Download - 141125 Madrid Speech

In the 40

bulk of e

shifted p

One thin

calm.

Because

reassurin

exports.

shortfall

Similarly

coming y

not to ta

There ha

number

United S

Sp

0 years since

energy dema

priorities, and

ng that has no

even for oi

ng. Markets

But the ris

. This may no

y, although g

years, geopo

ake steps to r

as also been

of recent po

States or the

pain, Euro

the IEA was

and, the thr

d LNG is rew

ot changed i

l, markets to

are surely c

k remains th

ot happen to

as supply is l

olitics is also

reduce relian

n positive ne

olicy efforts t

2030 frame

©

ope and th

established,

reat of clima

riting the glo

s the need fo

oday seem w

comforted th

hat long ter

oday, or tomo

likewise amp

creating un

nce on future

ws in terms

hat can help

work for ene

© OECD/IEA 2

he World:

, much has c

ate change a

obal gas land

or vigilance a

well-supplied

hat the turm

rm, instabilit

orrow, but is

ple and set to

certainty. De

e gas supply f

of climate c

p reduce CO2

ergy and clim

2014

The Geop

IEA ExecuCenter f

hanged. Eme

and the grow

scape.

and prepared

d, and prices

moil in Iraq h

ty will deter

s a possibility

o be reinforc

ebate in Eur

from Russia.

change and

2 emissions, s

mate in the E

politics of

tive Directorfor Global Ec

erging econo

wth of renew

dness, even i

are reflecti

has not disru

investment

y down the ro

ced by a new

ope has reig

the environm

such as the C

European Un

Energy

r Maria van donomy and GESADE Busin

25 Nove

omies now m

wable techno

n the case of

ng this supp

upted the co

, resulting in

oad.

w wave of LN

gnited over w

ment. We ha

Clean Power

ion. And of c

der HoevenGeopoliticsness School

Madridmber 2014

make up the

ologies has

f supposed

ply – this is

ountry’s oil

n a supply

G over the

whether or

ave seen a

Plan in the

course just

recently

together

emission

Indeed s

we know

To answ

Here in S

generate

news. W

But as w

When th

the syst

share of

Howeve

flexibility

likewise

gas capa

the United

r on reducin

ns, rising 2.6

some degree

w today, and

er that quest

Spain, your c

ed a full qua

With the EU ta

with all things

he sun doesn

em stands t

renewables.

r adding add

y dramatical

Spain could

acity. This cou

States and

g emissions.

percent ove

of uncertain

how can tha

tion, perhaps

country is ta

arter of its e

arget of 27%

s, it is not so

’t shine, or t

today, conve

.

ditional grid

lly. Excess p

import pow

uld in turn re

©

China have

. That said,

r 2012.

nty underlies

at help us to

s it is best to

king full adv

lectricity thr

renewable e

simple.

he wind doe

entional gen

interconnec

power from

wer when the

educe the vo

© OECD/IEA 2

signaled to

2013 was ye

s all discussio

prepare for t

o start at hom

antage of th

rough wind a

energy by 20

esn’t blow, th

eration capa

ctions with F

Spain’s rene

ere is less wi

latility of wh

2014

the world t

et another r

ons of energy

tomorrow?

me.

he promise o

and solar. On

30, Spain is a

hen alternativ

acity will be

rance, and t

ewables cou

nd and sun,

olesale elect

that they ar

ecord year i

y security. Th

f renewable

n its face, th

already well-

ve power so

needed to

the rest of E

uld be fed a

rather than

tricity prices.

re ready to

n terms of g

he question i

energy. In 2

his is nothing

-positioned.

urces are ne

complemen

Europe, woul

cross the bo

maintaining

.

take steps

global CO2

is, what do

2013, Spain

g but good

cessary. As

t this high

ld increase

order, and

g expensive

From th

Spain an

make th

And so f

Here it is

In this co

the Brot

not lead

complian

But ther

potentia

half. A k

account

dispropo

taking ad

But whil

of gas su

on impo

e perspectiv

nd Europe w

is happen is t

from Spain, w

s concerns ab

ontext Ukrai

therhood pip

to an interr

nce with the

re are reason

al interruptio

key reason f

for an inc

ortionate sha

dvantage of t

e, under the

upply, it cann

rts.

ve of both en

would be a p

the challeng

we take a ste

bout security

ine is extrem

peline. Contr

ruption of tr

Energy Char

ns to believe

ns to supply

for this is th

reasing sha

are of unde

this capacity

e right circum

not transform

©

nergy securit

ositive deve

e.

ep back and

y of gas supp

mely importa

rary to wides

ransit. The U

rter Treaty.

e that gas m

than they ar

e rise in LN

re in the g

erutilised LNG

a challenge.

mstances, LN

m over the lo

© OECD/IEA 2

ty, and clima

lopment for

look at Euro

ply that are m

ant: roughly

spread expe

Ukrainians ha

markets will

re today – ev

G, which alm

gas traded

G capacity,

.

