jessica barrett simpson, elizabeth coogan | dec. 2014 u.s. department of education 2014 fsa training...

TRANSCRIPT

Jessica Barrett Simpson, Elizabeth Coogan | Dec. 2014

U.S. Department of Education

2014 FSA Training Conference for Financial Aid Professionals

Session 37

Financial Literacy Resourcesand Updates

What Student Borrowers Need to Know

Agenda

2

1. Introductions

2. The Knowledge Gap

What do students know (or not know) about borrowing?

3. Financial Literacy and Decision Making

What do student borrowers need to know?

4. Resources and Best Practices

Introductions

3

Jessica Barrett SimpsonSenior AnalystCustomer AnalyticsCustomer Experience OfficeFederal Student [email protected]

Elizabeth CooganSenior Advisor on Financial LiteracyCustomer Experience OfficeFederal Student [email protected]

The Knowledge Gap

4

1. Where do students get their information on borrowing and repayment?

2. Do student borrowers understand their loan repayment options?

3. Once they complete or leave school, what do they wish they had done differently?

4. What are the characteristics of student borrowers who need this information the most?

The Knowledge Gap: Sources of Info

5

Students get most of their information on financial aid from their school’s financial aid office

Top 5 Ways Financial Information was Received %

Talking with financial aid counselors at your college or university 78%

Other online resources from your school’s office of financial aid 65%

Printed materials from your school’s office of financial aid 63%

Talking with friends or family about financial aid 59%

Talking with other staff or faculty at your school 52%

SOURCE: FSA survey of borrowers in school, 2014.

The Knowledge Gap: Sources of Info

6

Borrowers in their grace period get most of their information on repayment options from their loan servicer and FSA websites

Top 5 Sources of Info on Repayment Options %

Online loan servicer account management 43%

Studentloans.gov website 27%

NSLDS website 19%

Phone number for loan servicer 17%

Studentaid.gov website 17%

SOURCE: FSA survey of borrowers in grace, 2013.

The Knowledge Gap: Sources of Info

7

• Borrowers in school give high ratings for entrance and exit counseling, finding it to be helpful, convenient, and clear

• However, only half of those in grace report that they received exit counseling

SOURCES: FSA survey of borrowers in school (2014) and in grace (2013).

The Knowledge Gap: Repayment

34% of borrowers in their grace period report not being aware of their repayment options

28% are undecided about what action they will take on their loans at the end of their grace period

33% of those planning to go into repayment at the end of their grace period either don’t know or are undecided about their repayment plan

SOURCE: FSA survey of borrowers in grace, 2013.

8

9

The Knowledge Gap: Repayment

SOURCE: FSA survey of borrowers in grace, 2013.

Have you considered Income-Based Repayment or Pay as You Earn?

The Knowledge Gap: DecisionsWhat information do you feel you still need to help you make a decision about the right payment plan for you?

•I don't know any of the other option plans other than the standard repayment option•I did not even know there were any options. I just figured the bill would come and I would need to pay what it says•I really need to take some time and look at all the options but I feel a bit overwhelmed every time I do•A customized breakdown of my student loans other than examples presented•I wish there was a calculator of some sort so that I could put in my information without having to go through the actual process of choosing an option

10

SOURCE: FSA survey of borrowers in grace, 2013.

