early detection of potential bank bankruptcy ... - universitas...

TRANSCRIPT

1

EARLY DETECTION OF POTENTIAL BANK BANKRUPTCY

THROUGH FINANCIAL RATIO ANALYSIS:

MULTINOMIAL LOGISTIC REGRESSION MODEL

Tengku Nuzulul Qurriyani

Hilda Rossieta

(Department of Accounting, Faculty of Economics, Universitas Indonesia, Depok, Indonesia)

ABSTRACT

Prediction of potential bank bankruptcy based on financial ratios is a continuing

research. This study is aimed to provide prediction model capable of explaining bank’s health,

predicting or detecting early potential bankruptcy of bank, finding formula that can be applied

to all banks, promoting sound banking and simultaneously creating economic prosperity of

the country considering that bank is the country’s economic infrastructure. Statistical

technique based on multinomial logistic regression model is used as method to test the model

with categorical dependent variables given a set of independent variables. It is found that

financial ratio related to bank’s capital adequacy is statistically significant (in two logit

functions) in providing early detection of potential bank insolvency. The accuracy of

predictions by the model is 75% for failed banks (BL), 62.50% for banks classified under

special surveillance or banks in resolution (BDP), and 97.14% for healthy banks (BS).

Financial ratios are believed to have contributed to the bankruptcy prediction model by

89.36%.

Keywords: Financial ratios; Go-public bank; Multinomial logistic regression model;

Prediction accuracy; Prediction model of potential bank bankruptcy

INTRODUCTION

A nation is inevitably prone to monetary crisis. The most significant aspect of the

monetary crisis which affects a nation is banking. This is signified by a number of banks

which in turn belong to categories of BBO (suspended banks) and BTO (take-over banks).

This condition occurred in 1998 in Indonesia when monetary crisis turned into banking crisis.

Fraser and Fraser (1990) assumed that a failure in a bank might lead to a failure in whole

banking system, meaning that a failure in a bank causes other banks to be unhealthy and thus

puts them in danger. In the end, this bad circumstance would reduce a degree of people’s trust

toward banks. To sum up, it is the banking system which maintains the economic stability of a

nation. Bank plays a very important role as the country’s economic infrastructure; therefore, it

is very essential that the government continuously be doing monitoring and controlling of the

stability of all banks. Ghosh (2012) stated that “Banks are the key players in the financial

system, and the bank management is expected to take all prudent actions to ensure the

solvency of the institution and promote the soundness of the financial system” (491).

2

A very crucial indicator which might be representing bank surviving capability is

financial reports that are translated into financial ratios. As Choudhry (2007) mentioned, these

financial reports are primary resources of bank analysis. This research tried to re-evaluate

bank survival through financial ratios analysis and statistical methods. Statistical methods and

a bankruptcy prediction model are two united entities which cannot be separated. A designed

and modified prediction model results in the probability of a bank to be potentially bankrupt

or not (logit and probit methods) so that it is easier for regulators to take an immediate action

to anticipate banking failure (Cheng, Chen, and Fu, 2006; Martin, 1977). When dependent

variables are under more than two categories, a prediction model may be collaborated with

statistical method of multinomial logistic regression (Hosmer and Lemeshow, 2000). This

research uses three different categories of bank surviving capability: BS (surviving bank),

BDP (bank under special surveillance), and BL (failed bank). It is expected that through this

classification model, regulators are capable of taking a prompt action to anticipate the failure

of banking system which might affect the stability of the national economy.

Two models of ratios portraying bank financial condition—CAMEL, cash flow from

operations or operating cash flow (OCF), and market measurement—will also be variables of

this research. It is estimated that financial ratios of CAMEL, OCF, and market measurement

(market’s response to stock exchange) are closely connected to identifying bank performance;

therefore, it can be a prediction and early detection instrument of potential bank bankruptcy.

The effectiveness of the financial ratios above in the prediction and identification of

bank surviving capability requires empirical testing. This is necessary in an attempt to build a

prediction model which might be responding to whether or not accounting numbers are

actually capable of predicting and identifying bank’s health, not to mention detecting potential

bank bankruptcy early. This prediction model would be a supplementary asset for regulators

with their intervention authority to avoid failed operation of a bank as early as possible and

automatically reduce costs of failure.

2.

THEORETICAL REVIEW

Dynamic State of Banking in Indonesia

Indonesia had entered into a phase of the most rapid banking growth when Paket

Deregulasi Keuangan Moneter dan Perbankan [Deregulation Package of Monetary Finance

and Banking] (Pakto: the Package of 27 October 1988 regulation). Indonesian banking history

had shifted into a stage at which banks grew very fast. This was caused by a release of a

regulation which provided an easier access to do the followings: the opening of a new bank

3

office, the establishment and operation of a rural crediting bank, the establishment of a mixed

bank, the operation of a foreign bank, and the opening of a foreign bank branch office

(Mintorahardjo, 2001).

The above change brought a number of risks. Some of the negative consequences of the

Pakto 88 (Mintorahardjo, 2001) were as follow: (i) Principles of carefulness and

professionalism in controlling banking business operation has faded away. Enormous

violations occur and they were highly unlikely to prevent and monitor; (ii) Bank interest value

increased dramatically. Intensity of competition among banks in having as many clients as

possible was getting more obvious.

The Pakto 88 ended up with bank liquidation—banks were difficult in liquidity and

credits were not running smoothly. Monetary crisis in 1998 had ruined Indonesian banking

system, and thus a preventive action to save banking sector and economic stability was in

urgent need. Restructuring strategy had to involve three groups of bank, which were banks on

the brink of failure which needed to liquidate immediately, healthy banks, and banks likely to

perform better if provided support (Stiglitz, 2012).

Development of a Prediction Model of Potential Bank Bankruptcy

An interesting fact that accounting practice in a real world may be utilized to predict

and identify a phenomenon of bank bankruptcy has come into discussion. Accounting

numbers within one particular organization (company or bank) is believed to be reflecting an

actual financial condition of the organization. It is estimated that the numbers are useful to

detect potential bank bankruptcy earlier. This type of prediction model is usually using

accounting data in the form of financial ratios analysis (Watts and Zimmerman, 1986). This

implies that accounting numbers, reflected in financial reports, contain predicting information.

Bernstein (1989) stated that assessment of a company’s past and present financial condition

originated from its financial reports, and the reports might be used to predict its future

operational performance.

This study is narrowed down to banking system due to the fact that it is a pillar of a

nation’s economy. Bank plays a very significant role in maintaining people’s trust toward a

monetary system. Therefore, it is imperative to pay serious attention to bank’s health,

especially bank’s liquidation and solvability. Bank, moreover, functions as a regulator of

money flow and as financial intermediaries, meaning that it provides access for people and

business sectors to obtain financial resources (Ritter, Silber, dan Udell, 2009).

Qurriyani (2000) examined go-public banks’ health in 1997, one year before the

government released categories of BBO (suspended banks) and BTO (take-over banks). A

4

prediction model of potential bank bankruptcy was designed through financial ratios.

Trichotomous logistic regression model was a statistical method used to identify potential

bank bankruptcy. This method applies when trichotomous outcome variable—identification

of bank survival (BBO, BTO, and healthy banks)—becomes a dependent variable and

eventually a function for a number of independent variables (financial ratios of CAMEL).

Factor analysis was conducted with 9 financial ratios, and this led to 2 final factors: F1

(profitability ratio) and F2 (liquidity ratio). F1 showed bank’s capability of generating profit

through its resources utilization, while F2 was related to bank’s ability to fulfill its billed

obligations. From 22 go-public banks examined, Qurriyani (2000) found that they were highly

likely to be classified into BBO, BTO and surviving banks. Qurriyani’s research (2000)

resulted in a model with the prediction accuracy value of 63.6%, with details of BBO=75%,

BTO=50%, and surviving banks=66.7%.

