describing firm’s behavior using revenue and cost data

TRANSCRIPT

The Pennsylvania State University

The Graduate School

Department of Economics

DESCRIBING FIRM’S BEHAVIOR USING REVENUE AND COST DATA

A Thesis in

Economics

by

Sergio DeSouza

© 2004 Sergio DeSouza

Submitted in Partial Fulfillment of the Requirements

for the Degree of

Doctor of Philosophy

December 2004

The thesis of Sergio DeSouza was reviewed and approved* by the following:

James Tybout Professor of EconomicsThesis Advisor Chair of Committee

Mark Roberts Professor of Economics

Susana Esteban Assistant Professor of Economics

Spiro Stefanou Professor of Agricultural Economics

Robert Marshall Professor of Economics Head of the Department of Economics

*Signatures are on file in the Graduate School

iii

Abstract

The main objective of this research is to discuss and extend the existing literature that is concerned with the estimation of demand and supply parameters to determine unobserved prices, quantities, quality and marginal costs at the firm-level using data sets that reports only revenue and cost figures. A common approach to estimate these parameters is given by the production function. However, to be implemented it needs output data, which most plant-level data sets do not report. In the second chapter (the first one is an introduction), using the same framework, I shall investigate the consequences of ignoring price heterogeneity on the markup estimates from the production function in plant or firm–levels studies. I show that ignoring output price heterogeneity yield markup estimates severely biased towards one regardless of competitiveness levels. I set up an econometric model that assumes monopolistic competition and a CES demand function in a differentiated product market that is easy to estimate and allows for the use aggregate instruments to improve on the OLS estimations. In the third chapter, I discuss the estimation of discrete-choice model of demand. Katayma, Lu and Tybout (2003) used a nested logit model to derive consumer and producer surplus to measure efficiency. Their work (KLT) however differentiates from the others since the data set used there is not quite informative. Again, it assumes that only revenue and total costs are observed. Then combining these data with demand and the quasi-supply relation they demonstrate how to estimate the parameters of interest. I demonstrate how to extend the KLT framework by including the extra information provided by aggregate data. Although it may be difficult to obtain detailed data on quantities at the plant level, the same is not true for aggregate variables. I consider two different hypotheses on the nature of this aggregate measure. The first one assumes that this information is noisy, while the second assumes that this information is deterministic and therefore error free. Each assumption yields a different estimation strategy with potentially yield different parameter estimates. With the preference parameters, qualities and marginal costs determined according to the methodology developed in the third chapter, one is able to construct consumer and producer welfare measures. The first two sections of the third chapter present counterfactual experiments. They consist on assuming exogenous changes in the market environment and analyzing the consequent welfare variation. The former simulation assumes a sharp price decrease in the imported good price. As expected, due to competitive pressures and consequent lower prices, consumer welfare goes up and producers’ profits go down. In turn, the second section simulates a regulatory action whose objective is to split up the existing monopoly owned by Bavaria S.A. After the break up, the company does not internalize the price decision of all domestic beers in the market, then prices go down and similar welfare effects take place. Finally, the last section discusses the construction of welfare-based price indices and the identification of intertemporal welfare variation.

iv

Table of Contents

List of Figures………………………………………………………………………… vi

List of Tables…………………………………………………………………………... vii

Acknowledgements……………………………………………………………………..

viii

Chapter 1 Introduction …………………………………………………………….. 1

Chapter 2 Estimating Markups from Plant-Level Data …...………………………. 5

2.1 Model..……………………………………………………………….…. 7

2.2 Data….………………….………………………………………………. 14

2.3 Estimation ……………….……………………………………………... 16

2.4 Robustness Checks …………………………………………………….. 20

2.5 Fixed Capital …………………………………………………………... 24

2.6 Final Remarks 29

References ......…………………………………………………………………..

30

Chapter 3 Uncovering Marginal Cost and Quality from Revenue and Cost Data ... 35

3.1 Traditional approaches ….……………………………………………… 36

3.2 Data …………………….………………………………………………. 39

3.3 Model ………………….……………………………………………….. 40

v

3.4 Aggregate Information …………………………………………….…….. 44

3.5 Market Idiosyncrasies and Results ………………………………………. 46

3.6 Final Remarks …………………………………………………….……... 49

References ………………………………………………………………………. 51

Chapter 4 Welfare Analysis ………………………………………………………... 57

4.1 Import Competition …………………………………………………….... 57

4.2 Monopoly Power ……………………………………………………….... 63

4.3 Measuring intertemporal variation in Welfare …………………………... 71

4.4 Final Remarks …………………………………………………………… 77

References ………………………………………………………………………. 79

Appendix A Uncovering Relevant Quantities from Revenue and Cost Data with Multi-Plant Ownership ………………………………………….

87

Appendix B Gibbs Sampler ………………………………………………………… 89

vi

List of Figures

3.1 MCMC Simulation for α (NLB model) …..……………………………… 54

3.2 MCMC Simulation for σ (NLB model) …..……………………………… 55

3.3 MCMC Simulation for α (SL model) ……………………………………. 56

4.1 Change in Consumer Welfare ……………………………………………. 59

4.2 Change in Producer Welfare ……………………………………………... 60

4.3 Change in Social Welfare ………………………………………………... 62

vii

List of Tables

2.1 Parameters Estimates ………………………………………………………… 32

2.2 Robustness Checks …………………………………………..………………. 33

2.3 Fixed Capital …………………………………………………………………. 34

3.1 Parameters Estimates ……………………………………………….....……… 48

4.1 Market shares and Price variation as a result of the monopoly break-up (NLB) ………………………………………………. 67

4.2 Welfare equivalent price reduction and the Price Index (SLB model) ………. 76

4.3 Market shares and Price variation as a result of the monopoly break-up and 5% marginal cost increase (NLB) ………… 80

4.4 Market shares and Price variation as a result of the monopoly break-up (SLB) ………………………………………………..

81

4.5 Market shares and Price variation as a result of the monopoly break-up (PC) ………………………………………………….

82

4.6 Market shares and Price variation as a result of the monopoly break-up (scenario 1 ) …………………………………………

83

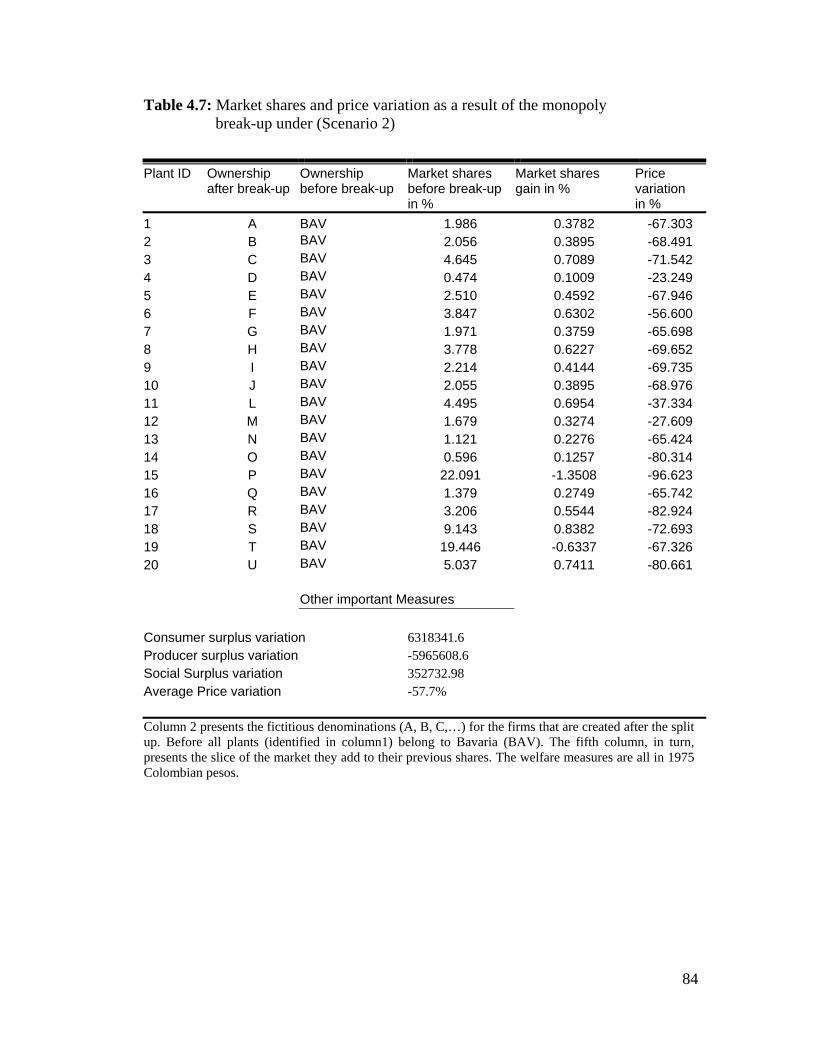

4.7 Market shares and Price variation as a result of the monopoly break-up (Scenario 2) ..………………………………………...

84

4.8 Welfare equivalent price reduction the Price Index (NLB model) …………... 85

4.9 Welfare equivalent price reduction the Price Index (PC model) …………….. 86

viii

Acknowledgements

First, I would like to thank my advisor Dr. James Tybout for his guidance

during the innumerous hours he dedicated to my work. I will always have him as

inspiration for my career as a Professor. My gratitude goes also to Dr. Roberts for his

always-insightful comments and to Dr. Esteban for her important suggestions.