11

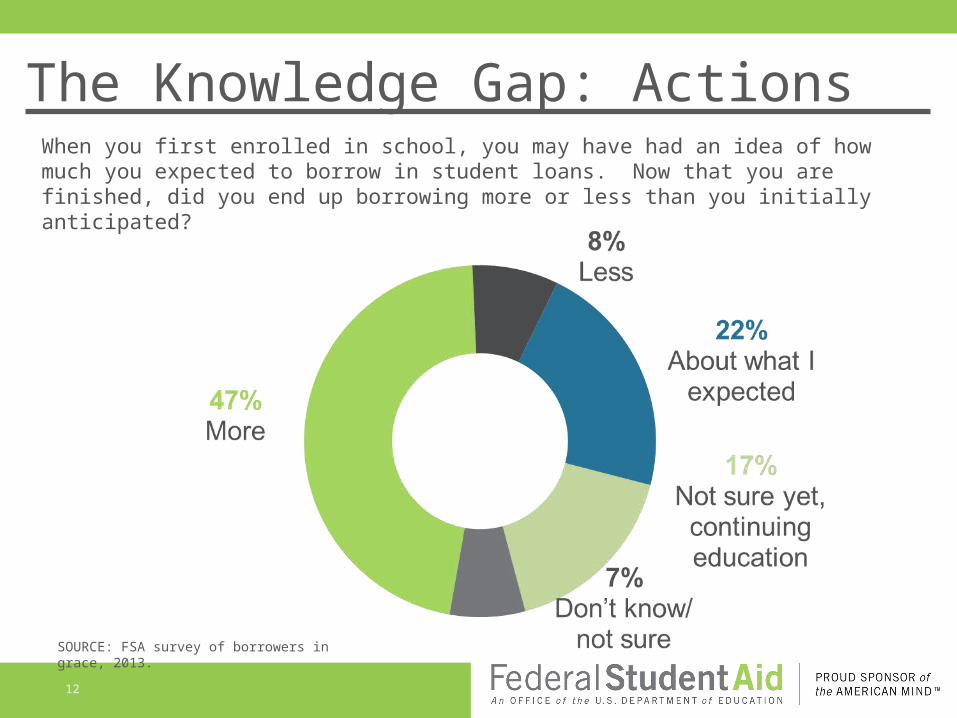

The Knowledge Gap: Actions

SOURCE: FSA survey of borrowers in grace, 2013.

If you could go through the process of taking out loans to pay for your education all over again, would you take the same actions or make a change?

When you first enrolled in school, you may have had an idea of how much you expected to borrow in student loans. Now that you are finished, did you end up borrowing more or less than you initially anticipated?

12

The Knowledge Gap: Actions

SOURCE: FSA survey of borrowers in grace, 2013.

If I could do it all over again…• I would begin paying my loans during my studies • I would have taken all subsidized loans and no unsubsidized ones• I would have taken out just enough and not the maximum amount• I would pay interest as I went• Pay some early on loans• Rethink how to spend my loan• Take more classes per semester to cut down on cost• I would borrow less, have a better understanding of loan repayment

options, and not accept refund checks to make my loan smaller• Find out exactly how much I am borrowing• Found other resources and researched how much education would cost• Get a loan counselor

SOURCE: FSA survey of borrowers in grace, 2013.

13

• Students often borrow more than they expected• Many are not aware of the options for loan repayment other

than the standard 10-year repayment plan• Many do not have enough information about income-driven

repayment plans• Without enough information, it is hard for them to make an

informed decision about repayment• Customized tools exist to help them understand their options,

such as the Repayment Estimator and FACT• Many borrowers access the tools, but not all are aware of them• FAAs have a window of opportunity while students are in

school to ensure students have the info they need

14

The Knowledge Gap: Summary

Students Most at Risk of Default

• Non-completers

• First-generation

• Non-traditional - age 25 or older

• Has dependents

• Not academically prepared – low high school GPA and/or

low standardized test scores

Note: FSA conference sessions #24 and #36 address in detail how to

help student borrowers at risk of default

15

• Timing matters: Information is needed at the point where decisions are made

• Make it simple: Don’t overload with information. Focus on the basics

• Information should be both push (sent out) and pull (available upon request)

• FSA resources are available: The Repayment Estimator, the Financial Aid Awareness Counseling Tool, publications, videos, infographics, social media, and more

16

The Knowledge Gap: How to Help

What is Financial Literacy?

17

“The ability to use knowledge and skills to manage financial

resources effectively for a lifetime of financial well being.”

2008 Annual Report, President’s Advisory Council on Financial Capability

Personal Finance State Requirements

18

SOURCE: Council for Economic Education, 2014 Survey of the States, http://www.councilforeconed.org/news-information/survey-of-the-states/

Financial Literacy State Rankings

2013 National Report Card on State Efforts to Improve Financial Literacy in High Schools

SOURCE: Champlain College’s Center for Financial Literacy,http://www.champlain.edu/centers-of-excellence/center-for-financial-literacy/report-making-the-grade

