doing business in brazil · t pis/cofins (social contribution on gross revenue) 0.65% or 1.65% t...

TRANSCRIPT

1

DOING BUSINESSIN BRAZIL

Greece, September 2014

CESAR CUNHA CAMPOS | DIRECTOR, FGV PROJETOS

2

ABOUT FGV AND FGV PROJETOS

Fundação Getulio Vargas (FGV) was founded in 1944

FGV is the leading Think Tank in Latin America and Top 25 in the world

Mission: boost the socioeconomic development of Brazil and increase its important role in the international scene

FGV’s technical advisory unit to public, private and third-sector institutions in Brazil and abroad

Develops projects in different areas: economics, administration, and public policy

30 years experience

Over 1300 projects developed

3

1. INVESTMENT CLIMATE

BRAZIL OVERVIEW

GLOBAL COMPETITIVENESS

TAXATION

TRADE PROFILE BRAZIL

2. TRADE: BRAZIL, EUROPEAN UNION AND GREECE

BRAZIL - EUROPEAN UNION

BRAZIL - GREECE

3. CONCLUSION

WHY DOING BUSINESS IN BRAZIL

GOVERNMENT SUPPORT PARTNERS

AGENDA

4

1. INVESTMENTCLIMATE

5

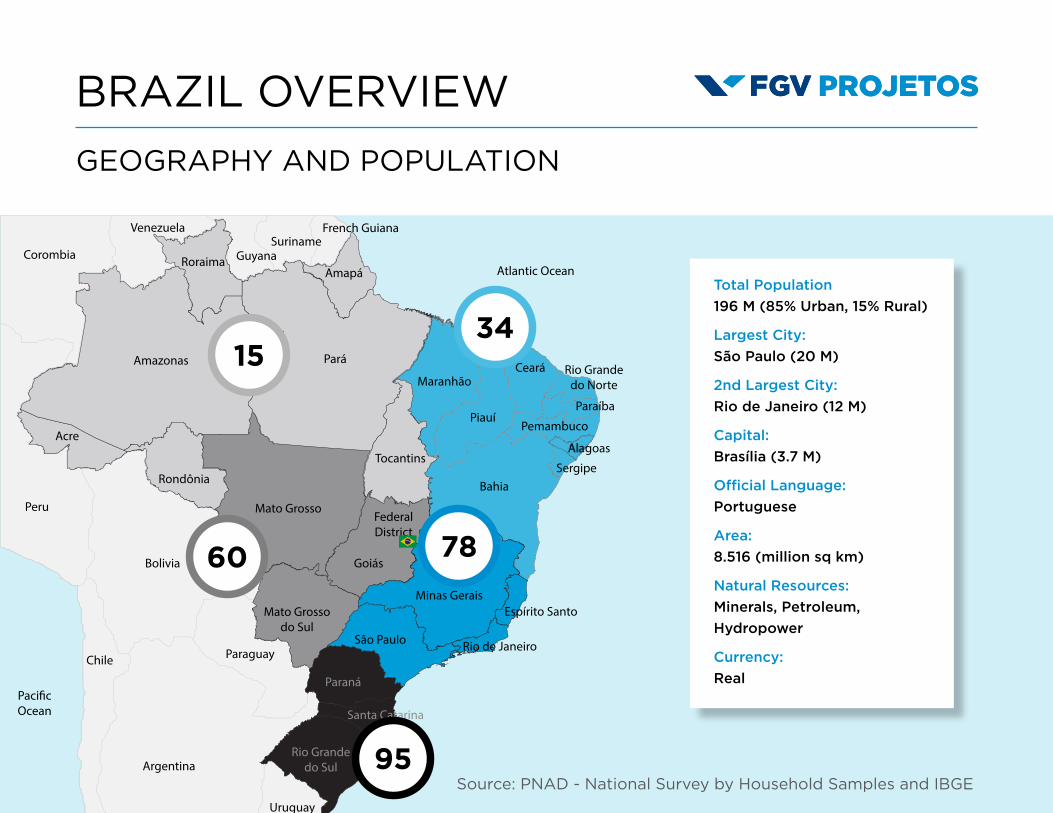

BRAZIL OVERVIEW

Source: PNAD - National Survey by Household Samples and IBGE

GEOGRAPHY AND POPULATION

15

60

95

78

34

Total Population

196 M (85% Urban, 15% Rural)

Largest City:

São Paulo (20 M)

2nd Largest City:

Rio de Janeiro (12 M)

Capital:

Brasília (3.7 M)

Official Language:

Portuguese

Area:

8.516 (million sq km)

Natural Resources:

Minerals, Petroleum,

Hydropower

Currency:

Real

6

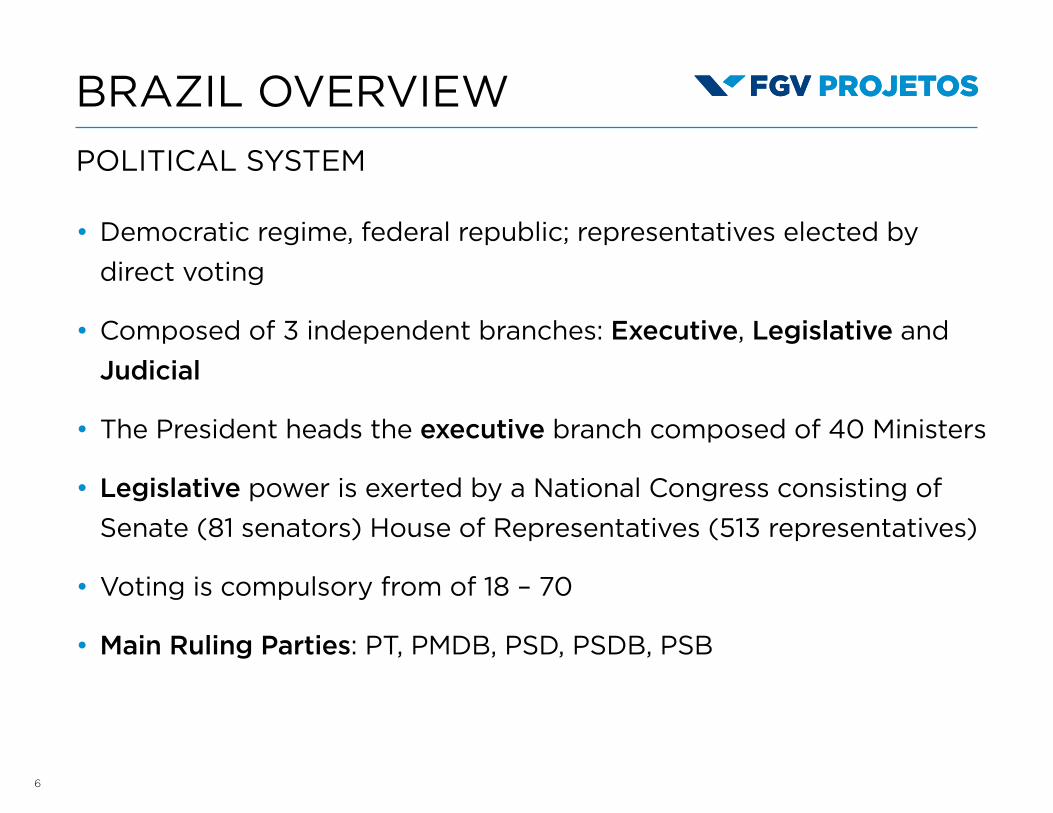

Democratic regime, federal republic; representatives elected by

direct voting

Composed of 3 independent branches: Executive, Legislative and

Judicial

The President heads the executive branch composed of 40 Ministers

Legislative power is exerted by a National Congress consisting of

Senate (81 senators) House of Representatives (513 representatives)

Voting is compulsory from of 18 – 70

Main Ruling Parties: PT, PMDB, PSD, PSDB, PSB

BRAZIL OVERVIEW

POLITICAL SYSTEM

7

BRAZIL OVERVIEW

ELECTIONS 2014: MAIN CANDIDATES

DILMA ROUSSEFF

Economic Development with

environmental sustainability

Strategic Outlook

Party

Candidates

1st round, October 5th: All presidential candidates

2nd round, October 26th: If none of the candidates obtains majority (50%+1), then the top two candidates will run again in this round

