employment tax responsibilities - in.gov · employment tax responsibilities sboa school for in...

TRANSCRIPT

1

Employment Tax Responsibilities

SBOA School for IN Clerk-TreasurersJune 27, 2012

Presenter:Raelane Hoff

FSLG Specialist

Resources

Independent Contractor vs. Employee

2

EMPLOYEE DEFINED:

IRC 3121(d) and Reg. 31.3121(d)-1– Any individual under usual common law

rules– Any individual who performs services for

pay for any person:– Statutory Employees

Continued on next slide

EMPLOYEE (Continued)

– Any individual who performs services that are included under an agreement entered into under Section 218 of Social Security Act

– ENTERED INTO BETWEEN GOVERNMENTAL AGENCY AND THE SOCIAL SECURITY ADMINISTRATION

COMMON LAW STANDARD

– Worker is subject to the will and control of the business:

not only as to what work shall be done but also

how work shall be done

Continued

3

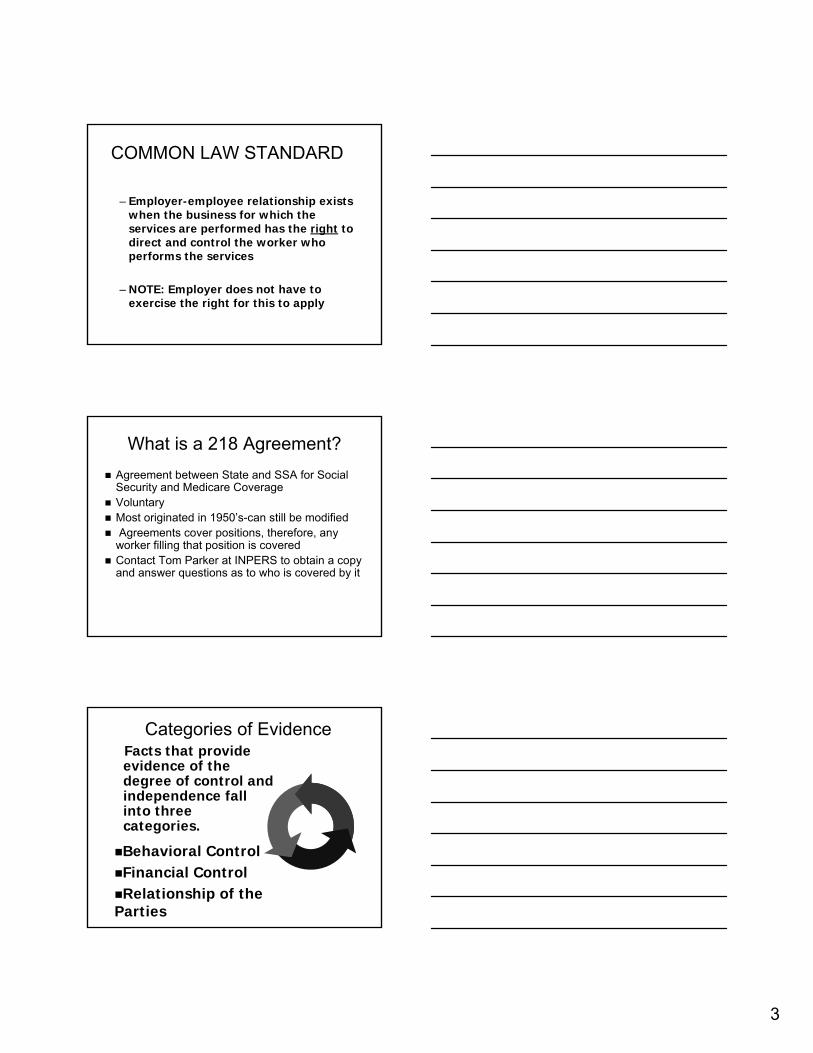

COMMON LAW STANDARD

– Employer-employee relationship exists when the business for which the services are performed has the right to direct and control the worker who performs the services

– NOTE: Employer does not have to exercise the right for this to apply

What is a 218 Agreement?Agreement between State and SSA for Social Security and Medicare CoverageVoluntary Most originated in 1950’s-can still be modifiedAgreements cover positions, therefore, any worker filling that position is coveredContact Tom Parker at INPERS to obtain a copy and answer questions as to who is covered by it

Categories of EvidenceFacts that provide evidence of the degree of control and independence fall into three categories.