This current research is a continuation of the above research. It is aimed to raise

predicting capability from financial ratios without using factor analysis. There are currently

17 financial ratios to predict and identify the potential of bank bankruptcy. It attempts to find

the most effective predicting ratio of all in order that the prediction model used provides

better classification accuracy. Logit model is still used within this research for banking system

refers to three different categories of bank: failed bank (liquidated bank), bank under special

surveillance, and healthy bank (surviving bank). The primary prerequisite of a logit is that a

dependent variable’s value or conditional mean must be bigger than or equal to 0, and lower

than or equal to 1 1|0 xYE (Hosmer and Lemeshow, 2000).

Statistical method utilized to predict the potential of bank bankruptcy—later forming an

early warning system model—frequently ends up with two different analyses: discriminant

analysis and logistic regression analysis or probit. However, the former type of analysis is not

appropriate to identify the potential of bank bankruptcy when its statistical approach is not

matched pair sampling but random sample from companies to be examined—the number of

bankrupt company samples is lower (Eisenbeis, 1977). Grice and Ingram (2001) proved that

discriminant analysis used by Altman (1986), re-used for present samples, had a lower

predicting accuracy value of 57.8%.

It is evident that logistic regression analysis enables readers to measure the bankruptcy

value of each bank or company more easily through looking at the bankruptcy percentage of

an examined bank or company. Logit model is more recommended than MDA due to the fact

that it is easier to do, and it doesn’t require independent variable data which have to be

normally distributed (Espahbodi, 1991). This condition also applies to multinomial logistic

5

regression model which is the extension of binary logistic regression (dichotomy). The only

feature differentiating logistic regression and multinomial logistic regression lies on the

number of dependent variables, meaning that the dependent variables within the latter analysis

are classified into more than two categories.

The computerized era has brought a variety of statistical methods in connection with the

prediction model of potential bank bankruptcy, and these methods are designed to end up with

prediction accuracy values closer to real prediction accuracy values. The methods include

artificial neural network (ANN) (Kumar and Ravi, 2007), data envelopment analysis (DEA)

(Premachandra, Chen, and Watson, 2011; Premachandra, Bhabra, and Sueyoshi. 2009), and

trait recognition analysis (TRA) (Kolari et al., 2002). The use of these current methods is

closely relevant to two popular multivariate statistical methods—multiple discriminant

analysis and logistic regression.

Kolari (2002) analyzed large bank failure in America with an attempt to build early

warning systems (EWSs) mainly based on accounting and published financial data. He used

two following methods to do so: logit and trait recognition models. Two failed bank samples

were divided into two groups: original sample (data was taken in 1989) to form classification

model, and holdout sample (data was taken in 1990, 1991, 1992) to determine the

effectiveness of an EWS prediction model. Accounting data was taken one until two years

before the banks came into failure. He found out that logit and trait recognition models had

capability of identifying risks of bank bankruptcy, especially on original sample classification

result, which resulted in the predicting accuracy percentage of 95%-100%.

Premachandra, Bhabra, and Sueyoshi (2009) were trying to compare logit and DEA

models in order to create a prediction model of corporate bankruptcy. DEA model was

naturally non-parametric and distribution-free-based. On the other hand, Premachandra, Chen,

and Watson (2011) revised the model which Premachandra, Bhabra, and Sueyoshi (2009)

used. They found that the effectiveness of super-efficiency DEA model in predicting failed

corporate was relatively lower than that in predicting surviving corporate. DEA model tended

to end up with efficiency scores. It was proved that DEA superior model successfully

identified corporate success.

In addition, Öğüt et al. (2012) took samples of banks in Turkey in order to measure

financial strength ratings of the bank samples through a series of financial ratios, and to do

statistical comparison between logistic regression and multiple discriminant analysis models

using data mining methodology (support vector machine and artificial neural network). It was

found that logit regression was still dominating over discriminant analysis in terms of

6

predicting banks’ financial strength ratings providing that independent variables were factor

scores, and that the most essential factors which contributed to the prediction effectiveness

included efficiency, profitability, and proportion of loans in the assets.

Multiple discriminant analysis tends to end up with a predictor capable of

discriminating failed corporate and successful (surviving) corporate. Nevertheless, a basic

fallacy of the utilization of multiple discriminant analysis is the subjective cutoff score which

is the most effective element in differentiating failed corporate and non-failed corporate

(Stickney and Brown, 1999). This circumstance encourages numerous researchers to design a

prediction model of bankruptcy through logistic regression analysis—which is relatively

easier to interpret because it results in percentage of bankruptcy. When dependent variables

belong to two categories, multinomial logistic regression model is regarded to be capable of

creating a prediction model of bankruptcy which is signified by the fact that each examined

organization or bank has its own bankruptcy percentage or value. This condition indicates the

predicting accuracy percentage of the model.

Financial Ratio as a Determining Factor of Bank Bankruptcy

CAMEL

Andersen (2008) claimed that the assumption on which CAMEL concept is associated

with conditions that cause banks prone to experiencing the following possible set of failures:

low capital adequacy, low assets quality and management, and decreased earnings and

liquidity. “As a bank or firm becomes more and more insolvent, it gradually enters a danger

zone. Then, changes to its operations and capital structure must be made in order to keep it

solvent” (Kumar and Ravi, 2007, 1).

Financial ratio of CAMEL, ratio of cash flow, and market assessment ratio are usually

used to analyze bank profitability, bank solvability, and bank risks. To what extent might

banks be able to tolerate risks to gain profits? Another thing which banks want to achieve is

sustainability of their business operations within banking market, meaning that they are

capable of remaining financially strong and healthy and backing a nation’s economic growth

simultaneously. In relation to operation sustainability, it is imperative that there be a primary

predictor which can define bank’s capability of putting operation risks and profit into balance

in order to find an early detection method of bank bankruptcy or bank failure. Many studies

have attempted to explore the potential of early warning systems for banking cases or bank

rating. Financial ratios utilized originate from fundamental analysis of corporate or banks

including profitability, liquidity, solvability, and efficiency. Fraser and Fraser (1990) claimed

7

that there were four determining factors of banking financial soundness, and these four factors

included (i) earnings; (ii) liquidity; (iii) asset quality; and (iv) capital adequacy.

CAMEL concept is actually an independent variable in research, originating from a

series of financial ratios used by previous researchers and having relevance to the

identification of bank bankruptcy or bank soundness. The CAMEL concept proxy used in this

study refers to Kasmir (2000), and it was proven significant based on previous research in

defining bank performance in Indonesia. For example, the significant ratios used in Surifah’s

research (2002) were risk assets ratio, RORA, assets utilization, ROA, leverage management,

ROE, quick ratio, and LDR; in Aryati’s and Manao’s research (2000), the ratios were RORA,

ROA, BOPO, net call money, and LDR; while in Payamta’s research (2008), the ratios were

CAR, ROA, ROE, LDR.

Cash Flow

In addition to CAMEL concept, cash flow (OCF) concept might be used to measure

bank performance, primarily bank bankruptcy. The information about corporate liquidity

condition and corporate capability of getting funding from corporate core business activities

might be obtained from cash flow report (White, Sondhi, and Fried, 2003). Providing that

OCF value was positive, then corporate was likely to be sustainable for long (FASB, 1978).

Beaver (1966) also stated that the higher the OCF value was the lower the probability of

failure was. Based on Beaver’s research (1966), it was found that cash flow/total liability

variable was a significant variable in predicting bank bankruptcy. The same outcome was also

shared by Rujoub, Cook, and Hay (1995) through their study that OCF was relatively

significant in predicting bank bankruptcy. It was tested through discriminant analysis.

A huge number of investors have used OCF as the most effective determinant factor in

identifying potential corporate bankruptcy since cash flow concept cannot be manipulated.

They all are merely interested in cash flow from operations, ignoring cash flow from investing

as well as cash flow from financing. Schilit and Perler (2010) assumed that OCF was ‘a

golden child’ for it contains inside corporate capability of generating revenues from their core

business operations.

