driving forces for the emerging workforce - deloitte

TRANSCRIPT

Driving forces for the emerging workforceApril 2021

02

Brochure / report title goes here | Section title goes here

Driving forces for the emerging workforce

03

Preface 04

Introduction 05

Key highlights 06

Chapter 1: Growing trend of working for

sectors other than technology 08

Chapter 2: A company’s impact on the

community and nation as primary motivators 10

Chapter 3: Commitment to invest in

long-term growth and development 13

Chapter 4: Rise of metropolitan cities has

changed the outlook towards jobs 16

Conclusive remarks 18

References 19

Connect with us 20

Contents

04

Preface

The Next-Gen Tech Talent Trends survey was conducted amidst COVID-19, which brought about radical changes in the world around us. The pandemic brought forth a sudden, unforeseen crisis in our lives. To embrace the new realities amongst the perpetual disruption, organisations were forced to rapidly adapt business models and expect employees to embrace new ways of working. In the post-pandemic world, organisations will find it imperative to orient themselves towards a “thriving” mindset − a shift from mere “survival” – to accomplish its strategic priorities and stay ahead of the competition. To live the “thrive” mindset, organisations will need to rely on their most valuable asset – human capital. In a dynamic world, a ‘people-centric’ approach to growth is more critical than algorithmic models that ‘predict ’ growth scenarios and situations. Predictability is passé.

Evidently, this has mandated organisations to focus on how to best manage talent and equip themselves to navigate through turbulent realities. To help organisations appraise talent, and understand how the pandemic has affected talent supply in India, and caused a shift in job expectations and preferences, Deloitte Touche Tohmatsu India LLP conducted a study with the final year students of top 30 engineering collages (ranked by National Institutional Ranking Framework ).1 The study’s objective was to understand their industry preferences, employment motivations, and career aspirations. With more than 10,000 responses, the survey was well received by the target population.

04

Driving forces for the emerging workforce

Driving forces for the emerging workforce

Introduction

The past decade has seen a radical change in almost every aspect of our lives. Dynamic forces at play have reshaped the cultural, economic, and technological landscapes we live in. These changes have also been experienced in the world of work.

An ever-evolving environment with myriad economic, health, social, and environmental challenges has given rise to a generation that is more “resilient” and learning to thrive in an ever-changing environment and reimagine the impossible.

The recent global pandemic has had a great impact on gen Z. “Instead of looking ahead to a world of opportunities, gen Z now peers into an uncertain future.” According to the Deloitte Global Millennial Survey 20202, 30 percent of the gen Z faced either a job loss or furlough due to the economic crisis caused by the pandemic. This has also shaped the mindset of gen Z at a critical time as they transition into the workforce. The report highlights a greater

commitment of the next generation of talent to financial and social responsibility, focus on individual’s life and development, and an orientation to see an opportunity in adversity.

The next-gen tech talent shows an increasing preference towards lifelong learning and development, challenging roles, and superior working culture. Organisations’ purpose and market reputation, and a good pay package hold prominence from an overall career standpoint.

Further, the uncertainty surrounding the COVID-19 scenario has brought about unprecedented changes across industries that has significantly changed the work environment. This has also resulted in shifts in the next generation’s workforce priorities and aspirations, such as drive to join public enterprises due to job stability and opportunity to service the nation.

05

Key highlights

1. Shift in sector and industry preference Increasing preference for working for sectors other than technology

While technology, media, and telecommunications is still the most preferred sector, a reasonable proportion of respondents ranked banking; financial services and insurance; and government and public services as the leading sector choice.

2. Changes in pull factor for gen Z A company’s impact on the community and nation are some of the primary motivators for gen Z.

Rising social awareness amongst gen Z is motivating campus graduates to seek companies that align with their values as a society. Factors such as nation building and inclusiveness attract gen Z to an organisation. However, these factors may not influence employee retention.

About 83 percent of the respondents find a company’s mission, vision, and values to be a strong motivator to join a company.

More than 50 percent respondents expressed interest in working for public-sector organisations as this gives them an opportunity to serve the nation, in addition to job security and stability.

Proportion of talent that gives importance to mission, vision, and values

06

Driving forces for the emerging workforce

3. Greater focus on personal development Gen Z prefers organisations committed to investing in their long-term growth and development.

A fulfilling career offering challenging roles, rapid advancement, and an opportunity for personal development are of prime importance to campus graduates. These aspects motivate them to stay in a job.

Unsurprisingly, engineering graduates continue to focus on pay packages when taking up their first job after campus. However, they are also keen on a sound and flexible work culture providing a platform to learn and grow.

