dsge models and central bank policy making: a critical review

TRANSCRIPT

DSGE Models and Central Bank Policy

Making: A Critical Review

Shiu-Sheng Chen

Department of Economics

National Taiwan University

12.16.2010

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 1 / 37

Motivations

On July 20, 2010, the U.S. House of

Representatives Committee on Science and

Technology held a hearing on “Building a Science of

Economics for the Real World.”

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 2 / 37

Motivations

The hearing explored◮ the failure of mainstream macroeconomic models to

foresee the recent financial and economic collapse◮ the promise and the limits of modern macroeconomic

theory in policy making.

The macroeconomic model called the Dynamic

Stochastic General Equilibrium model (DSGE) is

favored today, from academy to the world’s central

banks.

However, prominent economists disagree on the

extent to which applying this theoretical model to

policy decisions is practical.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 3 / 37

Motivations

The hearing explored◮ the failure of mainstream macroeconomic models to

foresee the recent financial and economic collapse◮ the promise and the limits of modern macroeconomic

theory in policy making.

The macroeconomic model called the Dynamic

Stochastic General Equilibrium model (DSGE) is

favored today, from academy to the world’s central

banks.

However, prominent economists disagree on the

extent to which applying this theoretical model to

policy decisions is practical.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 3 / 37

Motivations

The hearing explored◮ the failure of mainstream macroeconomic models to

foresee the recent financial and economic collapse◮ the promise and the limits of modern macroeconomic

theory in policy making.

The macroeconomic model called the Dynamic

Stochastic General Equilibrium model (DSGE) is

favored today, from academy to the world’s central

banks.

However, prominent economists disagree on the

extent to which applying this theoretical model to

policy decisions is practical.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 3 / 37

Agenda for Today’s Talk

Introduction to DSGE models.◮ To be fair, DGSE and similar macroeconomic models

were first conceived as theorists’ tools.◮ But why, then, are they being relied on as the platform

upon which so much practical policy advice is

formulated?

The critiques on the DSGE models.

The perspectives on the DSGE models.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 4 / 37

Agenda for Today’s Talk

Introduction to DSGE models.◮ To be fair, DGSE and similar macroeconomic models

were first conceived as theorists’ tools.◮ But why, then, are they being relied on as the platform

upon which so much practical policy advice is

formulated?

The critiques on the DSGE models.

The perspectives on the DSGE models.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 4 / 37

Agenda for Today’s Talk

Introduction to DSGE models.◮ To be fair, DGSE and similar macroeconomic models

were first conceived as theorists’ tools.◮ But why, then, are they being relied on as the platform

upon which so much practical policy advice is

formulated?

The critiques on the DSGE models.

The perspectives on the DSGE models.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 4 / 37

Part I

Introduction to DSGE Models

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 5 / 37

Introduction to DSGE Models

What is DSGE Model?

Dynamic Stochastic General Equilibrium Model

Dynamic: studying how the economy evolves over

time.

Stochastic: the economy is affected by random

shocks.

General Equilibrium: It depicts the macro-economy

as the sum of individual choices and decisions made

by firms, households, the government, and the

central bank, according to their own preferences and

views about the future.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 6 / 37

Introduction to DSGE Models

What is DSGE Model?

Dynamic Stochastic General Equilibrium Model

Dynamic: studying how the economy evolves over

time.

Stochastic: the economy is affected by random

shocks.

General Equilibrium: It depicts the macro-economy

as the sum of individual choices and decisions made

by firms, households, the government, and the

central bank, according to their own preferences and

views about the future.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 6 / 37

Introduction to DSGE Models

Advantages of the DSGE Models

Provide a coherent framework of analysis. This

coherence is brought by restricting acceptable

behavior of agents to dynamic utility maximization

and rational expectations.

The dynamic mechanics are more transparent and

clear and (impulse response functions with

structural shocks).Overcome the Lucas Critique (Policy experimentsare more reliable)

◮ Lucas (1976) argues that the Keynesian

Macroeconometric models are useless for policy analysis

because they fail to take expectations seriously.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 7 / 37

Introduction to DSGE Models

Advantages of the DSGE Models

Provide a coherent framework of analysis. This

coherence is brought by restricting acceptable

behavior of agents to dynamic utility maximization

and rational expectations.

