US Trailer Market OverviewOrders Continue, Backlogs Solid, Production Stable…but is There Any Speculation Beginning to Occur?

Frank MalyACT RESEARCH Co., LLC

ACT Research Fall SeminarSeptember 24, 2014

Agenda• Economy and freight review

• U. S. Trailer market update

• Trailers and Fracking (Natural Gas and Oil)

• Intermodal factors

• Upcoming Outlook enhancement

• Trailer forecast 2014 ‐ 2019

2 ACT Research Co., LLC, Copyright 2014

Outlook… Slow start for 2014, better pace ahead

3 ACT Research Co., LLC, Copyright 2014

Real Gross Domestic ProductQ/Q at SAAR Q1'10 - Q4'15

Source: BEA, ACT Research Co., LLC: Copyright 2014

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 410 11 12 13 14 15

0

2

4

6

8

-2

Percent Change

+2.2% +2.1%ANNUAL

+3.2%

4 ACT Research Co., LLC, Copyright 2014

Freight growth above GDP, generating capacity issues

ACT U.S. Freight Composite Q/Q at SAAR, Y/Y

Q1'10 - Q4'15

Source: ACT Research Co., LLC: Copyright 2014

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 410 11 12 13 14 15

0

2

4

6

8

10

-2

-4

Percent Change

+4.1%

ANN. AVG.

+3.3% +5.4%

Trailer freight – positive, but slower growth until 2015

5 ACT Research Co., LLC, Copyright 2014

Dry Van Freight Composite2008 - 2015

ACT Research Co., LLC: Copyright 2014

'08 '09 '10 '11 '12 '13 '14 '1540

50

60

70

80

90

100

110

120

130Index (2004=100)

0

2

4

6

8

10

12

-2

-4

-6

Y/Y % Chg.

Y/Y % Chg.

Dry Freight Index

Reefer Van Freight Composite2008 - 2015

ACT Research Co., LLC: Copyright 2014

'08 '09 '10 '11 '12 '13 '14 '1560

70

80

90

100

110

120

130Index (2004=100)

0

2

4

6

8

10

-2

-4

Y/Y % Chg.

Y/Y % Chg.

Reefer Freight Index

Volume returning to 2013 year‐end levels…with a bit of a summer pause

6 ACT Research Co., LLC, Copyright 2014

ATA SA Truck Tonnage IndexJanuary '10 - July '14

Source: American Trucking Associations, ACT Research Co., LLC: Copyright 2014

10 11 12 13 1480

90

100

110

120

130

140Index

0

5

10

15

20

25

30

35

40

45

50

-5

-10

Y/Y % Chg

ACT For-Hire Trucking IndexVolumes

January '10 - August '14

ACT Research Co., LLC: Copyright 2014

'10 '11 '12 '13 '1430

35

40

45

50

55

60

65

70

75

80

85Index

0

5

10

15

20

25

30

35

-5

-10

-15

-20

Growing

Contracting

ACT For‐Hire Trucking IndexCapacity adds limited by

driver availability

7 ACT Research Co., LLC, Copyright 2014

ACT For-Hire Trucking IndexFleet Capacity

January '10 - August '14

ACT Research Co., LLC: Copyright 2014

'10 '11 '12 '13 '1435

40

45

50

55

60

65Index

0

5

10

15

-5

-10

-15

Growing

Contracting

ACT For-Hire Trucking Index% Respondents Buying Equipment in Next 3 Months

January '10 - August '14

ACT Research Co., LLC: Copyright 2014

'10 '11 '12 '13 '140

10

20

30

40

50

60

70

80

90

100% of Respondents

Fleet purchase intentions remain strong

U.S. Trailer Market Update• Shipments up 7% ytd over 2014

– Van vs. Specialty Trailers continues to be a theme

– Total Vans +9%, Flats 6%, Dumps 29%, Tanks flat, Bulk 92%

• Cancellations lower y/y– Every category has a lower cancelation rate versus last year

– Fleet commitments and a long lead‐time queue

8 ACT Research Co., LLC, Copyright 2014

U.S. Trailer Market Update• 2013/2014 order season continues…

– “Seasonal slowing” has not really occurred

– YTD orders are up 40%

– Large fleets strength now moving into medium and small fleets, specialty segment

