document of the world bank report no ... - documents...

TRANSCRIPT

Document of The World Bank

Report No: ICR2565

IMPLEMENTATION COMPLETION AND RESULTS REPORT (IDA-38630 TF-55074)

ON A CREDIT

IN THE AMOUNT OF SDR67 MILLION (US$96.39 MILLION EQUIVALENT)

TO

BANQUE OUEST AFRICAINE DE DEVELOPPEMENT (BOAD)

FOR A

WEST AFRICA ECONOMIC AND MONETARY UNION (WAEMU) CAPITAL MARKET DEVELOPMENT PROJECT

February 28, 2013

Finance and Private Sector Department Country Department AFCW3 Africa Region

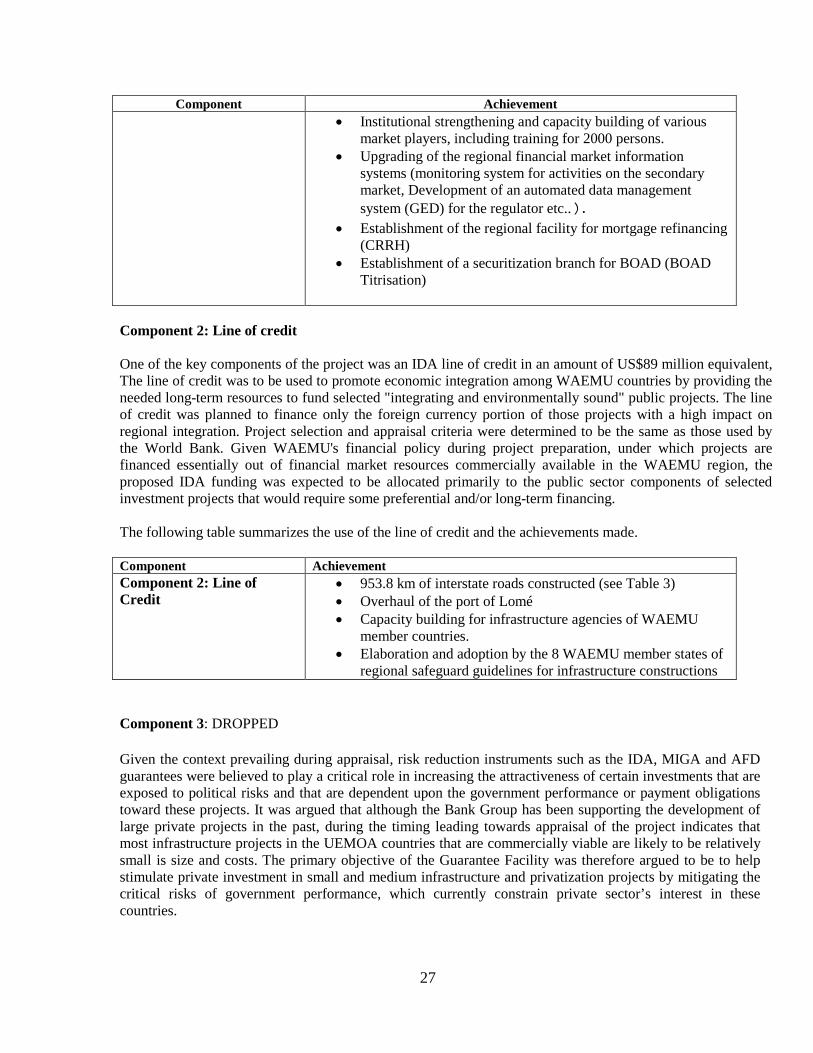

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective November 1, 2012)

Currency Unit = FCFA

US$ 1.00 = 496.7 FCFA US$ 1.00 = 0.66014 SDR

FISCAL YEAR

January 1 - December 31

ABBREVIATIONS AND ACRONYMS ACDI: Agence Canadienne de Développement International AFD: Agence Française de Développement (French Agency for Development) AfDB: African Development Bank BCEAO: Banque Centrale des Etats de 1 Afrique de L’Ouest BIDC: Bank for Investment and Development (ECOWAS) BOAD: Banque Ouest-Africaine de Développement BRVM: Bourse Régionale des Valeurs Mobilières (Regional Stock Exchange) CAS: Country Assistance Strategy CFAF: Communauté Financière Africaine Franc (African Financial

Community Franc) CIDA: Canadian International Development Agency CREPMF: Conseil Régional de l’Epargne publique et des Marches Financiers

(Regional Council for Public Savings and Financial Markets) CRRH: Caisse Régionale de Refinancement Hypothécaire (Regional Mortgage

Refinancing Institution) DCA: Development Credit Agreement ECOWAS: Economic Community of West African States EGDD: BOAD Safeguards Unit GED: Gestion Electronique des Données (Automated Data Management

System) IASC: International Association for Securities Commissions IBRD: International Bank for Reconstruction and Development ICR: Implementation Completion and Results IDA: International Development Association IFC: International Finance Corporation IFRS: International Financial Reporting Standard

ISR: Implementation Status Reports LOC: Line of Credit M&E: Monitoring and Evaluation MIGA: Multilateral Investment Guarantee Agency MOU: Memorandum of Understanding NEPAD: New Partnership for Africa's Development NGO: Non-Governmental Organization O&M: Operation and Maintenance PAD: Project Appraisal Document PCU: Project Coordination Unit PDO: Project Development Objectives PPIAF: Public-Private Infrastructure Advisory Facility PPP: Public-Private Partnerships QAE: Quality at Entry QER: Quality Enhancement Review RIAS: Regional Integration Assistance Strategy SGI: Market Intermediaries SME: Small and medium enterprises TA: Technical Assistance TTL: Task Team Leader WAEMU: West Africa Economic and Monetary Union

Vice President : Makhtar Diop Director, Strategy and Operations : Colin Bruce

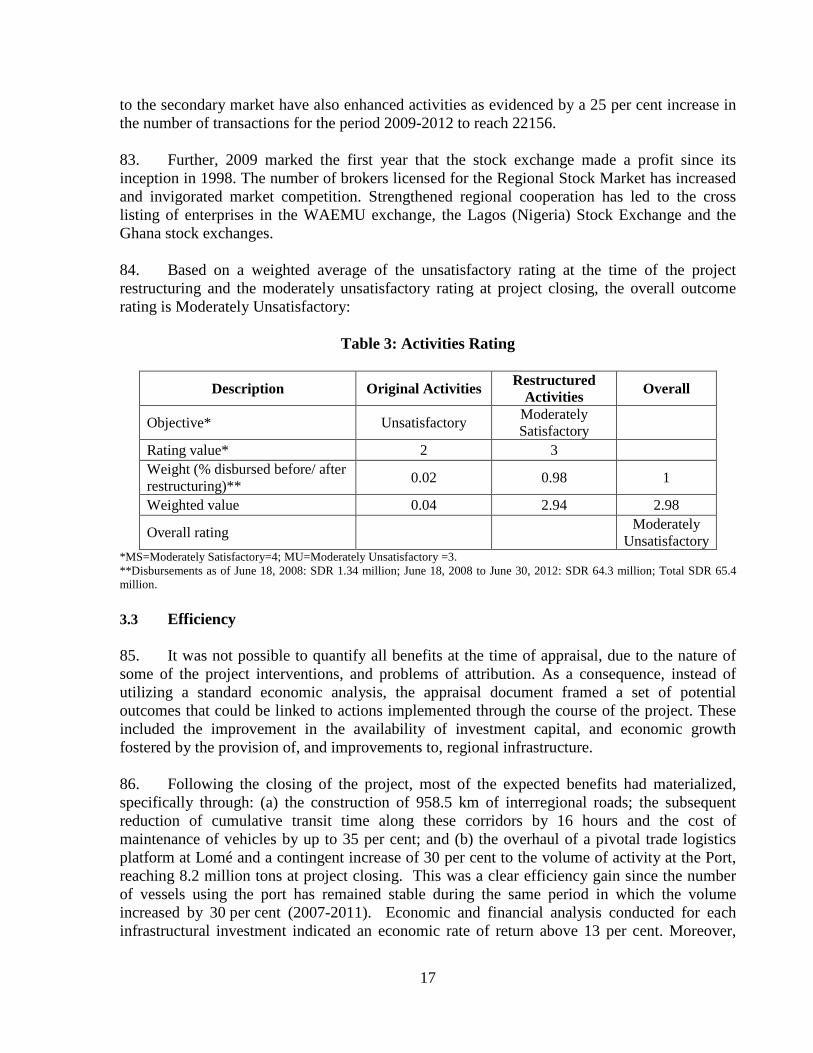

Sector Manager : Paul Noumba Um Project Team Leader : Djibrilla Amadou Issa

ICR Team Leader : Magueye Dia

WEST AFRICA ECONOMIC AND MONETARY UNION WAEMU

CAPITAL MARKET DEVELOPMENT PROJECT

CONTENTS

A. Basic Information ............................................................................................................ i B. Key Dates ........................................................................................................................ i C. Ratings Summary ............................................................................................................ i D. Sector and Theme Codes ................................................................................................ ii E. Bank Staff ....................................................................................................................... ii F. Results Framework Analysis .......................................................................................... ii G. Ratings of Project Performance in ISRs ....................................................................... vi H. Restructuring ................................................................................................................. vi I. Disbursement Profile .................................................................................................... vii 1. Project Context, Development Objectives and Design .................................................. 1