I dedicate this work to my wife Cristiane, who gave up on so much to

accompany me on this endeavor, and to my son Victor who was born just a few

months ago. Without them, it would have been hard go through the hardships of a

Doctorate Program. In addition, I dedicate this thesis to my parents, who serve as an

inspiration for me and were always supportive of my decision to study abroad.

Finally, I could not forget to thank CAPES. The financial support provided by the

Brazilian agency has turned possible the dream to study in the US.

Chapter 1

Introduction

The main objective of this research is to discuss and extend the existing

literature that is concerned with the estimation of demand and supply parameters to

determine unobserved prices, quantities, quality and marginal costs at the firm-level

using data sets that report only revenue and cost figures. A common approach to

estimate these parameters and variables is given by the production function.

However, to be implemented it needs output data, which most plant-level data sets do

not report. Most micro data studies solve this problem by ignoring price

heterogeneity. Output is then obtained by simply deflating the revenue series by a

commonly available price index.

Only recently, through the works of Klette and Griliches (1996) and

Melitz (2000), researchers gave a closer look into this issue. The former article shows

that simple OLS estimates of internal returns to scale that ignored the ratio of firm-

specific price to the industry price index are asymptotically downward biased.

Instead, focusing on the productivity measure, but using a similar idea, Melitz finds

that the productivity index is biased and spuriously procyclical since the production

function residual captures not only the “true” productivity but also firm-specific price

movements.

1

In the second chapter, using the same framework, I shall investigate the

consequences of ignoring price heterogeneity on the markup estimates from the

production function in plant or firm–levels studies. I show that ignoring output price

heterogeneity yield markup estimates severely biased towards one regardless of

competitiveness levels. I set up an econometric model that assumes monopolistic

competition and a CES demand function in a differentiated product market that is

easy to estimate and allows for the use aggregate instruments to improve on the OLS

estimations. These virtues, however, come with a cost: strong assumptions on the

firm’s decision model. For this reason we set aside a separate section to analyze the

robustness of our conclusions once we relax this assumption, at least for the capital

input choice. Using data from Colombian plants at selected three-digit level industries

from the period of 1979 to 1987 I demonstrate that the differentiated product model

estimation yields markup estimates considerably higher than one, rejecting the

hypothesis of competitive markets in the selected Colombian industries.

One problem with this approach is that monopolistic competition may not

be a reasonable model for many industries. It assumes that firms are not big enough to

influence the aggregate market variables and therefore a price change by one firm has

an irrelevant effect on the demand of any other firm. This assumption says that each

product has no neighbor in the product space, which strongly restricts cross-effects

and strategic interaction between products (Tirole, 1988).

The discrete-choice based demand function with oligopolistic competition

relaxes some of the undesirable results of the monopolistic setup. Consumers choose

among N products given the product’s prices and characteristics. Producers, in turn,

2

set optimal prices in a Bertrand fashion. This allows for a richer model of cross-

effects patterns and interactions among firms. Berry, Levinsohn and Pakes (1996)

develop an econometric methodology to estimate such model using market level data

on prices and quantities.

Along the same lines, Katayma, Lu and Tybout (2003) use a nested logit

model to derive consumer and producer surplus to measure efficiency. Their work

(KLT) however differentiates from the others since the data set used there is not quite

as informative. Again, it assumes that only revenue and total costs are observed. Then

combining these data with demand and the quasi-supply relation they demonstrate

how to estimate the parameters of interest.

In the third chapter, I shall extend the KLT framework by including the

extra information provided by aggregate data. Although it may be difficult to obtain

detailed data on quantities at the plant level, the same is not true for aggregate

variables. For instance, in the beverage sector, the amount of beer1, in liters,

consumed in a given year is widely available for many countries. Aggregate

quantities also carry information on demand parameters and therefore may help in the

estimation process, especially in small data sets. I consider two different hypotheses

on the nature of this aggregate measure. The first one assumes that this information is

noisy, while the second assumes that this information is deterministic and therefore

error free. Each assumption yields a different estimation strategy with potentially

yield different parameter estimates.

With the preference parameters, qualities and marginal costs determined

according to the methodology developed in the third chapter, it is possible to 1 The data set used in this chapter covers the period form 1977 to 1990 in the Colombian beer industry.

3

construct consumer and producer welfare measures. In this way, the first two sections

of the third chapter present counterfactual experiments. They consist on assuming

exogenous changes in the market environment and analyzing the consequent welfare

variation. The former simulation assumes a sharp price decrease in the imported good

price. As expected, due to competitive pressures and consequent lower prices,

consumer welfare goes up and producers’ profits go down. In turn, the second section

simulates a regulatory action whose objective is to split up the existing monopoly

owned by Bavaria S.A. After the break up, the company does not internalize the price

decision of all domestic beers in the market, then prices go down and similar welfare

effects take place. Finally, the last section discusses the construction of welfare-based

price indices and the identification of intertemporal welfare variation.

4

Chapter 2

Estimating Markups from Plant-Level Data

Is a certain industry competitive? If not, what is the degree of market

power in this industry? Answering theses questions has always been a central concern

in industrial organization. One of the most important contributions in this research

subject was formulated by Hall (1998), who proposed an interesting framework

where markups, as well as returns scale1, can be estimated from a simple production

function.

Nonetheless, while there is a vast literature on the estimation of markups it

comes as a surprise that only a smaller number of publications have used plant or

firm-level data2. The advantages of utilizing more disaggregated data are twofold.

First, it avoids the aggregation bias inherently present in industry level panel data.

Second, it is more consistent with the underlying theoretical models where the

decision unit is a firm, not an industry.

However it poses an additional difficulty, often neglected, in the

estimation of production functions that is particular to the use firm-level data:

unobserved firm prices. Econometricians circumvent this problem by assuming a

homogeneous product market. In this case individual firm prices equal the observable

industry aggregate price index and the econometric model is estimated in a standard

way. 1 Actually Hall (1988) assumes constant returns to scale but his framework can be easily extended to include internal returns to scale as a free parameter (Hall,1990). 2Three examples are Klette (1999),Harrison (1994) and Levinsohn (1993).

5

This chapter investigates the consequences of relaxing this assumption on

the markup estimates. It shows that ignoring price heterogeneity yield markup

estimates severely biased towards one regardless of competitiveness levels and that

an econometric model that embodies firm specific prices implies much higher

markups.

To set up the econometric model I depart from the simplifying and

potentially problematic assumption of a homogeneous product by assuming

monopolistic competition in a differentiated product industry. In this context this

model is a natural extension to previous studies that used a similar framework but

emphasized different objects. Klette and Griliches (1996) argued that simple OLS

estimates of internal returns to scale that ignored the ratio of firm-specific price to the

industry price index are asymptotically downward biased. They also assumed

monopolistic competition and identified the internal returns scale and the elasticity of

substitution in a price adjusted revenue production function. Focusing on the

productivity measure and using the same framework Melitz (2000) finds that the

productivity index is biased and spuriously procyclical.

Building on KGM3 I develop a technique for estimating markups that

assumes imperfect competition, is easy to estimate and allows for the use of aggregate

instruments to improve on the OLS estimations. These virtues, however, comes at a

cost: strong assumptions on the firm’s decision model. For this reason a separate

section is set aside to analyze the robustness of the conclusions once these

assumptions are relaxed, at least for the capital input.

3 The model developed by Klette and Griliches (1996) and Melitz (2000).

6

This chapter uses data on Colombian plants at the three-digit level

classification according to ISIC from the period of 1979 to 1987 and estimate

markups at selected industries. In the next section, I derive a simple model that

highlights the consequences of omitting output price variation. The following section

introduces measurement errors and the presence of externalities as a potential source

of misleading results for the markups. Finally, this chapter devotes a separate section

to evaluate the sensitivity of our conclusions once the strong assumption on the input

decision process mentioned above is relaxed.

2.1 Model

I begin by assuming monopolistic competition in industry j where firm i

faces a demand function given by

(2.1) t

t

t

itit P

RPP

Qσ−

⎟⎟⎠

⎞⎜⎜⎝

⎛=

Where Rt is the total revenue of industry j, Pt is an aggregate price index

and σ (σ>1) is the demand elasticity, which is also the elasticity of substitution. It is

straightforward to show that the markup is constant across firms and equal to

)1/( −σσ . This formulation is intuitively appealing. As goods become more

substitutable (σ goes to infinity) the markup approaches the competitive outcome.

