Property Market Update

29th March 2017

Welcome Gerry Devitt Managing Director

What’s Going On In Harvest these days?

We’ve recently hit €1 Billion in AUA

Adjudged the Best Retail Pension Advisory Firm for the Second Year

MiFID 2, MiFIR, IDD, GDPR, AML 4 . . . . . . .

160k Pension Schemes in Ireland today – 150 tomorrow??

So, business as usual then!

Investing in Property Terry Devitt Investment Director

The World We Are Living In

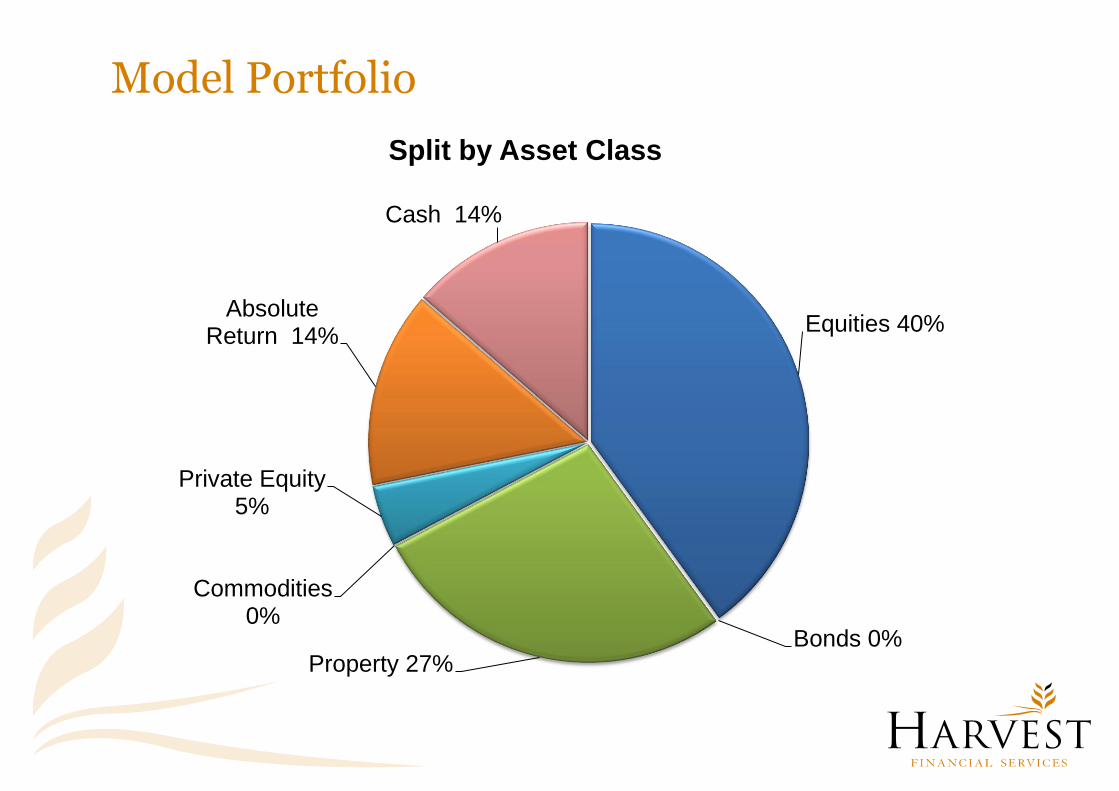

Model Portfolio

Equities 40%

Bonds 0% Property 27%

Commodities 0%

Private Equity 5%

Absolute Return 14%

Cash 14%

Split by Asset Class

Property vs Equities vs Bonds over 20 Years

Investing in Property

Property Options

Funds & REITS

Syndicated Investments

Development Properties

Direct Investments

Investment Option 1* - Funds and REITs

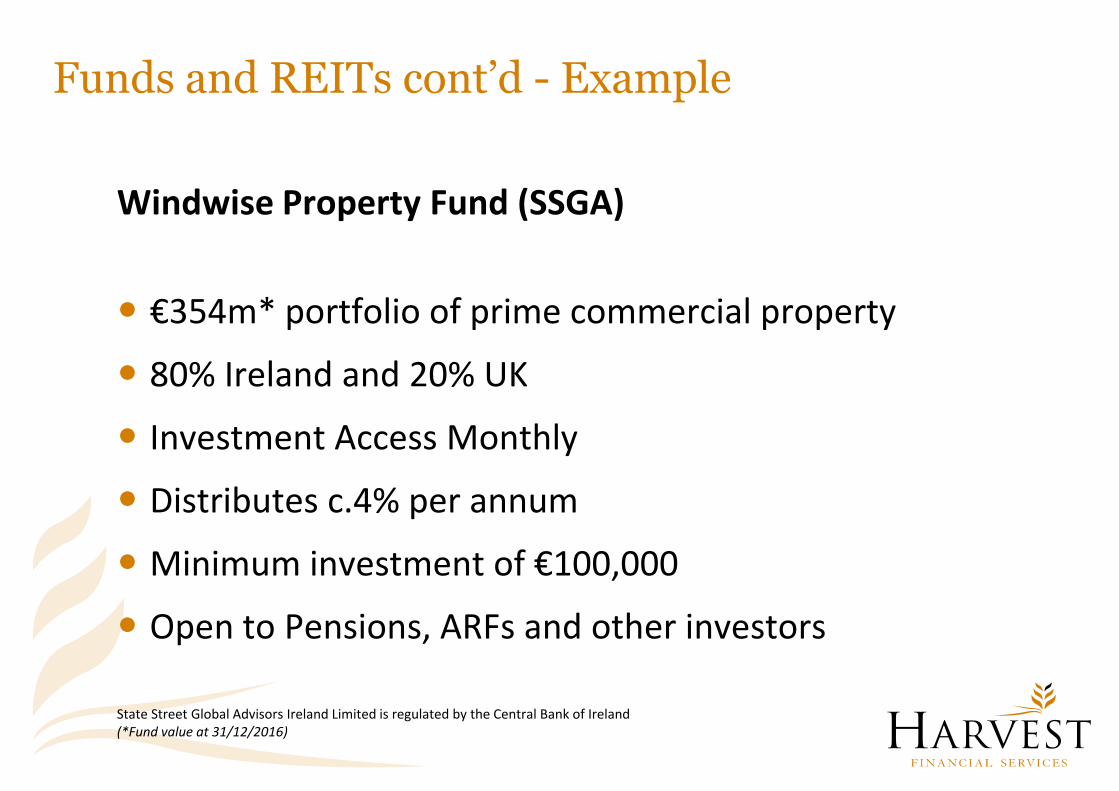

Funds and REITs cont’d - Example

Windwise Property Fund (SSGA)

€354m* portfolio of prime commercial property

80% Ireland and 20% UK

Investment Access Monthly

Distributes c.4% per annum

Minimum investment of €100,000

Open to Pensions, ARFs and other investors

State Street Global Advisors Ireland Limited is regulated by the Central Bank of Ireland (*Fund value at 31/12/2016)

Funds and REITs cont’d IPUT -10 Year Price Chart

Still c.20% off its 2007 high…but holders compensated by c.50% in distributions over 10 years

2012

Today Price still 20% below 2007 high – but investors have received c. 50% in dividends since then

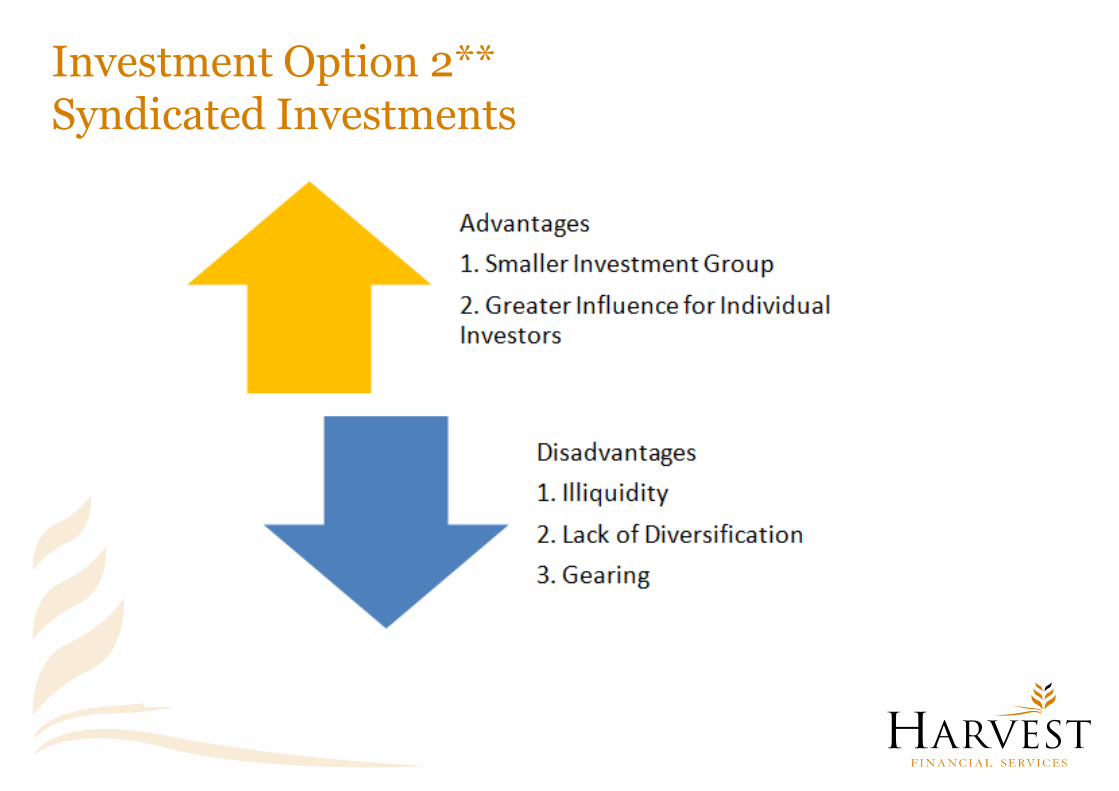

Investment Option 2** Syndicated Investments

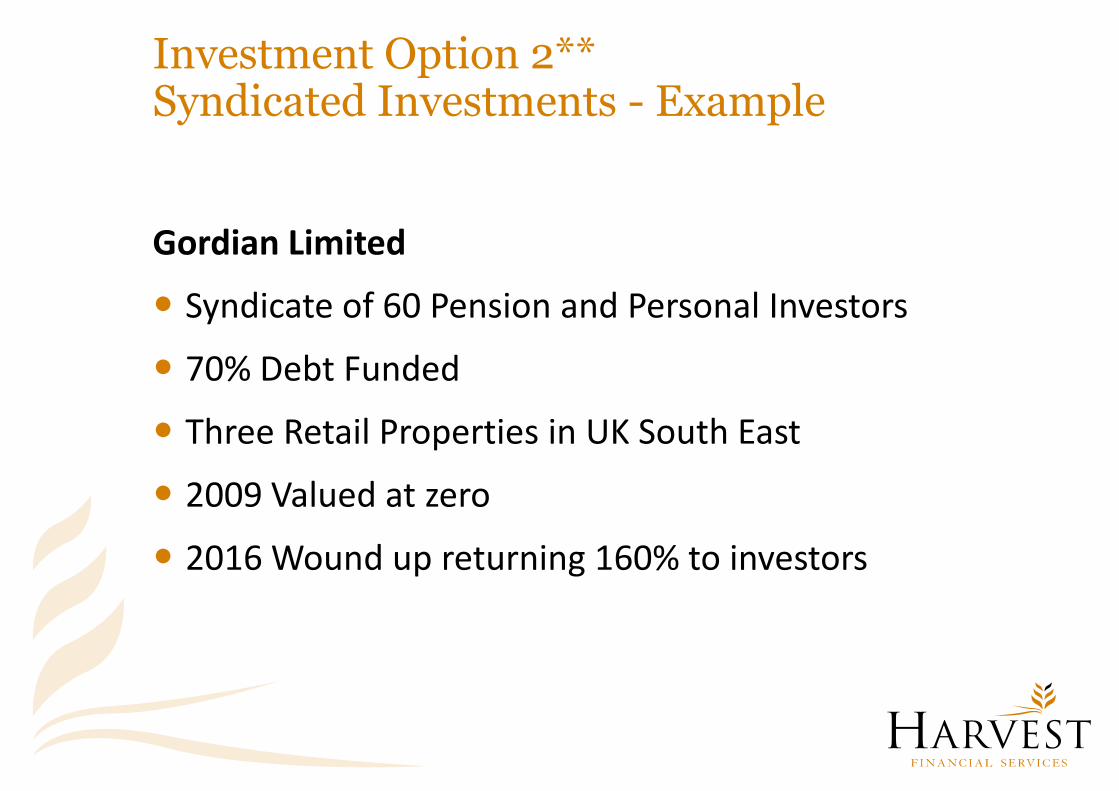

Investment Option 2** Syndicated Investments - Example

Gordian Limited

Syndicate of 60 Pension and Personal Investors

70% Debt Funded

Three Retail Properties in UK South East

2009 Valued at zero

2016 Wound up returning 160% to investors

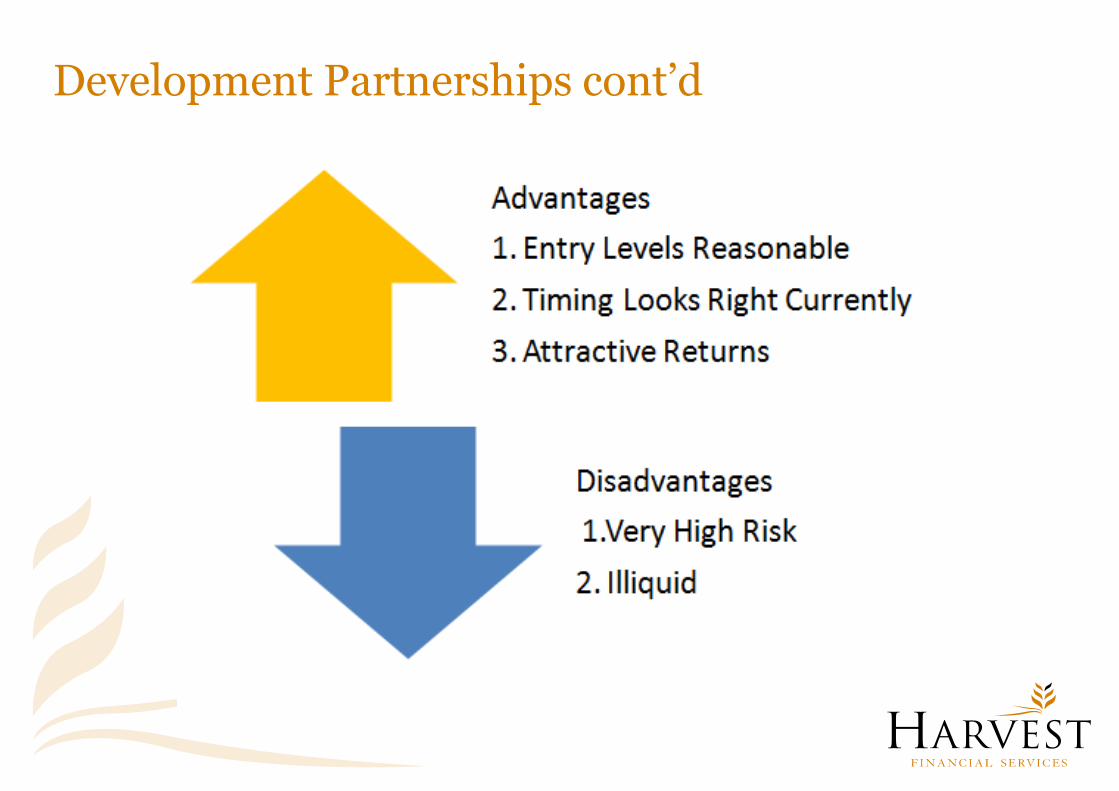

Investment Option 3** Development Partnerships

What are they?