2. Key Factors Affecting Implementation and Outcomes .................................................. 5

3. Assessment of Outcomes .............................................................................................. 10

4. Assessment of Risk to Development Outcome ............................................................ 19

5. Assessment of Bank and Borrower Performance ......................................................... 20

6. Lessons Learned ........................................................................................................... 23

7. Comments on Issues Raised by Borrower/Implementing Agencies/Partners .............. 24

Annex 1 Project Costs and Financing ............................................................................... 25

Annex 2 Outputs by Component....................................................................................... 26

Annex 3 Bank Lending and Implementation Support/Supervision Processes.................. 29

Annex 4 Summary of Borrower's ICR and/or Comments on Draft ICR .......................... 31

Annex 5 List of Supporting Documents ........................................................................... 36

MAP

i

A. Basic Information

Country: Africa Project Name: WAEMU Capital Market Development Project

Project ID: P074525 L/C/TF Number(s): IDA-38630,TF-55074 ICR Date: 02/28/2013 ICR Type: Core ICR

Lending Instrument: FIL Borrower: Banque Ouest Africaine de Développement BOAD

Original Total Commitment: XDR 67.00M Disbursed Amount: XDR 65.64M

Revised Amount: XDR 67.00M Environmental Category: F Implementing Agencies: Banque Ouest-Africaine de Développement Cofinanciers and Other External Partners: Agence Française de Développement Canadian International Development Agency France: Ministry of Foreign Affairs

B. Key Dates

Process Date Process Original Date Revised / Actual Date(s)

Concept Review: 01/23/2002 Effectiveness: 07/29/2005 07/29/2005

Appraisal: 06/04/2003 Restructuring(s): 06/18/2008

Approval: 02/26/2004 Mid-term Review: 01/29/08 11/30/2010

Closing: 09/30/2009 06/30/2012

C. Ratings Summary C.1 Performance Rating by ICR Outcomes: Moderately Unsatisfactory Risk to Development Outcome: Moderate Bank Performance: Moderately Unsatisfactory Borrower Performance: Moderately Satisfactory

C.2 Detailed Ratings of Bank and Borrower Performance (by ICR) Bank Ratings Borrower Ratings

Quality at Entry: Unsatisfactory Government: Moderately Satisfactory

Quality of Supervision:

Moderately Unsatisfactory

Implementing Agency/Agencies:

Moderately Satisfactory

Overall Bank Performance:

Moderately Unsatisfactory

Overall Borrower Performance:

Moderately Satisfactory

ii

C.3 Quality at Entry and Implementation Performance Indicators Implementation

Performance Indicators QAG Assessments (if any) Rating

Potential Problem Project at any time (Yes/No):

Yes

Quality at Entry (QEA): Focused on the Guarantee facility

None

Problem Project at any time (Yes/No): Yes Quality of

Supervision (QSA): None

DO rating before Closing/Inactive status:

Moderately Satisfactory

D. Sector and Theme Codes Original Actual Sector Code (as % of total Bank financing) Capital markets 58 58 Rural and Inter-Urban Roads and Highways 42 42

Theme Code (as % of total Bank financing) Other Private Sector Development 33 33 Regional integration 67 67 E. Bank Staff Positions At ICR At Approval Vice President: Makhtar Diop Callisto E. Madavo Country Director: Colin Bruce Nils O. Tcheyan Sector Manager: Paul Noumba Um Gerard A. Byam Project Team Leader: Djibrilla Adamou Issa Noel K. Tshiani ICR Team Leader: Magueye Dia ICR Primary Author: Magueye Dia F. Results Framework Analysis Project Development Objectives (from Project Appraisal Document) According to the PAD, the principal objective of the project was to develop the capital markets in the West Africa Economic and Monetary Union (WAEMU) region, and mobilize public and private financing for the region's infrastructure development. The project is expected to contribute to the West Africa Economic and Monetary Union (WAEMU) countries' efforts to achieve sustainable regional economic growth through the provision of efficient, region-wide infrastructure services and greater financial market integration. The Development Credit Agreement dated April 24, 2004, stated that the objectives of the Project were to assist the Borrower in developing the UEMOA capital market and in mobilizing public and private financing for the infrastructure development in such region. While there are minor differences between the two, the DCA focused on support towards developing capital market, unlike the PAD statement of outright aim to develop capital markets.

iii

Revised Project Development Objectives (as approved by original approving authority) (a) PDO Indicator(s)

Indicator Baseline Value

Original Target Values (from

approval documents)

Formally Revised Target Values

Actual Value Achieved at

Completion or Target Years

Indicator 1: Number of companies issuing bonds in the regional market (due to new rules and fee structure

Value (quantitative or qualitative)

25 50 48

Date achieved December 31, 2007 May 31, 2012 June 30, 2012

Comments (incl. % achievement)

96% of target met This target has been nearly achieved. Many firms including from CI have raised capital in the regional bond market. Four governments now regularity issue bonds

Indicator 2: Number of companies listed in the regional stock market (due to new rules and fee structure)

Value (quantitative or qualitative)

38 50 39

Date achieved December 31, 2007 December 31, 2010 June 30, 2010

Comments (incl. % achievement)

Target not met This indicator has not progressed much. Although the market has become more regional with companies from other countries listed.

(b) Intermediate Outcome Indicator(s)

Indicator Baseline Value

Original Target Values (from

approval documents)

Formally Revised Target Values

Actual Value Achieved at Completion or

Target Years

Indicator 1: BOAD publicly issues at least CFAF 10 billion bond per year in the regional capital market in 2004 and thereafter.

Value (quantitative or qualitative)

CFAF 7 billion in 2004 CFAF 10 billion per year CFAF 43 billion

Date achieved December 31, 2004 May 31, 2012 June 30, 2012 Comments (incl. % achievement)

430% of target achieved

iv

Indicator Baseline Value

Original Target Values (from

approval documents)

Formally Revised Target Values

Actual Value Achieved at Completion or

Target Years

Indicator 2: From the mid-term review, CREMPF shall inspect at least once a year the Commercial Financial Intermediaries, BRVM and DC/BR.

Value (quantitative or qualitative)

Inspections are far apart Inspections are

regularly conducted

As of December 31, 2012, 86 per cent of

planned inspections was undertaken.

Date achieved December 31, 2012 May 31, 2012 June 30, 2012

Comments (incl. % achievement)

Target was nearly met. Because of important changes at the regional institutions, some missions could not take place. It is important to note that number of inspections was on an upward trend over the last three years and reached 111 per cent of project target in 2011.

Indicator 3 : BOAD is rated by international rating agencies by 2010

Value (quantitative or qualitative)

BOAD has been shadow rated

BOAD is rated and improves by

two notches compared to

shadow rating

BOAD still not rated

Date achieved December 31, 2007 May 31, 2012 June 30, 2012

Comments

Target not met BOAD has prepared a memo to request rating. It will be submitted to rating agencies in 2013.

Indicator 4: Definition of and compliance with a prudential framework by BOAD, in line with internationally accepted best practices.

