LAS VEGASCOMMERCIAL REAL ESTATE

ROUNDUP

Presented by:

Presented to:

October 14, 2015

WHY WE’RE HERE

2

Source: Bureau of Labor Statistics.

Peak to Trough % Job Change: 1948-2001

Nevada job recovery: Previous 10 Recessions

Nevada

US

3

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

0 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84 87 90 93 96 99

% C

hang

e in

Jobs

(Pea

k to

Tro

ugh)

Number of Months After Peak Employment

1948 1953 1957 1960 19691974 1980 1981 1990 2001

Source: Bureau of Labor Statistics.

Peak to Trough % Job Change: 1948 to Present

Nevada job recovery from Great Recession (after 99 months)

Nevada

US

4

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

0 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84 87 90 93 96 99

% C

hang

e in

Jobs

(Pea

k to

Tro

ugh)

Number of Months After Peak Employment

1948 1953 1957 1960 1969 19741980 1981 1990 2001 2007 US 2007

US Jobs

NV Jobs

PART 1: THE SOUTHERNNEVADA JOB MARKET

5

JobsAbsorptionVacancyRents

Source: Bureau of Labor Statistics.

Rate of Nevada & Las Vegas MSA Job Recovery, by Jobs: 1/2007-8/2015

Las Vegas job recovery 88% complete,full recovery likely within 9 months

6

1,293,1001,263,600

931,100

916,300

750,000

850,000

950,000

1,050,000

1,150,000

1,250,000

1,350,000

# of

Non

-Far

m Jo

bs

NevadaLas Vegas

1,111,500

181,600 Total Jobs Lost in Nevada

798,200

132,900 Total Jobs Lost in Las Vegas

Aug-15:29,000 Jobs to Go for Recovery

Aug-15:16,200 Jobs to Go for Recovery

Source: Bureau of Labor Statistics.

Nevada Job Growth & Headline Unemployment Rate: 8/2006-8/2015

Unemployment continues to drop, job growth slowing but good

7

-15%

-10%

-5%

0%

5%

10%

15%

Perc

ent (

%)

Axis Title

Job Growth Unemp. Rate

Aug-15 Job Gr: +3.4%

Aug-15 Unemp: 7.1%

Source: Bureau of Labor Statistics.

Nevada U-3 & U-6 Rates: Q2, 2010-Q2, 2015

U-6 rate shows high share of forced part-time workers in Nevada

8

13.5

13.8

14.4

14.2

13.6

13.5

13.112.7

12.311.9

11.010.8

10.49.7

9.89.4

8.88.3

7.7

7.6

7.3

21.5

22.323.6

23.7

23.3

23.3

22.722.3

22.121.4

20.319.6

19.018.1

18.117.4

16.215.9

15.3

15.3

15.2

0

5

10

15

20

25

Perc

ent (

%)

U3 U6

Source: Bureau of Labor Statistics.

US, Nevada & Las Vegas MSA Average Weekly Hours: 8/2009-8/2015

Las Vegas MSA work hours continue to slide as unemployment rate improves

9

32

33

34

35

36

37

Aver

age

Wee

kly

Hour

s Wor

ked

United States

Nevada

Las Vegas MSA

US: Aug-15: 34.6

LV: Aug-15: 33.2

NV: Aug-15: 33.5

Source: Bureau of Labor Statistics.

Las Vegas MSA Average Weekly Earnings: 8/2009-8/2015

Las Vegas MSA earnings rising with improving unemployment rate

10

$550

$600

$650

$700

$750

Aver

age

Wee

kly

Earn

ings

Aug-15 Nominal: $715

Nominal Avg. Weekly Earnings

Inflation-Adjusted (2007$) Avg. Weekly Earnings

Aug-15 Real: $634

Source: Nevada Department of Taxation; calculated by RCG Economics.

Clark County Total Taxable Retail Sales (“TRS”) vs. Traditional Retailer TRS: 7/2013-7/2015

Retail sales holding steady, with slight drop-off going into summer

11

4.8% 5.2%5.8%

7.9%

8.1% 8.2% 7.2%

3.6%

4.7% 4.9%5.3%

4.7%4.5% 4.4%

0%

2%

4%

6%

8%

10%

12%

Taxa

ble

Reta

il Sa

les

Clark County TRS

CC Traditional Retailers TRS

PART 2: THE COMMERCIALREAL ESTATE MARKETS

12

JobsAbsorptionVacancyRents

*Natural resources, construction, manufacturing, and transportation & warehousing industries.Source: Bureau of Labor Statistics; calculated by RCG Economics.