• Tight freight capacity

– Resulting upward rate pressure

– Generates better short to medium term profitability

– Ability, and need, to buy

• Productivity improvements – difficult to come by

• Component comments

– Tires/stainless/lumber availability versus pricing as the year closes

9 ACT Research Co., LLC, Copyright 2014

Total Trailers Seasonals• Orders have run stronger than the

patterns would predict• Backlogs are likely to remain

stronger through Q3/Q4

10 ACT Research Co., LLC, Copyright 2014

‐0.25‐0.20‐0.15‐0.10‐0.050.000.050.100.150.200.25 NetOrds

‐0.25‐0.20‐0.15‐0.10‐0.050.000.050.100.150.200.25 Backlog

‐0.25‐0.20‐0.15‐0.10‐0.050.000.050.100.150.200.25

Build

ACT Research Co., LLC, Copyright 201411

TRAILER INDUSTRY FACTORY SHIPMENTSJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 140

5

10

15

20

25

30Units (000s)

CONTAINERS & CHASSIS:Monthly & 6 Mo. Avg.

TRAILERS ONLY:

Monthly &6 Mo. Avg.

• Best shipment levels since September 2006

• +1% m/m, +26% y/y, +7% ytd

• Normally, we are consuming down backlog mid-year through mid-fall

• Build season vs Order season

• Less change in backlog than anticipated – order driven

12 ACT Research Co., LLC, Copyright 2014

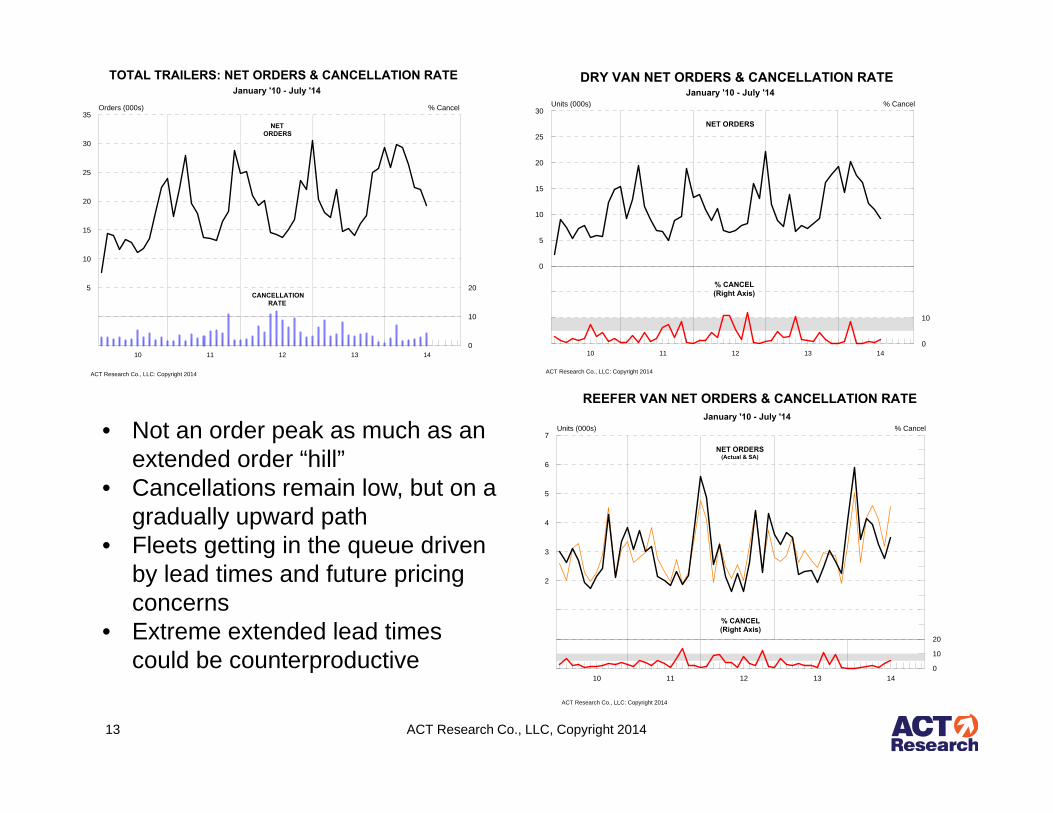

TOTAL TRAILERS: Past 12 Months NET ORDERS & Actual BUILD

January '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 140

5

10

15

20

25

30Units (000s)

