electricity market reform - gov.uk

TRANSCRIPT

June 2013

Electricity Market Reform: Delivering UK Investment

Electricity Market Reform: Delivering UK Investment

Presented to Parliament by the Secretary of State for Energy and Climate Change

by Command of Her Majesty

June 2013

Cm 8674 £6.25

http://www.nationalarchives.gov.uk/doc/open-government- licence/ or e-mail: [email protected]. Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned. Any enquiries regarding this publication should be sent to us at [email protected] You can download this publication from https://www.gov.uk/government/publications/electricity-market-reform-684

© Crown copyright 2013 You may re-use this information (excluding logos) free of charge in any format or medium, under the terms of the Open Government Licence. To view this licence, visit http://www.nationalarchives.gov.uk/doc/open-government-licence/ or e-mail: [email protected]. Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned. Any enquiries regarding this publication should be sent to us at [email protected] You can download this publication from https://www.gov.uk/government/publications/electricity-market-reform-

ISBN: 9780101867429 Printed in the UK by The Stationery Office Limited on behalf of the Controller of Her Majesty’s Stationery Office ID P002571270 06/13 Printed on paper containing 75% recycled fibre content minimum.

delivering-uk-investment.

Electricity Market Reform: Delivering UK Investment

5

Contents

Introduction ................................................................................................................................................ 6

Delivering UK Investment .......................................................................................................................... 6

Ensuring reliable electricity supplies for consumers ................................................................................... 6

Tackling climate change through investment in low-carbon generation ..................................................... 7

CfD strike prices ..................................................................................................................................... 7

CfD contract terms: decisions on approach ............................................................................................ 8

Building the UK supply chain .................................................................................................................. 8

Supporting early renewables projects ..................................................................................................... 8

Trading renewable electricity: Government response to call for evidence .............................................. 9

Keeping electricity bills down and protecting the consumer ................................................................... 9

Next Steps ................................................................................................................................................. 10

Devolution ................................................................................................................................................. 10

APPENDIX A: Levy Control Framework and Draft CfD Strike Prices .................................................. 12

APPENDIX B: Policy on CfD Terms ........................................................................................................ 15

Electricity Market Reform: Delivering UK Investment

6

Introduction 1. Electricity Market Reform (EMR) will deliver the greener energy and reliable supplies that the

country needs, at the lowest possible cost. It will transform the UK electricity sector to one where low-carbon can compete with conventional, fossil-fuel generation – ensuring we build the right mix of generation for the long-term.

2. Around a fifth of our power stations are due to close over the coming decade and consumers are facing rising energy costs due to growing dependence on uncertain supplies of imported fossil fuels, so now is the time to move towards a diverse and low-carbon electricity mix.

3. This presents a huge opportunity for growth and jobs, with EMR designed to unlock up to £110 billion investment in our electricity infrastructure and support up to 250,000 jobs during this decade alone. The electricity sector is one of the biggest areas in the UK economy for investment over this decade and the Government is keen to support industry to maximise this potential. This is why we have brought forward the key announcements that will give industry the early certainty they need on EMR to begin planning major capital investments in the UK and its supply chain.

Delivering UK Investment

Ensuring reliable electricity supplies for consumers

4. The country faces increasing risks to providing secure and reliable electricity supplies. New capacity is needed to replace retiring coal, nuclear and older gas power stations – which have historically provided us with significant amounts of predictable and flexible generation. It is therefore crucial that we deliver new investment, and that the market brings this forward in a world where we move to a more diverse portfolio of generation such as new nuclear power, onshore and offshore wind, and gas. The amount of gas capacity we will need to call on at times of peak demand will remain high, with potentially significant amounts of new gas generating capacity required by 2030. Other forms of capacity – such as demand side response1 – also have significant potential to ensure we continue to enjoy secure supplies.

5. This is why the Government has today set out further details about the proposed Capacity Market – including how and when it will run – which will provide steady payments to incentivise a range of reliable forms of capacity such as gas-fired generation and demand-side response. In particular we are announcing to investors that, subject to state aid approval, we will run the first capacity auction in 2014 which will result in construction of new capacity that will be available from 2018/19. We are also continuing to explore how projects that result in permanent reductions in electricity demand can participate in the Capacity Market and the Government has announced that funding will be available for a pilot.

6. Further detail on this and the detailed design of the Capacity Market has been published today2, along with announcements from Ofgem and National Grid on future electricity

1 Where large electricity users reschedule or temporarily reduce their demand for electricity. 2 https://www.gov.uk/government/publications/electricity-market-reform-capacity-market-proposals

Electricity Market Reform: Delivering UK Investment

7

margins (including measures to address potential short and medium-term risks, ahead of the Capacity Market delivering new reliable capacity towards the end of this decade).

Tackling climate change through investment in low-carbon generation

7. To bring forward the billions of pounds of investment needed in new, low-carbon electricity generation and associated network infrastructure, the Government is publishing key information on Contracts for Difference (CfDs).

