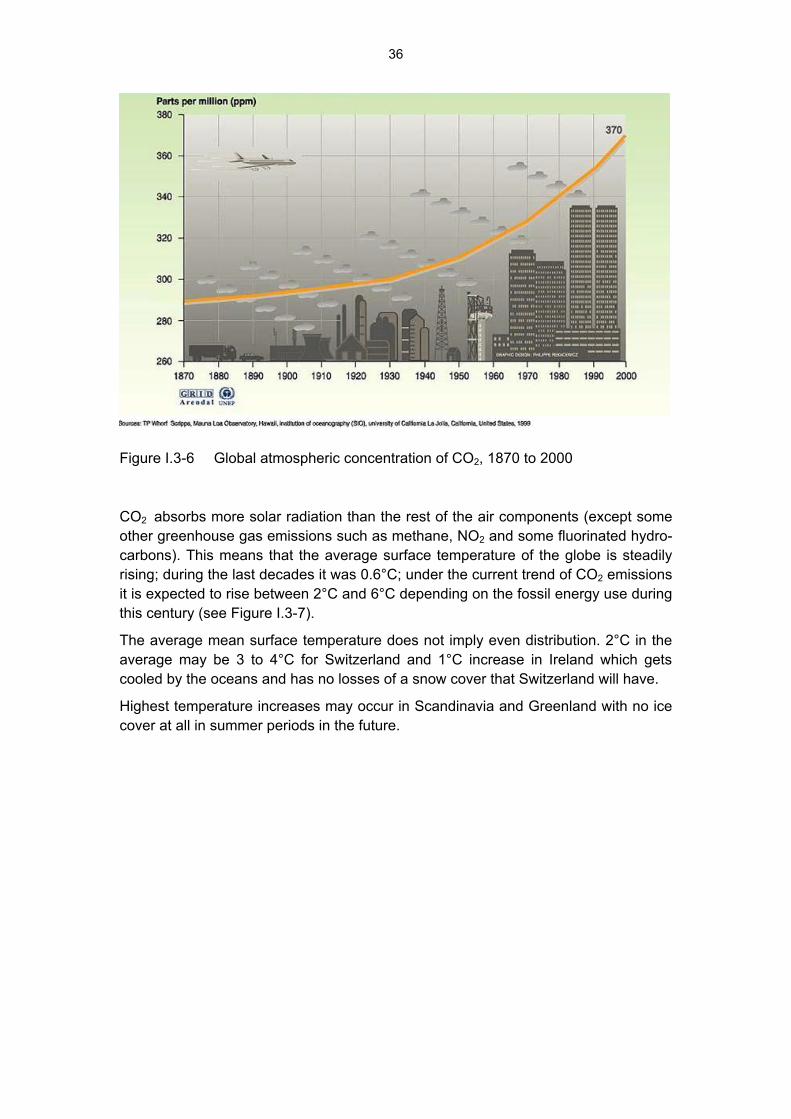

emissions remain for several hundred years in the atmosphere, before most of them gets absorbed by the oceans covering about 90% of the earth’s surface. As the life time of CO2 is so long and the emissions so high atmospheric concentration has in-creased since 1880 by 40 % from 270 ppm to 384 ppm in 2006 (see Figure I.3-6)

36

Figure I.3-6 Global atmospheric concentration of CO2, 1870 to 2000

CO2 absorbs more solar radiation than the rest of the air components (except some other greenhouse gas emissions such as methane, NO2 and some fluorinated hydro-carbons). This means that the average surface temperature of the globe is steadily rising; during the last decades it was 0.6°C; under the current trend of CO2 emissions it is expected to rise between 2°C and 6°C depending on the fossil energy use during this century (see Figure I.3-7).

The average mean surface temperature does not imply even distribution. 2°C in the average may be 3 to 4°C for Switzerland and 1°C increase in Ireland which gets cooled by the oceans and has no losses of a snow cover that Switzerland will have.

Highest temperature increases may occur in Scandinavia and Greenland with no ice cover at all in summer periods in the future.

37

High :18400 EJ conventional oil, 13000 EJ natural

gas, phase out nuclear by 2075

Constant aerosol concentrations beyond 1990 and high climate sensitivity of 4.5 °C

Low :8000 EJ conventional oil, 7900 EJ natural gas,

nuclear costs decline by 0.4% annualy

Constant aerosol concentrations beyond 1990 and high climate sensitivity of 1.5 °C

The 2 middle curves :12000 EJ conventional oil, 13000 EJ natural

gas, solar costs fall to 0.075$/kWh, 191 EJ ofbiofuels available at 70$/barrel

Upper curve : Constant aerosol concentrations beyond 1990 and climate sensitivity of 2.5 °C

Lower curve : changes in aerosolconcentration beyond 1990 and climatesensitivity of 2°C

Figure I.3-7: Temperature increase of mean surface temperature, global average

Sea level rise commitment : thermal expansion and land ice melt over 900 yearsafter an initial 1% increase in CO2 for 70 years, source IPCC, 1995

Figure I.3-8: Sea level rise due to thermal expansion and melting ice over 900 years

38

Figure I.3-9 Impacts of climate change on various fields of nature, economy and society

I.4. The concept of sustainable development

Definition

The concept of sustainable development has appeared as an answer to the major risks generated by the deterioration of the environment quality which has risen from pollution and harmful effects with a heavy influence on climatic changes and losses of biodiversity. But it also took into consideration the uneven distribution of wealth and resource use among the industrialised and developing countries.

