discussion “in search of a nominal anchor: what drives

TRANSCRIPT

DISCUSSIONldquoIn search of a nominal anchorWhat drives long-term inflation

expectationsrdquoby Carvalho EusepiMoench and Preston

Elmar Mertens

Federal Reserve Board

The results presented here do not necessarily representthe views of the Federal Reserve Systemor the Federal Open Market Committee

September 29 2016

OVERVIEW

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

OVERVIEW

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

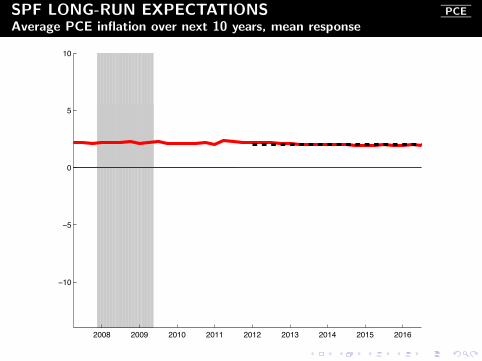

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 20160

05

1

15

2

25

3

35

4

45

5

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

PCE headline inflation (monthly change APR) SPF 10-year expectation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue 12m-inflation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

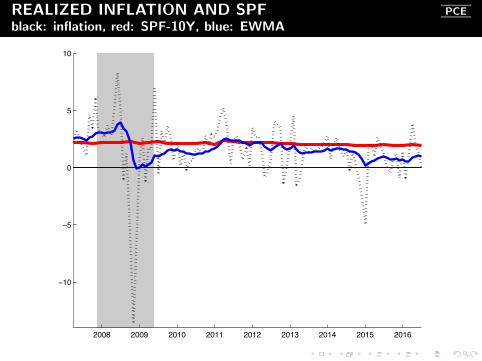

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue EWMA

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus K)τtminus1|tminus1 + Kπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UC model

πt = τt + πt τt = τtminus1 + ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus Kt)τtminus1|tminus1 + Ktπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UCSV model

πt = τt + πt τt = τtminus1 + σηt ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TIME-VARYING EWMA WEIGHT ldquoUCSVrdquoStock and Watson (2006 JMCB) partπt+infinpartet = Kt

1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

01

02

03

04

05

06

07

08

09

1

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

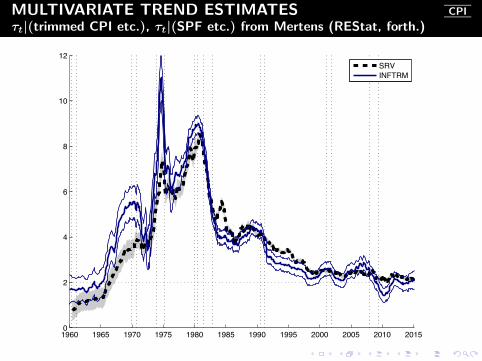

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12SRVINFTRM

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

SRVINFTRMCEMP

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

THIS PAPER

Ingredients

bull DSGE model with NK-Phillips Curve

bull Twist Learning with ldquoSS bandsrdquo for updating

πt =9830541 minus kminus1

tminus1

983055πtminus1 + kminus1

tminus1

983070πt minus (Etminus1πt minus πtminus1)