12MMA NO BUILD

• Order season has extended

• After remaining in a narrow band, build has broken out

• YTD new orders +41% and net orders +44%

• Build catching up with the orderboard

• Some issues with trailers on the ground

• Not an order peak as much as an extended order “hill”

• Cancellations remain low, but on a gradually upward path

• Fleets getting in the queue driven by lead times and future pricing concerns

• Extreme extended lead times could be counterproductive

13 ACT Research Co., LLC, Copyright 2014

TOTAL TRAILERS: NET ORDERS & CANCELLATION RATEJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

5

10

15

20

25

30

35

-5

Orders (000s)

0

10

20

30

40

50

60

70

80% Cancel

NET ORDERS

CANCELLATION RATE

DRY VAN NET ORDERS & CANCELLATION RATEJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

5

10

15

20

25

30

-5

-10

-15

Units (000s)

0

10

20

30

40

50

60

70

80

90% Cancel

% CANCEL(Right Axis)

NET ORDERS

REEFER VAN NET ORDERS & CANCELLATION RATEJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

1

2

3

4

5

6

7

-1

Units (000s)

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160% Cancel

% CANCEL(Right Axis)

NET ORDERS(Actual & SA)

• Flatbed orders continue on a gradual upward path, but adjustments to BL occurring

• Bulk tanks on a break-out…almost 50% above the average volume track

• Liquid tanks slow growth path, but well above on y/y basis

14 ACT Research Co., LLC, Copyright 2014

PLATFORM TRAILER NET ORDERS & CANCELLATION RATEJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

1

2

3

4

5

-1

-2

-3

Units (000s)

0

10

20

30

40

50

60

70

80% Cancel

% CANCEL(Right Axis)

NET ORDERS

LIQUID TANK TRAILER NET ORDERSJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

500

1000

1500

2000

-500

Net Orders

BULK TANK TRAILER NET ORDERSJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

250

500

750

1000

-250

-500

Net Orders

Net Orders& 6 Mo. Avg.

15 ACT Research Co., LLC, Copyright 2014

TOTAL TRAILERS BACKLOG & BACKLOG/BUILD RATIOJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

25

50

75

100

125

150

175

-25

-50

-75

Units (000s)

123456789101112131415161718192021

BL/BU Ratio (Months)

BACKLOG: Actual & SA

BL/BU RATIO(Right Axis)

DRY VAN BACKLOG & BACKLOG/BUILD RATIOJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

25

50

75

100

-25

-50

Units (000s)

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18BL/BU Ratio (Months)

BL/BU RATIO(Right Axis)

BACKLOG

REEFER VAN BACKLOG & BL/BU RATIOJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

5

10

15

20

25

-5

Units (000s)

0

2

4

6

8

10

12

14

16

18

20

22

24BL/BU Ratio (Months)

BL/BU RATIO(Right Axis)

BACKLOG

PLATFORM TRAILER BACKLOG & BL/BU RATIOJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

2

4

6

8

10

12

-2

-4

Units (000s)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17BL/BU Ratio (Months)

BL/BU RATIO(Right Axis)

BACKLOG

The Liquid and Bulk Trailers Tale…• Surge in natural gas and petroleum production• Huge surge in drilling…until late 2011• Explora on → Produc on• Cap‐ex fell on lower NG and oil prices• Shift from vertical/directional to horizontal• Speculation was flushed from orderboards• Bulk orders are now breaking out• NG prices have declined• NG stocks need to be rebuilt• Bulk tank demand more regional• No. Dakota flare gas opportunity?

– “Non‐marketed natural gas”– Roughly 30% is flared

16 ACT Research Co., LLC, Copyright 2014

• Horizontal and vertical wells• Equal in mid-09• Over 3x in ’14

• Directional…no change• Horizontal → Fracking →Freight• Evolving technology

• Deeper wells• Longer runs• Higher density

17 ACT Research Co., LLC, Copyright 2014

0

500

1,000

1,500

2,000

2,500US Rotary Rig Counts

Oil Gas Misc Total

0200400600800

1,0001,2001,4001,600

Rig Count by Trajectory

Dir. Horz Vert

• Total rig counts approaching previous peaks

• Primary oil wells have been surging

• Natural gas well counts down• Efficiency/Production versus

count

• Slow recovery from severe ‘13/’14 winter • Gap is narrowing• Added production

• Existing wells• Additional wells

• Foreign demand over and above….

