endeavour mining management presentation - denver … · endeavour mining management presentation...

TRANSCRIPT

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILTY

Endeavour Mining

Management Presentation

April 2015

Disclaimer & Forward Looking Statements

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY 2

This presentation contains “forward-looking statements” including

but not limited to, statements with respect to Endeavour’s plans

and operating performance, the estimation of mineral reserves

and resources, the timing and amount of estimated future

production, costs of future production, future capital expenditures,

and the success of exploration activities. Generally, these

forward-looking statements can be identified by the use of

forward-looking terminology such as “expects”, “expected”,

“budgeted”, “forecasts” and “anticipates”. Forward-looking

statements, while based on management’s best estimates and

assumptions, are subject to risks and uncertainties that may

cause actual results to be materially different from those

expressed or implied by such forward-looking statements,

including but not limited to: risks related to the successful

integration of acquisitions; risks related

to international operations; risks related to general economic

conditions and credit availability, actual results of current exploration

activities, unanticipated reclamation expenses; changes in project

parameters as plans continue to be refined; fluctuations in prices

of metals including gold; fluctuations in foreign currency exchange

rates, increases in market prices of mining consumables, possible

variations in ore reserves, grade or recovery rates; failure of

plant, equipment or processes to operate as anticipated;

accidents, labour disputes, title disputes, claims and limitations on

insurance coverage and other risks of the mining industry; delays

in the completion of development or construction activities,

changes in national and local government regulation of mining

operations, tax rules and regulations, and political and economic

developments in countries in which Endeavour operates.

Although Endeavour has attempted to identify important factors

that could cause actual results to differ materially from those

contained in forward-looking statements, there may be other

factors that cause results not to be as anticipated, estimated or

intended. There can be no assurance that such statements will

prove to be accurate, as actual results and future events could

differ materially from those anticipated in such statements.

Accordingly, readers should not place undue reliance on forward-

looking statements. Please refer to Endeavour’s most recent

Annual Information Form filed under its profile at www.sedar.com

for further information respecting the risks affecting Endeavour

and its business.

3

Business Overview

• A Canadian-based intermediate gold producer

– 4 producing mines across 4 West African countries

– Fully permitted and internally financed Houndé project

• Leading West African producer

– 2015E production of ~500,000 ozs

– Q1 2015 production of 124,000 ozs

– AISC/oz in mid-US$900 range

• Focused on

– Maximizing operating cash flow and profits

– Extending mine lives by adding reserves & resources

– Using free cash flow to repay debt

EDV EVR EDVMF

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

4

Investment Case

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

AISC/oz has declined from $1,137 in 2013 to under $1,000 in Q3+Q4 2014

2014 Exploration additions of 870,000 ozs at low cost

of $33/oz at mines and $13/oz at Houndé

Updated Houndé Feb 2015 +34% reserves to 2.1 Mozs

IRR of 31% at $1,250/oz

Extended credit facility to March 2020, ~3.5 years to first required repayment

Built Agbaou Mine under-budget and ahead of schedule

Exceeded 2014 production guidance and achieved AISC/oz cost guidance

2P Reserves increased to 4.5Mozs (Dec 2014) from

3.0Mozs (Dec 2012)

Track record of reducing costs and

generating cash flow at current gold prices

Demonstrated exploration successes that have

increased reserves and extended mine lives

Experienced management team with successful operating and project

delivery

Significant growth potential from attractive low-cost

Houndé project

Attractive valuation compared to fundamental value

and peers

Market Cap: US$200M

Enterprise Value: US$417M

5

Leading Intermediate Producer in West Africa

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Based on Company reports. AngloGold Ashanti and IAMGOLD presented on an attributable ounce basis for JV interests, West African gold production only.