Share Price as Market Response to Bank Performance

It is convinced that stock market is closely related to financial report analysis. The more

active the market is, the more critical the investors are to decide if or not they want to invest.

Accounting numbers are detrimental factors for investors to make a decision of whether or not

they want to invest in the market. It is believed that through investment they will be able to

improve their wealth. Bauman (2003) found out that earnings were correlated with and had a

8

significantly positive impact on market value of equity. When earnings fell, indicating that

earnings prospect was poor, market value of equity (ME) decreased, too.

White, Sondhi, and Fried (2003) took Fama’s and French’s statement (1992) that PBV

ratio was an important predictor of future stock returns. A company with a low PBV value

would have a higher return than that with a high PBV value. A low PBV value might be also

indicating a high BE/ME ratio which automatically referred to poor earnings prospects. This

fact signifies that PBV ratio is applicable for identification of potential bank bankruptcy.

According to Bodie, Kane, and Marcus (2011), PBV or market-price-to-book ratio indicated

firm value in terms of growth opportunities. It is believed that corporate having significant

growth are more able to identify their upcoming cash flow (Smith and Watts, 1992).

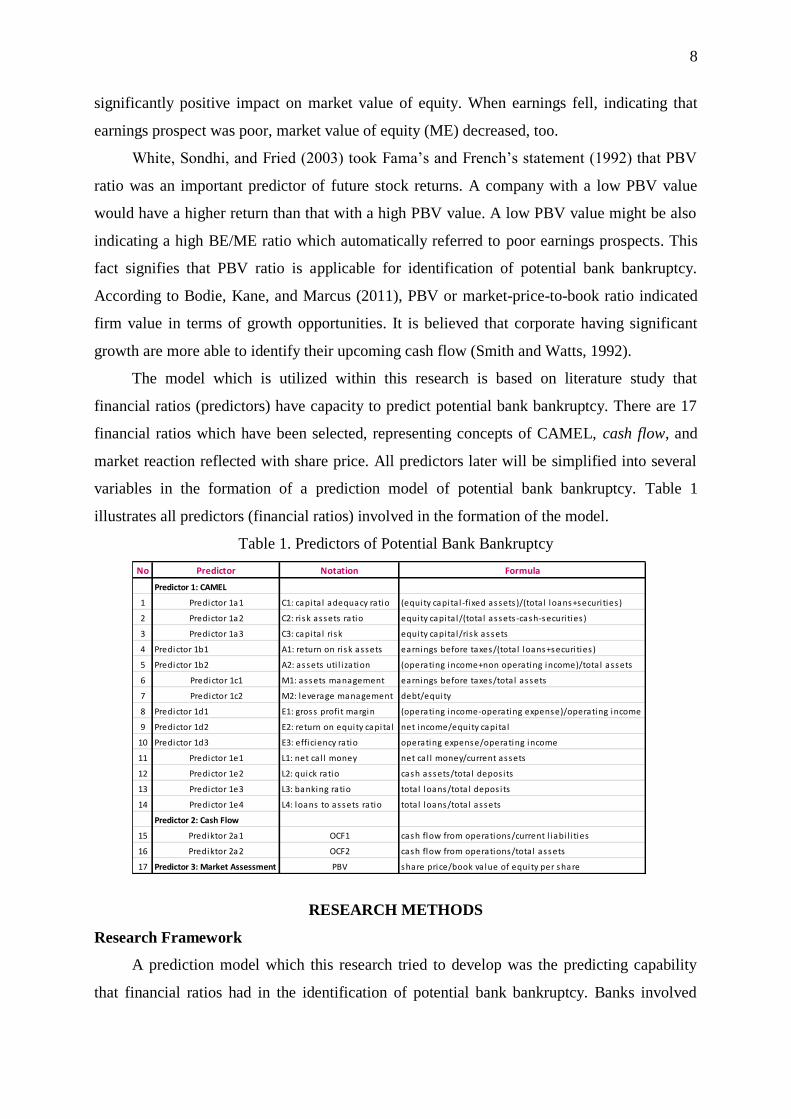

The model which is utilized within this research is based on literature study that

financial ratios (predictors) have capacity to predict potential bank bankruptcy. There are 17

financial ratios which have been selected, representing concepts of CAMEL, cash flow, and

market reaction reflected with share price. All predictors later will be simplified into several

variables in the formation of a prediction model of potential bank bankruptcy. Table 1

illustrates all predictors (financial ratios) involved in the formation of the model.

Table 1. Predictors of Potential Bank Bankruptcy

RESEARCH METHODS

Research Framework

A prediction model which this research tried to develop was the predicting capability

that financial ratios had in the identification of potential bank bankruptcy. Banks involved

No Predictor Notation Formula

Predictor 1: CAMEL

1 Predictor 1a1 C1: capita l adequacy ratio (equity capita l -fixed assets)/(total loans+securi ties )

2 Predictor 1a2 C2: ri sk assets ratio equity capita l/(total assets-cash-securi ties )

3 Predictor 1a3 C3: capita l ri sk equity capita l/risk assets

4 Predictor 1b1 A1: return on risk assets earnings before taxes/(total loans+securi ties )

5 Predictor 1b2 A2: assets uti l i zation (operating income+non operating income)/total assets

6 Predictor 1c1 M1: assets management earnings before taxes/total assets

7 Predictor 1c2 M2: leverage management debt/equity

8 Predictor 1d1 E1: gross profi t margin (operating income-operating expense)/operating income

9 Predictor 1d2 E2: return on equity capita l net income/equity capita l

10 Predictor 1d3 E3: efficiency ratio operating expense/operating income

11 Predictor 1e1 L1: net ca l l money net ca l l money/current assets

12 Predictor 1e2 L2: quick ratio cash assets/total depos its

13 Predictor 1e3 L3: banking ratio total loans/total depos its

14 Predictor 1e4 L4: loans to assets ratio total loans/total assets

Predictor 2: Cash Flow

15 Prediktor 2a1 OCF1 cash flow from operations/current l iabi l i ties

16 Prediktor 2a2 OCF2 cash flow from operations/total assets

17 Predictor 3: Market Assessment PBV share price/book va lue of equity per share

9

within this research were classified into three following categories: surviving banks (BS),

banks under special surveillance (BDP), and failed banks (liquidated banks) (BL). This

research was aimed to examine whether or not the following financial ratios: CAMEL, cash

flow, and share price were able to detect potential bank bankruptcy so that it can be a very

effective method of early detection which later would contribute to decision making in

whether or not to save or liquidate banks (Figure 1). An econometric model that this research

had selected for the formulation of early detection system of potential bank bankruptcy was

multinomial logistic regression.

