developing the networked content industry in malaysia ... · sms usage in europe, asia and us in...

TRANSCRIPT

27 June 2003

Developing the Networked Content Industry in MalaysiaDiscussion Paper

Attachments

Z HL

2A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

ObjectivesFigure 1 : Flow of Funds in Malaysia’s Networked Content Industry

DistributePackagePublishCreate DistributePackagePublishCreate

Private Free-to-Air TV

Subscription TV Operator

Telcos

Private Radio Operators

Advertising Production

Local Television Production

Advertising Agencies

Local Record Labels

Television Talent

Music Talent

ISP / Audio-text Providers

Interactive Developers

Government Television and Radio

Wireless \ Interactive Content Providers

Source: A.T. Kearney / ZOHL Group Analysis;

Satellite

Government

Advertiser

Subscription TV Subscribers

Internet and Audio Text Users

Wireless Data Users

3A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

ObjectivesFigure 2 : Networked Content Industry Objectives

Malaysia’s National Vision

Networked Content Industry Objectives

Cultural Objectives1. Consolidate racial and national unity through the

projection of national culture2. Encourage the production of content which is high quality,

innovative and creative3. Enrich and enhance the quality of material and spiritual

living in accord with social-economic development

Economic Objectives4. Make Malaysia a major centre for the national, regional

and global content industry5. Develop required capabilities to compete6. Achieve efficiency and financial viability 2

Social Objectives7. Contribute to Malaysia becoming a knowledge society8. Make access and content available everywhere and

affordable to all9. Establish a secure, robust and safe networking

environment 2

Notes: 1) Results of a government and industry survey conducted on 20 May 2003. Participants where asked to provide their personal opinion by allocating 1 through to 10 to the top 20 industry objectives.

2) For clarity sake, the survey objectives “Contribution to GDP” and “Job Creation” have been consolidated in to objective 3. Similarly, “secure and safe environment” and “ robust network environment” are consolidated in 6.

3) Objective 9 was not identified in the survey, but found important based on CMA 1998 and draft national content policySource: CMA 1998; Draft National Content Policy, A.T. Kearney/ZOHL Industry Survey 20 May, 2003

Relative Importance of Objectives 1

Gained from CMA and Draft National Content Policy 3

6.45.7

4.5

6.3

6.3

4.8

4.0

2.5

Most Importance

Least Importance

Proposed

4A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current Performance and Key IssuesFigure 3 : Local Content Popularity

Source: A.T.Kearney Analysis; OECD; Zenith Optimedia; Ovum; International Federation of the Phonographic Industry; ScreenDigest; Internet Software Consortium (ISC)

Television(Local Content in Top Ten Programs)

18

63

51 51

21 18

Malaysia S.Korea France UK Singapore Canada

Audio (Local Content % Share of Total Music revenues)

0.0

1.6

0.1 0.1 0.1 0.0

Malaysia S.Korea UK France Canada Singapore

Internet (Web pages in global Top 500 List per million capita)

0.6

2.9

1.7 1.51.3

Malaysia France Canada UK S.Korea

Moving Pictures (Number of local movies produced per million capita)

7

10 10 10

65

Malaysia France S.Korea UK Singapore Canada

5A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current Performance and Key IssuesFigure 4 : The Networked Content Industry Size relative to GDP

0.63

1.49 1.46

1.27 1.23

0.91

0

0.5

1

1.5

2

Malaysia Singapore S.Korea UK France Canada

US$0.6B US$5.6BUS$1.4B US$19.9B US$16.9B US$6.3BIndustry Value

Source: Local radio authorities;Zenith Optimedia; Ovum; IDC Note: 1) These figures represent networked content related revenue only; excludes box-office revenue, records sales,

SMS revenue and business internet subscription and usage

6A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current Performance and Key IssuesFigure 5 : Access Medium Penetration

1714

10

64

<1

Malaysia UK S.Korea Singapore Canada France

45

27

821

17

Malaysia S.Korea Canada Singapore UK France

12

5446 43

19

70

Malaysia Canada S.Korea UK Singapore France

Internet Penetration (% of households)

Broadband Penetration(% of households)

Wireless Data Penetration(% of users)

21

5743 43

26

10

Malaysia Canada Singapore UK France S.Korea

Subscription TV Penetration(% of households)

Note: 1) TV and radio penetration are not mentioned as they are close to 100% in all countriesSource: A.T.Kearney Analysis; IDC; A.T.Kearney Mobinet Survey 2003; Zenith Optimedia; Ovum

7A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current Performance and Key IssuesFigure 6 : Percentage of Networked Content Share of Total Advertisement Spend

33

49

43

4038

35

Malaysia Canada Singapore S.Korea France UK

Source: Zenith Optimedia

8A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current Performance and Key IssuesFigure 7 : Percentage of Advertising Expenditure on Malaysian Media 1998 – 2002