NG trade can

ong term the

2014

ate goals, in

r everyone. F

ope as a cont

making headl

15 percent o

ctations, the

ave acted wi

be better eq

ven as global

most double

between re

though wea

help to brin

competitive

creased inte

Finding an in

tinent.

ines.

of European

e Russian shu

th remarkab

quipped in t

demand for

es in terms o

gions. Spain

ak pipeline i

ng back confi

positive of g

erconnection

nvestment st

gas supplie

utdown of U

ble self-restra

he future to

r gas rises by

of volume b

n and Portu

interconnect

idence in the

gas in marke

ns between

tructure to

s arrive on

Ukraine did

aint, in full

o deal with

more than

by 2040, to

ugal has a

tions make

e reliability

ts that rely

Here we

Because

markets

LNG sim

There ar

transpor

always h

If Asia re

unconve

for gas in

From Eu

And glob

different

developi

In OECD

mirrorin

energy is

e step even fu

moving gas

will not swin

ply cannot b

re no prospe

rting gas wil

have relativel

eally wants c

entional reso

n the region.

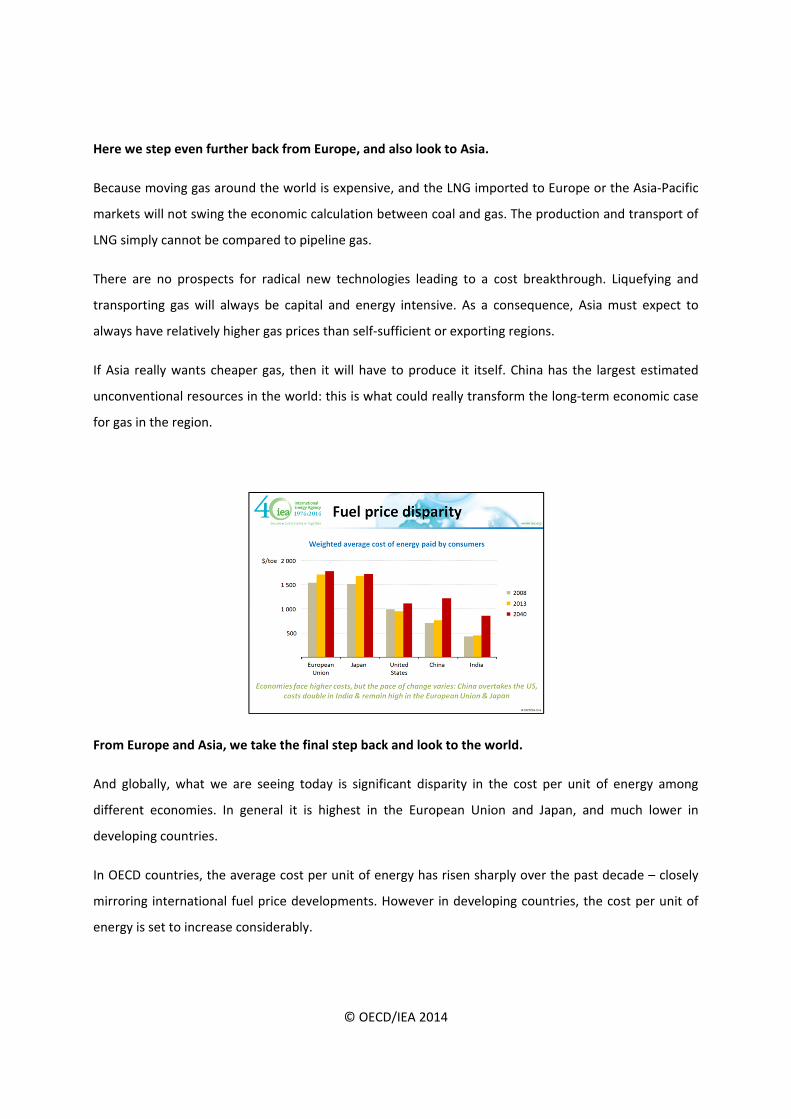

rope and As

bally, what w

t economies

ing countries

countries, t

g internation

s set to incre

urther back f

around the

ng the econo

e compared

ects for radi

l always be

ly higher gas

cheaper gas,

urces in the

sia, we take t

we are seein

s. In general

s.

he average c

nal fuel price

ease consider

©

from Europe

world is exp

omic calculat

to pipeline g

ical new tec

capital and

prices than

, then it will

world: this i

the final step

ng today is s

it is highes

cost per unit

e developme

rably.