In this economy gross output Qit is generated with capital X1, labor X2 and

materials X3 adjusted by a term W that indexes the productivity levels and a random

7

error N. Therefore, defining ),,(),,( 321ititititititit MLKXXXX ≡≡

rwe obtain the

production function below

(2.2) ),,( itititit NWXFQr

=

where F is homogeneous of degree γ in capital, labor and materials, and

of degree one in W and N. Note that the assumption of linear homogeneity in W is

made without loss of generality since this is just an index.

Log differentiating (2.2), defining the lowercases as the log of the

variables defined above and dropping the time index above yields

(2.3) dNFdwFdxQXF

dq Nwj

ii

jij

ji ++= ∑

It’s also assumed that firm's dynamic optimization problem can be well

approximated by successive and independent static decision problems and that factor

markets are competitive. Then, with the demand equation (2.1) firm’s input choice

problem imposes the following equality at each period t

(2.4) ijji rFP =−σ

σ 1

Pi, rj, and Fj represent respectively firm i’s output price, the price of the j-

th factor and the derivative of F with respect to this factor.

8

Now, it is possible to derive the simple expression for the inputs

coefficients since

(2.5) jii

jij

QXF

µα=

Where µ is the markup and αij is the revenue share of input j. Substituting

(2.5) into (2.3) yields

(2.6) iij

iji dndwdxdq ++= ∑αµ

This equation, first derived by Hall (1988) implies that the output

elasticity with respect to the j-th input is just this input’s revenue share adjusted by a

measure of firm's market power. It contains the Solow residual formulation as a

particular case. Indeed, in a competitive environment the Total Factor Productivity

reduces to a simple deterministic relation . 33

22

11 dxdxdxdqdndw ααα −−−=+

Equation (2.6) can be rewritten to express output growth as a function of

returns to scale and a cost-share weighted bundle of input growth (Hall,1990) as

follows

(2.7) iij

jiji dndwdxcdq ++= ∑γ

The symbols γ and c represent returns to scale and cost share respectively.

To derive the equation above note that the definition of returns to scale implies

(2.8) ∑∑ ==j

jj

jj

QXF

αµγ

9

and that cost shares and revenue shares values are constrained by the

following relation jii

ij c

QPTC

=α (TCi represents firm’s i total cost). From this equation

and (2.8) it easy to show that (2.6) implies (2.7). Obviously, it is possible to work

backwards and obtain (2.7) from (2.6).

Hall’s formulation - equations (2.6) and (2.7) - became a widely used

technique. It allowed researchers, using data sets at various aggregation levels, to

obtain output elasticities, returns to scale, productivity indexes, as well as a measure

of market power (µ) from simple production function estimations. However, in most

data sets, firms report revenue, not absolute quantities nor prices. A usual way to

proxy output is to divide firms’ revenues by an industry price index, common to all

firms.

This approach is justified by the assumption of a homogeneous product

market. In this case the price index coincides with firm’s individual prices and the

proxy is a perfect measure of each firm production level. However ignoring

fluctuations of firm-specific prices relative to the price index in a differentiated

product industry can yield severe econometric problems (Klette and Griliches ,1996,

and Melitz,2000). Below I shall develop a model that takes this potential distortion

into account.

10

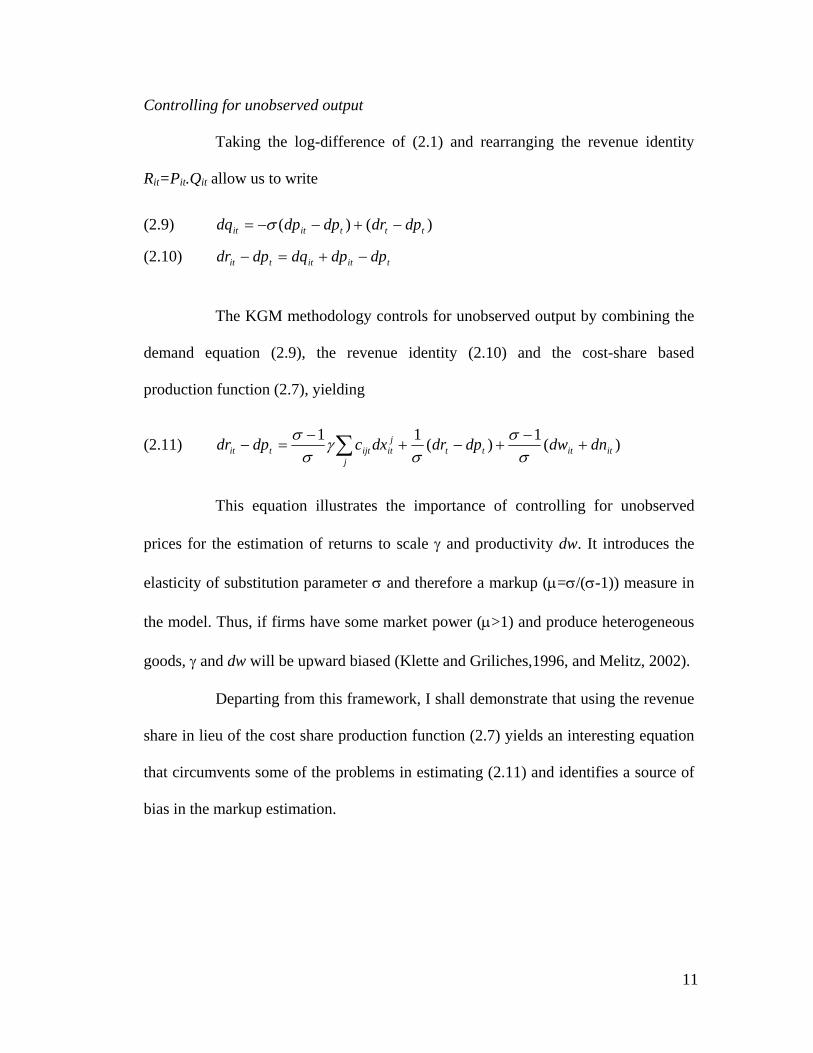

Controlling for unobserved output

Taking the log-difference of (2.1) and rearranging the revenue identity

Rit=Pit.Qit allow us to write

(2.9) )()( tttitit dpdrdpdpdq −+−−= σ

(2.10) titittit dpdpdqdpdr −+=−

The KGM methodology controls for unobserved output by combining the

demand equation (2.9), the revenue identity (2.10) and the cost-share based

production function (2.7), yielding

(2.11) )(1)(11itittt

j

jitijttit dndwdpdrdxcdpdr +

−+−+

−=− ∑ σ

σσ

γσ

σ

This equation illustrates the importance of controlling for unobserved

prices for the estimation of returns to scale γ and productivity dw. It introduces the

elasticity of substitution parameter σ and therefore a markup (µ=σ/(σ-1)) measure in

the model. Thus, if firms have some market power (µ>1) and produce heterogeneous

goods, γ and dw will be upward biased (Klette and Griliches,1996, and Melitz, 2002).

Departing from this framework, I shall demonstrate that using the revenue

share in lieu of the cost share production function (2.7) yields an interesting equation

that circumvents some of the problems in estimating (2.11) and identifies a source of

bias in the markup estimation.

11

Indeed, combining (2.6), instead of (2.7), with (2.9) and (2.10) results in

(2.12) )(1)(11itittt

jitijttit dndwdpdrdxdpdr +

−+−+

−=− ∑ σ

σσ

αµσ

σ

Note that the parameter on the input bundle cancels out, such that:

(2.13) )(1)][(1itittt

j

jitijttit dndwdpdrdxdpdr ++−=−− ∑ µσ

α

The estimation of (2.13) has several advantages over the KGM. First,

since the factor inputs variables appear on the LHS we do not have to worry about

their potential correlation with the productivity term. Therefore, even the OLS

estimator is consistent. Second, as discussed in further detail below, even if there is

still some correlation left between the error term (dwit +dnit) and the remaining

regressor (rt-pt), GMM estimation can be applied with traditional aggregate

instruments, instead of plant-levels ones which are usually difficult to find.

This equation also contains the Solow residual as a particular case. If the

market is in perfect competition, i.e the coefficient on (drt –dpt) is zero, eq. (2.13) is

just the computation rule for the Solow residual. Furthermore, it indicates that the

common finding that productivity is procyclical should be reviewed. It suggests that

the degree of correlation between the TFP growth and the business cycle should at

least be reduced since the residual, dependent variable minus the “fitted” input levels,

represents a measure of the TFP growth plus a term that appears after controlling for

the heterogeneity in prices and that includes an aggregate measure of the industry

output (drt–dpt) as a regressor.

12

Roeger (1995) also develops a strategy to estimate production function

parameters that avoids the necessity of disaggregated instruments4 and that control for

unobserved nominal prices. The basic idea is that both the primal- the one discussed

above- and the dual Solow residual5 contain the same unobservable productivity term

that cancels out if one residual is subtracted from the other. However, his

methodology only works under the hypothesis of constant returns to scale. Omitting

variations in this parameter can cause an upward (downward) bias if returns to scale

are decreasing (increasing) as shown by Basu and Fernald (1997).

