drybulk shipping where predictions go to die september … · robert perri, cfa +1 212 776 4918...

TRANSCRIPT

AXIA Capital Markets LLC Page 1

BI Oil

Industry Report Shipping

Robert Perri, CFA

+1 212 776 4918

Drybulk Shipping–Where predictions go to die The drybulk shipping industry has continually surprised and confused its participants. Over

the years, trying to predict the drybulk industry has been like trying to guess how many jelly beans are in a jar. You look at it, study the parameters, work out the calculations on what the average density of a jellybean is, and then calculate the volume of the jar, only to basically throw that all away and guess a number at random. The drybulk market has so many factors that are unpredictable, such as geo-political decisions and the weather, that no matter how much work you do, it seems that some random event changes everything. The market is actually comprised of hundreds of supply/demand equations that the task of predicting vessel earnings is complicated at best. That being said, we have done our analysis and believe the market will remain weak for at least the next two years.

This year looks to be the worst year for the drybulk market. 2015 may go down in the record books as one of the worst years for the market in its history. The combination of excess vessel supply with slowing demand drove rates to historically low levels to start the year, and while rates have recovered somewhat since the first quarter of the year, vessel earnings remain well below cash flow break-even levels for many companies.

The good news is that growth in vessel supply is finally coming under control. Since 2007, the supply of drybulk vessels has grown by an average of 9.8% per year, and by 93% overall. Fleet growth has slowed to an average of 5.1% since 2012, which was roughly in line with demand growth. Going forward, continued scrapping should slow net fleet growth further, and we estimate net fleet growth of 2.3% in 2015, 2.4% in 2016 and 2.3% in 2017.

The bad news is that demand growth, which was expected to remain strong, has collapsed and the market remains massively oversupplied. While fleet growth has been stunning over the past eight years, demand growth has been similarly astounding. For an industry that historically witnessed demand growth below 2%, demand for drybulk vessels increased by a CAGR of 5% since 2007, while demand for major bulks grew by a CAGR of 6.7% during the same period as the Chinese engine drove demand for iron ore and coal. However, demand growth in 2015 is expected to slow to 1% this year, as demand for coal has declined significantly year over year and iron ore demand growth is expected to be 3.5%, as China’s growth has cooled. We believe growth will bounce back slightly in 2016 and 2017, and coupled with ton mile demand growth, we expect the demand for drybulk vessels to increase by roughly 3.5% per year for the next two years.

What does this mean? We believe that demand will outpace supply over the next two years. However given the oversupply of vessels in the marketplace, we expect rates to remain at depressed levels as the excess supply gets absorbed. Based on our model, either global demand for coal imports needs to improve by more than 10% per year for the next two years (meaning India’s demand needs to grow by more than 55% annually for the next two years to make up for China’s declines) or an additional 33 million dwt of vessels needs to be scrapped (on top of the 48.5 million tons we estimate will be scrapped over the next two years), or roughly 448 Panamaxes in total. We do believe the market will be slightly improved going forward, with pockets of strength but on average we believe rates will remain well below historical averages for at least the next two years.

So you would avoid the sector? Despite our pessimistic view, we believe we are working our way off the bottom and vessel values are at historically low levels, so it is the time to get smart on the sector and look for opportunities as they arise, although there is no need to rush at this stage in the cycle.

September 21, 2015

Baltic Dry Index

Baltic Capesize Index

Baltic Panamax Index

Baltic Supramax Index

Baltic Handysize Index

AXIA Capital Markets LLC, 645 Fifth Avenue, Suite 903, New York, NY 10022 Tel: +1 212 776 4918, Fax: +1 212 792 0256, Web: www.axiacm.com

Please refer to the last page for disclosures and analyst certification

0

500

1,000

1,500

Jan-15 Mar-15 May-15 Jul-15 Sep-15

0

400

800

1,200

1,600

2,000

2,400

2,800

Jan-15 Mar-15 May-15 Jul-15 Sep-15

0

200

400

600

800

1,000

1,200

1,400

Jan-15 Mar-15 May-15 Jul-15 Sep-15

0

200

400

600

800

1,000

Jan-15 Mar-15 May-15 Jul-15 Sep-15

0

200

400

600

Jan-15 Mar-15 May-15 Jul-15 Sep-15

AXIA Capital Markets LLC Page 2

Table of Contents

1. The drybulk shipping market outlook 3

2. Demand overview 4

3. Supply overview 5

4. Supply/demand overview 6

5. Demand outlook 8

6. Iron ore outlook 8

7. Coal outlook 11

8. Grain outlook 13

9. Minor bulk outlook 14

10. Drybulk vessel supply 16

11. Supply/demand dynamic 19

12. Capesize outlook 19

13. Kamsarmax/Panamax outlook 21

14. Ultramax/Supramax/Handymax outlook 23

15. Handysize outlook 25

16. Supply/demand scenarios 27

17. Conclusions 29

18. Disclosures 30

AXIA Capital Markets LLC Page 3

The drybulk shipping market

Shipping moves over 80% of the world’s commodities and is the cheapest and most cost efficient way to transport large volumes of major

commodities and finished products. It was once said that if it wasn’t for shipping half the world would starve and the other half would freeze. Drybulk

shipping is the shipment of minerals, industrial raw materials and various agricultural products in large vessels that can store large quantities of

materials in a single hold, with little risk of cargo damage, and is instrumental in connecting resource extraction points (Australia, Brazil, Africa, etc.)

with end users, such as steel mills, power plants, and agriculturists (China, India, Europe, etc.). Overall, the drybulk shipping market is the largest

sub-sector of the shipping industry, carrying more than 42% of the total tons of cargoes transported on vessels per year. The drybulk shipping

industry is driven by the demand for the underlying commodities transported in drybulk carriers and the geographical distribution of the seaborne

drybulk trade, which is influenced by trends in the global economy.

During the 1980s and 1990s, seaborne drybulk trade increased by roughly 2.5% per annum, however once China entered the World Trade

Organization, there was a tremendous spike in activity, and the growth in drybulk trade increased to an average annual growth rate of 5.5% for the

past ten years. As demand for drybulk goods spiked, rates that vessels earned for transporting these goods also spiked as there was not enough

supply of vessels to meet the increased demand from China.

From the period 1985 until 2002, the Baltic Dry Index (BDI) averaged 1,289 with a low of 554 in 1986 and a high of 2,352 in 1995, as demand was

weak and the industry fought through periods of slow global growth. Then, China entered the World Trade Organization in December 2001, and all

of the drybulk dynamics changed. In the period between 2003 and 2008, demand from China boosted the index to record highs as rates skyrocketed

for drybulk vessels across the board as the index increased from 2,000 to a peak of 11,793 in 2008 before it collapsed to 663 at the end of 2008 in

the wake of the financial crisis. During this time, it came to the point where everyplace you went in Athens, someone was telling you about their

investments in newbuilding drybulk vessels. From the shipowner to the taxi driver, everyone wanted to invest in newbuildings because there was

the belief that you could flip the vessel before delivery and make a significant profit much like the real estate bubble in the United States. At the

time, it was common for commercial banks to lend up to 90%+ of the purchase price of the vessel to owners, so little money was needed up front

and returns looked phenomenal. This lasted until the global financial collapse of 2008, and the market has suffered for its gluttony ever since as the

mountain of newbuilding vessels were delivered into the market causing a vast oversupply of vessels, despite strong demand. At its peak, the

newbuilding orderbook was at 78% of the total fleet on the water. Once the banking market started functioning again in early 2009, the market

seemed to bounce back and rates rebounded to healthy levels between 2009 and 2011. Eventually, the oversupply finally caught up with the market

and rates fell to historically low levels. Since 2012, the market has been faced with a severe oversupply of vessels, and has yet to recover despite

several false starts and the BDI hit its all-time low of 509 in early 2015.

Exhibit 1: Baltic Dry Index 1985-2015

Source: Baltic Exchange

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15Slow growth1985-2002Avg.: 1,289Min.: 554Max.: 2,352

China Enters the WTO2003-2008

Avg.: 4,714Min.: 663Max.: 11,793

Return to growth2009-2011Avg.: 2,310Min.: 772

Max.: 4,661Oversupplied

market2012-2015Avg.: 1,103Min.: 509

Max.: 2,337

Lehman Collapse!

