developments in the atlantic lng - ihs markit · thank you! andrew ellis director of european gas...

TRANSCRIPT

Developments in the Atlantic LNG

Andrew EllisGlobal Insight

Copyright © 2006 Global Insight, Inc. 2

Changing Economics of LNG – Impact of Higher Costs

Changing Economics of LNG

Atlantic Basin Trade

Atlantic Arbitration Issue

Copyright © 2006 Global Insight, Inc. 3

Changes in the LNG equation

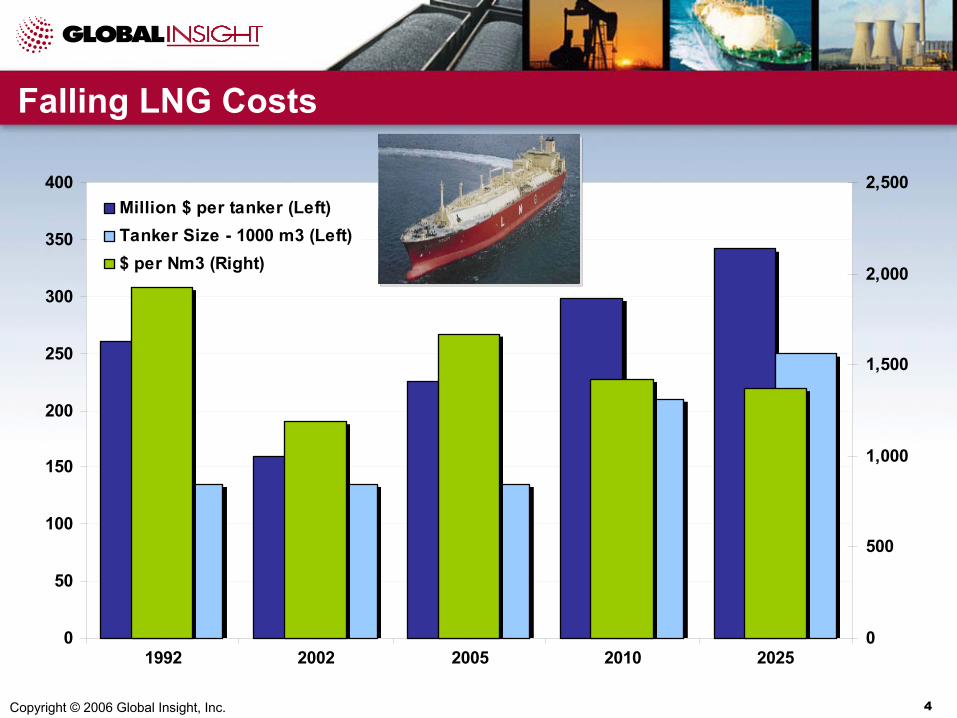

• Fundamentals shifted in favour of LNGInvestment costs fell over 1990sLNG competitive over shorter distances

• Gas prices have risen on higher oil pricesNetback margins have increased significantlyRecent cost escalation not reversed earlier fall

• Incremental supplies coming from further afield

90% of gas resources available to Europe are more than 3000 km away (60% are more than 4000 km away)

Copyright © 2006 Global Insight, Inc. 4

0

50

100

150

200

250

300

350

400

1992 2002 2005 2010 20250

500

1,000

1,500

2,000

2,500Million $ per tanker (Left)Tanker Size - 1000 m3 (Left) $ per Nm3 (Right)

