digitalization on financial services and implications for ... · greece 2015–2016 88 75 italy...

TRANSCRIPT

Monetary Policy Group, Bank of Thailand

December 2018

Digitalization on Financial Services and Implications for Monetary Policy in Thailand

Thematic Study 2018

Thitima ChucherdAcharawat Srisongkram

Thosapon Tonghui

Natta PiyakarnchanaSuparit Suwanik

Thanaphol Kongphalee

Bovonvich JindarakThiti TosborvornAniya Shimnoi

2

Financial innovation has been evolved over timee.g. e-Payment, e-Wallet, digital currencies

1960s

1980s

Barter Gold/coin Paper Money e-Payment Cryptocurrency

2000s

2010s618 AD 2000s1960s 1970s 1980s 1990s 2010s 2020s

Cellphone

2G 3G 4G 5G1G

Smartphone

Internet wolrd-wide-webPersonal computer

WiFi

Social media

Motivation

Remark: size of bubble = value of non-cash payment/GDP in 2016Sources: BIS statistics on payments and financial market infrastructures in the CPMI countries (Red Book statistics), Bank of Thailand

Chan

ge in

valu

e of

non

-cash

pay

men

t/GDP

du

ring 2

016-

2010

(tim

es)

Change in volume of non-cash payment/GDP during 2016-2010 (times)

in parallel with technological developmente.g. high-speed internet, smartphones, information technology,

block chain, and digital ledger technologies (DLT)

e-Payment has become increasingly important in most countries countriessignificantly

3

Scope of study

Electronic/Digital

Universally accessible

Central bank-issued

Peer-to-peer

Commodity money

Crypto-currency

CBDC(retail)

CBDC(wholesale)

Crypto-currency

(wholesale)Cash

Reserve accounts

Depositedcurrencyaccounts

Local currency

Virtual currency

Bank deposit,Mobile money,

e-Money

A taxonomy of money

Electronic payment (e-Payment) Digital currencies

Retail e-paymentCard paymentsInternet and mobile banking e-money

e-moneyCrypto-currencyCBDC

‘Digitalization’ in this paper

Source: BIS (2017)

• payment method has been developed and widely used, commonly linked to either bank or the 3rd party account

• An asset stored in electronic form that can serve essentially the same function as physical currency, namely, facilitating payments transactions

4

This paper aims to evaluate the impacts of digitalization in financial services on monetary policy in Thailand:

1. Understanding new development and trends pertaining to the digitalization including e-Payment and digital currencies and assessing its potential to permanently replace cash

2. Analyzing the implications for transmission and effectiveness of monetary policy

Objectives, Research questions, and Methodolody

Research questionse-Payment• How much retail e-Payment could substitute cash usage in Thailand?• How would e-Payment affect monetary aggregates, central bank's

balance sheet, velocity of money, money multiplier? How would this affect the transmission of monetary policy or monetary operations?

Digital currencies• How would the emergence of private digital currencies affect transmission

of monetary policy in 5 traditional channels?• What are the policy options available to central banks, and how

would this change the transmission of monetary policy?

Methodologye-Payment

- Literature review- Descriptive and empirical analysis• Monetary statistics• Substitution effect between

cash and e-Payment (GMM)• Monetary policy effectiveness

with and without e-payment (FAVAR)

Digital currencies- Literature review- Scenario analysis

Objectives

5

Outline

Part I e-Payment

I.I Development of cash usage behaviors and challenges in Thailand

I.II Empirical analysis of e-Payment and monetary policy

6

Cash usage in selected countries

Country PeriodCash usage

(% of transactions)

Cash usage (% of value)

Thailand 2017 93 -Euro area 2014–2016 79 54

Greece 2015–2016 88 75Italy 2015–2016 86 68Germany 2014 80 55France 2015–2016 68 28Finland 2015–2016 54 33Netherlands 2016 45 27

UK 2016 44 15US 2016 31 8Denmark 2017 23 16Sweden 2018 13 -Norway 2017-2018 11 6

Sources: Retail payment services 2017 Report, Norges Bank Survey of e-payment usage in Thailand in 2017, Payment Policy Department,

Bank of Thailand

0% 20% 40% 60% 80% 100%

60+

50-59

40-49

30-39

18-29

ATM transfer Debit card payment Credit card paymentInternet banking Mobile banking

0 50,000 100,000 150,000 200,000 250,000

60+

50-59

40-49

30-39

18-29 Non-cashCash

Cash usage (classified by age groups)e-Payment survey in Thailand (2017)

No. of monthly transactions for each person

e-Payment usage (classified by age groups)

Daily transactions in Thailand are mostly in cashTeenager and early working-aged groups are more welcome to non-cash usage esp. mobile/internet banking

Source: Survey of e-payment usage in Thailand in 2017, Payment Policy Department, Bank of Thailand

Part I e-PaymentDevelopment of cash usage behaviors and challenges in Thailand

7

0

50

100

150

200

0

1

2

3

2550 2552 2554 2556 2558 2560

cards

internet and mobile (RHS)

e-Money

0

10

20

30

40

2550 2552 2554 2556 2558 2560

Trillion baht

0

1

2

3

4

2550 2552 2554 2556 2558 2560

ATM or branchesinternet and mobilecardse-Money

Billion transactions

Value of retail payment

No. of retail payment Life cycle of payment services

Introduction Growth Saturation Decline

Debit cardCredit card

e-Money

Interbet banking

Mobile banking

Terminal Giros

Cheque

ATM

Terminal Giros

PC/Internet Giros

20182003Tr

ansa

ctio

ns

Norway

EFTPOS (mainly card payment)

Mail-based GirosGiros paid at counter

Source: Gresvik and Owre (2003), Rungsun Hataiseree (2008), and author’s estimates.

