did structured credit fuel the lbo...

TRANSCRIPT

THE JOURNAL OF FINANCE • VOL. LXVI, NO. 4 • AUGUST 2011

Did Structured Credit Fuel the LBO Boom?

ANIL SHIVDASANI and YIHUI WANG∗

ABSTRACT

The leveraged buyout (LBO) boom of 2004 to 2007 was fueled by growth in collat-eralized debt obligations (CDOs) and other forms of securitization. Banks active instructured credit underwriting lent more for LBOs, indicating that bank lending poli-cies linked LBO and CDO markets. LBO loans originated by large CDO underwriterswere associated with lower spreads, weaker covenants, and greater use of bank debtin deal financing. Loans financed through structured credit markets did not lead toworse LBOs, overpayment, or riskier deal structures. Securitization markets alteredbanks’ access to capital, affected their lending policies, and fueled the recent LBOboom.

FROM 2004 TO 2007, $535 billion of leveraged buyouts (LBOs) were completed,more than 10 times the $50 billion of volume over the previous 8 years from1996 to 2003 (see Figure 1), vastly eclipsing the $227 billion (in 2007 dollars)of volume during the prior 1986 to 1989 LBO boom. The LBO boom of 2004 to2007 collapsed as dramatically as it rose, with LBO volume dropping by 94%in the fourth quarter of 2007 from the prior-year level.

Most explanations for LBOs are based on trade-off theories of capital struc-ture whereby LBOs create value from interest tax shields, lower agency costs,and operational improvements. While variation in these benefits may havecontributed to the large changes in LBO volumes, the 2004 to 2007 LBO boomalso coincided with important developments in structured credit markets thatpotentially altered the supply of credit. In a Modigliani and Miller (1958) worldin which the supply of capital is perfectly elastic, leverage ratios and the inci-dence of highly leveraged transactions are determined only by the demand for

∗Shivdasani is at Kenan-Flagler Business School, University of North Carolina at Chapel Hill.Wang is at the Department of Finance, Chinese University of Hong Kong. We thank two anonymousreferees, an associate editor, Greg Brown, Sudipto Dasgupta, John Graham (Editor), Cam Harvey,Matthias Kahl, Wayne Landsman, Micah Officer, Paige Ouimet, Chris Parsons, Adam Reed, JayRitter, Steffen Sascha, Ed Van Wesep, and seminar participants at the 2010 American FinanceAssociation meeting in Atlanta, the 2010 China International Conference in Finance meetingin Beijing, the 2010 European Finance Association meeting in Frankfurt, American University,Australia National University Summer Finance Camp 2009, Chinese University of Hong Kong,City University of Hong Kong, Hong Kong Baptist University, Nanyang Technological University,Southern Methodist University, Texas Christian University, Tsinghua University, University ofFlorida, University of North Carolina, University of Oregon, and University of Wisconsin at Madi-son for helpful comments. We thank Chris Flanagan and Kedran Panageas of JP Morgan andMarc Auerbach and William Chew of S&P for helpful discussions. We thank Asset-Backed Alertfor sharing their data and updating the sample to include recent deals. An earlier version of thispaper was titled “Does Credit Supply Drive the LBO Market?.”

1291

1292 The Journal of Finance R©

0

30

60

90

120

150

180

0

20

40

60

80

100

120T

otal

CD

O I

ssua

nce

Vol

ume

($bn

)

Tot

al L

BO

Vol

ume

($bn

)

Total LBO Volume (Right) Total CDO Issuance (Left)

Figure 1. LBO volume and CDO issuance volume (1996–2009). Total LBO volume is theaggregate transaction value of deals announced in each quarter between 1996 and 2009 for a totalof 369 LBO deals from SDC satisfying the following criteria: The deal is completed by January 2010;the target is a U.S. company and publicly traded; transaction value is greater than $10 million; atleast 50% of common shares are acquired in the deal; and the acquirers own 100% of the sharesafter. Transaction value of LBO is the total value of consideration paid by the acquirer, excludingfees and expenses. The CDO issuance volume aggregates the total CDOs issued worldwide. TheCDO sample, from ABS Database, includes CDO issues rated by at least one major rating agencyand under the control of a trustee. LBO is leveraged buyout; CDO is collateralized debt obligation.

corporate debt. Under this framework, structural changes affecting the sup-ply of credit should not affect the volume and financing of LBO transactions.Evidence that such structural changes do in fact matter would thus indicatethat capital market frictions affecting the availability of credit are an impor-tant element missing from the Modigliani and Miller framework. Faulkenderand Petersen (2006), Sufi (2009), Lemmon and Roberts (2010), Leary (2009),and Becker and Ivashina (2010) explore the importance of such supply-sideeffects in capital structure decisions. We extend this work by studying whethersupply-side effects contributed to the large boom in the LBO market and howthey affected the quality of LBO deals.

A hallmark of the 2004 to 2007 period was the expansion of the marketfor collateralized debt obligations (CDOs). The growth was particularly sharpfor CDOs backed by corporate loans, also referred to as collateralized loanobligations (CLOs). Bank loans used to finance LBOs were often placed inthese CLO vehicles. Hence, the CDO channel potentially increased the supplyof credit by allowing a wide range of institutional investors such as hedge

Did Structured Credit Fuel the LBO Boom? 1293

funds, insurance companies, pension funds, and other institutional investorsthat invest in CDOs to indirectly invest in LBO loans. In addition, placing LBOloans into CLOs may have allowed banks to lend more because they becameless constrained by their balance sheets since they no longer needed to meetcapital requirements when the loans were sold to CLOs. To satisfy investordemand for CDOs, CDO issuers also needed collateral assets, providing banksthat underwrote CDOs an incentive to originate loans so as to fund LBOs thatcould be placed in CDOs. We argue that the growth in the CDO market providedan important source of funding to finance LBOs.

We document a high correlation between the growth of the LBO and CDOmarkets and show that CDO issuance exploded concurrently with the LBOboom of 2004 to 2007. Aggregate CDO issuance rose to $1.3 trillion over 2004to 2007, twice the total issuance volume over the previous 8 years (see Figure 1).CDO issuance then dropped sharply in the second half of 2007 when the LBOboom came to an end. This is consistent with the view that increased supplyof credit from the CDO market fueled LBO transactions. Alternatively, anincrease in the demand for LBO transactions could generate increased demandfor bank loans, leading banks to create CLO vehicles to distribute these loansto investors. In addition, it is possible that both the LBO and CDO marketsgrew simultaneously because of some omitted factors during the boom period.

To disentangle supply- and demand-side factors, we study securitizationssuch as structured product CDOs that are not directly affected by the demandfor LBOs. Structured product CDOs hold securitized assets1 but do not investin corporate loans or bonds generated by LBOs. We also study asset-backedsecurities (ABS), the collateral assets of which include home equity loans,credit card loans, auto loans, and student loans, none of which are driven by thedemand for LBOs. Though neither structured product CDOs nor ABS includeLBO loans as collateral, their issuance volumes are also highly correlated withLBO volume. Thus, the link between the LBO and CDO markets cannot beexplained by increased demand for LBO financing.

One of our primary results is that in a bank fixed effects model, we find apositive within-bank correlation between a bank’s LBO lending and its accessto CDO capital through underwriting capabilities. In the years when a bankunderwrote more structured CDOs (which exclude LBO loans or bonds), it alsooriginated a larger volume of loans to finance LBOs. Since this result holds ina bank fixed effects framework, it cannot be attributed to a bank-level time-invariant omitted factor. In addition, we do not find that a similar relation holdsfor investment-grade lending, indicating that the increased credit supply is ob-served only in the leveraged loan market, where structured credit vehicles wereactive. We also show that a bank’s experience in CDO underwriting prior to theLBO boom is strongly associated with its LBO lending during the boom years.This helps establish that a bank’s LBO lending during the boom is related to itsexpertise in securitization rather than some factor correlated with the boom.

1 Such assets include residential mortgage-backed securities, commercial mortgage-backed se-curities, collateralized mortgage obligations, asset-backed securities, and other securitized assets.

1294 The Journal of Finance R©

It is harder to rule out a link between the LBO and CDO markets thatarises from an omitted factor that varies over time. For example, it is possiblethat both markets grew due to a decrease in the perception of risk. While wecannot eliminate this possibility, we provide several pieces of evidence thatindicate a direct link between the two markets. We show that the institutionaltranches, which represent the allocation of LBO loans to institutional investorssuch as CLOs, were considerably higher during the LBO boom years than inthe preboom years. In addition, we find a positive association between theCDO underwriting activity of the lead banks and the allocation of the LBOloan to institutional investors. This suggests that CDOs were more importantinvestors in LBO loans during the boom years and that better access to CDOinvestors allowed banks to raise more capital from these investors to financetheir LBO loan commitments.