Value (quantitative or qualitative)

No rules and internationally accepted

standards in BOAD.

New rules and standards defined and

implemented.

Board of BOAD adopted new rules,

including IFRS in 2009. BOARD 2010 and 2011 accounts comply with

the new rules.

Date achieved December 31, 2007 May 31, 2012 June 30, 2012

Comments (incl. % achievement)

Target met

v

Indicator Baseline Value

Original Target Values (from

approval documents)

Formally Revised Target Values

Actual Value Achieved at Completion or

Target Years

Indicator 5: Timely approval and adoption by monetary authorities of new rules and regulations for credit ratings in relation to the removal and substantial relaxation of bank guarantee requirements.

Value (quantitative or qualitative)

100% guarantee is required for bond

issuance.

Rating system is in effect and

guarantee requirement

repealed.

Guarantee requirement rule repealed and new disclosure and rating

based system adopted in Nov 2009. Two rating agencies licensed, IFC,

AFD and Shleter Afrique issued bonds

using the rating system. Date achieved October 31, 2007 May 31, 2012 June 30, 2012 Comments (incl. % achievement)

Target Met The resources have been used to finance public infrastructure and private sector projects.

Indicator 6: Timely approval and adoption by the UEMOA Commission of harmonized taxes regimes on financial products.

Value (quantitative or qualitative)

Taxes on financial products not

harmonized across countries.

New taxes regime

implemented by all countries.

Tax harmonization approved and

implemented in 6 of the 8 countries.

Date achieved December 31, 2007 May 31, 2012 June 30, 2012

Comments (incl. % achievement)

Target met The law has been adopted by the regional council of ministers in Nov 2009, each country has now to enact incorporate the law into its domestic legislation and have it approved by parliament. So far 6 of the 8 countries have done so.

Indicator 7 : Amount of Line of Credit disbursed to regional infrastructures projects (in compliance with IDA fiduciary system).

Value (quantitative or qualitative)

No disbursement on the line of credit. 100% 100%

Date achieved December 31, 2007 May 31, 2012 June 30, 2012 Comments (incl. % achievement)

Target met and exceeded

vi

G. Ratings of Project Performance in ISRs

No. Date ISR Archived DO IP

Actual Disbursements (USD millions)

1 05/27/2004 Satisfactory Satisfactory 0.00 2 12/09/2004 Satisfactory Satisfactory 0.00 3 12/14/2004 Satisfactory Satisfactory 0.00 4 06/30/2005 Moderately Satisfactory Moderately Satisfactory 0.00 5 12/21/2005 Moderately Satisfactory Moderately Satisfactory 0.00 6 06/29/2006 Moderately Satisfactory Moderately Satisfactory 0.39 7 12/31/2006 Moderately Satisfactory Moderately Satisfactory 0.65 8 06/20/2007 Unsatisfactory Unsatisfactory 0.65 9 12/14/2007 Unsatisfactory Unsatisfactory 1.23 10 06/26/2008 Moderately Satisfactory Moderately Satisfactory 1.59 11 12/31/2008 Moderately Satisfactory Moderately Satisfactory 1.59 12 06/28/2009 Moderately Unsatisfactory Moderately Unsatisfactory 1.59 13 12/22/2009 Moderately Unsatisfactory Moderately Unsatisfactory 17.54 14 06/29/2010 Moderately Satisfactory Moderately Satisfactory 28.74 15 04/19/2011 Moderately Satisfactory Moderately Satisfactory 51.04 16 12/27/2011 Moderately Satisfactory Moderately Satisfactory 86.44 17 07/07/2012 Moderately Satisfactory Moderately Satisfactory 97.35

H. Restructuring

Restructuring Date(s)

Board Approved

PDO Change

ISR Ratings at Restructuring

Amount Disbursed at Restructurin

g in USD millions

Reason for Restructuring & Key

Changes Made DO IP

June 18, 2008 Unsatisfactory Unsatisfactory 1.59

Project was restructured mainly to address design issues. Key changes made included: i) Cancelation of the

Line of Credit under Component C;

ii) Expansion of the eligibility criteria of the Line of credit under component B.

Extension of the credit closing date by two years from September 30, 2009 to September 30, 2011 and the IDA managed CIDA trust fund by two years to March 31, 2010.

vii

I. Disbursement Profile

1

1. Project Context, Development Objectives and Design 1.1 Context at Appraisal Regional Context 1. During the decade preceding the preparation of this project, the member countries1 of WAEMU intensified their efforts to more effectively compete in global markets through the integration of economic and financial activities. The WAEMU envisaged the creation of a common market based on the free circulation of people, goods, services, and capital, with aligned commercial policies, and a single external tariff. A number of priorities interventions were identified to be addressed prior to the realization of the envisioned common market. 2. These included: (i) poor capacity on the part of regional institutions which served to undermine the

development of effective capital markets; (ii) absence of benchmark rates; (iii) lack of available long-term capital for investment projects; (iv) lack of financing for private infrastructure projects; (v) weakness enforcement of legal and regulatory frameworks; and (vi) inadequate harmonization of tax policies. 3. The WAEMU countries have made progress in implementing financial sector reforms through the course of the past fifteen years. Notable reforms have included the adoption of a new regional banking law in 1989; the establishment of a regional Banking Commission in 1990; and the introduction of a new regional insurance code. Commercial banks and the insurance sector have concurrently been significantly restructured through the privatization of many larger insurance companies. Moreover, a new regional stock market was established through the creation of the Bourse Régionale des Valeurs (BRVM) in Abidjan, with corresponding branches in each of the member countries. 4. Having successfully implemented these reforms, the WAEMU member countries decided to focus on deepening and improving the functioning of capital markets. Towards this end the Council of Ministers of WAEMU established a Steering Committee for Capital Market activities which drafted an action plan to jump-start stock and bond markets within the Union. 5. The action plan called for, among other things, the strengthening of critical institutions that interact in the capital market, including the West African Development Bank (BOAD), the Conseil Régional, West African Central Bank (BCEAO), the Regional Stock Exchange (BRVM), the WAEMU Commission and brokerage firms, as well as further improvement to the legal and regulatory environment.

1 The eight WAEMU member countries are: Benin, Burkina Faso, Cote d'Ivoire, Guinea-Bissau, Mali, Niger, Senegal and Togo

2

Rationale for Bank assistance 6. The three main objectives of the Bank's Regional Integration Assistance Strategy (RIAS dated July 11, 2001) were: (i) the development of a unified financial market; (ii) the promotion of efficient, region-wide infrastructure services; and (iii) the creation of a more stable and attractive economic environment for all investors. The creation of attractive economic conditions was expected to focus on further financial market integration and the progressive realization of free movement for capital and the harmonization of tax policies to promote private investments. 1.2 Original Project Development Objectives (PDO) and Key Indicators (as approved) 7. The principal objective of the proposed project was, to develop capital markets in the WAEMU region, and to mobilize public and private financing for the region's infrastructure development. The project was expected to contribute to WAEMU countries' efforts to achieve sustainable regional economic growth through the provision of efficient, region-wide infrastructure services and greater financial market integration. 1.3 Revised PDO (as approved by original approving authority) and Key Indicators,

and reasons/justification 8. The PDO was not revised. 1.4 Main Beneficiaries 9. Historically, poorly diversified financial products and services that have failed to meet the various needs of individuals and businesses, and the poor quality and reach of regional infrastructure have been major impediments to regional economic growth in West Africa. The PAD envisioned that the strengthening and expansion of financial infrastructure, and increasing competition would help to improve domestic resource mobilization and stimulate more effective financial intermediation. This in turn would lower financial intermediation costs, the benefits of which would be passed on to private investors and consumers in eligible WAEMU countries. 10. Specific benefits accruing to the population of WAEMU countries would be: (i) the development of an efficient and liquid regional capital market to more effectively finance economic development; (ii) the provision of resources to businesses and individual investors to finance investments and improve opportunities for employment and the extension of more efficient financial services to the population as a whole; and (iii) the development of private commercial financing to support local and region-wide infrastructure development. 1.5 Original Components (as approved) Component 1: Technical Assistance (US$3.52 million) 11. The aim of Technical Assistance and Institutional Support component of the project was to strengthen the regulatory framework for capital market operations as well as the institutional