AXIA Capital Markets LLC Page 4

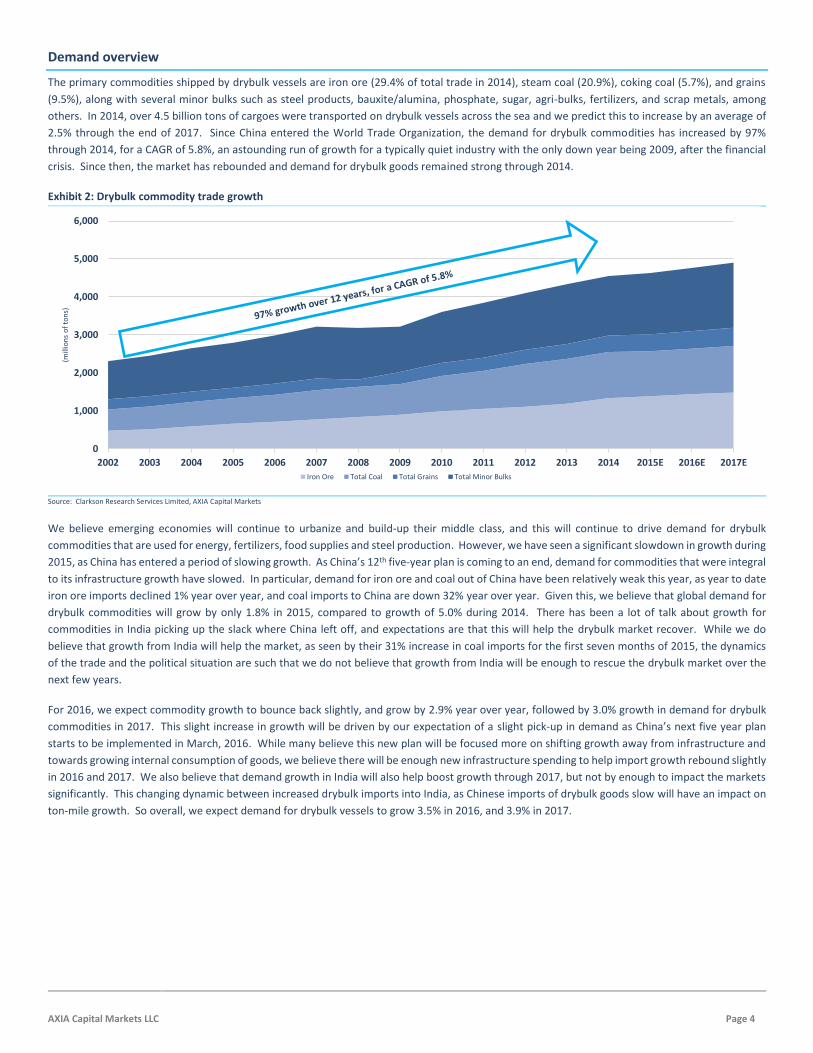

Demand overview

The primary commodities shipped by drybulk vessels are iron ore (29.4% of total trade in 2014), steam coal (20.9%), coking coal (5.7%), and grains

(9.5%), along with several minor bulks such as steel products, bauxite/alumina, phosphate, sugar, agri-bulks, fertilizers, and scrap metals, among

others. In 2014, over 4.5 billion tons of cargoes were transported on drybulk vessels across the sea and we predict this to increase by an average of

2.5% through the end of 2017. Since China entered the World Trade Organization, the demand for drybulk commodities has increased by 97%

through 2014, for a CAGR of 5.8%, an astounding run of growth for a typically quiet industry with the only down year being 2009, after the financial

crisis. Since then, the market has rebounded and demand for drybulk goods remained strong through 2014.

Exhibit 2: Drybulk commodity trade growth

Source: Clarkson Research Services Limited, AXIA Capital Markets

We believe emerging economies will continue to urbanize and build-up their middle class, and this will continue to drive demand for drybulk

commodities that are used for energy, fertilizers, food supplies and steel production. However, we have seen a significant slowdown in growth during

2015, as China has entered a period of slowing growth. As China’s 12th five-year plan is coming to an end, demand for commodities that were integral

to its infrastructure growth have slowed. In particular, demand for iron ore and coal out of China have been relatively weak this year, as year to date

iron ore imports declined 1% year over year, and coal imports to China are down 32% year over year. Given this, we believe that global demand for

drybulk commodities will grow by only 1.8% in 2015, compared to growth of 5.0% during 2014. There has been a lot of talk about growth for

commodities in India picking up the slack where China left off, and expectations are that this will help the drybulk market recover. While we do

believe that growth from India will help the market, as seen by their 31% increase in coal imports for the first seven months of 2015, the dynamics

of the trade and the political situation are such that we do not believe that growth from India will be enough to rescue the drybulk market over the

next few years.

For 2016, we expect commodity growth to bounce back slightly, and grow by 2.9% year over year, followed by 3.0% growth in demand for drybulk

commodities in 2017. This slight increase in growth will be driven by our expectation of a slight pick-up in demand as China’s next five year plan

starts to be implemented in March, 2016. While many believe this new plan will be focused more on shifting growth away from infrastructure and

towards growing internal consumption of goods, we believe there will be enough new infrastructure spending to help import growth rebound slightly

in 2016 and 2017. We also believe that demand growth in India will also help boost growth through 2017, but not by enough to impact the markets

significantly. This changing dynamic between increased drybulk imports into India, as Chinese imports of drybulk goods slow will have an impact on

ton-mile growth. So overall, we expect demand for drybulk vessels to grow 3.5% in 2016, and 3.9% in 2017.

0

1,000

2,000

3,000

4,000

5,000

6,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E 2016E 2017E

(mill

ion

s o

f to

ns)

Iron Ore Total Coal Total Grains Total Minor Bulks

AXIA Capital Markets LLC Page 5

Supply overview

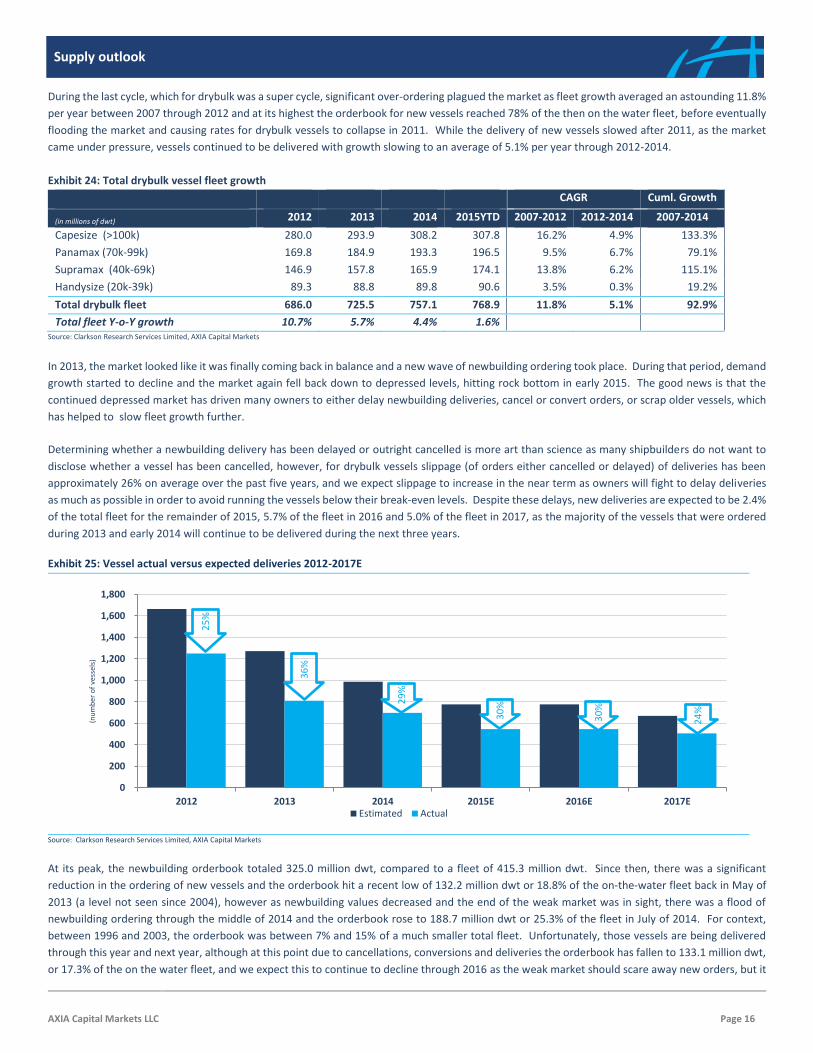

During the last cycle, which for drybulk was a super cycle, significant over-ordering plagued the market as fleet growth averaged an astounding 11.8%

per year between 2007 through 2012 and at its highest the orderbook for new vessels reached 78% of the then on the water fleet, before these

vessels were delivered and flooded the market, causing rates for drybulk vessels to collapse in 2011. While the delivery of new vessels slowed after

2011, as the market came under pressure, vessels continued to be delivered and fleet growth slowed to an average of 5.1% per year through 2012-

2014.

Exhibit 3: Drybulk vessel fleet development

Source: Clarkson Research Services Limited, AXIA Capital Markets

In 2013, the market appeared to be finally coming back in balance and then disaster struck as a new wave of newbuilding ordering took place from

owners looking to take advantage of an expected rebound, causing the orderbook to increase and a new wave of vessel were ordered with deliveries

scheduled for 2014 through 2017. During that period of renewed ordering, demand growth started to decline and the market again fell back to

depressed levels, and finally hit rock bottom in early 2015 as the BDI reached its all-time low in February. The good news is that the continued

depressed market has driven many owners to either delay newbuilding deliveries, cancel or convert orders, or scrap older vessels, which has helped

to slow fleet growth, and we expect this to continue for the next two years as the markets remain weak.

In 2014, net fleet growth was 4.4% in the drybulk sector, down from the 5.7% fleet growth experienced in 2013 as deliveries slowed in the second

half of the year. During 2014, most vessel classes grew by roughly 5% year over year, although growth in the Handysize sector was 1.1%, after

negative year over year growth in 2013. Year to date in 2015, we have seen net fleet growth of 1.6% as the acceleration of the scrapping of older

vessels, coupled with increasingly delayed newbuilding deliveries has hindered net fleet growth. For the full-year 2015, we project fleet growth of

2.2% as we project scrapping to slow and deliveries to accelerate slightly as we see rates improve slightly during the seasonally strong fourth quarter.

