endeavour mining management presentation 2014... · gold producer west africa cash flow endeavour...

TRANSCRIPT

GOLD PRODUCER WEST AFRICA CASH FLOW

Endeavour Mining

Management Presentation

September 2014

Disclaimer & Forward Looking Statements

GOLD PRODUCER WEST AFRICA CASH FLOW 2

This presentation contains “forward-looking statements” including

but not limited to, statements with respect to Endeavour’s plans

and operating performance, the estimation of mineral reserves

and resources, the timing and amount of estimated future

production, costs of future production, future capital expenditures,

and the success of exploration activities. Generally, these

forward-looking statements can be identified by the use of

forward-looking terminology such as “expects”, “expected”,

“budgeted”, “forecasts” and “anticipates”. Forward-looking

statements, while based on management’s best estimates and

assumptions, are subject to risks and uncertainties that may

cause actual results to be materially different from those

expressed or implied by such forward-looking statements,

including but not limited to: risks related to the successful

integration of acquisitions; risks related

to international operations; risks related to general economic

conditions and credit availability, actual results of current exploration

activities, unanticipated reclamation expenses; changes in project

parameters as plans continue to be refined; fluctuations in prices

of metals including gold; fluctuations in foreign currency exchange

rates, increases in market prices of mining consumables, possible

variations in ore reserves, grade or recovery rates; failure of

plant, equipment or processes to operate as anticipated;

accidents, labour disputes, title disputes, claims and limitations on

insurance coverage and other risks of the mining industry; delays

in the completion of development or construction activities,

changes in national and local government regulation of mining

operations, tax rules and regulations, and political and economic

developments in countries in which Endeavour operates.

Although Endeavour has attempted to identify important factors

that could cause actual results to differ materially from those

contained in forward-looking statements, there may be other

factors that cause results not to be as anticipated, estimated or

intended. There can be no assurance that such statements will

prove to be accurate, as actual results and future events could

differ materially from those anticipated in such statements.

Accordingly, readers should not place undue reliance on forward-

looking statements. Please refer to Endeavour’s most recent

Annual Information Form filed under its profile at www.sedar.com

for further information respecting the risks affecting Endeavour

and its business.

GOLD PRODUCER WEST AFRICA CASH FLOW 3

Endeavour Today

• A West African gold producer operating four mines

– 2014 Production 450,000 oz pa

– 2014 EBITDA $150 million pa

– AISC $1,000 per oz

• 180,000 oz pa Houndé

– Preconstruction development continues

– Mining permit is expected Q4 2014

– Construction decision will be based on

maximizing shareholder value, gold price and

finance

• Group exploration is focused on Houndé and

extending current mine lives

GOLD PRODUCER WEST AFRICA CASH FLOW 4

West African Projects

Mali

Cote d’Ivoire

Burkina Faso

Ghana

• Multiple operations

– Open-pit and underground

– Contract and owner mining

– Gravity/CIL plants

• Operations management based in Accra

GOLD PRODUCER WEST AFRICA CASH FLOW 5

Historic and Potential Growth

Gold

Production

(ozs)

