doug brown october 23, 2014. budget overview a budget planning process (overland park’s) financial...

TRANSCRIPT

APWA Public Works Institute

BUDGETING FINANCING

Doug Brown

October 23, 2014

• Budget Overview• A Budget Planning Process (Overland

Park’s)• Financial Management

AGENDA

BUDGET OVERVIEW

• It’s the Law– Kansas law requires a budget before a local

government can spend money and levy taxes(K.S.A. 79-2927)*

• To Manage Our Resources– People– Money– Time

*In some cases, Missouri requirements may differ

WHY WE BUDGET

• Planning• Management• Control

A BUDGET’S MAIN FUNCTION

• Used by Elected Officials to allocate resources

• Budget is first a policy document– Allocation of resources in line with City’s

policies– Resources allocated based on priorities

of Governing Body

PLANNING

• Budget is a management tool– Management allocates resources to

operational areas to meet Governing Body policy objectives

– Requires management to formulate a work plan

MANAGEMENT

• Provides assurance to citizens regarding wise use of tax money

• Budget provides control– Legal restraints– Resources are spent in accordance with plan

CONTROL

• Must have a fiscal year budget• Is done on an annual basis• Must hold public hearings• Must be balanced (no deficit)• Governing Body must approve it by August

25th of the year prior (in Kansas)

PREPARING THE BUDGET

• Ideal– Establish your mission

• Strategic Plan• Goals and Objectives

– Measure your mission• Assets – what and what condition• Benchmarking – cost of activities; people

requirements– Develop your budget requirements

• Incremental/program/zero-based

PREPARING YOUR BUDGETIdeal vs. Actual

• Actual– Typically, it’s incremental budgeting

• Assigned personnel costs• Assigned budget % increase (or decrease)• Expanded level packages (for increases in

mission or special requirements)• Mostly, it is “fill in the blanks”

PREPARING YOUR BUDGETIdeal vs. Actual

• General• Special Revenue• Debt Service• Capital Projects• Special

Assessment

BUDGET FUND TYPES

• Enterprise• Internal Service• Trust and Agency• Reserve

• Special Street and Highway

• 1/8 Cent Sales Tax Fund• Special Park and

Recreation• Special Alcohol Control

Fund• Convention Center• Transient Guest Tax Fund• Transient Guest Tax –

Capital

SPECIAL REVENUE FUNDSOverland Park Examples

• Transient Guest Tax – Operating

• Capital Improvement Fund• Equipment Reserve Fund• Special Street Improvement

Fund• Special Machinery &

Equipment• Stormwater Utility• Soccer Complex Fund

BUDGET PROCESSOverland Park Example

FINANCIAL PLANNING

FINANCIAL MANAGEMENT & REPORTING

BUDGET PROCESSING

• Actual vs. Budget• Adjustments• Adherence to Financial Plan• Telling the Story

• Process• Forms• Approval• Implement Policies

• Financial Priorities• Policies• Council Involvement

Effective Supervisory Skill Building, @ICMA 2005

• Long-Term Financial Plan– Five-year revenue and expenditure forecast

• Capital Improvement Program (5- year)– Expenditures for capital infrastructure, equipment and

facilities. Capital items are costly, nonrecurring, and have a life span of multiple years

• Maintenance Program (5-year)– Significant repair, rehabilitation, or in-kind replacement of

existing city infrastructure or facilities.• Operating Budget

– Supports ongoing operations & routine maintenance – Personnel– Supplies– Equipment– Operation of facilities

BUDGET COMPONENTS

Effective Supervisory Skill Building, @ICMA 2005

• Examines historical revenues & expenditures.• Examines historical, current & projected

economic & demographic indicators.• Projects future financial outlook of City based

on a set of assumptions.• Facilitates decisions that ensure the ongoing

financial solvency of the City.

FIVE-YEAR FINANCIAL PLAN

FIVE-YEAR FINANCIAL PLAN

Effective Supervisory Skill Building, @ICMA 2005

• Funds the first year of the capital improvement plan – a multi-year plan for the purchase and financing of infrastructure, major equipment, and facilities

• Financing may come from tax revenues, intergovernmental revenues, long-term borrowing, or combination

CAPITAL IMPROVEMENTS PROGRAM

Effective Supervisory Skill Building, @ICMA 2005

Project Types

Funding Sources

2010-2014 CIP = $159,785,000 2011-2015 CIP = $121,528,000 2012-2016 CIP = $98,923,000 2013-2017 CIP = $82,940,500 2014-2018 CIP = $121,582,000 2015-2019 CIP = $128,665,000