983071

kt =

983094ktminus1 + 1 if |Φ(past FE)| lt ν

gminus1 otherwise

Endogenous data feeds into learning behavior

bull Endogenous trend

bull State-dependent sensitivity of trend πt to data

bull Once anchored can tolerate deviations of inflation fromtrend up to a point

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SOME THOUGHTS

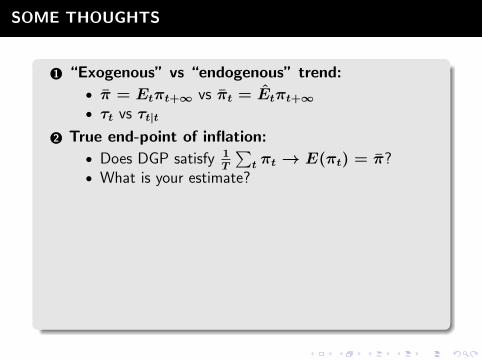

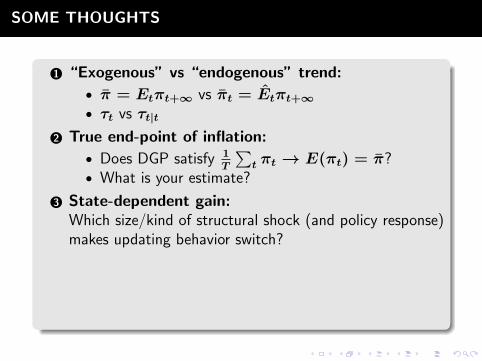

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2

True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SKETCH OF AN ALTERNATIVE MODEL

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τ

t

+ γπtminus1)

τt=τtminus1 + ηt

Monetary policy with inflation target τ

t

it = rt + τ

t

+ φπ(πt minus τ

t

) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

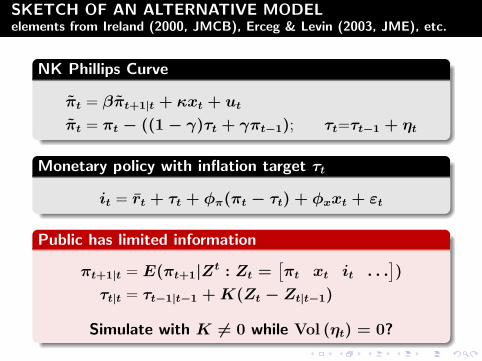

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB)

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt = τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4 Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

CONCLUSION

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

OVERVIEW

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

OVERVIEW

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 20160

05

1

15

2

25

3

35

4

45

5

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

PCE headline inflation (monthly change APR) SPF 10-year expectation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue 12m-inflation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue EWMA

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus K)τtminus1|tminus1 + Kπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UC model

πt = τt + πt τt = τtminus1 + ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus Kt)τtminus1|tminus1 + Ktπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UCSV model

πt = τt + πt τt = τtminus1 + σηt ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TIME-VARYING EWMA WEIGHT ldquoUCSVrdquoStock and Watson (2006 JMCB) partπt+infinpartet = Kt

1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

01

02

03

04

05

06

07

08

09

1

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12SRVINFTRM

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

SRVINFTRMCEMP

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

THIS PAPER

Ingredients

bull DSGE model with NK-Phillips Curve

bull Twist Learning with ldquoSS bandsrdquo for updating

πt =9830541 minus kminus1

tminus1

983055πtminus1 + kminus1

tminus1

983070πt minus (Etminus1πt minus πtminus1)

983071

kt =

983094ktminus1 + 1 if |Φ(past FE)| lt ν

gminus1 otherwise

Endogenous data feeds into learning behavior

bull Endogenous trend

bull State-dependent sensitivity of trend πt to data

bull Once anchored can tolerate deviations of inflation fromtrend up to a point

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2

True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SKETCH OF AN ALTERNATIVE MODEL

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τ

t

+ γπtminus1)

τt=τtminus1 + ηt

Monetary policy with inflation target τ

t

it = rt + τ

t

+ φπ(πt minus τ

t

) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB)

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt = τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4 Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

CONCLUSION

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

OVERVIEW

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 20160

05

1

15

2

25

3

35

4

45

5

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

PCE headline inflation (monthly change APR) SPF 10-year expectation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue 12m-inflation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue EWMA

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus K)τtminus1|tminus1 + Kπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UC model

πt = τt + πt τt = τtminus1 + ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus Kt)τtminus1|tminus1 + Ktπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UCSV model

πt = τt + πt τt = τtminus1 + σηt ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TIME-VARYING EWMA WEIGHT ldquoUCSVrdquoStock and Watson (2006 JMCB) partπt+infinpartet = Kt