Ignoring product differentiation

To estimate markups in a homogenous product industry it suffices to

deflate revenue by a common industry price to proxy quantity, yielding the following

equation:

(2.14) ititj

jitijttit dndwdxdpdr ++=− ∑αµ

By estimating variations of the equation above several plant–level data

studies have either supported competitive or oligopolistic markets with low markups,

usually close to one. For example, Klette (1999) using establishment data from the

manufacturing sector in Norway finds markups ranging from 0.972 to1.088. Although

his estimates are statistically different from one they are incredibly close to this

number. Using panel data of firms from cote d’ivoire Harrison (1993) presents similar

results. She finds supporting evidence of perfect competition for most of the sectors

4 See Konings and Vandenbussche(2004) for a firm level application of Roegers’s methodology. 5 The dual is obtained from the relation between marginal costs, factor inputs and productivity.

13

and low market power for the remaining ones. Below I argue that those results are

driven by a misspecification of the production function.

If we believe that (2.13) is the true data generating process, those

estimates are not so surprising at all. By comparing (2.13) to (2.14) and defining µ) as

a consistent estimator of µ as it appears in (2.14) it easy to show that plim µ) =1. That

is, the markup measure should be one regardless of competitive levels, or at least

evolve around one after considering different sources of biases from standard

econometric techniques.

2.2 Data

The data set analyzed in this chapter was obtained from the census of

Colombian Manufacturing plants, collected by the Departamento Administrativo

Nacional de Estadistica (DANE) and was cleaned by Roberts (1996). It covers all

plants in the manufacturing sector for 1980-1987 period and plants with ten or more

employees after 1982. In this study we consider six different sectors at the three digit

level: 311 (Food Products), 322 (Clothing and Apparel), 381 (Metal Products), 342

(Printing and Publishing), 383 (Electronic Machinery and Equipment) and 384

(Transportation Equipment).

Input data are available for book value of capital, number of employees

and book value of intermediate inputs. Intermediate inputs include material, fuels and

energy that are bundled together to form a unique measure M entering the equations

defined in the last section. The value of gross output is reported and accordingly

14

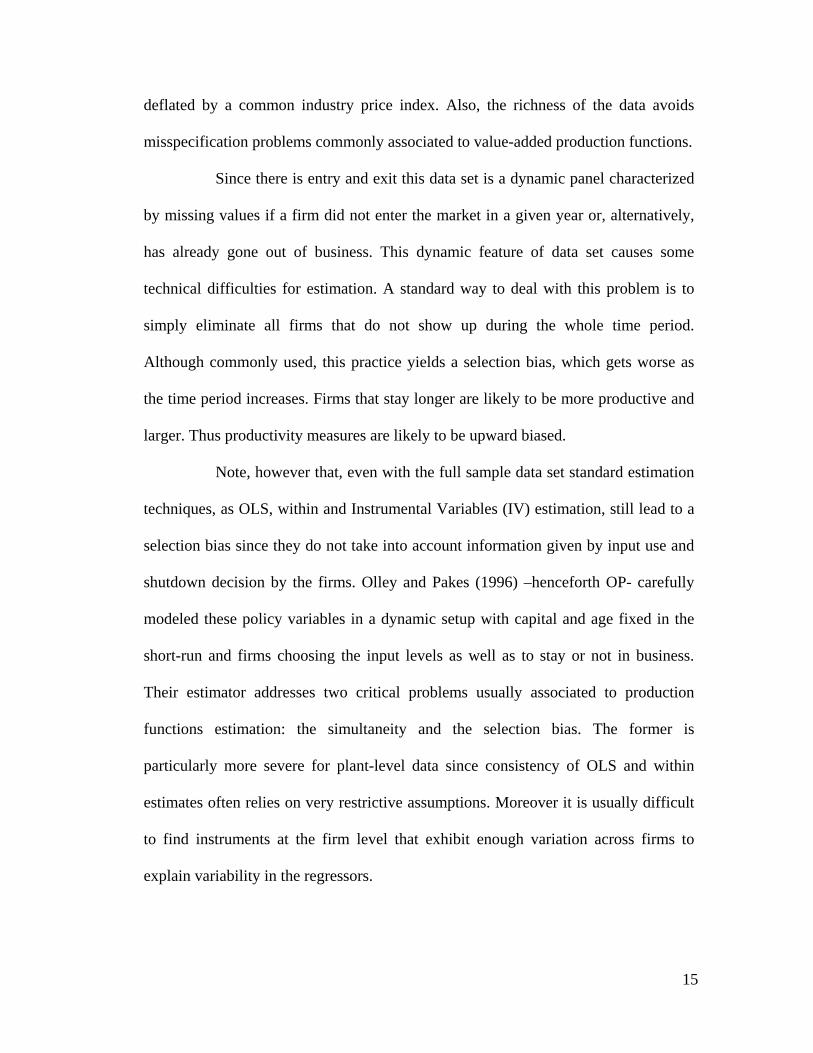

deflated by a common industry price index. Also, the richness of the data avoids

misspecification problems commonly associated to value-added production functions.

Since there is entry and exit this data set is a dynamic panel characterized

by missing values if a firm did not enter the market in a given year or, alternatively,

has already gone out of business. This dynamic feature of data set causes some

technical difficulties for estimation. A standard way to deal with this problem is to

simply eliminate all firms that do not show up during the whole time period.

Although commonly used, this practice yields a selection bias, which gets worse as

the time period increases. Firms that stay longer are likely to be more productive and

larger. Thus productivity measures are likely to be upward biased.

Note, however that, even with the full sample data set standard estimation

techniques, as OLS, within and Instrumental Variables (IV) estimation, still lead to a

selection bias since they do not take into account information given by input use and

shutdown decision by the firms. Olley and Pakes (1996) –henceforth OP- carefully

modeled these policy variables in a dynamic setup with capital and age fixed in the

short-run and firms choosing the input levels as well as to stay or not in business.

Their estimator addresses two critical problems usually associated to production

functions estimation: the simultaneity and the selection bias. The former is

particularly more severe for plant-level data since consistency of OLS and within

estimates often relies on very restrictive assumptions. Moreover it is usually difficult

to find instruments at the firm level that exhibit enough variation across firms to

explain variability in the regressors.

15

The OP technique nevertheless requires elimination of information on

plants with zero investments. This usually reduces considerably the number of

observations. In contrast, (2.13) presents a particular form that permits the use of

aggregate instruments. Also, the assumptions used to validate OLS estimates are not

as restrictive as commonly argued. And, as far as the selection bias is concerned, I try

to attenuate its magnitude by using the full sample instead of a balanced panel6.

2.3 Estimation

This section presents the markup estimates according to the misspecified

model (2.14) and the true model (2.13) for selected 3-digit industries in the

Colombian manufacturing sector. It should be noted that I randomly selected the

these industries for this study and that I paid no attention to the idiosyncrasies of

neither of them. This is justified here on the basis that the objective in this chapter is

to illustrate the methodological problems of ignoring price heterogeneity rather than

providing a detailed study of the idiosyncrasies of each industry. However, an

application of this methodology to study a particular industry in the Colombia

manufacturing sector would be a natural extension of this work.

6 Olley and Pakes (1996) results do not show much variation between their estimator and the traditional estimation using the full-sample.

16

Misspecified Model Estimation

As discussed above, ignoring price heterogeneity and deflating output by

an industry price index, which amounts to estimating (2.14), yields markup estimates

whose asymptotic value should be one regardless of competitive levels.

However, OLS does not yield consistent estimators of the true value of µ

(µ0=1) in (2.14). Two sources of upward bias can be identified. The former arises

from the potential positive correlation between input choices and productivity levels.

The latter originates from a traditional omitted variable problem caused by the

omission of the term (1/σ)(drt–dpt) in the misspecified equation (2.14). Since the

firm’s input choices are procyclical, i.e., positively correlated with aggregate activity,

it easy to show that this results in an overestimation of the true value v0=1. Results

show nonetheless that OLS are quite informative.

As presented in the first column of Table 2.1 the magnitudes of the

markups are close to one although statistically different from unity for all industries

except for 342. Thus, even though we do not control for the sources of upward biases,

the basic prediction of equation (2.12) that OLS estimates of the markup based on

(2.14) should be approximately one still comes through. If we were to have controlled

for these biases the coefficient would presumably be lower and even less plausible as

markups.

True model estimation

Since the input data are placed on the LHS of true model (2.13), I do not

have to worry about the simultaneity bias. Thus simple OLS regressions can be used

17

without strong assumptions on the co-movements of productivity and input use.

Nevertheless we have to assume that aggregate output, at the industry level, is

uncorrelated with productivity. The validity of this assumption depends upon the

extent that we believe that the productivity term dwit is a pure idiosyncratic shock or

not. If so, it is reasonable to assume that firm-specific shocks do not affect total

output. In a monopolistic competition market with many firms, an increase in the

quantity produced by a firm due to an idiosyncratic productivity improvement has

little effect on the aggregate measure of goods supplied in this market.