A bank’s underwriting in CDO markets was also strongly associated withthe cost of LBO loans for its borrowers. We show that banks with large CDOunderwriting businesses offered cheaper credit and looser covenant protectionand LBO transactions funded by these banks employed bank loans more ag-gressively. Thus, a bank’s CDO underwriting activity was linked to easier creditterms for LBO financing.

We examine the implications of the lower cost of credit for LBO financingassociated with the CDO channel. Lower financing costs should make morefirms desirable LBO candidates by making previously marginal LBO targetsmore attractive. It is also possible that the ability of banks to sell LBO loansto CDOs instead of holding the loans on their balance sheets reduced theirscreening incentives and led banks to finance lower quality transactions. Inthe context of the subprime mortgage market, Keys et al. (2010) argue thatsecuritization adversely affected the screening incentives of mortgage lenders.

To explore these issues, we examine whether banks’ access to structuredcredit markets was associated with changes in the quality of LBO transactions.Based on the characteristics of the LBOs, we do not find that bank fundingfrom structured credit was associated with weaker screening incentives in LBOlending. Target firms in CDO-driven deals generated more free cash flows, paidmore taxes, and were less risky. This finding is surprising if lower financingcosts allowed previously marginal LBO deals to become worthwhile duringthe boom period. One possible explanation is that CDO-driven LBOs weremuch larger firms—on average four times the size of non-CDO-led LBOs. Thus,a primary impact of the CDO channel was to facilitate much larger LBOsthan historically possible, potentially because it helped relax balance sheetconstraints that banks faced in financing large LBOs. This is consistent withdevelopments in structured credit markets allowing banks to finance largeLBOs rather than facilitating worse deals.

When we consider LBO pricing, we do not find evidence indicating over-payment in CDO-driven deals. In fact, the trajectory of credit ratings fol-lowing LBOs indicates better ex post performance of CDO-driven deals thannon-CDO-driven deals. We also do not find that CDO-driven deals during theboom period were financed with lower equity contributions compared to other

Did Structured Credit Fuel the LBO Boom? 1295

LBOs. Overall, these results suggest that banks retained their incentives toscreen borrowers when originating LBO loans even when they sold the loansto CLOs, possibly because of incentives to preserve their reputation as diligentunderwriters.

Our paper contributes to the emerging literature on how securitization af-fects the behavior of credit borrowers and lenders. Mian and Sufi (2009) findthat securitization contributed to the growth of the subprime mortgage market.Loutskina and Strahan (2009) show that mortgage securitization increased thewillingness of banks to increase their mortgage lending. Nini (2008) shows thatthe growth of institutional investors increased the supply of credit to firms withspeculative-grade ratings. We find a similar pattern in the context of LBO lend-ing by demonstrating an association between the growth of the securitizationmarket and LBOs. Though some have argued that deteriorating loan qualityassociated with securitization of subprime mortgages contributed to the recentfinancial crisis (Brunnermeier (2009)), we do not find evidence of lower qualityfor corporate lending in the setting of LBO transactions.

Our results suggest that financing from structured credit markets is notnecessarily associated with lower quality transactions. Kaplan and Stein (1993)show that junk bond investors contributed to overheating of the LBO marketin the late 1980s. Unlike high-yield bonds, loans sold to CDOs were originatedby banks, which may have resulted in stronger incentives for banks to screenborrower quality. Our evidence complements other studies of the recent LBOboom. Demiroglu and James (2010) and Ivashina and Kovner (2011) examinethe reputation of private equity groups and their relationship with lenders.Other studies exploring related issues include Acharya and Johnson (2010),Axelson et al. (2010), Boone and Mulherin (2009), Guo, Hotchkiss, and Song(2011), Kaplan and Stromberg (2009), Metrick and Yasuda (2010), and Officer,Ozbas, and Sensoy (2010).

The paper proceeds as follows. Section I describes the markets for CDOsand leveraged loans in more detail. Section II describes the sample and thedata. Section III presents our main results. Section IV examines the effects ofCDO lending on the structure, pricing, and quality of recent LBO transactions.Section V concludes.

I. Background: CDOs and Leveraged Loans

A. Collateralized Debt Obligations

CDOs are notes issued by a special purpose vehicle (also referred to as aCDO vehicle) that are collateralized by a portfolio of assets. Depending on theunderlying assets, CDOs are classified as CLOs, collateralized bond obliga-tions (CBOs), or structured product CDOs that invest in structured productsand notes. Unlike traditional pass-through securitization involving most ABSand mortgage-backed securities (MBS), CDO notes are usually divided intotranches with different seniority. The senior tranches have investment-graderatings, with the majority at AAA even though the collateral assets might be

1296 The Journal of Finance R©

rated much lower.2 Before the financial crisis of 2007 and 2008, almost 60% ofthe structured finance notes received an AAA rating (Fitch Ratings (2007)).

The higher rating of senior tranches allowed CDOs to be sold to a broaduniverse of investors such as banks, insurance companies, pension funds, andcertain asset managers that might not have otherwise invested in high-yield in-struments. Hence, the tranching process allowed speculative-grade assets un-derlying the CDOs to be financed using the much larger capacity of investment-grade markets. CLOs, which primarily held leveraged loans that could be usedto finance LBOs, were a very important part of the CDO market and attractedmany of the same investors that invested in CDOs.3 For example, about halfof the CDOs that insurance companies purchased were CLOs, according toCiti Credit Research (2007). Thus, CLOs helped bring new investors to theleveraged loan market, investors who had historically participated in securiti-zation markets primarily through traditional channels such as ABS and MBS.4

Figure 2 depicts how CDO markets were used in the financing of LBO trans-actions.

A potentially important driver behind the growth of CDOs was the changein banks’ incentives regarding tranching in securitization resulting from theBasel II Accord, published in June 2004.5 The CDO market allowed banks tosell risky assets with high capital requirements (such as leveraged loans) toCDO investors, while at the same time investing in the senior CDO tranches,which required less capital.6 The incentive of banks to hold senior trancheswas a critical element in the expansion of the CDO market because most ofthe other major CDO investors (e.g., hedge funds) were more interested inthe higher risk junior tranches. In addition, Coval, Jurek, and Stafford (2009a)and Brennan, Hein, and Poon (2009) document pricing errors for CDO tranches,

2 Coval, Jureck, and Stafford (2009b) discuss how high ratings were achieved given the muchriskier collateral assets in CDOs. Benmelech and Dlugosz (2009) and Griffin and Tang (2010) arguethat CDO notes were overrated before the crisis.

3 According to the Securities Industry and Financial Markets Association (SIFMA), all of theCLOs issued between 2005 and 2007 were backed by leveraged loans.

4 Though systematic data on investor participation in various securitization markets are un-available, discussions with industry professionals suggest a high overlap between investors inCDO, CLO, and ABS markets. Such overlap also exists between the CLO and MBS markets,though some credit and corporate funds tend to invest in CLOs but not in mortgage and realestate assets. On the other hand, some dedicated mortgage funds tend to invest in MBS and realestate–related equities but do not invest in CLOs. In subsequent tests, we focus more on the ABSmarkets than the MBS markets due to their higher potential overlap in investor base with CLOs.However, our results are qualitatively similar if we use variables based on MBS markets.

5 Though Basel II had not been uniformly implemented in the United States during our sampleperiod, JP Morgan (2007) argues that the effects of its implementation were clearly anticipatedin market prices. During this period, most large “internationally active” banks moved toward arisk-based capital approach both for their internal capital management and for communicatingtheir capital positions to analysts and investors.

6 Under Basel II, the weight on some AAA investments in securitized assets is only 7%. With an8% capital requirement, an investment in an AAA security requires banks to put up only 0.56%(7% x 8%) capital for the invested asset, an implicit leverage of 178 (1/0.56%). JP Morgan (2007,p. 118) notes that “the Basel II capital framework for securitization was a key driver of the excessiveleverage applied to ABS securities via structured finance CDOs.”

Did Structured Credit Fuel the LBO Boom? 1297

Figure 2. Illustration of LBO financing and the structure of securitization markets.LBO is leveraged buyout; CLO is collateralized loan obligation; CDO is collateralized debt obliga-tion; ABS is asset-backed securities; MBS is mortgaged-backed securities; CBO is collateralizedbond obligation; SIV is structured investment vehicle.

offering another potential explanation for the rapid growth in the CDO marketduring this period.

