edelweiss investment research · indian metals & ferro alloys ltd. 2 gwm imfa is the most...

TRANSCRIPT

1 GWM

Edelweiss Investment Research

Tactical BUY: Indian Metals & Ferro Alloys Ltd.

Healthy cash flows and attractive valuations to unlock value

Indian Metals & Ferro Alloys Ltd (IMFA) is the largest ferrochrome producer in India; it has

capacity of 275,000 tpa in Odisha with a captive chrome ore mine and coal-based power

plant capacity of 258MW. We believe IMFA would best benefit from the healthy demand for

ferrochrome, the current high realisations and the ongoing auctioning of ferrochrome assets

of bankrupt competitors in India. We expect IMFA to maintain an EBIDTA/tonne of INR

20,000/tonne for FY19–20E compared with INR 21,000/tonne for 9MFY18 due to its balanced

mix of long-term (70%) and short-term contracts (30%). Healthy cash flow generation, limited

capex, is expected to pare net debt by over INR 600 cr to just INR 22 cr by FY20E. We factor in

only a marginal volume growth of 2% due to current capacity constraints. We expect IMFA’s

EBIDTA and PAT to remain flattish, close to INR 500 cr and INR 225 cr, respectively. We

recommend a ‘Tactical BUY’ on IMFA with a target price of INR 733/share, valuing the stock

at EV/EBIDTA of 4x on FY20E basis.

Ferrochrome demand – Related to healthy growth in stainless steel industry

The Indian ferrochrome industry bases its growth on the Indian and global (especially Chinese)

stainless steel (SS) industry. Over the past decade, the global SS industry expanded at a CAGR

of 5.4%, bolstered by a 13.6% growth in China and 6.2% growth in India. Steady investments in

construction, transportation and process industries and increasing consumerism are set to

maintain expansion in the global SS market at a 5% CAGR over FY17–22E. As a primary raw

material in SS with no substitute, worldwide ferrochrome demand in the next 5 years is

expected to rise at a 5% CAGR. President Trump’s protectionism of the US steel industry and

planned impetus for their infrastructure segment could further boost the demand for

ferrochrome in the global market.

Integrated play – Globally competitive, dominant edge

IMFA is the only Indian player with captive chrome ore mines and captive power. As it

depends on the export market for around 80% of its production material, IMFA has to

compete with South African and Chinese ferrochrome producers in terms of cost

effectiveness. With backward integration, IMFA’s production cost matches that of most of the

efficient players in South Africa and it is lower by vast margn as China lacks chrome ore mines.

Increasing power costs in South Africa and pollution concerns in China over ferrochrome

production makes IMFA even more competitive in the global market.

Consolidation in domestic industry could led to capacity expansion

IMFA’s strategy of steady backward integration over aggressive capacity addition helps it

maintain profitability, sometimes over growth. Now, following the rounds of NCLT and bank

auctions of assets of FACOR Alloys and Rohit Ferro, we believe IMFA has a chance to boost

ferrochrome capacity by at least 40% and thus capture global growth opportunities. We

believe it would be able to increase chrome ore mining capacity with the additions. If IMFA

fails to buy assets in these auctions, it alternatively plans brownfield capacity expansion in the

next 1–2 years.

Valuation & recommendation – Lower valuation; strengthening balance sheet to drive upside

Barring capacity additions through auctions or brownfield expansion, there would be a

marginal growth of 2% in volumes over FY17–20E. We also maintain EBITDA at INR 20,000/tonne,

less than the 9MFY18 EBITDA of INR 21,000/tonne. We believe healthy cash flows in the next 2

years would reduce net debt by INR 600 cr. We believe a further strengthening balance sheet

would account for a large part of stock upside. We value the stock at a 2-year forward

EV/EBITDA of 4x, arriving at a target price of INR 733/share.

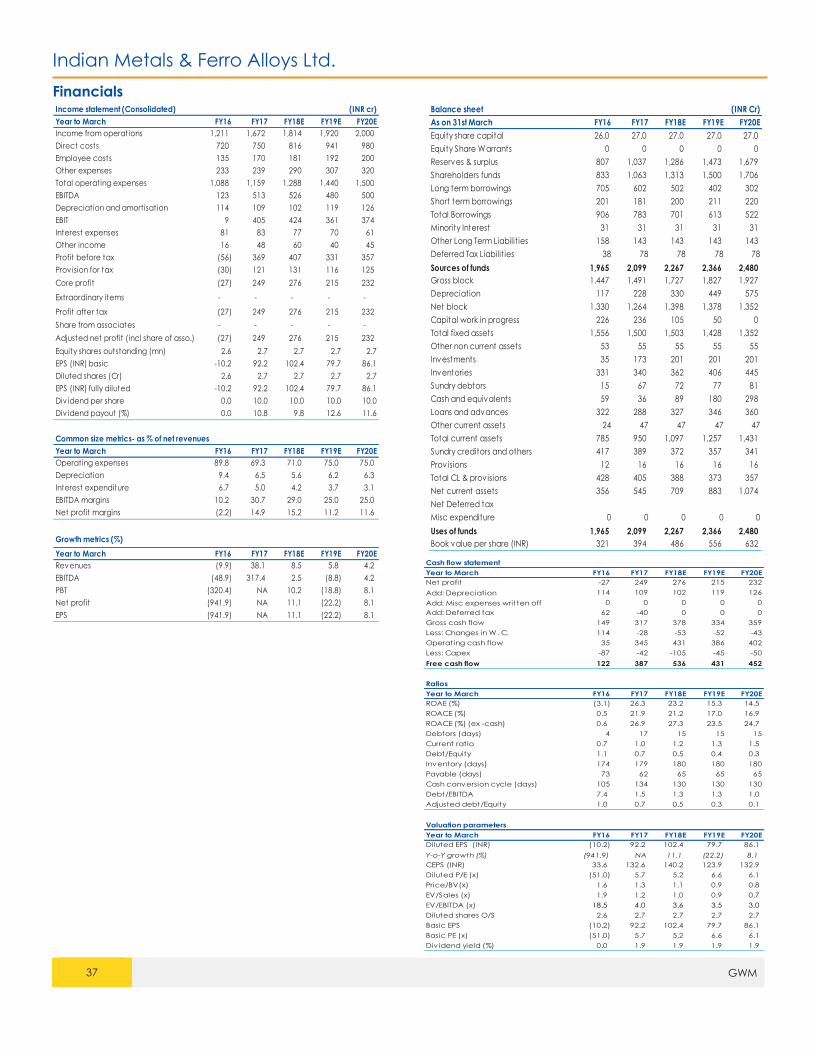

Year to March FY16 FY17 FY18E FY19E FY20E

Revenues (INR Cr) 1,211 1,672 1,814 1,920 2,000

Rev growth (%) (9.9) 38.1 8.5 5.8 4.2

EBITDA (INR Cr) 123 513 526 480 500

Net Profit (INR Cr) (27) 249 276 215 232

P/E (x) (51.0) 5.7 5.2 6.6 6.1

EV/EBITDA (x) 18.5 4.0 3.6 3.5 3.0

RoACE (%) 0.6 26.9 27.3 23.5 24.7

RoAE (%) (3.1) 26.3 23.2 15.3 14.5

CMP INR: 528

Rating: BUY

Target Price INR: 733

Upside: 39%

Salil Utagi

Research Analyst

Harsh Vijay Shah

Research Analyst

Bloomberg: IMFA:IN

52-week

range (INR): 799/ 385

Share in issue

(cr): 2.70

M cap (INR cr): 1,415

Avg. Daily Vol.

BSE/NSE :(‘000): 92

Promoter

Holding (%) 58.69

Date: 10th April 2018

Indian Metals & Ferro Alloys Ltd.

2 GWM

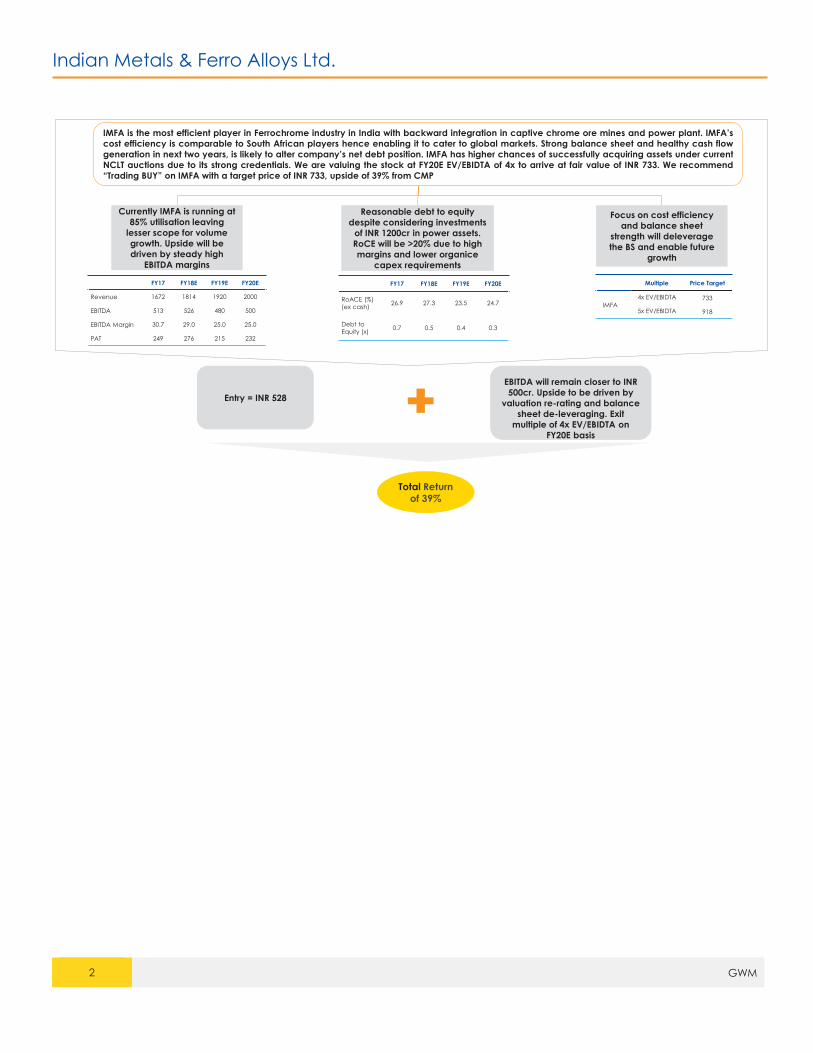

IMFA is the most efficient player in Ferrochrome industry in India with backward integration in captive chrome ore mines and power plant. IMFA’s

cost efficiency is comparable to South African players hence enabling it to cater to global markets. Strong balance sheet and healthy cash flow

generation in next two years, is likely to alter company’s net debt position. IMFA has higher chances of successfully acquiring assets under current

NCLT auctions due to its strong credentials. We are valuing the stock at FY20E EV/EBIDTA of 4x to arrive at fair value of INR 733. We recommend

“Trading BUY” on IMFA with a target price of INR 733, upside of 39% from CMP

Currently IMFA is running at

85% utilisation leaving

lesser scope for volume

growth. Upside will be

driven by steady high

EBITDA margins

Reasonable debt to equity

despite considering investments

of INR 1200cr in power assets.

RoCE will be >20% due to high

margins and lower organice

capex requirements

Focus on cost efficiency

and balance sheet

strength will deleverage

the BS and enable future

growth

FY17 FY18E FY19E FY20E

Revenue 1672 1814 1920 2000

EBITDA 513 526 480 500

EBITDA Margin 30.7 29.0 25.0 25.0

PAT 249 276 215 232

FY17 FY18E FY19E FY20E

RoACE (%)

(ex cash)26.9 27.3 23.5 24.7

Debt to

Equity (x)0.7 0.5 0.4 0.3

Multiple Price Target

IMFA

4x EV/EBIDTA 733

5x EV/EBIDTA 918

Entry = INR 528

EBITDA will remain closer to INR

500cr. Upside to be driven by

valuation re-rating and balance

sheet de-leveraging. Exit

multiple of 4x EV/EBIDTA on

FY20E basis

Total Return of 39%

Indian Metals & Ferro Alloys Ltd.