32 31 30 28 27

58 60 61 61 63

0

10

20

30

40

50

60

70

80

90

100

1998 1999 2000 2001 2002

Television Radio Newspapers Magazines Others

Source: ACNielsen 2002; Zenith Optimedia

9A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

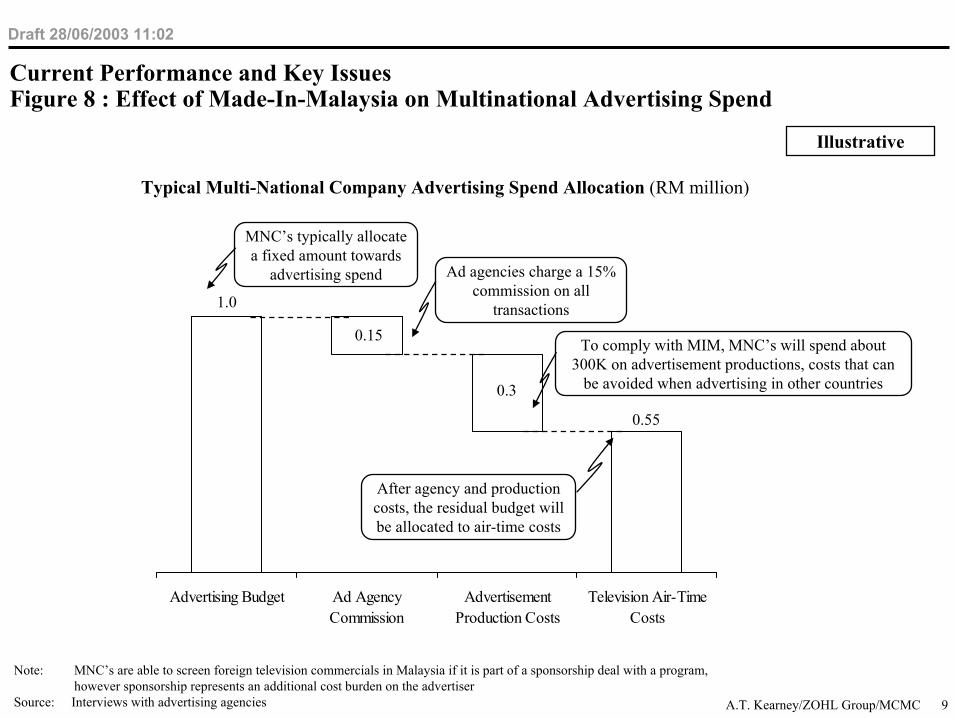

Current Performance and Key IssuesFigure 8 : Effect of Made-In-Malaysia on Multinational Advertising Spend

Typical Multi-National Company Advertising Spend Allocation (RM million)

Advertising Budget Ad AgencyCommission

AdvertisementProduction Costs

Television Air-TimeCosts

1.0

0.15

0.3

0.55

Ad agencies charge a 15% commission on all

transactions

To comply with MIM, MNC’s will spend about 300K on advertisement productions, costs that can

be avoided when advertising in other countries

MNC’s typically allocate a fixed amount towards

advertising spend

After agency and production costs, the residual budget will be allocated to air-time costs

Note: MNC’s are able to screen foreign television commercials in Malaysia if it is part of a sponsorship deal with a program, however sponsorship represents an additional cost burden on the advertiser

Source: Interviews with advertising agencies

Illustrative

10A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current State and Key IssuesFigure 9 : Revenue Redistribution to Local Content in Television

997 million

8%Subscriber TV

RevenueLocal Content

Spend

80 million

Subscriber Television Local Content Investment (RM)

76%

24%

Free-to-Air Television Local Content Investment

Foreign40% Local

60%

Source: Malaysian Broadcasters Television Alliance; Interviews with Astro

CMA Local Content Quota

Programming Costs in 2002

Local

Foreign

11A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current Performance and Key IssuesFigure 10 : Estimated Percentage of Moving Pictures and Music Revenue Lost from Piracy

Source: International Intellectual Property Alliance

1012121820

70

CanadaFrance UKSingaporeS.KoreaMalaysia

12A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

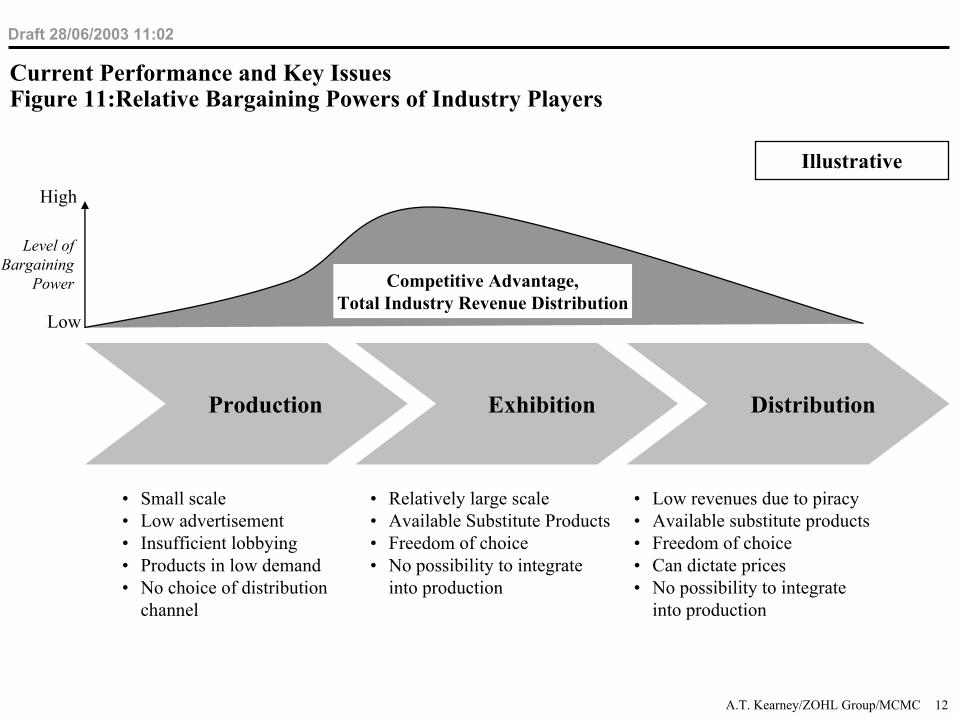

Current Performance and Key IssuesFigure 11:Relative Bargaining Powers of Industry Players