B. Leveraged Loans

Leveraged loans are bank loans issued to borrowers with speculative-graderatings, most of which are syndicated. In the syndicated loan market, investorscan be classified into pro rata investors and institutional investors. Accordingto S&P (2006), commercial banks and finance companies typically invest inrevolvers and term loan A (or amortizing term loan) tranches, also referredto as pro rata tranches. CLO vehicles, prime funds, hedge funds, and insur-ance companies typically comprise the bulk of institutional investors. Theseinvestors invest in the term loan B, C, and D tranches, also referred to as insti-tutional tranches. Term loan A tranches have an amortization structure whileinstitutional term loan tranches repay toward the end of the term. Hence, in-stitutional tranches tend to be riskier and are priced at higher spreads thanpro rata tranches.7 Since CLO vehicles invest in institutional tranches, our

7 After 2001, spreads on an increasing number of institutional tranches were priced closer topro rata tranches, and in some cases were even lower according to S&P (2006), which attributesthis pattern to the higher demand for leveraged loans from institutional investors.

1298 The Journal of Finance R©

0

10

20

30

40

50

60

70

0

20

40

60

80

100

120

140

160

$Bil

lion

$Bil

lion

Pro Rata Volume (Left) Institutional Volume (Left) CLO Issuance (Right)

Figure 3. Leveraged loan allocation and CLO issuance volume. The figure shows quar-terly volume of newly issued leveraged loans broken down by pro rata and institutional marketallocation, and the issuance volume of collateralized loan obligations (CLOs). The leveraged loanvolume is from S&P’s LCD and CLO volume is calculated using the ABS Database.

tests focus on the pricing of these tranches, which is referred to as the insti-tutional spread and measured as the spread on the term loan B tranche, themost common institutional tranche.

CLO vehicles were one of the most important investors in the institutionalmarket, representing 60% of the institutional investor volume in primary mar-kets of leveraged loans by 2006 (S&P (2006)). Thus, during the LBO boom, asubstantial part of the financing of leveraged loans came from CLO vehicles.Consistent with the active participation of CLOs in institutional tranches,Figure 3 displays a close linkage between CLO issuance volumes and the allo-cation of leveraged loans to institutional tranches during the LBO boom. Thefraction of institutional tranches in leveraged loans was 70% to 80% duringthe peak of the LBO boom but dropped to 40% by the end of 2008 as CLO is-suance declined sharply at the onset of the financial crisis. Figure 3 also showsthat CLO issuance volumes were not closely linked to the pro rata allocations,consistent with the observation that CLOs rarely invest in pro rata tranches.

II. Data and Sample Description

A. The LBO Sample

Our sample consists of 345 LBOs from SDC Platinum satisfying the followingcriteria: The transaction was announced between 1996 and the second quarterof 2008 and completed by July 2008; the target is a publicly traded U.S. com-pany; the transaction value is at least $10 million; at least 50% of the common

Did Structured Credit Fuel the LBO Boom? 1299

shares were acquired; and the buyers owned 100% of the shares upon comple-tion. Our minimum deal value of $10 million is lower than that in some otherstudies, such as Kaplan (1989b) and Guo, Hotchkiss, and Song (2011) and ischosen to avoid biasing against earlier time periods when smaller deals weremore common.

Figure 1 shows that LBO volume rose in the second quarter of 2004, when$5.6 billion of LBOs were announced. The pace of LBOs picked up dramatically,reaching $20 billion in the last quarter of 2005. At $255 billion of announceddeal volume, 2006 was a record year for LBOs. With the onset of the creditturmoil, LBO volume dropped to $32 billion in the third quarter of 2007 and tounder $5 billion in the first quarter of 2008. The number of deals also increasedduring 2004 and 2007 but less dramatically because much larger LBO deal sizeswere a hallmark of the boom period.

We match the LBO targets with LBO loans from Loan Pricing Corporation’s(LPC) DealScan and collect data on tranche types and amounts, lead arrangers,spreads, maturity, and other terms. We also manually collect data from proxyfilings as well as from schedules 14A, TO-T, S-4, and 13E3 when these filingsare available in Edgar. We check these filings for two reasons. First, someLBO loans, particularly for smaller deals, are not in DealScan. For these loans,we collect information on the loan contract whenever available. Second, sinceDealScan does not identify which loans are asset-backed, we use information inproxy filings to remove tranches that can be identified as asset-backed financ-ing.8 Asset-backed loans are excluded to avoid potential bias resulting fromsecuritized financing other than CDOs.9

We are able to collect data on lead arrangers and borrowing amounts for275 loans financing 241 deals (70% of the sample). We lose some observationsbecause several small deals were funded by cash, mezzanine finance, or equityand did not arrange bank loans to finance the deals. Other deals were notconditioned on the availability of financing and thus lack disclosure on loans.In addition, we exclude a few asset-backed loans, and, for some firms, filingsare unavailable on Edgar.

The volume of bank loans in each quarter is shown in the Internet Ap-pendix.10 The pattern mirrors the volume of LBO transactions, with heavyvolume between the second quarter of 2004 and the first half of 2007. To-tal bank borrowing peaked in the second quarter of 2007, while LBO volumepeaked at the end of 2006.11 On average, bank loans comprise 53% of LBO

8 For example, commercial mortgage-backed financings were used in the buyouts of UICI, LaQuinta, and Station Casinos, but these are included in DealScan and flagged as “other loan”tranches, which are not distinguishable from other loans.

9 When DealScan and proxy filings differ, we retain the DealScan information since termsspecified in proxy filings are sometimes adjusted after the filing and hence may not be the finalterms.

10 The Internet Appendix is available on The Journal of Finance website at http://www.afajof.org/supplements.asp.

11 The reason for LBO volume and LBO loan volume to peak at different times is because theloan sample excludes commercial mortgage financing for a few large deals announced in the fourth

1300 The Journal of Finance R©

volume, indicating that they represented the most important form of financingfor LBOs during our sample period.

We also identify the financing structure for 235 (68.1%) of the sample deals.We collect information on nonbank financing from proxy filings, supplementedwith SDC’s data on high-yield bond issuance. We record the total fundingneeded to complete the deal and the amounts of total equity financing frompost- and pre-LBO investors, asset-backed financing, high-yield bonds/notes,and mezzanine finance when available.12

B. Data on CDO and Other Securitized Issues

Data on CDOs and other securitized issues are from Asset-Backed Alert’sABS Database, which provides the initial terms of all rated issues of ABS,MBS, and CDOs worldwide.13 The first full year of CDO coverage begins in1996 and hence we use this as the starting point for our sample.

From 1996 through the second quarter of 2008, 4,542 CDOs with a total valueof $1.9 trillion were issued. Figure 1 shows the virtually identical trajectoriesin the LBO and CDO markets, with both markets rising and falling at the sametime. The correlation between the natural log of quarterly LBO volumes andof CDO issuance volumes is quite strong at 0.68.

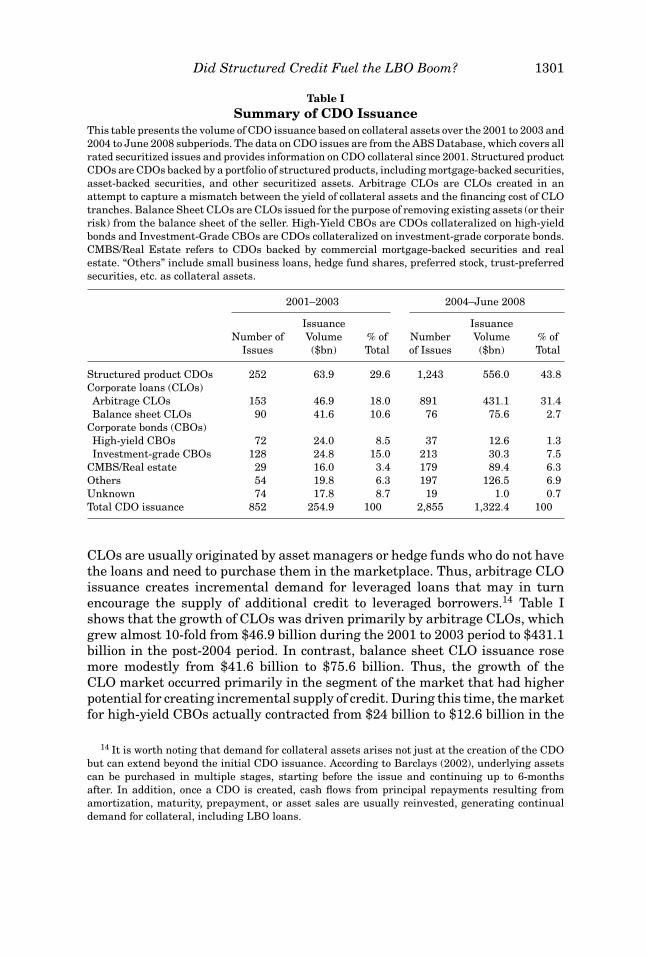

Table I summarizes the CDO market. We have detailed data on the under-lying collateral for CDOs after 2001. Hence, we compare CDO issuance during2001 and 2003 to the post-2004 period. The CDO market witnessed explosivegrowth during this period, rising from aggregate issuance volume of $255 bil-lion to over $1.3 trillion. The growth was particularly pronounced for structuredproduct CDOs, whose issuance volume rose from $63.9 billion over the 2001 to2003 period to $556 billion in the post-2004 period. CLOs also experienced verystrong growth, with issuance volume rising from $88.5 billion to $506.7 billion.

