el faro project: valuing an lng plant in honduras stan brunson rachel fefer andrew frankel carlos...

TRANSCRIPT

El Faro Project:Valuing an LNG Plant in Honduras

Stan BrunsonRachel Fefer

Andrew FrankelCarlos Sanchez

Emerging Markets Corporate FinanceProf. Campbell Harvey

Fuqua School of Business, Duke UniversityTerm 3, 2002

Case Issue

• Senior investment advisors Carlos Garcia and Stan Johnson must decide…

• Should United Energy invest $25 million for an equity stake in a Central American power plant project?

Agenda

• Background

• Key Parties

• Project Overview

• Financials

• Case Discussion

• Project Valuation and Decision

• Update

Background

• Honduras– Pro-market Stanford-educated President

• Central American electricity market currently fragmented– Puebla-Panamá Plan for regional wholesale

electricity market• $240 million IDB financing support

Key Parties

• AES– U.S. power company– International experience– Equity holder – offering 12.5% stake

• IFC– A-loans– B-loans

• Export Credit Agencies

Project Overview

• $650M: largest project ever in Central America• Construction of LNG power plant in El Faro,

Honduras– Capacity to grow in stages

• Upgrade to existing transmission line• Electricity to be sold below existing market rates

to Honduras, El Salvador, Nicaragua, Guatemala, Costa Rica

Project Integration

El Faro Site

Power Transmission Upgrade

El Faro Project$650M investment

Puebla-Panamá Plan$240M investment

El Faro Site

Artist’s Rendition

1-Steam Turbine3-LNG TurbinesStorage FacilityTerminal

El Faro

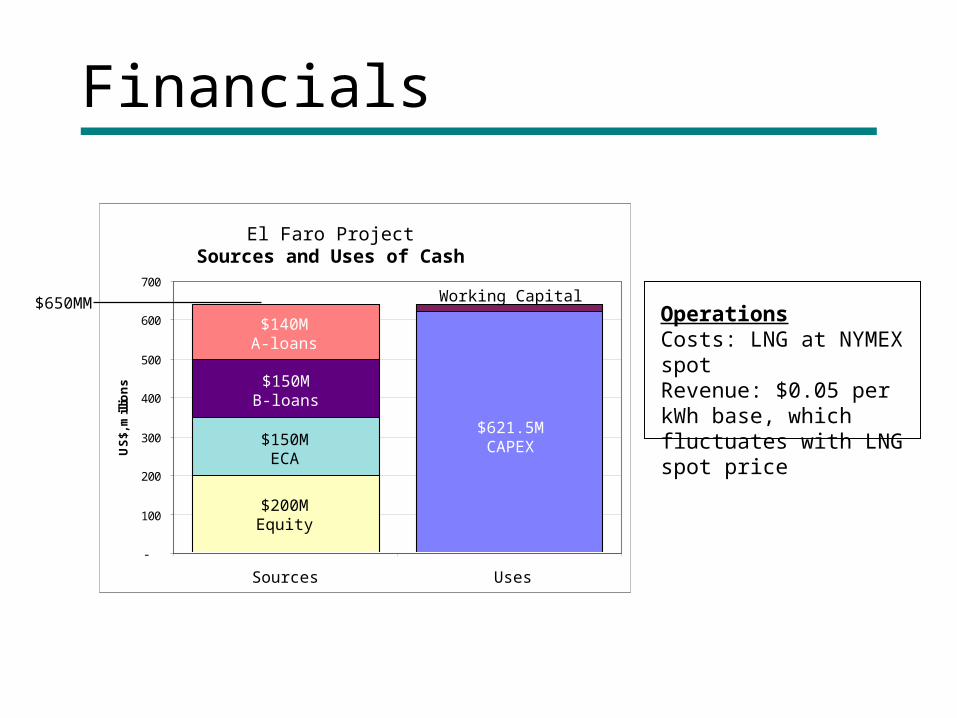

Financials

OperationsCosts: LNG at NYMEX spotRevenue: $0.05 per kWh base, which fluctuates with LNG spot price

El Faro ProjectSources and Uses of Cash

-

100

200

300

400

500

600

700

Sources Uses

US

$, m

illio

ns

$140MA-loans

$150MB-loans

$150MECA

$200MEquity

$621.5MCAPEX

Working Capital

El Faro ProjectSources and Uses of Cash

Sources Uses

$650MM

Case Discussion

• Should United Energy invest in this project?

