Analyst & InvestorAnalyst & Investor Presentation

LondonLondon4th July 2013

Table of contents

1. Market environment and group positioning p. 5

2 Strategy and equity story p 102. Strategy and equity story p. 10

3. Transport, logistics and freight forwarding activities p.19

4 Group Financials p 334. Group Financials p.33

5. Outlook p.40

6 Appendices p 426. Appendices p.42

DisclaimerThis document was prepared by Norbert Dentressangle for the sole purpose of presenting its situation onJuly 2013. This document may not be reproduced or distributed, in whole or in part, without the prioragreement of the Company. Norbert Dentressangle may not be held liable due to the use of this documentby any person not belonging to the Company. This document does not contain any quantified forecast ofresults. The Company makes no commitment or guarantee that it will meet its objectives or any goal that itmay state in its business plans. While the Company believes that its objectives are reasonable, readers arereminded that said targets are subject to risks and uncertainties, notably as described in the "Risk factors"

ti f th l "D t d Réfé " i t ti d t

2

section of the annual "Document de Référence" registration document.

Norbert Dentressangle a major supply chainNorbert Dentressangle, a major supply-chainmanagement player…

€ 3.9 billiont

3 continentsFrance41%

Spain

Italy4%

NL3,5%

Others *10,5%

* including 2% outside Europe

turnover

26 countriesUK

Spain10%

32,500employees

UK32%

employees

500 sites

7,4006,200,000 m2warehousing

vehicles

...With three main areas of expertise

FREIGHT FORWARDING

LOGISTICS

• €1,783m revenue

• €143m revenue (3%)

(46%)

TRANSPORT

• €2,038m revenue (51%)

4

1. Market Environment and Norbert Dentressangle Group PositioningDentressangle Group Positioning

5

GDP growth in Europe andGDP growth in Europe and evolution of world trade volumes

GDP Growth 2012 2013

Main ND marketsFrance 0,0% -0,1%

10,8%7,7%

9,2% 8,0%

3,1%

12,5%

6,0%

2 5% 3,6%5%

10%

15%

France 0,0% 0,1%United Kingdom 0,2% 0,7%Spain -1,4% -1,6%Italy -2,4% -1,5%Netherlands -0,9% -0,5%

2,6% 2,3% 3,6% 3,4%0,5%

‐4,2% 2,0% 1,6%‐0,2% 0,0%

2,5%

‐5%

0%

5%

Eastern & Central Europe 1,6% 2,2%

European Union -0,2% 0,0%World 3,2% 3,3%

‐10,6%‐15%

‐10%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

GDP Growth ‐ European Union Trade Volumes ‐World

• Further economic slowdown experienced in 2012 after two years of relative recovery

Source : International Monetary Fund

• Advanced economies are particularly impacted by flat growth or recession. With Germany, the United Kingdom appears as an exception in Western Europe

• A slight recovery is forecast in 2013, primarily over the second half of the year, but no sustainable growth is anticipated before 2014growth is anticipated before 2014

6

The European Road Freight market is largeThe European Road Freight market is large and highly fragmented

MARKET SIZE & TRENDS MARKET FRAGMENTATION

European market size: €292 billion European market concentration

France € 35 billion 12%

UK € 32 billion 11%

€ m 2012 Share EBITA%

DB Schenker 6 366 2,2% 2,2%DHL 4 192 1,4% 1,4%DSV 2 816 1,0% 4,5%

Spain € 30 billion 10%

Market dynamics (value growth)

Dachser 2 661 0,9% n.c.Kuehne Nagel 2 618 0,9% 0,3%N Dentressangle 2 038 0,7% 3,0%

3,6%4,2%

2,5%3,0%

4,0%

5,0% EuropeFrance / UK / Spain

Market dynamics (value growth)• The road freight market in Europe

offers significant room for growth

• France, UK and Spain (ND main markets) represent a global value of

1,4%

1,4% 1,5%

0,7%

1,9%

0,0%

1,0%

2,0%markets) represent a global value of €97 billion

• Norbert Dentressangle operates the #1 European owned fleet, a key

2010 2011 2012 2012‐15 CAGR

7Source : Transport Intelligence

p , ydifferentiator providing better pricing power

The European Contract LogisticsThe European Contract Logistics market is undergoing consolidation

MARKET SIZE & TRENDS

European market size: € 60 b . 31% outsourced

MARKET FRAGMENTATION

European market concentration

€ 2012 Sh EBITA%UK € 15 billion 49% outsourced

France € 8 billion 26% outsourced

€ m 2012 Share EBITA%

DHL 7 434 12,5% 2,9%Kuehne Nagel 2 313 3,9% 1,9%CEVA 2 167 3,6% n.c.