Behavioral ControlFinancial ControlRelationship of the

Parties

4

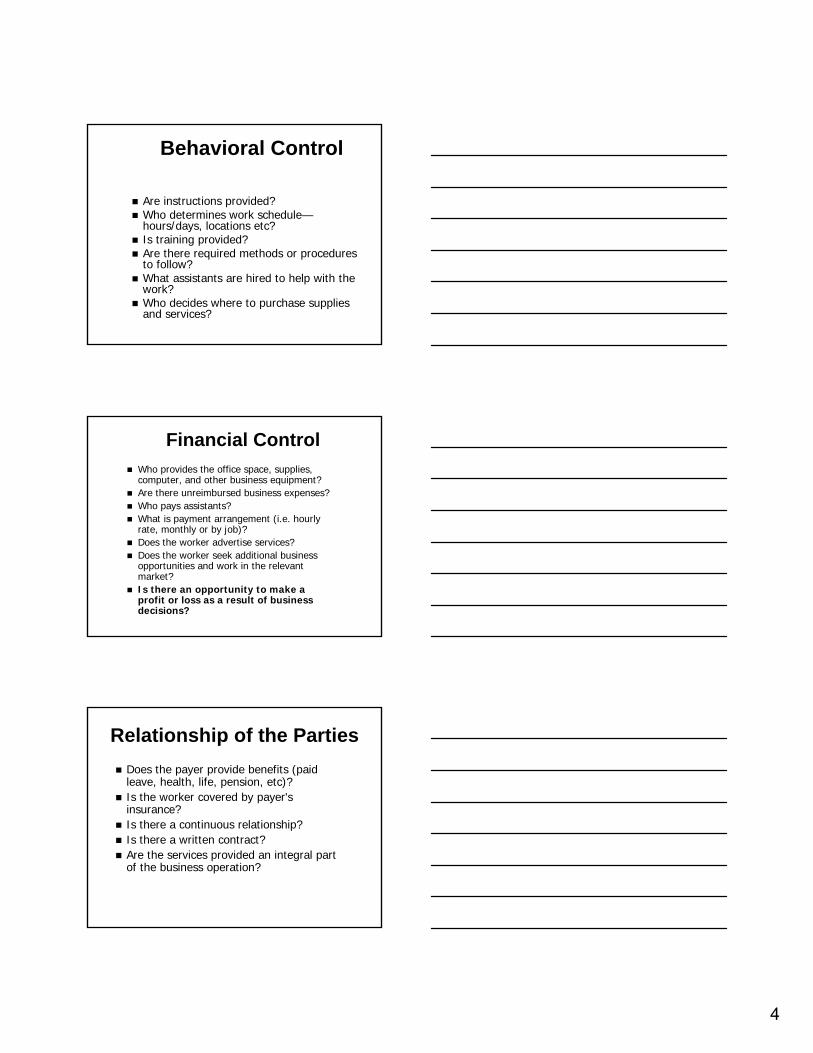

Behavioral Control

Are instructions provided?Who determines work schedule—hours/days, locations etc?Is training provided? Are there required methods or procedures to follow?What assistants are hired to help with the work?Who decides where to purchase supplies and services?

Financial ControlWho provides the office space, supplies, computer, and other business equipment? Are there unreimbursed business expenses?Who pays assistants?What is payment arrangement (i.e. hourly rate, monthly or by job)?Does the worker advertise services?Does the worker seek additional business opportunities and work in the relevant market?Is there an opportunity to make a profit or loss as a result of business decisions?

Relationship of the PartiesDoes the payer provide benefits (paid leave, health, life, pension, etc)?Is the worker covered by payer's insurance?Is there a continuous relationship?Is there a written contract?Are the services provided an integral part of the business operation?

5

Independent Contractor

Makes own scheduleBuys own productsHas own phone numberFurnishes own supplies Furnishes own equipmentMakes a profit or loss as a result of his own business decisions

•Some Factors that may indicate A Worker IS ANIndependent contractor

Employees...