3 GWM

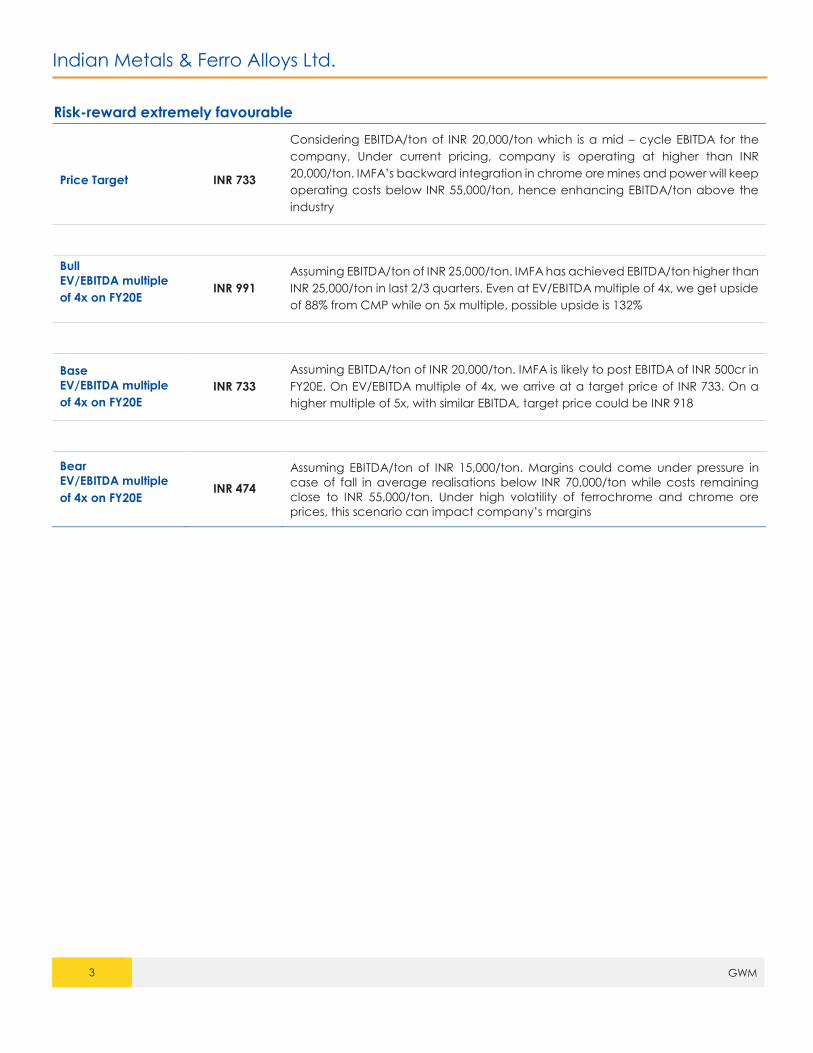

Risk-reward extremely favourable

Price Target INR 733

Considering EBITDA/ton of INR 20,000/ton which is a mid – cycle EBITDA for the

company. Under current pricing, company is operating at higher than INR

20,000/ton. IMFA’s backward integration in chrome ore mines and power will keep

operating costs below INR 55,000/ton, hence enhancing EBITDA/ton above the

industry

Bull

EV/EBITDA multiple

of 4x on FY20E INR 991

Assuming EBITDA/ton of INR 25,000/ton. IMFA has achieved EBITDA/ton higher than

INR 25,000/ton in last 2/3 quarters. Even at EV/EBITDA multiple of 4x, we get upside

of 88% from CMP while on 5x multiple, possible upside is 132%

Base

EV/EBITDA multiple

of 4x on FY20E

INR 733

Assuming EBITDA/ton of INR 20,000/ton. IMFA is likely to post EBITDA of INR 500cr in

FY20E. On EV/EBITDA multiple of 4x, we arrive at a target price of INR 733. On a

higher multiple of 5x, with similar EBITDA, target price could be INR 918

Bear

EV/EBITDA multiple

of 4x on FY20E INR 474

Assuming EBITDA/ton of INR 15,000/ton. Margins could come under pressure in

case of fall in average realisations below INR 70,000/ton while costs remaining

close to INR 55,000/ton. Under high volatility of ferrochrome and chrome ore

prices, this scenario can impact company’s margins

Indian Metals & Ferro Alloys Ltd.

4 GWM

Average Daily Turnover (INR cr) Stock Price (CAGR) Relative to Sensex, CAGR (%)

3 months 6 months 1 year 1 year 3 years 5 years Since Inception 1 year 3 years 5 years Since Inception

5.46 8.27 8.75 -33% 41% 17% 13% -47% 35% 4% -1%

Bu

sin

ess

Va

lue

Driv

ers

Nature of Industry The demand for ferrochrome largely depends on the global demand for SS. The Indian ferrochrome

industry is oligopolistic, with Balasore and IMFA controlling over one-third of this market. By far, IMFA is

the largest integrated ferrochrome manufacturer in India.

Opportunity Size

Global ferrochrome production was 12.03 mn tonnes in 2017; production is expected to grow at a

5.5% CAGR during 2017–21E to ~15 mn tonnes. Demand from China would be the key driver of the

global ferrochrome market. India as a country produced only 1.0–1.1 mn tonnes of ferrochrome, in

which IMFA produced 0.2 mn tonne in FY17, thus creating a huge opportunity for itself going ahead.

Capital Allocation IMFA has been prudent in capital allocation. The management considers both chrome ore mines

and power assets as key raw materials. IMFA will not add any ferrochrome capacity without

complete integration in mines and power

Predictability IMFA’s financials are highly related to the global SS and ferrochrome demand-supply scenario. We

believe that near-term demand from China and India would remain strong owing to visible capex

programs and consumer demand

Sustainability The global SS industry is cyclical in nature but IMFA would have sustainable demand as the

company enters into long term volume contracts for upto 70% of its production

Disproportionate

Future IMFA can achieve high growth in case of acquisition of NCLT assets at a bargain and/or further

sharp jump in average realisation of ferrochrome

Business Strategy &

Planned Initiatives IMFA is bidding for ferrochrome assets to be auctioned in NCLT. If company fails to purchase an

asset in this auction, they will incur capex for brownfield expansion

Near Term Visibility The demand for SS and ferrochrome is expected to remain strong in the near term due to strong

demand from China/India, the two largest global consumer, and one that remains a driver of the

global ferrochrome demand-supply balance.

Long-Term Visibility IMFA’s fortunes are linked to the SS industry cycle and more to the demand-supply balance of

ferrochrome. We believe the rising demand for ferrochrome is sustainable as China’s SS industry is

growing at a faster pace than the ferrochrome industry.

Indian Metals & Ferro Alloys Ltd.

5 GWM

Focus Charts – Story in a nutshell

Global Stainless Steel production forecast China remains global FeCr demand center

China overtakes South Africa as leading FeCr producer Ferrochrome prices – Benchmark up by 20% for Q2

Steady increase in average realisation and EBITDA/tonne

due to operational efficiency

Expect repayment of debt due to steady growth in OCF

Source: Edelweiss Investment Research

48,080

50,484

53,008

55,659

58,442

61,364

40,000

45,000

50,000

55,000

60,000

65,000

2017e 2018e 2019e 2020e 2021e 2022e

Pro

dn

(In

KT)

0

2

4

6

8

10

12

14

2013 2014 2015 2016 2017e 2018f

(In

mn

to

nn

e)

NAFTA European Union Japan

South Korea Others China

India Total

0.0

2.0

4.0

6.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017e

In M

n T

on

ne

s

Brazil EURussia, Turkey & Albania IndiaKazakhstan South AfricaZimbabwe Others

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

De

c,2

010

Ap

r,201

1

Au

g,2

011

De

c,2

011

Ap

r,201

2

Au

g,2

012

De

c,2

012

Ap

r,201

3

Au

g,2

013

De

c,2

013

Ap

r,201

4

Au

g,2

014

De

c,2

014

Ap

r,201

5

Au

g,2

015

De

c,2

015

Ap

r,201

6

Au

g,2

016

De

c,2

016

Ap

r,201

7

Au

g,2

017

De

c,2

017

HC

Fe

Cr

Pric

e (

In U

S $

/Po

un

d)

South Africa(USD/pound Cr)- 50%India(USD/pound Cr)-62%Kazakhstan(USD/pound Cr)-70%EU Benchmark (USD/pound)

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

E

FY

19

E

FY

20

E

Average Realisation (INR) EBITDA/Tonne (INR)

0

100

200

300

400

500

600

700

800

900

1,000

-

100

200

300

400

500

600

700

800

900

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

E

FY

19

E

FY

20

E

INR

in c

rs

INR

in c

rs

Long Term Loans Short Term Loans

Net Debt- RHS

Indian Metals & Ferro Alloys Ltd.

6 GWM

Ferrochrome Industry – Value Chain

Ferrochrome, an alloy of chrome ore and iron ore, is a key raw material in SS production.

Ferrochrome strengthens SS, brings lustre and offers corrosion resistance. Ferrochrome is used in

varying proportions of 10.5–30.0% in SS, depending upon final applications. On average, 25%

ferrochrome is used by weight to make 1 tonne of SS.

Ferrochrome Value Chain

Ferrochrome is an alloy of chromium and iron containing 40–70% chromium by weight.

Ferrochrome is produced by electric arc carbothermic reduction of chromite using coke and

other reductants.

Ferrochrome manufacturing is power-intensive; approximately 2.5 tonnes of chrome ore are

reduced with an estimated 600 kg of met coke and 3,800–4,000 units of power.

The demand for ferrochrome (almost 85%) is highly related to the demand for SS.

1 Tonne of Ferrochrome

(FeCr)

600 Kgs of Met Coke

~2.50 tonnes of Chrome

Ore

3600-4000

units of Power

Stainless Steel

•Accounts for 85% of global ferrochrome end use

Specialised Steel

•Accounts for 10% of global ferrochrome end use

Nickel Alloy & Foundry Products

•Accounts for 5% of global ferrochrome end use

0.25 tonne of

Ferrochrome

1 tonne of Stainless steel

Indian Metals & Ferro Alloys Ltd.

7 GWM

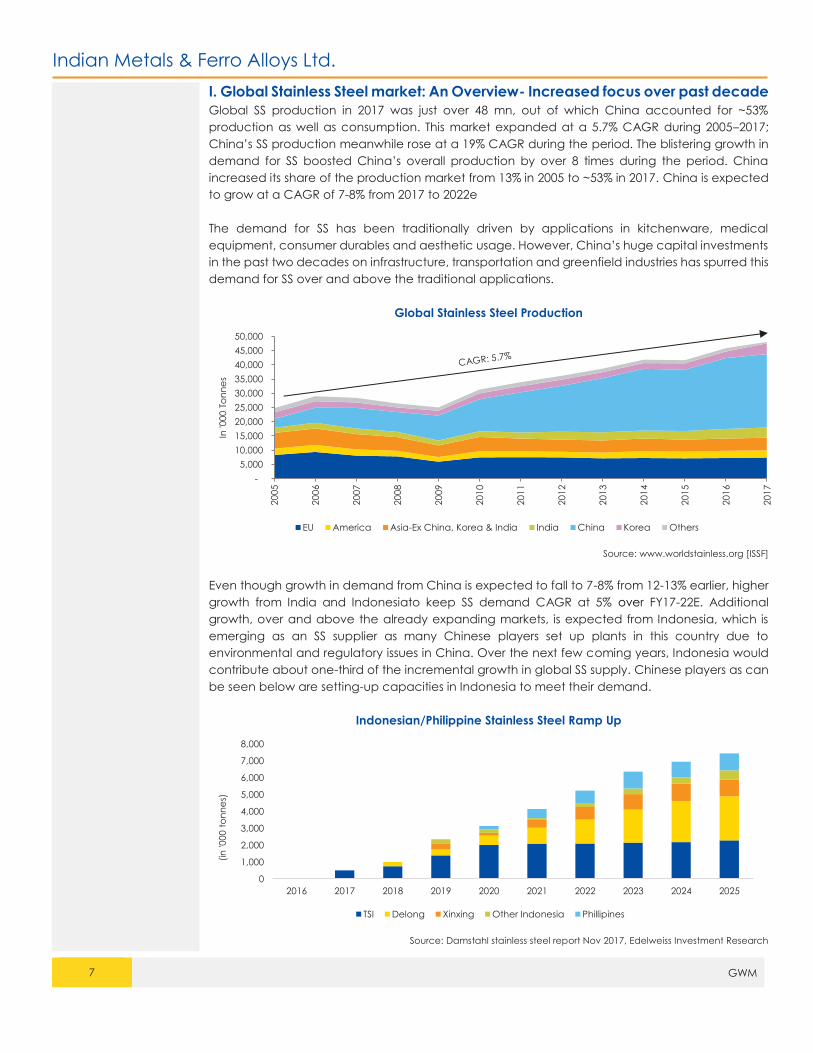

I. Global Stainless Steel market: An Overview- Increased focus over past decade

Global SS production in 2017 was just over 48 mn, out of which China accounted for ~53%

production as well as consumption. This market expanded at a 5.7% CAGR during 2005–2017;

China’s SS production meanwhile rose at a 19% CAGR during the period. The blistering growth in

demand for SS boosted China’s overall production by over 8 times during the period. China

increased its share of the production market from 13% in 2005 to ~53% in 2017. China is expected

to grow at a CAGR of 7-8% from 2017 to 2022e

The demand for SS has been traditionally driven by applications in kitchenware, medical

equipment, consumer durables and aesthetic usage. However, China’s huge capital investments

in the past two decades on infrastructure, transportation and greenfield industries has spurred this

demand for SS over and above the traditional applications.

Global Stainless Steel Production

Source: www.worldstainless.org [ISSF]

Even though growth in demand from China is expected to fall to 7-8% from 12-13% earlier, higher

growth from India and Indonesiato keep SS demand CAGR at 5% over FY17-22E. Additional

growth, over and above the already expanding markets, is expected from Indonesia, which is

emerging as an SS supplier as many Chinese players set up plants in this country due to

environmental and regulatory issues in China. Over the next few coming years, Indonesia would

contribute about one-third of the incremental growth in global SS supply. Chinese players as can

be seen below are setting-up capacities in Indonesia to meet their demand.

Indonesian/Philippine Stainless Steel Ramp Up

Source: Damstahl stainless steel report Nov 2017, Edelweiss Investment Research

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

In '0

00 T

on

ne

s

EU America Asia-Ex China, Korea & India India China Korea Others

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

(in

'000 t

on

ne

s)

TSI Delong Xinxing Other Indonesia Phillipines

Indian Metals & Ferro Alloys Ltd.

