1

Deborah Weinswig Execu4ve Director, Fung Global Retail & Technology [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 @debweinswig

Retailtainment Driven Trends

2

Agenda • About Fung Business Intelligent Centre (FBIC)

• Top 16 Global RETAIL Trends for 2016

• Stores are the New Engagement/Retailtain-‐me!

3

Fung Business Intelligence Centre (FBIC) • Established in 2000 and headquartered in Hong Kong • FBIC serves as the knowledge bank and think tank for the Fung Group

– Collects and analyzes market data on sourcing, supply chains, distribu4on and retail

– Provides thought leadership on technology and other key issues

• New York–based Global Retail & Technology team – Follows broader retail and technology trends – Provides advice and consultancy services to colleagues and business partners of the Fung Group

– Builds collabora4ve knowledge communi4es

4

Futureproofing • An4cipa4ng future trends and developments

• Plan for future value and avoid obsolescence – What problem are you trying to solve?

– How will it be used?

– How robust does it need to be?

• Ensure flexibility to manage changing formats and deployment pagerns

5

Our Partnership With Accelerators Alchemist Accelerator is an accelerator exclusively for startups whose revenue comes from enterprises, not consumers. CoCoon is a coworking space where entrepreneurs, creative talent, successful leaders and investors meet, collaborate and deliver results together. Member companies get access to networking opportunities, work space, a photography studio and mentors. Entrepreneurs Roundtable Accelerator (ERA) provides participant companies with an intensive four-month program, with the goal of helping early-stage companies progress rapidly into exciting, viable businesses. New York Fashion Tech Lab is an accelerator that is a result of a collaboration between the Partnership Fund for New York City, Springboard Enterprises and major fashion retailers. It focuses on early- and growth-stage companies.

Plug and Play is a global innovation platform. It connects startups to corporations, and invests in over 100 companies every year. Its 360° ecosystem allows for remarkable innovation to take shape on an international scale.

6

Fung Capital/FBIC Commerce Technology Landscape

7

1. Smart Malls

2. Silver Economy

3. Luxury Retail Landscape in Asia

4. Online Fashion Resale

5. Sharing Economy

6. One-‐Child Policy in China

7. Social Media Sways Shopper

8. Home Improvement Market

9. Growth of E-‐Commerce

10. The Store Gets a Makeover

11. Athleisure

12. Where to Find Growth: Off-‐Pricers

13. Caring Economy

14. Customer Loyalty

15. Amazon Becomes a Force in Omni-‐Channel

16. Experience Economy

RETAIL TRENDS FOR 2016

8

1. Smart Malls

2. Silver Economy

3. Luxury Retail Landscape in Asia

4. Online Fashion Resale

5. Sharing Economy

6. One-‐Child Policy in China

7. Social Media Sways Shopper

8. Home Improvement Market

9. Growth of E-‐Commerce

10. The Store Gets a Makeover

11. Athleisure

12. Where to Find Growth: Off-‐Pricers

13. Caring Economy

14. Customer Loyalty

15. Amazon Becomes a Force in Omni-‐Channel

16. Experience Economy

RETAILTAINMENT DRIVEN TRENDS

9

1. Shopping Malls Gejng “Smarter”

• In 2014, 44% of all the new shopping malls opened globally were in China, satura4ng the market

• Social media -‐ Shanghai’s Cloud Nine and Shenzhen’s SEG Plaza are using WeChat to reach shoppers directly with news and loyalty programs

• Mobile apps -‐ Wanda has partnered with Baidu to create the one-‐stop-‐shop app “Feifan” for in-‐mall use

• Holis[c Data Analy[cs -‐ Senzhen Rainbow, Xientendi use retail, shopping mall (beacon), and search engine data to analyze shopping behavior and deliver personalized promo4ons

Source: FBIC

Pressure from e-‐commerce and oversupply in some markets will make malls “smarter”

Selected features of the “Feifan” App

10

1. Shopping Malls Gejng “Smarter”

• Wespield operates Wes^ield Labs – a Silicon Valley-‐based unit which designs and experiments with retail innova4ons

– Malls include: touchscreen displays, electronic parking assistance, free Wi-‐FI

• HGTV partnered with Macerich shopping malls to launch virtual and hand-‐on technology-‐based experiences

