FORESTA2021

Roundwood markets in UNECE regions in 2021-22Key trends and outlook

Foresta2021 – Joint Session of the UNECE Committee on Forests and the Forest Industry and FAO European Forestry Commission

23rd November 2021

Market outlook

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Key dynamics impacting UNECE roundwood markets in 2021-22

Global trends

2

COVID rebound

Russian log export ban

Climate / forest health

Sustainability initiatives

• Strong lumber markets in US and Europe

• Paper and packaging rebounding

• Housing crisis in China?

• Challenge for China

• Opportunity for other log exporters

• Russian industrial expansion?

• Decline in BC harvests in wake of mountain pine beetle

• Fires in US West

• Temporary surge in Central European harvest

• LULUCF

• EU Forest Strategy

• Carbon forestry

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

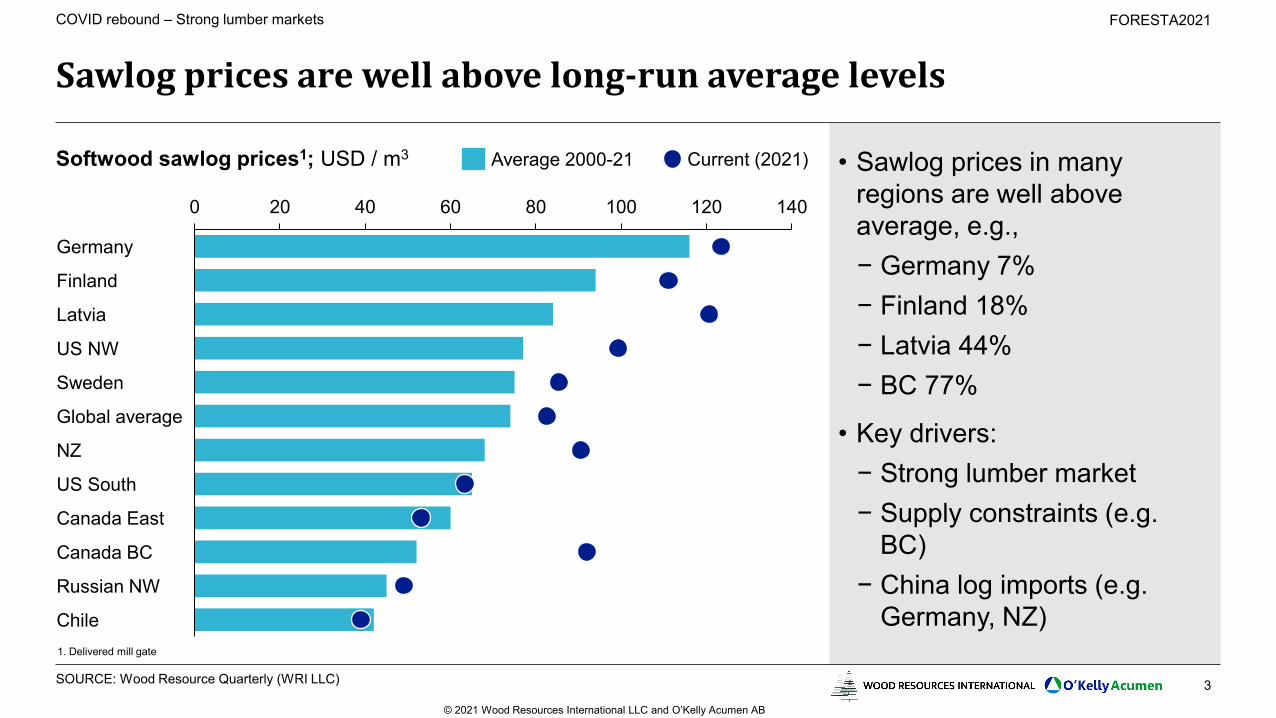

Sawlog prices are well above long-run average levels

Softwood sawlog prices1; USD / m3 • Sawlog prices in many regions are well above average, e.g., − Germany 7%− Finland 18%− Latvia 44%− BC 77%

• Key drivers:− Strong lumber market− Supply constraints (e.g.