This is where a consortium of investors wholly or partly replace the bank to finance a property development (usually residential).

Funds usually attract an interest rate of c.10% per annum and receive a share of the profits on completion.

Investment term is usually around 2 years

Development Partnerships cont’d

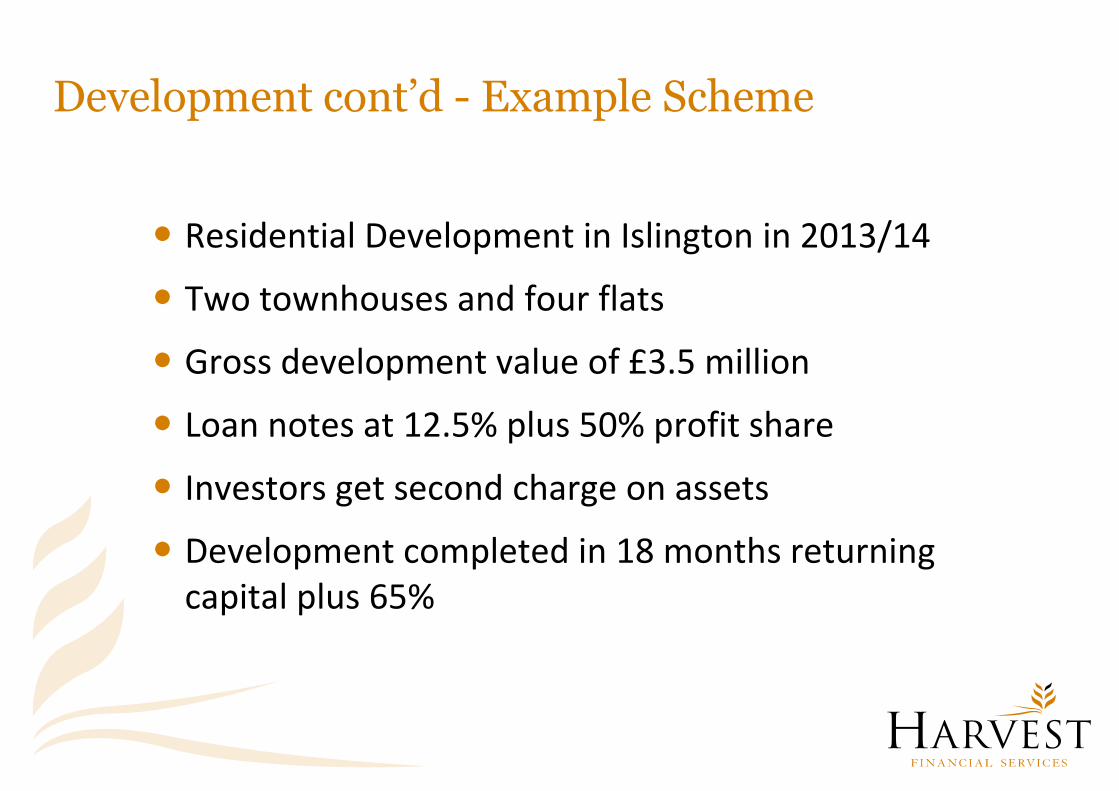

Development cont’d - Example Scheme

Residential Development in Islington in 2013/14

Two townhouses and four flats

Gross development value of £3.5 million

Loan notes at 12.5% plus 50% profit share

Investors get second charge on assets

Development completed in 18 months returning capital plus 65%

Development cont’d - Example Schemes

Harvest has Launched a Series of schemes over past two years in partnership with developers

Henley (Oxfordshire)

Maidstone (Kent)

Grove Road (Glasnevin)

Howth Road (Clontarf)

Church Road (Killiney)

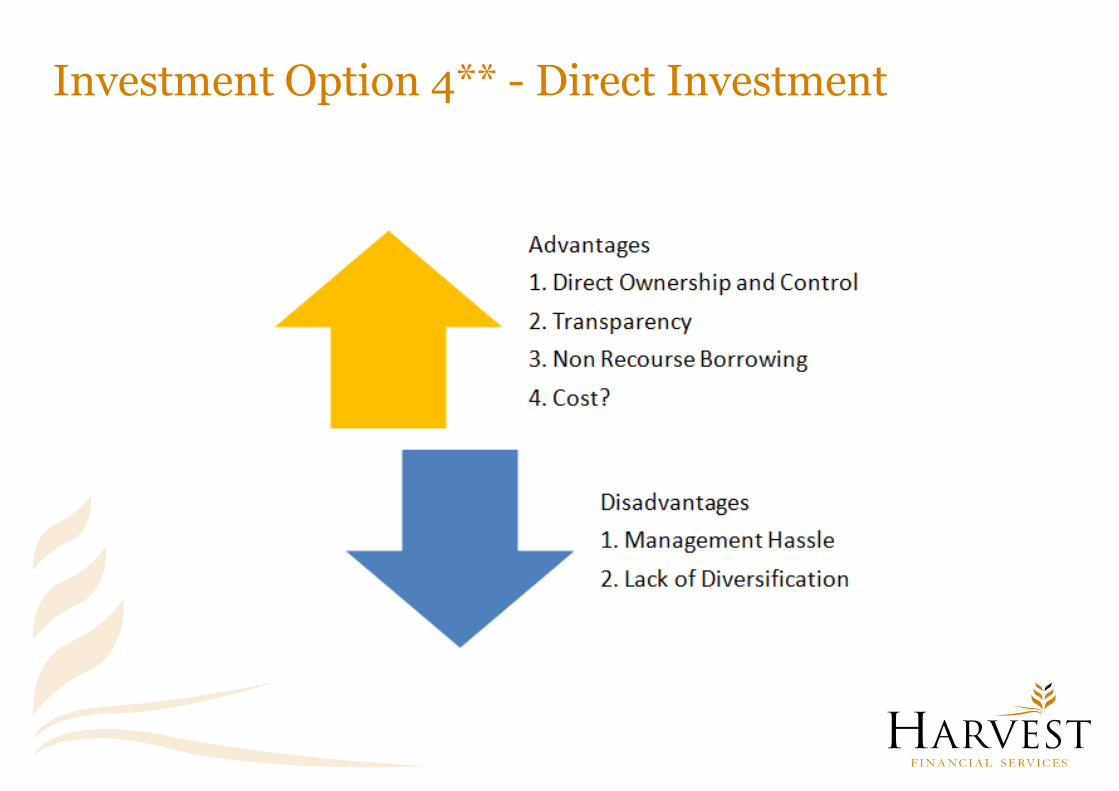

Investment Option 4** - Direct Investment

Investment Option 4** - Direct Investment

Individual Property Purchase

Residential or Commercial

Harvest Property Advisory Services

We provide specialist advice and help source commercial properties for clients

Lot Sizes €1m to €15m

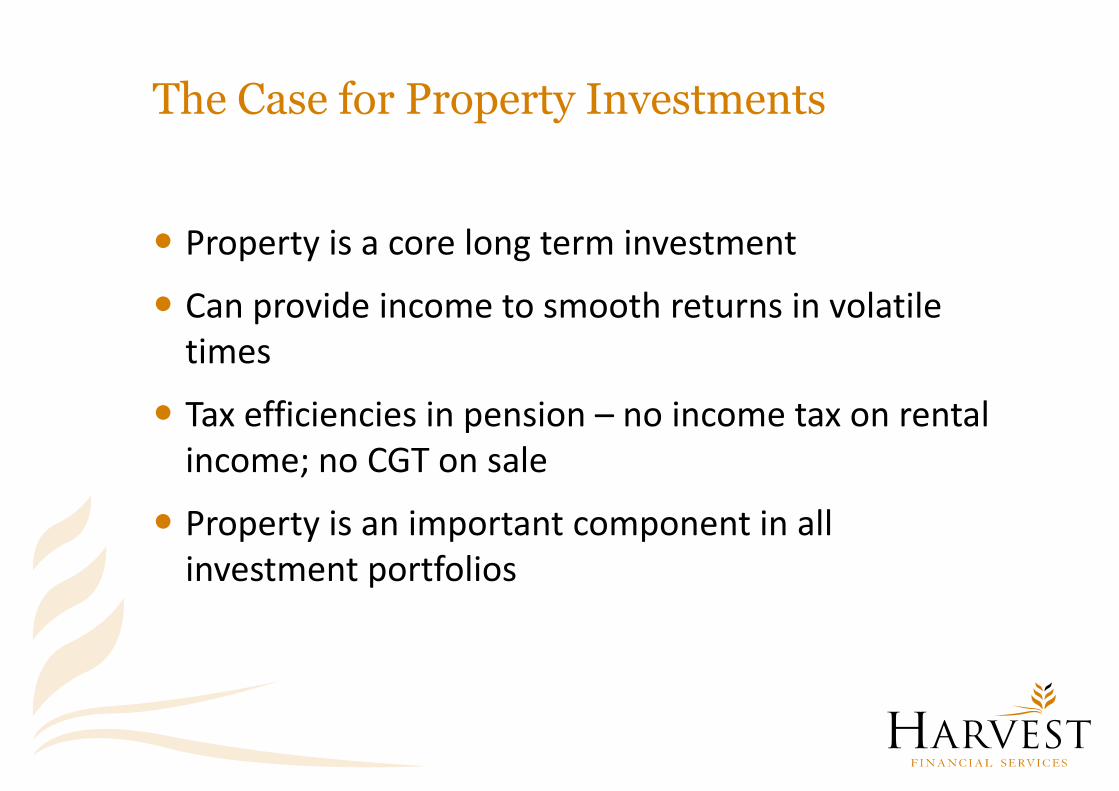

The Case for Property Investments

Property is a core long term investment

Can provide income to smooth returns in volatile times

Tax efficiencies in pension – no income tax on rental income; no CGT on sale

Property is an important component in all investment portfolios

The information contained herein is based on Harvest Financial Services Limited's understanding of current Revenue practice as at March 2017 and may change in the future. The material is not intended to provide advice and is provided for general information purposes only. ****Warnings: Investment in property involves special risks that could lead to a loss of all or a substantial portion of your investment. If you invest in this QIAIF you may lose some or all of the money you invest. If you invest in this QIAIF you will have restricted access to your money as the minimum holding in the QIAIF at all times is €100,000 and as redemption of units is restricted to 4 times a year. The projected figure is an estimate only and is not a reliable guide to the future annual payment from this QIAIF. The income you get from this QIAIF may go down as well as up and will fluctuate in accordance with market conditions and taxation arrangements. Warnings: Past performance is not a reliable guide to future performance. This QIAIF may be affected by changes in currency exchange rates. Changes in exchange rates may have an adverse effect on the value price or income of the QIAIF. The value of the QIAIF may be subject to sudden and large falls in value.

*Harvest Financial Services Limited is regulated by the Central Bank of Ireland **Please note that the provision of this product or service does not require licensing, authorisation, or registration with the Central Bank of Ireland and, as a result, it is not covered by the Central Bank's requirements designed to protect consumers or by a statutory compensation scheme.

Property Market Trends Past,

Present and Projections 29th March 2017

Prepared by

Marian Finnegan, Chief Economist

Economic and

Political Backdrop

24 Cushman & Wakefield and Sherry FitzGerald

AN OVERVIEW

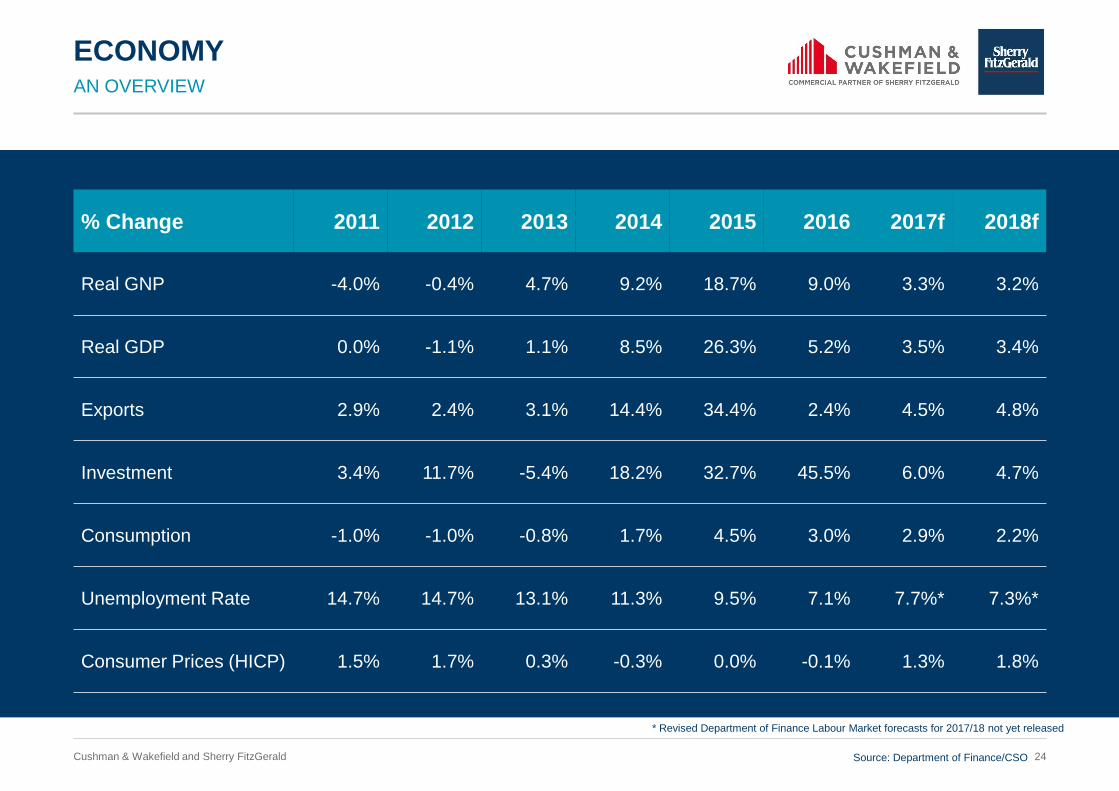

ECONOMY

% Change 2011 2012 2013 2014 2015 2016 2017f 2018f

Real GNP -4.0% -0.4% 4.7% 9.2% 18.7% 9.0% 3.3% 3.2%

Real GDP 0.0% -1.1% 1.1% 8.5% 26.3% 5.2% 3.5% 3.4%

Exports 2.9% 2.4% 3.1% 14.4% 34.4% 2.4% 4.5% 4.8%

Investment 3.4% 11.7% -5.4% 18.2% 32.7% 45.5% 6.0% 4.7%

Consumption -1.0% -1.0% -0.8% 1.7% 4.5% 3.0% 2.9% 2.2%

Unemployment Rate 14.7% 14.7% 13.1% 11.3% 9.5% 7.1% 7.7%* 7.3%*

Consumer Prices (HICP) 1.5% 1.7% 0.3% -0.3% 0.0% -0.1% 1.3% 1.8%

Source: Department of Finance/CSO

* Revised Department of Finance Labour Market forecasts for 2017/18 not yet released

25 Cushman & Wakefield and Sherry FitzGerald

CENTRAL BANK

PDH mortgages for non-first time buyers are subject to a limit

of 80 per cent LTV.

