elizabeth coogan | dec. 2015 u.s. department of education 2015 fsa training conference for financial...

TRANSCRIPT

Elizabeth Coogan | Dec. 2015

U.S. Department of Education

2015 FSA Training Conference for Financial Aid Professionals

Financial Literacy Matters

Session 48

AGENDA

• Benefits of financial literacy

• FSA resources

• Research on financial wellness and programming

• Best practices from higher education institutions

• Questions/Comments

• Appendix

2

Survey of Borrowers in School

Top 5 Ways Financial Information was Received %

Talking with financial aid counselors at your college or university 78%

Other online resources from your school’s office of financial aid 65%

Printed materials from your school’s office of financial aid 63%

Talking with friends or family about financial aid 59%

Talking with other staff or faculty at your school 52%

Source: FSA survey of borrowers in school, 2014

3

Financial Literacy Matters

Successful financial literacy programs benefit students, families, communities, and schools

• Equip students to make sound financial decisions

• Reduce loan default

• Improve retention and graduation rates

• Build a base of active and engaged alumni

• Build strong community relationships

4

FSA’s Support of Financial Literacy

• Hosting Community College Financial Capability Roundtable

• Promote Buy In from School Leadership

• Reviewing Entrance and Exit Counseling

• New Resources

• Sharing Best Practices

5

Treasury Postsecondary Opportunities Report

Opportunities to Improve the Financial Capability and Financial Well-being of Postsecondary Students

6

Summary of Financial Literacy Resources

Federal Student Aid Financial Literacy Resources

7

FINANCIAL LITERACY GUIDANCE

Financial Literacy Guidance From Federal Student Aid

8

9

RESEARCH ON FINANCIAL WELLNESS

STUDENT FINANCIAL STRESS

10

PAYING FOR SCHOOL

Nearly 60% of all students agree that they worry about having enough money to pay for school.

• Students at 2-year public institutions are more likely (65.5%) to agree that this is a worry

11

DEBT HAS CAUSED

12

First Year Students say they are frequently worried about their financial

situation

60%40%

more than

of students are Concerned/Very Concerned about their ability to pay for next years education expenses (SERU)

79%

of students say they frequently worry about debt

1 in 3

students described their finances as “traumatic” or “very difficult”

IMPACT OF FINANCIAL STRAIN ON STUDENTS

13

Academic Impact of Financial Strain on StudentsResearch shows that financial stress leads to poor academic performance

• Over 25% said they did not purchase required academic materials because they didn’t want to take out extra loans

• 80% of students who self-reported being “financially stressed” say concerns frequently impacted academic performance and/or investigated dropping out

• Finances are leading (self-reported) cause for not persisting

• As levels of student concern about education finances increased, cumulative GPA decreased

• When working 20+ hours per week, cumulative GPA decreased

14

• 40% of students say they did not participate in an activity because of finances