Production Exhibition Distribution

• Small scale• Low advertisement• Insufficient lobbying• Products in low demand• No choice of distribution

channel

• Relatively large scale• Available Substitute Products• Freedom of choice• No possibility to integrate

into production

• Low revenues due to piracy• Available substitute products• Freedom of choice• Can dictate prices• No possibility to integrate

into production

Competitive Advantage,Total Industry Revenue Distribution

Level of Bargaining

Power

High

Low

Illustrative

13A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current Performance and Key IssuesFigure 12 : Overlapping Regulation

Note: 1) List only includes primary regulations, however there are also site specific local permits required by local authorities

Pesticide ActTelemedicine Act 1997

University and University Colleges Act 1971

Medicine ActNational Anthem Act

Sale of Food and Drugs Act

Securities Industry Act 1983

Banking and Financial Institutions Act

Trade Description Act 1972

Communication and Multimedia Act

FINAS Act 1963 Cinema

TV

Radio

Internet

Advertising Guidelines

Broadcasting Guidelines

Emerging DistributeDistributePackagePublishCreate

Penal Code

Internal Security Act

Indecent Advertisement Act

Digital Signatures Act 1997

Sedition Act 1948

Consum

er Protection Act 2000

Defam

ation Act 1952

Trade Marks A

ct 1976C

opyright Act 1987

Geneva C

onvention, Berne C

onvention, other treatise

Made in Malaysia Guideline

Film (Censorship) Act 1952

Wireless

Film &TV

Radio & RM

P&M, B&L, IS

Various C

ontent Specific Acts

Pay TV

Acts governing content during and after “consumption”Input

Industries

Acts governing entire industry

Foreign Direct Investment Guideline

Federal Constitution

Networked Content Value Chain

Output Industries

Com

puter C

rimes A

ct

Printing Presses & Publications Act

Sale of Goods Act

14A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current Performance and Key IssuesFigure 13 : Government Bodies Involved in Regulating and Enforcing Networked Content Industry

Advisory

JAKIM(Advisory)

Domestic Trade

Consumer Affairs

FinanceEducationHealthAgricultureEnergy, Com. and Multim.

InformationHome AffairsMinistry

Intellectual Property & Consumer

Affairs Division

Administration

Division

Private Education Division

Food Quality Control

Division & Pharmac. Division

Pesticide Control Division

MCMCCommercial Department FINAS

LembagaPenapisan

Filem(LPF)

Governing Body

Monitoring of false

advertising

Monitoring of copyright and

piracy

Approving of all gaming adsas defined in

Common Gaming Act,

1953

Approving of all private

education ads

Approving of all poison &

medicine related ads

Approving of all pesticide

ads

Approval for advertising on

RTM (KP# Issuance)

Licensing of all TV adds

(MIM)Censoring of

all addsAdvertising

EnforcementLicensing of

film developers

and producers

Censoring of all audiovisual / promotional

contentContent

Licensing of wireless, ISP, TV and radio

Licensing of film

distributors and exhibitors

Access

Note: Content forum will be the body responsible for administering the content code once it is ratified

15A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current Performance and Key IssuesFigure 14 : Relative Broadband Subscription Fees (2003, US$ income adjusted)

Source: A.T. Kearney; Analysys

$0 $10 $20 $30 $40 $50 $60 $70 $80

Malaysia

South Korea

UK

France

Canada

Singapore

16A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

SMS Usage in Europe, Asia and US in 2002

29% 38%

81%

81%62%

19%

Europe Asia US

Never used SMS Used SMS

• US telecoms regulations, which permitteddifferent mobile operators to choose different, incompatible technologies has led to complexities in formulating interconnect agreements for data

• In late 2002, the largest US mobile operators agreed to pass text messages between their networks, however the agreement is still only partly implemented.

• Since interconnect agreements were formalised in September 2001, Malaysia has experienced a surge in SMS traffic

• In 2002, Malaysian telcos made preliminary agreements to share ‘shortcodes’ that allow users to access wireless data services from different providers on a single number

• Interconnect agreements are still outstanding in areas such as WiFi, MMS and 3G –which could pose a threat to the uptake of these new services

Mobile Data Service Interconnect ChallengesLow penetration of SMS usage

Current Performance and Key IssuesFigure 15 : Potential Adverse Impact of Ineffective Open Standards and Interconnectivity

Source: A.T.. Kearney Mobinet Survey

17A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Current Performance and Key IssuesFigure 16 : Ineffective Government Incentive Schemes

• In early 2000 the “One Family, One Computer” scheme enabledcontributors to the EPF to withdraw part of their savings forpersonal computer purchases, but was cancelled in 2002

Source: IDC

3446

606468

13

FranceUKCanadaSingaporeS.KoreaMalaysia

PC Penetration Rate(% of households)

