BABSON COLLEGE

UK/US Exchange Rate A study examining a set of financial and economic

variables that could influence the UK/US exchange rate

Eveline Dang

Anushka Doshi

Apurv Jhawar

Hanson So

“I pledge my honor that I have neither received nor provided any unauthorized assistance during the

completion of this work.”

“The authors of this paper hereby give permission to Professor Michael Goldstein to distribute this paper

by hard copy, to put it on reserve at Horn Library at Babson College, or to post a PDF version of this

paper on the internet.”

1

Table of Contents

Executive Summary

2

Introduction

3

Models and Analysis

3

-Data Selection

3

-Relationship of Interest Rate with Exchange Rate

4

-Relationship of Consumer Price Index with Exchange Rate

6

-Relationship of Gold Price with Exchange Rate

8

-Relationship of Crude Oil Price with Exchange Rate

9

- Relationship between Stock Markets and Exchange Rates

9

Methodology

10

-Further Study

10

Model 1A and 1B

11

-Model 1A

11

-Model 1B

14

Model 2A and 2B

16

-Model 2A

17

-Model 2B

17

Model 3

19

Works Cited

23

Exhibits 25

2

EXECUTIVE SUMMARY

The United States of America and the United Kingdom have had strong relationships even

before the Bretton Woods System was abandoned. Exchange rates and interest rates have been

used as mechanisms to influence each country’s economic monetary policy. Throughout this

paper, we discuss various variables that could impact the US/UK exchange rate and examine

such relationships by generating regression models. Studying past researches has led us to a

selection of eight variables: US treasury rate, UK treasury rate, US CPI, UK CPI, Gold Price,

Crude Oil Price, S&P 500 Change and FTSE 100 Change. We attempted to test the effect of

short-term and long-term treasury rates on the exchange rate by using 3-month T-Bill for both

countries in one model and 10-year treasury rates for both countries in another model, while

benchmarking the rest of the variables. The models show that long-term treasury rates tend to

display a better relationship with exchange rates. Commodity prices in general have an influence

on the direction of exchange rates’ movement. It also seems that exchange rates move in the

inverse direction with gold price and demonstrate a positive relationship with crude oil price. In

addition, the models imply that stock indices do not impact exchange rates.

We then ran a regression model for the errors between the observed and calculated exchange

rates (from the uncovered interest rate parity) against all the independent variables to see if any

variables were significantly contributing to the error. Most notably, it dawns on us that treasury

rates, whether short-term or long-term, can be used to explain the errors between the value of

exchange rates in theory and in reality. This is a result of arbitrage involved with investing

activities.

We also built an additional model to forecast exchange rates using an autoregression method.

We have found that our model functions fairly well in terms of forecasting exchange rate returns

of 1-steo horizon ahead. Given forecasting exchange rate returns of several months ahead, it is

unlikely that the model will be valid.

3

INTRODUCTION

The United States and the United Kingdom have shared a rich history. Post the revolutionary

war, which was a conflict between the two nations’ different ideologies and interests, the Jay

Treaty was signed in 1794. This peace treaty began the trade relationship between the United

States and the United Kingdom. Even though this treaty favored the British more than the

Americans in terms of trade, it was the first initiative taken by both nations to establish a brighter

trading future1. Since that moment, both nations have gone on making breakthroughs in the fields

of finance, R&D, arts and science, defense and many more sectors by working together. Today,

the trading relationship between the US and the UK has reached about one trillion dollars, having

almost two million expats in combined employment between the nations2. With the collapse of

the Bretton Woods system in 1971, many countries started holding US currency as a method of

holding foreign currency reserves. At that time, the UK discontinued its fixed exchange scheme

and decided to freely float its currency. Ever since then, the relationship between the US and UK

currency has become a subject of interest for several researchers3.

Moving onto the present early in November 2013, the Bank of England (BOE) mentioned

that they were thinking of raising interest rates earlier than planned. Though BOE representatives

reasoned that this plan was taken into consideration due to growing economy and declining

unemployment, such plan could possibly be interpreted as a response of the UK to the

expectation that US quantitative easing would no longer work in the near future. BOE’s initiative

in terms of interest rates is most likely an attempt to maintain the current exchange rate between

the UK and the US. The removal of quantitative easing would cause US interest rates to move

upward, and in order to have the US/UK exchange rates remained unchanged, the UK interest

rates would need to be increased.

MODEL AND ANALYSIS

Data Selection

1 http://history.state.gov/milestones/1784-1800/jay-treaty

2 http://ukustrade.com/

3 http://www.nber.org/chapters/c6876.pdf

4

We have selected several variables that we think could impact the UK/US exchange rate.

They are listed below:

1. USA 3-month T-bill

2. UK 3-month T-Bill

3. US CPI

4. UK CPI

5. Gold Price

6. Crude Oil Price

7. S&P 500 Change

8. FTSE 100 Change

All of the above variables have their values recorded in levels, except for S&P 500 Change

and FTSE 100 Change, which are in percentage.

The next parts of this section cover reasons for selecting these variables by examining

economic theories and other scholarly sources.

Relationship of Interest Rate with Exchange Rate

There have been several researches that look into the relationships between interest rates,

consumer price index and exchange rates. The basic Fisher equation below explains how the

expected real interest rate and expected inflation rate impact the nominal interest rate.

𝑛 = 𝑖𝑒 +𝜋e

𝑛: nominal interest rate

𝑖: real interest rate

𝜋: expected inflation.

The economic logic is, “Real interest rates fall as inflation increases, unless nominal rates

increase at the same rate as inflation4”

4 http://www.investopedia.com/terms/f/fishereffect.asp

5

Furthermore we have studied two theories that build these variables into an equation that

involve the spot exchange rate namely the:

1. Covered interest rate parity theorem

2. Uncovered interest rate parity theorem

For example, person A is choosing between the US and UK for investment opportunities.

Before making an investment, person A will have to consider the interest rates in both the US

and the UK, the spot exchange rate and the forward rate in order to make a sound decision.

Ignoring the forward rate can be detrimental to an investment decision.

The covered interest rate parity formula is:

𝑖 𝑖

: forward rate

: spot exchange rate.

The covered interest rate parity refers to a condition “where the relationship between interest

rates and the spot and forward currency values of two countries are in equilibrium. As a result,

there are no interest rate arbitrage opportunities between those two currencies.5”

Meanwhile, the uncovered interest rate parity formula is:

𝑖

𝑖

“The uncovered interest rate parity (UIRP) condition says that the dollar return on a dollar

investment should be the same as the dollar return on a euro investment6” Interest rates are a key

component that can determine exchange rates. For instance, if interest rates in the US are higher

than those of the UK, then, investors would invest in the US since they would obtain higher

returns. Hence, US dollars would appreciate due to the capital inflow into the country. In 2008,

Bank of England lowered interest rates, which meant that investors would achieve lower returns

5 http://www.investopedia.com/terms/c/covered-interest-rate-parity.asp

6 http://www.eco.uc3m.es/~desmet/development/notesuip.pdf

6

than what they were receiving previously. This is the reason why investors would take their

money back out of the UK to invest elsewhere. Thus, the demand for the British Pound fell,

which resulted in the depreciation of the British Pound’s value. This is shown in the graph

below where lowered interest rates lead to the value of GBP weakening7.

Within interest rates, we have selected 3-month T- bill rates and 10-year treasury rates to

make a comparison of how short-term and long-term interest rates will impact the exchange rate

of UK and US. According to secondary research we conducted on interest rates for bonds, “We

have seen that the volatility of interest rates depends on the maturity of the underlying bond:

long-term interest rates are less variable than short-term interest rates. Short-term interest rates

are procyclical while long-term interest rates co-vary little with movements in output over the

business cycle8”

Since different maturities of bonds could have varying effects on the exchange rate, we

wanted to incorporate both 3-month and 10-year treasury rates in the model to give us a

comparison, which we refer to as Model 1A and 1B (in our regression analysis).

Relationship of Consumer Price Index (CPI) with Exchange Rate:

The theory of Purchasing Power Parity (PPP) stresses that, “PPPs are price relatives, which

show the ratio of the prices in national currencies of the same good or service in different

7 http://www.economicshelp.org/macroeconomics/exchangerate/factors-influencing/

8http://www.phil.frb.org/research-and-data/publications/business-review/1996/january-february/cyclical-

volatility.cfm

7

countries9” PPP is an “economic theory that estimates the amount of adjustment needed on the

exchange rate between countries in order for the exchange to be equivalent to each currency's

purchasing power. The relative version of PPP is calculated as:

: exchange rate of currency 1 to currency 2

: cost of good "x" in currency 1

: cost of good "x" in currency 210

Another method that demonstrates the effect of CPI on exchange rates is shown in the

diagram below11

:

Relationship of Gold Price with Exchange Rate:

9 http://www.oecd.org/std/prices-ppp/2078177.pdf

10 http://www.investopedia.com/terms/p/ppp.asp

11 McCallum, Bennett T., and Edward Nelson (2000). “Monetary Policy for an Open Economy: An Alternative

Framework with Optimizing Agents and Sticky Prices,”Oxford Review of Economic Policy

The diagram alongside explains that as the exchange rate

depreciates, the CPI increases through a transmission mechanism.

The logic here is simple. If the exchange rate in the US were to

depreciate, it would be more expensive for the local people to import

products and exports would become more competitive. Americans

would essentially be paying more for a certain product than they

would have before because of the depreciation of the USD. Hence,

once the price of the imported product increases people would

switch to domestically produced goods. Hence, the demand for local

products would increase, causing rise in domestic aggregate demand.

Eventually this translates to prices in general going up, leading to a

hike in the CPI. Therefore, it is evident that the exchange rate

fluctuations have an impact on the CPI and we found it essential to

include this variable in our regression model. Our inclusion of CPI

also ties back to the original Fischer equation since expected

inflation will affect the nominal interest rate.

8

Gold has deep historical roots in determining purchase power parity12

. There have been

studies that suggest the relationship between gold price and exchange rates. The gold standard

was created in the United States and United Kingdom in the 19th

century. For paper currency to

be issued, it had to be backed by enough gold in the vaults. The gold exchange ratio is how

much unit of gold can be redeemed for each paper bill issued by the respective country. While

researching about the relationship between exchange rates and gold research, one main finding

was discovered: “The exchange ratio between a country’s money and gold did not vary when the

country was on a gold standard. The real exchange rate can be determined through the use of this

formula13

:

𝑒 (

)

: time-t real exchange rate

𝑒 time-t nominal exchange rate

and : time-t price levels in the foreign country and domestic country in gold value

14

To build the price indices for the domestic and foreign country, the country’s basket of goods

is multiplied by the gold exchange ratio. The real exchange rate is a measurement of one

country’s goods to another. The conclusion holds true over the long run that gold retains its

purchasing power parity.

However, there has been a transition in the image of gold today. Gold is considered an

alternative to the US currency. As a result, trend analysis shows gold and the dollar trading in

inverse directions over the past ten year period observed. When gold prices are rising, the US

Dollar is weakening as a result compared the British Pound. Why does the same not occur for

the British Pound when gold price rises? This is because the US dollar is considered to be the

international monetary reserve. When the world is starting to fear and distrust the reliability of

the US Dollar, they will demand more gold. Inflation, distrust, and fear are other factors that

will drive people to demand gold. This demand in gold will also put pressure pushing down the

12

http://www.sciencedirect.com.ezproxy.babson.edu/science/article/pii/S0301420708000202

13 http://www.minneapolisfed.org/research/dp/dp32.pdf

14 http://www.minneapolisfed.org/research/dp/dp32.pdf

9

price of the US dollar. The price of gold is a measurement of fear sentiment rather than priced

by the yearly output production. This inverse relationship is also because of the fact that gold

becomes more expensive to buy in other currencies as the US Dollar appreciates more. Gold in

US denominated currency would therefore decrease. This relationship concludes the inverse

relationship between gold and the US exchange rate with other countries. This evidence

supports the notion of the US dollar being an international currency15

.

Relationship of Crude Oil Price with Exchange Rate:

Crude oil is one of the most highly demanded commodities that essentially “power” the

economy. This commodity is required in order to run energy consuming production and

transportation resources. Since every nation requires oil, importing and exporting of oil is vital

for a countries finances, which is why it has an important relationship with exchange rates. If a

country is a major importer of crude oil, and if oil prices rise, then obviously the country

importing oil is worse off than the country exporting oil. The OPEC nations are all oil exporting

nations who have a great impact on the supply of crude oil. The price of oil is denominated in US

Dollars, and so, when the US Dollar weakens, the price of oil automatically reduces for the

countries that import oil. For instance, if the UK was importing oil, and the dollar weakened, the

UK government would pay fewer pounds for oil than they would have if the dollar had not

depreciated. In other words, the UK can buy more oil when the prices are lower. However, a

weakening dollar for the nations is not healthy as they receive fewer dollars for the quantities

they export16

. Hence, in order to make higher profits, these nations collectively decide to cut the

supply of oil, purely to increase oil prices. We found it useful to introduce a commodity such as

oil in our model because we wanted to see if it has a specific effect on the US/UK exchange rate.

Relationship between Stock Markets and Exchange Rates

The Standards & Poors 500, also known as the S&P 500, consists of the top 500 companies

in the US. It is also known to be the best representation of the US stock markets, and it is

different to other US indices such as the Dow Jones and NASDAQ because of its weighting

15

http://www.lbma.org.uk/assets/Alch6605Oconnor.pdf 16

http://www.economicinsight.ca/economic_docs/2009may_oilprices.pdf

10

methodology. In order to be listed on S&P 500, companies must have market capitalization of at

least four billion, and a minimum of 50% floated to the public17

.