8 GWM

Source: Edelweiss Investment Research

Source: Bloomberg, Edelweiss Investment Research

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1Q

CY

15

2Q

CY

15

3Q

CY

15

Q4C

Y15

1Q

CY

16

2Q

CY

16

3Q

CY

16

4Q

CY

16

1Q

CY

17

2Q

CY

17

3Q

CY

17

4Q

CY

17

In 0

00's

to

nn

e

Recent quarters' global stainless steel production

WESTERN EUROPE/AFRICA CENTRAL & EASTERN EUROPE THE AMERICAS

ASIA ( EXCLUDING CHINA ) CHINA OTHERS

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Ma

y-0

9Se

p-0

9Ja

n-1

0M

ay-1

0Se

p-1

0Ja

n-1

1M

ay-1

1Se

p-1

1Ja

n-1

2M

ay-1

2Se

p-1

2Ja

n-1

3M

ay-1

3Se

p-1

3Ja

n-1

4M

ay-1

4Se

p-1

4Ja

n-1

5M

ay-1

5Se

p-1

5Ja

n-1

6M

ay-1

6Se

p-1

6Ja

n-1

7M

ay-1

7Se

p-1

7Ja

n-1

8

IN U

SD

/To

nn

e

Global Stainless Steel price (In USD/Tonne)

48,080

50,484

53,008

55,659

58,442

61,364

40,000

45,000

50,000

55,000

60,000

65,000

2017e 2018e 2019e 2020e 2021e 2022e

Pro

dn

(In

KT)

Global Stainless Steel production forecast

Indian Metals & Ferro Alloys Ltd.

9 GWM

II. Demand for Ferrochrome - China remains global demand center

Source: Merafe, Edelweiss Investment Research

As China’s SS production rose from 3.1 mn tonnes in 2005 to 25.7 mn tonnes in 2017, its consumption

of ferrocrhome simultaneously increased from 2.27 mn tonnes to ~7.30 mn tonnes, respectively.

China’s share of global ferrochrome consumption rose from ~29% in 2005 to ~61% in 2017. This

consumption is met through domestic production plus imports from countries such as South Africa,

India, Zimbabwe, etc. China imports the most quantity of ferrochrome; ~30% of global imports

during 3QCY17. The US, South Korea and the EU are other leading ferrochrome importers.

India ranks 6th worldwide in terms of ferrochrome demand due to its sizeable (~2.5mn tonne)

domestic SS production. Its annual demand for ferrochrome is ~500,000 tonnes, met by domestic

production plus imports (geography-specific). The Indian SS market is set to rise at an 8% CAGR,

which would lead to over 7-8% growth in the domestic demand for ferrochrome.

The EU’s import share is decreasing as the bloc has been building its own capacities for domestic

consumption. However, due to political and economic instability, the EU’s ferrochrome demand

decelerated at a 3.4% CARC [note: CAGR is the growth rate; CARC is the ‘de-growth’ rate] during

2007–2017. Meanwhile, China’s demand rose at over 12.7% CAGR.

Demand from the US is negligible right now, but could become significant if the Trump

administration invests more in infrastructure. The US lacks chrome ore mines and would thus

depend on the world market for SS and ferrchrome

Share of main importing countries in global HC FeCr

imports- 3QCY17.

Share of main importing countries in global HC FeCr imports

2010-2017

Source: Official customs data, Edelweiss Investment Research

-

2.0

4.0

6.0

8.0

10.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017e 2018fIn

Mn

to

nn

es

NAFTA European Union Japan South Korea Others China India

China, 30.1%

European

Union

6.1%

Japan, 8.1%South Korea,

9.9%

USA, 10.6%

India, 6.6%

Taiwan, 5.8%

Indonesia,

2.7%

Canada,

1.0%

Thailand,

0.9%Rest of the

World, 18.3%

0

5,00,000

10,00,000

15,00,000

20,00,000

25,00,000

Q12

010

Q32

010

Q12

011

Q32

011

Q12

012

Q32

012

Q12

013

Q32

013

Q12

014

Q32

014

Q12

015

Q32

015

Q12

016

Q32

016

Q12

017

Q32

017

In T

on

ne

s

China EU28 Japan South Korea USA Rest of the World

Indian Metals & Ferro Alloys Ltd.

10 GWM

Global Ferrochrome production

Source: Mining-Bulletin, Edelweiss Investment Research

Global ferrochrome production grew in line with stainless steel production, rising from 7.2 mn tonne

in 2006 to ~12.03 mn tonne in 2017, a CAGR of 5.2%.

According to Mining Bulletin, ferrochrome production is to increase at a CAGR of 5% during 2017–

2021E to ~14.6 mn tonnes due to the expanding global SS market. China remains the key market

globally, the demand as well as the production hub, for ferrochrome and chrome ore

consumption.

China overtakes South Africa as world’s leading FeCr producer

Source: Merafe, Edelweiss Investment Research

For the longest while, South Africa was the largest ferrochrome producer worldwide as it posessed

the most chrome ore resources globally (~72%) and was the largest supplier to SS manufacturers

worldwide.

In line with its large capacity additions in SS, China increased its ferrochrome-manufacturing

capacities, thus boosting its market share in ferrochrome production from 25% in 2009 to over 36%

in 2017. As China has miniscule quantities of chrome ore available in its mines, it depends heavily

on chrome ore imports, mainly from South Africa.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17e

20

18e

20

19e

20

20e

20

21e

In '0

00 t

on

ne

s

Global Ferrochrome Production

CAGR: 5.2%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017e

In M

n T

on

ne

s

Brazil EU Russia, Turkey & Albania India Kazakhstan South Africa Zimbabwe Others China

Indian Metals & Ferro Alloys Ltd.

11 GWM

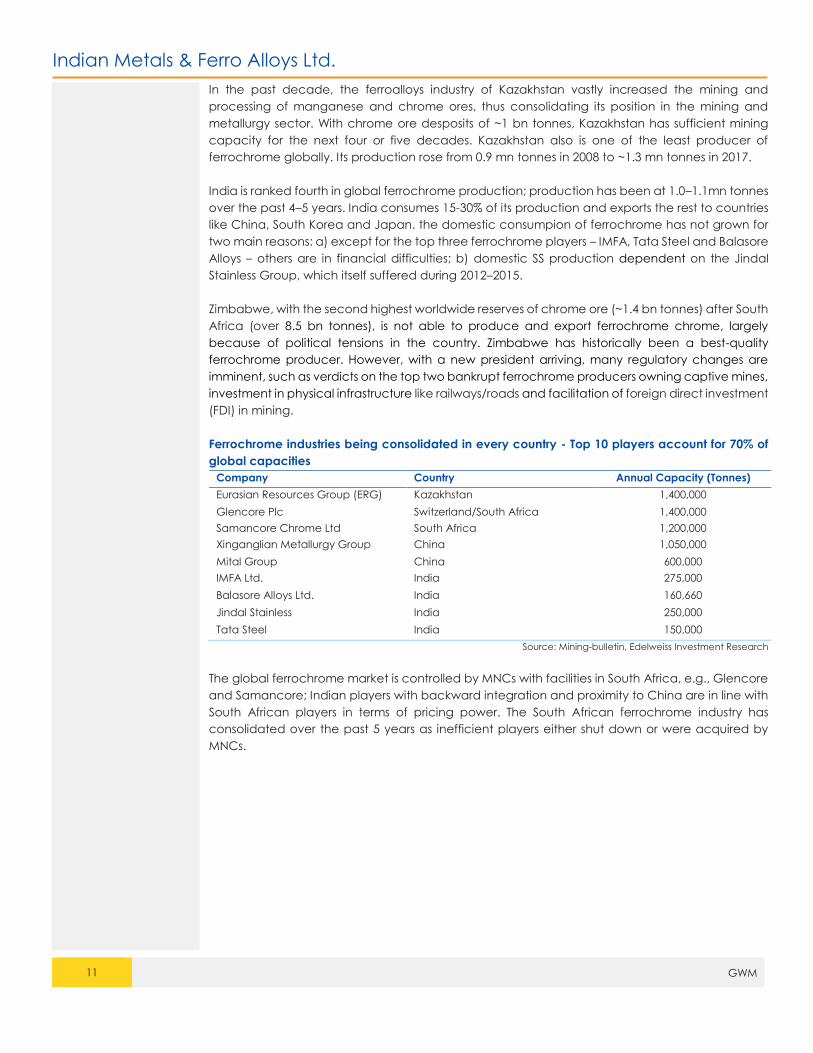

In the past decade, the ferroalloys industry of Kazakhstan vastly increased the mining and

processing of manganese and chrome ores, thus consolidating its position in the mining and

metallurgy sector. With chrome ore desposits of ~1 bn tonnes, Kazakhstan has sufficient mining

capacity for the next four or five decades. Kazakhstan also is one of the least producer of

ferrochrome globally. Its production rose from 0.9 mn tonnes in 2008 to ~1.3 mn tonnes in 2017.

India is ranked fourth in global ferrochrome production; production has been at 1.0–1.1mn tonnes

over the past 4–5 years. India consumes 15-30% of its production and exports the rest to countries

like China, South Korea and Japan. the domestic consumpion of ferrochrome has not grown for

two main reasons: a) except for the top three ferrochrome players – IMFA, Tata Steel and Balasore

Alloys – others are in financial difficulties; b) domestic SS production dependent on the Jindal

Stainless Group, which itself suffered during 2012–2015.

Zimbabwe, with the second highest worldwide reserves of chrome ore (~1.4 bn tonnes) after South

Africa (over 8.5 bn tonnes), is not able to produce and export ferrochrome chrome, largely

because of political tensions in the country. Zimbabwe has historically been a best-quality

ferrochrome producer. However, with a new president arriving, many regulatory changes are

imminent, such as verdicts on the top two bankrupt ferrochrome producers owning captive mines,

investment in physical infrastructure like railways/roads and facilitation of foreign direct investment

(FDI) in mining.

Ferrochrome industries being consolidated in every country - Top 10 players account for 70% of

global capacities

Company Country Annual Capacity (Tonnes)

Eurasian Resources Group (ERG) Kazakhstan 1,400,000

Glencore Plc Switzerland/South Africa 1,400,000

Samancore Chrome Ltd South Africa 1,200,000

Xinganglian Metallurgy Group China 1,050,000

Mital Group China 600,000

IMFA Ltd. India 275,000

Balasore Alloys Ltd. India 160,660

Jindal Stainless India 250,000

Tata Steel India 150,000

Source: Mining-bulletin, Edelweiss Investment Research

The global ferrochrome market is controlled by MNCs with facilities in South Africa, e.g., Glencore

and Samancore; Indian players with backward integration and proximity to China are in line with

South African players in terms of pricing power. The South African ferrochrome industry has

consolidated over the past 5 years as inefficient players either shut down or were acquired by

MNCs.

Indian Metals & Ferro Alloys Ltd.

12 GWM

Consolidation in Indian ferrochrome industry approaches

The Indian ferrochrome industry is likely to consolidate as capacity owned by the likes of Rohit

Ferro Alloys and FACOR Alloys would be auctioned through the National Company Law Tribunal

(NCLT) shortly.

Recently, NCLT released the results of bidding for FACOR’s assets. The committee of creditors

rejected all bids and the company is likely to be liquidated. FACOR received bids from the Swiss-

based metal trading group IMR and from IMFA and a couple of lesser known players like Synergy

Steel and Anik Industries. IMFA, one of the resolution applicants for FACOR, intervened in the

matter on Monday, seeking consideration of its bid, which it felt was wrongly rejected. IMFA’s

appeal against FACOR’s Corporate Insolvency Resolution Process is pending before the NCLT,

which reserved its order, although no stay has been granted on the liquidation. The next hearing

is due on 11 April.

Location Capacity

Chrome Ore Mines

Boula, Kathpal, Ostapal, Bhimthal, Sukinda 250,000 Tonnes pa

Ferrochrome-

Randia (Odisha) 65,000 Tonnes pa (LCFeCr)

ShreeramNagar, Garividi (AP) 72,000 Tonnes pa (HCFeCr)

Power-

Randia (Odisha) 50x2 MW Source: Edelweiss Investment Research

Indian Metals & Ferro Alloys Ltd.

13 GWM

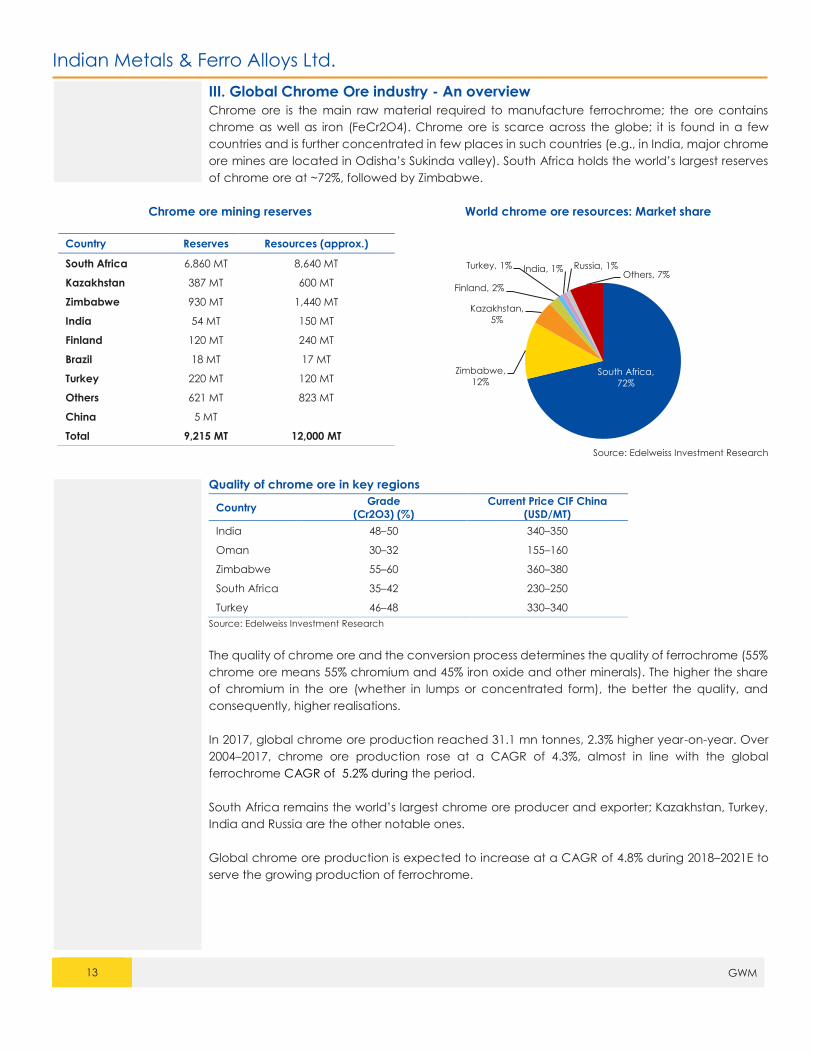

III. Global Chrome Ore industry - An overview

Chrome ore is the main raw material required to manufacture ferrochrome; the ore contains

chrome as well as iron (FeCr2O4). Chrome ore is scarce across the globe; it is found in a few

countries and is further concentrated in few places in such countries (e.g., in India, major chrome

ore mines are located in Odisha’s Sukinda valley). South Africa holds the world’s largest reserves

of chrome ore at ~72%, followed by Zimbabwe.