8. CfDs provide efficient and long term support for low carbon generation – including nuclear, renewables and carbon capture and storage – reducing risks faced by generators by increasing revenue certainty and through the backing of a long-term contract. Generators will receive revenue from selling their electricity into the market as usual, but will also receive a top-up to a pre-agreed ‘strike price’. Conversely, if the market price is higher than the strike price then the generator must pay back the difference, which reduces costs to consumers when electricity prices are high.

9. The CfD reduces costs to developers of financing a project, by reducing exposure to volatile wholesale prices and reducing project risks. It also provides investors with a familiar legal framework by establishing a CfD as a private law contract, with a single Government-owned counterparty that can raise money from electricity suppliers.

10. For CfDs to deliver their huge potential for growth, developers and investors need to know the strike prices and key contract terms that affect risk and value – such as contract length, change in law protection and inflation indexation. This will support timely investment decisions and allow developers to make financial commitments which will deliver benefits across the UK and to local supply chains. Announcements on these crucial areas are set out below, along with other important updates.

CfD strike prices

11. We have today published the draft strike prices for renewables technologies that help achieve the Government’s objectives on renewables and low-carbon generation. They enable a technology mix that is value for money for consumers, along with the upper limits on annual spending on low-carbon generation (including CfDs, the Renewables Obligation and the small scale Feed-in Tariff) as agreed in the Levy Control Framework3. The draft strike prices are set out in Appendix A and are informed by analysis from National Grid, who assessed the impact of different strike prices on the Government’s objectives of tackling climate change, ensuring security of supply and minimising costs to consumers.

12. The strike prices for key technologies come down over time showing that as technology costs come down, consumers will be paying less. These strike prices are set to be consistent with the Renewables Obligation4 levels of support (though adjusted down as the CfD protects the investor against additional risks), allowing continuity and continued investment in the renewable energy industry. They will enable over 30% of Britain’s electricity to come from renewable energy sources by 2020.

13. A Panel of Technical Experts was appointed to scrutinise National Grid’s analysis and its report will be published in July, alongside consultation on the draft EMR Delivery Plan which

3 The mechanisms and headroom arrangements underpinning the Levy Control Framework remain unchanged. 4 The existing support scheme for large-scale renewable generation.

Electricity Market Reform: Delivering UK Investment

8

will set out more detailed information on the draft strike prices. The Panel was appointed in February 20135. Since then, the Panel has been working alongside National Grid and reporting informally to DECC throughout the analytical process to enable them to scrutinise the analysis.

14. The conversion from the level of support under the Renewables Obligation into a CfD price takes into account a number of elements. This includes the current projections for wholesale prices; the level of support being for 15 years as opposed to 20 years (except in certain cases such as biomass conversion); the indexation to the Consumer Price Index (as opposed to the Retail Price Index); Power Purchase Agreement terms; the effective tax rate of an average developer; and the lower cost of capital as a result of the increased price certainty afforded by the CfD.

CfD contract terms: decisions on approach

15. We have worked with developers and investors on the design of the CfD, to ensure it provides a robust legal framework against which to secure investment in the UK. Today we are publishing, at Appendix B, our approach to the key terms which will form the basis for the final CfD contracts, the drafting of which will be discussed with stakeholders over the summer.

16. As well as providing the necessary safeguards and assurances for industry – such as protections against changes in law that target a particular project or technology – the contract will provide value for money for consumers by reducing the overall costs of attracting investment and by including provisions to ensure the timely construction of low-carbon generation.

Building the UK supply chain

17. The Government has been working with industry to produce three outward facing Energy Industrial Strategies. These will ensure innovative and cost competitive supply chains are able to develop in time to serve growing parts of the energy industry, and will ensure that the UK sees a wider economic benefit associated with the investment coming forward in the electricity sector – building on consumer support for low carbon technologies.

18. The nuclear and oil and gas industrial strategies have been published6, and we will publish the offshore wind industrial strategy in mid-July. The Government is looking to developers to engage proactively with the supply chain, and where possible design their projects in a manner that supports the development of a sustainable and competitive supply chain, with potential to reduce costs in the medium/long term.

Supporting early renewables projects

19. To facilitate support for early renewables projects, we have today published a second update on the Final Investment Decision Enabling for Renewables project7. This signals the start of

5 Details of the Panel members and their terms of reference are available at: https://www.gov.uk/government/news/new-appointments-announced-to-decc 6 https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/175480/bis-13-748-uk-oil-and-gas-industrial-strategy.pdf https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/168048/bis-13-627-nuclear-industrial-strategy-the-uks-nuclear-future.pdf 7 https://www.gov.uk/government/publications/increasing-certainty-for-investors-in-renewable-electricity-final-investment-decision-enabling-for-renewables

Electricity Market Reform: Delivering UK Investment

9

the process for renewable electricity developers experiencing investment hiatus to apply for Investment Contracts (an early form of CfD). It sets out the process and indicative timetable for developers to apply for Investment Contracts, as well as details of the evaluation criteria which they will be assessed against.