Falling LNG Costs

Copyright © 2006 Global Insight, Inc. 5

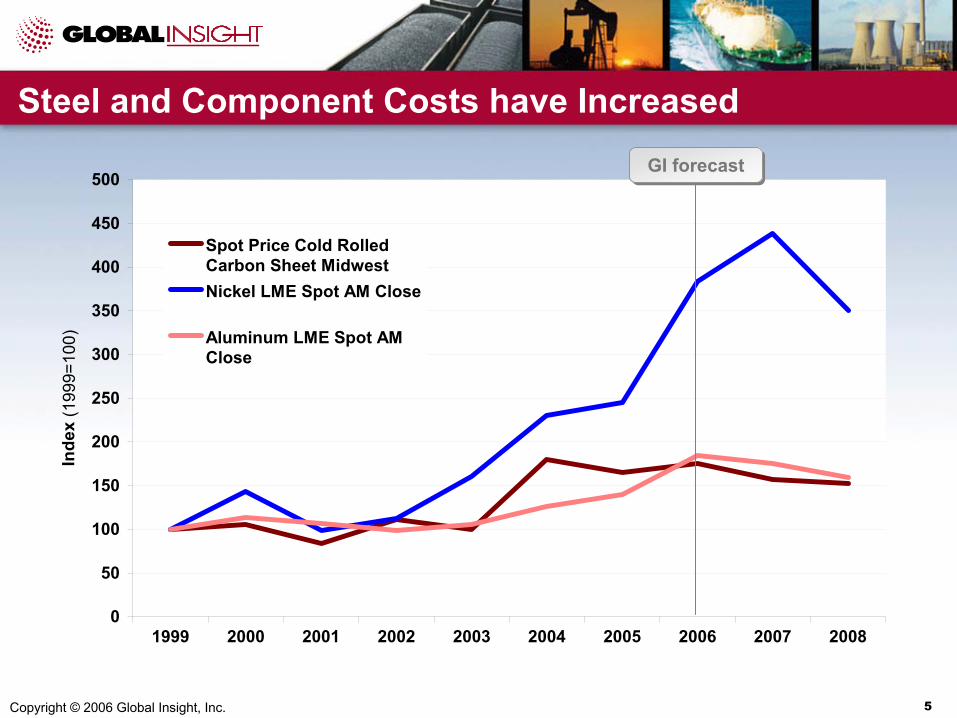

Steel and Component Costs have Increased

0

50

100

150

200

250

300

350

400

450

500

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Inde

x (1

999=

100)

Spot Price Cold RolledCarbon Sheet MidwestNickel LME Spot AM Close

Aluminum LME Spot AMClose

GI forecastGI forecast

Copyright © 2006 Global Insight, Inc. 6

Economics (LNG vs. Pipeline)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

100 500 900 1,300 1,700 2,100 2,500 2,900 3,300 3,700 4,100 4,500 4,900Distance (km)

$/m

mB

tu

Pipeline costs (2002) Pipeline costs (2006)LNG (mid-90s) LNG (2002)LNG (2006) LNG (2010)LNG (2025)

Copyright © 2006 Global Insight, Inc. 7

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

1990s 2004 2006

$/m

mB

tu

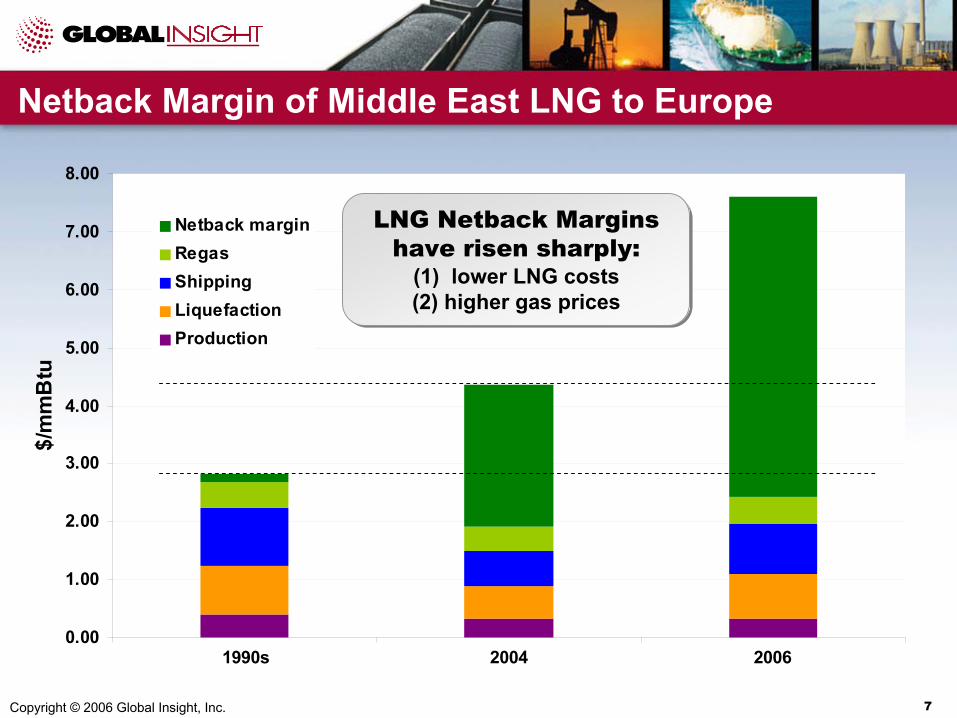

Netback marginRegasShippingLiquefactionProduction

Netback Margin of Middle East LNG to Europe

LNG Netback Margins have risen sharply:

(1) lower LNG costs(2) higher gas prices

LNG Netback Margins have risen sharply:

(1) lower LNG costs(2) higher gas prices

Copyright © 2006 Global Insight, Inc. 8

Atlantic Basin Trade – Burgeoning Growth

Changing Economics of LNG

Atlantic Basin Trade

Atlantic Arbitration Issue

Copyright © 2006 Global Insight, Inc. 9

Global Liquefaction & Regasification Capacity

0

50

100

150

200

250

300

350

400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

mill

ion

tonn

es L

NG

EuropeNorth AmericaSouth AmericaMiddle EastFar EastWest AfricaNorth Africa

0

100

200

300

400

500

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

mill

ion

tonn

es L

NG

South AmericaNorth AmericaEuropeChina & IndiaAsia Pacific

Key growth areas:• Africa (N & W)• Middle East• Australia

Key growth areas:• Africa (N & W)• Middle East• Australia

Key growth areas:• Europe• N. America

Key growth areas:• Europe• N. America

LiquefactionLiquefaction RegasifactionRegasifaction

Copyright © 2006 Global Insight, Inc. 10

Global Liquefaction & Regasification Capacity

0

50

100

150

200

250

300

350

400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

mill

ion

tonn

es L

NG

EuropeNorth AmericaSouth AmericaMiddle EastFar EastWest AfricaNorth Africa

0

100

200

300

400

500

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

mill

ion

tonn

es L

NG

South AmericaNorth AmericaEuropeChina & IndiaAsia Pacific

LiquefactionLiquefaction RegasifactionRegasifaction

Delays:• Australia – Gorgon – 10 mtpa• Bolivia – 7 mtpa• Nigeria – Brass River, OK, Ni T7 –

19.6 mtpa• Russia – Shtokman – 15 mtpa• Trinidad – Train X – 10.4 mtpa

Delays:• Australia – Gorgon – 10 mtpa• Bolivia – 7 mtpa• Nigeria – Brass River, OK, Ni T7 –

19.6 mtpa• Russia – Shtokman – 15 mtpa• Trinidad – Train X – 10.4 mtpa

Delays:• UK – Canvey Island• US – 2nd & 3rd stage expansion,

Cameron Parish, Mobile (Alabama)

Delays:• UK – Canvey Island• US – 2nd & 3rd stage expansion,

Cameron Parish, Mobile (Alabama)