Seniors

Intermediates & Junior Producers

2014 Gold Production – West Africa

6

With Near-term Production Growth

80,000 ozs

+700,000 ozs

Youga: 1st acquisition,

now a mature mine

Nzema: 2nd acquisition,

recapitalized

Tabakoto: 3rd acquisition, mill

expanded, converted to owner mining, improved mill feed

Agbaou: FS in 2012,

construction and start up in 2013, low-cost operations

Houndé: FS in 2013, fully

permitted, potential mid-2017 productionExpect to finance from cash flow,

corporate credit facility, and leasing of mining fleet

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

7

2015 AISC Guidance and Margin at $1,200/oz

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

• 2015 guidance of 475,000 to 500,000 ozs

at AISC/oz of $930 to $980

• At $1,200 gold, approx. $100 million of free

cash flow

2015 AISC Margin and Free Cashflow (US$ million, forecast)

Revenue $585

Less: AISC Costs ($930-$980/oz) 465

All-in sustaining margin (mid-guidance) 120

Add: 2015 fuel and FX cost savings 30 to 35

All-in sustaining margin (adjusted) 150 to 155

Non-sustaining capital: Kofi C and CRF plant 5

Non-sustaining exploration 15

Free cash flow (before tax & financing) $130 to 135

Less: Interest costs -22

Less: Tax -10

2015 Free cash flow Approx. $100

AISC/ounce – Cost trend versus Medium Producer AISC

8

Sustainable Low Operating and Corporate Costs

* Mid-point of 2015 AISC/oz guidance of $930-$980, including potential FX and fuel cost savings estimated at $30-$35 million1 Source: BMO Capital Markets – Gold Pages, 30 March 2015 – Medium Producers (production in 2014 >200kozs)2 Based on company reports; Corporate G&A & share-based compensation as percentage of gross revenue amd per ounce sold, 12 months ended December 31, 2014

2014 Corporate Efficiency Ratio2

Peer

G&A + share

comp as %

of gross

revenue

$ per

ounce sold ($/Au-eq oz)

Centamin 2.5% $31

Endeavour 3.9% $49

Acacia 4.4% $58

New Gold 4.5% $56

Centerra 4.6% $56

Golden Star 5.0% $63

Oceanagold 6.1% $79

Teranga 6.3% $80

SEMAFO 7.1% $90

Aurico 8.9% $114

Alamos 9.6% $122

Dundee Prec. 10.0% $136

Perseus 10.5% $122

B2Gold 11.1% $140

Primero 13.4% $167

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

$980

2015E Guidance

$930

2015E - Significant declines in

fuel costs and FX rates lead to

savings

• Fuel cost saving of ~$60/oz

at Tabakoto

• FX savings of ~$50/oz (all

production)

Combined 2015E cost savings

of $30 to $35 million

9

Maintaining an Efficient Capital Structure

• $300 million drawn on $350 million

credit facility (“RCF”)

• Significant headroom maintained

during Agbaou construction

• The RCF plus operating cash flow

and equipment leasing, provides

expectation to internally fund

Houndé construction

• Debt maturity is long-dated to

March 2020 with no repayment for

~3.5 years

• Regardless of comfortable debt

position, we will reduce debt

during 2015 from free cash flow

Note: Actual Leverage Ratio based on bank compliance certificate values, which include adjustments such that they may not agree with ratios calculated from Financial Statement values. Forecast Leverage Ratio based on Management projections.

Agbaouconstruction

period

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Incl. Houndé and $1,250/oz

(Q1/2016 construction)

Without Houndé and $1,100/oz

PotentialHoundé

constructionperiod

10

Share Price Since 2013 and Subsequent Accomplishments

2013 Today

# of mines3 and building Agbaou mine

4

Houndé project

FS in progress, unpermitted

Fully permitted; 2P reserve 2.1 Mozs; 10 year mine life

Production 324,275 ozs 475 – 500,000 ozs

AISC/oz (US$) $1,137 < $1,000 in Q3+Q4 2014

2P Reserves 3.0Mozs at 2.5 g/t1 4.5Mozs at 2.3 g/t2

M&I Resources 7.8Mozs at 1.9 g/t1 7.9Mozs at 2.0 g/t2

Long-termdebt

$300M drawn,July 2018 maturity, first repay Jan 2016

$300M drawn,March 2020 maturity, first repay Sept 2018

Cash flowFunding major

capex programs2015 non-sustaining capex only$20m; free cash to reduce debt

Share price $0.56 (June 28 2013) $0.58

Issued shares 412.8 million 413.1 million

• Significant valuation gap created during 2013 gold price decline

• Since June 2013, Endeavour’s share price highly correlated to the

market (S&P TSX Global Gold Index shown)