Economic Development with

environmental sustainability

Private investment

Focus on Sustainability

AÉCIO NEVES

MARINA SILVA

7

8

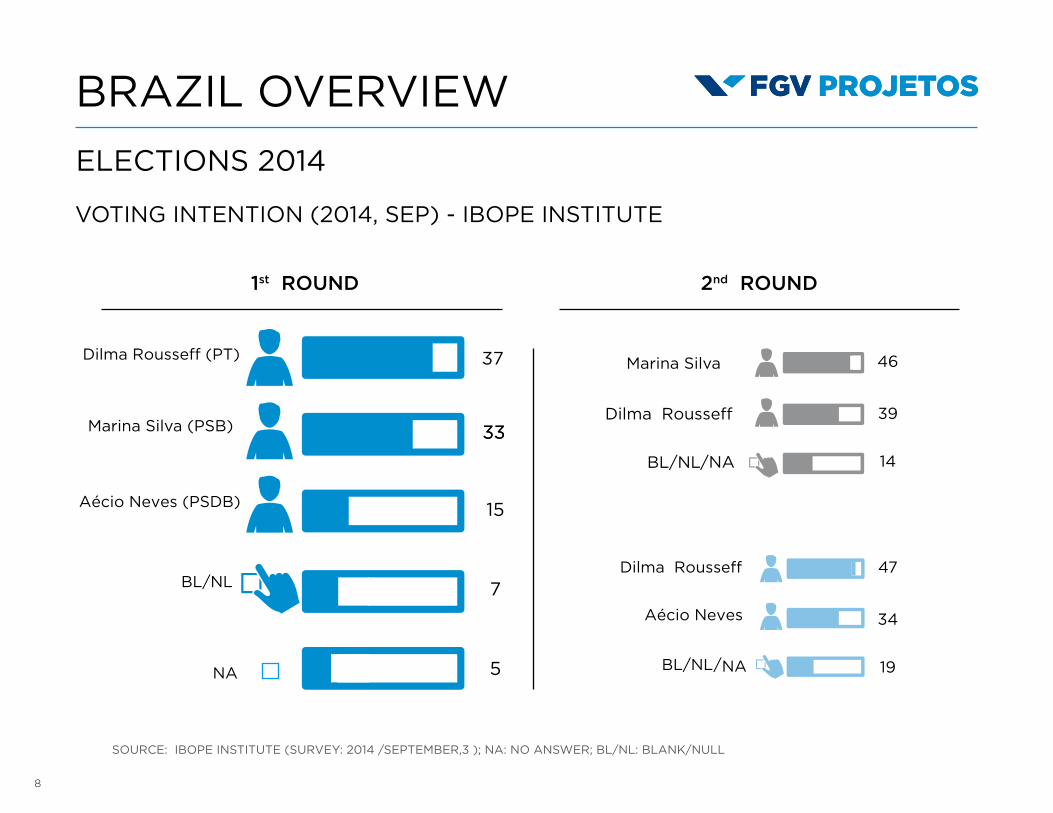

BRAZIL OVERVIEW

ELECTIONS 2014

VOTING INTENTION (2014, SEP) - IBOPE INSTITUTE

1st ROUND 2nd ROUND

SOURCE: IBOPE INSTITUTE (SURVEY: 2014 /SEPTEMBER,3 ); NA: NO ANSWER; BL/NL: BLANK/NULL

333339

34

14

19

46

47

7

5

15

Marina Silva (PSB)