CLOs are either balance sheet or arbitrage CLOs, depending on the purposeof issuance. A balance sheet CLO is typically originated by a bank that seeks toremove its existing loans (or their risk) from its balance sheet. Since the loansin a balance sheet CLO already exist on a bank’s loan book, these CLOs do notgenerate much additional demand for leveraged loans. In contrast, arbitrage

quarter of 2006, including the $41 billion LBO of Equity Office Properties and the $28 billionbuyout of Harrah’s Entertainment.

12 Total funding needs include cash needed to pay off equity, option, and warrant holders; retireexisting debt; and pay for fees and expenses related to the deal. The amount of bank financing isfrom the bank loan data set. When a deal cannot be matched with a bank loan in the loan sample,and the proxy filings indicate no bank financing, bank financing is assumed to be zero. Bridge loansor other bridge financing are recorded as high-yield bond/note and mezzanine finance. The amountof high-yield bond issues is supplemented by bond issuance data in SDC for 40 deals for whichthe hand-collected amounts are different from proceeds recorded in SDC. Equity contributions andasset-backed financing are from proxy filings.

13 To be included in the ABS Database, an issue must be rated by at least one major rating agency,under control of a trustee, and collateralized on some assets. The data set excludes commercialmortgage-backed issues, agency-sponsored MBS, issues by municipalities, tax-exempt issues, andasset-backed commercial paper issues.

Did Structured Credit Fuel the LBO Boom? 1301

Table ISummary of CDO Issuance

This table presents the volume of CDO issuance based on collateral assets over the 2001 to 2003 and2004 to June 2008 subperiods. The data on CDO issues are from the ABS Database, which covers allrated securitized issues and provides information on CDO collateral since 2001. Structured productCDOs are CDOs backed by a portfolio of structured products, including mortgage-backed securities,asset-backed securities, and other securitized assets. Arbitrage CLOs are CLOs created in anattempt to capture a mismatch between the yield of collateral assets and the financing cost of CLOtranches. Balance Sheet CLOs are CLOs issued for the purpose of removing existing assets (or theirrisk) from the balance sheet of the seller. High-Yield CBOs are CDOs collateralized on high-yieldbonds and Investment-Grade CBOs are CDOs collateralized on investment-grade corporate bonds.CMBS/Real Estate refers to CDOs backed by commercial mortgage-backed securities and realestate. “Others” include small business loans, hedge fund shares, preferred stock, trust-preferredsecurities, etc. as collateral assets.

2001–2003 2004–June 2008

Issuance IssuanceNumber of Volume % of Number Volume % of

Issues ($bn) Total of Issues ($bn) Total

Structured product CDOs 252 63.9 29.6 1,243 556.0 43.8Corporate loans (CLOs)Arbitrage CLOs 153 46.9 18.0 891 431.1 31.4Balance sheet CLOs 90 41.6 10.6 76 75.6 2.7

Corporate bonds (CBOs)High-yield CBOs 72 24.0 8.5 37 12.6 1.3Investment-grade CBOs 128 24.8 15.0 213 30.3 7.5

CMBS/Real estate 29 16.0 3.4 179 89.4 6.3Others 54 19.8 6.3 197 126.5 6.9Unknown 74 17.8 8.7 19 1.0 0.7Total CDO issuance 852 254.9 100 2,855 1,322.4 100

CLOs are usually originated by asset managers or hedge funds who do not havethe loans and need to purchase them in the marketplace. Thus, arbitrage CLOissuance creates incremental demand for leveraged loans that may in turnencourage the supply of additional credit to leveraged borrowers.14 Table Ishows that the growth of CLOs was driven primarily by arbitrage CLOs, whichgrew almost 10-fold from $46.9 billion during the 2001 to 2003 period to $431.1billion in the post-2004 period. In contrast, balance sheet CLO issuance rosemore modestly from $41.6 billion to $75.6 billion. Thus, the growth of theCLO market occurred primarily in the segment of the market that had higherpotential for creating incremental supply of credit. During this time, the marketfor high-yield CBOs actually contracted from $24 billion to $12.6 billion in the

14 It is worth noting that demand for collateral assets arises not just at the creation of the CDObut can extend beyond the initial CDO issuance. According to Barclays (2002), underlying assetscan be purchased in multiple stages, starting before the issue and continuing up to 6-monthsafter. In addition, once a CDO is created, cash flows from principal repayments resulting fromamortization, maturity, prepayment, or asset sales are usually reinvested, generating continualdemand for collateral, including LBO loans.

1302 The Journal of Finance R©

post-2004 period, indicating that CBOs were not an important channel throughwhich structured credit helped finance LBOs.

In the Internet Appendix, we summarize the size of the entire structuredcredit market. The total volume of securitized issues rose from $4.76 trillionover 1996 to 2003 to $8.07 trillion over the next four and half years. The bulk ofthe growth arises from expansion of the CDO market and of structured creditlinked to U.S. and non-U.S. residential real estate. Total CDO issuance morethan doubled during this period, and issuance of U.S. MBS and home equityloan ABS along with non-U.S. residential MBS/ABS also doubled.

III. Results

A. Correlation between LBO and CDO Markets

LBO and CDO volumes can be positively correlated due to factors affect-ing either the demand or the supply of LBO loans. Increased supply of capitalthrough structured credit may drive LBO activities. However, a higher demandto complete LBOs also results in new bank loans and high-yield bonds that maybe sold to CLOs and CBOs. As a first step in understanding the link betweenthese two markets, we examine the correlation of institutional spreads on lever-aged loans with LBO volumes and LBO loan volumes. While an outward shiftin LBO loan demand is expected to increase loan spreads, an outward shift inthe supply of credit should lower spreads. Hence, evidence of a negative corre-lation between changes in institutional spreads and changes in LBO volumeand LBO loan volume would be consistent with a shift in credit supply fromthe institutional market. For comparison, we also consider spreads on pro ratatranches. Since CDOs do not participate in pro rata tranches, examining prorata spreads serves as a useful control to isolate the effect of CDOs on thepricing of bank credit.

We find that quarterly changes in spreads on institutional tranches ratedBB and B display correlation of −0.32 and −0.39 with changes in loan volumesand of −0.28 and −0.30 with changes in LBO volumes. However, we do not finda meaningful correlation between changes in LBO volumes or loan volumeswith changes in pro rata spreads. While this does not mean that LBO demanddid not change during this period, it does indicate an outward shift in creditsupply in the institutional market, where CDOs were active investors duringthe boom.15

If credit expansion from the CDO market allowed banks to make more LBOloans, LBO lending should be correlated with all types of CDOs, not just theCLOs that hold leveraged loans or the CBOs that hold high-yield bonds. Ac-cordingly, we consider the volume of all CDOs excluding CLOs and CBOs. Wehenceforth refer to this group as structured CDOs since structured product

15 Arguably, LBO demand increased substantially before the third quarter of 2007. We also findevidence of a negative correlation between LBO loan volumes and institutional spreads in theperiod before the third quarter of 2007, suggesting that shifts in the supply of credit were notoffset by shifts in LBO demand during this period.

Did Structured Credit Fuel the LBO Boom? 1303

CDOs comprise the vast majority of these instruments. Structured CDO vol-ume is also highly correlated with LBO volume with a correlation of the naturallog amounts of 0.64. Thus, the link between LBO and CDO markets is not amechanical result of LBO loans and high-yield bonds being placed in CLO andCBO vehicles.

We also consider the more traditional securitization market of ABS. Thecollateral assets in ABS include home equity, auto, credit card, and studentloans. Since LBOs do not create these types of consumer loans, ABS issuanceis not affected by the demand for LBOs. Yet as an ancestor of CDOs, the ABSmarket shares a similar investor base to that of the CDO market. We find thatABS issuance volumes are also highly correlated with LBO volume, with acorrelation of the log amounts of 0.52.

B. Multivariate Evidence on LBO and CDO Markets

We next examine the link between the CDO and LBO markets in a multi-variate framework where we control for factors affecting the demand for LBOloans, macroeconomic conditions, and other potential sources of credit supply.The control variables include GDP growth, the high-yield spread calculated asthe Bank of America–Merrill Lynch High-Yield Index over 6-month LIBOR,the difference between prime and fed funds rates, and the equity market riskpremium calculated as the equity market return over the 90-day Treasury billreturn.