The dynamic mechanics are more transparent and

clear and (impulse response functions with

structural shocks).Overcome the Lucas Critique (Policy experimentsare more reliable)

◮ Lucas (1976) argues that the Keynesian

Macroeconometric models are useless for policy analysis

because they fail to take expectations seriously.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 7 / 37

Introduction to DSGE Models

Advantages of the DSGE Models

Provide a coherent framework of analysis. This

coherence is brought by restricting acceptable

behavior of agents to dynamic utility maximization

and rational expectations.

The dynamic mechanics are more transparent and

clear and (impulse response functions with

structural shocks).Overcome the Lucas Critique (Policy experimentsare more reliable)

◮ Lucas (1976) argues that the Keynesian

Macroeconometric models are useless for policy analysis

because they fail to take expectations seriously.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 7 / 37

Introduction to DSGE Models

Historical Background

Indeed, the DSGE approach is not new at all.

What was DSGE Model?

The Real Business Cycle (RBC) models in 1980s.◮ Kydland and Prescott (1982)◮ Long and Plosser (1983)

However, why did the RBC models fail to grab

Central Bankers’ attention?

Well, the related question is: why are the Central

Bankers so fascinated with DSGE models nowadays?

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 8 / 37

Introduction to DSGE Models

Historical Background

Indeed, the DSGE approach is not new at all.

What was DSGE Model?

The Real Business Cycle (RBC) models in 1980s.◮ Kydland and Prescott (1982)◮ Long and Plosser (1983)

However, why did the RBC models fail to grab

Central Bankers’ attention?

Well, the related question is: why are the Central

Bankers so fascinated with DSGE models nowadays?

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 8 / 37

Introduction to DSGE Models

Historical Background

Indeed, the DSGE approach is not new at all.

What was DSGE Model?

The Real Business Cycle (RBC) models in 1980s.◮ Kydland and Prescott (1982)◮ Long and Plosser (1983)

However, why did the RBC models fail to grab

Central Bankers’ attention?

Well, the related question is: why are the Central

Bankers so fascinated with DSGE models nowadays?

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 8 / 37

Introduction to DSGE Models

Historical Background

Indeed, the DSGE approach is not new at all.

What was DSGE Model?

The Real Business Cycle (RBC) models in 1980s.◮ Kydland and Prescott (1982)◮ Long and Plosser (1983)

However, why did the RBC models fail to grab

Central Bankers’ attention?

Well, the related question is: why are the Central

Bankers so fascinated with DSGE models nowadays?

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 8 / 37

Introduction to DSGE Models

Historical Background

In the past, RBC models have the following features:

◮ Flexible prices◮ Focus on calibration.

⋆ Moments matching and policy experiments.

◮ However, no emphasis on estimation and forecasting.◮ The RBC models (old DSGE models) have difficulty to

match persistence in data with i.i.d. structural shocks

(weak internal propagation mechanism).◮ Most importantly, the RBC models emphasize real

shocks only.◮ Although some researchers try to incorporate money into

the RBC models, it is in general found that money is

neutral under flexible-price framework.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 9 / 37

Introduction to DSGE Models

Historical Background

In the past, RBC models have the following features:

◮ Flexible prices◮ Focus on calibration.

⋆ Moments matching and policy experiments.

◮ However, no emphasis on estimation and forecasting.◮ The RBC models (old DSGE models) have difficulty to

match persistence in data with i.i.d. structural shocks

(weak internal propagation mechanism).◮ Most importantly, the RBC models emphasize real

shocks only.◮ Although some researchers try to incorporate money into

the RBC models, it is in general found that money is

neutral under flexible-price framework.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 9 / 37

Introduction to DSGE Models

Historical Background

In the past, RBC models have the following features:

◮ Flexible prices◮ Focus on calibration.

⋆ Moments matching and policy experiments.

◮ However, no emphasis on estimation and forecasting.◮ The RBC models (old DSGE models) have difficulty to

match persistence in data with i.i.d. structural shocks

(weak internal propagation mechanism).◮ Most importantly, the RBC models emphasize real

shocks only.◮ Although some researchers try to incorporate money into

the RBC models, it is in general found that money is

neutral under flexible-price framework.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 9 / 37

Introduction to DSGE Models

Historical Background

In the past, RBC models have the following features:

◮ Flexible prices◮ Focus on calibration.

⋆ Moments matching and policy experiments.