0 80,000 180,000 300,000 325,000 ~450,000 ~500,000/yr plus Houndé

2009 2010 2011 2012 2013 2014e 2015e 2016e 2017e

Potential for Houndé production in Q4 2016 or early 2017

80,000 ozs

+680,000 ozs

Youga

Nzema

Tabakoto

Agbaou

Houndé

GOLD PRODUCER WEST AFRICA CASH FLOW 6

Tabakoto Underground Mining

• Production and cost guidance

– Based on H1, expect to be at top end of production

guidance for 2014

– Within AISC cost guidance

• Agbaou ahead of expectations

– Construction completed ahead of schedule and

under budget

– Performing better than plan

• Tabakoto on track

– Tabakoto underground mine converted to owner

mining in Q2

– Segala underground mine commenced production

in Q2 and is ramping up to full production in H2

– Continuing optimization of operations expected to

be complete by end Q4

– Kofi road being built to provide an attractive third

source of ore in 2015

2014 Achievements

Gold Bar at Tabakoto

GOLD PRODUCER WEST AFRICA CASH FLOW 7

Agbaou – A Success Story

• Full commercial production started January 2014

• Demonstrating strong, sustained performance

− Produced 56,000 ozs in H1

− Cash cost of $638/oz1

− Strong cash flow generator

• Potential to produce over 120,000 ozs in 2014

• Resource definition program commenced to extend

mine life

– Three high priority targets currently being drilled

– Potential extensions of West Pit

Mining on North Pit of Agbaou

Truck Fleet at Agbaou

1 Based on 57,519 ozs sold

GOLD PRODUCER WEST AFRICA CASH FLOW 8

Tabakoto Mine Optimization Nears Completion

• AISC reductions and improved cash flow are being achieved by

– Q2 completion of conversion to owner mining at Tabakoto underground mine

– Q2 start of production from Segala underground mine

• Additional improvements are being implemented in H2

– Ramp up to full production from Segala

– Tailings expansion, cemented rockfill plant

– Processing improvements - pebble crusher and gold room improvements

– Closing Djambave open pit

– Rationalization of sub-contractors

– Road construction through Kofi deposits to Kofi C

• Production is transitioning to sources of cheaper higher grade ore

H2 2014

o Tabakoto Underground

o Segala Underground

o Djambaye Open Pit

2015

o Tabakoto Underground

o Segala Underground

o Kofi C Open Pit

H1 2014

o Tabakoto Underground

o Stockpiles

o Djambaye Open Pit

GOLD PRODUCER WEST AFRICA CASH FLOW 9

Kofi Mine Permit Received

• Mining permit received in H1 covers all

8 Kofi deposits

• Exploration continues to add to current

Indicated 0.6 million ozs plus Inferred 0.6

million ozs

• 38 km haul road to Kofi C now under

construction and due for completion by

December 2014

• Kofi C production will start at the beginning

of 2015 and other Kofi deposits along road

will be added later

• Kofi C open pit reserve grade of 4.13 g/t is

an attractive third source of ore to the

Tabakoto mill

Kofi Property

1 See Appendix for details on Tabakoto-Kofi Resources and Reserves

GOLD PRODUCER WEST AFRICA CASH FLOW 10

2014 AISC Guidance

All-in sustaining cost 2014 (AISC) guidance notes

a) Royalties: Approximately 5% to 6% of assumed $1,250 gold price

b) Corporate G&A: 2014 $/oz range based on $17 million budget, or approximately 3% of gold sales

c) Sustaining capital of approximately $50 million is inclusive of $27 million for underground development at Tabakoto and at Segala from mid-year following

commercial ore stoping and $16 million at Nzema for waste capitalization, TSF lift, deprivation of land use, and other sustaining capital investments

2014 Guidance, in $/oz Mid-2014 Guidance, in $Million

Gold Production Range (ozs) 400,000 - 440,000 420,000

$/oz $Million

Revenue (at $1,250) $525

Royalties $60 - $70 Royalties 27

Cash costs $775 - $825 Cash costs 336

Corporate G&A $40 - $45 Corporate G&A 17

"EBITDA" margin 145

Sustaining capital $110 - $130 Sustaining capital 50

AISC per ounce $985 - $1,070 AISC Margin $95

• Q2 2014 AISC of $1,021/oz was approximately 10% below Q1 2013

GOLD PRODUCER WEST AFRICA CASH FLOW 11

Developing the Houndé Project

• Feasibility study completed in 2013

– 2P Reserve1 of 25 million tonnes

at 1.95 g/t containing 1.55 million ozs

– 3.0 Mtpa SAG/Ball mill and Gravity/CIL

– 180,000 ozs per year over 8 years

– AISC/oz of less than $800/oz

– Upfront capital of $315M including

owner mining fleet

– IRR 22.4% at $1,300/oz (post tax)