Marina Silva

9

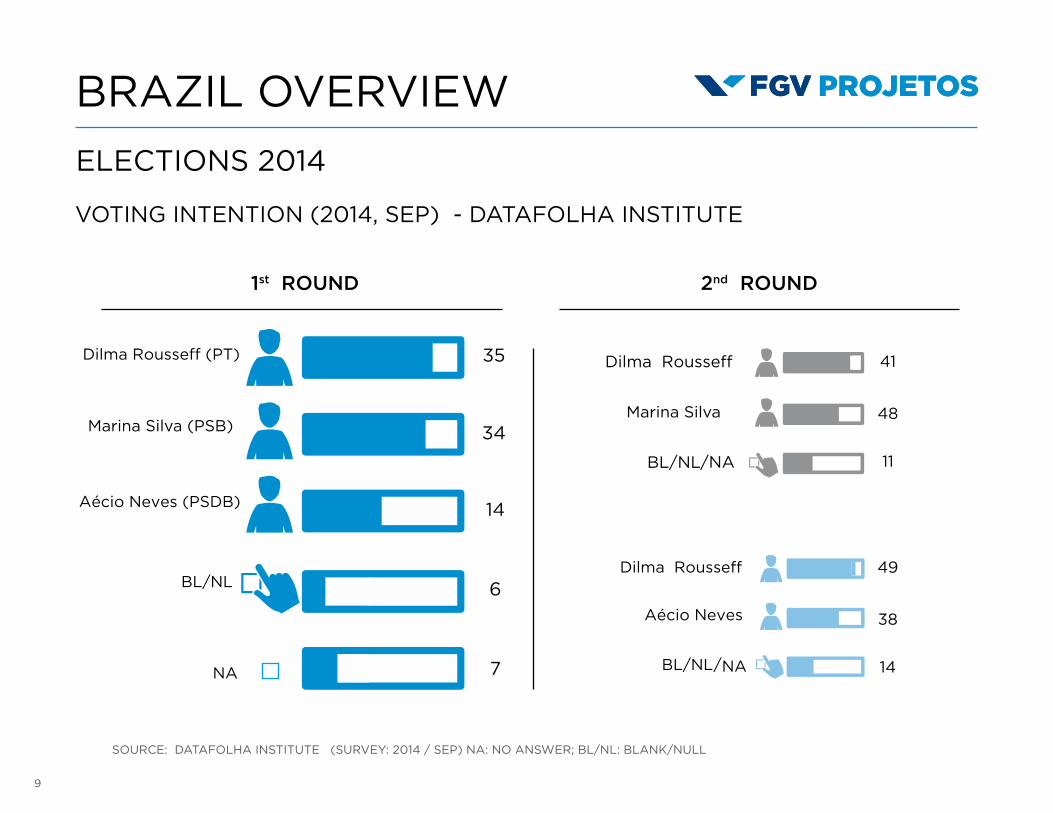

BRAZIL OVERVIEW

ELECTIONS 2014

VOTING INTENTION (2014, SEP) - DATAFOLHA INSTITUTE

1st ROUND 2nd ROUND

SOURCE: DATAFOLHA INSTITUTE (SURVEY: 2014 / SEP) NA: NO ANSWER; BL/NL: BLANK/NULL

34

35

48

38

11

14

41

49

6

7

14

Marina Silva (PSB)Marina Silva

10

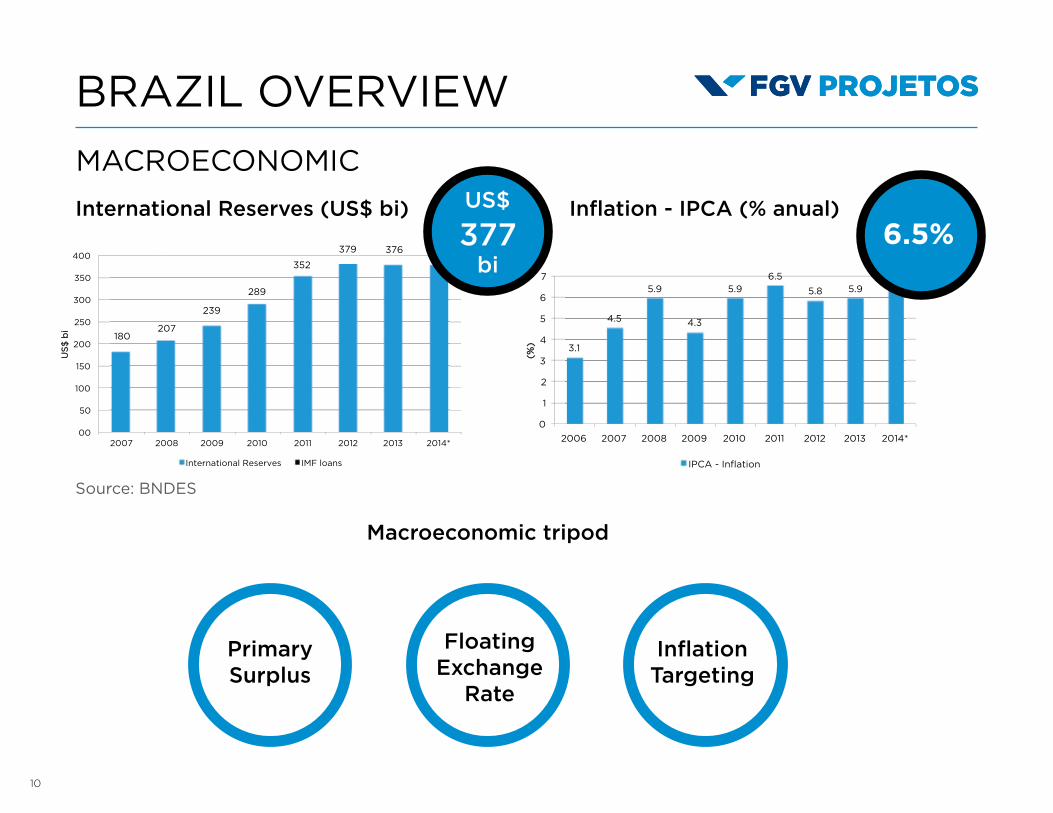

BRAZIL OVERVIEW

MACROECONOMIC

Source: BNDES

International Reserves (US$ bi)

Macroeconomic tripod

Inflation - IPCA (% anual)6.5%

FloatingExchange

Rate

PrimarySurplus

InflationTargeting

11

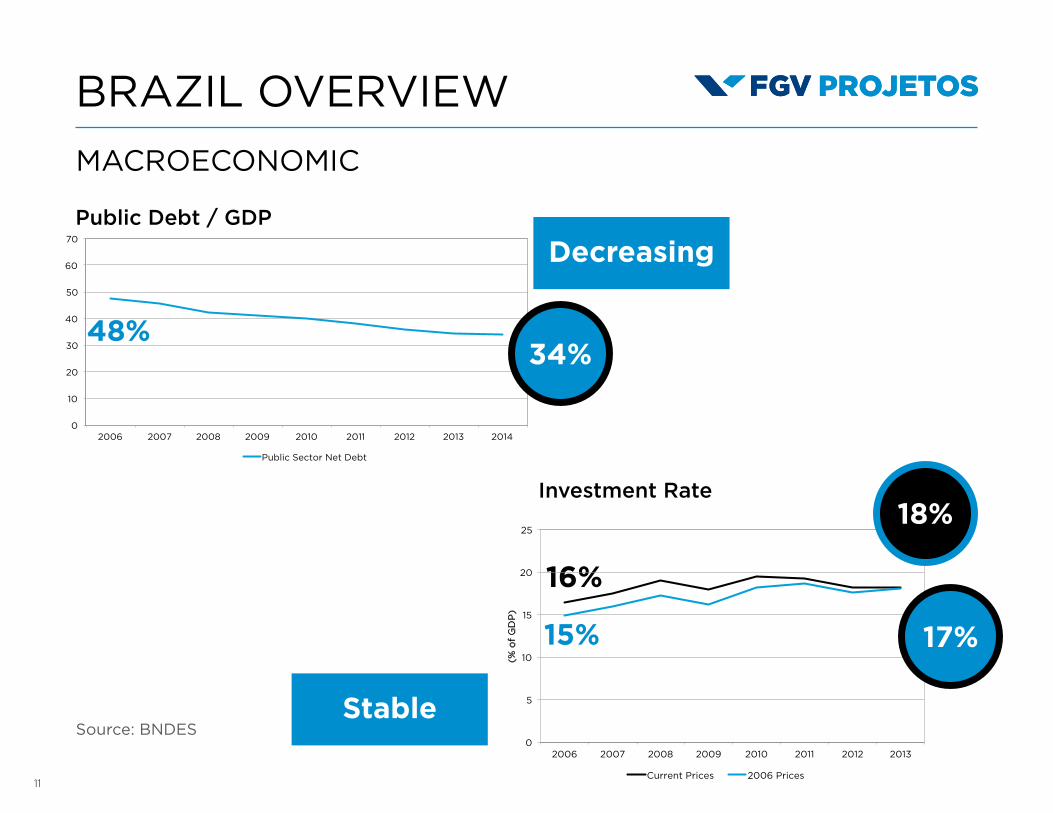

BRAZIL OVERVIEW

Investment Rate

Public Debt / GDP

MACROECONOMIC

Source: BNDES

16%

48%

15%

34%

18%

17%

Decreasing

Stable

12

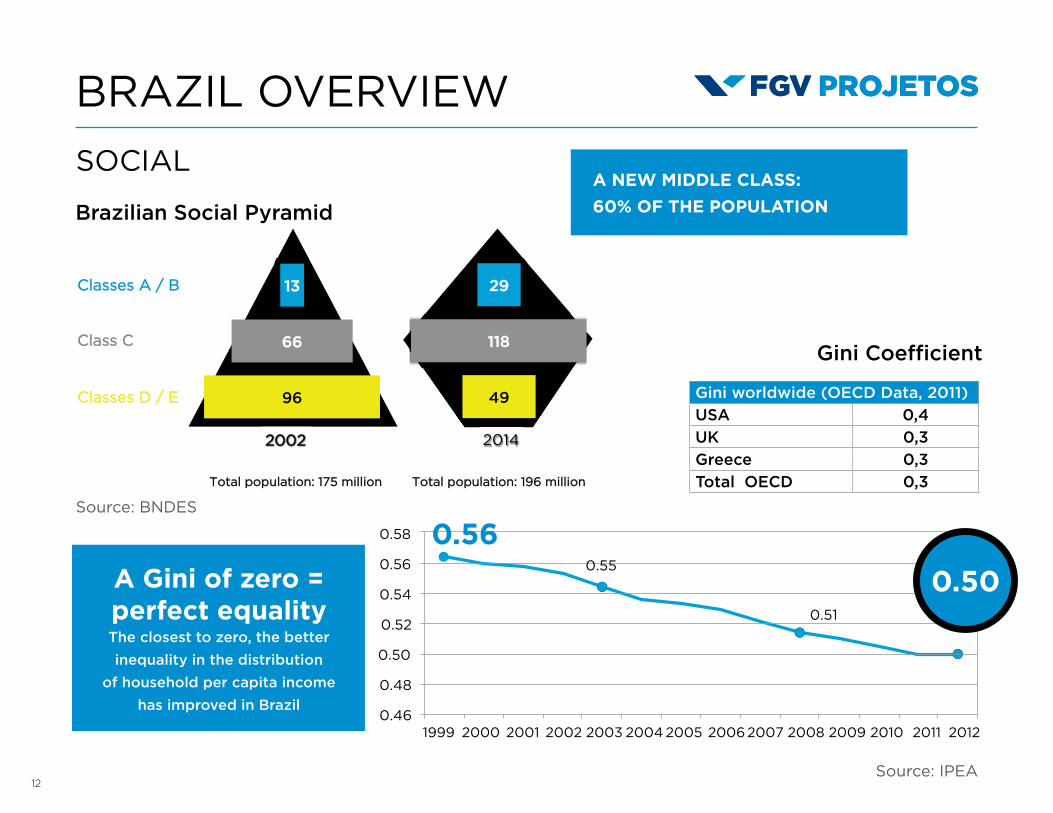

BRAZIL OVERVIEW

Brazilian Social Pyramid

Gini Coefficient

SOCIAL

Source: IPEA

Source: BNDES

0.56

0.50A Gini of zero =perfect equality The closest to zero, the better

inequality in the distribution

of household per capita income

has improved in Brazil

A NEW MIDDLE CLASS:

60% OF THE POPULATION

Gini worldwide (OECD Data, 2011)USA 0,4UK 0,3Greece 0,3Total OECD 0,3

13

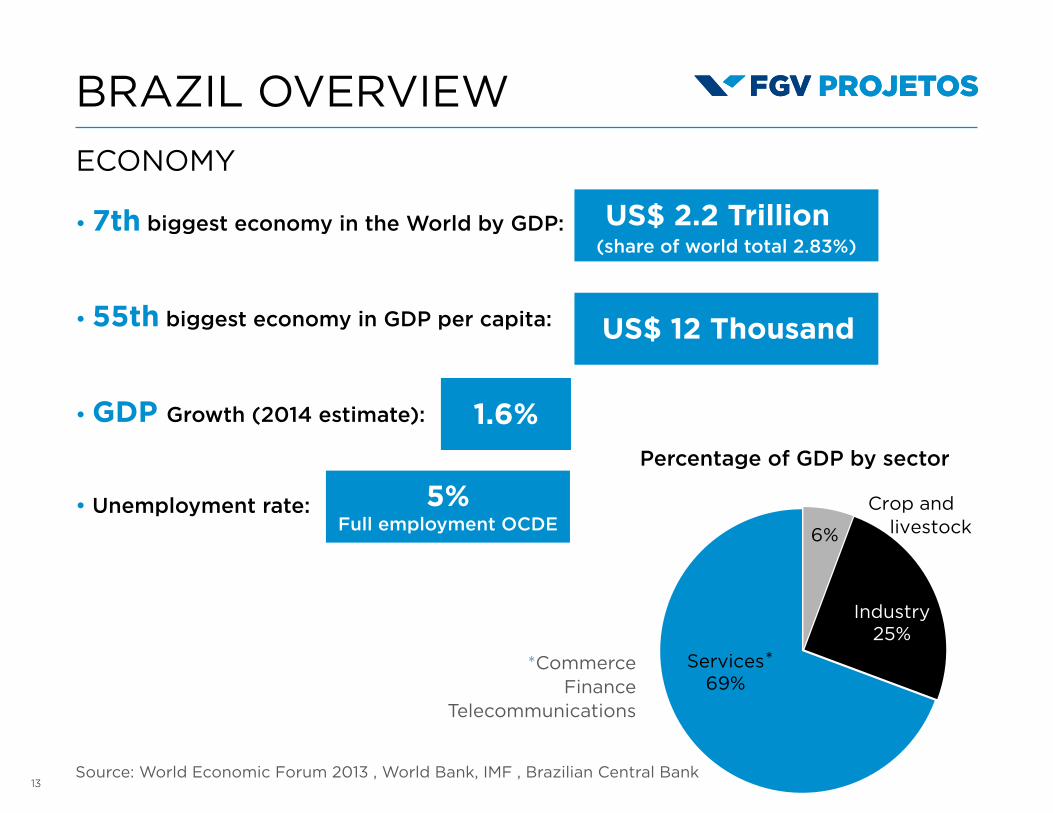

7th biggest economy in the World by GDP:

55th biggest economy in GDP per capita:

GDP Growth (2014 estimate):

Unemployment rate:

Source: World Economic Forum 2013 , World Bank, IMF , Brazilian Central Bank

US$ 2.2 Trillion

US$ 12 Thousand

(share of world total 2.83%)

Full employment OCDE

1.6%

5%

*CommerceFinance

Telecommunications

*

Percentage of GDP by sector

BRAZIL OVERVIEW

ECONOMY

14

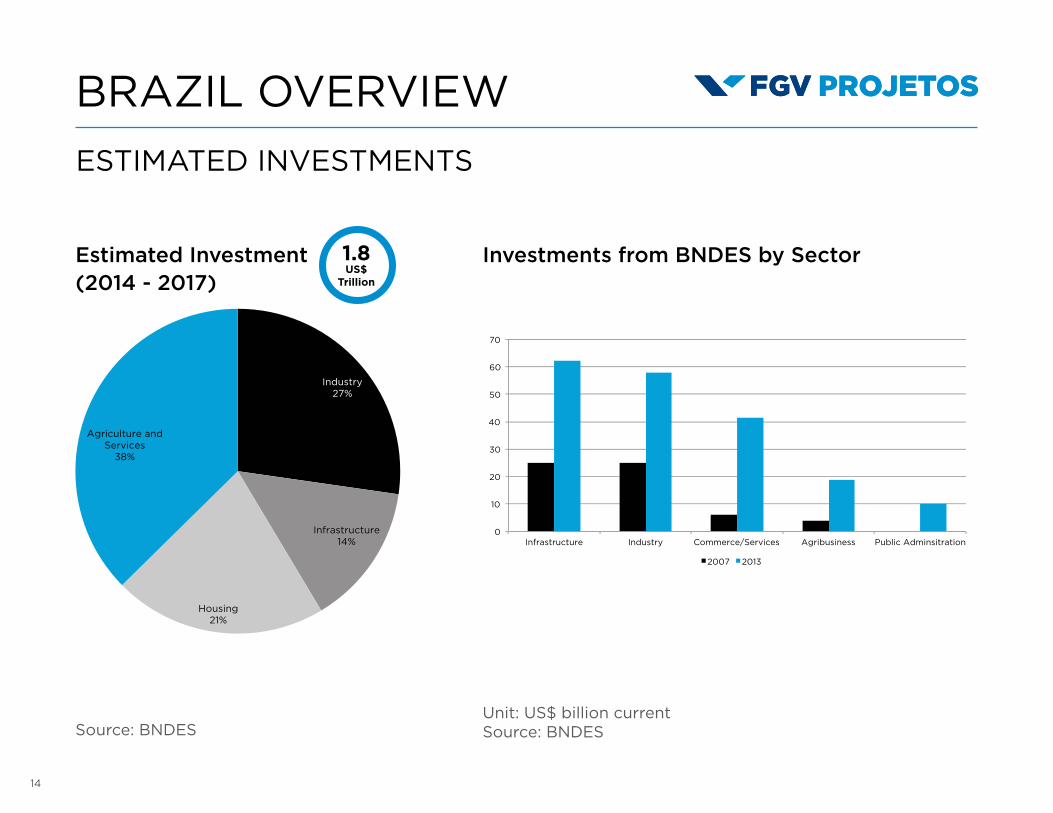

Estimated Investment(2014 - 2017)

Investments from BNDES by Sector

Source: BNDESUnit: US$ billion currentSource: BNDES

1.8US$

Trillion

BRAZIL OVERVIEW

ESTIMATED INVESTMENTS

15

During the period from 2014 to 2017, infrastructure investments amounting to US$ 261.4 billion are expected, with the following distribution amongst sectors:

The main energy-sector projects are hydroelectric plants, followed by nuclear and wind power

In telecommunications, third-generation mobile service and broadband wireless internet are at the forefront

Logistics investment is led by the railway segment followed by roadway and port projects

Infrastructure Investment Forecastedfor 2014 - 2017

Source: National Bank for Economic and Social Development (BNDES)