Two issues deserve further comments since they cast some doubt on the

OLS estimates of (2.13). First, the argument for using OLS is somewhat weakened if

we consider industry-wide productivity shocks. For instance, a new production

technique developed by a University and publicaly available in a scientific journal

affects every firm equally if we believe that firms have the same capabilities of

absorbing new technologies. Hence, movements in aggregate output are positively

related to movements in the composite shock (firm specific plus industry wide

productivity shock). Also macroeconomic shocks and trade liberalization policies

may equally affect every firm in the industry. Second, despite the fact that our

measure of productivity dw eliminates spurious sources of procyclical movements,

reasonable arguments may support the case for a positive correlation between the TFP

and aggregate fluctuations. One of them relies on the efficiency gains. Firms with

increasing returns to scale may exhibit efficiency gains by expanding supply.

Thus, the validity of OLS estimates relies on the intensity that the sources

of correlation between the regressor (drt –dpt) and the error term are present. If

18

aggregate shocks do not play an important role in the industries in the period

considered here and if firm exhibits relatively low returns to scale there is no reason

to try alternative and also problematic estimation techniques

A common way to control for the presence of industry-wide shocks is to

include time dummies in the econometric model. However, colinearity concerns may

undermine this approach since (2.13) already contains a variable whose only variation

is through time (drt-dpt). Thus, instead of testing for the presence of aggregate shocks

(or high internal returns to scale) I will test the robustness of the OLS results by

comparing them to the GMM estimates of (2.13) and performing a Hausman test to

verify the equivalence between the two techniques. Since the factor input coefficients

do not need to be estimated, the only regressor remaining in this equation is drt-dpt,

which is simply a proxy for the aggregate industry output. Hence, its coefficient (1/σ)

can be estimated by GMM with well-established instruments at the industry level7.

Table 2.1 shows the results for the OLS and GMM estimation of 1/σ. The

instruments set is composed of current and lagged growth rate of international oil

prices deflated by an index of imported goods. The resulting overidentified system

permits testing the validity of the instruments. Hansen (1982) showed that the J

statistic, defined there as the minimized value of the GMM objective function times

the number of observations, converges asymptotically to a chi-square distribution

with degrees of freedom equal to the number of moment restriction minus the number

of regressors under the null hypothesis that the moments are correct.

7 These are classical instruments in the aggregate productivity literature. They are correlated with the aggregate activity but not with productivity.

19

Note that a significant 1/σ estimate implies imperfect competition (σ is

finite) whereas a insignificant estimate supports the alternative hypothesis of perfect

competition .The implied markups (σ/σ-1) reported in the Table 2.1 show firms with

high market power, considerably above one in most of the sectors contrasting with the

markup estimates of (2.14) that report estimates close to one. This is a strong result.

Controlling for price heterogeneity yields markups much higher than the ones

implied by the misspecified model (2.14), which already contain upward biases.

The OLS estimates proved to be robust to the alternative estimation

technique since GMM estimates show similar point estimates for 1/σ. However due

to larger standard errors, data for industry 381 cannot reject the hypothesis of

competitive market. The model also passes the overidentification test for all industries

but one (383) confirming the finding that a negative 1/σ is inconsistent with the

assumptions imposed so far. A negative σ implies an upward sloping demand

schedule which is clearly inconsistent with the underlying monopolistic competition

demand function. The Hausman test confirms that OLS and GMM are statistically

equivalent estimation procedures. This result is consistent with the hypothesis that the

aggregate industry output is not significantly correlated with the error term.

2.4 Robustness checks

Measurement error

In many cases, the data collected for the factor inputs reflect installed

capacity, not the real level of factor utilization. In a recession, managers would rather

20

reduce the utilization level of the existing machines than sell some of them. Similarly,

they would rather reduce labor hours than lay off workers (labor hoard). Thus, using

the reported data directly in the production function estimation is potentially

misleading and yields a classical measurement error problem.

Rewriting (2.13) with an additional term dg, representing a measurement

error in the input levels, and denoting Y* as the LHS of (2.13) imply

(2.15) dwdgdpdrY tt }1{)(* 21 σσββ −

++−=

Now, defining as the OLS estimator of 1̂β 1β (β1=1/σ), and ignoring dg in

the OLS regression of the equation above yields the following asymptotic result

(2.16) 111 )(),cov(ˆlim βββ

tt

tt

dpdrVdpdrdg

p−−

+=

Thus, if changes in factor utilization are positively correlated with changes

in total industry output overestimates the parameter of interest 1/σ. Therefore β1̂β 1

may be capturing variations of factor utilization in addition to the measure of demand

elasticity. In the most extreme case, a significant may still show up even if

markets are perfectly competitive. Thus, not controlling for the measurement error

may be misleading us to conclude that markups are well above one and that markets

are in imperfect competition.

1̂β

To approximate the unmeasured term I use total wages expenditure per

employee. The choice of this proxy is justified by the assumption that workers are

rewarded based on variations in effort levels and that capital and labor utilization

21

rates are proportional 8. Results in Table 2.2 show that magnitudes do not change

significantly once the measurement error proxy is introduced in the model. This result

should be taken with caution though, since wages are expected to be endogenous.

Externalities

Theoretical models in macroeconomics have emphasized the importance

of external returns to predict and explain growth and business cycles trajectories. In

the growth literature for example the presence of externalities measured by aggregate

output or total employment help to explain why countries may exhibit long-run

growth even in the presence of constant or decreasing internal returns to scale. It is

based on the premise that human capital is a public good and therefore individual

firms should benefit from its aggregate level9. Also, Howitt (1985) considers the

reduction in the costs of transactions as the level of activity increases. Below a brief

summary of the findings in the empirical literature is presented.

Caballero and Lyons (1990) used European data at the 3-digit level (ISIC)

to measure economy-wide externalities. They approximated the externality effect by

aggregated output and found strong evidence of external returns. Following the same

framework, but using highly disaggregated data, Krizan (1998) and Lindsdtrom

(1999) found similar results. On the other hand Basu and Fernald (1995) using U.S

manufacturing data found no evidence of gross output related externalities. They

8 See Lindstrom (1997) for further details. Also I am implicitly assuming that materials are costlessly adjusted and therefore do not preset measurement errors. 9 See Lucas(1988).

22

argued that value-added output data fail to account properly for the intermediate

inputs leading to spurious externalities measures due to misspecification.

In this section I consider the consequences of neglecting external effects in

(2.13) on the markup estimates. I begin by defining the externality proxy as lagged

aggregate activity (rt-1-pt-1). More precisely it is assumed that individual firms should

benefit from past levels of industry–wide production10. However due to colinearity

problems only one lag is considered in the estimation procedure. This specification is

motivated by the idea that external effects do not have an immediate impact on firms’

efficiency. Instead they take one period to be effective. In this sense, the external

effect could be capturing learning-by-doing and human capital spillovers if we are

willing to assume that lagged aggregate production is a reasonable approximation to

both variables.

In order to check the robustness of the markup measures to the inclusion

of the externality effect in the revenue production function the following equation is

estimated

(2.17) dwdpdrdpdrY tttt }1{)()(* 1121 σσββ −

+−+−= −−

where all the variables are defined as in (2.16). Similarly to the measurement error

case neglecting (rt-1–pt-1) yields an upward bias in the estimation of 1/σ since the

aggregate deflated revenues series (rt–pt) are expected to be serially correlated.

Indeed, the results shown in the last column of Table 2.2 support the claim

of an upward bias. Except for 322 and 342, the 1/σ estimates are smaller than those

10 Cooper and Johri (1997) used lagged aggregate activity to study dynamic complementarities.

23

obtained by the OLS estimation of (2.13). However the bias is not severe enough to

change the significance of the estimates or to affect their magnitude considerably.

2.5 Fixed Capital

Although the econometric model represented by (2.13) is consistent with

the results presented in the previous sections it relies heavily on the assumption that

firms choose their inputs levels in a sequence of static problems and that factor

markets are competitive. These assumptions are certainly more problematic for

capital. In order to decide how much to invest in a given period, agents take into

account past levels of capital. Indeed, dynamic models of firm’s decision problems

have emphasized capital as a state variable, which enters as a parameter in the choice

of investment, employment, and materials levels.

Hence, those assumptions, crucial to derive (2.13), may potentially yield

misleading conclusions. Yet, as I shall argue below, the basic predictions of last

section remain and the data also supports the same claims as before when weaker

assumptions on the capital input decision are taken into consideration.

Model

Now, I assume that capital is fixed in the short-run. Thus, (2.5) no longer

holds for this input. Hence, (2.13) is no longer valid. Obviously, its main virtues, a

better argument for OLS and the use of industry-level instruments cannot be claimed

in this new set up.