• Permitting progress continues

– ESIA permit received in August

– Mining permit expected by year end

• Construction Service Team is now

reviewing and optimizing based on

recent Agbaou construction

experience

Houndé FS General Site Layout

Mine, Waste Dumps, and Plant Location

1 See Appendix for details on Houndé Reserves

GOLD PRODUCER WEST AFRICA CASH FLOW 12

Houndé Exploration Continues

Houndé Property Targets and Trends

• Exploration expected to

further improve the project

economics

• Targets include

– Parallel trends close to the

Vindaloo deposits

– Douhoun, Grand Espoir,

Bouéré and Kari Pomp to

the northwest

– Kopoi to the northeast

– Vindaloo Far South, Soukou

and Kari Sud zones to the

south

Pushing top end of 2014 production guidance

• Achieved record H1 production of 228,000 ozs

• Q2 2014 production was 16% increase in ounces

Continued reductions in AISC

• 4% reduction in AISC/oz as compared to Q1

• Benefiting from cost reduction program, Tabakoto mill

expansion and from low-AISC cost of newly

constructed Agbaou mine

• Segala commenced production in June and is ramping

up to full production later in H2 2014

Focus is on effectively managing our 4 mines

A Houndé production decision will be taken at the

appropriate time

Endeavour is an excellent value proposition for

gold investors

13GOLD PRODUCER WEST AFRICA CASH FLOW

Summary

Appendices

GOLD PRODUCER WEST AFRICA CASH FLOW 14

• Board of Directors

• Management

• Company Profile

• Operations

• Q2 2014 Cash Cost Detail by Mine

• Resources and Reserves

GOLD PRODUCER WEST AFRICA CASH FLOW 15

Board of Directors

Michael Beckett, Chairman

Former Chairman, Ashanti

Goldfields and former MD,

Consolidated Gold Fields

Ian Cockerill

Extensive African mining

experience, Former CEO, Gold

Fields

Frank Giustra

Founder: Wheaton River, Silver

Wheaton and Pacific Rubiales;

Former CEO, Yorkton Securities

Ian Henderson

Former Managing Director and

natural resources fund manager,

JP Morgan

Wayne McManus

Accounting professor: CPA, CFA,

LLM in taxation

Miguel Rodriguez

Former President Venezuela

Central Bank; former Governor

of IMF, World Bank and IADB

Neil Woodyer, CEO

Founded Endeavour in 1988;