Copyright © 2006 Global Insight, Inc. 11

Expanding Global LNG TradeFigures in BCM for 2010

Expanding markets• Europe & N. AmericaNew markets• China and India

Expanding markets• Europe & N. AmericaNew markets• China and India

Copyright © 2006 Global Insight, Inc. 12

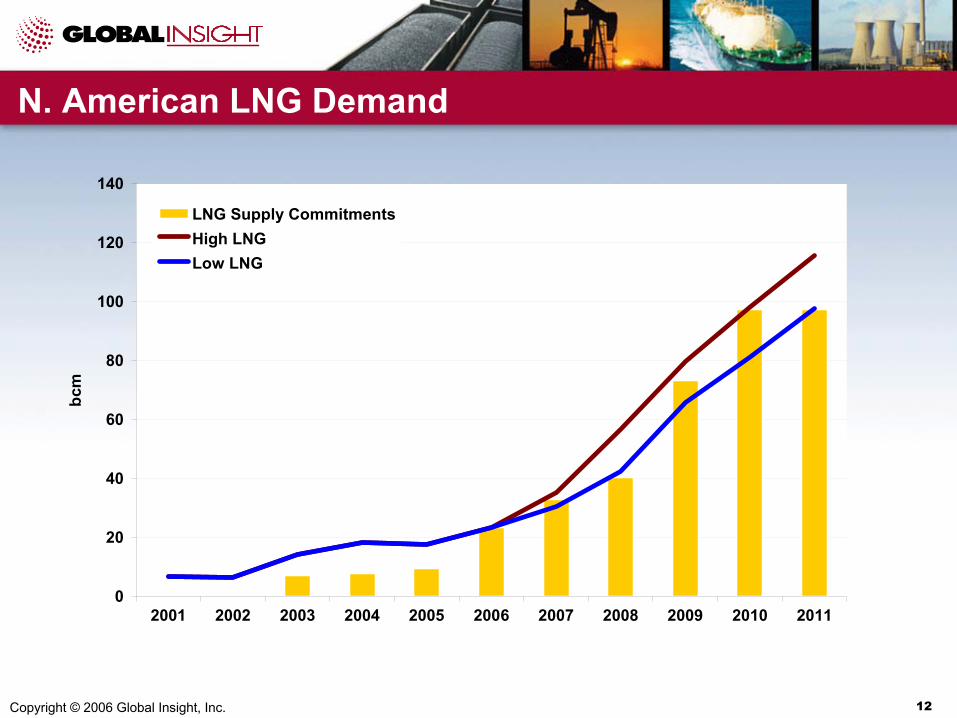

N. American LNG Demand

0

20

40

60

80

100

120

140

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

bcm

LNG Supply CommitmentsHigh LNGLow LNG

Copyright © 2006 Global Insight, Inc. 13

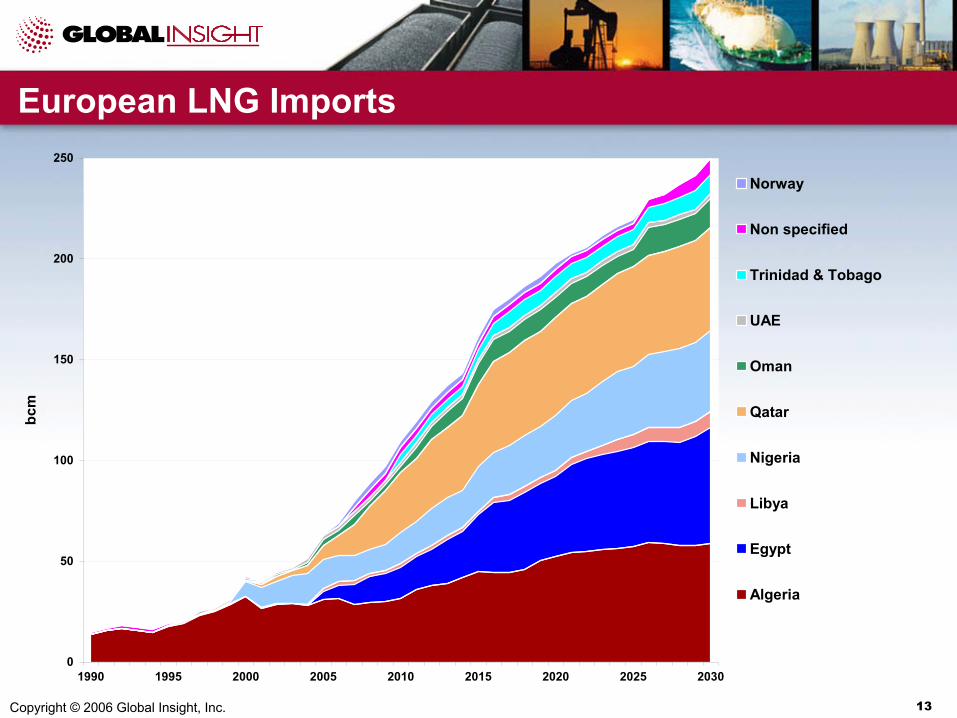

European LNG Imports

0

50

100

150

200

250

1990 1995 2000 2005 2010 2015 2020 2025 2030

bcm

Norway

Non specified

Trinidad & Tobago

UAE

Oman

Qatar

Nigeria

Libya

Egypt

Algeria

Copyright © 2006 Global Insight, Inc. 14

Atlantic Arbitration – Resource Competition, Pricing & Netbacks

Changing Economics of LNG

Atlantic Basin Trade

Atlantic Arbitration Issue

Copyright © 2006 Global Insight, Inc. 15

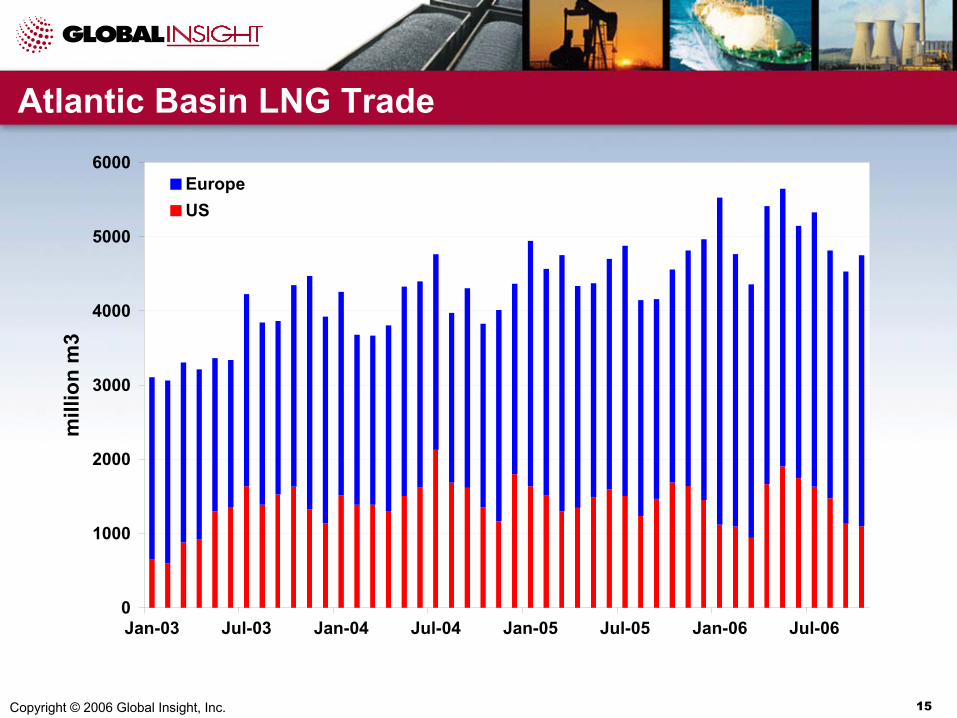

Atlantic Basin LNG Trade

0

1000

2000

3000

4000

5000

6000

Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06

mill

ion

m3

EuropeUS

Copyright © 2006 Global Insight, Inc. 16

U.S. vs. European Prices

Henry Hub versus Spanish Oil-indexed LNG

Henry Hub versus Spanish Oil-indexed LNG Henry Hub versus NBPHenry Hub versus NBP