• Market yet to recognize Endeavour’s growth and accomplishmentsMarket data sourced from Bloomberg LP, rebased to 100, last data point: March 31, 2015

1 As of Dec 31, 2012, M&I resources include 2P reserves2 As of Dec 31, 2014, M&I resources include 2P reserves

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

11

Growing Mineral Reserves

MINERAL RESERVES & RESOURCES1

As of: 2P Reserves Resources (M&I)

Dec 31, 2014 4.5Mozs at 2.3 g/t 7.9Mozs at 2.0 g/t

Dec 31, 2013 4.1Mozs at 2.3 g/t 7.2Mozs at 1.9 g/t

Dec 31, 2012 3.0Mozs at 2.5 g/t 7.8Mozs at 1.9 g/t

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

MINERAL RESERVES – Mining Depletion & Reserve Additions

• Added 2.3Mozs from 2013

• 2014 exploration program:

• $2.1M at Agbaou, exploration

additions almost all oxides

• $9.2M at Tabakoto, drilling

below development is

successfully upgrading

Inferred resources

• $6.7M at Houndé, 34%

increase in reserves at only

$13 per discovered ounce

• 2015 exploration program: $15M

focused at Agbaou and Tabakoto

1 Mineral Resources and Reserves available at www.endeavourmining.com/s/reserves.asp

12

Agbaou Mine – A construction and operating success story

• Demonstrated strong, sustained performance in 2014

− Produced 146,757 ozs

− Cash cost of $523/oz

− AISC of $621/oz

− Strong cash flow generator

• Successful resource definition program

– 2014 replaced mined ounces and extended life

– Expanded West pit and identified opportunity to

southwest

– Easy-milling oxides now 50% of reserves

– Successful 2014 exploration continues in 2015

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

13

Tabakoto Mine – Investment phase completed

• Three sources of lower cost ore

• New Kofi C open pit commenced

production in January 2015

• Tabakoto plant at sustainable levels above

4,000 tonnes per day

• Demonstrating potential for steady

replacement of reserves

− 2014 net gain in 2P reserves

− Drilling below development upgrading

Inferred resources

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Kofi Property

Underground Mining Cost per Tonne Ore

Contract mining Owner mining

14

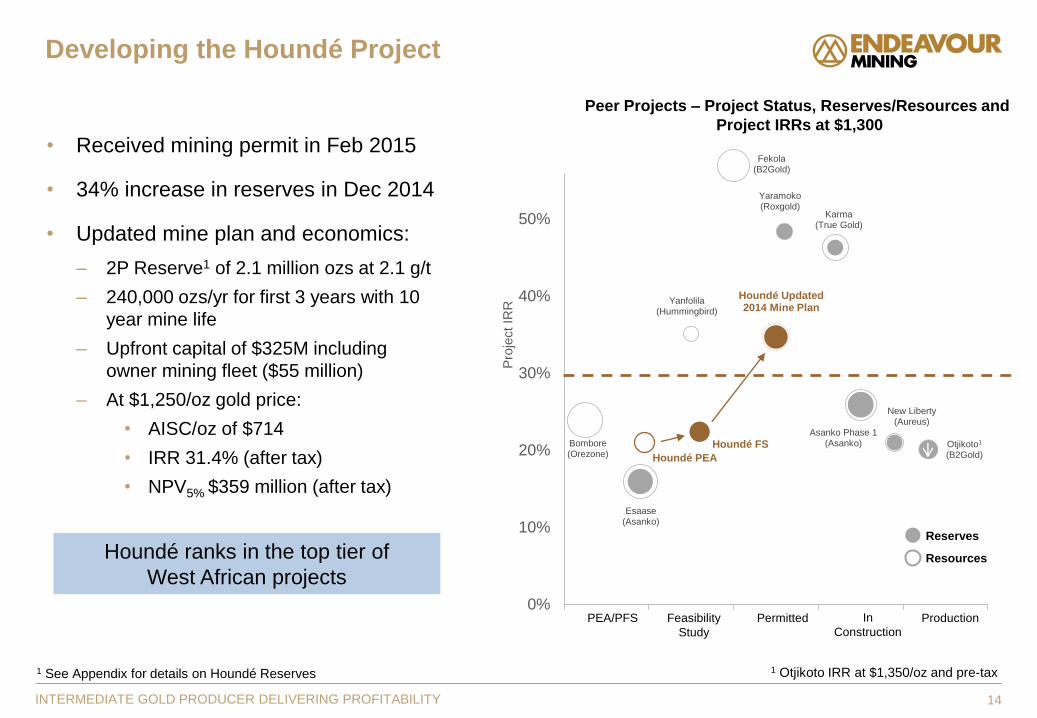

Developing the Houndé Project

• Received mining permit in Feb 2015

• 34% increase in reserves in Dec 2014

• Updated mine plan and economics:

– 2P Reserve1 of 2.1 million ozs at 2.1 g/t

– 240,000 ozs/yr for first 3 years with 10

year mine life