– Traffic at those [10] malls was up 45%

• RetailNext formed strategic alliance with StepsAway, an in-‐mall mobile retail solu4on provider offering shoppers smartphone access to hyperlocal in-‐store deals

– Timely, relevant promo4ons that measure the redemp4on and conversion rate

– If data shows that shoppers frequent healthy food op4ons, it can drive the opening of health-‐food restaurants in mall’s food court

Pressure from e-‐commerce and oversupply in some markets will make malls “smarter”

11

7. Social Media Sways Shoppers

• In 2015 Pinterest introduced “Buy it” bugon, and Instagram expanded its ad program

• Twiger, Facebook and Youtube also becoming more commerce-‐friendly and are experiment with buy bugons

• Fashion bloggers are becoming more influen4al than celebri4es when it comes to influencing buying decisions in the US

• In China, “verified” Key Opinion Leader with over one million fans on the microblogging plaporm, Weibo, are used by brands such as Burberry, Tommy Hilfiger, Gucci, and Diane von Furstenberg with great effec4veness

Social media will become more commerce-‐driven and the impact of influencers will increase

Source: Pinterest

Peter Xu Weibo Profile: Gucci Pinterest: Buyable Pins

Source: SocialBrnadWatch

12

7. Social Media Sways Shoppers

• WeChat leads the way in social selling -‐ “B2C2C” model (recommended purchase by friends) is the most advanced form of social commerce

• WeChat allows content distribu4on, targeted campaigns, in-‐app payment, friend/influencer recommenda4ons

• Before Singles’ Day in China, brands and retailers engaged shoppers ac4vely on WeChat via:

– Reward vouchers for fans who post a branded message or share it directly to with their friends

– Sharable WeChat s4ckers : The Cambridge Satchel Company partnered with Chinese KOL and ar4st, Zang Xiaobai to launch themed Singles’ Day illustra4ons

“Social selling” will reach a new level of importance Coach Handbags: Marke[ng and Selling on WeChat

