carrier billing in the nordics: 2016 market report by fortumo

TRANSCRIPT

Carrier billing in the Nordics: 2016 market report by Fortumo

The Nordic region is one of the wealthiest in the world, with all countries belonging to the top 20 countries globally in national income per capita. With a well-developed telecommunications infrastructure, high-speed mobile internet is accessible to almost everyone and has also resulted in very high smartphone ownership rates. This makes the region attractive for any digital merchant as user’s access to digital content and disposable income are high.

While a relatively large amount of people have access to card-based payments thanks to owning a credit card, carrier billing is still among the most popular payment methods for digital content. This is either due to inconvenience in the checkout process where card-based payments require the user to enter substantial amounts of personal data about themselves; or due to the fear of fraud - that the same information shared with merchants might become compromised. Due to this, carrier billing is a suitable alternative payment method to enable purchasing for people who either can not or do not want to make card payments online.

This market report gives an overview of the carrier billing landscape in 4 Nordic countries: Denmark, Finland, Norway and Sweden.

Introduction

Carrier billing in the Nordics: 2016 market report by Fortumo

Carrier billing data presented in the report has been taken from Fortumo’s cross-platform mobile payments product, available to users for payments on desktop and the mobile web.

Mattias LiivakHead of Marketing & PRFortumo

If you have any questions about the data in this report, please reach out to us at [email protected].

Andrea BoettiVP of Global Business Development & SalesFortumo

Carrier billing in the Nordics: 2016 market report by Fortumo

SwedenMarket profile

GNI per capita:Median age:

41

85%

10

Smartphonepenetration (of all

mobile phones):

Population:

$62,00015

Debit cardpenetration:

98%

Mobile phones:

1 Swedish Krona (SEK) = $0.11

91%

Mobile broadband

access:

23%

Prepaid SIMmarket share:

Credit cardpenetration:

45%

(exchange rate as of November 2nd, 2016)

million years Gross National Income (IMF 2014 estimate)

million

Currency:

Carrier billing in the Nordics: 2016 market report by Fortumo

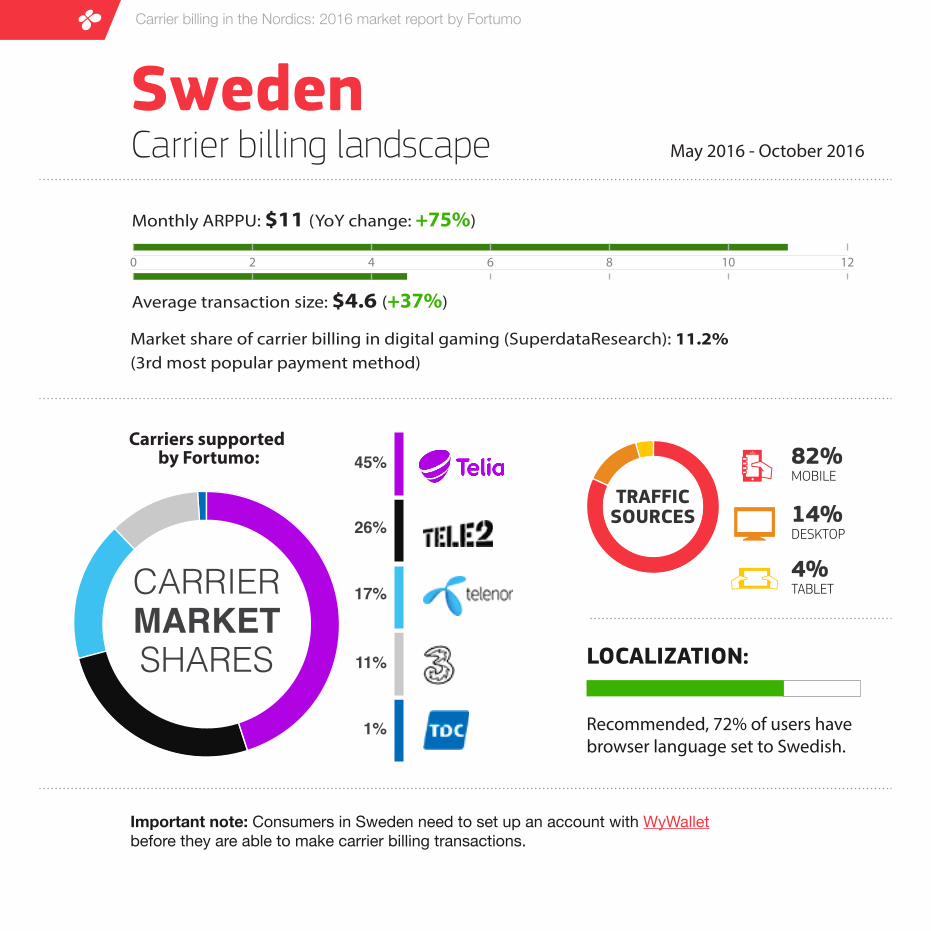

Carriers supported by Fortumo: 45%

26%

17%

11%

1%

CARRIERMARKETSHARES

82%

TABLET

DESKTOP

MOBILE

14%

4%

TRAFFICSOURCES

LOCALIZATION:

Recommended, 72% of users have browser language set to Swedish.

Carrier billing landscape May 2016 - October 2016

SwedenCarrier billing in the Nordics: 2016 market report by Fortumo

Average transaction size: $4.6 (+37%)

Monthly ARPPU: $11 (YoY change: +75%)

0 2 4 6 8 10 12

Market share of carrier billing in digital gaming (SuperdataResearch): 11.2% (3rd most popular payment method)

Important note: Consumers in Sweden need to set up an account with WyWalletbefore they are able to make carrier billing transactions.

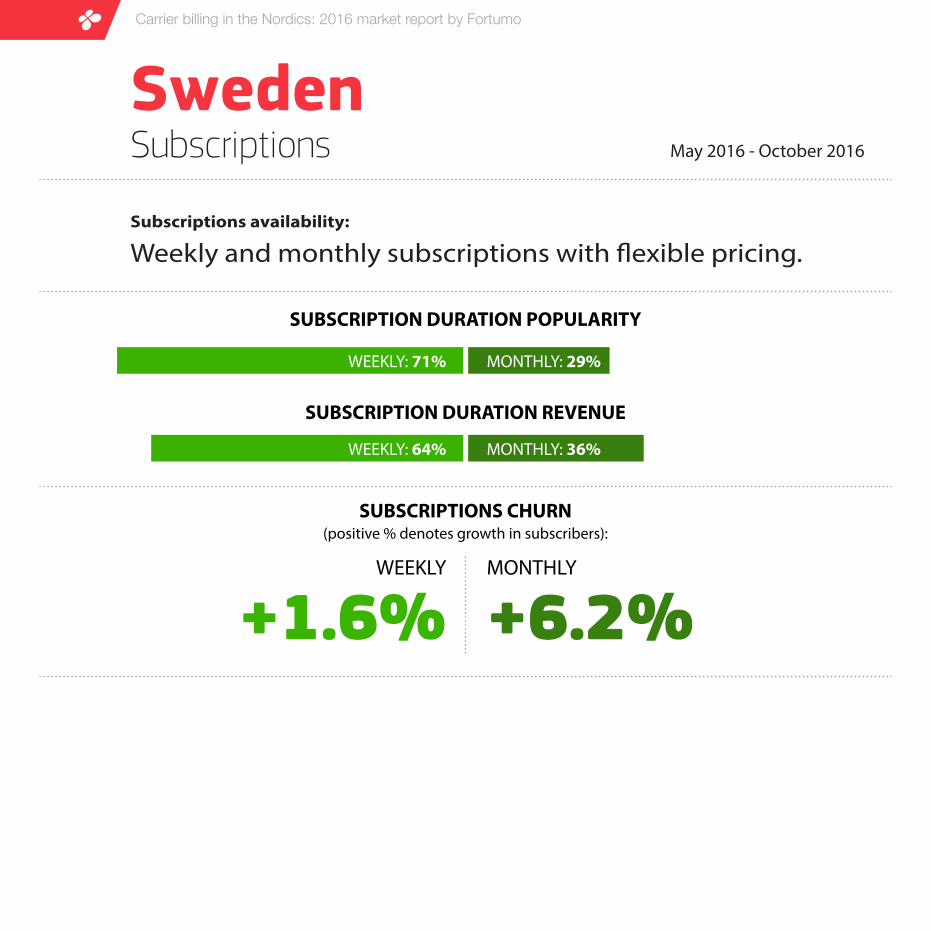

Subscriptions May 2016 - October 2016

SwedenCarrier billing in the Nordics: 2016 market report by Fortumo

Subscriptions availability:

Weekly and monthly subscriptions with �exible pricing.