Chrome ore mining reserves World chrome ore resources: Market share

Country Reserves Resources (approx.)

South Africa 6,860 MT 8,640 MT

Kazakhstan 387 MT 600 MT

Zimbabwe 930 MT 1,440 MT

India 54 MT 150 MT

Finland 120 MT 240 MT

Brazil 18 MT 17 MT

Turkey 220 MT 120 MT

Others 621 MT 823 MT

China 5 MT

Total 9,215 MT 12,000 MT

Source: Edelweiss Investment Research

Quality of chrome ore in key regions

Country Grade

(Cr2O3) (%)

Current Price CIF China

(USD/MT)

India 48–50 340–350

Oman 30–32 155–160

Zimbabwe 55–60 360–380

South Africa 35–42 230–250

Turkey 46–48 330–340

Source: Edelweiss Investment Research

The quality of chrome ore and the conversion process determines the quality of ferrochrome (55%

chrome ore means 55% chromium and 45% iron oxide and other minerals). The higher the share

of chromium in the ore (whether in lumps or concentrated form), the better the quality, and

consequently, higher realisations.

In 2017, global chrome ore production reached 31.1 mn tonnes, 2.3% higher year-on-year. Over

2004–2017, chrome ore production rose at a CAGR of 4.3%, almost in line with the global

ferrochrome CAGR of 5.2% during the period.

South Africa remains the world’s largest chrome ore producer and exporter; Kazakhstan, Turkey,

India and Russia are the other notable ones.

Global chrome ore production is expected to increase at a CAGR of 4.8% during 2018–2021E to

serve the growing production of ferrochrome.

South Africa,

72%

Zimbabwe,

12%

Kazakhstan,

5%

Finland, 2%

Turkey, 1% India, 1% Russia, 1%Others, 7%

Indian Metals & Ferro Alloys Ltd.

14 GWM

Source: Mining-bulletin, Edelweiss Investment Research

Chrome ore imports market share, Q3CY2017 China’s chrome ore and concentrate imports by region

Source: Official customs data, Edelweiss Investment Research

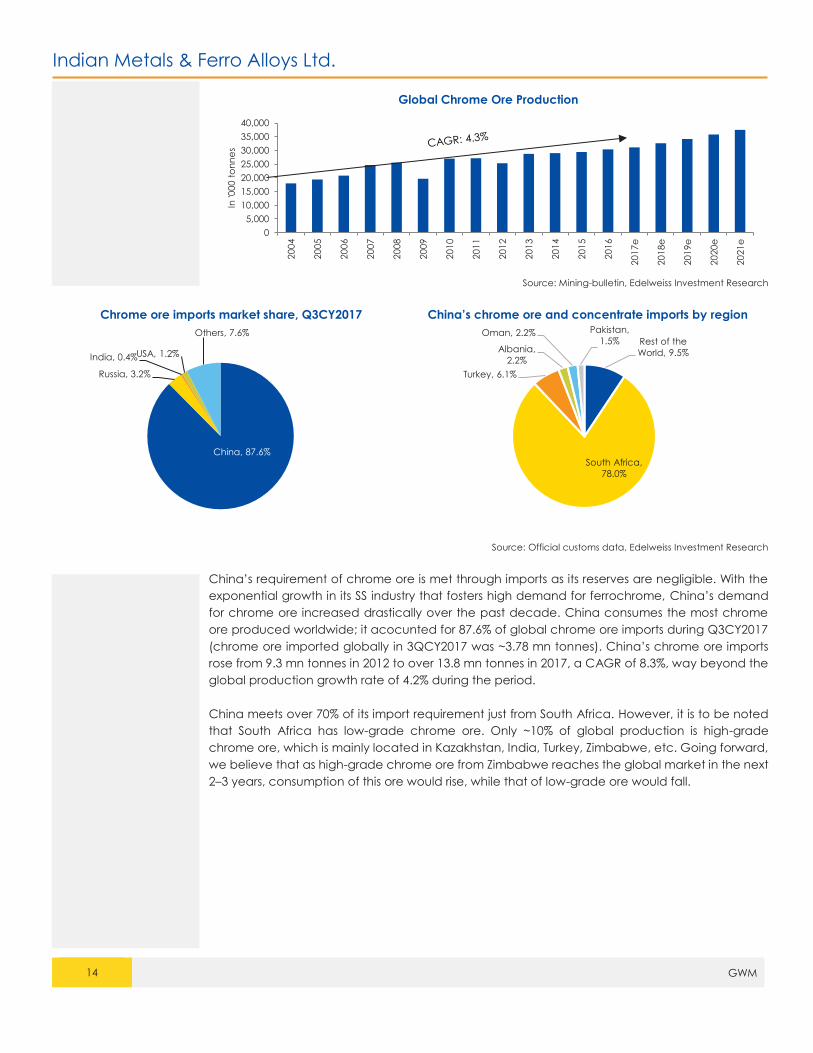

China’s requirement of chrome ore is met through imports as its reserves are negligible. With the

exponential growth in its SS industry that fosters high demand for ferrochrome, China’s demand

for chrome ore increased drastically over the past decade. China consumes the most chrome

ore produced worldwide; it acocunted for 87.6% of global chrome ore imports during Q3CY2017

(chrome ore imported globally in 3QCY2017 was ~3.78 mn tonnes). China’s chrome ore imports

rose from 9.3 mn tonnes in 2012 to over 13.8 mn tonnes in 2017, a CAGR of 8.3%, way beyond the

global production growth rate of 4.2% during the period.

China meets over 70% of its import requirement just from South Africa. However, it is to be noted

that South Africa has low-grade chrome ore. Only ~10% of global production is high-grade

chrome ore, which is mainly located in Kazakhstan, India, Turkey, Zimbabwe, etc. Going forward,

we believe that as high-grade chrome ore from Zimbabwe reaches the global market in the next

2–3 years, consumption of this ore would rise, while that of low-grade ore would fall.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17e

20

18e

20

19e

20

20e

20

21e

In '0

00 t

on

ne

s

Global Chrome Ore Production

China, 87.6%

Russia, 3.2%

India, 0.4%USA, 1.2%

Others, 7.6%Rest of the

World, 9.5%

South Africa,

78.0%

Turkey, 6.1%

Albania,

2.2%

Oman, 2.2% Pakistan,

1.5%

Indian Metals & Ferro Alloys Ltd.

15 GWM

IV. Supply demand mismatches and changes in currency rates cause price

fluctuations

Source: Mining-bulletin, Edelweiss Investment Research

China’s port inventory of chrome ore decreased from an average 2.5–3.0 mn tonnes per month

in 2013-14 to below 1 mn tonne in Q3 and Q42016 due to the consistently growing consumption

of chrome ore and supply issues in South Africa. Between January and November 2016, ore prices

jumped from USD90/tonne to ~USD400/tonne, nearing all-time high prices. With the resolution of

several supply issues in South Africa after Q2CY2017, chrome ore prices dropped to ~USD230–

240/tonne and have been hovering at that level since.

Source: Bloomberg, Edelweiss Investment Research

After years of depreciation, the rand started showing signs of appreciation recently (it

appreciated by ~40% between January 2016 and March 2018). One of the main reasons for this

strengthening was the election of Cyril Ramaphosa as the new president of South Africa. The jump

made the rand one of the fastest growing currencies in all emerging markets.

0

50

100

150

200

250

300

350

400

450

0

5,00,000

10,00,000

15,00,000

20,00,000

25,00,000

30,00,000

35,00,000

40,00,000

Ja

n-1

1

Ap

r-11

Ju

l-11

Oc

t-11

Ja

n-1

2

Ap

r-12

Ju

l-12

Oc

t-12

Ja

n-1

3

Ap

r-13

Ju

l-13

Oc

t-13

Ja

n-1

4

Ap

r-14

Ju

l-14

Oc

t-14

Ja

n-1

5

Ap

r-15

Ju

l-15

Oc

t-15

Ja

n-1

6

Ap

r-16

Ju

l-16

Oc

t-16

Ja

n-1

7

Ap

r-17

Ju

l-17

Oc

t-17

Ja

n-1

8

Shortage of port inventory led to chrome ore price rise

Chinese Port Inventory (In Tonnes) China Cr Ore price (In US$/Tonne)- RHS

0

20

40

60

80

100

120

140

160

01

-01

-20

08

01

-05

-20

08

01

-09

-20

08

01

-01

-20

09

01

-05

-20

09

01

-09

-20

09

01

-01

-20

10

01

-05

-20

10

01

-09

-20

10

01

-01

-20

11

01

-05

-20

11

01

-09

-20

11

01

-01

-20

12

01

-05

-20

12

01

-09

-20

12

01

-01

-20

13

01

-05

-20

13

01

-09

-20

13

01

-01

-20

14

01

-05

-20

14

01

-09

-20

14

01

-01

-20

15

01

-05

-20

15

01

-09

-20

15

01

-01

-20

16

01

-05

-20

16

01

-09

-20

16

01

-01

-20

17

01

-05

-20

17

01

-09

-20

17

01

-01

-20

18

Currency movements: China only country whose currency appreciated;

India, South Africa currency depreciated

Dollar Index INR-USD ZAR-USD CNY-USD

Indian Metals & Ferro Alloys Ltd.

16 GWM

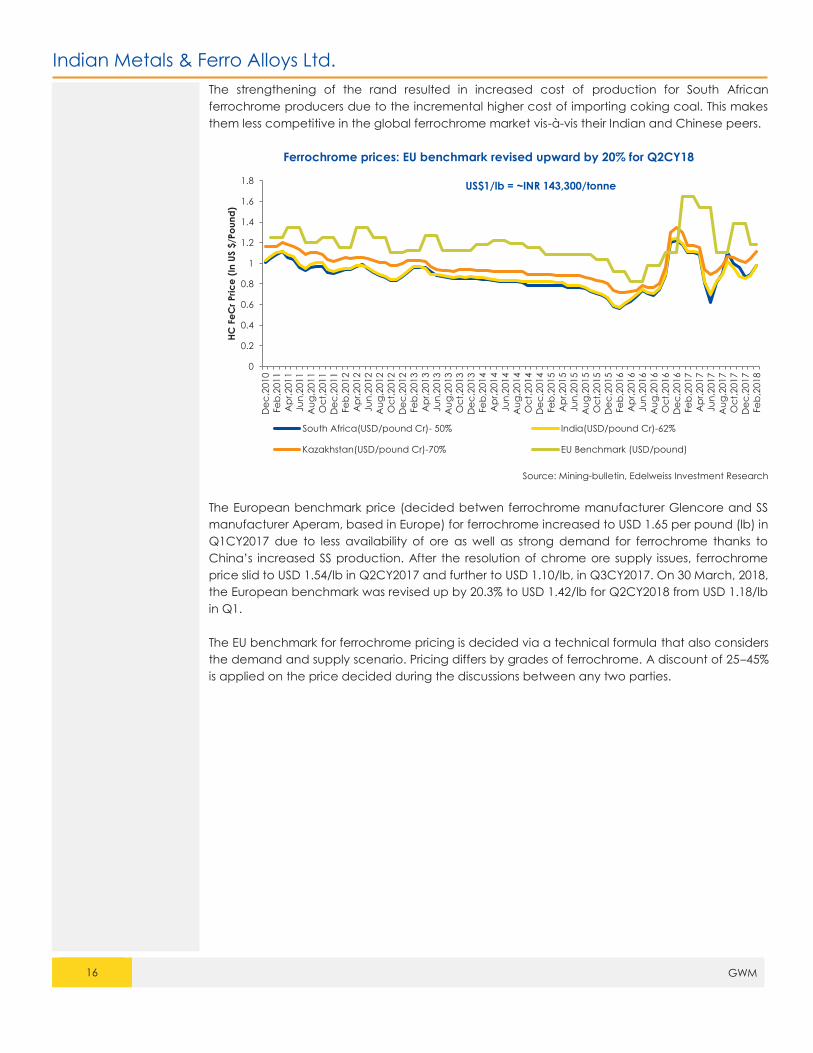

The strengthening of the rand resulted in increased cost of production for South African

ferrochrome producers due to the incremental higher cost of importing coking coal. This makes

them less competitive in the global ferrochrome market vis-à-vis their Indian and Chinese peers.

Ferrochrome prices: EU benchmark revised upward by 20% for Q2CY18

Source: Mining-bulletin, Edelweiss Investment Research

The European benchmark price (decided betwen ferrochrome manufacturer Glencore and SS

manufacturer Aperam, based in Europe) for ferrochrome increased to USD 1.65 per pound (lb) in

Q1CY2017 due to less availability of ore as well as strong demand for ferrochrome thanks to

China’s increased SS production. After the resolution of chrome ore supply issues, ferrochrome

price slid to USD 1.54/lb in Q2CY2017 and further to USD 1.10/lb, in Q3CY2017. On 30 March, 2018,

the European benchmark was revised up by 20.3% to USD 1.42/lb for Q2CY2018 from USD 1.18/lb

in Q1.