Table II shows three specifications linking overall LBO volume to the size ofthe CDO market, structured CDO market, and ABS market. Model (1) confirmsthe positive correlation between LBO volumes and CDO issuance volumes. Thecoefficient of 1.73 implies a partial correlation of 0.62 between the log of LBOand CDO volumes. Regression (2) shows that LBO and structured CDO volumesare also positively related, indicating that the relation between LBO and CDOvolumes is not driven by LBO loans being placed into CDO vehicles. The partialcorrelation between the log of LBO volumes and the log of Structured CDO is0.51. Regression (3) shows that LBO volumes are also positively linked to ABSissuance volumes. As in Axelson et al. (2010), this specification shows thatLBO volumes are negatively related to the high-yield spread, suggesting thatfinancing costs in high-yield bond markets affect LBO activity.

We estimate corresponding regressions for aggregate quarterly LBO loanvolumes and obtain similar results. Models (4) to (6) show that LBO loanvolumes are also positively related to issuance volumes in CDO, structuredCDO, and ABS markets. Among the control variables, GDP Growth tends tohave a positive effect on LBO volumes and loan volumes. The high-yield spreadhas a negative effect on LBO loan volumes, consistent with Axelson et al. (2010).

The last four columns link spreads on institutional tranches of leveragedloans to issuance volumes in the CDO market. A negative correlation betweeninstitutional spreads and CDO issuance volumes would be consistent with anexpansion in credit supply from the CDO market. Model (7) displays such anegative correlation. Point estimates indicate that a one-standard-deviation

1304 The Journal of Finance R©T

able

IIR

egre

ssio

ns

ofL

BO

Vol

um

eon

Siz

eof

CD

Oan

dS

ecu

riti

zati

onM

ark

ets

Th

ista

ble

pres

ents

the

regr

essi

ons

ofL

BO

volu

mes

,lo

anvo

lum

es,

and

spre

ads

onth

esi

zeof

CD

Oan

dse

curi

tiza

tion

mar

kets

.T

he

LB

Ovo

lum

ein

mod

els

(1)

to(3

)is

the

aggr

egat

equ

arte

rly

volu

me

ofal

lL

BO

deal

sfr

omS

DC

sati

sfyi

ng

the

foll

owin

gcr

iter

ia:

the

deal

isan

nou

nce

dbe

twee

n19

96an

dth

ese

con

dqu

arte

rof

2008

and

com

plet

edby

July

2008

;th

eta

rget

isa

U.S

.co

mpa

ny

and

ispu

blic

lytr

aded

;tr

ansa

ctio

nva

lue

isgr

eate

rth

an$1

0m

illi

on;a

tle

ast

50%

ofco

mm

onsh

ares

are

acqu

ired

inth

ede

al;a

nd

the

acqu

irer

sow

n10

0%of

the

shar

esaf

ter.

LB

OL

oan

Vol

um

eis

the

aggr

egat

eof

lon

g-te

rmba

nk

loan

borr

owin

gam

oun

tfo

rth

e24

1sa

mpl

ede

als

wh

ere

info

rmat

ion

onth

eam

oun

tsof

ban

klo

ans

can

beid

enti

fied

.S

prea

dsof

Lev

erag

edL

oan

sis

the

quar

terl

ysp

read

ofth

ein

stit

uti

onal

tran

ches

inle

vera

ged

loan

sra

ted

BB

orB

,pr

ovid

edby

LP

Cba

sed

onn

ewis

sues

ofle

vera

ged

loan

s.L

og(C

DO

)is

log

ofth

equ

arte

rly

issu

ance

volu

me

ofal

lty

pes

ofC

DO

s;L

og(S

tru

ctu

red

CD

O)

excl

ude

sC

DO

sba

cked

onco

rpor

ate

loan

s(C

LO

s)or

bon

ds(C

BO

s);

Log

(AB

S)

incl

ude

sis

suan

cevo

lum

esof

AB

S.

Pri

me

Ove

rF

edF

un

dR

ate

isca

lcu

late

das

the

prim

era

tem

inu

sth

efe

dera

lfu

nds

rate

.Hig

h-Y

ield

Spr

ead

isth

esp

read

ofth

eB

ank

ofA

mer

ica–

Mer

rill

Lyn

chH

igh

-Yie

ldIn

dex

over

the

6-m

onth

LIB

OR

rate

.G

DP

Gro

wth

isth

ese

ason

ally

adju

sted

perc

enta

gech

ange

inG

DP

over

aye

area

rlie

r.R

isk

Pre

miu

mis

calc

ula

ted

asth

ean

nu

aliz

edva

lue-

wei

ghte

dm

arke

tre

turn

min

us

retu

rnon

90-d

aybi

lls.

Th

efi

rst

row

for

each

inde

pen

den

tva

riab

lere

port

sth

ees

tim

ated

coef

fici

ent.

Th

ese

con

dro

wre

port

sab

solu

teva

lues

ofth

et-

stat

isti

cu

sin

gN

ewey

–Wes

tst

anda

rder

rors

adju

stin

gfo

rse

rial

corr

elat

ion

.∗∗∗

,∗∗ ,

and

∗in

dica

tes

stat

isti

cal

sign

ifica

nce

atth

e1%

,5%

,an

d10

%le

vel,

resp

ecti

vely

.

Log

(In

stit

uti

onal

Spr

eads

ofL

ever

aged

Loa

ns)

Log

(LB

OV

olu

me)

Log

(LB

OL

oan

Vol

um

e)B

BR

ated

BR

ated

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Log

(CD

O)

1.73

1.58

−0.2

0−0

.14

5.16

∗∗∗

4.79

∗∗∗

4.82

∗∗∗

3.35

∗∗∗

Log

(Str

uct

ure

dC

DO

)1.

501.

41−0

.20

−0.1

35.

64∗∗

∗5.

02∗∗

∗3.

26∗∗

∗2.

74∗∗

∗

Log

(AB

S)

2.59

2.40

4.67

∗∗∗

4.24

∗∗∗

Pri

me

Ove

rF

edF

un

ds

Rat

e4.

593.

6613

.86.

255.

2914

.72.

402.

471.

681.

740.

870.

672.

28∗∗

0.83

0.77

2.34

∗∗2.

85∗∗

∗3.

22∗∗

∗2.

22∗∗

2.47

∗∗

Hig

h-Y

ield

Spr

ead

−0.2

1−0

.23

−0.4

9−0

.25

−0.2

6−0

.51

0.01

0.01

0.02

0.02

1.60

1.60

3.90

∗∗∗

1.79

∗1.

76∗

3.71

∗∗∗

0.67

0.34

1.42

1.17

GD

PG

row

th0.

320.

10−0

.08

0.57

0.38

0.21

−0.0

4−0

.02

−0.0

4−0

.02

1.73

∗0.

500.

391.

91∗

1.32

0.62

1.48

0.75

1.26

0.80

Ris

kP

rem

ium

−0.7

2−1

.04

−0.3

4−1

.52

−1.8

3−1

.17

0.01

0.00

−0.0

10.

001.

041.

470.

511.

271.

501.

090.

110.

670.

150.

32C

onst

ant

−24.

4−1

7.1

−60.

0−2

9.7

−23.

2−6

2.9

0.59

0.14

2.21

1.86

1.29

0.96

2.95

∗∗∗

1.19

1.05

2.89

∗∗∗

0.23

0.06

0.91

0.85

Obs

erva

tion

s49

4949

4949

4941

4141

41A

dj.R

20.

520.

420.

430.

480.

420.

430.

590.

600.

610.

61

Did Structured Credit Fuel the LBO Boom? 1305

increase in the log of CDO issuance volume is associated with a 33 basis pointdecrease in the institutional spread of the BB-rated tranches. Model (8) showsthat this result holds if we use the volume of structured CDO underwriting.We also find a similar relation using ABS volume. Models (9) and (10) confirmthat the relation between CDO volume and leveraged loan spreads holds usingspreads of B-rated institutional loans.16 Interestingly, in all models, institu-tional spreads on leveraged loans are not significantly related to the high-yieldspread. This suggests that financing costs in the leveraged loan and high-yieldbond markets are determined by different factors and that the effect of CDO is-suance volume on institutional spreads on leveraged loans cannot be explainedby contemporaneous changes in high-yield spreads.

Overall, the aggregate-level evidence indicates a clear link between the CDOand LBO markets that cannot be explained by LBO loan demand fueling CDOissuance. However, it is possible that the link between the two markets is theoutcome of an omitted factor. We next turn to bank-level and loan-level analysesto address the possibility that omitted factors may be responsible for the linkbetween the LBO and CDO markets.