FTSE 100, on the other hand, is a major stock exchange in the UK. It represents the top 100

companies based on market capitalization from the London Stock Exchange. The index began in

1984, and has now become one of the major indices in the world. 18

There has been an extensive research on the relationship between stock markets and

exchange rates, so we were curious to see how stock indices would or would not “collaborate”

with other independent variables in displaying an aggregate relationship with exchange rates.

We came across many articles but decided to explore the research done by Desislava

Dimitrova on a deeper scale. His paper focuses on the relationship between exchange rates and

stock markets between the US and UK, which has been helpful for us to gain a better

understanding of the topic. In this paper, Dimitrova makes reference to “Ajayi and Mougoue”

who study the relationships between stock prices and exchange rates in “eight advanced

economies”. In their study, Ajayi and Mougoue notice that a hike in stock prices would cause the

currency to weaken for the US and the UK. They go on inferring that this happens because a

rising stock market would suggest a booming economy, which would lead to an increase in

inflation. A higher inflation would mean that the value of the currency would be worth less,

which in turn would lower the demand for the currency. Thus, the currency would become

weaker19

. With this study in our mind, we decided to include stock market indices such as S&P

500 and FTSE 100 as our variables that may have a relationship with the US/UK exchange rate.

METHODOLOGY

The goal f the models is to test whether 3- month T-bill rates, 10-year treasury rates and CPIs of

both the US and UK will have a significant relationship with the UK/US Exchange rate.

Further Study

17

http://www.spindices.com/documents/factsheets/fs-sp-500-ltr.pdf 18

http://www.londonstockexchange.com/exchange/prices-and-markets/stocks/indices/summary/summary-

indices.html?index=UKX 19

http://org.elon.edu/ipe/dimitrova%20final.pdf

11

Simultaneously we are studying whether 3-month (short-term) or 10-year (long-term) rates have

a greater impact on the exchange rate for UK/US, if any.

Model 1A and 1B explore the effect of UK and US treasury rates (short-term and long-term,

respectively), US CPI, UK CPI, Gold Price, Crude Oil Price, S&P 500 Change and FTSE 100

Change on the US/UK exchange rate. Data used is collected for monthly basis, from Bloomberg

and the FRED website to maintain consistency. All values were in levels except for the S&P 500

and FTSE 100 which were taken as a percentage change from the previous month. Our data set

ranges from January 1973 to December 2012, 40 X 12 = 480 observations. All data is available

across this time frame except for FTSE 100 which started in 1984. In addition, there were some

missing values of Crude Oil Price.

A large data set is more representative of the behavior of US/UK exchange rate over the

years. There are advantages and disadvantages of choosing a large data set. In terms of

advantages, many data points indicate a better trend of exchange rate and allow us to see the big

picture of how exchange rates move in relation to the movements of other predictor variables.

However, a large data set overlooks the specificity of certain time periods where significant

events happened that considerably impacted exchange rates. For the purpose of this paper, a

large sample size yields more advantages than disadvantages.

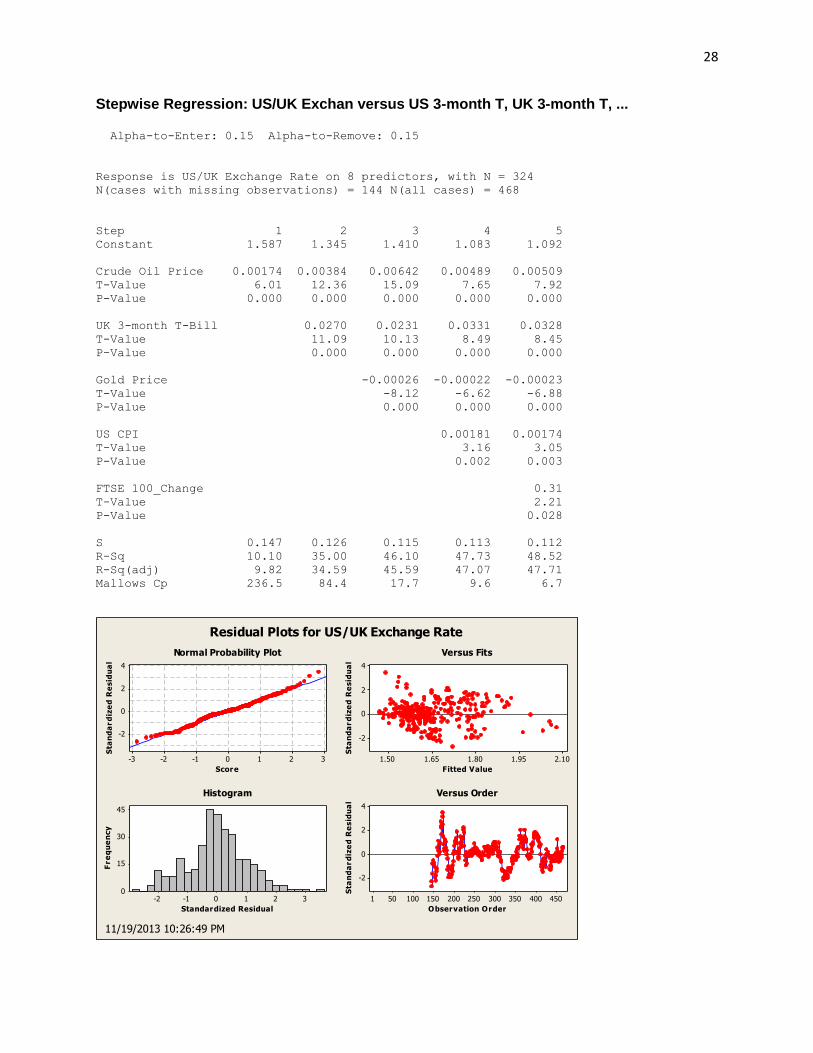

MODEL 1A AND MODEL 1B

Model 1A

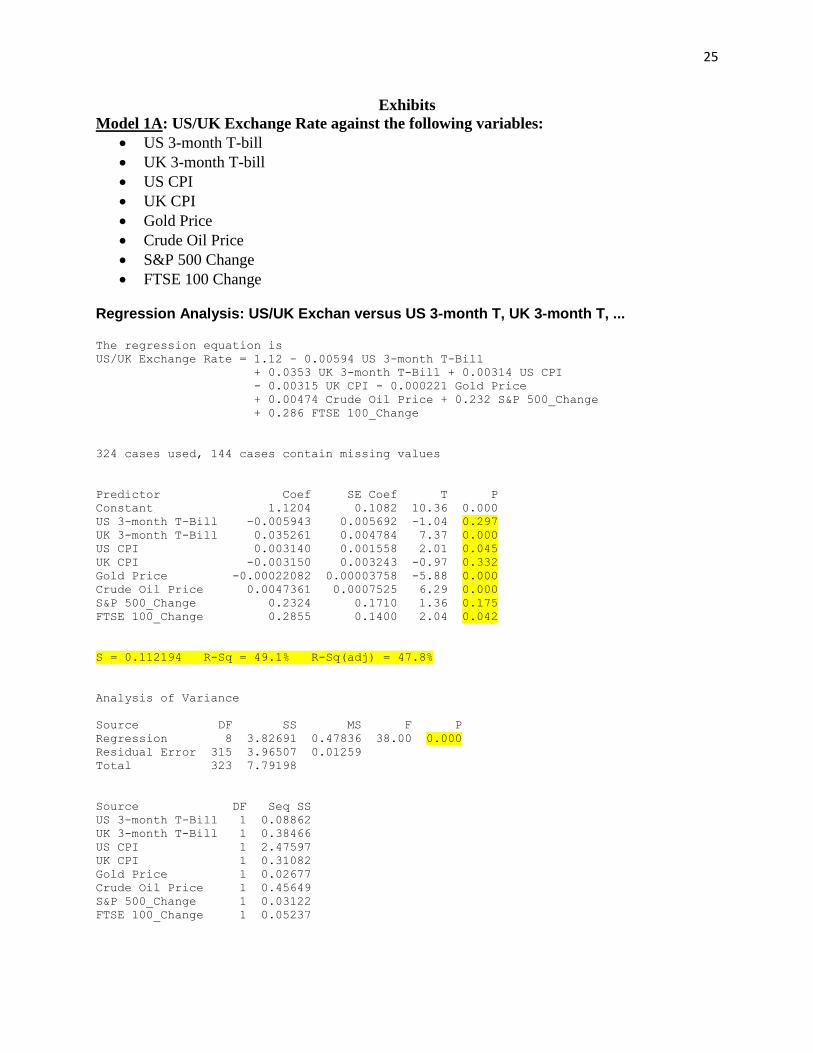

Model 1A serves to test the relationship between exchange rates and eight other variables. In

this model, we used the short-term 3-month T-Bill for both the US and UK. We ran an initial

simple regression against the US/UK exchange rate (commonly known as the spot rate), then

compared the p-values of individual variables with the level of significance . We found

that all variables were significant except for US 3-month T-bill (p-value is 0.297 > 0.05), UK

CPI (p-value is 0.332 > 0.05), and S&P 500 Change (p-value is 0.175 > 0.05). The FTSE 100

Change was almost on a border as its p-value is 0.042, showing weaker significance than the

other variables.

The overall regression equation was:

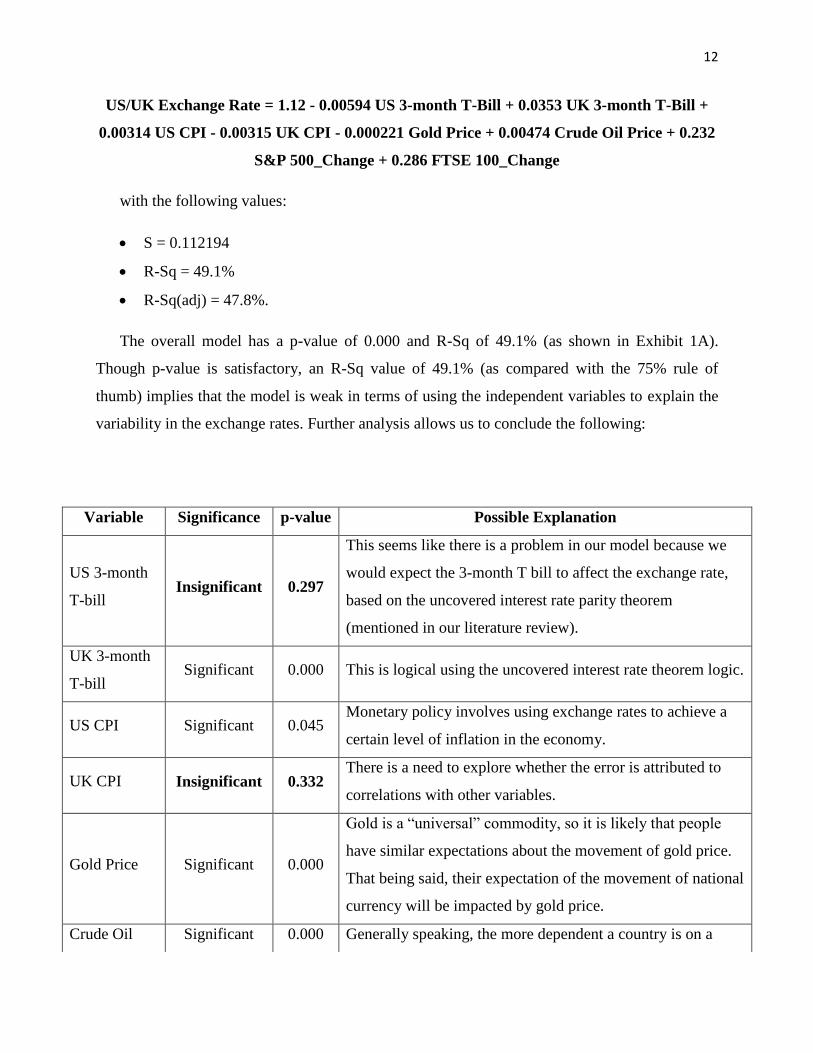

12

US/UK Exchange Rate = 1.12 - 0.00594 US 3-month T-Bill + 0.0353 UK 3-month T-Bill +

0.00314 US CPI - 0.00315 UK CPI - 0.000221 Gold Price + 0.00474 Crude Oil Price + 0.232

S&P 500_Change + 0.286 FTSE 100_Change

with the following values:

S = 0.112194

R-Sq = 49.1%

R-Sq(adj) = 47.8%.