The EU benchmark for ferrochrome pricing is decided via a technical formula that also considers

the demand and supply scenario. Pricing differs by grades of ferrochrome. A discount of 25–45%

is applied on the price decided during the discussions between any two parties.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

De

c,2

010

Fe

b,2

011

Ap

r,201

1

Ju

n,2

011

Au

g,2

011

Oc

t,2

011

De

c,2

011

Fe

b,2

012

Ap

r,201

2

Ju

n,2

012

Au

g,2

012

Oc

t,2

012

De

c,2

012

Fe

b,2

013

Ap

r,201

3

Ju

n,2

013

Au

g,2

013

Oc

t,2

013

De

c,2

013

Fe

b,2

014

Ap

r,201

4

Ju

n,2

014

Au

g,2

014

Oc

t,2

014

De

c,2

014

Fe

b,2

015

Ap

r,201

5

Ju

n,2

015

Au

g,2

015

Oc

t,2

015

De

c,2

015

Fe

b,2

016

Ap

r,201

6

Ju

n,2

016

Au

g,2

016

Oc

t,2

016

De

c,2

016

Fe

b,2

017

Ap

r,201

7

Ju

n,2

017

Au

g,2

017

Oc

t,2

017

De

c,2

017

Fe

b,2

018

HC

Fe

Cr

Pri

ce

(In

US $

/Po

un

d)

South Africa(USD/pound Cr)- 50% India(USD/pound Cr)-62%

Kazakhstan(USD/pound Cr)-70% EU Benchmark (USD/pound)

US$1/lb = ~INR 143,300/tonne

Indian Metals & Ferro Alloys Ltd.

17 GWM

V. Indian Ferrochrome & Chrome Ore Industry - Niche Businesses with Few

Players

The Indian ferrochrome industry is a niche business; annual production was ~1.1 mn tonne as of

2017, constituting 9% of the 12.03 mn-tonne global production. Domestic ferrochrome players can

be broadly classified as follows:

● Integrated players with captive chrome ore mines

● Producers who either buy chrome ore from the spot market or enter into conversion

agreement with merchant miners (non-integrated)

● Merchant miners

● SS manufacturers who produce ferrochrome for captive consumption

Integrated players with

captive chrome ore mines Non-integrated players Merchant miners SS producers

IMFA Vasavi Tata Steel Jindal Stainless

Balasore Alloys Nava Bharat Ventures OMC

FACOR Rohit Ferro-Tech BC Mohanty & sons

Visa Steel IDCOL

Source: Edelweiss Investment Research

Ferrochrome production in India has remained near stagnant at 1.0–1.1 mn tonnes for several

years due to multiple reasons. These include stressed balance sheets of several ferrochrome

producers, lack of mining licenses with all players and the smaller size of the Indian SS industry.

Apart from IMFA and Balasore Alloys in the integrated players and Visa Steel from the non-

integrated set, other players have consistently fallen back in increasing production over the past

decade.

India's FeCr production India consumes 15–30% of FeCr produced, exports rest

Source: Mining-bulletin, Edelweiss Investment Research

0

200

400

600

800

1000

1200

2009 2010 2011 2012 2013 2014 2015 2016 2017

In 0

00's

To

nn

es

Domestic

Consumption

25%

Exports

75%

Indian Metals & Ferro Alloys Ltd.

18 GWM

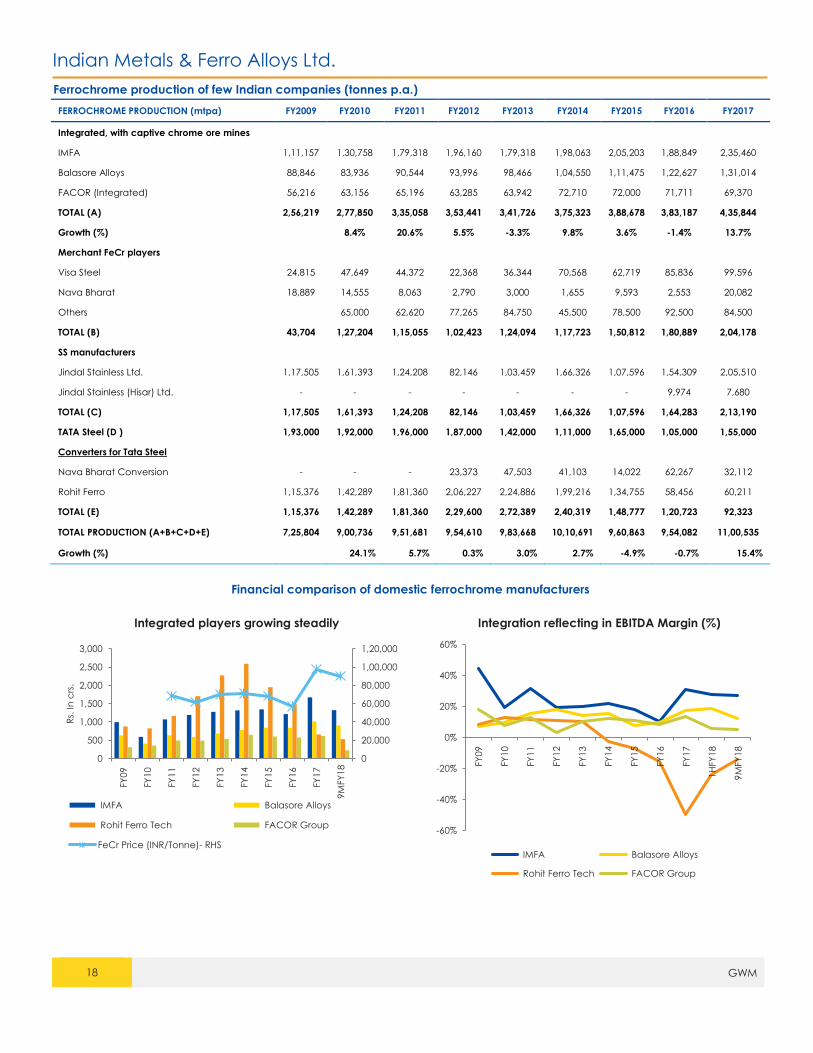

Ferrochrome production of few Indian companies (tonnes p.a.)

FERROCHROME PRODUCTION (mtpa) FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015 FY2016 FY2017

Integrated, with captive chrome ore mines

IMFA 1,11,157 1,30,758 1,79,318 1,96,160 1,79,318 1,98,063 2,05,203 1,88,849 2,35,460

Balasore Alloys 88,846 83,936 90,544 93,996 98,466 1,04,550 1,11,475 1,22,627 1,31,014

FACOR (Integrated) 56,216 63,156 65,196 63,285 63,942 72,710 72,000 71,711 69,370

TOTAL (A) 2,56,219 2,77,850 3,35,058 3,53,441 3,41,726 3,75,323 3,88,678 3,83,187 4,35,844

Growth (%) 8.4% 20.6% 5.5% -3.3% 9.8% 3.6% -1.4% 13.7%

Merchant FeCr players

Visa Steel 24,815 47,649 44,372 22,368 36,344 70,568 62,719 85,836 99,596

Nava Bharat 18,889 14,555 8,063 2,790 3,000 1,655 9,593 2,553 20,082

Others 65,000 62,620 77,265 84,750 45,500 78,500 92,500 84,500

TOTAL (B) 43,704 1,27,204 1,15,055 1,02,423 1,24,094 1,17,723 1,50,812 1,80,889 2,04,178

SS manufacturers

Jindal Stainless Ltd. 1,17,505 1,61,393 1,24,208 82,146 1,03,459 1,66,326 1,07,596 1,54,309 2,05,510

Jindal Stainless (Hisar) Ltd. - - - - - - - 9,974 7,680

TOTAL (C) 1,17,505 1,61,393 1,24,208 82,146 1,03,459 1,66,326 1,07,596 1,64,283 2,13,190

TATA Steel (D ) 1,93,000 1,92,000 1,96,000 1,87,000 1,42,000 1,11,000 1,65,000 1,05,000 1,55,000

Converters for Tata Steel

Nava Bharat Conversion - - - 23,373 47,503 41,103 14,022 62,267 32,112

Rohit Ferro 1,15,376 1,42,289 1,81,360 2,06,227 2,24,886 1,99,216 1,34,755 58,456 60,211

TOTAL (E) 1,15,376 1,42,289 1,81,360 2,29,600 2,72,389 2,40,319 1,48,777 1,20,723 92,323

TOTAL PRODUCTION (A+B+C+D+E) 7,25,804 9,00,736 9,51,681 9,54,610 9,83,668 10,10,691 9,60,863 9,54,082 11,00,535

Growth (%) 24.1% 5.7% 0.3% 3.0% 2.7% -4.9% -0.7% 15.4%

Financial comparison of domestic ferrochrome manufacturers

Integrated players growing steadily Integration reflecting in EBITDA Margin (%)

0

20,000

40,000

60,000

80,000

1,00,000

1,20,000

0

500

1,000

1,500

2,000

2,500

3,000

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

9M

FY

18

Rs.

In

crs

.

IMFA Balasore Alloys

Rohit Ferro Tech FACOR Group

FeCr Price (INR/Tonne)- RHS

-60%

-40%

-20%

0%

20%

40%

60%

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

1H

FY

18

9M

FY

18

IMFA Balasore Alloys

Rohit Ferro Tech FACOR Group

Indian Metals & Ferro Alloys Ltd.

19 GWM

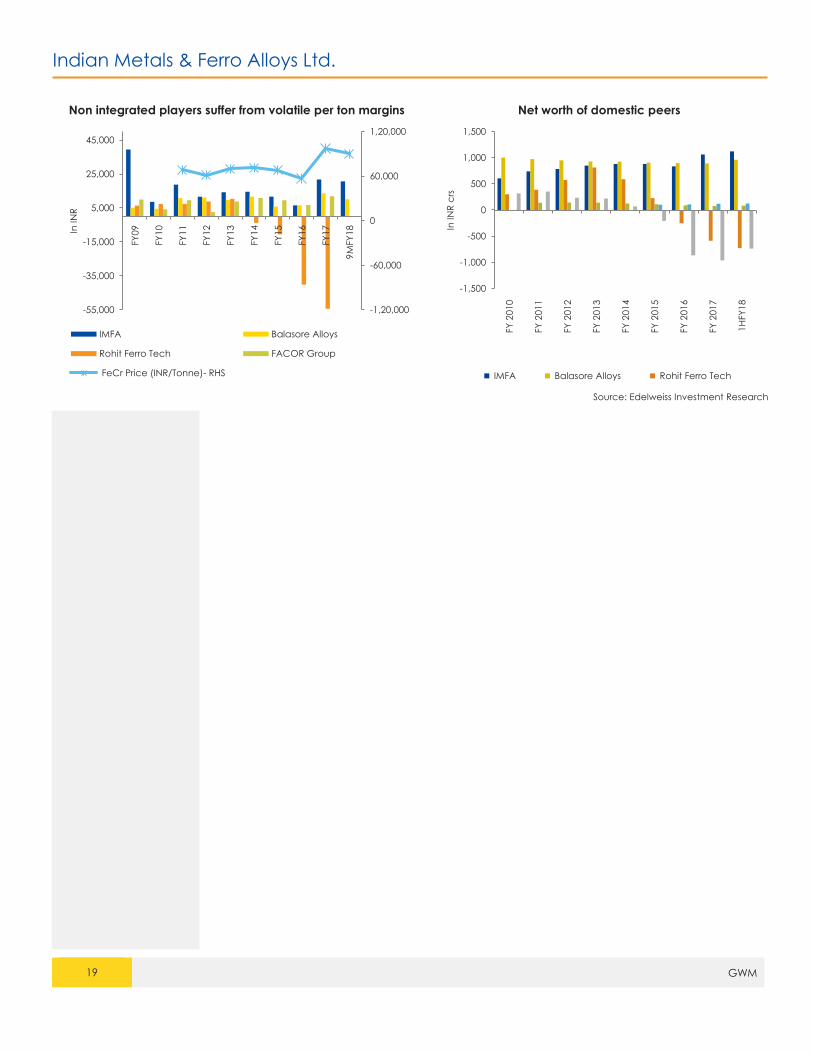

Non integrated players suffer from volatile per ton margins Net worth of domestic peers

Source: Edelweiss Investment Research

-1,20,000

-60,000

0

60,000

1,20,000

-55,000

-35,000

-15,000

5,000

25,000

45,000 F

Y09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

9M

FY

18In IN

R

IMFA Balasore Alloys

Rohit Ferro Tech FACOR Group

FeCr Price (INR/Tonne)- RHS

-1,500

-1,000

-500

0

500

1,000

1,500

FY

2010

FY

2011

FY

2012

FY

2013

FY

2014

FY

2015

FY

2016

FY

2017

1

HFY

18

In IN

R c

rs

IMFA Balasore Alloys Rohit Ferro Tech

Indian Metals & Ferro Alloys Ltd.