– Upfront capital of $325M including

owner mining fleet ($55 million)

– At $1,250/oz gold price:

• AISC/oz of $714

• IRR 31.4% (after tax)

• NPV5% $359 million (after tax)

1 See Appendix for details on Houndé Reserves

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Houndé ranks in the top tier of

West African projects

Houndé Updated 2014 Mine Plan

Yaramoko(Roxgold)

Karma(True Gold)

Asanko Phase 1(Asanko)

New Liberty(Aureus)

Otjikoto1

(B2Gold)

Bombore(Orezone)

Esaase(Asanko)

Fekola(B2Gold)

Yanfolila (Hummingbird)

Houndé PEA

Houndé FS

0%

10%

20%

30%

40%

50%

60%

70%

Pro

ject IR

R

1 Otjikoto IRR at $1,350/oz and pre-tax

In

Construction

ProductionPermittedFeasibility

Study

PEA/PFS

Reserves

Resources

Peer Projects – Project Status, Reserves/Resources and

Project IRRs at $1,300

15

Current Valuation and Analyst Views

Analyst coverage sourced from

Bloomberg. Peel Hunt sourced by

author. This list is provided for

informational purposes only. The

opinions, estimates, forecasts or any

analysis do not represent opinions,

forecasts or analyses of Endeavour

Mining Corporation or its Management.

Endeavour Mining Corporation does not

by its reference above imply any

endorsement of or concurrence with

such opinions, estimates or forecasts.

AUD/CAD conversion rate of 1.00

Analyst Coverage (April 9, 2015)

BMO Capital Markets C$0.75

Canaccord Genuity C$1.00

CIBC World Markets C$1.70

Clarus Securities C$1.75

GMP Securities C$1.30

Haywood Securities C$1.30

Pareto Securities C$1.19

Patersons Securities A$0.88

Peel Hunt C$0.87

Raymond James C$1.00

UBS A$1.10

CONSENSUS PRICE OBJECTIVE C$1.17

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Potential for

+100%

investment gains

Enterprise Value

Share price (April 1, 2015) C$0.61

Shares outstanding 413.1

Market capitalization1 (US$M) 200

Less: Cash2 62

Plus: Long-term debt2 300

Plus: Minority interest2 (21)

Enterprise value (US$M) 417

2014 EBITDA2 (US$M) 143

2014 AISC Margin2 (US$M) 117

EV / 2014 EBITDA 2.9 times

Peer average3 7.2 times

EV / 2P reserve ounce $93

Peer average3 $152

EV / resource ounce (M&I) $53

Peer average3 $131

1 CAD-USD exchange rate of 1.262 Cash, long-term debt, minority interest and adjusted EBITDA based on FY December 31, 2014 financial statements3 Source: BMO Capital Markets – Gold Pages, 30 March 2015 – Medium Producers (production in 2014 >200kozs)

