DESIGNING AND IMPLEMENTING LAST-

MILE SERVICE DELIVERY SOLUTIONS AND

INNOVATIONS: FINANCIAL INCLUSION

OF POOR THROUGH COMMUNITY

INSTITUTIONS IN INDIA

Livelihoods Story

Incomes Expenses

Wage Income 53% Food Expenses 58%

Farm 18% Healthcare 12%

Livestock 15% Personal 15%

Non Farm 14 % Interest Burden15%

Bleeding Livelihoods – Sheikwara, Gaya District (Birthplace of Bhoodan in Bihar)- Farm wages are paid in form of grain. NO WORK – NO FOOD.- All Bhoodan lands mortgaged due FOOD and HEALTH SHOCKS.- Lease-in land (up to 10 decimals) to GROW FOOD for own consumption.- FOOD LOANS repaid in kind or tied labour and/or produce.- MIGRATION offers plausible solution, but with heavy upfront costs .

Poor need financial products matching cash, income, expenditure and risk cycles in their life.

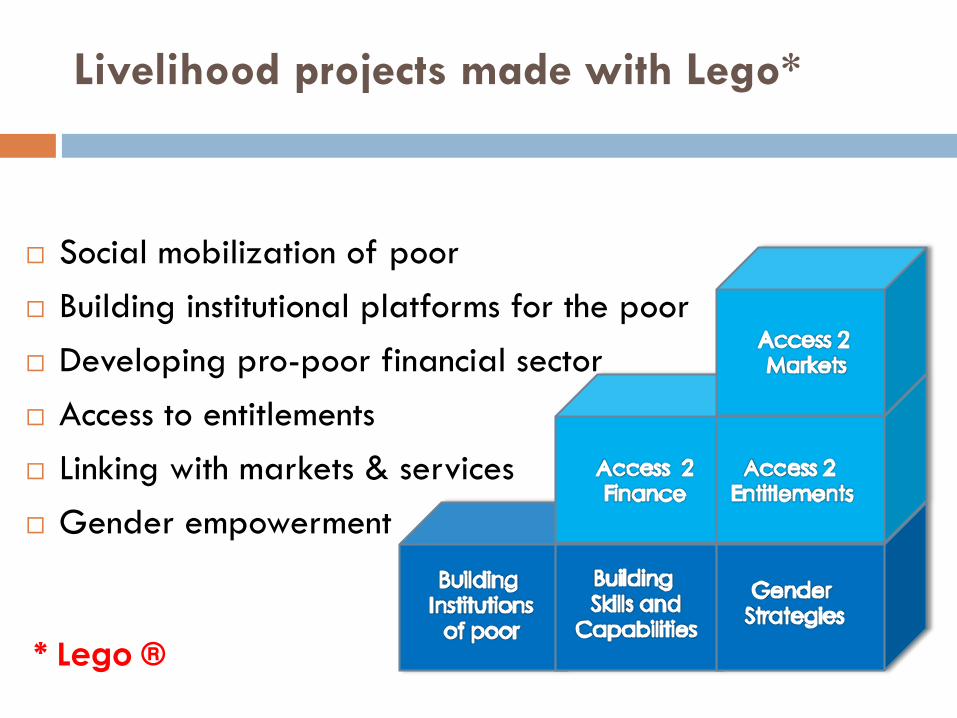

Livelihood projects made with Lego*

Social mobilization of poor

Building institutional platforms for the poor

Developing pro-poor financial sector

Access to entitlements

Linking with markets & services

Gender empowerment

* Lego ®

Investing on demand side:

Building access to markets agenda

Entitlements and Social Security

Food Security – PDS, Food Security Enterprise

Health Security – Nutrition, CMHS

Income Security – NREGA, Pensions

Risk Management – Insurance (Life, health, assets)

Access to Markets and Services

Productive assets and skills

Productivity Enhancement - SRI, SWI, CMSA, Dairy

Collective Marketing - Agri Commodities, NTFP, Dairy

Market linked Jobs

But Financial Inclusion has always

been a story of the Fox and the Crane

Both friends had an equal opportunity for nourishment, but each time one of them could not take advantage of the

opportunity.