(positive % denotes growth in subscribers):

SUBSCRIPTION DURATION POPULARITY

SUBSCRIPTION DURATION REVENUE

SUBSCRIPTIONS CHURN

WEEKLY MONTHLY

+6.2%+1.6%

WEEKLY: 71% MONTHLY: 29%

WEEKLY: 64% MONTHLY: 36%

DenmarkMarket profile

GNI per capita:Median age:

42

80%

6

Smartphonepenetration (of all

mobile phones):

Population:

$61,0009

Debit cardpenetration:

96%

Mobile phones:

1 Danish Krone (DKK) = $0.15

84%

Mobile broadband

access:

14%

Prepaid SIMmarket share:

Credit cardpenetration:

37%

(exchange rate as of November 2nd, 2016)

million years Gross National Income (IMF 2014 estimate)

million

Currency:

Carrier billing in the Nordics: 2016 market report by Fortumo

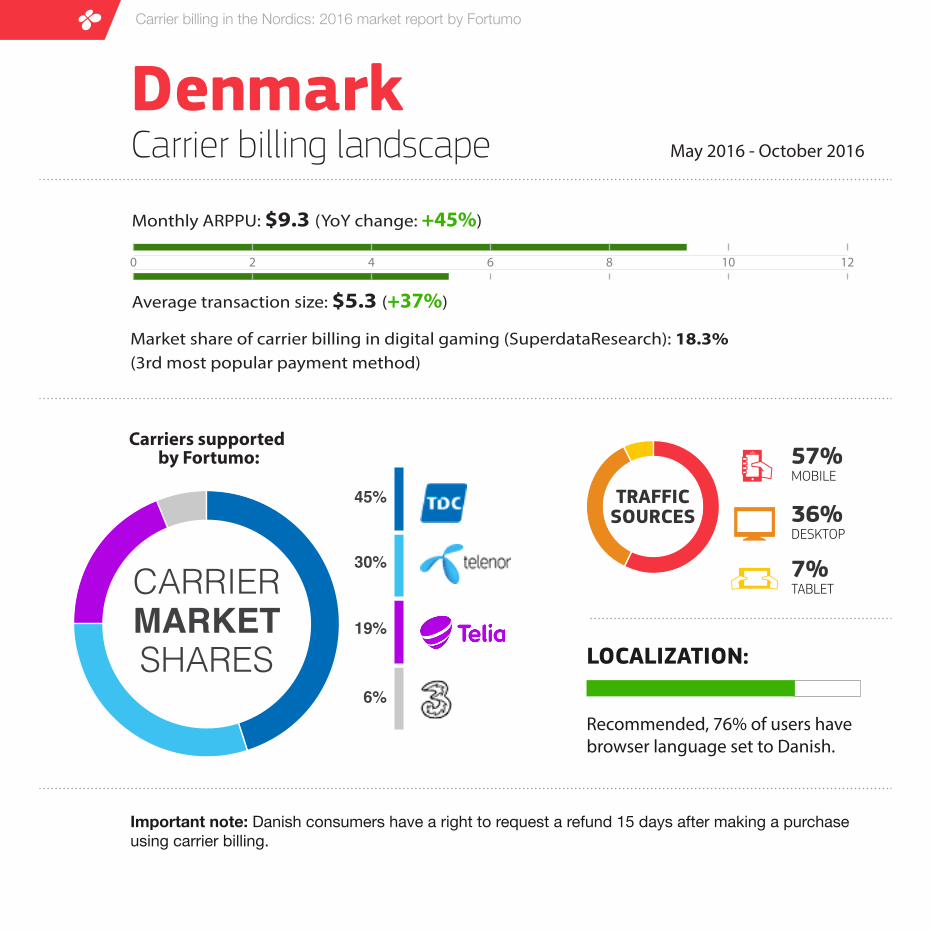

Average transaction size: $5.3 (+37%)

Monthly ARPPU: $9.3 (YoY change: +45%)

0 2 4 6 8 10 12

Carriers supported by Fortumo:

45%

30%

19%

6%

CARRIERMARKETSHARES

57%

TABLET

DESKTOP

MOBILE

36%

7%

TRAFFICSOURCES

LOCALIZATION:

Recommended, 76% of users have browser language set to Danish.