Introduction Growth Saturation Decline

e-Money

Debit cardCredit card

Internet bankingMobile banking

ATM Transfer

Counter TransferCheque

Cheque

ATM

Credit cardDebit card

Credit Transfer

e-Money

20182008Tr

ansa

ctio

ns

ThailandCash services at branch

e-Payment usage in Thailand still be in the early stage esp. Internet/mobile banking Value of payment per each transaction has been declined recently reflecting greater adoption of e-Payment in daily use

Part I e-PaymentDevelopment of cash usage behaviors and challenges in Thailand

Source: Bank of Thailand

Value of retail payment / transactionThousand baht

Thousand baht

8

Part I e-PaymentDevelopment of cash usage behaviors and challenges in Thailand

Cash transaction has declined continuously consistent with decelerating growth of cash in circulation

Growth of payment services

75

77

79

81

83

85

0.0

0.5

1.0

1.5

2.0

2550 2551 2552 2553 2554 2555 2556 2557 2558 2559 2560

Currency held by Depository Corp.Currency held by Gov.Currency outside DCs & Gov.Share of Currency outside DCs & Gov. (แกนขวา)

Trillion baht

Cash in circulation (classified by holders)

5

6

7

8

9

10

-4048

12162024

2550

Q125

50Q3

2551

Q125

51Q3

2552

Q125

52Q3

2553

Q125

53Q3

2554

Q125

54Q3

2555

Q125

55Q3

2556

Q125

56Q3

2557

Q125

57Q3

2558

Q125

58Q3

2559

Q125

59Q3

2560

Q125

60Q3

CIC growth CIC to GDP (%) RHS

-10% 0% 10% 20% 30% 40% 50% 60%

ATM withdraw

Counter withdraw

Cheque

ATM tranfser

Counter tranfser

Credit card

e-Money

Debit card

Internet&Mobile

man

ual

sem

iel

ectro

nic

2557255825592560

- 30,000- 20,000- 10,000

0 10,000 20,000 30,000 40,000

H2/2

557

H1/2

558

H2/2

558

H1/2

559

H2/2

559

H1/2

560

H2/2

560

H1/2

561

Cash deposit and withdrawalCash deposit Cash withdrawal

Billion baht

%

Avg. = 9.2%Avg. = 5.3%

Source: Bank of Thailand

9

0.00

0.05

0.10

0.15

0.20

0.25

0.30

1.00

1.50

2.00

2.50

3.00

2000Q1 2003Q1 2006Q1 2009Q1 2012Q1 2015Q1 2018Q1

Velocity of money

Base

Narrow

Broad (RHS)

6

7

8

9

10

11

12

13

14

0.91.01.11.21.31.41.51.61.7

2000Q1 2003Q1 2006Q1 2009Q1 2012Q1 2015Q1 2018Q1

Money multiplier

Broad (RHS)