Street In-frastruc-

ture67%

Other Infrastructure8%

6arks & Recre-ation2%

9acilities &

Equip-ment14%

In-ter-gov-ern-men-

tal32%

De-velop

er Fund-

ing10%

City at

Large33%

Sales Tax19%

Other 26%

2015 – 2019 CIP = $128,665,000

Effective Supervisory Skill Building, @ICMA 2005

• Funds the first year of the maintenance plan –a multi-year plan for major and preventive maintenance

• Financing may come from tax revenues, intergovernmental revenues, long-term borrowing, or dedicated sources

MAINTENANCE PROGRAM

Effective Supervisory Skill Building, @ICMA 2005

2010-2014 = $61,979,000 2011-2015 = $53,960,000 2012-2016 = $63,948,000 2013-2017 = $69,895,000 2014-2018 = $77,110,000 2015-2019 = $79,040,000

5treets79%

Traffic Mtg.4%

Storm Drainag

e9%

6acili-ties4%

7arks & Rec5%

Intergovern-mental35%

City at Large45%

6/8-Cent Sales Tax7% City Ded-

icated 14%

2015 – 2019 MAINTENANCE = $79,040,000

Project Types

Funding Sources

Effective Supervisory Skill Building, @ICMA 2005

• Can reduce major fluctuations in tax rates

• Encourages the coordination of capital, maintenance and operating expenditures

• Allows flexibility in scheduling bond issues

• Helps the city time projects to obtain state and federal funding

• Helps taxpayers understand the community’s long-range needs

CAPITAL IMPROVEMENT ANDMAINTENANCE PLANS

Effective Supervisory Skill Building, @ICMA 2005

• Maintain low property taxes

• Sales taxes are primary funding source

• Utilization of user fees

• Maintain adequate reserves

OVERLAND PARKFINANCIAL PLANNING POLICIES

Effective Supervisory Skill Building, @ICMA 2005

• Departments Develop Budget Proposals– Allocate resources for ongoing operations– New programs and / or increased funding– Developed by Line Item/Cost

Center/Department– Based on historical patterns and knowledge

about changes in patterns/approaches– Allocations/Re-allocations based on constraints– Use of consistent format/procedures