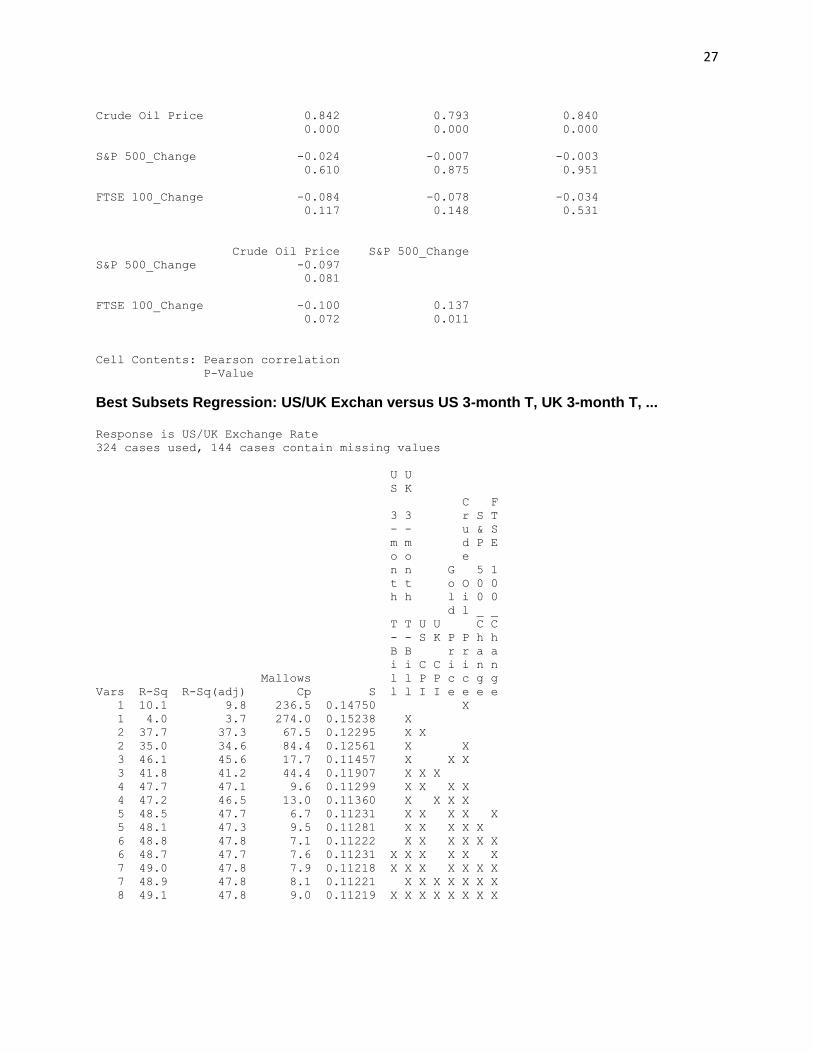

The overall model has a p-value of 0.000 and R-Sq of 49.1% (as shown in Exhibit 1A).

Though p-value is satisfactory, an R-Sq value of 49.1% (as compared with the 75% rule of

thumb) implies that the model is weak in terms of using the independent variables to explain the

variability in the exchange rates. Further analysis allows us to conclude the following:

Variable Significance p-value Possible Explanation

US 3-month

T-bill Insignificant 0.297

This seems like there is a problem in our model because we

would expect the 3-month T bill to affect the exchange rate,

based on the uncovered interest rate parity theorem

(mentioned in our literature review).

UK 3-month

T-bill Significant 0.000 This is logical using the uncovered interest rate theorem logic.

US CPI Significant 0.045 Monetary policy involves using exchange rates to achieve a

certain level of inflation in the economy.

UK CPI Insignificant 0.332 There is a need to explore whether the error is attributed to

correlations with other variables.

Gold Price Significant 0.000

Gold is a “universal” commodity, so it is likely that people

have similar expectations about the movement of gold price.

That being said, their expectation of the movement of national

currency will be impacted by gold price.

Crude Oil Significant 0.000 Generally speaking, the more dependent a country is on a

13

*Correlation among independent variables:

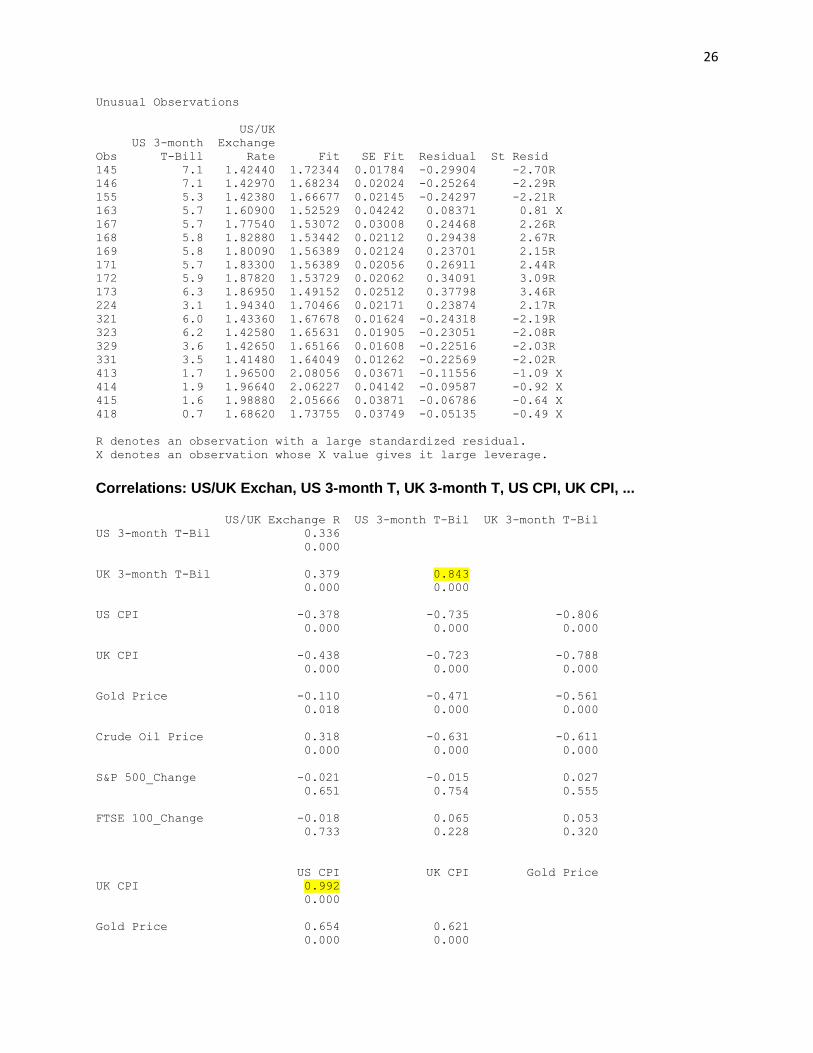

Of all the variables, the most notable and interesting correlations are coming from the US 3-

month T-bill. The US 3-month T-bill is highly correlated with the UK 3-month T-bill by a value

of 0.843. This could possibly indicate how the US and UK respond to each other’s treasury rate

through observing the other country’s monetary policy. The question is, if US and UK 3-month

T-bill were highly correlated, why was the UK 3 month T-Bill significant to the model, whereas

the US 3-month T-Bill failed to do so? The correlation between these two specific variables

indeed weakens the validity of our overall model. The study of literature reviews suggested that

we include both variables in the model. We believe it might have been due to our approach to the

individual variables: there could potentially be other ways of representing these two variables

such as taking the ratio of two countries’ short-term interest rates, taking the difference between

the countries’ interest rates, or taking the ratio of the change in the countries’ interest rates, etc.

In addition, the US 3-month T-bill is highly correlated with US CPI by a value of -0.735,

showing an inverse relationship between the two variables. As interest rates decrease, it is

cheaper to borrow money, hence investment and consumption in the economy increases, which

increases the overall aggregate demand and causes inflation. This would make the CPI index

rise. Similarly, the UK 3-month T-bill and UK CPI have a correlation of -0.788. As seen, interest

20

http://www.investopedia.com/ask/answers/06/forexcommodities.asp

Price primary domestic industry, the stronger the correlation

between the national currency and the industry’s commodity

prices.20

S&P

500_Change Insignificant 0.175

It is possible that this particular stock index was not

representative of the whole economy. Therefore, we cannot

make any conclusion for stock price in general. We would

have needed to calculate a weighted average of all stock

indices in USA.

FTSE

100_Change Significant 0.042

We cannot make a definitive conclusion of stock market in

general from this value only.

14

rates are inversely related to CPI for both countries. In a recent WSJ article, it quotes “The Bank

of England Wednesday said the U.K.'s economy is set to grow more rapidly than it had expected

just three months ago, but stressed that a subdued outlook for inflation means it is still unlikely to

raise interest rates soon21

" This article clearly displays the relationship between the inflation and

interest rate and reinstates our claim of how CPI and interest rate are closely related. Further, the

UK CPI and US CPI are correlated by 0.992, clearly demonstrating how both CPI indexes and

short-term treasury rates are strongly correlated between both these nations.

Another finding is that the Crude Oil Price has a high correlation with US CPI and UK CPI,

0.842 and 0.793 respectively. This can be attributed to the fact that both the US and UK are

importers of crude oil. Import costs of oil affect the transportation and manufacturing industries

and high costs will have spillover effects on overall price increases in the economy.

This model raised curiosity as to why the US 3-month T-bill was not significant as we had

hypothesized. One would assume from previous research that interest rates directly affect

exchange rates, which is why we had hypothesized that both 3-month T-bill of UK and US

would be significant. We wanted to carry out another regression analysis to explore whether the

10 year bond rates for UK and US different effects on the exchange rate for US/UK. Using this

model, we studied it in comparison to our short run 3-month T-bill model.

Model 1B

This model involves the same data set as Model 1A. The only difference is that both the US

and UK 3-month T-bills were substituted by US and UK 10-year treasury rates, respectively. WE

found more supporting results where, the US 10-year treasury rates were now significant. The

regression equation is:

US/UK Exchange Rate = 0.851 + 0.0337 US 10-year Treasury + 0.0267 UK 10-year

Treasury + 0.00627 US CPI - 0.00856 UK CPI - 0.000252 Gold Price + 0.00498 Crude Oil

Price + 0.314 S&P 500_Change + 0.289 FTSE 100_Change

with the following values:

21

http://online.wsj.com/news/articles/SB10001424052702303289904579195292401776098?mod=WSJ_hps_LEFTT

opStories

15

S = 0.117358

R-Sq = 44.3%

R-Sq(adj) = 42.9%.

The only variable that was insignificant in this model was the S&P 500 Change, having a p-

value of 0.081. The insignificance of S&P 500 Change is also reflected in Model 1A. The FTSE

100 Change is once again on a border as its p-value of approximately 0.05 implies a weaker

significance on exchange rates than other variables. From both Model 1 A and 1B, it is fair to say

that the S&P 500 Change and FTSE 100 Change do not contribute to determining the US/UK

exchange rate as much as the other variables. The following table explains our findings from

Model 1B:

22

http://www.investopedia.com/ask/answers/06/forexcommodities.asp

Variable Significance P Possible Explanation

US 10-year

rate Significant 0.008 Adheres to uncovered interest rate parity theorem

UK 10-year

rate Significant 0.004 Adheres to uncovered interest rate parity theorem

US CPI Significant 0.001 Logical using PPP theorem

UK CPI Significant 0.013 Logical using PPP theorem

Gold Price Significant 0.000

Gold is a “universal” commodity, so it is likely that people

have similar expectations about the movement of gold price.

That being said, their expectation of the movement of

national currency will be impacted by gold price.

Crude Oil

Price Significant 0.000

Generally speaking, the more dependent a country is on a

primary domestic industry, the stronger the correlation

between the national currency and the industry’s commodity

prices22

S&P

500_Change Insignificant 0.081

It is possibly not relevant to predicting the exchange rate

since it is also insignificant in Model 1A using short term T-

bill rate.

16

Analyzing the correlations, we see similarities in both Model 1A and 1B. In model 1B there

is once again a high correlation between US and UK 10-year treasury rate of 0.865. An article

talks about this in the WSJ in 2013, “The spread between ten-year treasury yields and those of

their British equivalents, gilts, is hovering at 2-year highs. So the pound gets support from all

angles, form the hard numbers, from rate differentials and from activist central bank23

” (From the

article: "Sterling Climbs, but what about those imbalances?" by David Cottle

Once again US 10-year rate is related to US CPI by -0.776 and UK 10 year rate is related to

UK CPI by -0.935, once again showing the negative relationship of interest and CPI. A finding

that is seen in the previous model as well, to add to its credibility.

UK CPI and US CPI are correlated by 0.992 establishing that irrespective of the time frame

of interest rates the two nations will affect each other’s CPI strongly.

MODEL 2A AND MODEL 2B

Model 1A and 1B bring us to an important question: do short term T-bills and long term 10-

year treasury bonds have different effects on the exchange rate from the above regressions

ceterus paribus? Using the uncovered interest rate parity formula we now try and predict the

future exchange rate, where we use the interest rate of US and UK and the current spot rate to

find E(S) – which is the predicted spot rate the following year.

𝑖

𝑖

23

http://blogs.wsj.com/moneybeat/2013/09/13/sterling-climbs-but-what-about-those-

imbalances/?KEYWORDS=British+Pound)

FTSE

100_Change Significant 0.050

This value is very close to the p value at 95% level of

significance making it difficult to make any conclusion about

the relationship between the FTSE 100 change and the

exchange rate.

17

The formula gives us a calculated value for the exchange rate. Meanwhile, our regression

equation also give us a value which is an estimated value based on the assumptions of our model.

We calculate the error as:

𝑒 𝑒 𝑛 𝑒 𝑒 𝑒 𝑛 𝑒 𝑒

𝑒 𝑒 𝑒 𝑛 𝑒 𝑒

It is fair to assume that larger the percentage error, the more inaccurate model 1A and 1B are,

and perhaps such error could possibly be attributed to one of the variables we used in our initial

regression models. Hence, we decided to run two other regression models, which we called

Model 2A (for short term 3-month T-bill) and Model 2B (for long term 10-year treasury), with

percentage error of spot exchange rate as out dependent variable. Meanwhile, we kept all

independent variables the same as model 1A and 1B to determine which variables would me

more significant to the percentage error of spot exchange rate.

Model 2A:

This model examined the relationship between the error of short-term spot exchange rate

against the following variables: US and UK 3 month T-bills, US and UK CPI, Gold Price, Crude

Oil Price, S&P 500 change and FTSE 100 change.

Studying the p-values from the regression it turned out that the only two variables that could

be used to explain the error in exchange rates are US and UK 3-month treasury bills. The other

variables all proved to be unable to account for the discrepancy between predicted exchange rate

and observed exchange rate. Logically, this finding gave us some insight in relation to the model

1A, which had previously revealed that short-term treasury rates, particularly US 3-month T-bill

rates, did not contribute to explaining the exchange rate. However, there remained one concern if

we solely went with this logic. As we recalled, the UK CPI were insignificant in model 1A, so

theoretically, we expected this variable to prove its significance in model 2A. Having been aware

of the “unusual behavior” of UK CPI, we understood that we would have to conduct further

analysis/ research to find out why UK CPI did not meet any of our expectation.