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Jan-98 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06

$/m

mB

tu

US minus NBPHenry HubNBP

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Jan-98 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06

$/m

mB

tu

US minus Spanish LNGHenry HubSpanish LNG

Copyright © 2006 Global Insight, Inc. 17

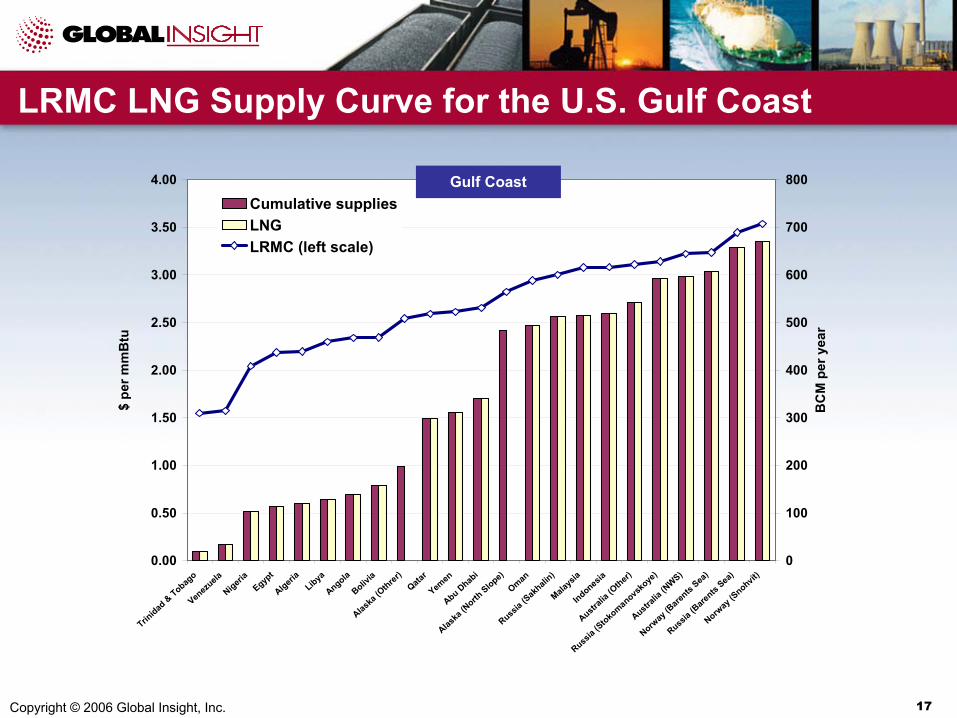

LRMC LNG Supply Curve for the U.S. Gulf Coast

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Trinidad

& Tobago

Venez

uela

Nigeria

Egypt

Algeria

Libya

Angola

Bolivia

Alaska

(Othrer

)Qata

r

Yemen

Abu Dhabi

Alaska

(North

Slope)

Oman

Russia (S

akhali

n)

Malays

ia

Indonesia

Australi

a (Other)

Russia

(Stokomanovs

koye

)

Australia

(NWS)

Norway

(Bare

nts Sea

)

Russia (B

arents

Sea)

Norway

(Snohvit

)

$ pe

r mm

Btu

0

100

200

300

400

500

600

700

800

BC

M p

er y

ear

Cumulative suppliesLNGLRMC (left scale)

Gulf Coast

Copyright © 2006 Global Insight, Inc. 18

LRMC LNG Supply Curve for the U.S. East Coast

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Canada (

exist

ing)

Trinidad

& Tobago

Venez

uela

Canad

a (Mac

kenzie

Delta)

Algeria

Nigeria

Egypt

Alaska

(Othrer

)Libya

Angola

Alaska

(North

Slope)