3

capacity of key institutions involved in regulating and overseeing regional capital markets. Institutions to be targeted were identified to include the BOAD, Conseil Régional, BRVM and commercial intermediaries (SGIs), as well as to the BCEAO and the WAEMU Commission. 12. It was envisaged that technical assistance (TA) and training provided to BOAD would help to expand and diversify its activities, build and update institutional capacity, and improve management and business practices. TA to the CREMPF was expected to focus on improving the regulatory framework for equity and bond markets. The project was planned to provide TA and training to the BCEAO to carry out training seminars for market participants. Finally, assistance was to provide to the WAEMU Commission to study the simplification and streamlining of regional tax regimes for medium-term bonds and other financial or capital market instruments, and to the BRVM to carry out training for staff and market participants. Component 2: Line of Credit (US$89.00 million) 13. The aim of this component was to extend a credit line to provide the long-term resources necessary to fund the foreign currency portion of projects aimed at deepening regional economic integration among WAEMU countries. The proposed IDA funding was to be allocated to the public sector components of selected investment projects that required preferential and/or long-term financing. BOAD, in turn, was expected to lend the resources at a maturity of 25 years with a 7-year grace period for repayment. Component 3: The Guarantee Facility supported by IDA, MIGA and AFD (US$70.00) 14. Supported by guarantee instruments provided under the auspices of IDA (the IDA Guarantee), MIGA (the MIGA Guarantee) and AFD (the French Development Agency - AFD Guarantee), the Guarantee Facility was envisioned to target the financing gap for private projects by catalyzing private investments in small and medium-sized infrastructure projects, including but not limited to privatization. The underlying guarantee investment was envisioned to mitigate real and perceived risks that limited the potential participation of other investors. The Guarantee Facility sought to facilitate access to these instruments for relatively small projects. 15. The use of BOAD as a well-positioned intermediary throughout the region was expected to assist in the accelerated identification and processing of small- to medium-sized infrastructure projects. The deployment of IDA, MIGA and AFD guarantees, with assistance from BOAD, would be complemented by capacity building initiatives targeting BOAD staff to more effectively execute private project financing and risk assessment. Improved capacity would allow BOAD to move away from its traditionally narrow focus limited to the financing of public projects and expand this to include private infrastructure projects through a diversity of financing options. 16. The Guarantee Facility was to be set up with an aggregate amount of about US$227.3 million. IDA and MIGA each committed US$70 million, and the AFD an amount of Euro 70 million.

4

Component 4: Project Implementation (US$3.2million ) 17. Implementation was planned to be coordinated through a Project Coordination Unit (PCU) within BOAD, with oversight from Project Component Managers and a Steering Committee. The PCU was expected to provide technical assistance to key institutions in an effort to improve coordination within and between WAEMU financial markets and institutions (WAEMU Commission, BRVM, Insurance supervisory body and Pension system supervisory committee, etc.). 1.6 Revised Components 18. Due to persistent implementation difficulties, the project underwent level I restructuring in June 2008. The PDO remained unchanged, but project components and activities were readjusted. The Monitoring and Evaluation (M&E) framework was revised to reflect changes applied to the components of the project, and envisaged activities. The table below lists the changes to project activities.

Table 1: Changes to project activities

No. PAD Activities Restructuring 1. Component 1: Technical assistance

and institutional support Activities supported by the project did not undergo major changes. The results framework was consolidated to focus more specifically on outcomes.

2. Component 2: Line of credit. This component was modified to align it with market demands. The finance ceiling for individual projects was raised to US$ 20 million and eligibility criteria expanded to include non-road integrating infrastructure projects (telecom, energy etc.) and cross-border projects related to food security.

3. Component 3: The guarantee facility The restructuring of this component consisted of: (i) cancelling the guarantee facility; (ii) signing a Memorandum of Understanding (MOU) between MIGA and BOAD whereby MIGA agreed to analyze projects presented by BOAD and provide guarantees based on its own Guidelines and Procedures; and (iii) strengthening BOAD’s capacity for risk mitigation through technical assistance allowing BOAD to eventually develop its own guarantee product.

1.7 Other significant changes 19. Implementation timeline. Through the life of the project, the closing date was extended twice for a cumulative period of two years and nine months:

i. As part of the 2008 level I restructuring, the Board approved an extension to the closing date from September 30, 2009 to September 30, 2011.

5

ii. In September 2011, World Bank management approved level II restructuring, extending the closing date by a further nine months to June 2011. The motivation for the second extension was to enable the project to make up for time lost due to the Ivorian crisis, and to improve the likelihood of achieving the PDO.

2. Key Factors Affecting Implementation and Outcomes 2.1 Project Preparation, Design and Quality at Entry

20. Overall, project design was complex and was insufficiently complete prior to implementation. The design was undermined by a lack of detailed technical analysis, incomplete stakeholder analysis, and a contingent failure to build and incorporate a strong partnership and build consensus among stakeholders prior to project effectiveness. The design also included cross conditionality that later contributed to effectiveness delay. 21. Insufficient technical analysis to inform design of project activities: Overall project orientation was premised on the recommendations of the RIAS and the country level strategies of WAEMU member states. However, insufficient attention was paid towards identifying interventions that would specifically contribute to the achievement of the PDO. For example, a demand assessment for the Line of Credit (LOC) was not undertaken during project preparation, and as a consequence there was an initial focus on road infrastructure at the expense of other important priority sectors for WAEMU governments, including power generation. 22. A demand assessment was conducted for the project’s guarantee facility, but this did not identify a pipeline of projects to benefit from the facility. As a consequence no guarantee was issued in the first three years of the facility’s term, which ultimately led to the cancellation of the facility. The failure to adequately assess contextual considerations and latent demand for the guarantee is not specific to this project, as is illustrated by the cancellation of the Peru Guarantee Fund project due to a lack of projects; and the Indonesia Infrastructure Guarantee Funds Project which was dropped after three years. 23. Project Development Objectives were broad and extremely high level. Project design incorporated a large number of stakeholders and envisaged a number of complex interventions each of which could have warranted stand-alone operations. Design was further complicated by the inclusion of four donors (IDA, MIGA, the French Development Agency --AFD, and the Canadian International Development Agency -- CIDA,) each of which had different sets of guidelines, protocols and policies. Direct beneficiaries of the project included five regional institutions of which two were responsible for implementation. Further, indirect beneficiaries of sub-projects funded by the line of credit or supported by the guarantee facility included eight WAEMU member states 24. Incomplete stakeholder analysis: Project design did not identify the full spectrum of stakeholders, and in many instances failed to provide the support to stakeholders necessary for the attainment of development objectives.

25. Oversight to assess capacity of member states: Disbursement of the LOC was dependent on the ability of beneficiary countries to quickly approve and procure finance for

6

projects. At entry, project design paid little attention to the importance of the capacity of country level project implementation units. No assessment was conducted and consequently there was a failure to recognize the critical need for technical assistance, and the contingent failure to plan for sorely needed capacity building activities. 26. Inefficient implementation mechanism: In multi-donor operations one option to simplify implementation is to pool the contributions of donors into a common account managed by a lead institution. In the context of this project, no consensus emerged around the need to establish a common fund. While CIDA and IDA agreed to deposit contributions into a common account to be managed by IDA, the French development agency elected to maintain its contribution separately. 27. As a consequence, to secure no-objection to activities funded by the AFD, documents had to first be reviewed by the AFD prior to an additional review by the World Bank. This extended the time required to secure no-objections and contributed to delays in project implementation. 28. Inadequate framework for partnerships: Project design envisaged the co-financing of sub-projects but neglected to take into account the potential for conflicting procedures governing the procurement of goods and works under the LOC. BOAD submitted eight road packages for funding under the LOC at implementation, all of which were deemed incompatible with IDA protocols. The projects were rejected as they had been initiated by the African Development Bank (AfBD) as the lead co-financier. This was eventually resolved by moving from a system of co-financing to parallel financing. 29. Inadequate demand assessment for the LOC: Due to the absence of a demand assessment at appraisal, the LOC focused solely on inter-regional road infrastructure projects and neglected to take into account the infrastructure development priorities of governments and the private sector (energy, telecom etc.). Moreover, the ceiling for total funding available under the LOC for individual projects was too low. 30. Project design could have integrated some lessons learned from previous projects: Lessons learned from previous guarantee facility operations with regard to: (i) the need for a strong intermediary; (ii) the importance of a well-defined pipeline of projects; and (iii) the need for strong and consistent ownership of project outcomes on the part of the borrower, were only partially incorporated into project design. A demand survey for the guarantee facility conducted during project preparation was limited to only three of the eight countries of the WAEMU, and was insufficiently rigorous given the size of the proposed facility. The absence at project effectiveness of a pipeline of pre-identified sub-projects to be supported by the project, delayed disbursement of the line of credit. 31. Insufficient review of risks: A case in point is the assumption that support to capital market development was expected to lead to an increase in the number of listed companies, driven in part by a privatization program. The PAD did not adequately foresee the risk that privatization programs could be discontinued or delayed and did not include any mitigation