4. Redefining workplace Rise of metropolitan cities has changed our outlook towards jobs, but upcoming graduates have a different preference for location.

Although Indian and international cities rank high amongst preferred work locations, many graduates are now exploring options to work in organisations closer to their base locations.

About 71 percent graduating students would prefer working in India.

About 79 percent respondents said that long-term learning and development is a key expectation from their career.

Segment of talent that ranks learning and development as a priority

Proportion of graduates who prefer working in India

07

Driving forces for the emerging workforce

Driving forces for the emerging workforce

08

Chapter 1: Growing trend of working for sectors other than technology

The next-gen talent is starry-eyed about the fast-paced and evolving technology sector. Working for leading American technology giants is a dream for a significant number of the survey respondents.

A closer analysis showed that nearly 63 percent graduates in the computer science and IT engineering programmes, and 52 percent in the electrical and electronics engineering programmes prefer working in the technology, media and telecom sectors as these are in line with their education streams.

However, this sector choice is not as unanimous as we would have expected. While the oh-so-ambitious job profiles and global-best working cultures offered at these technology companies do not cease to lure talent, there is a palpable shift in this common sentiment. Gen Z values job stability and security more than ever, with the uncertainty looming in job markets. A preliminary view of the talent pool’s sector preference shows that respondents have a keen interest in the Banking, Financial Services, and Insurance (BFSI), and government and public services sectors.

Driving forces for the emerging workforce

09

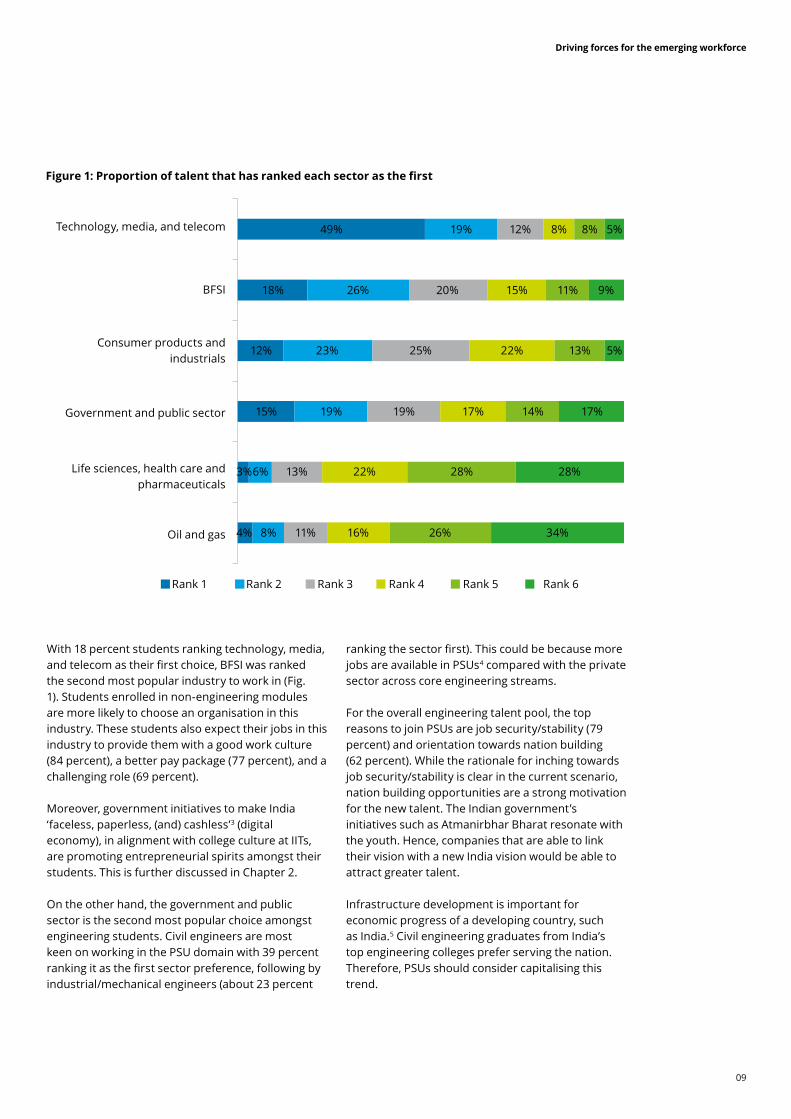

Figure 1: Proportion of talent that has ranked each sector as the first

With 18 percent students ranking technology, media, and telecom as their first choice, BFSI was ranked the second most popular industry to work in (Fig. 1). Students enrolled in non-engineering modules are more likely to choose an organisation in this industry. These students also expect their jobs in this industry to provide them with a good work culture (84 percent), a better pay package (77 percent), and a challenging role (69 percent).