Market dynamics (value growth)

Italy € 4 billion 20% outsourced

Netherlands € 4 billion 19% outsourced

N Dentressangle 1 783 3,0% 4,5%Fiege 1 610 2,7% n.c.Rhenus 1 553 2,6% n.c.

Market dynamics (value growth)

7,1%

3,7% 3,9%6,0%

8,0% EuropeMain ND markets

• The contract logistics market in Europe is undergoing consolidation, particularly in Western Europe

The UK France Italy and the ,

1,4%

5,3%

2,9%

1,0%

3,4%

0,0%

2,0%

4,0% • The UK, France, Italy and the Netherlands (ND largest markets) represent a global value of € 31 billion

• Norbert Dentressangle is a first-class 2010 2011 2012 2012‐16 CAGR

8Source : Transport Intelligence

gplayer in the market, delivering strong profitability

Apart from a few leading players global Air &Apart from a few leading players, global Air & Sea Freight markets are highly fragmented

AIR & SEA FREIGHT

Global market size: € 122 billion

MARKET FRAGMENTATION

Global market concentration

China € 13 billion 11%

USA € 25 billion 21%

Worldwide TOP 6 players* represent a 32% market share in 2012.*:CEVA, DB Schenker, DHL, Kuehne Nagel Panalpina and

UK € 5 billion 4%

Market dynamics (volume growth)

France € 4 billion 3%

Kuehne Nagel, Panalpina, and Sinotrans

Market dynamics (volume growth)• Both air & sea freight forwarding

markets are dominated by a limited number of major players

Behind these major players the freight 16,5% 6,7%

3,6%

18,5%

15%

25% Seafreight vol. (TEUs)Airfreight vol. (tons)

LTM year‐on‐year growth

• Behind these major players, the freight forwarding market is highly fragmented, with many niche players

• The US, China, UK and France, (our ‐11,7%

‐6,8%

‐3,4% ‐1,2%

‐15%

‐5%

5%

9Source : Transport Intelligence

, , , (main markets) represent a value of €47 billion

,Dec‐09 Jun‐10 Dec‐10 Jun‐11 Dec‐11 Jun‐12 Dec‐12

2. Strategy and Equity Story2. Strategy and Equity Story

10

Our ambition: to become a top tier playerOur ambition: to become a top-tier player in supply chain management

Geographic Scale Service offeringpresence Scale Service offering

S ti li t I i dibilit C bi i i & • Supporting our clients wherever they operate and moving with them whenever they need us

• Increasing our credibility to become the go-to “supply chain management expert” of

• Combining organic & external growth to acquire and expand our areas of expertisewhenever they need us management expert of

choice

• Always striving to increase our critical

areas of expertise

• Developing and expanding our range of services & solutionsincrease our critical

mass in our choosenmarkets

services & solutions

11

34 years of growthTDG (UK)

Christian SalvesenSchneider Log. (USA)

Turnover :$30m

Turnover : £700mTransport, Logistics &

Freight Fwding

Turnover

3 5763 880

16%

18%

20%

3 500

4 000

Christian Salvesen(UK)

Turnover : €1.3bnTransport & Logistics

Turnover :$30mFreight Fwding28 acquisitions

Transport & LogisticsMainly in France

TurnoverIn €M Organic growth

3 107

2 719 2 839

3 576

10%

12%

14%

16%

2 000

2 500

3 000

APC (China)Turnover : €50mF i ht F di

9 0% 8 6% 10 4% 7 0% 4 8% 5 7% 5 8% 5 3% 5 5% 8 1% 4 3% 3 4% 5 6% 0 0%647 744 838 972 1 0531 222 1 303 1 399

1 6081 804

2%

4%

6%

8%

500

1 000

1 500Freight Fwding

9,0% 8,6% 10,4% 7,0% 4,8% 5,7% 5,8% 5,3% 5,5% 8,1% 4,3% 3,4% 5,6% 0,0%6470%0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Organic growth Turnover

12

1979: Opening of the first company to support international Transport between Europe and the UK

1994: A family group listed on the Paris stock exchange

34 years of geographic and34 years of geographic and business transformation

Turnover breakdown by expertiseTRANSPORT LOGISTICS FREIGHT FORWARDING

2012 turnover breakdown

FREIGHT FORWARDING

Turnover breakdown by geographic areaFRANCEOUTSIDE FRANCE

France41%

S i

Italy4%

NL3,5%

Others *10,5%

UK

Spain10%

UK32%

19982010Launch of a third area of

2012Revenue: €3.9 billionOperations in 26 countries

2007Norbert Dentressangle doubles in size with

* including 2% outside Europe

998Integration of a second area of expertise: Logistics

third area of expertise: Freight Forwarding

32,500 employees worldwide doubles in size with the acquisition of British company Christian Salvesen