former mining banker/advisor

GOLD PRODUCER WEST AFRICA CASH FLOW 16

Management

Christian MilauCFO

• CA and US Certified Public

Accountant

• 18 years experience, previously

treasurer of New Gold Inc

Attie RouxCOO

• Built / commissioned Nzema

processing plant

• 34 years as metallurgist at

AngloGold

Neil WoodyerCEO

• Founder of Endeavour, 30+ years

experience in natural resources

• Project financed and advised on

the acquisition of over 30 mines

Doug ReddySVP Business Development

• Geologist with 30+ years

exploration and mining experience

• Manages relationships with

analysts and institutional investors

Jeremy LangfordEVP Construction Services

• Mechanical engineer with 10+

years experience

• Built Agbaou, Nzema and

Sabodala gold mines

Richard ThomasEVP Technical Services

• 20+ years experience in open pit

and underground mining

• Previously VP Mining for

Continental Africa for Anglogold

Gérard de HertVP Exploration

• Geologist with more than 14 years

experience in mining and

exploration in West and Central

Africa

Doug BowlbyEVP Corporate Development

• Chartered Financial Analyst with

corporate finance and M&A

background

• 18 years experience with mining

transactions & growth plans

Morgan CarrollSVP Corp. Finance/General Counsel

• Previously with finance group at

Mayer Brown International LLP

• Admitted as Attorney in the State

of New York, and as Solicitor in

England & Wales

GOLD PRODUCER WEST AFRICA CASH FLOW 17

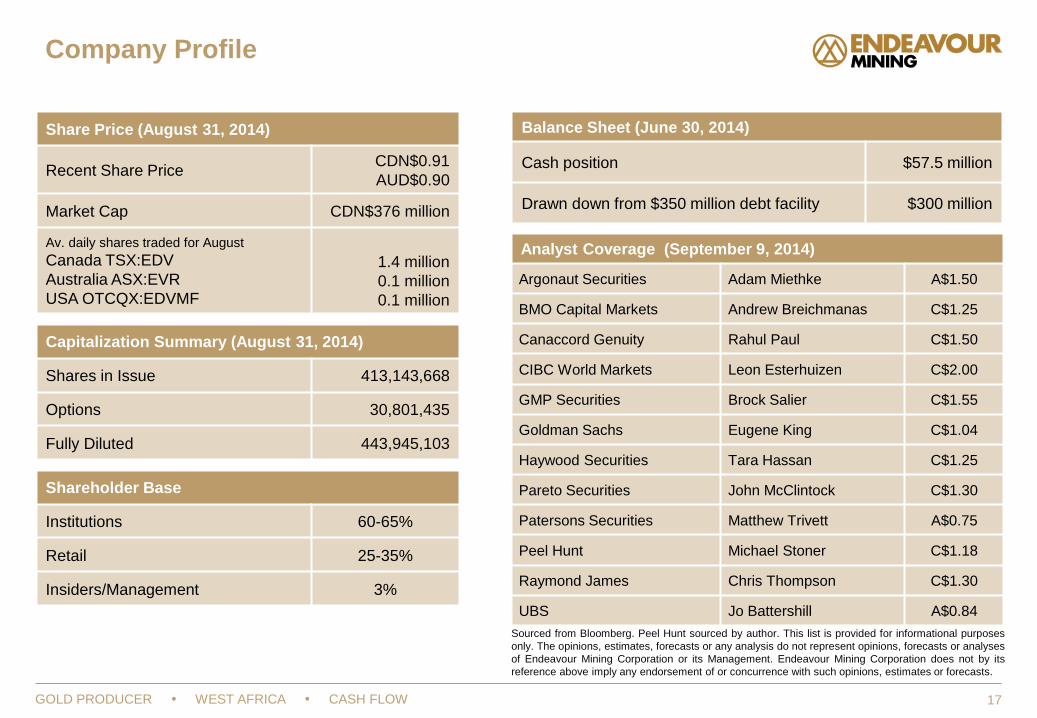

Company Profile

Capitalization Summary (August 31, 2014)

Shares in Issue 413,143,668

Options 30,801,435

Fully Diluted 443,945,103

Share Price (August 31, 2014)

Recent Share PriceCDN$0.91

AUD$0.90

Market Cap CDN$376 million

Av. daily shares traded for August

Canada TSX:EDV

Australia ASX:EVR

USA OTCQX:EDVMF

1.4 million

0.1 million

0.1 million

Shareholder Base

Institutions 60-65%

Retail 25-35%

Insiders/Management 3%

Sourced from Bloomberg. Peel Hunt sourced by author. This list is provided for informational purposes

only. The opinions, estimates, forecasts or any analysis do not represent opinions, forecasts or analyses

of Endeavour Mining Corporation or its Management. Endeavour Mining Corporation does not by its

reference above imply any endorsement of or concurrence with such opinions, estimates or forecasts.

Balance Sheet (June 30, 2014)

Cash position $57.5 million

Drawn down from $350 million debt facility $300 million

Analyst Coverage (September 9, 2014)

Argonaut Securities Adam Miethke A$1.50

BMO Capital Markets Andrew Breichmanas C$1.25

Canaccord Genuity Rahul Paul C$1.50

CIBC World Markets Leon Esterhuizen C$2.00

GMP Securities Brock Salier C$1.55

Goldman Sachs Eugene King C$1.04

Haywood Securities Tara Hassan C$1.25

Pareto Securities John McClintock C$1.30

Patersons Securities Matthew Trivett A$0.75

Peel Hunt Michael Stoner C$1.18

Raymond James Chris Thompson C$1.30

UBS Jo Battershill A$0.84

GOLD PRODUCER WEST AFRICA CASH FLOW 18

Tabakoto Gold Mine, Mali

Tabakoto Gold Mine (80% Endeavour, 20% Mali)

Kofi (84.4% Endeavour, 5.6% third-party, 10% Mali)

Resources

(incl. of Reserves,

100%)

M&I: 17.2Mt @ 3.0 g/t for 1.679Mozs

(~52% U/G @ 4.7 g/t)

Inferred: 19.0Mt @ 2.6 g/t for 1.603Mozs

(~59% U/G @ 4.6 g/t)

Reserves (100%)6.9Mt @ 3.6 g/t for 0.794Mozs

(~60% U/G @ 4.1 g/t)

