Economic rollers

Market updates

August 6, 2012

Issue 28

Volume III

Nishka A FINANCIAL NEWS LETTER FROM CUIM KENGERI

RBI column

Metal and Mining Sector Review

Finance buzz

Finance quiz

RBI COLUMN 01

ECONOMIC ROLLERS 03

CARTELIZATION OF CEMENT AND ITS LONG

TERM IMPACT

04

INDIA’S LOVE FOR GOLD HARMS GROWTH 06

INDIAN METALS AND MINING SECTOR: THE

HIDDEN POTENTIAL

08

FINANCE BUZZ 10

STOCK ANALYSIS-I

STOCK ANALYSIS-II

MARKET ROUND UP

11

12

13

CAMPUS POLL 14

PHOTO FIND 15

CROSSWORD 16

FINANCE QUIZ

ANSWERS

17

18

Ritesh

Kejriw

al, 2

MBA

F1

1

Metal and Mining industries are an indispensable part of an economy; they form the backbone of industrial development of any country. The metal industry consists of two major groups; Ferrous metals and Non-‐Ferrous metals. India's metal and mining industry grew to US$ 120.4 billion in 2011, an increase of 27 per cent from 2010. Iron and steel is the largest segment of the Indian metals and mining industry, accounting for 74 per cent of the overall industry value followed by coal segment accounting 20.8 per cent.

A growing sector:

Our main focus in this issue will be Ferrous metal which consist of different types of steels and Iron.

2

India has become 4th largest producer of crude steel in the world as against the 8th position in 2003 and is expected to become the 2nd largest producer of crude steel in the world by 2015. The steel sector contributes to nearly 2% of the GDP.

The major producers Steel Authority of India Limited, Rashtriya Ispat Nigam Limited, Tata Steel, Essar, JSW Steel, JSW Ispat Steel and Jindal Steel together produced 29.984 MT during 2011, which was a growth of 8.07% compared to last year.

The current market cap of Indian Metal and Mining sector is around $105 billion and major share held by Coal India, Tata Steel, SAIL, Sterlite, Jindal Steel, NMDC etc. BSE metal index gave

3

positive return of more than 21% in Q4FY2012, Steel stocks gained during 4QFY2012 mainly on account of improved demand in the domestic market, increased steel prices. JSW Steel gained 42.2% in 4QFY2012 on the hope of lifting of mining ban in Karnataka, fall in iron ore prices and improvement in utilization levels at its Karnataka plant. SAIL and Tata Steel stocks gained 15.6% and 40.7%, respectively. On the non-‐ferrous side, stock prices of Sterlite, Hindalco, Nalco and Hindustan Zinc increased by 23.8%, 11.7%, 7.0% and 10.6% respectively.

METAL AND MINING SECTOR REVIEW

(Continued)

1

Q1FY2013 will be tough for steel companies of because increase in excise duty that would be marginally negative for metal producers and lower industrial demand. The results of big companies are yet to come and small player already posted a negative growth

Untapped India:

India has turned into a net importer of steel due to strong growth in the manufacturing sector and rise in infrastructure projects. 100 per cent

2

foreign direct investment (FDI) is allowed in the mining sector under the automatic route. The FDI inflow worth US$ 5.4 billion was registered into the metals and mining industry during April 2000 to April 2011. Metals and mining industry accounted for 4 per cent of the total cumulative FDI in the same period. In 2010, mergers and acquisitions (M&A) deal value in the mining sector stood at US$ 2.0 billion, accounting for 24.9 per cent of the total M&A deal value. There is significant scope for new mining capacities in iron ore, bauxite,

3

and coal. Untapped metal reserves in India are to the tune of 82 billion tonnes. Strong long-‐term demand from the steel industry is expected to further boost the iron ore industry. Booming construction, automobiles, and packaging industries are expected to lend substantial support to the metals and mining industries.

World’s Top 10 Steel producers:

Source:

World Steel Association

www.ibef.org, www.moneycontrol.com/earnings/,www.steel.nic.in/overview.htm, Ernst & Young’s Reports.