20 GWM

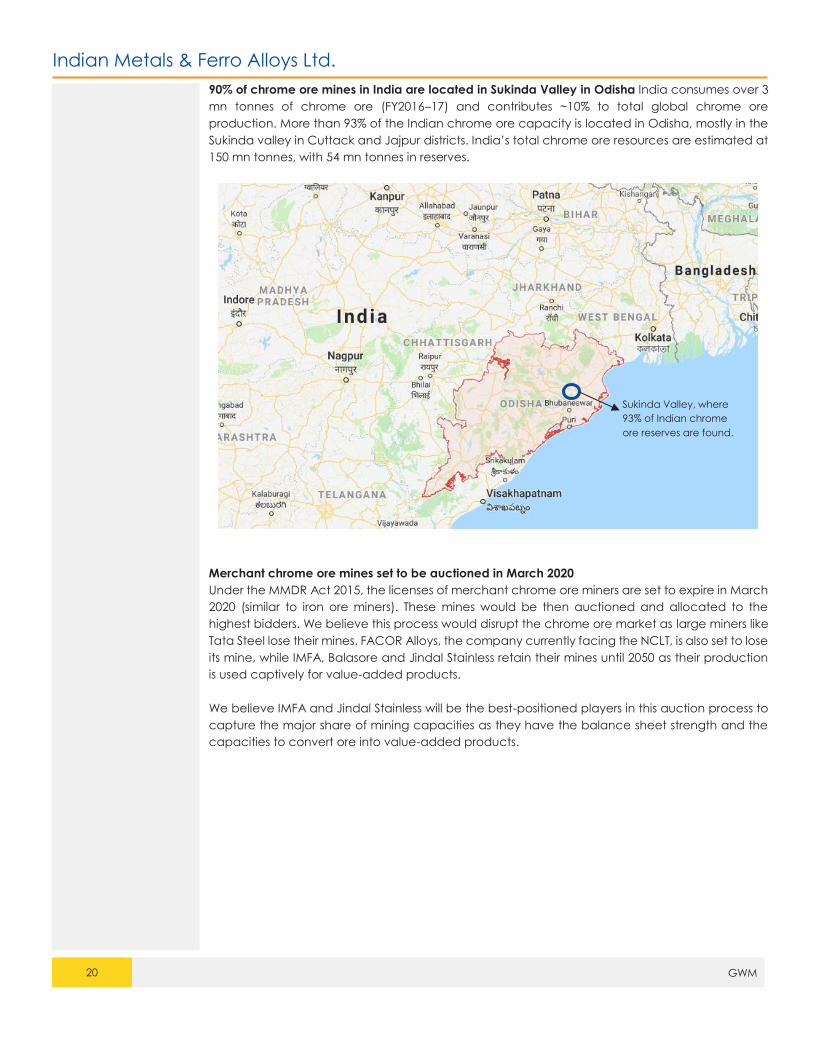

90% of chrome ore mines in India are located in Sukinda Valley in Odisha India consumes over 3

mn tonnes of chrome ore (FY2016–17) and contributes ~10% to total global chrome ore

production. More than 93% of the Indian chrome ore capacity is located in Odisha, mostly in the

Sukinda valley in Cuttack and Jajpur districts. India’s total chrome ore resources are estimated at

150 mn tonnes, with 54 mn tonnes in reserves.

Merchant chrome ore mines set to be auctioned in March 2020

Under the MMDR Act 2015, the licenses of merchant chrome ore miners are set to expire in March

2020 (similar to iron ore miners). These mines would be then auctioned and allocated to the

highest bidders. We believe this process would disrupt the chrome ore market as large miners like

Tata Steel lose their mines. FACOR Alloys, the company currently facing the NCLT, is also set to lose

its mine, while IMFA, Balasore and Jindal Stainless retain their mines until 2050 as their production

is used captively for value-added products.

We believe IMFA and Jindal Stainless will be the best-positioned players in this auction process to

capture the major share of mining capacities as they have the balance sheet strength and the

capacities to convert ore into value-added products.

Sukinda Valley, where

93% of Indian chrome

ore reserves are found.

Indian Metals & Ferro Alloys Ltd.

21 GWM

VI. Indian players have to be cost competitive versus South African and Chinese

players

Source: Edelweiss Investment Research

To manufacture 1 tonne of ferrochrome requires ~2.5 tonnes of chrome ore, 4,000 units of power

and 600 kg of coke along with a few other reductants and manpower.

In cost terms, players with captive chrome ore mines will always have the upper hand over players

buying ore from the market. Currently, IMFA’s chrome ore mining cost, including royalties/taxes, is

INR 5,500/tonne; the current price of 1 tonne chrome ore quoted by OMC is INR 13,000/tonne.

Similarly, the current cost for Chinese manufacturers is USD 220–240/tonne, increasing their cost of

chrome ore beyond that of Indian and South African integrated players.

Indian players, particularly IMFA, are among the world’s most cost-efficient producers of

ferrochrome. This is due to factors such as access to captive chrome ore mines and availability of

captive power. Thus, when ferrochrome prices fell to INR 62,000–65,000/tonne, the majority of

global players struggled to break even; but IMFA managed to post an EBITDA of INR 6,500/tonne.

Also, at least one-third of Chinese ferrochrome manufacturers are marginal players; they start

operations when ferrochrome prices move above INR 85,000/tonne.

Indian integrated players become more competitive vis-à-vis South African players

Chrome ore mining in South Africa is growing costlier with factors such as expensive labour and

the ever-increasing power cost. In South Africa, industries cannot set up captive power plants and

have purchase it from a single utility – Eskom – which virtually monopolises the power sector.

Eskom Average Tariff vs. Inflation (CPI)

Eskom drastically hike power costs after gaining a

monopoly during the power crisis in 2008. Power tariffs

rose by 356% during 2007–2017. Even in 2017, Eskom

recommended a further 19.9% per cent hike in tariff for

FY2018–2019, against which the National Energy

Regulator of SA (NERSA) approved an increase of only

5.23%. There are several news reports suggesting that

Eskom will further increase power cost in the coming

years

The current rate of power in South Africa is INR 4.7/unit

versus INR 3.5/unit for Indian players with captive power

plants and INR 5.7/unit for players dependent on the

grid.

Source: Eskom, Edelweiss Investment Research

13,200

38,250

12,500

18,000

18,800

19,050

5,000

5,500

5,150 9,750

9,555

9,945 8,000

8,000

8,000

-

20,000

40,000

60,000

80,000

1,00,000

IMFA CHINA SOUTH AFRICA

INR

/ To

nn

e

Cost Comparison between global peers

Chrome ore Power Reductants Coke Other cost

54,64553,950

80,105

Indian Metals & Ferro Alloys Ltd.

22 GWM

VII. Indian Metals and Ferro Alloys Ltd. (IMFA Ltd.): Company profile

A) Business description: Largest, only fully integrated player in India

Source: Company, Edelweiss Investment Research

Established in 1961, IMFA Ltd. is the largest integrated ferrochrome producer in india, with an

installed capacity of 275,000 tonnes per annum. It has three captive chrome ore mines (capacity

of 600,000 tonnes) at Sukinda, Mahagiri and Nuasahi; it also has a captive power plant (258 MW)

at its Choudwar manufacturing facility in Odisha.

As of FY2017, the company exported over 87% of its production to countries like China, Taiwan,

South Korea, Japan, etc. and sold the remaining domestically to customers like Jindal Stainless

Steel.

IMFA has three mines, of which Sukinda and Mahagiri are fully operational, while the Nuasahi mine

awaits environmental clearance. The Sukinda mines are completely opencast mines, the Mahagiri

mines are partially opencast, and the Nuasahi mines would be operated as completely

undergound mines. IMFA is now focusing on a capex of approximately INR 200 cr, specifically for

more underground mining, as it needs to ramp up production for future expansion.

SukindaMines

MahagiriMines

NuasahiMines

Choudwar, Odisha

Therubali, Odisha

FeCr

Domestic Sale 15%

Exports Sale 85%

80 km

500 km

100 km

520 km85 km

510 km

Indian Metals & Ferro Alloys Ltd.

23 GWM

B) Volume analysis: SS production demand drives growth

With the growin demand for SS, IMFA was able to raise its production of ferrochrome from 1.1 lakh

tonnes in FY2009 to 2.3 lakh tonnes in FY2017, a CAGR of 10%. We expect production to touch

250,000 tonnes in FY2020E, backed by the demand from its key customers in China and Taiwan.

Source: Edelweiss Investment Research

The majority of its production (~87% in FY2017) is exported, especially to regions like China and

Taiwan. IMFA has long-term contracts with POSCO (China), YUSCO (Taiwan) and Nisshin (Japan).

It supplied ~168,000 tonnes of ferrochrome to these three entities in FY2017 out of total sales of

233,698 tonnes.

Of IMFA’s total sales, 65–70% is in long-term volume contracts with the above mentioned clients.

Under these contracts, volumes are precided, while prices are re-negotiated every quarter. The

company sells the remaining 30–35% of the production via medium-term contracts or on spot basis

in Indian and international markets. IMFA would continue to export 80–90% of its production as

demand from the Indian market is yet insufficient to alter market dynamics.

C) Realisations remain strong due to healthy demand

Recently, the peak price of ferrochrome was upward of INR 110,000/tonne, mainly due to

increased demand for SS in China, coupled with lower inventory there, and a shortage of supply

from various regions. IMFA had an average realisation of INR 71,560/tonne in FY2017, its highest in

the past 7–8 years. For 9MFY2018, the company sold 173,405 tonnes at an average realisation of

INR 76,257/tonne.

Currently, prices of ferrochrome, realisation ex-India, are at INR 80,000–85,000/tonne, maintaining

a steady momentum. As on 01 April, 2018, Europenan benchmark prices were revised up by 20.3%

to USD 1.42/lb, implying a strong demand momentum. We believe that the steady demand for SS

would maintain the buoyancy in ferrochrome prices for another 2–3 years. For IMFA, we assume

a steady average realisation of INR 80,000/tonne for FY2019–2020E.

-

20.0

40.0

60.0

80.0

100.0

-

50,000

1,00,000

1,50,000

2,00,000

2,50,000

3,00,000

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Buoyancy in demand spurs higher production

Installed Capacity (In Tonnes) Ferro Chrome production (In Tonnes)

Capacity Utilisation (In %)- RHS

Indian Metals & Ferro Alloys Ltd.

24 GWM

Source: Edelweiss Investment Research

D) Backward integration with mines and power bring higher per unit EBITDA

With its access to chrome ore mines, IMFA’s cost of chrome ore procurement is ~INR 5,500/tonne

versus INR 12,000/tonne for any other company purchasing chrome ore from the open market.

This accords IMFA a huge advantage over competitors.

IMFA also gains a power cost advantage with its captive power plant of 258MW. While the cost

of power purchased from the grid is INR 5.5–6.0/unit, the cost for a company with a captive power

plant and coal mine should ideally be INR 3.8-4/unit. The company lost its coal mines during the

mine deallocation in 2014. Afterwards, IMFA obtained a coal linkage of 1 mn tonnes against its

requirement of 1.5mn tonnes, thus raising its average power cost to INR 4.0/unit. In FY2018, the

company’s power cost rose further to INR 4.5/unit as it had to purchase power from the grid at a

spot price of INR 6.2/unit due to a shortage of coal linkages caused by coal supply issues in Odisha.

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Electricity generated (In Mn Units) 747 715 625 726 774 777 792 910 914 858 1,037

Electricity sold (In Mn Units) 187.4 47.0 3.4 26.1 54.8 18.0 - -

Source: Company, Edelweiss Investment Research

Source: Edelweiss Investment Research

The rise in prices of coking coal from a low of USD 140/tonne to the recent USD 397/tonne has

raised the company’s cost of operations as it requires 600 kg of coking coal per ton of ferrochrome

produced. This industry-wide cost increase has spiked the cost of production, which has been

passed on to customers. Any reduction in coking coal price would have a corresponding effect

on ferrochrome finished products.

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1,00,000

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

3,00,000

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Sales volume vs average realisation

Sales Volume (In Tonnes) Average Realisation (In Rs.)- RHS

0

100

200

300

400

500

600

Ju

n-0

6

Oc

t-06

Fe

b-0

7

Ju

n-0

7

Oc

t-07

Fe

b-0

8

Ju

n-0

8

Oc

t-08

Fe

b-0

9

Ju

n-0

9

Oc

t-09

Fe

b-1

0

Ju

n-1

0

Oc

t-10

Fe

b-1

1

Ju

n-1

1

Oc

t-11

Fe

b-1

2

Ju

n-1

2

Oc

t-12

Fe

b-1

3

Ju

n-1

3

Oc

t-13

Fe

b-1

4

Ju

n-1

4

Oc

t-14

Fe

b-1

5

Ju

n-1

5

Oc

t-15

Fe

b-1

6

Ju

n-1

6

Oc

t-16

Fe

b-1

7

Ju

n-1

7

Oc

t-17

Fe

b-1

8

IN U

SD

/To

nn

e

Coking coal prices still holding high

Indian Metals & Ferro Alloys Ltd.

25 GWM

Significant increase in recent quarters' EBITDA/tonne Improving Realisation and EBITDA/Tonne in last 2 years

Source: Edelweiss Investment Research

-

20,000

40,000

60,000

80,000

1,00,000

1,20,000

(10,000)

-

10,000

20,000

30,000

40,000

50,000

60,0001Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

EBITDA/Ton (INR) FeCr Price (INR/Tonne)- RHS

0

20,000

40,000

60,000

80,000

1,00,000

1,20,000

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

E

FY

19

E

FY

20

E

EBITDA/Tonne (INR) FeCr Price (INR/Tonne)- RHS

Indian Metals & Ferro Alloys Ltd.