24

With fixed capital and assuming that (2.5) holds for the remaining inputs

the log differentiated production function can be written as

(2.18) iij

ij

iijii dndwdxdxdxdq ++−+= ∑= 3,2

11 )(αµγ

This equation, (2.9) and (2.10) form a system that yields the following

revenue production function

(2.19) ititttitj

itj

itijttit dndwdpdrdxdxdxdpdr ++−+−

=−−− ∑= µσ

γσ

σα 1][1)(1)( 1

3,2

1

Specification (2.18) is the most commonly used in this literature. Not only

it relaxes the strong assumptions on capital but it also permits the estimation of

internal returns as well as markups. However the assumption of homogenous product

still leads to misleading estimates of markups.

Using firm’s revenue deflated by a common industry price to control for

the unobserved firm-specific output results in the following equation:

(2.20) itititj

itijtmittit dndwdxdxdxdpdr ++−+=− ∑ )( 11 αµγ

Again, if we believe that (2.9) is the true model it becomes clear that µ) ,

now the estimator of µ as it appears in (2.20), converges in probability to one

regardless of competition levels. Note that (2.19) is similar to (2.13). The only

fundamental difference is that coefficient on capital (dx1) cannot be placed on the

LHS of the estimating equation and therefore aggregate instruments are no longer

sufficient to ensure consistency. Furthermore, the arguments in favor of OLS are

somewhat weakened since dx1 appears as a regressor in (2.19) and is expected to be

correlated with the error term.

25

In the absence of good disaggregate instruments researchers started

searching for alternative methods to deal with the simultaneity problem. Leading this

recent literature, the OP method proposes an innovative technique that avoids the

difficult task of searching for instruments. This method can be briefly summarized as

follows. Using the information that investment levels are a deterministic function of

productivity levels and by inverting this relationship, it is possible to uncover the

unobservable productivity term as a non-parametric function of investment and the

state variable capital. In this way, the only unobservable error term left in the

estimation is not expected to be correlated with the regressors.

Another way to deal with this problem was developed by Levinhson and

Petrin (2000)-LP hereafter. They argue that investment may only respond to the “non-

forecastable” part of the productivity term since the capital input may have already

adjusted to its “forecastable” part. Therefore some correlation would still remain

between the regressors and the error term.

By using intermediate inputs to proxy the productivity term they are able

to develop a simpler methodology that improves on the OP methodology since

intermediate inputs respond to the whole productivity shock. It also avoids a major

drawback of the OP method, which is the necessity to drop information on industries

that report zero investment in a given period.

The availability of intermediate input in our data set and the arguments

discussed above make the LP our natural choice for estimating equation (2.19). It is

worth pointing out however two limitations concerning the LP method. First, it does

not control for the selection bias. That is, unlike OP, it does not use information on

26

firms shut down decision rule in the estimation process. Second, it assumes

competitive and homogeneous product markets to validate the use of the intermediate

output as proxy for the unobservable term.

While the effects of former limitation can be partially attenuated by the

use of the full-sample instead of a balanced panel, the effects of the latter requires a

more careful look into the technique itself, for our model assumes a differentiated

product market, not a homogeneous one.

The basic result that supports LP is the monotonic relation between

productivity and the optimal intermediate input level. In a competitive framework it is

straightforward to prove that. With fixed output and input prices an increase in

productivity implies a higher intermediate input marginal product at the existing input

levels. Therefore firms will decide to produce more output so that marginal product

falls back to equal the intermediate input price. Therefore as output goes up demand

for inputs also increases.

In an oligopolistic market this monotonic property may not hold anymore.

The marginal product still follows the same qualitative movements as before, but now

firms realize that prices decrease as output goes up. Thus, the net effect of a supply

expansion will ultimately depend on the elasticity of demand. It is possible to set up a

scenario where one firm facing higher demand elasticity actually reduces output

whereas another firm facing less responsive prices increases production levels. In a

monopolistic competitive environment, however, the proof of the monotonic

condition is very similar to the one presented in Levinsohn and Petrin (2000) and,

therefore, will be omitted here.

27

From the monotonic property we can write wit =w(X1,X3). Expressing this

equality in differences and dropping the firm specific and time subscripts yields

dw=dw(x1,dx1,x3,dx3). Following Olley and Pakes11 (1996) a third order series

approximation to this function is used12. Plugging it as a regressor in (2.19) implies

(2.21) ititititititttitit dndxxdxxdwdpdrdxY ++−+−

= ),,,(][1)(1 33111

σγ

σσ

Where ∑ −−−=

jit

jitijttitit dxdxdpdrY )( 1α . Since the observable variables

x1,dx1,x3,dx3 control for the productivity term, 1/σ can be consistently estimated by

OLS. If we were interested in pinning down the coefficient on dx1 the LP technique

becomes more involved since it is not identified in the equation above.

Again, as shown in Table 2.3 the estimates are not greatly affected once

the hypothesis of flexible capital is relaxed. The only exception is the 384 sector13,

which shows 1/σ estimate (0.069) contrasting with the OLS estimate (0.163) of

equation 2.13. For the other sectors the implied markups are considerably above one,

providing further evidence that the estimation of the misspecified production function

yields misleading assessments about competition levels.

11 OP also used a non-parametric approach 12 A forth order approximation was also used but the results did not vary by much. 13 More information on this sector would be necessary to interpret this result.

28

2.6 Final Remarks

This chapter shows that neglecting output price heterogeneity in plant or

firm level studies can be misleading, yielding spurious markup estimates. Assuming a

differentiated product market, a competitive factor market and strong assumptions on

firms’ input level decisions yields an econometric model that demonstrates that a

misspecified version of Hall’s equation implies markups equal to one regardless of

the market environment. Furthermore, this model avoids the search for good

disaggregated instruments, usually difficult to find, and can be consistently estimated

by GMM and even OLS. These consistent estimates, in turn, show markups much

higher than one.

I also perform robustness checks by controlling for alternative

explanations that could be driving our finding of a significant coefficient on the

output aggregate measure (measurement errors and externalities). Robust estimates of

1/σ are found. Its statistical significance and magnitude present very little change

compared to the previous estimates.

In the latter part of the chapter I recognize that those nice features, the use

of aggregate instruments and the validation of the OLS estimation, come at the cost of

imposing a restrictive assumptions on the model. Yet, relaxing the most disputable

assumption imposed in the first part of the chapter (flexible capital) does not change

the results significantly.

29

References

Aitken, B. and Harrison, A. (1999), “Do Domestic Firms Benefit from Foreign Direct Investment? Evidence from Panel Data,” American Economic Review, 89(3), pp. 605-618.

Basu, S. and Fernald, J. (1997). “Returns to Scale in U.S production: Estimates and

Implications” Journal of Political Economy 105,249-283. Bartelsman, J., Caballero, R. (1991), “ Short and Long Run externalities”, NBER

Working Paper No. 3810. Caballero, R. and Lyons, R. .(1991). “Internal Versus External Economies in

European Industry.” European Economic Review 34,805-26. Cooper, R. and Johri, A. (1997) “Dynamic Complementarities: A Quantitative

Analysis” Journal of Monetary Economics 40, pp. 97-119. Griliches, Z. (1957), “ Specification Bias in Estimates of Production Functions”,

Journal of Farm Economics, 39, pp 8-20. Griliches, Z. and Mairesse, J. (1995) “Production Functions: the Search for

Identification”, NBER Working Paper No. 5067. Hall, R.(1988). “The Relation Between Price and Marginal Cost in U.S. Industry”

Journal of Political Economy 96. Hall, R. (1990). “ Invariance Properties of Solow’s Productivity Residual”, In P.

Diamond (ed.), Growth, Productivity, Unemployment, MIT Press, Cambridge, MA.

Harrison, A. (1994) “Productivity, Imperfect Competition and Trade Reform: Theory and Evidence”. Journal of International Economics 36, 53-73.

Klette, T.J. (1999): “Market Power, Scale Economies and Productivity: Estimates

from a Panel of Establishment Data” Journal of Industrial Economics, 47, pp. 451-76.

Klette, T. and Griliches, Z. (1996), “The Inconsistency of Common Scale Estimators

When Output Prices Are Unobserved and Endogenous,” Journal of Applied Econometrics, 11(4), pp. 343-61.

Krizan, C. J.(1995). “External Economies of Scale In Chile, Mexico and Morrocco:

Evidence from Plant-level Data”. Georgetown University, Washington, D.C.

30

31

Konings and Vandenbussche(2004). “Antidumping Protection and Markups of Domestic firms: Evidence from Firm-Level data”. LICOS Discussion Paper No.141.