Carrier billing landscape May 2016 - October 2016

DenmarkCarrier billing in the Nordics: 2016 market report by Fortumo

Market share of carrier billing in digital gaming (SuperdataResearch): 18.3% (3rd most popular payment method)

Important note: Danish consumers have a right to request a refund 15 days after making a purchase using carrier billing.

Subscriptions May 2016 - October 2016

DenmarkCarrier billing in the Nordics: 2016 market report by Fortumo

Subscriptions availability:

Daily, weekly and monthly subscriptions with �exible pricing (up to 200 DKK)

(positive % denotes growth in subscribers):SUBSCRIPTIONS CHURN

WEEKLY

+2.9%

FinlandMarket profile

GNI per capita:Median age:

42

56%

6

Smartphonepenetration (of all

mobile phones):

Population:

$48,00010

Debit cardpenetration:

97%

Mobile phones:

1 Euro (EUR) = $1.11

78%

Mobile broadband

access:

8%

Prepaid SIMmarket share:

Credit cardpenetration:

63%

(exchange rate as of November 2nd, 2016)

million years Gross National Income (IMF 2014 estimate)

million

Currency:

Carrier billing in the Nordics: 2016 market report by Fortumo

Average transaction size: $3.8 (+6%)

Monthly ARPPU: $7.5 (YoY change: +27%)

0 2 4 6 8 10 12

Carriers supported by Fortumo:

42%

37%

21%

CARRIERMARKETSHARES

57%

TABLET

DESKTOP

MOBILE

31%

12%

TRAFFICSOURCES

LOCALIZATION:

Recommended, 75% of users have browser language set to Finnish.

Carrier billing landscape May 2016 - October 2016

FinlandCarrier billing in the Nordics: 2016 market report by Fortumo

Market share of carrier billing in digital gaming (SuperdataResearch): 16.4% (4th most popular payment method)