© OECD/IEA 2

e, and also lo

ensive, and t

tion between

gas.

chnologies le

energy inte

self-sufficien

have to pro

s what could

p back and lo

significant d

st in the Eu

t of energy h

ents. Howeve

2014

ook to Asia.

the LNG imp

n coal and ga

eading to a c

nsive. As a c

nt or exportin

oduce it itse

d really trans

ook to the w

isparity in th

ropean Unio

has risen sha

er in develop

ported to Eur

as. The produ

cost breakth

consequence

ng regions.

lf. China has

sform the lon

world.

he cost per

on and Japa

rply over the

ping countrie

rope or the A

uction and tr

hrough. Liqu

e, Asia must

s the largest

ng-term econ

unit of ene

n, and muc

e past decad

es, the cost

Asia-Pacific

ransport of

efying and

t expect to

estimated

nomic case

rgy among

h lower in

de – closely

per unit of

The aver

decreasi

increasin

average

of oil co

electricit

This disp

world m

competit

investme

energy, g

In this re

This yea

period to

switchin

For now

problem

To unde

come fro

rage cost in

ng importan

ngly being re

cost per uni

onsumption

ty prices due

parity can be

may represe

tiveness. Fal

ents. Like th

geopolitical l

egard, it is im

ar’s World En

o 2040, altho

g.

w, markets a

ms that may b

rstand why,

om over the

China, for e

nce of energ

eplaced by m

t of energy i

subsidies re

e to a change

a source of c

ent an oppo

ling prices e

he shift in e

landscape.

mportant to k

nergy Outloo

ough the rat

re currently

be around the

we need to

next two dec

©

xample, is se

gy-intensive

more expens

in India is als

eforms, a st

of the powe

concern, dep

ortunity for

lsewhere ma

energy dema

keep track of

ok sees oil d

te of increase

y well-supplie

e corner.

o look at the

cades: the Un

© OECD/IEA 2

et to overtak

industries a

ive gas and

so gradually

rong growth

er mix toward

pending on y

r fuel produ

ay increase c

and, such di

demand and

demand incr

e slows as hi

ed; but shor

longer term

nited States,

2014

ke that of th

and changes

electricity in

approaching

h of the tra

ds more expe

your perspect

ucers, yet

competitiven

sparities hav

d how deman

reasing by 14

igh prices en

rt-term cond

m and see wh

Canada, Bra

he United Sta

in the fuel

n the industr

g that of the

ansport secto

ensive fuels

tive. Rising p

be an impe

ness, yet put

ve the poss

nd affects inv

4 million ba

ncourage ene

ditions shou

here the ext

azil and the M

ates by 2040

mix, with c

ry sector. Sim

United State

or and an i

and technolo

prices in one

ediment to

bottlenecks

ibility of cha

vestment.

rrels per da

ergy efficienc

ld not blind

ra barrels ar

Middle East.

0, due to a

cheap coal

milarly, the

es, a result

ncrease of

ogies.

part of the

economic

on energy

anging the

y over the

cy and fuel

us to the

re going to

© OECD/IEA 2014

Tight oil production is making the United States the largest oil producer in the world – and it stays that

way in our projections until the late 2020s. But, by then, US production is already starting to fall back

and, by 2040, output is back to where it is today. Instead, it is the oil sands in Canada that takes over as

the main source of North American supply growth, assuming that a way can be found to bring this oil to

market. The other major non-OPEC source of supply growth is Brazil, with its prolific, complex and

capital-intensive deepwater fields – where delay is an ever-present risk. These suppliers do a lot to

satisfy growing demand over the period to 2020, but after this, there is a large and growing gap in the

market.

This is the gap that needs to be filled by the only remaining large source of low-cost oil, the Middle

East.

More than half of this growth comes only from one country, Iraq. There is no shortage of resources to

meet this challenge. But, looking at the turmoil in parts of the Middle East today, there is a real concern

about a shortfall in investment.

This is a decade away, but we should not be lulled into a false sense of security. To be producing extra

barrels in the 2020s requires investment today. Aside from the obvious security concerns in parts of the

region, there are also fiscal and demographic pressures that could squeeze the funds available for the

upstream.

What would be the implications of a shortfall in investment? Tighter markets and higher prices. The

effects would be felt around the world. But vulnerability would be particularly acute in those countries

that are actually looking for these extra barrels.

First among the sources of demand growth are the large importers in Asia, notably China, but also India

and others. By 2040, two out of every three barrels of crude oil that are traded internationally –

including 90 percent of Middle East exports – will be heading for Asia.

But for today, there is plenty of supply, and prices are low.

As you are all well aware, following three consecutive years of prices above 100 dollars, the price of

Brent crude has fallen by almost 30 percent since the middle of this year.

