drimcgrawhill_platts_oilgram price report nov 96

TRANSCRIPT

A daily international oil/gas market report. Established in 1923. Published by The Commodities Division of Standard & Poor's.

Oilgram Price Report PLATT'S INDEX

Volume 74, No. 219 Jet Kerosene Gasoline G m i l Monday, November 11,1996 142.071' 0.99 131.601' 1.49 149.251' 1.77 Prices Effective November 8,1996 Page 1 Naphtha Resid Atlantic Sweet Crude

147.661' 1.99 193.241' 2.09 143.38 1' 6.90

Med Sour Crude PGlAsia Crude 146.051' 8.16 149.91 1' 2.02

US. Pi eline Crude 138.7211. 5.27

Canadian ship historic IPL no New York--Canadian crude shippers will seek National En- ergy Board approval for a re- turn to historic nomination limits for December apportion- ment on the Interprovincial PipeLine, a slupper said No- vember 8.

The move has earned sup- port from between 80% and 90% of Canadian light crude shippers, one source said. The action was called for after No- vember apportionment for lights reached 39% on lines 2 and 13, he added. "Apportion- ment would blow up to over 50% if nothing is done," an- other shipper said.

Although contingent on a final go-ahead from the NEB, historic nomination limits would require that shippers nominate no more than the av- erage amount of crude they moved to the IPL for the past four months, a shipper ex- plained.

Originally, maximum nomi- nations were to be based on the shippers' throughput highs but

pers seek nination limits

maximums kept to average crude movement, apportion- ment was expected to be 7% for light sweet and sour and medium sweet crude, Traders attributed current over-nomi- nation to "game-playing" and other market factors.

With typical seasonal de- creases in product demand, less crude throughput at Edmonton refineries has led to an increase in the amount of crude that ship- pers want to get out of Alberta, a shipper said. More of those ship- pers havetumedtoIPLasTrans- mountain PipeLine is "full like never before," a shipper said. Transmountain ships crude west, out of Alberta.

The return to historic nomi- nations for December will likely take place, a shipper said. There was said to be little industry opposition. At this point, shippers said they do not see aneed for the historic limits beyond December.

Light crude apportionment was originally issued at 33% for November but was increased bv

apportionment levels would a further 6% apportionment at have remained in the double dig- 1 Superior on Lines 5 and 6a on its, he said. With nomination Continued on page 4 . -

1 Holiday Note: Asia Because of a public holiday November 1 1 (OPR November 12, 1996 issue), there will be no Platt's Asia-Pacific crude assessments or products assessments for Singapore, Japan, the

BP to close Lima, Ohio plant after "unacceptable" bids London/New York--BP re- ceived only three bids for its Lima, Ohio refinery and all were "unacceptable," a BP spokesman said. "The sales process ...y ielded only three bids and all of them were unac- ceptable," he said.

The company said it would take up to two years to close the plant because it would take that long to arrange new supply sources. "The company will ... continue to refine crude oil while it pursues other options for supplying products to the mar- ketplace," BPsaid in a statement. "This process is expected to take about two years."

But while the company has now said it will close Lima, this did not mean that a new offer for the plant would automat- ically be rejected, a source close to the refinery said. "BP

will still entertain offers," the source said. "They've not closed the door. They've just stopped the act of marketing."

BP plans to turn the Lima refinery into an oil storage ter- minal when operations at the plant are suspended in two years' time, a spokesman said.

The suspension of refining operations at Lima would not affect BP's plans to upgrade its other Ohio refinery at Toledo, the spokesman said.

The closure of the Limaplant is expected to have a positive impact on the US Midwest mar- ket, Oppenheimer analyst Asit San said. "It will have apositive impact on operators in (the Mid- west)," he said. "Whenever you have conversion capacity com- ing out of the system it gives such apsychological boost to the

Continued on page 4

NYMEX contracts gain on technicals and heating oil New York--Energy markets made major gains on techni- cals and strong heating oil prices in mostly thin volume trade Friday on the New York Mercantile Exchange. Late short-covering and market talk sent crude and product prices even higher during the after-

noon, a trader said. Friday marked the first time

in recent trade that December crude was able to maintain support above $23.00, a trader said. Traders considered $23.00 a "bellwether" of mar- ket strength, he said. Energy

Continued on page 4

Copyright 0 1996 The McCraw-Hill Companies, Inc. All rights reserved.

c Page 2 Volume 74, No. 219 Platt's Oilgram Price Report Monday, November 11,1996 Prices Effective November 8,1996

~ quiet but steady buying interest the market was recovering. MARKET BY MARKET wasreportedintoGreece. I Trade was also heard on

Asia: Tight mogas Xghtness in November to early December boosted prices in the Singapore high RON unleaded gasoline market. Sources said some traders were short- cov- ering into Taiwan, and some refiners in Australia also were sourcing barrels to meet firmer demand.

In Singapore, a bid was seen at $24.90/bbl FOB for 95 RON unleaded loading December 3- 7. There was no selling interest.

The open-spec naphtha market was active for second half January and forward- month spreads. Second half January deals were done in range of $213.50-214.50/mt. A

upplies buying two January cargoes at a mean plus $1.50/bbl.

In Singapore, a trader of- fered 130,000 bbl loading No- vember 23-27 at $30.30 and then at $30.40/bbl. Bidding for 100,000 bbl was heard at $30.05/bbl.

A Singapore based trader bought additional parcels of gasoil in an active market. In- itially, atrader offered 150,000 bbl loading November 26-30 at $30.40/bbl, with two traders bidding at $30.30 and 30.40hbl for three 150,000 bbl parcels. A parcel was sold at $30.35/bbl loading November 26-30 and two Darcels loading

second half Decembedfirst November 23-27 and Novemy

Barges were heard trading i straight run at a $3 premium to 1 at November flat for Rotter- the means formula.

dam refinery and November minus 50 cts €or Amsterdam storage material.

High sulfur cracked fuel oil cargoes were marked un- changed in NWE as higher swap values left physical play- ers unimpressed. In the Med, there were bits and pieces of spot-related trade and the pre- miums achieved suggested that

Low sulfur cracked was clearly stronger with negotia- tion heard inNWE at $123.50- 124.00 FOB and a growing conviction among traders that Med demand was kicking in.

High sulfur barges traded very early at $107.50 FOB ARA before swiftly moving up to $1 10 FOB ARA and ending the day some way above this.

MTBE: Limited interest Despite gasoline's stronger ' prompt buyerindicating86cts. showing on the NYMEX, ADecofferfor50,000bbl was MTBE buying interest re- j heard at 86.25 cts/gal FOB mained flat. USG.

Friday morning, a prompt In New York Harbor, 10,ooO bbl parcel was sold at ~ sources reported decreased 86.50 ctdgal FOB US Gulf. No I blender demand due to re-

ber 30-December 4 were done , other deal; were confirmed dox. ~ duced gasoline supplies for ~ at $30.60/bbl. I November offers were re- blending. An any November

ported at 86.25-86.50 cts/gal deal was done at 90 &gal I FOB USG with most bids be- FOB NYH for 10,000 bbl, pro-

Paper was moderately ac- tlve at around $29.65/bbl for

first half January at $216.00- 1 December. 217.00/mt. Second half De- Singapore fuel oil prices cember was assessed at drewstrengthonstrongbuying $21 8.00-219.00/mt.

1 low 86 ctdgal, except for one ' ducer to blender.

US Crude: Sweets stay popular ' interest. Inthephysicalmarket, 1 Us Gulf Coast sweet crude

a trader sold a 20,000mt 180 grades gained while sour

half January spread was done at plus $2.00/mt. At the close, second half January was talked at $215.00-215.50/mt. with

The Singapore paper market edged up with November trad- ing at $22.05-22.10. December [email protected]/bbl.

The jet kerosene market was active. A 35,000mt cargo was heard sold into South Ko- rea at close to a $1.50/bbl pre- mium. A cargo was heard sold into the Shanghai market at a $1.55/bbl premium. A Japa- nese refiner was also heard

CST cargo at $119.25/mt for November 26-30. A second trader bid at $119.00/mt for November 29-December 3. The fuel oil swaps market opened unchanged from late Thursday, but later rose with November trading at $1 18.50/mt and $119.00/mt. December traded at $117.75/mt and 118.00/mt.

Europe: Gasoil strength Gasoline barge markets ended 1 up more slowly, with trades the week on a more subdued notedupto$212.50CIFNWE. note. The bulk of business on premium unleaded was con- cluded at $218-219 FOB. One deal was heard for Rotterdam refinery material at $220 FOB early in the day, while full ARA material was talked at much lower numbers.

On cargoes, further players were heard trying to move bar- rels transatlantic as the arbi- trage began to look more attractive.

Naphtha price ideas edged higher. In the north, pipeline spec for delivery by November 20 was bid at $221 CIF NWE, while a Greek cargo was indi- cated at $224 CIF.

November swaps climbed steadily to close at around $221 CIF NWE. December moved

Jet barges were active with trade reported at stable levels. Ex-Antwerp, 2,300mt was done at DecemberlPE gasoil plus $3 1 for loading next week, whileDt- cember plus $32.25 was done FOB Rotterdam for 5,200mt loading November 12- 15.

grades grdually slipped in oth- erwise quiet trade, sources said Friday.

Sweet grades like LLS and HLS remain popular and buy- ing interest Is still steady, said a trader. December LLS was heard done at 65,67, and 68 cts over Cushing WTI.

December HLS gained 2-3 cts withdealsheardat71,72,and 73 cts over Cushing WTI. De- cember Midland was hearddone at 1 and 2 cts over Cushing WTI.