Narrow

02468

1012141618

2001Q1 2004Q1 2007Q1 2010Q1 2013Q1 2016Q1

Growth of monetary aggregateBroad

Narrow

Base

%YoY

times

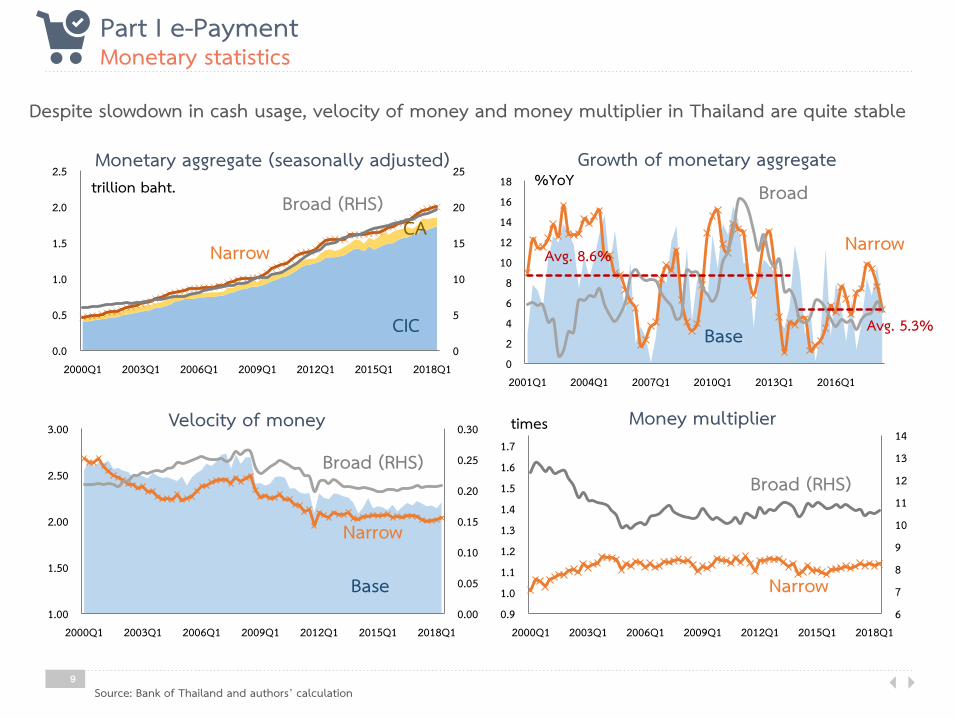

Despite slowdown in cash usage, velocity of money and money multiplier in Thailand are quite stable

0

5

10

15

20

25

0.0

0.5

1.0

1.5

2.0

2.5

2000Q1 2003Q1 2006Q1 2009Q1 2012Q1 2015Q1 2018Q1

trillion baht.Broad (RHS)

Narrow

CIC

CA

Monetary aggregate (seasonally adjusted)

Avg. 8.6%

Avg. 5.3%

Part I e-PaymentMonetary statistics

Source: Bank of Thailand and authors’ calculation

10

Unlike Sweden, cash in circulation continuously declines and velocity of money rises fast

Velocity of M0 Velocity of M1

Velocity of M2 Velocity of M3

Cash/GDP

SEK bil.

Source: Dalebrant (2016)

Part I e-PaymentMonetary statistics

Transition towards a cashless society in Sweden

11

Currency in circulation

(CIC)

Macroeconomic variables

Opportunity cost

e-Payment usage(value)

CEI

3-m deposit interest rate

Internet/mobile card payment e-Money-

Model I Model II Model III Model IVCoincident economic index 0.497 *** 0.517 *** 0.491 *** 0.211 *ST interest rate -0.012 *** -0.014 *** -0.012 *** -0.013 ***Retail e-payment -0.058 **Card payment -0.089 ***Internet and mobile banking -0.054 **e-money 0.023SET return -0.085 *** -0.090 *** -0.083 *** -0.087 ***C 0.060 *** 0.060 *** 0.059 *** 0.048 ***Adjusted R-squared 0.393 0.344 0.394 0.358

-

+

SET return

Source: Authors’ calculationRemark: This study employs generalized method of moments (GMM) approach, using monthly data from Jan10 to Jun18

***, **, * = statistical significance at 0.01, 0.05, and 0.1 respectivelyAll variables, except for deposit rates, are in real terms and expressed in log with the first-difference form

Our empirical study also shows that e-Payment usage in Thailand slightly substitutes cashIf Thai people use 1% more for retail e-Payment, demand for money will decline by 0.05 - 0.1%

However, e-Payment shows smaller impact on cash compared to economic activities and opportunity cost

Part I e-PaymentSubstitution effect on demand for money

12

Part I e-PaymentLiterature reviews

Past studies in e-Payment and implication on monetary policy are mostly descriptive and focus in digital moneyGrowing use of digital money could lessen central bank’s ability to control money supply under monetary targeting framework.

However, it will not affect monetary policy under inflation targeting

Area of study Implications for monetary policy

Monetary operation

- Reduce central bank’s control over money supply and complicate monetary operation under monetary targeting due to higher and more volatile velocity of money and money multiplier(Neda popovska-Kammnar 2014, Qin 2017)

Central bank independence

- Decline in CIC led to smaller amount of asset-backed currency and smaller size of central bank’s balance sheet that could affect monetary operation (Barentsen 1997, Rogoff 2014)

- Decline in CIC could lessen seigniorage that could affect central bank’s revenue to pursue its mission(Fung et al 2014, BOK 2005). However, no central bank reported that its balance sheet has been effected from decline in CIC (BIS Survey 2000)

Monetary policy transmission

- Credit channel e-money will turn cash usage in deposit transfer that could promote money creation process (ธรรมรักษ์ 2011, Payment system insight 2013)

- Information-based lending could facilitate greater credit approval (นันทวัลลิ์ 2018)- Digital money issuer (non-bank) and disintermidiation (Lagard, 2017)

- Exchange rate channel e-Payment supports international trade via e-commerce. However, buyers and sellers might reduce their FX risk by using foreign currencies for domestic spending (dollarization). If this behaviorbecomes more popular, policy rate could have smaller impact on domestic spending (only via its local currency)

- Asset price channel e-Payment reduces transaction cost that could make money demand more sensitive to interest rates (flatter money demand curve). When policy rates change, demand for money will adjust faster(IMF, 2004)