Year to date, the Capesize fleet has actually shrunk by 0.1% year over year, due to scrapping although we expect net fleet growth for Capes to be

approximately 0.2% year over year as there are many deliveries expected in the next few months. For the Panamax fleet, we have seen net fleet

growth of 1.7% year to date, and project 2.0% growth for the full-year 2015. The biggest growth has come from the Supramax/Ultramax fleet, which

has grown by 5.0% year over year, and we expect this accelerated growth to continue for the rest of the year, expanding the fleet by 6.7% for the

full-year 2015. Lastly, the Handysize fleet has grown by 0.8% year to date, and while there have been roughly the same amount of vessels scrapped

and new deliveries, the newer Handysize vessels are typically larger than the older vessels, which causes the net fleet growth on a tonnage basis. For

the full-year 2015, we are projecting net fleet growth of 1.2% for the Handysize fleet.

Going forward, we project fleet growth to pick up slightly in 2016 to 2.4% year over year growth, as scrapping slows slightly and the delayed vessels

from 2015 get delivered, while in 2017 we project 2.3% growth, as scrapping slows and the orderbook to finally lighten up enough to alleviate

significant concerns going forward. However, it is important to understand that drybulk vessels are not as complicated to build as tankers,

containerships or LNG carriers, so the orderbook could quickly get out of hand again if the market improves and people get ahead of themselves

again.

0

100

200

300

400

500

600

700

800

900

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E 2016E 2017E

(mill

ion

s o

f d

wt)

Handysize Supramax/Handmax Panamax Capesize

AXIA Capital Markets LLC Page 6

Demand/supply dynamic

Based on our estimates of how demand for drybulk trade will develop going forward coupled with our projection of vessel supply, it is important to

translate this into what it means for drybulk shipping. We have developed a standard methodology of analyzing this which is premised on the

following (and is consistent across all supply/demand scenarios and commodities we analyze in this report):

We can estimate where the commodities are produced in each originating country and where they are transported to. We understand how many

days a round trip takes in order to load a cargo, deliver and discharge it at the destination port, and have the vessel return to the originating port.

The combination of these two factors allows us to calculate the demand for ton miles on any given year (i.e. the carrying capacity required to get

these commodities from the origination to the destination port and the vessel back without carrying any cargo)

We make assumptions on what type(s) of vessel(s) typically carry these commodities and compare that to the number of available vessels in that

asset class (given that what is called a 'Cape' can vary in its size from 110,000dwt for mini-capes to 400,000dwt for VLOCs, we pick the most 'standard'

size for each asset class - in the case of Capes 170,000dwt - and convert the entire fleet into 'typical size equivalents').

Below, and in more detail at the end of this report we put it all together to draw some conclusions on how over- or under-supplied the market is

today and by the end of 2017. Obviously this methodology is, by necessity, more simplistic than how the market actually functions as it cannot/does

not account for a number of factors, that can move the market, including:

Changes in the trade routes in any point in time

Changes in duration of trips as a result of vessels speeding up, slowing down, congestion, weather, just to name a few

Days that a vessel may not be available as a result of drydocking, repairs, piracy, acts of god (although a safe assumption is that 5% of the fleet is unavailable at any given time, so 100% utilization translates to 95% of the total fleet)

Vessels that are taken off the trade and operate for storage, coastal trades, etc.

The fact that vessels do not simply go from port A to port B with a cargo (or laden) and straight back empty (or ballast), but can either triangulate (especially common in the Handysize trade) or carry a cargo on the way back, known as a backhaul trade

When looking at the fleet and orderbook in this way, we can see that while the oversupply of vessels is improving over the next two years, it remains

an issue. The most important thing to keep in mind is the dynamics between the size classes, as nothing is clear cut. When Capesize vessels can’t

find typical employment, the can move into the coal trade or the grain trade and steal cargoes from Panamax vessels on occasion, and vice versa if

Capesize rates improve to a level twice that of Panamax vessels, as it starts to make sense to split the cargoes on two Panamaxes instead of one

Capesize vessel.

In the same sense, when there is an oversupply of Supramax vessels, they tend to beat out Handysize vessels for business, and they also can compete

with Panamaxes on some trades, and this flexibility is why their rates have held up so well over the past several years. However, they currently have

the largest orderbook of newbuilding vessels being delivered in the next two years, causing the oversupply to get worse which should have a negative

impact on freight rates going forward. There is also a large amount of Handysize vessels that are employed in the coastal trades, especially in China,

that do not show up in this data but can take up to 10% or more of the Handysize fleet.

Exhibit 4: Estimated weighted average scenario in 2015 (in m. dwt) Exhibit 5: Estimated weighted average scenario in 2017 (in m. dwt)

Source: AXIA Capital Markets Source: AXIA Capital Markets

173.2

31.7

53.3

55.1

23.0

40.0

27.2

112.6

80.4

81.868.9

9.510.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cape Panamax Supramax Handy

(per

cen

tage

of

trad

e)

Iron ore Coal Grain Minor bulk Excess

186.7

34.0

55.3

57.1

23.7

41.4

29.2

116.1

87.8

73.6 69.9

23.1 3.6

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cape Panamax Supramax Handy

(per

cen

tage

of

trad

e)

Iron ore Coal Grain Minor bulk Excess

AXIA Capital Markets LLC Page 7

When looking at these figures, it is always important to note that approximately 7% to 10% of the fleet is unavailable due to several factors such as

port delays, drydocking and repairs, or vessels being utilized in coastal trades, which are not counted in our supply/demand forecast. However, when

looking at the current fleet, we can see that the oversupply of vessels amounts to 170.3 million tons, or 22.2% of the fleet, and even backing out a

generous 10% of the fleet that may be inactive or unavailable for international trade, that still leaves 12.2% of the fleet as excess capacity, or in other

words, you can basically scrap the entire Handysize fleet and the market would still not be fully balanced.

Due to this severe imbalance, we do not expect the market to fully recover for some time; however there will be pockets of opportunity as we are

currently at the bottom of the cycle and the market should start to heal going forward. We believe that in the second half of 2016, we will start to

see the effects of China’s next 5 year plan begin to take effect and demand for drybulk commodities should ramp up slightly. In particular, we expect

iron ore demand to improve in the second half of 2016, which should help Capesize vessels during the fourth quarter of 2016, although we believe

the market will continue to be challenging in the first half of the year. That being said, we believe the oversupply in Capesize vessels will also hinder

any sustained rally and rates will fall back to depressed levels during the first half of 2017.

In addition, we expect the Panamax sector to remain challenged over the next two years as coal demand will remain sluggish and our expectations

of a strong grain season in 2016 will not be enough to create a sustainable rally. In order for the excess supply of Panamax vessels to be absorbed,

we would need demand for grain exports to increase by over 10% and coal exports to increase by over 7% in the next two years in order to see a

booming market again, or another 33 million tons would need to be scrapped on top of our projected 48.5 million tons. We also believe by the end

of next year that Supramax rates will come under additional pressure as the vessel deliveries accelerate and we project freight rates will again fall

below Panamax vessels. We also believe that the excess supply of Supramaxes will continue to put pressure on Handysize rates, so while we do

believe we are at the start of a turn-around in the drybulk sector and rates should start to improve slightly going forward, we do not see a light at

the end of the tunnel yet and fear it may be another two or three years before the market gets back on its feet, depending on how scrapping and

new ordering develops over the next year.

Exhibit 6: Drybulk spot rate development (in U.S dollars per day)

Historical rates and AXIA estimates 2012 2013 2014A 2015E 2016E 2017E 5-yr avg.

Capesize 24,385 28,018 13,800 8,355 12,625 13,250 16,408

Panamax 7,684 9,471 7,718 6,700 7,800 8,500 12,460

Supramax 9,453 10,275 9,818 7,675 8,250 8,500 13,029

Handysize 7,626 8,179 7,681 6,225 6,875 7,200 9,809

Quarterly estimates 2Q15A 3Q15E 4Q15E 1Q16E 2Q16E 3Q16E 4Q16E

Capesize 6,358 10,500 13,000 8,000 9,500 13,000 20,000

FFAs 11,530 16,403 8,520 9,300 13,030 16,310

Panamax 6,845 8,000 9,000 6,500 7,750 8,000 9,000

FFAs 7,529 8,035 6,808 7,608 7,433 8,167

Supramax 6,137 9,000 8,500 7,000 8,500 9,000 8,500

FFAs 8,521 8,470 7,067 7,604 7,358 8,623

Handysize 6,292 7,000 8,000 7,000 6,000 7,000 7,500

FFAs 6,469 6,496 5,638 6,350 5,975 6,589 1 As of September 18, 2015

Source: Baltic Exchange, AXIA Capital Markets

While we are slightly more optimistic than the forward freight agreement (FFA) market, as our view on China is slightly different than current

sentiment, we still believe we will be in a challenging market for at least the next two years, and our annual average rate estimates for 2016 remain

well below historical averages but on the aggregate rates should be better than 2015.

In terms of what this means for asset values, we believe the continued pressure from Chinese shipyards to generate new orders by keeping

newbuilding prices competitive, coupled with the decline in scrap rates and the average age of a scrapped vessel, will continue to keep vessel values

for on-the water ships from increasing significantly even if the market was strong. Therefore, while we believe asset values have bottomed, we do

not expect a significant increase in values for at least the next two years or more until owners will start to see the light at the end of the tunnel and

drive up values slightly.

AXIA Capital Markets LLC Page 8

Demand Outlook

Over the past 12 years, demand for drybulk commodities has grown at an accelerated rate, and 2009 was the only year we experienced a decline in

growth year over year. That being said, the recent slowdown in China has put pressure on the demand for drybulk commodities and while we expect

that 2016 will be better than 2015, we continue to expect a significant slowdown in demand compared to what we have witnessed during the

previous 12 years and do not expect demand for drybulk carriers to exceed 3.5% year over year growth through at least the end of 2017.