Abu Dhabi

Qatar

Yemen

Bolivia

Oman

Russia (S

tokomanovs

koye

)

Norway

(Bare

nts Sea

)

Malays

ia

Indonesia

Australia

(Other)

Russia (B

arents

Sea)

Russia (S

akhali

n)

$ pe

r mm

Btu

0

100

200

300

400

500

600

700

800

BC

M p

er y

ear

Cumulative suppliesLNGLRMC (left scale)

East Coast

Copyright © 2006 Global Insight, Inc. 19

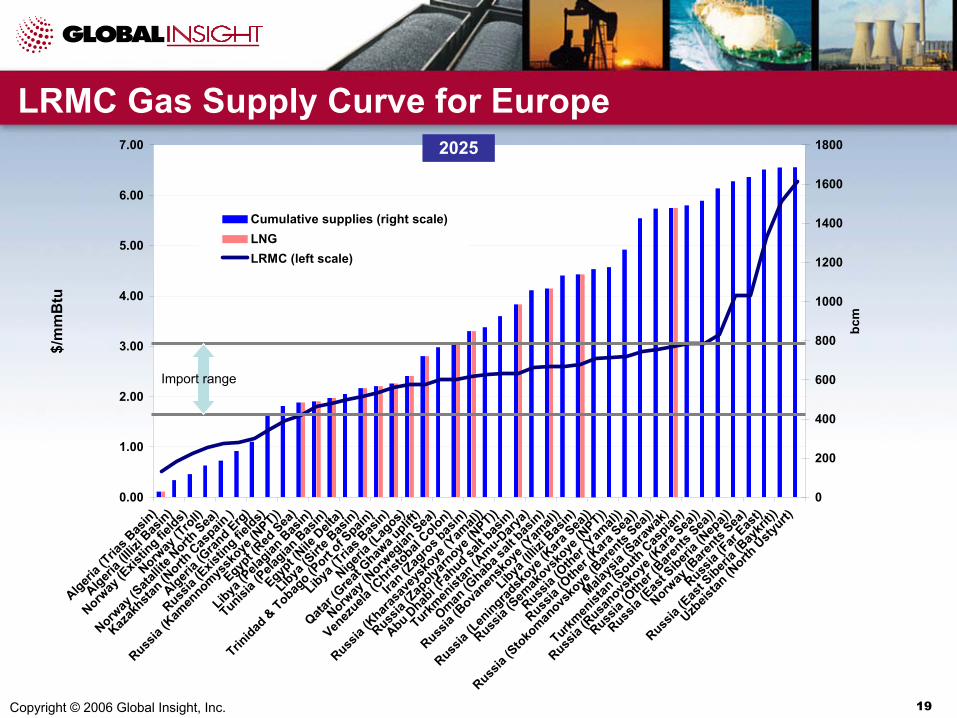

LRMC Gas Supply Curve for Europe

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Algeria (

Trias B

asin)

Algeria (

Illizi

Basin)

Norway

(Exis

ting fie

lds)

Norway

(Tro

ll)

Norway

(Sata

llite N

orth Sea

)

Kazak

hstan (N

orth C

aspain

)

Algeria (

Grand Erg

)

Russia

(Exis

ting fie

lds)

Russia

(Kam

ennomys

skoye

(NPT))

Egypt (R

ed Sea

)

Libya (P

elagian

Bas

in)

Tunisia (

Pelagian

Bas

in)

Egypt (N

ile D

elta)

Libya (S

irte B

asin)

Trinidad

& Tobag

o (Port

of Spain

)

Libya (T

rias B

asin)

Nigeria (

Lagos)

Qatar (

Great G

hawa u

plift)

Norway

(Norw

egian

Sea)

Venez

uela (C

hristobal

Colon)

Iran (Z

agro

s bas

in)

Russia

(Khara

save

ysko

ye (Y

amal)

)

Russia

(Zapolya

rnoye

(NPT))

Abu Dhab

i (Fah

ud salt b

asin)

Turkmen

istan

(Amu-D

arya)

Oman (G

haba s

alt bas

in)

Russia

(Bova

nensk

oye (Y

amal)

)

Libya (Il

lizi B

asin)

Russia

(Leningrad

skoye

(Kara

Sea))

Russia

(Sem

akovs

koye

(NPT))

Russia

(Other

(Yam

al))

Russia

(Other

(Kara

Sea))

Russia

(Stoko

manovs

koye

(Bare

nts Sea

))

Malays

ia (S

arawak

)

Turkmen

istan

(South C

aspian

)

Russia

(Rusa

novsko

ye (K

ara Sea

))

Russia

(Other

(Bare

nts Sea

))