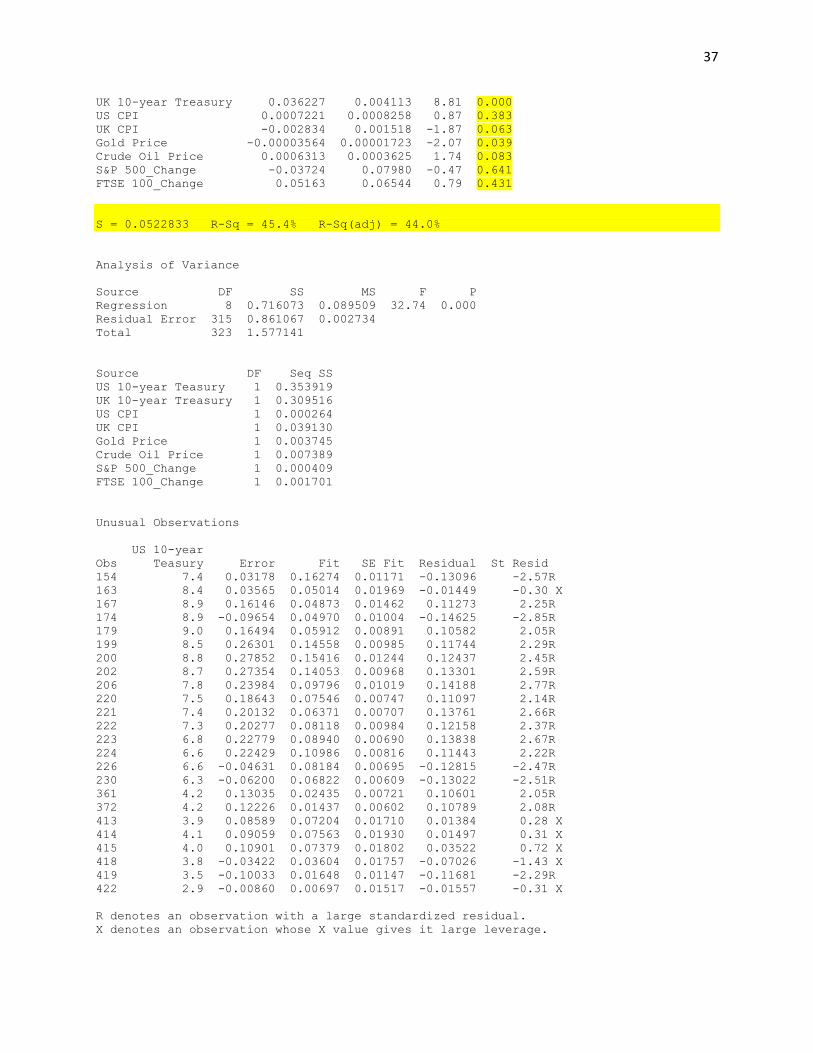

Model 2B:

Our findings from model 1B suggested that 10-year treasury rates for both the US and UK

had an impact on the exchange rate. With this in mind, we hoped to see these two variables as

insignificant in model 2B. However, the predictor variables that turned out to be significant

18

included US and UK 10-year Treasury, US and UK CPI, and S&P 500. At first sight, this

seemed contradictory with what we had hypothesized given the result and logic derived from

model 2A. However, both findings from Model 2A and 2B were assuring in a sense that they

“claimed” treasury rates, regardless of maturity term, as being able to explain the error between

observed spot exchange rate and calculated spot exchange rate. Strictly and hypothetically

speaking, treasury rates should not account for the error between the observed and calculated

spot exchange rates, because they “determine” the spot exchange rate, based on the uncovered

interest rate parity.

This seemingly contradiction could be attributed to the different rates at which US and UK

treasury rates changed. The formula associated with the uncovered interest rate parity only gave

us the spot exchange rate based on the primary assumptions of capital mobility and perfect

substitutability of domestic and foreign assets24

. For example, if investors expect the rate of

return to be higher in the US, this would attract capital into the U.S., driving US interest rates

down and moving UK interest rates up, causing a dollar appreciation against the British Pound.

This process continues until the URIP equation holds again. However, in reality, investors can

actually earn arbitrage profits by borrowing in a country with lower interest rates, exchange for

foreign currency, and investing in a foreign country with higher interest rates, while allowing for

any losses (or gains) from exchanging back to their domestic currency at maturity25

. This

explains the deviation from UIRP, which in turn provides an insight into why there were

differentials in our observed and calculated spot exchange rates. In addition, the UIRP does not

specify whether the interest rates used for the equation are short-term or long-term rates. For this

reason, we can safely assume that the lack of compensating capital flows also have similar

effects on both 3-month T-Bill rates and 10-year treasury rates in causing the differentials in

observed and calculated spot exchange rates.

24

http://arxiv.org/abs/1303.4314 25

http://arxiv.org/abs/1303.4314

19

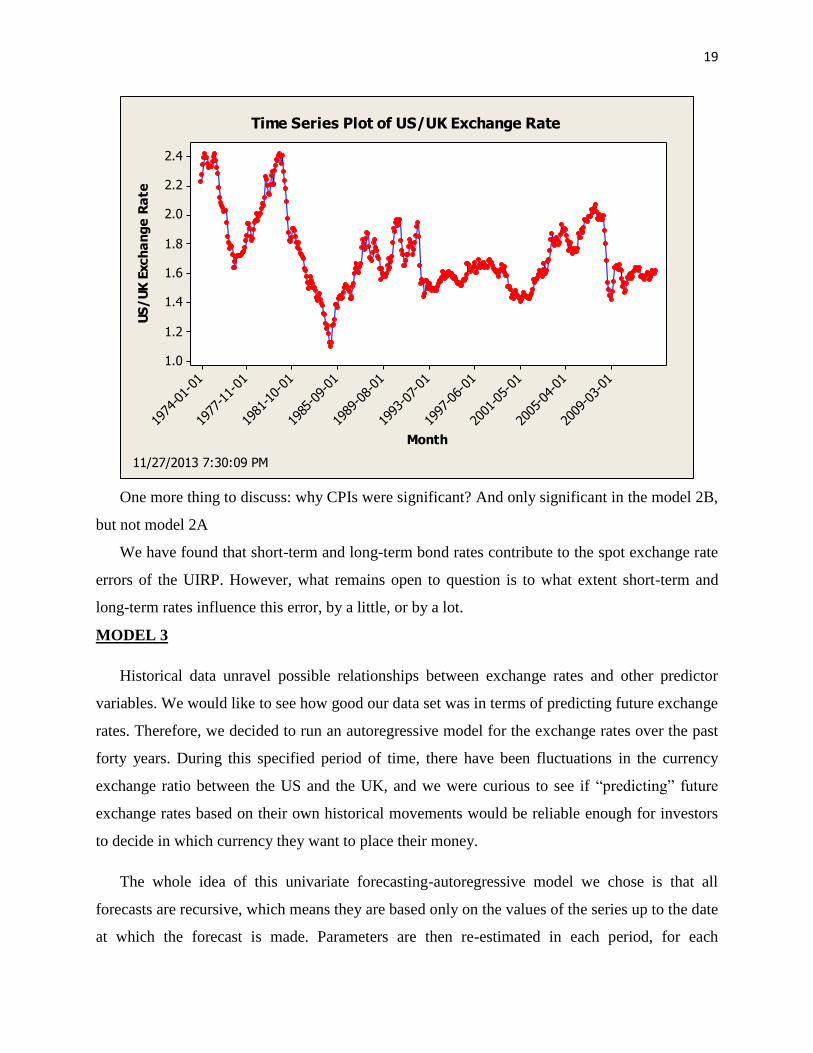

2009

-03-01

2005

-04-01

2001

-05-

01

1997

-06-

01

1993

-07-01

1989

-08-01

1985

-09-01

1981

-10-

01

1977

-11-

01

1974

-01-

01

2.4

2.2

2.0

1.8

1.6

1.4

1.2

1.0

Month

US

/U

K E

xch

an

ge

Ra

te

Time Series Plot of US/UK Exchange Rate

11/27/2013 7:30:09 PM

One more thing to discuss: why CPIs were significant? And only significant in the model 2B,

but not model 2A

We have found that short-term and long-term bond rates contribute to the spot exchange rate

errors of the UIRP. However, what remains open to question is to what extent short-term and

long-term rates influence this error, by a little, or by a lot.

MODEL 3

Historical data unravel possible relationships between exchange rates and other predictor

variables. We would like to see how good our data set was in terms of predicting future exchange

rates. Therefore, we decided to run an autoregressive model for the exchange rates over the past

forty years. During this specified period of time, there have been fluctuations in the currency

exchange ratio between the US and the UK, and we were curious to see if “predicting” future

exchange rates based on their own historical movements would be reliable enough for investors

to decide in which currency they want to place their money.

The whole idea of this univariate forecasting-autoregressive model we chose is that all

forecasts are recursive, which means they are based only on the values of the series up to the date

at which the forecast is made. Parameters are then re-estimated in each period, for each

20

forecasting model, using data from the beginning of the sample through the current forecasting

date. For forecasts that entail data-based model selection, the order of the model is also selected

recursively, and thus can change over the sample as new information is added to the forecast data

set. We chose the period between 1973-1 and 1982-12 as our “burning” period, whose

terminology is “estimation subsample”. This “burning” period created a preliminary

autoregressive model which provided us with the coefficients for forecasting purposes.

For the time series regression to be externally valid, it is essential to assume stationary,

which says that history is relevant26

. Many macroeconomic time series appear to be non-

stationary in the sense of having one or more unit roots, which should explain why we transform

the real value of exchange rates into exchange rate returns by taking their first difference27

.

We proceeded with this model by calculating the exchange rate returns between 1973-1 and

2012-12. This was done by taking the difference between the natural logarithm of one month’s

exchange rate and the natural logarithm of the previous month’s exchange rate. The calculated

exchange rate returns were then used as our dependent variable, which we labelled as Y1, Y2…

Yt-1, Yt (t: the observations on the time series random variable Y).

The autoregressive model that we chose does not formulate causal interpretations. It simply

performs a forecasting function for out-of-sample data. In this model, Yt (value of Y in period t)

is regressed against its own lagged values. The number of lags used as regressors is called the

order of the autoregression. In a first order autoregression, Yt is regressed against Yt–1. In a pth

order autoregression, Yt is regressed against Yt–1, Yt–2,…, Yt–p. For the purpose of simplicity, we

solely used the first order autoregression to forecast the exchange rate returns.

The population autoregressive model is28

:

The above model is characterized by:

and do not have causal interpretations

26

http://www.princeton.edu/~mwatson/papers/PhillipsCurveInflationForecasts_Sept2008.pdf 27

http://www.princeton.edu/~mwatson/papers/Marcellino_Stock_Watson_FinalVersion_hstep.pdf 28

http://www.econ.brown.edu/fac/Frank_Kleibergen/ec163/ch14_slides_1.pdf

21

If then is not useful for forecasting

The autoregressive model can be estimated by OLS regression of against

Testing vs. provides a test of the hypothesis that is not useful for

forecasting

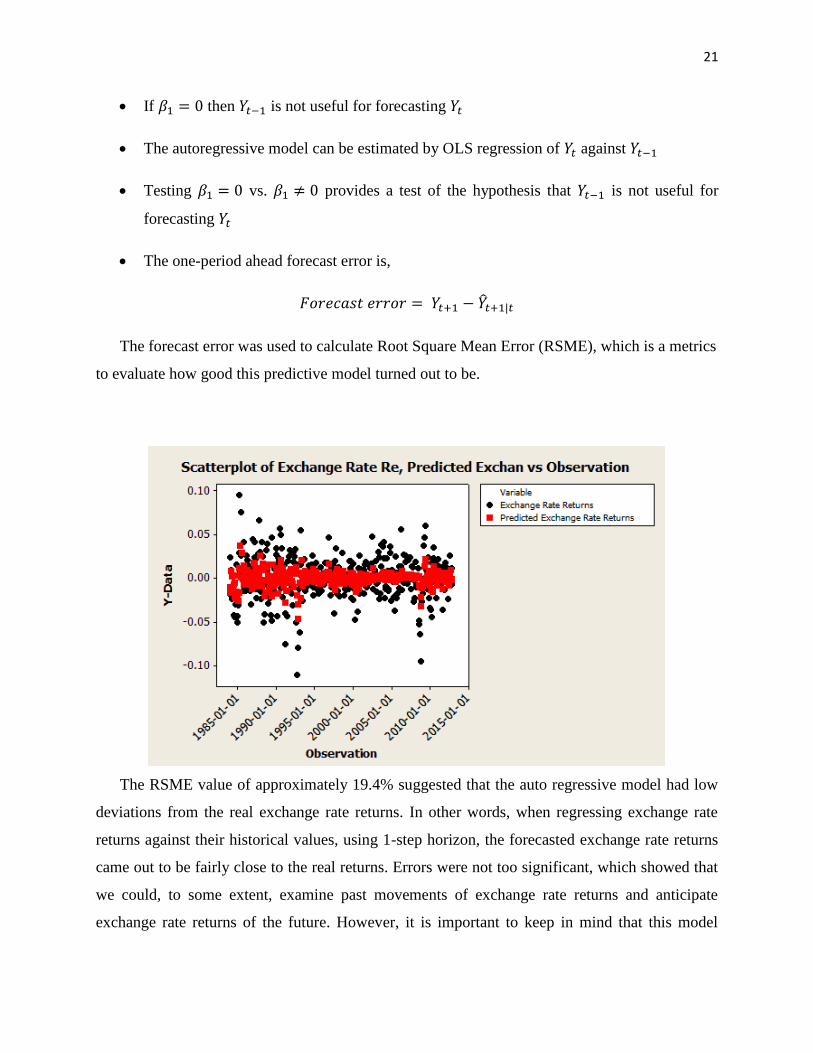

The one-period ahead forecast error is,

𝑒 𝑒 ̂

The forecast error was used to calculate Root Square Mean Error (RSME), which is a metrics

to evaluate how good this predictive model turned out to be.