7

measures in this regard. This risk materialized and the indicator related to the increase in the number of firms listed in the secondary market was not met. 2.2 Implementation 32. There were significant delays in the implementation of activities resulting in the closing date for the project being extended twice for a cumulated period of two and a half years. A combination of factors caused these delays and impacted implementation and outcomes:

i. Meeting effectiveness conditions took a year and half. Cross-conditionality between the development credit and guarantee facility agreements was further complicated by the requirement that the credit guarantee had to be ratified by national Parliaments with corresponding legal opinions from the eight Supreme Courts, before the whole project could become effective. An amendment to the guarantee facility agreement was eventually signed by the eight ministers of finance authorizing the guarantee facility agreement to be ratified by four of the member countries to enable effectiveness. This amendment allowed effectiveness to be reached just a couple of days prior to the expiration date of the second extension.

ii. Failure to ensure the signing of a subsidiary agreement between the Bank (managing entity of the CIDA trust fund) and BOAD as the borrower further delayed the implementation of TA components. As a result the first batches of reimbursement requests (funded with proceeds of the CIDA trust fund) were rejected in 2007. Beneficiaries that had pre-financed their activities had to suspend implementation of their work due to cash flow constraints resulting in implementation delays. It took two years to address this flaw.

iii. An absence of infrastructure and environment specialists on the Bank team slowed the review of sub-projects resulting in significant early delays to implementation of the LOC.

iv. A Quality at Entry Review of the guarantee facility was conducted by QAG and rated Unsatisfactory. The review rated the preparation of the facility as unsatisfactory on the ground that the demand assessment was inadequate; and that BOAD was not equipped to act as an effective intermediary.

v. Delays in restructuring: The project did not advance in the first four years of implementation and required a thorough assessment and restructuring. Notwithstanding that the project implementation was suffering from delays, it took more than four years to undertake the restructuring. After four years of implementation, the projects disbursement rate was only two per cent and that for a project expected to be implemented in five year period. Despite a series of restructuring recommendations arising from the QAE review in 2006, restructuring only occurred in June of 2008.

8

vi. Despite the PDO remaining unchanged, project restructuring entailed significant changes including the cancelation of the guarantee facility and the expansion of infrastructure sub-projects, in addition to roads, eligible for financing under the LOC.

vii. Following project restructuring, the Bank’s proactive role contributed to improved

disbursement and project implementation. As an illustration, the Bank team deployed high level missions to countries in support of country-level procurement specialists to expedite procurement process of BOAD financed projects. These measures contributed to a rapid improvement in procurement and a significant increase in the disbursement rate.

viii. Political turmoil in Cote d’Ivoire slowed activities relating to the Stock Exchange

and Capital Market regulator both based in Abidjan. At the height of the crisis, these institutions were closed and relocated to Bamako in 2011.

2.3 Monitoring and Evaluation (M&E) Design, Implementation and Utilization Monitoring and Evaluation Design Rating: Unsatisfactory 33. At entry, key performance indicators in the M&E framework were measurable. However, the framework included some outcome indicators that posed attribution problems or were not based on good practice. For example, increasing the number of firms listed on the BRVM does not solely depend on regulations or fee structures operating in this trading venue, but is also influenced by macro, or firm-specific factors (opportunity to broaden the shareholder base, etc.). Another attribution problem arose with the intermediate indicator tracking the volume of bonds issued by BOAD in CFAF billions which did not take into account the possible effects of currency devaluation and/or inflation on the value of the bonds issued. 34. Following restructuring and the cancelation of the guarantee facility, the M&E framework was amended and the indicators linked to the guarantee facility were dropped. Thereafter the two outcome indicators – “number of companies listed in the regional stock market” and the “number of companies issuing bonds in the regional markets” – only referred to the capital market development aspects of the PDO. As a result, none of the outcome indicators in the M&E framework captured the infrastructure development aspect of the project. 2.4 Safeguard and Fiduciary Compliance Safeguards 35. At entry, BOAD developed and adopted a safeguard policy based on the World Bank’s standard policies. The project helped to establish environmental and social units within BOAD that would be responsible for the management of the safeguard policy for all BOAD financed projects.

9

36. To this end, the capacity of the BOAD safeguards unit (EGDD), and the capacity of beneficiaries, was reinforced to speed-up the review and approval of projects submitted for funding, and to ensure effective safeguard supervision of project implementation. Consultants were hired to carry out environmental audits of the project and to update existing safeguard studies. 37. With project support, the BOAD Safeguard Unit has successfully developed safeguard policies governing all BOAD funded projects and more broadly, all infrastructure projects in WAEMU countries. Financial management was moderately satisfactory 38. In the early phases of project implementation, financial management was compromised by unethical practice on the part of the accountant assigned to the PCU. The contract of individual concerned was terminated in April 2008. In the interim, the financial department of BOAD and an external consultant were retained to support the PCU and mitigate delays in the submission of interim financial reports. Through this period designated accounts remained inactive and the recording of financial data was inadequate. 39. Disbursement was initially slow due to implementation problems (discussed above). Following restructuring improved performance in financial management directly contributed to more effective project implementation. Procurement was satisfactory 40. Overall performance of procurement management is rated Satisfactory. 41. The project required the procurement of large infrastructure, information systems and consultancy services. Delays in procurement mostly affected activities related to the LOC, and were rooted in complex and unclear procurement arrangements and weak country level capacity. The clarification of procurement procedures, the provision of technical assistance, and close monitoring helped to significantly improve procurement management after restructuring. 2.5 Post-completion Operation/Next Phase 42. Following the closure of the project, the institutional arrangements and systems initiated under the auspices of the project have continued to be operational. Financing needs, to a large extent, are being fulfilled from domestic resources. Infrastructure built, as a consequence of the project, has developed their own Operation and Maintenance (O&M). However, the recent crisis in Cote d’Ivoire has underscored the urgent need for the regional financial market to develop a contingency system to allow for the safeguarding of critical information and ensure business continuity in the context of a crisis. 43. Important institutional and regulatory reforms that contributed to improving trading conditions in the regional financial market should be complemented going forward with the

10

development of a new facility with less stringent eligibility conditions to enable SMEs to more easily access the capital market. 44. Despite BOAD not being rated, project support has demonstrably contributed to improving its operations and strengthening institutional capacity. Second-generation reforms and follow-up actions will be required to ensure the sustainability of project outcomes and their resistance to future shocks. Critical to BOAD’s continued relevance and sustainability, and in a context of growing demand from member countries and the private sector, BOAD must obtain a rating to sustain the progress achieved thus far, and to enable the institution to raise more capital on the market. A rating memo, prepared with project support, is expected to be submitted to ratings agencies in 2013. 45. BOAD is now engaged in new initiatives to support the development of mortgage finance through a refinancing facility, as well as the provision of advisory services in support of Public-Private Partnerships (PPPs). It is likely that BOAD will require further technical assistance to develop and successfully implement these new initiatives. In addition, there is an understanding that within the West Africa context, there is a need for a parallel facility to facilitate SME access to capital markets. These activities are beyond the scope of the project under review, but demonstrate that the project has positively contributed to the conditions necessary for the development of functioning capital markets. BOAD has now moved towards further strengthening its capacity and expansion of its area of operations.