◮ However, no emphasis on estimation and forecasting.◮ The RBC models (old DSGE models) have difficulty to

match persistence in data with i.i.d. structural shocks

(weak internal propagation mechanism).◮ Most importantly, the RBC models emphasize real

shocks only.◮ Although some researchers try to incorporate money into

the RBC models, it is in general found that money is

neutral under flexible-price framework.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 9 / 37

Introduction to DSGE Models

Historical Background

In the past, RBC models have the following features:

◮ Flexible prices◮ Focus on calibration.

⋆ Moments matching and policy experiments.

◮ However, no emphasis on estimation and forecasting.◮ The RBC models (old DSGE models) have difficulty to

match persistence in data with i.i.d. structural shocks

(weak internal propagation mechanism).◮ Most importantly, the RBC models emphasize real

shocks only.◮ Although some researchers try to incorporate money into

the RBC models, it is in general found that money is

neutral under flexible-price framework.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 9 / 37

Introduction to DSGE Models

Historical Background

In the past, RBC models have the following features:

◮ Flexible prices◮ Focus on calibration.

⋆ Moments matching and policy experiments.

◮ However, no emphasis on estimation and forecasting.◮ The RBC models (old DSGE models) have difficulty to

match persistence in data with i.i.d. structural shocks

(weak internal propagation mechanism).◮ Most importantly, the RBC models emphasize real

shocks only.◮ Although some researchers try to incorporate money into

the RBC models, it is in general found that money is

neutral under flexible-price framework.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 9 / 37

Introduction to DSGE Models

Historical Background

In the past, RBC models have the following features:

◮ Flexible prices◮ Focus on calibration.

⋆ Moments matching and policy experiments.

◮ However, no emphasis on estimation and forecasting.◮ The RBC models (old DSGE models) have difficulty to

match persistence in data with i.i.d. structural shocks

(weak internal propagation mechanism).◮ Most importantly, the RBC models emphasize real

shocks only.◮ Although some researchers try to incorporate money into

the RBC models, it is in general found that money is

neutral under flexible-price framework.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 9 / 37

Introduction to DSGE Models

Historical Background

So how can we expect that Central Bankers would

enjoy a model that monetary policy plays no role?

Nowadays, the development of DSGE models

become a broad-ranging search to discover a set of

frictions to reproduce realistic dynamics.

In particular, the most popular frictions are the

Keynesian elements such as sticky prices/wages.

Frictions such as stick prices open up the possibility

of the non-neutrality of monetary policy.

No wonder the central bankers like the models now.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 10 / 37

Introduction to DSGE Models

Historical Background

So how can we expect that Central Bankers would

enjoy a model that monetary policy plays no role?

Nowadays, the development of DSGE models

become a broad-ranging search to discover a set of

frictions to reproduce realistic dynamics.

In particular, the most popular frictions are the

Keynesian elements such as sticky prices/wages.

Frictions such as stick prices open up the possibility

of the non-neutrality of monetary policy.

No wonder the central bankers like the models now.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 10 / 37

Introduction to DSGE Models

Historical Background

So how can we expect that Central Bankers would

enjoy a model that monetary policy plays no role?

Nowadays, the development of DSGE models

become a broad-ranging search to discover a set of

frictions to reproduce realistic dynamics.

In particular, the most popular frictions are the

Keynesian elements such as sticky prices/wages.

Frictions such as stick prices open up the possibility

of the non-neutrality of monetary policy.

No wonder the central bankers like the models now.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 10 / 37

Introduction to DSGE Models

Historical Background

So how can we expect that Central Bankers would

enjoy a model that monetary policy plays no role?

Nowadays, the development of DSGE models

become a broad-ranging search to discover a set of

frictions to reproduce realistic dynamics.

In particular, the most popular frictions are the

Keynesian elements such as sticky prices/wages.

Frictions such as stick prices open up the possibility

of the non-neutrality of monetary policy.

No wonder the central bankers like the models now.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 10 / 37

Introduction to DSGE Models

Historical Background

So how can we expect that Central Bankers would

enjoy a model that monetary policy plays no role?

Nowadays, the development of DSGE models

become a broad-ranging search to discover a set of

frictions to reproduce realistic dynamics.

In particular, the most popular frictions are the

Keynesian elements such as sticky prices/wages.

Frictions such as stick prices open up the possibility

of the non-neutrality of monetary policy.

No wonder the central bankers like the models now.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 10 / 37

Introduction to DSGE Models

Historical Background

It is thus called a New Keynesian DSGE model, and

I will call it a “New DSGE” Model, in short.