BRAZIL OVERVIEW

ESTIMATED INVESTMENTS

16

*

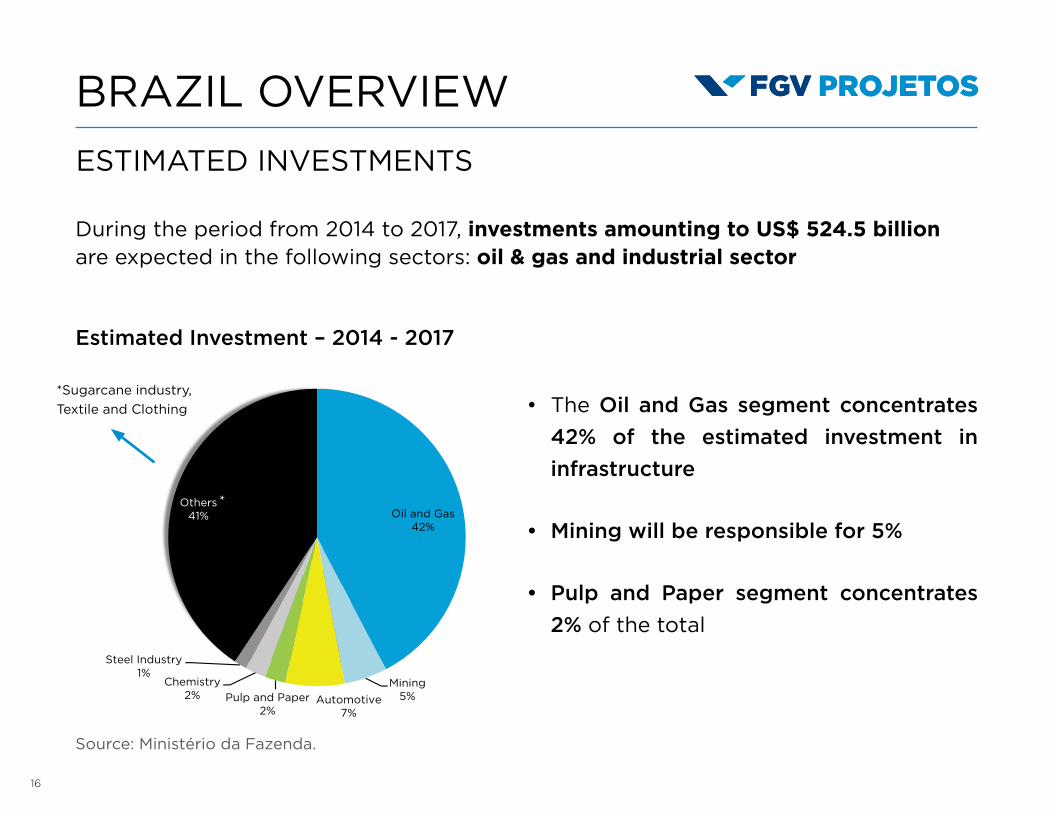

During the period from 2014 to 2017, investments amounting to US$ 524.5 billion are expected in the following sectors: oil & gas and industrial sector

Estimated Investment – 2014 - 2017

Source: Ministério da Fazenda.

The Oil and Gas segment concentrates

42% of the estimated investment in

infrastructure

Mining will be responsible for 5%

Pulp and Paper segment concentrates

2% of the total

*Sugarcane industry,

Textile and Clothing

BRAZIL OVERVIEW

ESTIMATED INVESTMENTS

17

Pre-SaltThe discovery of new deepwater oilfields (pre-salt) has opened a new frontier for the oil and gas industries

Development of the pre-salt will bring Brazil to a new position in the oil market by increasing proven reserves and doubling the production capacity by 2020

Pre-salt development also represents overcoming challenges related to technology, infrastructure and logistics, regulation, taxes and human capital

TOTAL INVESTMENT RELATED TO THE OIL AND GAS SECTOR IS ESTIMATED

AT US$ 400 BILLION OVER THE DECADE.

SÃO PAULO

RIO DE JANEIRO

PRE-SALT LAYER300 KM

ATLANTIC OCEAN

BRAZIL OVERVIEW

ESTIMATED INVESTMENTS

18

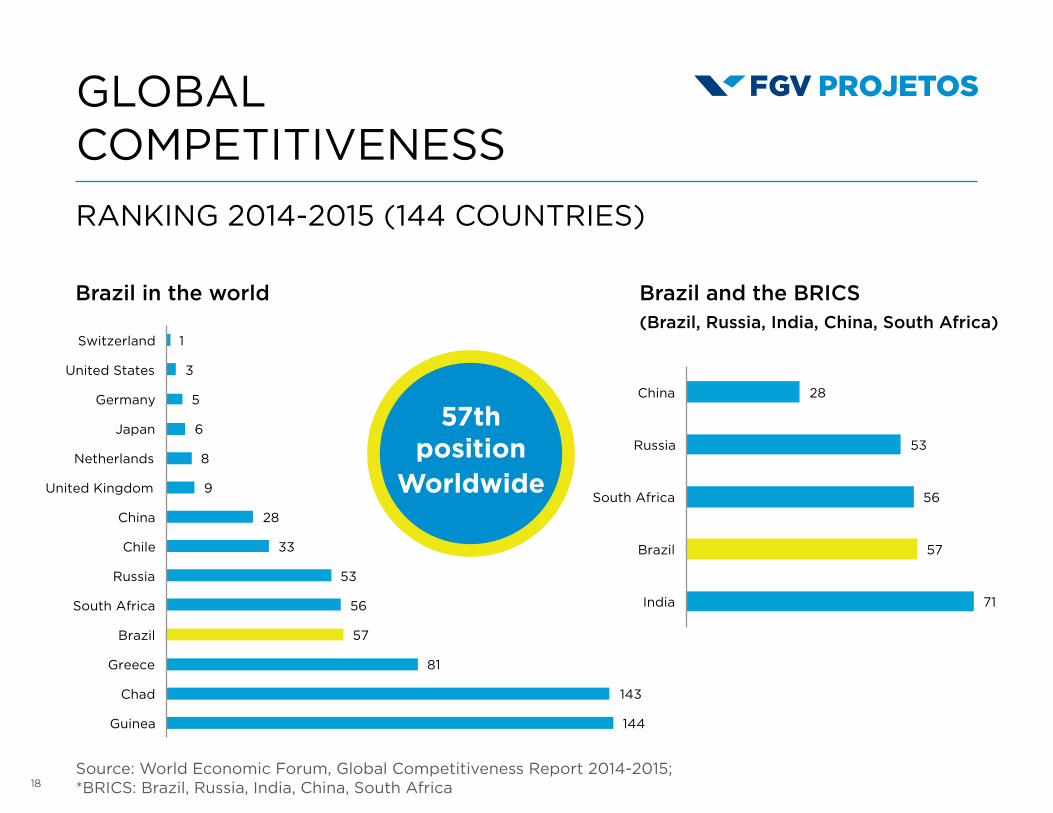

RANKING 2014-2015 (144 COUNTRIES)

GLOBALCOMPETITIVENESS

57thposition

Worldwide

Brazil in the world Brazil and the BRICS(Brazil, Russia, India, China, South Africa)

Source: World Economic Forum, Global Competitiveness Report 2014-2015;*BRICS: Brazil, Russia, India, China, South Africa

19

TAXATION

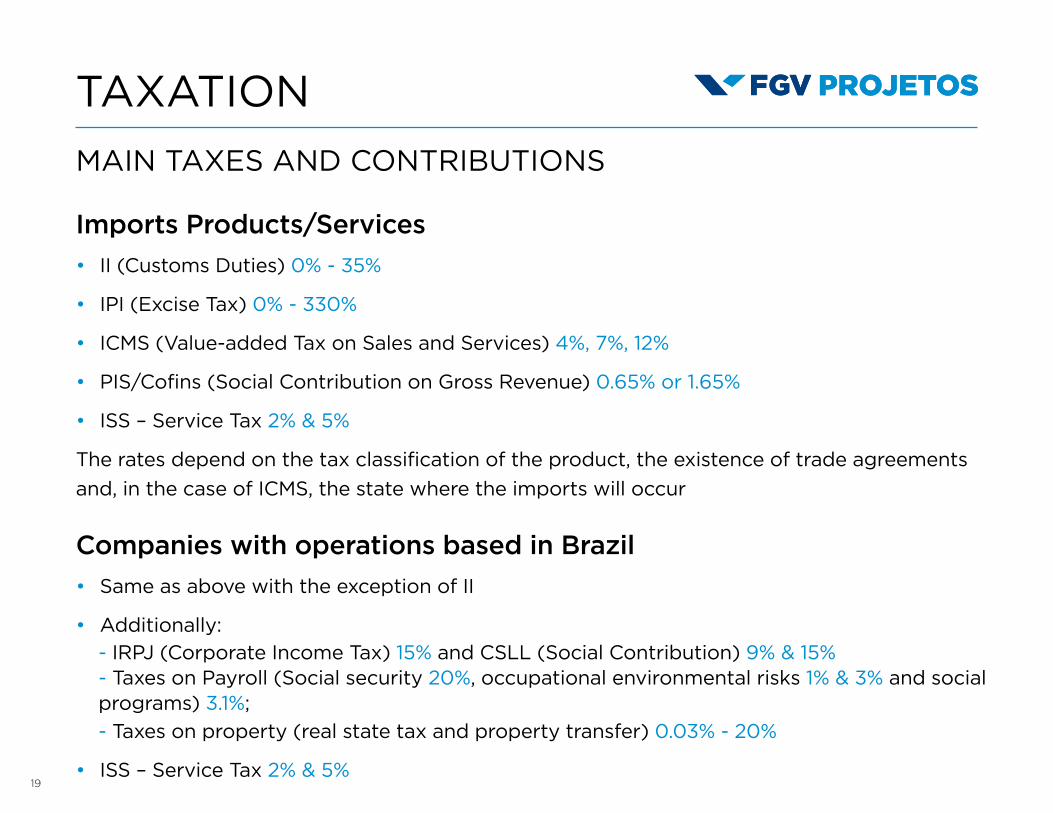

MAIN TAXES AND CONTRIBUTIONS

Imports Products/Services

II (Customs Duties) 0% - 35%

IPI (Excise Tax) 0% - 330%

ICMS (Value-added Tax on Sales and Services) 4%, 7%, 12%

PIS/Cofins (Social Contribution on Gross Revenue) 0.65% or 1.65%

ISS – Service Tax 2% & 5%

The rates depend on the tax classification of the product, the existence of trade agreements