C. Results from Bank-Level Analysis

We test whether a bank’s activities in the CDO markets affected its lendingbehavior. If an increased supply of credit through the CDO market made abank a more aggressive LBO lender, we expect that a bank with substantialCDO underwriting activities would originate more LBO loans. The presence ofan established distribution channel to structured credit investors should allowa bank with CDO underwriting capabilities to distribute its LBO loans to CLOvehicles. To test the effect of a bank’s CDO underwriting on its LBO lending, weconstruct a panel data set to estimate the following bank fixed effects model:

LBOLendingit =K∑

i=1

αi + β × CDOit + γ ′ × Xit + δ′ × Zt + εit, (1)

where LBOLendingit is the total volume of LBO loans that bank i arranges inyear t, αi is the bank fixed effect, Xit and Zt are proxies for bank characteristicsand macroeconomic conditions, respectively. The term CDOit is the volume ofCDOs underwritten by bank i in year t. We also use our two non-LBO-relatedmeasures of the structured credit market to proxy for CDOit. If the supply ofcapital through structured credit led a bank to be a more aggressive lender, weexpect β > 0.

16 As an additional test of the credit supply view, we examine the difference between institutionaland pro rata spreads. The supply of credit from CLOs is expected to lower institutional spreads butshould have little impact on pro rata spreads. Hence, the difference in institutional and pro rataspreads should also be negatively correlated with CDO volumes. Results presented in the InternetAppendix display such a pattern. For both BB- and B-rated loans, we find that the differencebetween institutional and pro rata spreads is negatively related to CDO and structured CDOunderwriting volumes.

1306 The Journal of Finance R©

Using a fixed effects approach allows us to control for bank-level fixed omit-ted variables. This helps address the possibility that an unobserved factorsimultaneously drove both a bank’s decision to originate LBO loans as well asthe growth in its CDO underwriting. Bank-level time-invariant omitted fac-tors cannot explain a correlation between a bank’s LBO lending and it’s CDOunderwriting in this setting.

To construct the bank-level panel data set on banks’ annual LBO lendingvolumes and their CDO underwriting activity, we start with all the lead banksin the LBO loan sample. For each bank, we calculate the total volume of LBOloans it originates and the total volume of CDOs it underwrites in each year.For sole-led loans, we assign full lending credit to the lead bank.17 For co-led loans, we divide the loan amount equally among all the lead banks. Asin Sufi (2007), the banks are consolidated with the parent holding companyin the loan allocation algorithm. When banks merge, loan allocations of theacquired bank are aggregated with those of the acquirer as of the effective dateof the merger. Allocation of CDO underwriting volumes across lead banks isperformed similarly. Only 8.3% of the CDO issues in our sample had multipleunderwriters.

In the Internet Appendix, we show the structured credit underwriting activ-ities for the top LBO lenders. In the post-2004 period, the top 10 LBO lendersoriginated $225 billion in LBO loans, with a 94% market share in LBO lending.During this time, these top LBO lenders were all major CDO underwriters, andeach ranked among the top 13 CDO underwriters with a collective 55% marketshare in CDO underwriting. However, this tight correspondence between LBOlending and CDO underwriting activity did not exist pre-2004. Before 2004,the top 10 LBO lenders had a 79% market share in LBO loan origination butonly a 25.5% market share in CDO underwriting. Four of the top LBO lendershad no CDO underwriting activity. Similar patterns hold using the ranking ofthe top LBO lenders in structured CDO and ABS markets. The contrast in theoverlap between LBO lending and structured credit underwriting before andafter 2004 suggests these two activities were much more closely linked duringthe LBO boom than was historically the case.

For each bank-year, we calculate the bank’s underwriting activity in struc-tured credit markets using variables that correspond to our aggregate mea-sures of market size: Bank CDO is the aggregate volume of CDOs under-written by a bank in a given year, Bank Structured CDO measures a bank’snon-CLO and non-CBO underwriting, and Bank ABS represents the volume ofABS underwritten by the bank in a given year. The models include Bank Size(measured as log of total bank assets), Capital Ratio (the ratio of total equityto total assets), Deposits (total customer deposits over total assets), and FedFunds Rate as controls.

17 As described by Sufi (2007), lead banks are primary negotiators of the loans. They are re-sponsible for collecting information and negotiating loan terms, they typically hold a larger shareof the loan, and they charge up-front fees. Other syndicate participants maintain an arm’s-lengthrelationship with the borrower by interacting with lead banks. Our allocation of loan amounts isalso consistent with how league tables for banking transactions are computed.

Did Structured Credit Fuel the LBO Boom? 1307

One concern is that a number of banks merged during our sample periodand in some cases might have gained CDO underwriting capabilities throughacquisitions. To account for bank mergers in the panel data regressions, wemerge the lending and underwriting activity as well as balance sheet data forthe acquired bank with that of the acquirer throughout the sample period. Withthis process, we treat an acquired and acquiring bank as a single bank in theregressions. Our LBO loan panel data contain 36 banks and 368 bank-yearobservations.

Results from the bank fixed effects models shown in Table III indicate that abank’s activities in CDO underwriting and its LBO lending are related. Model(1) shows that the volume of LBO lending in a given year is positively re-lated to the bank’s CDO underwriting volume in that year at the 10% level ofsignificance. Model (2) shows that this relation also holds if we only considerunderwriting volumes of structured CDOs. In model (3), we use the volume ofa bank’s underwriting in the broader ABS market and find that it is also posi-tively related to its LBO lending in a given year. The coefficient on underwritingactivity is significant at the 5% level or better in both specifications.

We also consider bank lending for investment-grade loans and collect thesedata from Dealscan. If supply from the structured credit market drove LBOlending, we expect that investment-grade lending should be relatively unaf-fected by a bank’s underwriting in structured credit markets because CLOsprimarily purchase leveraged loans. This is exactly what we observe. Columns(4) to (6) present bank fixed effects models and show that a bank’s originationof investment-grade loans is not systematically related to its CDO, structuredCDO, or ABS underwriting.

We also estimate cross-sectional regressions of LBO lending during the 2004to 2008 period using CDO underwriting volumes in the preboom period of1996 to 2003. Model (7) shows that a bank’s LBO lending during the boom ispositively related to its CDO underwriting in the preboom years. Models (8)and (9) display a similar pattern using the volume of a bank’s structured CDOunderwriting and ABS underwriting volumes.

Finally, we estimate similar cross-sectional regressions for investment-gradelending as a control group that should be relatively unaffected by structuredcredit markets. Columns (10) and (11) show that investment-grade lending inthe LBO boom years was unrelated to a bank’s activities in CDO and structuredCDO markets prior to the LBO boom. We find some evidence in model (12) thatinvestment-grade lending is linked to pre-boom ABS underwriting at the 10%level of significance, but the coefficient estimate is about one-third the size forLBO lending.

These results point to a direct connection between the LBO lending policyof a bank and its underwriting activities in the CDO and structured creditmarkets. Since this result holds in a bank fixed effects framework, it cannotbe explained by the possibility of bank-level omitted variables driving both abank’s lending policies and its CDO underwriting. A potential explanation forthis result is that the supply of capital from structured credit investors allowedbanks to finance their leveraged lending. The result cannot be explained by a

1308 The Journal of Finance R©

Tab

leII

IB

ank

-Lev

elR

egre

ssio

ns

ofL

BO

Len

din

gon

CD

OU

nd

erw

riti

ng

Act

ivit

yT

his

tabl

epr

esen

tsre

gres

sion

sof

ban

ks’l

endi

ng

tofu

nd

LB

Os

and

thei

rin

vest

men

t-gr

ade

len

din

gon

thei

rC

DO

un

derw

riti

ng

volu

mes

for

ban

ksth

atse

rved

asle

adar

ran

gers

inL

BO

loan

s.T

he

ban

kpa

nel

cove

rs19

96to

2007

.We

mer

geta

rget

ban

ksin

toac

quir

ing

ban

ksth

rou

ghou

tth

esa

mpl

epe

riod

.Th

ispa

nel

ofba

nks

isu

sed

toru

nth

efo

llow

ing

fixe

def

fect

mod

elfo

rba

nks

’LB

Ole

ndi

ng

and

inve

stm

ent-

grad

ele

ndi

ng,

resp

ecti

vely

:

Ban

kL

end

ing i

t=

K ∑ i=1

αi+

β×

CD

Oit

+γ

′ ×X

it+

δ′ ×

Z t+

ε it.

Th

ede

pen

den

tva

riab

leis

the

log

ofba

nks

’LB

Ole

ndi

ng

inco

lum

ns

(1)t

o(3

).B

ank

i’sL

BO

loan

amou

nt

inye

arti

sca

lcu

late

das

the

sum

ofth

ecr

edit

the

ban

kre

ceiv

edas

ale

adar

ran

ger

inan

yof

the

sam

ple

LB

Olo

ans

arra

nge

din

year

t.L

BO

loan

sar

ecr

edit

sole

lyto

lead

arra

nge

rsan

deq

ual

lydi

s-tr

ibu

ted

toal

llea

dsw

hen

mu

ltip

lele

ads

pres

ent.