Rank 2001 2010 1 ArcelorMittal ArcelorMittal 2 POSCO Baosteel 3 Nippon Steel POSCO 4 Ispat International Nippon Steel 5 Shangai Baosteel JFE 6 Corus Jiangsu Shagang 7 ThyssenKrupp Tata Steel 8 Riva US Steel 9 NKK Ansteel

10 Kawasaki Gerdau

1

Reflections on the growth of MSMEs in India

Key notes:

The Economic survey 2011-‐12 has stated, “MSME is a dynamic and vibrant sector that nurtures entrepreneurial talent besides meeting social objectives including that of providing employment to millions of people across the country”. In terms of output, MSMEs produce more than 6000 products ranging from machinery and equipment, to apparels to food products to furniture and account for 45% of the manufacturing output and 40% of the total exports of the country. About 45.2% of the enterprises are located in rural areas, thus offering a great potential for

2

rural development and for reducing the strain on urban infrastructure. The fourth census of MSME sector revealed that only 5.18% of the units had availed of finance through institutional sources while 2.05% had finance from non-‐institutional sources, the majority of funds i.e. 92.77%, had no finance or depended on self finance.

Policy Initiatives:

1. With an objective of ensuring provision of banking services in all parts of the country, banks were advised to draw up a roadmap to provide banking services through a banking outlet in every unbanked village having a population of over 2,000 by March 2012.

2. The limit for collateral free loans to

3

the MSMEs has been increased from the level of Rs. 5 lakh to Rs. 10 lakh and has been made mandatory for banks. The implementation should result in enhanced usage of the Guarantee scheme and facilitate increase in quality and quantity of credit to MSEs, leading, eventually to sustainable and inclusive growth.

3. Timely detection of sickness is critical for any enterprise as any delay in this regard impinges on the revival prospects of sick, but potentially viable units.

4. All Scheduled Commercial Banks have also been advised to review and put in place MSE loan policy, restructuring/rehabilitation

Nidhi Ja

iswal, 2

MBA

F1

RBI COLUMN

1

(Continued)

1

policy and Non-‐Discretionary One Time Settlement scheme for recovery of non-‐performing loans, duly approved by their Board of directors.

5. Products such as equipment lease finance can address the need for term finance, whereas products such as receivables financing, bills discounting, reverse factoring etc. could provide working capital finance.

6. Technology is a game changer. It has the potential to cut down operating costs, enhance efficiency and also open up new markets and opportunities for MSMEs. SMEs will have to continuously strive to

2

incorporate the latest technology into their production processes as well as in their marketing and management functions, to cut costs, gain efficiency and consistency.

7. The MSMEs need to understand with appropriate support from the capacity building institutions in the form of seminars and workshops, the importance of corporate governance and its linkages with risk management.

8. At the international level, MSMEs may have to face global competition, but the opportunities for growth are immense only if MSMEs are focused on quality and use appropriate technologies.

9. The Chambers of Commerce and

3

MSME associations create greater awareness among their MSME members about credit facilities from banks, NBFCs and financial institutions, benefits of credit rating, alternate finance options such as venture capital, factoring, bills discounting, recently launched SME exchange /platform etc. in addition to engaging with policymakers and organizing training/capacity building programmes.

10. Human resource development issues are fundamental in improving SME competitiveness.The Government of India and various State governments have been implementing a number of schemes and programs over the years for skill development

2

Source: www.rbi.org.in

Address by Shri Anand Sinha, Deputy Governor of the RBI, at the National Conference on Enhancing Competitiveness with MSME linkages, organised by

the Indian Chamber of Commerce, Kolkata, July 12, 2012

ECONOMIC ROLLERS

-‐ Dhawal Parmar, 2 MBA F1

• Repo Rate: 8.00%

• Reverse Repo Rate: 7.00%

• CRR: 4.75%

• SLR: 23.0%

• CBLO: 7.92% (as on August 1st 2012)

• MIBOR (1 month as of August 1st 2012): 8.89%

• Inflation (Based on All India Consumer Price Index as On July 16th 2012): 10.02%

• Forex Reserves (as of July 20th 2012): $ 287.34 billion

• IIP (Released On July 12th 2012, for May): 2.4%

• 91 Days T bills (As on August 1st 2012): 8.227%

• 10 year G-‐ Sec Yield (As on August 1st 2012): 8.22%

• Exports during June 2012: $ 25.00 billion

• Imports during June 2012: $ 35.37 billion

Source: Reserve Bank Of India, Ministry Of Finance, Office of Economic Advisory, Ministry of Commerce, Central

statistics Office, The Clearing Corporation Of India Ltd., FIMMDA.