and, in the case of ICMS, the state where the imports will occur

Companies with operations based in Brazil

Same as above with the exception of II

Additionally: - IRPJ (Corporate Income Tax) 15% and CSLL (Social Contribution) 9% & 15%- Taxes on Payroll (Social security 20%, occupational environmental risks 1% & 3% and social programs) 3.1%; - Taxes on property (real state tax and property transfer) 0.03% - 20%

ISS – Service Tax 2% & 5%

20

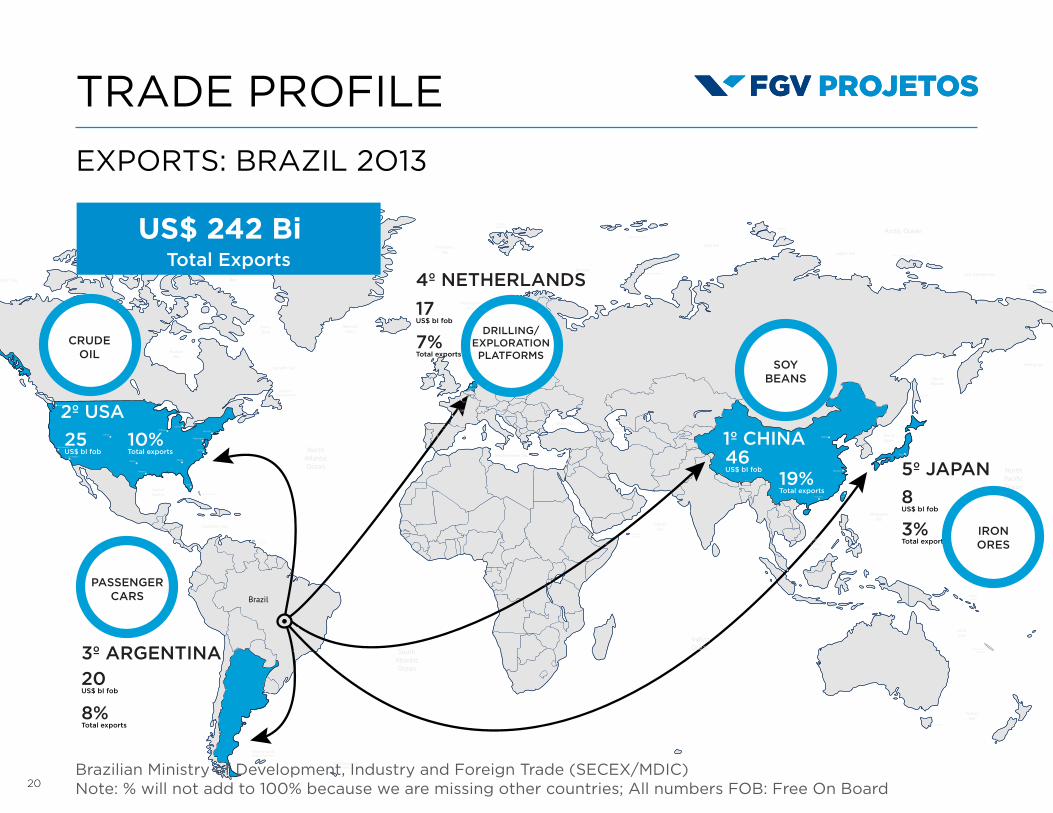

TRADE PROFILE

Brazilian Ministry of Development, Industry and Foreign Trade (SECEX/MDIC)Note: % will not add to 100% because we are missing other countries; All numbers FOB: Free On Board

EXPORTS: BRAZIL 2O13

US$ 242 BiTotal Exports

21

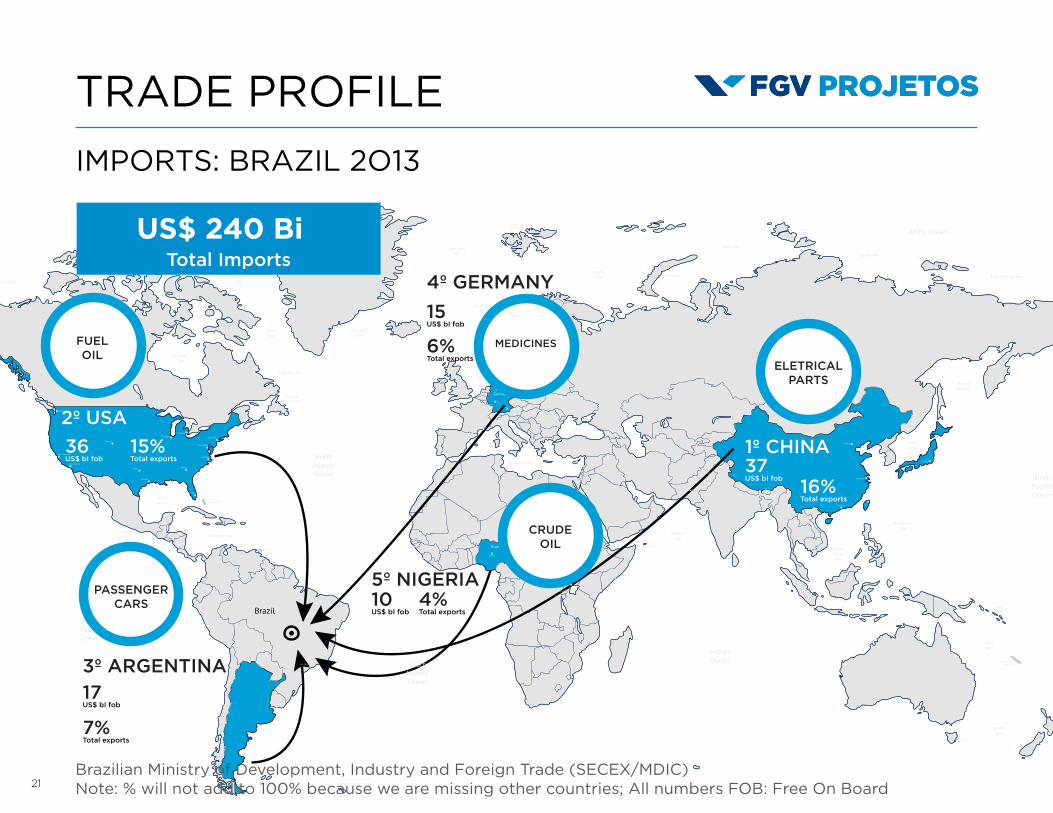

TRADE PROFILE

IMPORTS: BRAZIL 2O13

US$ 240 BiTotal Imports

Brazilian Ministry of Development, Industry and Foreign Trade (SECEX/MDIC)Note: % will not add to 100% because we are missing other countries; All numbers FOB: Free On Board

22

TOP 10 BRAZILIAN EXPORT& IMPORT COMPANIES

TOP 10 Brazilian Export Companies

2013Sector

US$Bi

Metals & Mining 27

Oil & Gas 14

Agribusiness, Food & Bioenergy

7

Food 5

Beef, Lamb and Poultry

processing5

Agricultural processors 4

Aircraft 4

Food and Agriculture 4

Beef, Lamb and Poultry processing

4

Oil & Gas (Platforms

builder)4

TOP 10 Brazilian Import Companies

2013Sector

US$Bi

Oil & Gas 40

IT Solutions 4

Petrochemicals 3

Automotive 3

ICT 3

Aircraft 3

Automotive 3

Automotive 2

IT Solutions 2

Agribusiness 2

Exports Imports

Source: Brazilian Ministry of Development, Industry and Foreign Trade (SECEX/MDIC). All numbers FOB: Free On Board