Trading renewable electricity: Government response to call for evidence

20. The Government is looking at how to enable industry to export renewable electricity out of the UK, as well as enabling it to be imported from qualifying generators. A Call for Evidence was launched in April 2012 and our response to this has now been published on DECC’s website8. This:

recognises that importing electricity could be an attractive opportunity with much potential;

confirms that Government is minded to take up some level of physical trading so long as it can be made to work; and

outlines the further actions it is taking in order to overcome barriers to trade in renewable energy.

21. Final decisions will be announced at the end of the year.

Keeping electricity bills down and protecting the consumer

22. Electricity Market Reform is good for the consumer. As well as reducing the exposure to volatile and rising fossil fuel prices, the CfD ensures that generators pay back when the price of electricity goes too high; this makes it more efficient at delivering low-carbon generation. CfDs will make it cheaper to deliver low-carbon generation by around £5 billion up to 20309 because they will deliver cost of capital reductions that cannot be achieved through existing policy instruments. The wider benefits of CfDs will be considered in the next revision of the EMR Impact Assessment (as set out below).

23. The most recent Impact Assessment10 estimated average annual household electricity bills to be 6-8% (£38 – £53) lower over the period 2016 to 2030 under EMR, compared to decarbonising through existing policy instruments. Our analysis is being updated to take into account the draft strike prices published in this document, including the price and bill savings for different types of consumer, and a further Impact Assessment will be published alongside the draft EMR Delivery Plan in July.

24. The overall support will reduce over time, as reflected by the draft strike prices (see Appendix A), to take into account the cost reductions we expect to see as a technology becomes more mature. This will ensure that support is targeted only where it helps a technology to become competitive, and maximises value for consumers.

8 https://www.gov.uk/government/publications/response-to-call-for-evidence-on-renewable-energy-trading 9 This captures the impact of a reduced cost of capital under CfDs. Net Present Value up to 2030 (in 2012 prices). 10 https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/197904/cfd_ia_may_update.pdf

Electricity Market Reform: Delivering UK Investment

10

Next Steps 25. Over the coming months we will continue to work with developers and other stakeholders on

the development of Electricity Market Reform. We will publish the draft EMR Delivery Plan for consultation in July, including information on the methodology and analysis behind the draft CfD strike prices, as well as the proposed draft reliability standard which will inform the level of capacity to contract through the Capacity Market. A ten-week consultation will begin following the publication of that document.

26. We will engage with stakeholders through a number of workshops to be held over the summer during the consultation period – details of which will be published on DECC’s website. These interactive sessions will be held to explain the way we have arrived at our proposed strike prices in more detail and provide an opportunity for stakeholders to ask questions before finalising any written responses they may wish to make to the consultation.

27. Final strike prices will be set in December 2013 (subject to state aid and Royal Assent of the Energy Bill). We will also confirm the level of the reliability standard for the Capacity Market at this point.

28. We will publish further detail on the CfD contract terms in early August, including draft contract terms for all the key terms which go to the value of the CfD contract. At the same time, we will set out more detail on the allocation of CfDs, and the Government response to the call for evidence on the CfD supplier obligation. We will engage with interested stakeholders on the detailed drafting of the CfD contract, with two events in August to seek views. The final contract drafting will be published in December alongside the final strike prices, and implemented through regulations laid before Parliament in 2014.

29. In parallel, the Government will consult on the secondary legislation for the implementation of EMR from October this year. The EMR programme is on track to be implemented in 2014, with the first CfDs under the generic regime expected to be signed in the second half of 2014, and the first capacity auction at the end of 2014.

30. Finally – alongside the draft EMR Delivery Plan – we will publish a consultation on the transition arrangements from the Renewables Obligation, the current support mechanism for large-scale renewable generation, to CfDs. These arrangements will ensure that this transition is smooth and straightforward for investors and developers, maintaining confidence in the support landscape.

31. The announcements in this document are subject to state aid approval. The Government is in discussion with the European Commission to secure this.

Devolution

32. EMR will benefit consumers in all parts of the UK – delivering green growth and jobs, reliable supplies of electricity and at least cost. It will provide a consistent and integrated framework for investors, which is essential if we are to attract the private capital we need.

33. The draft strike prices published for consultation are underpinned by analysis conducted by DECC, National Grid and the System Operator Northern Ireland (SONI), and analysis has been shared and discussed with the Devolved Administrations through the Devolved Administration Consultation Group. We will continue to develop this engagement before the strike prices are set in the final Delivery Plan. We will also be seeking to agree a

Electricity Market Reform: Delivering UK Investment

11

Memorandum of Understanding on how the UK Government and Devolved Administrations will work together on EMR on an ongoing basis.

34. Following a joint research project with the Scottish Government on how to support renewables on Scottish islands, we are committed to taking forward work to consider how to provide additional support. The strong emerging option is to provide a separate strike price for renewables projects located on such islands (where these have clearly distinct characteristics to typical mainland projects). We expect further consideration of this emerging option to feed into a consultation on this issue in the summer. This consultation will consider what level of additional support would be appropriate, as well as deliverability, the potential impact on deployment, and affordability. We will take forward this work in time to allow a differential strike price to be set for these projects in the final Delivery Plan in December.

35. We will continue to work with Department of Enterprise, Trade and Investment in Northern Ireland on their decision on applying these strike prices in Northern Ireland, thus enabling a coherent UK-wide system for supporting low-carbon generation.