Inco

lum

ns

(4)t

o(6

),th

ede

pen

den

tva

riab

leis

the

log

ofin

vest

men

t-gr

ade

loan

sth

eba

nk

arra

nge

din

year

t,w

hic

his

obta

ined

from

Dea

lSca

nle

agu

eta

ble

repo

rts

and

adju

sted

for

mer

gers

.αi

isth

efi

xed

effe

ctfo

rba

nk

i.C

DO

itde

not

esu

nde

rwri

tin

gac

tivi

tyin

the

CD

Oor

broa

der

secu

riti

zed

mar

kets

for

ban

kii

nye

art.

Spe

cifi

call

y,L

og(B

ank

CD

O)i

sth

elo

gari

thm

ofth

eto

tala

mou

nt

ofC

DO

sba

nk

iun

derw

rite

sin

year

t;L

og(B

ank

Str

uct

ure

dC

DO

)exc

lude

sC

DO

sba

cked

byco

rpor

ate

loan

sor

bon

ds;L

og(B

ank

AB

S)i

sth

elo

gari

thm

ofth

eto

talv

ol-

um

eof

AB

Sth

eba

nk

un

derw

rite

sin

year

t.O

ne

isad

ded

toal

lth

ese

mea

sure

sbe

fore

taki

ng

the

log

toav

oid

zero

valu

es.X

itre

fers

toti

me-

vary

ing

ban

kch

arac

teri

stic

s.F

inan

cial

data

for

ban

ksar

eta

ken

from

Com

pust

at’s

Glo

balF

inan

cial

Ser

vice

.Bal

ance

shee

tsof

targ

etba

nks

are

mer

ged

into

acqu

ir-

ing

ban

ksth

rou

ghou

tth

esa

mpl

e.B

ank

Siz

eis

the

loga

rith

mof

the

tota

lass

ets

ofth

eba

nk.

Cap

ital

Rat

iois

tota

lequ

ity

divi

ded

byto

tala

sset

s.D

epos

itis

tota

lcu

stom

erde

posi

tsdi

vide

dby

tota

lass

ets.

Zt

refe

rsto

tim

e-va

ryin

gm

acro

vari

able

s;F

edF

un

ds

Rat

eis

the

ann

ual

aver

age

fede

ralf

un

dsra

te.

Col

um

ns

(7)

to(1

2)re

port

cros

s-se

ctio

nal

regr

essi

ons

ofba

nks

’tot

alL

BO

len

din

gan

din

vest

men

t-gr

ade

len

din

gdu

rin

g20

04to

Jun

e20

08on

thei

rC

DO

un

derw

riti

ng

volu

mes

duri

ng

1996

to20

03u

sin

gth

efo

llow

ing

mod

el:

Ban

kL

endi

ngbo

om,i

=α

+β

×C

DO

pre−

boom

,i+

γ′ ×

Xbo

om,i

+ε i

.

Th

ede

pen

den

tva

riab

leis

the

log

ofth

eto

tal

volu

me

ofL

BO

loan

sa

ban

kar

ran

ged

duri

ng

2004

toJu

ne

2008

inco

lum

ns

(7)

to(9

)an

dis

the

log

ofin

vest

men

t-gr

ade

len

din

gdu

rin

gth

esa

me

peri

odin

colu

mn

s(1

0)to

(12)

.L

og(B

ank

CD

O),

Log

(Ban

kS

tru

ctu

red

CD

O),

and

Log

(Ban

kA

BS

)ar

elo

gof

the

ban

k’s

tota

lu

nde

rwri

tin

gvo

lum

eof

all

CD

Os,

stru

ctu

red

CD

Os

(i.e

.,C

DO

sex

clu

din

gC

LO

san

dC

BO

s),

and

AB

Sdu

rin

g19

96to

2003

.O

bser

vati

ons

wit

hze

role

ndi

ng

duri

ng

the

boom

and

zero

preb

oom

CD

Ou

nde

rwri

tin

gar

eex

clu

ded.

Th

efi

nan

cial

rati

osof

the

ban

ksar

eca

lcu

late

das

the

aver

age

ofth

ean

nu

alra

tios

over

the

boom

peri

odfo

rea

chba

nk.

Abs

olu

teva

lues

oft-

stat

isti

csar

ere

port

edbe

low

coef

fici

ent

esti

mat

es.∗

∗∗,∗

∗ ,an

d∗

indi

cate

sst

atis

tica

lsig

nifi

can

ceat

the

1%,5

%,a

nd

10%

leve

l,re

spec

tive

ly.

(con

tin

ued

)

Did Structured Credit Fuel the LBO Boom? 1309

Tab

leII

I—C

onti

nu

ed

Ban

kF

ixed

-Eff

ect

Reg

ress

ion

sB

ank

Cro

ss-s

ecti

onal

Reg

ress

ion

s

Log

(LB

OL

oan

s)L

og(I

nv.

-Gra

deL

oan

s)L

og(L

BO

Loa

ns)

Log

(In

v.-G

rade

Loa

ns)

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

(12)

Log

(Ban

kC

DO

)0.

140.

100.

390.

121.

88∗

1.47

2.19

∗∗1.

34L

og(B

ank

Str

uct

ure

d0.

220.

080.

430.

13C

DO

)3.

08∗∗

∗1.

292.

35∗∗

1.28

Log

(Ban

kA

BS

)0.

140.

030.

450.

162.

00∗∗

0.46

3.22

∗∗∗

1.90

∗

Ban

kS

ize

1.11

1.06

1.20

1.04

1.07

1.13

1.73

1.51

0.84

1.53

1.51

1.31

4.89

∗∗∗

4.79

∗∗∗

5.62

∗∗∗

5.23

∗∗∗

5.49

∗∗∗

6.05

∗∗∗

1.99

∗1.

690.

952.

58∗∗

2.46

∗∗2.

22∗∗

Cap

ital

Rat

io−1

.26

−1.2

3−1

.32

−0.3

9−0

.39

−0.4

267

.564

.050

.451

.049

.645

.20.

830.

830.

880.

290.

300.

323.

44∗∗

∗3.

39∗∗

∗2.

98∗∗

∗4.

27∗∗

∗4.

16∗∗

∗3.

86∗∗

∗

Dep

osit

2.54

6.09

2.82

23.1

23.2

21.3

−8.0

4−8

.41

−4.5

512

.812

.313

.10.

330.

780.

363.

40∗∗

∗3.

37∗∗

∗3.

13∗∗

∗1.

031.

110.

632.

31∗∗

2.27

∗∗2.

58∗∗

Dep

osit

Squ

ared

−5.0

0−7

.53

−4.9

3−2

1.9

−21.

9−2

0.5

2.54

4.27

0.33

−16.

7−1

5.9

−16.

40.

681.

030.

683.

42∗∗

∗3.

39∗∗

∗3.

19∗∗

∗0.

240.

420.

034

2.22

∗∗2.

16∗∗

2.40

∗∗

Fed

Fu

nd

sR

ate

0.25

0.24

0.26

−0.0

6−0

.07

−0.0

63.

61∗∗

∗3.

51∗∗

∗3.

72∗∗

∗1.

031.

151.

07C

onst

ant

−13.

1−1

3.6

−14.

4−1

1.3

−11.

6−1

1.8

−20.

4−1

7.5

−8.9

0−1

5.8

−15.

4−1

3.0

4.13

∗∗∗

4.31

∗∗∗

4.51

∗∗∗

4.06

∗∗∗

4.18

∗∗∗

4.19

∗∗∗

1.92

∗1.

600.

822.

13∗∗

2.01

∗1.

75∗

Ban

kfi

xed-

effe

cts

Yes

Yes

Yes

Yes

Yes

Yes

Obs

erva

tion

s36

836

836

836

836

836

824

2424

3131

31N

um

ber

ofba

nks

3636

3636

3636

R2

0.14

0.15

0.14

0.15

0.15

0.15

0.76

0.77

0.81

0.78

0.78

0.79

1310 The Journal of Finance R©

reverse causality effect where the demand for LBOs led to greater volumes ofCDO underwriting since it also holds for structured CDOs and ABS, which donot invest in leveraged loans or high-yield bonds. In addition, the finding thata bank’s LBO lending in the boom years is related to its preboom underwritingin structured credit is reassuring in light of the high correlations of manyfinancing and underwriting activities during the boom years. Finally, consistentwith CDOs increasing the supply of capital for higher risk assets, we find thatstructured credit markets have a unique effect on lending in leveraged loanmarkets that is not observed in investment-grade loan markets.