• Despite an investment of RM 5.1 billion over 5 years in ICT initiatives, Malaysia’s internet subscription rate still lags benchmark countries

12

5446 43

19

70

Malaysia Canada S.Korea UK Singapore France

Internet Subscription (% of households)

18A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Create Publish Package Distribute Total

1,967 million

Subscription TV (66%)

Free-to-Air TV (34%)

170 million

1,257 million

398 million

143 million

Satellite (53%)Terrestrial (47%)

Free-to-Air Programming (66%)

Advertising Production (19%)Subscription Programming (15%)

1

TelevisionFigure T.1 : Malaysian Television Industry Size in 2002 (RM)

Note: 1) ‘Create’ represents the talent pool required for television production and is typically 25% of production costsSource: Zenith 2002; ACNielsen; A.T. Kearney / ZOHL Group Analysis

19A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

TelevisionFigure T.2 : Relative Networked Content Industry Size (Revenue % of Total NCI Revenue)

0%

25%

50%

75%

100%

Malaysia UK France Canada S.Korea Singapore

WirelessInternetRadioTelevision

Source: Zenith 2002; ACNielsen; A.T. Kearney / ZOHL Group Analysis

20A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

TelevisionFigure T.3 : Estimated Revenue Growth for Total Television Industry in Malaysia 1997 -2002

643 663770

1179

1493

1808

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1997 1998 1999 2000 2001 2002

RTM AdEx RTM Government Funding

TV3 & NTV7 AdEx Astro AdEx & Fees

Rev

enue

(RM

mill

ions

)CAGR (%)

97 - 02

Source: Zenith 2002; ACNielsen; A.T. Kearney / ZOHL Group Analysis

26% - Total

15% TV3 & NTV7

66% - Astro

10% - RTMGrowth due to launch

of NTV7 in 1998 –however 0% CAGR

over 2000-2002

4% - Total FTA

21A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

TelevisionFigure T.4 : Television Penetration of Households in 2002

Total Households Free-to-Air TV Households

5.3 million(100%)

4.3 million(82%)

Source: MCMC Statistical Bulletins (2002); ITU Note: TV Households Figures assume 2% growth from 2001 ITU estimates

59%

31%

10%

Indian

Chinese

10%

63%

27%

Malay

22A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

TelevisionFigure T.5 : Subscription Television Penetration (% of households)

21

57

43 43

26

10

Malaysia Canada Singapore UK France S.Korea

Source: Zenith Optimedia

23A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

TelevisionFigure T.6 : Television Industry Size (Revenue % of GDP)

Source: Zenith Optimedia; IDC Note: 1) These figures represent networked content related revenue only; excludes television content creation

0.52 0.50 0.450.59

0.870.95

UK France S.Korea Singapore Canada Malaysia

An addition 0.05% of GDP is an increase of 11% or RM 175 million

An addition 0.23% of GDP is an increase of 53% or RM 830 millionAverage of benchmark countries

RM

1.575 m

illion

24A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

TelevisionFigure T.7 : Number of Local Programs in the Top Ten Television Programs

Source: A.T.Kearney Analysis

7

10 10 10

65

Malaysia France S.Korea UK Singapore Canada

25A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

TelevisionFigure T.8 : Free-to-Air Television Advertising (RM millions)

0

100

200

300

400

500

600

1997 1998 1999 2000 2001 2002

Source: ACNielsen 2002

CAGR (%)

1%

-2%

Nominal

Real

26A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

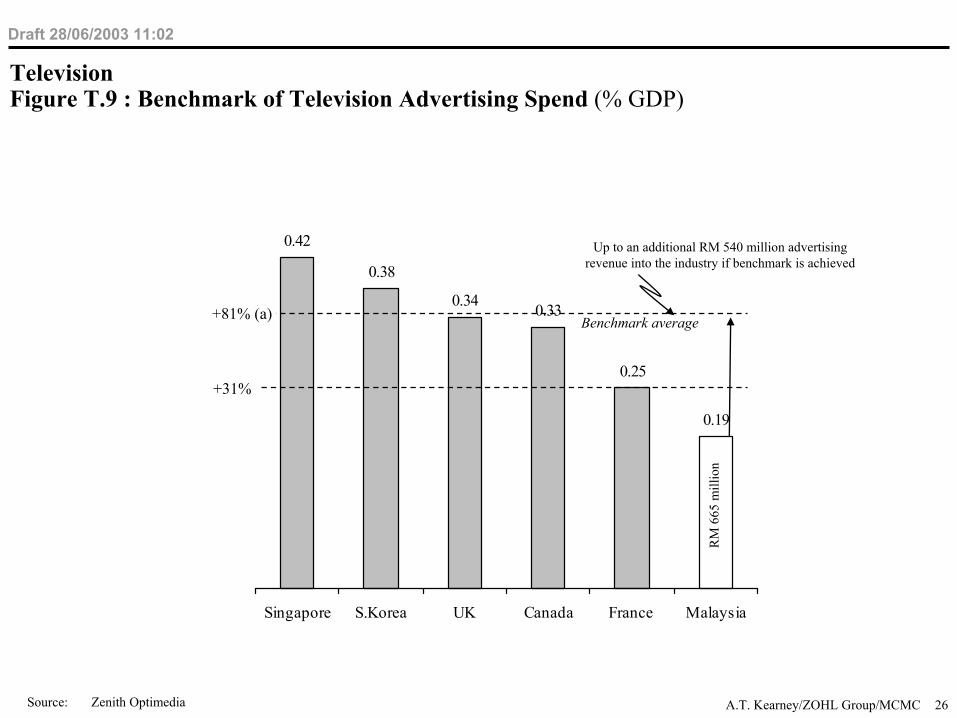

TelevisionFigure T.9 : Benchmark of Television Advertising Spend (% GDP)