• Produce 475,000 to 500,000 ounces

• Maintain AISC/oz improvements

• Q1 2015 at mid-point of $930-$980

• To extend mine life through exploration

success

• To be profitable

• Use free cash flow to reduce debt

16

Summary – Key objectives for 2015

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Positioned for a value re-rating

Appendices

17

• 2015 Production and AISC/oz Guidance by Mine

• Board of Directors

• Management

• Endeavour’s Operating Mines – Summary Table

• FY 2014 Cash Cost Detail by Mine

• Resources and Reserves

• Company Profile

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

18

2015 Production and AISC/oz Guidance by Mine

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Production

Guidance Range (ozs)

AISC/oz

Guidance Range ($/oz)

Agbaou 150,000 - 155,000 $690 - $740

Nzema 110,000 - 115,000 $1,000 - $1,050

Tabakoto 155,000 - 165,000 $950 - $1,000

Youga 60,000 - 65,000 $975 - $1,025

475,000 - 500,000 $883 - $933

Plus: Corporate G&A (~$18 million) $37

Plus: Exploration (sustaining) & Other (~$5 million) $10

$930 - $980

19

Board of Directors

Michael Beckett, Chairman

Former Chairman, Ashanti Goldfields and former MD, Consolidated Gold Fields

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Frank Giustra

Founder: Wheaton River, Silver Wheaton and Pacific Rubiales; Former CEO, Yorkton Securities

Wayne McManus

Accounting professor: CPA, CFA, LLM in taxation

Neil Woodyer, CEO

Founded Endeavour in 1988; former mining banker/advisor

Ian Cockerill

Extensive African mining experience, Former CEO, Gold Fields

Ian Henderson

Former Managing Director and natural resources fund manager, JP Morgan

Miguel Rodriguez

Former President Venezuela Central Bank; former Governor of IMF, World Bank and IADB

20

Management

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Neil Woodyer, CEO

• Founder of Endeavour, 30+ years experience in natural resources

• Project financed and advised on the acquisition of over 30 mines

Attie Roux, COO

• Built / commissioned Nzema processing plant

• 34 years as metallurgist at AngloGold

Ota Hally, CFO

• Chartered Accountant and Chartered Financial Analyst

• Previous experience with Pan American Silver

Doug Bowlby, EVP Corporate Development

• Chartered Financial Analyst with corporate finance and M&A background

• 19 years experience with mining transactions & growth plans

Doug Reddy, SVP Business Development

• Geologist with 30+ years exploration and mining experience

• Manages relationships with analysts and institutional investors

Jeremy Langford, EVP Construction Services

• Mechanical engineer with 10+ years experience

• Built Agbaou, Nzema and Sabodala gold mines

Richard Thomas, EVP Technical Services

• 20+ years experience in open pit and underground mining

• Previously VP Mining for Continental Africa for AngloGold

21

Endeavour’s Operating Mines – Summary Table

Agbaou Gold Mine

(85% Endeavour, 10% Côte

d’Ivoire, 5% SODEMI)

Nzema Gold Mine

(90% Endeavour, 10% Ghana)

Tabakoto Gold Mine

(80% Endeavour, 20% Mali)

(Kofi: 90% Endeavour, 10% Mali)

Youga Gold Mine

(90% Endeavour; 10% Burkina

Faso)

Resources

(incl. Reserves,

100%)

M&I: 13.9Mt @ 2.5 g/t for

1.109Moz

Inferred: 2.1Mt @ 2.3 g/t for

0.154Moz

M&I: 36.7Mt @ 1.3 g/t for

1.590Moz

Inferred: 7.6Mt @ 1.3 g/t for

0.311Moz

M&I: 19.0Mt @ 3.0 g/t for

1.839Moz

Inferred: 17.6Mt @ 2.8 g/t for

1.582Moz

Youga & Ouaré

M&I: 17.0Mt @ 1.5g/t for 0.812Moz

Inferred: 2.8Mt @ 1.6g/t for

0.141Moz

Reserves (100%) 11.5Mt @ 2.5 g/t for 0.926Moz 7.3Mt @ 2.1 g/t for 0.496Moz6.7Mt @ 3.7 g/t for 0.807Moz