Levinsohn, J.(1993). “Testing the Imports-as-Market-Discipline Hypothesis”. Journal

of International Economics 35,1-22. Levinsohn, J. and Petrin, A. (2000), “Estimating Production Functions Using Inputs

to Control for Unobservables” NBER Working Paper No. 7819. Lindstrom, T. (1997).“External Economies at the Firm Level: Evidence from Swedish

Manufacturing” Mimeo. Lucas, R. (1988) “ On the mechanics of economic development”. Journal of

Monetary Economics, 22, pp. 3-42. Melitz M. J.(2000) “Estimating Firm-Level Productivity in Differentiated Product

Industries”. Mimeo. Mundlak, Y. and Hoch, I. (1965) “ Consequances of alternative Specifications of

Cobb-Douglas production functions”, Econometrica,33, pp. 814-828.

Olley, S. and Pakes, A. (1996), “The Dynamics of Productivity in the Telecommunications Equipment Industry,” Econometrica, 64(6), pp. 1263-1297.

Roberts, Mark (1996). “Colombia, 1977-85: Producer Turnover,Margins, and Trade

Exposure”. In Mark Roberts and James Tybout, editors, Industrial Evolution in Developing countries. New York: Oxford University Press.

Roeger, W. (1995) “Can imperfect Competition Explain the Difference between

Primal and Dual Productivity Measures? Estimates from US Manufacturing”. Journal of Political Economy, 103(21).

Tirole, J. (1988), The Theory of Industrial Organization, MIT Press, Cambridge, MA.

Tybout, J. (forthcoming) “Plant and Firm-level evidence on the ‘New’ Trade

Theories” in James Harrigan (ed.) Handbook of International Trade, Oxford: Basil-Blackwell.

Table 2.1: Parameters Estimates 14

Method OLS

OLS

GMM15 Hausman test16

Specification Equation (2.14 ) Equation (2.13 ) Equation (2.13 ) v estimates 1/σ Estimates Implied

markups 1/σ Estimates Jstatistic Implied

markups

311 0.975(0.0078)

0.380 (0.0277)

1.61

0.415 (0.1407)

1.723 1.71 0.064

322 1.065(0.01060)

0.392 (0.0325)

1.63

0.454 (0.1402)

0.889

1.81 0.203

381

1.052 (0.0124)

0.330 (0.0374)

1.49

0.300 (0.2202)

0.606 1.43

0.018

342 0.964(0.0204)

0.413 (0.0416)

1.72 0.447(0.1620)

3.871

1.78 0.048

383

1.036 (0.0212)

-0.244 (0.0681)

inconsistent -0.266(0.2925)

7.469 inconsistent -

384

1.065 (0.0205)

0.163 (0.0328)

1.20

0.220 (0.1285)

0.615 1.29

0.206

14 Standard errors in parentheses. 15 GMM is performed with the following instruments: current and lagged growth of the international oil price and a constant.. χ(1)=5.02 is the critical value at 5% significance level. 16 This column presnts the results of a Hausman Test between OLS and GMM estimation of (1.9). χ(1)=5.02 is the critical value at 5% siginificance level.

32

Table 2.2: Robustness Checks

Method OLS

OLS

Specification Equation (2.15 ) Equation (2.17 ) β1 Estimates β1 estimates

311

0.317(0.0284)

0.369 (0.0373)

322 0.148(0.0337)

0.583 (0.0412)

381

0.385 (0.0373)

0.334 (0.0401)

342 0.416(0.0415)

0.449 (0.0407)

383

-0.297 (0.0694)

-0.307 (0.0691)

384

0.185 (0.0328)

0.157 (0.0341)

33

Table 2.3: Fixed Capital

Method OLS

OLS

Specification Equation(2.21 ) 1/σ Estimates Implied Markups

311

0.417(0.2154)

1.71

322 0.434(0.1216)

1.77

381

0.208 (0.1944)

1.27

342 0.443(0.0412)

1.79

383

-0.2116 (0.3510)

-

384

0.0699 (0.5761)

1.08

34

Chapter 3

Uncovering Marginal Cost and Quality from Revenue and Cost Data

With assumptions on a discrete-choice demand system, technology,

Katayma, Lu and Tybout (2003), KLT henceforth, develop a methodology to uncover

marginal costs, quality, prices and quantities from plant-level data that report only

revenue and cost data. Once these variables are determined it is possible to perform

policy analysis and counterfactual experiments as discussed in the next chapter.

Using data from the Colombian beer industry, originally containing only

plant-level information on revenue and total costs from 1977 to 1990, I shall

demonstrate how to extend the KLT framework by including the extra information

provided by aggregate data. Although it may be difficult to obtain detailed data on

quantities at the plant level, the same is not true for aggregate variables. For instance,

in the beverage sector, the amount of beer, in liters, consumed in a given year is

widely available for many countries. Aggregate quantities also carry information on

demand parameters and therefore may help in the estimation process, especially in

small data sets. I consider two different hypotheses on the nature of this aggregate

measure. The first one assumes that this information is noisy, while the second

assumes that this information is deterministic and therefore error free. Each

assumption yields a different estimation strategy with potentially different parameter

estimates.

35

This chapter is organized as follows. Section 1 describes the traditional

approaches to estimating discrete-choice based demands. The next section provides

details of data set to be analyzed. The following section shows how to incorporate the

aggregate information into the model. And finally, the last section discusses the

results.

3.1 Traditional approaches

In this section, I shall describe the discrete-choice model commonly used

in the literature and the different econometric strategies to estimate its parameters.

Consumers rank products according to their characteristics and prices.

There are N+1 choices in the market, N inside goods and one outside good. Consumer

i chooses among those goods, given prices pj, observed characteristic xj, quality ξj and

unobserved idiosyncratic preferences εij , according to the following equation

ijjijijij hphxu εξθβθβ ++−= );();( 2211

where );(1 dih θβ is a function of a vector demographic variables hi, like

income , age, and marital status and 1θ is a vector of parameters defining that

function. The coefficient for price, );( 22 θβ ih , is defined similarly.

Assuming that εij has a Type I Extreme Value distribution, the probability

of individual i choosing good j takes the familiar logit form

(3.1) ∑ +−

+−=

kjikik

jijiji hphx

hphxhjp

));();(exp());();(exp(

)/(2211

2211

ξθβθβξθβθβ

36

If the econometrician observes prices, individuals’ choices and their

characteristics, the vector of parameters can be estimated by setting up the maximum

likelihood profile of all the observed consumer choices. Goldberg (1995) and

Trajtenberg (1990) are two examples of this approach. The former author observes

the new car choices of a random sample of consumers in the U.S from the Consumer

Expediture Survey, whereas the latter author collected data on purchases of CT

scanners1.

Suppose now that consumer-level data is not available, the econometrician

observes only prices, market shares, and characteristics. Then, the estimation

procedure has to be changed, since it is no longer possible to construct the maximum

likelihood profile. Instead, some aggregation argument has to be invoked. Indeed,

taking the expected value with respect to consumer attributes h yields the market

share implied by the model )]/([ hjpEs jj = which in extensive form is simply

(3.2) ∫∑ +−

+−= )(

));();(exp());();(exp(

),,,(2211

2211 hdFhphx

hphxpxs

kjikik

jijijj ξθβθβ

ξθβθβξθ

A regression equation can now be written by matching observed market

share of product j ( js ) with the one implied by the model, which gives

(3.3) ),,,( ξθpxss jj =

Firms take into account the unobservables (ξ) when setting its prices.

Thus, the endogeneity of prices requires the use of instrumental variables. However,

since the unobservables enter the regressions equation non-linearly some simulation

37

1 Actually, these authors use a variation of the logit model known as the nested logit model, which I shall discuss later in this chapter.

method has to be applied. Shortly, it involves solving for the ξj’s given data and the

parameters to construct moment restrictions conditional on available instruments (for

further details see Berry, Levinshon, and Pakes,1995).

When setting prices, firms take into account demand and cost

determinants. Therefore, the pricing decision also contains information on consumer

preferences such that efficiency can be improved by incorporating it in the estimation

procedure. And, as it shall be demonstrated in a later chapter, it also allows for the

simulation of different economic environments.

First, assume that each firm f produces a subset Ff of the goods sold in this

market and maximizes the sum of profits given by

(3.4) ∑∈

−=ΠfFj

jjjf sMmcp .).(

where M is the total market size and mcj is the marginal cost of producing

brand j. Then, it can be shown that the price pj of any product j produced by firm f

must satisfy the following equation

(3.5) 0)( =∂∂

−+ ∑∈ fFr j

rrrj p

smcps

Note that (3.5) is flexible enough to accommodate different market

structures. The first structure is the single firm product, in which the firm can only

control the price of its unique brand. The second is the multi-product firm, in which

the firm internalizes the price decision of all of its brands. I shall discuss these

different market structures in a separate section.

38

In turn, let marginal cost be modeled as

jjj wmc ψγ +=

where wj is a vector of cost characteristics and jψ is an unobserved cost

component. Similarly to the demand side unobservable, given ),,,,,( γξθ wpx one can

solve for the vector ψ from the quasi-supply relation (3.5) and set up the moment

conditions based on appropriate instruments. All the parameters of the model can then

be estimated through GMM using the demand and supply side moments. KLT goes a

little further by devising a methodology to estimate the demand parameters without

directly observed market-level data (prices and market shares).