For first time buyers of properties a maximum LTV of 90 per cent

will apply.

These LTV limits should not be exceeded by more than 20 per

cent of the euro value of all housing loans for second and

subsequent PDH purposes, and not be exceeded by more than 5

per cent of the euro value of all housing loans for first time

buyers, during an annual period.

LOAN TO VALUE (LTV) FOR

PRINCIPAL DWELLING HOUSES (PDH)

BTL mortgages are subject to a limit of 70 per cent LTV.

This limit can only be exceeded by no more than 10 per cent of

the euro value of all housing loans for non PDH purposes during

an annual period.

LOAN TO VALUE (LTV) FOR

BUY TO LET MORTGAGES (BTLS)

PDH mortgage loans are subject to a limit of 3.5 times loan to

gross income.

This limit should not be exceeded by more than 20 per cent of

the euro value of all housing loans for PDH purposes during an

annual period.

LOAN TO INCOME (LTI) FOR

PDH MORTGAGES

Source: Department of Finance/CSO

26 Cushman & Wakefield and Sherry FitzGerald

PROPERTY MEASURES

BUDGET 2017

THE HELP-TO-BUY SCHEME

APPLIES TO NEW HOMES

A tax rebate of up to

€20,000 or 5%

of the value of the house to

first time buyers of new homes.

OTHER MEASURES

• Home Renovation Scheme – Extended to end 2018

• Mortgage Interest Relief – Increasing from 75% to

80% in 2017

• Living City initiative – scope has been expanded

WHO QUALIFIES?

Only first time buyers of a new home from

July 19 2016 to 2019.

€250,000

€300,000

€400,000

VALUE REBATE

€12,500

€15,000

€20,000

Source: Sherry FitzGerald Research

RESIDENTIAL MARKET

28 Cushman & Wakefield and Sherry FitzGerald

2011 – Q4 2016

VOLUME OF SALES

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Q1

20

11

Q2

20

11

Q3

20

11

Q4

20

11

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

12

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

13

Q1

20

14

Q2

10

14

Q3

20

14

Q4

20

14

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

15

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

16

44,700 sales in Ireland*

Source: PPR/Sherry FitzGerald Research

*Excludes multi-family/block sales

29 Cushman & Wakefield and Sherry FitzGerald

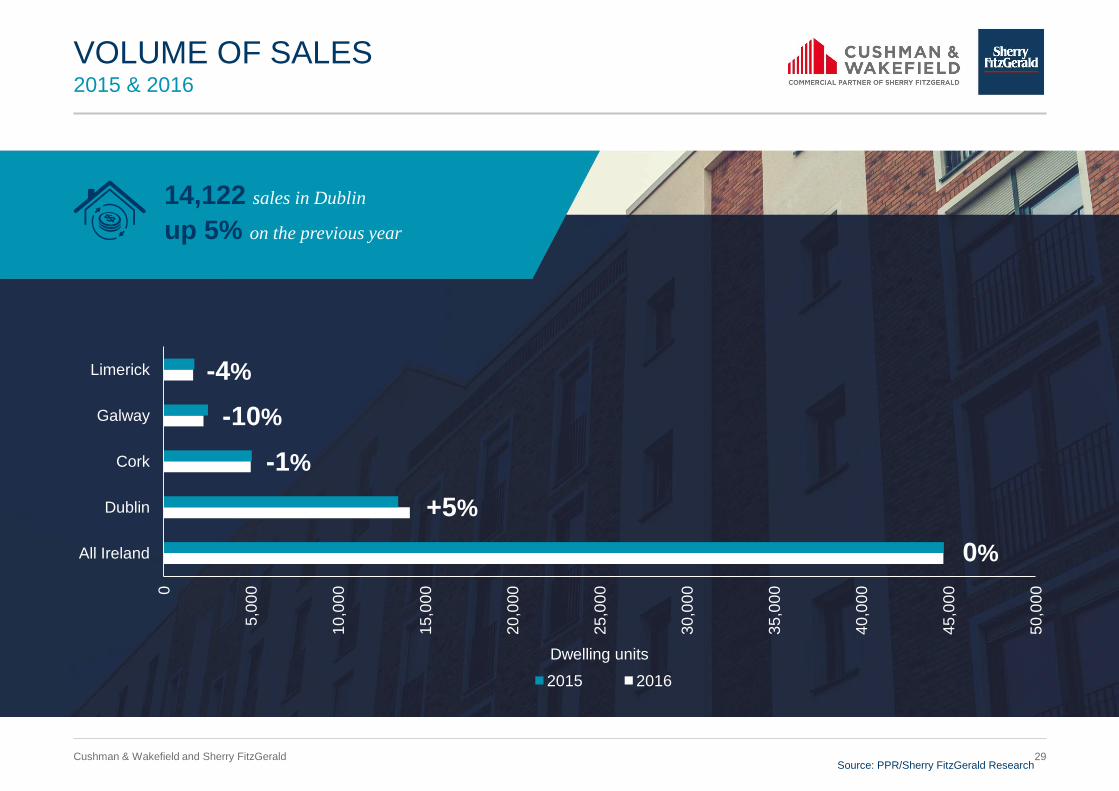

2015 & 2016

VOLUME OF SALES

14,122 sales in Dublin

up 5% on the previous year

0

5,0

00

10

,00

0

15

,00

0

20

,00

0

25

,00

0

30

,00

0

35

,00

0

40

,00

0

45

,00

0

50

,00

0

All Ireland

Dublin

Cork

Galway

Limerick

Dwelling units

2015 2016

-4%

-10%

-1%

+5%

0%

Source: PPR/Sherry FitzGerald Research

30 Cushman & Wakefield and Sherry FitzGerald

2007 – 2016

MORTGAGE DRAWDOWNS*

17,295 mortgages with a value of

€3.4 billion drawn down YTD

Cash buyers account for 47% of market

0

5,000

10,000

15,000

20,000

25,000

Q3

20

07

Q4

20

07

Q1

20

08

Q2

20

08

Q3

20

08

Q4

20

08

Q1

20

09

Q2

20

09

Q3

20

09

Q4

20

09

Q1

20

10

Q2

20

10

Q3

20

10

Q4

20

10

Q1

20

11

Q2

20

11

Q3

20

11

Q4

20

11

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

12

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

13

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

14

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

15

Q1

20

16

Q2

20

16

Q3

20

16

Units

*Excludes top-ups and re-mortgages

Source: BPFI/Sherry FitzGerald Research

31 Cushman & Wakefield and Sherry FitzGerald

2016

PROFILE OF PURCHASERS

Ireland Dublin

Owner Occupation 71% 78%

Investment 20% 16%

Additional Residence 8% 6%

Development 1% 1%

Source: Sherry FitzGerald Research

32 Cushman & Wakefield and Sherry FitzGerald

DEMOGRAPHIC PROJECTIONS

FUTURE DEMANDS

Year Population Ireland Population Dublin

2016 4.76 million 1.35 million

2021 4.88 million 1.38 million

2026 5.04 million 1.43 million

Source: CSO/Sherry FitzGerald Research

33 Cushman & Wakefield and Sherry FitzGerald

DEMOGRAPHIC PROJECTIONS

FUTURE DEMANDS

Year Housing Demand Ireland Housing Demand Dublin

2016-21 36,950 10,400

2021-26 34,400 10,300

Average PA 35,700 10,350

Source: CSO/Sherry FitzGerald Research

34 Cushman & Wakefield and Sherry FitzGerald

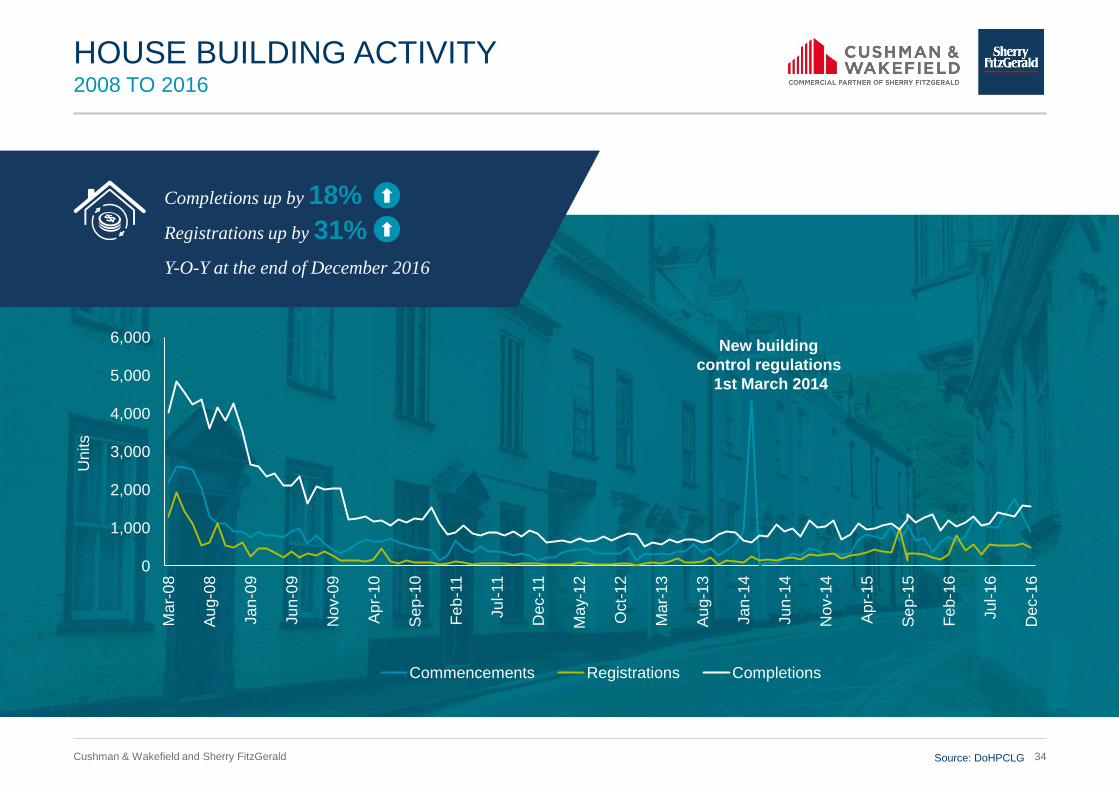

2008 TO 2016

HOUSE BUILDING ACTIVITY

Completions up by 18%

Source: DoHPCLG

Registrations up by 31%

Y-O-Y at the end of December 2016

0

1,000

2,000

3,000

4,000

5,000

6,000

Ma

r-0

8

Au

g-0

8

Ja

n-0

9

Ju

n-0

9

Nov-0

9

Ap

r-1

0

Se

p-1

0

Feb

-11

Ju

l-11

Dec-1

1

Ma

y-1

2

Oct-

12

Ma

r-1

3

Au

g-1

3

Ja

n-1

4

Ju

n-1

4

Nov-1

4

Ap

r-1

5

Se

p-1

5

Feb

-16

Ju

l-1

6

Dec-1

6

Commencements Registrations Completions

Units

New building

control regulations

1st March 2014

35 Cushman & Wakefield and Sherry FitzGerald

1973 – 2016

HOUSING COMPLETIONS

14,932 units completed in 2016

Source: DoHPCLG

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

36 Cushman & Wakefield and Sherry FitzGerald

2015 – 2016

HOUSING COMPLETIONS – REGIONAL CENTRES

Dublin Cork Galway Limerick

+46% +27% +13% +4%

2,8

91

4,2

34

1,4

32

1,8

17

72

2

81

7

47

9

45

9

January – December 2015 January – December 2016

Completions up by 46%

in Dublin Y-O-Y

Source: DoHPCLG

37 Cushman & Wakefield and Sherry FitzGerald

2016 – IRELAND

VENDOR ANALYSIS

32% of Vendors ‘Selling Investment’

