Lecturer: Tran Viet Thang

ACCACertified Accounting Technician

(CAT)Paper 1 - Recording Financial

Transactions

Syllabus overview

Part A Introduction to transaction accounting1 Business transactions and documentation2 Assets, liabilities and the accounting

equation3 Statement of financial position and income

statement4 Recording, summarising and posting

transactions5 Completing ledger accounts

Syllabus overview

Part B Recording and accounting for cash transactions6 Receiving and checking money7 Banking monies received8 Recording monies received9 Authorising and making payments10 Recording payments11 Maintaining petty cash records12 Bank reconciliations

Syllabus overview

Part C Recording and accounting for credit transactions13 Sales and sales returns day books14 The receivables ledger 15 Purchase and purchase returns day books 16 The payables ledger17 Control accounts

Part D Payroll18 Recording payroll transactions

CHAPTER 1Business transactions and documentation

Contents overview

Types of business transaction Documenting business transactions Invoices and credit notes Discounts, rebates and allowances Sales tax Contract law Storage of information Data protection

Types of business transaction What is a business?

Uses economic resources to create goods or services which customers will buy

Provides jobs for people to work in Invests money in resources in order to

make even more money for its owners Business transactions?

Property changes hands Two main types: sales and purchases

By cash or on credit

Sales By cash: goods or services given in

exchange for immediate payment (in notes, coins, cheques)

On credit: cash received later Purchases:

For cash: payment made immediately On credit: cash paid later

Other business transactions

Payment of wages Borrowing money Lending money Offering a discount Receiving a discount

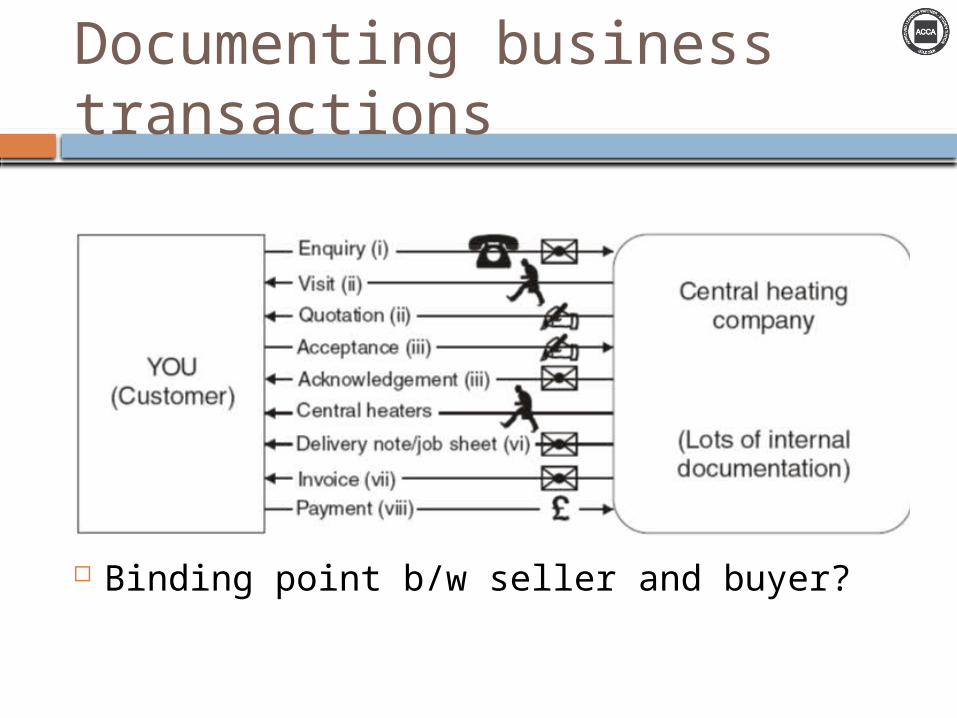

Documenting business transactions

Binding point b/w seller and buyer?

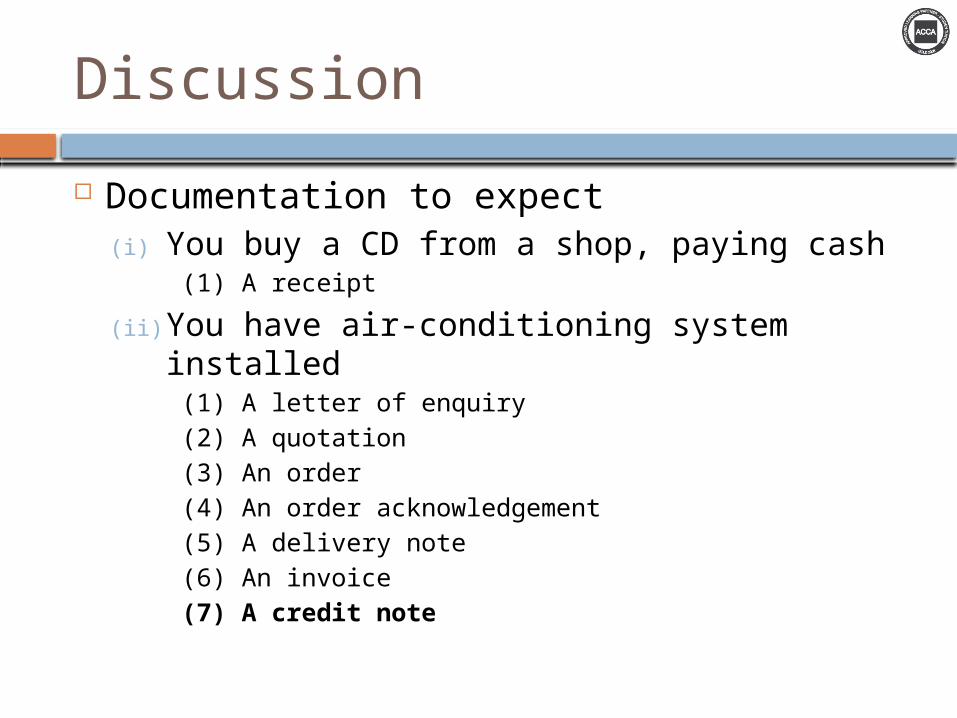

Discussion

Documentation to expect(i) You buy a CD from a shop, paying cash

(1) A receipt

(ii) You have air-conditioning system installed(1) A letter of enquiry(2) A quotation(3) An order(4) An order acknowledgement(5) A delivery note(6) An invoice(7) A credit note