3

1

The recent imposition of a heavy fine of Rs. 6300 crores on 11 cement companies by Competition Commission of India has raised eyebrows. There have been mixed reactions regarding the implications of fixing the prices through the cartel.

A stringent watchdog:

It is however said that the Competition Commission of India, a watchdog for the competition has probed as many as 39 companies in order to come to the conclusion of finding them guilty of cartelisation.

Those guilty are supposed to pay as much as 8% of their average turnover in the last 3 years. This fine also amounts to 50% of these

2

companies’ profits for FY 09-‐10 and FY 10-‐11. Cartels are groups of companies who syndicate in order to regulate the prices and supplies in order to maintain controlled capacity utilisation, controlled production and huge profits. Apart from this, cartelisation may also involve distribution of market shares, allocation of sales territories, controlled supplies etc. to gain above average profits. Under CPACA, such activities are strictly prohibited. Normally, they are verbal in nature and very difficult to track.

The adverse effect:

The most adverse impact of this decision could be on the real estate sector. Since this decision is expected to affect the FY13E profits of the major cement players like Ultratech Cement,

3

ACC, Century Textiles and Industries Ltd, Ambuja, Jaypee Cements etc. to name a few, the prices of cement are expected to go up, which in turn would impact the land and property rates in the long run. CREDAI has sought help from GOI in this regard to regulate the cement prices in order to avert any situations of crisis pertaining to shortage in supply or increase in prices. This can also be because of the fact that the cement companies were found way below their capacity utilisation, upto 70%. One reason why industry might stay brazen despite deterrent fines is that cartels are very hard to detect and require a high standard of proof given that the possible punitive liability can be

Akh

ilesh

C, 2

MBA

F1

CARTELIZATION OF CEMENT AND ITS

LONG TERM IMPACT

4

(Continued)

1

prohibitively high.

Because it is clearly illegal -‐ and, in some jurisdictions, a criminal act -‐ it is also conducted in great secrecy. This is why all modern competition laws provide for leniency programmes that offer immunity to cartel members to come forward and

2

confess the details of the cartel.

The programmes that have been the most successful give complete amnesty to the first conspirator to come forward and reveal the inner workings of the cartel to competition law enforcers, and experience shows these programmes work. Under our

3

Competition Act too, there is a leniency programme provision to encourage cooperation. Though the fines are already imposed, it would be interesting to watch how the cement companies and courts react to the same and whether or not, the smaller companies benefit from this imposition.

Fingers crossed!!

5

1

“Gold has been a part and parcel of India's culture and tradition.”

As money, jewellery, status symbol and investment, gold has played a crucial role in the lives of Indians for centuries. The question arises here is that is this craze for yellow metal that is deemed to be increasing the investors’ wealth, hampering the Indian Economy? The answer is a definite yes!

According to Global consultant McKinsey & Company, India is the world’s single largest gold bullion consumer with 18000 tonnes of above ground stocks worth a little over Rs 40 lakh crores-‐ almost double the gold maintained by the US Federal Reserve-‐ sitting idle in

2

family vaults as ornaments, coins and bars. Figures show that in the first three months of 2012, gold purchase in India jumped nearly 35 percent. As an investment, gold has been an easier bet to hedge against inflation and other risks. Indians have been buying and trading in gold since time immemorial, and continue to buy it even now when it is more expensive than ever.

This continued fetish for gold is denting the country’s economy in two aspects:

Burden on the existing current account deficit:

Massive gold imports have rung alarm bells with Indian economists, investment bankers and analysts stating that India's fascination with gold could be a reason why growth appears to be flagging. The gold import bill is expected to touch $100 billion by 2015-‐16, putting pressure on the existing current account deficit, industry body ASSOCHAM (Associated Chambers of Commerce and Industry) has said. "Calculated on the basis of CAGR of period 2010-‐11 over 1999-‐2000, the gold import bill could total $100 billion soon. At these levels, gold imports are a huge burden on the balance of payments and accentuates the current account deficit," said ASSOCHAM secretary general D S Rawat.