AP

PE

ND

IX A

: L

evy

Co

ntr

ol F

ram

ewo

rk a

nd

Dra

ft C

fD S

trik

e P

rice

s

Lev

y C

on

tro

l F

ram

ewo

rk –

Up

per

Lim

its

on

Sp

end

(£m

) (2

011/

12 p

rice

s)11

2014

/15

2015

/16

2016

/17

2017

/18

2018

/19

20

19/2

0 20

20/2

1

3,30

0 4,

300

4,90

0 5,

600

6,45

0 7,

000

7,60

0

Ren

ewab

le T

ech

no

log

y D

raft

Str

ike

pri

ces

(£/M

Wh

) (2

012

pri

ces)

P

ote

nti

al 2

020

Dep

loym

ent

Sen

siti

viti

es

(su

bje

ct t

o V

fM a

nd

co

st

red

uct

ion

) (G

W)12

20

14/1

5 20

15/1

6 20

16/1

7 20

17/1

8 20

18/1

9

Adv

ance

d C

onve

rsio

n T

echn

olog

ies13

(w

ith o

r w

ithou

t C

HP

14)

155

155

150

140

135

c. 0

.3

Ana

erob

ic D

iges

tion

(with

or

with

out

CH

P)

145

145

145

140

135

c. 0

.2

Bio

mas

s C

onve

rsio

n15

10

5 10

5 10

5 10

5 10

5 1.

2 –

4

Ded

icat

ed B

iom

ass

(with

CH

P) 1

6 17

120

120

120

120

120

c. 0

.3

Ene

rgy

from

Was

te (

with

CH

P)18

90

90

90

90

90

c.

0.5

11 C

ontr

ol to

tals

for

the

Levy

Con

trol

Fra

mew

ork

will

be

set i

n no

min

al te

rms

at th

e re

leva

nt S

pend

ing

Revi

ew.

12 D

epen

dent

on

indu

stry

cos

t red

uctio

ns o

ver t

ime

– fig

ures

are

not

Gov

ernm

ent f

orec

asts

and

do

not i

nclu

de d

eplo

ymen

t sup

port

ed u

nder

the

smal

l-sca

le F

eed-

In T

ariff

.

13 S

tand

ard

and

adva

nced

gas

ifica

tion

and

pyro

lysi

s, in

clud

ing

adva

nced

bio

liqui

ds.

14 C

ombi

ned

Hea

t and

Pow

er.

15 B

ased

on

biom

ass

cont

ract

s ce

asin

g to

pay

in 2

027.

16

The

pol

icy

of w

heth

er a

nd h

ow d

edic

ated

bio

mas

s w

ill b

e su

ppor

ted

unde

r Cf

Ds

will

be

conf

irm

ed w

ithin

the

draf

t EM

R D

eliv

ery

Plan

, pub

lishe

d in

July

201

3.

17 T

he d

raft

str

ike

pric

e is

bas

ed o

n th

e as

sum

ptio

n th

at D

edic

ated

Bio

mas

s CH

P ge

nera

tors

can

app

ly fo

r the

cur

rent

(1p/

kWh)

Ren

ewab

le H

eat I

ncen

tive

(RH

I) la

rge

biom

ass

tari

ff.

This

as

sum

ptio

n al

so a

pplie

s to

oth

er te

chno

logi

es w

ith C

HP.

Rev

ised

RH

I tar

iffs

wer

e co

nsul

ted

on in

Sep

tem

ber

2012

and

a G

over

nmen

t res

pons

e is

pen

ding

. D

ECC

may

adj

ust t

he D

edic

ated

Bi

omas

s CH

P st

rike

pri

ce (a

nd o

ther

tech

nolo

gies

with

CH

P) o

nce

RHI t

ariff

s ha

ve b

een

conf

irm

ed.

18 E

nerg

y fr

om w

aste

with

out C

HP

is n

ot s

uppo

rted

und

er C

fDs,

whi

ch is

con

sist

ent w

ith th

e po

sitio

n un

der

the

Rene

wab

les

Obl

igat

ion.

12

Electricity Market Reform: Delivering UK Investment

The

uppe

r en

d of

the

offs

hore

win

d ra

nge

is r

each

ed if

cos

ts c

ome

dow

n to

mee

t ind

ustr

y as

pira

tions

and

ther

e is

som

e de

lay

to n

ucle

ar a

nd C

CS b

uild

out

.

Geo

ther

mal

(w

ith o

r w

ithou

t CH

P)19

12

5 12

0 12

0 12

0 12

0 <

0.1

Hyd

ro20

95

95

95

95

95

c.

1.7

Land

fill G

as

65

65

65

65

65

c. 0

.9

Offs

hore

Win

d 15

5 15

5 15

0 14

0 13

5 8

– 16

Ons

hore

Win

d 10

0 10

0 10

0 95

95

9

– 12

Sew

age

Gas

85

85

85

85

85

c.

0.2

Larg

e S

olar

Pho

to-V

olta

ic

125

125

120

115

110

2.4

– 3.