Red Envelope: Viral Sharing Lifestyle Content: 57,161 view

Source: WeChat

13

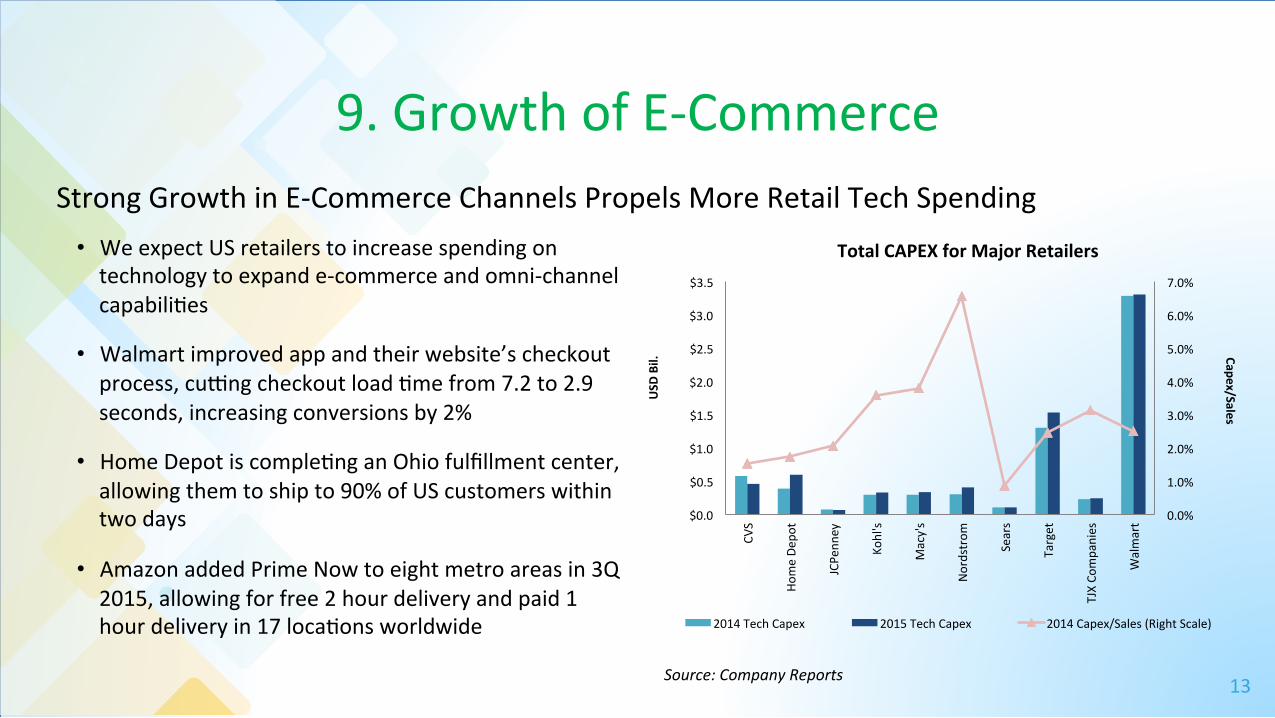

9. Growth of E-‐Commerce

• We expect US retailers to increase spending on technology to expand e-‐commerce and omni-‐channel capabili4es

• Walmart improved app and their website’s checkout process, cujng checkout load 4me from 7.2 to 2.9 seconds, increasing conversions by 2%

• Home Depot is comple4ng an Ohio fulfillment center, allowing them to ship to 90% of US customers within two days

• Amazon added Prime Now to eight metro areas in 3Q 2015, allowing for free 2 hour delivery and paid 1 hour delivery in 17 loca4ons worldwide

Strong Growth in E-‐Commerce Channels Propels More Retail Tech Spending

Source: Company Reports

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

CVS

Home De

pot

JCPe

nney

Kohl's

Macy's

Nordstrom

Sears

Target

TJX Co

mpanies

Walmart

Capex/Sales

USD

Bil.

2014 Tech Capex 2015 Tech Capex 2014 Capex/Sales (Right Scale)

Total CAPEX for Major Retailers

14

9. Growth of E-‐Commerce

• Millennials prefer mono-‐brand brick-‐and-‐mortar stores, and they shi{ between online and offline along the shopping journey

• Warby Parker: Targe4ng millennials

– Started exploring offline with pop-‐ups and a showroom in its NYC office; now expanding to over 20 ci4es in the US

– Warby Parker’s stores make more than $3,000 per sq. {., pujng the retailer in an elite category with companies such as Tiffany and Apple

– Offline feeding ecommerce : more than 85% of store shoppers will later visit the website, increasing the chances for further orders

E-‐Commerce players go offline Retailer # of Stores

1

1

20

26

Source: Company Websites

15

10. The Store Gets a Makeover

• “Retailtainment” is being added to stores by incorpora4ng interac4ve components in the customer experience

• Urban Oupigers, Club Monaco and Kohl’s are part of a trend of retailers that are opening coffee shops and restaurants in their stores.

– In 2015, Urban Oupigers acquired Vetri Family group of restaurants

• Rebecca Minkoff and Tommy Hilfiger have provided shoppers with VR headsets to re-‐experience runway shows

• Prolifera4on of mobile apps to improve in-‐store experience:

– customizable shopping list, loca4on-‐relevant promo4ons, and product and inventory informa4on

Stores will make the shopping experience more fun and entertaining to drive traffic