0.42

0.38

0.34 0.33

0.25

0.19

Singapore S.Korea UK Canada France Malaysia

+31%

RM

665

mill

ion

Up to an additional RM 540 million advertising revenue into the industry if benchmark is achieved

+81% (a) Benchmark average

Source: Zenith Optimedia

27A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

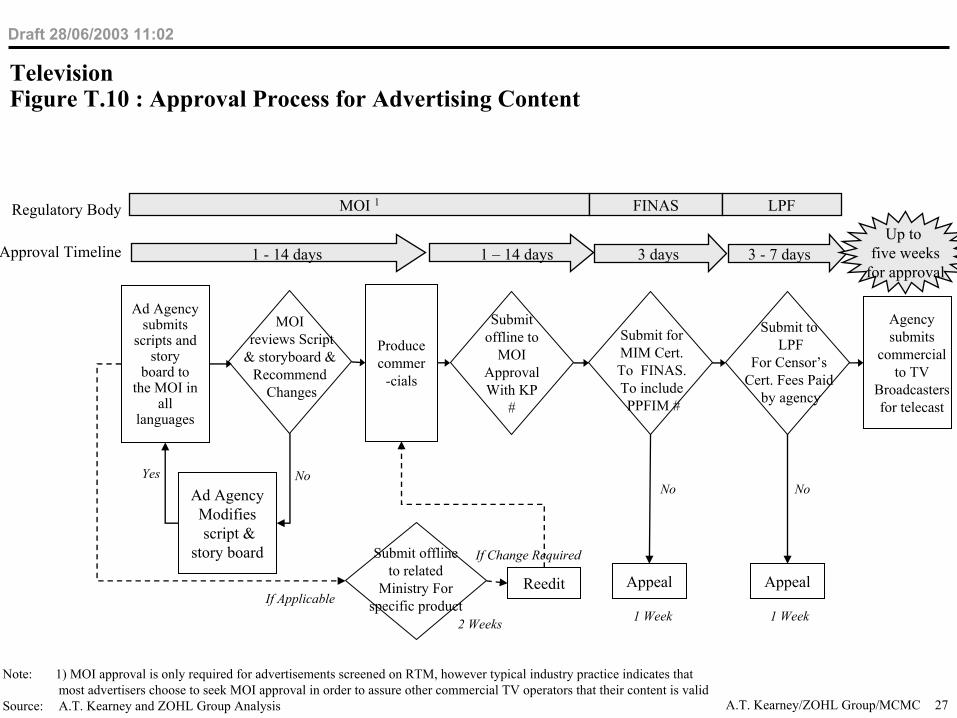

TelevisionFigure T.10 : Approval Process for Advertising Content

1 – 14 days 3 days 3 - 7 days1 - 14 days

Yes

MOIreviews Script

& storyboard & Recommend

Changes

Submit for MIM Cert. To FINAS. To includePPFIM #

Submit toLPF

For Censor’s Cert. Fees Paid

by agency

Produce commer

-cials

Agency submits

commercial to TV

Broadcasters for telecast

Submit offline to

MOI ApprovalWith KP

#

Ad Agency Modifiesscript &

story board

AppealAppealReedit

No

1 Week 1 Week2 Weeks

Submit offline to related

Ministry For specific product

If Change Required

No No

MOI 1 FINAS LPF

Up to five weeks

for approval

Regulatory Body

Ad Agency submits

scripts and story

board to the MOI in

all languages

Approval Timeline

If Applicable

Note: 1) MOI approval is only required for advertisements screened on RTM, however typical industry practice indicates that most advertisers choose to seek MOI approval in order to assure other commercial TV operators that their content is valid