Moreover, government initiatives to make India ‘faceless, paperless, (and) cashless’3 (digital economy), in alignment with college culture at IITs, are promoting entrepreneurial spirits amongst their students. This is further discussed in Chapter 2.

On the other hand, the government and public sector is the second most popular choice amongst engineering students. Civil engineers are most keen on working in the PSU domain with 39 percent ranking it as the first sector preference, following by industrial/mechanical engineers (about 23 percent

ranking the sector first). This could be because more jobs are available in PSUs4 compared with the private sector across core engineering streams.

For the overall engineering talent pool, the top reasons to join PSUs are job security/stability (79 percent) and orientation towards nation building (62 percent). While the rationale for inching towards job security/stability is clear in the current scenario, nation building opportunities are a strong motivation for the new talent. The Indian government’s initiatives such as Atmanirbhar Bharat resonate with the youth. Hence, companies that are able to link their vision with a new India vision would be able to attract greater talent.

Infrastructure development is important for economic progress of a developing country, such as India.5 Civil engineering graduates from India’s top engineering colleges prefer serving the nation. Therefore, PSUs should consider capitalising this trend.

Technology, media, and telecom

BFSI

4%

3%

15%

12%

18%

49%

8%

6%

19%

23%

26%

19%

11%

13%

19%

25%

20%

12%

16%

22%

17%

22%

15%

8%

26%

28%

14%

13%

11%

8%

34%

28%

17%

5%

9%

5%

Consumer products and industrials

Government and public sector

Oil and gas

Life sciences, health care and pharmaceuticals

Rank 1 Rank 2 Rank 3 Rank 4 Rank 5 Rank 6

Driving forces for the emerging workforce

10

Chapter 2: A company’s impact on the community and nation as primary motivators

The current unemployment rate in India is 6.6 percent6 (as of March 2021), which is lower compared with the past year’s average. As an organisation, understanding how to attract the brightest candidates is more important. The prime motivators for the majority of the engineering graduates is the company’s commitment towards the society and nation.

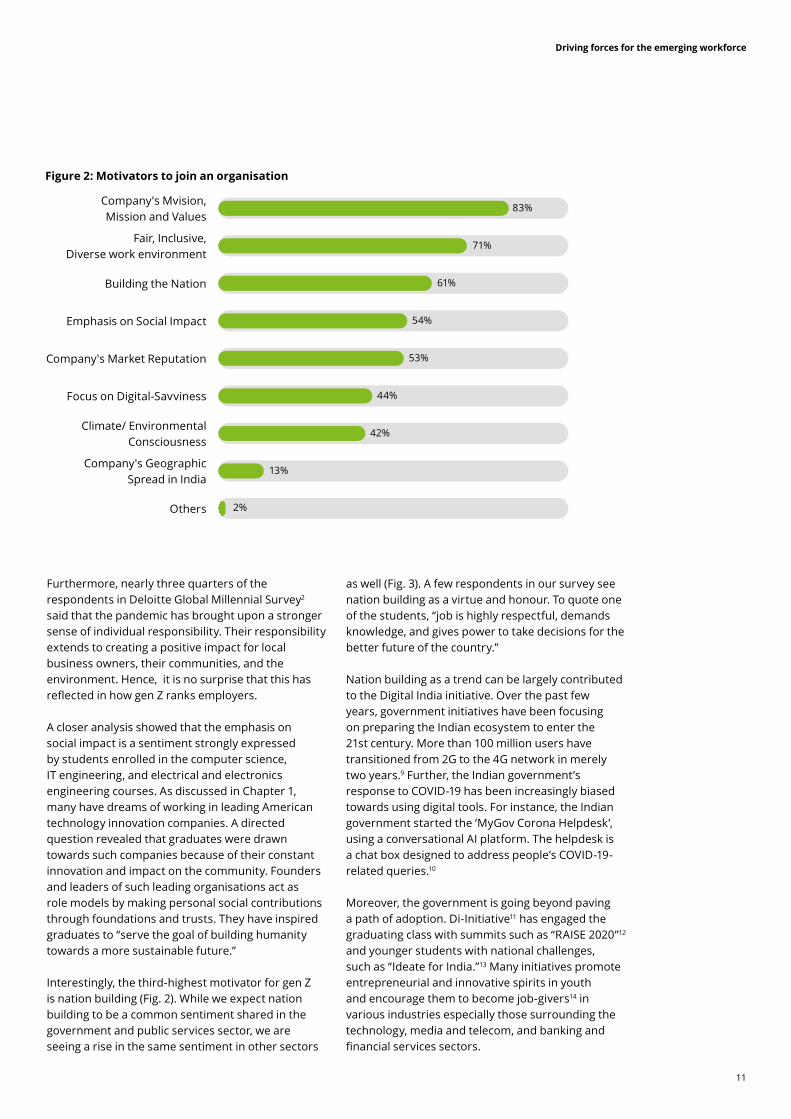

The most important pull factor for gen Z is alignment with a company’s vision, mission, and values, followed by a company providing a culture