19

Basics for Student Loan Borrowers

20

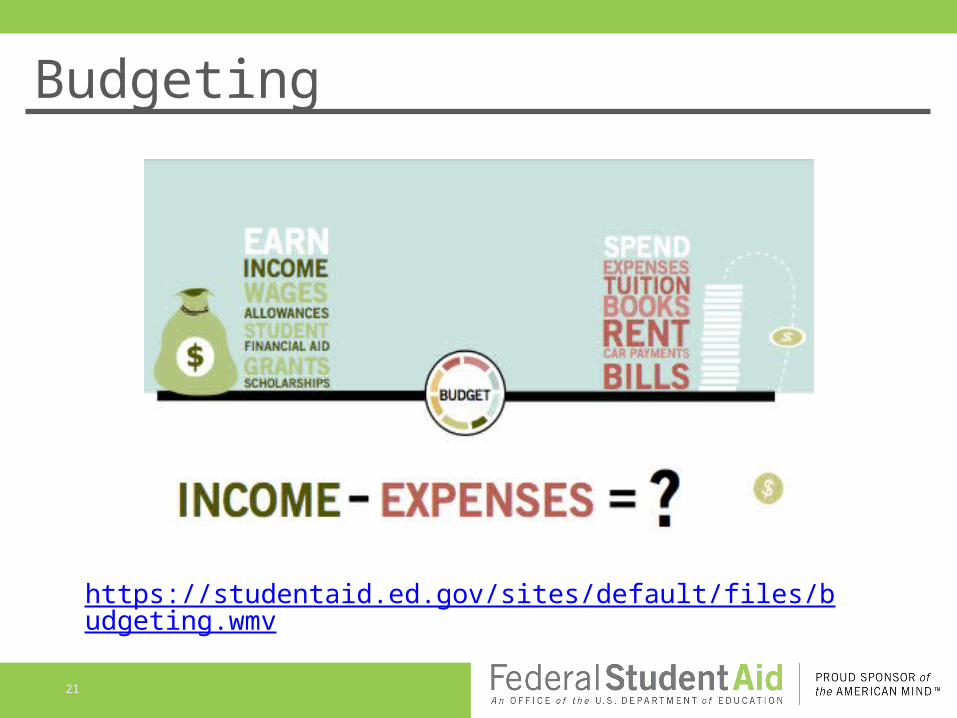

Budgeting Borrowing Repayment Strategies

21

Budgeting

https://studentaid.ed.gov/sites/default/files/budgeting.wmv

•Only borrow what is needed• Free money first• Federal loans vs. private loans

•Keep track of what is being borrowed

•Know what is owed prior to entering repayment

•Pay interest while in school

22

Basics for Borrowers

23

Financial Awareness Counseling ToolThe Financial Awareness Counseling Tool (FACT) is on Studentloans.gov