Sales from the Strategic Pe- troleum Reserve, meanwhile, may not create huge price drops but the ongoing process places pressure on markets, said a trader. December WTS was heard done at $1.60 and $1.61 undercushing WTJ. De- cember Eugene Island was

$1.80,1.81,1.82, 1.90,and 1.92. Rumors of a Cusiana and a

Vasconia deal were unconfirmed in an otherwise quiet day of Latm American trade. The last Vas- conia deal was said to be done at the $1.95-2.00 under Cushmg WTI level. Mid December Can0 Limon was heard on offer at $1.35-1.40 under Cushing WTI. Can0 Limon is called tighter be- cause it is a popular short-haul crude and competition is limit4 said a seller.

On the US West Coast, the main spot seller offered De- cember A N S at $2.00 under Cushing WTI-I0 cts tighter than previous levels--but the new offer i n not likely to change weeks of a stalemate between buyer and seller, said a trader. The last deal was nearly a month ago and since then, A N S has steadilv talked

Heitinrr oil values were bid heard doneat $1.25 under I at $2.10-2.50 under Cushinrr up, with 5ecember plus $8 heard bid CIF Hamburg, but few offers were reported. Fuel Oil Domestique was heard dis- cussed at December plus $9.50 equivalent CIF Le Havre.

EN590 was done at Decem- ber plus $15 CIF La Pallice for November 22-28 delivery. Lev- els into ARA were notionally pegged at December plus $13.50 for prompt arrival.

The Mediterranean was

Cushing WTI. December P- 1 WTI. A new bid against th; plus has been heard done at new offer was unavailable.

US West Coast: Focus on unl and jet Strengthon theNew YorkMer- cantile Exchange produced a busy market early but the pace waned later in the day. "At least there were some bids in the market," said one trader. Un- leaded was reported better bid and the range was slightly higher 58.25-59.25 cts. De-

cember unleaded was pegged 1.00 ct over November.

CARB unleaded rose and fell with conventional un- leaded. CARB unleaded prices were again pegged 4.00 cts over unleaded in Los Angeles. Bay prices were a loose 2.75 cts under Los Angeles for both

Prices Effective November 8,1996 Platt's Oilgram Price Report Monday, November 11,1996 Page 3 Volume 74, No. 219

points under the print. No.2 oil differentials re-

mained steady in November

unleaded and CARB unleaded. Portland unleaded remained quiet at around 60.00 cts.

Higher prices were seen in the jet market as NYMEX and cargo talk favored the bulls. Talk was around 67.50-68.50 cts in Los Angeles, up 0.50 cts on the day. Some traders had it pegged higher in the morning,

bulk buyer seen at $16.75/bbl, but no sellers there.

High sulfur resid swaps

considering the number of in- dividual transactions reported in the market. By noon, 32 pieces of business were re- ported for various grades of bunker fuel and for marine die- sel oil in Los Angeles, Seattle, and Portland. Values were clearly defined within surpris- ingly tight ranges, considering

ct over low sulfur No. 2 oil in the day. I Prompt November unleaded Los Angeles. Traders said prices were weakened in differential to

There were a few buyers re- higher based on stronger crude 375-425 points over the De- poedly in the portland US 1 values and healthy demand. cember print. Cash values, No. 2 oil market where the 1 Los Angeles 380 CST traded however, managed to gain

futures market, up 75 points to range tightened slightly to within $118-$121 while 180 strengthon the backofabullish 73.00-73.75 cts. CARB diesel sold about $124 and $125.

i

Premium unleaded was 325 points over unleaded.

No.2 oil values were up 100 points in cash value to 71.00- 71.25 cts, or 200-225 points

was talked 350-400 points over thepnnt. Low sulfur No.2

les after several inactive days, 1 the same levels as in Los Ange- selling at 73.50 cts. Bay CARE3 I les for 380 CST and for 180. was reported losing its grip on 1 Seattlepricesweremoreelusive,

TET propane was early at 50.75 cts, while late day trade was done at 52.00 cts and slightly higher. Offers in the Group were pegged at 52.50 cts, with afternoon bbl trading at 52.00 cts.

Purity ethane traded as high as 31.25 cts, with offers 0.25 ct higher. E/P mix was done at 30.25 cts.

Non-TET normal butane sold at 54.50 cts, with TETnor-

Chicago: Unleaded slips Unleaded differentials weak- ' strong spike in futures prices

mal butane done 0.50 ct/gal lower. Iso-butane for sale at 56.00 cts, but no deals con- firmed done. Conway normal butane moved at 54.00 cts, while iso-butane sellers were at 55.75 cts.

Non-Warren natural gaso- line was done as high as 56.50 cts, with other trades at 55.75 cts, 56.00 cts and 56.375 cts. Warren natural gasoline heard done around 57.50 cts/gal.

cycle November fell 2.00 cts to 600-650 cts over the December contract. The news plus a

cis, or 260-225 points over the December screen. Low sulfur No.2 was 350-400 points over.

Atlantic Coast: Backwardation Tight avails for very prompt product and reports that a large amount of resupply is due to hit the USAC near the end of No- vember resulted in steep back- wardation in the cash market.

Prompt RFG regular un- leaded 87 barge trade was

~ heard at 350 points over the December screen. Less prompt

The 32nd cycle unleaded dif- 1 points under. Back 33rd cycle values were pegged at 275-325 ferentials started the day trad- , unleaded was 150-125 points ~ points over. Any-November ing 325 points over the , under December, only to fall ~ tall< was at 75-100 points over December NYMEX print only back to 200- 175 points off. ' the screen. to weaken as buyers dropped RFG was quiet; pegged I New York-sized cargoes out of the market. Deals later ~ 125-150 points over unleaded. , were valued at a steep discount traded 300,275 and 175 points 1 LOW sulfur No.2 demand ~ to barges as result of back- over. In the afternoon, the mar- 1 this morning picked up in 1 wardation, Sources said. ket reversed and traded higher: I value. The back 3 1 st cycle was , Oxygenated RFG regular 225, 250 and 275 points over 125-1 10 points under Decem- ~ unleaded 87 barge values were the print. ber NYMEX No.2 contract. I pegged at 450-500 points over

Front 33rd cycle weaker I The back 32nd cycle was 160- ~ the print, Front November with trade done 75, 50 and 25 140 points under. , RFG Boston unleaded cargo

~ sellers wanted 450 points over. Back November values were

Contract spot ~ pegged at 300-375 points over. ctslgal Houston 74.25-78.50 +68.25-68.75+ Conventional regular un-

E. Chicago -75.75-82.00 +72.00-72.2~+ leaded87bargeofferswereat300 Linden -75.75-81.25 +70.75-71.00+ points over the December print Los Angeles 79.25-84.25 +67.50-68.50+ ~ for very prompt bbl. Less prompt Denver 83.00-83.75 ~ talk was at 225-250 points over Tulsa -78.00-84.00 +71.75-72.25+ ' the screen. Trade was reported for Pt Everglades +69.00-69.50+ , 200,000 bbl at 50 points over the San Antonio

1 Despite forecasts for a cold Boston 8 1.50-84.00

I snap in the Northeast, No.2 oil

i US Gulf Coast: Weaker deltas

Jet Fuel Prices

-76.25-78.50-

-73.00-79.50 December screen. Alaska 83.25-88.25

Effective November 8

trade was thin. Prompt No.2 oil barge offers weakened to 35 points under the December print. Bids were located at 60 points under. Front November Boston No.2 cargo values were pegged around 45-75 points over. Back November sellers were at 90 points over with bids at 55 points over.

Low sulfur No.2 oil trade was reported earlier at 200 points over the December print. Offers weakened to 180 points over later. Bids were at 155 points over. Off-line 54 grade talk was heard at 175- 200 points over the N0.2 print.

Bunkers were higher, with IF0 380 at the end of the day topping off at $125/mt, ex- tremely strong.

High sulfur resupply was bid at $17.75/bbl or higher for good quality material, for barge volumes.

The 2.2%S market was quiet, bids seen as high as $19/bbl, although a seller with Caribbean barrel might have done lower levels, for a barge or cargo.

One percent was talked markedly higher by some, a buyer seen in the high $19/bbl

Continued on page 4

I

range, for end November bar- rels; another physical seller was only able to get a floating deal.

Note to readers: FOB Med Naphtha

There was a sale made of 0.3%SHP, 100,000 bbl at 21.50/bbl, and 0.3%SHF' was bid at $22.50/bbl.

Effective January 1, 1997 Plunk will amend its methodology for the naphtha FOB Mediterranean assessments. FOB values will be assessed as a differential to CIF Med assessments using a freight value between Alexandria and Laveracalculated using Plattk cross Med clean tanker assessments plus 10 worldscale points for naphtha tonnage and a further $3/mt for port and associated costs. For historical analysis showing the possible impact of this change, please fax Chris Judge/Sharon Young, Fax: +44 181 545 6172.

The dated Brent market ap- pared to rebound Friday, with a November 22-24 cargo sold at

In Dubai, January Brent/Dubai ended at $1.93- 1.95. A bid appearedin late trade

cargoholders quickly adjusted their offers to reflect the new level. Dated Brent was sold down to December minus 57 cts this week, as the North Seamar- ket struggled to place several end November grades. Separately, a November 21-23 Brent was head sold dated-related.

There were still signs of pressure on some markets. One million barrels of November 20 Ekofisk was sold at dated plus 5 cts Friday, with rumors of another Ekofisk sold at dated plus 2 cts Thursday.

Flotta also appeared weaker, with a November 24- 26 cargo moved at dated minus 80 cts, following a deal the day before at dated minus 78 cts. November 20-22 Statfjord was heard traded at dated plus 7 cts.

Fifteen-day Brent outright levels moved higher, with De- cember Brent cargoes sold al $23.20, $23.30 in the US after- market. DecembedJanuary traded at plus 40 cts. Novem- bedDecember became very notional, with value pegged anywhere between minus 1.5 cts to flat.

levels indicated crude would

cts, but disappeared ;he; an of- fer came in at that level.