26 GWM

VIII. Consolidated Financials – Steady and healthy

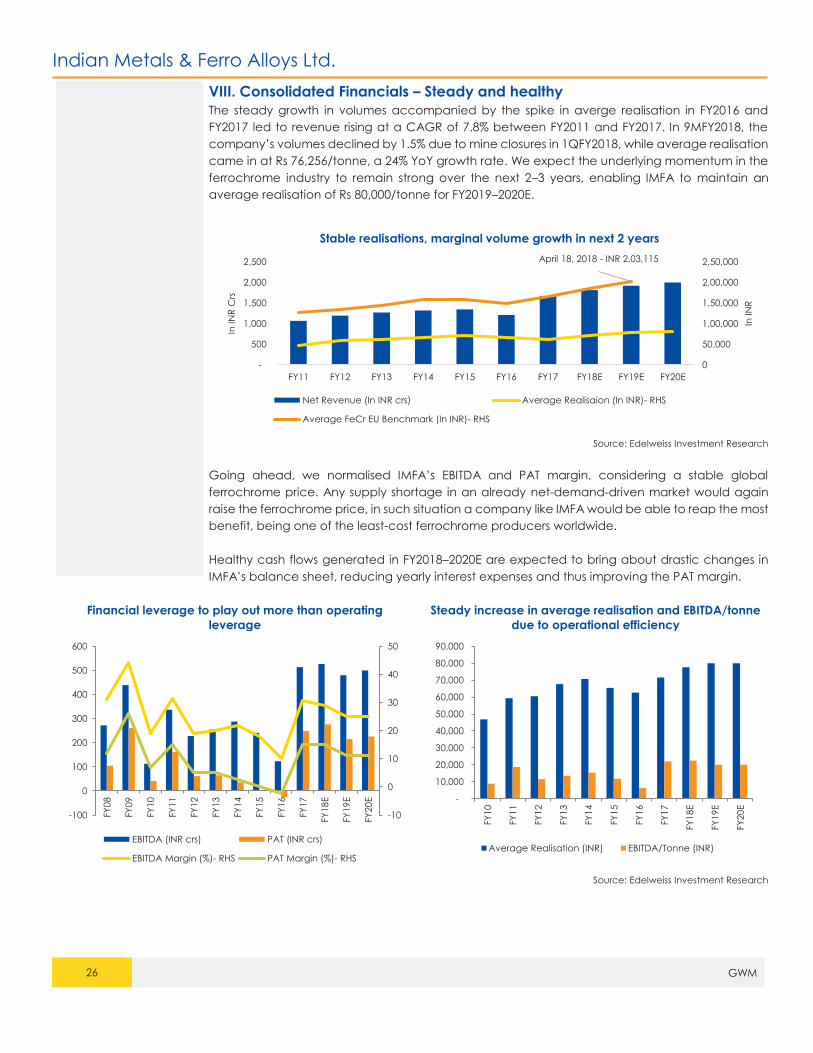

The steady growth in volumes accompanied by the spike in averge realisation in FY2016 and

FY2017 led to revenue rising at a CAGR of 7.8% between FY2011 and FY2017. In 9MFY2018, the

company’s volumes declined by 1.5% due to mine closures in 1QFY2018, while average realisation

came in at Rs 76,256/tonne, a 24% YoY growth rate. We expect the underlying momentum in the

ferrochrome industry to remain strong over the next 2–3 years, enabling IMFA to maintain an

average realisation of Rs 80,000/tonne for FY2019–2020E.

Source: Edelweiss Investment Research

Going ahead, we normalised IMFA’s EBITDA and PAT margin, considering a stable global

ferrochrome price. Any supply shortage in an already net-demand-driven market would again

raise the ferrochrome price, in such situation a company like IMFA would be able to reap the most

benefit, being one of the least-cost ferrochrome producers worldwide.

Healthy cash flows generated in FY2018–2020E are expected to bring about drastic changes in

IMFA’s balance sheet, reducing yearly interest expenses and thus improving the PAT margin.

Financial leverage to play out more than operating

leverage

Steady increase in average realisation and EBITDA/tonne

due to operational efficiency

Source: Edelweiss Investment Research

April 18, 2018 - INR 2,03,115

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

-

500

1,000

1,500

2,000

2,500

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

In IN

R

In IN

R C

rsStable realisations, marginal volume growth in next 2 years

Net Revenue (In INR crs) Average Realisaion (In INR)- RHS

Average FeCr EU Benchmark (In INR)- RHS

-10

0

10

20

30

40

50

-100

0

100

200

300

400

500

600

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

E

FY

19

E

FY

20

E

EBITDA (INR crs) PAT (INR crs)

EBITDA Margin (%)- RHS PAT Margin (%)- RHS

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

E

FY

19

E

FY

20

E

Average Realisation (INR) EBITDA/Tonne (INR)

Indian Metals & Ferro Alloys Ltd.

27 GWM

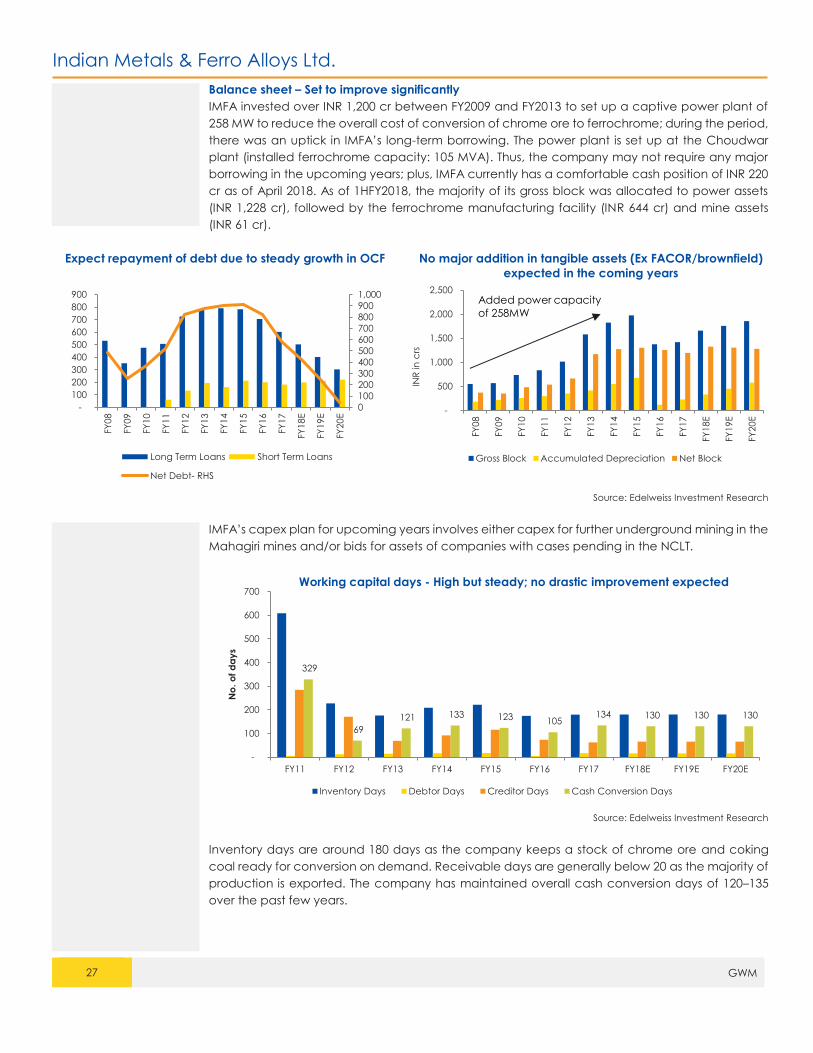

Balance sheet – Set to improve significantly

IMFA invested over INR 1,200 cr between FY2009 and FY2013 to set up a captive power plant of

258 MW to reduce the overall cost of conversion of chrome ore to ferrochrome; during the period,

there was an uptick in IMFA’s long-term borrowing. The power plant is set up at the Choudwar

plant (installed ferrochrome capacity: 105 MVA). Thus, the company may not require any major

borrowing in the upcoming years; plus, IMFA currently has a comfortable cash position of INR 220

cr as of April 2018. As of 1HFY2018, the majority of its gross block was allocated to power assets

(INR 1,228 cr), followed by the ferrochrome manufacturing facility (INR 644 cr) and mine assets

(INR 61 cr).

Expect repayment of debt due to steady growth in OCF No major addition in tangible assets (Ex FACOR/brownfield)

expected in the coming years

Source: Edelweiss Investment Research

IMFA’s capex plan for upcoming years involves either capex for further underground mining in the

Mahagiri mines and/or bids for assets of companies with cases pending in the NCLT.

Source: Edelweiss Investment Research

Inventory days are around 180 days as the company keeps a stock of chrome ore and coking

coal ready for conversion on demand. Receivable days are generally below 20 as the majority of

production is exported. The company has maintained overall cash conversion days of 120–135

over the past few years.

0

100

200

300

400

500

600

700

800

900

1,000

-

100

200

300

400

500

600

700

800

900

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

E

FY

19

E

FY

20

E

Long Term Loans Short Term Loans

Net Debt- RHS

-

500

1,000

1,500

2,000

2,500

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

E

FY

19

E

FY

20

E

INR

in c

rs

Gross Block Accumulated Depreciation Net Block

Added power capacity

of 258MW

329

69

121 133 123 105 134 130 130 130

-

100

200

300

400

500

600

700

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

No

. o

f d

ay

s

Working capital days - High but steady; no drastic improvement expected

Inventory Days Debtor Days Creditor Days Cash Conversion Days

Indian Metals & Ferro Alloys Ltd.

28 GWM

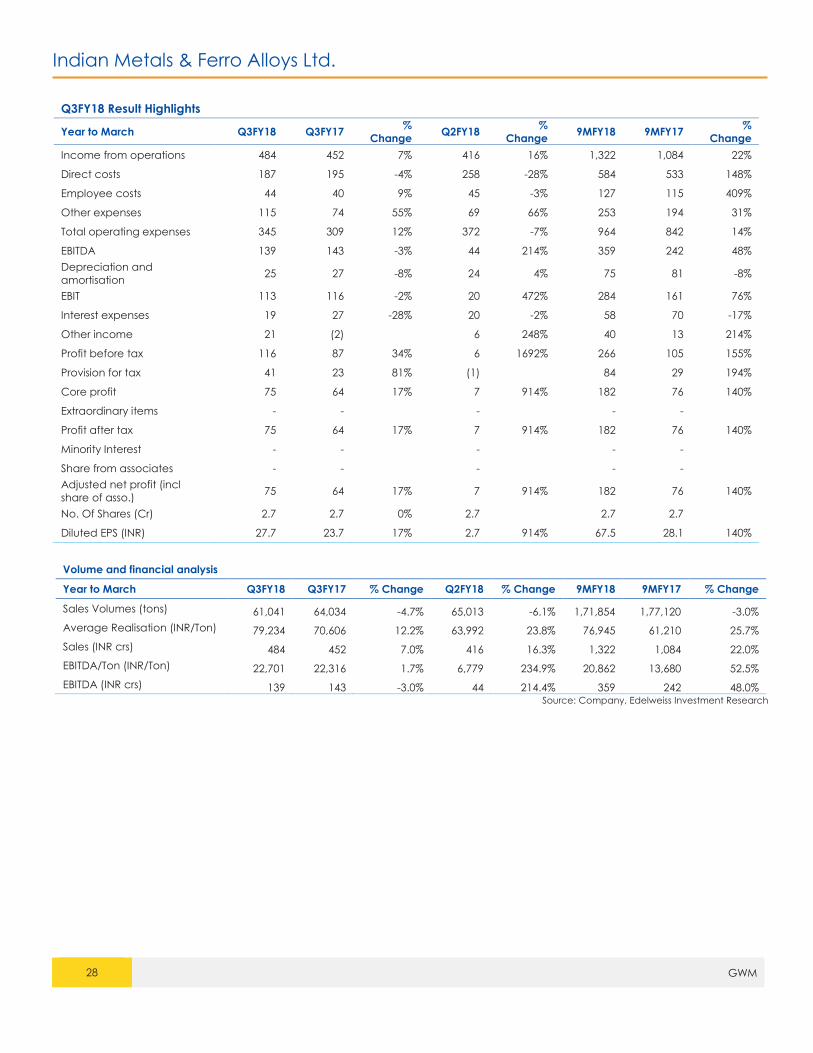

Q3FY18 Result Highlights

Year to March Q3FY18 Q3FY17 %

Change Q2FY18

%

Change 9MFY18 9MFY17

%

Change

Income from operations 484 452 7% 416 16% 1,322 1,084 22%

Direct costs 187 195 -4% 258 -28% 584 533 148%

Employee costs 44 40 9% 45 -3% 127 115 409%

Other expenses 115 74 55% 69 66% 253 194 31%

Total operating expenses 345 309 12% 372 -7% 964 842 14%

EBITDA 139 143 -3% 44 214% 359 242 48%

Depreciation and

amortisation 25 27 -8% 24 4% 75 81 -8%

EBIT 113 116 -2% 20 472% 284 161 76%

Interest expenses 19 27 -28% 20 -2% 58 70 -17%

Other income 21 (2) 6 248% 40 13 214%

Profit before tax 116 87 34% 6 1692% 266 105 155%

Provision for tax 41 23 81% (1) 84 29 194%

Core profit 75 64 17% 7 914% 182 76 140%

Extraordinary items - - - - -

Profit after tax 75 64 17% 7 914% 182 76 140%

Minority Interest - - - - -

Share from associates - - - - -

Adjusted net profit (incl

share of asso.) 75 64 17% 7 914% 182 76 140%

No. Of Shares (Cr) 2.7 2.7 0% 2.7 2.7 2.7

Diluted EPS (INR) 27.7 23.7 17% 2.7 914% 67.5 28.1 140%

Volume and financial analysis

Year to March Q3FY18 Q3FY17 % Change Q2FY18 % Change 9MFY18 9MFY17 % Change

Sales Volumes (tons) 61,041 64,034 -4.7% 65,013 -6.1% 1,71,854 1,77,120 -3.0%

Average Realisation (INR/Ton) 79,234 70,606 12.2% 63,992 23.8% 76,945 61,210 25.7%

Sales (INR crs) 484 452 7.0% 416 16.3% 1,322 1,084 22.0%

EBITDA/Ton (INR/Ton) 22,701 22,316 1.7% 6,779 234.9% 20,862 13,680 52.5%

EBITDA (INR crs) 139 143 -3.0% 44 214.4% 359 242 48.0% Source: Company, Edelweiss Investment Research

Indian Metals & Ferro Alloys Ltd.