3. Assessment of Outcomes 3.1 Relevance of Objectives, Design and Implementation Relevance of the Objectives: High 46. Support for infrastructure development and financial market integration in the service of sustainable regional economic growth in the WAEMU, and the deepening of economic integration remain extremely relevant. Project design accurately incorporated priorities identified by the WAEMU and was aligned with national and regional development strategies including with the Bank’s Regional Integration Strategy for Africa. While overall the objective is highly relevant, whether the project should have taken all the activities included is questionable and it is this ICR’s conclusion that the project should have been trimmed and the interventions planned in sequence. 47. The continued relevance of project objectives is reflected in the recently adopted WAEMU economic plan which emphasizes the deepening of regional financial markets to close regional infrastructure gaps. The development of infrastructure through public-private partnerships is, moreover, identified as a priority objective in National Country Assistance Strategies (CAS) of member states. The project objective both during the design and exit are highly relevant to the conditions in WAEMU and is in line with Bank strategy – both regionally and in the context of individual country strategies. The Project is also reflects the current Africa Strategy (March 2011) which plans to close the gap between infrastructure needs and

11

investments -- currently about $48 billion annually -- and support efforts to make it easier for business to operate.2 Relevance of design 48. Preparatory work was sub-optimal and the choice and design of instruments was in some instances inadequate. Given the initial institutional weakness of BOAD and the poor state of the PPP agenda in the region, it appears that project design was overoptimistic. In addition, the design did not consider sequenced interventions to substantively address the limited capacity of targeted countries. 49. The lack of a thorough demand analysis for the LOC is further buttressed by the fact that the LOC design was not aligned with demand and the development priorities of the region, as evidenced by the effective exclusion of non-road infrastructure sub-projects. 50. The technical assistance component was undermined by an incomplete stakeholder analysis, and the role and importance of market intermediaries was underestimated which, in turn, limited their involvement in efforts to support market development. Relevance of Implementation 51. Despite challenges to implementation in the early stage of the project, (inadequate skill mix, lack of proactivity as evidenced by the delayed restructuring) which were addressed through project restructuring, the Bank’s implementation support was relevant.

3.2 Achievement of Project Development Objectives 52. The achievement of the PDO is rated Moderately Unsatisfactory. The ICR rating weighed heavily the amount of time required to implement project objectives, in addition to the relevance and achievement of the stated objectives. In addition, the overall rating will be a weighted average of project performance before and after restructuring. 53. The last ISR of the Project rated the outcome as Moderately Satisfactory. This rating is correct if the time element is not included and if the rating refers to the implementation and achievements after project restructuring. The timing element is critical because of the unaccomplished activities, such as rating of BOAD, which is now in process, would have been completed earlier. The ICR authors find it very difficult to justify the Moderately Satisfactory rating given that the project has to drop some activities and has delivered only on one of the three outcome indicators even recognizing the weakness of the indicators chosen. Also, it is the conclusion of this ICR that the indicators should have been revised during the restructuring.

2 Africa’s Future and the World Bank’s Support to It http://siteresources.worldbank.org/INTAFRICA/Resources/AFR_Regional_Strategy_3-2-11.pdf

12

Before restructuring Rating: Unsatisfactory 54. Delays were experienced throughout the implementation of the LOC and the guarantee facility. After four years of implementation, aside from successes in deploying TA, project implementation remained poor. As of January 2008, not a single guarantee had been issued and not one infrastructure project had been financed under the LOC. Furthermore, most reforms envisioned in the project required additional time to be completed. Unsurprisingly, not one of the three outcome indicators, and none of the intermediate outcome indicators, had been met and disbursement stood at two per cent, four years after Board approval. This serious underperformance in project implementation translated into a three year disbursement lag. After restructuring Rating: Moderately Unsatisfactory 55. Bold restructuring was undertaken to realign the project to the borrower’s priorities and context. Close supervision was provided to accelerate implementation. Following restructuring, project performance was significantly improved with a dramatic hike in activity and the materialization of tangible impacts across components. 56. As previously indicated, there were a number of shortcomings in the original M&E framework to preclude an evaluation of the project achievements based on outcome indicators. The indicator aiming to measure the development of the capital market premised on the “Number of firms listed in the regional secondary market” generates attribution problems as the conditions informing decisions by firms to list on a stock market are influenced by factors beyond the scope addressed by project assistance. Moreover the “mobilization of public and private financing for infrastructure development” part of the PDO was not captured in the development outcome indicators3. 57. Against this background, achievement of the PDO post-restructuring will be assessed by initially discussing the outcome indicators and then providing alternate evidence to show results achieved by the project and directly connected to the PDO, even if these are not fully captured by the M&E framework Analysis of development outcome indicators 58. Outcome Indicator #1: “Number of companies issuing bonds in the regional market”: The number of firms that engaged in raising funds from the regional capital market increased from 25 to 48 at project closing, just two units short of the target of 50. In addition to these private companies, four member countries of the WAEMU now routinely raise funds in the capital market through the issuance of bonds; a positive externality associated with the project.

3 The intermediate outcome indicator relating to the amount of the LOC disbursed to regional infrastructure projects partly captures achievements in relation to this aspect of the PDO

13

59. Outcome Indicator #2: “Number of companies listed in the regional stock market”: As of June 30, 2012, the net number of companies listed in the stock market had increased from the baseline by only one unit, from 38 to 39, against a target of 50. Given their nature and scope4, project interventions in isolation were not sufficient to ensure a 20 per cent increase in the number of firms listed on the regional trading venue. 60. It had been expected that improvements to the market structure (supported by the project) combined with the completion of the privatization programs (over which project had no control) in WAEMU member countries would boost company listings on the BRVM. This outcome was undermined by the discontinuation of privatization programs in the region.5

Project outputs related to the PDO 61. Following restructuring, the project achieved marked results that can be directly linked to the PDO, but these are not fully reflected in the M&E framework. Table 2 illustrates the results chain. Notwithstanding these positive developments, the ICR questions the time period required to achieve these results. A detailed description of component outcomes is presented in Annex 2.

Table 2: PDO Results Chain

PDO Main Related Output Causal link to PDO

Mobilization of public and private financing:

US$ 89 million Line Of Credit was fully disbursed

direct

US$ 346 million donors resources were mobilized

Direct

US$ 67 million raised in the market direct

BOAD has become an important development finance institution

indirect

Provision of regional infrastructure

11 sub-projects have financed the construction of 953.8 km of interstate roads

direct

Port of Lomé was upgraded direct

Enhancement of the integration

Tax regimes as applied to financial products across all eight countries were harmonized

direct

Capital Market fee structures were revised and simplified

direct

4 Consisted in technical assistance to improve the regulatory framework and make public listing less costly but did little to convince private owned firms or even client governments to list their firms on the regional stock market. 5 It is important to note that few private firms in member countries were capable of meeting the stringent eligibility conditions necessary for listing, while others were unwilling to comply with disclosure rules.

14

PDO Main Related Output Causal link to PDO

The harmonization of the accounting system for financial intermediaries

indirect

Performance of the Regional Capital market

The reform of the credit guarantee system and the introduction of a disclosure and a rating system

indirect

A legal framework governing the mortgage market was established

direct

Key institutions for the primary mortgage market were established and operationalized: The CRRH, a regional mortgage refinancing institution; and “BOAD Titrisation”, the securitization branch of BOAD

direct

BOAD has implemented institutional reforms indirect

62. The following review of achievement of PDO based on alternative evidence is divided in two parts, each focusing on one of the specific targets, namely: (i) the mobilization of public and private financing for the provision of regional infrastructure; (ii) the enhancement of the integration and performance of the Regional Capital market. Mobilization of public and private financing for the provision of regional infrastructure:

63. The project directly contributed to the mobilization of public and private funds in support of regional infrastructure development. Resources mobilised through the LOC have contributed to the construction of important portions of four regional corridors and the upgrading of the port of Lomé. 64. The total costs of these projects amounted to US$ 506 million (financed by $156 million of which US$ 89 million from the LOC and US$67 million from resources raised in the market) and other donors for US$ 350 million. In line with the development objectives of the project, the resources of the LOC successfully leveraged other resources (from BOAD, the private sector and other donors) at a ratio of 1 to 6 in support of infrastructure development. 65. At project closing 11 sub-projects had financed the construction of 953.8 km of interstate roads. (See table in annex 2). 66. The new roads will also contribute to increasing access to health and education services for rural communities, and help facilitate market access. For example, the volume of cereals and milk traded is expected to rise by 25 and 10 per cent respectively (to reach respectively10.000 litre, and 6500 Tons) on the Mali Senegal southern corridor. 67. The upgrading of the Lomé port has significantly improved the efficiency of this important logistical platform for neighbouring landlocked countries (Burkina, Niger). Truck access to the port has been improved with the construction of a 40,000 square meter parking