Urds prices in the Mediter- ranean were again marked higher as a 135,000mtNovem- ber 15-17 cargo moved be- tween traders at datedminus 74 cts and end-November 60- 80,OOOmt piece was sold to a refiner at the same level. Some end-users expressed surprise at these prices, but anotherpoten- tial seller indicated his offer Monday would come in at above dated minus 70 cts.

Iranian grades moved up in sympathy, but no other deals were reported.

UralsinNWEwasalsoquiet, with some traders arguing that prices theE should move up af- ter bad weather in the Baltic re- gion delayed some loadings, but this was hard to square with the weakness shown in alternatives such as Flotta.

West African markets were quiet, with traders focusing on a possible recovery by Cabinda. There were rumors that a late December Cabinda was sold at dated minus $1.40 Friday. But most players said

this weekend, a trader said. Un-

c

that earlier cargoes were Val- 1 spite thin buying interest. Buy- ued at cheaper levels. i ers viewed both light and me-

One trader noted that, while dium crude under downside Far East demand had in- pressure and adopted a "wait creased, USG demand re- ~ andsee'lattitude. mained lethargic. There are several cargoes of West African crude said to be on offer in the USG, including Brass River and Qua Ibo.

The Far East crude market was reported quiet Friday. Sell- ers were generally not willing to move down their offers de-

Two Japanese trading houses still targeted to sell De- cember Minas at ICP plus 41- 45 cts. In the light crude market, a Japanese trading house was seeking to sell close to 500,000 bbl of the second half of December Tapis with no firm indication yet.

BP. ..Continued from page 1 market."

BP's announcement was "no surprise to the market," San said. "Refining margins are so depressed so they couldn't find a buyer willing to pay a price acceptable to them."

The decision was part of "longer term trend," San sug- gested. "We predict more con- solidation i n the longer te rm... more capacity will be

taken out of the system and there will a drive towards more efficiency. "

Low refining margins have forced refiners to either aggres- sively cut costs, make acquisi- tions at "rock bottom prices," or follow BP, Elf, Chevron's example and consolidate, he said. "More refiners will at- tempt to reduce exposure to the refining business."

maintain support above $23.00, the same trader added.

Market talk of apossible oil workers' strike in Venezuela has been supportive, a trader said. Reports that an Illinois state circuit court judge had re- fused to order the closing of a Clark refinery following a court order were somewhat bearish, he said. But with De- cember crude at such suppor- tive levels, products did not come off on the reports on

leaded, which had been the weakest of the complex in re- cent trade, retraced upward as part of a "buy-back'' or correc- tion, he said.

Although trading activity picked up during the afternoon, volume was said to have re- mained thin. December crude closed up 85 cts at $23.59. De- cember unleaded closed up 1.47 cts at 65.27 cts. December heating oil closed up 2.04 cts at 68.93 cts.

Closing Commodity Levels Change Change Change Total Volume

$/Bbl NYMEXCrude Dec 23.59 +0.85 Jan 23.39 +0.76 Feb 23.06 +0.70 105,277 NYMEX Sr. Crude Dec n.a. n.a. Jan n.a. n.a. Fe b n.a. n.a. n.a. IPE Crude Dec 22.98 +0.77 Jan 22.60 +0.71 Feb 22.10 + O S 9 37,738

c/Gal NYMEX No. 2 Dec 68.93 +2.04 Jan 68.68 +2.06 Feb 67.08 +1.96 30,453 NYMEX NY Unl Dec 65.27 +1.47 Jan 63.56 + IS7 Feb 63.16 + I S 7 30,445 NYMEXGC Unl Dec n.a. n.a. Jan n.a. n.a. Feb n.a. n.a. n.a.

$/MT IPE Unl Nov n.a. n.a. Dec n.a. n.a. Jan n.a. n.a. n.a. IPE Gasoil Nov 219.75 +1.00 Dec 21 1.06 +1.25 Jan 206.75 +1.25 23,628

Prices Effective November 8, 1996 Platt's Oilgram Price Report Monday, November 11, 1996 Volume 74, No. 219 Page 5 - -. J

U.S. Tank Car Truck TransDotl Wholesale prices, FOB refineries, pipeline terminals and inland water- way barge terminals. At most points bulk consumer prices are slightly

above reseller postings. Discounts or temporary allowances which may be offered by individual companies are not included in posted prices.

- 1 - - - - _ _ _ _ - _ _ _ _ - ~~-~

PAD1 Regular ConvenJionai- ~ ~

MetroNY * N New Jersey* Albany(d) Atlanta(d) Baltimore* Rnctnn*

Unleaded Midg rade Premium Kerosene Unleaded ~ - N o l F u e l - ~ ~-~ - ~-~

87 65-87 65 +77 85-77 85+

+71 75-75 25 +73 85-81 40 +77 00-80 95 +69 25-71 75 +68 20-69 85+ +7 I 00-72 IS+ -73 70-80 35+

+81 15-88 50

Diesel No.2 Fuel

-69.90-71.65+ +7 1. 15-7 1.65+ +70.25-70.65+ +66.85-67.95 +67.60-69.30+ +70.50-75.00

Low Sulfur No. 2 Diesel +72.35-73.25+ +73.00-73.85

-68.90-70.95 69.85-71 .00

.~

-71.80-73.25

+73.40-78.75 ---.".. Charleston +69.50-70.70+ +72.05-73.50+ +77.00-78.20+ -77.45-77.45- -70.45-71.55 Greensboro,NC +69.20-70.85+ +72.00-73.20+ +76.15-81.35+ +73.55-78.25 +67.05-68.90+ -69.10-71.25

New Haven* +77.15-82.15+ +70.30-71.00- +72.90-73.20+ Norfolk +68.90-71.60 +7 1.62-75 .75 +76.70-81.60 +67.25 -69.25 + +69.60-7 I . 2.5 Philadelphia* 74.00-74.80+ +67.75-69.05+ -69.75-?1.20+ Pittsburgh +69.44-71.45- +72.30-75.45- +77.61-80.45- -79.15-79.15- +69.35-69.60+ +73.20-74.31-

Savannah +70.65-70.90+ +73.29-73.60+ +78.20-78.60+ 7 1.10-71. IO -7 I . 10-72.10 Spartanburg +68.90-71.35+ +7 1.65-72.25+ 74. 15-81 .35+ +66.85-68.90+ -69.00-71. 10 Tampa +68.85-72.15+ +7 1.40-75.15+ +76.35-79.65+ +67.75-68.70+ -69.10-72.35+ Wilmington,NC +69.50-69.50+ +72.75-72.75+ +76.50-76.50+ -71.25-71.25- -71.00-71 .00-

Miami +69.80-72.05+ +72.80-75.05+ +76.30-80.30+ +69.90-72.05 +7 1.20-73.00+

Portl and,ME 70.70-70.90 74.10-74.40 80.70-80.90 +81.35-81.35+ +69.75-75.20 77.75-77.75

PAD2 Chicago Columbus Des Moines(d) Detroit Mpls/St.Paul(a,d) Oklahoma St.Louis

74.75-74.75 77.95-77.95 82.75-82.75

-72.75-75.70 -79.75-82.95 74.15-76.75+ 77.30-79.75+ 82.15-86.10+

-73.15-77.35+ -76.30-80.35+ -80.65-86.70+ -73.45-78.75- +83.10-83.75- -70.25-72.25 +74.25-74.45 +77.75-79.25 +7 2.80-74.75 + +80.55-82.70+

No.6 Fuel 35.00-42.00 +71.75-71.75+ +73.40-73.55

+7 I.S0-73.15+ +73.90-77.80- 75.00-76.50+ +76.50-78.30+

+70.75-70.75 +72.90-76. 15 3 8.00-40 .OO -73.95-77.20+ -75.95-79.20+

+72.35 -72.68- +74.17-75.50- +70.90-73.35+ 71.85-76.80+

PAD3 81.05-82.00 AI buquerque(a,d) -74.40-82.00- -83.90-90.50-

Amarillo 71.40-71.40 75.40-75.40 79.40-79.40 +76.35-76.35+ Arkansas +72.55-75.10 +75.45-77.85 +80.00-81.80- +68.90-68.90+ +72.60-76.25 Binningham +67.90-70. 10 +7 1.60-73.90 -73.85-81.10 +66.95-70.75+ -68.60-69.50- Corpus Christi(d) +66.70-67.60+ +70.00-71 . I O + +74.70-77. IO+ +65.40-66.30 66.30-69.00 Dallas/Ft.Worth(d) 7 I . 10-72.50 80.50-80.60 +68.65-68.65+ +67.55-70.60- Houston(d) 69.10-69.10 72.60-72.60 78.60-78.60 +65.70-68.00 67.15-71.40 N .Orleans Area(d) +67.80-68.85 +70.35-72.85 +74.55-78.35 +66.30-66.45 -67.55-69.90+

PAD4 87.75-88.95 Billings -8 I .S0-8 I .SO- -93.00-93 S O

Casper 8 1.75-82.10- 90.25 -9 I . 85 - 85.75-86.15 + Denver +72.45-73.50 7.5.45-76.50 +81.20-82.00 +76.05-76.05+ +76.75-77.75+ Salt Lake 73.75-74.20 83.75-83.95 -79.75-79.75- -84.00-84.25-

PAD5 Los Angeles(a,e) Phoenix(a) Portl and, OR (a) S anFran -EB ay ( e ) Seattle/Tacoma(a) Spokane(a)

6 1.50-62.25+ 65.50-66.25+ 70.50-72.25+ 64.25-73.00 68.25-77.00 75.25-83.00 6 I.SO-69.2S 73.50-81.25 60.00-60.75 + 64.00-6475+ 70.00-70.75+ 60.50-60.50 72.50-72.50

-7 I .70-77.60 -76.20-76.20- -83.45-88.60

-80.50-81.00- +78.00-78.50+

-73.25-75 .OO 74.00-75.00- -71.75-71.7s- 73.00-73.00

82.50-82.50 83.00-84.20

(a)=Includes oxygenated gasoline. (b)=lncludes low sulfur kero. (c)=Includes 7.8 RVP. *Conventional gasoline no longer at the location. (d)=Includes branded gasoline. (c)=CARB gasoline.