Processing Rate 1.4 Mtpa Gravity/CIL Plan

Mining TypeTabakoto (UG), Segala (UG) & Djambaye

II Open Pit Mine

Met. Recovery 92% - 95%

Production

2012 – 110,301 ozs

2013 – 125,231 ozs

2014 H1 – 69,880 ozs

2014e – 140,000 to 155,000 ozs

Cash Costs ($/oz)

2013 - $972

2014 H1 - $1,145

2014e - $790 to $840

Royalty 6%

Corporate Tax 25%

GOLD PRODUCER WEST AFRICA CASH FLOW 19

Agbaou Gold Mine, Côte d’Ivoire

Agbaou Gold Mine (85% Endeavour, 10% Côte d’Ivoire, 5%

SODEMI)

Resources

(incl. of Reserves,

100%)

M&I: 15.0Mt @ 2.3 g/t for 1.100Moz

Inferred: 2.2Mt @ 2.3 g/t for 0.165Moz

Reserves (100%) 11.4Mt @ 2.4 g/t for 0.880Moz

Strip Ratio 7.9 to 1

Processing Rate Up to 1.6 Mtpa Gravity/CIL plant

Met. Recovery 92.5%

Mining Type Open Pit – Contractor Mining (BCM)

Production

2013 – 6,132 ozs (during commissioning)

2014 H1 – 55,964 ozs

2014e – 85,000 to 95,000 ozs

Cash Costs ($/oz)2014 H1 – $638

2014e – $730 to $780

Expected Mine Life 8 years from current Reserves

Royalty 3% - 5% sliding scale

Corporate Tax 25% with 5 year corporate tax holiday

GOLD PRODUCER WEST AFRICA CASH FLOW 20

Nzema Gold Mine, Ghana

Nzema Gold Mine (90% Endeavour, 10% Ghana)

Resources

(incl. of Reserves,

100%)

M&I: 38.4Mt @ 1.4 g/t for 1.693Moz

Inferred: 7.7Mt @ 1.3 g/t for 0.313Moz

Reserves (100%) 9.9Mt @ 2.1 g/t for 0.602Moz

Strip Ratio 4.8 to 1 (2014)

Processing Rate 1.6 to 2.1Mtpa Gravity/CIL plant

Met. Recovery 91% to 75% depending on ore type

Production

2012 – 109,447 ozs

2013 – 103,464 ozs

2014 H1 – 64,433 ozs

2014e – 110,000 to 120,000 ozs

Cash Costs ($/oz)

2013 - $917

2014 H1 - $816

2014e – $780 to $830

Expected Mine Life 6 years from current Reserves

Royalty 5% (+1% third-party at Adamus pits)

Corporate Tax 35%

GOLD PRODUCER WEST AFRICA CASH FLOW 21

Youga Gold Mine, Burkina Faso

Youga Gold Mine (90% Endeavour; 10% Burkina Faso)

Resources (incl. of

Reserves, 100%)

Youga & Ouaré

M&I: 15.5Mt @ 1.6g/t for 0.805Moz

Inferred: 2.2Mt @ 1.4g/t for 0.099Moz

Reserves (100%) 4.0Mt @ 2.0g/t for 0.265Moz

Strip Ratio 3.5 to 1 (2014)

Processing Rate 1.0Mtpa Gravity/CIL plant

Met. Recovery 94%

Production

2012 – 91,030 ozs

2013 – 89,448 ozs

2014 H1 – 47,002 ozs

2014e – 65,000 to 70,000 ozs

Cash Costs ($/oz)

2013 - $730

2014 H1 - $656

2014e – $790 to $840

Expected Mine Life2 years at current grade (with potential for

5+ years with satellite deposits and Ouaré)