2

Tid

al S

trea

m21

30

5 30

5 30

5 30

5 30

5 c.

0.1

W

ave22

30

5 30

5 30

5 30

5 30

5

Not

es:

F

urth

er d

etai

l will

be

publ

ishe

d in

Jul

y, a

s pa

rt o

f co

nsul

tatio

n on

the

dra

ft E

MR

Del

iver

y P

lan.

E

xpec

ted

depl

oym

ent u

nder

thes

e st

rike

pric

es is

bro

adly

con

sist

ent w

ith d

eplo

ymen

t sce

nario

s pr

esen

ted

in th

e R

enew

able

s R

oadm

ap23

an

d re

flect

s ne

w c

ost a

ssum

ptio

ns a

nd th

e gr

owth

fig

ures

ann

ounc

ed a

t B

udge

t 201

3.

The

y ar

e su

bjec

t to

chan

ge p

rior

to p

ublic

con

sulta

tion

in J

uly

2013

, as

par

t of

the

draf

t EM

R D

eliv

ery

Pla

n.

19 T

he p

ropo

sed

stri

ke p

rice

s fo

r ge

othe

rmal

hav

e be

en s

et w

ith th

e ai

m o

f giv

ing

equi

vale

nt r

etur

ns fr

om in

vest

men

t as

coul

d be

acc

rued

und

er th

e RO

. The

Gov

ernm

ent h

as c

omm

issi

oned

an

ext

erna

l rep

ort o

n th

e po

tent

ial o

f geo

ther

mal

pow

er in

the

UK

– du

e to

con

clud

e in

July

– a

nd it

s fin

ding

s w

ill b

e in

corp

orat

ed in

set

ting

the

final

str

ike

pric

es.

20 F

or la

rger

hyd

ro p

roje

cts,

DEC

C w

ill c

onsi

der

how

bes

t to

pric

e Cf

Ds

and

the

appr

opri

ate

leng

th o

f con

trac

ts o

n a

case

by

case

bas

is, s

imila

r to

the

prop

osed

app

roac

h fo

r Ti

dal R

ange

. 21

The

str

ike

pric

es fo

r Ti

dal S

trea

m a

nd W

ave

are

inte

nded

for

the

first

30

MW

cap

acity

of a

ny p

roje

ct.

For

high

er c

apac

ity p

roje

cts,

sup

port

for t

he a

dditi

onal

MW

will

be

set a

t the

off

shor

e w

ind

stri

ke p

rice.

22

As

per

prev

ious

foot

note

. 23

htt

ps:/

/ww

w.g

ov.u

k/go

vern

men

t/up

load

s/sy

stem

/upl

oads

/att

achm

ent_

data

/file

/802

46/1

1-02

-13_

UK_

Rene

wab

le_E

nerg

y_Ro

adm

ap_U

pdat

e_FI

NA

L_D

RAFT

13

Electricity Market Reform: Delivering UK Investment

T

here

is n

o pu

blis

hed

strik

e pr

ice

for

Tid

al R

ange

. In

stea

d, g

iven

the

lack

of c

ost d

ata

avai

lab

le,

DE

CC

will

co

nsid

er h

ow b

est

to p

rice

CfD

s an

d th

e ap

prop

riate

leng

th o

f con

trac

ts fo

r tid

al r

ange

pro

ject

s on

a c

ase

by c

ase

basi

s.

P

leas

e no

te th

at th

ere

are

14 p

ublis

hed

strik

e pr

ices

, in

cont

rast

to th

e 35

Ren

ewab

les

Obl

igat

ion

(RO

) su

ppor

t ban

ds fo

r re

new

able

s.

In

som

e ca

ses,

we

are

offe

ring

one

strik

e pr

ice

to c

over

two

or m

ore

supp

ort

band

s un

der

the

RO

, as

we

are

mov

ing

away

fro

m h

avin

g m

ore

than

one

sup

port

leve

l for

a s

ingl

e te

chno

logy

. In

add

ition

, we

are

not

offe

ring

strik

e pr

ices

for

a n

umbe

r of

RO

tec

hnol

ogie

s at

the

pres

ent

time,

for

exam

ple

due

to s

usta

inab

ility

rea

sons

.

S

ome

tech

nolo

gies

are

offe

red

the

sam

e st

rike

pric

e w

heth

er o

r no

t the

y ar

e C

ombi

ned

Hea

t and

Pow

er (

CH

P)

proj

ects

, as

note

d in

the

tabl

e ab

ove.

C

HP

pro

ject

s w

ill a

lso

rece

ive

supp

ort a

nd r

even

ue fo

r th

e he

at e

lem

ent o

f the

ir ge

nera

tion,

ther

efor

e ov

eral

l the

y w

ill r

ecei

ve g

reat

er

supp

ort

than

non

-CH

P g

ener

ator

s.

Thi

s is

inte

nded

to in

cent

ivis

e C

HP

gen

erat

ion.