Exhibit 7: Drybulk commodity trade (in m. tons)

CAGR Cuml. Growth

Major Bulks 2012A 2013A 2014A 2015E 2016E 2017E 2007-2012 2012-2014 2007-2014

Iron ore 1,110 1,189 1,337 1,384 1,439 1,483 7.4% 9.8% 72.1%

Total coal 1,123 1,179 1,213 1,187 1,199 1,226 7.9% 3.9% 57.9%

Steam coal 889 915 950 931 941 960 9.2% 3.4% 65.7%

Coking coal 234 264 263 255 258 266 3.8% 5.9% 34.9%

Grains 374 387 430 447 461 479 4.1% 7.2% 40.5%

Total major bulks 2,607 2,758 2,980 3,018 3,099 3,187 7.1% 6.9% 61.0%

Total minor bulks 1,493 1,575 1,569 1,611 1,663 1,716 2.0% 1.8% 14.8%

Total trade 4,100 4,330 4,549 4,629 4,762 4,904 5.0% 5.3% 41.4%

Year over year growth 6.7% 5.6% 5.0% 1.8% 2.9% 3.0%

Source: Clarkson Research Services Limited, AXIA Capital Markets

When looking at seaborne demand for commodities, there are three commodities that

are considered the major bulks. As shown in Exhibit 8, Iron ore comprises 29% of the

total drybulk trade, coal 27%, and grains 9% and these major bulks comprise 65% of

the commodities transported by sea. Given this, we believe it is important to look at

each of these commodities individually as each of their demand drivers are different.

As emerging economies continue to urbanize and build-up their middle class, we

expect the demand for drybulk commodities that are used for energy, fertilizers, food

supplies and steel production to continue to grow at an accelerated rate. While we

don’t expect growth to get back to the average growth rates of 6.8% we experienced

from 2003 to 2007, we do expect demand growth to continue to increase through

2017. For drybulk shipping, our estimates are for ton mile growth to remain weak

through the remainder of 2015, growing by only 2.1% year over year, which translates

into a utilization rate of 79%, and to improve over the next two years, as ton mile

demand growth increases faster than supply growth, although this demand imbalance is not large enough to make up for the years of excess growth

in the supply of vessels unless either scrapping continues at an accelerated rate, or demand increases faster than expected over the next two years.

Over the next two years, we believe demand for drybulk commodities will increase by 2.9% and 3.0% in 2016, and 2017, respectively.

Iron ore outlook

Iron ore is the primary ingredient for the production of steel, along with limestone & coking coal and is the largest single commodity shipped on

drybulk vessels. The main producers of iron ore are Australia (53.6% of global iron ore exports in 2014) and Brazil (25.8%), while the main importers

are China, the European Union, Japan and South Korea. Iron ore is processed into pig iron, which in turn is used in steel production. Virtually all of

the world’s iron ore goes into making steel, which is primarily used for construction, machine production, shipbuilding, and car manufacturing, along

with many other uses. Given the primary uses of iron ore, industrial production, urbanization and construction growth are the drivers for demand.

We believe that as emerging economies continue to urbanize and build up their infrastructure, we will continue to see strong demand for iron ore

transported by sea as it is vital to the steel industry.

While countries such as Japan and South Korea have continually been stable importers of iron ore, it is the growth from the emerging markets,

particularly China, that has driven demand growth for iron ore over the past ten years, and we expect this trend to continue going forward. The vast

majority of iron ore is transported on Capesize vessels, although some cargoes are carried on Panamax vessels.

Exhibit 8: Breakdown of drybulk commodity cargoes

Source: Clarkson Research Services Limited

Iron ore29%

Coal27%

Grains9%

Minor bulks35%

AXIA Capital Markets LLC Page 9

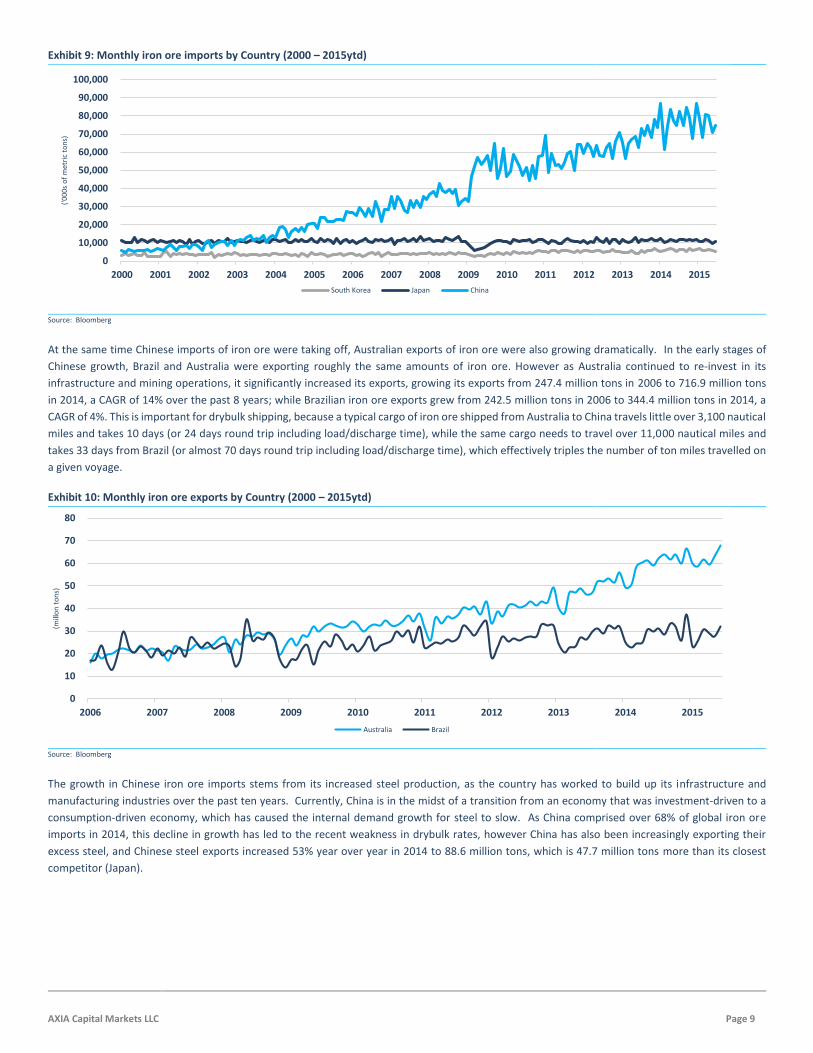

Exhibit 9: Monthly iron ore imports by Country (2000 – 2015ytd)

Source: Bloomberg

At the same time Chinese imports of iron ore were taking off, Australian exports of iron ore were also growing dramatically. In the early stages of

Chinese growth, Brazil and Australia were exporting roughly the same amounts of iron ore. However as Australia continued to re-invest in its

infrastructure and mining operations, it significantly increased its exports, growing its exports from 247.4 million tons in 2006 to 716.9 million tons

in 2014, a CAGR of 14% over the past 8 years; while Brazilian iron ore exports grew from 242.5 million tons in 2006 to 344.4 million tons in 2014, a

CAGR of 4%. This is important for drybulk shipping, because a typical cargo of iron ore shipped from Australia to China travels little over 3,100 nautical

miles and takes 10 days (or 24 days round trip including load/discharge time), while the same cargo needs to travel over 11,000 nautical miles and

takes 33 days from Brazil (or almost 70 days round trip including load/discharge time), which effectively triples the number of ton miles travelled on

a given voyage.

Exhibit 10: Monthly iron ore exports by Country (2000 – 2015ytd)

Source: Bloomberg

The growth in Chinese iron ore imports stems from its increased steel production, as the country has worked to build up its infrastructure and

manufacturing industries over the past ten years. Currently, China is in the midst of a transition from an economy that was investment-driven to a

consumption-driven economy, which has caused the internal demand growth for steel to slow. As China comprised over 68% of global iron ore

imports in 2014, this decline in growth has led to the recent weakness in drybulk rates, however China has also been increasingly exporting their

excess steel, and Chinese steel exports increased 53% year over year in 2014 to 88.6 million tons, which is 47.7 million tons more than its closest

competitor (Japan).

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

('00

0s o

f m

etri

c to

ns)

South Korea Japan China

0

10

20

30

40

50

60

70

80

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

(mill

on

to

ns)

Australia Brazil

AXIA Capital Markets LLC Page 10

Exhibit 11: Monthly Chinese steel production Exhibit 12: Monthly Chinese steel product exports

Source: World Steel Association Source: Customs General Administration of the People’s Republic of China

China has always used a mix of imported iron ore and its own supplies, however iron ore prices have fallen from a high of $158 per ton back in 2013

to below $60 today, which has caused many Chinese mines to shut down as their cost of extraction is much higher, and the ore quality is lower, than

imports from Australia and Brazil. Given this, we expect imports of iron ore into China to continue to grow, despite the declining growth in its steel

manufacturing industry.

Exhibit 13: Chinese iron ore output year over year growth

Source: Bloomberg

In 2014, total global iron ore exports reached 1,337.3 million tons, and Australia was the largest exporter of iron ore by far, with exports of 716.9

million tons or 53.6% of the total exports, followed by Brazil at 344.4 million tons for 2014, or 25.8% of global exports, and these two countries

combined for over 79.4% of global iron ore exports in 2014.