The RSME value of approximately 19.4% suggested that the auto regressive model had low

deviations from the real exchange rate returns. In other words, when regressing exchange rate

returns against their historical values, using 1-step horizon, the forecasted exchange rate returns

came out to be fairly close to the real returns. Errors were not too significant, which showed that

we could, to some extent, examine past movements of exchange rate returns and anticipate

exchange rate returns of the future. However, it is important to keep in mind that this model

22

demonstrated insignificant errors only when it was used to forecast the exchange rate returns of

one period ahead ( in this case, one month ahead). It is unlikely that the model will hold its

validity in forecasting exchange rate returns of more than one month ahead.

The graph that features the time series of real exchange rate returns and forecasted exchange

rate returns reveals a pattern. It seems that forecasted exchange rate returns are distributed more

densely around the center line (the mean exchange rate returns). This pattern of distribution

could be interpreted as a sign of the predictive model being consistent; meaning the coefficients

which had been re-estimated (for every month period) managed to forecast the exchange rate

returns of the following months at a consistently accurate rate. In addition, the model did not

appear to have any noticeable outliers. Though it is ideal to have a model free of outliers, it is

essential to pay attention to unusual observations. Looking at the real exchange rates data, there

are a few observations where exchange rates return were unusually high or low. The model,

however, did not appear to reflect these unusual observations. We believe this is where we need

to be concerned about the model. The auto regression somehow failed to take into account the

months where exchange rate returns behaved unusually. For further study, this concern needs to

be addressed because at this point, we are not certain about the possibility of the model failing to

incorporate the unusual real exchange rate returns and reflect them in the forecasted exchange

rate returns. If an investor were to monitor the current real exchange rate but note that the current

rate has been unusual, he would not have any confidence in using this model to make educated

guesses about how the exchange rate would be in the upcoming month.

23

Works Cited

Ames, Matthew. "Reinvestigating the Uncovered Interest Rate Parity Puzzle via Analysis of

Multivariate Tail Dependence in Currency Carry Trades." Reinvestigating the Uncovered

Interest Rate Parity Puzzle via Analysis of Multivariate Tail Dependence in Currency

Carry Trades. Cornell, Mar. 2013. Web. 4 Dec. 2013.

"Business Is Great." Business Is Great. British Embassy, 2012. Web. 04 Dec. 2013.

Brittain, Alex. "BOE Opens Door to Earlier Rate Rise." BOE Opens Door to Earlier Rate Rise.

N.p., 13 Nov. 2013. Web. 4 Dec. 2013.

"Covered Interest Rate Parity." Investopedia. N.p., n.d. Web. 03 Dec. 2013.

Cottle, David. "Sterling Climbs, But What About Those Imbalances?" Sterling Climbs, But What

About Those Imbalances? WSJ, 13 Sept. 2013. Web. 4 Dec. 2013.

Desmet, Klaus. "Notes on Uncovered Interest Parity." Notes on Uncovered Interest Parity. N.p.,

2000. Web. 3 Dec. 2013.

Dimitrova, Desislava. "The Relationship between Exchange Rates and Stock Prices: Studied in a

Multivariate Model." N.p., 14 Aug. 2005. Web. 20 Nov. 2013.

Garber, Peter. "The Collapse of the Bretton Woods Fixed Exchange Rate System." The Collapse

of the Bretton Woods Fixed Exchange Rate System. University of Chicago Press, Oct.

1993. Web.

"Fisher Effect." Investopedia. N.p., n.d. Web. 03 Dec. 2013.

"FTSE 100." - London Stock Exchange. N.p., n.d. Web. 20 Nov. 2013.

"John Jay's Treaty, 1794–95 - 1784–1800 - Milestones." John Jay's Treaty, 1794–95 - 1784–

1800 - Milestones - Office of the Historian. N.p., 2010. Web. 01 Dec. 2013.

Kleibergen, Frank. "Introduction to Time Series Regression and Forecasting." Introduction to

Time Series Regression and Forecasting. N.p., 2010. Web.

24

Marcellino, Massimiliano. "A Comparison of Direct and Iterated Multistep AR Methods for

Forecasting Macroeconomic Time Series." A Comparison of Direct and Iterated

Multistep AR Methods for Forecasting Macroeconomic Time Series. Princeton, Feb.

2004. Web.

McCallum, Bennett T., and Edward Nelson (2000). “Monetary Policy for an Open Economy: An

Alternative Framework with Optimizing Agents and Sticky Prices,”Oxford Review of

Economic Policy

O'connor, Fergal. "Gold’s Negative Relationship with the US Dollar." Gold’s Negative

Relationship with the US Dollar. N.p., Feb. 2012. Web.

Pettinger, Tejvan R. "Factors Which Influence the Exchange Rate." Economics Help. N.p., Jan.

2009. Web. 03 Dec. 2013.

"Purchasing Power Parity - PPP." Investopedia. N.p., 2010. Web. 03 Dec. 2013.

Rush, Mark. "Real Exchange Rates under the Gold Standard." Real Exchange Rates under the

Gold Standard. N.p., Oct. 1990. Web. 3 Dec. 2013.

Schreyer, Paul. "Purchasing Power Parities – Measurement and Uses." Purchasing Power Parities

– Measurement and Uses. N.p., Web. March 2002.

Sill, Keith. "The Cyclical Volatility of Interest Rates." The Cyclical Volatility of Interest Rates.

N.p., 1996. Web. 03 Dec. 2013.

Sjaastada, Larry. "The Price of Gold and the Exchange Rates: Once Again." The Price of Gold

and the Exchange Rates: Once Again. N.p., June 2008. Web.

"S&P 500 Equity Indices." S&P Dow Jones Indices. McGraw Hill Financial, 28 Mar. 2013.

Web. 20 Nov. 2013.

Stock, James. "Phillips Curve Inflation Forecasts." Phillips Curve Inflation Forecasts. N.p., 2012.

Web.

"What is the Relationship Between the Exchange Rate and Oil Prices?." Dale ORR Economic

Insight. N.p. ,n.d. Web.18 November 2013.

25

Exhibits

Model 1A: US/UK Exchange Rate against the following variables:

US 3-month T-bill

UK 3-month T-bill

US CPI

UK CPI

Gold Price

Crude Oil Price

S&P 500 Change

FTSE 100 Change Regression Analysis: US/UK Exchan versus US 3-month T, UK 3-month T, ... The regression equation is

US/UK Exchange Rate = 1.12 - 0.00594 US 3-month T-Bill

+ 0.0353 UK 3-month T-Bill + 0.00314 US CPI

- 0.00315 UK CPI - 0.000221 Gold Price

+ 0.00474 Crude Oil Price + 0.232 S&P 500_Change

+ 0.286 FTSE 100_Change

324 cases used, 144 cases contain missing values

Predictor Coef SE Coef T P

Constant 1.1204 0.1082 10.36 0.000

US 3-month T-Bill -0.005943 0.005692 -1.04 0.297

UK 3-month T-Bill 0.035261 0.004784 7.37 0.000

US CPI 0.003140 0.001558 2.01 0.045

UK CPI -0.003150 0.003243 -0.97 0.332

Gold Price -0.00022082 0.00003758 -5.88 0.000

Crude Oil Price 0.0047361 0.0007525 6.29 0.000

S&P 500_Change 0.2324 0.1710 1.36 0.175

FTSE 100_Change 0.2855 0.1400 2.04 0.042

S = 0.112194 R-Sq = 49.1% R-Sq(adj) = 47.8%

Analysis of Variance

Source DF SS MS F P

Regression 8 3.82691 0.47836 38.00 0.000

Residual Error 315 3.96507 0.01259

Total 323 7.79198

Source DF Seq SS

US 3-month T-Bill 1 0.08862

UK 3-month T-Bill 1 0.38466

US CPI 1 2.47597

UK CPI 1 0.31082

Gold Price 1 0.02677

Crude Oil Price 1 0.45649

S&P 500_Change 1 0.03122

FTSE 100_Change 1 0.05237

26

Unusual Observations

US/UK

US 3-month Exchange

Obs T-Bill Rate Fit SE Fit Residual St Resid

145 7.1 1.42440 1.72344 0.01784 -0.29904 -2.70R

146 7.1 1.42970 1.68234 0.02024 -0.25264 -2.29R

155 5.3 1.42380 1.66677 0.02145 -0.24297 -2.21R

163 5.7 1.60900 1.52529 0.04242 0.08371 0.81 X

167 5.7 1.77540 1.53072 0.03008 0.24468 2.26R

168 5.8 1.82880 1.53442 0.02112 0.29438 2.67R

169 5.8 1.80090 1.56389 0.02124 0.23701 2.15R

171 5.7 1.83300 1.56389 0.02056 0.26911 2.44R

172 5.9 1.87820 1.53729 0.02062 0.34091 3.09R

173 6.3 1.86950 1.49152 0.02512 0.37798 3.46R

224 3.1 1.94340 1.70466 0.02171 0.23874 2.17R

321 6.0 1.43360 1.67678 0.01624 -0.24318 -2.19R

323 6.2 1.42580 1.65631 0.01905 -0.23051 -2.08R

329 3.6 1.42650 1.65166 0.01608 -0.22516 -2.03R

331 3.5 1.41480 1.64049 0.01262 -0.22569 -2.02R

413 1.7 1.96500 2.08056 0.03671 -0.11556 -1.09 X

414 1.9 1.96640 2.06227 0.04142 -0.09587 -0.92 X

415 1.6 1.98880 2.05666 0.03871 -0.06786 -0.64 X

418 0.7 1.68620 1.73755 0.03749 -0.05135 -0.49 X

R denotes an observation with a large standardized residual.

X denotes an observation whose X value gives it large leverage.

Correlations: US/UK Exchan, US 3-month T, UK 3-month T, US CPI, UK CPI, ... US/UK Exchange R US 3-month T-Bil UK 3-month T-Bil

US 3-month T-Bil 0.336

0.000

UK 3-month T-Bil 0.379 0.843

0.000 0.000

US CPI -0.378 -0.735 -0.806

0.000 0.000 0.000

UK CPI -0.438 -0.723 -0.788

0.000 0.000 0.000

Gold Price -0.110 -0.471 -0.561

0.018 0.000 0.000

Crude Oil Price 0.318 -0.631 -0.611

0.000 0.000 0.000

S&P 500_Change -0.021 -0.015 0.027

0.651 0.754 0.555

FTSE 100_Change -0.018 0.065 0.053

0.733 0.228 0.320

US CPI UK CPI Gold Price

UK CPI 0.992

0.000

Gold Price 0.654 0.621

0.000 0.000

27

Crude Oil Price 0.842 0.793 0.840

0.000 0.000 0.000

S&P 500_Change -0.024 -0.007 -0.003

0.610 0.875 0.951

FTSE 100_Change -0.084 -0.078 -0.034

0.117 0.148 0.531

Crude Oil Price S&P 500_Change

S&P 500_Change -0.097

0.081

FTSE 100_Change -0.100 0.137

0.072 0.011

Cell Contents: Pearson correlation

P-Value

Best Subsets Regression: US/UK Exchan versus US 3-month T, UK 3-month T, ... Response is US/UK Exchange Rate

324 cases used, 144 cases contain missing values

U U

S K

C F

3 3 r S T

- - u & S

m m d P E

o o e

n n G 5 1

t t o O 0 0

h h l i 0 0

d l _ _

T T U U C C

- - S K P P h h

B B r r a a

i i C C i i n n

Mallows l l P P c c g g

Vars R-Sq R-Sq(adj) Cp S l l I I e e e e

1 10.1 9.8 236.5 0.14750 X

1 4.0 3.7 274.0 0.15238 X

2 37.7 37.3 67.5 0.12295 X X

2 35.0 34.6 84.4 0.12561 X X

3 46.1 45.6 17.7 0.11457 X X X

3 41.8 41.2 44.4 0.11907 X X X

4 47.7 47.1 9.6 0.11299 X X X X

4 47.2 46.5 13.0 0.11360 X X X X

5 48.5 47.7 6.7 0.11231 X X X X X

5 48.1 47.3 9.5 0.11281 X X X X X

6 48.8 47.8 7.1 0.11222 X X X X X X

6 48.7 47.7 7.6 0.11231 X X X X X X

7 49.0 47.8 7.9 0.11218 X X X X X X X

7 48.9 47.8 8.1 0.11221 X X X X X X X

8 49.1 47.8 9.0 0.11219 X X X X X X X X

28

Stepwise Regression: US/UK Exchan versus US 3-month T, UK 3-month T, ... Alpha-to-Enter: 0.15 Alpha-to-Remove: 0.15