The concept, in its current acceptance, has spread over time since the beginning of the seventies. Its course is marked out by a gradual awakening through several is-sues among which:

• the OPEC petroleum crisis in 1973 and again in 1979/80,

• the discovery of the Antarctic ozone hole in 85 or,

• the accident of the nuclear power plant of Chernobyl in 86,

and important contributions from studies like:

39

• the report of the “Club de Rome” in 1971 which has highlighted the threat of natural resources exhaustion by an extrapolation of the economic growth over one century, or,

• “Stratégie mondiale de la conservation”1 in 1980 in which the term of sustain-able development has been used for the first time.

Various definitions followed one another until the consensus introduced by the Brundtland UN-Commission Report in 1987 whose work was confirmed in a formal way by the Conference of the United Nations for the environment and the develop-ment held in Rio de Janeiro in 1992.

The adopted general definition presents the sustainable development as a develop-ment "which meets the current needs without compromising the capacity of the future generations to satisfy their own needs". It delimits sustainable develop-ment as the intersection of three spheres by postulating that a development cannot be viable unless reconciling the three undissociable social, economic and ecological aspects.

sustainable

Figure I.4-1: Principle of sustainable development – as an accepted equilibrium of societal, economic, and environmental concerns of today and in the long term future

However, this consensus lies between two opposite visions of sustainable develop-ment, which are the strong and weak visions (see also Figure I.4-1).

Weak vision of Sustainable Development (from the view of economics)

The soft vision is an ecologist and natural science position which considers that eco-nomic and social development would not be effectively sustainable unless making the environmental issues as a priority and accepting laws of natural sciences such as the second law of thermodynamics. This point of view is based on:

1 UICN (Union Internationale sur la Conservation de la Nature), Gland, Suisse.

Social Economic

Environment

Sustainable Bearable Viable

Fair

40

• The fact that the capacities of the ecological system are not extensible; in par-ticular, the second law of thermodynamics says that for each energy use there is a loss of energy in the form of exergy; this means that capital cannot entirely substitute the use of energy, and energy will always be needed e.g. by using some forms of the solar radiation on earth.

• The irremediable character of the deterioration of the environment (more than the social issues) such as extinction of species, halt of the Gulf Stream.

• And the principle of precaution (without including any considerations for the development of future technologies); it is unclear when sudden changes in the biosphere occur which would accelerate climate change (e.g. fast death of boreal forests that new Southerly forests could grow).

This approach deals with the decision making process in a hierarchical way by con-sidering the environmental aspects or issues first as the principal criteria for the evaluation of a project. In general, the partisans of the strong vision militate for a radical change of the society.

Discipline Principle Limits

Environmental scientist Carrying capacity Definite / unalterable

Strong sustainability Limits of substitutability Economist

Week sustainability substitutability of different capital

Manager / World Business Council

Eco-efficiency / Product stewardship

No limits to carrying capacity

Many engineers More efficient is better Often only physical limits

Figure I.4-2 Different interpretations and visions of sustainability by various disci-plines and professional communities

Strong concept of Sustainable Development (from the economic perspective)

The strong concept corresponds to an economist approach, which argues that "the natural capital which is threatened by exhaustion is entirely substitutable over time by technological progress and financial capital" (see Figure I.4-4). The priority here is thus given to the economic aspects while considering that the environment (and so-cial) protection must be based on a strong economy that can cope with all resource and social problems.

These two opposite perceptions are also reflected, to a certain extent, on the level of the development policies of the industrialized countries, the countries in economic transition, and the emerging and developing countries (Figure III.4-3). The first will tend to give a relatively higher importance to the environmental and social aspects while the others are likely to focus on the economic aspects of their development. Of course, the perceptions of countries, politicians, and scientists will change over time.

41

Environmental Economic

Social

OECD countries

Transition-economies

Developing countries

Figure I.4-3 Social, environmental and economic aspects of development policies objectives of industrialised, transition-economies and developing coun-tries

energyuse combination at low energy prices and

present technology

combination at high energy prices and present technology

combination at high energyprices and future tehnology

present technology options

future technology options

needed capitalM:\CEPE Zürich\Vorlesung\Lausanne\SS-2004\Folien\Vorlesung 4\Vorlesung 4.ppt

Figure I.4-4 Substitution between capital and the use of natural resources

The relation between the use of natural resources and of capital can be considered in a wide range as a substitution relation: the more capital in the efficient use of a natu-ral resource is invested the less of this resource is needed (see Figure I.4-4). Tech-nological progress opens up new opportunities of efficient use of natural resources over time. However, there are the limitations from natural sciences.

There may also be limitations of social acceptability regarding differences of the use of natural resources and economic well being which may limit capital accumulation in the North of the globe (see Figure I.4-5). There may be even limits of social differen-tiation in a country given the fact that the energy use per capita in one country (like Russia 4 kW/cap and 23 kW/cap for the last and first 10% of the population) can dif-fer more than a factor of 5 (see Figure I.4-6).

42

2

2000 2050 2100

4

6

Anteil fossile Energieträger ~90%

Anteil fossile Energieträger < 30

kW/capita

Untere (Armuts-) Grenze ~ konst. (Ansprüche steigen, Wirkungsgarde auch

Trotz abnehmendem Anteil an fossilen Brennstoffen wird die, aufgrund von Klima-Modellrechnungen bestimmte, obere (ökologische) Grenze immer enger.

Figure I.4-5 Energy demand per capita and limits of social acceptability of the poor

Figure I.4-6 Energy use per capita in different countries and class of population

43

II. Drivers of Energy Demand

II.1. The energy flow diagram – starting at the energy ser-vices