18 ACT Research Co., LLC, Copyright 2014

Natural Gas stockpiles still recovering

LIQUID TANK TRAILER BACKLOG & BL/BU RATIOJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

1

2

3

4

5

6

7

8

-1

-2

-3

Units (000s)

0

3

6

9

12

15

18

21

24

27

30

33BL/BU Ratio (Months)

BACKLOG

BL/BU RATIO(Right Axis)

Liquid and Bulk segments now have different challenges

19 ACT Research Co., LLC, Copyright 2014

BULK TANK TRAILER BACKLOG & BL/BU RATIOJanuary '10 - July '14

ACT Research Co., LLC: Copyright 2014

10 11 12 13 14

0

1

2

3

4

5

-1

-2

-3

Units (000s)

0

3

6

9

12

15

18

21

24BL/BU Ratio (Months)

BACKLOG

BL/BU RATIO(Right Axis)

• 15 Months of tight market conditions• Early year break-out on orders• Initially driven by NG price surge• Now NG production rushing to fill

storage for upcoming heating season• Oil production growth as well

• Liquid tank BL has stabilized• Production continues to be well

balanced to BL

Trailer market factors continue positive• Freight growing, capacity challenged, and “low hanging” productivity gains waning

• Improved fleet profitability and attitudes– Ability and willingness

• Fleet age has improved noticeably, and that will continue– Long‐term deferred replacement…finally making gains– Old equipment impacts customer service and productivity

• Replacement now joined by additions to the fleet• The trailer/tractor balance

– Catch up for lack of trailer investment– Order ratio high for 12 months– Build ratio reacting to that orderboard

20 ACT Research Co., LLC, Copyright 2014

10 11 12 13 14

0

5

10

15

20

25

30

-5

-10

-15

Units (000s)

0.00.51.01.52.02.53.03.54.04.55.05.56.06.57.07.58.08.59.0

Trailer:Tractor Ratio

BUILD RATIOU.S. TRAILERS and U.S. CL.8 TRACTORS

3 Month Moving Averages, January '10 - July '14

ACT Research Co., LLC: Copyright 2014

CL. 8TRACTORS

TRAILERS

BUILD RATIO(Right Axis)

21 ACT Research Co., LLC, Copyright 2014

• At, or above, range since mid-2011 • Delayed trailer capex catch-up• Order ratio impacted by some mid-

year seasonality

• Build ratio has a delayed response to the order ratio

• Solid but a bit less robust y/y• Less oscillation in the past 3

quarters

Trailer/Tractor Ratios

10 11 12 13 14

0

5

10

15

20

25

30

35

-5

-10

-15

-20

Units (000s)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0Trailer:Tractor Ratio

NET ORDER RATIOU.S. TRAILERS & U.S. CL.8 TRACTORS

3 Month Moving Averages, January '10 - July '14

ACT Research Co., LLC: Copyright 2014

CL. 8TRACTORS

TRAILERS

TRAILER:TRACTORORDER RATIO

(Right Axis)