13

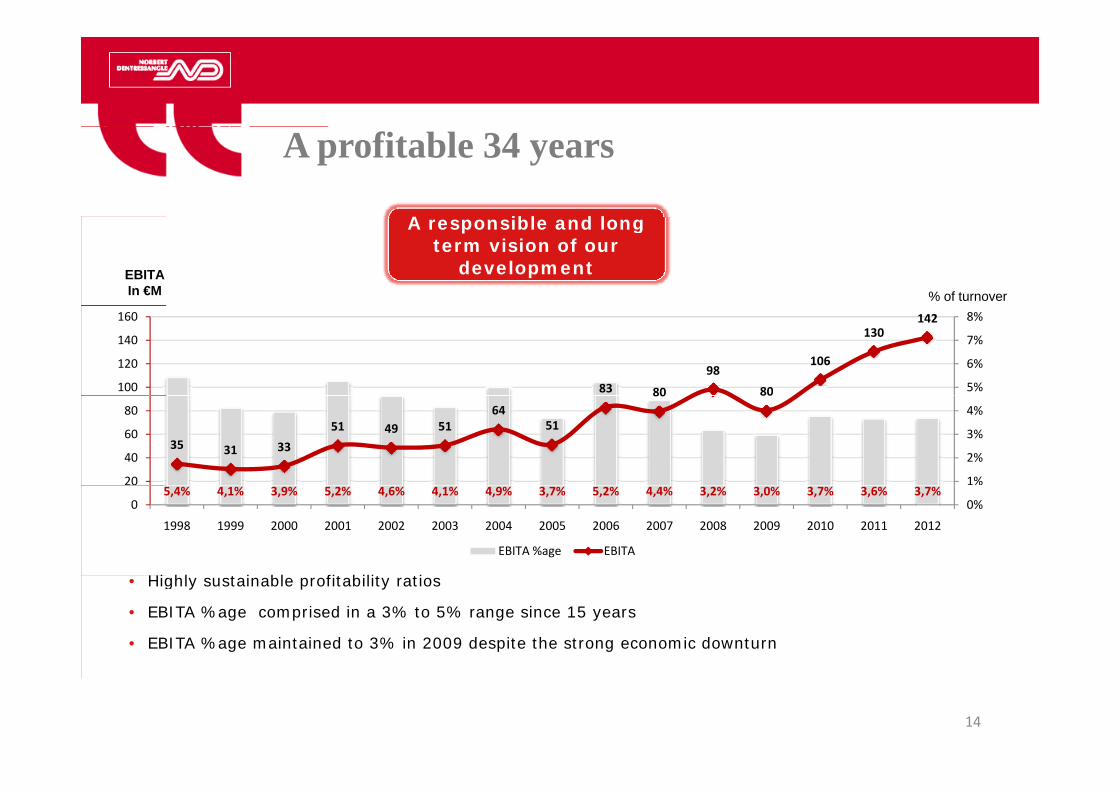

A profitable 34 years

A ibl d l A responsible and long term vision of our

developmentEBITAIn €M % of turnover

83 80

98

80

106

130142

5%

6%

7%

8%

100

120

140

160

35 31 3351 49 51

6451

80 80

1%

2%

3%

4%

20

40

60

80

5,4% 4,1% 3,9% 5,2% 4,6% 4,1% 4,9% 3,7% 5,2% 4,4% 3,2% 3,0% 3,7% 3,6% 3,7%0%0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

EBITA %age EBITA

Hi hl t i bl fit bilit ti• Highly sustainable profitability ratios

• EBITA %age comprised in a 3% to 5% range since 15 years

• EBITA %age maintained to 3% in 2009 despite the strong economic downturn

14

A strong and diversified customer base

RetailHousehold

Textile2% Paper

2%

High Tech2%

Luxury1%

• Very well balanced client portfolio

• #1 customer< 4% of turnoverRetail18%

Other7%

Metal3%

3%• Top 10 < 20% of turnover

• Very low exposure to specific customer / sector / end-market risks

Food14%

Special t il

Construct.5%

• Key customers are both leading and innovative players in their own markets

Industry11%

FMCG7%

retail7%

Top 10

Chemical10%

Auto8%

7%

15

A rigorous management structure

90%100%

T t t t t

Strict cost controls% of turnover

27% 26% 26% 25% 26% 24% 21% 24% 22% 22%

25% 26% 28% 32% 32% 32% 34% 37% 40% 41%

40%50%60%70%80%90%

Other (overheads, etc.)