13

Part I e-PaymentMonetary policy implication

Greater use of e-payment in Thailand has no direct impact on monetary operation under inflation targeting using short-term interest rate as operational target. However, it will affect central bank undermonetary targeting framework since velocity of money and money multiplier are more unpredictable

Monetary operation

Excess reserve

Required reserve OMOs

Standing facilities

Autonomous factors

Demand for reserves Supply of reserves

Source: FAQ issue 32 (Roong Mallikamas, 2554)

• CIC (e-Payment not significantly affected this part yet)• Government

deposit• FX intervention• Other factors

Monetary targeting framework (1998-2000)

Estimate velocity of money (V)

from MV = PY

Estimate money multiplier (m) from M = mB

Inflation targeting framework (2000 - present)

Assess economic activities and economic outlook

Ultimate target: GDP and Price (PY)

Specify i=intermediate target:Money Supply (M = PY/V)

Specify operational target:Monetary Base (B = M/m)

Increase or absorb:to achieve operational target

via R/P or swap

D0 D0

D1

S0

S1

R0 R1=R0

i0 i0

i1

Interest rate

Reserve balance

1) MPC hikes policy rate

2) BOT will adjust interest rate corridor following new policy rate

3) The demand for reserve curve shifts upward consistence with the new liquidity management behavior

14

Part I e-PaymentMonetary policy implication

0

2,000

4,000

6,000

8,000

Source: Bank of Thailand and authors’ calculation

Assets Liabilities

Foreign assets Current account(CA)

Domestic assets Notes issued

… OMOs

2

3

1 Customers convert their cash to prepaid e-money (less cash usage)

E-money issuers are required to deposit prepaid cash at the bank

Under excess liquidity condition, banks will deposit this extra liquidity in CA at BOT and invest in OMOs to earn interest income

Payment system Act B.E. 2560 said that the e-money issuers have to deposit the float to the commercial bank only e-money spending purpose

Seigniorage

=∆𝑚𝑜𝑛𝑒𝑦 𝑟𝑒𝑠𝑒𝑟𝑣𝑒 − 𝑐𝑜𝑠𝑡 𝑜𝑓 𝑖𝑠𝑠𝑢𝑖𝑛𝑔 𝑚𝑜𝑛𝑒𝑦

𝑐𝑜𝑛𝑠𝑢𝑚𝑒𝑟 𝑝𝑟𝑖𝑐𝑒 𝑖𝑛𝑑𝑒𝑥

0.00

0.01

0.02

0.03

0.04

0.05

0.06

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Net interest rate income

Monetary seigniorage

ลลบ.

0

2,000

4,000

6,000

8,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

BOT’s balance sheet Asset

Bn THB

International assets

Domestic asset

Liability and equity

Open Market Operations(BOT Bond, BRP)

EquityBanknotes in circulation

1980-1985 1999-2001 2006-2017

0.3 0.1 0.08*

0

Source: Bank of Korea (2005) * Bank of Thailand and authors’ calculation

Source: Bank of Thailand balance sheet (CUR)

Despite more popular use of e-Payment in Thailand, cash still grows and seigniorage has not declined yet. The BOT’s balance sheet expands overtime from FX reserve accumulation.However, decline in cash could impact BOT balance sheet by changing structure of liabilities with greater composition of interest-bearing liabilities from OMOs and smaller portion of cash (non-interest bearing) with lower seigniorage

Central bank independence

1

2

3

% of GDP

15

Part I e-PaymentMonetary policy implication

Channels Effectiveness of monetary policy

Interest rate Status quo depending on Banks’ balance sheet, the elasticity of interest rate on demand for deposits and the competition in banking sector.

Credit Slightly more effective1. Banks can reduce cash operation and allocate larger amount of money kept in bank accounts for lending2. Digital banking help facilitate banks to gain benefit from information-based lending

Asset price More effective Saver can switch their saving into various forms of financial assets easily with lower transaction cost

Exchange rate Tend to be more effective e-Payment facilitates cross-border capital flows movement and promotes e-commerce transaction across countries. Exchange rate could be more volatile by greater volume of transactions

Expectation Status quo depending on business and households' views on economic outlook and policy rate path