throughout organization

BUDGET PROCESS

BUDGET PROCESSYour Role In The

Effective Supervisory Skill Building, @ICMA 2005

• Prepare early

• Keep track of changes in your workload

• Identify ways in which your work unit can become more efficient

• Talk to other supervisors

ROLE OF THE SUPERVISOR

Effective Supervisory Skill Building, @ICMA 2005

• Monitor Budget Expenditures

• Purchasing in Accordance with Policy

• Expenditure Management

• Performance Measures

FINANCIAL MANAGEMENT

BUDGET QUIZOverland Park

Effective Supervisory Skill Building, @ICMA 2005

Effective Supervisory Skill Building, @ICMA 2005

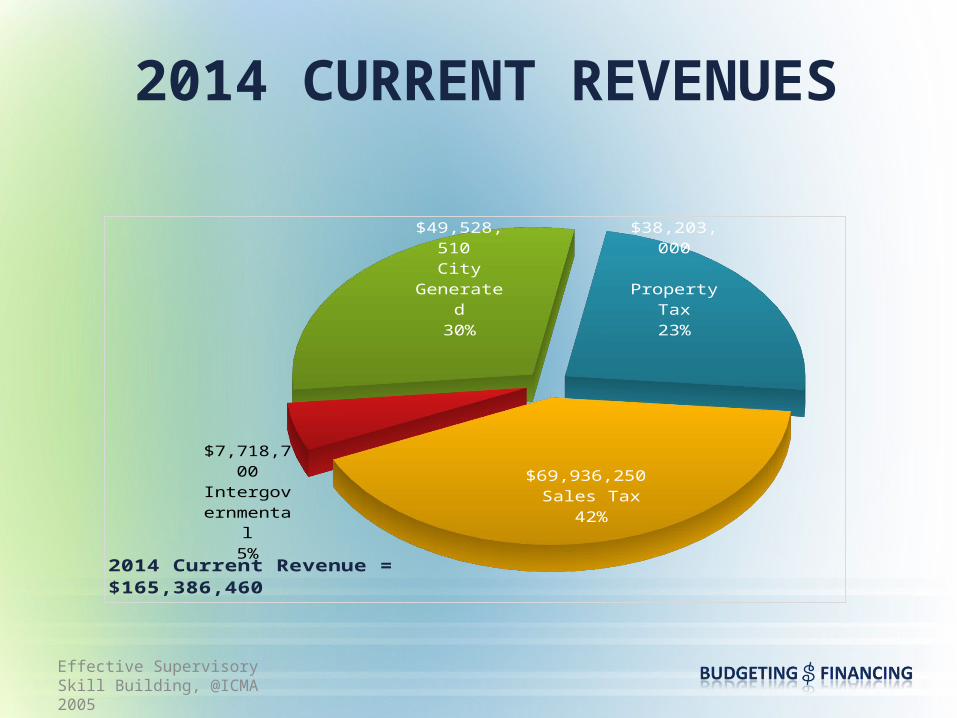

Overland Park receives most of its revenue

from what source? • Property Taxes

• Sales Taxes

• Fines

• Building Permit Fees

• Grants

Effective Supervisory Skill Building, @ICMA 2005

$38,203,000

Property Tax23%

$69,936,250 Sales Tax

42%

$7,718,700 Intergov-ernmental

5%

$49,528,510

City Gen-erated30%

2014 Current Revenue = $165,386,460

2014 CURRENT REVENUES

Effective Supervisory Skill Building, @ICMA 2005

Overland Park Mill Levy is 12.833 mills to support the 2012 Budget.

What percent is that of a homeowner’s property tax bill?

• Approximately 4%

• Approximately 11%

• Approximately 23%

• Approximately 37%

Effective Supervisory Skill Building, @ICMA 2005

PROPERTY TAX RATES2014 Budget

2014 Budget - Mill LeviesBy School District By School District

Mill Levy Rate Property Tax Amounts

Taxing Entity

Shawnee

Mission Blue Valley Olathe Spring Hill

Shawnee

Mission Blue Valley Olathe Spring Hill

State of Kansas 1.500 1.500 1.500 1.500 $43.13 $43.13 $43.13 $43.13Johnson County 17.745 17.745 17.745 17.745 $510.17 $510.17 $510.17 $510.17JCCC 9.551 9.551 9.551 9.551 $274.59 $274.59 $274.59 $274.59JOCO Parks & Rec 2.347 2.347 2.347 2.347 $67.48 $67.48 $67.48 $67.48JOCO Library 3.155 3.155 3.155 3.155 $90.71 $90.71 $90.71 $90.71School District - District Assessment & Bond35.611 50.036 49.486 45.242 $1,023.82 $1,438.54 $1,422.72 $1,300.71School District - State General 20.000 20.000 20.000 20.000 $529.00 $529.00 $529.00 $529.00Recreation Commission 0.000 2.201 0.000 3.250 $0.00 $63.28 $0.00 $93.44Overland Park 12.833 12.833 12.833 12.833 $368.95 $368.95 $368.95 $368.95

Total Mills 102.742 119.368 116.617 115.623 $2,907.83 $3,385.83 $3,306.74 $3,278.16

Effective Supervisory Skill Building, @ICMA 2005

Approximately how much does an owner of a $250,000 house pay in

property taxes to the City?

• $197 per year

• $368 per year

• $533 per year

• $869 per year

Effective Supervisory Skill Building, @ICMA 2005

The amount the owner of a $250,000 house pays

in property taxes to the City?

• $368 per year

• 1 mill = $1 for every $1,000 of assessed value

• $250,000 * assessment rate of 11.5% / 1,000 * mill levy rate of 12.814 = $368.40

Effective Supervisory Skill Building, @ICMA 2005

What percentage of the City’s 2012 operating budget is allocated for

public safety services? • 19%

• 32%

• 48%

• 63%

Effective Supervisory Skill Building, @ICMA 2005

$17,637,389

Finance & Adminis-

tration16.2%

$51,519,255

Public Safety47.3%

$16,369,566

Public Works15.0%

$23,216,790 Com-munity Devel-opment21.4%

2014 Budget = $108,743,000

2014 OPERATING BUDGET(By Area)

Effective Supervisory Skill Building, @ICMA 2005

What is the largest category of expenditures

in the budget?

• Personnel Costs

• Commodities & Contractual Services

• Capital Improvements & Debt Service

Effective Supervisory Skill Building, @ICMA 2005

Commodities3.52%

Contractual Services9.99%

Capital Outlay1.44%

Maintenance 10.57%

Debt Service13.03%Capital

Imp5.28%

Contingency5.41%

Salary and Wages69.40%

Medical & Life Insurance 11.45%

Payroll Taxes6.29%

Retirement12.86%

2014 BUDGET(Excluding Transfers)

• Use of debt in financing• Public Private Partnerships • Privatization• Grants

OTHER BUDGET TOPICS

• Budgeting is a year-round activity (Plan, Develop, Execute)

• The budget is the supervisor’s resource and authority

• Use performance measures (output) to link to the budget (input)

• Use OPM (Other People’s Money) whenever possible

SOME FINAL THOUGHTS