Apu

rva Pa

thak

, 2 M

BA F1

INDIA’S LOVE FOR GOLD HARMS

GROWTH

6

(Continued)

1

Hinders investment in other financial instruments:

Another important point to be noted here is that India’s fascination for gold comes in the way of investment in other productive assets. The amount of GDP value lost by parking Rs 40 lakh crores worth of savings in gold is very huge and has impacted the investments in property, shares and mutual funds. Experts say that if Indians had invested in other instruments such as equity and mutual funds, the country’s annual GDP would have been higher by 0.4 percent. The government would prefer savings to be invested in more

2

productive assets such as equity and mutual funds that would help boost the growth rate.

However the repeated warnings of the Government to contain the excessive demand for gold has been taken seriously the result of which shows as fall in India’s trade deficit to 15 month low of Rs 10.3 billion dollars due to sharp fall in imports. Thomson Reuters poll shows that India's gold imports fell by more than a half in the June quarter and could slide by a third in the next three months as prices inflated by a weak rupee and a 4% import duty.

Now to curb the situation excessive

3

investment in gold, the government should undertake extensive financial education campaigns and encourage channelizing savings in other financial instruments. Also measures must be taken to educate Indians who are apprehensive about investing in the stock market and continue to invest their money in gold.

This can be seen as a welcome step in the age of rising middle class who can better mobilize their savings in the unexplored options.

References:

www.moneycontrol.com

www.commodityonline.com

7

1

According to a recent report published by EXIM bank of India, India as a nation holds abundant reserves of minerals such as non-‐coking coal, bauxite, dolomite, gypsum, limestone and mica; adequate levels of reserves of minerals such as lignite, metallic chromite, manganese, zinc and graphite.

The fastest maturing industries in India:

The Metals & Mining industry are one of the highest contributing sector in terms to the economy of the country and it encompasses the extraction (mining) as well as the primary and secondary processing of metals and minerals such as aluminium, gold, precious metals, coal and steel. The industry is oligarchic in structure, with a few

2

producers accounting for the lion’s share of the output. It is also one of the fastest maturing industries in India, consisting aluminium, iron and steel, precious metals and minerals, coal and base metal markets as the major contributors. For instance, the Indian metals & mining industry had total revenues of $106.4 billion in 2010, representing a compound annual growth rate (CAGR) of 15.5% for the period spanning 2006-‐2010. Industrial production volumes have increased with a CAGR of 5.7% between 2006-‐2010, to reach a total of 684.4 million metric tons in 2010.

As far as the consumption is concerned, in this financial year, India’s steel consumption has grew to about 8.1% YoY(Year over Year) during April-‐May 2012 as growth was less than 2% last year. Weak IIP performance and

3

slowdown in GDP growth is not helping in reviving weak domestic steel demand. Q1FY13 is expected to be a lack-‐lustre-‐quarter for the metals and mining industry due to expected lower volume on QoQ(Quarter over Quarter) basis and lower realizations due to sharp fall in metals prices. Exchange rate also had a key role to play.

The rupee impact:

Steel prices for the quarter remained steady however there could be pressure in the near term due to surge in imports. EBITDA margins are expected to improve. However, due to depreciation of Indian rupee, impact on profitability could be negative for companies having foreign currency loans leading to high MTM charges.

Ank

ur Gos

wam

i, 2 MBA

F1

INDIAN METALS AND MINING

SECTOR: THE HIDDEN POTENTIAL

8

(Continued)

1

Going ahead, steel prices are expected to remain subdued whereas margins will come under pressure due to rupee depreciation and high coking coal prices. Global steel spot prices have declined by more than 10% over last two months but Indian steel mills were largely cushioned due to sharp Rs depreciation. The automotive and construction markets have historically been the largest consumers of steel. The automotive sector has shown significant promise. In February 2012, total motor vehicle sales reached their highest level since February 2008 at 15.1 million SAAR (Seasonally Adjusted Annual Rate). For the first five months of 2012, sales have averaged 14.4 million SAAR. Many auto manufacturers made their best Memorial Day sales in over five years. Motor vehicle sales were at 13.8 million in May, declining from 14.4 million in April. Even though sales slid to the lowest level so far in 2012, it is still better than consensus expectations from the beginning of

2

the year. On a year-‐over-‐year basis, sales increased 26% inMay.

Hurdles along the way:

One of the major hurdles in investment in metals and mining sector are the delays in approval due to bureaucracy, discretionary interpretation and need to get approval of numerous agencies at state and central government level. Also, infrastructure impediments like high railway freight, inadequate availability of rail wagons and inadequate power evacuation infrastructure also create problems.