Source: A.T. Kearney and ZOHL Group Analysis

28A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

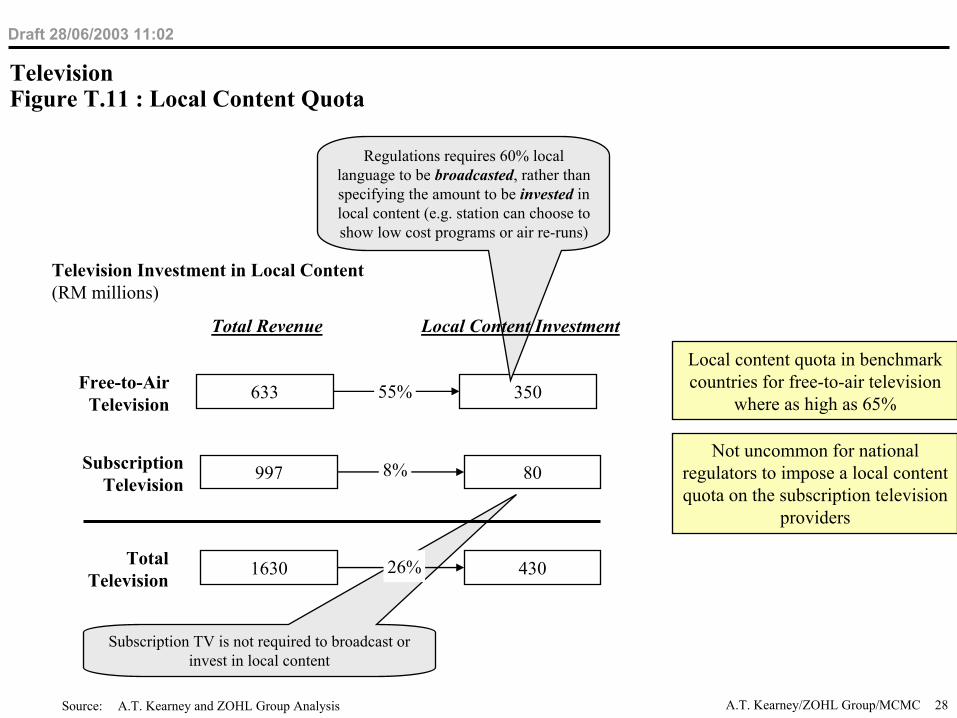

TelevisionFigure T.11 : Local Content Quota

Television Investment in Local Content(RM millions)

Subscription TV is not required to broadcast or invest in local content

Free-to-Air Television

633 350

997 80

1630 430

Subscription Television

Total Television

Total Revenue

55%

8%

26%

Regulations requires 60% local language to be broadcasted, rather than specifying the amount to be invested in local content (e.g. station can choose to show low cost programs or air re-runs)

Local Content Investment

Source: A.T. Kearney and ZOHL Group Analysis

Local content quota in benchmark countries for free-to-air television

where as high as 65%

Not uncommon for national regulators to impose a local content quota on the subscription television

providers

29A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

TelevisionFigure T.12 : Index of Free-to-Air Television Operators Local Content Spend (estimated)

10054

131

72

181

99

Total Free-to-AirTelevision Revenue

Current Local ContentSpend

Potential Free-to-AirTelevision Revenue

Potential Local ContentSpend

RM 350 million

Annual spend in local content could increase to RM 470 million

Annual spend on local content could increase to RM 700 million

Current Potential

Growth to Average International Benchmark

Growth to Nearest Benchmark

Source: A.T. Kearney / ZOHL Group Estimates

30A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Moving PicturesFigure M.1 : Total and Local Content Box Office Revenue (RM million)

88

69

110

140

18.4

6.5

18.38.6

1999 2000 2001 2002

TotalLocal Content

Source: Zenith Optimedia; FINAS

31A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Moving PicturesFigure M.2 : Index of International and Malaysian Sources of Revenue for Movie Producers

0

25

50

75

100

International Malaysia

BoxOffice

TV

Video

Pric

e Pr

essu

re o

nV

ideo

Roy

altie

s

26

28

46

82

144

Potential130%

revenueincrease

Source: A.T. Kearney / ZOHL Group Estimates

32A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Moving PicturesFigure M.3 : Box Office Revenues and Local Producers Market Share in Malaysia (RM million)

185.0

122

4.3

3.4

5.3

Box Office Revenues Local Production Houses

Others

Metrowealth

Tayangan

Skop

ForeignContent

LocalContent

Source: FINAS; ZOHL Group Analysis

33A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Moving PicturesFigure M.4 : Cinema Admission Prices (US$ income adjusted)

4.44.75.5

6.1

9.7

5.2

CanadaSingaporeFranceUKS.KoreaMalaysia

Source: Zenith Optimedia; Cannes.Market; Screen Digest

34A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Moving PicturesFigure M.5 : Annual Admissions Per Capita

1.9

2.6

3.143.3

3.93

0.5

S.KoreaUKFranceSingaporeCanadaMalaysia

Source: Cannes Market; Screen Digest

35A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Moving PicturesFigure M.6 : Current Industry Size per Capita (US$ income adjusted)

3

14

1617

1819

Malaysia S.Korea Singapore France UK Canada

Needto increase 4-5times to reach

next benchmarklevel

Source: Cannes Market

36A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Moving PicturesFigure M.7 : Approval Process for Film Content

Submit to LPF for Censor’s

Certificate

Producers submit for

FC approval toshoot from

FINAS

Producer obtain

productionLicense from

FINAS (onetime only)

Producer start the production

& submit completed

product to LPF

Film producer request for

Compulsory Screening Dates

from FINAS

Film is screened on the

designated dates allocated by

FINAS

Appeal Edit and resubmit

30 days30 days

FINAS LPF FINAS

Up to Two monthsfor approval

Regulatory Body

Approval Timeline

Inconsistent content regulation increases the risk upfront of investing in content that will

not be screened

Content that is approved by LPF can still be censored or banned when the content is

broadcast on television

Content that is approved must comply with a simplistic ratings systems that categorises content

as general viewing or 18+

Source: A.T. Kearney and ZOHL Group Analysis

37A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Audio/RadioFigure A.1 : Malaysian Radio Industry Size in 2002 (RM)

Note: Networked content for audio only includes content broadcast on radio networksSource: Zenith 2002; ACNielsen; A.T. Kearney / ZOHL Group Analysis

221 million23 million

197 million

0.8 million0.2 million

Royalties to local artists

Royalties to record labels

Radio advertising / government funding

Terrestrial broadcasting

Create Publish Package Distribute Total

38A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Audio/RadioFigure A.2 : Radio Industry Advertising Revenue Growth 1997 - 2002