More documents

Inventory lists: check availability of all the parts Supplier lists: where to buy parts Staff schedules: plan for human resource Timesheet: record the actual hours staff spent Goods received notes Expense claims: Employees may incur

expenses which need to be reimbursedAccounting system: records, summarizes and

presents the information contained in these documents

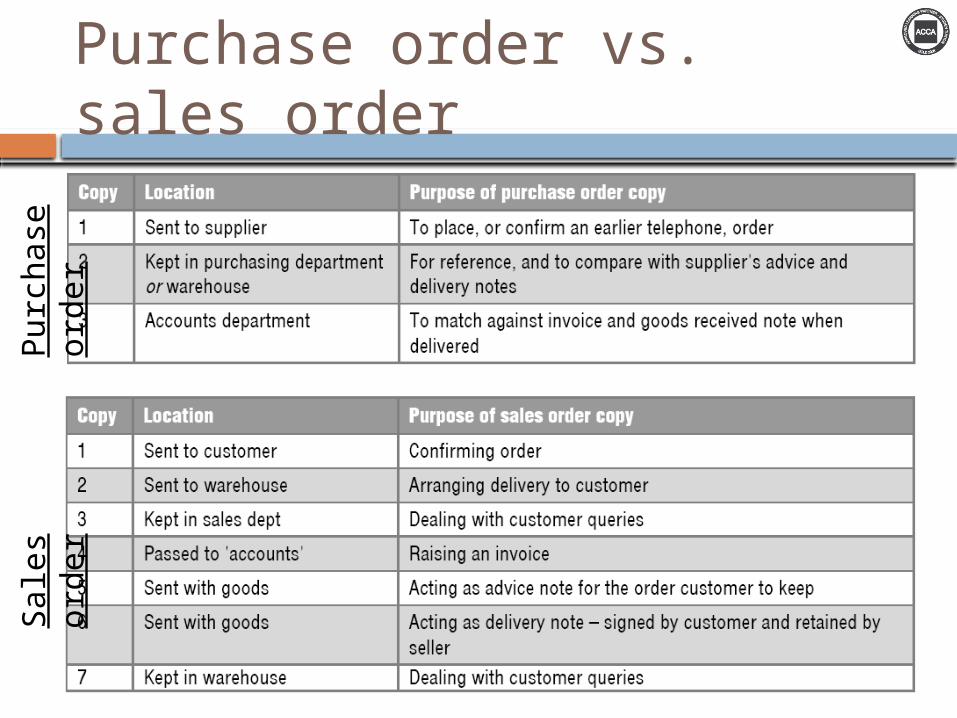

Purchase order vs. sales order

Pu

rchase

ord

er

Sale

s ord

er

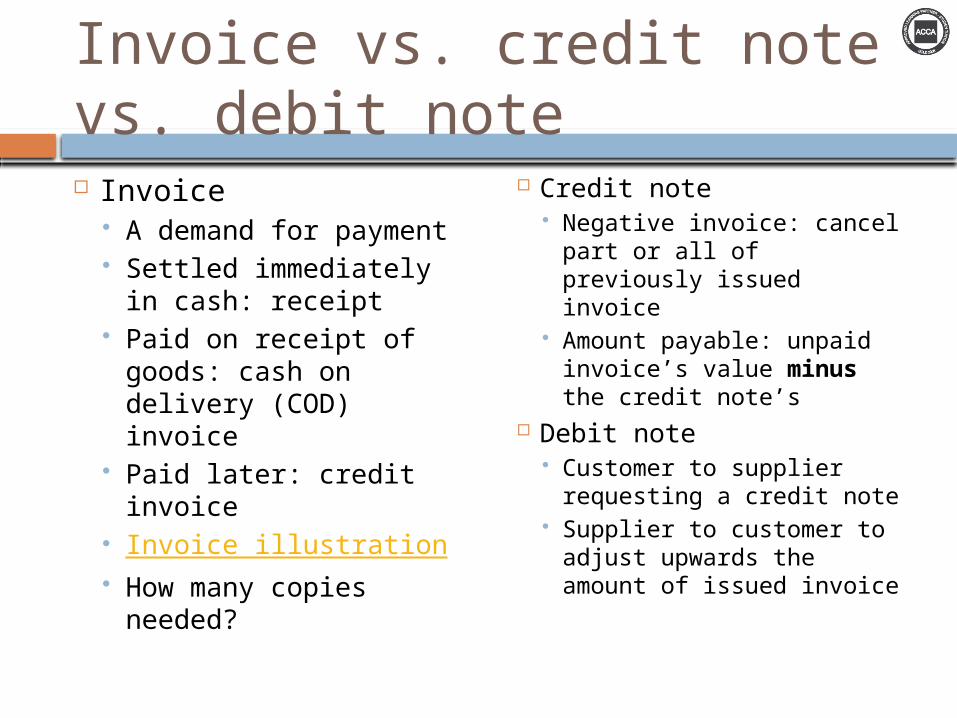

Invoice vs. credit note vs. debit note Invoice

A demand for payment Settled immediately in

cash: receipt Paid on receipt of

goods: cash on delivery (COD) invoice

Paid later: credit invoice

Invoice illustration How many copies

needed?