Moreover, new DSGE models start to focus on

structural estimations (GMM, MLE, Bayesian).

So it is also called an Estimated DSGE Model,

which is able to provide forecasts on a regular basis.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 11 / 37

Introduction to DSGE Models

Historical Background

It is thus called a New Keynesian DSGE model, and

I will call it a “New DSGE” Model, in short.

Moreover, new DSGE models start to focus on

structural estimations (GMM, MLE, Bayesian).

So it is also called an Estimated DSGE Model,

which is able to provide forecasts on a regular basis.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 11 / 37

Introduction to DSGE Models

Historical Background

It is thus called a New Keynesian DSGE model, and

I will call it a “New DSGE” Model, in short.

Moreover, new DSGE models start to focus on

structural estimations (GMM, MLE, Bayesian).

So it is also called an Estimated DSGE Model,

which is able to provide forecasts on a regular basis.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 11 / 37

Introduction to DSGE Models

Macroeconometric Models, SVAR and DSGE Models

Macroeconometric SVAR Models DSGE Models

Models

Dynamic Yes Yes Yes

Stochastic Regression Residuals Structural Shocks Structural Shocks

General Loosely based on Based on Explicitly based on

Equilibrium theory in ad hoc economic structure optimization in

manner and theory coherent manner

Invalid Exogeneity Yes No No

Assumption

Policy Experiment Yes Yes Yes

(Reliable?) (No) (Yes) (Yes)

Forecast Yes Yes Yes

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 12 / 37

Introduction to DSGE Models

DSGE and Central Banks

According to the overall victory for DSGE models in

the above Table, no wonder why DSGE models are

becoming increasingly popular in central banking

circles over the past decade.

European Central Bank US Federal Reserve Bank

Sveriges Riksbank Bank of Canada

Bank of England Norges Bank

Bank of Finland Reserve Bank of New Zealand

Bank of Spain Central Bank of Brazil

Central Bank of Chile Central Reserve Bank of Peru

Bank of Thailand IMF

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 13 / 37

Introduction to DSGE Models

DSGE and Central Banks

However, before the central bankers proceed to

move to the new framework, some warnings about

the flaws and limitations of DSGE models should be

heeded.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 14 / 37

Introduction to DSGE Models

The State-of-the-Art DSGE Models

Smets and Wouters (2007) model◮ a large set of persistent exogenous shocks:

⋆ total factor productivity

⋆ investment-specific technology

⋆ risk premium

⋆ government spending

⋆ price mark-up

⋆ wage mark-up

⋆ monetary policy

◮ a large set of frictions:⋆ sticky wages and prices

⋆ sticky adjustment of capacity utilization

⋆ investment adjustment cost

⋆ habit formation in consumption

◮ a Taylor-rule-type monetary policy

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 15 / 37

Introduction to DSGE Models

The State-of-the-Art DSGE Models

The model is able to track and forecast 7macroeconomic time series data very well.

◮ GDP◮ consumption◮ investment◮ prices◮ wages◮ employment◮ short-run interest rates

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 16 / 37

Introduction to DSGE Models

The State-of-the-Art DSGE Models

I focus on this popular model because it is widely

considered to be the state-of-the-art DSGE model.

A version of the Smets-Wouters model is now being

used to inform policymaking at the European

Central Bank.

Hence, new DSGE models that follow approximately

this recipe are being formulated and coming into use

at central banks around the world.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 17 / 37

Introduction to DSGE Models

The State-of-the-Art DSGE Models

I focus on this popular model because it is widely

considered to be the state-of-the-art DSGE model.

A version of the Smets-Wouters model is now being

used to inform policymaking at the European

Central Bank.

Hence, new DSGE models that follow approximately

this recipe are being formulated and coming into use

at central banks around the world.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 17 / 37

Introduction to DSGE Models

The State-of-the-Art DSGE Models

I focus on this popular model because it is widely

considered to be the state-of-the-art DSGE model.

A version of the Smets-Wouters model is now being

used to inform policymaking at the European

Central Bank.

Hence, new DSGE models that follow approximately

this recipe are being formulated and coming into use

at central banks around the world.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 17 / 37

Part II

Critiques on New DSGE Models

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 18 / 37

Critiques

Critiques on New DSGE Models

The critiques I am going to offer are not meant to

humiliate the new DSGE models; however, I think

that the policymakers should ask hard questions

about the value of the model before adopting the

new approach.