Year to date, in 2015 Australian iron ore exports have increased 9.1% year over year to 370.1 million tons, and Brazilian exports increased by 7.1%

year over year to 167.8 million tons despite concerns about slowing demand growth for steel and steel products. This is partly due to the lower cost

of producing iron ore in these countries, and their quest to improve their market share, despite the weak price at the expense of the Chinese, and

other higher-cost providers or iron ore, and we expect this to continue for the next year at least.

Over the past five years, the CAGR of global iron ore imports has been 6.9%, and while we do not expect growth to continue at that pace, we do

expect an average growth of 3.5% over the next three years. We believe that as Chinese mines decrease production, the Chinese will source a higher

percentage of their additional iron ore needs from Brazil rather than Australia as we enter the second half of 2015 and into 2016 which will boost

ton miles and increase demand for seaborne vessels going forward. It is also important to note that historically, Brazilian iron ore exports to China

increase by roughly 20% compared to the first half of the year, while exports from Australia increase by roughly 10% in the second half of the year,

which is why the fourth quarter is typically the best for Capesize vessels.

For each commodity, we present two cases: the first assumes that the most 'typical' vessel carrying that commodity carries 100% of that commodity

and the second assumes a more realistic mix of vessels used in every trade.

40

45

50

55

60

65

70

75

2010 2011 2012 2013 2014 2015

(mill

ion

s o

f to

ns)

0

2

4

6

8

10

12

2010 2011 2012 2013 2014 2015

(mill

ion

s o

f to

ns)

(20.0%)

(15.0%)

(10.0%)

(5.0%)

0.0%

5.0%

10.0%

15.0%

Mar-13 May-13 Jul-13 Sep-13 Nov-13 Mar-14 May-14 Jul-14 Sep-14 Nov-14 Mar-15 May-15 Jul-15

AXIA Capital Markets LLC Page 11

Iron ore is predominantly transported on Capesize vessels, and roughly 85% of this commodity is transported by Capes, while the remaining 15% is

transported on Panamax vessels (with small quantities also being transported by smaller vessels sporadically). Exhibit 14 illustrates the iron ore

supply/demand assuming only Capesize vessels were used for this trade, and Exhibit 15 illustrates the same assuming the 85/15 mix referred to

above between Capesize and Panamax vessels.

Exhibit 14: Iron ore vessel supply/demand in Capesize equivalents Exhibit 15: Iron ore vessel supply/demand in est. mixed equivalents

Source: AXIA Capital Markets Source: AXIA Capital Markets

What these graphs above show is that if iron ore is to be exclusively transported in Capesize vessels, it would occupy only 63% and 66% of the

available tonnage in 2015 and 2017, respectively. This means that the remaining fleet would need to be occupied by other commodities or become

redundant, which would create excess supply and pressure rates and values to decline.

In the more realistic case, in Exhibit 15, we see that roughly 54% of the Capes are needed for the iron ore trade, and 16% of the Panamax fleet,

leaving the remainder of the vessels to be employed on other trade routes.

Coal outlook

The seaborne coal trade is comprised of two different types of coal; steam coal (which is used for electricity generation and industrial uses), and

coking coal (which is a key ingredient for steelmaking). Coal is the second-largest commodity shipped by sea, and in 2014 a total of 1,212.8 million

tons were transported by ships. The biggest importers of coal are China, India, Japan and Western Europe while the biggest exporters of steam coal

are Australia, Indonesia, the United States and Canada and the biggest exporters of coking coal are Australia, Russia, Columbia, South Africa, and the

United States.

Over the past twelve years, there has been a major change in the trade patterns of coal, as China went from being one of the largest exporters of

coal to being the largest importer. This was primarily due to the increased needs of coal for power generation; however over the past two years, its

demand for coal has declined as the country has been trying to clean up its pollution problems and is moving to increase its hydro power generation,

along with other cleaner energy alternatives. While there has been a decline in coal imports to China, there has been a significant increase in imports

into India, as the country continues to build out its own infrastructure and its power generation needs increase. The other major importers, such as

Western Europe and Japan continue to be dependent on coal imports, however their usage has been stable. The transportation of coal by sea used

to be dominated by Panamax vessels, but today, 40% is transported on Capes, 40% on Panamaxes and 20% on Supramaxes.

In 2014, total global coal exports by sea reached 1,212.8 million tons up 2.8% year over year, with Australia (32% of global exports) being the largest

exporter, with exports of 387.3 million tons, then Indonesia (30% of global exports) with 356.3 million tons, and followed by the Columbia and the

United States with around 7.0% of global exports each. While Australia has an almost equal mix of thermal and coking coal exports, other countries

such as Indonesia and Columbia primarily export thermal coal while the United States exports more coking coal. In 2014, Chinese imports of coal fell

15% year over year to 228.0 million tons, down from 267.5 million tons in 2013, while India’s imports of coal rose 17% to 194.1 million tons from

166.5 million tons in 2013 and Japan’s imports fell 1.7% year over year, to 115.3 million tons in from 117.3 million tons in 2013.

During the first seven months of 2015, Australian coal exports increased 2% year over year to 221.8 million tons, while Indonesian exports declined

by roughly 18.2% to 211.0 million tons. On the demand side for the first seven months of 2015, Chinese imports have declined 35% year over year

to 92.4 million tons, down from 141.5 million tons as an increased focus on cleaner energy sources in China has taken hold as the country fights its

pollution issues. Offsetting this steep decline from China was India where imports increased 25% to 127.1 million tons from 102.1 million tons in the

1,081 1,158

1,714 1,754

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2015E 2017E

(nu

mb

er o

f ve

ssel

s)

Demand Supply

919 985

1,714 1,754

399 428

2,503 2,594

0

500

1,000

1,500

2,000

2,500

3,000

2015E 2017E

(nu

mb

er o

f ve

ssel

s)

Cape Demand Cape Supply Panamax Demand Panamax Supply

AXIA Capital Markets LLC Page 12

first seven months of 2014. It is important to note that Indonesia accounts for over 70% of India’s coal imports, which typically takes 24 days round

trip, and 13.5% from Australia, which is a 40 day round trip voyage. While Australia accounts for 42.7% of Chinese imports (32 day round trip voyage),

and Indonesia accounts for 26% of its total imports (16 day round trip). The bad news is that the combination of declining coal imports from China,

coupled with increasing imports (with shorter distances travelled) from India has caused freight rates to be under pressure. The good news is Australia

has been fighting hard to maintain its market share and has more than doubled its exports into India in the past year, which increases ton mile

demand for drybulk vessels.

We expect India’s growing demand for coal to partly offset China’s recent declines over the next few years as India’s energy generation remains

predominantly coal-fired. We also believe that as Australia continues to win market share from Indonesia as the Indonesian Government continues

to cause issues for the country’s exporters, that the incremental coal needed for India’s growth will be sourced from further locations, which should

help offset the slowdown in growth in the coal trade over the near term.

Exhibit 16: Monthly coal imports for China, India and Japan

Source: Bloomberg

Coal is predominantly transported on Panamax vessels, although recently it is evenly split with 40% on Panamaxes and 40% on Capesize vessels with

the remaining 20% being carried on Supramaxes. Exhibit 17 illustrates the iron ore supply/demand assuming only Panamax vessels were used for

this trade, and Exhibit 18 illustrates the same assuming the 40/40/20 mix referred to above between Panamax, Capesize and Supramax vessels.

Exhibit 17: Coal vessel supply/demand in Panamax equivilents Exhibit 18: Coal vessel supply/demand in est. mixed equivilents

Source: AXIA Capital Markets Source: AXIA Capital Markets

If Coal was purely transported on Panamax vessels, it would occupy 69% and 67% of the available tonnage in 2015 and 2017, respectively. While this

looks better than the supply/demand for Capesize vessels on iron ore, it remains a large amount of oversupply in the market, especially when we

look at the more realistic case.

0

5

10

15

20

25

30

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15

(mill

ion

s o

f to

ns)

India China Japan

1,739 1,756

2,503 2,594

0

500

1,000

1,500

2,000

2,500

3,000

2015E 2017E

(nu

mb

er o

f ve

ssel

s)

Demand Supply

283 292

1,714 1,754

696 718

2,503 2,594

426 440

3,207

3,540

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2015E 2017E

(nu

mb

er o

f ve

ssel

s)

Cape Demand Cape Supply Panamax Demand

Panamax Supply Supramax demand Supramax supply

AXIA Capital Markets LLC Page 13

In the more realistic case, in Exhibit 18, we see that roughly 28% of the Panamaxes are needed for the coal trade, along with 16% of the Capesize

vessels fleet and 13% of the Capesize fleet, leaving the remainder of the vessels to be employed on other trade routes.

Grain outlook

The seaborne trade of grains consists primarily of wheat, coarse grains (such as corn, barley, oats, and rye) and soya bean/meal. The largest of the

three grains is soya bean/meal. The primary exporters of grains are the United States, Brazil and Argentina, while the primary importers are China,

Europe and Far Eastern Asia. The grain trade is very seasonal, as the Southern hemisphere exporters are the most active in the second quarter of

the year, while the Northern hemisphere exporters are most active in the fourth quarter of the year. The grain season is also very sensitive to the

weather, and in years of too much or too little rainfall, the global grain trade is affected. Currently, we are experiencing an El Nino weather

phenomenon, which is characterized by warmer waters in the Pacific Ocean, causing draughts in parts of Asia, and excess rains in North America.

Historically, in times of El Nino, soya bean crop yields are 2%-4% higher, while wheat and corn crop yields are 1%-5% lower than in a typical season

and this year we have seen strong soya bean crops out of South America to start the season.