BC)− China log imports (e.g.

Germany, NZ)

COVID rebound – Strong lumber markets

3

1. Delivered mill gate

SOURCE: Wood Resource Quarterly (WRI LLC)

0 20 40 60 80 100 120 140

US South

Global average

Germany

Latvia

Finland

US NW

Sweden

NZ

Canada East

Canada BC

Russian NW

Chile

Current (2021)Average 2000-21

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Pulplog prices are mostly around long-run average levels

Softwood pulplog prices1; USD / m3 • Pulplog prices around average level in most regions.

• Some exceptions (e.g. strong prices in Finland, weak in Germany, Brazil).

• Key drivers:− Slight rebound in P&P and

panel markets− Elevated sawmill residue

supply

COVID rebound – Strong lumber markets

4

1. Delivered mill gate

SOURCE: Wood Resource Quarterly (WRI LLC)

0 20 40 60 80 100 120 140 160

Brazil

Germany

Austria

Canada BC

Sweden

Global average

Finland

Canada East

US NW

US South

Russia NW

Chile

Current (2021)Average 2000-21

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

China and Finland are both dependent on Russian logs; China mainly for sawmills, Finland for pulp and paper

Imported wood from Russia, 2020e; Million m3• Important for Chinese

sawmill industry− 10-15% of softwood log

imports, 30% of hardwood log imports

− Secondary impact on residues for panel mills

• Less impact on Finland− Russian import mostly

hardwood pulplogs (not covered)

− Softwood imports mainly as chips not covered

Russia log export ban

5

1. Delivered mill gate

SOURCE: Customs data; WRI/OA analysis

Sawlogs

Pulplogs

Chips

Softwood Hardwood

5.3

2.5

~0 ~0

~0 ~0

0.7 ~0

0.1

4.5

2.0

~0

Softwood Hardwood

China Finland

Expected to be covered by ban

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Of the largest lumber-exporting regions, Russia has the greatest potential to increase exports

6SOURCE: Customs data; WRI/OA analysis

Russia log export ban

30.0

26.0

23.0

16.0

12.0

6.0

5.0Baltic

Canada

Russia

EasternEurope2

Nordic

CentralEurope1

LatAm

Total softwood lumber exports 2020e Million m3 Potential to increase lumber exports

Low High

Large potential and incentives improving with expected log export ban and investment support for sawmill expansion and improved quality (kiln-drying). However, dependent on investment in Russian sawmill industry.

Some potential to increase harvest in the region; we estimate Finland could increase sawlog harvest 6-7 mlnm3, Norway 2-3 mln m3 and Sweden 2-3 mln m3. Most lumber production is already for export, with small domestic markets.

Lumber export will stabilize and log export decline following mountain pine beetle damage and salvage in BC. Geographic shift with more export from eastern Canada and less from the west. US will remain the most attractive export market for lumber, with only limited export to Asia from western Canada.

Harvests will decline in the coming 1-2 years after short-term surge related to salvage of forests affected by bark beetle epidemic. Long-term reduction in harvest is likely due to scale of the damage and salvage harvests.

Some potential to increase export. Although log markets are tight (harvest rate of 75-85%, and log markets tightly coupled with Nordic region), reduced log export would enable increased domestic lumber production. Likely strong domestic demand growth but most lumber production will remain for export.

Some countries (e.g., Czech Rep.) also impacted by bark beetle, but others (e.g., Belarus, Ukraine, Romania) have low wood costs, potential to increase harvest, and are attractive for sawmill investments. Strong domestic demand growth is likely with post-COVID economic recovery, reducing share of lumber for export. Limited potential; export is currently at high levels due to weak domestic demand. Domestic demand will increase and export fall as the regions economies improves long-term. Also, a decline in planted softwood area over the last 10-20 years will limit future size of lumber industry.