Figure 1. Research Framework

Sample Selection

Secondary data was the main source of research data—banks as analysis unit. Financial

statements as of 31 December 2006 to 31 December 2007 (income statement, balance sheet,

cash flow statement) and stock market data (2006 and 2007) were taken from go-public banks

(registered at BEI (Indonesia Stock Exchange)). The data was available on BEI website, bank

websites, Indonesian Capital Market Directory (ICMD), Indonesia Stock Exchange (IDX),

and Yahoo Finance. Research population was go-public banks with consideration that it was

relatively easy to get financial statements of these banks which had been audited. Another

consideration was indeed transparency. Research samples were narrowed to go-public banks

operating in years 2006 and 2007, with a minimum listing period of one year to avoid

Prediction Model of Potential Bank Bankruptcy

Probability of Bankruptcy

Early Detection of Potential Bank Bankruptcy

Financial RatiosBank Survival Categories

Surviving Bank (BS)

Bank under Special

Surveillance (BDP)

Failed Bank (BL)

CAMEL

Cash Flow

Share Price

Capital Adequacy

Assets Quality

Management

Earnings

Liquidity

Capital Adequacy Ratio, C1

Risk Assets Ratio, C2

Capital Risk, C3

Return on Risk Assets, A1

Assets Utilization, A2

Assets Management, M1

Leverage Management, M2

Gross Profit Margin, E1

Return on Equity Capital, E2

Efficiency Ratio (BOPO), E3

Net Call Money, L1

Quick Ratio, L2

Banking Ratio (LDR), L3

Loans to Assets Ratio, L4

OCF/Current Liabilities, OCF1

OCF/Total Assets, OCF2

Price to Book Value Ratio PBV

10

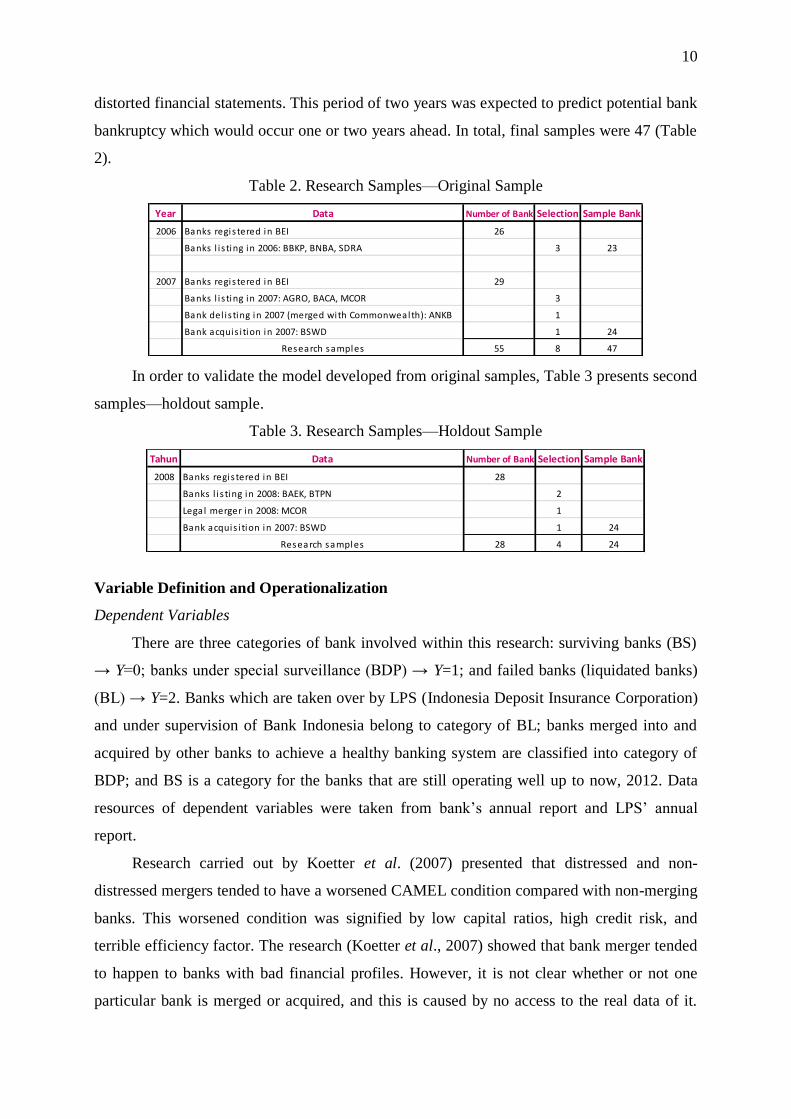

distorted financial statements. This period of two years was expected to predict potential bank

bankruptcy which would occur one or two years ahead. In total, final samples were 47 (Table

2).

Table 2. Research Samples—Original Sample

In order to validate the model developed from original samples, Table 3 presents second

samples—holdout sample.

Table 3. Research Samples—Holdout Sample

Variable Definition and Operationalization

Dependent Variables

There are three categories of bank involved within this research: surviving banks (BS)

→ Y=0; banks under special surveillance (BDP) → Y=1; and failed banks (liquidated banks)

(BL) → Y=2. Banks which are taken over by LPS (Indonesia Deposit Insurance Corporation)

and under supervision of Bank Indonesia belong to category of BL; banks merged into and

acquired by other banks to achieve a healthy banking system are classified into category of

BDP; and BS is a category for the banks that are still operating well up to now, 2012. Data

resources of dependent variables were taken from bank’s annual report and LPS’ annual

report.

Research carried out by Koetter et al. (2007) presented that distressed and non-

distressed mergers tended to have a worsened CAMEL condition compared with non-merging

banks. This worsened condition was signified by low capital ratios, high credit risk, and

terrible efficiency factor. The research (Koetter et al., 2007) showed that bank merger tended

to happen to banks with bad financial profiles. However, it is not clear whether or not one

particular bank is merged or acquired, and this is caused by no access to the real data of it.

Year Data Number of Bank Selection Sample Bank

2006 Banks regis tered in BEI 26

Banks l i s ting in 2006: BBKP, BNBA, SDRA 3 23

2007 Banks regis tered in BEI 29

Banks l i s ting in 2007: AGRO, BACA, MCOR 3

Bank del is ting in 2007 (merged with Commonwealth): ANKB 1

Bank acquis i tion in 2007: BSWD 1 24

Research samples 55 8 47

Tahun Data Number of Bank Selection Sample Bank

2008 Banks registered in BEI 28

Banks l i s ting in 2008: BAEK, BTPN 2

Legal merger in 2008: MCOR 1

Bank acquis i tion in 2007: BSWD 1 24

Research samples 28 4 24

11

Merger or acquisition issues are raised with the main objective to strengthen banking capital

for business expansion and competitive survival, not to mention a demand from API

(Indonesia Banking Architecture) for the fulfillment of minimum banking capital.

Independent Variables as Predictors of Potential Bank Bankruptcy

CAMEL-oriented predictors which were popular in previous research include capital

adequacy, assets quality, management, earnings, and liquidity. Besides, cash flow from

operations and market assessment (shares price assessment) are detrimental predictors of

potential bank bankruptcy. It is expected that all ratios utilized within this research, using

statistical approach, are able to create a prediction model of bankruptcy with dominant

predictors capable of early detecting of potential bank bankruptcy.

Stepwise Procedure

Researchers prefer to use this stepwise estimation because it is capable of improving the

accuracy of a prediction model with the involvement of variables significantly contributing to

the identification of potential bank bankruptcy. Hair et al. (2010) claimed that the objective

method in selecting variables to maximize prediction accuracy is stepwise method. Stepwise

regression is very popular in the establishment of a prediction model. Researchers tend to use

many independent variables and later select them to be the variables only having significant

correlation (Hosmer and Lemeshow, 2000). In stepwise procedure, several variables are

united to be a group which has a high significance value, while the others are no longer

existent from statistical model. A variable is deemed important providing that its coefficient

value is statistically significant, signified by the lowest p-value (Hosmer and Lemeshow,

2000). The aid instrument is SPSS 19.

Multinomial Logistic Regression Model

When dependent variables belong to more than two categories (no longer binary nor

dichotomy), the most likely statistical model which accommodates this is multinomial logistic

regression model. Model with three categories results in two logit functions (BS → reference

outcome value (comparing category)). This model is expected to answer a research question.

STATA 11 would be used to run this multinomial logistic regression model. Hosmer and

Lemeshow (2000) said that logistic regression model with dependent variables in the form of

dichotomy data only had one logit function, which was the logit of Y=1 versus Y=0. On the

contrary, when the variables belong to three categories, there would be two logit functions:

the logit of Y=1 versus Y=0, and the logit of Y=2 versus Y=0 (Y=0 functions as a comparing

category). Codes 0, 1, 2 were chosen as dependent variables: BS → Y=0; BDP → Y=1; and

BL → Y=2.