Source: ACNielsen 2002; Zenith Media

Adv

ertis

ing

Rev

enue

(RM

mill

ions

)

0

20

40

60

80

100

120

140

160

1997 1998 1999 2000 2001 2002

19%

CAGR97-02

39A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Audio/RadioFigure A.3 : Radio Industry Market shares and Advertising Premiums 2002

0

50

100

150

200

250

0 5 10 15 20 25 30

Ave

rage

Rat

e pe

r A

dver

tisem

ent

Total Advertising Revenue (RM millions)

Era FMMy FM

redi 988

Mix FMhitz.fm

THR

Light & Easy

RM Saluran Muzik

red 104.9RM Saluran 5

RM Saluran 6

RM Saluran 4

RM Saluran 1

RM Kuala Lumpur

RM Selangor

Era FM18%

hitz.fm12%

Light & Easy6%

Mix FM13%

My FM15%

red 104.92%

redi 99814%

RM Saluran8%

THR9%

Other3%

AMP Rediffusion RM THR

Source: ACNielsen 2002 Note: RM Saluran includes 7 radio station: RM Saluran 1, 4, 5, 6, Selangor, Kuala Lumpur

AMP

Radio Station Market share in 2002 Radio Station Advertising Premiums in 2002

40A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Audio/RadioFigure A.4 : Radio Penetration Rates in Malaysia 2002

Population Living in Households /+15 Years Age

Radio Coverage

11.4 million(100%)

10.3 million(90%)

Source: ACNielsen 2002; Malaysian Department of Statistics

Indian Chinese Malay

Total Households Radio Households

5.3 million(100%)

4.2 million(79%)

63%

27%

10%

11%

31%

58%

Radio Penetration of Households in 2002 Radio Coverage of Consumers in 2002

41A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

Audio/RadioFigure A.5 : Malaysian Local Content as Percentage of Total Music Industry 1998 – 2002

24

1516 16

18

0

5

10

15

20

25

30

1998 1999 2000 2001 2002

Loc

al c

onte

nt m

arke

t sha

re (%

)

Source: International Federation of the Phonetic Industry

42A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

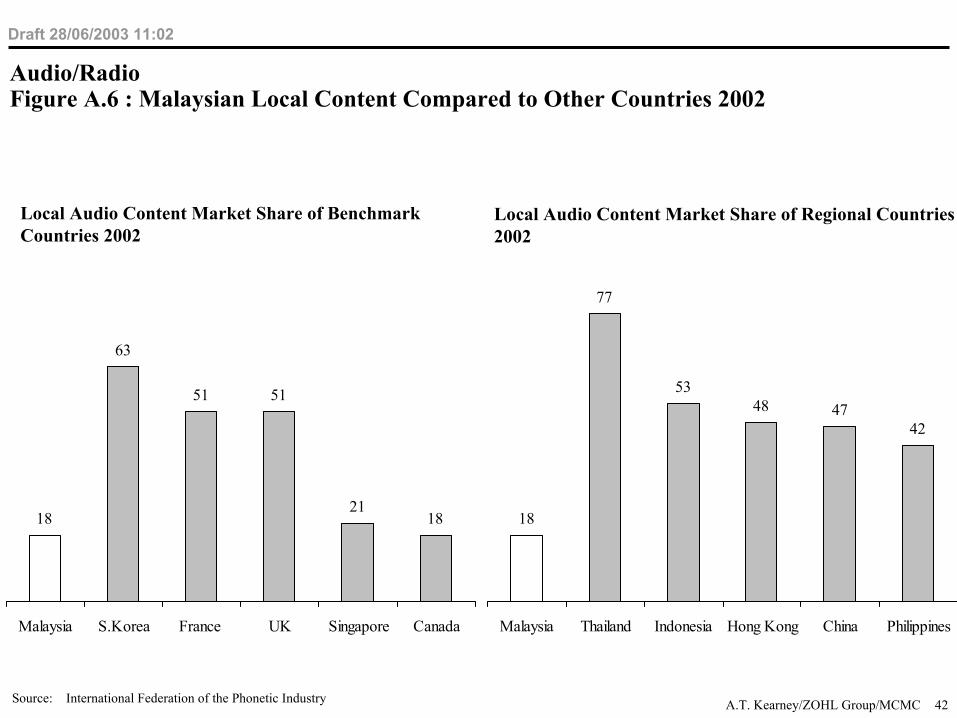

Audio/RadioFigure A.6 : Malaysian Local Content Compared to Other Countries 2002

Source: International Federation of the Phonetic Industry

18

63

51 51

2118

Malaysia S.Korea France UK Singapore Canada

18

77

5348 47

42

Malaysia Thailand Indonesia Hong Kong China Philippines

Local Audio Content Market Share of Benchmark Countries 2002

Local Audio Content Market Share of Regional Countries 2002

43A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

InteractiveFigure I.1 : Malaysian Interactive Industry Size in 2002 (RM)

Source: Gartner; A.T. Kearney estimates

541 million67 million

450 million

21 million3 million

ISP access revenue

ISP PSTN Charges (90%)

Audio-text (10%)

Audio-text (55%)Internet Content (45%)

Create Publish Package Distribute Total

44A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

InteractiveFigure I.2 : Internet Penetration (% of households)

12

54

4643

19

70

Malaysia Canada S.Korea UK Singapore France

Source: IDC;