Subcontracting & disbursements

Transport cost structure 2003-2012

35% 34% 34% 33% 31% 32% 33% 31% 29% 29%

24% 21% 24% 22% 22%

0%10%20%30%40% Vehicle costs, including fuel

Personnel expenses

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

16% 18% 17% 16% 15% 18% 16% 16% 17% 18%80%90%

100%

Logistics cost structure 2003-2012

% of turnover

29% 28% 28% 29% 30% 21% 23% 24% 22% 22%

30%40%50%60%70%

Other (overheads, etc.)

Subcontracting & transport

Rental costs

l

16

45% 44% 45% 45% 46% 50% 51% 52% 50% 52%

0%10%20%30%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Personnel expenses

A robust governance

• The benefits from a family owned company and a managerial organisation

• A supervisory board:DISTRIBUTION OF CAPITAL

A supervisory board:

• 10 Directors of which 6 are independent Directors

A di i

• 30% PUBLIC

• An audit committee

• A European Executive Board

EXECUTIVE BOARD

From left to right:

M l l WilMalcolm WilsonLogistics Division MD

Hervé MontjotinCEO

Patrick BataillardCFO

• 68% DENTRESSANGLE INITIATIVES + FAMILY

17

CFO

Luis Angel GomezTransport Division MD

INITIATIVES + FAMILY

People engagement: developing the Norbert Dentressangle way

• A decentralised and flat organisation to keep our entrepreneurial spirit and business agilityp p g y

• A specific commitment towards people: “you grow, we grow”grow, we grow– Priority to internal promotion: 60% of managers are

promoted internally

• The benefits of a strong Franco-British culture and experience

• Expertise in integrating businesses and staff– Local HR expertise

Accumulated experience through acquisitions

18

– Accumulated experience through acquisitions

3. Transport, Logistics and Freight Forwarding activitiesForwarding activities

19

Transport businessMarket conditions and our response

• A highly fragmented market

• Important room for growth in Europe

• Network scale is key for sales development and competitiveness

E t ti f f i dl t t l ti• Expectations for eco-friendly transport solutions

• Develop value added transport service offerings• Develop value-added transport service offerings

• Grow in Europe

• Expand network to remain competitive

• Commit to reducing carbon footprint and road accidents through continuous improvement and innovation

20

Transport by Norbert Dentressangle

A major European player with robust and mature operations in France, United Kingdom and Spain, and with an improved network coverage and increased presence in Central and Eastern Europe

• €2,038m revenue (51%)

• €60.4m EBITA

• 13,560 employees

• 171 sites in 13 countries171 sites in 13 countries

• #1 vehicle fleet in Europe with 7,400 tractor units

E ' l t hi l fl t• Europe's cleanest vehicle fleet• 95% EURO IV & V. 95% Euro IV & V

• Each driver runs an average 620,000

21

kms without causing accidents

Focus on the development of value-added B2B service offerings

Norbert Dentressangle 4PL model: Key PL®

€185m

InternationalFTL &

Cross-Channel€510m*

DomesticPallet

Distribution€504m*

InternationalGroupage &

PalletDistribution

€132m*

DomesticFTL

€500m*

DedicatedFleet

€330m*€132m*

CO2 emissions declaration (carbon calculator attested by Bureau Veritas)

* FY 2012 / To be added: €62m of warehouse storage associated with transport services

22

Diff ti ti th hDifferentiation through innovative solutions

• Delivering daily to 100 stores in Paris City centre via the Seine

• 37% reduction in CO2 emissions• 3,900 vehicles on average per year• 450,000 km on the road on average per year