• Over 40% report investigating working more to meet expenses

• 48.6% worry about meeting monthly expenses

• 34% say the amount of debt causes them a large or extreme amount of stress

• 22.7% are not confident they can pay off the amount they’ve borrowed

Impact of Financial Strain on Student Retention

15

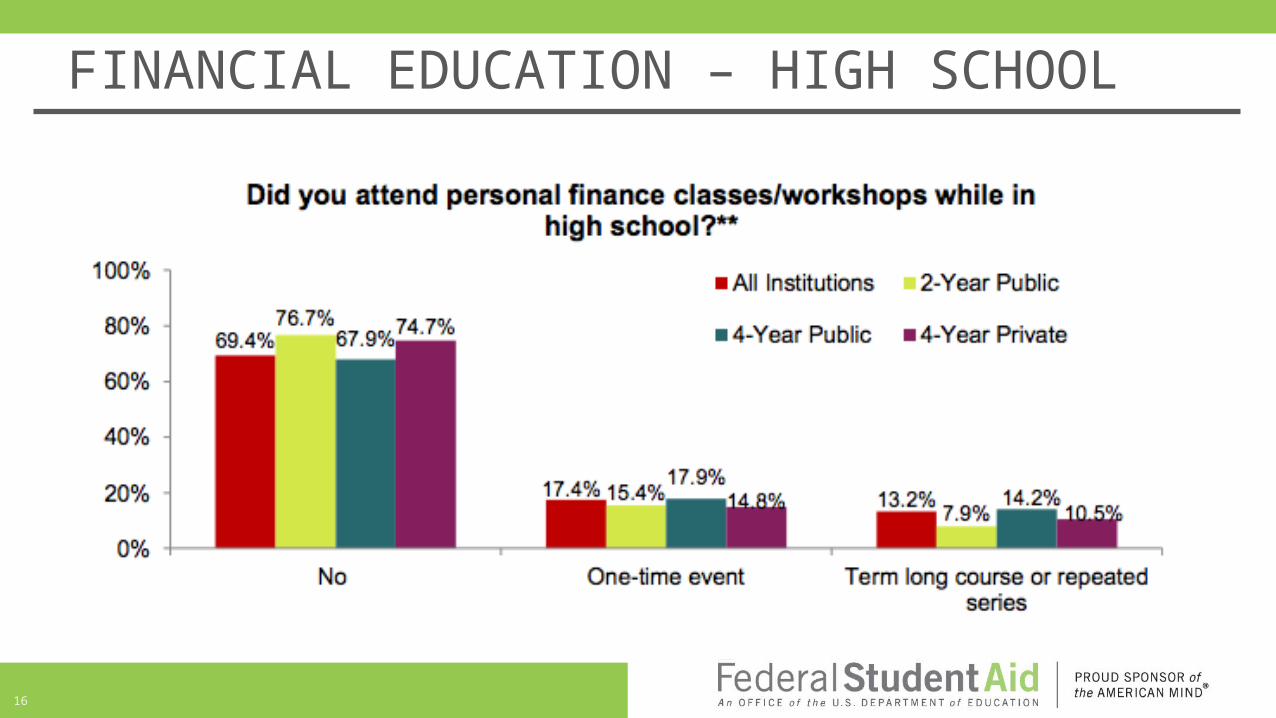

FINANCIAL EDUCATION – HIGH SCHOOL

16

17

FINANCIAL EDUCATION – COLLEGE

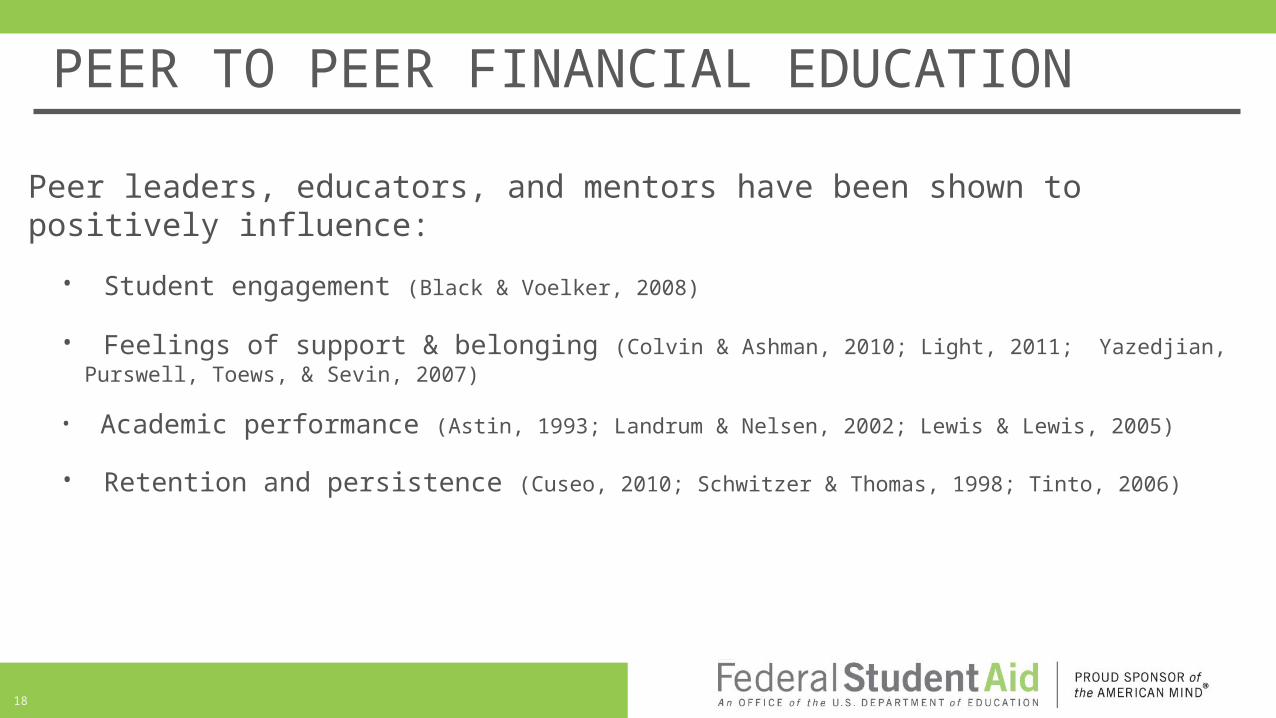

PEER TO PEER FINANCIAL EDUCATION

Peer leaders, educators, and mentors have been shown to positively influence:

• Student engagement (Black & Voelker, 2008)

• Feelings of support & belonging (Colvin & Ashman, 2010; Light, 2011; Yazedjian, Purswell, Toews, & Sevin, 2007)

• Academic performance (Astin, 1993; Landrum & Nelsen, 2002; Lewis & Lewis, 2005)

• Retention and persistence (Cuseo, 2010; Schwitzer & Thomas, 1998; Tinto, 2006)

18

EFFECTS OF PEER TO PEER EDUCATION

19

PEER COACHING

• Fall participants were more likely to have a plan to pay back debt than their peers who had not yet completed the intervention (p<.05)

• A mandatory one-on-one coaching session contributes to a significant decrease in financial stress for STEP participants (p<.05)

• Increased financial awareness and slight increase in financial knowledge (pilot data)

• Increased financial efficacy (pilot data)

20

NSCFW• The National Summit on Collegiate Financial Wellness

• Over 200 attendees

• 120 Institutions

• 39 States

• Connecting practitioners, researchers and policy makers in a growing field

• Sessions on:– How to start a program– Effective practices– Assessing Interventions– Curriculum– Gamification– More

21

22

BEST PRACTICES

Indiana University Office of Financial Literacy

• Provide financial education for students to help them improve decision-making during and after college

• Goal to get students to afford their careers and not be influenced by debt

• Focus on providing multiple options for interaction with program to reach all learning types

• Improve Financial Aid Business Processes

• $44 Million reduction in student debt

23

Moneysmarts.iu.edu• Portal to all things financial literacy at IU

Podcasts• How Not to Move Back in With

Your Parents (9/13 – 5/15)• Lesson on financial topic every week• Designed to educate on basics

• MoneySmarts U• Interview students every week• Designed to make finances relevant to students by talking

with students facing similar crises• Created for national audience

24

Indiana University MoneySmarts

Moneysmarts.iu.edu• Portal to all things financial literacy at IU

Podcasts• How Not to Move Back in With

Your Parents (9/13 – 5/15)• Lesson on financial topic every week• Designed to educate on basics

• MoneySmarts U• Interview student every week• Designed to make finances relevant to students by talking with students facing similar crises• Created for national audience

25

Indiana University MoneySmarts

Indiana University MoneySmarts

• Required Financial Literacy

• New students to University

• 80% completion rate

• One Credit-Hour Courses

• Split three credit-hour class

• Required for some business students

• IU MoneySmarts Team

• Implemented on three of IU campuses

• Partnership with School of Public Health

26

The Ohio State University

• Financial Wellness Advisory Board helps to formalize partnership with over 32 departments

• Strong partnerships with Student Financial Aid, Bursar’s Office, One Stop Center

• Two Colleges help to contribute to the base of student volunteer peer educators

• Research partnership with the Center for the Study of Student Life and College of Education and Human Ecology

27

The Ohio State University

1:1 Financial Coaching Appointments • Proactive • Reactive • Help Seeking

Group Workshops• Classes, Student Organizations, Residence Halls, Student

Athletes etc.

Online Interventions • Knowledge Modules• ITunes U• Course Interventions

28

The Ohio State UniversitySecond Year Transformational Experience Program Requirement

• Holistic Second Year Experience for Students • 1,400 students currently enrolled in a pilot program• All students must complete a financial wellness requirement to receive their fellowship• 1st Part: Online Module (Knowledge Gain) and 2nd Part: In Person Appointment (Attitudes

and Behaviors)

•Students receiving emergency loans/grants

•Students on the University payment plan

•Collaboration between our office and the Graduate School• Better targeting resources to graduate students

29

Champlain College

Part of LEAD Program• Financial Sophistication• Lifelong Career Management• Engaged Citizenship

Participate in financial literacy all four years• Menu of programs on website• Awesome Island