12

The formation of the prediction model with the availability of p covariates and x

constant as a vector of p+1 with a value of =1 resulted in denotation of 2 logit functions

(Hosmer and Lemeshow, 2000):

11212111101 '...)|0(

)|1(ln)( xxxx

xYP

xYPxg pp

22222121202 '...)|0(

)|2(ln)( xxxx

xYP

xYPxg pp

Conditional probability was later formed from each dependent variable:

0)()(2

1

)(211

1

1

1)|0(

xgxg

j

xg eee

xYPj

1)()(

)(

2

1

)(

)(

21

11

11

)|1(

xgxg

xg

j

xg

xg

ee

e

e

exYP

j

2)()(

)(

2

1

)(

)(

21

22

11

)|2(

xgxg

xg

j

xg

xg

ee

e

e

exYP

j

RESEARCH FINDINGS

Description of Dependent and Independent Variables

Numerous data were collected to answer whether or not financial ratios were capable of

detecting potential bank bankruptcy early. Table 4 illustrates description of dependent

variables after they were identified based on their definition. Description of independent

variables, on the other hand, is presented in Appendix 1, including 6 financial ratios after they

were analyzed using stepwise procedure.

0x

13

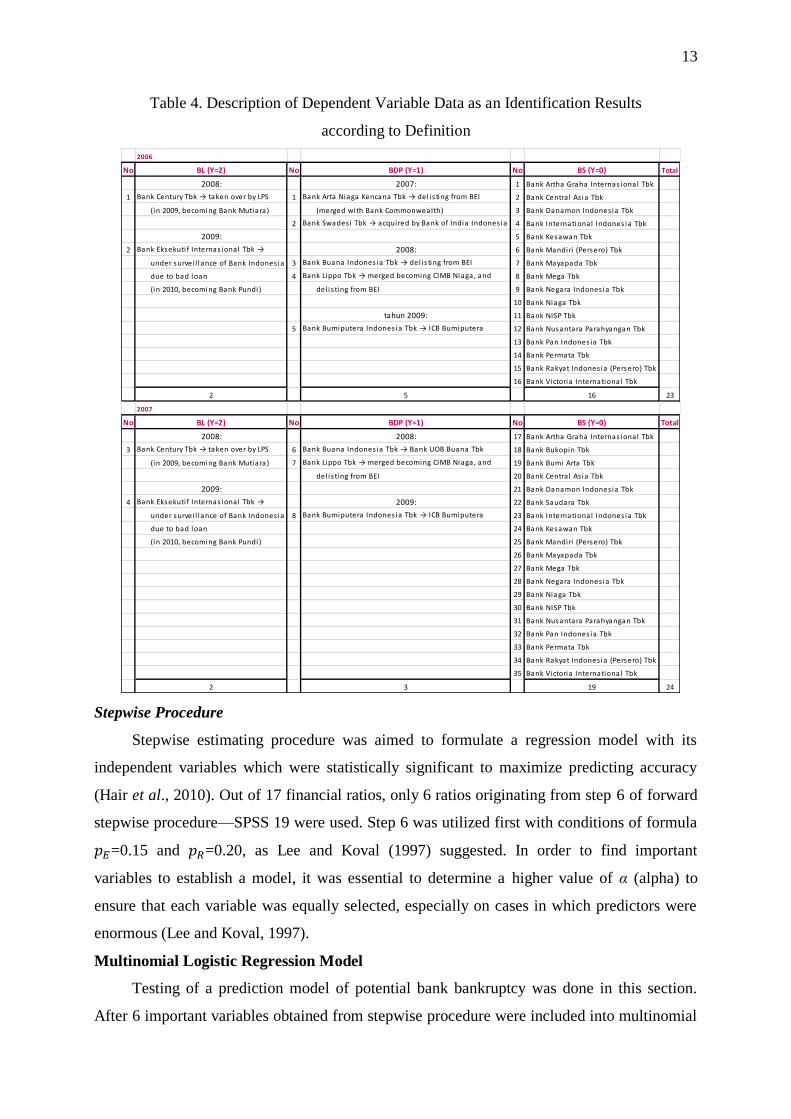

Table 4. Description of Dependent Variable Data as an Identification Results

according to Definition

Stepwise Procedure

Stepwise estimating procedure was aimed to formulate a regression model with its

independent variables which were statistically significant to maximize predicting accuracy

(Hair et al., 2010). Out of 17 financial ratios, only 6 ratios originating from step 6 of forward

stepwise procedure—SPSS 19 were used. Step 6 was utilized first with conditions of formula

=0.15 and =0.20, as Lee and Koval (1997) suggested. In order to find important

variables to establish a model, it was essential to determine a higher value of α (alpha) to

ensure that each variable was equally selected, especially on cases in which predictors were

enormous (Lee and Koval, 1997).

Multinomial Logistic Regression Model

Testing of a prediction model of potential bank bankruptcy was done in this section.

After 6 important variables obtained from stepwise procedure were included into multinomial

2006

No BL (Y=2) No BDP (Y=1) No BS (Y=0) Total

2008: 2007: 1 Bank Artha Graha Internas ional Tbk

1 Bank Century Tbk → taken over by LPS 1 Bank Arta Niaga Kencana Tbk → del is ting from BEI 2 Bank Centra l As ia Tbk

(in 2009, becoming Bank Mutiara) (merged with Bank Commonwealth) 3 Bank Danamon Indones ia Tbk

2 Bank Swades i Tbk → acquired by Bank of India Indones ia 4 Bank International Indones ia Tbk

2009: 5 Bank Kesawan Tbk

2 Bank Eksekuti f Internas ional Tbk → 2008: 6 Bank Mandiri (Persero) Tbk

under survei l lance of Bank Indones ia 3 Bank Buana Indones ia Tbk → del is ting from BEI 7 Bank Mayapada Tbk

due to bad loan 4 Bank Lippo Tbk → merged becoming CIMB Niaga, and 8 Bank Mega Tbk

(in 2010, becoming Bank Pundi ) del i s ting from BEI 9 Bank Negara Indones ia Tbk

10 Bank Niaga Tbk

tahun 2009: 11 Bank NISP Tbk

5 Bank Bumiputera Indones ia Tbk → ICB Bumiputera 12 Bank Nusantara Parahyangan Tbk

13 Bank Pan Indones ia Tbk

14 Bank Permata Tbk

15 Bank Rakyat Indones ia (Persero) Tbk

16 Bank Victoria International Tbk

2 5 16 23

2007

No BL (Y=2) No BDP (Y=1) No BS (Y=0) Total

2008: 2008: 17 Bank Artha Graha Internas ional Tbk

3 Bank Century Tbk → taken over by LPS 6 Bank Buana Indones ia Tbk → Bank UOB Buana Tbk 18 Bank Bukopin Tbk

(in 2009, becoming Bank Mutiara) 7 Bank Lippo Tbk → merged becoming CIMB Niaga, and 19 Bank Bumi Arta Tbk

del i s ting from BEI 20 Bank Centra l As ia Tbk

2009: 21 Bank Danamon Indones ia Tbk

4 Bank Eksekuti f Internas ional Tbk → 2009: 22 Bank Saudara Tbk

under survei l lance of Bank Indones ia 8 Bank Bumiputera Indones ia Tbk → ICB Bumiputera 23 Bank International Indones ia Tbk

due to bad loan 24 Bank Kesawan Tbk

(in 2010, becoming Bank Pundi ) 25 Bank Mandiri (Persero) Tbk

26 Bank Mayapada Tbk

27 Bank Mega Tbk

28 Bank Negara Indones ia Tbk

29 Bank Niaga Tbk

30 Bank NISP Tbk

31 Bank Nusantara Parahyangan Tbk

32 Bank Pan Indones ia Tbk

33 Bank Permata Tbk

34 Bank Rakyat Indones ia (Persero) Tbk

35 Bank Victoria International Tbk

2 3 19 24

14

logistic regression model, multinomial logistic regression equation from STATA 11 data

analysis was obtained.