In 2014, total global grain exports by sea increased by 10.3% year over year to 430 million tons, as both North and South American grain seasons

were exceptionally strong and to date through the first half of 2015, the South American grain exports are stronger than last year, as Brazilian exports

are forecasted to increase by 16% to 26.1 million tons in 2015, and Argentinian exports are up 46% year over year to 14.3 million tons in the first six

months of the year compared to 9.7 million tons last year. However, the strong growth in the South American grain trade has been slightly offset by

the weakness out of Canada this year, where exports are expected to decline by 13.3% year over year to 24.8 million tons in 2015, and sluggish

growth out of the United States as seaborne imports are expected to grow by only 1% year over year to 80.7 million tons.

Going forward, we continue to expect the growth in seaborne grain exports to be consistent with its five-year CAGR of 5.4%, as the continued growth

in the population coupled with the growth in the middle class in emerging economies will continue to need food stocks to feed their population.

When thinking about the grain trade, it is important to note that for every kilo of poultry meet produced, 2-3kg of grain is needed to feed the animal

during its lifetime, while for pork the amount of grain increases to 4-5.5kg per kilo, and for beef you need 10kg of grain per kilo of meat, so we believe

as the growth in the middle class of China, the Middle East, Asia and Latin America grows, there will be increased demand for livestock, which will

continue to drive the grain trade going forward.

Exhibit 19: Global seaborne grain exports by category and year over year growth

Source: Clarkson Research Services Limited, AXIA Capital Markets

Grain is predominantly transported on Panamax vessels, and roughly 55% of this commodity is transported by Panamaxes, with the remaining 45%

being transported on Supramaxes, although Capes have been known to enter this market on occasion. Exhibit 20 illustrates the grain supply/demand

assuming only Panamax vessels were used for this trade, and Exhibit 21 illustrates the same assuming the 55/45 mix referred to above between

Panamax, Capesize and Supramax vessels.

343.0 346.0 374.0 390.0

430.0 446.8 461.4

479.3

0%

2%

4%

6%

8%

10%

12%

0

100

200

300

400

500

600

2010A 2011A 2012A 2013A 2014A 2015E 2016E 2017E

(mill

ion

s o

f to

ns)

Wheats/Coarse grains Soyabean Y-o-y growth

AXIA Capital Markets LLC Page 14

Exhibit 20: Grain vessel Supply/Demand in Panamax equivilents Exhibit 21: Grain vessel Supply/Demand in est. mixed equivilents

Source: AXIA Capital Markets Source: AXIA Capital Markets

If grains were purely transported on Panamax vessels, it would occupy only 37% of the available tonnage in 2015 and 2017. While grains are

considered a major bulk, the amount transported by sea is more than half the size of coal and is very seasonal, so the size and seasonality create

significant swings in how this commodity affects the drybulk trade.

In the more realistic case, in Exhibit 21, we see that roughly 20% of the Panamaxes are needed for the grain trade, along with 16% of the Supramax

fleet, leaving many vessels underutilized.

Minor bulks (including bauxite and phosphate) outlook

There are several other bulks goods such as phosphate rock, fertilizers,

bauxite, steel products, forest products, nickel ore, sugar, salt and

many others that comprise the minor bulk category. In aggregate,

these bulks comprised 1,434.0 million tons in 2014, up 2% year over

year and has a CAGR of 3.8% over the past five years. The primary

cause of the decline in growth in 2014 was due to the Indonesian ban

on exports of Bauxite and Nickel ore. Bauxite is an aluminum ore that

is the main source material for aluminum in the world. In 2013, China

imported 68% of its Bauxite needs from Indonesia, and due to the ban,

this number fell to 24% in 2014 (which even that was primarily cargoes

loaded in Indonesia before the ban was in place as China stockpiled as

much as they could before the ban took effect) while global bauxite

exports declined to 105 million tons from 139 million tons in 2013.

However, at this stage most of those stores have been depleted, and

China has invested heavily in Africa to ensure it can secure a new

source of Bauxite once its mines there are operational.

These bulk goods are typically traded in geared vessels such as

Supramax and Handysize vessels. We expect growth in this category

to accelerate slightly in 2015 to 3% and continue to grow at similar levels for the next few years. This growth will be driven by the increased exports

of steel out of China, along with growth in several other of the subsectors such as forest products and fertilizers.

Minor bulks are predominantly traded on Supramax and Handysize vessels, but although some cargoes like bauxite and phosphate rock have been

known to trade on Panamaxes and Capesize vessels.

917 947

2,503 2,594

0

500

1,000

1,500

2,000

2,500

3,000

2015E 2017E

(nu

mb

er o

f ve

ssel

s)

Demand Supply

504 541

2,503 2,594

506 543

3,207

3,540

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2015E 2017E

(nu

mb

er o

f ve

ssel

s)

Panamax demand Panamax supply Supramax demand Supramax supply

Exhibit 22: Breakdown of minor bulks

Source: Clarkson Research Services Limited

AXIA Capital Markets LLC Page 15

Exhibit 23: Minor bulk vessel Supply/Demand in Supramax/Handysize equivilents

Source: AXIA Capital Markets

For minor bulks it is a clearer picture as this trade is predominantly all Supramaxes and Handysize vessels, although it is difficult to distinguish the

percentages between the two classes, and given that they are both geared vessels, we combine them in this category to see the supply. The minor

bulk trade occupies roughly 78% and 77% of the available tonnage in 2015 and 2017, respectively. There is also a percentage of Handysize vessels

that occupy the costal trades, transporting cargoes between different ports in the same countries, such as China or India, where it is cheaper than

transportation by land, possibly 10% of the Handysize fleet or more, although data for those types of trades is unreliable.

5,036 5,196

6,424 6,708

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2015E 2017E

(nu

mb

er o

f ve

ssel

s)

Demand Supply

AXIA Capital Markets LLC Page 16

Supply outlook

During the last cycle, which for drybulk was a super cycle, significant over-ordering plagued the market as fleet growth averaged an astounding 11.8%

per year between 2007 through 2012 and at its highest the orderbook for new vessels reached 78% of the then on the water fleet, before eventually

flooding the market and causing rates for drybulk vessels to collapse in 2011. While the delivery of new vessels slowed after 2011, as the market

came under pressure, vessels continued to be delivered with growth slowing to an average of 5.1% per year through 2012-2014.

Exhibit 24: Total drybulk vessel fleet growth

CAGR Cuml. Growth

(in millions of dwt) 2012 2013 2014 2015YTD 2007-2012 2012-2014 2007-2014

Capesize (>100k) 280.0 293.9 308.2 307.8 16.2% 4.9% 133.3%

Panamax (70k-99k) 169.8 184.9 193.3 196.5 9.5% 6.7% 79.1%

Supramax (40k-69k) 146.9 157.8 165.9 174.1 13.8% 6.2% 115.1%

Handysize (20k-39k) 89.3 88.8 89.8 90.6 3.5% 0.3% 19.2%

Total drybulk fleet 686.0 725.5 757.1 768.9 11.8% 5.1% 92.9%

Total fleet Y-o-Y growth 10.7% 5.7% 4.4% 1.6% Source: Clarkson Research Services Limited, AXIA Capital Markets

In 2013, the market looked like it was finally coming back in balance and a new wave of newbuilding ordering took place. During that period, demand

growth started to decline and the market again fell back down to depressed levels, hitting rock bottom in early 2015. The good news is that the

continued depressed market has driven many owners to either delay newbuilding deliveries, cancel or convert orders, or scrap older vessels, which

has helped to slow fleet growth further.

Determining whether a newbuilding delivery has been delayed or outright cancelled is more art than science as many shipbuilders do not want to

disclose whether a vessel has been cancelled, however, for drybulk vessels slippage (of orders either cancelled or delayed) of deliveries has been

approximately 26% on average over the past five years, and we expect slippage to increase in the near term as owners will fight to delay deliveries

as much as possible in order to avoid running the vessels below their break-even levels. Despite these delays, new deliveries are expected to be 2.4%

of the total fleet for the remainder of 2015, 5.7% of the fleet in 2016 and 5.0% of the fleet in 2017, as the majority of the vessels that were ordered

during 2013 and early 2014 will continue to be delivered during the next three years.

Exhibit 25: Vessel actual versus expected deliveries 2012-2017E

Source: Clarkson Research Services Limited, AXIA Capital Markets

At its peak, the newbuilding orderbook totaled 325.0 million dwt, compared to a fleet of 415.3 million dwt. Since then, there was a significant

reduction in the ordering of new vessels and the orderbook hit a recent low of 132.2 million dwt or 18.8% of the on-the-water fleet back in May of

2013 (a level not seen since 2004), however as newbuilding values decreased and the end of the weak market was in sight, there was a flood of

newbuilding ordering through the middle of 2014 and the orderbook rose to 188.7 million dwt or 25.3% of the fleet in July of 2014. For context,

between 1996 and 2003, the orderbook was between 7% and 15% of a much smaller total fleet. Unfortunately, those vessels are being delivered

through this year and next year, although at this point due to cancellations, conversions and deliveries the orderbook has fallen to 133.1 million dwt,

or 17.3% of the on the water fleet, and we expect this to continue to decline through 2016 as the weak market should scare away new orders, but it

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2012 2013 2014 2015E 2016E 2017E

(nu

mb

er o

f ve

ssel

s)

Estimated Actual

36

%

30

%29

%

25

%

24

%

30

%

AXIA Capital Markets LLC Page 17

is important to watch newbuilding orders as if there is a glut of new ordering at the first signs of a rebound, we may be right back where we were in

2014.