Community involvement for K-12 and adults

30

Champlain LEAD Website

Cuyahoga Community College

• Redefined financial aid beyond grants, loans, and scholarships

• Integrated benefits access services (applying for SNAP, utility assistance, cash assistance, etc.) into financial aid application processes and financial education initiatives

• aligns with college’s initiative to reduce student loan debt by obtaining other financial resources

• Target potentially eligible students by “flagging” financial aid records to encourage students to complete “quick check” for public benefits eligibility

31

Cuyahoga Community College Project Go Website

University of California, Berkeley

Peer-to-peer financial wellness program

Workshops:• Creating a spending plan• Managing Debt• Understanding Credit• Understanding Credit Cards• Savings Banking• Identity Theft

One-on-One consultations (coming soon)

Website resources

32

Bears for Financial Success Website

Best PracticesStrengths commonly found in successful programs

• Accessibility and ease of use

• Prioritizing students who need it most

• Outcome tracking and measurement

• Networking and partnerships

• Positioning and infrastructure

• Peer-to-peer coaching

• Student-initiated and funded

• Focus on success of student

33

QUESTIONS?

34

35

Contact Us

Phil SchumanDirector of Financial LiteracyIndiana [email protected]

Phil SchumanDirector of Financial LiteracyIndiana [email protected]

Elizabeth CooganSenior Advisor, Customer Experience OfficeFederal Student [email protected]

Bryan AshtonAssistant Director, Student Wellness CenterThe Ohio State [email protected]

AppendixEffectiveness and Best Practices Research•COHEAO. (2014). Financial Literacy in Higher Education: The Most Successful Models and Methods for Gaining Traction. Retrieved from http://www.coheao.com/wp-content/uploads/2014/03/2014-COHEAO-Financial-Literacy-Whitepaper.pdf

•Federal Reserve Bank of Boston. (2015). Promoting Pathways to Financial Stability. A Resource Handbook on Building Financial Capabilities of Community College Students. Retrieved from http://www.bostonfed.org/education/financial-capabilities/handbook/financial-capabilities-handbook.pdf

•Fernandes, D. , Lynch J. G., Netemeyer, R. G. (2013). The Effect of Financial Literacy and Financial Education on Downstream Financial Behaviors. Retrieved from http://www.nefe.org/Portals/0/WhatWeProvide/PrimaryResearch/PDF/CU%20Final%20Report.pdf

•Financial Literacy and Education Commission. (2015). Opportunities to Improve the Financial Capability and Financial Well-being of Postsecondary Students. Retrieved from http://www.treasury.gov/resource-center/financial-education/Documents/Opportunities%20to%20Improve%20the%20Financial%20Capability%20and%20Financial%20Well-being%20of%20Postsecondary%20Students.pdf

•Goetz, J., Cude, B. J., Nielsen, R. B., Chatterjee, S., & Mimura, Y. (2011). College-based personal Finance education: Student interest in three delivery methods. Journal of Financial Counseling and Planning, 22(1), 27-42.

•iGrad. (2014). Financial Literacy Compendium: Colleges Setting the Bar for Financial Literacy. Retrieved from http://schools.igrad.com/blog/best-college-financial-literacy-programs

36

AppendixEffectiveness and Best Practices Research•Lumina Foundation. (2015). Beyond Financial Aid How Colleges Can Strengthen the Financial Stability of Low-Income Students and Improve Outcomes. Retrieved from https://www.luminafoundation.org/beyond-financial-aid

•Mandell, L., & Klein, L. S. (2009). The impact of financial literacy education on subsequent financial behavior. Journal of Financial Counseling and Planning, 20(1), 15-24.

•President’s Advisory Council on Financial Capability (2012). Key Themes for President’s Advisory Council on Financial Capability. Retrieved from http://www.treasury.gov/resource-center/financial-education/Documents/Key_Themes.pdf

•TG Research and Analytical Services. (2015). Above and Beyond: What Eight Colleges Are Doing to Improve Student Loan Counseling. Retrieved from http://www.tgslc.org/pdf/Above-and-Beyond.pdf

Need for Financial Literacy•Consumer Finance Protection Bureau [CFPB]. (2013). Financial literacy annual report. Retrieved from http://files.consumerfinance.gov/f/201307_cfpb_report_financial-literacy-annual.pdf

•Council for Economic Education. (2012). Economic and Personal Finance Education in our Nation’s Schools. Retrieved from http://www.councilforeconed.org/policy-and-advocacy/survey-of-the-states/#findings