15

area. Security in the port has substantially improved and has been certified ISPS. Water and electricity supply has also substantially improved as a consequence of project support. 68. Project support played an important hand in the strengthening of the capacity of BOAD as a development finance institution. BOAD is now in a position to raise capital from the regional capital market, effectively extend public and private project finance loans, and offer technical assistance to member countries. 69. As an illustration, BOAD’s contribution to the execution of the road program of the Economic Regional Program (2006-2010) amounted to US$ 246 million, exceeding the cumulated funding provided by ECOWAS Investment Development Bank (BIDC) and IDA (US$ 226 million). BOAD has developed its fiduciary capacity and has established safeguard policies overseen by a dedicated environmental unit for all infrastructure projects. 70. BOAD is now a more profitable and efficient institution and is preparing to initiate steps to ensure that it is rated by sovereign credit agencies. The memo to rating agencies has been prepared but was placed on hold on the advice of the Board due to the financial crisis. It should be restarted early 2013. Enhancement of integration and performance of the Regional Capital market 71. The project contributed to the achievement of this aspect of the PDO through the implementation of market reforms, and the establishment and strengthening of key market players, which are discussed below. Reform of the legal framework and structure of the Market 72. Major structural reforms to the regional financial market implemented under the auspices of the project included: (i) the reform of the credit guarantee system and the introduction of a disclosure and rating system; (ii) the harmonization of tax regimes as applied to financial products across all eight countries; and (iii) the revision and simplification of capital market fee structures, (iv) the harmonization of the accounting system for financial intermediaries, and (v) the establishment of a legal framework governing the mortgage market. 73. The harmonization of taxes on financial products has contributed to the deepening of financial market integration by increasing transparency, removing double taxation between countries, and reducing country-level inconsistencies regarding taxation of capital gains. Reforms to the accounting framework governing market intermediaries, has contributed to the improvement of the quality of financial information generated by market intermediaries. 74. Following the revision of the capital market fees structure, fees for issuers on the primary market have been reduced up to 75 per cent. On the secondary market the fees structure has been optimized and ensures better repartition of transaction costs between market actors.

16

Strengthening and establishment of key market players 75. Important capacity building activities undertaken as a consequence of the project contributed directly to the strengthening and improved efficiency of the market regulator. Following project interventions, the time required for listing and the issuance of bonds by companies or governments has been cut in half. An evaluation conducted by the International Association for Securities Commissions (IASC) found that the regulator adequately performs its role in supervising and regulating market activities. 76. The project assisted BOAD to implement reforms including: (i) the adoption of a modern assets/liability management system; (ii) reform to the liquidity management system to increase predictability and efficiency; (iii) improved human resource planning and management; and (iv) the adoption of the international accounting standard (IFRS). 77. BOAD is, as a consequence of project interventions, more profitable and efficient, and has increased its capacity to issue bonds in the regional market. Over the last five years (2007-2012), BOAD was able to raise more than US$ 500 million on the regional financial market. This represents 51 per cent of resources borrowed by BOAD, compared to only 35 per cent in the period 2003 through 2007. 78. Institutional strengthening improved borrowing conditions, enabling BOAD to become a benchmark issuer in the regional market in a context where previously no single country was able to play that role. 79. The project contributed to BOAD reaching the final stage of preparation for rating. The memo to rating agencies has been prepared but was put on hold on the advice of the Board due to the financial crisis. 80. The project helped to establish and operationalize two key institutions for the primary mortgage market: The CRRH, a regional mortgage refinancing institution created in July 2011; and “BOAD Titrisation”, the securitization branch of BOAD created in December 2011 with a mandate to promote securitization as a financing instrument in the WAEMU. 81. Assistance provided by the project contributed to the finalization of procedures manuals, the installation of information systems, the purchase of specialized software and the setting-up of an intranet and external website. Both institutions are fully operational. In July 2012, CRRH raised, around US$ 25 million by issuing bonds on the regional financial market. As a consequence, CRRH has refinanced the mortgage portfolios of nine regional banks at ten years maturity and an interest rate of 6.1 per cent. This in turn has contributed to the extension of cheap long-term housing finance to the customers as well as to other banks unable to issue bonds or do securitization. 82. The impact of the project’s interventions to develop the regional financial market is evident in an increase of 75 per cent in the issuing of bonds, moving from US$ 400 million over the period 2005-2008 to US$ 700 million over the 2009-2012 period, which translates into 65 per cent growth in primary market capitalization (US$ 1.6 billion as of October 2012). Reforms

17

to the secondary market have also enhanced activities as evidenced by a 25 per cent increase in the number of transactions for the period 2009-2012 to reach 22156. 83. Further, 2009 marked the first year that the stock exchange made a profit since its inception in 1998. The number of brokers licensed for the Regional Stock Market has increased and invigorated market competition. Strengthened regional cooperation has led to the cross listing of enterprises in the WAEMU exchange, the Lagos (Nigeria) Stock Exchange and the Ghana stock exchanges. 84. Based on a weighted average of the unsatisfactory rating at the time of the project restructuring and the moderately unsatisfactory rating at project closing, the overall outcome rating is Moderately Unsatisfactory:

Table 3: Activities Rating

Description Original Activities Restructured Activities Overall

Objective* Unsatisfactory Moderately Satisfactory

Rating value* 2 3 Weight (% disbursed before/ after restructuring)** 0.02 0.98 1

Weighted value 0.04 2.94 2.98

Overall rating Moderately

Unsatisfactory *MS=Moderately Satisfactory=4; MU=Moderately Unsatisfactory =3. **Disbursements as of June 18, 2008: SDR 1.34 million; June 18, 2008 to June 30, 2012: SDR 64.3 million; Total SDR 65.4 million. 3.3 Efficiency 85. It was not possible to quantify all benefits at the time of appraisal, due to the nature of some of the project interventions, and problems of attribution. As a consequence, instead of utilizing a standard economic analysis, the appraisal document framed a set of potential outcomes that could be linked to actions implemented through the course of the project. These included the improvement in the availability of investment capital, and economic growth fostered by the provision of, and improvements to, regional infrastructure. 86. Following the closing of the project, most of the expected benefits had materialized, specifically through: (a) the construction of 958.5 km of interregional roads; the subsequent reduction of cumulative transit time along these corridors by 16 hours and the cost of maintenance of vehicles by up to 35 per cent; and (b) the overhaul of a pivotal trade logistics platform at Lomé and a contingent increase of 30 per cent to the volume of activity at the Port, reaching 8.2 million tons at project closing. This was a clear efficiency gain since the number of vessels using the port has remained stable during the same period in which the volume increased by 30 per cent (2007-2011). Economic and financial analysis conducted for each infrastructural investment indicated an economic rate of return above 13 per cent. Moreover,

18

technical assistance provided to the regional financial market institutions, and to BOAD, led directly to the execution of important reforms that strengthened the regional capital market. TA, moreover, contributed to the transformation of the BOAD into a more profitable regional development finance institution, with a larger stock of capital and a benchmark issuer of bonds in the regional market 87. Delivery of these objectives helped to further develop regional consultancy services, boosted demand for local equipment vendors, and funded construction of road infrastructure. Analysis of roads constructed indicates that least-cost approach was followed with the cost per km of road constructed under the project falling below the regional average of US$ 800,000.