1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

01

02

03

04

05

06

07

08

09

1

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12SRVINFTRM

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

SRVINFTRMCEMP

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

THIS PAPER

Ingredients

bull DSGE model with NK-Phillips Curve

bull Twist Learning with ldquoSS bandsrdquo for updating

πt =9830541 minus kminus1

tminus1

983055πtminus1 + kminus1

tminus1

983070πt minus (Etminus1πt minus πtminus1)

983071

kt =

983094ktminus1 + 1 if |Φ(past FE)| lt ν

gminus1 otherwise

Endogenous data feeds into learning behavior

bull Endogenous trend

bull State-dependent sensitivity of trend πt to data

bull Once anchored can tolerate deviations of inflation fromtrend up to a point

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2

True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SKETCH OF AN ALTERNATIVE MODEL

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τ

t

+ γπtminus1)

τt=τtminus1 + ηt

Monetary policy with inflation target τ

t

it = rt + τ

t

+ φπ(πt minus τ

t

) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB)

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt = τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4 Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

CONCLUSION

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 20160

05

1

15

2

25

3

35

4

45

5

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

PCE headline inflation (monthly change APR) SPF 10-year expectation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue 12m-inflation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue EWMA

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus K)τtminus1|tminus1 + Kπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UC model

πt = τt + πt τt = τtminus1 + ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus Kt)τtminus1|tminus1 + Ktπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UCSV model

πt = τt + πt τt = τtminus1 + σηt ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TIME-VARYING EWMA WEIGHT ldquoUCSVrdquoStock and Watson (2006 JMCB) partπt+infinpartet = Kt

1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

01

02

03

04

05

06

07

08

09

1

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12SRVINFTRM

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

SRVINFTRMCEMP

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

THIS PAPER

Ingredients

bull DSGE model with NK-Phillips Curve

bull Twist Learning with ldquoSS bandsrdquo for updating

πt =9830541 minus kminus1

tminus1

983055πtminus1 + kminus1

tminus1

983070πt minus (Etminus1πt minus πtminus1)

983071

kt =

983094ktminus1 + 1 if |Φ(past FE)| lt ν

gminus1 otherwise

Endogenous data feeds into learning behavior

bull Endogenous trend

bull State-dependent sensitivity of trend πt to data

bull Once anchored can tolerate deviations of inflation fromtrend up to a point

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2

True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SKETCH OF AN ALTERNATIVE MODEL

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τ

t

+ γπtminus1)

τt=τtminus1 + ηt

Monetary policy with inflation target τ

t

it = rt + τ

t

+ φπ(πt minus τ

t

) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB)

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt = τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4 Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

CONCLUSION

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 20160

05

1

15

2

25

3

35

4

45

5

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

PCE headline inflation (monthly change APR) SPF 10-year expectation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue 12m-inflation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue EWMA

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus K)τtminus1|tminus1 + Kπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UC model

πt = τt + πt τt = τtminus1 + ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus Kt)τtminus1|tminus1 + Ktπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UCSV model

πt = τt + πt τt = τtminus1 + σηt ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TIME-VARYING EWMA WEIGHT ldquoUCSVrdquoStock and Watson (2006 JMCB) partπt+infinpartet = Kt

1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

01

02

03

04

05

06

07

08

09

1

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12SRVINFTRM

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

SRVINFTRMCEMP

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

THIS PAPER

Ingredients

bull DSGE model with NK-Phillips Curve

bull Twist Learning with ldquoSS bandsrdquo for updating

πt =9830541 minus kminus1

tminus1

983055πtminus1 + kminus1

tminus1

983070πt minus (Etminus1πt minus πtminus1)

983071

kt =

983094ktminus1 + 1 if |Φ(past FE)| lt ν

gminus1 otherwise

Endogenous data feeds into learning behavior

bull Endogenous trend

bull State-dependent sensitivity of trend πt to data

bull Once anchored can tolerate deviations of inflation fromtrend up to a point

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2

True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SKETCH OF AN ALTERNATIVE MODEL