Tommy Hilfiger VR experience, Source: New York Times

Urban OuIiJers Coffee Shop, Source: parhamsantana.com

16

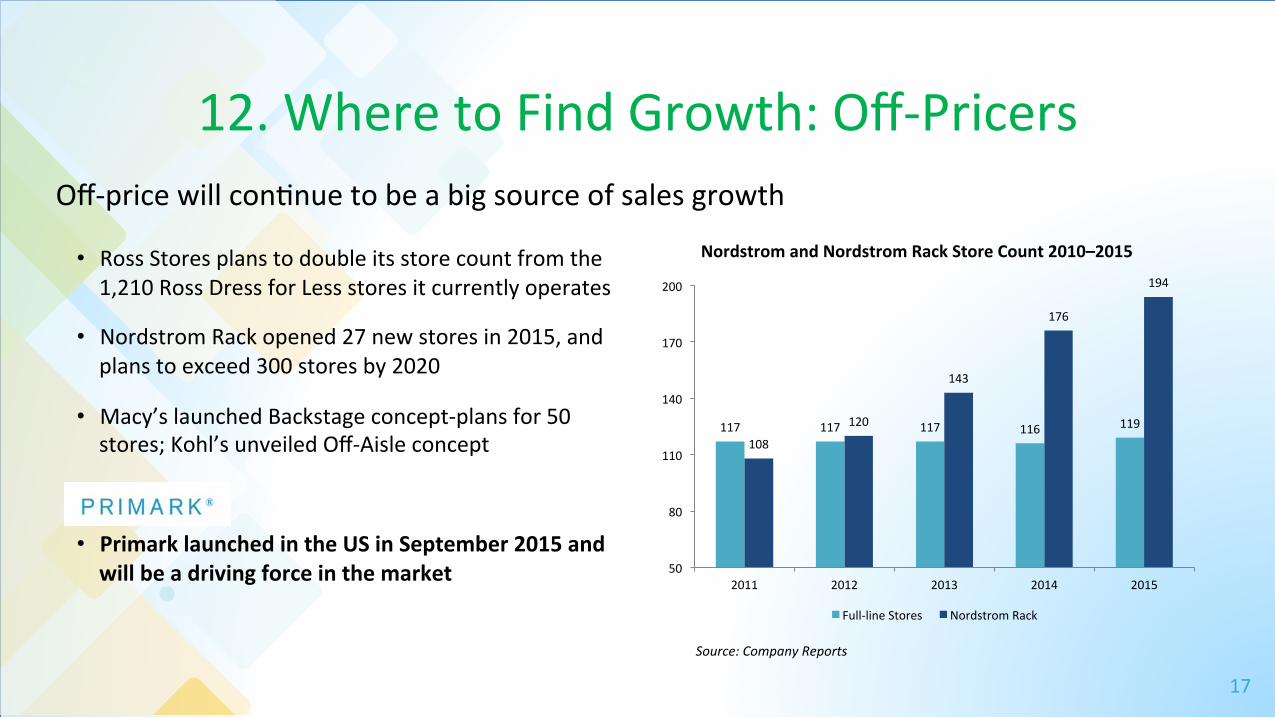

12. Where to Find Growth: Off-‐Pricers

• Off-‐price chains sell high-‐profile brands and designer goods for 20-‐60% less than department and specialty stores – T.J.Maxx and Marshalls pump out roughly $304 in sales per square foot, on average, and Ross generates about $288 in sales

per square foot versus JCPenney, $101 sales per square foot, and Macy’s about $158 (eMarketer)

• Sales will increase by 6% to 8% over the next five years in the US, outpacing the apparel sector by 4% (Moody’s)

Off-‐price will con4nue to be a big source of sales growth

1950 1972

1976 2015 2010

Nov 2015

1973 1995

1956

17

• Ross Stores plans to double its store count from the 1,210 Ross Dress for Less stores it currently operates

• Nordstrom Rack opened 27 new stores in 2015, and plans to exceed 300 stores by 2020

• Macy’s launched Backstage concept-‐plans for 50 stores; Kohl’s unveiled Off-‐Aisle concept

• Primark launched in the US in September 2015 and will be a driving force in the market

12. Where to Find Growth: Off-‐Pricers Off-‐price will con4nue to be a big source of sales growth

Nordstrom and Nordstrom Rack Store Count 2010–2015

Source: Company Reports

117 117 117 116 119 108

120

143

176

194

50

80

110

140

170

200

2011 2012 2013 2014 2015

Full-‐line Stores Nordstrom Rack

18

14. Customer Loyalty

• Customer loyalty has become increasingly difficult to generate and maintain in the omni-‐channel world

• Walmart launched Savings Catcher in 2014 to give customers the difference in price if a product is cheaper elsewhere

• American Express launched Plen[, allowing customers to earn rewards points from AT&T, ExxonMobil, Hulu, Macy’s, among others

• Smartphone apps are becoming more prominent in loyalty programs, likely to replace plas4c cards more in the years ahead

More retailers will facilitate personalized experiences for customers via loyalty programs

19

16. Experience Economy

• According to a Harris Poll survey in 2014: – 78% of millennials prefer to spend money on an

experience than goods

– 69% of respondents said they believe agending live experiences helps them connect beger with friends, community and people around the world

• Mintel expects vaca4ons and tourism to beat out all other categories between 2014 and 2019, at 27%

• Startups have entered the scene to capitalize on the experience economy: IfOnly, Zaptravel, Gigzolo

We expect the experience economy to grow significantly during 2016

Source: Company Websites

20

STORES ARE THE NEW ENGAGEMENT

Retailtain-‐me!