MP ST rate LT rate

bank reserves

asset prices wealth

Supply of loan total demand

Interest rate diff. exchange rate

expectation

bank lending

balance sheet

Transmission Mechanism

16

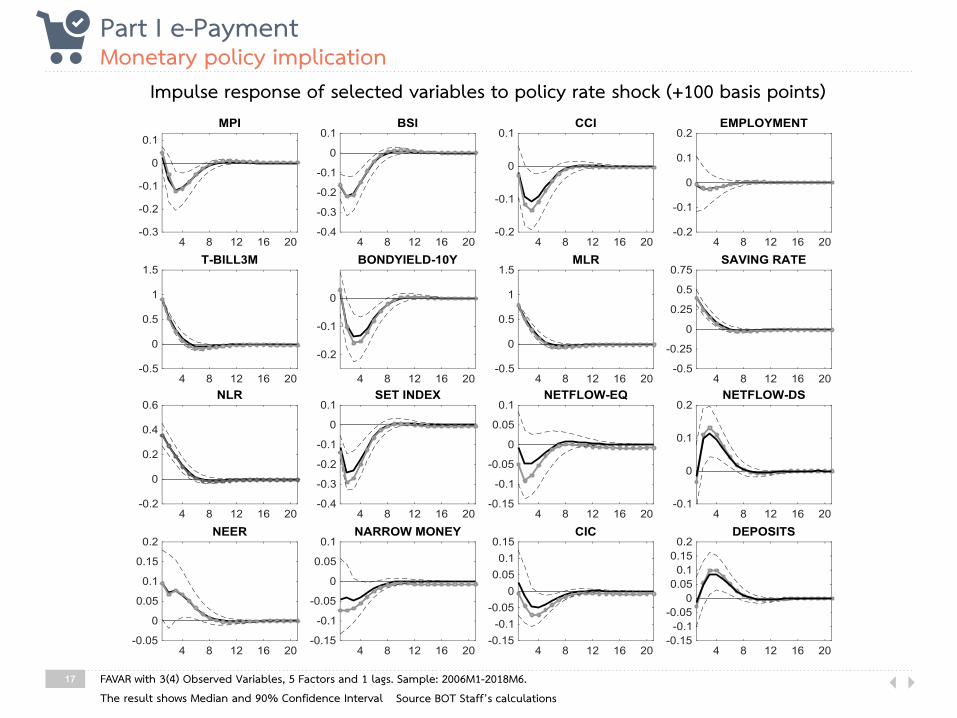

Part I e-PaymentMonetary policy implication

Empirical study of MP transmission mechanism in Thailand

where Ft = unobserved vector (k x 1)Yt = observed vector (m x 1)ф L = coefficient matrix of lag orderν t = error term (zero mean with constant covariance matrix)

Ft

Yt = ф L

Ft-i

Yt-i + νt

Observed Variables

Inflation, CEI, RP

113 Unobserved Variables

Baseline model Alternative modelInflation, CEI, RP, e-Payment

Consumption and investment 11Production, Expectation and Labor indicators 22Real estate and Price indicators 18Interest rates 22Exchange rate 7Money and credit quantity aggregates 10External sector and capital flow 7Government sector 7Stock price, Oil price, Global policy rates 9Total 113

Factor-Augmented Vector Autoregressive (FAVAR) model:

Source BOT Staff’s calculationsFAVAR with 3(4) Observed Variables, 5 Factors and 1 lags. Sample: 2006M1-2018M6. The result shows Median and 90% Confidence Interval

Base modelAlternative Model

Impulse response of selected variables to policy rate shock (+100 basis points)

17

Part I e-PaymentMonetary policy implication

Source BOT Staff’s calculationsFAVAR with 3(4) Observed Variables, 5 Factors and 1 lags. Sample: 2006M1-2018M6. The result shows Median and 90% Confidence Interval

Impulse response of selected variables to policy rate shock (+100 basis points)

18

Role of foreign non-bank

e.g. Alipay, Wechat

Crypto and its substitution effect on e-Payment usage

Exponential growth of e-Payment usage and

payment policy

Consumer behavior Large-scale competition

Regulatory and supervisory role for private digital

money issuers

Disintermediation

Promoting digital payment amid an increasing role of non-bank and FinTech

“With the amount of electronic money still very small …, the effect on monetary policy is not yet absolutely determinable. However, the central banks and economists must try

to anticipate the effects before it becomes more significant. ” Reynolds G. and Stephen F. (2013) Electronic money and monetary policy

• Streamline laws and regulations to support innovations • Build Interoperable Payment Infrastructures to support all sectors and further development• Enhance cross-border payment efficiency• Strengthen cyber resilience to maintain stability and trust• Increase adoption as well as improve literacy for a sustainable development

Part I e-PaymentFuture trend of e-Payment

19

Outline

Part II Digital currenciesII.I Current situation and looking ahead

II.II Policy options

20

Part II Digital currenciesDefinitions and current situation

Digital Currency (DC)

Crypto-currency• a separate sub-class of digital currencies, with their distinguishing

feature depending on the consensus mechanism applied for updating the ledger (Barrdear and Kumhof, 2016)

Crypto-currency => Non-fiat backed currency

DefinitionsAn asset stored in electronic form that can serve essentially the same function as physical currency, namely, facilitating payments transactions (BIS 2015)

Current situation

• Crypto-currency performs very poorly the 3 functions of money (Ali et al., 2014) Medium of exchange: very few merchants accept them Unit of account: ambiguous as some merchants adjust prices according

to exchange rate fluctuations vis-à-vis fiat currencies Store of value: more volatile than national currency pairs

21

Uses of Digital Currency (not mutually exclusive)I. Wholesale (B2B)II. Retail (B2C and C2C)III. New Asset Class

Note: limit scope to exclude lending/borrowing of digital currencies

Means of exchange

Part II Digital currenciesScenario analysis

22

• Digital currencies are popular among businesses, while regular people still use cash at large