234 tonnes of CO on average per year

Bourdonnais Port

• 234 tonnes of CO2 on average per year

Chennevières‐sur‐MarneLoading of goods on pallets into swap bodies

Bourdonnais PortUnloading of containers and shipments of

goods in the Franprix networkFor Franprix, a river/road transport solution

(containers)Bonneuil‐sur‐Marne PortLoading of full containers onto the barge

Each day:• 1 barge

• 26 containers of goodsg• 450 pallets

23

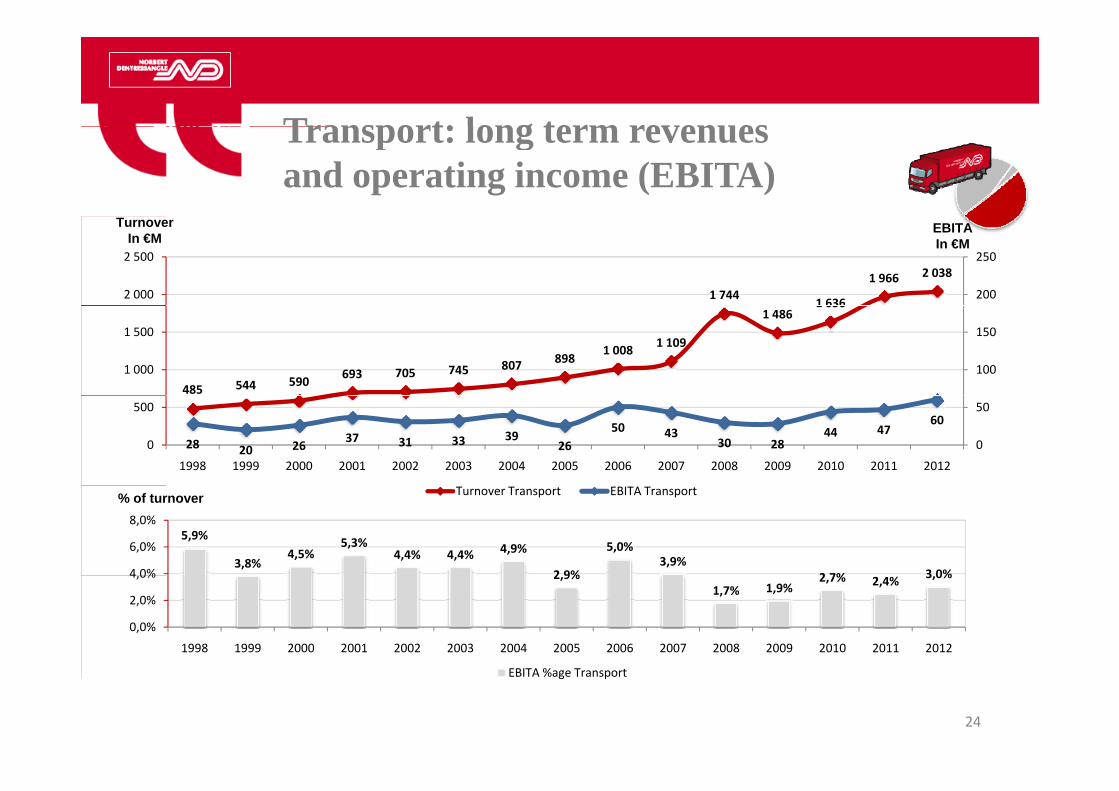

Transport: long term revenuesTransport: long term revenues and operating income (EBITA)

1 744 1 636

1 966 2 038

200

250

2 000

2 500

EBITAIn €M

TurnoverIn €M

485 544 590 693 705 745 807 898 1 008 1 109

1 4861 636

100

150

1 000

1 500

28 20 26 37 31 33 3926

50 4330 28

44 4760

0

50

0

500

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Turnover Transport EBITA Transport

5,9%

3,8%4,5%

5,3%4,4% 4,4% 4,9%

2 9%

5,0%3,9%

2 7% 3 0%4 0%

6,0%

8,0%

% of turnover

2,9%1,7% 1,9%

2,7% 2,4% 3,0%

0,0%

2,0%

4,0%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

24

EBITA %age Transport

Logistics businessMarket conditions and our response

• Few European players• Few European players

• Business is 100% contracted

• Retail and FMCG sectors are key commercial targets

• Profitability and international expansion make the difference

E l i i i b d E• Export logistics expertise beyond Europe

• Raise international profile

• Accompany blue-chip customers in their global developmentAccompany blue chip customers in their global development

• Strengthen expertise in Retail and FMCG sectors

• Ensure efficiency of the operations

25

Logistics by Norbert Dentressangle

One of the few European players with an increasing international profile

• €1 783m revenue (46%)

(UK represents now 42% of the total sales)

• €1,783m revenue (46%)

• €77.9m EBITA

• 18,250 employees

• 256 sites in 14 countries

• Total warehouse surface area of 6 2m sq meters6.2m sq. meters

• Temperature Controlled volume of 3.9m m3

€3 0

26

• €370 m turnover

Logistics: mastery of key logisticsLogistics: mastery of key logistics skills throughout Europe