32% Selling Investment

13% Executor Sale

11% Relocating in Ireland

11% Larger House

11% Bank Repossession

10% Smaller House

12% Other

Source: Sherry FitzGerald Research

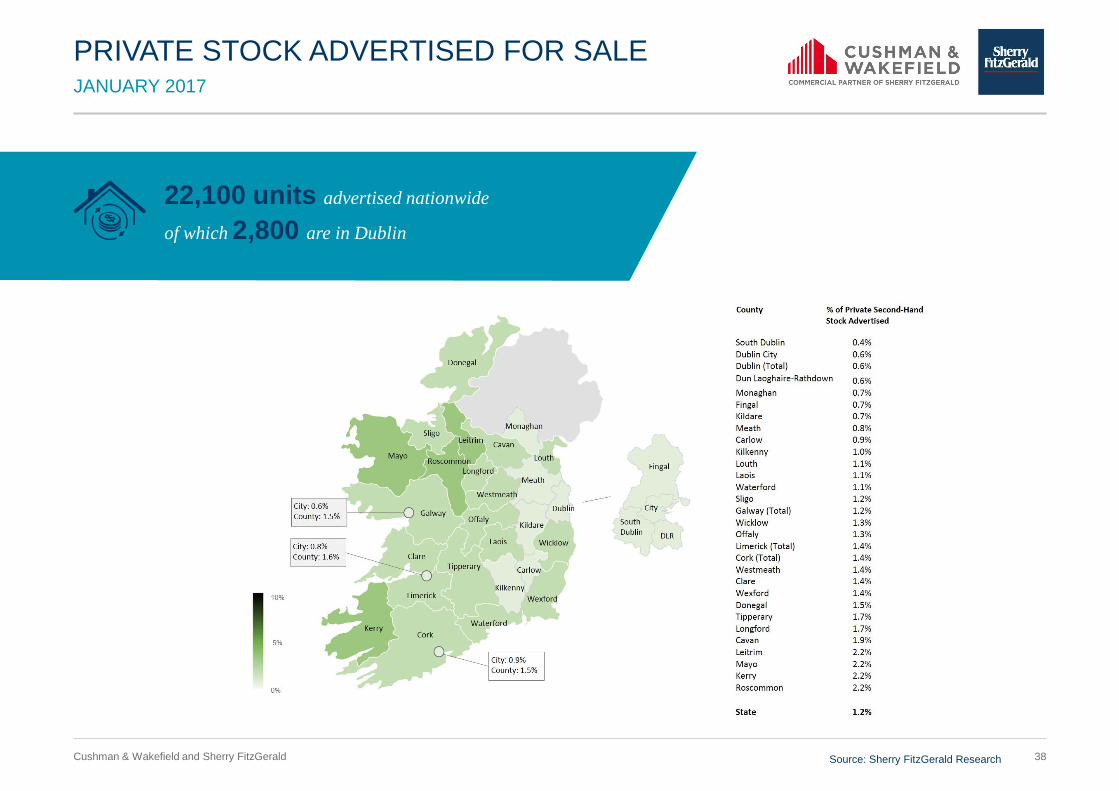

38 Cushman & Wakefield and Sherry FitzGerald

JANUARY 2017

PRIVATE STOCK ADVERTISED FOR SALE

22,100 units advertised nationwide

of which 2,800 are in Dublin

Source: Sherry FitzGerald Research

39 Cushman & Wakefield and Sherry FitzGerald

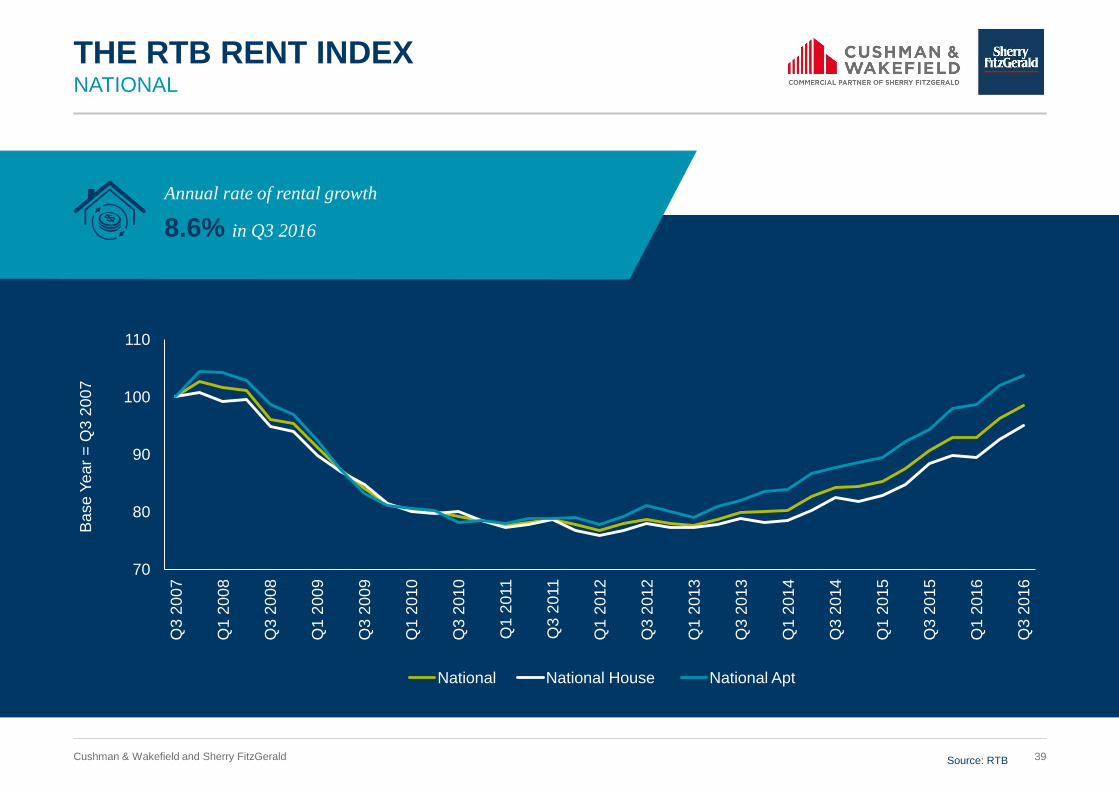

NATIONAL

THE RTB RENT INDEX

Annual rate of rental growth

8.6% in Q3 2016

70

80

90

100

110

Q3

20

07

Q1

20

08

Q3

20

08

Q1

20

09

Q3

20

09

Q1

20

10

Q3

20

10

Q1

20

11

Q3

20

11

Q1

20

12

Q3

20

12

Q1

20

13

Q3

20

13

Q1

20

14

Q3

20

14

Q1

20

15

Q3

20

15

Q1

20

16

Q3

20

16

Ba

se

Ye

ar

= Q

3 2

00

7

National National House National Apt

Source: RTB

40 Cushman & Wakefield and Sherry FitzGerald

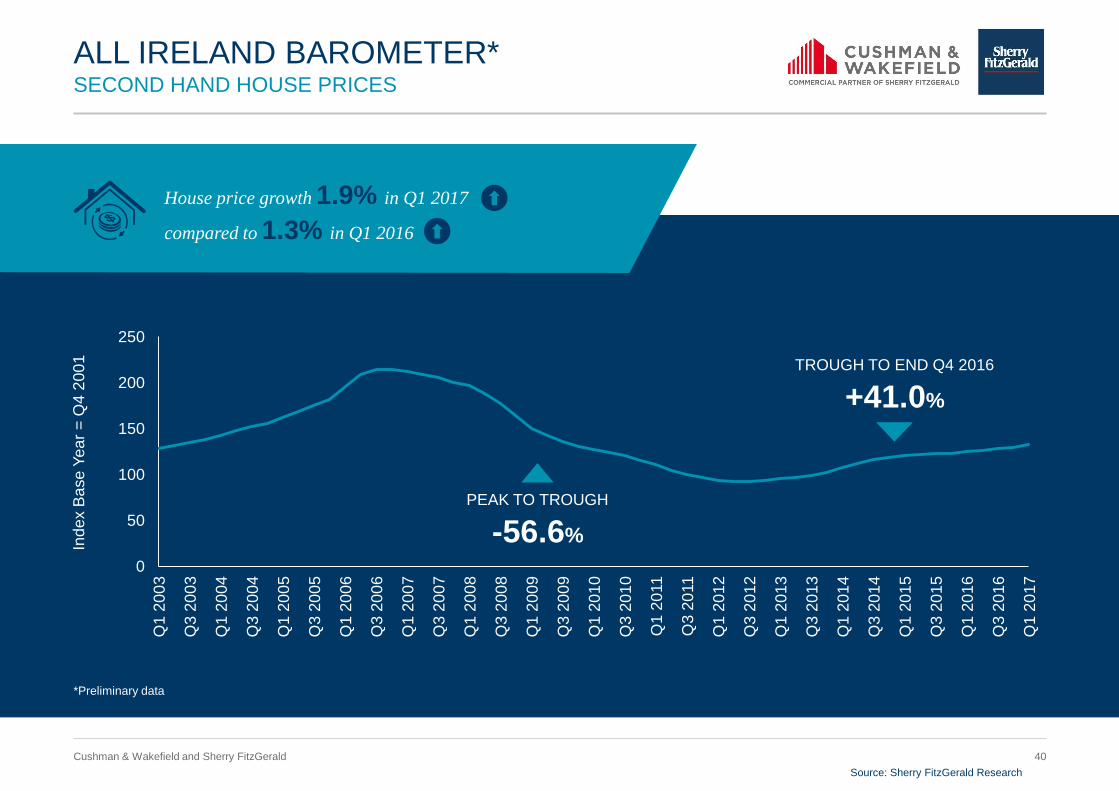

SECOND HAND HOUSE PRICES

ALL IRELAND BAROMETER*

House price growth 1.9% in Q1 2017

compared to 1.3% in Q1 2016

0

50

100

150

200

250

Q1

20

03

Q3

20

03

Q1

20

04

Q3

20

04

Q1

20

05

Q3

20

05

Q1

20

06

Q3

20

06

Q1

20

07

Q3

20

07

Q1

20

08

Q3

20

08

Q1

20

09

Q3

20

09

Q1

20

10

Q3

20

10

Q1

20

11

Q3

20

11

Q1

20

12

Q3

20

12

Q1

20

13

Q3

20

13

Q1

20

14

Q3

20

14

Q1

20

15

Q3

20

15

Q1

20

16

Q3

20

16

Q1

20

17

Ind

ex B

ase

Ye

ar

= Q

4 2

00

1

PEAK TO TROUGH

-56.6%

TROUGH TO END Q4 2016

+41.0%

Source: Sherry FitzGerald Research

*Preliminary data

41 Cushman & Wakefield and Sherry FitzGerald

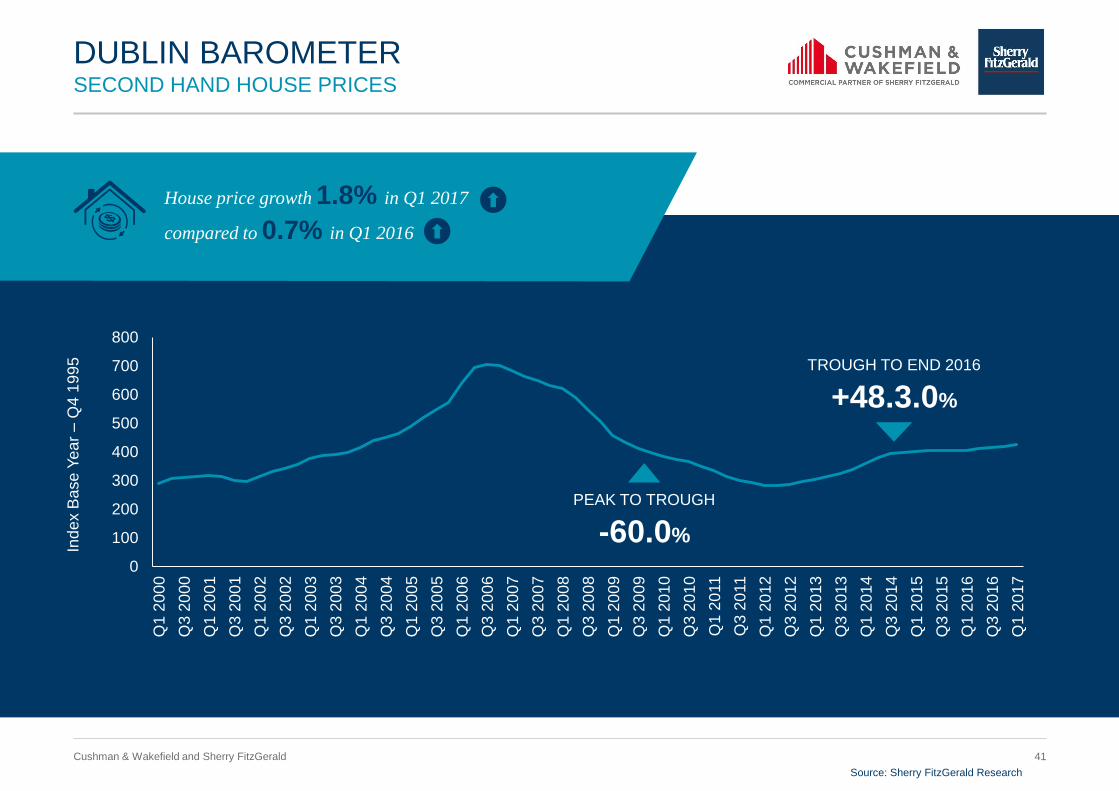

SECOND HAND HOUSE PRICES

DUBLIN BAROMETER

House price growth 1.8% in Q1 2017

compared to 0.7% in Q1 2016

0

100

200

300

400

500

600

700

800

Q1

20

00

Q3

20

00

Q1

20

01

Q3

20

01

Q1

20

02

Q3

20

02

Q1

20

03

Q3

20

03

Q1

20

04

Q3

20

04

Q1

20

05

Q3

20

05

Q1

20

06

Q3

20

06

Q1

20

07

Q3

20

07

Q1

20

08

Q3

20

08

Q1

20

09

Q3

20

09

Q1

20

10

Q3

20

10

Q1

20

11

Q3

20

11

Q1

20

12

Q3

20

12

Q1

20

13

Q3

20

13

Q1

20

14

Q3

20

14

Q1

20

15

Q3

20

15

Q1

20

16