The critiques:

◮ Lucas Critique strikes back◮ The shocks are dubiously structural◮ Empirical performance of the model

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 19 / 37

Critiques

Critiques on New DSGE Models

The critiques I am going to offer are not meant to

humiliate the new DSGE models; however, I think

that the policymakers should ask hard questions

about the value of the model before adopting the

new approach.

The critiques:

◮ Lucas Critique strikes back◮ The shocks are dubiously structural◮ Empirical performance of the model

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 19 / 37

Critiques

Lucas Critique Strikes Back

Indeed, the new DSGE models do not have solid

micro-foundation.

That is, some of the parameters are not “deep”

enough to be immune to the Lucas Critique.

The deep parameters are those that do not vary

with policy regime changes.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 20 / 37

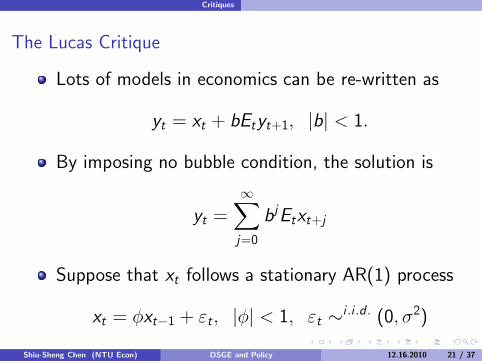

Critiques

The Lucas Critique

Lots of models in economics can be re-written as

yt = xt + bEtyt+1, |b| < 1.

By imposing no bubble condition, the solution is

yt =∞∑

j=0

bjEtxt+j

Suppose that xt follows a stationary AR(1) process

xt = φxt−1 + εt, |φ| < 1, εt ∼i .i .d . (0, σ2)

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 21 / 37

Critiques

The Lucas Critique

Hence,

Etxt+j = φjxt ,

and the model solution is

yt =1

1− bφxt .

It is called a reduced-form solution.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 22 / 37

Critiques

The Lucas Critique

The structural model is

yt =

∞∑

j=0

bjEtxt+j

The reduced-form representation

yt =1

1− bφxt

depends on the process for xt with a particular form.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 23 / 37

Critiques

The Lucas Critique

Hence, if the xt process change, the reduced-form

process will change. For instance, if the precess

changes to xt = ωxt−1 + εt , the reduced-form

representation changes as well:

yt =1

1− bωxt

Robert Lucas pointed out that the reduced-form

econometric model based on historical data

yt = βxt

is useless for policy analysis.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 24 / 37

Critiques

The Lucas Critique

Hence, if the xt process change, the reduced-form

process will change. For instance, if the precess

changes to xt = ωxt−1 + εt , the reduced-form

representation changes as well:

yt =1

1− bωxt

Robert Lucas pointed out that the reduced-form

econometric model based on historical data

yt = βxt

is useless for policy analysis.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 24 / 37

Critiques

Lucas Critique Strikes Back

Well, what’s wrong with the new DSGE models?

The new DSGE models generally exogenously

impose that firms can only change prices at certain

exogenously chosen points in time–those points may

be stochastic (Calvo pricing) or deterministic

(Taylor contracts).

These frictions are ad hoc, i.e., no micro-foundation

for price stickness is provided.

The deep parameters that govern the firms’ optimal

choice to fix the price have not been investigated.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 25 / 37

Critiques

Lucas Critique Strikes Back

Well, what’s wrong with the new DSGE models?

The new DSGE models generally exogenously

impose that firms can only change prices at certain

exogenously chosen points in time–those points may

be stochastic (Calvo pricing) or deterministic

(Taylor contracts).

These frictions are ad hoc, i.e., no micro-foundation

for price stickness is provided.

The deep parameters that govern the firms’ optimal

choice to fix the price have not been investigated.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 25 / 37

Critiques

Lucas Critique Strikes Back

Well, what’s wrong with the new DSGE models?

The new DSGE models generally exogenously

impose that firms can only change prices at certain

exogenously chosen points in time–those points may

be stochastic (Calvo pricing) or deterministic

(Taylor contracts).

These frictions are ad hoc, i.e., no micro-foundation

for price stickness is provided.