14

Electricity Market Reform: Delivering UK Investment

AP

PE

ND

IX B

: P

olic

y o

n C

fD T

erm

s C

fD T

erm

D

escr

ipti

on

D

ecis

ion

Con

trac

t te

rm

Leng

th o

f the

con

trac

t fro

m

poin

t pr

ojec

t is

com

mis

sion

ed

(i.e.

sta

rts

gene

ratin

g).

Co

ntr

act

len

gth

sta

nd

ard

ised

, bu

t fl

exib

ility

to

ad

apt

to t

ech

no

log

y re

qu

irem

ents

R

enew

able

s pr

ojec

ts (

unde

r th

e ‘s

tand

ard’

allo

catio

n m

echa

nism

) –

15 y

ears

of

paym

ents

.

B

iom

ass

conv

ersi

on –

all

cont

ract

s ce

ase

to p

ay in

202

7 (r

egar

dles

s of

sta

rt d

ate)

, co

nsis

tent

with

the

appr

oach

und

er th

e R

enew

able

s O

blig

atio

n an

d re

flect

ing

the

tran

sitio

nal n

atur

e of

the

tec

hnol

ogy.

F

lexi

bilit

y fo

r th

e S

ecre

tary

of S

tate

to a

djus

t con

trac

t ter

m fo

r pr

ojec

ts w

here

te

chno

logy

just

ifies

a d

iffer

ent

dura

tion

(e.g

. nuc

lear

, CC

S, t

idal

ran

ge a

nd

pote

ntia

lly la

rge

hydr

o pr

ojec

ts).

Infla

tion

inde

xatio

n H

ow s

trik

e pr

ices

are

ad

just

ed fo

r in

flatio

n.

Ind

ex-l

inke

d p

aym

ents

S

trik

e pr

ice

fully

inde

xed

100%

to C

onsu

mer

Pric

e In

dex

(CP

I) th

roug

hout

ent

ire

term

.

Ref

eren

ce p

rice

The

diff

eren

ce p

aym

ents

are

ba

sed

on th

e di

ffere

nce

betw

een

the

refe

renc

e pr

ice

(a m

easu

re o

f the

ele

ctric

ity

mar

ket p

rice)

and

the

strik

e pr

ice.

Pay

men

ts b

ased

on

a r

elia

ble

mea

sure

of

the

mar

ket

pri

ce

In

term

itten

t te

chno

logi

es (

e.g.

win

d) –

hou

rly d

ay-a

head

pric

e.

B

asel

oad

tech

nolo

gies

(e.

g. n

ucle

ar)

– se

ason

-ahe

ad p

rice,

mov

ing

to y

ear-

ahea

d pr

ice

whe

n co

nditi

ons

allo

w.

15

Electricity Market Reform: Delivering UK Investment

Ref

inan

cing

W

heth

er to

incl

ude

any

arra

ngem

ents

to r

ecov

er

high

er r

etur

ns f

rom

pro

ject

re

finan

cing

.

Dev

elo

per

s fr

ee t

o r

ecyc

le c

apit

al, c

on

sum

ers

pro

tect

ed b

y p

rice

-set

tin

g p

roce

ss

N

o re

finan

cing

cla

use

in th

e ge

neric

CfD

con

trac

t.

B

ilate

rally

neg

otia

ted

CfD

s fo

r la

rge

proj

ects

may

hav

e di

ffere

nt a

ppro

ache

s,

incl

udin

g po

ssib

le r

efin

anci

ng c

laus

es.

Cha

nge

in la

w

and

othe

r ad

just

men

ts

Pro

tect

ions

giv

en to

de

velo

pers

aga

inst

cer

tain

ch

ange

s in

law

.

Dev

elo

per

s p

rote

cted

ag

ain

st c

han

ges

in

law

th

at t

arg

et a

pro

ject

, te

chn

olo

gy

or

the

CfD

C

ompe

nsat

ion

avai

labl

e fo

r m

ater

ial a

nd u

nfor

esea

ble

chan

ges

in la

w th

at u

niqu

ely

targ

et s

peci

fic te

chno

logi

es, i

ndiv

idua

l pro

ject

s or

CfD

hol

ders

as

a gr

oup.

P

rote

ctio

n al

so c

over

s po

litic

al d

ecis

ions

to s

hut d

own

a ge

nera

tor,

and

gen

eral

ch

ange

s in

law

tha

t ha

ve d

iscr

imin

ator

y ef

fect

s w

ithou

t obj

ectiv

e ju

stifi

catio

n.

P

rote

ctio

n ex

tend

s to

suc

h ch

ang

es in

law

that

lim

it a

gene

rato

r’s a

bilit

y to

eith

er

deliv

er it

s ou

tput

or

to r

ecei

ve a

ppro

pria

te p

aym

ent.

C

ompe

nsat

ion

will

adj

ust

strik

e pr

ices

to

refle

ct 1

00%

of

oper

atin

g co

sts,

a

prop

ortio

n of

cap

ital c

osts

(ta

perin

g ov

er ti

me

) an

d fo

r lo

st r

even

ues,

ove

r th

e te

rm

of th

e C

fD.

P

rote

ctio

n ag

ains

t ce

rtai

n ch

ange

s in

net

wor

k ch

arge

s, r

elat

ing

to th

e co

sts

of th

e ba

lanc

ing

syst

em a

nd tr

ansm

issi

on lo

sses

.