that includes a fair, inclusive, and diverse work environment (Fig. 2). These were predictable outcomes as globally gen Z and millennials are making their voices heard for social and political injustice. This passion has inspired Indian students to express their concerns. Companies can no longer focus just on shareholders. Deloitte has shifted to define this as a social enterprise where a company’s mission must respect, and support its community and environment.7 Thus, their decisions and choices need to reinforce their commitment to stakeholders.8

Driving forces for the emerging workforce

11

Furthermore, nearly three quarters of the respondents in Deloitte Global Millennial Survey2 said that the pandemic has brought upon a stronger sense of individual responsibility. Their responsibility extends to creating a positive impact for local business owners, their communities, and the environment. Hence, it is no surprise that this has reflected in how gen Z ranks employers.

A closer analysis showed that the emphasis on social impact is a sentiment strongly expressed by students enrolled in the computer science, IT engineering, and electrical and electronics engineering courses. As discussed in Chapter 1, many have dreams of working in leading American technology innovation companies. A directed question revealed that graduates were drawn towards such companies because of their constant innovation and impact on the community. Founders and leaders of such leading organisations act as role models by making personal social contributions through foundations and trusts. They have inspired graduates to “serve the goal of building humanity towards a more sustainable future.”

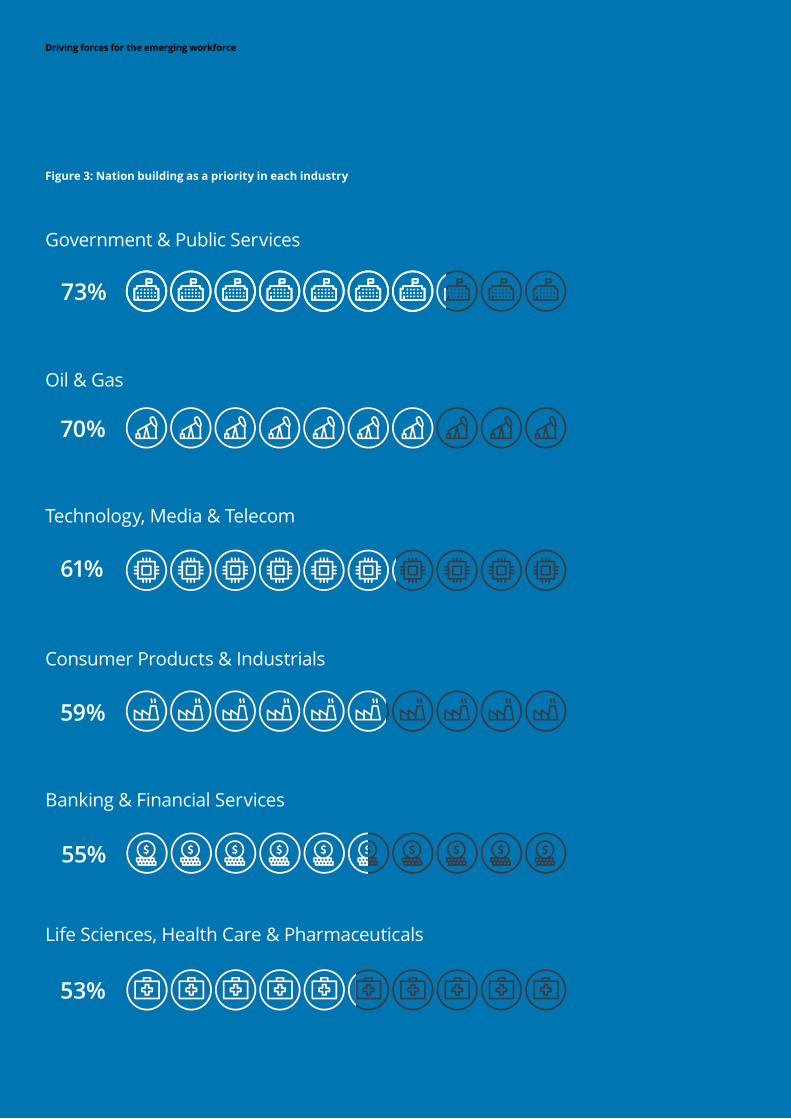

Interestingly, the third-highest motivator for gen Z is nation building (Fig. 2). While we expect nation building to be a common sentiment shared in the government and public services sector, we are seeing a rise in the same sentiment in other sectors

as well (Fig. 3). A few respondents in our survey see nation building as a virtue and honour. To quote one of the students, “job is highly respectful, demands knowledge, and gives power to take decisions for the better future of the country.”