(~65% U/G @ 3.9 g/t)3.5Mt @ 1.8g/t for 0.202Moz

Strip Ratio 8 to 1 (2015); 11 to 1 LOM 6.2 to 1 (2015); 5.6 to 1 LOM

Tabakoto & Segala U/G: N/A

Kofi B: 6 to 1 LOM

Kofi C: 10 to 1 LOM

4.0 to 1 (2015); 4.2 to 1 LOM

Processing RateUp to 2.2 Mtpa Gravity/CIL plant -

oxides; 1.6 Mtpa fresh ore 1.6 to 2.1 Mtpa Gravity/CIL plant 1.4 Mtpa Gravity/CIL plant 1.0 Mtpa Gravity/CIL plant

Met. RecoveryAchieving 97% at present; 92.5%

design91% to 75% depending on ore type 92% - 95% 94%

Production2014 – 146,757 ozs

2015e – 150,000 to 155,000 ozs

2013 – 103,464 ozs

2014 – 115,129 ozs

2015e – 110,000 to 115,000 ozs

2012 – 110,301 ozs

2013 – 125,231 ozs

2014 – 127,323 ozs

2015e – 155,000 to 165,000 ozs

2013 – 89,448 ozs

2014 – 76,561 ozs

2015e – 60,000 to 65,000 ozs

Cash Costs

($/oz)2014 – $523

2013 - $918

2014 - $880

2013 - $981

2014 - $1,172

2013 - $732

2014 - $742

All-in Sustaining

Costs

(Mine Level)

2014 – $621/oz

2015e $690 - $740/oz

2014 - $1,036/oz

2015e $1,000 - $1,050/oz

2014 – $1,335/oz

2015e $950 - $1,000/oz

2014 - $824/oz

2015e $975 - $1,025/oz

Expected Mine

Life7 years from current Reserves 5 years from current Reserves 5 years from current Reserves

2 years at current grade (potential

for 5 years with satellite deposits

and Ouaré)

Royalty 3% - 5% sliding scale 5% (+1% 3rd party at Adamus pits) 6% 3% - 5% sliding scale

Corporate Tax 25% (5 year corporate tax holiday) 35% 25% 17.5%

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

22

FY 2014 Cash Cost Detail by Mine

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Agbaou Nzema Tabakoto Youga Total

Mining Physicals

Total tonnes mined - Open pit 000t 19,560 8,769 7,046 4,993

Total ore tonnes - Open pit 000t 2,741 1,366 638 1,161

Total ore tonnes - Underground 000t - - 807 -

Total tonnes milled 000t 2,241 1,587 1,485 991

Gold sold ozs 143,772 2 114,044 127,357 76,582 461,757

Unit cost analysis

Mining costs - Open pit1 $/t mined 2.61 4.56 4.55 4.98

Mining costs - Underground1 $/t ore - - 57.90 -

Processing and maintenance $/t milled 7.66 17.90 30.11 24.24

Site G&A $/t milled 3.84 7.87 17.62 10.88

Cash cost details

Mining costs - Open pit $000s $46,395 $34,821 $32,035 $24,887 $138,138

Mining costs - Underground $000s - - 40,956 - 40,956

Processing and maintenance $000s 17,175 28,410 44,696 24,022 114,303

Site G&A $000s 8,601 12,491 26,164 10,783 58,039

Purchased ore at Nzema $000s - 24,409 - - 24,409

Inventory adjustments $000s 2,999 231 5,376 (2,882) 5,725

Cash costs for ounces sold $000s $75,170 $100,362 $149,227 $56,810 $381,570

Royalties $000s $6,399 $8,014 $9,665 $4,229 $28,307

Sustaining capital $000s $7,650 $9,795 $11,078 $2,057 $30,580

Cash cost per ounce sold $/oz $523 $880 $1,172 $742 $826

Mine-level AISC per ounce sold $/oz $621 $1,036 $1,335 $824 $954

Other costs used to derive unit mining cost

Capitalized mining costs $000s $4,609 $5,147 $5,759 -

Numbers may not add due to rounding, 1Includes capitalized mining costs and partial year of lower cost owner-mining, 2 Excludes pre-commercial production