Royalty 3% - 5% sliding scale

Corporate Tax 17.5%

22

Q2 2014 Cash Cost Detail by Mine

GOLD PRODUCER WEST AFRICA CASH FLOW

Tabakoto Nzema Youga Agbaou Total

Mining Physicals

Total tonnes mined - Open pit 000t 1,954 2,045 1,014 4,328

Total tonnes mined - Underground 000t 222 - - -

Total ore tonnes - Open pit 000t 157 368 344 527

Total ore tonnes - Underground 000t 175 - - -

Total tonnes milled 000t 373 391 254 520

Gold sold ozs 34,916 35,878 18,360 29,499 118,653

Unit cost analysis

Mining costs - Open pit1 $/t mined 4.55 4.83 6.11 2.93

Mining costs - Underground1 $/t ore 56.19 - - -

Processing and maintenance $/t milled 34.19 19.82 22.94 9.32

Site G&A $/t milled 17.50 7.46 10.54 4.58

Cash cost details

Mining costs - Open pit $000s $8,895 $8,439 $6,199 $12,667 $36,200

Mining costs - Underground $000s 9,571 - - - 9,571

Processing and maintenance $000s 12,752 7,748 5,828 4,847 31,175

Site G&A $000s 6,526 2,916 2,678 2,379 14,499

Purchased ore at Nzema $000s - 6,516 - - 6,516

Inventory adjustments $000s 1,829 1,575 41 -111 3,334

Cash costs for ounces sold $000s $39,573 $27,194 $14,746 $19,782 $101,295

Royalties $000s $2,686 $2,557 $1,055 $1,377 $7,675

Sustaining capital $000s $2,541 $3,098 $511 $312 $6,462

Cash cost per ounce sold $/oz $1,133 $758 $803 $671 $854

Mine-level AISC per ounce sold $/oz $1,283 $916 $888 $728 $973

Other costs used to derive unit mining cost

Capitalized mining costs $000s $262 $1,445

Numbers may not add due to rounding1 Includes capitalized mining costs

GOLD PRODUCER WEST AFRICA CASH FLOW 23

Mineral Reserves as at Dec 31, 2013

Mine / Project

Reserves

Proven Probable Proven & Probable Gold

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces Price

Mt g/t k Ozs Mt g/t k Ozs Mt g/t k Ozs US$/oz

Nzema1 - Total 6.7 2.0 434 2.3 2.3 168 9.0 2.1 602 US$ 1,350

Attributable - 90% 391 151 542

Youga2 - Total 2.7 2.0 172 1.3 2.2 93 4.0 2.0 265 US$ 1,250

Attributable - 90% 156 84 239

Agbaou4 - Total 3.1 2.8 279 8.3 2.2 601 11.4 2.4 880 US$ 1,350

Attributable - 85% 237 511 748

Tabakoto 5 – Kofi5 - Total 3.2 2.6 265 3.7 4.4 529 6.9 3.6 794US$ 1,200 -

1,350

Attributable - 81% 212 432 644

Houndé6- Total 3.8 2.4 300 20.9 1.9 1,250 24.6 2.0 1,550 US$ 1,144

Attributable - 90% 270 1,125 1,395

Total 1,450 2,641 4,091

Total Attributable 1,265 2,303 3,567

Note: Percent attributable at Tabakoto–Kofi is weighted by contribution to reserves.

GOLD PRODUCER WEST AFRICA CASH FLOW 24

Mineral Resources as at Dec 31, 2013

Mine / Project

Resources (including reserves) Lower

cutoffMeasured Indicated Measured & Indicated Inferred

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

Mt Au g/t koz Mt Au g/t koz Mt Au g/t koz Mt Au g/t koz Au g/t

Nzema1 - Total 25.2 1.4 1,130 13.2 1.3 563 38.4 1.4 1,693 7.7 1.3 313 0.5

Attributable - 90% 1,017 507 1,524 282

Youga2 - Ouaré3 - Total 6.9 1.4 322 8.6 1.7 484 15.5 1.6 805 2.2 1.4 99 0.5

Attributable - 90% 290 435 725 89

Agbaou4- Total 3.2 2.9 307 11.7 2.1 793 15.0 2.3 1,100 2.2 2.3 165 0.5

Attributable - 85% 261 674 935 140

Tabakoto5 – Kofi5- Total 4.4 2.9 412 12.8 3.1 1,267 17.2 3.0 1,679 19.0 2.6 1,603 0.5 to 1.5

Attributable - 82% 338 1,039 1,377 1,314

Houndé6- Total 3.8 2.5 303 25.7 1.9 1,571 29.4 2.0 1,874 1.8 2.2 133 0.35

Attributable - 90% 273 1,414 1,687 120

Total 2,474 4,677 7,151 2,313

Total Attributable 2,178 4,069 6,247 1,945

Note: Percent attributable at Tabakoto–Kofi is weighted by contribution to resources.