Nation building as a trend can be largely contributed to the Digital India initiative. Over the past few years, government initiatives have been focusing on preparing the Indian ecosystem to enter the 21st century. More than 100 million users have transitioned from 2G to the 4G network in merely two years.9 Further, the Indian government’s response to COVID-19 has been increasingly biased towards using digital tools. For instance, the Indian government started the ‘MyGov Corona Helpdesk’, using a conversational AI platform. The helpdesk is a chat box designed to address people’s COVID-19-related queries.10

Moreover, the government is going beyond paving a path of adoption. Di-Initiative11 has engaged the graduating class with summits such as “RAISE 2020”12 and younger students with national challenges, such as “Ideate for India.”13 Many initiatives promote entrepreneurial and innovative spirits in youth and encourage them to become job-givers14 in various industries especially those surrounding the technology, media and telecom, and banking and financial services sectors.

Figure 2: Motivators to join an organisation

Company's Mvision, Mission and Values

83%

Fair, Inclusive, Diverse work environment

71%

Building the Nation 61%

Emphasis on Social Impact 54%

Company's Market Reputation 53%

Focus on Digital-Savviness 44%

Climate/ Environmental Consciousness

42%

Company's Geographic Spread in India

13%

Others 2%

Figure 3: Nation building as a priority in each industry

Government & Public Services

73%

Technology, Media & Telecom

61%

Oil & Gas

70%

Consumer Products & Industrials

59%

Banking & Financial Services

55%

Life Sciences, Health Care & Pharmaceuticals

53%

Driving forces for the emerging workforce

Driving forces for the emerging workforce

13

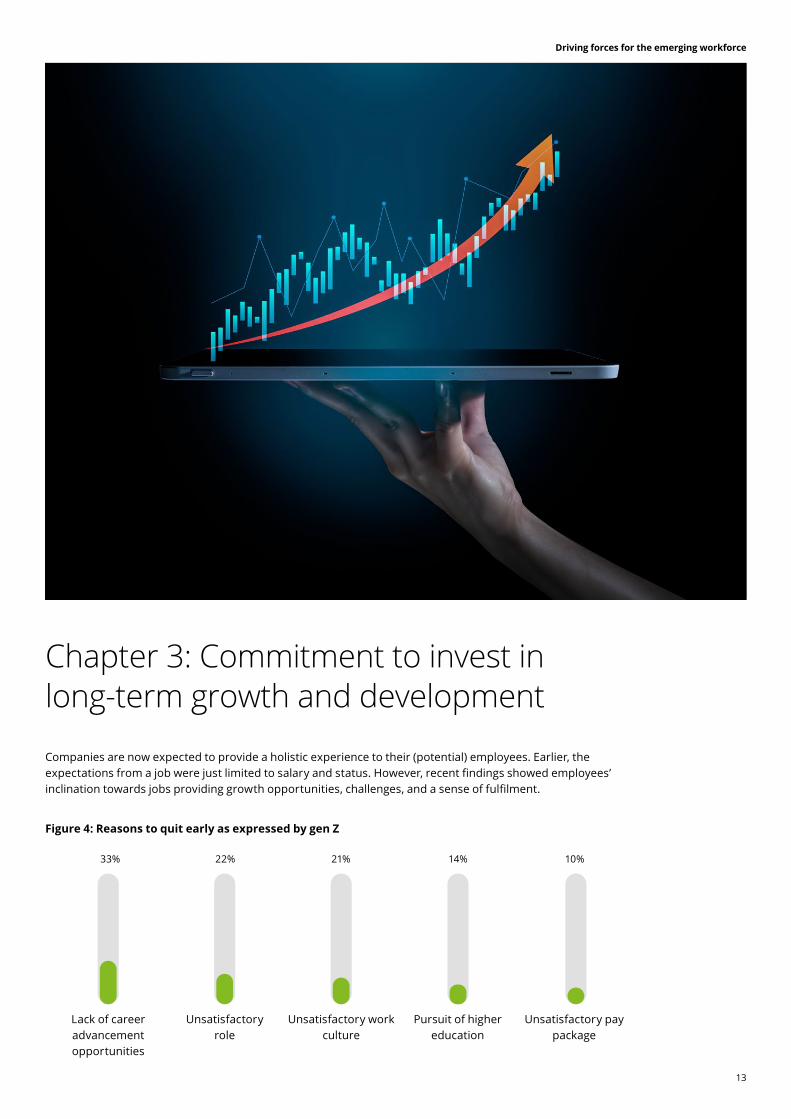

Figure 4: Reasons to quit early as expressed by gen Z

Chapter 3: Commitment to invest in long-term growth and development

Companies are now expected to provide a holistic experience to their (potential) employees. Earlier, the expectations from a job were just limited to salary and status. However, recent findings showed employees’ inclination towards jobs providing growth opportunities, challenges, and a sense of fulfilment.

Lack of career advancement opportunities

Unsatisfactory work culture

Unsatisfactory role

Pursuit of higher education

Unsatisfactory pay package

33% 22% 21% 14% 10%

Driving forces for the emerging workforce

14

Figure 5: Long term-career expectation as expressed by gen Z who identified lack of career advancement as a reason to quit early

Our recent study highlighted one of the most prominent reasons to quit early in a job is lack of career advancement opportunities (Fig. 4). To understand what factors would encourage these

individuals to not quit their organisations, we did further analysis of their responses pertaining to their long-term career expectations.

Our survey findings highlighted three key areas that can ensure career advancement and retention: life-long learning opportunity, work-life balance, and job stability/security (Fig. 5).

The thirst for knowledge has also translated into the expectations of future graduates. In our survey, nearly 80 percent respondents expect lifelong learning and development to be a part of their job profiles.