Reformulated Gasoline Unleaded Midg rade Premium

~

MetroNY(a,d) 72.90-74.75- N.New Jersey(a,d) 72.05-75.41+ Albany +7 1.25-7 I .25+ R al ti more -68.60-71.10- Boston +70.25-72. 15 New Haven(a) 71.00-72.30- Norfolk +70.25-73.80+ Philadelphia +70.05-70.70 Pottland,ME(d) 7 1.70-7 1.70 Chicago +8 1.05-82.75 Dallas/Ft.Worth(d)t69.00-70.40+ Houston +68.80-69.20+ (a)lncludes oxygenated gasoline. (

~- ~~

77.10-77.25- 75.10-78.91+

+73.80-73.80+ -7 1.60-73.55- +72.20-75.55

74.50-75.7s- +73.00-77.85 +72.65-74.80

74.90-75.20 +83.86-83.86+ +72.25-73.40+ +72. IO-72.45+

d)=Includes branded gar

Unleaded~_- ~

79.05-81.91+ -82.75-82.90-

+76.55-76.55+ -74.25-77.80- +75.65-82.15 -79.30-81.25- -75.90-83.70 +76.70-79.70

80.80-81.70 +88.55-90.75 +77 .00-79.90+ +76.40-78.20+

;oline.

Qatar issues October crude prices Singupore--Qatar General Petroleum Corp has raised its offi- cial crude prices for October by $1.36-1.37/bbl from the pre- vious month, traders said.

QGPC set the retroactive price for Qatar Land (Dukhan) crude at $23. l lhbl , up from $21.75/bbl for September, while Qatar Marine was set at $23.03hbl, up from $21.66/bbl in September.

The retroactive price for Qatar Land crude marks a 6 1 ctshbl premium above the Oman MPM price, while Qatar Marine reflects a 53 ctshbl premium above Oman MPM. In Septem- ber, the premiums over Oman MPM had been 55 cts/bbl and 46 ctshbl for Qatar Land and Marine, respectively.

Volume 74, No. 219 Page 6 Platt's Oilgram Price Report Monday, November 11,191 Prices Effective November 8,1996

Five-Day Rolling Averages * GasoilIHeating Oil $lBbl clGal Singapore 30.06--30.18 7 I .57 **7 1 .86 Arab Gulf 28.59-28.67 68.07**68.26 W.C. cargo 27.48--27.88 65.43**66.38 L.A. LS.2 27.93 **28.35 66.50-67.50 S.F. LS.2 27.95 *'28.37 66.55-67.55

0.2 CIF ARA ENS90 CIF ARA 0.2 Rotterdam Barge 0.2 FOB NWE 0.2 CIF MED EN590 CIF MED NY Cargo NY Barge US Gulf Water US Gulf Pipe Grouo 3 Carid cargo NYMEX NO. 2

$IMT 21 3.00--214.80 224.10--226.00 21 1.80--212.50 204.00--205.80 21 1.00--213.00 223.40--227.40 206.80**207.59 207.59**208.37 194.81 **195.73 193.73**194.96 212.98**213.91 196.85-197.78 208.73

clGal 68.05 **67.76 7 1.60**72.20 67.67**67.89 65.18**65.75 67.41 **67.19 71.37**72.65 65.65-65.90

63.25-63.55

69.15--69.45 63.30**63.60 66.26

65.90--66.15

62.90-63.30

Naphtha $/Bbl cIGal Singapore 22.06--22.16 52.52**52.76

QMT clGal Japan c/F 212.40--214.20 56.19**56.67 Arab Gulf 187.87--189.67 49.70**50.18 CIF NWE Physical 218.20--220.20 57.72**59.51 Rotterdam Barge 215.20--217.20 56.93 **58.70 FOB Med 197.60--199.60 52.28**53.95 CIF Genoa 214.60--216.60 56.77**58.54

Carib Cargo 223.97--225.97 61.70**62.25 US Gulf W 238.65**240.69 64.50--65.05

Jet Kerosene $IMT c1Gal ClF NWE Carzo 237.30- 239.30 71.91**72.08 Rotterdam Barge FOB Med US Gulf Water US Gulf Pipe Carib Cargo NY Cargo LA Pipeline Group 3 Chicago

24 1.50--242.50 219.30--221.30 21 9.29**220.28 21 9.29**220.28 216.29--217.26 223.41 **224.24 21 2.77**216.28 228.25**229.25 227.92**228.9 I

73.18**73.04 66.45 * * 66.66 66.05--66.35 66.05--66.35

67.70--67.95 66.70--67.80 68.75--69.05 68.65--68.95

66.96**67.26

Gasoline,lntl. Market c/Gal Prem $/Mt CIF ARA 0.15 66.04**66.89 23 1.80--234.80 Rotterdam Barge 0.15 FOB NWE 0.15 FOB Med 0.15

64.10**64.90 225.00--227.80 63.19**64.05 22 1.80--224.80 63.70**64.56 223.60--226.60

CIF Med 0.15 66.55**67.41 233.60-236.60

Atlantic & Gulf Coast Resid New York Albany

Baltimore Boston

Charleston Jacksonville

Mobile New Haven Norfolk Philadelphia Portland Providence Tampa Wilmington

0.3% 1 .5 1.7 I .o 0.5 1 .o 2.2 I .7 I .7

1 .o 1.7 0.5 1 .s 1 .o 0.5 1.7

No. 4 Fuel 29.90-30.30

-27.65-28.95 28.15

-27.25-29.00 32.25-34.50 31.00-33.25

-26.60-26.60- -26.85

-27.85-3 1.25 -26.60-31.25 25.25-28.35- 32.25-33.20 29 .OO-33.25 21 .oo

-26.60-28.00

0.3% I .5

1 .o 0.5 1 .o 2.2 2.1 1.7 2.5 2.2 I .o 2.1 0.5 2.5 1 .O 2.5 2. I

No. 6 Fuel 27.20-27.85- 25.95-28.55

-24.35 -25 S O 26.50-29.95 25.00-28.00 22.75-25.00 2 3 . 5 2 3 . I 5 23.05 22.55-22.55 16.50

-24.80-26.00 24.95-26.50 22.75-26.05- 24.00-27.25 25.00-28.00

23.15-24.15 18.40

Gasoline, U.S. Market Unleaded Premium 65.20--65.60 70.40--70.75 NY Cargo

NY Barge 65.9.5-66.40 US Gulf Water 65.50--66.90 67.7569.15

70.90-71.25

67.35--68.75 US Gulf Pipe 65. IO--66.50 Group 3 68.55--68.90 72.35-72.70

63.25.-64.25 LA Pipeline S 8.80--59.80

Gasoline, U.S. Market Unleaded Premium NY Cargo 65.20--65.60 70.40--70 75 NY Barge US Gulf Water US Gulf Pipe Group 3 LA Pipeline

65.9.5-66.40 70.90--71:21 65.50--66.90 67.7569.15

67.35--68.75 65. IO--66.50 68.55--68.90 72.35-72.70

63.25.-64.25 S 8.80--59.80 SF Pipeline 56.3.5-57.40 61 60.42 64 Chicago 70.25--70.55 72 go--% iS NYMEX Unl 64 35

Low Sulfur Resid Fuel Oil $IBbl $IM t Singapore LSWR Mixedcracked 18.08--18.19 121.14** 121.87

19.75** 19.91 126.40- 127.40 CIF ARA 1 % Rot Bar 1% 19.03** 19.05 12 1.80--123.80 NWE FOB 1% 18.66** 18.52 119.40--120.40 MedFOB 1% 18.64**18.66 119.30--121.30 NY Cargo .3% HP 21.01--21.26 140.77** 142.44 NY Cargo .3% LP 22.55 -22.80 151.09**152.76

126.30** 127.92 NY Cargo .7% Max 19.43-19.68 NY Cargo I% MU 19.27--19.52 125.26** 126.88

18.25--18.50 116.62**118.22 US Gulf .7% 17.80--18.05 113.74**115.34 US Gulf 1%

Hi Sulfur Resid Fuel Oil $/Bbl $lMt Singapore 180 17.85**17.98 116.00-- 116.90 Singapore 380 17.34** 17.48 111.00--111.90

17.52**17.64 110.40--112.00 CIF ARA 3.5% NWE FOB 3.5% 16.25** 16.38 102.40-- 104.00

CIF Med 3.5% 18.61 -- 18.86 119.10**120.70 NY Cargo 2.2% 17.05--17.40 109.12**11 1.36 NY Cargo 3.0%

US Gulf 3%; I 6.22-- 16.47 103.81 ** 105.41 17.5 1-17.76 112.06**113.66 Carib 2.0%

Carib 2.8% 16.20- 16.53 103.68**105.79

Arab Gulf 180 16.77**16.91 107.35--108.25

Med FOB 3.5% 16.87**17.06 106.30--108.30 18.52** 18.69 116.70--118.70

Crude Oil, FOB Source $lBbl West Texas Int 22.77--22.80 NYMEX Crude Brent (DTD) Brent (First Month) Dubai Iran (Sidi) ANS (California) WTI Posting Plus

22.78 21.81--21.85 22.20-22.25 20.36-20.45 19.93--20.03 20.45--20.52

1.94 -1.96

*Five Days ending November 7 Conversions either side of asterisks

Contract Cargo Prices No. 2 Fuel Barge clGal 77.50-78.75(a)

No. 6 Fuel Cargoes $/Bbl Company EffDate 0.3pct O.5pct I.0pct 2.2pct 2.8pct

Coastal 10/08 27.25 26.75 25.25 22.00 20.75 Global 09/20 29.00 28.00 27.00 21.75 20.55 Hess 05/10 25.00 23.50 23.00 Apex 06/18 18.50 17.50 Sprague 06/24 26.50 25.50 Northeast 11\04 28.00 27.25 25.50 28.25 Ranges(b) 0.3pct 27.25-28 .OO 0.Spct 26.50-27.25 I .Opct 25.25-25.50 2.2pct 21.75-22.00 2.8pct 20.55-20.55

All prices delivered, N.Y. Harbor. Residual fuels are low pour. (a)Barge prices, FOB Terminal. Some suppliers grant TVAs. (b)Ranges excluded low and high for each grade.