Credit note Negative invoice: cancel

part or all of previously issued invoice

Amount payable: unpaid invoice’s value minus the credit note’s

Debit note Customer to supplier

requesting a credit note Supplier to customer to

adjust upwards the amount of issued invoice

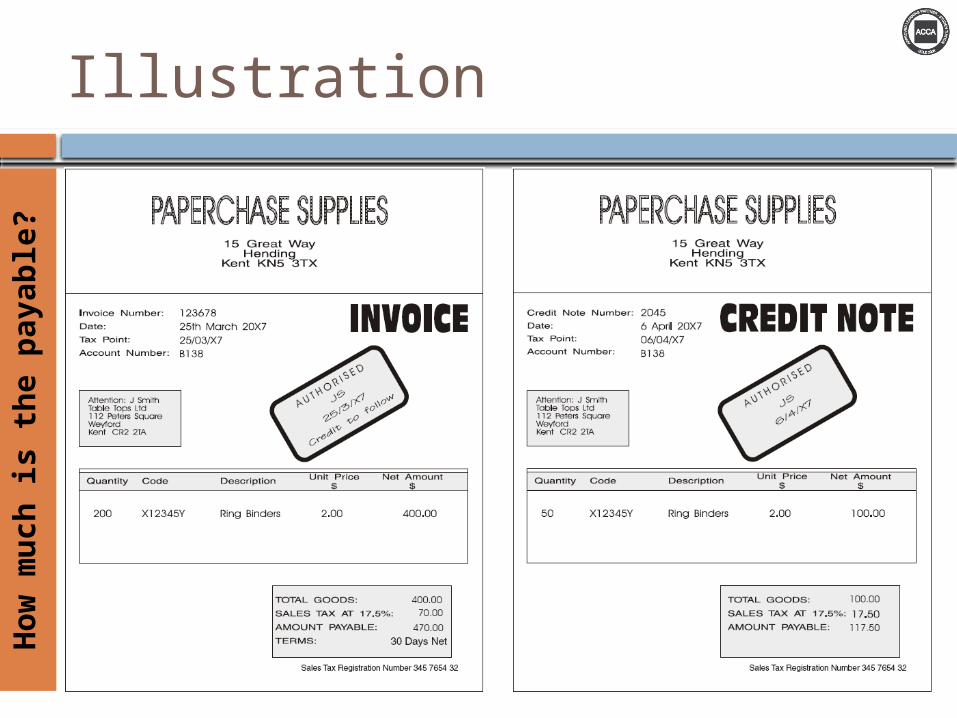

IllustrationH

ow

mu

ch

is t

he p

ayab

le?