Russia

(Eas

t Siberi

a (Nep

a))

Norway

(Bare

nts Sea

)

Russia

(Far Eas

t)

Russia

(Eas

t Siberi

a (Bay

krit))

Uzbeis

tan (N

orth U

styurt)

$/m

mB

tu

0

200

400

600

800

1000

1200

1400

1600

1800

bcm

Cumulative supplies (right scale)LNGLRMC (left scale)

2025

Import range

Copyright © 2006 Global Insight, Inc. 20

Comparative LRMC of Supply (Europe vs. U.S.)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Spain UK East Coast Gulf Coast

$/m

mB

tu

Middle EastNorth AfricaWest AfricaTrinidad

Copyright © 2006 Global Insight, Inc. 21

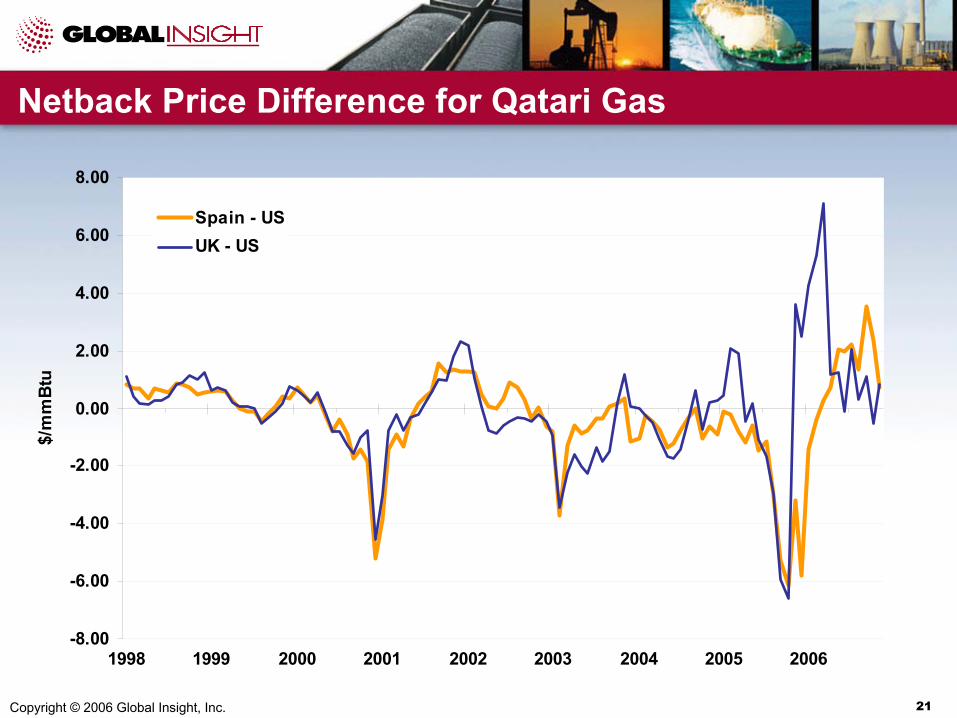

Netback Price Difference for Qatari Gas

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

1998 1999 2000 2001 2002 2003 2004 2005 2006

$/m

mB

tu

Spain - USUK - US

Copyright © 2006 Global Insight, Inc. 22

Average Netback Difference (U.S. vs. EU)