Response is US/UK Exchange Rate on 8 predictors, with N = 324

N(cases with missing observations) = 144 N(all cases) = 468

Step 1 2 3 4 5

Constant 1.587 1.345 1.410 1.083 1.092

Crude Oil Price 0.00174 0.00384 0.00642 0.00489 0.00509

T-Value 6.01 12.36 15.09 7.65 7.92

P-Value 0.000 0.000 0.000 0.000 0.000

UK 3-month T-Bill 0.0270 0.0231 0.0331 0.0328

T-Value 11.09 10.13 8.49 8.45

P-Value 0.000 0.000 0.000 0.000

Gold Price -0.00026 -0.00022 -0.00023

T-Value -8.12 -6.62 -6.88

P-Value 0.000 0.000 0.000

US CPI 0.00181 0.00174

T-Value 3.16 3.05

P-Value 0.002 0.003

FTSE 100_Change 0.31

T-Value 2.21

P-Value 0.028

S 0.147 0.126 0.115 0.113 0.112

R-Sq 10.10 35.00 46.10 47.73 48.52

R-Sq(adj) 9.82 34.59 45.59 47.07 47.71

Mallows Cp 236.5 84.4 17.7 9.6 6.7

4

2

0

-2

3210-1-2-3

Sta

nd

ard

ize

d R

esid

ua

l

Score

2.101.951.801.651.50

4

2

0

-2

Fitted Value

Sta

nd

ard

ize

d R

esid

ua

l

3210-1-2

45

30

15

0

Standardized Residual

Fre

qu

en

cy

450400350300250200150100501

4

2

0

-2

Observation Order

Sta

nd

ard

ize

d R

esid

ua

l

Normal Probability Plot Versus Fits

Histogram Versus Order

Residual Plots for US/UK Exchange Rate

11/19/2013 10:26:49 PM

29

Model 1B: US/UK Exchange Rate against the following variables:

US 10-year treasury rate

UK 10-year treasury rate

US CPI

UK CPI

Gold Price

Crude Oil Price

S&P 500 Change

FTSE 100 Change

Regression Analysis: Error versus US CPI, UK CPI, ... The regression equation is

Error = 0.294 - 0.00130 US CPI - 0.00100 UK CPI - 0.000027 Gold Price

+ 0.00140 Crude Oil Price - 0.0421 S&P 500_Change

+ 0.103 FTSE 100_Change

324 cases used, 144 cases contain missing values

Predictor Coef SE Coef T P

Constant 0.29449 0.02337 12.60 0.000

US CPI -0.0012962 0.0007932 -1.63 0.103

UK CPI -0.000998 0.001674 -0.60 0.551

Gold Price -0.00002748 0.00001841 -1.49 0.136

Crude Oil Price 0.0014035 0.0003603 3.89 0.000

S&P 500_Change -0.04212 0.08876 -0.47 0.635

FTSE 100_Change 0.10259 0.07275 1.41 0.159

S = 0.0583422 R-Sq = 31.6% R-Sq(adj) = 30.3%

Analysis of Variance

Source DF SS MS F P

Regression 6 0.498133 0.083022 24.39 0.000

Residual Error 317 1.079007 0.003404

Total 323 1.577141

Source DF Seq SS

US CPI 1 0.379632

UK CPI 1 0.046001

Gold Price 1 0.017450

Crude Oil Price 1 0.047908

S&P 500_Change 1 0.000373

FTSE 100_Change 1 0.006769

Unusual Observations

Obs US CPI Error Fit SE Fit Residual St Resid

30

163 114 0.03565 0.08342 0.02150 -0.04777 -0.88 X

174 118 -0.09654 0.09873 0.00901 -0.19527 -3.39R

193 128 0.20381 0.08465 0.00839 0.11915 2.06R

197 129 0.19700 0.07166 0.00816 0.12534 2.17R

198 130 0.19440 0.06801 0.00847 0.12640 2.19R

199 131 0.26301 0.08215 0.00548 0.18086 3.11R

200 132 0.27852 0.09680 0.01064 0.18172 3.17R

202 133 0.27354 0.09997 0.00846 0.17357 3.01R

205 135 0.20920 0.08229 0.00533 0.12692 2.18R

206 135 0.23984 0.06985 0.01032 0.16999 2.96R

216 138 0.19075 0.05889 0.00705 0.13186 2.28R

220 139 0.18643 0.05798 0.00794 0.12844 2.22R

221 140 0.20132 0.05890 0.00784 0.14242 2.46R

222 140 0.20277 0.07597 0.01096 0.12680 2.21R

223 141 0.22779 0.06684 0.00701 0.16095 2.78R

224 141 0.22429 0.06690 0.00699 0.15738 2.72R

230 143 -0.06200 0.05797 0.00552 -0.11997 -2.07R

317 171 -0.09083 0.03033 0.00719 -0.12115 -2.09R

360 186 0.11586 -0.00076 0.00687 0.11663 2.01R

361 186 0.13035 0.00558 0.00752 0.12477 2.16R

372 192 0.12226 0.00534 0.00656 0.11691 2.02R

413 215 0.08589 0.07590 0.01856 0.00999 0.18 X

414 217 0.09059 0.06950 0.02115 0.02109 0.39 X

415 219 0.10901 0.06850 0.01975 0.04051 0.74 X

416 219 -0.00500 0.05310 0.01519 -0.05810 -1.03 X

418 217 -0.03422 0.00447 0.01916 -0.03869 -0.70 X

422 213 -0.00860 -0.04077 0.01567 0.03217 0.57 X

452 226 0.00538 -0.02690 0.01626 0.03228 0.58 X

R denotes an observation with a large standardized residual.

X denotes an observation whose X value gives it large leverage.

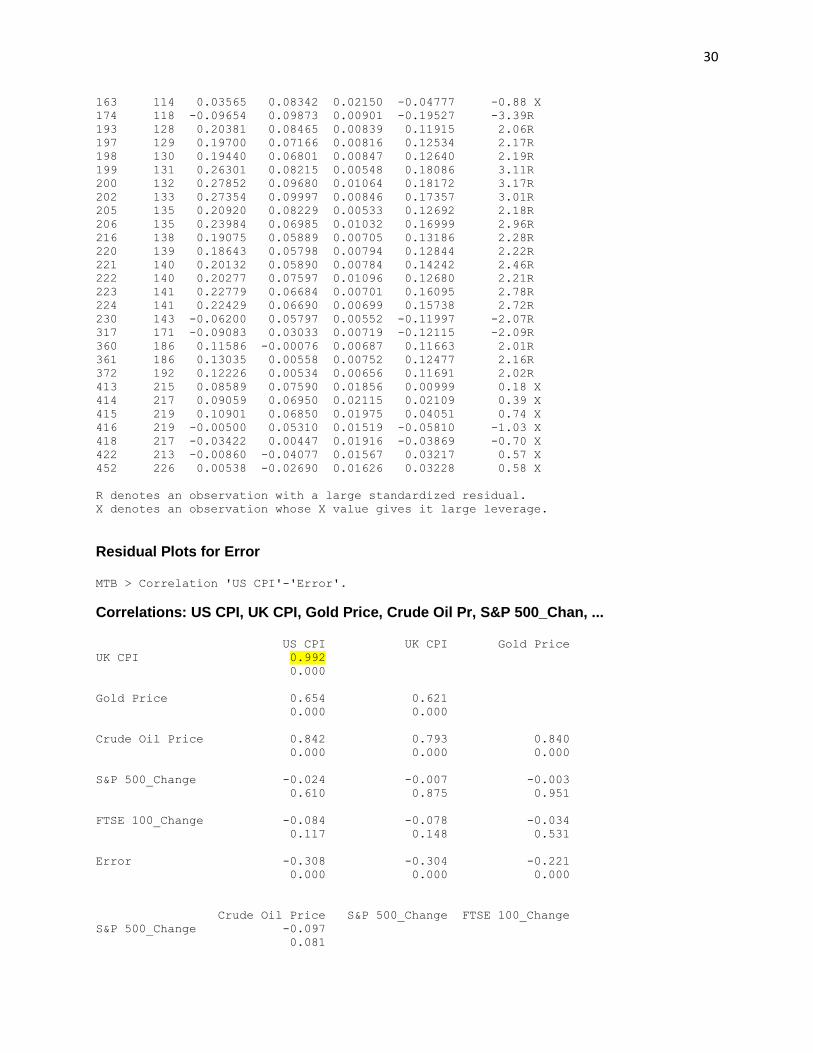

Residual Plots for Error MTB > Correlation 'US CPI'-'Error'.

Correlations: US CPI, UK CPI, Gold Price, Crude Oil Pr, S&P 500_Chan, ... US CPI UK CPI Gold Price

UK CPI 0.992

0.000

Gold Price 0.654 0.621

0.000 0.000

Crude Oil Price 0.842 0.793 0.840

0.000 0.000 0.000

S&P 500_Change -0.024 -0.007 -0.003

0.610 0.875 0.951

FTSE 100_Change -0.084 -0.078 -0.034

0.117 0.148 0.531

Error -0.308 -0.304 -0.221

0.000 0.000 0.000

Crude Oil Price S&P 500_Change FTSE 100_Change

S&P 500_Change -0.097

0.081

31

FTSE 100_Change -0.100 0.137

0.072 0.011

Error -0.280 0.095 0.056

0.000 0.041 0.299

Cell Contents: Pearson correlation

P-Value

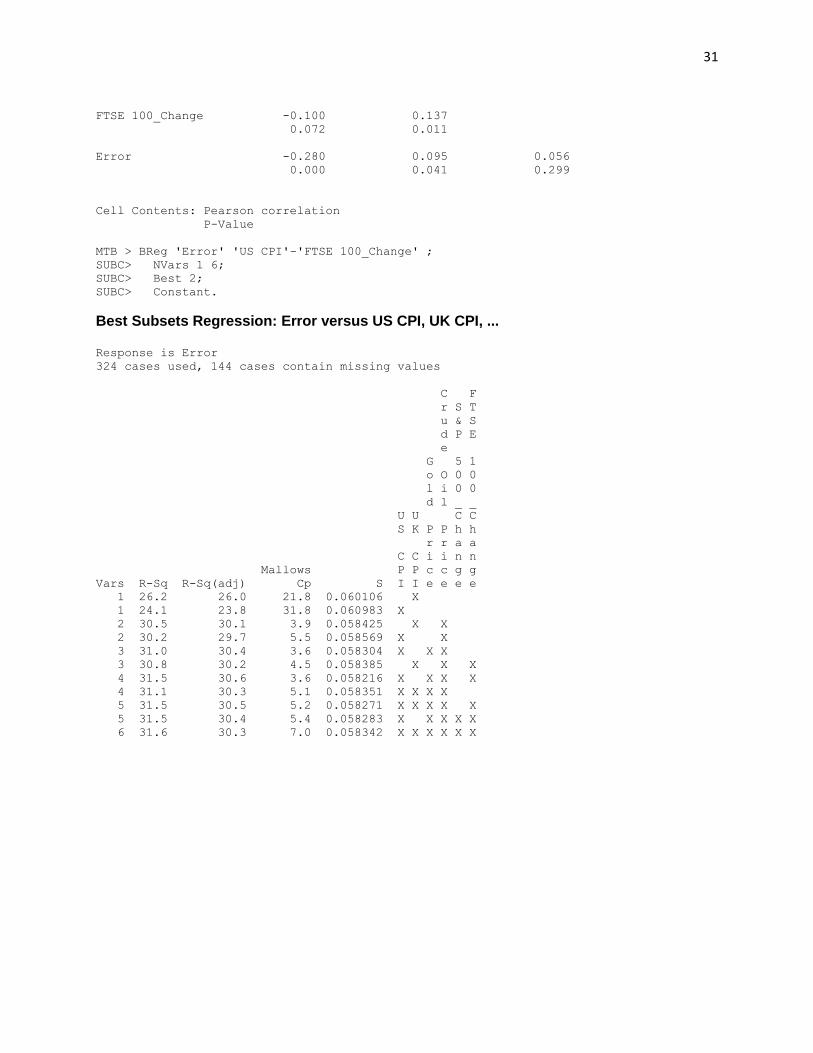

MTB > BReg 'Error' 'US CPI'-'FTSE 100_Change' ;

SUBC> NVars 1 6;

SUBC> Best 2;

SUBC> Constant.