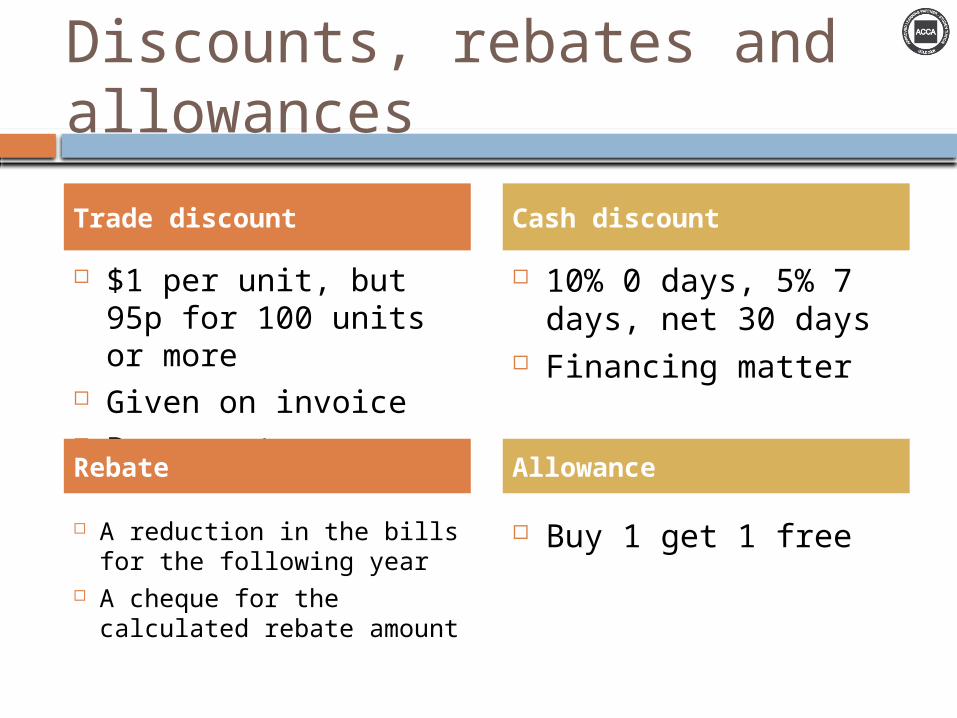

Discounts, rebates and allowances

$1 per unit, but 95p for 100 units or more

Given on invoice Permanent

10% 0 days, 5% 7 days, net 30 days

Financing matter

Trade discount Cash discount

A reduction in the bills for the following year

A cheque for the calculated rebate amount

Buy 1 get 1 free

Rebate Allowance

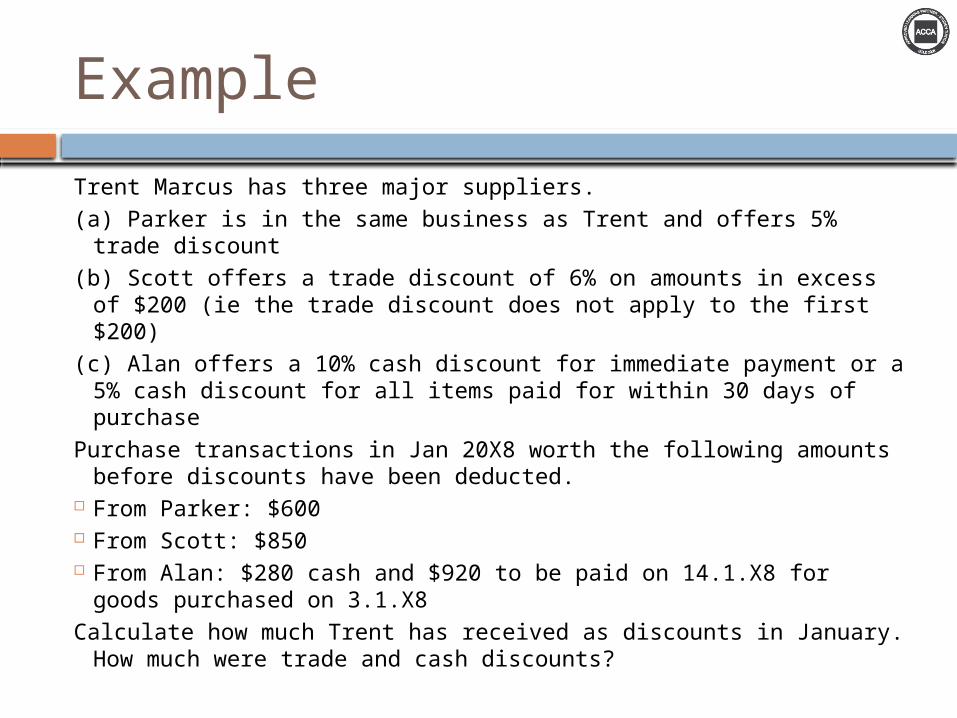

Example

Trent Marcus has three major suppliers.(a) Parker is in the same business as Trent and offers 5% trade

discount(b) Scott offers a trade discount of 6% on amounts in excess of

$200 (ie the trade discount does not apply to the first $200)(c) Alan offers a 10% cash discount for immediate payment or a

5% cash discount for all items paid for within 30 days of purchase

Purchase transactions in Jan 20X8 worth the following amounts before discounts have been deducted.

From Parker: $600 From Scott: $850 From Alan: $280 cash and $920 to be paid on 14.1.X8 for goods

purchased on 3.1.X8Calculate how much Trent has received as discounts in January.

How much were trade and cash discounts?

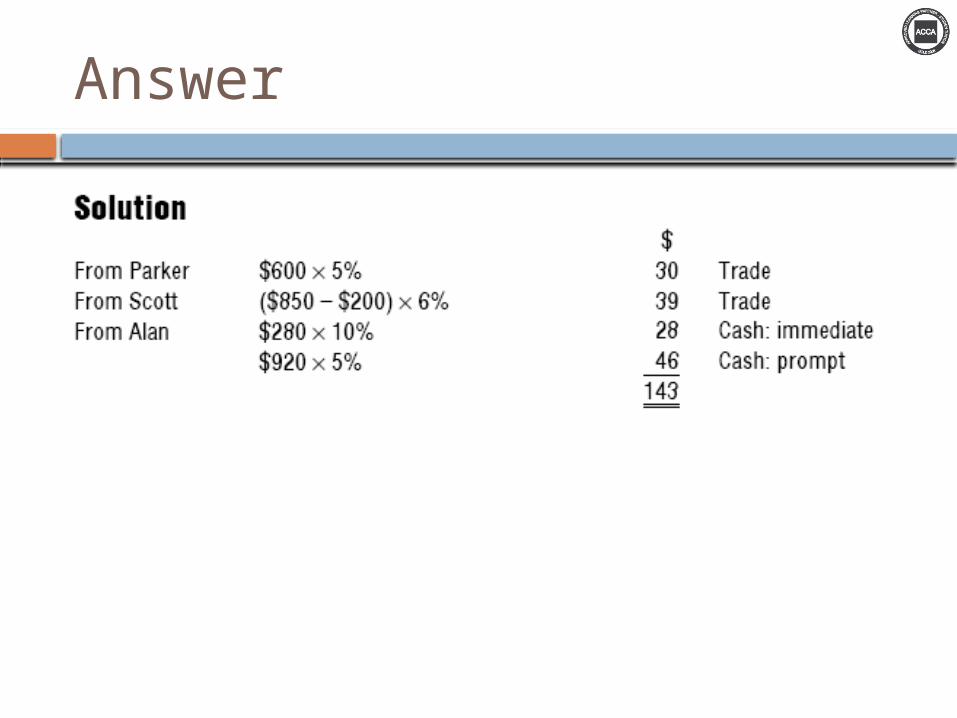

Answer

Example

Product A is quoted at $10 per each. A lower price of 95% per unit for buying 100 units or more at a time. One company purchased 150 units.

What is accounting treatment?