1. Germany and Austria, 2. Belarus, Ukraine, Czech Republic, Romania, Slovenia, Poland, Slovakia, Bosnia and Herzegovina

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Forest damage, related to climate change, is impacting roundwood supply in Canada and Europe – for many years to comeCanada harvest and lumber export to US; Million m3 Central European1 harvest and export; Million m3

Climate / forest health

7

1. Germany and Czech Republic

SOURCE: FAOSTAT; WRI/OA analysis

Implication: Temporary surge in log exports to China, supply to domestic lumber industry

Implication: Reduced lumber supply to US and Asia

0

10

20

30

40

0

50

100

150

200

250

1990 20151995 2000 20102005 2020

Harvest Lumber export

0

10

20

30

0

50

100

202020152000 2005 2010

Harvest Log export

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Sustainability initiatives, while arguably necessary, will have a large impact on wood supply

Example: Potential impact of LULUCF on Sweden wood supplySustainability initiatives impacting forestry

• LULUCF (EU)− Targets for increased

forest sequestration

• EU Forest Strategy− Continuous cover forestry

(selective logging)− Increased forest protection

• Forest carbon markets− NCX (US)− Voluntary carbon offsetting

Sustainability initiatives

8

1. If full LULUCF target achieved by reducing harvests, baseline felings ~94 million m3

SOURCE: European Commission; Swedish Forest Industries Federation; OA analysis

Target sink 2030 (MtCO2eq./year)

Swedish industry fears

Official (intended)

Current sink (MtCO2eq./year)

Required increase of sink

CO2 per m3 factor

Required addition forest sequestration (million m3/ year)

Impact on wood supply1

4.7

42.6

47.3

3.4

1.375

4 %

11.8

47.3

35.5

13.6

0.87

15 %

Estimates

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Global roundwood market outlook (pricing)

Roundwood market outlook

9SOURCE: WRI/OA analysis

UNECE regions Other regions

North America Asia-PacificEurope (EU) CIS, Central Asia Latin America

Sawlogs

Pulpwood

Things to watch for

Strong lumber marketAdditional potential in US South, Canada E, US NW

• Housing starts

• US South expansion

• Carbon forestry

• Sawmill expansion

• LULUCF, end of clear-cuts?

• Pellet / panel / P&P expansion with new sawmlls

• Chinese housing crisis?

• NZ peak export

• Afforestation for climate

Tight Balanced Soft

Strong sawmill residue supplyP&P demand returning to normal

Strong lumber market / exportPost bark beetle

Central: sawmill residues

Nordic: strong pulp production, harvest constraints

Russia log export ban

Sawmill expansion

Strong pellet industry

Strong lumber marketRussia export banReduced NthAm export

Plantations expanding with demand (e.g. new pulp mills)

Declining exports, with reduced supply and more domestic demand

Pulpmill expansionChina restrictions on RCP import and log import from Australia

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Total

UNECE Timber Forecasts for 2020-22

Roundwood market outlook

10SOURCE: UNECE COFFI and FAO EFC Foresta2021

North America Europe (EU) CIS, Central Asia

297 307303

+1.7%

187188 187

-0.2%

Hardwood Softwood

1515 15

0.0%

2020 2021

62

2022

62 62

+0.1%

216220 221

-0.8%

163159 165

+2.0%

76 7

+4.7%

2020 2021

115113112

2022

+1.2%

135 132137

-1.2%

49 50 50

+0.6%

1818 17

-2.0%

18

20222020

18

2021

18

-0.8%

Sawlogs

Pulplogs

Other industrial

Wood fuel

CAGR

Demand drivers

• SW lumber ++

• HW lumber +

• Plywood and veneer +

• Pulp for paper +/-

• Pulp for other uses +

• Panels +

• Posts and poles +/-

• Residential heating +/-

• Bioenergy plants +

+0.8% +0.7% -0.8%

x

Forecast roundwood removals; Million m3

FORESTA2021

Contact details

Wood Resources International O’Kelly Acumen

Mr. Håkan EkströmSeattleUSA

Phone: +1-425-402-8809E-mail: [email protected]