23

2. TRADE:BRAZIL,

EUROPEAN UNIONAND GREECE

24

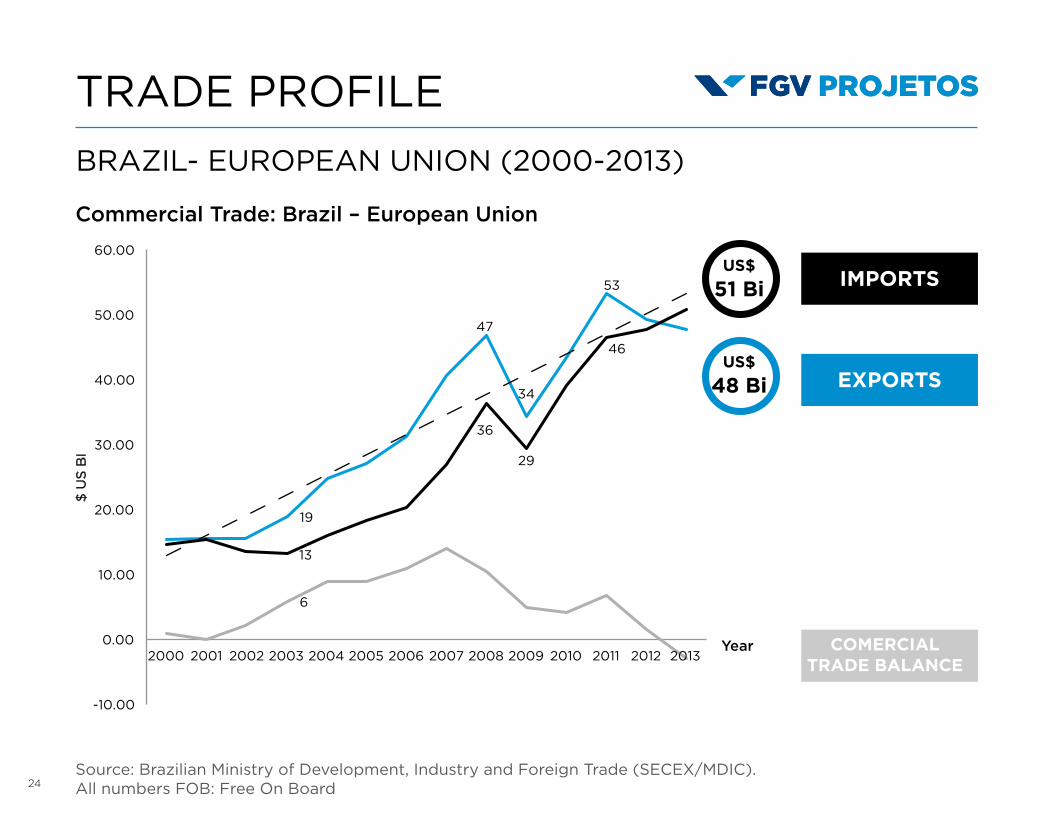

TRADE PROFILE

BRAZIL- EUROPEAN UNION (2000-2013)

Source: Brazilian Ministry of Development, Industry and Foreign Trade (SECEX/MDIC). All numbers FOB: Free On Board

Commercial Trade: Brazil – European Union

US$

51 Bi

US$

48 Bi

IMPORTS

EXPORTS

COMERCIALTRADE BALANCE

Year

25

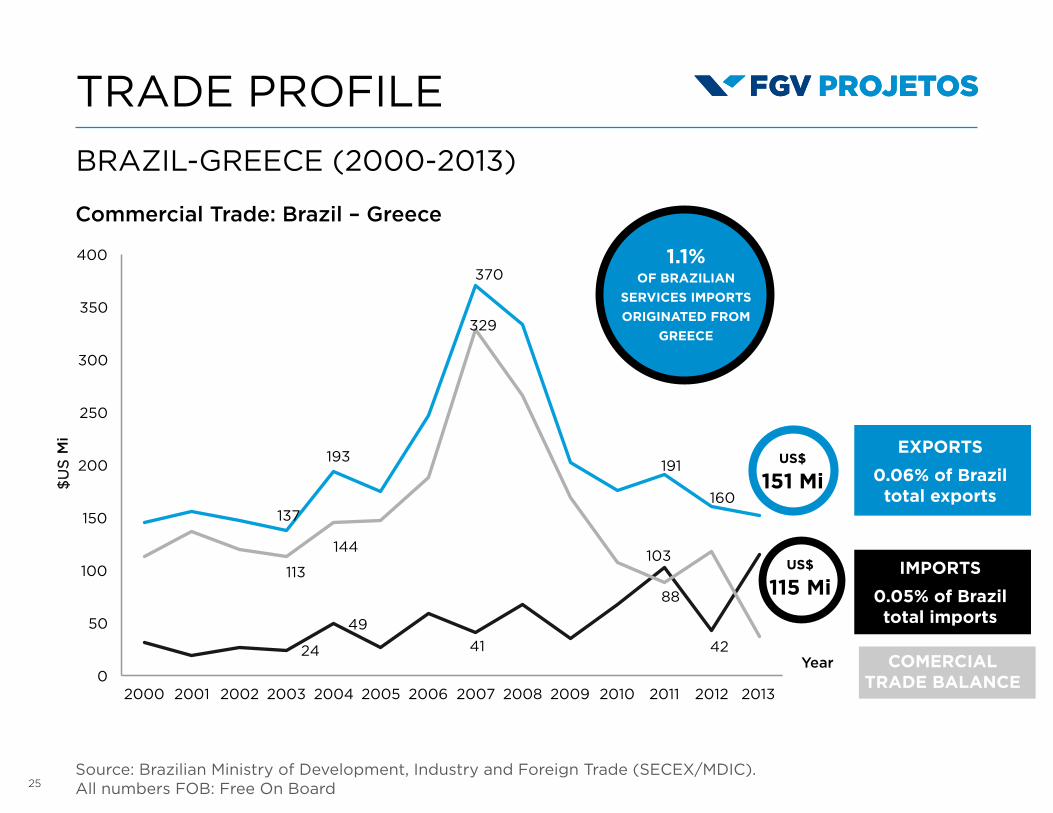

TRADE PROFILE

BRAZIL-GREECE (2000-2013)

Source: Brazilian Ministry of Development, Industry and Foreign Trade (SECEX/MDIC). All numbers FOB: Free On Board