Trade discount The value of those goods recorded in accounting

book should be the net amount after discount i.e, $1,425

($1,425 = 150*$10*95%)

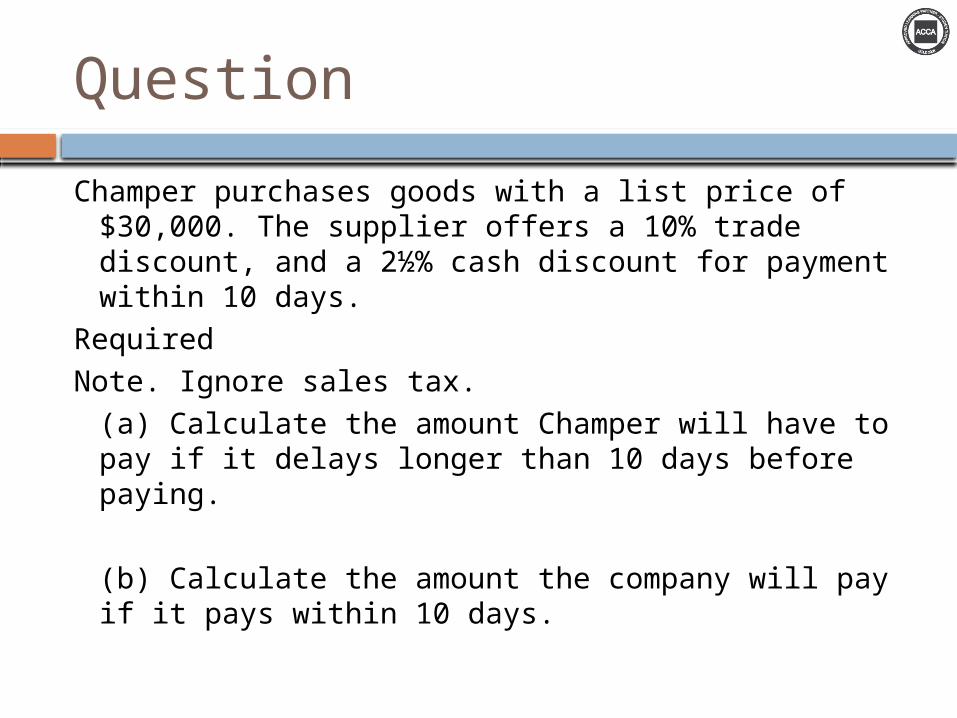

Question

Champer purchases goods with a list price of $30,000. The supplier offers a 10% trade discount, and a 2½% cash discount for payment within 10 days.

RequiredNote. Ignore sales tax.

(a) Calculate the amount Champer will have to pay if it delays longer than 10 days before paying.

(b) Calculate the amount the company will pay if it pays within 10 days.