According to an estimate, India has 85 billion tonnes of mineral reserves which are still to be exploited. There is an estimated 13000 deposits of non-‐fuel mineral types in India. Also, India welcomes joint ventures between foreign and domestic partners to mobilise finances and technologies and hence secure its access to global markets.

The main opportunities in the mining sector lie in the development and

3

production of surplus commodities such as iron ore, bauxite, mica, potash, gold deposits, located in belts of Himalayas, using better mining technologies, eliminating mafias and smuggling of these precious reserves and to remove the FDI limit in order to use this sector as a growth and stability sector for a few years to come.

9

Man

isha

B, 2

MBA

F1

FINANCE BUZZ

BULLION

This denotes gold and silver that is refined and officially recognized as high quality (at least 99.5%pure). It is usually in the form of bars rather than coins.

LONDON METAL EXCHANGE:

LME is one of the main metal markets in the world and allows for the hedging of metals risk through highly liquid and standardized exchange-‐traded future contracts.

GLENCORE-‐XSTRATA MERGER

On a standalone basis, Xstrata is a strong business with a bright future and Glencore as a 34% shareholder. The $65 billion mega-‐merger between commodities giant Glencore and miner Xstrata is close to collapse after Qatar’s sovereign wealth fund said it was unhappy with the deal.

SCRAP RECOVERY

Scrap recovery refers to the worldwide supply of gold from sources other than mine production. This includes recovered old jewellery, industrial by products etc.

BARRICK GOLD CORPORATION

It is engaged in the production and sale of gold, as well as related activities. Barrick also hold interests in oil and gas properties located in Canada.

10

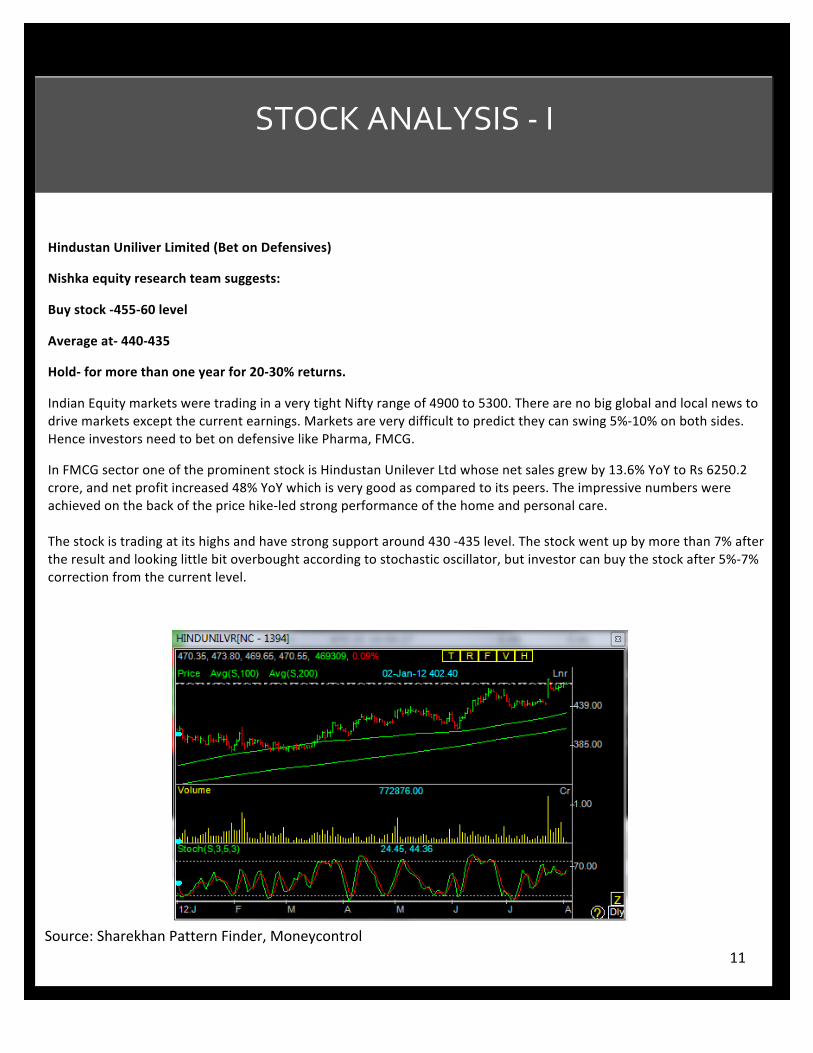

STOCK ANALYSIS -‐ I

Hindustan Uniliver Limited (Bet on Defensives)

Nishka equity research team suggests:

Buy stock -‐455-‐60 level

Average at-‐ 440-‐435

Hold-‐ for more than one year for 20-‐30% returns.