24

Financial Awareness Counseling ToolExpenses Funds

The Financial Awareness Counseling Tool (FACT) is on Studentloans.gov

How Schools Are Using FACT

Incorporating FACT into the financial aid process

• Encourage completion of FACT before disbursement of any loan

• Direct students to FACT after completing promissory note

Utilizing FACT as a resource

• Include as part of annual loan counseling on default aversion

• Incorporate into student success courses

• Direct link on financial aid office home page

25

Repayment Strategies

Basic fundamentals of a loan• Loan fees• Interest rates

• Capitalized interest• Daily interest formula

Rights and responsibilities• Benefits of a federal loan

Loan servicer• Know who to contact and how

26

27

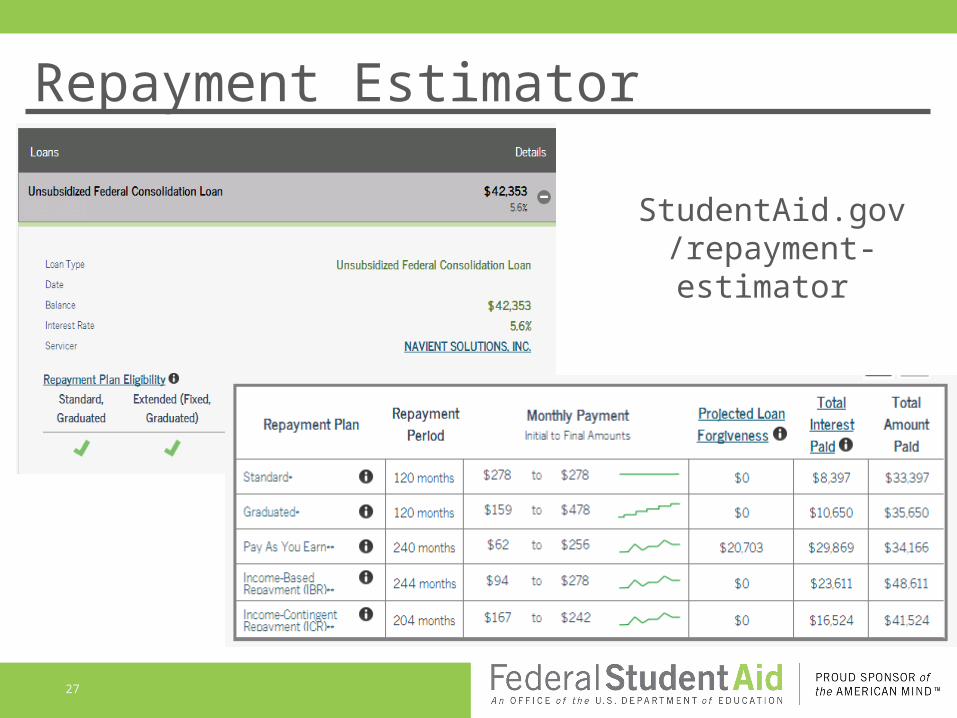

Repayment Estimator

StudentAid.gov/repayment-estimator

28

StudentAid.gov My Federal Student AidNEWNEW

FSA Publications

29

StudentAid.gov/Resources

30

FSA on Social Media

Leverage FSA’s social media messages to do your own outreach

http://www.financialaidtoolkit.ed.gov/tk/outreach/social-media.jsp

Videos

31

Infographics

http://visual.ly/users/federalstudentaid

Financial Aid Toolkitwww.financialaidtoolkit.ed.gov

33

Financial Aid Toolkit: Financial Literacy

34

Search for Financial Literacy Resources

Successful Outreach

35

Campus-Based

•Presentation to freshmen and transfers•Program for students and alumni for career exposure and loan management•One credit course on financial education•Financial Wellness part of Office of Student Services, Student Health•Money management fairs with prizes•Financial literacy for students with SAP issues •Students and teachers provide free tax assistance and financial literacy information•Deliver to athletic teams and housing students

Successful Outreach

36

Delivery Methods

•Peer counselors trained for personal finance counseling/coaching•Financial Aid office provides sub for absent professors•Near-to-peer counselors deliver to secondary students•One-on-one counseling/coaching

Third Party Resources

•Loan servicers•Non-profit organizations•State and regional associations•Mymoney.gov

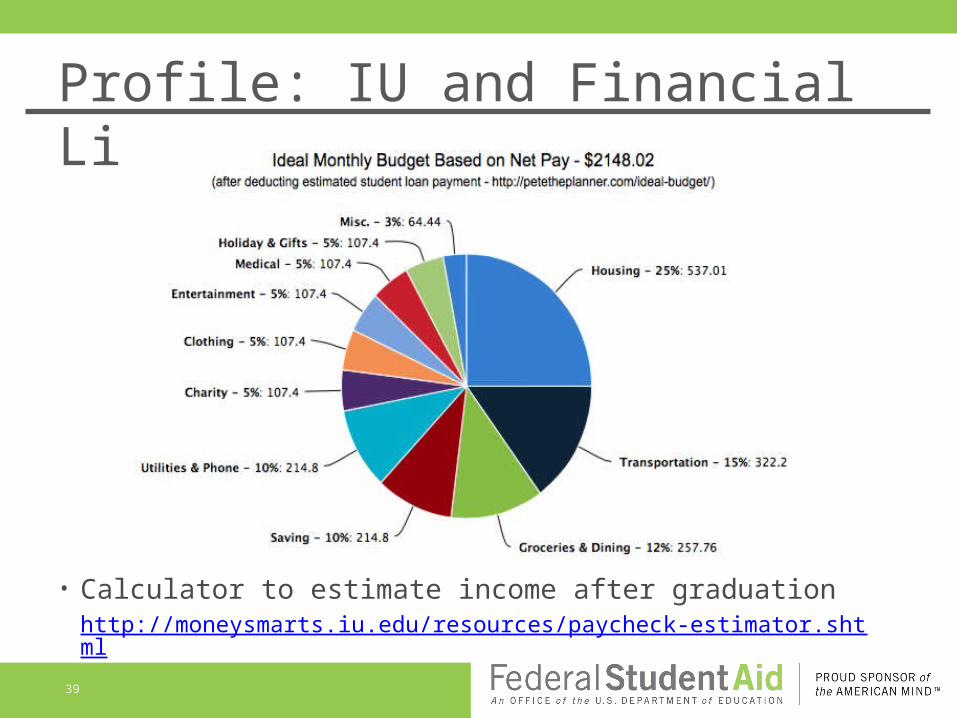

Profile: IU and Financial Literacy

37

• New Office of Financial Literacy

• MoneySmarts.iu.edu portal for financial literacy programs

• One credit courses on financial management

• Peer-to-peer advising SOURCE: http://news.iu.edu/releases/iu/2014/02/fewer-students-borrowing.shtml

Profile: IU and Financial Literacy • Annual “debt letter”

explaining how much students owe and the estimated amount of their monthly payments

• Results: borrowing decreased by 12% from 2012/13 to 2013/14

• Standardized student aid letter that clearly separates grants from loans

38

Profile: IU and Financial Literacy

• Calculator to estimate income after graduationhttp://moneysmarts.iu.edu/resources/paycheck-estimator.shtml

39

Share Your Best Practices

40

41

QUESTIONS?