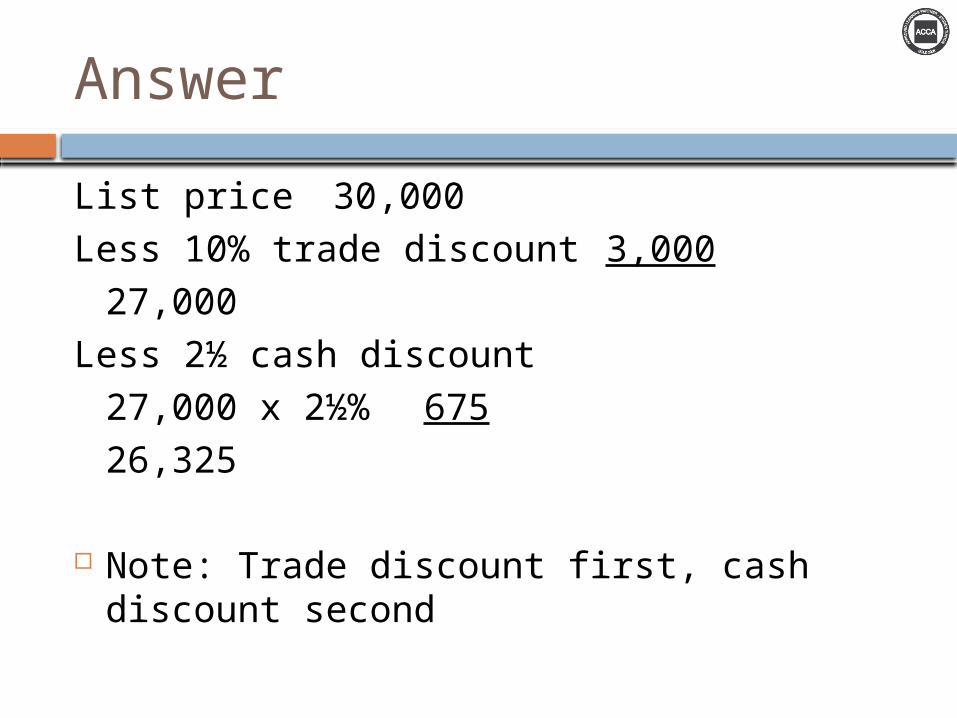

Answer

List price 30,000Less 10% trade discount 3,000

27,000Less 2½ cash discount

27,000 x 2½% 67526,325

Note: Trade discount first, cash discount second

Example

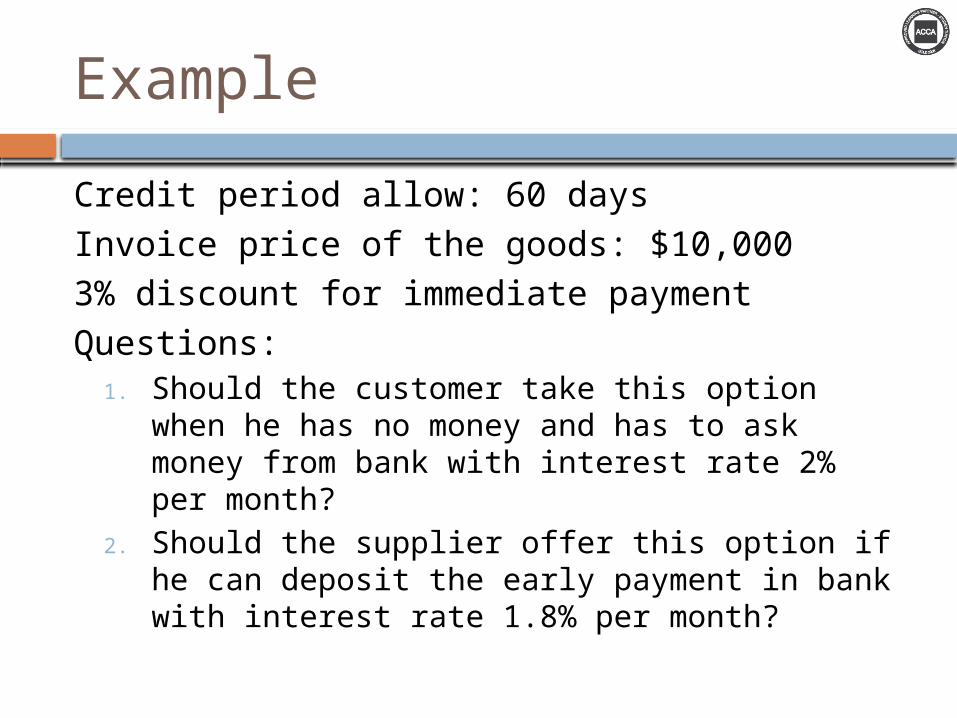

Credit period allow: 60 daysInvoice price of the goods: $10,0003% discount for immediate paymentQuestions:

1. Should the customer take this option when he has no money and has to ask money from bank with interest rate 2% per month?

2. Should the supplier offer this option if he can deposit the early payment in bank with interest rate 1.8% per month?

Answer

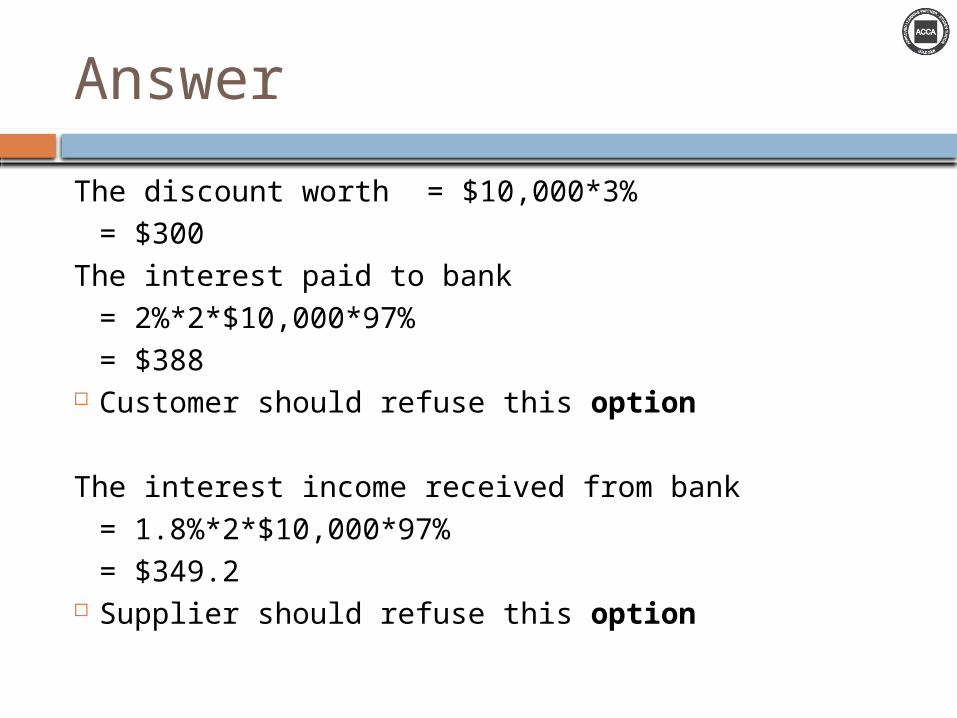

The discount worth = $10,000*3% = $300

The interest paid to bank= 2%*2*$10,000*97%= $388

Customer should refuse this option

The interest income received from bank= 1.8%*2*$10,000*97%= $349.2

Supplier should refuse this option

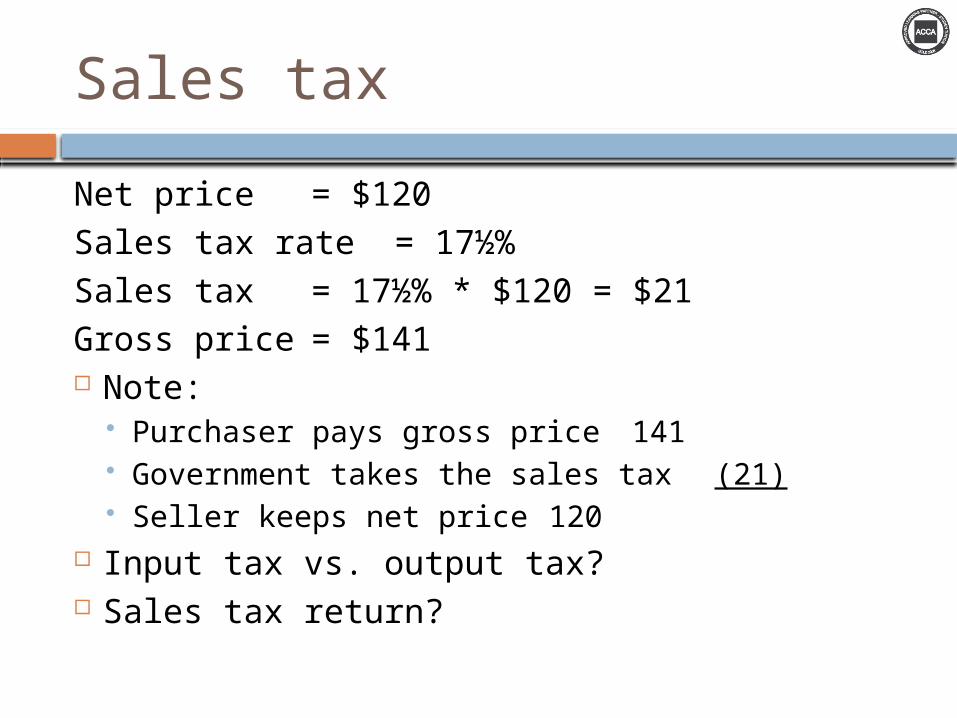

Sales tax

Net price = $120Sales tax rate = 17½% Sales tax = 17½% * $120 = $21Gross price = $141 Note:

Purchaser pays gross price 141 Government takes the sales tax (21) Seller keeps net price 120

Input tax vs. output tax? Sales tax return?