Exhibit 26: Drybulk orderbook versus total fleet

Source: Clarkson Research Services, AXIA Capital Markets

In shipping, when vessels get past a certain age they become candidates for scrapping, which basically means that the vessels are sold to companies

that tear the vessel apart and sell the scrap metal. For context, a typical drybulk vessel can last anywhere between 20 to 30 years, depending on

how it is maintained and many people use 25 years as the average life of a vessel. As a vessel ages, you are required to undergo a dry dock every five

years for its special survey and routine repairs that cannot be done when the vessel is in the water. Typically, as a vessel gets older, these survey

costs increase as the integrity of the steel diminishes with age and there is more wear on the engine. So, as a vessel approaches its 20th birthday and

its fourth special survey is pending, an owner typically looks at the market to determine whether it will be strong enough so that the vessel will be

able to earn enough during the next five years to pay back the costs of the special survey (which sometimes costs upwards of $1 million or more,

depending on the size of the vessel), and still leave some profit. Therefore, in periods of strong freight markets, vessels continue to operate longer

than in periods of weak freight markets. Recently, due to the weak market we have seen vessels as young as 16 to 17 years old scrapped due to the

weak market conditions, and we expect this to continue going forward.

Exhibit 27: Vessel scrapping

Source: Clarkson Research Services Limited, AXIA Capital Markets

Currently, 9% of the total drybulk fleet or 69.1 million dwt is older than 20 years, and over the next two years, an additional 30.1 million tons (or over

500 vessels) will hit the 20 year mark and come upon their next special survey, which we consider likely scrapping candidates. Out of this total we

estimate about 50% of these vessels will go to the scrapyards over the next two years. To date, 2015 has been a strong year for scrapping as 22.5

million tons have already been scrapped year to date, and we estimate 28.3 million dwt to be scrapped by the end of the year, or 3.7% of the total

fleet.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

100

200

300

400

500

600

700

800

900

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

(% o

f fl

eet)

(mill

ion

dw

t)

Total drybulk fleet Orderbook Orderbook as a % of fleet

5.610.6

6.5

23.2

33.4

23.3

16.222.5

5.9

24.518.1

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012 2013 2014 2015E 2016E 2017E

(mill

ion

dw

t)

Actual vessel scrapping Estimated vessel scrapping

AXIA Capital Markets LLC Page 18

However, it is always important to remember that the decision on whether to scrap a vessel is dependent not only on the current market, but also

future expectations and we believe that as the market starts to see a light at the end of the tunnel, vessel scrapping will slow slightly in 2017 and

beyond. In addition, the recent decline in the price of scrap steel has also hindered the amount of vessels scrapped this year and the price for a

typical Capesize vessel sent to scrap has fallen from $10.6 million in October, 2014 to $6.8 million today.

While scrapping has helped slow down the growth of the drybulk fleet in recent years, the pool of vessels that would qualify for scrapping has been

declining, and in some vessel sizes, the fleets are relatively young due to the recent over-ordering so we do not expect scrapping alone to save the

drybulk market unless the market becomes so depressed that vessels less than 15 years old start heading to the scrap heap.

Exhibit 28: Age profile of the drybulk fleet

Source: Clarkson Research Services, AXIA Capital Markets

Putting it all together, we believe that the drybulk fleet will grow by 2.2% for the full-year 2015, a significant drop from the 4.4% growth experienced

in 2014, as increased scrapping during the first four months of the year coupled with delayed deliveries has helped keep growth in check. In 2016,

we expect to continue to see continued scrapping of older vessels and delayed deliveries which will translate into 2.4% growth for the year, and for

2017 we expect fleet growth to continue to slow to 2.3% as most of the orderbook will be worked off by then.

Exhibit 29: Drybulk fleet development

(in millions of DWT) 2012 2013 2014A 2015A1 2015E 2016E 2017E Capesize (>100k) 280.0 293.9 308.2 307.8 308.7 313.8 317.5

Panamax (70k-99k) 169.8 184.9 193.3 196.5 197.2 200.5 204.2

Supramax (40k-69k) 146.9 157.8 165.8 176.9 176.9 187.0 197.3

Handysize (20k-39k) 89.3 88.8 89.8 90.9 90.9 91.2 91.7

Total drybulk fleet 686.0 725.5 757.1 768.9 773.9 792.5 810.6

Capesize (>100k) Y-o-Y Change 12.0% 5.0% 4.9% (0.1%) 0.2% 1.6% 1.2%

Panamax (70k-99k) Y-o-Y Change 12.2% 8.9% 4.5%

5.0% 2.0% 1.7% 1.8%

Supramax (40k-69k) Y-o-Y Change 12.2% 7.4% 5.0% 5.0% 6.7% 5.5% 5.5%

Handsize (20k-39k) Y-o-Y Change 2.6% (0.6%) 1.1% 0.8% 1.2% 0.3% 0.6%

Total Fleet Y-o-Y Growth 10.7% 5.7% 4.4% 1.6% 2.2% 2.4% 2.3% 1 As of August 1, 2015

Source: Clarkson Research Services Limited, AXIA Capital Markets

46.5%52.7% 50.1% 54.3%

18.0%

20.4%18.4%

19.9%8.5%

11.4%13.1%

8.7%11.0%

9.5% 11.2% 7.9%15.9%

6.0% 7.1% 9.1%

0%

20%

40%

60%

80%

100%

Handysize Supramax Panamax Capesize

(per

cen

tage

of

flee

t in

dw

t)

0 - 4 yrs 5 - 9 yrs 10 - 14 yrs 15 - 19 yrs 20 yrs & over

AXIA Capital Markets LLC Page 19

Supply/Demand dynamic

Given our views on the supply and demand outlook for the dry sector, we believe that the oversupply of vessels that has been building since 2007

will finally start to be worked off, and that the market should start to move towards a balance by the end of 2016 as we expect demand to finally

start outpacing supply as deliveries continue to be delayed and the scrapping of older vessels continues. However, moving towards a balance is NOT

a balanced market and we believe it will take several years before the market becomes balanced. It is important to note, however, that the market

remains volatile and we will see pockets of strength like last month, and people will begin to get excited. When this happens, scrapping slows and

new orders start to creep up, as we witnessed in late 2013/early 2014, and these actions delay any true recovery. It appears for the time being that

lessons have been learned but it remains to be seen if this will continue to be remembered as time goes on. Any additional ordering or slowdown in

scrapping will only serve to delay the balancing of the market and cause rates to remain depressed even longer.

Exhibit 30: Total drybulk supply/demand growth

Source: Clarkson Research Services, AXIA Capital Markets

Capesize fleet

Capesize vessels range from 100,000 dwt and above, and specialize in iron ore, although they are known to also carry coal cargoes. Capesize vessels

have four sub-categories; the mini-Cape vessel is typically between 100,000-139,999 dwt, the Capesize vessel is between 140,000-199,999 dwt, the

Valemax vessel is between 200,000-219,999 dwt, and the Very Large Ore Carrier (VLOC) vessel is 220,000 dwt and above, sometimes up to 400,000

dwt. The primary routes used to calculate the average time charter rates are Australia to China and Japan, Brazil to China, the U.S. to Rotterdam,

and Europe to the Far East. The Capesize fleet has witnessed strong growth over the past five years, growing at an average rate of 12.5%, although

this year we expect that growth to finally slow significantly as year to date, the fleet has actually shrunk by 0.1% in 2015 as the 61 vessels that have

been delivered were offset by the 75 vessels that were scrapped, although we estimate that by the end of the year, the fleet will grow by 0.2%. Going

forward, we expect net fleet growth of 1.6% in 2016 and 1.2% in 2017 as the orderbook for Capesize vessels currently stands at 17% of the current

fleet, and we expect the scrapping of older tonnage in the Capesize market to continue at an accelerated rate through the end of this year, and for

the first half of 2016 as rates remain at depressed levels and should help keep net fleet growth in check for the next two years.

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

100.0%

(5.0%)

0.0%

5.0%

10.0%

15.0%

20.0%

2008 2009 2010 2011 2012 2013 2014 2015E 2016E 2017E

(Ves

sel u

tiliz

atio

n)

(Yea

r o

ver

year

gro

wth

)

Dry bulk demand Dry bulk supply Vessel Utilization

AXIA Capital Markets LLC Page 20

Exhibit 31: Capesize fleet additions/deletions

Source: Clarkson Research Services, AXIA Capital Markets

In periods of strong market conditions, Capesize vessels do the best relative to any other vessel class, but they also do the worst in times of weak

markets. The freight market for Capesize vessels is notorious for being extremely volatile, and average monthly freight rates have hit highs of over

$188,000 per day and lows of $4,000 per day. However, over the past five years, rates for Capesize vessels have been subdued due to the oversupply

of vessels in the marketplace. As freight rates have remained weak, asset values have followed suit and the price of a five year old vessel has fallen

to $35 million today, down from its all-time highs of $155 million back in 2008, however this value is up slightly from its low of $31 million earlier this

year. We believe that the rates for Capesize vessels will pick up slightly for the remainder of this year, although we expect the first half of 2016 to

be challenging as the supply of vessels typically increases during the first few months of the year and values may test the lows witnessed in early

2015 again. We also expect vessel earnings to average below $10,000 per day for the first half of 2016. Then as we progress to the second half of

2016, we expect both freight rates and values to increase slightly as the oversupply in the market works itself out, however our estimate for Capesize

earnings to average $12,500 per day in 2016 is well below the five year average rate of $16,408 per day and we believe there is a lot of work to be

done before rates improve to healthy levels again.

