direct carrier billing in 2016 - global market report by fortumo

TRANSCRIPT

Direct Carrier Billing

Global market report by Fortumo

You are reading the �rst annual overview published by Fortumo on direct

carrier billing, taking a look back at the previous year. In this report, we give

an overview of 3 countries of each region (Asia Paci�c, Latin America, Middle

East & Africa, Western Europe and Central & Eastern Europe) that had the

biggest growth in direct carrier billing transaction volume.

For anyone keeping an eye on mobile industry news, it should come as no

surprise that Asia Paci�c has grown to dominate the global digital landscape.

Currently, Latin America is still the biggest overall region in transaction

volume for carrier billing. However, the signi�cant growth in smartphone

ownership combined with lack of payment cards means Asia Paci�c will more

than likely take over this position during 2017.

Introduction

Direct Carrier Billing in 2016: Global Market Report

If you wish to refresh your memory on what happened during 2016, please check out our monthly news summaries, highlighting the biggest stories of the mobile industry from each month of last year:

Data presented in this report has been aggregated across all digital and virtual products and services sold through Fortumo’s Cross-Platform Payment Solution, which is available to consumers on desktop devices, smartphones, tablets as well as feature phones.

Mattias LiivakHead of Marketing & PR

Should you have any questions about the report, please reach out to us at [email protected].

Andrea BoettiVP of Global Business Development & Sales

January February March April

May June July August

September October November December

2016 news summaries17 News 26 News 25 News 28 News

32 News 25 News 27 News 20 News

20 News 16 News 14 News 18 News

Direct Carrier Billing in 2016: Global Market Report

Asia Pacific

Fortumo coverage:

Australia, Bangladesh, Cambodia, Hong Kong, India,

Indonesia, Malaysia, New Zealand, Pakistan, Philippines,

Singapore, South Korea, Taiwan, Thailand, Vietnam

Monthly ARPPUof region:

Monthly medianARPPU of region:

Average transactionvalue in region:

Median ATVof region:

Language localization: 91% of all users in Asia Paci�c have browser language set to English

67%

TABLET

DESKTOP

MOBILE

30%

3%

TRAFFICSOURCES

% denotes 2015-2016 change

$7.3 $3.1 $2.8 $2.37% 3%7% 4%% denotes 2015-2016 change % denotes 2015-2016 change % denotes 2015-2016 change

15

2016 REGIONAL OVERVIEW

1605

LANGUAGELOCALIZATION

91% English

COUNTRIESMILLION USERS

Direct Carrier Billing in 2016: Global Market Report

Other languages9%

Direct Carrier Billing in 2016: Global Market Report

6%

30%

44%

30% 53%

138%

100%

200%

6%

26%

5%

21%

TABLET

DESKTOP

MOBILE

PHILIPPINES INDIA

160%

Population 102 million 1300 million 24 millionGross National Income (GNI) per

capita (IMF 2014 estimate): $4,000 $2,000 $65,000

Mobile phonesin market: 122 million 1000 million 31 million

265% 175%

AUSTRALIA

2015-2016growth %

Smartphone penetration: 20% 68%

Debit card penetration: 21% 22% 89%

Credit card penetration: 3% 2% 59%

Monthly ARPPU, 2016 (change % compared to 2015) $9.5 $2.3 $11

Median monthly ARPPU $3.3 $1.9 $7.8

Average transactionvalue $3.2 $2.0 $6.3

Median ATV $1.8 $1.8 $5.7

Localization Not necessary, majority of users have browser language

set to English

As only 10% of people speak English, localization is recom-

mended. Hindi (422 million speakers) is the primary language to localize for

Not necessary, majority of users have browser language

set to English

Tra�c sources

2016 top 3 growth markets in Asia Pacific

40%

77%

14%

9%TABLET

DESKTOP

MOBILE63%

35%

2%TABLET

DESKTOP

MOBILE85%

8%

7%

Central & Eastern Europe

Fortumo coverage:

Albania, Armenia, Azerbaijan, Belarus, Bosnia and

Herzegovina, Bulgaria, Croatia, Czech Republic, Estonia,

Georgia, Hungary, Kazakhstan, Kosovo, Latvia, Lithuania,

Macedonia, Moldova, Montenegro, Poland, Romania, Russia,

Serbia, Slovakia, Slovenia, Ukraine

Monthly ARPPUof region:

Monthly medianARPPU of region:

Average transactionvalue in region:

Median ATVof region:

61%

TABLET

DESKTOP

MOBILE

31%

8%

TRAFFICSOURCES

% denotes 2015-2016 change

$4.7 $2.2 $2.2 $1.92% 5% 10% 6%% denotes 2015-2016 change % denotes 2015-2016 change % denotes 2015-2016 change

25

2016 REGIONAL OVERVIEW

345

LANGUAGELOCALIZATION

28% Russian

COUNTRIESMILLION USERS

Users browser language:

Direct Carrier Billing in 2016: Global Market Report

Polish

English

Russian28%

13%

7%

Other languages52%

Direct Carrier Billing in 2016: Global Market Report

5%

8%

19%

16%

TABLET

DESKTOP

MOBILE

CZECH REPUBLIC HUNGARY

5%

Population 10 million 10 million 43 millionGross National Income (GNI) per

capita (IMF 2014 estimate): $27,000 $17,000 $6,800

Mobile phonesin market: 14 million 12 million 63 million

16% 14%

UKRAINE

2015-2016growth %

Smartphone penetration: 34% 50%

Debit card penetration: 68% 63% 29%

Credit card penetration: 14% 7% 39%

Monthly ARPPU, 2016 (change % compared to 2015) $6.1 $4.7 $2.3

Median monthly ARPPU $2.6 $1.7 $1.1

Average transactionvalue $3.3 $2.7 $1

Median ATV $2.5 $1.7 $0.9

Localization Recommended, 90% users have browser language set to

Czech

Recommended, 94% users have browser language set to

Hungarian

Recommended, users have browser language set to

Russian (79%) and Ukrainian (13%)

Tra�c sources

2016 top 3 growth markets in Central & Eastern Europe

75%

62%

29%

9%TABLET

DESKTOP

MOBILE65%

29%

6%TABLET

DESKTOP

MOBILE47%

48%

5%

4%

UNCHANGED

UNCHANGED

UNCHANGED

9%

10%

15%

15%

Latin America

Fortumo coverage:

Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica,

Dominican Republic, Ecuador, Mexico, Panama, Paraguay,

Peru, Uruguay, Venezuela

Monthly ARPPUof region:

Monthly medianARPPU of region:

Average transactionvalue in region:

Median ATVof region:

58%

TABLET

DESKTOP

MOBILE

39%

3%

TRAFFICSOURCES

% denotes 2015-2016 change

$3.7 $1.6 $1.3 $1.311% 7%% denotes 2015-2016 change % denotes 2015-2016 change % denotes 2015-2016 change

14

2016 REGIONAL OVERVIEW

524

LANGUAGELOCALIZATION

63% Spanish

COUNTRIESMILLION USERS

UNCHANGED

Users browser language:

Portuguese

Spanish63%

31%

Direct Carrier Billing in 2016: Global Market Report

Other languages6%

UNCHANGED

Direct Carrier Billing in 2016: Global Market Report

6%

6%

36% 30%

61%

8%

21%

TABLET

DESKTOP

MOBILE

PERU CHILE

19%

Population 32 million 18 million 48 millionGross National Income (GNI) per

capita (IMF 2014 estimate): $6,000 $15,000 $8,000

Mobile phonesin market: 32 million 18 million 48 million

72% 52%

COLOMBIA

2015-2016growth %

Smartphone penetration: 50% 40%

Debit card penetration: 21% 54% 30%

Credit card penetration: 11% 28% 13%

Monthly ARPPU, 2016 (change % compared to 2015) $3.4 $3.9 $3.4

Median monthly ARPPU $1.9 $2.1 $1.1

Average transactionvalue $1.4 $21.4 $1.1

Median ATV $1.4 $1.3 $1.1

Localization Recommended, 94% of users have browser language set to

Spanish

Recommended, 95% of users have browser language set to

Spanish

Recommended, 93% of paying users have browser locale set

to Spanish

Tra�c sources

2016 top 3 growth markets in Latin America

30%

62%

35%

3%TABLET

DESKTOP

MOBILE45%

53%

2%TABLET

DESKTOP

MOBILE49%

47%

4%

54%

UNCHANGED

15%

15%

15%

Middle East & Africa

Fortumo coverage:

Algeria, Bahrain, Cote d'Ivoire, Egypt, Ethiopia, Iraq, Israel,

Jordan, Kenya, Kuwait, Lebanon, Morocco, Mozambique,

Nigeria, Oman, Qatar, Saudi Arabia, Senegal, South Africa,

Tunisia, Turkey, United Arab Emirates

Monthly ARPPUof region:

Monthly medianARPPU of region:

Average transactionvalue in region:

Median ATVof region:

72%

TABLET

DESKTOP

MOBILE

21%

7%

TRAFFICSOURCES

% denotes 2015-2016 change

$8.4 $3.2 $2.5 $2.18% 19%% denotes 2015-2016 change % denotes 2015-2016 change % denotes 2015-2016 change

22

2016 REGIONAL OVERVIEW

603

LANGUAGELOCALIZATION

55% English

COUNTRIESMILLION USERS

13% 11%

Users browser language:

Arabic

French

English55%

17%

17%

Turkish6%

Other languages5%

Direct Carrier Billing in 2016: Global Market Report

Direct Carrier Billing in 2016: Global Market Report

18%

31%

23%

8%

4%

3%

60%

40%

60%

TABLET

DESKTOP

MOBILE

TUNISIA LEBANON

58%

Population 11 million 6 million 47 millionGross National Income (GNI) per

capita (IMF 2014 estimate): $4,000 $10,000 $1,000

Mobile phonesin market: 17 million 4 million 36 million

184% 159%

KENYA

2015-2016growth %

Smartphone penetration: 48% 36%

Debit card penetration: 12% 33% 35%

Credit card penetration: 6% 11% 5%

Monthly ARPPU, 2016 (change % compared to 2015) $3.4 $9.1 $1.6

Median monthly ARPPU $2.3 $3.9 $0.8

Average transactionvalue $1.4 $2.9 $0.7

Median ATV $1.3 $3 $0.8

Localization Recommended, 90% of users have browser language set to

French

Recommended, 21% of users have browser language set to

Arabic

Not necessary, 97% of users have browser language set to

English

Tra�c sources

2016 top 3 growth markets in Middle East & Africa

27%

76%

21%

3%TABLET

DESKTOP

MOBILE53%

43%

4%TABLET

DESKTOP

MOBILE83%

14%

3%

9%

4%

6%

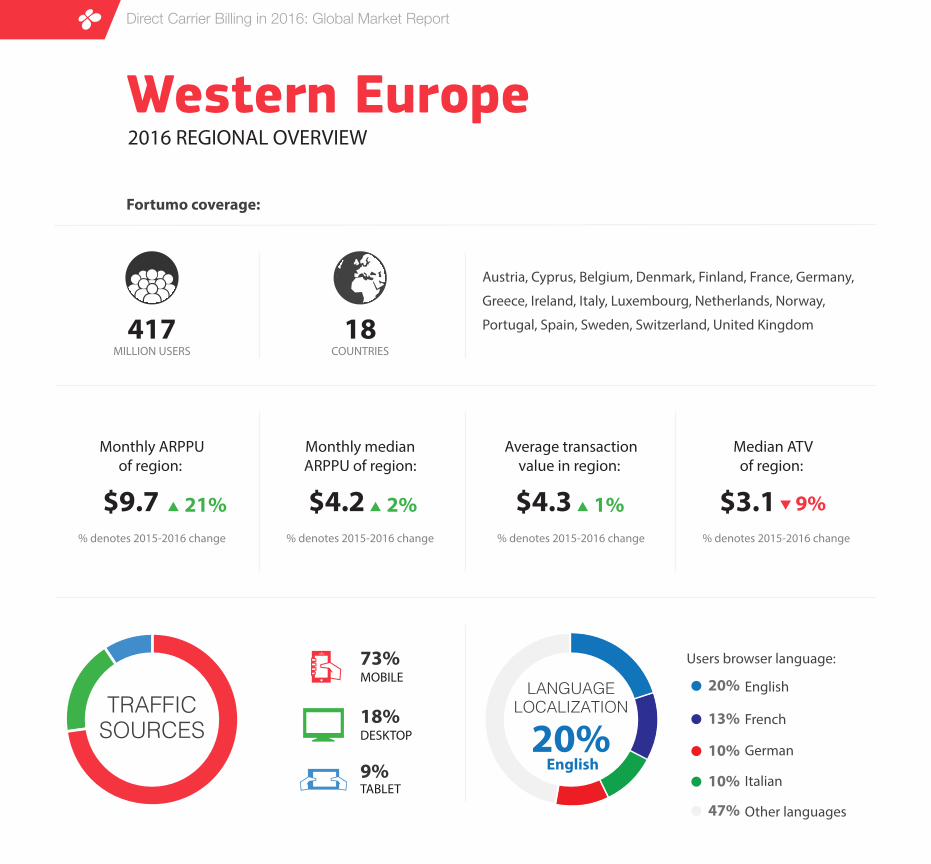

Western Europe

Fortumo coverage:

Austria, Cyprus, Belgium, Denmark, Finland, France, Germany,

Greece, Ireland, Italy, Luxembourg, Netherlands, Norway,

Portugal, Spain, Sweden, Switzerland, United Kingdom

Monthly ARPPUof region:

Monthly medianARPPU of region:

Average transactionvalue in region:

Median ATVof region:

73%

TABLET

DESKTOP

MOBILE

18%

9%

TRAFFICSOURCES

% denotes 2015-2016 change

$9.7 $4.2 $4.3 $3.121% 1%2% 9%% denotes 2015-2016 change % denotes 2015-2016 change % denotes 2015-2016 change

18

2016 REGIONAL OVERVIEW

417COUNTRIESMILLION USERS

LANGUAGELOCALIZATION

20% English

Users browser language:

German

French

English20%

13%

10%

Italian

Other languages47%

10%

Direct Carrier Billing in 2016: Global Market Report

Direct Carrier Billing in 2016: Global Market Report

4%

37%

25%

11%

21%

16%

TABLET

DESKTOP

MOBILE

NORWAY PORTUGAL

23%

Population 5 million 10 million 65 millionGross National Income (GNI) per

capita (IMF 2014 estimate): $104,000 $21,000 $43,000

Mobile phonesin market: 6 million 15 million 74 million

63% 38%

UNITED KINGDOM

2015-2016growth %

Smartphone penetration: 59% 68%

Debit card penetration: 99% 66% 96%

Credit card penetration: 67% 28% 61%

Monthly ARPPU, 2016 (change % compared to 2015) $7.4 $6.3 $13.5

Median monthly ARPPU $3 $2.6 $6.4

Average transactionvalue $4.1 $2.9 $6.2

Median ATV $2.3 $2.3 $4.2

Localization Recommended, 54% of users have browser language set to

Norwegian

Recommended, 94% of users have browser language set to

Portuguese

Not necessary

Tra�c sources

2016 top 3 growth markets in Western Europe

83%

53%

39%

8%TABLET

DESKTOP

MOBILE36%

56%

8%TABLET

DESKTOP

MOBILE69%

25%

7%

23%

19%

20%

22%

UNCHANGED

UNCHANGED

Additional reading

What metrics to measure for your payment solutions?

Read now

How to do a background check on your carrier billing provider?

Read now

Who to partner with to launch carrier billing?

Read now

https://fortumo.comhttps://facebook.com/fortumohttps://twitter.com/fortumohttps://www.linkedin.com/company/fortumo-ltd.

Fortumo is a mobile payments company that enables direct carrier billing with more than 350 mobile operators in 90+ countries. Fortumo's payment products work across a wide range of platforms including desktop devices, smartphones, feature phones, tablets and smart TV-s. These products give consumers a simple, 1-click payment method to charge online purchases to their phone bill. For app stores, digital media companies and game developers, Fortumo provides one integration with 350 mobile operators as well as a single point of contact for settlements, reporting, support and infrastructure upgrades. Founded in 2007, Fortumo has offices in Estonia, San Francisco, Beijing, Delhi, Singapore & Hanoi and is backed by Intel Capital and Greycroft Partners.

This document is for informational purposes only. Fortumo and the authors make no expressed or implied warranties in this document. Fortumo and the author(s) make no representation or warranty in relation to the accuracy, completeness or reliability of the information contained in this document. Any opinions expressed in this document are subject to change without notice. This document may be based on a number of assumptions and different assumptions could result in materially different results. This document should not be regarded by recipients as a substitute for obtaining independent advice and/or the exercise of their own judgement, and is not to be relied upon by recipients. Fortumo and the authors, and any of their members, directors, employees or agents do not accept any liability for any loss or damage arising out of the use of all or any part of this document. Copyright © 2017 Fortumo | All rights reserved.