Las Vegas MSA Industrial-Using* Jobs & Growth: 8/2014-8/2015

Industrial jobs still growing but rate slowing, possible due lack of space

13

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

118,000

120,000

122,000

124,000

126,000

128,000

130,000

132,000

134,000

Perc

ent G

row

th

Indu

stria

l-Usi

ng Jo

bs

Industrial Jobs YOY % Gr.

*Information, financial activities, professional & business and health care & social assistance. Source: Bureau of Labor Statistics; calculated by RCG Economics.

Las Vegas MSA Office-Using* Jobs & Growth: 8/2014-8/2015

2015 office job growth generally trending upward after slow start

14

0%

1%

2%

3%

4%

5%

6%

238,000

240,000

242,000

244,000

246,000

248,000

250,000

252,000

254,000

Perc

ent G

row

th

Off

ice-

Usi

ng Jo

bs

Office Jobs YOY % Gr.

Source: Bureau of Labor Statistics; calculated by RCG Economics.

Las Vegas MSA Retail-Using Jobs & Growth: 8/2014-8/2015

Retail job growth falling big during summer doldrums; will pick-up in holidays

15

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

96,000

98,000

100,000

102,000

104,000

106,000

108,000

110,000

Perc

ent G

row

th

Reta

il-U

sing

Jobs

Retail Jobs YOY % Gr.

Source: RCG Economics.

Las Vegas Valley Industrial YOY Absorption & Completions: Q2, 2013-Q2, 2015

Industrial absorption over 4M SF for 7 straight quarters

16

2,10

5,81

8

3,77

5,92

2

4,62

6,07

4

4,76

6,83

1

5,01

1,93

4

4,58

5,83

6

5,23

3,36

5

4,98

0,85

6

4,27

5,31

0

449,

473

801,

473

801,

473

773,

473

920,

000

607,

490

607,

490

586,

992

555,

195

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

SF

Net Absorption Completions

Source: RCG Economics.

Las Vegas Valley Spec Office YOY Absorption & Completions: Q2, 2013-Q2, 2015

Office absorption declined 3 quarters in a row

17

235,

712

-100

,701

129,

477

593,

814

826,

613

1,62

0,09

9

1,23

0,73

7

954,

786

754,

556

67,6

92

26,0

00

81,0

00

126,

700

126,

700

270,

700

225,

700

392,

868

392,

868

-800,000

-300,000

200,000

700,000

1,200,000

1,700,000

2,200,000

SF

Net Absorption Completions

Source: RCG Economics.

Las Vegas Valley Anch. Retail YOY Absorption & Completions: Q2, 2013-Q2, 2015

Retail absorption effectively zero over last 2 quarters

18

698,

027

419,

235

484,

504

436,

903

350,

775

594,

326

320,

789

24,5

31

1,64

4

0 0 0 0 0 0

222,

000

222,

000

222,

000

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

SF

Net Absorption Completions

Source: RCG Economics.

Las Vegas Valley Industrial Vacancy Rate, by Product: Q2, 2014-Q2, 2015

All Industrial space types experienced improvement in vacancy rate

19

0%

5%

10%

15%

20%

25%

Vaca

ncy

Rate

Q2 '14

Q2 '15

Source: RCG Economics.

Las Vegas Valley Industrial Vacancy Rate, by Submarket: Q2, 2014-Q2, 2015

North Las Vegas, Henderson leading submarkets in occupied Industrial space

20

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Vaca

ncy

Rate

Q2 '14

Q2 '15

Source: RCG Economics.

Las Vegas Valley Spec Office Vacancy Rate, by Product: Q2, 2014-Q2, 2015

Class C driving improvement inSpec Office vacancy rate

21

0%

5%

10%

15%

20%

25%

30%

35%

40%

All Prod. Class A Class B Class C Medical

Vaca

ncy

Rate

Q2 '14

Q2 '15

Source: RCG Economics.

Las Vegas Valley Spec Office Vacancy Rate, by Submarket: Q2, 2014-Q2, 2015

Class C-heavy NLV doing well, Class A-heavy East LV (Hughes Center) lagging

22

0%

5%

10%

15%

20%

25%

30%

35%

Vaca

ncy

Rate

Q2 '14

Q2 '15

Source: RCG Economics.

Las Vegas Valley Anch. Retail Vacancy Rate, by Product: Q2, 2014-Q2, 2015

Improvement in Retail vacancy rate stall, Power Centers strengthening

23

0%

4%

8%

12%

16%

All Prod. Power Community Neighborhood

Vaca

ncy

Rate

Q2 '14

Q2 '15

Source: RCG Economics.

Las Vegas Valley Anch. Retail Vacancy Rate, by Submarket: Q2, 2014-Q2, 2015

NE, NW & SW markets healthy, while Downtown, University East struggling

24

0%

4%

8%

12%

16%

20%

Vaca

ncy

Rate

Q2 '14

Q2 '15

Source: RCG Economics.