Financial Inclusion Strategies

Building an inclusive financial sector

Making poor preferred clients for banking system

Monetize livelihoods economy of the poor

Reduction in high cost indebtedness for the poor

Financial education for planned investments

Leveraging investments from mainstream banks

Pro-active and systematic initiatives working on both ‘supply’ and ‘demand’ side of financial inclusion agenda

Lessons from banking with the poor

Initial engagement in AP, Tamil Nadu and Orissa

Saturation approach to SHG formation

Saturated training and sensitization effort

Coordination mechanisms: Govt, NABARD & banks

Sharing of MIS with banks and tracking credit linkage

Result: Initial inertia overcome, momentum picked up

Accelerated change in AP, Bihar and Odisha

Micro Credit Plan based lending

Community involvement for bank linkage & recovery

Livelihood innovations triggered financial innovations

Transformation in Delivery of Financial

Services to the Poor

Product innovations by the communities by

bundling micro-credit with livelihood services

Food Credit and Nutrition Credit

Co-production model for rural financial services

Relationship managers for the poor (Bima Mitras)

Agency arrangements for financial services delivery

New technologies and business models transform

last mile service delivery

IT enabled with Micro-insurance Companies

Smart Card based Payment Systems

Co producing Financial Services:

Innovations

Strategic Partnerships with Commercial Banks AP: New product development

Bihar & MP: Business process re-engineering

Bihar: Dedicated spear head teams

Product Innovations AP & Bihar: Bundling microcredit with Food & Nutrition

AP & Bihar: Health savings

Bihar: Swapping high cost debts – land and milk

Bihar: Loans for land and animal leasing

AP & Bihar: Loans against anticipated NREGA payments

AP: AP: Bank product for assistance food security line

AP: Bank assistance for Total Financial Inclusion (TFI)

Co producing Financial Services:

Innovations

Service Innovations AP & Bihar: Help-desks at Bank Branches (Bank Mitras)

AP: Branchless Banking for Social Security Payments

AP & Bihar: SHG Federations as Banking Touch Points/CSC

AP: SHG Federations as micro insurance franchisees enabling universal access to insurance by setting high standard of service delivery

Consumer Innovations AP: Savings from social security payments

Bihar: Poor use savings accounts of SHGs on CBS platform

to make and receive remittances at ZERO COST

Bihar: Micro Credit Planning as tool for financial and

business education

Co producing Financial Services:

Innovations

Service Innovations

Bihar & Odisha: Financial literacy and credit

counseling – Vitta Mitra

AP, Bihar & Odisha: Help desks - Bank Mitra

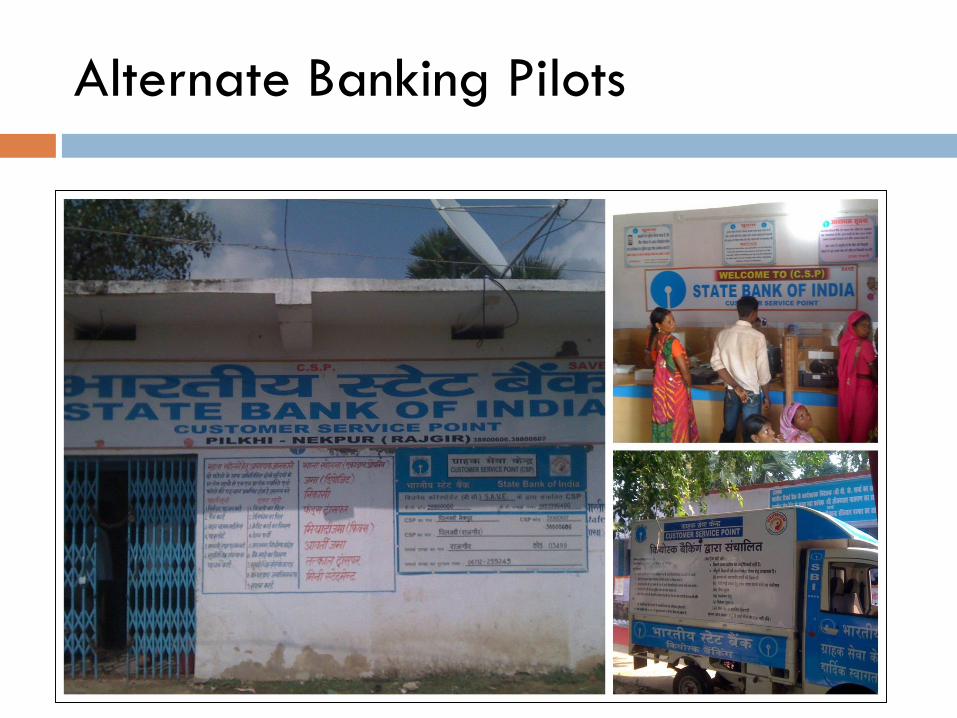

Alternative Banking Channels

Odisha: Mobile Van (UCO Bank)

Bihar: Kiosk Banking (SBI)

AP & Bihar: Dairy Banking (HDFC Bank)

Financial Inclusion

Building Informed, Empowered and Responsible Clients

Micro Planning

Financial Literacy and Counselling “Vitta Mitras”

Community Managed audit and recovery Mechanism

Enabling access to Insurance

Product Innovations using CIF as catalytic fund

Debt Swapping, Food Security Fund, Health Risk Fund etc.