Tabel 5. Multinomial Logit Model

Multinomial logistic regression model resulted in 2 logit functions, with condition that

surviving banks (BS) became a comparing category. These two functions later were becoming

2 formulas leading to three probabilities of BS, BDP, and BL. These five formulas would

eventually become prediction models of potential bank bankruptcy, and tested through

holdout sample data (go-public banks registered in BEI in 2008). These holdout sample data

would be used to validate prediction models of potential bank bankruptcy which were

formulated from original sample. Here is presented 5 aforementioned formulas:

1200.392609.242710.1191845.4132088.621159.67182.5)|(

)|(ln)( OCFLEACC

xBSP

xBDPPxg BDP

1100.152653.352179.1401609.3782508.751550.50730.10)|(

)|(ln)( OCFLEACC

xBSP

xBLPxgBL

variable coefficient std error z p-value

Logit Model

bdp

c1 67.159 34.037 1.97 0.048**

c2 -62.088 28.580 -2.17 0.03**

a1 413.845 217.937 1.90 0.058*

e2 -119.710 57.099 -2.10 0.036**

l2 -24.609 11.366 -2.17 0.030**

ocf1 39.200 18.164 2.16 0.031**

intercept 5.182 3.870 1.34 0.181

bl

c1 50.550 30.270 1.67 0.095*

c2 -75.508 65.685 -1.15 0.250

a1 378.609 503.527 0.75 0.452

e2 -140.179 96.664 -1.45 0.147

l2 -35.653 29.036 -1.23 0.219

ocf1 15.100 16.123 0.94 0.349

intercept 10.730 8.161 1.31 0.189

Number of obs = 47

LR chi2(12) = 39.43

Prob > chi2 = 0.0001

Pseudo R2 = 0.5742

(**s igni fikan=5%; *s igni fikan=10%)

Prediction Correct predicted

survival 0 1 2 tota l

bs 34 1 0 35

97.14 2.86 0.00 100.00

bdp 2 5 1 8

25.00 62.50 12.50 100.00

bl 0 1 3 5

0.00 25.00 75.00 100.00

tota l 36 7 4 47

76.60 14.89 8.51 100.00

overa l l percentage 89.36

source: data processed_stata11

15

BSOCFLEACCOCFLEACC eexBSP

11.152653.352179.1401609.3782508.75155.5073.1012.392609.24271.1191845.4132088.621159.67182.51

1)|(

BDPOCFLEACCOCFLEACC

OCFLEACC

ee

exBDPP

11.152653.352179.1401609.3782508.75155.5073.1012.392609.24271.1191845.4132088.621159.67182.5

12.392609.24271.1191845.4132088.621159.67182.5

1)|(

BLOCFlEACCOCFLEACC

OCFLEACC

ee

exBLP

11.152653.352179.1401609.3782508.75155.5073.1012.392609.24271.1191845.4132088.621159.67182.5

11.152653.352179.1401609.3782508.75155.5073.10

1)|(

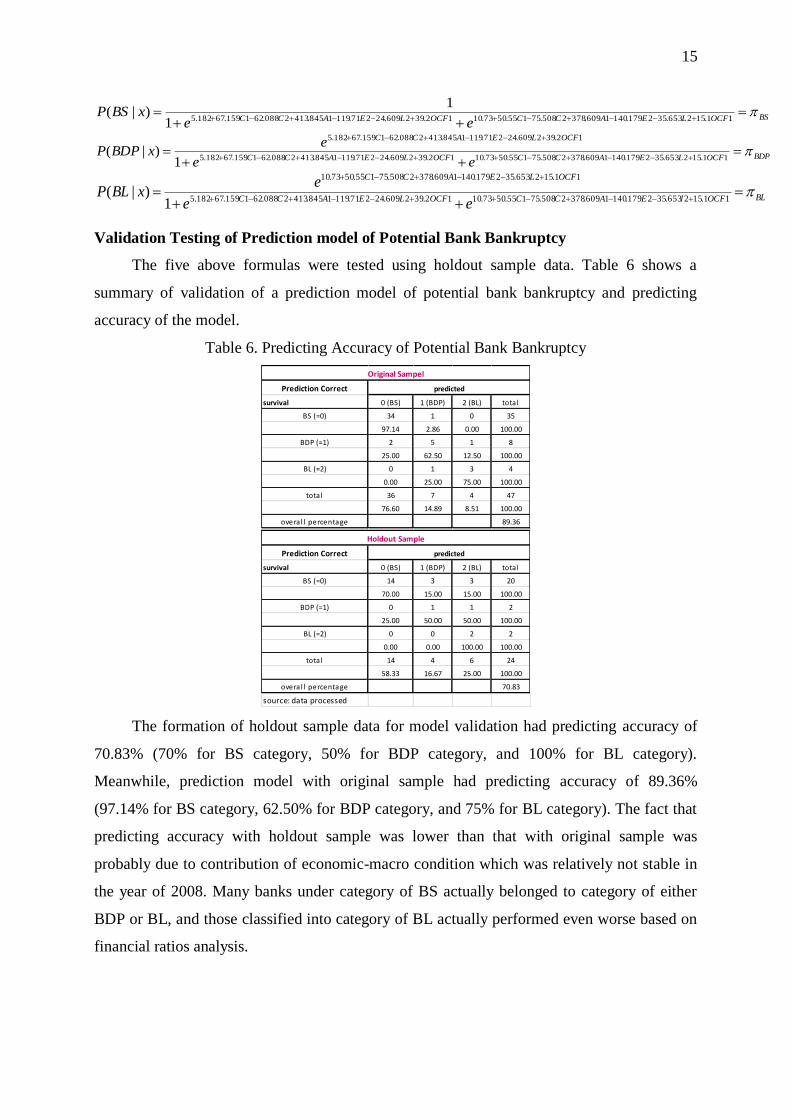

Validation Testing of Prediction model of Potential Bank Bankruptcy

The five above formulas were tested using holdout sample data. Table 6 shows a

summary of validation of a prediction model of potential bank bankruptcy and predicting

accuracy of the model.

Table 6. Predicting Accuracy of Potential Bank Bankruptcy

The formation of holdout sample data for model validation had predicting accuracy of

70.83% (70% for BS category, 50% for BDP category, and 100% for BL category).

Meanwhile, prediction model with original sample had predicting accuracy of 89.36%

(97.14% for BS category, 62.50% for BDP category, and 75% for BL category). The fact that

predicting accuracy with holdout sample was lower than that with original sample was

probably due to contribution of economic-macro condition which was relatively not stable in

the year of 2008. Many banks under category of BS actually belonged to category of either

BDP or BL, and those classified into category of BL actually performed even worse based on

financial ratios analysis.

Prediction Correct

survival 0 (BS) 1 (BDP) 2 (BL) tota l

BS (=0) 34 1 0 35

97.14 2.86 0.00 100.00

BDP (=1) 2 5 1 8

25.00 62.50 12.50 100.00

BL (=2) 0 1 3 4

0.00 25.00 75.00 100.00

tota l 36 7 4 47

76.60 14.89 8.51 100.00

overa l l percentage 89.36

Prediction Correct

survival 0 (BS) 1 (BDP) 2 (BL) tota l

BS (=0) 14 3 3 20

70.00 15.00 15.00 100.00

BDP (=1) 0 1 1 2

25.00 50.00 50.00 100.00

BL (=2) 0 0 2 2

0.00 0.00 100.00 100.00

tota l 14 4 6 24

58.33 16.67 25.00 100.00

overa l l percentage 70.83

source: data processed

Original Sampel

Holdout Sample

predicted

predicted

16

Analysis of Prediction model of Potential Bank Bankruptcy

In order to create a firm pillar for Indonesia banking system, Indonesia government

established API in January 2004. It has done numerous preventive actions to save Indonesian

banking business. One of these actions was merger and acquisition of banks. It was found that

there were go-public banks under Bank Indonesia’s (BI) special surveillance because of

credits which did not run smoothly; liquidated (acquired) banks; and merged banks to save

them from bankruptcy and enable them to perform better. This research attempted to analyze

whether or not financial ratios were capable of predicting bank survival and classifying banks

in Indonesia into three categories: BS, BDP and BL.