88. Project interventions helped to halve the time required to process the listing and the issuance of bonds by companies or governments. Commissions (IASC) found that the regulator adequately performs its role in supervising and regulating market activities 89. As indicated in Annex 1 actual costs at project closure amounted to US$100.6 million, which compare favorably with estimated costs at appraisal of US$102.6 million, while achieving most of what it set out to do. This shows an actual spending of 98.11 per cent that could be characterized as an efficiency gain. Evidence of efficiency in utilizing the credit proceeds are provided by the least cost approach followed for the procurement of road construction discussed below, but also in the cost of project implementation. Some of the PIU experts were hired by BOAD to staff the safeguard unit created with project support and to strengthen its existing infrastructure department. These staff were moved to the BOAD payroll. 90. Total Bank administrative costs for project supervision over the 9 years implementation period were $1,107,600, or an average per annum of $123,000 which was slightly above the Africa regional annual average of $110,000. The slightly higher cost may be explained by the characteristics of this operation (multi-donor, multi-sectoral, regional project) and the high level of coordination required. 91. However, the overall efficiency is compromised by the time needed to achieve the result. Since time is a major factor in efficiency achievement, again, given the number of years taken to achieve this level of efficiency, it is rated as Modest. 3.4 Justification of Overall Outcome Rating Rating: Moderately Unsatisfactory 92. Despite a cumbersome design, which led to significant delays in implementation, restructuring enabled the project to achieve a substantial part of the PDO. Important reforms have been supported to improve the regulatory framework and cost structure of regional financial markets. Capacity building has contributed to the strengthening of the regulatory body and has enhanced its credibility. Project resources helped to leverage donor and private sector money to develop and enhance regional infrastructure. Technical assistance provided to BOAD transformed this key regional development finance instrument into a strong institution able to extend public and private project finance loan and TA to member countries.

19

3.5 Overarching Themes, Other Outcomes and Impacts (a) Poverty Impacts, Gender Aspects, and Social Development (b) Institutional Change/Strengthening 93. The construction of regional infrastructure (roads, logistic platforms) under the auspices of the project positively contributed to the deepening of economic and financial integration in the WAEMU Zone. The project contributed to strengthening of regional financial market institutions, and the BOAD has strengthened its operations, fulfilled all requirements for rating and has developed in-house capacity for safeguards management. BOAD is now an efficient and profitable development finance institution and a benchmark issuer in the regional market. The regional regulator of the capital market is stronger and more efficient. The time required to process a listing or bond issuance request has been significantly reduced. The BRVM has become profitable, ten years after its inception. 94. The project moreover supported a feasibility analysis of the housing refinancing facility as well as its operationalization. The latter included the formulation of procedures manuals, the procurement of IT equipment, specialized software and a Website. At project closing, the CRRH was fully operational and had successfully raised funds from the regional capital market. (c) Other Unintended Outcomes and Impacts (positive or negative)

4. Assessment of Risk to Development Outcome Rating: Moderate 95. The project’s main deliverables were focused in the areas of road infrastructures, institution and capacity building, and financial markets regulatory framework. Road and logistical infrastructure are largely irreversible once constructed and are likely remain in place after project closing if proper maintenance is undertaken. Road maintenance funds have been created in most WAEMU member states and could contribute to the maintenance of infrastructure funded by the project. 96. Important investments in building the capacity of the CREMPF has contributed to the institutional strengthening of the main supervisory and regulatory authority of the regional financial market. These outcomes will require timely follow-up in order to guarantee the sustainability of the institutional changes. The recently approved Regional Economic Program indicates a strong commitment on the part of the WAEMU commission or members to deepen the capital market and envisions the provision of resources to ensure the required follow-up interventions to sustain the institutional changes supported by the project. 97. The risk of reversal of improvements to the financial market regulatory framework and the fee structure is low. Tax reforms implemented under the project are now regional directives and cannot be overturned at the national level. Strong competition from trading venues in Accra,

20

Libreville, Douala, and Casablanca will make it difficult for the BRVM to reverse its fee structure and the reduction of costs supported by the project.

98. Technical knowledge provided to BOAD to support project implementation will remain in the institution after project closing. Experts recruited to the PU to support project implementation have been permanently hired by BOAD to staff the safeguard unit created with project support and to strengthen its existing infrastructure department.

99. Project support to BOAD in the areas of assets/ or liquidity management, as well as on the fundamental functions of internal audit and human resources management, have contributed to transforming BOAD into a profitable institution. The envisioned rating of the institution in 2013 should help maintain and sustain the progress achieved.

5. Assessment of Bank and Borrower Performance 5.1 Bank Performance (a) Bank Performance in Ensuring Quality at Entry Rating: Unsatisfactory 100. The PDO was consistent with the WAEMU priorities and the Bank’s strategy at project inception. Issues to be addressed built on existing national strategic plans and policies, and were properly identified. 101. However, project design was complex, with a cumbersome array of interventions and beneficiaries. Not all risks and mitigation measures were adequately identified, and when articulated, were not commensurate with the implications of realization of these risks. 102. The main shortcoming of project design was the inadequate assessment of demand for the guarantee facility and the failure to identify capacity shortcomings at BOAD. Project design was insufficiently flexible to accommodate critical infrastructures needs beyond those associated with roads. Both of these shortcomings were later addressed through restructuring (guarantee canceled, eligibility criteria of the line of credit expanded and ceiling increased). 103. Other shortcomings included:

i) Complex cross-conditionality between the DCA and the guarantee facility agreement that required the approval of the latter by the eight national parliaments of the WAEMU member countries, with judicial opinion from respective supreme courts. Inability to control or manage this process contributed to effectiveness delays.

ii) Project design envisioned co-financing of sub-projects funded by the LOC credit

but overlooked the implications of such arrangements in terms of procurement management. Internal institutional protocols required co-financiers (often the lead

21

financier) to apply their own procedures in addition to IDA procedures. This contributed to delays during the implementation of the LOC, which were only resolved by moving from co-financing to parallel financing.

104. The budget devoted to preparation (US$1.1 million) was commensurate with the regional dimension and the complexity of the operation, and reflects the level of support provided by the regional integration department and country management of WAEMU member countries. 105. The Bank’s performance in ensuring quality at entry is therefore rated Unsatisfactory. (b) Quality of Supervision Rating: Moderately Unsatisfactory 106. Supervision was conducted regularly, with approximately two missions per year. There were three Task Team Leaders (TTLs) over the course of the project life. The final two TTLs were located in the field. The turnover of TTL did not negatively impact implementation support or significantly disrupt continuity of dialogue with the borrower. 107. Bank’s performance during the 8 years of project implementation was mixed but improved substantially following the restructuring of the project.

108. Prior to restructuring bank supervision was less than satisfactory because of inadequate skill mix in the task team and a lack of proactivity. Specifically, the team could have been more proactive in ensuring a more timely restructuring of the project. 109. Implementation Status Reports (ISRs) were regularly updated, with management regularly commenting on ISRs and providing guidance to the team. However, the overall performance ratings through the early stages of the project may have been too optimistic. For example between 2004 and 2006, implementation progress and development objectives were assessed to be moderately satisfactory despite a disbursement rate of only 2 per cent and the failure to initiate flagship activities (LOC, guarantee facility). This was only downgraded to moderately unsatisfactory in October 2007. 110. Management of the CIDA trust fund was inadequate. Delays in the signing of agreements between the Bank and CIDA and the Bank and BOAD negatively affected the mobilization of the TA Component. 111. Following a TTL change in early 2008, bold restructuring was undertaken to refocus project activities and align them with the priorities and capacity of the borrower. The guarantee facility was canceled, the eligibility conditions for the LOC expanded to include non-road infrastructure, and the cap on financing of individual sub-projects was raised. The restructuring recommended utilization of parallel financing instead of co-financing to resolve procurement inconsistencies between co-financiers. Internal restructuring entails the formation of a stronger task team staffed with a more applicable mix of skills. Following the formalization of the

22

restructuring initiative, the task team reengaged with the project and gave it the needed impetus to expedite implementation and achieve the full development objective. However, restructuring failed to address significant shortcomings in the M&E framework, and an opportunity was missed to more effectively align outcome indicators to the different aspects of the PDO. 112. Innovative measures were implemented by the task team to boost disbursement. Under the Line of Credit Component, Project Coordination was urged to conduct regular missions to beneficiary member countries to provide assistance to the units in charge of procurement of supported projects, and to brief governments regarding associated risks and the need to take bold actions. This initiative helped expedite the procurement process at the national level and was instrumental in achieving full disbursement with regard to the Line of Credit.