With a rise in AI, bots and blended HR are slowly taking over a workplace's day-to-day operations.15 The expectations from the future workfore has changed. Most of the gen Z recognise the value of continuous learning via online learning platforms

and internal training programmes. Indian learning platforms16 have also collaborated with National Skill Development Corporation (NSDC) to provide learning material in multiple Indian languages to create a future-ready workforce.

This observation has been in line with our previous findings.17 Earlier, we had highlighted that both graduates and business leaders have realised that constant changes in technology, work practices, and business models alongside frequent job changes and accelerating rate of skills obsolescence, have forced individuals to focus on multiskilling.18 Hence, both stakeholders are responsible to find new approaches to integrate continuous and lifelong development into day-to-day lives.

Lifelong learning and development

Job stability/security

Work-life balance

Making an impact on society

Rapid and flexible career progression

Servicing the nation

82%

77%

68%

65%

60%

54%

Driving forces for the emerging workforce

15

An unsatisfactory role was identified as another prominent reason by (potential) employees to quit in their organisations early (Fig. 4). Our survey indicated that for nearly 41 percent (potential) employees, both corporate and challenging roles are associated with what gen Z would term as a satisfactory role. This further reinforces how attractive corporate jobs have proved for the future workforce. Work-

life balance has evolved from being a buzzword to an expectation. Gen Z has seen its parents and grandparents struggle with separating work from personal life and most often, giving more importance to their professional goals. The importance of work-life balance has been heightened by COVID-19. At present, India is the second-largest country to face burnout.19

Our survey showed that 86 percent of the graduating individuals expect a good working culture and 67 percent count on a flexible working environment, which includes timing and location (Fig. 6). Many respondents have said that they would prefer working in the public and government sector as it can be a source of stable income and timing.

This was a predictable finding as the Deloitte Global Millennial Survey2 found that 48 percent of the gen Z

and 44 percent millennial respondents were stressed always or most of the time before the pandemic. However, as the crisis has unfolded, respondents have reported to be less stressed and anxious all the time. This is a result of spending more time with family, shorter commute, and more flexibility at the workplace.

Good working culture

Good pay package

Challenging role

Flexible work environment

Rapid career progression

Culture of recognition

Allows for travel

Job autonomy 30%

Figure 6: First job expectation as expressed by gen Z

86%

79%

69%

67%

59%

51%

48%

Driving forces for the emerging workforce

16

Chapter 4: Rise of metropolitan cities has changed the outlook towards jobs

In the previous chapters, we have been looking at various factors that come into play when joining a company and changing roles. In our survey, we have asked students studying in tier 1 and 2 cities regarding their next moves.