D. Loan-Level Results on Allocation to Institutional Investors

The bank fixed effects results do not rule out the possibility of a time-varyingomitted factor. For example, it is possible that banks pursued riskier strategiesduring the LBO boom, lending more to LBOs and underwriting more CDOs,but that these activities were not directly linked to each other. While we cannotdirectly test for such time-varying omitted factors, we examine how LBO loanswere financed in the syndicated loan market. If the ability to obtain capitalfrom structured credit investors led a bank to extend LBO loans, these loansshould be heavily financed by CLO vehicles when the bank had access to theseinvestors through its underwriting capabilities.

To examine if LBO loans were financed from CLOs, ideally we would trackthe allocation of each loan to CLO vehicles but data do not permit this level ofprecision. However, we are able to identify a closely related measure, namely,the percentage of a loan that is placed with institutional investors, by calcu-lating the size of the institutional tranches of the loan. We expect this variableto reflect the allocation to CLO vehicles because they had become the mostimportant institutional investors during the LBO boom, accounting for 60% ofprimary activity in leveraged loans by 2006 (S&P (2006)).

We calculate the institutional loan allocation of each loan as the sum of theterm loan B, C, and D tranches that were sold to institutional investors andscale it by the amount of the loan. LBO loans in the post-2004 period werefinanced heavily by institutional investors (average of 60% vs. 44% in pre-2004). The term loan B, the most common institutional term loan, accountedfor 47% of LBO loans post-2004, compared to only 24% before.18 In the InternetAppendix, we provide summary statistics on LBO loans and their institutionalallocations.

Results from a Tobit model estimating the fraction of an LBO loan placedin institutional tranches are presented in Table IV. We use the total volumeof CDO underwriting (Total Lender CDO) of the lead banks in the year of theloan origination as an independent variable. To control for loan attributes,

18 The CLO market suffered after the third quarter of 2007 with issuance volume dropping to$34 billion from $48 billion in the prior quarter. As the CLO market declined, the bulk of newleveraged loans were sold to pro rata investors. In the second quarter of 2007, the institutionalallocation averaged 77%, which dropped to 45% in 2008 and to 29% in the first quarter of 2009.

Did Structured Credit Fuel the LBO Boom? 1311

Table IVTobit Regressions of Fraction of Institutional Tranches on Lenders’

CDO Underwriting ActivityThe dependent variable is the percentage of institutional tranches, calculated as all institutionalterm loans over total long-term borrowing amount of the LBO loan. Log(Total Lender CDO) is thelogarithm of the total volume of CDOs underwritten by all lead banks of the loan in the year theLBO deal is announced. Log(Total Lender Structured CDO) excludes alls CLOs and CBOs. LoanAmount is total long-term borrowing amount of the loan. LBO Deal Value is the transaction valueof the LBO deal net of fees and expenses. Loan Maturity is the value-weighted average maturityof all institutional tranches. Target EBITDA is the firm’s operating income over total assets inthe year before the deal. Std. Dev. of Target EBITDA is the standard deviation of Target EBITDAin the 5 years before the deal, and Industry Std. Dev. of EBITDA is the median of the standarddeviation of EBITDA for firms in the same Fama–French 48 industry over 5 years before the deal.Number of Banks is the number of lead banks and Bank Size is the logarithm of the average totalassets of the lead banks. The R2 from a corresponding OLS regression is reported for each model.Absolute values of t-statistics are reported in the second row for each independent variable. ∗∗∗, ∗∗,and ∗ indicates statistical significance at the 1%, 5%, and 10% level, respectively.

Percentage of Institutional Tranches

(1) (2) (3) (4) (5) (6)

Log(Total Lender CDO) 1.79 1.72 1.762.74∗∗∗ 2.73∗∗∗ 2.12∗∗

Log(Total Lender Structured CDO) 1.59 1.62 1.882.33∗∗ 2.46∗∗ 2.23∗∗

Loan Amount/LBO Deal Value −5.45 −2.28 −5.85 −5.32 −2.38 −5.923.02∗∗∗ 1.30 3.32∗∗∗ 2.92∗∗∗ 1.34 3.36∗∗∗

Loan Maturity −0.19 −0.04 −0.24 −0.18 −0.03 −0.241.76∗ 0.42 2.27∗∗ 1.70∗ 0.34 2.24∗∗

Loan Amount/EBITDA 0.55 0.24 0.57 0.52 0.21 0.582.41∗∗ 1.12 2.56∗∗ 2.28∗∗ 1.00 2.57∗∗

Log(LBO Deal Value) 3.94 2.61 3.02 4.07 2.57 3.002.59∗∗ 1.90∗ 1.86∗ 2.64∗∗∗ 1.84∗ 1.86∗

Target EBITDA −0.35 −0.25 −0.17 −0.38 −0.26 −0.191.39 1.08 0.71 1.48 1.12 0.78

Std. Dev. of Target EBITDA 0.66 0.87 0.77 0.66 0.89 0.801.10 1.62 1.31 1.09 1.65 1.37

Industry Std. Dev. of EBITDA 0.87 0.84 1.02 0.83 0.80 1.001.91∗ 2.06∗∗ 2.20∗∗ 1.81∗ 1.97∗ 2.17∗∗

Number of Banks 0.25 −3.05 12.5 0.62 −2.75 12.40.08 1.08 1.90∗ 0.20 0.98 1.88∗

Bank Size −0.14 −1.17 1.59 0.19 −1.03 1.680.08 0.71 0.85 0.11 0.62 0.91

Year dummies No Yes No No Yes NoBank dummies No No Yes No No YesConstant 40.58 26.94 24.5 37.57 30.50 23.6

1.90∗ 1.10 0.97 1.75∗ 1.21 0.94Observations 170 170 170 170 170 170OLS R2 0.32 0.47 0.31 0.32 0.47 0.31

1312 The Journal of Finance R©

we include the amount of the bank loan (relative to deal size and the tar-get’s operating cash flow) and its maturity, measured as the weighted averagematurity of all institutional tranches. The models control for several deal- andbank-specific variables. Deal-specific control variables include the size of theLBO deal measured by transaction value, the target’s operating cash flow, thevolatility of the target’s cash flow over the past 5 years, and the industry’scash flow volatility. Bank-specific controls include the number of lead arrang-ing banks and the size of the banks as measured by their total assets. Wealso estimate specifications with year dummies to alleviate concerns that theresults may be affected by the contemporaneous growth in other institutionalinvestors such as hedge funds during the LBO boom years. We also includebank dummies to control for bank-specific effects.

The results show a strong relation between the lead bank’s CDO underwrit-ing and the fraction of the loan funded through institutional tranches. Models(1) and (2) display a positive correlation between the institutional allocationand the total CDO underwriting volume of the lead banks. The point estimatesimply that a one-standard-deviation increase in the log of the bank’s CDO un-derwriting volume is associated with a 7% higher allocation to institutionaltranches. Model (3) shows that the relation between lead bank CDO under-writing and the fraction of institutional tranches holds with bank fixed effects.In models (4) to (6), we use the total structured CDO underwriting volumeof the lead banks (Total Lender Structured CDO) as an independent variableto alleviate concerns about reverse causality. We obtain similar results. Thus,the lead bank’s activities in structured CDO underwriting are also positivelyrelated to the fraction of the LBO loan allocated to institutional tranches andthe effect is of similar economic magnitude as Total Lender CDO.

Among the control variables, larger LBOs involve a higher proportion of loansfunded through institutional tranches, suggesting that structured credit mar-kets played a more important role for larger LBO transactions. Institutionalallocations are also larger when the LBO target is in an industry with morevariable cash flows, possibly reflecting greater risk appetite of institutional in-vestors such as CLOs than pro rata investors. Overall, the results suggest thata bank’s access to CDO capital through its underwriting activities is associatedwith a larger portion of its loan commitments being financed from CLOs.

E. CDO Access and Contractual Loan Terms

For further evidence linking a bank’s CDO underwriting activities to its LBOlending, we study the contractual terms of LBO loans. If CLOs increased thesupply of credit, we expect that banks with access to this supply through theirunderwriting activities should be able to offer lower spreads, all else equal.Financing LBO loans through CLOs might affect the covenant structure of LBOloans as well. Since banks are less likely to fund the loans from their balancesheet in such transactions, their incentive to monitor is potentially reduced.This may lead to less restrictive loan covenants if banks do not intend to monitorthe firm on an on-going basis. On the other hand, if loans financed through the

Did Structured Credit Fuel the LBO Boom? 1313

CLO channel are riskier, we may observe tighter covenants attached to theseloans to alleviate adverse selection concerns on the part of CLO investors.