• How should Carlos and Stan value this investment opportunity?

Major RisksRisk Mitigation

Operational Completion AES experience

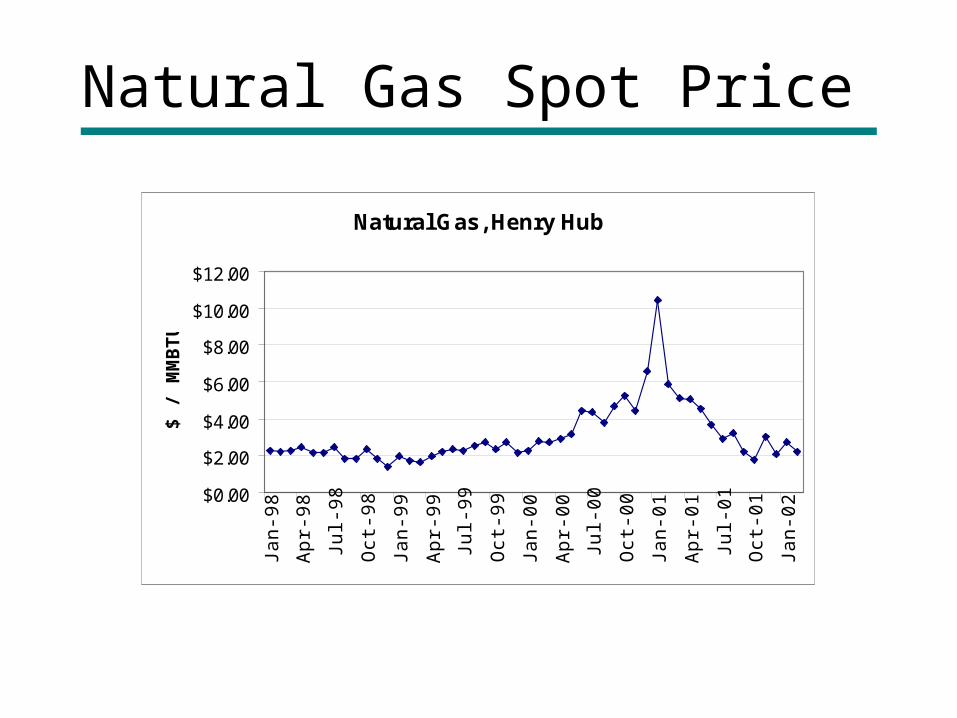

Natural gas price volatility

Some hedging in tariff structure

Sovereign Currency USD denominated

Expropriation IFC involvement

Financial Cost of debt IFC involvement

Natural Gas Spot Price

Natural Gas, Henry Hub

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00Ja

n-9

8

Ap

r-9

8

Jul-

98

Oct

-98

Jan

-99

Ap

r-9

9

Jul-

99

Oct

-99

Jan

-00

Ap

r-0

0

Jul-

00

Oct

-00

Jan

-01

Ap

r-0

1

Jul-

01

Oct

-01

Jan

-02

$ /

MM

BT

U

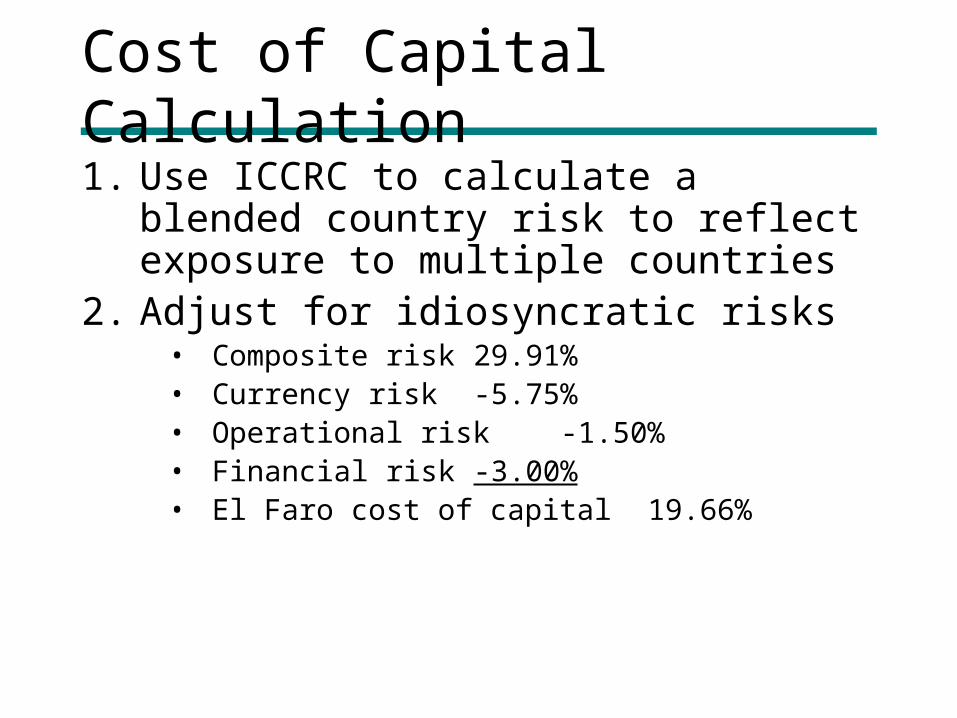

Cost of Capital Calculation

1. Use ICCRC to calculate a blended country risk to reflect exposure to multiple countries

2. Adjust for idiosyncratic risks• Composite risk 29.91%• Currency risk -5.75%• Operational risk -1.50%• Financial risk -3.00%• El Faro cost of capital 19.66%

Project Valuation and Decision

• IRR

• Project valuation: Monte Carlo analysis

• Real options

• Sensitivity analysis

• United Energy recommendation

IRR, Static Results

IRR, Year 10: 18.6%

IRR, Year 15: 25.3%

IRR, Year 20: 26.7%

IRR, Year 25: 27.1%

Cost of Capital: 19.66%

Monte Carlo Results

Abnormal Earnings ModelNPV positive project

LNG price modeled in10-50-90 distribution