21

Shopper Engagement Is Key For Brick & Mortars Retailers must engage shoppers in a new and personal way

• Use social media and digital experience to build big data to personalize consumer journey and promo4on

– iBeacons to launch personal deals

– Full roll out of CRM

– Apps

• Retailtainment – Ar4ficial Intelligence

– Robo4cs

– Augmented / Virtual Reality

22

Retailtainment • Disney stores transport consumers to a magical wonderland

• 45% of Cabela store space is devoted to entertainment features and displays

• Loblaw has cooking classes; Lululemon offers yoga classes

• Burberry creates a seamless experience integra4ng mul4media technologies – Full length interac4ve screens & magic mirrors

– Live streaming hubs

– RFID tags

– Customiza4on Room

23

Augmented / Virtual Reality • 360 degree video technology allows consumers to

learn more about products before going to the store

• The Line, a luxury bou4que, has experiments with this using the Samsung Gear VR headset

– Allows customers to explore the store

– Clear descrip4on (and price tag) appear when an object catches customer’s agen4on

• The Samsung Gear VR headsets hit stores next year

• Widespread adop4on of VR in the retail space is expected in as ligle as three years

• Industry even has a new term for selling through VR: V-‐Commerce

24

25

26

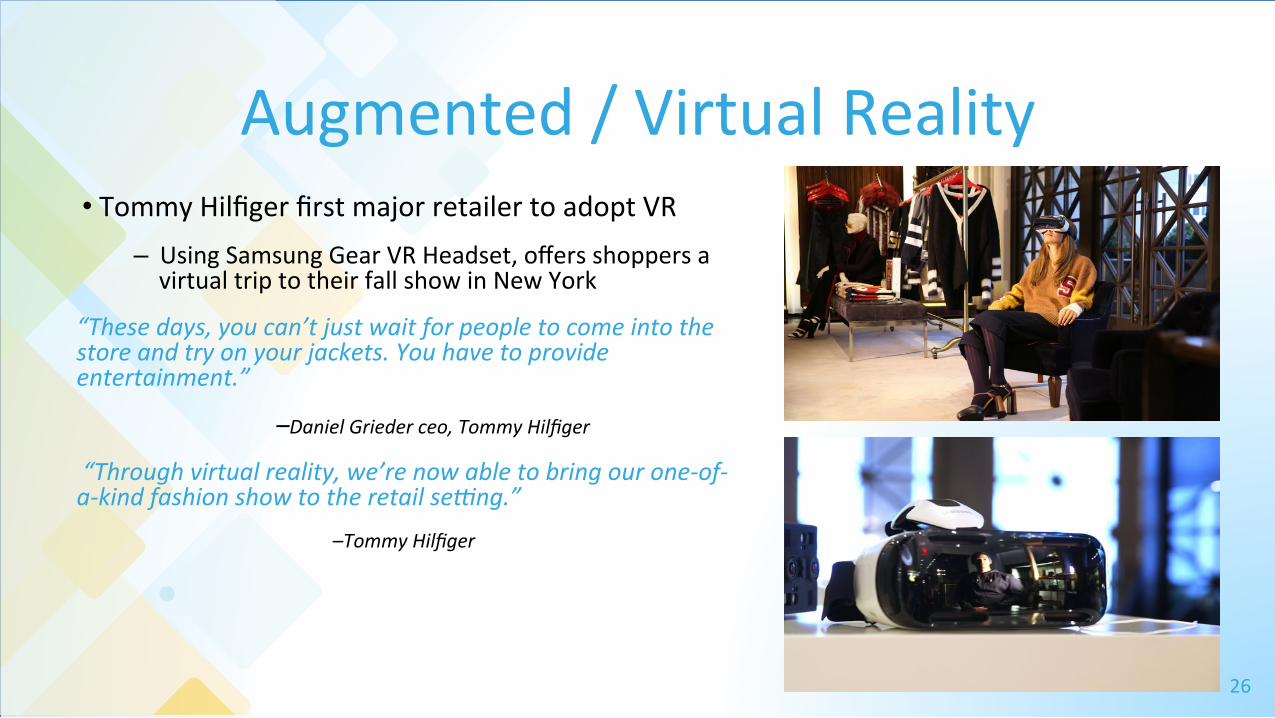

Augmented / Virtual Reality • Tommy Hilfiger first major retailer to adopt VR

– Using Samsung Gear VR Headset, offers shoppers a virtual trip to their fall show in New York

“These days, you can’t just wait for people to come into the store and try on your jackets. You have to provide entertainment.”