A majority of the participants interested in the technology sector have chosen metro cities as their work destination due to the availability of decent infrastructure (Fig. 7). Bengaluru is the preferred city for aspiring professionals. According to the India

Skills Report 2021, tier 2 states, such as Rajasthan, Gujarat, and Telangana, have made it to the top 10 states with employable talent.20

Government initiatives have increased the inclination towards nation building. As a result, a majority (71 percent) of the respondents chose to stay in India rather than pursue opportunities abroad. A deeper analysis shows that there is an increasing trend of choosing to live outside of metropolitan cities.

Driving forces for the emerging workforce

17

Figure 7: Location preference of talent choosing to work in India

Moreover, metropolitan cities, such as Mumbai and Delhi, no longer appeal to graduates due to cramped housing, high cost of living, and high pollution levels; they prefer tier 1 cities, such as Pune and Bengaluru.21

Developers are looking at tier 2/3 cities for their next project.22 Their infrastructure caters to demands from gen Z and millennials with a stronger focus on the walk-to-work concept, connectivity, and quality of life. Moreover, an Economic Times survey discovered that 40 percent23 of the working population said that they would take a pay cut to move to a tier 2 or 3 city.

With all factors included, gen Z (and to same extent, millennials) would rather move away from metropolitan cities. About 25 percent graduates have stated that they would prefer working in a tier 2 or 3 city than a tier 1 city.

Ignoring the implications of COVID-19 on this decision is not easy. The lockdown has shown organisations and employees the ease of remote working. The Times of India has also reported that 69 percent24 of the workforce believe that their productivity has increased while working remotely. In the Deloitte Global Millennial survey2, more than 60 percent gen Z and millennials would want the option of working remotely more frequently. Nearly the same number of respondents also believe that remote working would enable a better work-life balance. Furthermore, more than half of the respondents said that if given the opportunity to work from home, they would choose to live outside of major cities. The effect of such thinking is currently being reflected in the Indian market. A JLL India report mentioned a 50 percent drop in office leasing space across seven major Indian cities.

Metro cities in India Any location

in India18%

76%

5% Rural locations in India

18

Conclusive remarks

In the future, employers need to consider a holistic approach while planning their talent pipelines. With a new generation entering the workforce, rethinking the way we attract, retain, and manage our talent is important.

Today, workforce is affected by a generational change and COVID-19 has also shifted the norms of defining motivators. We have seen an increasing popularity in job security and growth opportunity being a priority for job seekers. The pandemic brought forward the fear of job losses and livelihood in everyone. As a result, we may see a rise in a workforce that is more averse to taking risks compared with its predecessor.

COVID-19 has also helped employers gain trust in the work-from-home model and allowed many employees to embrace this as a permanent solution. Many employees have chosen to live in tier 2 or 3 cities. More gen Z engineers are interested in being part of an alternative workforce, such as freelancers, as they try to find a balance between their professional lives and personal lives. Moreover, many organisations have taken swift actions in their digital journeys. Demand for digital skills is expected to increase but supply may remain low. The emerging workforce realises the importance of staying relevant and continuing their learning journeys.

As gen Z joins the workforce, leaders need to embrace their roles outside their job description as they become the face of their company’s value. Their role in creating a transparent and fair work environment while also challenging their team to reach new targets every day is now paramount in becoming a market differentiator.

Managers also need to adopt such traits as they play an important role in fostering an environment of trust in day-to-day operations. They also need to have more frequent check-ins with their team members to understand their medium- and long-term aspirations, and give them directions on how the organisation can meet and manage expectations.