COMERCIALTRADE BALANCE

1.1%OF BRAZILIAN

SERVICES IMPORTS

ORIGINATED FROM

GREECE

Year

Mi

Commercial Trade: Brazil – Greece

US$

151 Mi

US$

115 Mi

EXPORTS

0.06% of Braziltotal exports

IMPORTS

0.05% of Braziltotal imports

26

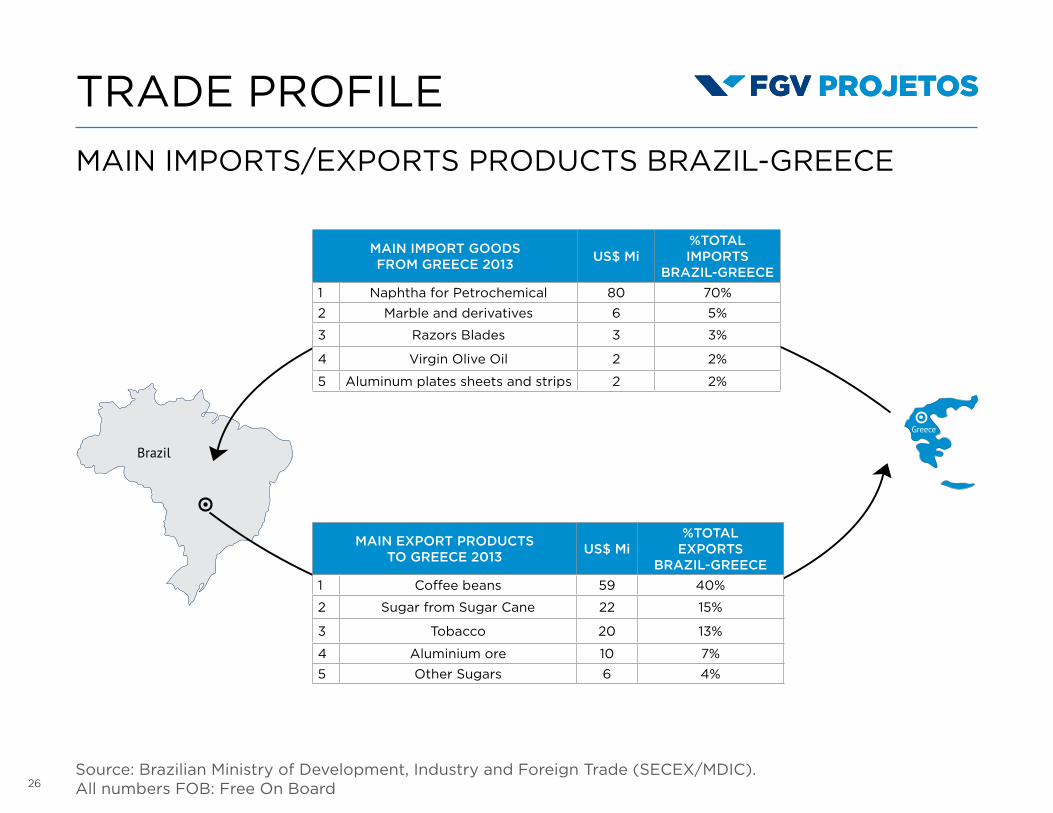

TRADE PROFILE

MAIN IMPORTS/EXPORTS PRODUCTS BRAZIL-GREECE

MAIN IMPORT GOODSFROM GREECE 2013

US$ Mi%TOTALIMPORTS

BRAZIL-GREECE

1 Naphtha for Petrochemical 80 70%

2 Marble and derivatives 6 5%

3 Razors Blades 3 3%

4 Virgin Olive Oil 2 2%

5 Aluminum plates sheets and strips 2 2%

MAIN EXPORT PRODUCTSTO GREECE 2013

US$ Mi%TOTAL

EXPORTSBRAZIL-GREECE

1 Coffee beans 59 40%

2 Sugar from Sugar Cane 22 15%

3 Tobacco 20 13%

4 Aluminium ore 10 7%

5 Other Sugars 6 4%

Source: Brazilian Ministry of Development, Industry and Foreign Trade (SECEX/MDIC). All numbers FOB: Free On Board

27

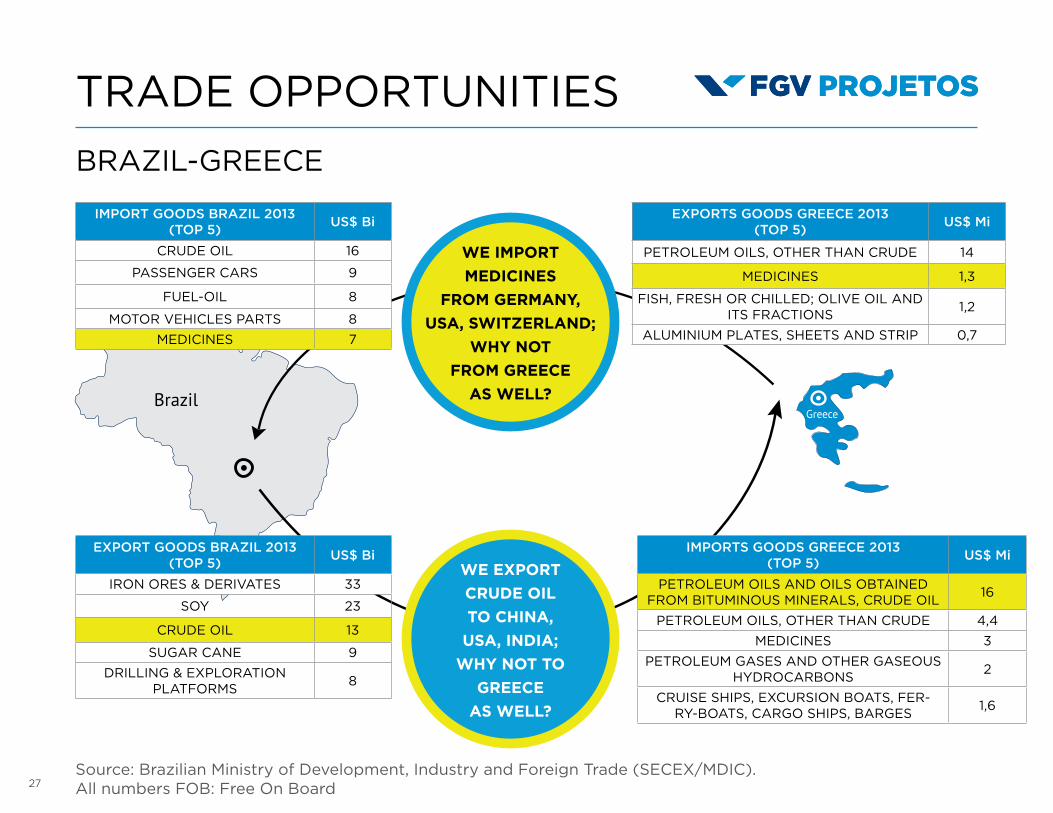

TRADE OPPORTUNITIES

BRAZIL-GREECE

IMPORT GOODS BRAZIL 2013 (TOP 5)

US$ Bi

CRUDE OIL 16

PASSENGER CARS 9

FUEL-OIL 8

MOTOR VEHICLES PARTS 8

MEDICINES 7

EXPORTS GOODS GREECE 2013(TOP 5)

US$ Mi

PETROLEUM OILS, OTHER THAN CRUDE 14

MEDICINES 1,3

FISH, FRESH OR CHILLED; OLIVE OIL AND ITS FRACTIONS

1,2

ALUMINIUM PLATES, SHEETS AND STRIP 0,7

IMPORTS GOODS GREECE 2013(TOP 5)

US$ Mi

PETROLEUM OILS AND OILS OBTAINED FROM BITUMINOUS MINERALS, CRUDE OIL

16

PETROLEUM OILS, OTHER THAN CRUDE 4,4

MEDICINES 3

PETROLEUM GASES AND OTHER GASEOUS HYDROCARBONS

2

CRUISE SHIPS, EXCURSION BOATS, FER-RY-BOATS, CARGO SHIPS, BARGES

1,6

EXPORT GOODS BRAZIL 2013 (TOP 5)

US$ Bi

IRON ORES & DERIVATES 33

SOY 23

CRUDE OIL 13

SUGAR CANE 9

DRILLING & EXPLORATIONPLATFORMS

8

WE IMPORT

MEDICINES

FROM GERMANY,

USA, SWITZERLAND;

WHY NOT

FROM GREECE

AS WELL?

WE EXPORT

CRUDE OIL

TO CHINA,

USA, INDIA;

WHY NOT TO

GREECE

AS WELL?

Source: Brazilian Ministry of Development, Industry and Foreign Trade (SECEX/MDIC). All numbers FOB: Free On Board

28

3. CONCLUSION

29

WHY DOING BUSINESSIN BRAZIL?

1. Stable democracy

2. Leading regional economy & global player

3. Strong financial system and largest stock market in Latin America

4. Gateway to Latin America: Mercosul & ALADI member

5. Safe investment environment: 5th in global FDI inflows

(2013: US$ billion 64; 2.5 % of GDP)

6. Huge domestic market: large and fast growing consumer market

7. Infrastructure investments

Source: Brazilian Investment Information Network (RENAI).

30

GOVERNMENTSUPPORT PARTNERS

In Brazil Local Partners

31

INVITATIONRIO OLYMPICGAMES 2016

TOTAL INVESTMENT OFUS$ 29 BILLIONS

32

CESAR CUNHA CAMPOS

Director, FGV Projetos

www.fgv.br/fgvprojetos

THANK YOU