Indian Equity markets were trading in a very tight Nifty range of 4900 to 5300. There are no big global and local news to drive markets except the current earnings. Markets are very difficult to predict they can swing 5%-‐10% on both sides. Hence investors need to bet on defensive like Pharma, FMCG.

In FMCG sector one of the prominent stock is Hindustan Unilever Ltd whose net sales grew by 13.6% YoY to Rs 6250.2 crore, and net profit increased 48% YoY which is very good as compared to its peers. The impressive numbers were achieved on the back of the price hike-‐led strong performance of the home and personal care. The stock is trading at its highs and have strong support around 430 -‐435 level. The stock went up by more than 7% after the result and looking little bit overbought according to stochastic oscillator, but investor can buy the stock after 5%-‐7% correction from the current level.

Source: Sharekhan Pattern Finder, Moneycontrol 11

STOCK ANALYSIS -‐ II

BATA INDIA

Buy at: 910

Sell target: 980

Stop loss: 880

Nishka equity research team

recommends a buy on Bata India at

current levels. The company has been

a continuous outperformer in the last

1 year giving a good return to the

investors unlikely the index which is

continuing its bad run from last 1

year. Revenues of the company have

grown at around 20% YOY to 506 cr

and bottomline also grows with the same percentage.

Company has been in the expansion mode and expects a capital expenditure of Rs 100 cr in Fy 2013 in opening 150 new

stores. The stock has been recommended by various analysts. The stock is trading at its years high and is expected to

continue its trend.

The company trades at a very high PE of 36. Regarding the technical’s the short term moving average of the company is

higher than its long term moving averages and the relative sensitivity Index is also stable which gives a bullish signal.

12

MARKET ROUND UP

-‐ Abhishek Jain, 2 MBA F1

The Indian equity markets this month were stuck in a very tight range where Sensex was fluctuating between 17631 and

16598 and Nifty between 5348 and 5042, The reason for this trading in tight range is due to continuous news flows,

both positive and negative in nature. There has been some stability in Europe in last 1 month where the unemployment

rate in nearly all the European economies has declined and also there has been positive data flow from the American

economy. On the other hand there has been a lot disturbing news flows in domestic Indian economy where the inflation

number is continuously disappointing and also there was a bit of political instability when the presidential elections

were due.

The most disappointing factor was the delay of monsoon in India on which the India economy is heavily dependent. The

technical’s of the market has been good and fundamentally also the markets look like breaking this trading range. The

only thing it is waiting for is some trigger, which may be revival of monsoon.

In brief we can conclude that though there is positive news flows from global economy, but our interior problems are

restraining the equity markets. The future performance of Indian equity markets is now hugely dependent on the

monsoon conditions.

13

Best comment

1. The comment is more of a motivation to India rather than expecting another wave of economic reforms from India to make India more competitive in the global economy.

As compared to other BRICS nation, India is lagging far behind in the growth & the future expectation shows there will not be more than 6% of growth for the coming 2-‐3 years. India has been warned already to improve it's economy otherwise we may lose our participation from great BRICS group.

Obama's comment may be a strategy to motivate India to do better as far as global business is concerned.

-‐ Mayank Kumar Gupta -‐1221416

CAMPUS POLL

- Abhisek Roy, 2 MBA F1

- Arun P, 2 MBA F2

The time may be right for another wave of economic reforms to make India more competitive in the global economy." -‐ Barack Obama. Do you agree?

Total respondents: 72

Yes – 59

No – 8

Cant Say – 5

Yes No Cant Say

2. The time right now is not for more economic reforms but to implement whatever changes have been proposed. The problem in India is not about planning but putting those plans into action.