Illustration

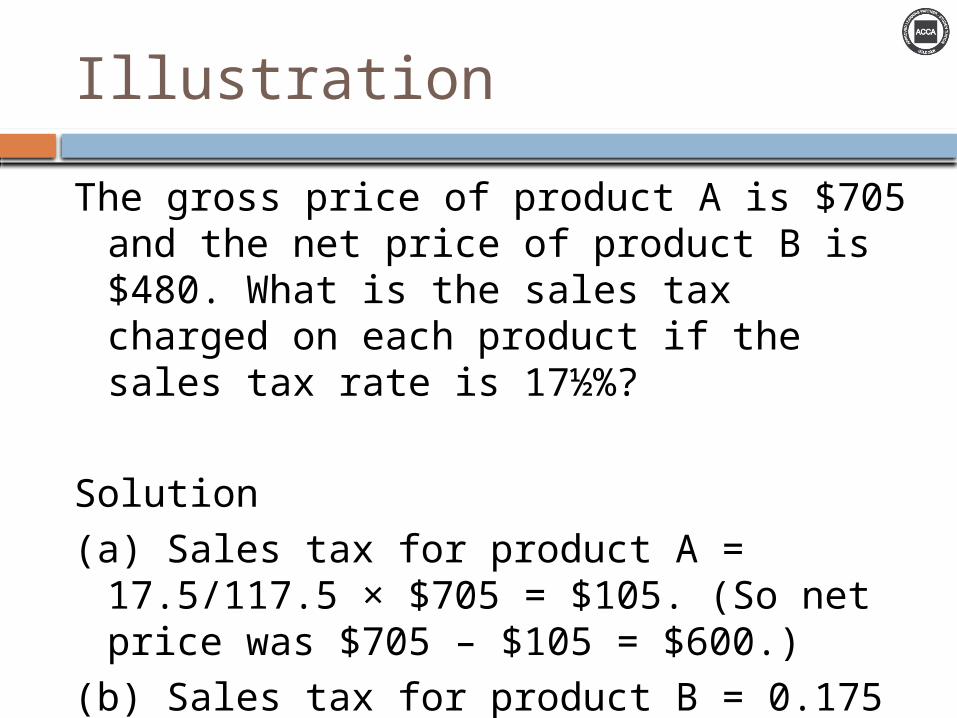

The gross price of product A is $705 and the net price of product B is $480. What is the sales tax charged on each product if the sales tax rate is 17½%?

Solution(a) Sales tax for product A = 17.5/117.5 ×

$705 = $105. (So net price was $705 – $105 = $600.)

(b) Sales tax for product B = 0.175 × $480 = $84. (So gross price was $480 + $84 = $564.)

Question

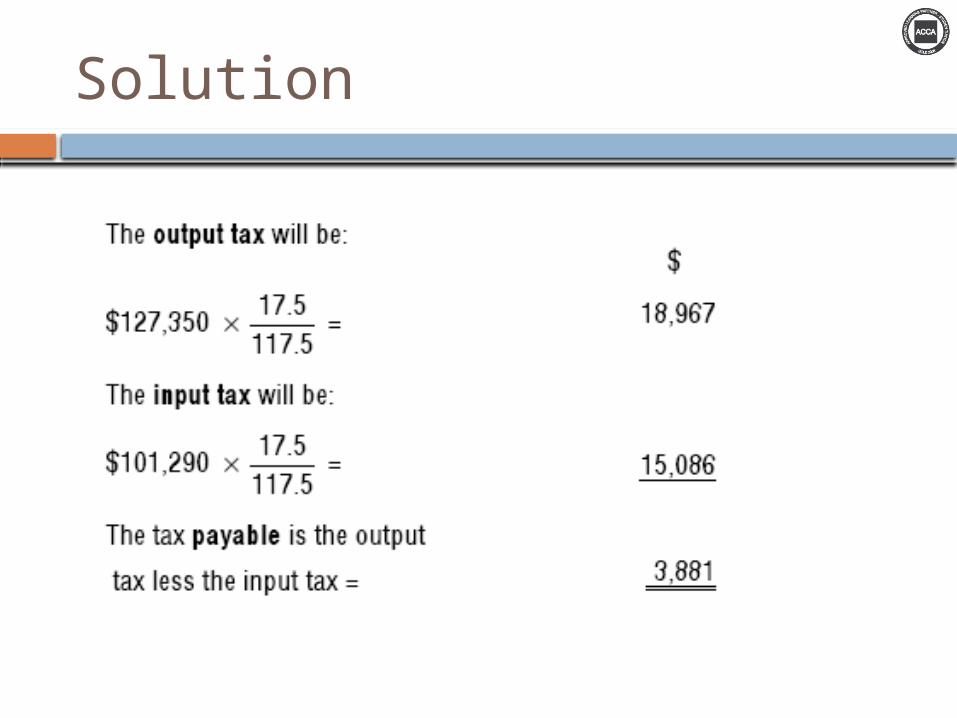

A company sells goods for $127,350 including sales tax at 17 ½% in a quarter. It buys goods for $101,290 including sales tax. What amount will it pay to or receive from the tax authorities for the quarter (round to the nearest $)?

