deloitte cfo survey q1 2013 fewer risks, greater optimism feel free to use these slides in your...

TRANSCRIPT

Deloitte CFO Survey Q1 2013Fewer risks, greater optimism

Feel free to use these slides in your presentations

Internal webinar event, 16th April

CFO Survey team: Ian Stewart, Chief Economist, Debapratim De & Alex Cole

© 2013 Deloitte LLP. All rights reserved.2 Economics & Markets Research, Deloitte LLP, London

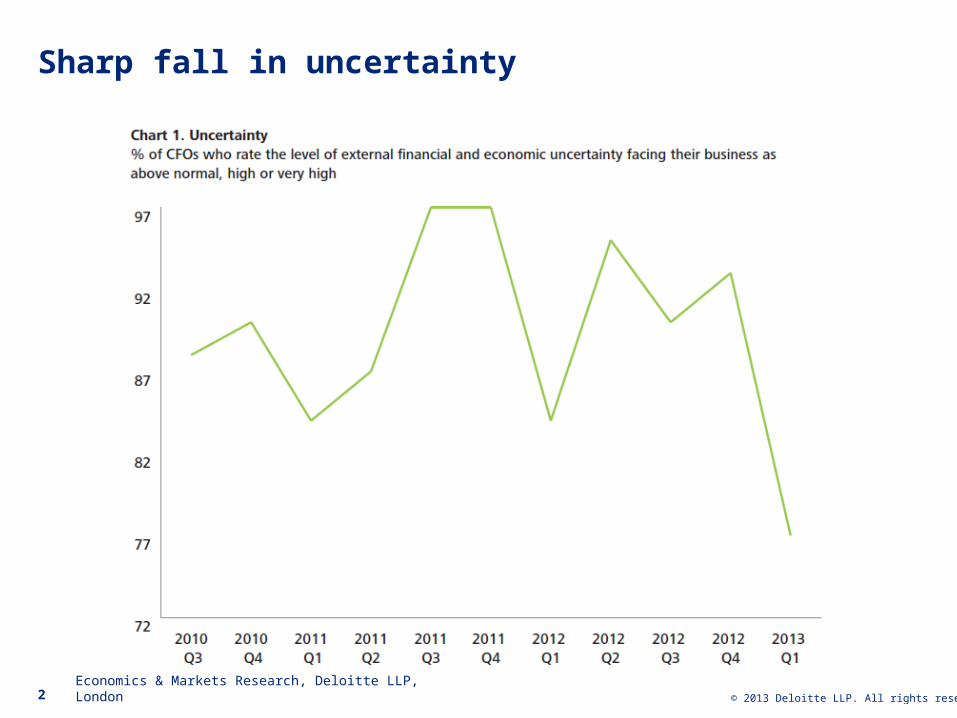

Sharp fall in uncertainty

© 2013 Deloitte LLP. All rights reserved.3 Economics & Markets Research, Deloitte LLP, London

Euro breakup fears easing

© 2013 Deloitte LLP. All rights reserved.4 Economics & Markets Research, Deloitte LLP, London

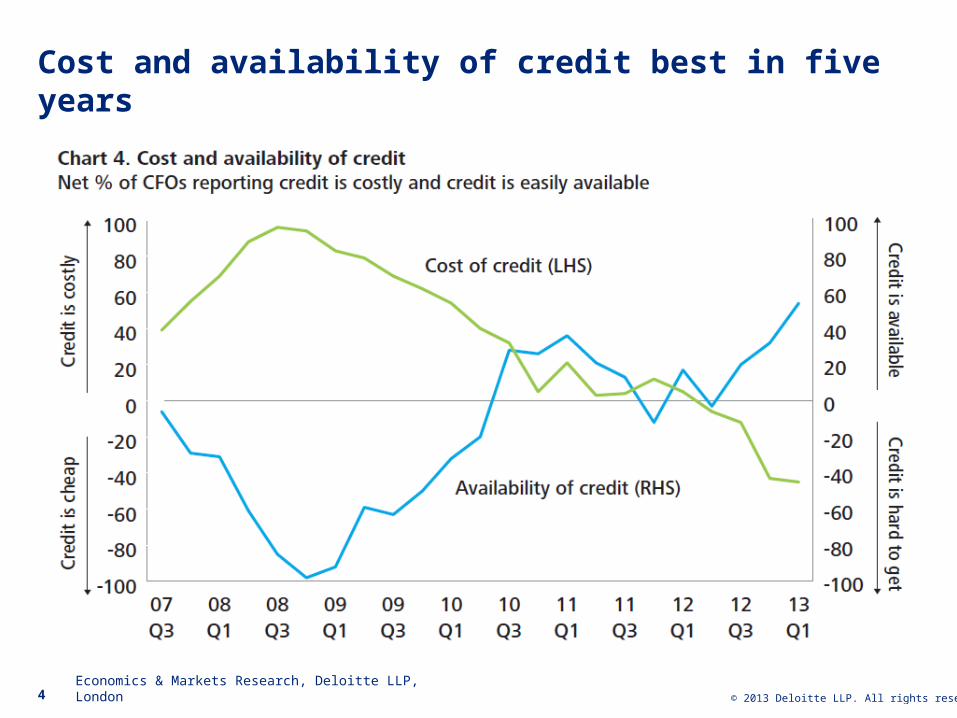

Cost and availability of credit best in five years

© 2013 Deloitte LLP. All rights reserved.5 Economics & Markets Research, Deloitte LLP, London