-‐ Pavitra Narayanan -‐ 1120347

14

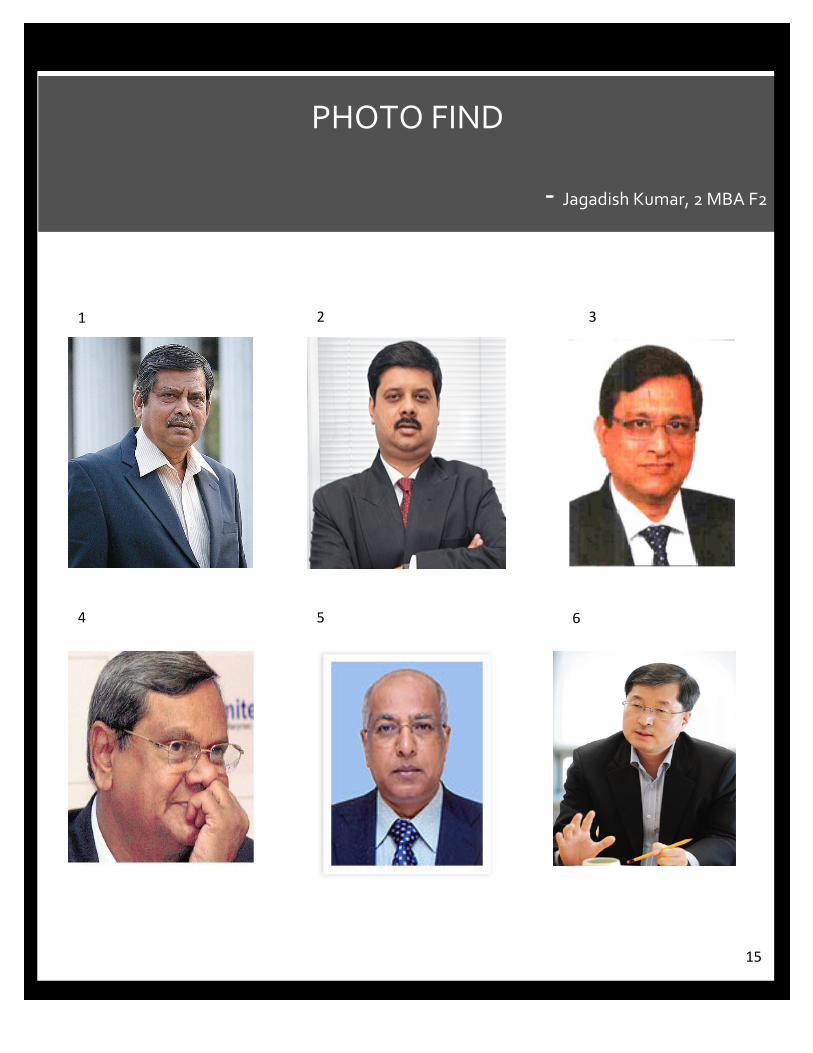

PHOTO FIND

-‐ Jagadish Kumar, 2 MBA F2

1 2 3

4 5 6

15

CROSSWORD

-‐ Nagarajan, 2 MBA F1

16

Across

1. An ___________ is granted for undertaking operations to mine any mineral. This is for any mineral or prescribed

group of associated minerals is granted for a minimum period of 20 years and a maximum period of 30 years. (Abbreviated) (2)

3. A specific pattern of a candlestick chart that indicates that a security's open and close prices were nearly identical. It generally looks like a cross or a plus sign. (4)

5. India’s major workable coal deposits occur in India. Part of it is overlaid with alluvium, and in the west it is overlaid with the igneous rocks of the Deccan Traps. (8)

6. Bharat Coking Coal Limited (BCCL) and Coal Mines Authority Limited (CMAL) were merged to form the holding company. This company is named as __________. (Abbreviated) (3)

7. The rent fixed for mines without considering the fact whether the mine is profitable or not. It is mostly fixed in a mineral lease. This rent must be paid whether or not minerals are being extracted from the mines. (4)

Down

2. The coal segment in India consists of three components. Anthracite, Bituminous and ____________ (7) 3. The Honorable Minister for Mines (First name) (6) 4. The Honda committee has come up with the setting up of this fund. (Abbreviated) (3) 8. A technical indicator that measures the level at which a security or asset is either oversold or overbought.

Applying the same factors as the relative strength index (RSI), this index also employs a self-‐adjusting mechanism that accounts for varying degrees of market volatility, which produces a more accurate reading. (Abbreviated) (3)

1) Which mineral has the highest share in the Indian mining industry?

2) How many different types of minerals are produced in India?