The deep parameters that govern the firms’ optimal

choice to fix the price have not been investigated.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 25 / 37

Critiques

Lucas Critique Strikes Back

Well, what’s wrong with the new DSGE models?

The new DSGE models generally exogenously

impose that firms can only change prices at certain

exogenously chosen points in time–those points may

be stochastic (Calvo pricing) or deterministic

(Taylor contracts).

These frictions are ad hoc, i.e., no micro-foundation

for price stickness is provided.

The deep parameters that govern the firms’ optimal

choice to fix the price have not been investigated.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 25 / 37

Critiques

The Shocks are Dubiously Structural

A structural shock must have two properties◮ The shocks must be uncorrelated with policy

interventions.◮ The shocks should have an appropriate economic

interpretation.

Most of the shocks in the new DSGE models:◮ wage markup shocks◮ price markup shocks◮ government spending shocks◮ risk premium shocks

fail to meet the above requirements, and are

dubiously structural.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 26 / 37

Critiques

The Shocks are Dubiously Structural

A structural shock must have two properties◮ The shocks must be uncorrelated with policy

interventions.◮ The shocks should have an appropriate economic

interpretation.

Most of the shocks in the new DSGE models:◮ wage markup shocks◮ price markup shocks◮ government spending shocks◮ risk premium shocks

fail to meet the above requirements, and are

dubiously structural.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 26 / 37

Critiques

The Shocks are Dubiously Structural

In particular, wage markup shocks are frequently

criticized on the basis that they have different and

somewhat conflicted interpretations/policy

implications.

Wage markup shocks◮ Bargaining power of the labor union

(Allocation is inefficient, the optimal policy is to limit

the monopoly power)◮ Worker’s leisure preference

(Allocation is efficient, laissez-faire is optimal)

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 27 / 37

Critiques

The Shocks are Dubiously Structural

Moreover, price markup shocks are not orthogonal

to other structural shocks.

Price markup shocks

◮ Change in tax rate◮ Degree of competition

Clearly, these interpretations are affected by

economic situations, which are certainly moved by

monetary shocks.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 28 / 37

Critiques

Empirical Evaluation of the Model

The good performance (such as matching the

AR(1) dynamics of several macroeconomic

variables) may be due to the assumption of serially

correlated shocks, which is in question.

Morley (2010) describes that it is just like the “the

rabbit and the hat trick”: a rabbit was stuffed into

the hat and then a rabbit jumped out of the hat.

“What you put in is what you get out”!

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 29 / 37

Critiques

Empirical Evaluation of the Model

The good performance (such as matching the

AR(1) dynamics of several macroeconomic

variables) may be due to the assumption of serially

correlated shocks, which is in question.

Morley (2010) describes that it is just like the “the

rabbit and the hat trick”: a rabbit was stuffed into

the hat and then a rabbit jumped out of the hat.

“What you put in is what you get out”!

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 29 / 37

Critiques

Empirical Evaluation of the Model

The new DSGE model (i.e., Smets-Wouters

medium-scale model) are fit to much smaller set of

variables than that of the older macroeconometric

models.

The forecasting performance should be compared

with older macroeconometric models, not the

VAR/BVAR models.

Variables are linearly detrended. Fail to account for

possible unit root and cointegration.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 30 / 37

Critiques

Empirical Evaluation of the Model

The new DSGE model (i.e., Smets-Wouters

medium-scale model) are fit to much smaller set of

variables than that of the older macroeconometric

models.

The forecasting performance should be compared

with older macroeconometric models, not the

VAR/BVAR models.

Variables are linearly detrended. Fail to account for

possible unit root and cointegration.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 30 / 37

Critiques

Empirical Evaluation of the Model

The new DSGE model (i.e., Smets-Wouters

medium-scale model) are fit to much smaller set of

variables than that of the older macroeconometric

models.

The forecasting performance should be compared

with older macroeconometric models, not the

VAR/BVAR models.

Variables are linearly detrended. Fail to account for

possible unit root and cointegration.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 30 / 37

Critiques

Empirical Evaluation of the Model

No formal tests such as the Diebold and Mariano

(1995) test are conducted for out-of-sample

forecasts.

Only a small set of variables is chosen to be

observable variables (7 of 14). Guerron-Quintana

(2010) find that the empirical results are not robust

to the selection of observable variables.