• DLT’s efficiency and traceability prompt some businesses to adopt crypto as their means of exchange

• This has already happened in some business sectors, e.g. Ripple

Possibility: Very likely How to get here?• We’re already here!• If people trust this alternative system more,

then more businesses will move here

Part II Digital currenciesScenario I: Wholesale

Implications for Monetary Policy Transmission

Transmission channels Scenario I (Wholesale)

Interest rate Status quo

Credit Status quo

Asset price Status quo

Exchange rate Status quo

Expectation Status quo

Scenario I: Wholesale

23

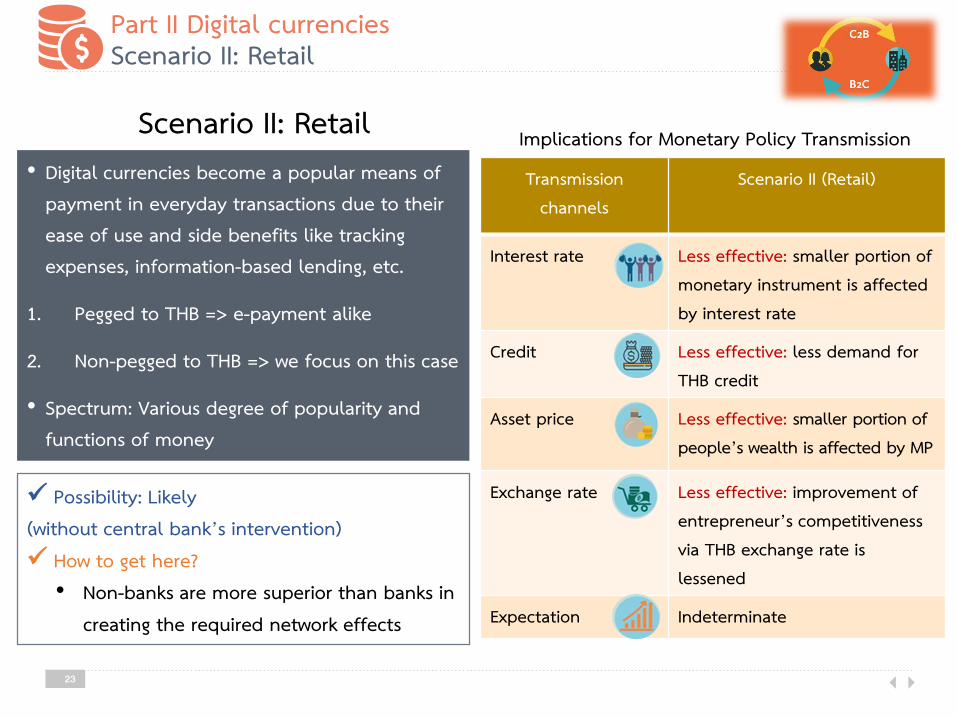

• Digital currencies become a popular means of payment in everyday transactions due to their ease of use and side benefits like tracking expenses, information-based lending, etc.

1. Pegged to THB => e-payment alike

2. Non-pegged to THB => we focus on this case

• Spectrum: Various degree of popularity and functions of money

Possibility: Likely (without central bank’s intervention) How to get here?• Non-banks are more superior than banks in

creating the required network effects

Part II Digital currenciesScenario II: Retail

Implications for Monetary Policy TransmissionScenario II: RetailTransmission

channelsScenario II (Retail)

Interest rate Less effective: smaller portion of monetary instrument is affected by interest rate

Credit Less effective: less demand for THB credit

Asset price Less effective: smaller portion of people’s wealth is affected by MP

Exchange rate Less effective: improvement of entrepreneur’s competitiveness via THB exchange rate is lessened

Expectation Indeterminate

24

Transmission channels

Scenario III(New Asset Class)

Interest rate Status quo

Credit Status quo

Asset price Indeterminate:• more asset choice for people

to invest in (Hawkins 2017) • the value of digital assets

depend on their properties.

Exchange rate Status quo

Expectation Status quo

• Digital currencies become digital assets instead

o e.g. cryptocurrencies, no longer functioned as means of exchange, become a conventional asset like stock, gold, or other commodities