Statistics ValuationTrials 5000.00Mean 45713964.13Median 44583056.14Mode ---Standard Deviation 13439785.67Variance 180627838889182.00Skewness 0.41Kurtosis 2.96Coeff. of Variability 0.29Range Minimum 15048155.10Range Maximum 107275218.75Range Width 92227063.65Mean Std. Error 190067.27

Real Options

Best OutcomeBuild LNG 2 and LNG 3 on time

0.8Build LNG 3 On Time

14,084,611$ 14,084,611$ 14,084,611$

0.85 0.15Build LNG 2 On Time Build LNG 3 Delayed

8,330,408$ 0 11,293,362$ 8,330,408$ 8,330,408$

0.05Don't Build LNG 3

(24,477,760)$ (24,477,760)$ (24,477,760)$

0.7Build LNG 3 On Time

5,911,683$ Construct Plant 5,911,683$ 5,911,683$

0 5,665,447$ 0.1 0.2Build LNG 2 Delayed Build LNG 3 Delayed

157,481$ 0 872,789$ 157,481$ 157,481$

0.1Don't Build LNG 3

(32,968,853)$ 1 (32,968,853)$ (32,968,853)$

5,665,447$ 0.05

Don't Build LNG 2(80,423,793)$

(80,423,793)$ (80,423,793)$

Don't Construct0

0 -$

Static Model

Sensitivity Analysis

Terminal Growth RateNot sensitive

Terminal Growth Rate Value

0.020 14,121,208.09$ 0.025 14,103,442.68$ 0.030 14,084,610.77$ 0.035 14,064,613.33$ 0.040 14,043,338.71$

Recommendation

• We recommend investment in this project– NPV positive given electricity pricing

fluctuates with LNG spot price.– Static IRRs higher than cost of capital, except

for IRR at year 10.– Even with construction delays or change to

capacity built, project NPV positive.

Update

• February 19, 2002:– AES announces major divestitures of Latin

American interests

• What will happen to the El Faro Project?