18

Driving forces for the emerging workforce

Driving forces for the emerging workforce

19

References

1 MHRD, National Institute Ranking Framework (NIRF). (2021).https://www.nirfindia.org/2020/Ranking2020.html2 Deloitte, Global Millennial Survey. (2020). https://www2.deloitte.com/global/en/pages/about-deloitte/articles/millennialsurvey.html 3 Modi government’s six-point action plan to boost digital transactions. (2021). https://www.financialexpress.com/opinion/modi-governments-six-point-action-plan-to-boost-digital-transactions/1174867/4 PSU Jobs 2021 | Public Sector Company Jobs. (2021).https://www.indgovtjobs.in/2019/07/PSU-Govt-Jobs.html 5 Today, E. (2020). India needs skilled civil engineers for the booming construction industry, but how can we close the skill gap? https://www.indiatoday.in/education-today/jobs-and-careers/story/india-needs-skilled-civil-engineers-for-the-booming-construction-industry-1457173-2019-02-15 6 Center of Monitoring Indian Economy. (2021).Retrieved 9 March 2021, from https://cmie.com/7 Deloitte, Ethics and the future of work. (2020).https://www2.deloitte.com/us/en/insights/focus/human-capital-trends/2020/ethical-implications-of-ai.html8 Vance, Robert J. "Employee engagement and commitment." SHRM foundation. (2006).9 Jio poised to play key role in development of 5G ecosystem in India: RIL. (2020). https://economictimes.indiatimes.com/industry/telecom/telecom-news/jio-poised-to-play-key-role-in-development-of-5g-ecosystem-in-india-ril/articleshow/76551117.cms?from=mdr 10 #IndiaFightsCorona COVID-19 https://www.mygov.in/covid-1911 Di-Initiatives | Digital India Programme | Ministry of Electronics & Information Technology(MeitY) Government of India https://digitalindia.gov.in/di-initiatives 12 RAISE 2020 - Responsible AI for Social Empowerment https://raise2020.indiaai.gov.in/13 Ideate for India – Creative Solutions Using Technology https://ideateforindia.negd.in/14 Kapoor, N. (2017). How Digital India Concept Has Changed Face of Start-Ups and Entrepreneurs in India https://yourstory.com/mystory/c7887d8bf5-how-digital-india-conc#:~:text=Digital%20India%20programme%20was%20introduced,face%20of%20entrepreneurship%20in%20India.15 Deloitte, Transitioning to the future of work and the workplace. (2020).https://www2.deloitte.com/in/en/pages/human-capital/articles/gx-transitioning-to-the-future-of-work-and-the-workplace.html 16 Home - TiE - Global Entrepreneurship Organization. (2020). https://delhi.tie.org/

17 Deloitte, Learning in the Flow of Life. (2019).https://www2.deloitte.com/us/en/insights/focus/human-capital-trends/2019/reskilling-upskilling-the-future-of-learning-and-development.html

18 Deloitte, Laying the foundation for the future of work in India. (2019). https://www2.deloitte.com/us/en/insights/focus/reimagining-higher-education/future-of-work-in-india.html19 https://timesofindia.indiatimes.com/life-style/relationships/work/india-is-the-second-largest-country-to-face-employee-burnouts-with-29-per-cent-survey/articleshow/78532285.cms20 India is the second-largest country to face employee burnouts with 29 per cent: Survey - Times of India. (2020). https://timesofindia.indiatimes.com/life-style/relationships/work/india-is-the-second-largest-country-to-face-employee-burnouts-with-29-per-cent-survey/articleshow/78532285.cms 21 ET survey: Why people are willing to take 40% pay cut, move to non-metro city. (2020). https://economictimes.indiatimes.com/wealth/personal-finance-news/et-survey-why-people-are-willing-to-take-40-pay-cut-move-to-non-metro-city/articleshow/71771233.cms?from=mdr 22 Akhtar, N. Tier II & III Cities - Growth Engines for the Future. (2020). https://www.nbmcw.com/report/construction-infra-industry/30474-tier-ii-a-iii-cities-growth-engines-for-the-future.html 23 88% of workers in India prefer work from home - Times of India. (2020). https://timesofindia.indiatimes.com/business/india-business/88-of-workers-in-india-prefer-work-from-home/articleshow/77234342.cms 24 Work from home: Top bosses share their take. (2020). https://www.timesnownews.com/business-economy/companies/article/work-from-home-top-bosses-share-their-take/664413

Driving forces for the emerging workforce

20

Connect with us

Contributors

Anand Shankar Partner, [email protected]

Saurabh DwivediPartner, [email protected]

Shruti Mehrotra

Ayesha Lal

Devika Shanbhag

Ashwini Hembram

Akanksha Mehta

Sanjana Marda

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms. This material is prepared by Deloitte Touche Tohmatsu India LLP (DTTILLP). This material (including any information contained in it) is intended to provide general information on a particular subject(s) and is not an exhaustive treatment of such subject(s) or a substitute to obtaining professional services or advice. This material may contain information sourced from publicly available information or other third party sources. DTTILLP does not independently verify any such sources and is not responsible for any loss whatsoever caused due to reliance placed on information sourced from such sources. None of DTTILLP, Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this material, rendering any kind of investment, legal or other professional advice or services. You should seek specific advice of the relevant professional(s) for these kind of services. This material or information is not intended to be relied upon as the sole basis for any decision which may affect you or your business. Before making any decision or taking any action that might affect your personal finances or business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person or entity by reason of access to, use of or reliance on, this material. By using this material or any information contained in it, the user accepts this entire notice and terms of use.

© 2021 Deloitte Touche Tohmatsu India LLP. Member of Deloitte Touche Tohmatsu Limited