Possibility: Likely How to get here?• Cryptocurrencies cannot become means of

exchange• The market becomes thicker, reducing the

volatility of the asset

Part II Digital currenciesScenario III: New Asset Class

Implications for Monetary Policy TransmissionScenario III: New Asset Class

25

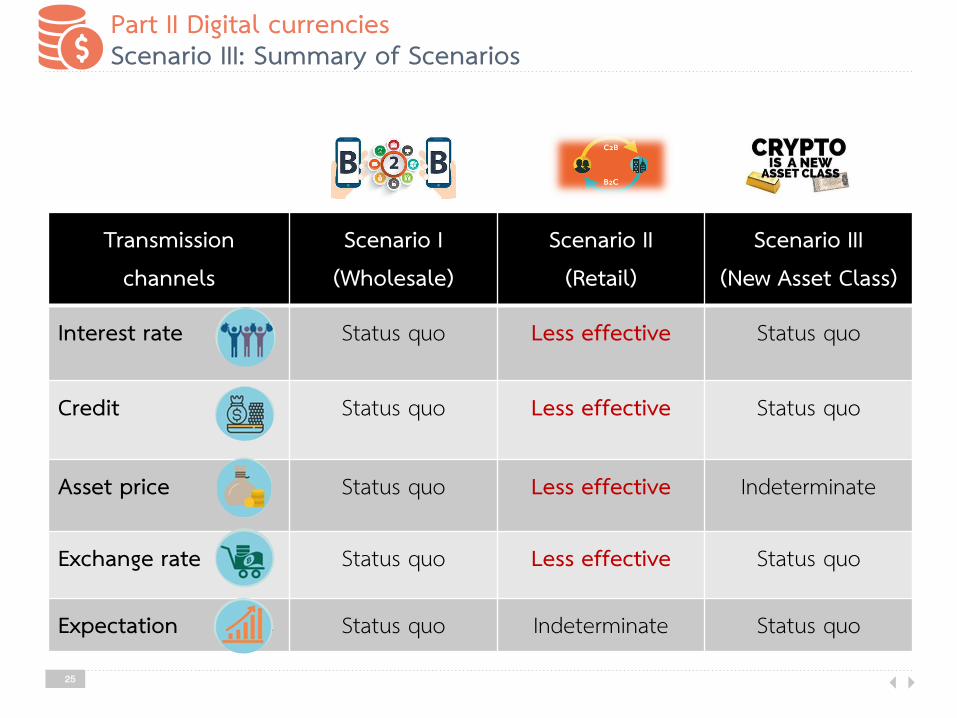

Transmission channels

Scenario I(Wholesale)

Scenario II(Retail)

Scenario III(New Asset Class)

Interest rate Status quo Less effective Status quo

Credit Status quo Less effective Status quo

Asset price Status quo Less effective Indeterminate

Exchange rate Status quo Less effective Status quo

Expectation Status quo Indeterminate Status quo

Part II Digital currenciesScenario III: Summary of Scenarios

26

• Doing nothing?• e-Payment?• Stricter investment regulations on digital currencies?• CBDC as a policy tool?

• If CB offers competing products that would enhance consumers’ retail payment experience, that would curb retail use of non-bank wallets

How to deal with these scenarios then?

Part II Digital currenciesBottom line

27

“central bank-issued money that combine cryptography and DLTs” (BBVA)

o Digitize cash to improve efficiency in payments (BIS)

o Develop a new monetary policy tool to overcome zero-bound interest rates (BBVA, BIS)

o Maintain access to central bank money given increasing competition from private DCs and e-payment (BBVA, BIS)

o Maintain control over financial conditions (BBVA, BIS)

Part II Digital currenciesCentral Bank Digital Currency (CBDC)

What are CBDCs?

Why are central banks considering them?

28

• Design of each case is based on their purpose • Operational aspects will be disregarded for brevity

3 Design options of CBDC

Objective Accessibility Interest-bearing Example

Design “A” For Interbank Settlement Restricted : Wholesale Unremunerated Project Inthanon

Design “B” Similar to cash Universal : Retail Unremunerated E-Krona

Design “c” Policy Tool Universal : Retail Remunerated ???

Design featuresAccessibility

Interest-bearingUniversal

Non-zero

Limited

Zero

Continuity24 / 79 to 5

AnonymityIdentified Anonymous

Part II Digital currenciesCentral Bank Digital Currency (CBDC)

Types of CBDC under consideration

29

Analysis of impact on MP transmission will focus on how each case would affect balance sheet composition of each agent, in terms of both quantity (q) and price (p)

Key assumptions

1) Supply of CBDC is controlled by the central bank through a market-based mechanism whereby cash/assets are exchanged for CBDC tokens in-kind.

2) No change in MP framework (IT). Policy rate is the main policy tool (no QE).

Asset LiabilityBalance Sheet

Transmission Mechanism

Part II Digital currenciesAssessment Framework

30

CBDC Designs

Design A: Wholesale CBDC Design B: Unrenumerated Retail CBDC Design C: Renumerated Retail CBDC

Part II Digital currenciesCBDC Designs

31

MP Transmission channels Case A – Wholesale CBDC

Interest rate Status quo

Credit Status quo

Asset price Status quo

Exchange rate Status quo

Expectation Status quo

Wholesale CBDC is unlikely to affect MP transmission because it does not contend with the two-tier banking system and is just a change in infrastructure intended to improve efficiency of RTGS systems (BIS, 2018).

Central bankBond Reserves

International reserves - CBDC

Other assets - CIC

Other debtEquity

Comm. BankLoans BorrowingBond Deposits

Reserves Other debt - CBDC Equity - Cash

Other assets

Non-bank

Deposits Borrowing

Bond Others

Cash

CBDC

Other assets

Implications for Monetary Policy Transmission

Part II Digital currenciesDesign A – Wholesale CBDC

32

Channels Case B – Unrenumerated retail CBDC

Interest rate Status quo

Credit Status quo (except during stress: Shift from deposits to CBDC could impact bank funding and credit provision especially during stress periods (bank runs).) During normal times however, such shift is unlikely since deposits still pays interest.