I

Prices Effective November 8,1996 Platt's Oilgram Price Report Monday, November 11,1996 Volume 74, No. 21 9 Page 7

Spot Crude Price Assessments International $/Bbl Brent(N0V)

Brent(DEC) Brent(JAN) Brent(DTD) Forties Ekofisk Statfjord Oseberg Flotta Forcados BQ Cabinda

+23.14-23.25+ Dubai(DEC) +23.26-23.28+ Dubai(JAN) +22.86-22.88+ Dubai(FEB) +22.90-22.94+ Oman(DEC) +22.95-23.04+ Oman "MPM" +22.95-23.04+ Ural (Med) +22.97-23.04+ Ural (Rdam) +23.12-23.18+ Es Sider +22.09-22. IS+ Iran Lt(Sidi) +23.41-23.47+ Iran Hvy(Sidi) +23.30-23.39+ Suez Blend +21.18-21.24+

+2 I . 16-21.23+ +20.91-20.95+ +20.49-20.57+ +2 I .7S-21 .EO+

0.10-0.1 1 +22.15-22.21+ +22.30-22.39+ +22.95-23.04+ +2 1.67-21.77+ +21.17-21.27+ +20.75-20.84+

Canada CD$/CM US$/BBL Par Crude 18.5.75-187.75 +22.18-22.42+ Mixed Lt. Sr 170.00- 172.00 +20.30-20.54+ Bow River/ 154.00- 156.00 + I 8.39- 18.63+ Hardisty

Spot Price Assessments Latin America, FOB $/Bbl Argentina Ecuador Gasoline 84 +30.77-30.87+ FO 1S%S -18.16-18.31- Gasoil + 29.40-29.82+ FO 1.7%S -17.86-18.06- FO 0.6%S +17.96-i8.16+ Brazil Peru FO 0.4%S +20.05-20.15+ Naphtha +27.00-27. IO+ Colombia FO 0.9%S +16.98- l7.13+ FO I.S%S 17.88-17.98 FO 1.4%S +16.13-16.18+

Group Three 13.5 RVP c/Gal Unleaded +69.00-69.50+

Prern. Unleaded +7 2.25 -72.75 + No. 2 +7 1.00-71.25+ LS No. 2 +72.50-73.00+ Jet Fuel +7 1.75-72.25+

Chicago Pipeline 13.5 RVP clGal Unleaded 87 -7 1.25-71.75

Unleaded 89 -72.25-72.75

RBOB -72.25-72.75 Jet Fuel +72.00-72.25+ No. 2 +71.00-71.25+ LS No. 2 +72.50-73.00+

Prem. Unl 92 -73.75-74.25-

Gas Liquids Mont Belvieu Conway clGal Ethane +28.15-29.25+

EthandPropane 29.75-30.25+ Ethane Purity 31.00-31.50+ Propane +s 1.50-52.00+ -52.00-s2.50- Propane ' E T +5 1.75-52.25+ Normal Butane +54.50-54.75+ 53.75-54.25 Butane TET +5 4.00-54.25 Isobutane +SS.S0-56.00+ 55.25-55.75 Natural Gasoline 57.00-57.50 Natural Non-Warren +56.00-56.50+ Natural Warren +57.00-57.50+

South China,C&F South China Hong Kong $/MT

Mogas 90 0.4 G/L +223.00-230.00+ Mogas 83 0.4 G/L +215 0G-220.00+ Mogas 70 0.4 G/L +208.00-2!5.00+ Jet Kerosene -24 1.00-245.00- Gasoil UP 0.510s +234.00-236.00+ Fuel Oil 180 cst +!25.00-125.50 132.00-135.00 Fuel Oil 380 cst + 120.00- 120.50 - 128.00- 130.00 Marine Diesel -220.00-223.00

~~ ~~ ~~

U.S. $/Bbl WTI(DEC) +23.63-23.65+

WTI(JAN) +23.43-23.47+ Eugene Island +22.36-22.42+ WTI Midland +23.64-23.67+ Line 63

LLS +24.30-24.33+ Kern River HLS +24.34-24.38+ ANS(Cal) Wyo. Sweet +23.56-23.62+ P-Plus Line 63 1.00-1.05

+20.57-20.61+ 17.56-17.60 WTS +22.02-22.06+ THUMS 16.23-16.27

+21.31-21.37+

P-PIUS WTI -1.84-1.86-

Pacific Rim $/Bbl Spread Pap. Tapis(DEC ) +23.05-23.15+ Tapis +24.25-24.30 1.00-1.20 Pap. Tapis(JAN ) 22.70-22.80 Thevenard+24.70-24.75 1.50-1.60 Labuan +24.35-24.40 Griffin +23.25-23.30 0.0.5-0.15 Miri +24.25-24.30 Cossack 23.40-23.50+ 0.20-0.25 Gippsland t22.95-23.00 Kutubu 23.45-23.55+ 0.25-0.30 Jabiru +24.40-24.45 Nanhai +23.25-23.30 0.05-0. 15 Daqing +22.70-22.80+ NW Shelf +23.10-23.20+ 0.50-0.60 Shengli +21.30-21.40+

Minas +22.50-22.60+ 0.35-0.45 Cinta +21.75-21.85+ 0.35-0.45 Attaka +23.70-23.80+ 0.50-0.60 Duri +2 1.05-21.15+ 0.50-0.60 Arun +22.55-22.65+ 0.35-0.45 Widuri +21.70-21 .EO+ 0.35-0.45 Ardjuna +22.65-22.75+ 0.35-0.45 Belida +23.75-23.85+ 0.60-0.70 Handil +22.15-22.25+ 0.25-0.35 Lalang +22.40-22.50+ 0.30-0.40

Spread Vs. ICP Spread Vs. ICP

Latin America Crude $/Bbl Canadon Seco +21.18-21.25+ Escalante +20.53-20.59+

+22.18-22.25+ Loreto + I 9.33- 19.SO+ Medanito Oriente + I 8.72- 18.8 I + Cano Limon +22.13-22.20+ Vasconia +21.48-21.55+ Cusiana +23.53-23.60+

Arab Gulf, FOB $/MT Naphtha + 190.40- I92.40+

HSFO 180cst + I 10.35-1 10.85 $Bbl Kerosene 28.75-28.80

Gasoil -28.95-29.05

SingaporelJapan Cargoes C&F Japan Singapore $/Bbl Mogas Unl +26.00-26. IO+

Mogas 92 Unl ~24.15-24.20+ +25.00-25. IO+ Mogas 95 Unl

Mogas 95 Unl Pap.(DEC ) +24.80-2S .00+ Mogas 95 Unl Pap.(JAN ) +24.50-24.80+ Mogas 97 Unl +25.75-25.85+

270.00-275.00- $IMT MTBE Naphtha +215.00-217.00+ +22.40-22.50+ Naphtha 30-45 +218.00-219.00+ Naphtha 45-60 +216.00-217.00+

$/Bbl Kerosene 31.55-31.65 -30.05-30.30+ Naphtha 60-75 +215.00-215.50+

Gasoil "Cracked" -31.60-31.70 Gasoil "Pure" -32.10-32.25 Gasoil O.S%S -30.35-30.70+ Gasoil l.O%S -30.15-30.50+ Gasoil LoPr -30.35-30.70+ LSWR Mixedcracked +18.40- 18.50+ Naphtha Pap.(DEC ) +21.70-21 .85+ Naphtha Pap.(JAN ) +21 .SO-21.60+ Kerosene Pap.(DEC ) -30.10-30.20-

Gasoil Pap.(DEC ) -29.60-29.70- Gasoil Pap.(JAN ) -29.00-29. IO-

Kerosene Pap.(JAN ) -30.05-30. 15-

$/MT FO I80 cst 2% +124.00-124.50 HSFO 180cst +128.25-128.75 +1!9.00-1 19.50 HSFO 380cst + 114.00- I 14.50 HSFO 180cst Pap.(DEC ) + I I 7 .SO- 1 1 8 .OO HSFO l80cst Pap.(JAN ) +116.00-116.50

Caribbean Cargoes, FOB WMT c/Gal Naohtha +228.69-231.41+ +63.0n-A? 75s " <,.I. I J I

Jet 'Kerosene +224.25-225.88+ +69.00-69.50+ Gasoil +204.60-206.15+ +66.00-66.50+

$/Bbl No.6 2.0%S 17.6.5-17.90 No.6 2.8%S +16.65-17.15+

Volume 74, No. 219 Page 8 Platt’s Oilgram Price Report Monday, November 11,1996 Prices Effective November 8,1996

active in the marketplace All U S gasoline quotes represent nonoxygen-

An assessment of cargo and barge prices made by the Oilgram staff based Spot Price Assessments on transactions and market informa- tion from sources deemed reliable and

ated product unless otherwise-id- cated.