www.woodprices.com

Mr. Glen O’KellyStockholmSweden

Phone: +46-73-56-98-039E-mail: [email protected]

www.okelly.se

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Backup slides for questions

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

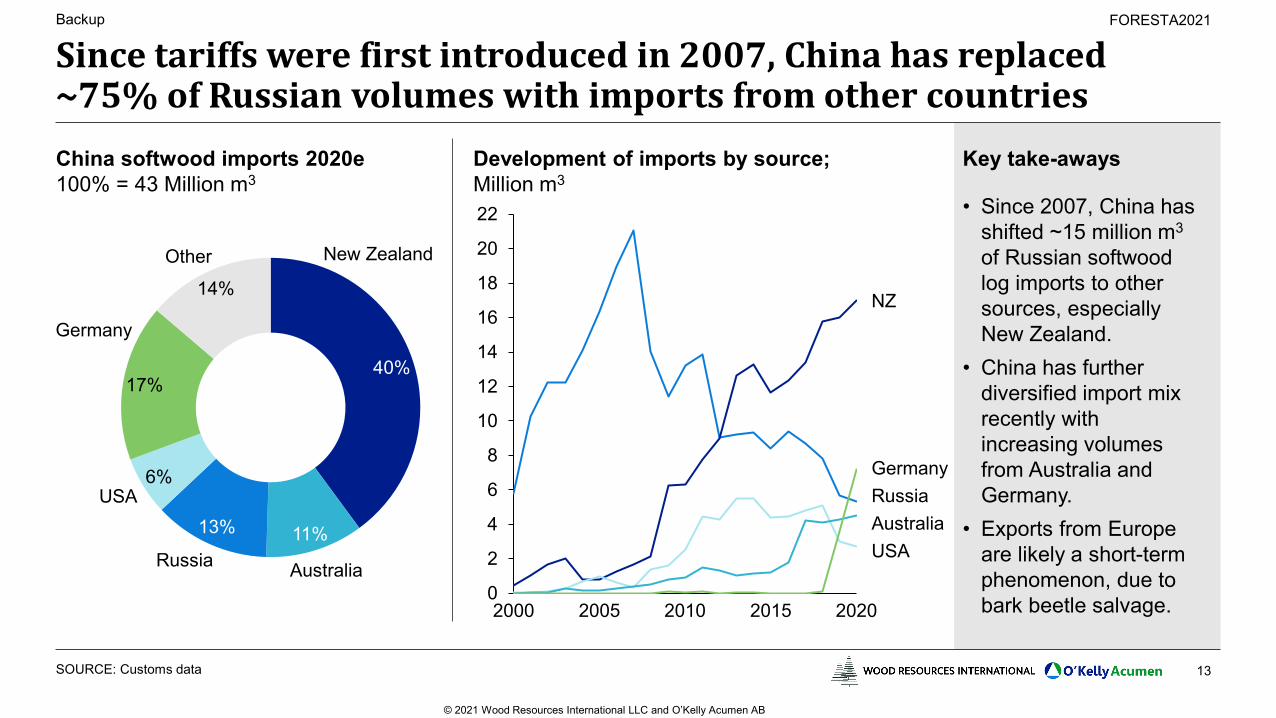

Since tariffs were first introduced in 2007, China has replaced ~75% of Russian volumes with imports from other countries

13

China softwood imports 2020e100% = 43 Million m3

Key take-aways

• Since 2007, China has shifted ~15 million m3

of Russian softwood log imports to other sources, especially New Zealand.

• China has further diversified import mix recently with increasing volumes from Australia and Germany.

• Exports from Europe are likely a short-term phenomenon, due to bark beetle salvage.