3.2 Data

The data set consists of an unbalanced panel of plants in the beer industry,

with more than 10 employees, covering the period from 1977 to 1990. Originally

these data were gathered by the Colombia’s Departamento Nacional de Estadistica

(DANE) and have been cleaned as described in Roberts (1996). The revenue series

are constructed as the total sale revenue divided by a general wholesale price deflator.

The total variable costs are defined as the sum of payments to labor, intermediate

input purchases and energy purchases. Since some of the cost is incurred in the export

activity one has to scale it by the ratio of total domestic sales to total sales and deflate

the result by the same wholesale price deflator mentioned before.

From an additional source (UN database) I obtain the quantity of beer (in

hectoliters) produced in the country for the same sample period. Ideally, one would

39

want to have data on the quantity of beer consumed in the country. However, the data

in hand is not so restrictive since there is very little export activity in this sector

I also use auxiliary data to uncover the price of the imported good (p0t) 2 as

well as its imported quantity in hectoliters (q0t). In a separate publication DANE also

reports the net weight (in kilos) and the monetary value of imports (in pesos).

Assuming that beer has the same density as water (1kg per liter) it easy to transform

the net weight in kilos to volume of imported beer in hectoliters (q0t). Then, p0t

follows from the ratio of the peso value of imports to q0t.

3.3 Model

In this section I shall lay out the model used in this investigation. For

expositional purposes I assume first that market-level data on prices and quantities are

available. Then, I shall demonstrate, how to estimate the model with limited data

(only revenue and cost data) according to the methodology developed by KLT.

Assume now that products are divided into nests, g=0,1. The first nest

contains only the outside good (imported variety) while the second collects all the

inside goods (domestic varieties). For product j belonging to nest g define utility as

ijigjjij pu εσςαξ )1( −++−= for j=0,1,..,N

The first random term on the RHS ( igς ) is a common shock to all products

in nest g and its distribution depends on the parameter σ ( 10 <≤ σ ). As σ

approaches zero the within correlation of utilities within each nest decreases.

2 This as composite good that bundles together all the different imported varieties.

40

Furthermore, McFadden (1981) shows that we can integrate out ijig εσς )1( −+ ,

which is assumed to be identically and independently distributed extreme value, to

obtain a closed form solution for the within aggregate market shares for an inside

good as follows

(3.6) ]exp[

]exp[

0

0

δδ

δδ

−

−=

∑ kk

jjsw , j=1,2,…,N

Here, =jδ jjp ξα +− and 000 ξαδ +−= p . The share of all domestic

brands is given by )1/( += DDsd , where . Thus the

market share for a domestic variety s

σσδδ −

=

−−= ∑ 10

1)]1/()exp([

N

kkD

j is given by

⎥⎦⎤

⎢⎣⎡

+⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜

⎝

⎛

−

−=

∑ 1.

]exp[

]exp[

0

0

DDs

kk

jj

δδ

δδ

which is just the product of swj times sd. Further, taking the log-difference

between sj and s0 the demand equation takes the simple linear relation

(3.7) 000 ln).(lnln ξξσα −+−−=− jwjj sppss

The Nested Logit demand model also yields a closed form solution for the

cross-price derivatives entering the supply equation (3.5). For the domestic varieties k

and j the cross-price derivatives are given by

(3.8) ])1(1[1 wjjjk sssps σσ

σα

−−−−

−=∂∂ if k=j , and

(3.9) ])1([1 wjkjk sssps σσ

σα

−−−−

−=∂∂ otherwise.

41

If prices and quantities were available the model above could be estimated

using the methodologies described in section 3.1. Indeed, notice that, under some

rearrangements, (3.7) is a closed form version of (3.3) that can be solved, up the

model parameters, for the unobservable term 0ξξ −j . Also, the marginal cost

unobservable can be uncovered by substituting equations (3.8) and (3.9) into firms’

FOC (3.5). Then, these unobservables can be combined with appropriate instruments

to estimate the parameters through GMM.

Obviously, in the absence of market level data (prices and quantities) this

strategy is unfeasible. However, KLT show that commonly available information on

revenue and total costs along with some assumption on the technology can be used to

uncover relevant variables and estimate the model.

Using the fact that Rj=pj.qj, TCj=mcj.qj, and sj=qj/(Q+Q0) where Rj ,TCj, Q

and Q0 are revenue, total variable cost3, total output produced by domestic firms and

total imported quantity respectively, it is easy to demonstrate that these two identities

together with the F.O.C (3.5) can be solved for quantity as a function of data

(Rj,TCj,Q0t) and the demand parameters (α,σ)

Similarly, from the same system of equations one can retrieve

mcjt=mcjt(α,σ,Rjt ,TCjt, Qt ,Q0t), pjt= pjt(α,σ,Rjt ,TCjt, Qt ,Q0t) . Assume temporarily

that Qt is not observed. Thus, from ∑ =N

tttjtjtj QQQTCRq ),,,,,( 0σα , one is able to

solve for Qt=Qt(α,σ,Rjt ,TCjt,Q0t). Then, using prices and market shares, relative

quality, defined as tjtjta 0ξξ −= , can be determined from the demand system. To

3 TCj=mcj.qj as long as marginal costs are flat.

42

summarize, for a given set (α,σ,Rjt ,TCjt,Q0t), the KLT algorithm shows how to obtain

firm level prices, marginal costs, relative quality and quantities as well as aggregate

output (Qt). For more details see appendix A, which is a generalization4 of the

original transformation algorithm found in KLT.

Moreover, dynamics is introduced into the model through the assumption

that relative quality and marginal cost follow a VAR process given by

ajtjt

cjtjt tmcaba εβϕϕ ++++=+ 011

cjtjt

ajtjt tamcbmc εφλλ ++++= −− 1102

Estimation strategy

From the demand system, the price setting game and the VAR one is able

to uncover demand and supply side “errors”, represented respectively by and .

At this point the model seems awfully close to the BLP (Berry, Levinsohn and

Pakes,1995) methodology where similar error terms are combined with exogenous

product characteristics to form the identifying moment conditions. Here, however,

these data are not available. Note that not even prices or quantities are observed; they

are themselves functions of data and demand parameters to be estimated within the

model. The model is therefore not identified such that traditional econometric

technique like GMM and ML do not apply.

cjtε a

jtε

To identify it more structure has to be imposed on the parameters. This is

achieved by assuming a prior knowledge of the parameters distribution and using the

43

4 The original transformation algorithm had to be modified to accommodate multi-plant firms.

data set and the structure imposed by the model to update this prior according to the

Bayes rule

)().;();( θθθ pDLDp ∝

The LHS is the posterior probability updated by the data D, and the RHS

is the product of the likelihood function of the data times the prior distribution of the

parameters. However, only in special cases, the posterior distribution has a closed

form from which one can make inference either by sampling from it or by consulting

easily available tables. Fortunately, Monte Carlo techniques have been developed to

deal with such problem. Shortly, it relies on ergodic theory to guarantee that a

computable statistic converges to the true posterior distribution. Then, once

convergence has been attained, one can sample from this statistic and make inference.

3.4 Aggregate information

Aggregate quantities also carry information on demand parameters and

therefore may help in the estimation process, especially in small data sets. Below I

discuss two different assumptions on the properties of this aggregate measure. The

first one amounts to just appending the KLT econometric approach described above,

while the second yields a completely different estimation approach.

Assumption 1: Aggregate information is noisy.

Assume now that the amount of beer consumed in a given year is observed

up to a measurement error. Note that the model implies an aggregate quantity given

44

some parameters and data. One can then ask the model to match this observed

quantity according to

(3.10) tobstjtjtt wQQTCRQ −=),,,,( 0σα

where wt is assumed to be a serially uncorrelated and normally distributed

mean zero error term which is independent of the VAR error terms. To include this

new “moment” in the estimation it suffices to incorporate the likelihood of in the

likelihood function

tobsQ

);( θjtDL .

Assumption 2: Aggregate information is not noisy and σ=0

From this assumption one can conclude that the quantity implied by the

model matches exactly its empirical counterpart and that the discrete choice model is

the simple logit form instead of its nested version (σ=0). Then

(3.11) obstjtjttt QQTCRQ =),,,( 0α

All data in this equation are observed which implies that αt can be

determined for each time period t. This approach has two limitations though. Firstly,

the simple logit model (σ=0) places very restrictive assumptions on consumer

preferences such that cross-price elasticities have somewhat undesirable properties.

Secondly, it requires a very reliable source for the total quantity since measurement

error is not allowed.

45

Given these drawbacks, a legitimate question may arise. Why bother

making these restrictions on the model (assumption2)? The reason is that the

Bayesian technique proved to be a little cumbersome to implement computationally

and many government agencies and students are somewhat reluctant to adopt the

Bayesian approach, especially one that requires Monte Carlo simulation. This

technique also requires the imposition of priors on the parameters distribution, which