Asset price Status quo

Exchange rate Status quo

Expectation Indeterminate (but might lead to higher ELB due to less carrying cost of ‘cash’)

Implications for Monetary Policy Transmission

Unrenumerated Retail CBDC might affect MP transmission during stress because it is a safe asset that could be considered a ‘safer’ alternative to bank deposits.

Part II Digital currenciesDesign B – Unrenumerated retail CBDC

Central bankBond Reserves

International reserves - CBDC

Other assets - CIC

Other debtEquity

Comm. BankLoans BorrowingBond Deposits

Reserves Other debt - CBDC Equity - Cash

Other assets

Non-bank Deposits Borrowing

Bond Others Cash CBDC

Other assets

33

Channels Case C – Renumerated retail CBDC

Interest rate More effective: Bank rates would become more sensitive to changes in the policy rate to prevent deposit flight (CPMI, 2017) and minimize opportunity costs. The policy rate would act as a interest rate floor/ceiling (Meaning et al, 2018).

Credit Less effective: Mass conversion from deposits to CBDC would affect bank’s lending capacity (Stevens, 2017; BIS, 2018).

Asset price More effective: Changes in policy rate directly affects wealth.

Exchange rate Status quo

Expectation More effective: No ELB allows central banks to send strong policy signals through extreme rate cuts, especially in the down cycle (Stevens, 2017)

Implications for Monetary Policy Transmission

Renumerated Retail CBDC could affect MP transmission significantly as it gives central banks stronger control over domestic financial conditions through the CBDC interest rate (policy rate).

Part II Digital currenciesDesign C – Renumerated retail CBDC

Central bankBond Reserves

International reserves - CBDC

Other assets - CIC

Other debtEquity

Comm. Bank Loans Borrowing

Bond Deposits

Reserves Other debt - CBDC Equity - Cash

Other assets

Non-bank Deposits Borrowing Bond Others Cash CBDC

Other assets

34

Part II Digital currenciesSummary of the implications of CBDC designs

Channels Design A(Wholesale)

Design B(Unrenumerated Retail)

Design C(Renumerated Retail)

Interest rate Status quo Status quobut may cause one-time

shift in bank rates

More effective

Credit Status quo Status quo(except during stress)

Less effective

Asset price Status quo Status quo More effective

Exchange rate Status quo Status quo Status quo

Expectation Status quo Indeterminate More effective

Disintermediation of commercial banks / emergence of narrow-banking

• Retail banking would face direct competition from central banks narrow banking with the result threat to aggregate credit (BBVA, 2017)

Validity of ELB argument

• Negative interest rate policy (NIRP) not be politically feasible.

• Eliminating larger bank notes to increases costs of holding cash lowers ELB (Rogoff, 2016; Engert, 2017)

Financial stability implications

• Banks may engage in high risk lending to offset higher funding cost (BIS, 2018)

• CBDCs allow for ‘digital runs’ towards the central bank with unpredecented speed and scale (BIS, 2018)

Autonomy problem

• Loss of seigniorage income might not an issue for some central banks (Engert, 2017)

• Unlikely that cryptocurrencies will completely replace fiat currencies unless there is massive lost of trust in the central bank. Central banks must maintain trust through credible policies (He, 2018)

Part II Digital currenciesAre retail CBDCs really the solution to the autonomy problem?

• With increasing competition from private DCs would force central bank to move towards CBDCs.

• However, central banks must carefully weigh the implications for financial stability and monetary policy of issuing each case of CBDC.

Part II Digital currenciesBottom line

Issues for consideration Case “A” Case “B” Case “C”

Perform full functions of money

Able to compete with retail crypto-currencies -

Net Impact on MP transmission mechanism Status quo Status quo More effective

Financial stability issues - - • Narrow banking• Moral Hazard

e-Payment• How much retail e-payment could substitute cash usage in Thailand?

Small substitution effect

• How would e-payment affect monetary aggregates, central bank's balance sheet, velocity of money, money multiplier? How would this affect the transmission of monetary policy or monetary operations? Not yet observe any negative impact from e-Payment on monetary operation in the transition

toward less-cash society. E-payment trend strengthens MP transmission via credit and asset price channels.

Conclusione-Payment & Digital Currencies

Digital Currencies• How would the emergence of private digital currencies affect transmission of monetary policy in 5

traditional channels? Most likely affect through credit and asset price channels (depends on each scenario)

• What are the policy options available to central banks, and how would this change the transmission of monetary policy? e-Payment, Regulations, CBDC

“Central banks must maintain the public’s trust in fiat currencies and stay in the game in a digital, sharing, and decentralized service economy.”

Dong HeDeputy Director, IMF

Monetary Policy in the Digital Age, June 2018

39

Thank you