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τ

t

+ γπtminus1)

τt=τtminus1 + ηt

Monetary policy with inflation target τ

t

it = rt + τ

t

+ φπ(πt minus τ

t

) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB)

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt = τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4 Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

CONCLUSION

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 20160

05

1

15

2

25

3

35

4

45

5

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

PCE headline inflation (monthly change APR) SPF 10-year expectation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue 12m-inflation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue EWMA

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus K)τtminus1|tminus1 + Kπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UC model

πt = τt + πt τt = τtminus1 + ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus Kt)τtminus1|tminus1 + Ktπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UCSV model

πt = τt + πt τt = τtminus1 + σηt ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TIME-VARYING EWMA WEIGHT ldquoUCSVrdquoStock and Watson (2006 JMCB) partπt+infinpartet = Kt

1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

01

02

03

04

05

06

07

08

09

1

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12SRVINFTRM

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

SRVINFTRMCEMP

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

THIS PAPER

Ingredients

bull DSGE model with NK-Phillips Curve

bull Twist Learning with ldquoSS bandsrdquo for updating

πt =9830541 minus kminus1

tminus1

983055πtminus1 + kminus1

tminus1

983070πt minus (Etminus1πt minus πtminus1)

983071

kt =

983094ktminus1 + 1 if |Φ(past FE)| lt ν

gminus1 otherwise

Endogenous data feeds into learning behavior

bull Endogenous trend

bull State-dependent sensitivity of trend πt to data

bull Once anchored can tolerate deviations of inflation fromtrend up to a point

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2

True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SKETCH OF AN ALTERNATIVE MODEL

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τ

t

+ γπtminus1)

τt=τtminus1 + ηt

Monetary policy with inflation target τ

t

it = rt + τ

t

+ φπ(πt minus τ

t

) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB)

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt = τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4 Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

CONCLUSION

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

PCE headline inflation (monthly change APR) SPF 10-year expectation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue 12m-inflation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue EWMA

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus K)τtminus1|tminus1 + Kπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UC model

πt = τt + πt τt = τtminus1 + ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus Kt)τtminus1|tminus1 + Ktπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UCSV model

πt = τt + πt τt = τtminus1 + σηt ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TIME-VARYING EWMA WEIGHT ldquoUCSVrdquoStock and Watson (2006 JMCB) partπt+infinpartet = Kt

1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

01

02

03

04

05

06

07

08

09

1

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12SRVINFTRM

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

SRVINFTRMCEMP

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

THIS PAPER

Ingredients

bull DSGE model with NK-Phillips Curve

bull Twist Learning with ldquoSS bandsrdquo for updating

πt =9830541 minus kminus1

tminus1

983055πtminus1 + kminus1

tminus1

983070πt minus (Etminus1πt minus πtminus1)

983071

kt =

983094ktminus1 + 1 if |Φ(past FE)| lt ν

gminus1 otherwise

Endogenous data feeds into learning behavior

bull Endogenous trend

bull State-dependent sensitivity of trend πt to data

bull Once anchored can tolerate deviations of inflation fromtrend up to a point

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2

True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SKETCH OF AN ALTERNATIVE MODEL

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τ

t

+ γπtminus1)

τt=τtminus1 + ηt

Monetary policy with inflation target τ

t

it = rt + τ

t

+ φπ(πt minus τ

t

) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB)

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt = τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SKETCH OF AN ALTERNATIVE MODELelements from Ireland (2000 JMCB) Erceg amp Levin (2003 JME) etc

NK Phillips Curve

πt = βπt+1|t + κxt + ut

πt = πt minus ((1 minus γ)τt + γπtminus1) τt=τtminus1 + ηt

Monetary policy with inflation target τt

it = rt + τt + φπ(πt minus τt) + φxxt + εt

Public has limited information

πt+1|t = E(πt+1|Zt Zt =983056πt xt it

983057)