~ ~ ~~~

European Bulk Cargoes Cargoes CIF Cargoes Barges Cargoes FOB Med Med Basis CIF NWE FOB FOB Basis Italy GenodLavera Basis ARA Rotterdam NWE

$/MT Prem 0.15 G/L ................ -219.00-222.00- ............... -229.00-232.00- ............. -228.00-231.00- .................... 219.00-222.0 0- ........... -218.00-221.00-

Prem Unl ......................... -216.00-219.00- ............... -226.00-229.00- ............. -225.00-228.00- 216.00-219.0 0- 215.00-218.00- Reg Unl ............................................................................................................. -214.00-217.00- ................... 208.00-209.00- 204.00-207.00- MTBE ............................................................................................................................................................ .-289.00-292.00- .................................... Naphtha Physical ........... +199.00-202.00+ ............. +216.00-219.0O+ ........... +219.00.222.00+ .................+ 216.00-21 9.00+ .................................. Naphtha Swaps ................................................................................................ +2L 1.00-212.50+ ................................................................................. Jet Kerosene ..................... 222.00-224.00 ........................................................ 240.00-242.00 ................... 242.00-243.00 ............ 23 1.00-233.00 Gasoil EN590 ................... 216.00-219.00 ................ 225.50-229.50 ............. -224.00-226.00 .................. + 23 1.50-233.50+ 215.00-217.00 Gasoil 0.2 ....................... +207.50-209.00+ ............. +216.50-218.50+ ........... +218.00-220.00+ .................+ 219.00-22 O.OO+ ......... + 209.00-21 1.00+ 1 % Fuel Oil .................... +122.50-124.00+ ............. +132.50.134.00+ ........... +129.50.130.50+ .................. 121.00-123.00 ........... + 122.50-123.50+ 3% FuelOil ........................................................................................................ 109.00-11 1.00 ......................................................... 101.00-103.00 3.5% Fuel Oil ................. +106.00-108.00+ ............. + I 16 .00- 118.00+ ............. 109.00-111.00 .................. + 109.50-110.50+ .......... 101.00-103.00 380 CST ......................................................................................................................................................... + 11 1.00-1 12.00+ ...................................

.-234.00-237.00- ............................................................................................................................. ....................................

E4 Feedstock ......................................................................................................... 19.00-20.00 .................................................................................... M-40 Feedstock ......................................................... +15.00-16.00+ ........................................................................................................................... 0.5%-0.7% Straight Run ...................................................................................................................................................................... +141.00-143.00+

0.2 PCT Gasoil does not include -5 -15 spec.lPE Average (Nov) +220.00. IPE Average (Dec) 21 1.00+.

NewYorklBoston Cargo Barge 15.0 RVP Unl 87 +66.25-66.75+ +67.50-68.25+

Unl87 RFG +66.75-67.50+ +68.00-68.75+ Unl 87 RFG OXY +69.00-69.50+ +69.75-70.25+

Unl 87 (Boston RFG) +68.25-69.75+

Unl89 RFG +68.75-69.50+ +70.00-70.75+ Unl 89 RFG OXY +71.25-71.75+ +71.75-72.25+

Super Unl 93 RFG +73.00-73.50+ +73.50-74.00+ Super Unl 93 RFG OXY +74.50-74.75+ +75.00-75.25+

LS Jet/Kero(Boston) +72.00-72.25+

Unl 87 (Boston) +67.75-68.50+

Unl89 +69.25-69.75+ +69.75-70.25+

Super Uni 93 +72.75-73.00+ +73.25-73.50+

Jet Fuel +70.25-70.50+ +70.75-71 .OO+ LS Jet/Kero +7 1.50-71.75+ +72.00-72.25+

No. 2 +68.00-68.25+ +68.25-68.50+ LS No. 2 +70.25-70.50+ +70.50-70.75+ No. 2 (Boston) +69.50-69.75+ LS No. 2 (Boston) +71.50-71.75+ No. 6 0.3%S HiPr +21.00-21.25+ +21.25-21.50+ No. 6 0.3%S LoPr +22.50-22.75+ +22.50-22.75+ No. 6 0.7%S Max + 19.50- 19.75+ + 19.50- 19.75+

No. 6 2.2%S Max 18.75- 19.W 18.50-18.75 No. 6 2.2%S Max (Bstn) 18.85-19.10 No. 6 3.0%S Max +17.50- R O O + + 17.75- 18.00+ No. 6 I.O%S Pap. 1st M +21.00-21.25+ No. 6 I.O%S Pap. 2nd M +22.00-22.25+ No. 6 I.O%S Pap. Qtrly +20.00-20.50+

No. 6 1%S Max + I 9.25-19.50+ +19.25-19.50+

$/Bbl

West Coast Waterborne c/Gal Unleaded 87 +56.50-57.50+

Jet Fuel

No. 6 O S % S No. 6 I.O%S

$/Bbl Gasoil +66.25-67.25+ 28.00-28.40 18.50-19.00 17.25-17.75

I Superfund tax in 1996 Autliorization for the Superfund tax of 9.7 ctshbl expired as of December 31, 1995. Therefore, as of January 2, 1996 Platt’s US spot market assessment for refined products and Platt’s wholesale rack prices no longer include the Superfund tax.

US. Gulf Coast Waterborne Pipeline 13.5 RVP c/Gal

$/B bl

15.0 RVP c/Gal

Unl87 +68.25-68.50+ Unl87 RFG +69.75-70.00+ Unl89 +69.25-69.50+ Unl89 RFG +70.75-71.00+ Prem UnlY2 +7 0.25 -70.50 + Prem Unl92 RFG +71.75-72.00+

Prem Unl93 RFG +72.25-72.50+ MTBE

JetIKero 54 +68.25-68.75+

No. 2 +65.75-66.25+

No. 6 0.7%S 17.75- 18.00 No. 6 I.O%S 8 API 17.30-17.55 No. 6 1.08s 10.5 APJ 17.50-17.75 No. 6 3.0%S +16.40- l6.90+ No. 6 3.O%S Pap. 1st M 17.00-17.25 No. 6 3.O%S Pap. 2nd M 17.15-17.40 No. 6 3.O%S Pap. Qtrly 17.00-17.25 Supplemental--Northern Grade Gasoline

Prem Unl93 +70.75-71 .00+

85.50-86.50 Naphtha +66.00-66.75+

Jet/Kero 55 +68.75-69.25+

LS No. 2 +67.75-68.25+

Unl 87 RFG +69.25-69.50+

+67.75-68.00+ +69.25 -69.50+ +68.75 -69 .OO+ +70.25-70.50+

+71.2S-71.50+ +69.75-70.00+

+70.25-70.50+ +71.75-72.00+

Conventional gasoline assessments reflect the 32nd cycle. RFG as- sessments reflect the 32nd c cle US No.2 assessments reflect the 31st cycle. No.2 assessments refLct ;he 31st cycle. Jet assessments reflect the 32nd cycle.

West Coast Pipeline California c/Gal Unl87

CARB Unl Prem Unl92 CARB Prem Jet Fuel LS No. 2 CARB Diesel

$/MT 180 cst 380 cst

Los Angeles(a) San Francisco(b) +58.25-59.25+ 55.50-56.50 +62.25-63.25+ 59.50-60.50 +62.75-63.75+ +60.00-61 .00+ +66.25-67.25+ [email protected]+ +67.50-68.50+ +67.25-68.25+ +66.50-67.50+ +66.50-67.50+ -73.25-74.25 - -69 .OO-70.00- 123.00- 126.00

+ I 18.00- 121.00+

Northwest Po rtland(c) Seattl e(d) clGal Unl 87 59.50-60.50 58.50-59.50

Prem Unl92 66.00-67.00 65.00-66.00 Jet Fuel 72.00-73.00 LS No. 2 73.00-73.75- 72.00-73.00

380 cst - I 1 8.00- 12 1.00 + I 16.00-1 19.00t $/MT 180 cst + 122.00-125.00+ 1 l8.oO-l2l.00

(a)=RVP is 7.8, CARB is 11.5. (b)=RVP is 12.5, CARB is 13.5. (c)=RVP is 15.5. (d)=RVP is 15.5.

Prices Effective November 8,1996 Platt’s Oilgram Price Report Monday, November 11,1996 Volume 74, No. 21 9 Page 9