Q3

20

16

Q1

20

17

Ind

ex B

ase

Ye

ar

– Q

4 1

99

5

PEAK TO TROUGH

-60.0%

TROUGH TO END 2016

+48.3.0%

Source: Sherry FitzGerald Research

42 Cushman & Wakefield and Sherry FitzGerald

Q4 2016 – VALUES OFF PEAK %

SECOND-HAND HOUSE PRICES

Galway

-39.7%

Dublin

-40.8%

Limerick

-39.7%

Cork

-36.8%

Source: Sherry FitzGerald Research

43 Cushman & Wakefield and Sherry FitzGerald

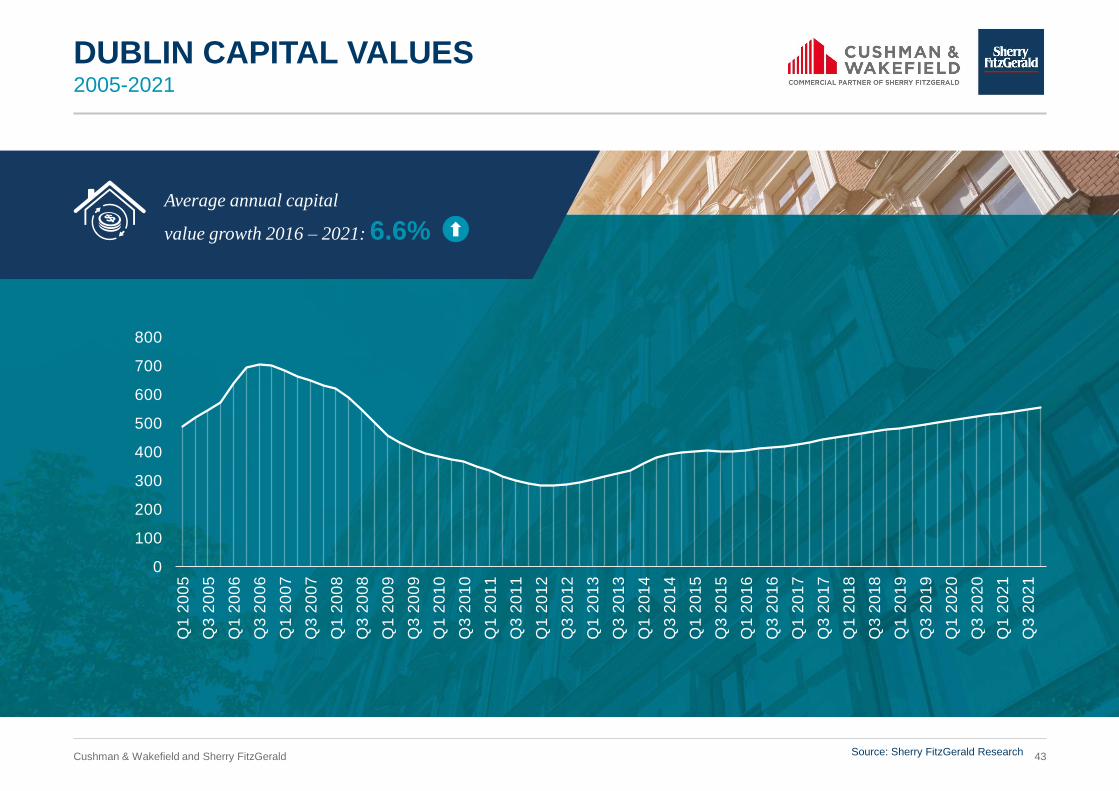

2005-2021

DUBLIN CAPITAL VALUES

Average annual capital

value growth 2016 – 2021: 6.6%

0

100

200

300

400

500

600

700

800

Q1

20

05

Q3

20

05

Q1

20

06

Q3

20

06

Q1

20

07

Q3

20

07

Q1

20

08

Q3

20

08

Q1

20

09

Q3

20

09

Q1

20

10

Q3

20

10

Q1

20

11

Q3

20

11

Q1

20

12

Q3

20

12

Q1

20

13

Q3

20

13

Q1

20

14

Q3

20

14

Q1

20

15

Q3

20

15

Q1

20

16

Q3

20

16

Q1

20

17

Q3

20

17

Q1

20

18

Q3

20

18

Q1

20

19

Q3

20

19

Q1

20

20

Q3

20

20

Q1

20

21

Q3

20

21

Source: Sherry FitzGerald Research

Commercial Market

Investment & Occupier Trends

45 Cushman & Wakefield and Sherry FitzGerald

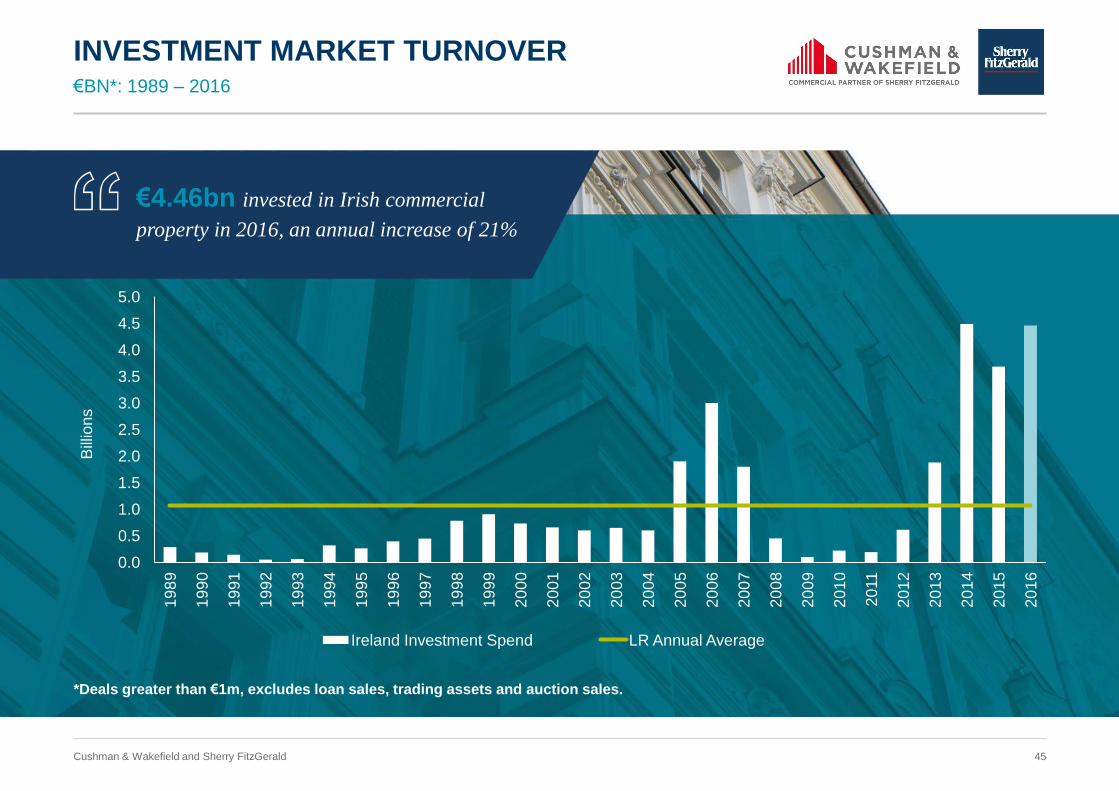

€BN*: 1989 – 2016

INVESTMENT MARKET TURNOVER

€4.46bn invested in Irish commercial

property in 2016, an annual increase of 21%

*Deals greater than €1m, excludes loan sales, trading assets and auction sales.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Bill

ion

s

Ireland Investment Spend LR Annual Average

46 Cushman & Wakefield and Sherry FitzGerald

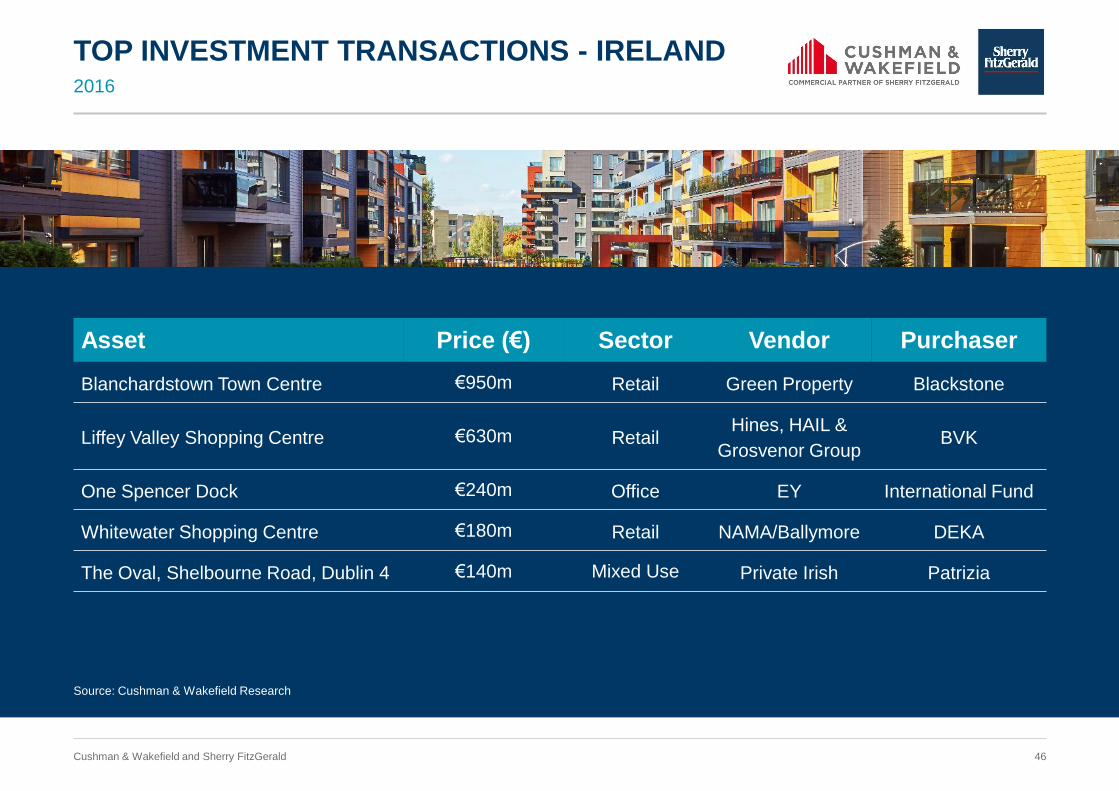

TOP INVESTMENT TRANSACTIONS - IRELAND 2016

Asset Price (€) Sector Vendor Purchaser

Blanchardstown Town Centre €950m Retail Green Property Blackstone

Liffey Valley Shopping Centre €630m Retail Hines, HAIL &

Grosvenor Group BVK

One Spencer Dock €240m Office EY International Fund

Whitewater Shopping Centre €180m Retail NAMA/Ballymore DEKA

The Oval, Shelbourne Road, Dublin 4 €140m Mixed Use Private Irish Patrizia

Source: Cushman & Wakefield Research

47 Cushman & Wakefield and Sherry FitzGerald

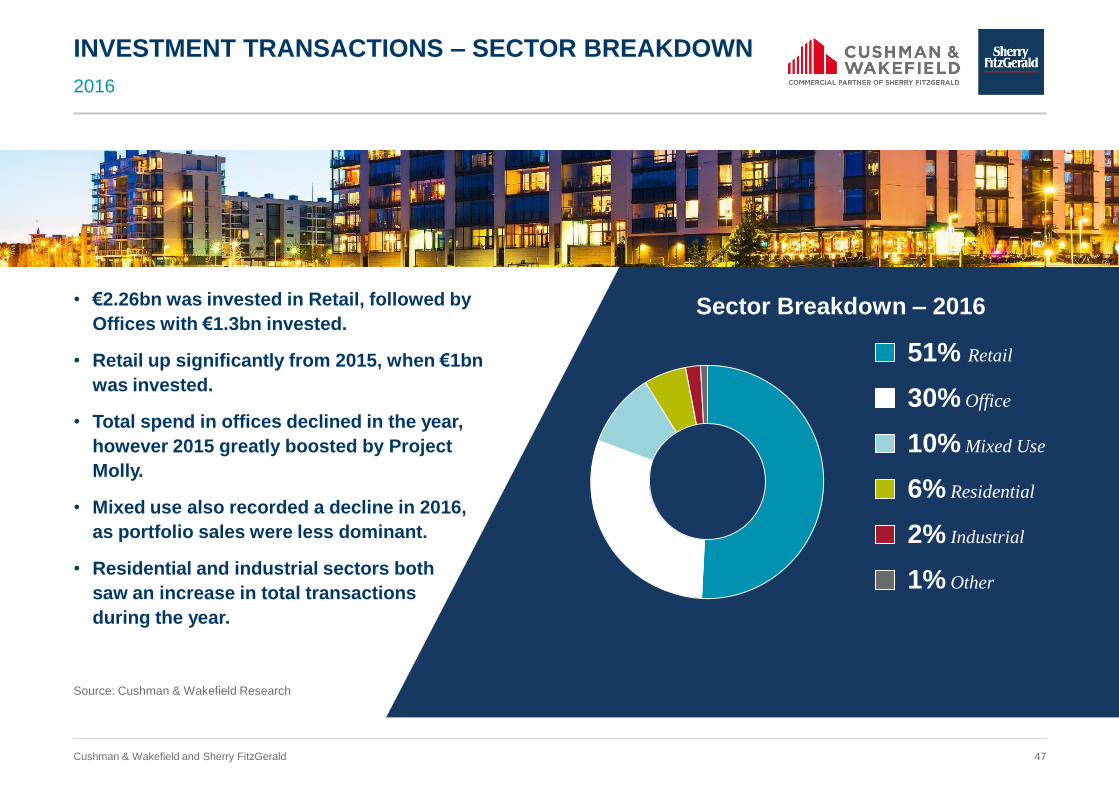

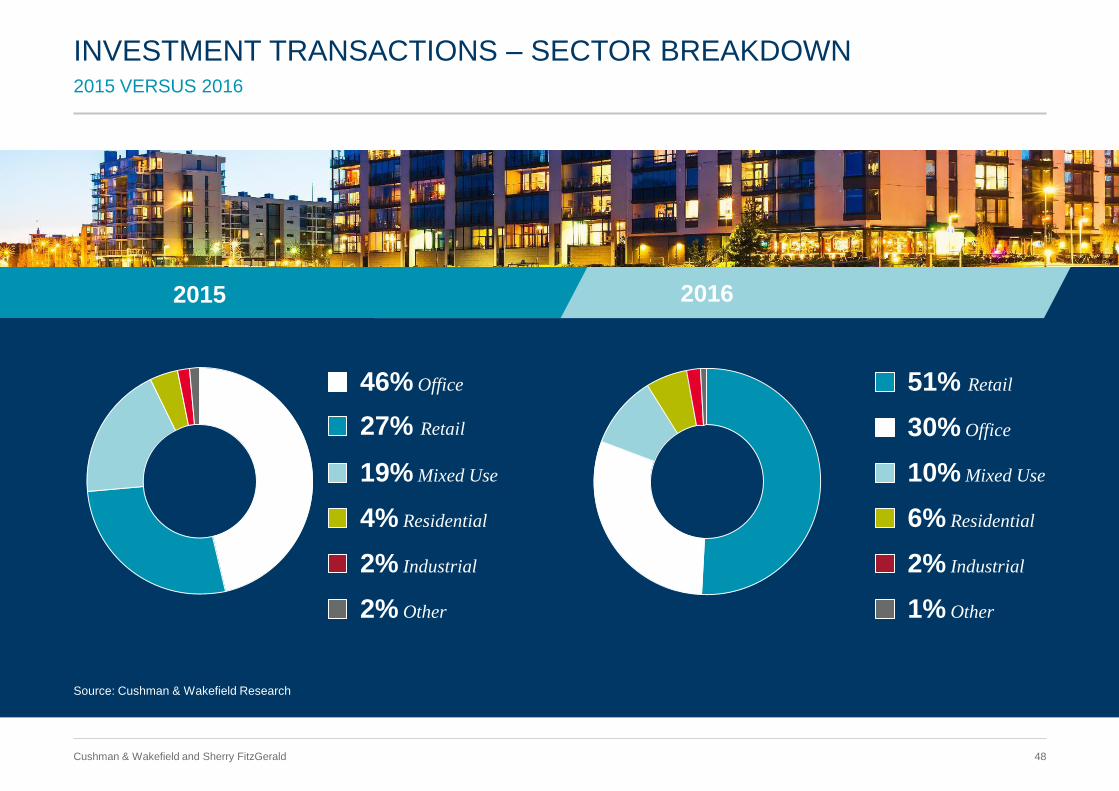

2016

INVESTMENT TRANSACTIONS – SECTOR BREAKDOWN

• €2.26bn was invested in Retail, followed by

Offices with €1.3bn invested.