Las Vegas Valley Industrial Vacancy Rate & Rents: Q2, 2014-Q2, 2015

Industrial rents rising slowly as vacancy rate drops below10%; quality space gone

25

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

$ PS

F Pe

r Mon

th (N

NN

)

% V

acan

t

Vacancy - Q2-15 = 6.2%

Asking Rents - Q2-15 = $0.66 PSF/Mo.

Source: RCG Economics.

Las Vegas Valley Spec Office Vacancy Rate & Rents: Q2, 2014-Q2, 2015

Office rents roughly stable with a high but stable vacancy rate

26

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

0%

5%

10%

15%

20%

25%

30%

$ PS

F Pe

r Mon

th (F

SG)

% V

acan

t

Vacancy - Q2-15 = 21.6%

Asking Rents - Q2-15 = $2.14 PSF/Mo.

Source: RCG Economics.

Las Vegas Valley Anch. Retail Vacancy Rate & Rents: Q2, 2014-Q2, 2015

Retail rents leveling off; vacancy rate stabilizing at ~11.5%

27

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

$ PS

F Pe

r Mon

th (N

NN

)

% V

acan

t

Vacancy - Q2-15 = 11.9%

Asking Rents - Q2-15 = $1.29 PSF/Mo.

Source: RCG Economics.

Las Vegas Valley Industrial Completions as % of Inventory: Q2, 2014-Q2, 2015

Industrial completions picking up; more space on the way

28

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Com

plet

ions

as %

of I

nven

tory

Source: RCG Economics.

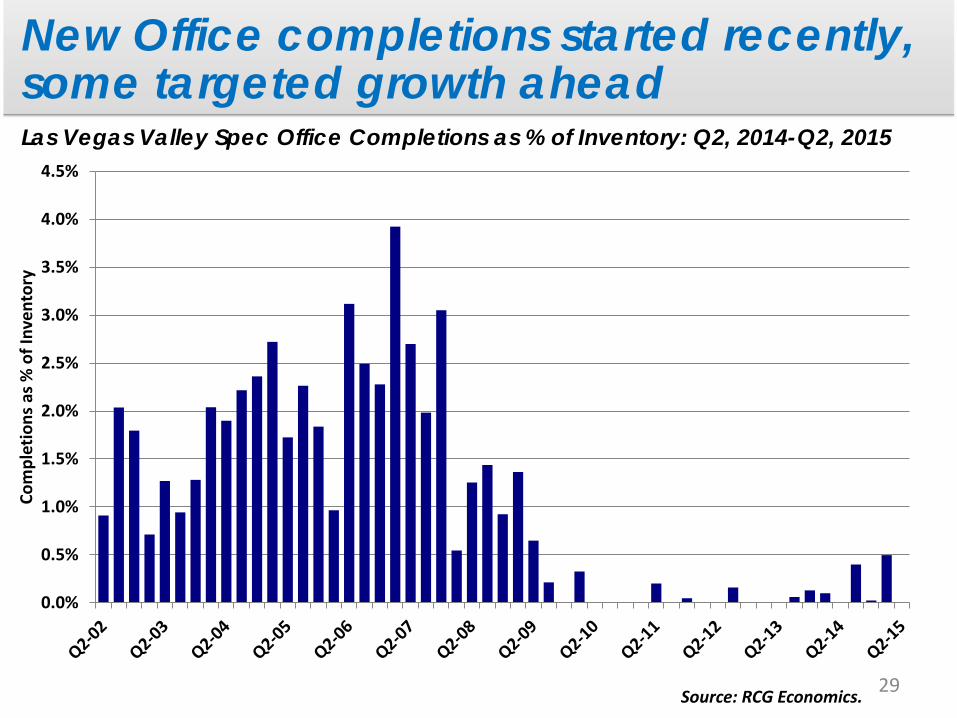

Las Vegas Valley Spec Office Completions as % of Inventory: Q2, 2014-Q2, 2015

New Office completions started recently,some targeted growth ahead

29

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

Com

plet

ions

as %

of I

nven

tory

Source: RCG Economics.

Las Vegas Valley Anch. Retail Completions as % of Inventory: Q2, 2014-Q2, 2015

Retail completions near zero, flickers of hope on horizon

30

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Com

plet

ions

as %

of I

nven

tory

Our Services & Products

Our Services Real Estate Market Research Regional Economics Demographics Public Policy Research Tax Policy Analysis

Our Products The Stat Pack Nevada Job Flash Quarterly Commercial Real Estate Services Metro Area Overviews

31

Questions?

32