16

Electricity Market Reform: Delivering UK Investment

17

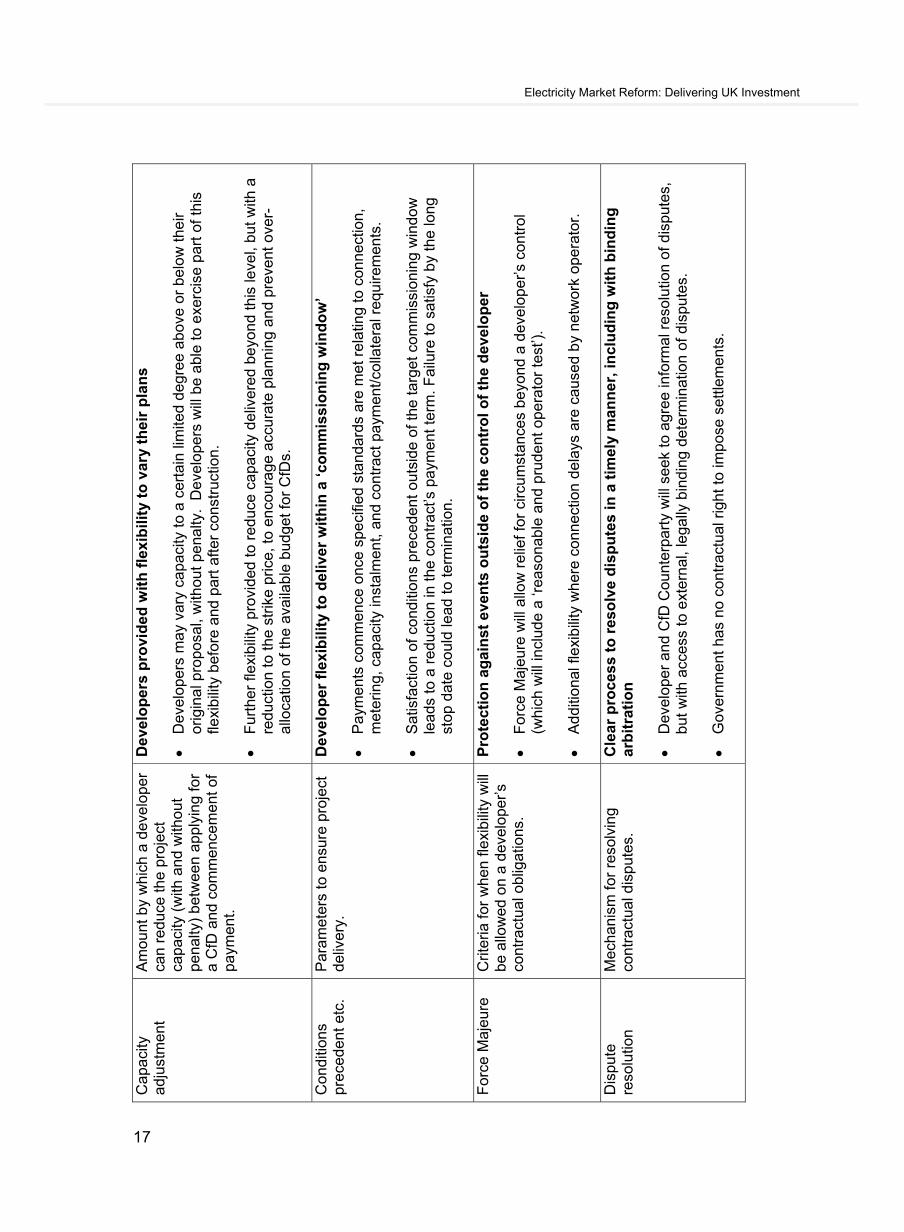

Cap

acity

ad

just

men

t A

mou

nt b

y w

hich

a d

evel

oper

ca

n re

duce

the

proj

ect

capa

city

(w

ith a

nd w

ithou

t pe

nalty

) be

twee

n ap

plyi

ng fo

r a

CfD

and

com

men

cem

ent o

f pa

ymen

t.

Dev

elo

per

s p

rovi

ded

wit

h f

lexi

bili

ty t

o v

ary

thei

r p

lan

s

D

evel

oper

s m

ay v

ary

capa

city

to a

cer

tain

lim

ited

degr

ee a

bove

or

belo

w th

eir

orig

ina

l pro

posa

l, w

ithou

t pen

alty

. D

evel

ope

rs w

ill b

e a

ble

to e

xerc

ise

part

of t

his

flexi

bilit

y be

fore

and

par

t afte

r co

nstr

uctio

n.

F

urth

er fl

exib

ility

pro

vide

d to

red

uce

capa

city

del

iver

ed b

eyon

d th

is le

vel,

but

with

a

redu

ctio

n to

the

strik

e pr

ice,

to e

ncou

rage

acc

urat

e pl

anni

ng a

nd p

reve

nt o

ver-

allo

catio

n of

the

ava

ilabl

e bu

dget

for

CfD

s.