Buoyant supply from North America has been instrumental in bringing prices down. What remains to be

seen is for how long this supply can keep prices at or around today’s levels.

Around t

being cu

are being

We estim

percent

see the

constrain

producti

This brin

Middle E

price.

So while

longer-te

The thre

Over the

demand

growth o

countrie

today’s price

urtailed or ca

g revised dow

mate, for exa

fall in US up

postponeme

nt on the m

ion that we a

ngs us back a

East, where f

e today’s pric

erm market d

ead weaving t

e past 14 yea

in OECD co

over the pas

s in the Midd

e levels, we w

ancelled. The

wnwards; on

ample, that a

pstream capi

ent of new o

medium-term

anticipate fro

again to the

fiscal and ge

ce levels off

dynamics.

through all o

ars, global en

untries is alm

st decade w

dle East.

©

will start to s

ere are signs

nly projects w

a price aroun

tal expendit

oil sands pro

m outlook fo

om non-OPEC

question ma

eopolitical ch

er some com

of these issue

nergy deman

most the sam

was entirely d

© OECD/IEA 2

see some inv

s already tha

with strong e

nd today’s le

ure in 2015,

ojects. Lowe

or Brazil. Ta

C suppliers.

arks that we

allenges only

mfort to con

es is the glob

nd has grown

me today as

driven by no

2014

vestment in l

at, in some c

conomics are

evels – if mai

compared w

er cash flows

ken togethe

have about

y become m

sumers, they

al shift in en

n by around

it was in 20

on-OECD cou

ow-margin f

ases, investm

e likely to ga

intained – w

with this yea

s from oper

er, this coul

the adequac

more intense

y don’t prov

ergy demand

one-third. H

000. Indeed,

untries, inclu

fields around

ment budget

ain approval.

ould result in

ar. In Canada

ations could

d slow the

cy of investm

with the rec

vide reassura

d.

However ove

global energ

uding China,

d the world

ts for 2015

n a 5 to 10

a, we could

d also be a

growth in

ment in the

cent falls in

ance about

rall energy

gy demand

India, and

And it is

accounts

demand

growth s

As the p

energy d

capita as

China di

our proje

the lead

What th

system.

energy s

establish

Ladies an

We cann

about oi

gas with

consider

s China that

s for more th

reaches a pl

slows and as

pace of grow

demand grow

s China had

d at the time

ections, Indi

from China w

is shift in de

Emerging ac

should be ap

hed, tradition

nd gentleme

not talk abo

l prices with

hout conside

ring the effec

remains the

han one-thir

lateau by the

population g

wth in China

wth. This is p

some 10 yea

e, which ind

a accounts fo

with one-qua

emand mean

ctors may ha

pproached in

nal actors are

n, energy an

out renewab

hout discussin

ering Russia

cts of fuel pr

©

e driving for

rd of global e

e late 2030s.

growth slows

loses steam

particularly t

ars ago, but

icates the la

or 15 percen

arter of glob

ns, is a poss

ave different

n terms of co

e prepared fo

nd geopolitics

les in Spain

ng security is

’s relationsh

ice disparity,

© OECD/IEA 2

rce in global

energy dema

This occurs

s and starts t

m, other cou

rue for India

uses only lit

rge potentia

nt of global e

al growth aft

sible shift in

t priorities, d

ooperation, e

or this shift.

s are often o

without tal

ssues in the

hip with Eur

, competitive

2014

demand gro

and growth.

as efficiency

to slowly dec

ntries assum

a, which has

ttle more tha

al for energy

energy dema

ter 2025.

roles and re

different rul

engagement,

ne and the s

king about E

Middle East.

rope. We ca

eness, and th

owth until th

But then gro

y measures ta

cline.

me its role a

today a simi

an half the e

demand gro

and until 202

esponsibilitie

es, and diffe

, and compe

same.

EU climate p

. It is likewis

annot discus

he changing l

he mid-2020

owth slows a

ake effect, as

as the engine

ilar level of i

energy per p

owth in this c

25, and then

es in the glo

erent ideas a

etition. It is c

policy. We c

e impossible

ss fuel price

landscape of

0s, when it

and energy

s economic

e of global

ncome per

person that

country. In

takes over

bal energy

about how

crucial that

cannot talk

e to discuss

es without

f the global

© OECD/IEA 2014

energy system. And I have not even had time to discuss energy poverty, and the remarkable impact that

energy demand growth will have in Sub-Saharan Africa and South Asia over the coming decades.

All of these issues present us with uncertainties.

However there is one thing of which we can be certain. Countries will always require energy, and the

ways in which we generate, transport, and use this energy may not be the same tomorrow as they are

today. Being vigilant, having foresight, and ensuring energy security today is the best way to stay

prepared for tomorrow.