TOTAL TRAILERS: Factory Shipments Less Scrappage

1990 - 2020

ACT Research Co., LLC: Copyright 2014

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20

0

25

50

75

100

125

150

-25

-50

-75

-100

-125

-150

Thousands

NET POPULATION GROWTH

NET POPULATION SHRINKAGE

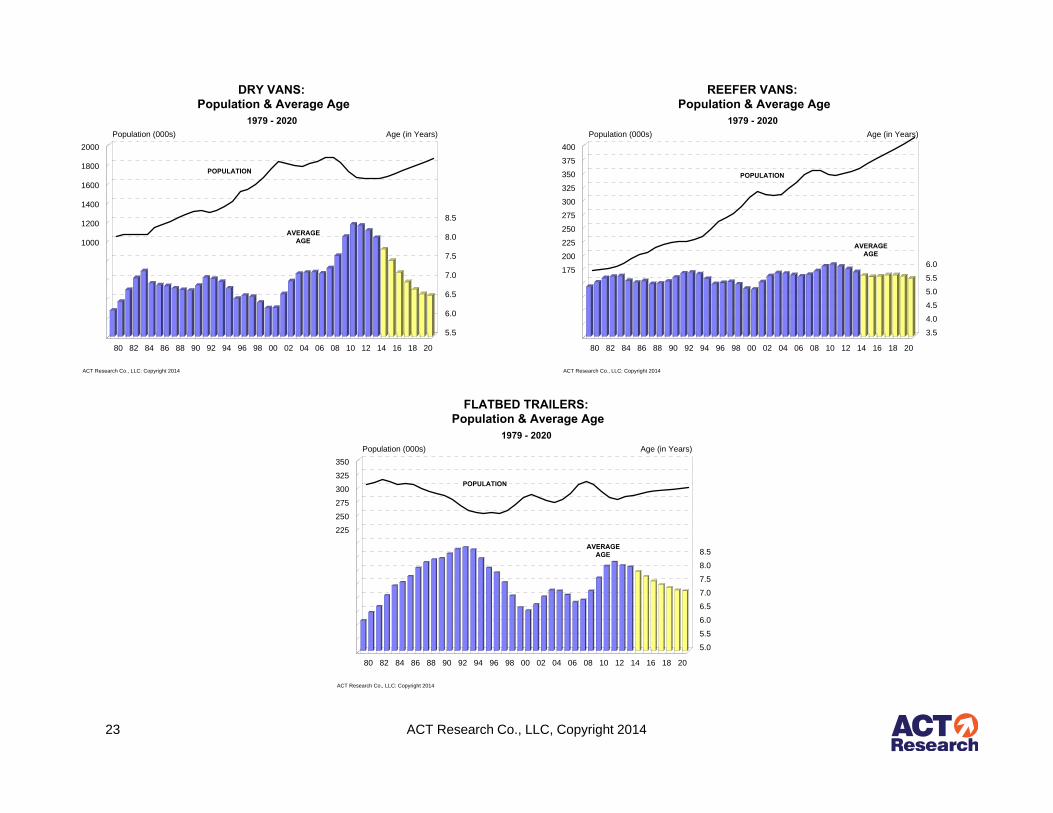

TOTAL TRAILERS: Population & Average Age

1979 - 2020

ACT Research Co., LLC: Copyright 2014

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 201000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

3200

3400Population (000s)

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5Age (in Years)

AVERAGE AGE

POPULATION

Fleet growing and getting younger through the forecast From 2007 to

2011, the U.S. trailer fleet shrank by 9%, dry vans 12%

Still below pre-recession peaks

Now in third year of fleet growth

Growth impacted by driver issues and productivity gains

22ACT Research Co., LLC, Copyright 2014

23 ACT Research Co., LLC, Copyright 2014

DRY VANS: Population & Average Age

1979 - 2020

ACT Research Co., LLC: Copyright 2014

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 200

200

400

600

800

1000

1200

1400

1600

1800

2000Population (000s)

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5Age (in Years)

POPULATION

AVERAGE AGE

REEFER VANS: Population & Average Age

1979 - 2020

ACT Research Co., LLC: Copyright 2014

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 2050

75

100

125

150

175

200

225

250

275

300

325

350

375

400Population (000s)

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5Age (in Years)

POPULATION

AVERAGE AGE

FLATBED TRAILERS: Population & Average Age

1979 - 2020

ACT Research Co., LLC: Copyright 2014

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 200

25

50

75

100

125

150

175

200

225

250

275

300

325

350Population (000s)

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0Age (in Years)

POPULATION

AVERAGE AGE

24 ACT Research Co., LLC, Copyright 2014

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20100

120

140

160

180

200

220

240Units (000s)

TOTAL TRAILERS:Underlying Replacement Demand

1990 - 2020

ACT Research Co., LLC: Copyright 2014

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 2060

70

80

90

100

110

120

130

140Units (000s)

DRY VANS:Underlying Replacement Demand

1990 - 2020

ACT Research Co., LLC: Copyright 2014

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 2010

15

20

25

30

35Units (000s)