SOURCE: Customs data

0

2

4

6

8

10

12

14

16

18

20

22

20152000 20102005 2020

Russia

USA

NZ

Australia

Germany

Development of imports by source; Million m3

40%

11%13%

6%

17%

14%

New ZealandOther

AustraliaRussia

USA

Germany

Backup

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Decreased Russian exports of softwood logs to China will create opportunity for New Zealand and European exporters

14

Global trade-flows 2020e – Softwood logs; Million m3 Largest exporters

NZ

4

USA

5

1

SOURCE: Customs data; WRI/OA analysis

Backup

2

Korea & JapanChina

17

1

3Russia

Nordics

Central Europe

Baltics1

2

Largest importers

20

13

12

7

6

Germany

NZ

Czech R.

USA

Russia

43

11

5

5

2

Austria

China

Germany

Sweden

Japan

LatAm

Canada

121

1. Mainly from Germany (~8 mln m3) and Czech Republic (~3 mln m3)

3

1

Australia

India

3

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Most potential for additional log supply is in the east of Russia

15SOURCE: WRI/OA Analysis

76

133

Siberian

268

16

62

Far East

92

16

74

Ural

99

30

24

Volga

7086

Southern and North Caucasian

22

23

Central

56

53

37

120

Northwestern

Russia’s annual allowable cut and harvest by Federal District, 2017; Million m3

Unutilized

Registered removals

Harvest loss1

Illegal logging2

1. Estimated, assuming logging waste and bark is 25% of total (registered and illegal) fellings2. Estimated, assuming 25% of harvests in Siberia and Fast East are illegal, 15% in rest of Russia (20% overall)

Large unutilized potential in east of Russia – not currently available due to cost constraints and long distances from processing facilities or railroad.

Backup

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Forest growth of ~315 million m3 across the region, in production forests, of which ~175 million m3 is harvested

16SOURCE: USDA Forest Service

Backup

15

11

Louisiana

27

16

11

Arkansas

28

18

22

Mississippi

44

18

1031

Nth Carolina20

286

Sth Carolina

31

1047

Georgia127

21

Florida

24

19

Alabama

48

Unutilized

HarvestMortality

13

Texas

320

89

Virginia

20

315

282

107

175

Netgrowth

Harvest

Grossgrowth

Unutilized(added tostock)

33Mortality

Softwood growth, productive forest, US South, 2017-201; Million m3 Total across US South

Some of forest growth is lost to mortality (tree death, fires, storms). Of net growth, only about 62% is currently harvested, including harvest losses –remainder is added to stock.

1. Assessment dates vary by state, from 2017 to 2020

FORESTA2021

© 2021 Wood Resources International LLC and O’Kelly Acumen AB

Global lumber markets are in flux, with several trends suggesting a tighter demand-supply balance in years to come

17SOURCE: WRI/AO analysis

Backup

Supply Demand

Actual/ near term

Potential/ long-term

Developments in global lumber markets

• Russia expected to introduce an export ban on softwood logs and high-value hardwood logs from Jan 2022− Restricted sawlog supply to China, increased import of lumber and

sawlogs from other regions− Increased Russian export of lumber, and investments in improved

quality (kiln-drying).• Canada’s harvest potential reduced with mountain pine beetle in BC.• Central Europe harvests increased short-term due to bark beetle

damage but will fall to below pre-beetle levels from 2022/23. • Decreased export from LatAm to domestic economy rebound and

reduced sawlog supply.

• Strong demand in US due to COVID stimulus and increased DIY• Continued strong demand growth in China post-COVID

• Additional US South supply potential of ~20 million m3 long-term• Increased focus on forests’ role in climate change abatement, growth

in forestry carbon markets− Longer rotations and forest protection (esp. NthAm and Europe)− Surge in new forest planting (e.g., Southern Hemisphere)

• Increased frequency of climate-related forest damage (insects, fire)• Increased investment in plantation forestry in new regions, e.g.,

Africa, SE Asia, increasing sawlog and lumber supply.

• Increased use of wood in construction, including multi-family and non-residential, driven by interested in “green building materials” and innovation in modular solutions (e.g., CLT).

Tighter markets Softer markets Mixed impact