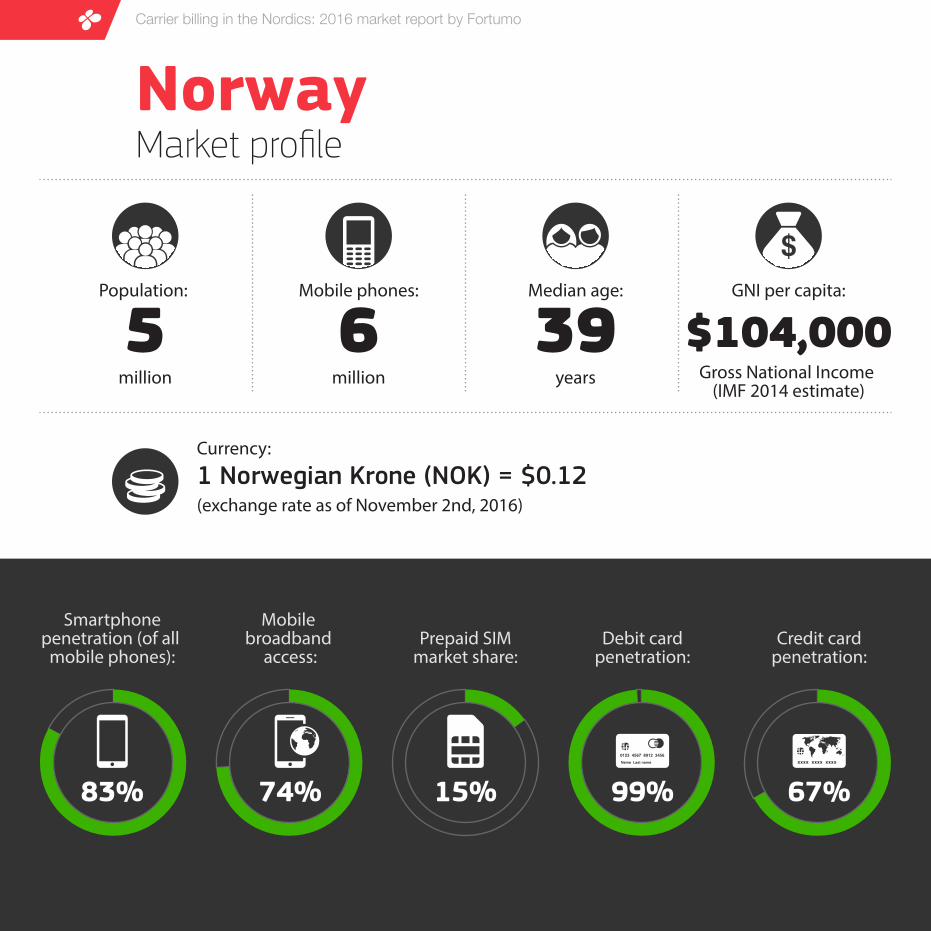

NorwayMarket profile

GNI per capita:Median age:

39

83%

5

Smartphonepenetration (of all

mobile phones):

Population:

$104,0006

Debit cardpenetration:

99%

Mobile phones:

1 Norwegian Krone (NOK) = $0.12

74%

Mobile broadband

access:

15%

Prepaid SIMmarket share:

Credit cardpenetration:

67%

(exchange rate as of November 2nd, 2016)

million years Gross National Income (IMF 2014 estimate)

million

Currency:

Carrier billing in the Nordics: 2016 market report by Fortumo

Average transaction size: $4.2 (+13%)

Monthly ARPPU: $8.2 (YoY change: +48%)

0 2 4 6 8 10 12

Carriers supported by Fortumo: 51%

37%

9%

2%

1%

CARRIERMARKETSHARES

53%

TABLET

DESKTOP

MOBILE

39%

8%

TRAFFICSOURCES

LOCALIZATION:

Recommended, 54% of users have browser language set to Norwegian.

Carrier billing landscape May 2016 - October 2016

NorwayCarrier billing in the Nordics: 2016 market report by Fortumo

Market share of carrier billing in digital gaming (SuperdataResearch): 19.9% (3rd most popular payment method)

Important note: Carrier billing in Norway is processed through the mobile operator owned payments solution Strex.

Additional reading

Infographic:carrier billing deployment tracker

Infographic:how do credit cards stack up against carrier billing?

Carrier billing in Middle East & Africa: 2016 market report by Fortumo

Read now

Read now

Read now

https://fortumo.comhttps://facebook.com/fortumohttps://twitter.com/fortumohttps://www.linkedin.com/company/fortumo-ltd

Fortumo is a mobile payments company that enables direct carrier billing with more than 350 mobile operators in 90+ countries. Fortumo's payment products work across a wide range of platforms including desktop devices, smartphones, feature phones, tablets and smart TV-s. These products give consumers a simple, 1-click payment method to charge online purchases to their phone bill. For app stores, digital media companies and game developers, Fortumo provides one integration with 350 mobile operators as well as a single point of contact for settlements, reporting, support and infrastructure upgrades. Founded in 2007, Fortumo has offices in Estonia, San Francisco, Beijing, Delhi, Singapore & Hanoi and is backed by Intel Capital and Greycroft Partners.

This document is for informational purposes only. Fortumo and the authors make no expressed or implied warranties in this document. Fortumo and the author(s) make no representation or warranty in relation to the accuracy, completeness or reliability of the information contained in this document. Any opinions expressed in this document are subject to change without notice. This document may be based on a number of assumptions and different assumptions could result in materially different results. This document should not be regarded by recipients as a substitute for obtaining independent advice and/or the exercise of their own judgement, and is not to be relied upon by recipients. Fortumo and the authors, and any of their members, directors, employees or agents do not accept any liability for any loss or damage arising out of the use of all or any part of this document. Copyright © 2016 Fortumo | All rights reserved.