REEFER VANS:Underlying Replacement Demand

1990 - 2020

ACT Research Co., LLC: Copyright 2014

Fleet ProductivityThe positives and the negatives…

• Logistics/routing/tracking• Regulatory issues

– HOS/Equipment regulations– Weight/length

• Driver availability• Emissions/mileage• Intermodal All have an impact on the amount of equipment

needed

25 ACT Research Co., LLC, Copyright 2014

Intermodal• Service levels have become a major issue

– Train speed and dwell times

• Coal, petroleum, and chemical volumes consuming capacity

• Inconsistent service has negatively impacted temperature‐controlled offerings

• Recent moves toward bulk chemical transport– Addressing “driver availability issues”

26 ACT Research Co., LLC, Copyright 2014

Estimated Intermodal ImpactDomestic Container volume doubled in 10 years, but still a small part of total freight movement

TOFC was the only category down y/y in 2013

Estimate: Population impact for every 1M shift in domestic IM loads:

• Reduces need for C8 tractors by ~10k units

• Reduces the need for trailers by ~20k

• Comparable math for TOFC conversion

27 ACT Research Co., LLC, Copyright 2014

Intermodal Loads by Type1999 - 2013

Source: IANA, ACT Research Co., LLC: Copyright 2014

2.2 2.4 2.5 2.7 3.0 3.1 3.1 3.3 3.6 3.8 4.0 4.5 4.9 5.6 6.12.9 2.6 2.4 2.3 2.4 2.6 2.6 2.4 2.1 2.1 1.6

1.7 1.71.6

1.64.8 5.3 5.4 5.9

6.57.1 7.9 8.5 8.3 7.7

6.17.2

7.57.6

7.8

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0Intermodal Loads (millions)

Dom Cont Dom Trlrs Internatl Cont

Trailer Forecast Update• Outlook continues to improve, edging higher• Concerns beginning to be expressed on components

– “Shared” components, such as tires• Solid quote activity and continued order flow• Supported by

– Freight, both amount and pricing– Tight capacity – Resulting fleet profitability

• Outlook:– 2014 +10.3% / 2015 +0.6% / 2016 +3.0%

28 ACT Research Co., LLC, Copyright 2014

Longer Pups still in the cards…• 28ft vs 33ft – 18% capacity increase

– LTL / Expedited…cube out vs. weigh out

• Projected timing of new bill is mid‐15– Likely to include 33 foot pups

• Estimated 325k pup population• Timing and opportunity…

– Delay of 15k in 2014/15– Pull‐forward 15k/12k/10k in 2016‐18– “Extending” 28 foot trailers another alternative

• “Dimensional Weight” pricing – (L x H x W) / “Factor”

• Factor: FedEx – 139 UPS – 166

29 ACT Research Co., LLC, Copyright 2014

An OUTLOOK enhancement…• North America Total Trailer reporting

• Including Canada and Mexico trailer totals

• Built off our knowledge gained from Global Trailer Project

• Projected October Outlook release

30 ACT Research Co., LLC, Copyright 2014

31 ACT Research Co., LLC, Copyright 2014

U.S. TRAILER FACTORY SHIPMENTS2010 - 2019

ACT Research Co., LLC: Copyright 2014

'10 '11 '12 '13 '14 '15 '16 '17 '18 '190

50

100

150

200

250

300

350

Orders (000s)

Dry Vans Reefer Vans Flatbeds All Other Trailers

Dry Vans 60 117 130 135 153 157 170 163 160 154Reefer Vans 27 33 34 36 38 37 35 36 38 40

Flatbeds 8 16 25 22 25 25 24 23 23 23All Other Trailers 30 43 49 47 50 49 46 47 48 47

Total Trailers 126 210 237 240 266 267 275 269 269 264

32

ACT Research Company, LLC4400 Ray Boll BoulevardColumbus, IN 47203

Phone: (812) 379‐2085Fax: (812) 378‐5997

Email: [email protected]

![Automating Reefer Monitoring in Terminalswebinar-1]-automating-reefer... · •No terminal solution for full site coverage Stable and Proven Reefer Monitoring Solution RMM Slave PowerLine](https://cdn.vdocuments.us/doc/165x107/5dd0cf52d6be591ccb62ce92/automating-reefer-monitoring-in-terminals-webinar-1-automating-reefer-ano.jpg)