Best Subsets Regression: Error versus US CPI, UK CPI, ... Response is Error

324 cases used, 144 cases contain missing values

C F

r S T

u & S

d P E

e

G 5 1

o O 0 0

l i 0 0

d l _ _

U U C C

S K P P h h

r r a a

C C i i n n

Mallows P P c c g g

Vars R-Sq R-Sq(adj) Cp S I I e e e e

1 26.2 26.0 21.8 0.060106 X

1 24.1 23.8 31.8 0.060983 X

2 30.5 30.1 3.9 0.058425 X X

2 30.2 29.7 5.5 0.058569 X X

3 31.0 30.4 3.6 0.058304 X X X

3 30.8 30.2 4.5 0.058385 X X X

4 31.5 30.6 3.6 0.058216 X X X X

4 31.1 30.3 5.1 0.058351 X X X X

5 31.5 30.5 5.2 0.058271 X X X X X

5 31.5 30.4 5.4 0.058283 X X X X X

6 31.6 30.3 7.0 0.058342 X X X X X X

32

2

0

-2

-4

3210-1-2-3

Sta

nd

ard

ize

d R

esid

ua

l

Score

0.100.050.00-0.05

2

0

-2

-4

Fitted Value

Sta

nd

ard

ize

d R

esid

ua

l

2.41.20.0-1.2-2.4

60

40

20

0

Standardized Residual

Fre

qu

en

cy

450400350300250200150100501

2

0

-2

-4

Observation Order

Sta

nd

ard

ize

d R

esid

ua

l

Normal Probability Plot Versus Fits

Histogram Versus Order

Residual Plots for Error

11/19/2013 11:30:36 PM

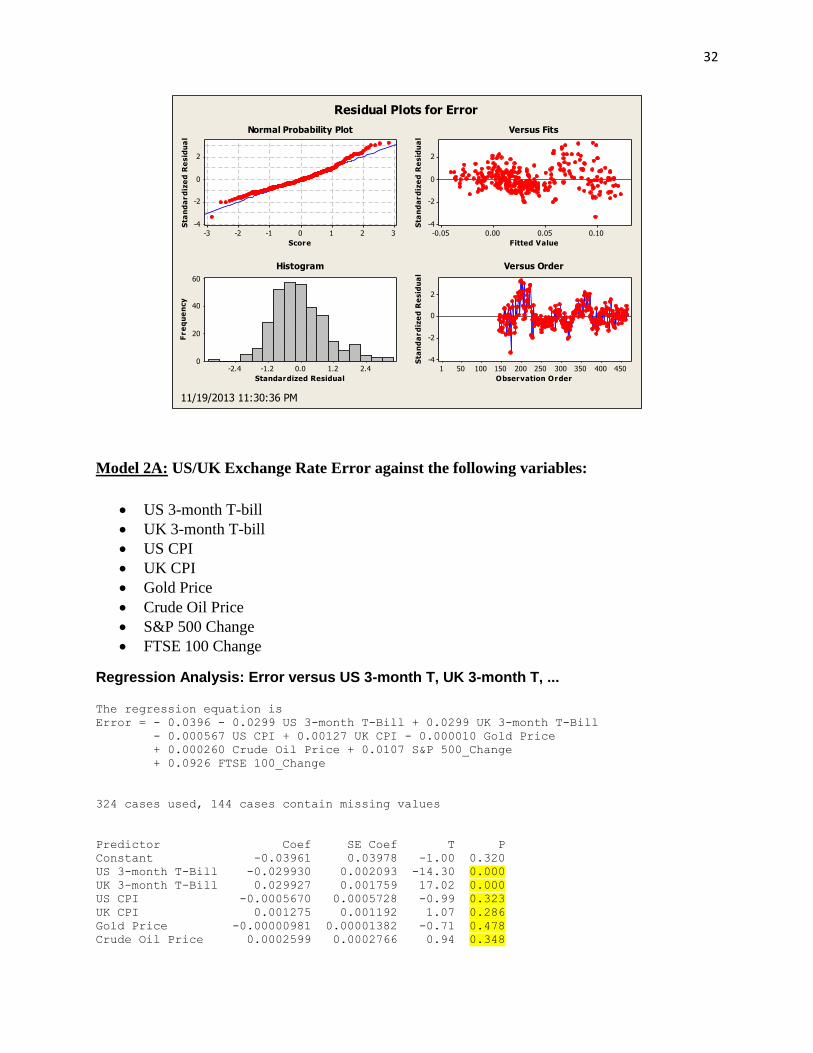

Model 2A: US/UK Exchange Rate Error against the following variables:

US 3-month T-bill

UK 3-month T-bill

US CPI

UK CPI

Gold Price

Crude Oil Price

S&P 500 Change

FTSE 100 Change

Regression Analysis: Error versus US 3-month T, UK 3-month T, ... The regression equation is

Error = - 0.0396 - 0.0299 US 3-month T-Bill + 0.0299 UK 3-month T-Bill

- 0.000567 US CPI + 0.00127 UK CPI - 0.000010 Gold Price

+ 0.000260 Crude Oil Price + 0.0107 S&P 500_Change

+ 0.0926 FTSE 100_Change

324 cases used, 144 cases contain missing values

Predictor Coef SE Coef T P

Constant -0.03961 0.03978 -1.00 0.320

US 3-month T-Bill -0.029930 0.002093 -14.30 0.000

UK 3-month T-Bill 0.029927 0.001759 17.02 0.000

US CPI -0.0005670 0.0005728 -0.99 0.323

UK CPI 0.001275 0.001192 1.07 0.286

Gold Price -0.00000981 0.00001382 -0.71 0.478

Crude Oil Price 0.0002599 0.0002766 0.94 0.348

33

S&P 500_Change 0.01067 0.06287 0.17 0.865

FTSE 100_Change 0.09258 0.05146 1.80 0.073

S = 0.0412439 R-Sq = 66.0% R-Sq(adj) = 65.2%

Analysis of Variance

Source DF SS MS F P

Regression 8 1.04131 0.13016 76.52 0.000

Residual Error 315 0.53583 0.00170

Total 323 1.57714

Source DF Seq SS

US 3-month T-Bill 1 0.16455

UK 3-month T-Bill 1 0.86881

US CPI 1 0.00042

UK CPI 1 0.00099

Gold Price 1 0.00001

Crude Oil Price 1 0.00080

S&P 500_Change 1 0.00021

FTSE 100_Change 1 0.00551

Unusual Observations

US 3-month

Obs T-Bill Error Fit SE Fit Residual St Resid

154 5.2 0.03178 0.13141 0.00775 -0.09963 -2.46R

163 5.7 0.03565 0.03836 0.01560 -0.00271 -0.07 X

167 5.7 0.16146 0.04525 0.01106 0.11621 2.92R

171 5.7 0.14126 0.03948 0.00756 0.10178 2.51R

174 6.5 -0.09654 0.06586 0.00665 -0.16241 -3.99R

185 8.4 0.00453 0.11500 0.00655 -0.11047 -2.71R

186 8.2 0.02441 0.12680 0.00696 -0.10239 -2.52R

199 7.6 0.26301 0.17071 0.00790 0.09230 2.28R

200 7.5 0.27852 0.17767 0.00976 0.10085 2.52R

202 7.2 0.27354 0.15143 0.00715 0.12210 3.01R

206 5.9 0.23984 0.14744 0.00863 0.09239 2.29R

207 5.9 0.04787 0.13430 0.00579 -0.08643 -2.12R

226 2.9 -0.04631 0.08744 0.00625 -0.13374 -3.28R

227 3.1 -0.04687 0.07371 0.00571 -0.12058 -2.95R

230 2.9 -0.06200 0.04540 0.00582 -0.10740 -2.63R

389 4.7 0.06475 -0.03493 0.00620 0.09968 2.44R

413 1.7 0.08589 0.08597 0.01350 -0.00008 -0.00 X

414 1.9 0.09059 0.06895 0.01523 0.02164 0.56 X

415 1.6 0.10901 0.07596 0.01423 0.03306 0.85 X

416 1.7 -0.00500 0.07529 0.01100 -0.08029 -2.02R

417 1.1 -0.01019 0.08183 0.00959 -0.09203 -2.29R

418 0.7 -0.03422 0.04954 0.01378 -0.08376 -2.15RX

419 0.2 -0.10033 0.00588 0.00850 -0.10621 -2.63R

426 0.2 0.07941 -0.01520 0.00540 0.09461 2.31R

R denotes an observation with a large standardized residual.

X denotes an observation whose X value gives it large leverage.

Correlations: US 3-month T, UK 3-month T, US CPI, UK CPI, Gold Price, ... US 3-month T-Bil UK 3-month T-Bil US CPI

34

UK 3-month T-Bil 0.843

0.000

US CPI -0.735 -0.806

0.000 0.000

UK CPI -0.723 -0.788 0.992

0.000 0.000 0.000

Gold Price -0.471 -0.561 0.654

0.000 0.000 0.000

Crude Oil Price -0.631 -0.611 0.842

0.000 0.000 0.000

S&P 500_Change -0.015 0.027 -0.024

0.754 0.555 0.610

FTSE 100_Change 0.065 0.053 -0.084

0.228 0.320 0.117

Error -0.013 0.418 -0.308

0.783 0.000 0.000

UK CPI Gold Price Crude Oil Price

Gold Price 0.621

0.000

Crude Oil Price 0.793 0.840

0.000 0.000

S&P 500_Change -0.007 -0.003 -0.097

0.875 0.951 0.081

FTSE 100_Change -0.078 -0.034 -0.100

0.148 0.531 0.072

Error -0.304 -0.221 -0.280

0.000 0.000 0.000

S&P 500_Change FTSE 100_Change

FTSE 100_Change 0.137

0.011

Error 0.095 0.056

0.041 0.299

Cell Contents: Pearson correlation

P-Value

Stepwise Regression: Error versus US 3-month T, UK 3-month T, ... Alpha-to-Enter: 0.15 Alpha-to-Remove: 0.15

Response is Error on 8 predictors, with N = 324

N(cases with missing observations) = 144 N(all cases) = 468

Step 1 2 3

35

Constant -0.03848 -0.02668 -0.02686

UK 3-month T-Bill 0.01240 0.02952 0.02954

T-Value 15.05 22.65 22.73

P-Value 0.000 0.000 0.000

US 3-month T-Bill -0.0300 -0.0301

T-Value -15.02 -15.11

P-Value 0.000 0.000

FTSE 100_Change 0.086

T-Value 1.71

P-Value 0.088

S 0.0536 0.0412 0.0410

R-Sq 41.29 65.52 65.83

R-Sq(adj) 41.10 65.31 65.51

Mallows Cp 224.4 1.7 0.8

Best Subsets Regression: Error versus US 3-month T, UK 3-month T, ... Response is Error

324 cases used, 144 cases contain missing values

U U

S K

C F

3 3 r S T

- - u & S

m m d P E

o o e

n n G 5 1

t t o O 0 0

h h l i 0 0

d l _ _

T T U U C C

- - S K P P h h

B B r r a a

i i C C i i n n

Mallows l l P P c c g g

Vars R-Sq R-Sq(adj) Cp S l l I I e e e e

1 41.3 41.1 224.4 0.053626 X

1 26.2 26.0 363.9 0.060106 X

2 65.5 65.3 1.7 0.041158 X X

2 43.3 43.0 207.5 0.052770 X X

3 65.8 65.5 0.8 0.041035 X X X

3 65.6 65.3 3.2 0.041190 X X X

4 65.9 65.5 2.1 0.041058 X X X X

4 65.9 65.5 2.3 0.041067 X X X X

5 65.9 65.4 3.9 0.041108 X X X X X

5 65.9 65.4 4.1 0.041119 X X X X X

6 66.0 65.3 5.5 0.041148 X X X X X X

6 65.9 65.3 5.9 0.041171 X X X X X X

7 66.0 65.3 7.0 0.041180 X X X X X X X

7 66.0 65.2 7.5 0.041212 X X X X X X X

8 66.0 65.2 9.0 0.041244 X X X X X X X X

36

2

0

-2

-4

3210-1-2-3

Sta

nd

ard

ize

d R

esid

ua

l

Score

0.150.100.050.00-0.05

2

0

-2

-4

Fitted Value

Sta

nd

ard

ize

d R

esid

ua

l

3210-1-2-3-4

75

50

25

0

Standardized Residual

Fre

qu

en

cy

450400350300250200150100501

2

0

-2

-4

Observation Order

Sta

nd

ard

ize

d R

esid

ua

l

Normal Probability Plot Versus Fits

Histogram Versus Order

Residual Plots for Error

12/4/2013 1:02:37 AM

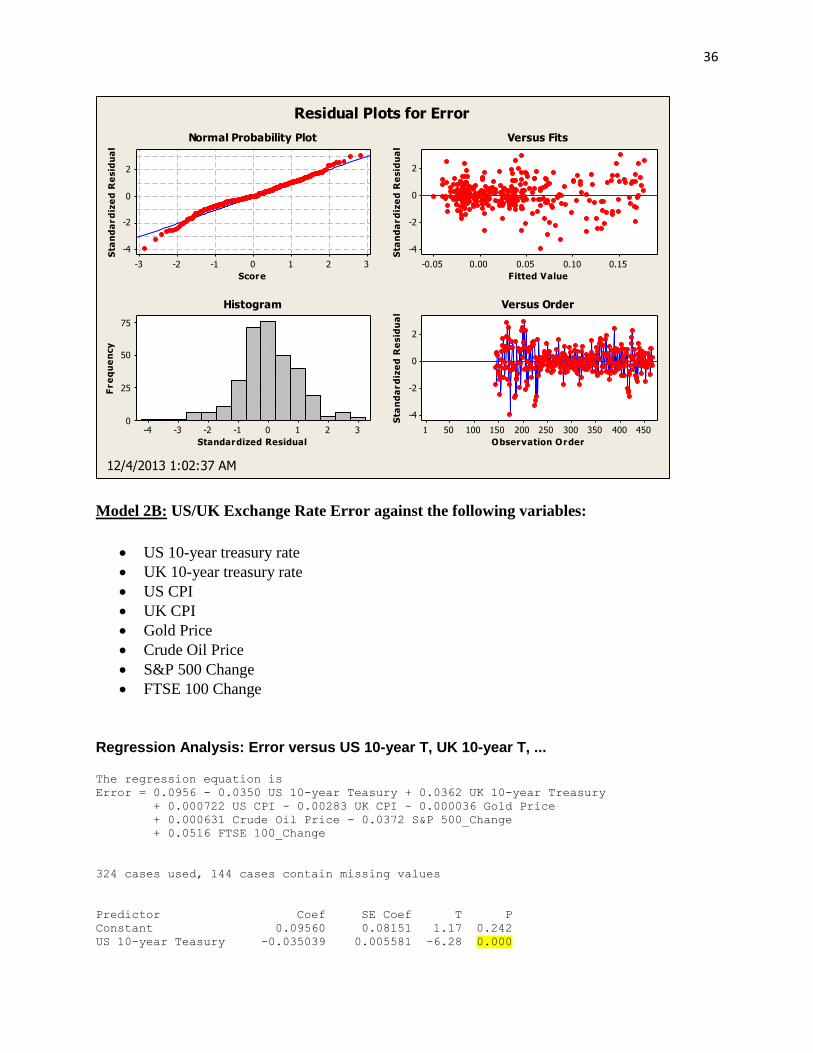

Model 2B: US/UK Exchange Rate Error against the following variables:

US 10-year treasury rate

UK 10-year treasury rate

US CPI

UK CPI

Gold Price

Crude Oil Price

S&P 500 Change

FTSE 100 Change

Regression Analysis: Error versus US 10-year T, UK 10-year T, ... The regression equation is