τt|t = τtminus1|tminus1 + K(Zt minus Zt|tminus1)

Simulate with K ∕= 0 while Vol (ηt) = 0

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4

Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2 True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3 State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4 Fitting long-term forecastsSuppose survey forecasts and inflation are cointegratedrsquolsquoCloserdquo fit better than mimicking same low-frequencybehavior

CONCLUSION

Key question

What drives long-run inflation expectations

This paper

bull State-dependent sensitivity of πt to incoming data

bull Learning with ldquoSS bandsrdquofor updating behavior

bull Induces endogenous variations in trend inflation

Great Paper

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

ANCHORED INFLATION EXPECTATIONSChairman Bernanke Speech at the NBER SI July 10 2007

bull I use the term rdquoanchoredrdquo to mean [long-runexpectations that are] relatively insensitive to incomingdata

bull the extent to which they are anchored can changedepending on economic developments and (mostimportant) the current and past conduct of monetarypolicy

bull If inflation [runs] higher than [expected] but expectation[s] change little then inflationexpectations are well anchored

bull If the public reacts to higher-than-expectedinflation by marking up their long-run expectationconsiderably then expectations are poorly anchored

SPF LONG-RUN EXPECTATIONS PCE

Average PCE inflation over next 10 years mean response

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

PCE headline inflation (monthly change APR) SPF 10-year expectation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue 12m-inflation

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

REALIZED INFLATION AND SPF PCE

black inflation red SPF-10Y blue EWMA

2008 2009 2010 2011 2012 2013 2014 2015 2016

minus10

minus5

0

5

10

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus K)τtminus1|tminus1 + Kπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UC model

πt = τt + πt τt = τtminus1 + ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TREND INFLATION 101

EWMA Trend is your Friend

τt|t = (1 minus Kt)τtminus1|tminus1 + Ktπt

bull simple filter for persistent component

bull Muth (1961 ECA) Optimal filter in ldquolocal level modelrdquo

Local level UCSV model

πt = τt + πt τt = τtminus1 + σηt ηt πt sim mds

econometricianrsquos BN-trend τt|t = E(πt+infin|πt )

UC BN-trend τt = E(πt+infin|τ t )

TIME-VARYING EWMA WEIGHT ldquoUCSVrdquoStock and Watson (2006 JMCB) partπt+infinpartet = Kt

1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

01

02

03

04

05

06

07

08

09

1

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12SRVINFTRM

MULTIVARIATE TREND ESTIMATES CPI

τt|(trimmed CPI etc) τt|(SPF etc) from Mertens (REStat forth)

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 20150

2

4

6

8

10

12

SRVINFTRMCEMP

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

THIS PAPER

Ingredients

bull DSGE model with NK-Phillips Curve

bull Twist Learning with ldquoSS bandsrdquo for updating

πt =9830541 minus kminus1

tminus1

983055πtminus1 + kminus1

tminus1

983070πt minus (Etminus1πt minus πtminus1)

983071

kt =

983094ktminus1 + 1 if |Φ(past FE)| lt ν

gminus1 otherwise

Endogenous data feeds into learning behavior

bull Endogenous trend

bull State-dependent sensitivity of trend πt to data

bull Once anchored can tolerate deviations of inflation fromtrend up to a point

AGENDA

1 The Problem (aka the motivation)

2 The Paper (aka the solution)

3 The Praise (aka my thoughts)

SOME THOUGHTS

1 ldquoExogenousrdquo vs ldquoendogenousrdquo trend

bull π = Etπt+infin vs πt = Etπt+infinbull τt vs τt|t

2

True end-point of inflation

bull Does DGP satisfy 1T

983134t πt rarr E(πt) = π

bull What is your estimate

3

State-dependent gainWhich sizekind of structural shock (and policy response)makes updating behavior switch

4