It was found that according to data analysis using STATA 11, financial ratios which had

capability of predicting bank survival were capital adequacy ratio (C1, C2), assets quality

ratio (A1), earnings (E2), liquidity (L2), and cash flow from operations (OCF1). Significant

value was obtained for functions of logit 1 (BDP) and logit 2 (BL) toward variable C1 (capital

adequacy ratio). On the other hand, toward variables C2, E2, L2, and OCF1, the value was

obtained for function of logit 1 (BDP), meaning that p-value was lower than alpha 0.05, while

the value of variable A1 was statistically significant for function of logit 1, with alpha 0.10.

Capital is an important factor for the establishment of sustainability of banking

business. Once one particular bank has settled its capital, it would try to expand its business

operations, anticipate coming risks, develop its technological system, and improve its capacity

of distributing loan (credit). These all actions are initiated to strengthen its capacity of

generating profits. At the end, it would achieve its ultimate sustainability. Ratios of assets

quality, earnings, liquidity, and cash flow from operations have significantly contributed to

the establishment of prediction model of potential bank bankruptcy. Strong capital, increased

profits, high liquidity, and cash flow from operations are capable of maintaining sustainability

of bank business operations, as well as there is no poor corporate governance prone to moral

hazard. As a consequence, this condition leads to sustainability of banking business

operations.

CONCLUSION AND SUGGESTIONS

Conclusion

It was evident that financial ratios on the basis of multinomial logistic regression model

might significantly be a detecting device of early potential bank bankruptcy. These ratios

included C1: capital adequacy ratio, C2: risk assets ratio, A1: return on risk assets, E2:

return on equity capital, L2: quick ratio, and OCF1: cash flow from operations/current

17

liabilities. These six ratios eventually formulated five statistical formulas, expected to

contribute to the early anticipation and prevention of bank failure. Predicting accuracy of this

model was 89.36% for original sample, and 70.83% for holdout sample used for model

validation.

C1 ratio was proved effectively contributing to the classification of banks into BDP

category and BL category, shown by a significant value of 2 logit functions. High capital

could improve bank business operations, with condition that there should be well-maintained

risk management system to avoid credits which didn’t run well. Meanwhile, earnings and

liquidity ratios had negative influence on function of logit 1, and were not significantly

correlated with function of logit 2. This means that the higher the earnings (E2) and liquidity

(L2) ratios were, the lower risk it was that the bank belonged to BDP category.

Suggestions

This prediction model had Pseudo R2 57.42%, indicating that there was other

information which probably influences the prediction of potential bank bankruptcy. Banking

system might also be influenced by political situation of a country (Indonesia), economic

macro condition, BI (Bank Indonesia) policies, and corporate governance of a particular bank

itself. These elements must be the main focus in next studies in an attempt to obtain a more

comprehensive prediction model of bank bankruptcy for the sake of the achievement of good

economic welfare of a nation through strong banking system. It is evident that poor

management causes moral hazard which may ruin a bank.

Computerized world which develops very rapidly bears a variety of statistical methods

allowing researchers to establish prediction models of potential bank bankruptcy. Next studies

need to compare statistical methods in order to obtain prediction model which is close to the

real condition. These statistical methods include neural network, trait recognition, data

envelopment analysis (DEA) though they are hardly easy to interpret and their mathematical

language seems hard.

REFERENCES

Andersen, Henrik. (2008). Failure prediction of Norwegian banks: A logit approach.

Working Paper. Financial Markets Department, Norges Bank.

Aryati, Titik, & Hekinus Manao. (2000). Rasio Keuangan sebagai Prediktor Bank

Bermasalah di Indonesia. Simposium Nasional Akuntansi III, Depok.

Bauman, Mark P. (2003). The Impact and Valuation of Off-Balance-Sheet Activities

Concealed by Equity Method Accounting. Accounting Horizons, Vol. 17(4): 303-314.

Beaver, William H. (1966). Financial Ratios As Predictors of Failure. Journal of Accounting

Research, Vol. 4: 71-111.

18

Bernstein, Leopold A. (1989). Financial Statement Analysis: Theory, Application, and

Interpretation. Richard D. Irwin, Inc., Illinois.

Bodie, Kane, & Marcus. (2011). Investments and Portfolio Management, 9th

Edition, Irwin

McGraw Hill, Singapore.

Cheng, Chi-Bin, Ching-Lung Chen, & Chung-Jen Fu. (2006). Financial Distress Prediction

by a Radial Basis Function Network with Logit Analysis Learning. Computers and

Mathematics with Applications, 51: 579-588.

Choudhry, Moorad. (2007). Bank Asset and Liability Management: Strategy, Trading,

Analysis. John Wiley & Sons (Asia) Pte. Ltd., Singapore.

Eisenbeis, Robert A. (1977). Pitfalls in the Application of Discriminant Analysis in Business,

Finance, and Economics. The Journal of Finance, Vol. 32(3): 875-900.

Espahbodi, Pouran. (1991). Identification of problem binary choice models. Journal of

Banking and Finance, Vol. 15: 53-71.

FASB. (1978). Statement of Financial Accounting Concept No. 1: Objectives of Financial

Reporting by Business Enterprises.

Fraser, Donald R., & Lyn M. Fraser. (1990). Evaluating Commercial Bank Performance: A

Guide to Financial Analysis. Bankers Publishing Company, Illinois.

Ghosh, Amalendu. (2012). Managing Risks in Commercial and Retail Banking. John Wiley

& Sons (Asia) Pte. Ltd., Singapore.

Grice, John Stephen, & Robert W. Ingram. (2001). Tests of the generalizability of Altman’s

bankruptcy prediction model. Journal of Business Research, 54: 53-61.

Hair, Joseph F., William C. Black, Barry J. Babin, & Rolph E. Anderson. (2010).

Multivariate Data Analysis: A Global Perspective. Pearson Prentice Hall, New Jersey.

Hosmer, David W., & Stanley Lemeshow. (2000). Applied Logistic Regression, 2nd

Edition.

John Wiley & Sons, Inc.

Kasmir. (2000). Manajemen Perbankan. PT RajaGrafindo Persada, Jakarta.

Koetter, M., J.W.B. Bos, F. Heid, J.W. Kolari, C.J.M. Kool, D. Porath. (2007). Accounting

for distress in bank mergers. Journal of Banking & Finance, 31: 3200-3217.

Kolari, James, Dennis Glennon, Hwan Shin, & Michele Caputo. (2002). Predicting large US

commercial bank failures. Journal of Economics and Business, 54: 361-387.

Kumar, P. Ravi, & V. Ravi. (2007). Bankruptcy prediction in banks and firms via statistical

and intelligent techniques – A review. European Journal of Operational Research, 180:

1-28.

Lee, Kang-In, & John J. Koval. (1997). Determination of the Best Significance Level in

Forward Stepwise Logistic Regression. Communication in Statistics–Simulation and

Computation, 26(2): 559-575.

Lembaga Penjamin Simpanan (LPS). (2010 & 2011). Laporan Tahunan.

Martin, Daniel. (1977). Early Warning of Bank Failure: A logit regression approach. Journal

of Banking and Finance, 1: 249-276.

Mintorahardjo, Sukowaluyo. (2001). BLBI Simalakama. Riset Ekonomi Sosial Indonesia,

Jakarta.

19

Öğüt, Hulisi, M. Mete Doğanay, Nildağ Başak Ceylan, & Ramazan Aktaş. (2012). Prediction

of bank financial strength ratings: The case of Turkey. Economic Modelling, 29: 632-

640.