Ambient and temperature-controlled logisticsGlobal and industry solutions

Value-added servicesWarehousing

and inventory management

€480m

Downstream transport

management€465m

Order preparation

€660m

services€178m

Of which €200m of turnover in e-Commerce

The highest safety and quality standardsService: ISO 9001 – Food safety: ISO 22000 & HACCP

27

Service: ISO 9001 – Food safety: ISO 22000 & HACCPStaff safety: ISO 18001 – Safety of medical devices: ISO 13845

S l ff t th l tScale effect, a growth accelerator: UK logistics case study

700£14m pa £8m pa

£25m pa

Major High Street Retailer

600

500400

363£6m pan

£ M

£25m pa

£13m pa

£14m pa

300200

1000

363 351332

549

643

£9m pap

even

ue

in

02008

20092010

2011

700

An

nu

al r

e

• Acquisition of 2011

2012

2013

A qChristian Salvesen– Integration into

the Norbert Dentressangle

– Renewed expansion and growth in new services

• Acquisition of TDG

New critical size– Access to new

clientsDentressangle culture

services– E-commerce

– New critical size– New skills

clients– Strong internal

growth

28

Logistics: long term revenues andLogistics: long term revenues and operating income (EBITA)

1 3641 233 1 239

1 5891 783

150

175

200

1 500

1 750

2 000

EBITAIn €M

TurnoverIn €M

279 348477 497 502

600 648

1 233 1 239

81 78 50

75

100

125

150

500

750

1 000

1 250

1 500

162 199 249 279 348

6 8 11 14 18 18 25 25 33 3749 52

6378

0

25

50

0

250

500

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Turnover Logistics EBITA Logistics

3,9% 4,0% 4,5%5,1% 5,1%

3,8%5,1% 5,0% 5,5% 5,7%

3,6%4,2%

5,1% 5,1%4,4%

4 0%

6,0%

8,0%% of turnover

0,0%

2,0%

4,0%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

EBITA %age Logistics

29

Freight forwarding businessMarket conditions and our response

• Few large players and many small ones• Few large players and many small ones

• Integrated global network / niche players

• Expand international freight forwarding network

G i i i l k d l• Gain critical mass on key trade lanes

• We walk the talk

• Scalable businessScalable business

• Break-even position

30

Freight forwarding by Norbert Dentressangleg

• Launched from scratch in 2010

• €143m revenue (3%)

• €1.0m EBITA€1.0m EBITA

• 600 employees

• 54 offices in 14 countries

• 22,000 airfreight volumes in tons and 60,000 sea-freight volumes in TEUs in 2012

,• More than 90,000 files

31

Freight forwarding: revenues and operating income (EBITA)

86

1433

4

150

200

EBITAIn €M

TurnoverIn €M

12

86

01

‐1

0

1

2

0

50

100

‐1

‐3

‐2

‐100

‐50

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0,3% 0,7%0%

4%

Turnover Overseas EBITA Overseas% of turnover

‐6,7%‐8%

‐4%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

32

EBITA %age Overseas

4. Group Financials4. Group Financials

33

Consolidated income statementConsolidated income statement and contribution by division

In €mTransport Logistics Freight

Fwding

Group31-Dec

2012

Group31-Dec

2011

Revenue * 1,961 1,772 139 3,880 3,576

EBITDA - - - 244.8 252.3

+8.5%

Operating profit before goodwill (EBITA)

60.43.1%

77.94.4%

1.00.7%

142.33.7%

130.43.6%

EBIT - - - 130.13.4%

124.63.5%

+9.1%

Net financial expensesCorporate income taxCVAEAssociates

- - -

(26.3)(15.1)(13.2)

0.0

(25.4)(22.2)(13.1)

0.2AssociatesMinority interests 0.8 0.7

Net income - - - 74.71.9%

63.31.8% +18%

34

* Breakdown by Division is net of intercompany revenueRevenue in 2012 includes €8m generated at the Dagenham site disposed of in October 2012 (€2.9m at direct operating margin level)

Simplified consolidated balance sheet

GOODWILL & INTANGIBLE 660m€• Goodwill 549m€

• Intangible incl. customer relation 111m€

EQUITY 575m€

PROVISIONS & OTHERS 229m€

TANGIBLE & OTHER NON CURRENT

ASSETS 670m€

WORKING CAPITAL 37m€

ASSETS 670m€• Tangible fixed assets 586m€

• Other fixed and non current assets 86m€NET FINANCIAL DEBT 489m€

35

Long Term consolidated cashLong-Term consolidated cash flow statement (5 years)In €m Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Cash flowChange in operating WCR - - -

223(28)(13)