GOLD PRODUCER WEST AFRICA CASH FLOW 25

Notes to Mineral Resource and Reserves

1 Nzema Report with mineral resource update of the Adamus deposit effective November 7, 2013 prepared by N.J. Johnson (MPR Geological Consultants Pty Ltd.) and

updated internal mineral reserve estimates effective December 31, 2013 prepared by M. Alyoshin (Endeavour). Most recent filed report is "Technical Report and Mineral

Resource and Reserve Update for the Nzema Gold Mine, Ghana, West Africa", effective date December 31, 2012, prepared by N.J. Johnson (MPR Geological Consultants

Pty Ltd.), Q. De Klerk (Cube Consulting Pty Ltd.) and W.J.A. Yeo and A.A. Roux of Endeavour.

2 Youga Report with mineral resource update for Youga Main, East, West, NTV, and Leduc deposits effective December 31, 2013 prepared by B. Diouf (Endeavour) and

reviewed by K. Harris (Endeavour). Zergoré and A2NE deposit internal mineral resource estimates, prepared by AMEC under supervision of K. Woodman (Endeavour)

effective December 31, 2012. Internal mineral reserve estimates effective December 31, 2013 prepared by E. Kadio Kakou under the supervision of A. de Freitas

(Endeavour). Most recent filed report is "Technical Report and Update of Mineral Resources and Mineral Reserves for the Youga Gold Mine, Burkina Faso, West Africa"

effective date December 31, 2010, prepared by A. de Freitas and K. Woodman of Endeavour.

3 Ouaré deposit - Resource Estimate 2012, project 171880, dated December 31, 2012, prepared by AMEC under supervision of K. Woodman (Endeavour).

4 Agbaou Report with "Updated Mineral Resource Estimate for the Agbaou Gold Mine, Cote d'Ivoire, effective August 2013" prepared by M. Wanless (SRK Consulting).

Internal mineral resource update for satellite zones effective December 31, 2013 prepared by K. Harris (Endeavour). Mineral reserve update effective March 2014 prepared by

M. Alyoshin (Endeavour). Most recent filed report is "Agbaou Gold Mine, Côte d'Ivoire, NI 43-101 Technical Report" effective date May 25, 2012, prepared by M. Wanless, H.

Theart and M. Sturgeon of SRK Consulting South Africa (Pty) Ltd., N. Senior (SENET), and D. Grant-Stuart and A. Rowland of Knight Piésold (Pty) Ltd.

5 Tabakoto and Kofi are reported within “Technical Report and Mineral Resource and Reserve Update for the Tabakoto Gold Mine, Mali, West Africa” effective date December

31, 2013. Prepared by G. de Hert (Endeavour), K. Harris (Endeavour), M. Alyoshin (Endeavour), V. Duke (Sound Mining), A. Roux (Endeavour), E. Puritch (P&E Mining

Consultants Inc.), and A. Yassa (P&E Mining Consultants Inc.).

6 Houndé Project “Houndé Gold Project – Burkina Faso, Feasibility Study NI 43-101 Technical Report” effective date October 31, 2013. Prepared by M. Zammit MAIG (Cube

Consulting), M. Warren MIEAust CPEng (Lycopodium), R.M. Cheyne FAusIMM (ORELOGY), D. Morgan CPEng (Knight Piésold), P. O’Bryan MAusIMM (CP) (Peter O’Bryan

and Associates).

The following notes apply to the tables:

• Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

• Tonnages are rounded to the nearest 100,000 tonnes; gold grades are rounded to one decimal place; ounces are rounded to the nearest 1,000 ounces. Rounding may result in apparent

summation differences.

• Tonnes and grade measurements are in metric units; contained gold is in troy ounces.

GOLD PRODUCER WEST AFRICA CASH FLOW 26

Neil Woodyer

CEO

+377 97 98 7161

SVP Business Development

+1 604 609 6114

Doug Reddy