Exhibit 32: Capesize earnings per day, actual and estimated Exhibit 33: Capesize asset values (actual and estimated)

Source: Baltic Index, AXIA Capital Markets Source: Clarkson Research Services Limited, AXIA Capital Markets

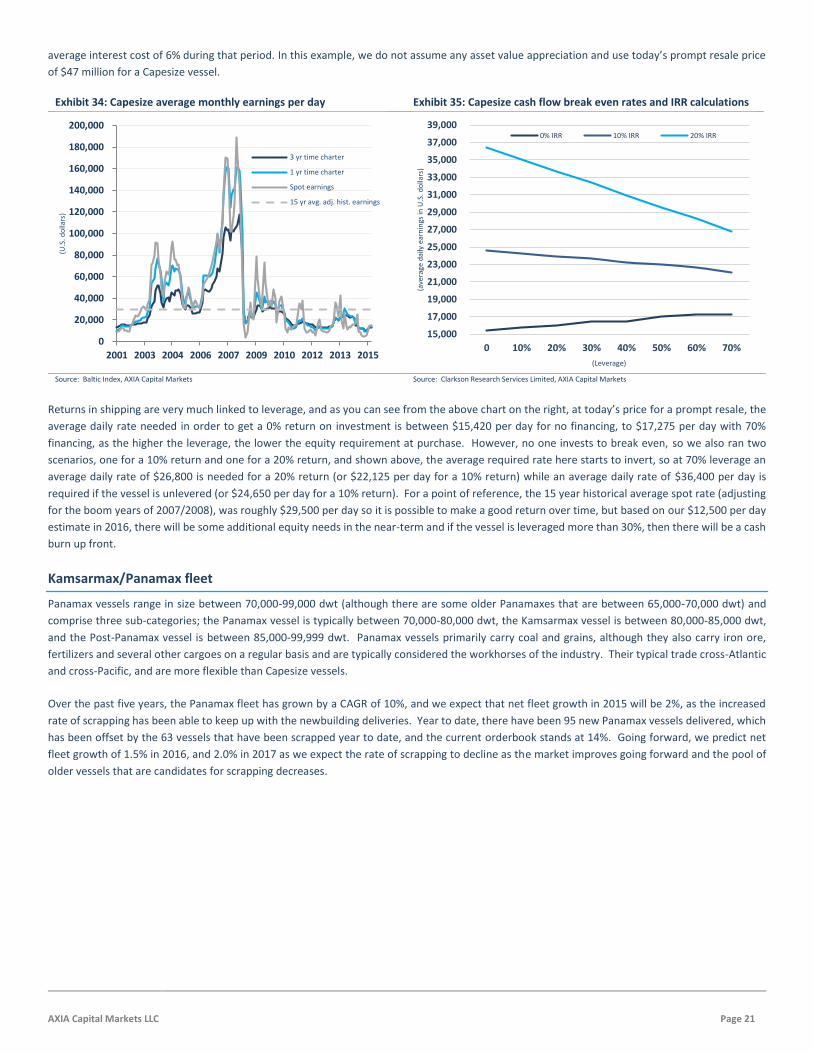

Given our rate assumption, it is also important to look at average operating expenses and cash flow break even rates in order to put the vessel

earnings in the context of returns. Below, we have ran a historical calculation of the daily running costs for a Capesize vessel, and financing costs of

purchasing a prompt resale vessel based on today’s prices, and then scrapping the vessel after 20 years at historical scrap rates, which is basically in

line with today’s scrap values. Given this, you can calculate what the vessel’s earnings would need to be over its useful life at specific return

parameters. For leverage, we assume the amount borrowed is amortized over the first fifteen years of the vessel’s operations down to zero, with an

(1.0%)

(0.8%)

(0.6%)

(0.4%)

(0.2%)

0.0%

0.2%

0.4%

0.6%

0.8%

(25)

(20)

(15)

(10)

(5)

0

5

10

15

20

Jan-1

5

Feb-1

5

Mar-1

5

Ap

r-15

May-1

5

Jun

-15

Jul-15

Au

g-15

Sep-1

5

Oct-15

No

v-15

De

c-15

Jan-1

6

Feb-1

6

Mar-1

6

Ap

r-16

May-1

6

Jun

-16

Jul-16

Au

g-16

Sep-1

6

Oct-16

No

v-16

De

c-16

(% c

han

ge in

fle

et

size

m-o

-m)

(nu

mb

er o

f ve

ssel

s )

Deliveries Scrapping Net fleet growth

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2014 2015 2015e 2016e 5-year avg.

0

10

20

30

40

50

60

70

80

2010 2011 2012 2013 2014 2015 2016

(mill

ion

s o

f U

.S. d

olla

rs)

Newbuilding Prompt resale 5 yr old 10-yr old

AXIA Capital Markets LLC Page 21

average interest cost of 6% during that period. In this example, we do not assume any asset value appreciation and use today’s prompt resale price

of $47 million for a Capesize vessel.

Exhibit 34: Capesize average monthly earnings per day Exhibit 35: Capesize cash flow break even rates and IRR calculations

Source: Baltic Index, AXIA Capital Markets Source: Clarkson Research Services Limited, AXIA Capital Markets

Returns in shipping are very much linked to leverage, and as you can see from the above chart on the right, at today’s price for a prompt resale, the

average daily rate needed in order to get a 0% return on investment is between $15,420 per day for no financing, to $17,275 per day with 70%

financing, as the higher the leverage, the lower the equity requirement at purchase. However, no one invests to break even, so we also ran two

scenarios, one for a 10% return and one for a 20% return, and shown above, the average required rate here starts to invert, so at 70% leverage an

average daily rate of $26,800 is needed for a 20% return (or $22,125 per day for a 10% return) while an average daily rate of $36,400 per day is

required if the vessel is unlevered (or $24,650 per day for a 10% return). For a point of reference, the 15 year historical average spot rate (adjusting

for the boom years of 2007/2008), was roughly $29,500 per day so it is possible to make a good return over time, but based on our $12,500 per day

estimate in 2016, there will be some additional equity needs in the near-term and if the vessel is leveraged more than 30%, then there will be a cash

burn up front.

Kamsarmax/Panamax fleet

Panamax vessels range in size between 70,000-99,000 dwt (although there are some older Panamaxes that are between 65,000-70,000 dwt) and

comprise three sub-categories; the Panamax vessel is typically between 70,000-80,000 dwt, the Kamsarmax vessel is between 80,000-85,000 dwt,

and the Post-Panamax vessel is between 85,000-99,999 dwt. Panamax vessels primarily carry coal and grains, although they also carry iron ore,

fertilizers and several other cargoes on a regular basis and are typically considered the workhorses of the industry. Their typical trade cross-Atlantic

and cross-Pacific, and are more flexible than Capesize vessels.

Over the past five years, the Panamax fleet has grown by a CAGR of 10%, and we expect that net fleet growth in 2015 will be 2%, as the increased

rate of scrapping has been able to keep up with the newbuilding deliveries. Year to date, there have been 95 new Panamax vessels delivered, which

has been offset by the 63 vessels that have been scrapped year to date, and the current orderbook stands at 14%. Going forward, we predict net

fleet growth of 1.5% in 2016, and 2.0% in 2017 as we expect the rate of scrapping to decline as the market improves going forward and the pool of

older vessels that are candidates for scrapping decreases.

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2001 2003 2004 2006 2007 2009 2010 2012 2013 2015

(U.S

. do

llars

)

3 yr time charter

1 yr time charter

Spot earnings

15 yr avg. adj. hist. earnings

15,000

17,000

19,000

21,000

23,000

25,000

27,000

29,000

31,000

33,000

35,000

37,000

39,000

0 10% 20% 30% 40% 50% 60% 70%

(ave

rage

dai

ly e

arn

ings

in U

.S. d

olla

rs)

(Leverage)

0% IRR 10% IRR 20% IRR

AXIA Capital Markets LLC Page 22

Exhibit 36: Panamax/Kamsarmax fleet additions/deletions

Source: Clarkson Research Services, AXIA Capital Markets

Panamax vessels tend to move in a similar pattern to Capesize vessels, although their earnings are affected by the seasonality of the grain trades, so

rates always tend to be better in the second and fourth quarters of the year. Panamax vessels can also be used as a substitute for Capesize vessels

if the earnings for Capesize vessels significantly outperforms those of Panamax vessels (typically if you see Capesize rates at levels that are more than

double Panamax rates, charterers may start to split cargoes). Asset values have bottomed recently at $16.5 million for a five-year old vessel but have

bounced back slightly to $18 million, well below their all-time highs of $92 million in late 2007. Going forward, we expect rates for Panamax vessels

to remain flat at depressed levels with some volatility through mid-2016, as they continue to be challenged by the weakness in the coal trades and

the uncertainty of the grain trade.

Exhibit 37: Panamax earnings per day, actual and estimated Exhibit 38: Panamax vessel values (actual and estimated)

Source: Bloomberg, AXIA Capital Markets Source: Bloomberg, AXIA Capital Markets

Based on our estimates for daily running costs for a Panamax vessel, and financing costs of purchasing a prompt resale vessel based on today’s prices,

and then scrapping the vessel after 20 years at historical scrap rates, which is basically in line with today’s scrap values. Given this, you can calculate

what the vessel’s earnings would need to be over its useful life at specific return parameters.

(1.0%)

(0.5%)

0.0%

0.5%

1.0%

(15)

(10)