21742

(11)UK pension fund financing (13) (11)

Net cash flow from operations 110 205 183 182 247

CAPEX (net of disposals)Sales of warehouses and sites - - -

(122)30

(93)23Sales of warehouses and sites

Acquisition of securities less acquired cash30

(288)23

(3)

Net cash flow from investment activities (91) (64) (86) (380) (73)

Free Cash Flow (before external growth) 21 141 103 90 178

DividendsRemaining amount of financing operationsRepurchase of own shares

- - -(11)176(6)

(12)(70)

(3)

Net cash from financing transactions (133) (38) (43) 159 (85)g ( ) ( ) ( ) ( )

Forex impact - - - - 1

Change in cash (110) 104 55 (39) 90

Cash available at period end 37 141 196 157 247

36

p

Medium term historical trendsMedium-term historical trendsKey financial indicators

11,0% 11,3%

14,9%

12,0% 11,7% 1 500

2 000

15%

20%

9880

106

130 142

6%

8%

120

160

Strong profitability Resilient business model€M €M

894 709 714 1 089 1 2140

500

1 000

0%

5%

10%

3,2% 3,0% 3,7% 3,6% 3,7%

80

0%

2%

4%

0

40

80

00%

2008 2009 2010 2011 2012Capital Employed ‐ avg ROCE

0%0

2008 2009 2010 2011 2012EBITA %age EBITA

Tight capex monitoring Working capital structurally negative €M€M

2,9%2,4%

2,8%2,6%

1,8%60

90

120

2%

3%

4%

‐1721

‐1,4%

‐0,6% ‐0,9%‐0,6%

‐0,9%‐20

‐10

0

‐2%

‐1%

0%

g p g g p y g €M€M

89 64 80 92 710

30

60

0%

1%

2%

2008 2009 2010 2011 2012

‐44

‐25‐21

‐37

‐50

‐40

‐30

‐5%

‐4%

‐3%

2008 2009 2010 2011 2012

37

2008 2009 2010 2011 2012Capex Capex %age

2008 2009 2010 2011 2012Net Working Capital NWC Intensity (turnover %age)

Consolidated net financial debtConsolidated net financial debt and projected amortisation

In €mGroup

31-Dec-12Group

31-Dec-11

Acquisition debtRevolving facility (€150m available)

24295

27795Revolving facility (€150m available)

Asset financingProfit-sharing (classified as other financial liabilities in 2012)

95398

-

95401

9

GROSS FINANCIAL DEBT 736 781

CASH & CASH EQUIVALENTS 247 157

NET FINANCIAL DEBT 489 624

355

42

3075

75500600700800

Private placement

Asset financing £

81 66 51

256 232 203

275185

102

19

10

75

75

0100200300400

Asset financing £

Asset financing €

Syndicated loan £

Syndicated loan €

38

81 66 51 1020

31‐Dec‐12 31‐Dec‐13 31‐Dec‐14 31‐Dec‐15

Strong financial resources to support ourStrong financial resources to support our development projects

Acquisition Acquisition

AcquisitionTDG

APC BeijingAcquisition

TNT LogisticsVenditelli

AcquisitionUTL

3,5 x

700

800

3 5 x

4,0 x

cqu s t oChristian Salvesen

AcquisitionNova NatieJohn Keells

AcquisitionStockalliance

Seroul

€M

1,6 x 1 6 x

2,8 x

2,3 x

1,8 x

2,5 x

2,0 x400

500

600

700

2,0 x

2,5 x

3,0 x

3,5 x

1,6 x 1,6 x1,3 x

0,4 x

1,0 x

0,5 x

1,3 x 1,4 x

0,8 x

100

200

300

0,5 x

1,0 x

1,5 x

,

76 80 69 31 74 43 165 159 121 533 553 445 382 624 4890

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0,0 x

Net financial debt Leverage ratio

39

g

5. Outlook5. Outlook

40

To remain a top tier player in globalTo remain a top-tier player in global supply chain management

There is room for doubling the size of the company

TRANSPORT• Consolidating our market position in Europe (especially in

pallet network)

• Raising our European 4PL profileg p p

• Being scalable in our key European countries

LOGISTICS• Going global

• Non European targeted countries / Accompanying key customers into new markets/geographies

FREIGHT FORWARDING

• Consolidating our market position after 3 years of targeted acquisitions

Fo on kill p o e nd bottom line

41

FORWARDING p g

• Focus on skills, process and bottom line

• Developing current trade lanes

6. Appendices6. Appendices

42

Consolidated turnover in Q1 2013Consolidated turnover in Q1.2013Breakdown by activity

Transport Q1.13 Q1.12 Change LfL **In €m

Transport Q1.13 Q1.12 Change LfL

Transport 500 522 -4.1% -3.7%

Logistics 436 422 +3.4% +2.3%

Freight Forwarding 33 32 +1.4% -8.7%

Inter-divisions (20) (17) * n.a. n.a.