• Retail up significantly from 2015, when €1bn

was invested.

• Total spend in offices declined in the year,

however 2015 greatly boosted by Project

Molly.

• Mixed use also recorded a decline in 2016,

as portfolio sales were less dominant.

• Residential and industrial sectors both

saw an increase in total transactions

during the year.

Sector Breakdown – 2016

51% Retail

30% Office

10% Mixed Use

6% Residential

2% Industrial

1% Other

Source: Cushman & Wakefield Research

48 Cushman & Wakefield and Sherry FitzGerald

2015 VERSUS 2016

INVESTMENT TRANSACTIONS – SECTOR BREAKDOWN

2015 2016

Source: Cushman & Wakefield Research

51% Retail

30% Office

10% Mixed Use

6% Residential

2% Industrial

1% Other

46% Office

27% Retail

19% Mixed Use

4% Residential

2% Industrial

2% Other

49 Cushman & Wakefield and Sherry FitzGerald

2016

INVESTMENT TRANSACTIONS – LOCATION BREAKDOWN

The share of total spend outside of Dublin in 2016 was 14%

86% Dublin

14% Outside of Dublin

Source: Cushman & Wakefield Research

50 Cushman & Wakefield and Sherry FitzGerald

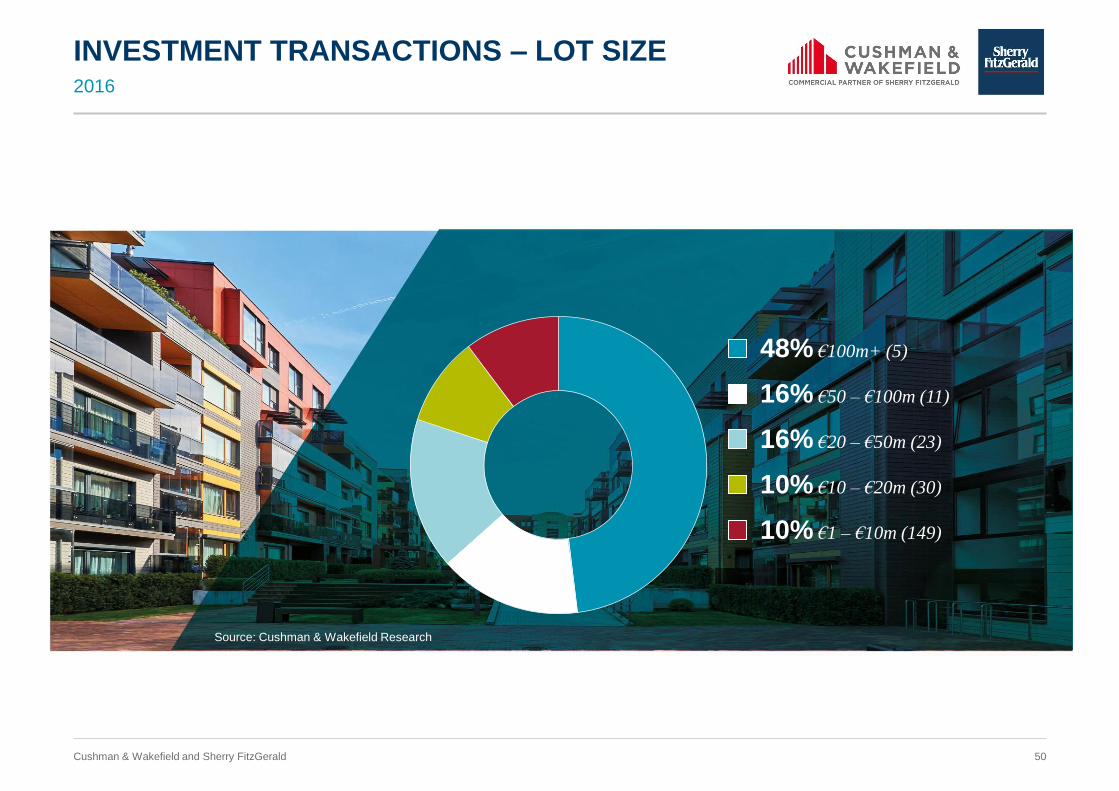

INVESTMENT TRANSACTIONS – LOT SIZE 2016

48% €100m+ (5)

16% €50 – €100m (11)

16% €20 – €50m (23)

10% €10 – €20m (30)

10% €1 – €10m (149)

Source: Cushman & Wakefield Research

51 Cushman & Wakefield and Sherry FitzGerald

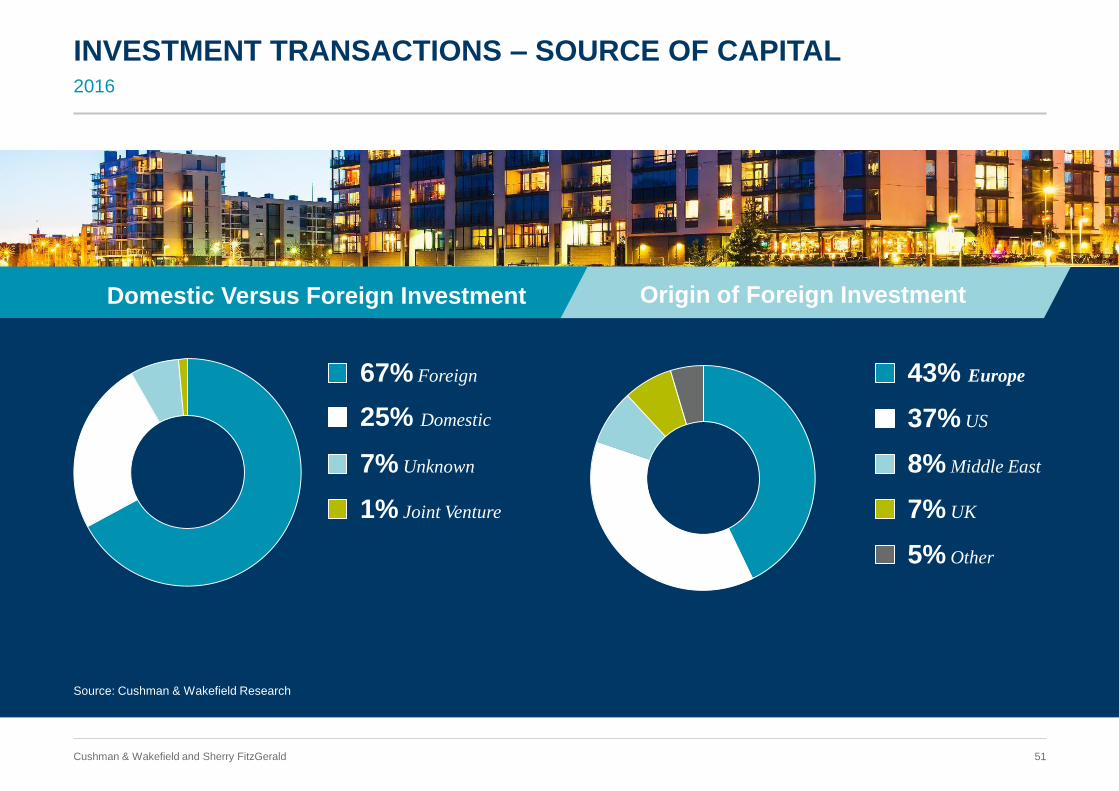

2016

INVESTMENT TRANSACTIONS – SOURCE OF CAPITAL

Source: Cushman & Wakefield Research

43% Europe

37% US

8% Middle East

7% UK

5% Other

67% Foreign

25% Domestic

7% Unknown

1% Joint Venture

Origin of Foreign Investment Domestic Versus Foreign Investment

Irish Office Market

53 Cushman & Wakefield and Sherry FitzGerald

Irish Office Market Q4 2016

Source: Cushman & Wakefield Research

Market Stock: 304,000 sq m

Take Up 2016: 5,750 sq m

Availability: 24,400 sq m

Vacancy Rate: 8.0%

Under Construction: 0 sq m

Completions 2016: 2,250 sq m

Market Stock: 337,600 sq m

Take Up 2016: 10.450 sq m

Availability: 66,150 sq m

Vacancy Rate: 17.6%

Under Construction: 28,450 sq m

Completions 2016: 7,850 sq m

Market Stock: 3.37 million sq m

Take Up 2016: 261,700 sq m

Availability: 412,150 sq m

Vacancy Rate: 12.2%

Under Construction: 373,300 sq m

Completions 2016: 31,100 sq m

Market Stock: 564,850 sq m

Take Up 2016: 21,500 sq m

Availability: 65,000 sq m

Vacancy Rate: 11.5%

Under Construction: 5,000 sq m

Completions 2016: 15,850 sq m

1 Grade A Building > 5,000 sq m

GALWAY

LIMERICK

CORK

DUBLIN

54 Cushman & Wakefield and Sherry FitzGerald

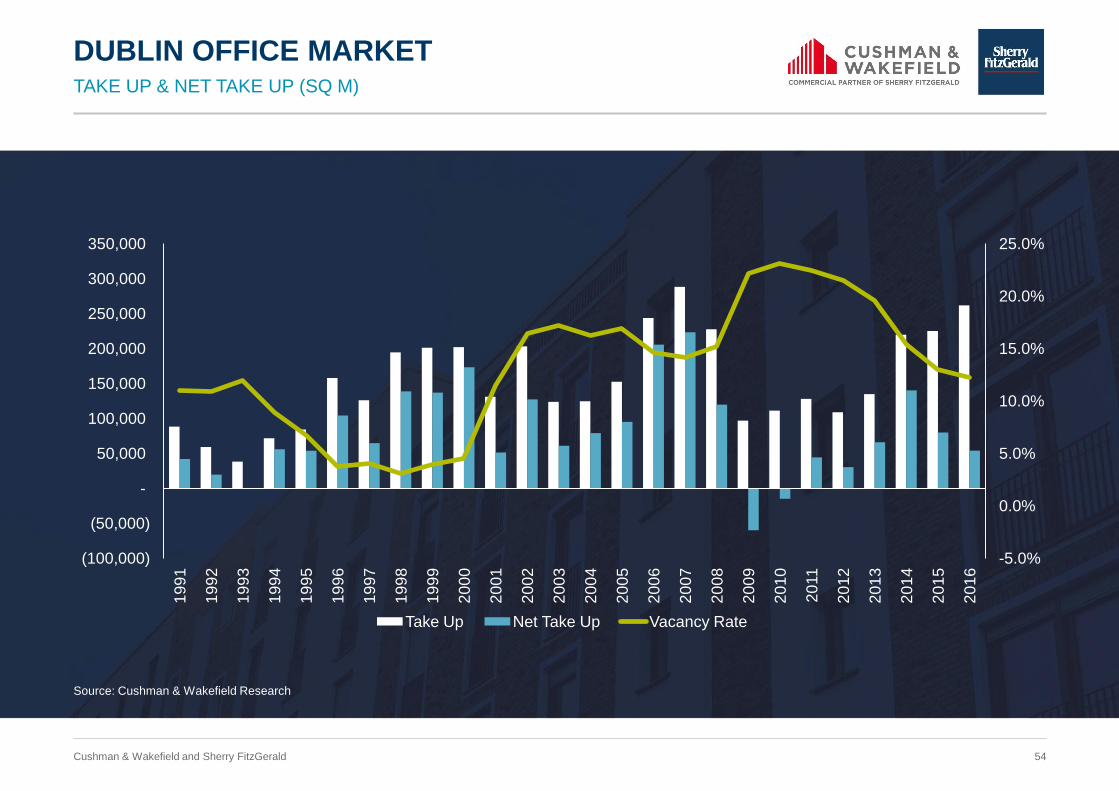

DUBLIN OFFICE MARKET TAKE UP & NET TAKE UP (SQ M)

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

(100,000)

(50,000)

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Take Up Net Take Up Vacancy Rate