Required to wear uniformsRequired to work certain hoursDoes not handle own sales receiptsDoes not make own appointmentsOwner provides trainingOwner provides equipment, supplies and materialsCan quit job without liability to employerStands no risk of loss

•Some Factors that may indicate A worker IS AN employee

WHO ARE GOVERNMENT EMPLOYEES?

6

GOVERNMENT EMPLOYEES

GOVERNMENTAL ENTITY EMPLOYEES

– Elected and Appointed Officials– Volunteer Firefighters– Election Workers – All Groups under a Section 218

Agreement

7

Elected & Appointed Officials

Elected Officials are ALWAYS Employees for Federal Income Tax Withholding--IRC 3401(c)

Elected and Appointed officials will usually be employees for FICA Withholding--IRC 3121(d)(2), due to these factors: – Position established by law – Duties defined by statute– Performs duties as a public official– Responsible to the public– Paid out of governmental funds

Elected & Appointed Officials

Examples – Mayor – City Attorney– Judge or Justice of the Peace– Building Inspector– Board Members (Township, Health, Drainage,

Council, etc)

– Road Commissioner– Animal Control Officer

Elected & Appointed Officials

8

VOLUNTEER FIREFIGHTERSVolunteer firefighters are employees for tax purposes if they meet the common law testsAll employment tax rules applyPer diem/Per call, Training/Meeting payments—considered wages—subject to all employment taxesAllowance or Reimbursement of protective fire clothing—follows accountable plan rules, non-taxable with receiptAllowance or Reimbursement of mileage—commuting to fire station is personal, taxable to employee

ELECTION WORKERS

Wages exempt from Federal Income Tax withholdingWages exempt from FICA tax withholding up to $1,500Wages subject to W-2 reporting if paid $600 or more in a calendar year All income paid Poll Workers is includible on their income tax returnRevenue Ruling 2000-6 Reference

ELECTION WORKERS

9

Employee or Independent?

Funding for the work is through a Grant

Careful analysis should be made to determine if common law factors are present

Form SS-8 can be submitted for determination of treatment

GOVERNMENTAL ENTITY EMPLOYEES

Effective 4/1/86, State and local government employees who are not covered for social security under a Section 218 Agreement or by mandatory law, and who were hired or rehired after March 31, 1986, are subject to mandatory Medicare only coverage

Effective 7/1/91, full social security is mandatory, for all State and local government employees who are not covered by a qualified retirement system—IRC 3121(d)(4)

Independent Contractor vs. Employee

Publication 1779 Provides factors used to help determine worker status as either an independent contractor or an employee

SS-8 Can be filed by firm or worker with Internal Revenue Service to determine worker status

10

Independent Contractor/Employee

The bottom line:Each case is dependent on the exact facts and circumstances and the evaluation of the control factors…

If you have an employer-employee relationship, it makes no difference how it is labeled

The substance of the relationship, not the label nor source of funding, govern the worker’s status

Voluntary Classification Settlement Program (VCSP)

Allows eligible taxpayers who are not under audit to voluntarily reclassify their workers as employees for future tax periodsTaxpayer pays reduced amount for employment tax dueMust meet certain criteria to applyNot available for workers covered under the Taxpayer’s Section 218 agreementMore information available at FSLG website

Fringe Benefits

11

Definition and Taxability of Fringe Benefits

A fringe benefit is a form of pay for the performance of services.

Property,Services,Cash or Cash Equivalent

All fringe benefits are taxable, subject to employment tax & must be included in the recipients pay unless the law specificallyexcludes it.

Fringe Benefit Process

Identify specific benefit provided to employee(s);

Determine if benefit is excluded by law; and

Determine if benefit is fully taxable, or only partially.