–Daniel Grieder ceo, Tommy Hilfiger

“Through virtual reality, we’re now able to bring our one-‐of-‐a-‐kind fashion show to the retail seWng.”

–Tommy Hilfiger

27

Robo4cs • Advances in technology are improving

capabili4es, decreasing cost, and making robots easier use

• Lowe’s piloted the OSHbot in 2014 in San Francisco

• Alibaba and Foxconn invest roughly $118 million in So{Bank Robo4cs Holdings, maker of Pepper

• AI-‐powered digital assistants: Messenger M, Cortana, Siri, IBM Watson

28

29

Robo4cs Increasing Use of Robots • Advances in technology are improving capabili4es, decreasing cost, and making robots easier to install and use

• Robots can li{ payloads, load pallets and bring goods to fulfilment agents

• Amazon spent $775 million to acquire robot maker Kiva systems for an expected savings of $400–$900 million per year

• Venture capital investment increased 24% last year to $239 million (excluding drones), driving future innova4on

30

Robo4cs • Suitable Technologies opens store staffed

solely with robots However, in Suitable Technologies showroom, salespeople appear only as robots

• Target teams with Techstars to improve shopper experience and will test robot workers at its upcoming concept store

31

3D Prin4ng Inside Retail Stores • UPS launched in-‐store 3D prin4ng service in 2013

• Macy’s new millennial floor at its NYC flagship store has a 3D prin4ng shop

• Staples has offered 3D prin4ng services in stores since 2014

32

Shopper Engagement Is Key For Brick & Mortars Example: Starbucks Mobile Ordering

• Mobile Order & Pay allows customers to locate the nearest store, select and customize their food and drink items, receive an es4mate of when the order will be ready, and prepay

• Mobile payments now account for 20% of the transac4ons in its stores (nearly 9 million transac4ons per week are mobile)

• Loca4on based promo4on, Star Reward, Skip the line

33

The Seamless Shopping Experience Example Digital Integra4on in

• At London flagship, Burberry has successfully integrated mul4media technologies to create a seamless shopping experience

– Full-‐length screens with audio-‐visual content – Live streaming hubs – Magic mirrors that allow customers to explore products they see

models wearing – RFID tags on apparel and beauty products – Portable point-‐of-‐sale systems – Customiza4on Room where shoppers can design their own garment and

share it social media

• Burberry Kisses – With Google technology, Burberry Kisses allows users to capture and

send a kiss to anyone in the world

34

35

Target’s Connected Home Store • Target gets into the connected home with a new retail

concept and an experimental store, in San Francisco

• Experimental store to figure out the challenge of selling the smart home to mainstream consumers

• Demonstrates how customers can bring together their new devices and make them work in their lives

• Highlight: Interac4ve Tables, Devices Usage Monitoring

36

37

Home Automa4on and Connected Home Store

• Big box retailers such as Lowes’ and Staples have launched their own line of home automa4on and connected home products

• Home Depot signed a partnership with Wink, while also promo4ng products such as the Nest thermostat, Rachio sprinklers, and products from other startups.

• Best Buy is crea4ng new in-‐store Connected Home departments to help customers understand and compare their op4ons, as well as improve home security, save energy costs and simplify the management of their homes.

38

The Omnishopper • She is your new best shopper, using technology everywhere to

discover, compare and learn. Hungry for informa4on. Diversity of opinions and sources of info drive an ‘in-‐charge’ feeling of confidence

• The store is the center of gravity. The omnishopper goes to stores for entertainment value, superior inventory and social interac4on

• The omnishopper is comfortable with stores she knows

• Omnishoppers visit fewer stores and focus research on extensive product knowledge

• Omnishoppers are not a path to the bogom. Their path to purchase discovers real value in deeper product knowledge, the more informa4on, the more comfortable they are making the purchase

• Promo4ons are important to only 18% of Omnishoppers

39

Deborah Weinswig Execu4ve Director, Fung Global Retail & Technology [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 @debweinswig

THANK YOU!