3) India is the largest producer of which mineral in the world

4) Recently a mining sector reform named Executive Order 79 was signed name the country

5) Top mining company in India according to:

i) Market capitalization

ii) Net profits

6) First Exchange Traded Fund of World TIP 35 is set up in 1989 in which country?

7) Mutual offsetting of claims and liabilities from identical types of transaction between two parties

8) Expand NASDAQ?

9) RBI governor Dr.Subbarao D is the successor of

10) Who is the President of Federal Reserve Bank?

QUIZ

-‐ Kumaran S, 2 MBA F1

17

ANSWERS

Photo find:

1. Ashok Kumar Sinha CFO of Coal India pvt ltd

2. Koushik chattarjee – CFO of Tata Steel

3. MG Gupta-‐ Director of finance, MMTC

4. Rana Som-‐ MD of NMDC

5. Subhra Sengupta-‐ CFO of Tata Metaliks

6. Park Ki Hong – CFO of Posco

1. Coal (80%)

2. 89 minerals (4 fuel minerals, 11 metallic, 52 non-‐metallic and 22 minor minerals)

3. Mica

4. Philippines (President Benigno S. Aquino III)

5. (i) Market capitalization: Coal India

(ii) Net profit: NMDC

6. Canada.

7. Netting.

8. National Association of Securities Dealer automated Quotations

9. Dr.Y V Reddy

10. Ben Bernanke.

18

Crossword: Across

1. ML (Mining Lease) A ___________ is granted for undertaking operations to mine any mineral. This is for any

mineral or prescribed group of associated minerals is granted for a minimum period of 20 years and a maximum period of 30 years. (Abbreviated)

3. DOJI—A specific pattern of a candlestick chart that indicates that a security's open and close prices were nearly identical. A doji generally looks like a cross or a plus sign.

5. GONDWANA—India’s major workable coal deposits occur in India. Part of it is overlaid with alluvium, and in the west it is overlaid with the igneous rocks of the Deccan Traps.

6. CIL (Coal India Limited) Bharat Coking Coal Limited (BCCL) and Coal Mines Authority Limited (CMAL) were merged to form the holding company. This company is named as __________.(Abbreviated)

7. DEAD—The rent fixed for mines without considering the fact whether the mine is profitable or not. It is mostly fixed in a mineral lease. This rent must be paid whether or not minerals are being extracted from the mines.

Down

2. LIGNITE—The coal segment in India consists of three components. Anthracite, Bituminous and ____________ 3. DINSHA—The Honorable Minister for Mines (First name) 4. MDF (Mines Development Fund) the Honda committee has come up with the setting up of this fund.

(Abbreviated) 8. DMI (Dynamic Momentum Index) A technical indicator that measures the level at which a security or asset is

either oversold or overbought. Applying the same factors as the relative strength index (RSI), this index also employs a self-‐adjusting mechanism that accounts for varying degrees of market volatility which produces a more accurate reading. (Abbreviated)

19

Faculty Coordinator

Co-‐ordinators:

Niveda S (MBA F1)

Dr. Anirban Ghatak

Abby Jacob

(MBA F2)

Editors: Creative and Designing:

Sheena Renu

(MBA F1)

Bala Surya Kiran R (MBA F2)

Karthik R (MBA F2)

Stock Analysis:

Articles:

Abhishek Jain

(MBA F1)

Akhilesh C (MBA F1)

Ritesh (MBA F1)

Marina Kurian (MBA F1)

Sivakumar (MBA F2)

RBI column:

Crossword:

Nidhi Jaiswal (MBA F1)

Nagarajan (MBA F1)

Finance Buzz:

Photo Find

Manisha B (MBA F1)

Jagadish Kumar

(MBA F2)

Economic Rollers:

Campus Poll:

Dhawal Parmar (MBA F1)

Abhisek Roy

(MBA F1)

Arun P

(MBA F2)

Finance Quiz:

Kumaran (MBA F1)

Dolor sit amet.

NISHKA is a monthly finance magazine brought by the students of the

finance club of CHRIST UNIVERSITY Institute of Management

Kengeri Campus. The Idea behind coining the issue of this magazine is

to establish a learning among the students, which helps them to gain an

insight about the world of finance.

- TEAM NISHKA

ABOUT NISHKA

Institute Of Management

Kengeri, Bangalore

Please mail your valuable feedbacks, reviews at [email protected]

(For Private Circulation Only)