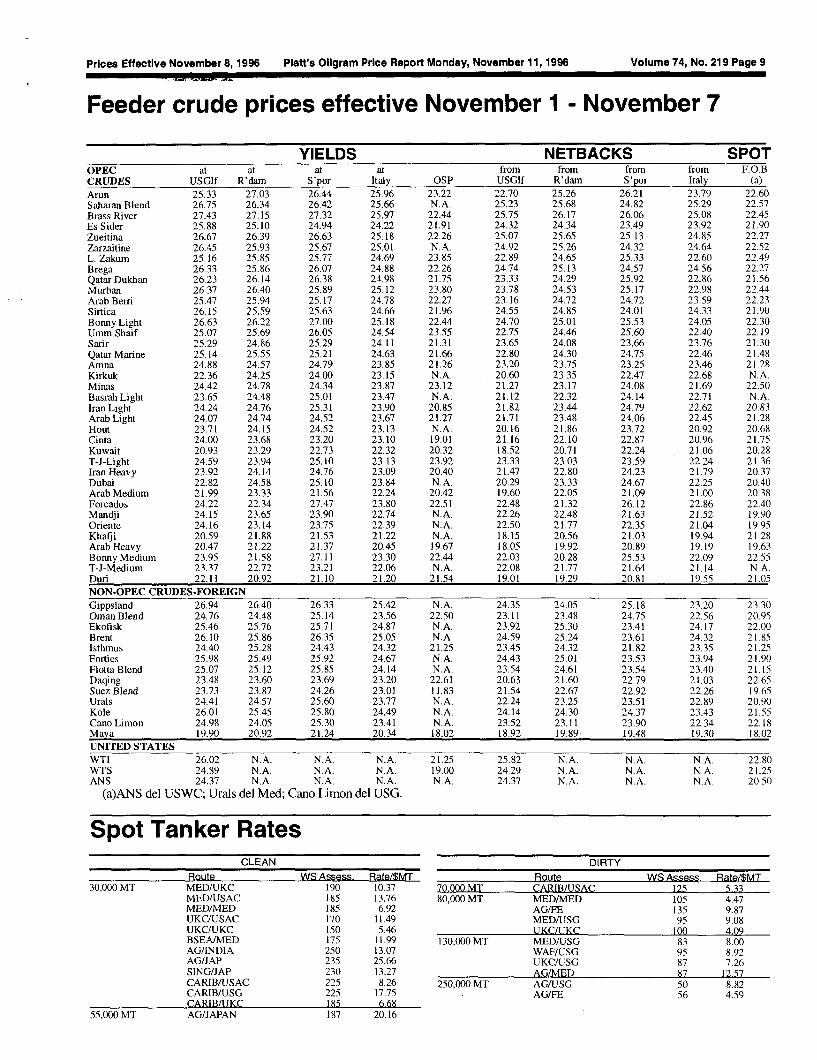

Feeder crude prices effective November 1 - November 7

NETBACKS SPOT YIELDS OPEC at at at at from from from from F.O.B.

27.03 26.44 25.96 23.22 22.70 25.26 26.21 23.79 22.60 26.34 26.42 25.66 N.A. 25.23 25.68 24.82 25.29 22.57 27.15 27.32 25.97 22.44 25.75 26.17 26.06 25.08 22.45 25.10 24.94 24.22 21.91 24.32 24.34 23.49 23.92 2 1.90

CRUDES USGlf R’dam S’por Italy OSP USGlf R’dam S’por Italy (a) Arun Saharan Blend Brass River Es Sider Zueitina Zarzaitine L. Zakum Brega Qatar Dukhan Murban Arab Bern Sirtica Bonny Light Umm Shaif Sarir Qatar Marine Amna Kirkuk Minas Basrah Light Iran Light Arab Light Hout Cinta Kuwait T-J-Light Iran Heavy Dubai Arab Medium Forcados Mandji Oriente Khafji Arab Heavy Bonny Medium T-J-Medium

25.33 26.75 27.43 25.88 26.67 26.45 25.16 26.33 26.23 26.37 25.47 26.15 26.63 25.07 25.29 25.14 24.88 22.36 24.42 23.65 24.24 24.07 23.71 24.00 20.93 24.59 23.92 22.82 2 1.99 24.22 24.15 24.16 20.59 20.47 23.95 23.37

26.39 25.93 25.85 25.86 26.14 26.40 25.94 25.59 26.22 25.69 24.86 25.55 24.57 24.25 24.78 24.48 24.76 24.74 24.15 23.68 23.29 23.94 24.14 24.58 23.33 22.34 23.65 23.14 21.88 21.22 2 1 .58 22.72

26.63 25.67 25.77 26.07 26.38 25.89 25.17 2.5.63 27.00 26.05 25.29 25.21 24.79 24.00 24.34 25.01 25.31 24.52 24.52 23.20 22.73 25.10 24.76 25.10 21.56 27.47 23.90 23.75 21.53 21.37 27. I 1 23.21

25.18 25.01 24.69 24.88 24.98 25.12 24.78 24.66 25.18 24.54 24.1 1 24.63 23.85 23.15 23.87 23.47 23.90 23.67 23.13 23.10 22.32 23.13 23.09 23.84 22.24 23.80 22.74 22.39 21.22 20.45 23.30 22.06

22.26 N.A.

23.85 22.26 21.75 23.80 22.27 21.96 22.44 23.55 21.31 21.66 21.26 N.A.

23.12 N.A.

20.85 21.27 N.A. 19.01 20.32 23.92 20.40 N.A.

20.42 22.5 1 N.A. N.A. N.A. 19.67 22.44 N.A.

25.07 24.92 22.89 24.74 23.33 23.78 23.16 24.55 24.70 22.75 23.65 22.80 23.20 20.60 21.27 21.12 21.82 21.71 20.16 21.16 18.52 23.33 2 1.47 20.29 19.60 22.48 22.26 22.50 18.15 18.05 22.03 22.08

25.65 25.26 24.65 25.13 24.29 24.53 24.72 24.85 25.01 24.46 24.08 24.30 23.75 23.35 23.17 22.32 23.44 23.48 21.86 22.10 20.71 23.03 22.80 23.33 22.05 21.32 22.48 21.77 20.56 19.92 20.28 21.77

25.13 24.85 22.27 24.32 25.33 24.57 25.92

24.64 22.52 22.60 22.49 24.56 22.27 22.86 21.56

25.17 24.72 24.01 25.53 25.60 23.66 24.75 23.25 22.47 24.08 24.14 24.79

22.98 22.44 23.59 22.23 24.33 21.90 24.05 22.30 22.40 22.19 23.76 2 1.30 22.46 21.48 23.46 2 I .28 22.68 N.A. 21.69 22.50 22.7 1 N.A. 22.62 20.83 22.45 21.28 20.92 20.68 20.96 21.75 2 1.06 20.28 22.24 21.36

24.06 23.72 22.87 22.24 23-59 24.23 24.67 21.09

21.79 20.37 22.25 20.40 21.00 20.38

26.12 21.63 22.35 21.03 20.89 25.53 21.64

22.86 22.40 2 1.52 19.90 21.04 19.95 19.94 21.28 19.19 19.63 22.09 22.55 21.14 N.A.

Duri 22.11 20.92 21.10 21.20 21.54 19.0 1 19.29 20.81 19.55 21.05 NON-OPEC CRI JDES-FOREIGN . . -. _ _ - - _ _ _ _ _ __ - -~~

Gippsland 26.94 26.40 26.33 25.42 N.A. 24.35 24.05 25.18 23.20 23.30 Oman Blend 24.76 24.48 25.14 23.56 22.50 23. I I 23.48 24.75 22.56 20.95 Ekofisk 25.46 25.76 25.7 1 24.87 N.A. 23.92 25.30 23.41 24.17 22.00 Brent 26.10 25.86 26.35 25.05 N.A. 24.59 25.24 23.61 24.32 21.85 Isthmus 24.40 25.28 24.43 24.32 21.25 23.45 24.32 21.82 23.35 2 1.25 Forties 25.98 25.49 25.92 24.67 N.A. 24.43 25.01 23.53 23.94 21.90 Flotta Blend 25.07 25.12 25.85 24.14 N.A. 23.54 24.61 23.54 23.40 21.15 Daqing 23.48 23.60 23.69 23.20 22.61 20.63 2 1.60 22.79 21.03 22.65 Suez Blend 23.73 23.87 24.26 23.01 11.83 21.54 22.67 22.92 22.26 19.65 Urds 24.41 24.57 25.60 23.77 N.A. 22.24 23.25 23.51 22.89 20.90 Kole 26.01 25.45 25.80 24.49 N.A. 24.14 24.30 24.37 23.43 21.55 Can0 Limon 24.98 24.05 25.30 23.41 N.A. 23.52 23. I I 23.90 22.34 22.18 Maya 19.90 20.92 21.24 20.34 18.02 18.92 19.89. 19.48 19.30 18.02 UNITED STATES WTI 26.02 N.A. N.A. N.A. 21.25 25.82 N.A. N.A. N A. 22.80 ~~

WTS 24.89 N.A. N.A. N.A. 19.00 24.29 N.A. N.A. N.A. 21.25 ANS 24.37 N.A. N.A. N.A. N.A. 24.37 N.A. N.A. N.A. 20.50

(a)ANS del USWC; Urds del Med; Can0 Limon del USG.

Spot Tanker Rates CLEAN . . .

Route WS Assess. Rate/$M T 20.00 MT CARIB/USAC 125 5.33 80,OOO MT MEDMED 105 4.47

AG/FE 135 9.87 MEDAJSG 95 9.08

Route WS Assess. RateBMT 30.000 MT MED/UKC I90 I O 37

MEDIUSAC MEDIMED UKUUSAC UKUUKC BSEAhIED AG/INDIA AG/JAP SING/JAP

185 13 76 185 6 92 I70 1 I 49 I 50 5 46 175 I1 99 250 13 07 275 25 66 270 13 27

UKC/UKC I30.000 MT MEDAJSG

100 4.09 83 X M

WAFIUSG UKC/USG AG/MED

250.000 MT AGlUSG

-. - - .. 95 8.92 87 7.26 87 12.57 50 8.82 CARIBIUSAC 225 8.26

CARIB/USG 225 17.75 CARIB/UKC 1 85 6.68

AG/FE 56 4.59

55.066MT ~ AG/JAPAN 187 20.16

Volume 74, No. 219 Page 10 Platt's Oilgram Price Report Monday, November 11,1996 Prices Effective November 8,1996

VLCC rates look bullish London--VLCC rates looked to be on the point of a major upward move, as a couple of ships fixed into Taiwan in the w64-65 range, several points higher than last done.

Brokers predicted that if a couple more charterers needed to find quality modem tonnage in the late November period, and were unable to look at older vessels, there could be worldscale point moves higher earlier than predicted. South Korean refin- ers however, who were the main charterers left in the November market, were able to exercise some flexibility on vessel type, and fixed ships still around the mid-high w50s.

Afiamax demand in the Persian Gulfremained fm, and quality vessels have become hardex to find The November 2G30 period is said to be particularly tight on good modem tonnage, and rata have stayed around w135 and even higher for Persian Gulfeast voyages.

