determing cash flows for investing analysis

TRANSCRIPT

Chapter - 10

DeterminingCash Flows for

Investment Analysis

2Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Chapter Objectives Show the conceptual difference between

profit and cash flow. Discuss the approach for calculating

incremental cash flows. Highlight the interaction between financing

and investment decisions.

3Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Introduction Sound investment decisions should be based

on the net present value (NPV) rule. Problem to be resolved in applying the NPV

rule: What should be discounted? In theory, the answer

is obvious: We should always discount cash flows.

What rate should be used to discount cash flows? In principle, the opportunity cost of capital should be used as the discount rate.

4Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Cash Flows Versus Profit Cash flow is not the same thing as profit, at

least, for two reasons: First, profit, as measured by an accountant, is based

on accrual concept. Second, for computing profit, expenditures are

arbitrarily divided into revenue and capital expenditures.

CF (REV EXP DEP) DEP CAPEXCF Profit DEP CAPEX

5Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Incremental Cash Flows Every investment involves a comparison of

alternatives: When the incremental cash flows for an

investment are calculated by comparing with a hypothetical zero-cash-flow project, we call them absolute cash flows.

The incremental cash flows found out by comparison between two real alternatives can be called relative cash flows.

The principle of incremental cash flows assumes greater importance in the case of replacement decisions.

6Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Components of Cash Flows Initial Investment Net Cash Flows

Revenues and Expenses Depreciation and Taxes Change in Net Working Capital

Change in accounts receivable Change in inventory Change in accounts payable

Change in Capital Expenditure Free Cash Flows

7Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Components of Cash Flows Terminal Cash Flows

Salvage Value Salvage value of the new asset Salvage value of the existing asset now Salvage value of the existing asset at the end of its

normal Tax effect of salvage value

Release of Net Working Capital

8Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Depreciation for Tax Purposes Two most popular methods of charging

depreciation are: Straight-line Diminishing balance or written-down value (WDV)

methods. For reporting to the shareholders, companies

in India could charge depreciation either on the straight-line or the written-down value basis.

For the tax purposes, depreciation is computed on the written down value (WDV) of the block of assets.

9Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

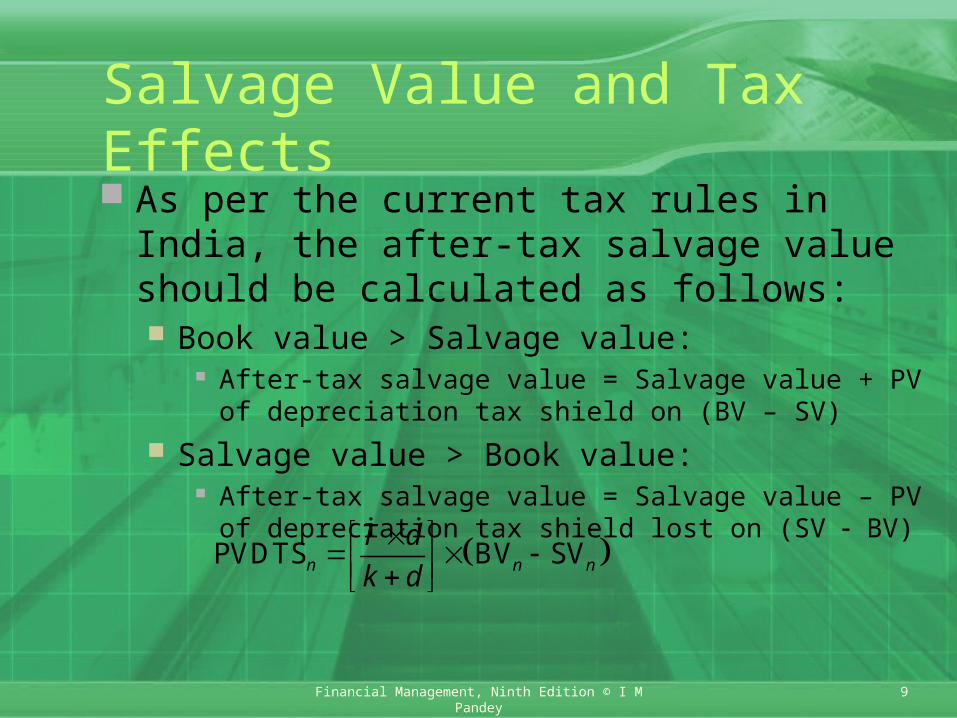

Salvage Value and Tax Effects As per the current tax rules in India, the after-tax

salvage value should be calculated as follows: Book value > Salvage value:

After-tax salvage value = Salvage value + PV of depreciation tax shield on (BV – SV)

Salvage value > Book value: After-tax salvage value = Salvage value – PV of depreciation

tax shield lost on (SV BV)

PVDTS BV SVn n nT dk d

10Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Terminal Value for a New Business The terminal value included the salvage value of the

asset and the release of the working capital. Managers make assumption of horizon period because

detailed calculations for a long period become quite intricate. The financial analysis of such projects should incorporate an estimate of the value of cash flows after the horizon period without involving detailed calculations.

A simple method of estimating the terminal value at the end of the horizon period is to employ the following formula, which is a variation of the dividend—growth model:

1NCF 1 NCFTV n n

n

gk g k g

11Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Cash Flow Estimates for Replacement Decisions The initial investment of the new machine will

be reduced by the cash proceeds from the sale of the existing machine:

The annual cash flows are found on incremental basis.

The incremental cash proceeds from salvage value is considered.

12Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Additional Aspects of Incremental Cash Flow Analysis Allocated Overheads Opportunity Costs of Resources Incidental Effects

Contingent costs Cannibalisation Revenue enhancement

Sunk Costs Tax Incentives

Investment allowance Until Investment deposit scheme Other tax incentives

13Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Investment Decisions Under Inflation Executives generally estimate cash flows assuming unit costs

and selling price prevailing in year zero to remain unchanged. They argue that if there is inflation, prices can be increased to cover increasing costs; therefore, the impact on the project’s profitability would be the same if they assume rate of inflation to be zero.

This line of argument, although seems to be convincing, is fallacious for two reasons. First, the discount rate used for discounting cash flows is generally

expressed in nominal terms. It would be inappropriate and inconsistent to use a nominal rate to discount constant cash flows.

Second, selling prices and costs show different degrees of responsiveness to inflation:

The depreciation tax shield remains unaffected by inflation since depreciation is allowed on the book value of an asset, irrespective of its replacement or market price, for tax purposes.

14Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

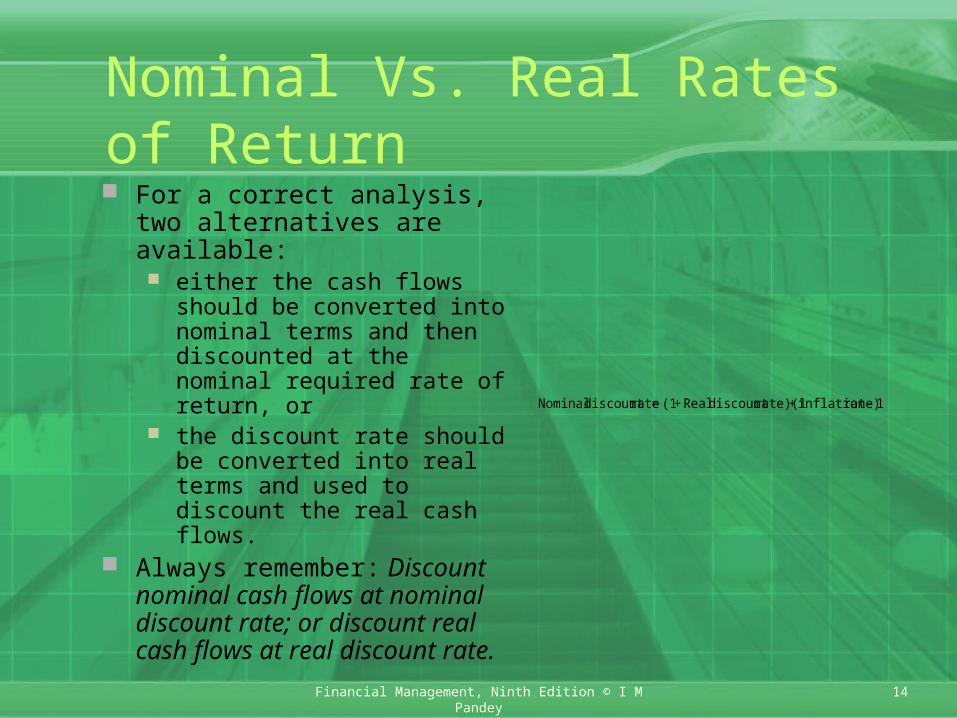

Nominal Vs. Real Rates of Return For a correct analysis, two

alternatives are available: either the cash flows should

be converted into nominal terms and then discounted at the nominal required rate of return, or

the discount rate should be converted into real terms and used to discount the real cash flows.

Always remember: Discount nominal cash flows at nominal discount rate; or discount real cash flows at real discount rate.

1rate)inflation +rate)(1discount Real+(1=ratediscount Nominal

15Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

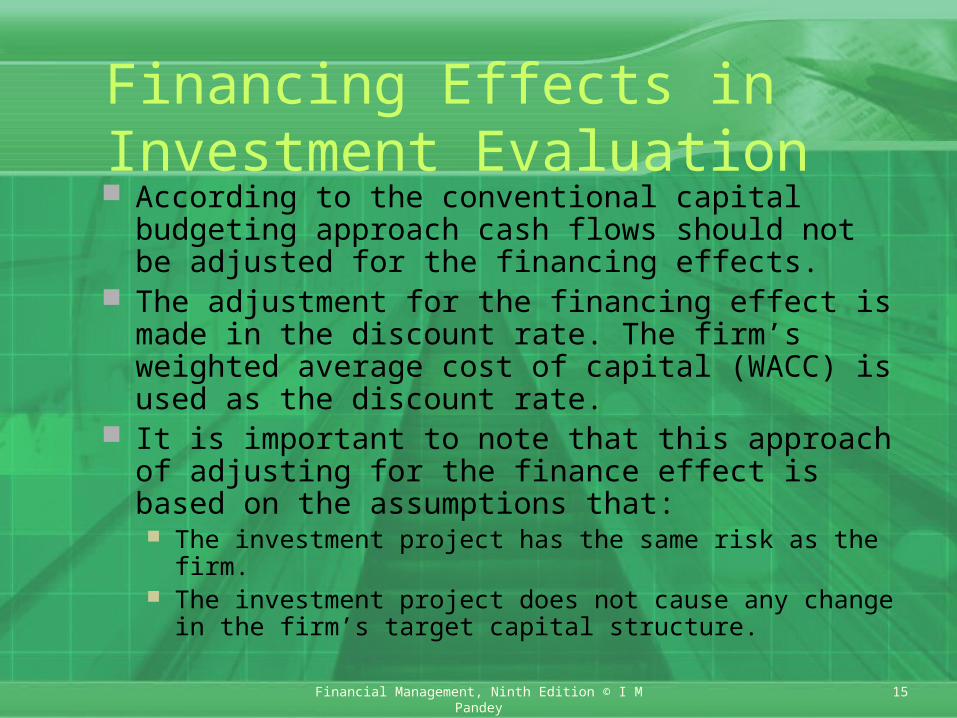

Financing Effects in Investment Evaluation According to the conventional capital budgeting

approach cash flows should not be adjusted for the financing effects.

The adjustment for the financing effect is made in the discount rate. The firm’s weighted average cost of capital (WACC) is used as the discount rate.

It is important to note that this approach of adjusting for the finance effect is based on the assumptions that: The investment project has the same risk as the firm. The investment project does not cause any change in the

firm’s target capital structure.