Using real time data from the US, Edge and

Gurkaynak (2010) find that the Smets-Wouters

medium-scale DSGE model forecasts inflation and

GDP growth poorly.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 31 / 37

Critiques

Empirical Evaluation of the Model

No formal tests such as the Diebold and Mariano

(1995) test are conducted for out-of-sample

forecasts.

Only a small set of variables is chosen to be

observable variables (7 of 14). Guerron-Quintana

(2010) find that the empirical results are not robust

to the selection of observable variables.

Using real time data from the US, Edge and

Gurkaynak (2010) find that the Smets-Wouters

medium-scale DSGE model forecasts inflation and

GDP growth poorly.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 31 / 37

Critiques

Empirical Evaluation of the Model

No formal tests such as the Diebold and Mariano

(1995) test are conducted for out-of-sample

forecasts.

Only a small set of variables is chosen to be

observable variables (7 of 14). Guerron-Quintana

(2010) find that the empirical results are not robust

to the selection of observable variables.

Using real time data from the US, Edge and

Gurkaynak (2010) find that the Smets-Wouters

medium-scale DSGE model forecasts inflation and

GDP growth poorly.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 31 / 37

Part III

Perspectives on New DSGE Models

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 32 / 37

Perspectives

On The Perspectives of DSGE Modeling and Policy Making

I will discuss perspectives from which the central

bankers can have some ideas about what they

should bear in mind when deciding to construct

their own DSGE models.

◮ The new DSGE models are not yet useful for policy

analysis.◮ Inclusion of a more sophisticated financial intermediation

sector.◮ Better forecasting.◮ More sensible shocks.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 33 / 37

Perspectives

On The Perspectives of DSGE Modeling and Policy Making

First, as criticized above, the new DSGE models are not

yet useful for policy analysis.

So do not be frightened and confused by these

tedious and fancy mathematical equations.The current new DSGE model is full of dubiousstructures and features, which may misleadpolicymaking.

◮ Chari, Kehoe, and McGrattan (2009)◮ Faust (2008, 2009)

Keep in mind that the success in capturing business

cycle dynamics may be simply “made up” by an

implausible framework.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 34 / 37

Perspectives

On The Perspectives of DSGE Modeling and Policy Making

First, as criticized above, the new DSGE models are not

yet useful for policy analysis.

So do not be frightened and confused by these

tedious and fancy mathematical equations.The current new DSGE model is full of dubiousstructures and features, which may misleadpolicymaking.

◮ Chari, Kehoe, and McGrattan (2009)◮ Faust (2008, 2009)

Keep in mind that the success in capturing business

cycle dynamics may be simply “made up” by an

implausible framework.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 34 / 37

Perspectives

On The Perspectives of DSGE Modeling and Policy Making

First, as criticized above, the new DSGE models are not

yet useful for policy analysis.

So do not be frightened and confused by these

tedious and fancy mathematical equations.The current new DSGE model is full of dubiousstructures and features, which may misleadpolicymaking.

◮ Chari, Kehoe, and McGrattan (2009)◮ Faust (2008, 2009)

Keep in mind that the success in capturing business

cycle dynamics may be simply “made up” by an

implausible framework.Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 34 / 37

Perspectives

On The Perspectives of DSGE Modeling and Policy Making

Second, consider the inclusion of a more sophisticated

financial markets. For example,

Financial vulnerabilities and crisis

Collateral constraints and real estate markets

Choice of exchange rate regime

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 35 / 37

Perspectives

On The Perspectives of DSGE Modeling and Policy Making

Next, seek for better forecasting of macroeconomic

variables.

The DSGE model may be useful as a mechanism for

generating a prior which aids the estimation of a

BVAR: DSGE-VAR, see Del Negro et al. (2004).

The DSGE models need to forecast macroeconomic

variables out-of-sample well in level (rather than the

deviations from steady states) and in real time.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 36 / 37

Perspectives

On The Perspectives of DSGE Modeling and Policy Making

Next, seek for better forecasting of macroeconomic

variables.

The DSGE model may be useful as a mechanism for

generating a prior which aids the estimation of a

BVAR: DSGE-VAR, see Del Negro et al. (2004).

The DSGE models need to forecast macroeconomic

variables out-of-sample well in level (rather than the

deviations from steady states) and in real time.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 36 / 37

Perspectives

On The Perspectives of DSGE Modeling and Policy Making

Finally, all the structural shocks should be sensible.

Shocks should have a good interpretation.

It’s better to assume an i.i.d. shocks.

Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 37 / 37