Consolidated TURNOVER 949 958 -1.0% -1.3%

* Including Dagenham business, sold in October 2012** Percentage change at a constant scope and exchange rate

43

g g p g

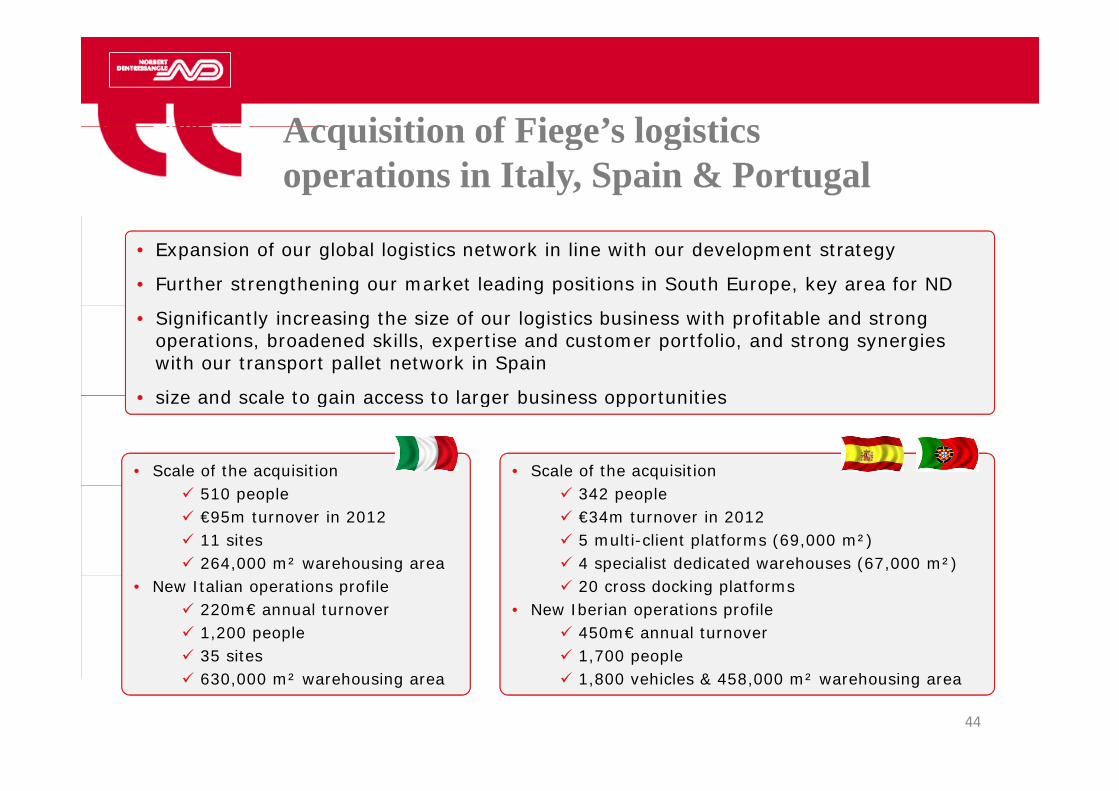

Acquisition of Fiege’s logisticsAcquisition of Fiege’s logistics operations in Italy, Spain & Portugal

• Expansion of our global logistics network in line with our development strategy

• Further strengthening our market leading positions in South Europe, key area for ND

• Significantly increasing the size of our logistics business with profitable and strong operations, broadened skills, expertise and customer portfolio, and strong synergies with our transport pallet network in Spain

• size and scale to gain access to larger business opportunities• size and scale to gain access to larger business opportunities

• Scale of the acquisition • Scale of the acquisition 510 people €95m turnover in 2012 11 sites 264,000 m² warehousing area

342 people €34m turnover in 2012 5 multi-client platforms (69,000 m²) 4 specialist dedicated warehouses (67,000 m²)

• New Italian operations profile 220m€ annual turnover 1,200 people 35 sites

20 cross docking platforms • New Iberian operations profile

450m€ annual turnover 1,700 people

44

630,000 m² warehousing area 1,800 vehicles & 458,000 m² warehousing area

Analyst & InvestorAnalyst & Investor Presentation

LondonLondon4th July 2013