Con

ditio

ns

prec

eden

t etc

. P

aram

eter

s to

ens

ure

proj

ect

deliv

ery.

D

evel

op

er f

lexi

bili

ty t

o d

eliv

er w

ith

in a

‘co

mm

issi

on

ing

win

do

w’

P

aym

ents

com

men

ce o

nce

spec

ified

sta

nda

rds

are

met

rel

atin

g to

con

nect

ion,

m

eter

ing,

cap

acity

inst

alm

ent,

and

cont

ract

pay

men

t/col

late

ral r

equ

irem

ents

.

S

atis

fact

ion

of c

ondi

tions

pre

cede

nt o

utsi

de o

f the

targ

et c

omm

issi

onin

g w

indo

w

lead

s to

a r

educ

tion

in t

he c

ontr

act’s

pay

men

t ter

m. F

ailu

re to

sat

isfy

by

the

long

st

op d

ate

coul

d le

ad to

term

inat

ion.

For

ce M

ajeu

re

Crit

eria

for

whe

n fle

xib

ility

will

be

allo

wed

on

a de

velo

per’s

co

ntra

ctua

l obl

igat

ions

.

Pro

tect

ion

ag

ain

st e

ven

ts o

uts

ide

of

the

con

tro

l of

the

dev

elo

per

F

orce

Maj

eure

will

allo

w r

elie

f for

circ

umst

ance

s be

yond

a d

evel

oper

’s c

ontr

ol

(whi

ch w

ill in

clud

e a

‘rea

sona

ble

and

prud

ent

oper

ator

test

’).

A

dditi

ona

l fle

xib

ility

wh

ere

conn

ectio

n d

elay

s ar

e ca

used

by

netw

ork

oper

ator

.

Dis

pute

re

solu

tion

Mec

hani

sm fo

r re

solv

ing

cont

ract

ual d

ispu

tes.

C

lear

pro

cess

to

res

olv

e d

isp

ute

s in

a t

imel

y m

ann

er, i

ncl

ud

ing

wit

h b

ind

ing

ar

bit

rati

on

D

evel

ope

r an

d C

fD C

ount

erpa

rty

will

see

k to

agr

ee in

form

al r

esol

utio

n of

dis

pute

s,

but

with

acc

ess

to e

xter

nal,

lega

lly b

indi

ng d

eter

min

atio

n of

dis

pute

s.

G

over

nmen

t ha

s no

con

trac

tual

rig

ht t

o im

pose

set

tlem

ents

.

Electricity Market Reform: Delivering UK Investment

Ter

min

atio

n C

ircum

stan

ces

whe

n co

ntra

ct

can

be te

rmin

ated

. A

pro

po

rtio

nat

e ap

pro

ach

to

co

ntr

act

enfo

rcem

ent

In

clud

es m

ater

ial b

reac

hes

of c

ontr

act

by g

ener

ator

s –

such

as,

non

-pay

men

t, fr

aud

and

non-

deliv

ery

of c

apac

ity (

subj

ect

to F

orce

Maj

eure

or

dela

y to

grid

con

nect

ion)

.

M

easu

res

that

enc

oura

ge g

ener

ator

s to

mov

e ba

ck in

to c

ompl

ianc

e w

ith th

e co

ntra

ct e

.g.

‘rem

edia

tion

plan

s’ a

nd p

aym

ent

susp

ensi

on.

Met

erin

g ar

rang

emen

ts

How

low

-car

bon

elec

tric

ity

gene

ratio

n is

rec

orde

d fo

r th

e pu

rpos

es o

f bill

ing.

Arr

ang

emen

ts t

o s

up

po

rt a

wid

e-ra

ng

e o

f p

roje

ct t

ypes

, usi

ng

exi

stin

g p

roce

sses

w

her

e p

oss

ible

Lo

ss a

djus

ted

net m

eter

ed e

nerg

y.

M

akin

g us

e of

exi

stin

g se

ttlem

ent a

rran

gem

ents

, whe

re p

ossi

ble.

A

rran

gem

ents

will

be

deve

lop

ed f

or t

rans

mis

sion

, di

strib

utio

n an

d pr

ivat

e w

ire

gene

ratio

n.

18

Electricity Market Reform: Delivering UK Investment

Department of Energy & Climate Change 3 Whitehall Place London SW1A 2AW www.decc.gov.uk

URN 13D/149

Published by TSO (The Stationery Office) and available from:

Onlinewww.tsoshop.co.uk

Mail, Telephone, Fax & E-mailTSOPO Box 29, Norwich, NR3 1GNTelephone orders/General enquiries: 0870 600 5522Order through the Parliamentary Hotline Lo-Call 0845 7 023474Fax orders: 0870 600 5533E-mail: [email protected]: 0870 240 3701

The Parliamentary Bookshop12 Bridge Street, Parliament SquareLondon SW1A 2JXTelephone orders/General enquiries: 020 7219 3890Fax orders: 020 7219 3866Email: [email protected]: http://www.bookshop.parliament.uk

TSO@Blackwell and other Accredited Agents

ISBN 978-0-10-186742-9

7