Making Formal Financial Sector Deliver

Partnerships ( formal MoUs) with commercial banks & sensitization of local bankers

Placement of customer relations managers (Bank Mitra) to smoothen the transactions at the branch level

Alternate Banking Models for Total Financial Inclusion

Enabling access to a suite of financial services at the doorstep

SHG women as CSPs at the last mile

Vitth Mitra – Financial Counseling

Bank Mitra – Help Desk

Outreach4500 Bank Mitras

across the Country

Impact• Transaction time

down from 2.5 hours

to just 15 minutes

• 95 + percent SHGs in

these branches are

credit linked

• NPA is less by at least

30%

Alternate Banking Pilots

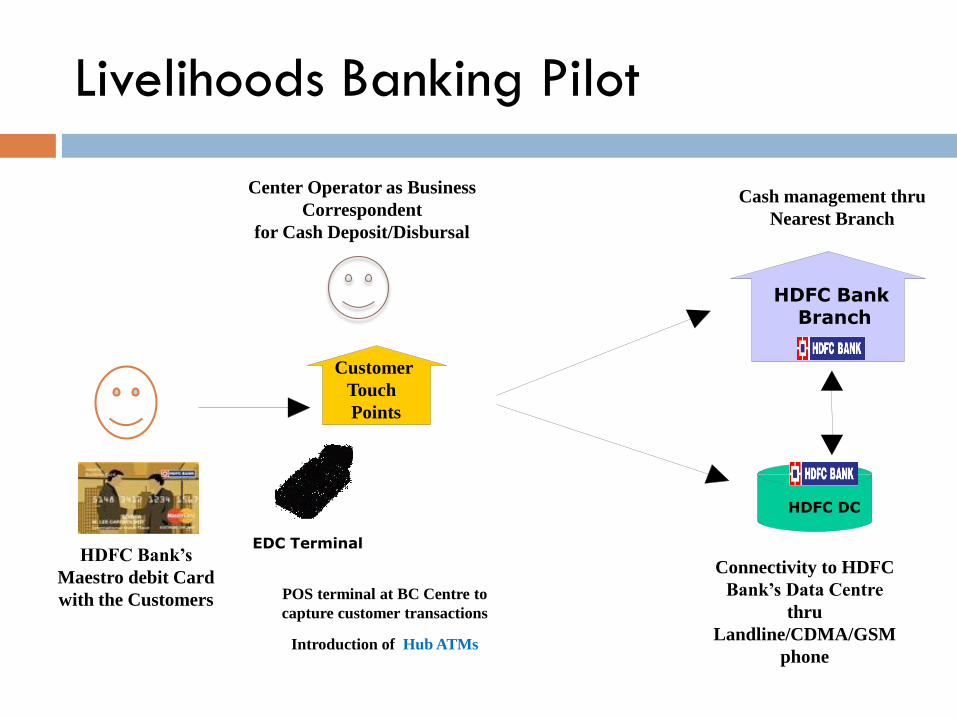

Livelihoods Banking Pilot

HDFC BankBranch

Customer

Touch

Points

HDFC Bank’s

Maestro debit Card

with the Customers

EDC Terminal

HDFC DC

Connectivity to HDFC

Bank’s Data Centre

thru

Landline/CDMA/GSM

phonephone

Cash management thru

Nearest Branch

Center Operator as Business

Correspondent

for Cash Deposit/Disbursal

POS terminal at BC Centre to

capture customer transactions

Introduction of Hub ATMs

Mobile-bookkeeping

Payment of

Solatium/Relief

Claim village Call Centre located in

District Federation

Area Committee

Members

Commercial

Bank

AlertUS$ 125

Phone

Insurance Claim Settlement Process

• Area Committee completes documentation and sends e-Claim to Insurance Company via District

Federation

Community led Micro Insurance

Model

ATM

Favorable Investment Climate for Rural Poor

Saving 5.5 billion

Learnings

Invest with a long term perspective

Investing in institutions requires experimentation,

failure and learning. We need to put risk capital in

and learn from failures

Invest in political economy from the beginning.

Governments need to see a political value

preposition

Need to invest in aggregate forms of social capital

and institutions to create a favorable investment

climate