Continued rise in optimism

© 2013 Deloitte LLP. All rights reserved.6 Economics & Markets Research, Deloitte LLP, London

Revenues to increase

© 2013 Deloitte LLP. All rights reserved.7 Economics & Markets Research, Deloitte LLP, London

Risk assets rallying

© 2013 Deloitte LLP. All rights reserved.8 Economics & Markets Research, Deloitte LLP, London

Sharp rise in corporate risk appetite

© 2013 Deloitte LLP. All rights reserved.9 Economics & Markets Research, Deloitte LLP, London

Less emphasis on cost control and increasing cash flow

© 2013 Deloitte LLP. All rights reserved.10 Economics & Markets Research, Deloitte LLP, London

Sharp fall in defensiveness

© 2013 Deloitte LLP. All rights reserved.11 Economics & Markets Research, Deloitte LLP, London

International corporates turn decisively expansionary

© 2013 Deloitte LLP. All rights reserved.12 Economics & Markets Research, Deloitte LLP, London

Corporate investment drivers

© 2013 Deloitte LLP. All rights reserved.13 Economics & Markets Research, Deloitte LLP, London

Equities overvalued for the first time in 3 years

© 2013 Deloitte LLP. All rights reserved.14 Economics & Markets Research, Deloitte LLP, London

Confidence rising amongst smaller companiesConfidence about next 12 months profitability highest since Q4 2007, for both manufacturing and service sectors

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013-60

-40

-20

0

20

40

60

Manufacturing

Services

Source: British Chamber of Commerce Quarterly Economic Survey

© 2013 Deloitte LLP. All rights reserved.15 Economics & Markets Research, Deloitte LLP, London

Increasing optimism about the housing marketUK RICS Housing Market: price expectations

2006 2007 2008 2009 2010 2011 2012 2013-100

-80

-60

-40

-20

0

20

40

60

© 2013 Deloitte LLP. All rights reserved.17 Economics & Markets Research, Deloitte LLP, London

Growth to remain weak in 2013

©2012 Deloitte LLP. All rights reserved.18

Key points from the 2013 Q1 survey

Economics & Markets Research, Deloitte LLP, London

• CFO optimism has risen for the third consecutive quarter, taking it above its average for the last five and a half years. Corporate risk appetite is at its third highest level.

• Fears of a euro breakup have receded, despite the survey period having coincided with the crisis in Cyprus.

• Perceptions of economic and financial uncertainty have fallen to the lowest level since early 2010.

• Credit availability is at its highest level in five and a half years.

• CFOs’ balance sheet policies are becoming less defensive, with less emphasis on cost cutting and cash. Breaking the results down we find that this has been driven by companies with strong overseas exposure which have become markedly more expansionary in the way they run their balance sheets. UK-facing corporates remain in defensive mode.

© 2013 Deloitte LLP. All rights reserved.19 Economics & Markets Research, Deloitte LLP, London

2012 2013

©2012 Deloitte LLP. All rights reserved.Economics & Markets Research, Deloitte LLP, London20

About the Deloitte CFO Survey

The Deloitte CFO Survey, launched in 2007, is a quarterly survey of Chief Financial Officers and Group Finance Directors of major UK companies. The Survey captures shifts in UK CFOs' opinions on valuations, risks and financing and has become a benchmark for gauging financial attitudes of major corporate users of capital. Over 300 CFOs, mainly from FTSE 350 companies, have joined the CFO Survey panel. In the latest survey, covering the first quarter of 2013, 120 CFOs participated, including CFOs of 26 FTSE 100 and 44 FTSE 250 companies. The rest were CFOs of other UK listed companies, large private companies and UK subsidiaries of major companies listed overseas. The combined market value of the 69 UK-listed companies surveyed is £671 billion, or approximately 32% of the UK quoted equity market. The Deloitte CFO Survey has been widely quoted in the media and is firmly established with the policymakers. The Bank of England has cited the CFO Survey several times in its publications such as the quarterly Inflation Report and the monthly Trends in Lending report. The findings have also been quoted in the minutes of the Bank's Monetary Policy Committee meetings.

To learn more about the CFO Survey please visit our website www.deloitte.co.uk/cfosurvey

Contacts

To discuss the Survey findings and methodology contact:

Ian Stewart, Chief Economist, Deloitte UK on 020 7007 9386 or [email protected] De, Senior Economic Analyst, Economics & Markets Research on 020 7303 0888 or [email protected] Cole, Economic Analyst, on 020 7007 2947 or [email protected]

To sign your clients up to the CFO Survey panel please contact Alex Cole.

© 2013 Deloitte LLP. All rights reserved.22

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.

© 2013 Deloitte LLP. All rights reserved.

Member of Deloitte Touche Tohmatsu Limited