Source: Cushman & Wakefield Research

55 Cushman & Wakefield and Sherry FitzGerald

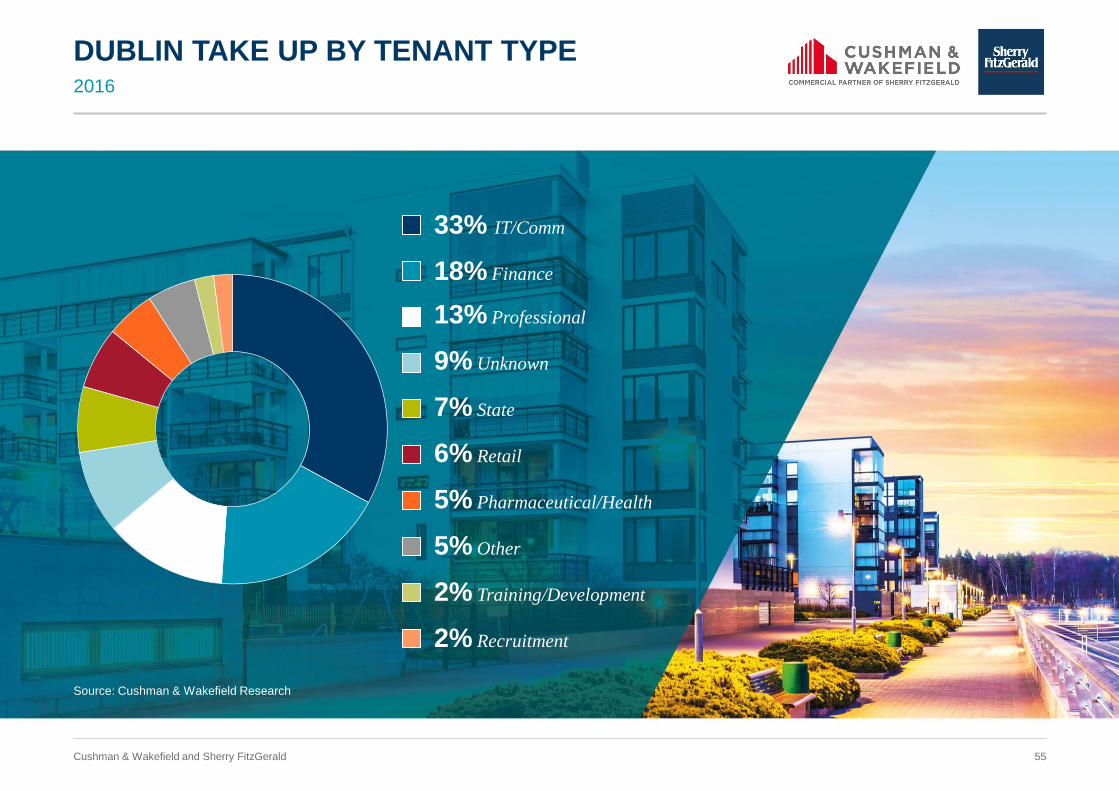

DUBLIN TAKE UP BY TENANT TYPE 2016

Source: Cushman & Wakefield Research

33% IT/Comm

18% Finance

13% Professional

9% Unknown

7% State

6% Retail

5% Pharmaceutical/Health

5% Other

2% Training/Development

2% Recruitment

56 Cushman & Wakefield and Sherry FitzGerald

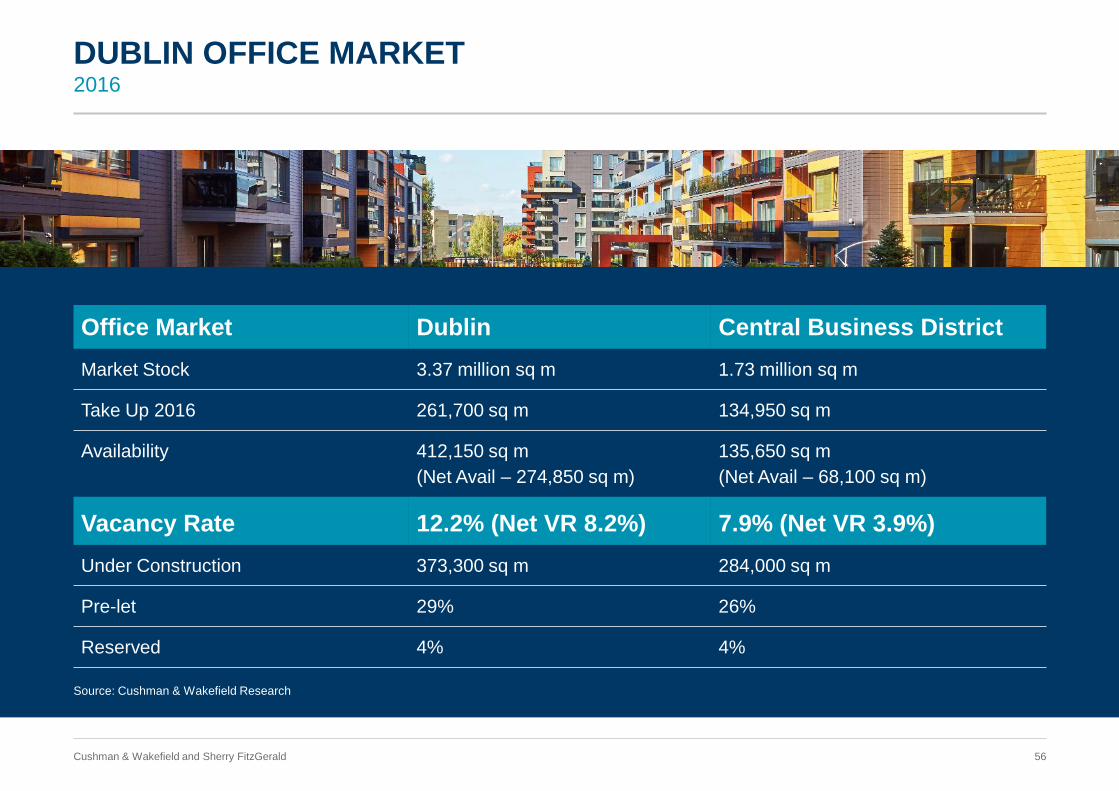

DUBLIN OFFICE MARKET 2016

Office Market Dublin Central Business District

Market Stock 3.37 million sq m 1.73 million sq m

Take Up 2016 261,700 sq m 134,950 sq m

Availability 412,150 sq m

(Net Avail – 274,850 sq m)

135,650 sq m

(Net Avail – 68,100 sq m)

Vacancy Rate 12.2% (Net VR 8.2%) 7.9% (Net VR 3.9%)

Under Construction 373,300 sq m 284,000 sq m

Pre-let 29% 26%

Reserved 4% 4%

Source: Cushman & Wakefield Research

57 Cushman & Wakefield and Sherry FitzGerald

58 Cushman & Wakefield and Sherry FitzGerald

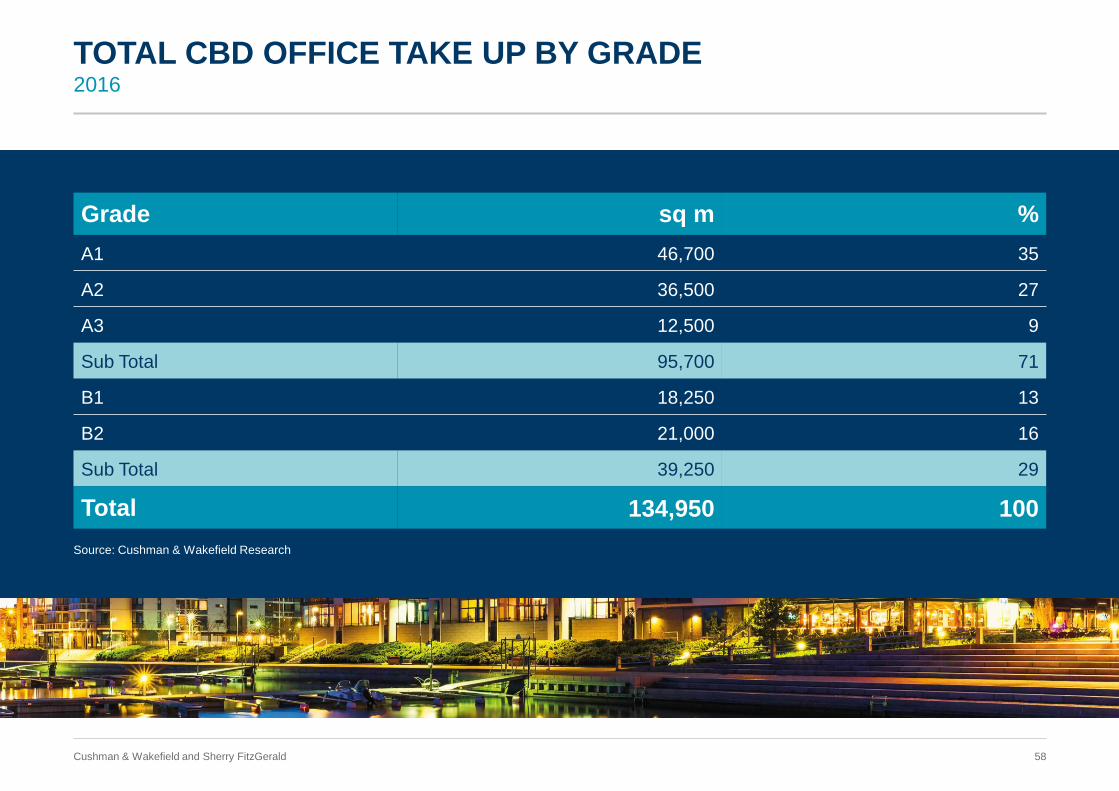

TOTAL CBD OFFICE TAKE UP BY GRADE 2016

Source: Cushman & Wakefield Research

Grade sq m %

A1 46,700 35

A2 36,500 27

A3 12,500 9

Sub Total 95,700 71

B1 18,250 13

B2 21,000 16

Sub Total 39,250 29

Total 134,950 100

59 Cushman & Wakefield and Sherry FitzGerald

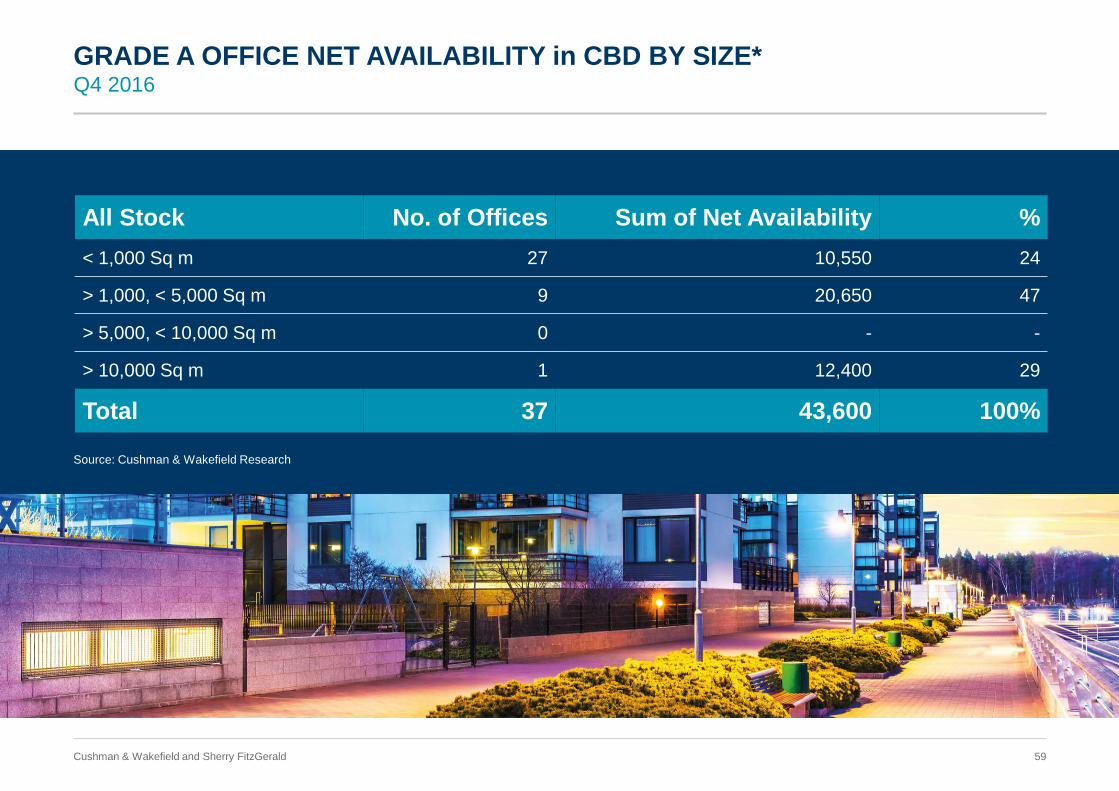

GRADE A OFFICE NET AVAILABILITY in CBD BY SIZE* Q4 2016

All Stock No. of Offices Sum of Net Availability %

< 1,000 Sq m 27 10,550 24

> 1,000, < 5,000 Sq m 9 20,650 47

> 5,000, < 10,000 Sq m 0 - -

> 10,000 Sq m 1 12,400 29

Total 37 43,600 100%

Source: Cushman & Wakefield Research

60 Cushman & Wakefield and Sherry FitzGerald

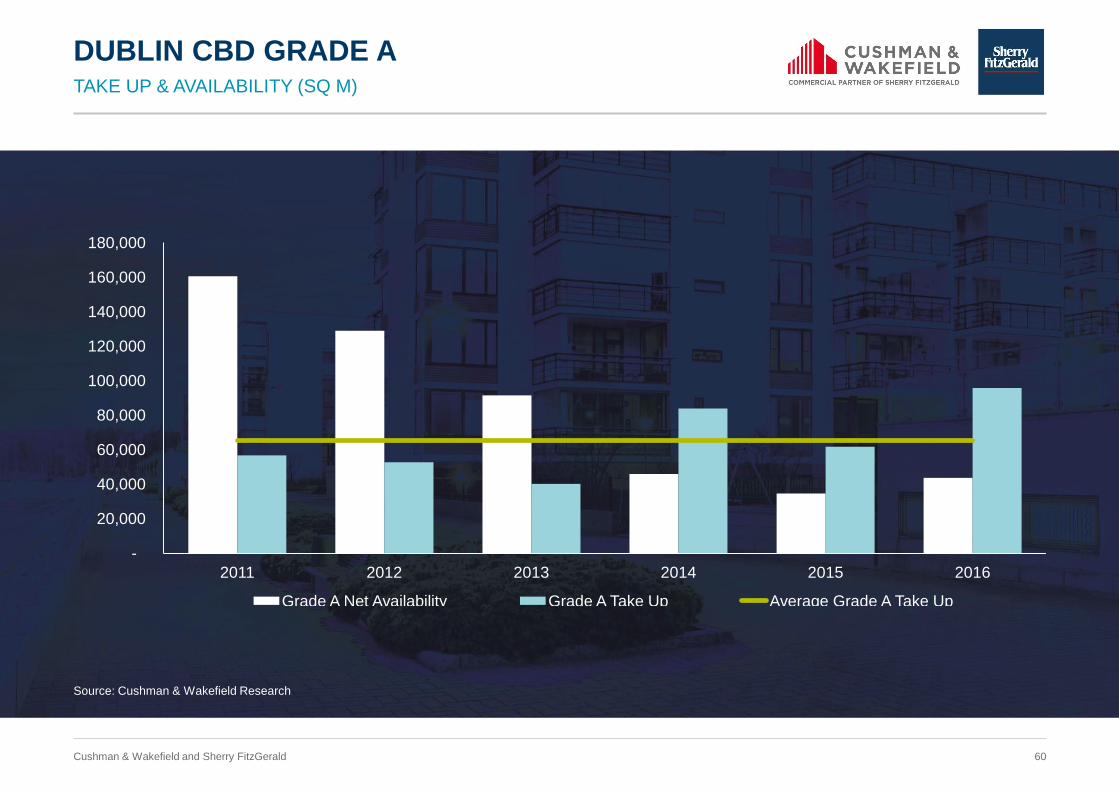

DUBLIN CBD GRADE A TAKE UP & AVAILABILITY (SQ M)

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2011 2012 2013 2014 2015 2016

Grade A Net Availability Grade A Take Up Average Grade A Take Up

Source: Cushman & Wakefield Research

61 Cushman & Wakefield and Sherry FitzGerald

DUBLIN OFFICE DEVELOPMENT 1990 – 2019

0

50,000

100,000

150,000

200,000

250,000

300,000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

f

20

18

f

20

19

f

Completions Under Construction - Let Under Construction - Available LR Average Take Up