29 GWM

Return ratios – Best in the industry, attributed to backward integration

DuPont Analysis FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Tax Burden (%) 48% 74% 71% 65% 66% 57% 70% 11% 48% 67% 68% 65% 65%

Interest Burden (%) 94% 87% 80% 85% 55% 66% 36% 21% -626% 91% 96% 92% 93%

EBIT Margin (%) 27% 40% 12% 28% 14% 14% 11% 9% 1% 24% 23% 19% 19%

Asset Turnover (x) 1.07 1.10 0.57 0.93 0.92 0.79 0.69 0.65 0.61 0.88 0.86 0.82 0.80

Equity Multiplier (x) 5.47 4.13 2.98 2.60 2.61 3.09 3.39 3.56 3.38 3.04 2.73 2.52 2.37

ROE (%) 71% 119% 12% 37% 12% 12% 6% 0% -5% 40% 36% 23% 21%

Source: Edelweiss Investment Research

IMFA’s backward integration into mines and power has enabled it to post margins higher than the

industry’s. We expect IMFA to maintain high margins in FY2018–2020E leading to an RoCE of over

20% for the company.

Valuation analysis: At a significant discount to historical ratios

Source: Edelweiss Investment Research

IMFA’s average EV/tonne from FY2008 to FY2017 stands at INR 120,008, which captures more than

one business cycle for the ferrochrome industry. At the CMP, the company’s EV/tonne on FY2018E

basis stands at INR 80,542. Thus, IMFA trades at a significant discount to the average ratio seen

over FY2008–2017. Healthy cash flows expected to be generated over the next 2 years would

significantly pare the company’s net debt, thus lowering its EV.

1,50,977

1,09,605

1,29,904 1,20,775

86,772 80,542

59,906

-

20,000

40,000

60,000

80,000

1,00,000

1,20,000

1,40,000

1,60,000

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

EV/Tonne (In INR)

Indian Metals & Ferro Alloys Ltd.

30 GWM

IX. Valuation: 2-year forward EV/EBITDA and P/E chart

IMFA: 1-yr forward EV/EBITDA chart IMFA: 2-yr Forward EV/EBITDA chart

Source: Edelweiss Investment Research

0

1000

2000

3000

4000

5000

6000

Ma

r-1

1

Au

g-1

1

Ja

n-1

2

Ju

n-1

2

No

v-1

2

Ap

r-13

Se

p-1

3

Fe

b-1

4

Ju

l-14

De

c-1

4

Ma

y-1

5

Oc

t-15

Ma

r-1

6

Au

g-1

6

Ja

n-1

7

Ju

n-1

7

No

v-1

7

INR

in

crs

.

IMFA EV 3 5 7 9 10

0

1000

2000

3000

4000

5000

6000

Ma

r-1

1

Au

g-1

1

Ja

n-1

2

Ju

n-1

2

No

v-1

2

Ap

r-13

Se

p-1

3

Fe

b-1

4

Ju

l-14

De

c-1

4

Ma

y-1

5

Oc

t-15

Ma

r-1

6

Au

g-1

6

Ja

n-1

7

Ju

n-1

7

No

v-1

7

INR

in

crs

.

IMFA: 2-yr Forward EV/EBITDA chart

IMFA EV 3 5 7 9 10

-200

0

200

400

600

800

1000

1200

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

Ma

r-1

2

Ju

n-1

2

Se

p-1

2

De

c-1

2

Ma

r-1

3

Ju

n-1

3

Se

p-1

3

De

c-1

3

Ma

r-1

4

Ju

n-1

4

Se

p-1

4

De

c-1

4

Ma

r-1

5

Ju

n-1

5

Se

p-1

5

De

c-1

5

Ma

r-1

6

Ju

n-1

6

Se

p-1

6

De

c-1

6

Ma

r-1

7

Ju

n-1

7

Se

p-1

7

De

c-1

7

Ma

r-1

8

INR

IMFA: 2-yr P/E chart

Price 2 4 6 8 10

Indian Metals & Ferro Alloys Ltd.

31 GWM

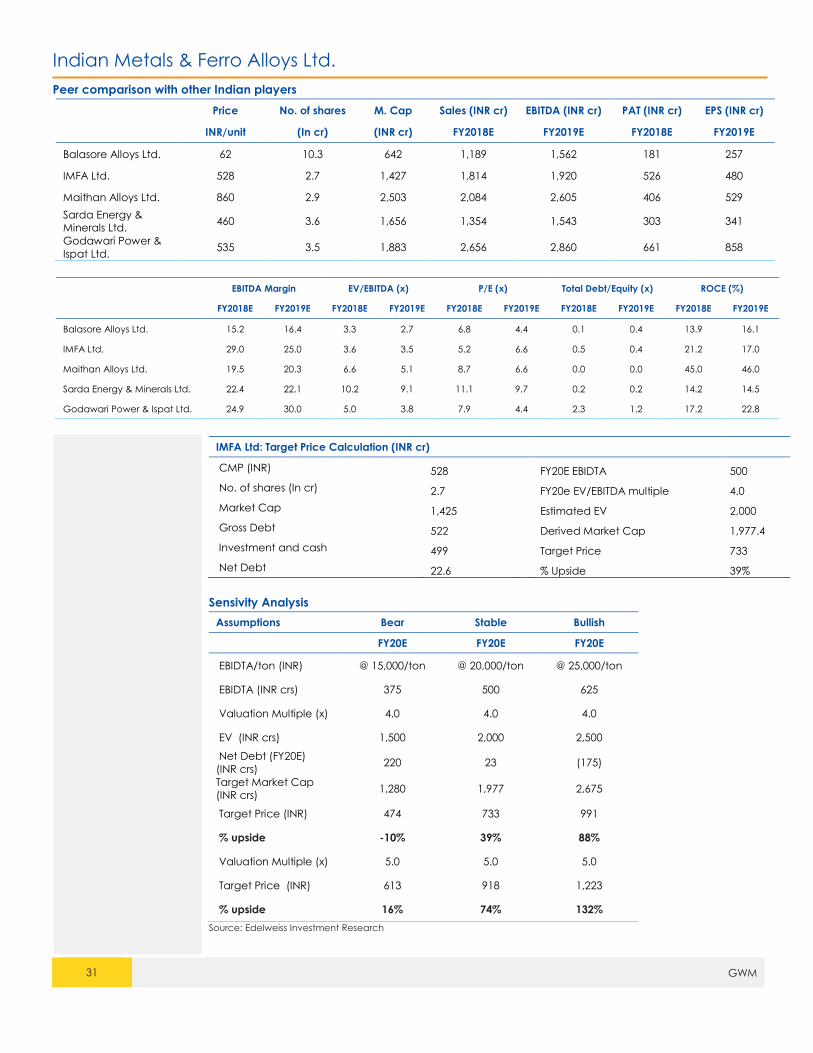

Peer comparison with other Indian players

Price No. of shares M. Cap Sales (INR cr) EBITDA (INR cr) PAT (INR cr) EPS (INR cr)

INR/unit (In cr) (INR cr) FY2018E FY2019E FY2018E FY2019E

Balasore Alloys Ltd. 62 10.3 642 1,189 1,562 181 257

IMFA Ltd. 528 2.7 1,427 1,814 1,920 526 480

Maithan Alloys Ltd. 860 2.9 2,503 2,084 2,605 406 529

Sarda Energy &

Minerals Ltd. 460 3.6 1,656 1,354 1,543 303 341

Godawari Power &

Ispat Ltd. 535 3.5 1,883 2,656 2,860 661 858

EBITDA Margin EV/EBITDA (x) P/E (x) Total Debt/Equity (x) ROCE (%)

FY2018E FY2019E FY2018E FY2019E FY2018E FY2019E FY2018E FY2019E FY2018E FY2019E

Balasore Alloys Ltd. 15.2 16.4 3.3 2.7 6.8 4.4 0.1 0.4 13.9 16.1

IMFA Ltd. 29.0 25.0 3.6 3.5 5.2 6.6 0.5 0.4 21.2 17.0

Maithan Alloys Ltd. 19.5 20.3 6.6 5.1 8.7 6.6 0.0 0.0 45.0 46.0

Sarda Energy & Minerals Ltd. 22.4 22.1 10.2 9.1 11.1 9.7 0.2 0.2 14.2 14.5

Godawari Power & Ispat Ltd. 24.9 30.0 5.0 3.8 7.9 4.4 2.3 1.2 17.2 22.8

IMFA Ltd: Target Price Calculation (INR cr)

CMP (INR) 528 FY20E EBIDTA 500

No. of shares (In cr) 2.7 FY20e EV/EBITDA multiple 4.0

Market Cap 1,425 Estimated EV 2,000

Gross Debt 522 Derived Market Cap 1,977.4

Investment and cash 499 Target Price 733

Net Debt 22.6 % Upside 39%

Sensivity Analysis

Assumptions Bear Stable Bullish

FY20E FY20E FY20E

EBIDTA/ton (INR) @ 15,000/ton @ 20,000/ton @ 25,000/ton

EBIDTA (INR crs) 375 500 625

Valuation Multiple (x) 4.0 4.0 4.0

EV (INR crs) 1,500 2,000 2,500

Net Debt (FY20E)

(INR crs) 220 23 (175)

Target Market Cap

(INR crs) 1,280 1,977 2,675

Target Price (INR) 474 733 991

% upside -10% 39% 88%

Valuation Multiple (x) 5.0 5.0 5.0

Target Price (INR) 613 918 1,223

% upside 16% 74% 132%

Source: Edelweiss Investment Research

Indian Metals & Ferro Alloys Ltd.

32 GWM

Claims with various entities: could become bonanza if received in next 1 year

Company/body

involved Matter Invested amount Claims Remarks

Utkal Coal Ltd

During the de-allocation of coal mines, IMFA

had to give up its mine under the subsidiary

Utkal Coal Ltd. The company filed a claim

following the de-allocation.

Equity: INR 111 cr

Loans: INR 262 cr INR 373 cr

Case pending with the

Supreme Court of India

Indmet Mining Pte.

Ltd.

Via its Singapore subsidiary, IMFA invested in

coal mines in Indonesia. However, due to

overlapping boundary issues, the concession

could not be operated until now. IMFA has

initiated arbitration proceedings against the

government of the Republic of Indonesia,

citing the bilateral treaty between India and

Indonesia.

INR 53 cr USD 50 mn Results expected by

September 2018

State Electricity

Board (Govt. of

Odisha)

Pursuant to the order of the Orissa High Court

dated 21 April, 2005, the company was paying

electricity duty at 6 paise/unit to the state

government and keeping the differential duty

of 14 paise/unit in a separate ‘no lien account’

until the final disposal of its writ petition. IMFA

then deposited the 14 paise with the state

exchequer and later in an escrow account. It

has filed for a refund of the entire amount.

Amount deposited - INR 100 cr.

INR 100 cr Case pending with the

Supreme Court of India

Source: Company, Edelweiss Investment Research

Key risks

a. Unfavourable Supreme Court verdicts on the mining cases (illegal as well as environmentally

detrimental mining) for various mining companies, including chrome ore miners like Balasore

Alloys, IMFA Ltd, etc.

b. Currency rate fluctuation

c. Raw material price fluctuation

d. Chinese stainless steel demand slowdown

Indian Metals & Ferro Alloys Ltd.

33 GWM

Business Overview

Company Brief:

IMFA Ltd is one of India’s largest ferrochrome producers, with facilities in Odisha. It has three chrome ore mines in Odisha

and a captive power plant, making it the only Indian company to have both a captive mine and a captive power plant.

IMFA is thus one of the lowest cost producers worldwide.

Business Model

IMFA has chrome ore capacity of 6 lakh tonnes (with total reserves of ~21 mn tonnes) and

ferrochrome capacity of 275,000 tonnes at both of its manufacturing facilities in Odisha. IMFA also

has a captive power plant with capacity of 258 MW.

Strategic Positioning

IMFA Ltd., due to its access to captive chrome ore mines and captive power plant, is one the lowest

cost ferrochrome producer globally. It is one of the three players who has captive mines (Other

being Balasore Alloys Ltd and FACOR ltd) and amongst the player who has captive chrome ore

mines, IMFA Ltd. is the largest player giving it significant margin advantage during ferrochrome price

resistance.

Competitive Edge

It has a cost advantage over other partially integrated/non-integrated players; where IMFA’s

operating cost is INR 52,000–55,000, a partially integrated player’s operating cost is upward of INR

58,000, giving IMFA a better margin profile than its competitors.

Financial Structure Current debt to equity stands at 0.5x which is reasonable considering company’s investments over

INR 1200cr in captive power and chrome ore mines

Key Competitors

Balasore Alloys Ltd. (~160,000 tonnes) is IMFA’s closest competitor in India. Both companies export

over 80% of their production, with the majority of exports going to China, Taiwan and South Korea.

Both the players compete with South African players to supply to the global markets

Industry Revenue Drivers Growth in global stainless steel industry along with increasing focus on higher grade ferrochrome

will be the key industry revenue driver

Shareholder Value

Proposition

Considering average EBITDA/tonne of INR 20,000/ton in FY20E, we are valuing the stock at an

EV/EBIDTA multiple of 5x on FY20E basis. We recommend a 'Trading BUY' on the stock with a TP of INR

950/share, an upside of 70% from current levels.

Indian Metals & Ferro Alloys Ltd.

34 GWM

SWOT ANALYSIS

• Fully integrated player with captive chrome ore