-2.00

-1.50

-1.00

-0.50

0.00

0.50

Middle East North Africa West Africa Trinidad

$/m

mB

tu

1998-20032004-present

Copyright © 2006 Global Insight, Inc. 23

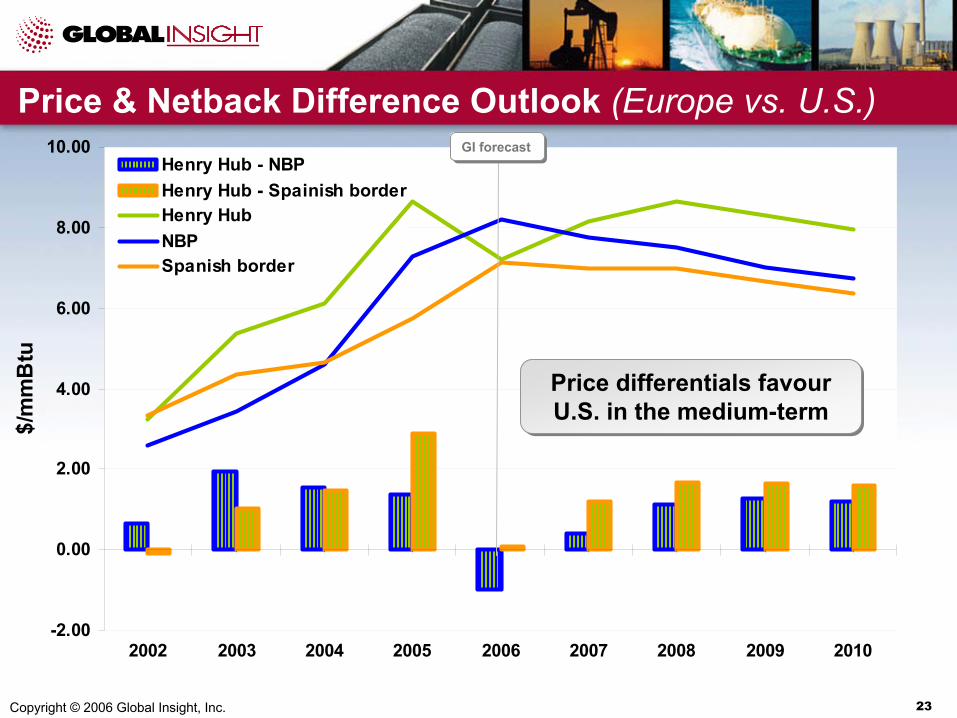

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

2002 2003 2004 2005 2006 2007 2008 2009 2010

$/m

mB

tu

Henry Hub - NBPHenry Hub - Spainish borderHenry HubNBPSpanish border

Price & Netback Difference Outlook (Europe vs. U.S.)GI forecastGI forecast

Price differentials favour U.S. in the medium-termPrice differentials favour U.S. in the medium-term

Copyright © 2006 Global Insight, Inc. 24

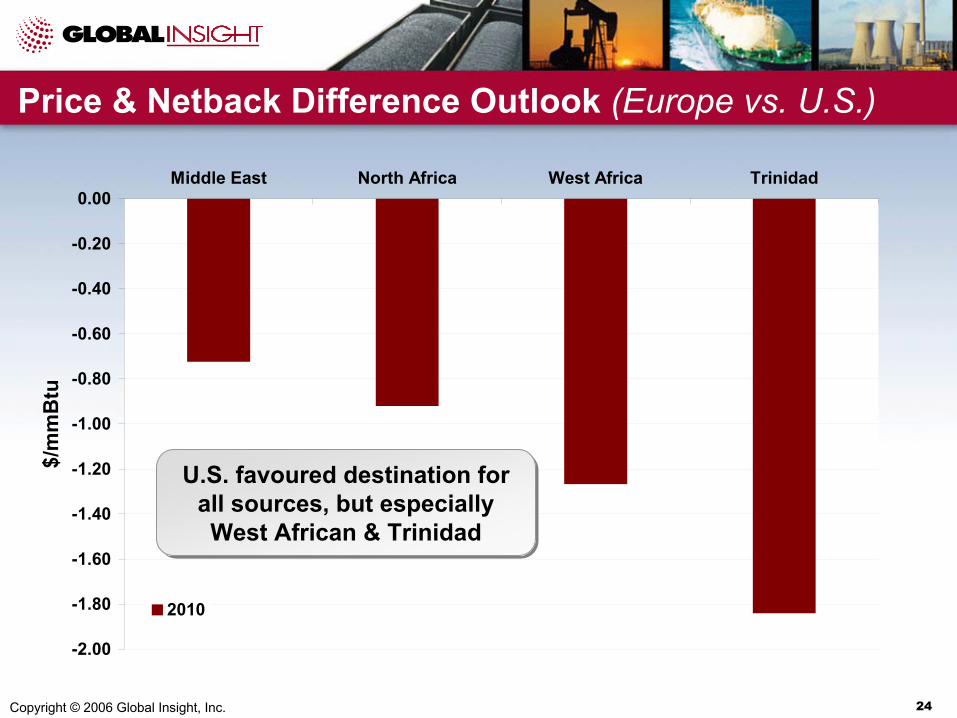

Price & Netback Difference Outlook (Europe vs. U.S.)

-2.00

-1.80

-1.60

-1.40

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00Middle East North Africa West Africa Trinidad

$/m

mB

tu

2010

U.S. favoured destination for all sources, but especially West African & Trinidad

U.S. favoured destination for all sources, but especially West African & Trinidad

Copyright © 2006 Global Insight, Inc. 25

Conclusions

• Recent cost inflation not undermined economics of LNGLNG competitive with pipe around 2,000-2,500 km

• Resource constraints delayed FIDMaterials, equipment, peopleLead times stretched: 45-48 month from 36

• Atlantic Basin a major source of LNG demand by 2010Large volumes provide flexibility optionsCosts dictate primary relationship

• Europe losing out to U.S. in resource competitionWest African gas favours the U.S.Europe takes more Middle East LNG