23

Mineral Reserves as at December 31, 2014

Mine / Project

Reserves

Proven Probable Proven & Probable Gold

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces Price

Mt g/t k Ozs Mt g/t k Ozs Mt g/t k Ozs US$/oz

Nzema1 - Total 5.2 2.0 339 2.1 2.3 156 7.3 2.1 496 US$ 1,350

Attributable - 90% 305 141 446

Youga2 - Total 2.5 1.7 139 1.0 2.0 63 3.5 1.8 202 US$ 1,250

Attributable - 90% 125 57 181

Agbaou3 - Total 2.7 2.7 236 8.8 2.4 690 11.5 2.5 926 US$ 1,350

Attributable - 85% 200 587 787

Tabakoto 4 – Total 2.3 3.3 249 4.4 4.0 558 6.7 3.7 807 US$ 1,350

Attributable – 80%-90% 202 470 672

Houndé5 – Total 3.7 2.5 295 26.9 2.1 1,780 30.6 2.1 2,073 US$ 1,300

Attributable - 90% 266 1,602 1,866

Total 1,258 3,247 4,503

Total Attributable 1,098 2,856 3,952

Note: Percent attributable at Tabakoto–Kofi is weighted by contribution to reserves.

Notes to Mineral Resources and Reserves available at www.endeavourmining.com/s/reserves.asp

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

24

Mineral Resources as at December 31, 2014

Mine / Project

Resources (including reserves) Lower

cutoffMeasured Indicated Measured & Indicated Inferred

Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

Mt Au g/t koz Mt Au g/t koz Mt Au g/t koz Mt Au g/t koz Au g/t

Nzema1 - Total 23.7 1.4 1,040 13.0 1.3 550 36.7 1.3 1,590 7.6 1.3 311 0.5

Attributable - 90% 936 495 1,431 280

Youga2 - Total 7.3 1.3 317 9.7 1.6 494 17.0 1.5 812 2.8 1.6 141 0.5

Attributable - 90% 285 444 730 127

Agbaou3- Total 2.9 2.8 255 11.1 2.4 854 13.9 2.5 1,109 2.1 2.3 154 0.5

Attributable - 85% 216 726 942 131

Tabakoto4 - Total 5.6 2.9 529 13.4 3.0 1,310 19.0 3.0 1,839 17.6 2.8 1,5820.5 to

1.5

Attributable – 80%-90% 433 1,110 1,543 1,315

Houndé5- Total 3.7 2.6 305 34.1 2.1 2,242 37.8 2.1 2,546 3.2 2.6 273 0.5

Attributable - 90% 274 2,017 2,291 246

Total 2,446 5,449 7,896 2,462

Total Attributable 2,146 4,792 6,938 2,099

Note: Percent attributable at Tabakoto–Kofi is weighted by contribution to resources.

Notes to Mineral Resources and Reserves available at www.endeavourmining.com/s/reserves.asp

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

25

Company Profile

Capitalization Summary (March 31, 2015)

Shares in Issue 413,143,668

Options 30,796,868

Warrants none

Fully Diluted 443,940,536

Share Price (March 31, 2015)

Recent Share PriceCDN$0.58

AUD$0.60

Market Cap CDN$240 million

Av. daily shares in March 2015

Canada TSX:EDV

Australia ASX:EVR

USA OTCQX:EDVMF

2.9 million

0.3 million

0.1 million

Shareholder Base

Institutions 60-65%

Retail 25-35%

Insiders/Management 3%

Balance Sheet (December 31, 2014)

Cash position $62 million

Drawn down from $350 million debt facility $300 million

INTERMEDIATE GOLD PRODUCER DELIVERING PROFITABILITY

Shareholder Geographic Mix

26

+1 604 609 6114

Doug Reddy, SVP Business Development

Neil Woodyer, CEO

+377 97 98 7130