IRS Publication 15-B

Taxable Fringe Benefit How to Report:

INCLUDE in Employee’s wages and on Form W-2 (Never on 1099-MISC)Subject to Federal Withholding, Social Security and MedicareTaxable even if benefit is received by/for spouse or child of employee

12

Fringe Benefit Exclusions:

Medical Premiums IRC 106Qualified Tuition Reduction IRC 117Meals or Lodging for Employer’s Convenience IRC 119Cafeteria Plans IRC 125Education Assistance IRC 127Dependent Care IRC 129

Fringe Benefit Exclusions Cont’dCertain Fringe Benefits IRC 132:

No additional cost service-(ex: pool passes)Qualified employee discounts-(ex: green fees)Working condition fringe-(ex: autos)De minimis fringe-(small value, administrative accounting is not practical)Qualified transportation or moving expenses, Retirement planning

Working Condition FringeIRC 132(d)

Requirements:Benefit must relate to employer's businessEmployee would have been entitled to a Form 1040 deductionBusiness use must be substantiated with records

13

No Additional Cost Service & Employee Discount

No Additional Cost Service & Employee Discount

No Additional Cost FringeNo Additional cost service must be a service offered by the employer to its customers in the ordinary course of businessEmployee receiving the benefit performs substantial services in providing the serviceEmployer incurs no substantial additional cost (including lost revenue) in providing the benefit to the employee

Publication 15-B

14

Qualified Employee DiscountsProperty or service must be offered to the public in the ordinary course of businessExcludable discount cannot exceed:

For merchandise or other property, the employer’s gross profit % times the price charged to the public

For services, no more than 20% of the price charged to the general public

Publication 15-B

Fringe BenefitsCell Phones

Notice 2011-72 issued Sept. 14, 2011 addresses tax treatment of Employer provided cellphonesTo be excluded as a fringe, cellphone must be provided primarily for noncompensatory business reasonsPersonal use of employer provided cellphone if issued for noncompensatory business reason is excluded as a de minimis fringeSimilar treatment for allowances/reimbursement of employee owned cellphones

Publication 15-B

VEHICLES

-EMPLOYER VEHICLES-EMPLOYEE VEHICLES

15

EMPLOYER - PROVIDED VEHICLES

– Personal use is taxableCommutingVacation, weekend, use by spouseApplies even if employee is on 24 hour call

– Valuing Personal UseEmployee must keep record of personal and business useNo records kept - all use is taxable

–withhold and report on Form W-2

VALUING PERSONAL USE -THREE RULES:

Automobile Lease Valuation RuleCents-Per-Mile RuleCommuting Rule

Quick Reference GuideTaxable Fringe Benefit GuidePublication 15-B

EMPLOYER PROVIDED VEHICLES

Qualified Non-Personal Use Vehicle

By design, vehicle is unlikely to have personal use

– Use of vehicle is tax-free, including commuting

– Substantiation/recordkeeping of vehicle use not required

16

QUALIFIED NON-PERSONALUSE VEHICLE

(Reg. 1.274-5(k)(2)

Clearly marked police, fire & public safety officer vehicles (marking on license plate doesn’t qualify)

Unmarked law enforcement vehicles Ambulance or hearseVehicle with gross weight over 14,000 lbs.20 passenger bus and school busTractor and other farm equipmentDelivery truck with driver seating only

QUALIFIED NON-PERSONALUSE VEHICLE

Clearly marked police, fire & public safety officer vehicles:

--Employee must always be on call

--Employer requires employee to commute in vehicle

--Employer prohibits personal use (other than commuting) travel outside of employee’s jurisdiction

QUALIFIED NON-PERSONALUSE VEHICLE

(Rev. Ruling 86-97)

Vehicles with loaded GVW under 14,000 lbsPick-up Trucks or Vans-Must be permanently & clearly marked and have permanent modificationsPick-up truck modifications include Hydraulic lift gate, tanks, drums, permanent side boardsVan modifications include seating for driver only or one passenger, permanent shelving in cargo area OR cargo area always contains equipment, materials, merchandise used in trade or business

Publication 15-B

17

EMPLOYEE’S VEHICLE USED FOR EMPLOYER’S BUSINESS

REIMBURSED BUSINESS USE ISNON-TAXABLE IF AT OR BELOW

FEDERAL MILEAGE RATE

RATE IS 55.5 CENTS PER MILE (2012)

ACCOUNTABLE PLAN RULES APPLY

UNIFORMS AND CLOTHING ALLOWANCES

UNIFORMSTwo Requirements for NON-taxable status:

REQUIRED as a condition ofemployment

Apparel is NOT suitable for everydaywear

(Applies whether the clothing is worn after hours or kept on work premises)

If allowance or reimbursement to employee, accountable plan rules must be met

18

UNIFORMS

Plain pants and shirt do not qualify as uniformSuits, sports coats, etc worn be plain clothes officers do not qualify as uniformsIf uniform is NON-taxable, cleaning costs are NON-taxable

FORMS 1099-MISC

Form 1099-MISC

19

W-9 or substitute form (Rev. 12-2011)Form 1099-MISCForm 945 for Backup Withholding of Tax

Required Forms for Vendor Payments

What is a W-9 and why is it needed?