•Harnish, T.L. (2010). Boosting financial literacy in America: A role for state colleges and universities. Perspectives. Retrieved from http://www.aascu.org/policy/publications/perspectives/financialliteracy.pdf

37

AppendixPeer to Peer Education•Astin, A.W. (1993). What Matters in College? Four Critical Years Revisited. Retrieved from http://www.researchgate.net/profile/Alexander_Astin/publication/242362064_What_Matters_in_College_Four_Critical_Years_Revisited/links/00b7d52d094be57582000000.pdf

•Black, K., Voelker, J. (2008). The role of preceptors in first-year student engagement in introductory courses. Retrieved from http://www.ingentaconnect.com/content/fyesit/fyesit/2008/00000020/00000002/art00002

•Colvin, J.W., Ashman, M. (2010). Roles, risks, and benefits of peer mentoring relationships in higher education. Retrieved from http://www.tandfonline.com/doi/abs/10.1080/13611261003678879

•Cuseo, J.B., Fecas, V.S., Thompson, A. (2010). Thriving in College and Beyond: Research-Based Strategies for Academic Success and Personal Development

•Landrum, R.E., Nelsen, L. R. (2002). The Undergraduate Research Assistanceship: An Analysis of the Benefits. Retrieved from http://www.tandfonline.com/doi/abs/10.1207/S15328023TOP2901_04#.VjosFberTIU

•Schweitzer, A., Thomas, C. (1998). Implementation, Utilization, and Outcomes of a Minority Freshman Peer Mentor Program at a Predominantly White University. Retrieved from http://www.ingentaconnect.com/content/fyesit/fyesit/1998/00000010/00000001/art00002

•Tinto, V. (2006). Research and Practice of Student Retention: What Next? Retrieved from http://csr.sagepub.com/content/8/1/1.short

•Yazedjian, A., Purswell, K., Toews, M., Sevin, T.. (2007). Adjusting to the First Year of College: Students’ Perceptions of the Importance of Parental, Peer, and Institutional Support. Retrieved from http://www.ingentaconnect.com/content/fyesit/fyesit/2007/00000019/00000002/art00002

38

AppendixTerminology•Huston, S. J. (2010). Measuring financial literacy. Retrieved from http://onlinelibrary.wiley.com/doi/10.1111/j.1745-6606.2010.01170.x/pdf

Understanding Student Finances•Center for the Study of Student Life. (2011). Ohio Student Financial Wellness Survey: Student Loans, Credit Cards and Stress. Retrieved from http://cssl.osu.edu/posts/documents/09-01-11-ohio-financial-wellness-report-final-no-watermark.pdf

•Center for the Study of Student Life. (2015). National Student Financial Wellness Study: National Descriptive Report. Retrieved from http://cssl.osu.edu/posts/documents/nsfws-national-descriptive-report.pdf

•EverFi, Inc. (2015). Money matters on campus: How early attitudes and behaviors affect the financial decisions of first-year college students . Retrieved from http://moneymattersoncampus.org/wp-content/uploads/2013/02/MoneyMatters_WhitePaper_2015_FINAL.pdf

•Fosnacht, K. (2013). Undergraduate coping with financial stress: A latent class analysis. Paper presented at the annual meeting of the American College Personnel Association, Las Vegas, NV, March 2013. Retrieved from http://cpr.iub.edu/uploads/Fosnacht%20-%20ACPA%20-%20Financial%20Stress.pdf

•Gutter, M., Copur, Z. (2011). Financial Behaviors and Financial Well-Being of College Students: Evidence from a National Survey. Journal of Family Economics iss, 32, 699-714.

39

AppendixUnderstanding Student Finances•Shim, S., Barber, B., Card, N., Xiao, S., Serido, J. (2009). Financial Socialization of First-Year College Students: The Roles of Parents, Work, and Education. J Youth Adolescence, 1007 (10), 10964-10978

•Trombitas, K. (2012). College students are put to the test: The attitudes, behaviors, and knowledge levels of financial education . Inceptia. Retrieved from https://www.inceptia.org/about/resources/college-students-are-put-to-the-test/

Workplace Finances•PwC. (2015). Employee Financial Wellness Survey: 2015 Results. Retrieved from http://www.pwc.com/us/en/private-company-services/publications/assets/pwc-employee-financial-wellness-survey-2015.pdf

40