Solution

Example: Discounts and sales taxA company buys goods for sale costing

$6,000. A cash discount of 5% is offered for payment within 10 days. If the sales tax rate is 17½%, what is the sales tax due? Is your answer different if the company pays after 10 days?

Answer

Sales tax is calculated on the discounted price regardless of whether the discount is actually taken.

Home Reading

Contract law - Discussion

Situation 1

You pick up something in a department store which is priced at $24. When the assistant scans it, the price appears as $26.

You tell her that, as it was marked at $24, the store is legally obliged to sell it to you at that price. Are you correct?

No, you are not correct. The price label in the store is an 'invitation to treat' (invitation to make an offer). Your proposal to pay $24 is the offer. There is no acceptance from the store, so no contract has been made.

Situation 2

R bought a car from D, which D had unknowingly bought from a thief. When this was discovered, the car was returned to the true owner. R sued D for the return of the full purchase price (as damages).

The court decided that, although R had used the car for several months, he had not had ownership of it, which is what he had paid for. D therefore had to repay the full amount.

Situation 3

A sells goods to B, who sells them on to C. B then fails to pay A for the goods and disappears without trace. Then how A and C should go on?

If A can demonstrate that he was genuinely mistaken as to the identity of B and would not have dealt with him had he known who B really was, then A can recover the goods which were subject to the original contract from C.

This is because the law takes the view in such a situation that the original contract between A and B was no contract at all. Therefore C, who was an innocent third party acting in good faith, has to return the goods to A and either bear the loss or find and sue B.

Situation 4

A seller advertised a second-hand reaping machine, describing it as new the previous year. The buyer bought it without seeing it. When it arrived he found that it was much more than a year old and rejected it. The seller sued for the price.

It was held that this was a sale by description, the goods had not corresponded to the description, and the buyer was therefore entitled to reject the goods.

Situation 5

Peter buys an electronic keyboard from his local catalogue store. He pays $199 for it. He returns to the store the next day complaining that, although the main keys work, none of the pre-set rhythm buttons seem to function. He demands an immediate refund. The sales assistant refuses to given him a refund or take back the goods, and instead gives him a card with the name and address of the manufacturer, suggesting that Peter contacts them to obtain a refund or a replacement.

Questions: (a) Was the sales assistant legally justified in refusing to give

a refund?NO

(b) Give briefly a reason for your answer.Contracts of sale are between the buyer and the seller

Home Reading

Information and data

Retention policy

Sets down how long different kinds of information are retained Master files and reference files: charter

agreement, legal documents Temporary or transitory files Active files: invoices, GRNs files Non-active file: purchase invoices of

previous years

No long needed info and data Will you throw it away??? Ways to deal:

Microfilmed or microfiched Stored elsewhere (archiving) Securely destroyed

QB 1

1 A trade discount is best described as

A A reduction in the amount of money demanded from a customer

B An optional reduction in the amount of money payable by a customer

C A reduction by the supplier of the amount payable by a customer in return for prompt payment

D An offer by the supplier to reduce the amount demanded on the invoice if certain conditions are fulfilled

Answer: A

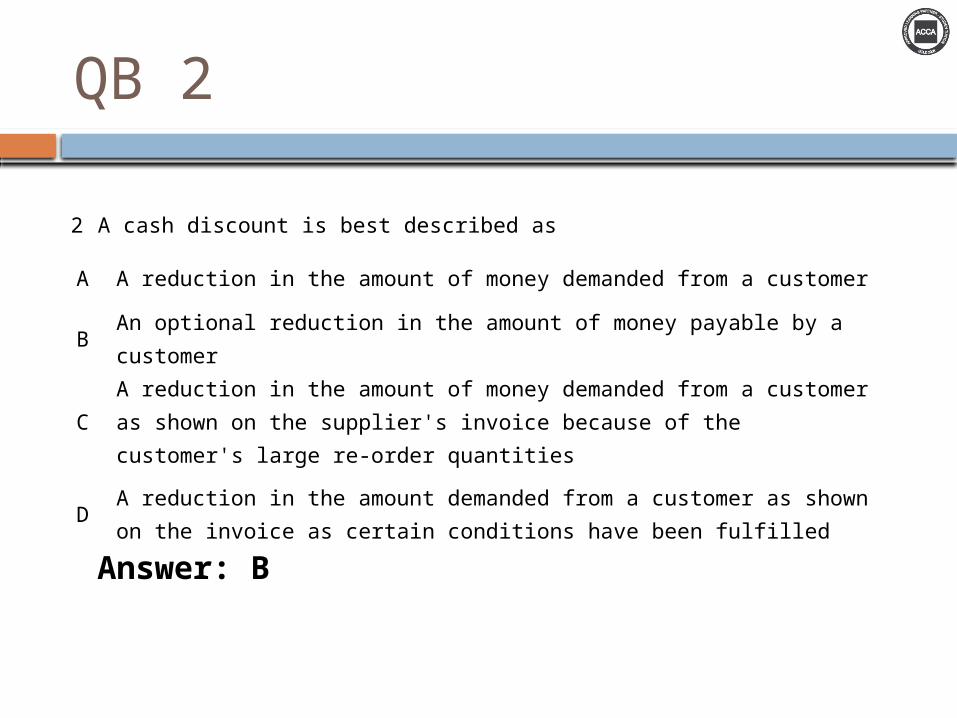

QB 2

2 A cash discount is best described as

A A reduction in the amount of money demanded from a customer

B An optional reduction in the amount of money payable by a customer

C A reduction in the amount of money demanded from a customer as shown on the supplier's invoice because of the customer's large re-order quantities

D A reduction in the amount demanded from a customer as shown on the invoice as certain conditions have been fulfilled

Answer: B