Required for reportable payments of $600 or morePayee certifies he/she is not subject to backup withholding or is exemptProvides information to prepare Form 1099

Failure to obtain, when required, results in liability for 28% backup withholding

Payments that should not be reported

on Form 1099-MISCpayments to employees; such as fringe benefits or travel reimbursements (note: if not paid as part of an accountable plan, travel reimbursements and auto expenses should be included in wages and reported on W-2)

generally, payments to corporations

20

Information ReturnsForm 1099-MISC

■ Payments of $600 or more ■ Rents■ Services performed by

Individuals who are not your Employees, i.e:– Subcontractors– Attorneys– Medical payments

■ Combination of services and product

Payments to AttorneysTreasury Regulation 1.6045-5 requires reporting payments to attorneys (individuals, partnerships and corporations)– gross proceeds, and– payments for services of

attorneysthis change was effective for 1998 and later yearsSettlement payments that are in attorney and claimant names may require Form 1099MISC to both parties

Medical and Healthcare Payments

Report payments of $600 or more in Box 6

Report payments to allindividuals, partnerships, and corporations

Medical payments include doctor fees, drug testing, lab fees, physical therapy, etc.* Do not report payments to pharmacies or tax exempt hospitals

21

One ormore owners

LLC’s and Reportable payments

An LLC may be taxed as either a sole proprietorship, a partnership, or a corporation Obtain a W-9 from the payee to determine their statusreport payments to sole proprietors and partnerships; and, in some cases, to corporations

General Exemptions to Filing Form 1099-MISC

Payments for only merchandisePayments of rent to real estate agents acting as an agent for the ownerPayments to a corporation ■ Exceptions:

■Payments to medical and health care providers ■Payments to Attorneys for legal services

When to File Forms 1099-MISC

Report payments on calendar year basisProvide copy of Form 1099 MISC to recipient by Jan. 31 of the following yearFile with IRS by Feb. 28 of the following yearUse Form 1096 transmittal form to submit Forms 1099 to IRSMaintain copies for three years from the due date (4 years if back up withholding applies)

22

COMMON QUESTIONS

Can I file an extension to file Forms 1099?– Form 8809 (file by Jan 31 for a 30 day extension)

What if I file the information returns late?– Penalties apply unless reasonable cause

Form 1099-Misc PenaltiesFailure to Furnish Form to Recipient

Correctly file by March 30 $30/return

Correctly file after March 30 but before August 1 $60/return

Correctly file August 1 or later $100/return

Failure to File with IRS

$100* for every 1099-Misc Form*Penalty amount can be less if filed by due dates

above

IMPORTANT

Common Errors that prevent issuance of“correct" or “required” information returns

Failure to obtain identifying information before making payment (use Form W-9 Dec. 2011)

Failure to aggregate payments from all expense categories (use vendor files)

Assuming payee is a corporation:– because name is “Company or Associates”– because an EIN is furnished

23

NO W-9 INFORMATION

No TINBackup Withhold 28%File 945TIP!! Get the W-9 information before job is awarded

Form 945 Annual Return of Withheld Federal Income

TaxForm 945 is used to report and pay backup withholding to the IRS.

This is an annual return, due 1/31 of the following year

ordinary deposit rules apply(However, see Instructions for Form 945 to determine your

deposit schedule)make Form 945 deposits separate from Form 941 deposits

How to report Backup Withholding

Report withholding to payee and to IRS in Box 4 of Form 1099-MISC

This applies even though the amount of the payment may be below the normal threshold for filing Form 1099.

Send Copies A of all paper Forms 1099 to the IRS with Form 1096.

24

FEDERAL STATE AND LOCAL GOVERNMENTS

and