Brokers now predict that the rash of vessels due to come open in the Far East will find few cargoes to fix in that region, and so owners will ballast back to the Persian Gulf. The tightness in tonnage could therefore ease by the beginning of December, but in the meantime rates are likely to remain strong.

West Africa activity has fallen quiet, and VLCC interest in particular has been very slow. A couple of VLCCs were heard due to come open in the area over the next couple of weeks, while one was reported lying open spot in the prompt period. Charterers were said to have little interest in the larger ships, de- spite Suezmax rates still in the mid w90s into the US.

The only clear effect so far of a slowing in demand has been a widening of the spread between modern and older tonnage,

PLAT-TIS 7 API 19% Grand Hyatt Washington D.C. November 10-12,1996

During this year's conference, Platt's electronic services wiU be available for demonstration in the hospitality

suites of the following network information providers:

Please drop by to saa our family of Alert products for the Petroleum. Petrochemical, Electricity, Natural Gas and Shipping markets.

with some bargain rates fiied into Europe as a function of an in- crease in availability of quality ships.

In the clean market, players said product prices in Asia ap- peared still to be such that importing from the US was viable. The Tikhoretsk and the Plumeria were among those fixed US- Far East off first half November dates. The ships arriving in Asia from the US were expected to ballast back to the US, with char- terers saying it was unlikely the usually US-based vessels would find cargoes moving Asia-US. Rates US-west were being fixed in the range $950,000-1.2-mil for 30,000-40,000mt cargoes.

Owners ideas for Singapore-Japan stems were said to be around w235 for 30,000mt cargoes, with players saying they be- lieved w230 was achievable. Brokers in Japan said December cargoes were beginning to be fixed in the Persian Gulf, with the Petrobulk Mars, the Pacific Ruby, the Lucy and the Venture o/o Loyalty all said fixed into South Korea/Japan off late Novem- bedearly December dates. Rates at around wl87.5 into Japan were expected to hold despite the onslaught of December de- mand. "Worldscale 187.5 is already high enough," a broker said.

Shell sees 25,000 b/d rise in Norway Draugen 1997 output to 165,000 b/d London--Shell is expecting to raise average production from its Draugen field in Norway to around 165,500 b/d next year, an official with Norske Shell said Friday.

Output so far this year has averaged around 140,000 b/d, but the company is in the middle of an upgrade of the Norwegian Sea field's production facilities, the official said.

Upgrading of the platform's processing capacity has already been finished, he said, and work on Draugen's water injection wells should be completed "by the end of the year." Production has also been boosted by the return at the start of October of a subsea well shut in since the beginning of last year, he added.

Shell operates Draugen with a 16.2% stake, with partners BP 10.8%) and Statoil (73%).

Note to readers: US Gulf Coast For the US Gulf Coast (Waterborne and Pipeline) Platt's will add a new, separate forward cycle assessment for N0.2 oil, low sulfur N0.2 oil, and jet/kero 54 grade effective November 25. The first forward cycle assessment will be the 34th cycle. The new assessments will run separately and be distinct from current spot assessments. Comments should be sent to Robert Sharp, Houston by No- vember 15. Tel: 7131658-3215. Fax: 713/658-0515.

Oilgram Price Report

EDITORIAL: S. Savage, Editor-in-Chief; N. Graham, Mana ing Editor; J.R. Keller, Executive Editor; B. Evans, Crude Oil Manager; J. dicholson, Euro-

ew York: A. Herbst; J. Sanders;??. Havens; J. Link; G. Raynaldo; M. Misner; H. Weissman; K. Hall; B. Greenbaum; C.Reed. Houston: R . Shar J DeMoor; J. Martin: R . Camchino: A. Hueh. West Coast: J. Gilman: E. Anderson.

Publisher Vice President, Platt's Editorial

Circulation Manager

Harry G. Sachinis James Trotter

Editorial Director; J. Monte que, Asia Pacific Editorial Manager. Staff: Editor Emeritus Onnic Marashian Marguerite F. Stanford

London: C. Hallihg; C. Jud e; J. "alsh; A. Giles; S. Young: K. Emond; P. Cully; J. Moran. J y : D. &ann,; K. Takenaka; C. Park. Singupore: S. Ping; E. Ramasamy; A.

Editorial Offices:

hia. Hong Kmg: W. Lee. Moscow: J . Upperton.

New York, NY 10020 - 1221 Avenue ofthe Americas 212612-3320 Editorial Fax: 2 1215 12-3212 Houston, TX 77002 - 1200 Smith Street, Ste 2220 West Coast Gardena, CA 90248 - 1515 W 190th Street London SW19 3RU - 1 Hartfield Road Singapore 0104 -The Exchange, 20 Cecil Street #21-03 Tokyo 105 - 4-1-20 Toranomon, Minato-ku

7 13/658-9261 3 10/715-9OO5

01 81 -543-1 234 65-532-2800 3-5403-2730

Published every business day in New York and Houston by the Commodities Division of Standard &Poor's. Principal Orice: 1221 Avenue ofthe Americas, New York, New York 10020. Corporute c;#icers: Jose h L Dionne, charman and chief executive officer; Harold McGraw 111, presijent hnd chef operating officer; Kenneth M. Vittor, senior vice president, general counsel, and secretary; Frank D. Penglase, senior vice president-treasury operations.

Subscriptions: $1,807 per year by fastest mail in the US., Canada and Mexico. Airmail or airfreieht to other countnes: $2.057. For all subscri tionin uiries: tele~hone212/512-3703; fG21U512: w Telephone 01 1-545-6148; telex 267710 MCGRAW G. ISSN Number 0162-1292.

2596. In d r o ~ : Aatt's, I Hartfield Road, London SW19 3RU.

Copyri ht 01996 The McGraw-Hill Companies, Inc. All rights reserved. No reproduction ma)! be made without prior written authorization from McGraw-Hill, nor sh& this information, either in whole or in part, be redistributed or put into an information retrieval system without the prior written permission of The McGraw-Hill Companies, Inc. Platt's and Standard & Poor's are trademarks of McGraw-Hill. hfiirmution has been obtuined ,from sources believed reliuble. However, becuuse of the possibility of' humun or mechunicul error by sources, McGruw-Hill or others, McGruw-Hill does not guuruntee the uccurucy, udeyuucy or completeness of any such infiwmution und is not responsible .for uny errors or omissions or,jiJr results obtuined,from use of such infimmtion. See buck of publication invoice,fiw complete terms und conditions.

Global Commodities Intelligence

phtt’s, the leading source

of energy market intelligence

now offers you the same

coverage for the petrochemical,

electricity, natural gas and

metals markets.

Real-time, breaking news,

market analysis, transaction

reporting and benchmark

pricing, 24-hours-a-day,

from the experts at Platt’s,

McGraw-Hill’s Power

Markets Week, Inside FERC‘s

Natural Gas Alert and

Platt’s Metals Week.

Now available on delivery

platforms from Bloomberg,

Dow Jones Telerate, Bridge

(formerly Knight-Ridder

Financial), Reuters and

Standard & Poor’s

ComStock.

STANDARD &POOR’S

PLATT’S New York

+212-512-4047/+800-437-3725 Houston

+713-658-9261/+800-279-8618

PUTTS 800-437-3725 for more information fax to New York: 21 2-51 2-2596,

PLATT'S NEWSLETTERS 0 Oilgram News 0 Oilgram Price Report

PLATT'S WIRES 0 Asia PacificIArab Gulf Marketscan 0 Bunkerwire 0 ChinaWire 0 Clean Tankerfax 0 Crude Oil Marketwire 0 Dirty Tankerfax 0 European Marketscan 0 European Natural Gas Report 0 European Petrochemicalscan 0 Feedstock Report 0 Oilgram News Fax 0 US Marketscan 0 Latin American Wire 0 LPGaswire

PLATT'S HANDBOOKS

17 0 Petrochemical Price Handbook

Oil Price Handbook and Oilmanac

PLATT'S REAL-TIME & DIAL-UP SERVICES

0 Global Alert 0 Oilgram News electronic 0 0 Natural Gas Alert 0 Electricity Alert

Dispatch (and Sarus analytical software)

PLATT'S NEWSLETTERS 0 International Petrochemical Report

PLATT'S WIRES

0 European Petrochemicalscan 0 Far East Petrochemicalscan

Houston: +713-658-0125

0 Intermediate Wire 0 Latin American Pertochemicalscan 0 LPGaswire 0 Olefinscan 0 Polymerscan 0 Solventwire 0 US Petrochemicalscan

PLATT'S HANDBOOKS

0 Petrochemical Price Handbook

PLATT'S REAL-TIME & DIAL-UP SERVICES 0 Petrochemical Alert 0 Dispatch (and Sarus analytical software)

PLATT'S NEWSLETTERS 0 Metals Week

PLATT'S WIRES 0 Metals Price Alert 0 Metals Week Price Notification

PLATT'S HANDBOOKS

0 Platt's Metals Week Price Handbook

PLATT'S REAL-TIME & DIAL-UP SERVICES

0 Metals Alert 0 Dispatch (and Sarus analytical software)

PLATT'S WIRES

0 Bunkerwire 0 Clean Tankerfax 0 Dirty Tankerfax

PLATT'S REAL-TIME & DIAL-UP SERVICES 0 Marine Alert 0 Dispatch (and Sarus analytical software)

~~

NAME E - .

COMPANY

ADDRESS

CITY STATE OR PROVINCE

POSTAL CODE COUNTRY

FAX TELEPHONE -

................................................................................................................................................................................................................................................................��

................................................................................................................................................................................................................................................................�� -

................................................................................................................................................................................................................................................................��

................................................................................................................................................................................................................................................................��