Payamta. (2008). Model Deteksi Dini Kesehatan Bank Umum di Indonesia. Jurnal Bisnis &

Manajemen, Vol. 8(2): 163-178.

Premachandra, I.M., Gurmeet Singh Bhabra, Toshiyuki Sueyoshi. (2009). DEA as a tool for

predicting corporate failure and success: A case of bankruptcy assessment. European

Journal of Operational Research, 193: 412-424.

Premachandra, I.M., Yao Chen, & John Watson. (2011). DEA as a tool for predicting

corporate failure and success: A case of bankruptcy assessment. Omega, 39: 620-626.

Qurriyani, Tengku Nuzulul. (2000). Indikasi Potensial menuju Bank Survival melalui Analisis

Rasio Keuangan: Model Regresi Logistik Trikotomi. Karya Akhir. Program Magister

Akuntansi, Fakultas Ekonomi Universitas Indonesia, Jakarta.

Ritter, Lawrence S., William L. Silber, & Gregory F. Udell. (2009). Principles of Money,

Banking & Financial Markets.Pearson Education, Inc., Boston.

Rujoub, Mohamed A., Doris M. Cook, & Leon E. Hay. (1995). Using Cash Flow Ratios To

Predict Business Failures. Journal of Managerial Issues, Vol. 7(1): 75-90.

Schilit, Howard M., & Jeremy Perler. (2010). Financial Shenanigans. McGraw-Hill.

Smith, C. W. Jr., & Ross L. Watts. (1992). The investment opportunity set and corporate

financing, dividend and compensation policies. Journal of Financial Economics, 32:

263-292.

Stickney, Clyde P., & Paul R. Brown. (1999). Financial Reporting and Statement Analysis: A

Strategic Perspective, 4th

Edition. Harcourt Brace & Company, Orlando.

Stiglitz, Joseph E. (2012). Kegagalan Globalisasi dan Lembaga-Lembaga Keuangan

Internasional. PT Ina Publikatama, Jakarta.

Surifah. (2002). Kinerja Keuangan Perbankan Swasta Nasional Indonesia sebelum dan

setelah Krisis Ekonomi. Jurnal Auditing dan Akuntansi Indonesia, Vol. 6(2): 23-50.

Watts, Ross L., & Jerold L. Zimmerman. (1986). Positive Accounting Theory. Prentice-Hall

Inc.

White, Gerald I., Ashwinpaul C. Sondhi, & Dov Fried. (2003). The Analysis and Use of

Financial Statements, 3rd

Edition. John Wiley & Sons, Inc., USA.

20

Appendix 1. Description of Independent Variable Data

2006

no bank go public C1 C2 A1 E2 L2 OCF1

bank likuidasi (bl) (Y=2)

1 Bank Century Tbk. 0.103 0.087 0.008 0.046 0.149 -0.014

2 Bank Eksekutif International Tbk. 0.014 0.097 -0.022 -0.118 0.105 0.016

bank dalam penyelamatan (bdp) (Y=1)

3 Bank Arta Niaga Kencana Tbk. 0.090 0.153 0.016 0.088 0.090 0.036

4 Bank Swadesi Tbk. 0.220 0.208 0.026 0.071 0.486 0.071

5 Bank UOB Buana Tbk. 0.213 0.268 0.043 0.125 0.091 0.058

6 Bank Lippo Tbk. 0.202 0.148 0.045 0.151 0.350 0.146

7 Bank Bumiputera Indonesia Tbk. 0.111 0.115 0.003 0.015 0.109 0.036

bank sehat (bs) (Y=0)

8 Bank Artha Graha International Tbk. 0.050 0.065 0.005 0.056 0.122 0.012

9 Bank Central Asia Tbk. 0.139 0.242 0.053 0.235 0.310 0.046

10 Bank Danamon Indonesia Tbk. 0.122 0.191 0.032 0.140 0.126 0.027

11 Bank International Indonesia Tbk. 0.119 0.160 0.020 0.121 0.102 -0.001

12 Bank Kesawan Tbk. 0.055 0.080 0.004 0.032 0.097 -0.143

13 Bank Mandiri (Persero) Tbk. 0.109 0.199 0.014 0.092 0.185 0.056

14 Bank Mayapada Tbk. 0.055 0.105 0.021 0.107 0.077 0.018

15 Bank Mega Tbk. 0.049 0.145 0.009 0.078 0.111 0.216

16 Bank Negara Indonesia (Persero) Tbk. 0.098 0.140 0.026 0.130 0.129 0.062

17 Bank Niaga Tbk. 0.112 0.130 0.024 0.135 0.091 0.037

18 Bank NISP Tbk. 0.092 0.139 0.017 0.097 0.089 0.008

19 Bank Nusantara Parahyangan Tbk. 0.098 0.137 0.017 0.109 0.105 0.100

20 Bank Pan Indonesia Tbk. 0.249 0.235 0.049 0.110 0.365 -0.093

21 Bank Permata 0.082 0.137 0.016 0.085 0.143 0.048

22 Bank Rakyat Indonesia (Persero) Tbk. 0.143 0.181 0.056 0.252 0.314 0.109

23 Bank Victoria International Tbk. 0.109 0.224 0.016 0.095 0.072 -0.027

2007

no bank go public C1 C2 A1 E2 L2 OCF1

bank likuidasi (bl) (Y=2)

24 Bank Century Tbk. 0.144 0.114 0.007 0.049 0.108 -0.030

25 Bank Eksekutif International Tbk. 0.006 0.097 0.002 0.006 0.090 -0.014

bank dalam penyelamatan (bdp) (Y=1)

26 Bank UOB Buana Tbk. 0.207 0.253 0.039 0.118 0.084 -0.084

27 Bank Lippo Tbk. 0.154 0.142 0.053 0.190 0.308 0.027

28 Bank Bumiputera Indonesia Tbk. 0.107 0.099 0.007 0.038 0.114 -0.016

bank sehat (bs) (Y=0)

29 Bank Artha Graha International Tbk. 0.064 0.072 0.004 0.024 0.239 -0.010

30 Bank Bukopin Tbk. 0.064 0.083 0.021 0.191 0.140 -0.074

31 Bank Bumi Arta Tbk. 0.332 0.391 0.038 0.056 0.653 0.022

32 Bank Central Asia Tbk. 0.132 0.214 0.046 0.220 0.342 0.046

33 Bank Danamon Indonesia Tbk. 0.137 0.171 0.048 0.195 0.126 -0.081

34 Bank Saudara Tbk 0.135 0.133 0.040 0.176 0.082 -0.003

35 Bank International Indonesia Tbk. 0.110 0.144 0.009 0.076 0.110 -0.107

36 Bank Kesawan Tbk. 0.051 0.090 0.004 0.047 0.100 -0.023

37 Bank Mandiri (Persero) Tbk. 0.113 0.174 0.029 0.149 0.225 0.022

38 Bank Mayapada Tbk. 0.206 0.250 0.017 0.043 0.082 -0.282

39 Bank Mega Tbk. 0.077 0.174 0.026 0.177 0.116 -0.009

40 Bank Negara Indonesia (Persero) Tbk. 0.099 0.158 0.011 0.052 0.139 0.067

41 Bank Niaga Tbk. 0.105 0.112 0.023 0.148 0.082 -0.024

42 Bank NISP Tbk. 0.116 0.147 0.015 0.074 0.101 -0.046

43 Bank Nusantara Parahyangan Tbk. 0.093 0.162 0.015 0.102 0.120 0.125

44 Bank Pan Indonesia Tbk. 0.153 0.196 0.038 0.127 0.168 -0.055

45 Bank Permata 0.093 0.133 0.026 0.130 0.234 -0.001

46 Bank Rakyat Indonesia (Persero) Tbk. 0.132 0.159 0.058 0.249 0.323 0.140

47 Bank Victoria International Tbk. 0.063 0.166 0.013 0.123 0.078 -0.024