Error = 0.0956 - 0.0350 US 10-year Teasury + 0.0362 UK 10-year Treasury

+ 0.000722 US CPI - 0.00283 UK CPI - 0.000036 Gold Price

+ 0.000631 Crude Oil Price - 0.0372 S&P 500_Change

+ 0.0516 FTSE 100_Change

324 cases used, 144 cases contain missing values

Predictor Coef SE Coef T P

Constant 0.09560 0.08151 1.17 0.242

US 10-year Teasury -0.035039 0.005581 -6.28 0.000

37

UK 10-year Treasury 0.036227 0.004113 8.81 0.000

US CPI 0.0007221 0.0008258 0.87 0.383

UK CPI -0.002834 0.001518 -1.87 0.063

Gold Price -0.00003564 0.00001723 -2.07 0.039

Crude Oil Price 0.0006313 0.0003625 1.74 0.083

S&P 500_Change -0.03724 0.07980 -0.47 0.641

FTSE 100_Change 0.05163 0.06544 0.79 0.431

S = 0.0522833 R-Sq = 45.4% R-Sq(adj) = 44.0%

Analysis of Variance

Source DF SS MS F P

Regression 8 0.716073 0.089509 32.74 0.000

Residual Error 315 0.861067 0.002734

Total 323 1.577141

Source DF Seq SS

US 10-year Teasury 1 0.353919

UK 10-year Treasury 1 0.309516

US CPI 1 0.000264

UK CPI 1 0.039130

Gold Price 1 0.003745

Crude Oil Price 1 0.007389

S&P 500_Change 1 0.000409

FTSE 100_Change 1 0.001701

Unusual Observations

US 10-year

Obs Teasury Error Fit SE Fit Residual St Resid

154 7.4 0.03178 0.16274 0.01171 -0.13096 -2.57R

163 8.4 0.03565 0.05014 0.01969 -0.01449 -0.30 X

167 8.9 0.16146 0.04873 0.01462 0.11273 2.25R

174 8.9 -0.09654 0.04970 0.01004 -0.14625 -2.85R

179 9.0 0.16494 0.05912 0.00891 0.10582 2.05R

199 8.5 0.26301 0.14558 0.00985 0.11744 2.29R

200 8.8 0.27852 0.15416 0.01244 0.12437 2.45R

202 8.7 0.27354 0.14053 0.00968 0.13301 2.59R

206 7.8 0.23984 0.09796 0.01019 0.14188 2.77R

220 7.5 0.18643 0.07546 0.00747 0.11097 2.14R

221 7.4 0.20132 0.06371 0.00707 0.13761 2.66R

222 7.3 0.20277 0.08118 0.00984 0.12158 2.37R

223 6.8 0.22779 0.08940 0.00690 0.13838 2.67R

224 6.6 0.22429 0.10986 0.00816 0.11443 2.22R

226 6.6 -0.04631 0.08184 0.00695 -0.12815 -2.47R

230 6.3 -0.06200 0.06822 0.00609 -0.13022 -2.51R

361 4.2 0.13035 0.02435 0.00721 0.10601 2.05R

372 4.2 0.12226 0.01437 0.00602 0.10789 2.08R

413 3.9 0.08589 0.07204 0.01710 0.01384 0.28 X

414 4.1 0.09059 0.07563 0.01930 0.01497 0.31 X

415 4.0 0.10901 0.07379 0.01802 0.03522 0.72 X

418 3.8 -0.03422 0.03604 0.01757 -0.07026 -1.43 X

419 3.5 -0.10033 0.01648 0.01147 -0.11681 -2.29R

422 2.9 -0.00860 0.00697 0.01517 -0.01557 -0.31 X

R denotes an observation with a large standardized residual.

X denotes an observation whose X value gives it large leverage.

38

Correlations: US 10-year T, UK 10-year T, US CPI, UK CPI, Gold Price, ... US 10-year Teasu UK 10-year Treas US CPI

UK 10-year Treas 0.865

0.000

US CPI -0.776 -0.942

0.000 0.000

UK CPI -0.753 -0.935 0.992

0.000 0.000 0.000

Gold Price -0.485 -0.557 0.654

0.000 0.000 0.000

Crude Oil Price -0.728 -0.672 0.842

0.000 0.000 0.000

S&P 500_Change 0.002 -0.001 -0.024

0.963 0.985 0.610

FTSE 100_Change 0.064 0.079 -0.084

0.234 0.143 0.117

Error 0.035 0.308 -0.308

0.444 0.000 0.000

UK CPI Gold Price Crude Oil Price

Gold Price 0.621

0.000

Crude Oil Price 0.793 0.840

0.000 0.000

S&P 500_Change -0.007 -0.003 -0.097

0.875 0.951 0.081

FTSE 100_Change -0.078 -0.034 -0.100

0.148 0.531 0.072

Error -0.304 -0.221 -0.280

0.000 0.000 0.000

S&P 500_Change FTSE 100_Change

FTSE 100_Change 0.137

0.011

Error 0.095 0.056

0.041 0.299

Cell Contents: Pearson correlation

P-Value

Stepwise Regression: Error versus US 10-year T, UK 10-year T, ... Alpha-to-Enter: 0.15 Alpha-to-Remove: 0.15

39

Response is Error on 8 predictors, with N = 324

N(cases with missing observations) = 144 N(all cases) = 468

Step 1 2 3 4

Constant -0.06663 -0.03444 0.06841 0.04192

UK 10-year Treasury 0.0157 0.0367 0.0350 0.0368

T-Value 13.14 10.43 9.50 10.06

P-Value 0.000 0.000 0.000 0.000

US 10-year Teasury -0.0298 -0.0339 -0.0325

T-Value -6.30 -6.22 -6.06

P-Value 0.000 0.000 0.000

UK CPI -0.00087 -0.00456

T-Value -1.50 -3.78

P-Value 0.136 0.000

US CPI 0.00177

T-Value 3.47

P-Value 0.001

S 0.0565 0.0534 0.0532 0.0524

R-Sq 34.90 42.07 42.47 44.56

R-Sq(adj) 34.70 41.70 41.93 43.87

Mallows Cp 55.6 16.3 15.9 5.8

Best Subsets Regression: Error versus US 10-year T, UK 10-year T, ... Response is Error

324 cases used, 144 cases contain missing values

U

U K

S

1

1 0 C F

0 - r S T

- y u & S

y e d P E

e a e

a r G 5 1

r o O 0 0

T l i 0 0

T r d l _ _

e e U U C C

a a S K P P h h

s s r r a a

u u C C i i n n

Mallows r r P P c c g g

Vars R-Sq R-Sq(adj) Cp S y y I I e e e e

1 34.9 34.7 55.6 0.056466 X

1 26.2 26.0 105.6 0.060106 X

2 42.1 41.7 16.3 0.053352 X X

2 37.4 37.0 43.2 0.055463 X X

3 42.5 41.9 15.9 0.053249 X X X

3 42.4 41.9 16.2 0.053273 X X X

4 44.6 43.9 5.8 0.052353 X X X X

4 44.1 43.4 8.6 0.052581 X X X X

5 45.1 44.2 4.7 0.052179 X X X X X

40

5 44.8 43.9 6.5 0.052322 X X X X X

6 45.3 44.2 5.8 0.052182 X X X X X X

6 45.2 44.2 6.1 0.052207 X X X X X X

7 45.4 44.2 7.2 0.052219 X X X X X X X

7 45.3 44.1 7.6 0.052252 X X X X X X X

8 45.4 44.0 9.0 0.052283 X X X X X X X X

4

2

0

-2

3210-1-2-3

Sta

nd

ard

ize

d R

esid

ua

l

Score

0.150.100.050.00-0.05

2

0

-2

Fitted Value

Sta

nd

ard

ize

d R

esid

ua

l

2.251.500.750.00-0.75-1.50-2.25

40

20

0

Standardized Residual

Fre

qu

en

cy

450400350300250200150100501

2

0

-2

Observation Order

Sta

nd

ard

ize

d R

esid

ua

l

Normal Probability Plot Versus Fits

Histogram Versus Order

Residual Plots for Error

12/4/2013 1:05:11 AM

Model 3:

Observation

US/UK

Exchange

Rate

Exchange

Rate

Returns

Intercept Slope

Predicted

Exchange

Rate

Returns

Forecasting

Error

Squared

Error RSME

1974-01-01 2.2240 0.19387

1974-02-01 2.2749 0.02263

1974-03-01 2.3406 0.02847

41

1974-04-01 2.3886 0.02030

1974-05-01 2.4137 0.01045

1974-06-01 2.3902 -0.00978

1974-07-01 2.3896 -0.00025

1974-08-01 2.3456 -0.01858

1974-09-01 2.3165 -0.01248

1974-10-01 2.3330 0.00710

1974-11-01 2.3252 -0.00335

1974-12-01 2.3294 0.00180

1975-01-01 2.3623 0.01402

1975-02-01 2.3958 0.01408

1975-03-01 2.4180 0.00922

1975-04-01 2.3707 -0.01976

1975-05-01 2.3205 -0.02140

1975-06-01 2.2803 -0.01748

1975-07-01 2.1845 -0.04292

1975-08-01 2.1143 -0.03266

1975-09-01 2.0834 -0.01472

1975-10-01 2.0568 -0.01285

1975-11-01 2.0484 -0.00409

1975-12-01 2.0221 -0.01292

1976-01-01 2.0286 0.00321

1976-02-01 2.0262 -0.00118

1976-03-01 1.9428 -0.04203

1976-04-01 1.8463 -0.05095

1976-05-01 1.8079 -0.02102

1976-06-01 1.7640 -0.02458

1976-07-01 1.7850 0.01183

1976-08-01 1.7828 -0.00123

1976-09-01 1.7272 -0.03168

1976-10-01 1.6377 -0.05321

1976-11-01 1.6381 0.00024

1976-12-01 1.6784 0.02430

1977-01-01 1.7124 0.02005

1977-02-01 1.7103 -0.00123

1977-03-01 1.7174 0.00414

1977-04-01 1.7190 0.00093

1977-05-01 1.7185 -0.00029

1977-06-01 1.7191 0.00035

1977-07-01 1.7226 0.00203

1977-08-01 1.7397 0.00988

1977-09-01 1.7431 0.00195

1977-10-01 1.7711 0.01594

1977-11-01 1.8178 0.02603

1977-12-01 1.8546 0.02004

42

1978-01-01 1.9353 0.04259

1978-02-01 1.9396 0.00222

1978-03-01 1.9055 -0.01774

1978-04-01 1.8497 -0.02972

1978-05-01 1.8181 -0.01723

1978-06-01 1.8372 0.01045

1978-07-01 1.8949 0.03092

1978-08-01 1.9406 0.02383

1978-09-01 1.9595 0.00969

1978-10-01 2.0075 0.02420

1978-11-01 1.9608 -0.02354

1978-12-01 1.9861 0.01282

1979-01-01 2.0053 0.00962

1979-02-01 2.0042 -0.00055

1979-03-01 2.0378 0.01663

1979-04-01 2.0735 0.01737

1979-05-01 2.0587 -0.00716

1979-06-01 2.1119 0.02551

1979-07-01 2.2598 0.06769

1979-08-01 2.2368 -0.01023

1979-09-01 2.1966 -0.01814

1979-10-01 2.1438 -0.02433

1979-11-01 2.1352 -0.00402

1979-12-01 2.2007 0.03022

1980-01-01 2.2641 0.02840

1980-02-01 2.2891 0.01098

1980-03-01 2.2045 -0.03766

1980-04-01 2.2094 0.00222

1980-05-01 2.3020 0.04106

1980-06-01 2.3359 0.01462

1980-07-01 2.3732 0.01584

1980-08-01 2.3704 -0.00118

1980-09-01 2.4012 0.01291

1980-10-01 2.4165 0.00635

1980-11-01 2.3941 -0.00931

1980-12-01 2.3459 -0.02034

1981-01-01 2.4029 0.02401

1981-02-01 2.2941 -0.04634

1981-03-01 2.2319 -0.02749

1981-04-01 2.1753 -0.02569

1981-05-01 2.0884 -0.04077

1981-06-01 1.9738 -0.05644

1981-07-01 1.8737 -0.05205

1981-08-01 1.8203 -0.02891

1981-09-01 1.8146 -0.00314

43

1981-10-01 1.8407 0.01428

1981-11-01 1.9025 0.03302

1981-12-01 1.9033 0.00042

1982-01-01 1.8860 -0.00913

1982-02-01 1.8470 -0.02090

1982-03-01 1.8053 -0.02284

1982-04-01 1.7720 -0.01862

1982-05-01 1.8104 0.02144

1982-06-01 1.7563 -0.03034

1982-07-01 1.7354 -0.01197

1982-08-01 1.7250 -0.00601

1982-09-01 1.7120 -0.00756

1982-10-01 1.6962 -0.00927

1982-11-01 1.6321 -0.03852

1982-12-01 1.6160 -0.00991

1983-01-01 1.5756 -0.02532

1983-02-01 1.5329 -0.02747

1983-03-01 1.4900 -0.02839

1983-04-01 1.5361 0.03047

1983-05-01 1.5722 0.02323

1983-06-01 1.5480 -0.01551

1983-07-01 1.5273 -0.01346

1983-08-01 1.5026 -0.01630

1983-09-01 1.4986 -0.00267

1983-10-01 1.4969 -0.00114

1983-11-01 1.4766 -0.01365

1983-12-01 1.4338 -0.02941

1984-01-01 1.4076 -0.01844 -0.00230 0.47017 -0.01613 -0.00231 0.00001

1984-02-01 1.4417 0.02394 -0.00224 0.45305 -0.01060 0.03454 0.00119

1984-03-01 1.4557 0.00966 -0.00234 0.44835 0.00840 0.00127 0.00000

1984-04-01 1.4210 -0.02413 -0.00262 0.44084 0.00164 -0.02577 0.00066

1984-05-01 1.3894 -0.02249 -0.00257 0.44677 -0.01335 -0.00914 0.00008