Source: Cushman & Wakefield Research

62 Cushman & Wakefield and Sherry FitzGerald

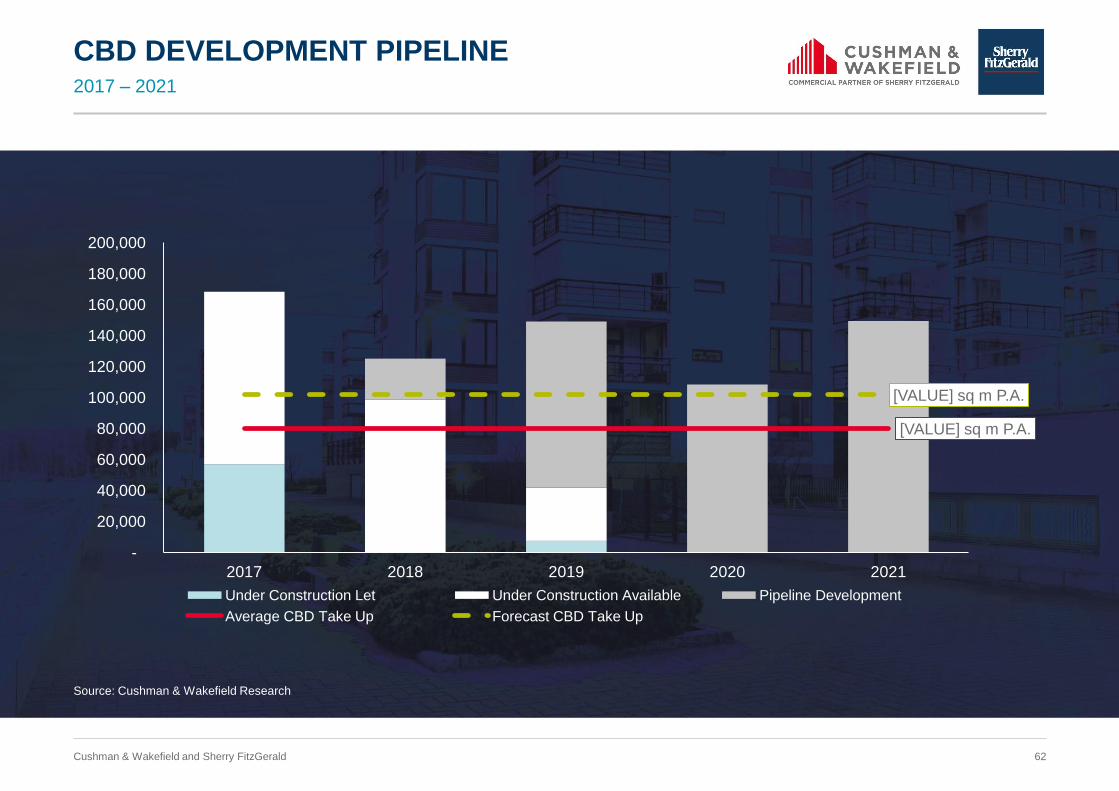

CBD DEVELOPMENT PIPELINE 2017 – 2021

[VALUE] sq m P.A.

[VALUE] sq m P.A.

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2017 2018 2019 2020 2021

Under Construction Let Under Construction Available Pipeline Development

Average CBD Take Up Forecast CBD Take Up

Source: Cushman & Wakefield Research

63 Cushman & Wakefield and Sherry FitzGerald

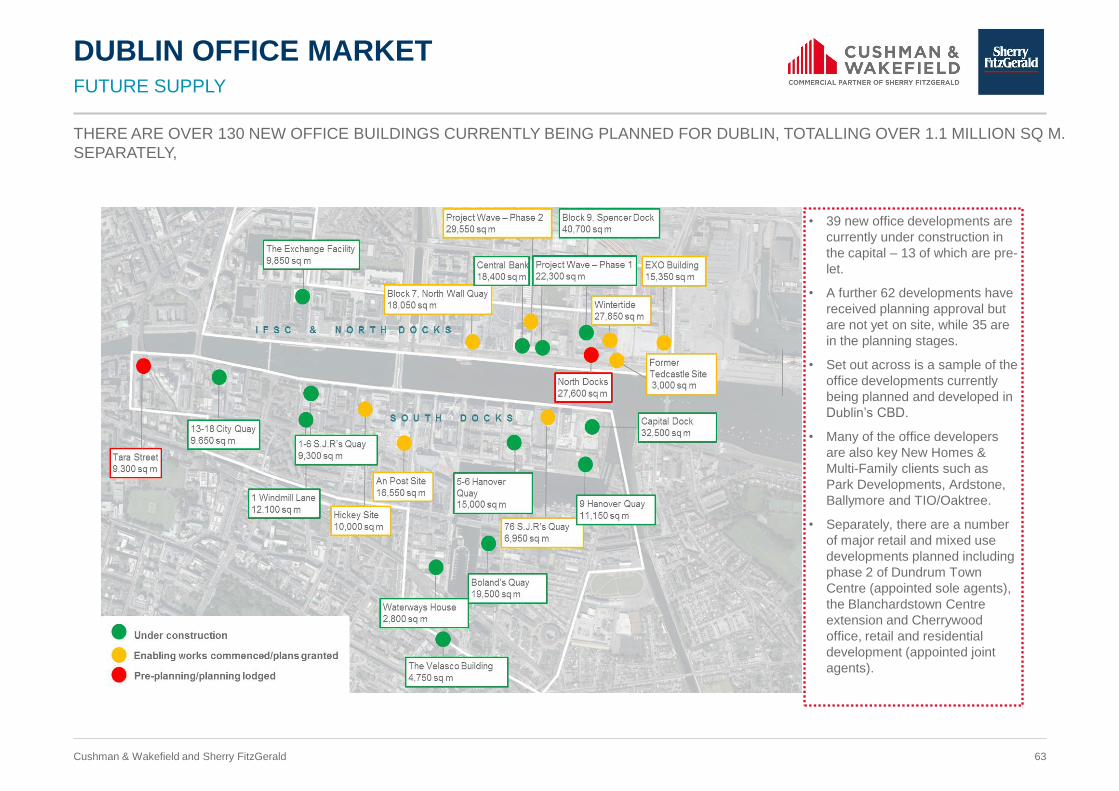

FUTURE SUPPLY

DUBLIN OFFICE MARKET

• 39 new office developments are

currently under construction in

the capital – 13 of which are pre-

let.

• A further 62 developments have

received planning approval but

are not yet on site, while 35 are

in the planning stages.

• Set out across is a sample of the

office developments currently

being planned and developed in

Dublin’s CBD.

• Many of the office developers

are also key New Homes &

Multi-Family clients such as

Park Developments, Ardstone,

Ballymore and TIO/Oaktree.

• Separately, there are a number

of major retail and mixed use

developments planned including

phase 2 of Dundrum Town

Centre (appointed sole agents),

the Blanchardstown Centre

extension and Cherrywood

office, retail and residential

development (appointed joint

agents).

THERE ARE OVER 130 NEW OFFICE BUILDINGS CURRENTLY BEING PLANNED FOR DUBLIN, TOTALLING OVER 1.1 MILLION SQ M.

SEPARATELY,

64 Cushman & Wakefield and Sherry FitzGerald

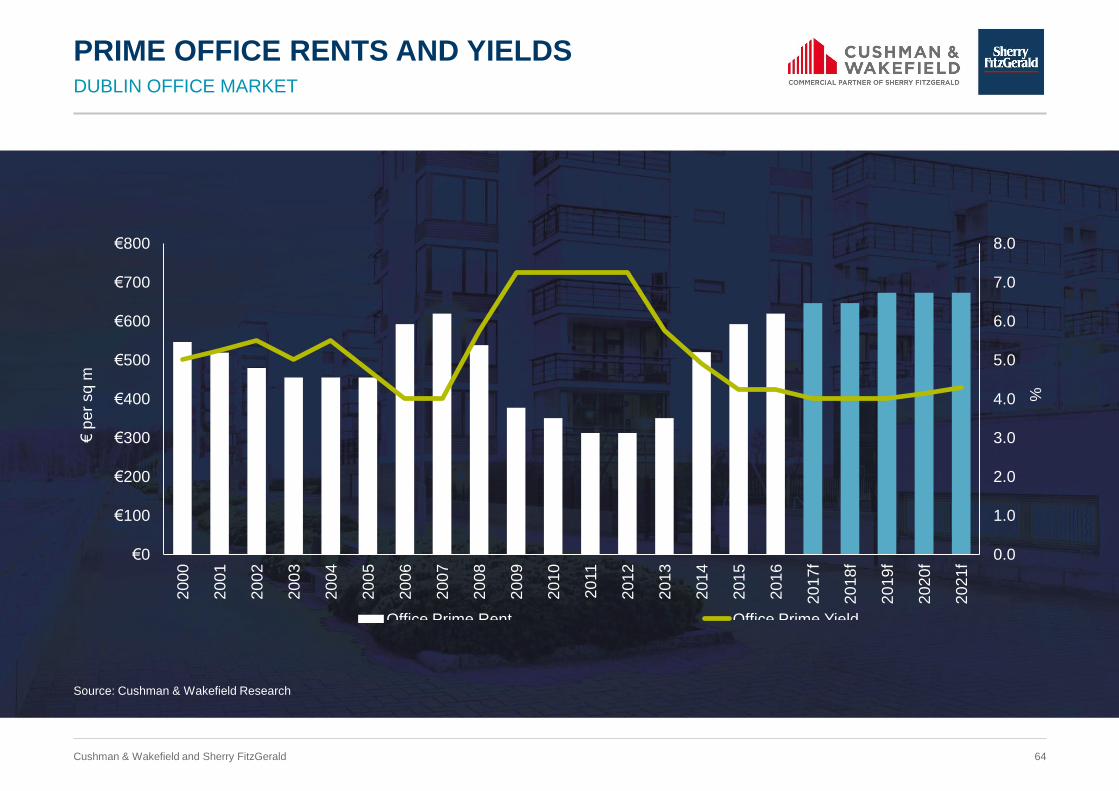

PRIME OFFICE RENTS AND YIELDS DUBLIN OFFICE MARKET

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

€0

€100

€200

€300

€400

€500

€600

€700

€800

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

f

20

18

f

20

19

f

20

20

f

20

21

f

%

€ p

er

sq m

Office Prime Rent Office Prime Yield

Source: Cushman & Wakefield Research

65 Cushman & Wakefield and Sherry FitzGerald

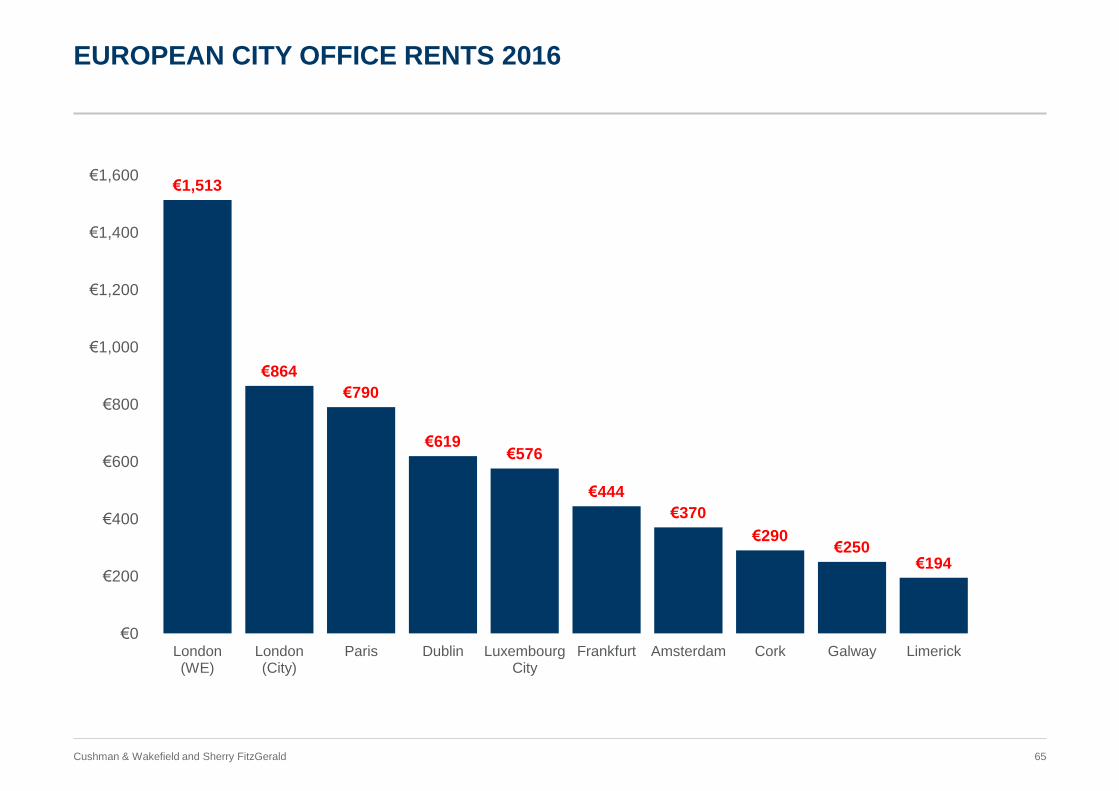

EUROPEAN CITY OFFICE RENTS 2016

€1,513

€864

€790

€619 €576

€444

€370

€290 €250

€194

€0

€200

€400

€600

€800

€1,000

€1,200

€1,400

€1,600

London (WE)

London (City)

Paris Dublin Luxembourg City

Frankfurt Amsterdam Cork Galway Limerick

MARIAN FINNEGAN

Chief Economist

Marian Finnegan

JONATHAN HILLYER

Director, Investments

THANK YOU….ANY QUESTIONS?

67 Cushman & Wakefield and Sherry FitzGerald

67

CAVEATS

This report should not be relied upon as a basis for entering transactions without seeking specific, qualified, professional

advice. It is intended as a general guide only. This report has been prepared on the basis of publicly available information,

internally developed data and other sources believed to be reliable. While reasonable care has been taken in the

preparation of the report, neither Cushman & Wakefield / Sherry FitzGerald nor any of directors, employees or affiliates

guarantees the accuracy or completeness of the information contained in the report. Any opinion expressed (including

estimates and forecasts) may be subject to change without notice. No warranty or representation, express or implied, is or

will be provided by Cushman & Wakefield / Sherry FitzGerald, its directors, employees or affiliates, all of whom expressly

disclaim any and all liability for the contents of, or omissions from, this document, the information or opinions on which it is

based. Information contained in this report should not, in whole or part, be published, reproduced or referred to without

prior approval. Any such reproduction should be credited to Cushman & Wakefield / Sherry FitzGerald.

Thank you for attending www.harvestfinancial.ie