45A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

InteractiveFigure I.3 : Affordability and Accessibility of Broadband in Malaysia

Malaysia has the highest average ADSL monthly subscription fees (2003, US$, income adjusted)

0

10

20

30

40

50

1999 2000 2001 2002 2003 2004 2005

Malaysia is behind in broadband roll-out(% of homes connected)

S. Korea

Australia

Malaysia

Canada

Source: IDC; A.T. Kearney; Analysys$0 $10 $20 $30 $40 $50 $60 $70 $80

Malaysia

South Korea

UK

France

Canada

Singapore

46A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

InteractiveFigure I.4 : Cost of a basic PC (US$, PPP adjusted)

1,583

1,452

1,204 1,185

990

694

Malaysia France UK Canada S.Korea Singapore

Note: 1) Based on price comparison for Dell 4600

47A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

InteractiveFigure I.5 : PC Penetration Rate (% of households)

34

46

6064

68

13

FranceUKCanadaSingaporeS.KoreaMalaysia

Source: ACNielsen

48A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

InteractiveFigure I.6 : Internet Broadband Subscribers 2002 Q3 – 2003 Q1

1%

1%

3%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2002 Q3 2002 Q4 2003 Q1

Penetration rates of households

Source: MCMC Statistical Bulletins (2002)

Subs

crib

ers

49A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

InteractiveFigure I.7 : Internet Access Market Shares in 2002

Observations

• 98% of the PSTN usage is billed per minute and provided by Telekom Malaysia

• Celcom Net is now owned by Telekom Malaysia

Malaysian Internet Access Market Shares 2002

TM Net55.2%Jaring

26.3%

Time Net15.6%

Other0.9%

Celcom Net2.0%

Source: MCMC Statistical Bulletins (2002)

50A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

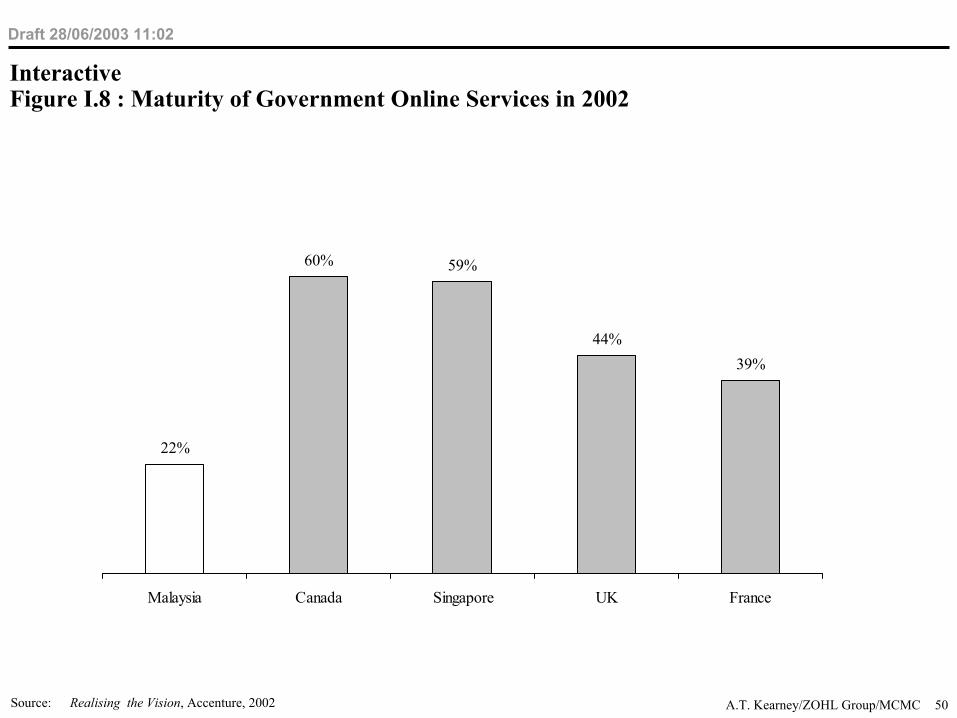

InteractiveFigure I.8 : Maturity of Government Online Services in 2002

22%

60% 59%

44%39%

Malaysia Canada Singapore UK France

Source: Realising the Vision, Accenture, 2002

51A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

WirelessFigure W.1 : Cellular Subscriber Growth in Malaysia 1997 – 2008

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Cel

lula

r Ph

one

Subs

crib

ers (

Tho

usan

ds)

Forecast

Source: MCMC Statistical Bulletins (2002); A.T. Kearney Analysis

52A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

WirelessFigure W.2 : Revenue of the overall wireless industry (US$ billion)

0

1

2

3

4

2001 2002 2003 2004 2005 2006

Source: Ovum

53A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

WirelessFigure W.3 : Malaysian Wireless Services Industry Size in 2002 (RM)

Content Access Total

50 million

Wireless content providers such as audio-text providers

40 million

10 million

Mainly premium SMS services

Source: Industry interviews

54A.T. Kearney/ZOHL Group/MCMC

Draft 28/06/2003 11:02

WirelessFigure W.4 : Usage of wireless data services around the world (% of users who have used the service)

11

28

310

77

27

38

53

21

6 4

Malaysia Europe North America Japan

EmailNewsTravelBanking

Still in a testing state

Source: A.T. Kearney Mobinet Survey